Embed Size (px)

Citation preview

Annual Economic Review

2013

Ministry of Finance, Republic of Liberia

i

FOREWORD

In this second edition of the Annual Economic Review we present highlights of the developments in the real, fiscal, monetary and external sectors of the economy; report on the progress in the implementation of a number of the projects in the Agenda for Transformation, as well as the steps Government is taking to remove the binding constraints to growth.

Despite a slow global recovery, the Liberian economy continues to be resilient. In 2013, the economy experienced steady growth in real GDP of 8.1%, well above the African average by 2.5 percentage points. This strong economic performance is driven partly by increased activities in the mining sector, which, along with other concessions activity, is expected to continue to perform well in the medium-term. This highlights both the opportunities for Liberia – in terms of employment, business growth and government revenue – and the challenges we face in achieving broad based growth that achieves development for all members of our society.

Accordingly, the Government is currently striving to create more diversified output, higher up the value chain, particularly in the industrial and agricultural sectors. Already the government has worked to create opportunities for small and medium enterprises by reducing the barriers to business registration and instituting fiscal rules that will ensure local contents of consumables for government and the concession companies.

In continuation of its expansionary fiscal policy, the Government of Liberia (GoL), in 2013, made concrete efforts to focus resources onto the development priorities set out in the Agenda for Transformation. In particular this has meant ensuring investment in the key infrastructure needed, to address the infrastructure deficit and enhance private sector led growth. These included the rehabilitation of the Mt. Coffee Hydroelectric Plant, participation in the West Africa Power Pool, the construction of new Heavy Fuel Oil (HFO) power plants, and the commencement of major road projects linking growth corridors, such as the Monrovia-Ganta Highway and a major urban artery expansion to Somalia Drive.

ii

We would like to thank all of the ministries, agencies and commissions, and donor partners for providing the necessary data to compile this report. We welcome any comments and suggestions that will help us improve on the coverage and quality of subsequent editions of the Economic Review.

Amara M. Konneh Minister of Finance, Republic of Liberia March 2014

3

TABLE OF CONTENTS

TABLE OF CONTENTS ..................................................................................................................................... 3

LIST OF FIGURES ............................................................................................................................................ 4

LIST OF TABLES .............................................................................................................................................. 4

EXECUTIVE SUMMARY ................................................................................................................................... 6

1. INTRODUCTION ....................................................................................................................................... 12

2. GLOBAL ECONOMIC DEVELOPMENTS AND OUTLOOK ............................................................................ 13

3. DOMESTIC MACROECONOMIC DEVELOPMENTS .................................................................................... 14

3.1 DOMESTIC DEVELOPMENT STRATEGY ............................................................................................... 15

3.2 ECONOMIC CHALLENGES .................................................................................................................. 15

3.3 REMOVING BOTTLENECKS TO CONCESSIONAIRES ............................................................................ 16

3.4 FISCAL RULES ..................................................................................................................................... 16

3.4.1 EXPENDITURE ............................................................................................................................. 16

3.4.2 BORROWING .............................................................................................................................. 17

3.5 MONETARY POLICY ............................................................................................................................ 17

4. REAL SECTOR DEVELOPMENTS ................................................................................................................ 18

4.1 AGRICULTURE .................................................................................................................................... 18

4.1.1 DONOR FUNDED PROJECTS IN AGRICULTURE ............................................................................ 19

4.1.2 AGRICULTURAL CONCESSIONS ................................................................................................... 19

4.2 FORESTRY SUB-SECTOR ..................................................................................................................... 20

4.3 COMMERCE AND INDUSTRIES ........................................................................................................... 22

4.3.1 OUTPUT OF THE INDUSTRIAL SECTOR ........................................................................................ 23

4.4 MINING AND PETROLEUM ................................................................................................................ 24

4.5 SOCIAL AND BASIC SERVICES ............................................................................................................. 25

4.5.1 EDUCATION ................................................................................................................................ 25

4.5.2 HEALTH AND SOCIAL WELFARE .................................................................................................. 26

4.5.3 PRIORITY INFRASTRUCTURE PROJECTS ....................................................................................... 28

4.5.4 WATER AND SEWERAGE SERVICES ............................................................................................. 31

4.5.5 TRANSPORT SERVICES ................................................................................................................ 33

4.5.6 ENERGY GENERATION, TRANSMISSION AND DISTRIBUTION ...................................................... 33

5. FISCAL SECTOR DEVELOPMENTS ............................................................................................................. 36

5.1 FISCAL OVERVIEW ............................................................................................................................. 36

5.1.1 REVENUE .................................................................................................................................... 37

5.1.2 EXPENDITURE ............................................................................................................................. 37

4

5.1.3 GOL TREASURY BILLS .................................................................................................................. 38

5.2 FISCAL YEAR 2013/14 ........................................................................................................................ 39

5.3 TAX EXPENDITURES ........................................................................................................................... 41

6. MONETARY SECTOR DEVELOPMENTS ..................................................................................................... 43

6.1 MONETARY INDICATORS ................................................................................................................... 43

6.2 MONETARY AGGREGATES ................................................................................................................. 44

6.2.1 LIBERIAN DOLLARS IN CIRCULATION .......................................................................................... 44

6.2.2 MONEY SUPPLY (M1) .................................................................................................................. 45

6.2.3 BROAD MONEY (M2) .................................................................................................................. 45

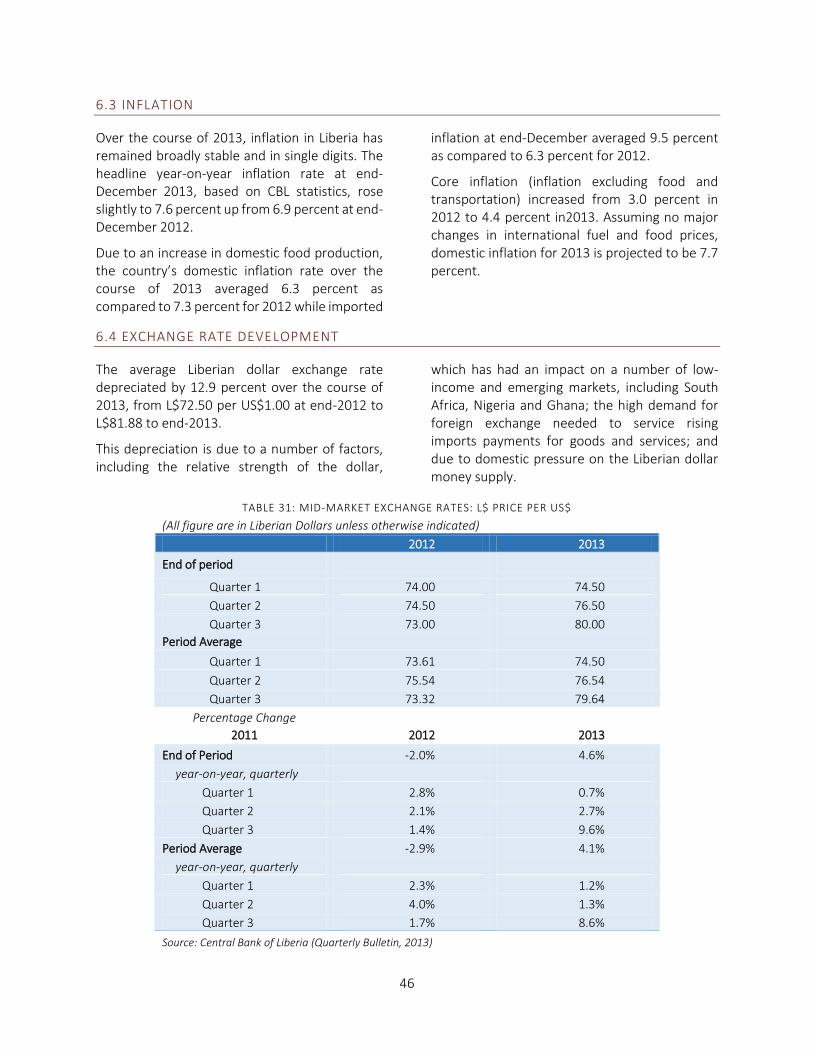

6.3 INFLATION ......................................................................................................................................... 46

6.4 EXCHANGE RATE DEVELOPMENT ...................................................................................................... 46

6.4.1 FOREIGN EXCHANGE AUCTIONS ................................................................................................. 47

6.5 INTEREST RATES AND BANK LENDING ............................................................................................... 48

6.5.1 DEPOSIT RATE ............................................................................................................................. 48

6.5.2 LENDING RATE ............................................................................................................................ 48

6.5.3 COMMERCIAL BANK CREDITS ..................................................................................................... 49

6.6 EXPANSION OF THE MONEY MARKET ............................................................................................... 52

6.6.1 CBL NOTES .................................................................................................................................. 52

7. EXTERNAL SECTOR DEVELOPMENTS ....................................................................................................... 53

7.1 EXPORT OF GOODS AND SERVICES .................................................................................................... 54

7.2 IMPORT OF GOODS AND SERVICES ................................................................................................... 55

REFERENCE DOCUMENTS ............................................................................................................................ 57

L IST OF FIGURES

Figure 1: SECTORAL DISTRIBUTION OF THE AGENDA FOR TRANSFORMATION FUNDING .......................... 29 Figure 2: TRENDS IN THE GOL REVENUE ..................................................................................................... 37 Figure 3: TRENDS IN GOL EXPENDITURES .................................................................................................... 38 Figure 4: TRENDS IN EXPENDITURES ON PRODUCTIVE AND NON-PRODUCTIVE SECTORS ......................... 38 Figure 5: CBL NET FOREIGN RESERVE POSITION, OCTOBER 2012- JULY 2013 ............................................. 43 Figure 6: LIBERIA DOLLAR PRICE PER US$, JAN - JUNE, 2013 ...................................................................... 47 Figure 7: COMMERCIAL BANK LOANS TO ECONOMIC SECTORS, 2011: Q3 & 2013:Q3 ............................... 50 Figure 8: TREASURY BILLS AND CBL NOTES ISSUED ..................................................................................... 52 Figure 9: BALANCE OF PAYMENTS 2011-13 (US$ MILLIONS) ...................................................................... 54

L IST OF TABLES

5

Table 1: COMPARATIVE GDP GROWTH RATES FOR SELECTED WEST AFRICAN COUNTRIES ....................... 14 Table 2: 2013 AGRICULTURAL OUTPUT (US$) ............................................................................................. 18 Table 3: REVENUES FROM THE AGRICULTURE SECTOR ............................................................................... 19 Table 4: DONOR-FUNDED PROJECTS IN THE AGRICULTURE SECTOR .......................................................... 19 Table 5: AGRICULTURAL CONCESSIONS OPERATING IN LIBERIA ................................................................. 20 Table 6: LAND USE RIGHTS .......................................................................................................................... 20 Table 7: EXPORT AND GDP CONTRIBUTION OF THE FORESTRY SECTOR ..................................................... 21 Table 8: REVENUES FROM THE FORESTRY SECTOR ..................................................................................... 22 Table 9: BUSINESSES OPERATING IN LIBERIA .............................................................................................. 22 Table 10: INDUSTRIAL OUTPUT ................................................................................................................... 23 Table 11: MINERAL EXPLORATION AND MINING COMPANIES OPERATING IN LIBERIA ............................... 24 Table 12: REVENUES FROM THE MINING SECTOR ...................................................................................... 25 Table 13: REVENUES FROM THE PETROLEUM SECTOR ............................................................................... 25 Table 14: HEALTH INDICATORS ................................................................................................................... 28 Table 15: PRIORITY INFRASTRUCTURE PROJECTS ........................................................................................ 30 Table 16: ROADS - WORK UNDERWAY ........................................................................................................ 30 Table 17: WATER AND SEWER DEVELOPMENTS IN LIBERIA FOR 2013 ........................................................ 32 Table 18: REGISTERED VEHICLES ................................................................................................................. 33 Table 19: DRIVER'S LISCENSES ISSUED ........................................................................................................ 33 Table 20: ELECTRICITY INDICATORS BETWEEN 2010 AND 2013 .................................................................. 34 Table 21: LEC CUSTOMER SEGMENTATION................................................................................................. 35 Table 22: MONTHLY KWH OF POWER SUPPLIED ......................................................................................... 35 Table 23: BREAKDOWN OF THE UNIT COST OF POWER .............................................................................. 35 Table 24: GOL TREASURY BILLS (MAY - DECEMBER 2013) ........................................................................... 39 Table 25: QUARTERLY REVENUE PERFORMANCE FOR FY 2013/2014 ......................................................... 39 Table 26: PRELIMINARY GFS TABLE FOR FY 2013/2014............................................................................... 40 Table 27: CUMULATIVE MID-YEAR (FY2013/14) DISBURSEMENTS BY SECTOR ........................................... 40 Table 28: MONTHLY TAX EXPENDITURES FOR 2013 .................................................................................... 42 Table 29: LIBERIAN DOLLAR CURRENCY IN CIRCULATION (L$) .................................................................... 44 Table 30: LIBERIAN DOLLAR MONETARY AGGREGATES (L$) ....................................................................... 45 Table 31: MID-MARKET EXCHANGE RATES: L$ PRICE PER US$ .................................................................... 46 Table 32: CENTRAL BANK OF LIBERIA FOREIGN EXCHANGE ........................................................................ 48 Table 33: COMMERCIAL BANKS’ INTEREST RATES, 2012-2013 ................................................................... 49 Table 34: COMMERCIAL BANKS’ LOANS TO ECONOMIC SECTORS (L$) ....................................................... 51 Table 35: CBL BILL ISSUANCE (JULY – NOVEMBER 2013) ............................................................................ 52 Table 36: BALANCE OF PAYMENTS 20011-2013 (US$ MILLIONS) ............................................................... 53 Table 37: EXPORT OF COMMODITIES, 2008-2013 ....................................................................................... 55 Table 38: IMPORT OF GOODS, 2008-2013 .................................................................................................. 56

6

EXECUTIVE SUMMARY

MACROECONOMIC DEVELOPMENTS & CHALLENGES

In 2013, Liberia’s real Gross Domestic Product (GDP) growth was estimated at 8.1 percent, slightly lower than the 8.3 percent growth recorded in 2012. The growth in 2013 was driven largely by increased activities in the mining sector, and this is expected to continue in the medium-term, particularly with the commencement of iron ore exports by China Union and the ramping up of production by Arcelor Mittal.

Despite the macroeconomic stability that has prevailed and the successes in supporting the private sector to date, a number of challenges are facing the Liberian economy in the near-term. Many of them are structural in nature, but exogenous factors also play a leading role around both domestic and external demand, as Liberia is a recipient of large aid and security related inflows, which are likely to fall over time; and is subject to global demand and prices, having a productive base mostly characterized by the export of primary commodities.

The draw-down of the United Nations Mission in Liberia (UNMIL) (including secondary effects) and arguably lower levels of NGO activity are likely to be causing a slowdown in domestic demand for services – with a corresponding impact on employment and secondary effect on economic activity. The government is also facing difficulties in achieving high rates of public capital expenditure as a constrained resource envelope and pressures on the recurrent side consume resources that could otherwise have gone towards investment projects. The budget for FY2014/15 will look to address these issues, with a focus on investment and enhancing the productive capacity of the economy.

REAL ECONOMY

Agriculture and Forestry

According to the Central Bank of Liberia (CBL), rubber production declined by 12.8 percent in 2013 compared to 2012. The fall in rubber production is mainly attributed to aging rubber trees and the longevity in the gestation period of newly planted rubber trees, which are further exacerbated by the decline in global rubber prices.

The CBL reports that cocoa and coffee production for 2013 increased by 3.2 percent and 49.6 percent, respectively, compared to 2012. The improved performance is attributed to increases in the maturity of newly planted cocoa and coffee trees. Owing to the moratorium on the export of timber, round logs production declined by 51.1 percent in 2013 relative to 2012.

About US$36 million in recently ratified credits are being invested to boost smallholder productivity, providing micro-loans, inputs and enhancing access to market. Palm Oil Concessionaires are also expanding their activity, creating thousands of new jobs. The government through the Ministry of Agriculture is working with concessionaires and civil society partners to operationalize the agreed upon out-grower schemes, which will provide training and financing to independent farmers, allowing them to grow palm oil and sell it back to the concessionaires.

Manufacturing

In 2013, the manufacturing sector expanded by 13 percent as compared to 21 percent for 2012. Despite this expansion, the manufacturing sector still faces major binding constraints, including an insufficient supply and prohibitively high cost of energy generation, which makes products expensive and reduces

7

demand for locally manufactured goods. The industrial sector is also faced with a shortage of skilled labor and limited local inputs.

As a result, in the short-term, manufacturing – especially of cement, beverages, woodwork, printing, and various consumer goods – is expected to continue to have a limited impact on output and growth and correspondingly on jobs creation and improvements in socioeconomic conditions.

Cement output increased by 49.5 percent in 2013 as compared to 2012. This can be directly attributed to an expansion in local construction and the corresponding increase in the demand for cement, which necessitated additional manufacturing capacity that is being met by expansion at the cement plant.

Beverage production, on the other hand, increased slightly by 3.9 percent in 2013 as compared to the volume produced in 2012.

Mining and petroleum

Mining is a significant sector to the Liberian economy, given that the country is endowed with a vast amount of metallic and non-metallic minerals. Liberia’s abundant mineral resources include gold, diamond, iron ore and oil. Concession agreements have been granted to six iron ore mining companies and 17 gold and diamond mining companies, and petroleum exploration rights have been awarded to 10 companies. Mining concessions cover an operational area of 113,256 hectares.

Production of iron ore increased dramatically in 2013 resulting in export earnings from the mining sector rising to US$351.2 million in 2013, up from US$155.8 million the previous year, representing an increase of 125.4 percent. This has enabled the government to collect more revenues from the sector; in FY 2012/13 government revenues on mining specific tax lines (excluding income taxes) amounted to US$23.4 million, up from US$11.7 million in FY 2011/12, driven by higher mineral royalties.

Removing Bottlenecks to Concessionaires

In order to achieve the growth trajectory necessary for achieving the Liberia RISING National Vision 2030, the government made significant efforts in 2013 to expand the private sector and more importantly remove the bottlenecks to concessionaires. The Inter-Ministerial Concessions Commission (IMCC) conducted a national dialogue between key ministries, government agencies, NGO’s and concessionaires to remove bottlenecks to production and exportation timelines. These actions could increase capital investment by approximately US$7.5 billion over the AfT period, boost tax revenue collection by approximately US$400 million per annum, and enhance employment by approximately 80,000-90,000 jobs in the next 10-15 years.

Major strides have also been taken to resolve the infrastructure, bureaucratic and community interest issues facing concessionaires across the board (mining, forestry and palm oil industries) through numerous roundtable discussions between relevant government stakeholders and concessionaires. In the mining sector, through an inter-Ministerial effort, GoL successfully settled the housing unit issue with China Union, paying US$4 million to former Bong Mines workers and approximately US$500,000 to resettle squatters. This enabled China Union to reach its intended production capacity and exportation timeline. Concerned about the slowdown in exports, GoL has targeted logistical bottlenecks in the forestry sector and is signing memorandums with forestry companies, authorizing them to rehabilitate primary roads in exchange for clearance of their tax arrears.

8

SOCIAL AND BASIC SERVICES

Education

Achievements in the education sector reflect the priority that the government and its development partners have placed on education, and are consistent with the previously agreed 2009 Education Sector Plan, the five-year (2012-2017) Medium Term Plan for Education Reform and Development in Liberia, the Education Reform Act of 2011 and the draft Technical and Vocational Education and Training (TVET) Policy of 2011. As a result in 2013 key achievements recorded in the educational sector included successfully developing an Education Management Information System, the construction and furnishing of County Education Offices, Learning Resources Centers and schools, and the provision of grants to school boards amongst others.

Health and social welfare

The health sector succeeded in increasing the percentage of deliveries assisted by skilled birth attendants; the number of families with access to family planning; the percentage of children under the age of one-year who received DPT3/pentavalent-3 vaccinations against diphtheria, pertussis (whopping cough) and tetanus; the percentage of pregnant women provided with second dose of Intermittent Preventative Treatment (IPT) for malaria; the percentage of pregnant women testing HIV+ that are receiving antiretroviral (ARV) prophylaxis to reduce mother-to-child-transmission (MTCT); and the percentage of facilities with no out-of-stock tracer drugs.

Priority Infrastructure Projects

Investment in infrastructure is a critical step towards generating and sustaining rapid economic growth and development. The Agenda for Transformation (AfT), Liberia’s poverty reduction strategy plan, identifies the government’s priority projects, a large portion of which cover infrastructure. The total cost of the AfT is estimated at US$3.2 billion over the five-year period (2012-2017); the Government has succeeded in mobilizing more than US$2 billion in committed financing for the AfT, including US$114 million of its own resources through the Public Sector Investment Plan (PSIP) and US$393 million from borrowing. During the period under review, as part of efforts to finance the AfT, donors have disbursed US$673,824,913 while the government under its PSIP has disbursed US$100,120,870.

Notably, the needs of the energy and environment sector under the AfT have been met by commitments from government and donors. However, due to the infrastructure needs of the country, a significant funding gap estimated at US$825 million remains in the infrastructure sector.

Roads and Bridges

The Government, with the help of its development partners, has embarked upon a nation-wide effort to rehabilitate roads and bridges prominent among which are: Red Light to Ganta (180.4 km), Gbarnga to Ganta to Guinea border (68.6 km), Caldwell to Louisiana road (12km); S.K.D. Blvd. (5.1 km), Somalia Drive linking the Freeport of Monrovia to Red Light (13.2 km), Kolahun junction to Vahun to Bomaru road, and Kaweaken to Barclayville road (86km). These roads constitute segments of a vital transport artery linking the country, from Harper to Ganta to Monrovia and across to the border with Sierra Leone. The Liberian government is working to secure funds for outstanding segments that will boost the domestic economy

9

and enhance international trade. The government is also rehabilitating the symbolically important Caldwell Bridge (385 ft.).

Water and Sewerage Services

In 2013, the Liberia Water and Sewer Corporation’s overall coverage decreased by 17.6 percent compared to 2012, with its business and family customers decreasing by 11.8 percent and 21.8 percent respectively compared to 2012. This can be attributed to the 87.7 percent increase in the cost per cubic meter of water.

Transport Services

The number of registered vehicles in 2013 amounted to 33,309, representing an increase of 13.7 percent over the number of registered vehicles for 2012. The most notable increase in registration was motorcycles at 231.3 percent. The most notable decrease occurred with respect to the Gratis (NGO) registration which fell by 33.9 percent. There were 15,972 driver’s licenses issued in 2013 - representing a decrease of 23.2 percent as compared to that of 2012.

Energy Generation and Distribution

The government of Liberia has made significant strides in increasing access to energy. With the Liberia Accelerated Electricity Expansion Project (LACEEP), the government has concluded plans to expand 66 KV lines from Paynesville to Kakata. Consequently, the distribution chain will commence from Duport Road North through Soul Clinic, Pipeline Road, Mount Barclay, and Careysburg up to 15th Gate Community, with further expansion from Kakata up to Weala in Margibi County.

The GoL has also garnered support for the West Africa Power Pool (WAPP – CLSG) project along with Côte d’Ivoire, Sierra Leone and Guinea. Partners supporting this project – namely World Bank International Development Assistance (IDA), the African Development Bank (AfDB), KFW, and the European Investment Bank – are providing resources for construction of a 225 KV transmission line. The transmission lines run from Mahn, Ivory Coast to Yekepa for onward transmission to N’Zerekore in Guinea and Bo Waterside in Sierra Leone. Through the WAPP cross border electrification project, 33km of lines have been constructed to supply power to 18 communities in Nimba, Grand Gedeh and Maryland Counties.

The government in 2013 made payments toward Liberia’s capital contribution and Resettlement Action Plan (RAP) compensation to ensure the effective implementation of WAPP.

The government also commenced the rehabilitation of the Mt. Coffee Hydroelectric Power Plant, which will provide an additional 80 Mega Watts (MW) when completed, and made disbursements towards the government funded 10 MW Heavy Fuel Oil (HFO) Plant project.

Other energy projects include the 10MW HFO Plant sponsored by the Japan International Cooperation Agency (JICA), and the World Bank’S US$10 million 10MW HFO Plant, both of which will be installed at the Liberia Electricity Corporation (LEC) Bushrod Island Site. Also included is the ELTEL Accelerated Transmission and Distribution (T&D) Project, which involves rehabilitation of four substations, construction of distribution lines from downtown Monrovia up to Sinkor 20thStreet, and installation of 66KV lines between Capitol Hill and Paynesville Substation as well as New Kru Town Substation. The project will connect 6,000 new consumers to the national energy grid. The Liberian Government in September 2013 signed a line of credit agreement in the amount of US$144 million with the Indian Exim Bank for a Transmission and Distribution project from Ganta to Kakata and Buchanan.

10

FISCAL SECTOR DEVELOPMENTS

FY2012/13 saw the successful execution of the first year of the Medium Term Expenditure Framework (MTEF) budget process, with the FY2013/14 budget now building on the successes and lessons learned. Crucially, the MTEF process and other improvements in Public Financial Management have allowed the government to focus resources on priorities linked to the Agenda for Transformation, including energy and road projects.

Revenues have increased from US$148.5 million in FY 2006/2007 to a projection of US$582 million in FY 2013/2014, although recent revenue performance has fallen short of projections, which has had an adverse effect on expenditure execution.

In May 2013 the Central Bank of Liberia, began the issuance of Liberian-Dollar denominated Treasury Bills (T-bills). These T-bills will be used in the short run to manage revenue volatility and, in the longer run, to expand the money market and provide an additional policy instrument to manage Liberian dollar liquidity. Between L$81 million and L$228 million (US$1 million and US$3 million equivalent, respectively) 91-day T-bills were issued in each month from May through December 2013, at record low interest rates averaging 2.06 percent.

MONETARY SECTOR DEVELOPMENTS

The Central Bank of Liberia (CBL) maintained its monetary policy stance with the overarching goal of achieving overall price stability, stable exchange rate and promoting economic growth.

The dominance of the US dollar in the Liberian economy continues to pose significant challenges for the formulation and implementation of monetary policy. In 2013, monetary policymakers heavily relied on the use of foreign exchange reserves to stabilize the exchange rate in order to achieve the objective of price level stability, though this was complemented by the issuance for the first time of CBL bills (short term debt instruments) and the easing of the reserve requirement for US dollar deposits.

During the course of 2013 the Liberian Dollar depreciated against the US Dollar, alongside currencies in a number of other low-income and emerging markets, including South Africa, Nigeria and Ghana. Partly due to the high demand for foreign exchange needed for rising imports payments for goods and services, the average Liberian dollar exchange rate depreciated by 4.6 percent to L$80/US$1.00 at end September 2013 and by December 2013 the rate was L$87/US$1.00. In response, the CBL enhanced interventions through foreign exchange operations and commenced the issuance of CBL bills, and the Ministry of Finance engaged in a taxpayer education campaign to enhance Liberian Dollar revenue in order to reduce pressure on the exchange rate.

The Liberian Dollars in circulation as at end of September 2013 totaled L$8.6 billion. The average savings deposit rate at the end of the third quarter showed a year-on-year decrease by 4.3 percent compared to the same period in 2012. Over the course of 2013, up to end-September 2013, the average lending rate decreased by 70 basis points. Commercial banks credit to major sectors of the economy at end September 2013 amounted to L$25.6 billion, a 39 percent increase on than that recorded at the end of the same period in 2012. The increase in credit to important sectors of the economy supports a deepening of financial services and is expected to expand economic activities.

11

EXTERNAL SECTOR DEVELOPMENTS

Liberia’s current account deficit extended further in 2013, although this masked a 13% increase in commodities exports, driven by iron ore, which is now the largest export commodity by value at US$312.2 million. Despite the increase in iron ore production and export, the net merchandize position deteriorated to negative US$667.2 million in 2013 due to an increase in merchandize imports of 12.5%, largely driven by beverages and tobacco, chemical and related products, and petroleum products.

Rubber exports fell by 32% to US$120.5 million, reflecting lower production due to aging rubber trees and weaker global rubber prices. Round logs exports were also weak, falling 67% from US$48.4 million in 2012 to US$16.0 million in 2013, largely as a result of the moratorium on Private Use Permits (PUPs). Gold and diamond exports continued to exhibit volatility, with a fall of 16% and an increase of 37% respectively. Cocoa and coffee beans remain small scale exports in comparison to other commodities. Cocoa exports grew by 51%, however this followed a 50% fall between 2011 and 2012.

Net services also fell, to negative US$ 667.5 million, having improved previously from negative US$865.0 million in 2011 to negative US$658.4 million in 2012. Net income improved from a deficit of US$943.0 million in 2012 to US$633.9 million in 2013.Net current transfers deteriorated substantially from a recent peak of US$1,233.4 million in 2011 and US$1,097.1 million in 2012, to just US$680.8 million in 2013, driven by a reduction in net public transfers and a substantial fall in net workers’ remittances, from US$140.3 million in 2012 to US$31.1 million in 2013. The fall in remittance outflows, from US$369 million in 2012 to US$255 million in 2013 (likely linked to a reduction in NGOs activities and UNMIL operations), was outweighed by the reduction in inflows, from US$509 million in 2012 to US$297 million in 2013.

The current account deficit is linked in large part to significant capital inflows related to aid, UNMIL, remittances and foreign direct investment (FDI), rather than by unsustainable domestic consumption. While it also reflects weak domestic productive capacity, particularly around agricultural goods (e.g. rice), there is no immediate concern about the build-up of external private debt.

The current account may widen further in 2014 due to further investment related imports, but is expected to narrow over the medium term as these imports unwind and exports, particularly iron ore, rubber and palm oil, rise.

12

1. INTRODUCTION

This report covers key achievements made during the course of 2013 and measures progress against the baseline established in the 2012 Economic Review. The report has slightly expanded in scope and focus as a result of changes in data availability. The completion of the Establishment Survey in 2013 and the commencement of the Household Income Expenditure Survey in January 2014 by LISGIS is expected to significantly contribute to improved data in the near-term, particularly the government’s ability to construct accurate national accounts (required to re-estimate GDP). As data availability and quality improves this will be reflected in future Economic Reviews.

The report focuses on:

The real sector - agriculture and fisheries, forestry, mining and commerce, and industry;

The social services sector - the activities of institutions providing basic social services such as health and sanitation, education, electricity generation and distribution, water and sewage, transportation and the government’s priority projects;

The fiscal sector - the central government operations;

The monetary sector - the changes in interest and inflation rates as well as other monetary developments; and

The external sector - the country’s trade performance and changes in the balance of payments.

The review of social conditions and living standards has selected a few specific variables – from education levels to road completion – to present a picture of the changing living conditions in Liberia. This is a sample of information available intended to provide some overview of the situation. Fiscal data up to quarter 2 of fiscal year 2012/13 is recorded by the Ministry of Finance and the Central Bank, with most data now being captured on automated systems – increasing the accuracy and speed of data access.

This report is not intended as a policy document; it merely sets out the current economic conditions and highlights some areas of growth and potential risks to the economy. The Ministry of Finance would like to thank the Central Bank, Ministries and Agencies and donor partners for their efforts in data provision.

13

2. GLOBAL ECONOMIC DEVELOPMENTS AND OUTLOOK

According to the IMF World Economic Outlook, in 2013 the global economy grew at a rate of 3.0 percent, slightly lower than the 3.1 percent estimate for 2012. This slower global growth is attributed to weaker output in emerging and developing economies, despite the fact that advanced economies have made modest relative gains.

Advanced Economies grew by 1.3 percent in 2013, down from 1.4 percent in 2012. The growth has occurred largely on account of the ease of fiscal consolidation in the USA coupled with the country’s accommodative monetary policy; this resulted in a gradual recovery of the housing sector, easier bank lending conditions and increased borrowing. Owing to the gradual recovery of the US economy coupled with the increased business confidence in the Euro Area, global output for 2014 is projected to grow by 3.7 percent.

Emerging and Developing Economies expanded by 4.7 percent in 2013 as compared to 4.9 percent in 2012. This relatively slower output growth can be attributed to tightening capacity constraints in emerging and developing economies, stabilizing or falling commodity prices which are the major exports of emerging and developing economies. However, growth in emerging and developing economies is projected at 5.1 percent in 2014.

Of the emerging and developing economies, output in Sub-Saharan Africa (SSA) expanded by 5.1 percent in 2013 as compared to 4.8 percent in 2012. Growth in SSA is projected at 6.1 percent in 2014 and 5.8 percent in 2015.

Table 1 provides a comparative analysis of economic growth rates for selected West African countries.

In 2013, world trade volumes increased by 2.9 percent as compared to 2.7 percent in 2012. A more optimistic forecast projects world trade volumes to increase by 4.9 percent in 2014.

Imports of advanced economies increased by 1.5 percent in 2013 as compared to 1.0 percent in 2012 while imports of emerging and developing economies increased by 5.0 percent in 2013 as compared to 5.5 percent in 2012. However, going forward into 2014, imports of advanced economies are projected to increase by 4.0 percent while imports for emerging and developing economies are projected to increase by 5.9 percent.

On the other hand, exports of advanced economies expanded by 2.7 percent in 2013 as compared to 2.0 percent in 2012 while exports of emerging and developing economies increased by 3.5 percent in 2013 as compared to 4.2 percent in 2012. For 2014, exports of advanced economies have been projected to increase by 4.7 percent as compared to 5.8 percent for emerging and developing economies.

Oil prices decreased by 0.5 percent in 2013 as compared to an increase of 1.0 percent in 2012 while prices for non-fuel commodities decreased by 1.5 percent in 2013 as compared to a decrease of 9.9 percent in 2012. For 2014, oil prices are projected to decrease by 3.0 percent while non-fuel prices are projected to decrease by 4.2 percent.

Consumer prices in advanced economies increased by 1.4 percent in 2013 as compared to 2.0 percent in 2012 while in emerging and developing economies, consumer prices increased by 6.2 percent in 2013 as compared to 6.1 percent in 2012. For 2014, consumer prices are projected to increase by 1.8 percent and 5.7 percent respectively for advanced economies and emerging and developing economies.

14

3. DOMESTIC MACROECONOMIC DEVELOPMENTS

From 2006 to 2013, the Liberian economy grew on average by 8.0 percent per annum. In 2013, Liberia’s real Gross Domestic Product (GDP) is estimated to have grown by 8.1 percent, slightly

lower than the 8.3 percent growth recorded in 2012. Real GDP is expected to grow at 5.9 percent in 2014. Table 1 provides trends in Liberia’s real GDP growth rate.

TABLE 1: COMPARATIVE GDP GROWTH RATES FOR SELECTED WEST AFRICAN COUNTRIES

2006 2007 2008 2009 2010 2011 2012 2013 2014 Cote D’Ivoire 0.7 1.6 2.3 3.8 2.4 -4.7 9.8 8.0 8.0 Ghana 6.1 6.5 8.4 4.0 8.0 15.0 7.9 7.9 6.1 Guinea 2.5 1.8 4.9 -0.3 1.9 3.9 3.9 2.9 5.2 Liberia 8.9 13.2 6.2 5.3 6.1 7.9 8.3 8.1 6.8 Niger 5.8 0.6 9.6 -1.0 10.7 2.2 11.2 6.2 6.3 Nigeria 6.2 7.0 6.0 7.0 8.0 7.4 6.6 6.2 7.4 Sierra Leone 4.2 8.0 5.2 3.2 5.3 6.0 15.2 13.3 14.0 Source: World Economic Outlook, October 2013

Liberia’s strong economic performance over preceding years is attributed to the revitalization of economic activities, including from 2011 resumption in iron ore production, and expansion of the construction and services sectors. As a result of the economic expansion, there has been a concomitant rise in government revenue, which increased the fiscal space and enabled the Government to expand the provision of basic social services and fund public sector investment projects (PSIPs), especially infrastructure.

The growth in the mining sector is expected to continue in the medium-term, particularly with the commencement of iron ore exports by China Union and the ramping up of production by Acerlor Mittal, facilitated by government efforts to unlock bottlenecks to concession production.

In 2013, the mining sector accounted for 10 percent of GDP. During the same period, non-resource real GDP grew by 5.2 percent; a

downward revision of the previous estimates due to the sluggish pace of implementation of public investment projects which were in part due to delays in the passage of the National Budget by the Legislator.

In 2006, the Ellen Johnson-Sirleaf led Administration inherited an economy that was hugely driven by activities in the agricultural sector. Since 2006, the Liberian economy has undergone considerable transformation. Over time, there has been a shift in focus from agriculture towards service-led growth. In 2013, the services sector contributed around 42 percent of GDP, while agriculture, fisheries and forestry contributed around 35 percent. The main activities within this sector include trade and hotels, government services, real estate, transportation, communication and construction.

15

3.1 DOMESTIC DEVELOPMENT STRATEGY

Liberia’s domestic development strategies are outlined in two prominent documents; the Agenda for Transformation (AfT) and the Liberia Rising 2030. The AfT is the country’s five-year development plan which serves as a platform for achieving the objectives of the country’s long-term development plan – Liberia Rising 2030. The AfT focuses on investment in five strategic pillars intended to increase productivity, boost economic growth, and improve social inclusion, particularly among the youth. The pillars are:

Peace, Security and the Rule of Law;

Economic Transformation;

Human Development;

Governance and Public Institutions; and

Cross-cutting Issues.

To achieve the objectives of the Agenda for Transformation, the Government continues with the implementation of the Medium Term Expenditure Framework (MTEF). To ensure that key policy objectives are successfully implemented, the Government formulated fiscal rules which are being implemented to guide Government spending of revenue and its borrowing.

3.2 ECONOMIC CHALLENGES

Despite the macroeconomic stability that has prevailed and the successes in supporting the private sector to date, a number of challenges are facing the Liberian economy, including negative demand-shocks related to UNMIL drawdown, difficulties in achieving high rates of public capital expenditure and constraints to business investment and productivity, such as access to finance.

In 2006 agriculture was the largest contributor to GDP. Over time this has shifted towards the services sector, which in 2013 accounted for 42% of GDP, up from 22% in 2006. It is likely that UNMIL and NGOs consume a large proportion of this service sector output. As such, the UNMIL draw-down and arguably lower levels of NGO activity are thought to be causing a slowdown in domestic demand for services – with a corresponding impact on employment and secondary effect on economic activity.

The government is committed to increasing capital expenditure to meet the infrastructure deficit in line with the Public Sector Investment Plan, However, finding the fiscal space to achieve this continues to prove challenging. Government headcount/employees and recurrent spending has continued to rise quickly, with unclear outputs and benefits for the Liberian economy. Headcount has increased from around 38,800 in

FY1983/1984 to 45,600 in FY2006/2007 and 50,500 in FY2012/2013.

As a result, resources available for capital expenditure as part of the PSIP have come under pressure as large recurrent budgets use up resources that could otherwise have gone towards investment projects. In addition, both recurrent and capital expenditure is focused on using foreign rather than local firms and goods and services, leaving government as a weak driver of demand for Liberian products and services.

Although the current binding constraint to private sector investment (and through this, sustainable economic growth) has been identified as infrastructure – particularly energy and roads – and is now a focus of government capital expenditure, access to finance is also likely to be a major barrier to private investment. A significant percentage of Liberian businesses face difficulties in gaining access to finance from financial institutions owing to stringent requirements, including the lack of collateral. Moreover, the tenor of loans provided by financial institutions are relatively short, meaning that businesses may be unable to invest in long-term projects and instead invest in risky short-term projects that may increase the likelihood of loan default and business bankruptcy.

16

3.3 REMOVING BOTTLENECKS TO CONCESSIONAIRES

In order to achieve the growth trajectory necessary for achieving Vision 2030, during 2013 the government made significant efforts to expand the private sector and more importantly to remove the bottlenecks to concessionaires.

The Ministry of Finance facilitated a national dialogue between key ministries, government agencies, NGO’s and concessionaires to remove bottlenecks to production and exportation timelines. These actions could increase capital investment by approximately $7.5 billion, boost tax revenue collection by approximately $400 million per annum, and enhance employment by approximately 80,000-90,000 jobs in the next 10-15 years.

Major strides have been taken to resolve the infrastructure, bureaucratic and community

interest issues facing concessionaires across the board (mining, forestry and palm oil industries) via numerous roundtable discussions between relevant government stakeholders and concessionaires.

In the mining sector, through an inter-Ministerial effort, GoL successfully settled the housing unit issue with China Union, paying US$4 million to former Bong Mines workers and approximately $500,000 to resettle squatters. This enabled China Union to reach its intended production capacity and exportation timeline. Concerned about the slowdown in exports, GoL has targeted logistical bottlenecks in the forestry sector and is signing memorandums with forestry companies, authorizing them to rehabilitate primary roads in exchange for clearance of their tax arrears.

3.4 FISCAL RULES

3.4.1 EXPENDITURE

In the formulation of the 2012/13 and 2013/14 National Budgets, the Government crafted a set of fiscal rules to help guide spending and ensure it is in line with the Government’s priorities. These rules are as follow:

Twenty-five (25) percent of the Budget should be on investment, of which, at least ten (10) percent should be expenditure on the energy sector (i.e. at least 2.5 percent of the Budget);

No more than thirty-four (34) percent of the Budget should be on personnel costs;

At least twenty-five (25) percent of the Government spending should be on Goods and Services provided by Liberian businesses;

At least twenty-five percent of Government spending on furniture should be from capable local manufacturers;

Transfers from investment to recurrent should be no more than five (5) percent of M&A investment appropriations in a given year; and

No more than fifteen (15) percent of capital projects should be administrative overheads.

17

3.4.2 BORROWING

Following the completion of the Heavily Indebted Poor Countries (HIPC) debt relief program in 2010, and the corresponding forgiveness and write-down of around US$4.5 billion debt, the Government put in place fiscal rules as part of the FY2012/2013 and FY2013/2014 Budgets to guide borrowing and ensure that future borrowing is undertaken with fiscal prudence and sustainability in mind:

All borrowing must be undertaken for the purposes of investment, consistent with the Public Sector Investment Plan (PSIP);

Total debt stock must not exceed sixty (60) percent of the given calendar year’s

GDP as contained in the PFM regulations (2009);

Prior to new borrowing being undertaken, a Debt Sustainability Analysis (DSA) must be carried out and presented to the Debt Management Committee (DMC) to ensure debt rules are not breached; and

Individual loans are governed by rules stating that concessional loans are those with a grant element of above thirty-five (35) percent.

3.5 MONETARY POLICY

The Central Bank of Liberia seeks to support macroeconomic and financial stability by formulating and implementing policies geared towards:

Promoting, achieving and maintaining price level stability in the Liberian economy;

Maintaining constant regulatory surveillance and effective prudential controls over the domestic financial sector while at the same time encouraging competition, improving financial services and accessibility for the benefit of the public;

Encouraging the mobilization of domestic as well as foreign savings and

their efficient allocation for productive economic activities to engender sustained economic growth and development;

Facilitating the creation of financial and capital markets that are capable of responding to the needs of the national economy;

Fostering monetary, credit and financial conditions conducive to orderly, balanced and sustained economic growth and development; and

Providing sound economic and financial advice to the Government.

18

4. REAL SECTOR DEVELOPMENTS

Growth in the real sector of the economy has historically been, and remains, driven by concession activities in the agriculture and mining sectors and, more recently, activities in the services sector. Small household farming and artisanal mining activities as well as commercial activities in urban and semi-urban areas by

retailers and other service providers—mainly in Monrovia and a few satellite cities around the country—serve as key contributors to the output of the national economy. This section provides highlights of the major activities ongoing in this sector of the economy for the period under review.

4.1 AGRICULTURE

Agriculture contributes significantly to export trade and earnings and it serves as a major source of livelihood for a significant proportion of Liberia’s population. Based on estimates from the 2008 National Population and Housing Census, about 53 percent of Liberia’s population lives in rural areas of which 70 percent of those who are economically active are engaged in agricultural activities. However, this sector is characterized by the lack of modern technology which means that traditional subsistence farming is prevalent. The most dominant production method of farming in Liberia is slash and burn coupled with mixed crop farming. Other sources of agricultural output for Liberia are commercial and concessional farming.

Agriculture contributed 35 percent of Liberia’s Gross Domestic Product in 2013 with the food crops sub-sector being the most dominant component of the agricultural sector while rubber is the most dominant cash crop produced in Liberia.

Rice is Liberia’s staple food followed by cassava. In 2012, rice production decreased by 2.4 percent compared to 2011; this can be attributed to the increased importation of rice. Cassava production, however, increased significantly, potentially due to the fact that cassava to some extent serves as a substitute for rice.

Looking at a selection of agriculture specific revenue lines (excluding income taxes) shows that revenues generated from the agricultural sector decreased by 10.8 percent between FY2011/12 and FY2012/13 due to a fall in taxes received from levies on exported goods.

TABLE 2: 2013 AGRICULTURAL OUTPUT (US$)

COMMODITY 2011 2012 Cassava 51,500 500,000 Rice, Paddy 298,000 291,000 Sugar Cane 265,000 265,000 Bananas 125,000 127,000 Vegetables, Fresh 84,300 85,000 Rubber, natural 63,000 63,000 Plantains 46,500 47,000 Oil, Palm 42,000 43,500 Taro (cocoyam) 27,000 27,500 Maize, green 23,000 24,500 Sweet potatoes 22,000 23,000 Yams 21,000 21,500 Cocoa, beans 11,700 12,000 Meat indigenous, Chicken 11,421 12,000 Palm kernels 11,000 11,581 Meat indigenous, Pig 9,720 9,800 Oranges 8,000 8,500 Pineapples 8,000 8,250 Meat, game 8,000 8,000 Coconuts 6,500 6,600 Source: Food and Agriculture Organization

19

TABLE 3: REVENUES FROM THE AGRICULTURE SECTOR

4.1.1 DONOR FUNDED PROJECTS IN AGRICULTURE

According to the Global Hunger Index, Liberia remains a highly food insecure country. In an effort to contribute to food security and poverty reduction in Liberia on a sustainable basis, the government along with its international development partners have launched and implemented a number of agricultural projects, detailed below.

TABLE 4: DONOR-FUNDED PROJECTS IN THE AGRICULTURE SECTOR

PROJECT NAME FUNDING TYPE PROJECT COST (US$ MILLION)

PROJECT DURATION

Agriculture Sector Rehabilitation Project (ASRP-AfDB)

Grant 18.30 2010 - 2015

Agriculture Sector Rehabilitation Project (ASRP-IFAD)

Grant 5.00 2010 - 2013

Smallholder Tree Crop Revitalization Support Project (STCRSP-IFAD)

Loan 24.90 2012 - 2017

Smallholder Tree Crop Revitalization Support Project (STCRSP-IDA)

Grant & Loan 23.10 2013 - 2017

West African Agricultural Productivity Project (WAAPP-Liberia) IDA & Japanese Trust Fund)

Grant (Japanese Trust Fund) & Loan (IDA)

14.60 2012 - 2017

Agriculture Infrastructure Development Project (AIDP- IDA)

Grant 8.00 2007 - 2014

Enhancing Resilience to Climate Change by Mainstreaming Adaptation Concerns into Agricultural Sector (GEF-UNDP)

Grant 2.58 2012 - 2016

Smallholder Productivity Enhancement and Commercialization Enhancement (SAPEC) Project (IDA-AfDB)

Grant (GAFSP/WB) & Loan (AfDB)+J8

54.40 2013 - 2018

West Africa Regional Fisheries Project (WARFP) Grants (IDA and GEF) 14.00 2010 - 2014

(Phase I)

Total Resource Mobilized 164.88

Source: PMU, Ministry of Agriculture

4.1.2 AGRICULTURAL CONCESSIONS

Foreign investment in the agricultural sector has increased tremendously since 2006. To date, agricultural concessions cover an operational area

of 1,140,408 hectares. The major cash crop being grown by agricultural concessions are rubber and oil palm.

(US$ '000s) FY11/12 FY12/13

Taxes on export 493 256

Social devt contributions 50 57

Surface rental 450 574

Royalties / fees 0 0

Sign-on bonus 0 0

Total 993 886

Source: Ministry of Finance Note: Figures for selected revenue lines only

20

TABLE 5: AGRICULTURAL CONCESSIONS OPERATING IN LIBERIA

Concession Location Sub-Sector

Libinc Oil Palm Grand Bassa Oil Palm

Equatorial Palm Oil Grand Bassa Oil Palm

Liberia Forest Inc./LFPI (EBF) Sinoe Oil Palm

Decoris Maryland Oil Palm

Golden Veroleum Sinoe Oil Palm

Sime Darby Cape Mount Oil Palm & Rubber

Firestone Plantation Company Margibi Rubber

Salala Rubber Corporation Margibi Rubber

Liberia Agriculture Company Grand Bassa Rubber

Maryland Oil Palm Plantation Maryland Oil Palm

Sinoe Rubber Corporation Sinoe Rubber

Cavalla Rubber Corporation Maryland Rubber

Liberia Company Nimba Rubber

Source: Revenue Department/MOF; MOA

4.2 FORESTRY SUB-SECTOR

Liberia is endowed with a vast and diverse forestry resource which in the past has contributed significantly to economic growth and development. However, a significant challenge facing the forestry sector in the past has been the lack of capacity to manage the resources in a

sustainable manner as most of the forest revenue was used to fund the country’s civil war. This resulted into the imposition of a sanction on timber exports by a resolution of the United Nations.

TABLE 6: LAND USE RIGHTS

Land Use Rights Actually issued

(hectares) Potential to be issued

(hectares) Agricultural Concessions 1,140,408.00 1,140,408.00

Forest Management Concessions (FMC)

1,007,266.00 2,270,097.00

Timber Sale Contracts (TSC) 65,000.00 230,000.00

Community Forest Management Agreements (CFMA)

126,785.00 194,102.00

Mining Concessions 113,256.00 113,256.00

Private Use Permits 2,239,630.00 2,239,630.00

Protected Areas 193,932.00 1,037,865.00

Total 4,886,277.00 7,225,358.00

% of Liberian Land Mass 50.95 75.33 Source: Land Rights, Private Use Permits and Forest Communities; a Land Commission Report

With the ushering in of a democratically elected government in 2006, a Forest Concession Review was conducted to assess the state of the country’s forest concessions, the outcome of which revealed that all forest concessionaires were in

gross violation with the government’s logging regulations and that the total arrears in forest charges amounted to US$64 million. This prompted the issuance of Executive Order #1 in 2006 declaring all existing forest contracts null

21

and void thus setting the basis for the conduct of a forestry reform. In 2006, a new National Forest Reform Law was passed and in 2007 a Forest Strategy was developed.

Based on the new National Forest Reform Law and the Forest Strategy, forest resource licenses were characterized into the following:

Forest Management Contract (FMC): which is granted to forest concessionaires for an operational period of twenty-five years and covers an operational area of around 50,000 to 400,000 hectares excluding private land;

Timber Sale Contract (TSC): which is granted for an operational period of three years and covers an operational area not exceeding not 5,000 hectares and excluding private land;

Private Use Permit (PUP): this is granted to private landowners (individual, group and community) for the purpose of extracting wood. However, there is no specific regulation for handling PUPs thus all PUPs operations are currently suspended;

Forest Use Permit (FUP): this is a forest license issued for small scale forest exploitation, research, NTFP activities or other uses with no detail on land size or land ownership type; and

Community Forest Management Agreement (CFMA): this is a license issued to communities for the purpose of community based forest management and covers an operational area of less than 50 hectares.

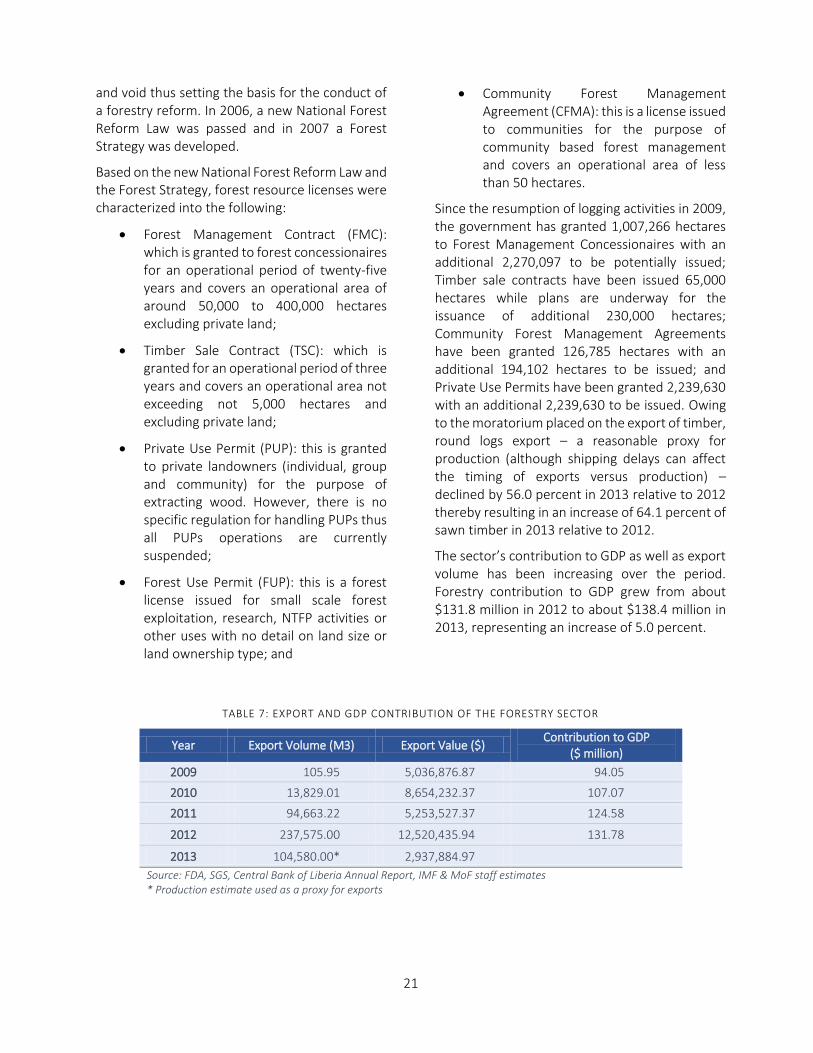

Since the resumption of logging activities in 2009, the government has granted 1,007,266 hectares to Forest Management Concessionaires with an additional 2,270,097 to be potentially issued; Timber sale contracts have been issued 65,000 hectares while plans are underway for the issuance of additional 230,000 hectares; Community Forest Management Agreements have been granted 126,785 hectares with an additional 194,102 hectares to be issued; and Private Use Permits have been granted 2,239,630 with an additional 2,239,630 to be issued. Owing to the moratorium placed on the export of timber, round logs export – a reasonable proxy for production (although shipping delays can affect the timing of exports versus production) – declined by 56.0 percent in 2013 relative to 2012 thereby resulting in an increase of 64.1 percent of sawn timber in 2013 relative to 2012.

The sector’s contribution to GDP as well as export volume has been increasing over the period. Forestry contribution to GDP grew from about $131.8 million in 2012 to about $138.4 million in 2013, representing an increase of 5.0 percent.

TABLE 7: EXPORT AND GDP CONTRIBUTION OF THE FORESTRY SECTOR

Year Export Volume (M3) Export Value ($) Contribution to GDP

($ million)

2009 105.95 5,036,876.87 94.05

2010 13,829.01 8,654,232.37 107.07

2011 94,663.22 5,253,527.37 124.58

2012 237,575.00 12,520,435.94 131.78

2013 104,580.00* 2,937,884.97

Source: FDA, SGS, Central Bank of Liberia Annual Report, IMF & MoF staff estimates * Production estimate used as a proxy for exports

22

Over the course of FY 2012/13, the forestry specific revenues collected from the forestry sector (excluding income taxes) amounted to US$6.6 million, down from US$8.46 million for FY 2011/12, representing a decrease of 22.0 percent.

This fall in revenues from the forestry sector came from lower receipt of export taxes and can be attributed to the poor transport infrastructure affecting the industry.

TABLE 8: REVENUES FROM THE FORESTRY SECTOR

FORESTRY (US$ '000s)

FY11/12 FY12/13

Taxes on export 2,896.77 24.80

Social development contributions 0.00 0.00

Surface rental 982.21 1,571.30

Royalties / fees 4,577.00 4,998.97

Sign-on bonus 0.00 0.00

Total 8,455.97 6,595.07

Source: Ministry of Finance Note: Figures for selected revenue lines only

4.3 COMMERCE AND INDUSTRIES

As the economy continues to diversify, commercial and industrial activities have shown remarkable improvement in the country. In 2013, of the total number of registered businesses in the economy, Liberian-owned businesses accounted for 84.0 percent while foreign owned businesses accounted for 16.0 percent.

Corporations and branches of corporations accounted for 35.3 percent of the registered businesses in Liberia in 2013 of which Liberian-owned businesses accounted for 73.9 percent

while foreign owned businesses accounted for 26.1 percent.

Partnerships and branches of partnership accounted for 6.0 percent of the registered businesses in 2013 of which Liberian-owned partnership accounted for 48.1 percent while foreign-owned partnership accounted for 52.05 percent.

Sole proprietorships accounted for 58.7 percent of the registered businesses in 2013 of which 93.7 percent while foreign-owned sole proprietorships accounted for 6.3 percent.

TABLE 9: BUSINESSES OPERATING IN LIBERIA

Business Category FY 2012 – 2013

Liberian owned Foreign owned Total

Corporations 2,174 646 2,820

Branches of corporations 391 262 653

Partnerships 220 215 435

Branches of partnerships 64 92 156

Sole proprietorships 5,406 362 5,768

Total 8,255 1,577 9,832 Source: Revenue Department, MOF

23

4.3.1 OUTPUT OF THE INDUSTRIAL SECTOR

Liberia’s industrial sector is characterized by light manufacturing. In 2013, cement production increased 49.5 percent. This can be attributed to an increase in activities within the construction sector over the course of 2013.

In 2013, beverages production increased slightly by 4.1 percent. This can be attributed to the increased importation of beverages which serve as substitute for locally produced beverages.

Despite the rapid increase in activities within the construction sector, paint output over the course of 2013 declined by 40.1 percent compared to 2012. The decrease in paint output can in part be attributed to depreciation in the Liberian dollar/US dollar exchange rate which has resulted into the decline in the paint input imports.

Candle production over the course of 2013 declined by 45.3 percent as compared to 2012. This can be attributed to the increased expansion of coverage by the Liberia Electricity Corporation in Monrovia and its environs and in Ganta coupled with the increased use of dry cell lamps.

Chlorox production over the course of 2013 increased by 19.9 percent as compared to 2012; this is linked to the expansion of activities within the services sector as Chlorox is used for hygiene purposes.

In 2013, rubbing alcohol production increased by 14.7 percent as compared to 2012. This may be linked to an increase in demand for the commodity as a result of increased activities in the health sector.

Mattress production in 2013 declined by 7.3 percent as compared to 2012.

Gold production over the course of 2013 declined by 6.4 percent as compared to 2012; this can be attributed to a fall in the global demand for the commodity as the global economy stabilizes owing to the fact that gold is used as a store of value. However, diamond production over the course of 2013 increased by 29.4 percent as compared to 2012; this can be attributed to an increase in the global demand of diamonds.

Iron ore production over the course of 2013 increased by 98.3 percent as compared to 2012; this can be attributed to rapid mechanization of the mining sector.

Finished water production over the course of 2013 increased by 3.3 percent in 2013 as compared to 2012; this can be attributed to an increase in production of beverages and an expansion of activities within the services sector.

TABLE 10: INDUSTRIAL OUTPUT

Commodity

Unit 2011 2012 2013

Cement Mt. 80,594 121,592 181,829

Beverages Liter 30,503,151 28,099,740 29,239,260 Paints Liter 295,179 354,005 212,226

Candle Kg. 442,575 299,229 163,682

Chlorox Liter 694,593 681,160 816,800

Rubbing Alcohol Liter 221,184 198,620 227,901

Mattresses Pcs. 142,000 108,667 100,704 Gold Ounce 14,427 20,609 19,298

Diamond Carat 39,866 34,271 44,334

Iron Ore Mt. 386,968 2,369,850 4,698,281

Finished Water Gallon 930,159,178 1,752,158,793 1,809,781,771

24

4.4 MINING AND PETROLEUM

Mining is a significant sector to the Liberian economy based on the fact that the country is endowed with vast amount of metallic and non-metallic minerals. Liberia’s abundant mineral resources include gold, diamond, iron ore and oil. Since the cessation of hostilities, the country has succeeded in attracting massive foreign direct

investment particularly in the iron ore sector in the tune of US$7.6 billion. This has resulted into the granting of concession agreements to 6 iron ore mining companies, 17 gold and diamond mining companies and petroleum exploration rights to 10 companies. Mining concessions cover an operational area of 113,256 hectares.

TABLE 11: MINERAL EXPLORATION AND MINING COMPANIES OPERATING IN LIBERIA

Petroleum Companies

Oranto Petroleum Woodside West Africa Repsol Exploracian

Woodside West Africa Regal Liberia and European Anadarko Liberia

Oranto Petroleum and Chevron Repsol Exploracian CNOOC International

Broadway Consolidated

Iron Ore Mining Companies

Arcelor Mittal BHP Billiton China Union

Western Cluster Putu Iron Ore Mining

Gold and Diamond Mining Companies

Amlib, Inc. Ascension Resource Corp Hummingbird Resources Inc.

Gold Investment Limited Belle Resources Ltd/SAMLEC Superior Minerals Resources, Inc.

Explorex Oversea, Ltd International Business Exchange Shankil Resources (Liberia) Inc.

Gryphon Minerals Limited Konblo Bumi, Inc. Pedra Mining Corporation

African Gold Mining (Lib) Jamu Resource Incorporated Pedra Mining

Archean Gold Thackett Mining Inc. Middle Island Resources-(Lib)

Source: Revenue Department, MOF

The mining sector’s contribution to the Liberian economy continues to grow. Export earnings from the mining sector in 2013 amounted to US$351.2 million up from US$155.8 million the previous year, representing an increase of 125.4 percent. This has enabled the government to collect more revenues from the sector. In FY 2012/13, government revenues on mining specific tax lines (excluding income taxes) amounted to US$23.4 million, up from US$11.7 million in FY 2011/12, thus representing an increase of 99.8 percent.

For FY 2012 – 2013, mineral royalties accounted for 21.9 percent of the total revenues from the mining sector; surface rental, 7.5 percent; sign-on bonuses, 2.6 percent; and revenues from the mining sector intended for social development, 29.2 percent.

Petroleum sector revenue on petroleum specific tax lines (excluding income taxes) contributed US$58.1 million for FY 2012 – 2013 as compared to US$1.42 million for FY 2011 – 2012.

25

TABLE 12: REVENUES FROM THE MINING SECTOR

Mining (US$ '000s) FY11/12 FY12/13

CIT mining 0.00 0.70

Social development contributions 10,134.00 11,149.00

Surface rental 2,322.00 2,859.96

Royalties 3,932.00 8,367.40

Fees 0.00 67.48

Sign-on bonus 1,400.00 1,000.00

Other (e.g. transfers) 0.00 14,775.00

Total 17,788.00 38,219.55 Source: Ministry of Finance Note: Figures for selected revenue lines only

TABLE 13: REVENUES FROM THE PETROLEUM SECTOR

Petroleum (US$ '000s) FY11/12 FY12/13

CIT petroleum 0.0 162.7

Social development contributions 0.0 8.7

Surface rental 1,418.7 1,500.0

Royalties 0.0 0.0

Sign-on bonus 0.0 0.0

NOCAL 0.0 11,416.9

Other (e.g. transfers) 0.0 45,000.0

Total 1,418.7 58,088.2

Source: Ministry of Finance Note: Figures for selected revenue lines only

4.5 SOCIAL AND BASIC SERVICES

4.5.1 EDUCATION

Education is essential for developing the necessary human capital needed for maintaining and sustaining rapid economic growth and development. Realizing this potential benefit, the government has placed education as a high priority issue along with its development partners. Investment in the sector is intended to increase classroom infrastructure as well as to increase the knowledge and skills of teachers. This is consistent with the 2009 Education Sector Plan, the five-year (2012-2017) Medium Term Plan for Education Reform and Development in Liberia, the Education Reform Act of 2011 and

the draft Technical and Vocational Education and Training (TVET) Policy of 2011. The aim of the government investment in education is five-fold:

To ensure equitable access to free basic education for all children and youth, including the most marginalized in society;

To improve quality, relevance and accessibility of secondary, tertiary, vocational/technical education programs and to alternative basic education programs for out-of-school adolescents and youth;

26

To efficiently strengthen educational services and information management at the national level with focus at the community level;

To improve Parent Teacher Associations (PTA) and national oversights, standards and coordination to ensure quality education; including non-government early child care and development (ECCD) programs for children aged 0 to 5 years; and

To increase the numbers of and improve competencies of teachers in formal schools and alternative basic education programs.

Key achievements recorded in the educational sector in 2013 are:

Successful implementation of an Education Management Information System (EMIS) data collection for the period 2012/2013 that compiles education statistics, personal listings and GIS school verification;

Construction, including the furnishing and equipping with all needed furniture and

equipment, of County Education Offices and Learning Resources Centers in four counties (Bomi, Grand Cape Mount, Gbarpolu and Margibi);

Provision of School Grants for School based management and strengthening of school administrations across the country;

Construction of eight new primary schools in Rivercess, Nimba, Maryland, Lofa, Grand Cape Mount and Gbarpolu and one combined primary and junior high school in Grand Cape Mount. Moreover, thirty-three out of forty schools were renovated in Rivercess, Sinoe, Nimba, Montserrado, Grand Gedeh, Bong and Bomi; and

Development of a diagnostic report on higher education resulting in the formulation of a five-year Higher Education Strategic Plan (HESP) to guide the sector and the decentralization of education. Thus the Grand Gedeh Community College was established with 65 percent of construction work on facilities completed.

4.5.2 HEALTH AND SOCIAL WELFARE

Good health is an important development outcome, with improved health care delivery services bringing broader benefits, including enhanced economic development.

Health impacts economic growth by reducing production losses due to worker illnesses, increasing the productivity of adult as a result of better nutrition, lowering absenteeism rates and improving learning among school children. Moreover, it permits for the use of natural resources that used to be totally or partially inaccessible due to illness and the different use of financial resources that might normally be destined for the treatment of ill health.

The Ministry of Health and Social Welfare in 2011 published the National Health and Social Welfare Policy and Plan 2011-2021 which sets the sector strategy for 2012-2017 and beyond. Consistent

with the strategy, the goal of the heath sector is to improve the health and social welfare status of the population of Liberia on an equitable basis by means of a three-pronged strategic objective:

Increasing access to and utilization of quality health and social welfare services to be delivered to communities endowed with the necessary resources and offering a comprehensive package of interventions of proven effectiveness;

Ensuring that health and social welfare services are more responsive to people’s needs, demands and expectations by transferring management and decision making in order to lower administration levels thus ensuring a fair degree of equity;

27

Ensuring that health care and social protection available to all of Liberia’s population, regardless of an individual’s position in society, at a cost that is affordable to the country.

Combined efforts by the government and its development partners to improve the country’s health systems have resulted in:

An increase in the percentage of deliveries assisted by skilled birth attendants;

An increase in the number of families with access to family planning;

An increase in the percentage of children under the age of one year who received DPT3/pentavalent-3 vaccination;

An increase in the out-patient-delivery (OPD) consultations per inhabitant per year;

An increase in the percentage of pregnant women provided with second dose of IPT for malaria;

An increase in the percentage of pregnant women testing HIV+ that are receiving ARV prophylaxis to reduce mother-to-child-transmission (MTCT);

A reduction in the number of smear positive TB cases notified per 100,000 population;

An increase in the number of skilled birth attendants (physicians, nurses, midwives and physician assistants) per 10,000 population;

An increase in the percentage of facilities with no stock-out of tracer drug during the period (amoxicillin, cotrimoxazole, paracetamol, ORS, iron folate, ACT and FP commodity).

The Malaria Control Program successfully distributed 1,000,000 long lasting mosquito nets to the general population and pregnant women attending antenatal clinics in six counties. Moreover, an in-door spraying exercise of 40,000 rural households along with an awareness campaign on malaria prevention and distribution

of tracer drugs to all public health facilities was conducted during the period under review.

In an attempt to improve the eye sight of the citizenry, 23,959 persons were provided health services with respect to cataract surgery, trauma, glaucoma, refractive error and other eye condition while 5,711 persons were provided mental health services to treat anxiety disorder, mood disorder, impulse control, substance abuse, etc.).

In an attempt to increase the expansion of health services so as to improve access to the delivery of under skilled birth attendants for pregnant women with poor geographic access,

Three maternal waiting rooms and four maternal wings were constructed at various health facilities;

Five microscopic laboratories were constructed in five counties;

Eight incinerators were constructed to improve waste management and sanitation at eight health facilities;