Embed Size (px)

Citation preview

Annual Compilation Update 2014

A RealisticApproach Seminars Conference Presentation

Topics to be Covered by Today’s Session

1. Statement on Standards for Accounting and Review Services (SSARS) No. 19, Compilation and Review Engagements A. Chapter 1 – Framework for Performing and

Reporting on Compilation and Review Engagements B. Chapter 2 – Compilation of Financial Statements

A RealisticApproach Seminar Presentation 2

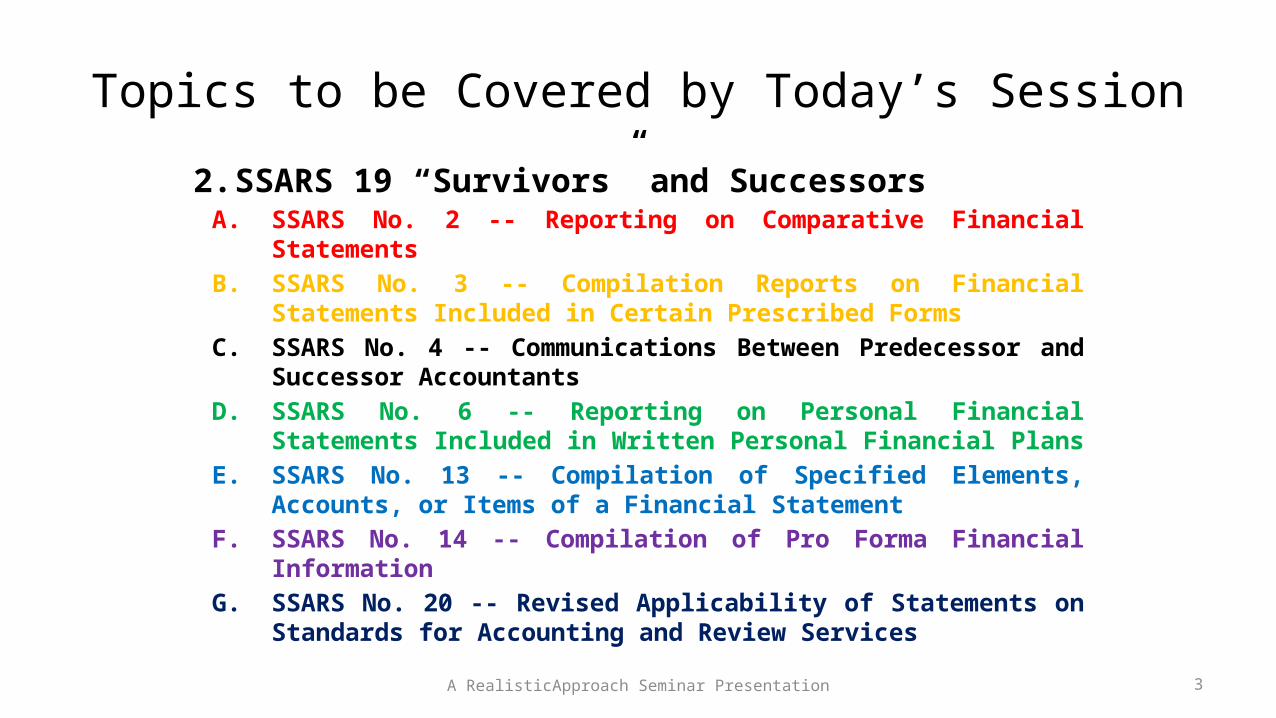

Topics to be Covered by Today’s Session2. SSARS 19 “Survivors” and Successors

A. SSARS No. 2 -- Reporting on Comparative Financial Statements B. SSARS No. 3 -- Compilation Reports on Financial Statements

Included in Certain Prescribed Forms C. SSARS No. 4 -- Communications Between Predecessor and

Successor Accountants D. SSARS No. 6 -- Reporting on Personal Financial Statements

Included in Written Personal Financial Plans E. SSARS No. 13 -- Compilation of Specified Elements, Accounts, or

Items of a Financial Statement F. SSARS No. 14 -- Compilation of Pro Forma Financial Information G. SSARS No. 20 -- Revised Applicability of Statements on

Standards for Accounting and Review Services A RealisticApproach Seminar Presentation 3

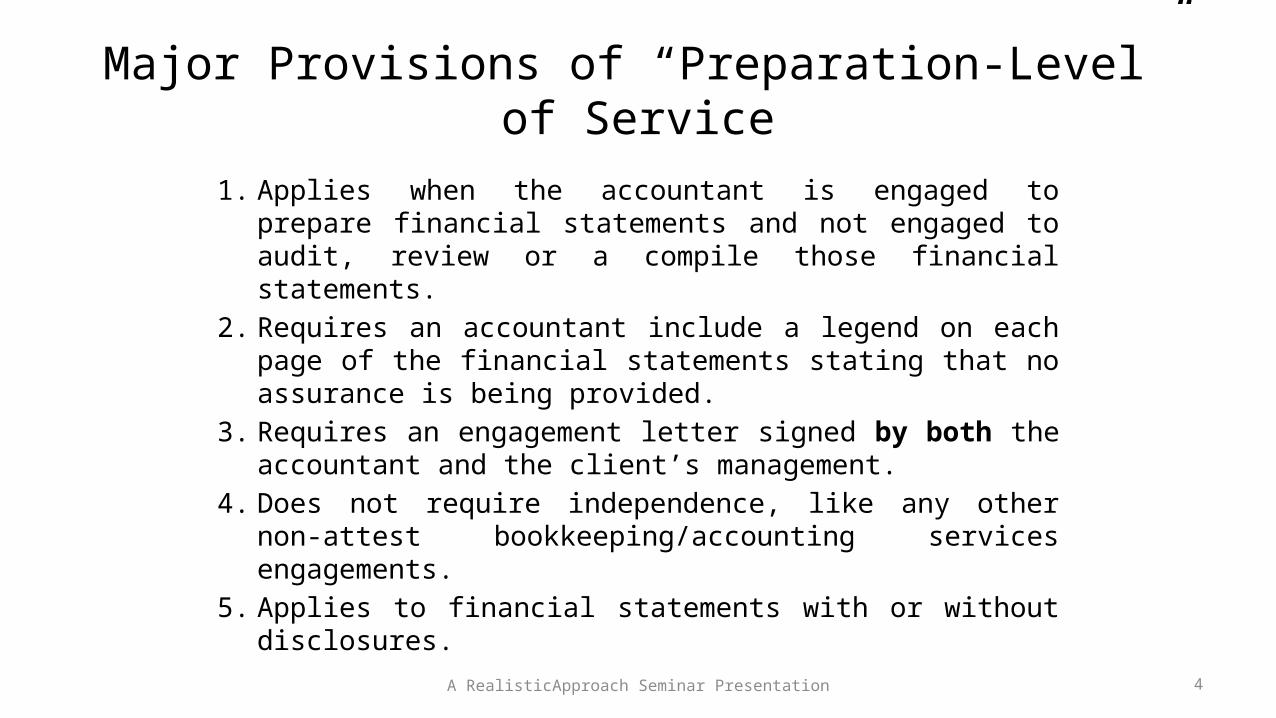

Major Provisions of “Preparation-Level” of Service

1. Applies when the accountant is engaged to prepare financial statements and not engaged to audit, review or a compile those financial statements.

2. Requires an accountant include a legend on each page of the financial statements stating that no assurance is being provided.

3. Requires an engagement letter signed by both the accountant and the client’s management.

4. Does not require independence, like any other non-attest bookkeeping/accounting services engagements.

5. Applies to financial statements with or without disclosures.

A RealisticApproach Seminar Presentation 4

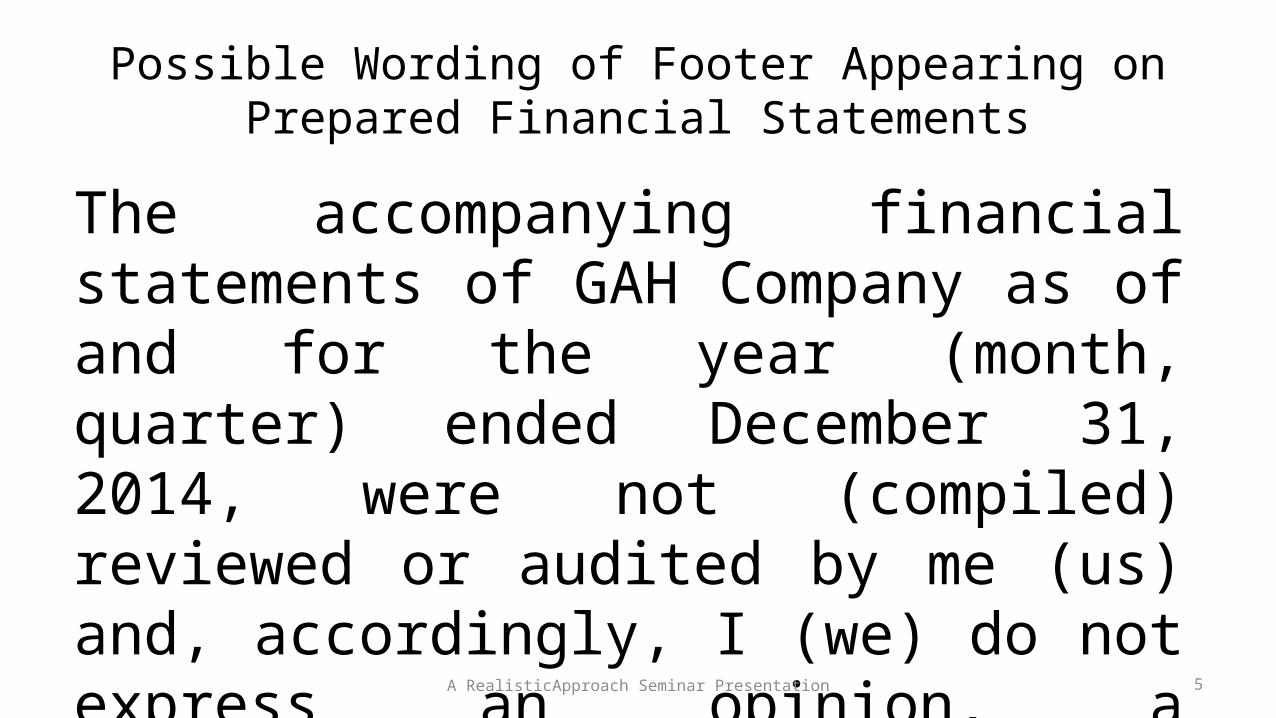

Possible Wording of Footer Appearing on Prepared Financial Statements

The accompanying financial statements of GAH Company as of and for the year (month, quarter) ended December 31, 2014, were not (compiled) reviewed or audited by me (us) and, accordingly, I (we) do not express an opinion, a conclusion, nor provide any assurance on them.

A RealisticApproach Seminar Presentation 5

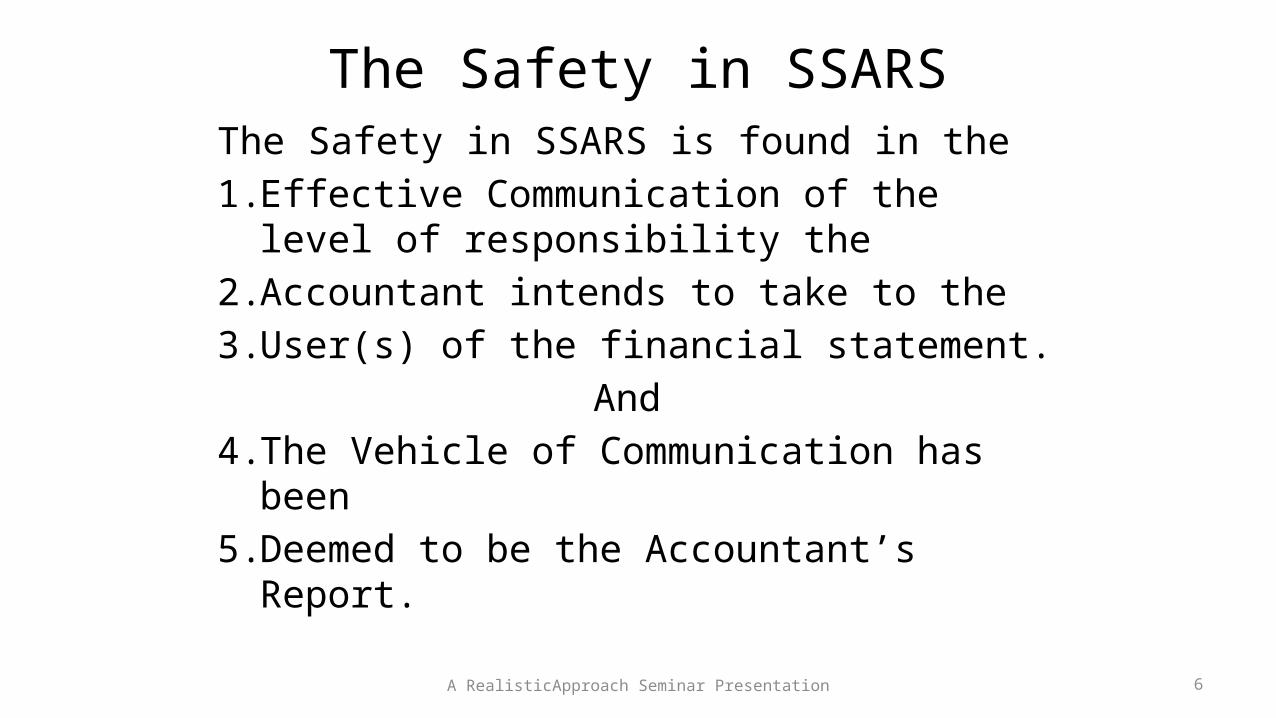

The Safety in SSARSThe Safety in SSARS is found in the1. Effective Communication of the level of

responsibility the2. Accountant intends to take to the3. User(s) of the financial statement.

And 4. The Vehicle of Communication has been 5. Deemed to be the Accountant’s Report.

A RealisticApproach Seminar Presentation 6

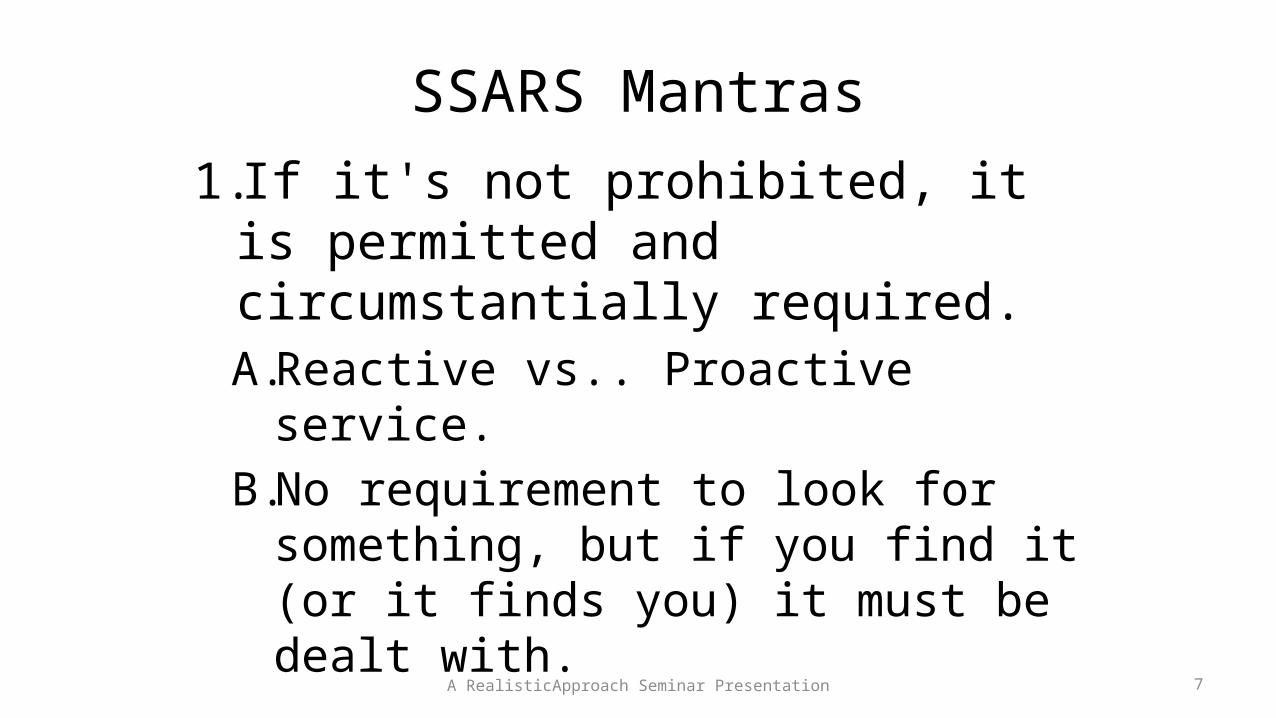

SSARS Mantras

1.If it's not prohibited, it is permitted and circumstantially required. A.Reactive vs.. Proactive service. B. No requirement to look for

something, but if you find it (or it finds you) it must be dealt with.

A RealisticApproach Seminar Presentation 7

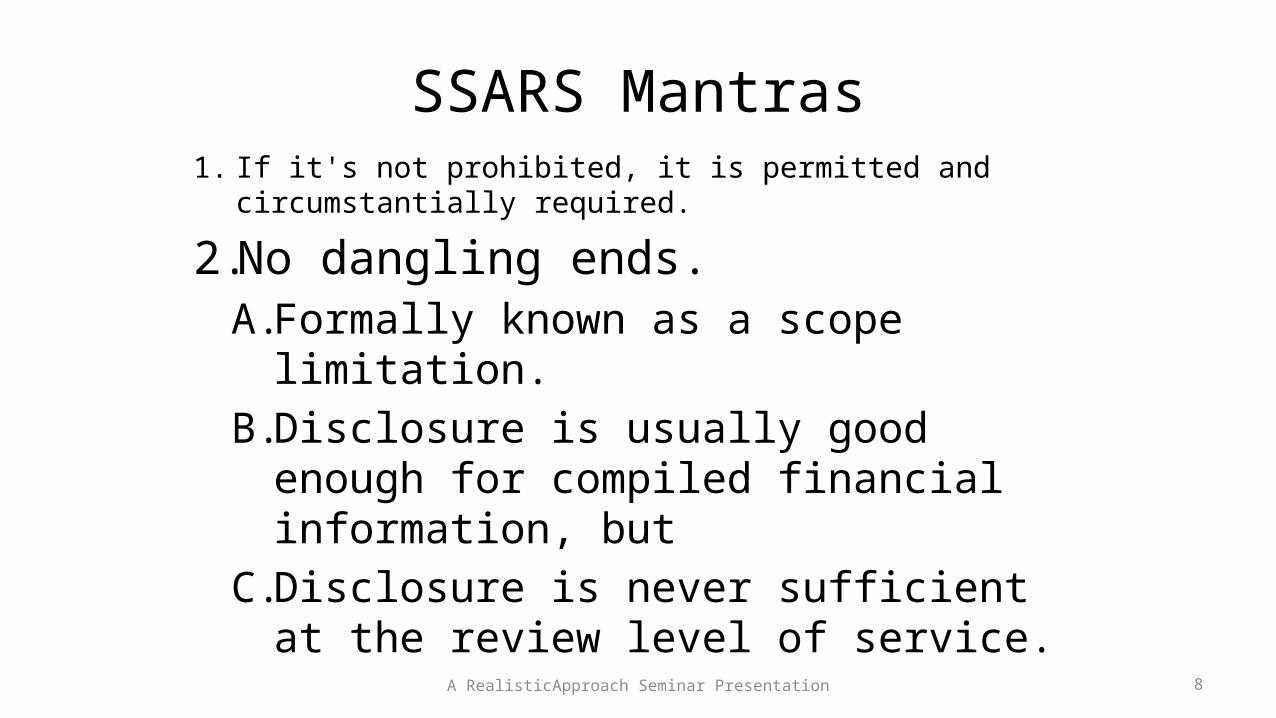

SSARS Mantras1. If it's not prohibited, it is permitted and circumstantially

required.

2. No dangling ends. A. Formally known as a scope limitation.B. Disclosure is usually good enough for

compiled financial information, butC. Disclosure is never sufficient at the

review level of service.A RealisticApproach Seminar Presentation 8

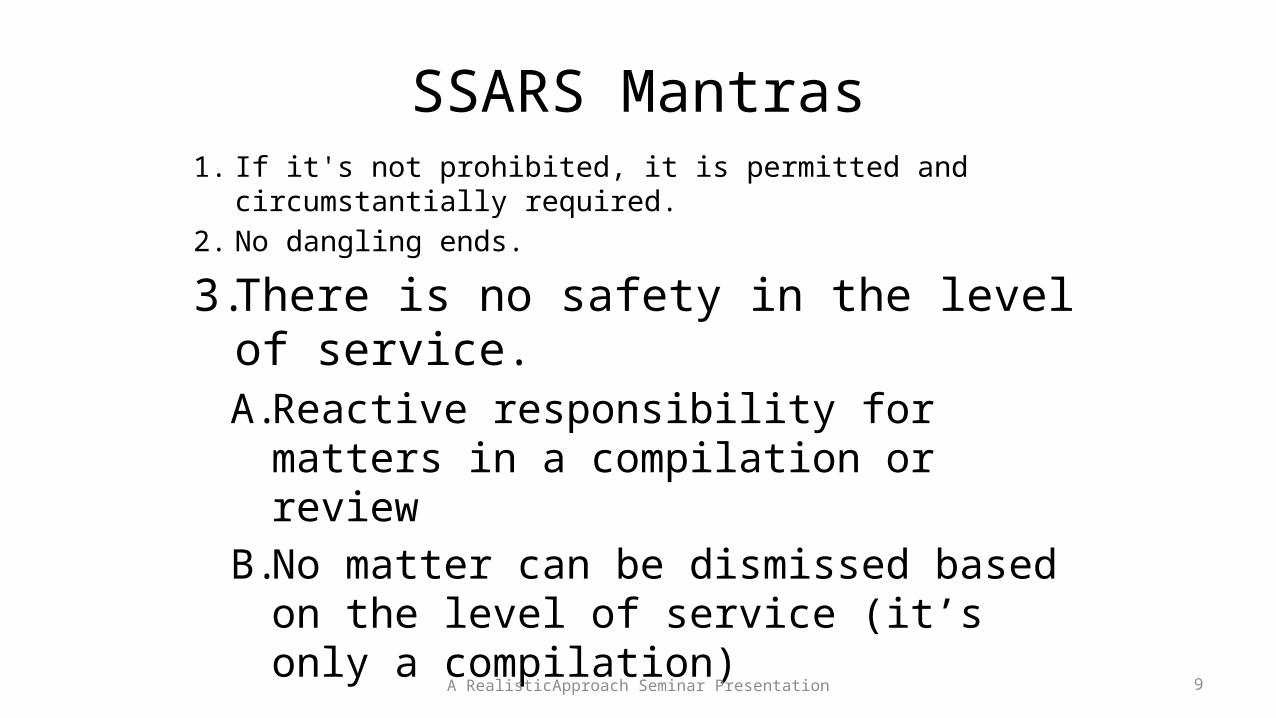

SSARS Mantras1. If it's not prohibited, it is permitted and circumstantially

required. 2. No dangling ends.

3. There is no safety in the level of service. A. Reactive responsibility for matters in a

compilation or review B. No matter can be dismissed based on the

level of service (it’s only a compilation)A RealisticApproach Seminar Presentation 9

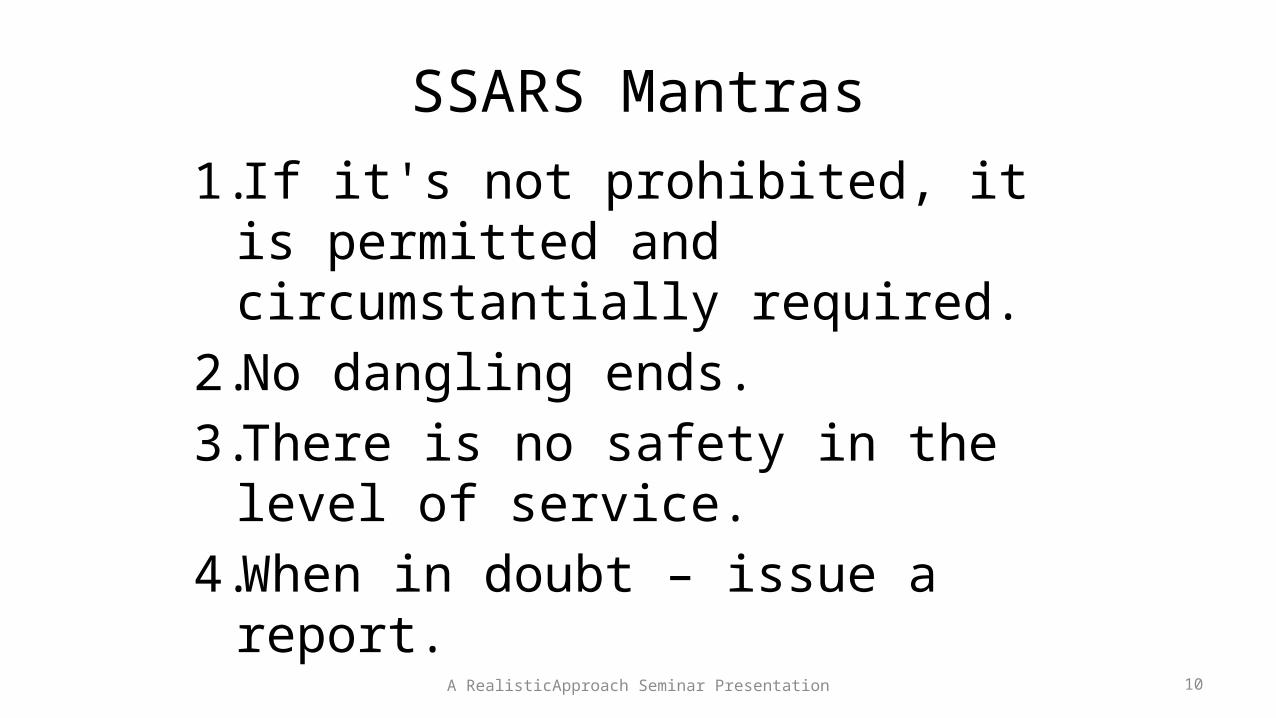

SSARS Mantras

1. If it's not prohibited, it is permitted and circumstantially required.

2. No dangling ends. 3. There is no safety in the level of

service. 4. When in doubt – issue a report.

A RealisticApproach Seminar Presentation 10

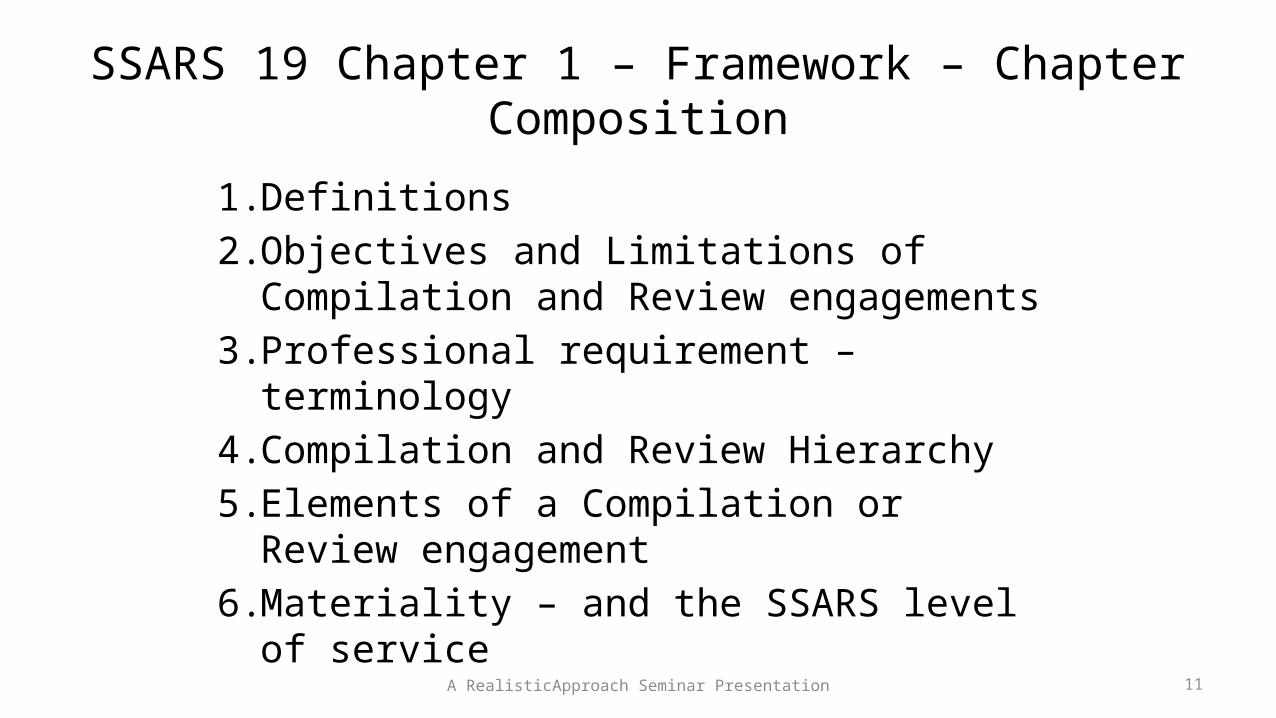

SSARS 19 Chapter 1 – Framework – Chapter Composition

1. Definitions 2. Objectives and Limitations of Compilation

and Review engagements 3. Professional requirement – terminology 4. Compilation and Review Hierarchy 5. Elements of a Compilation or Review

engagement 6. Materiality – and the SSARS level of service

A RealisticApproach Seminar Presentation 11

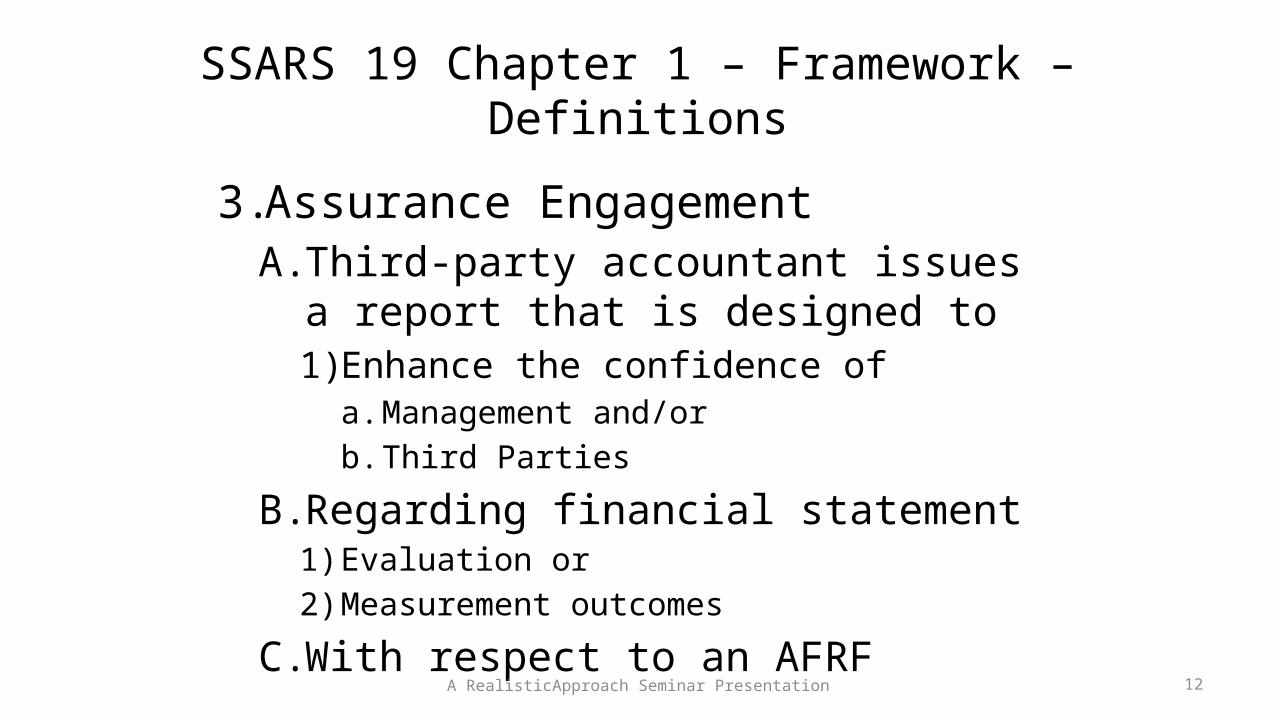

SSARS 19 Chapter 1 – Framework – Definitions

3. Assurance Engagement A. Third-party accountant issues a report

that is designed to1) Enhance the confidence of

a. Management and/orb. Third Parties

B. Regarding financial statement 1) Evaluation or 2) Measurement outcomes

C. With respect to an AFRFA RealisticApproach Seminar Presentation 12

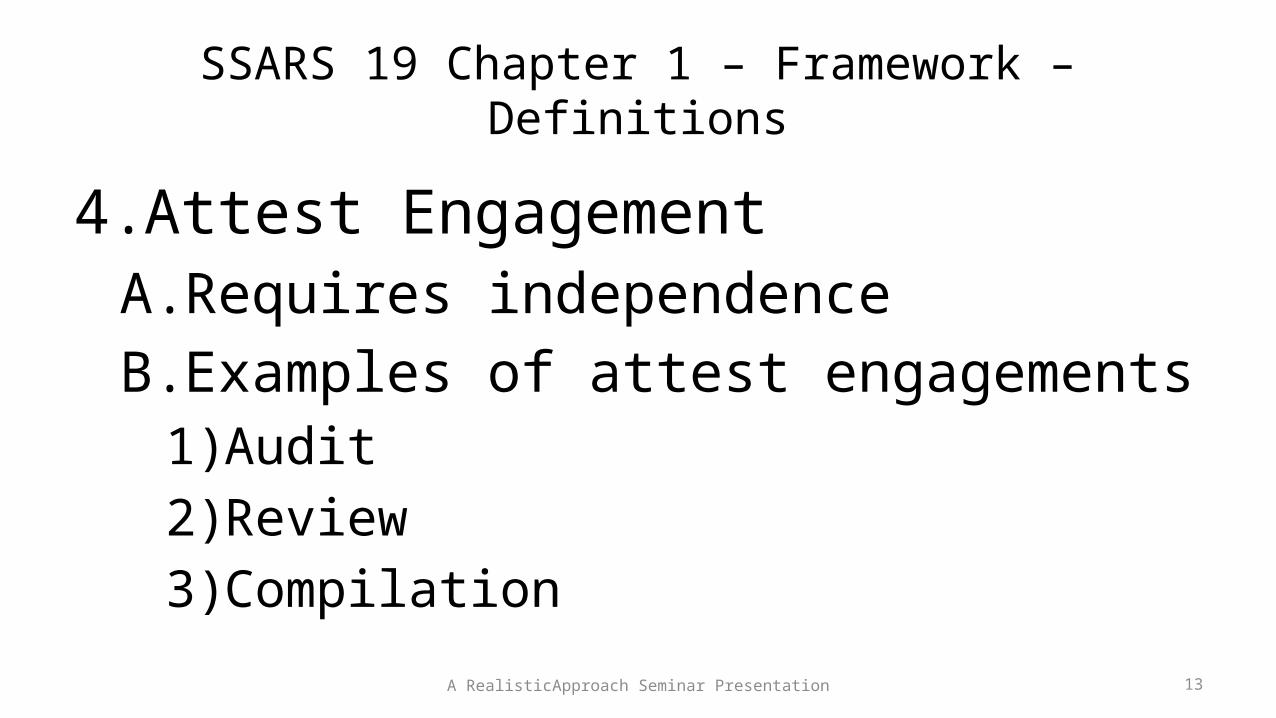

SSARS 19 Chapter 1 – Framework – Definitions

4.Attest Engagement A.Requires independenceB. Examples of attest engagements

1)Audit2)Review 3)Compilation

A RealisticApproach Seminar Presentation 13

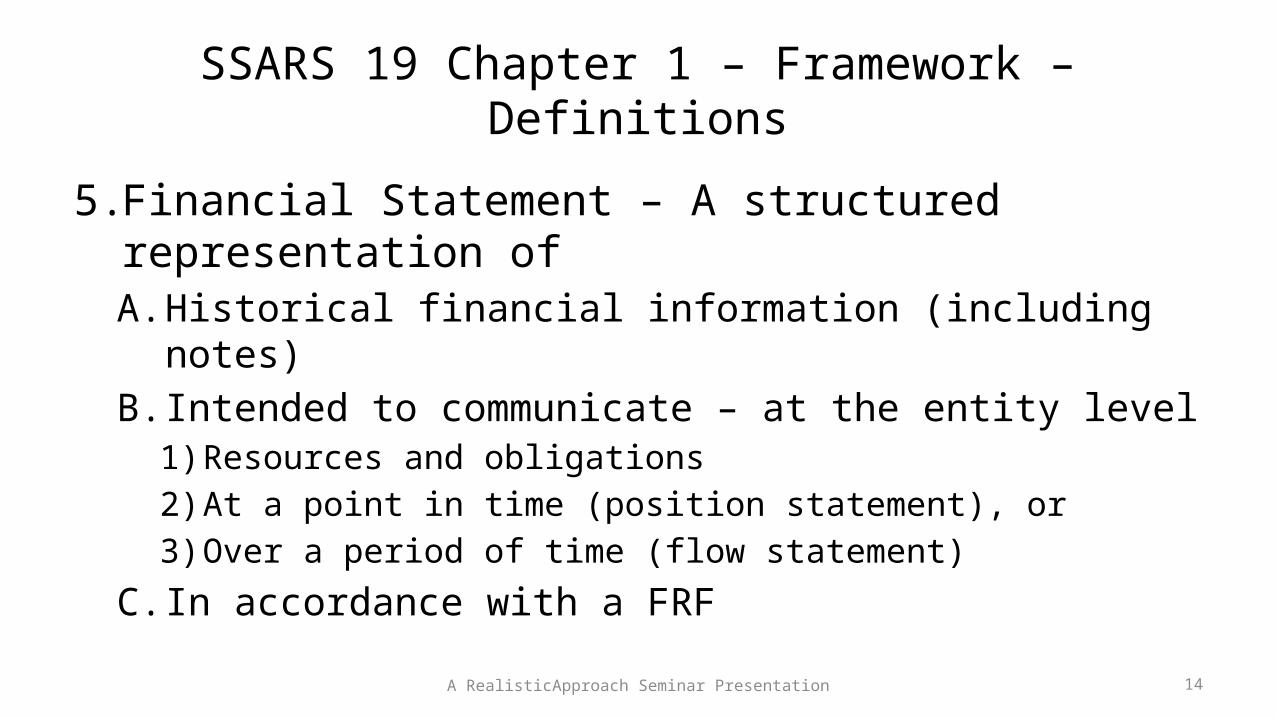

SSARS 19 Chapter 1 – Framework – Definitions

5. Financial Statement – A structured representation of A. Historical financial information (including notes) B. Intended to communicate – at the entity level

1) Resources and obligations 2) At a point in time (position statement), or 3) Over a period of time (flow statement)

C. In accordance with a FRF

A RealisticApproach Seminar Presentation 14

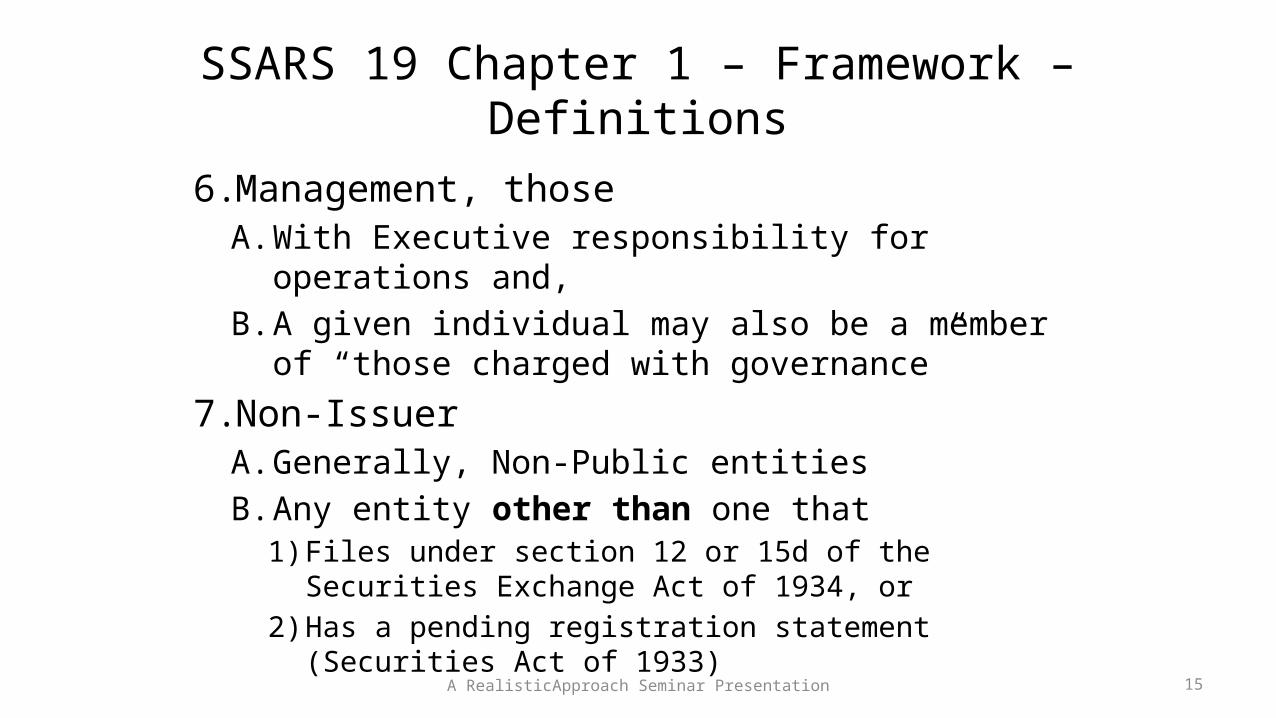

SSARS 19 Chapter 1 – Framework – Definitions

6. Management, thoseA. With Executive responsibility for operations and, B. A given individual may also be a member of “those

charged with governance”

7. Non-Issuer A. Generally, Non-Public entitiesB. Any entity other than one that

1) Files under section 12 or 15d of the Securities Exchange Act of 1934, or

2) Has a pending registration statement (Securities Act of 1933) A RealisticApproach Seminar Presentation 15

SSARS 19 Chapter 1 – Framework – Definitions

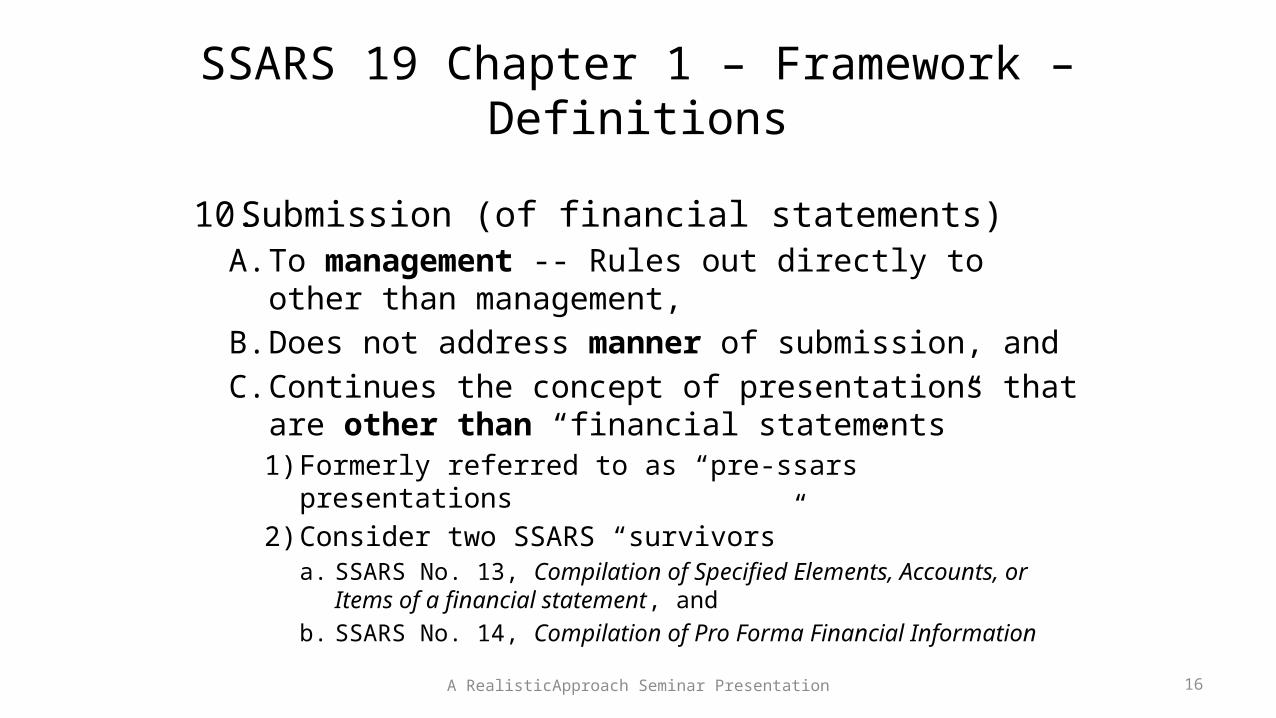

10.Submission (of financial statements)A. To management -- Rules out directly to other than

management, B. Does not address manner of submission, and C. Continues the concept of presentations that are

other than “financial statements” 1) Formerly referred to as “pre-ssars” presentations 2) Consider two SSARS “survivors”

a. SSARS No. 13, Compilation of Specified Elements, Accounts, or Items of a financial statement, and

b. SSARS No. 14, Compilation of Pro Forma Financial Information A RealisticApproach Seminar Presentation 16

SSARS 19 Chapter 1 – Framework – Definitions

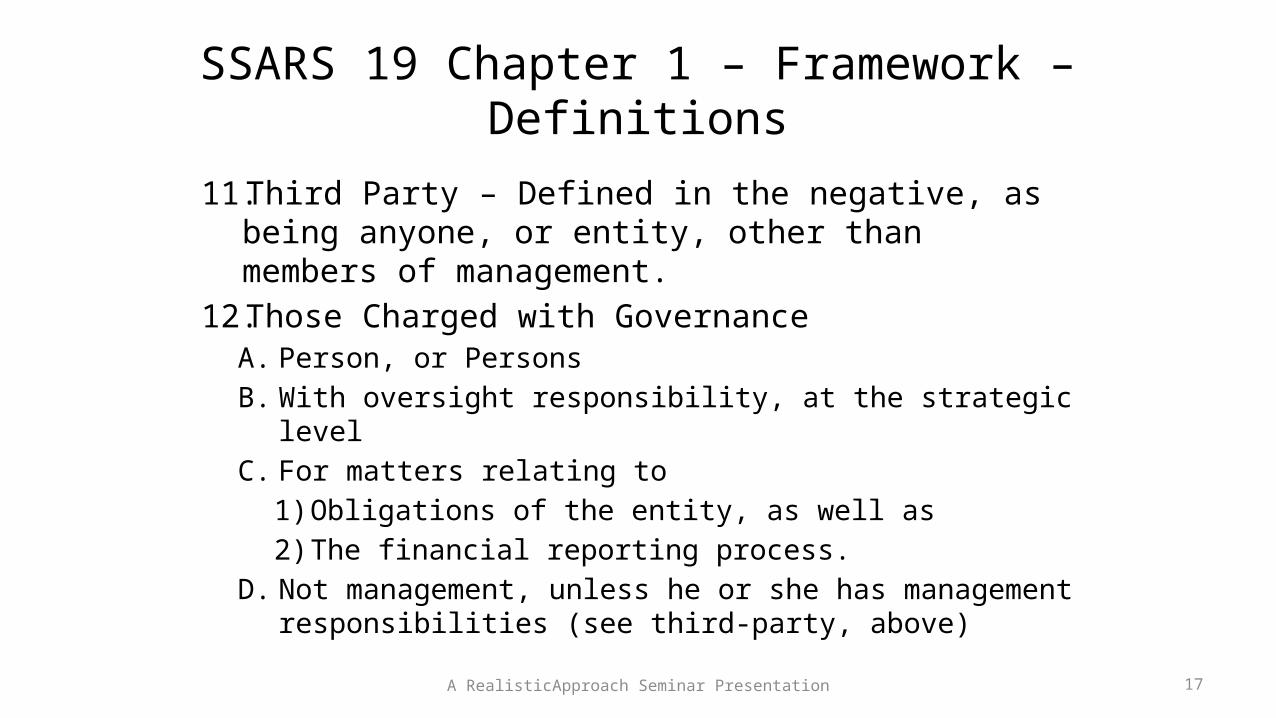

11.Third Party – Defined in the negative, as being anyone, or entity, other than members of management.

12.Those Charged with Governance A. Person, or Persons B. With oversight responsibility, at the strategic level C. For matters relating to

1) Obligations of the entity, as well as2) The financial reporting process.

D. Not management, unless he or she has management responsibilities (see third-party, above)

A RealisticApproach Seminar Presentation 17

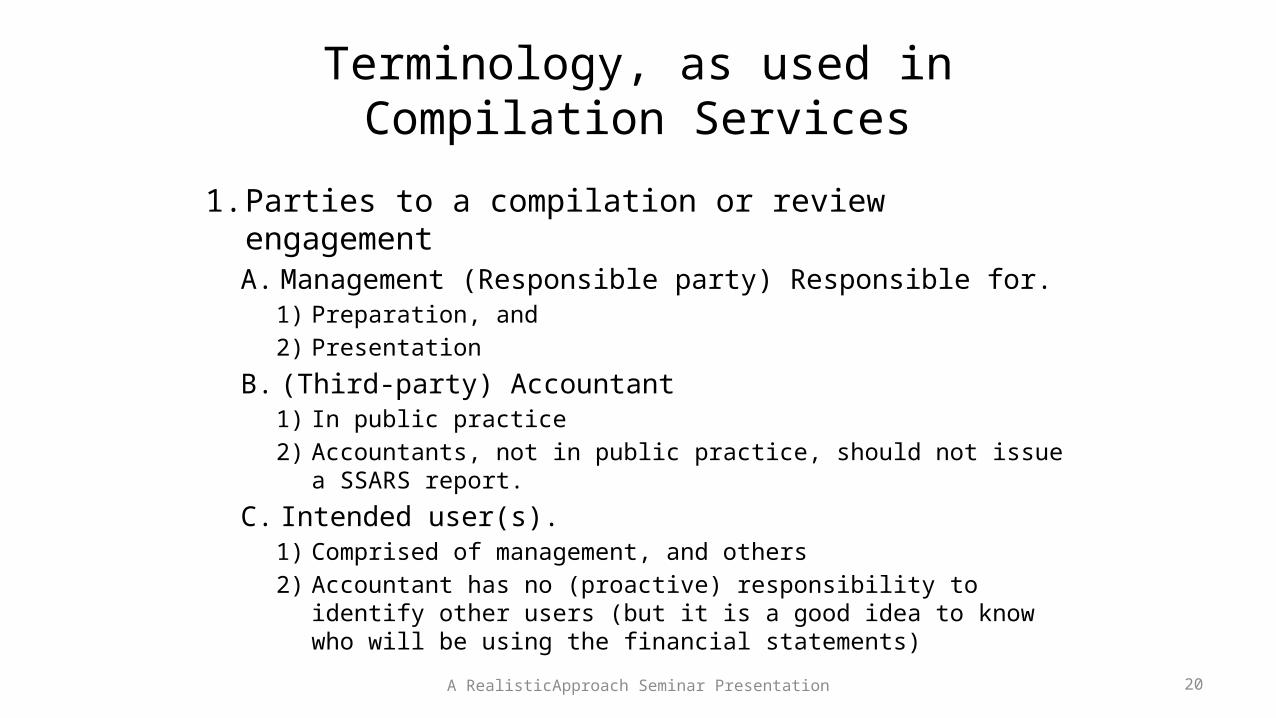

Terminology, as used inCompilation and Review Services

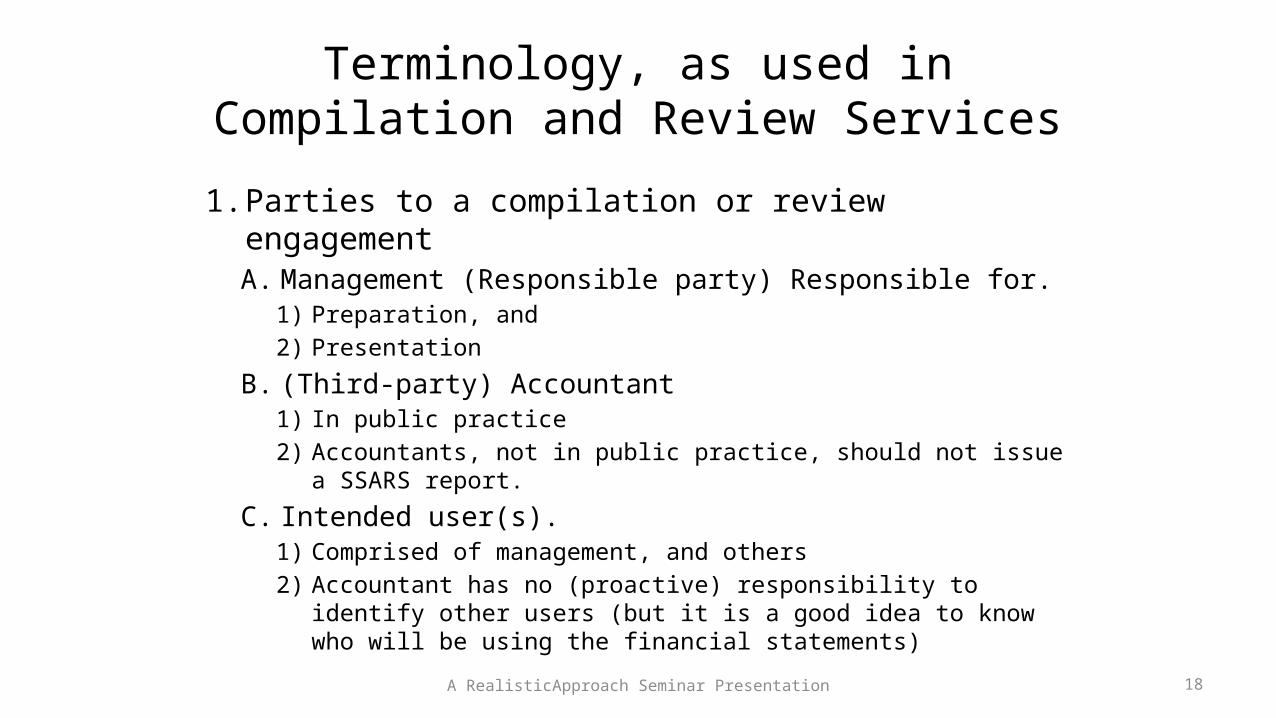

1. Parties to a compilation or review engagement A. Management (Responsible party) Responsible for.

1) Preparation, and 2) Presentation

B. (Third-party) Accountant 1) In public practice 2) Accountants, not in public practice, should not issue a SSARS

report.

C. Intended user(s). 1) Comprised of management, and others 2) Accountant has no (proactive) responsibility to identify other

users (but it is a good idea to know who will be using the financial statements)A RealisticApproach Seminar Presentation 18

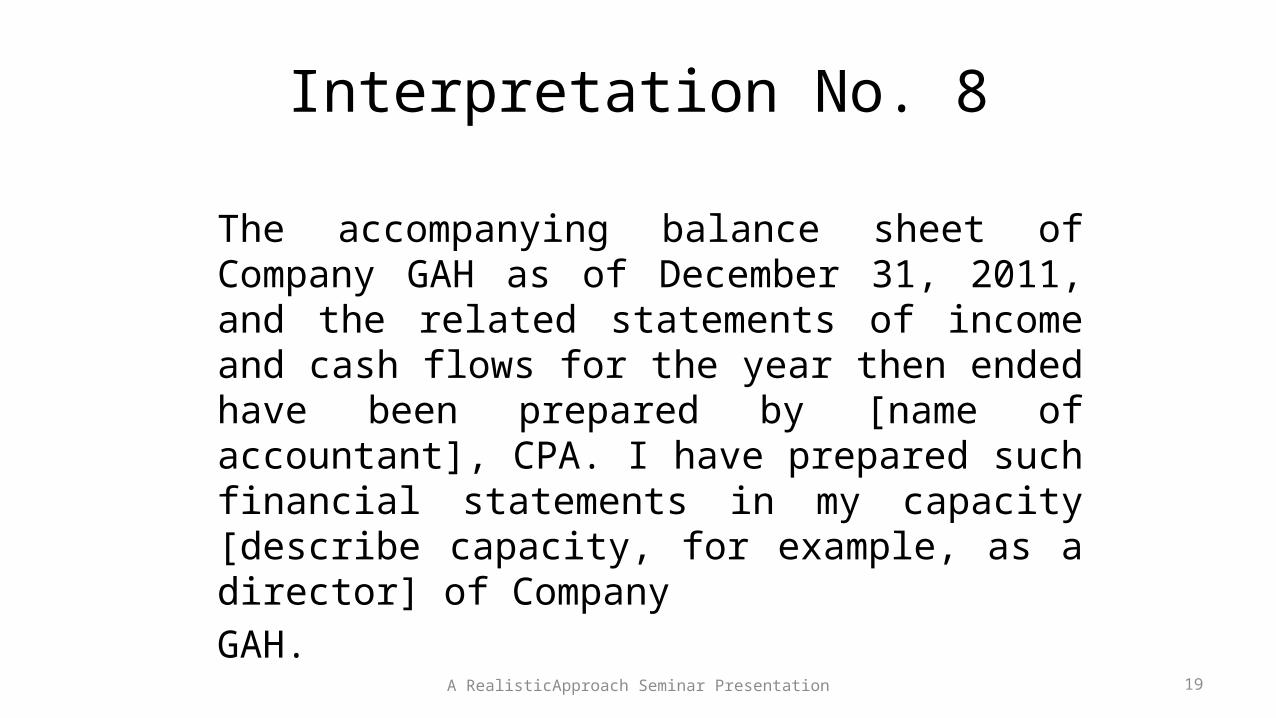

Interpretation No. 8

The accompanying balance sheet of Company GAH as of December 31, 2011, and the related statements of income and cash flows for the year then ended have been prepared by [name of accountant], CPA. I have prepared such financial statements in my capacity [describe capacity, for example, as a director] of CompanyGAH.

A RealisticApproach Seminar Presentation 19

Terminology, as used inCompilation Services

1. Parties to a compilation or review engagement A. Management (Responsible party) Responsible for.

1) Preparation, and 2) Presentation

B. (Third-party) Accountant 1) In public practice 2) Accountants, not in public practice, should not issue a SSARS

report.

C. Intended user(s). 1) Comprised of management, and others 2) Accountant has no (proactive) responsibility to identify other

users (but it is a good idea to know who will be using the financial statements)A RealisticApproach Seminar Presentation 20

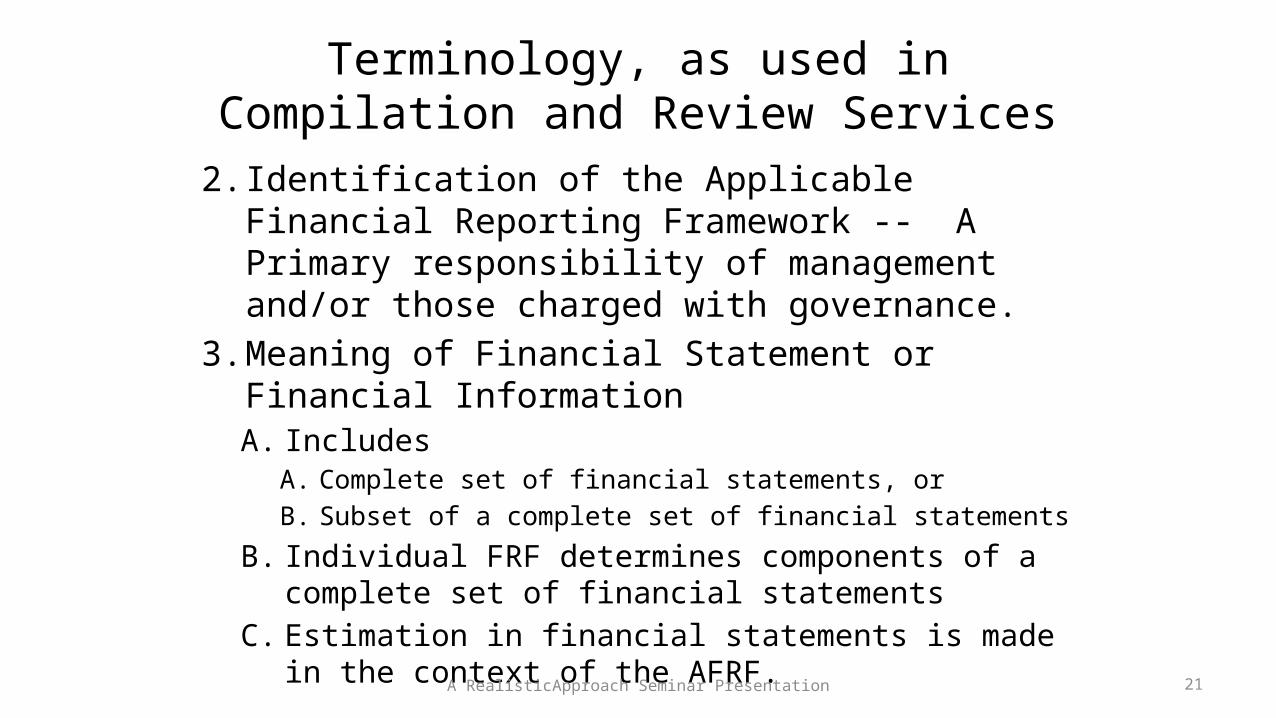

Terminology, as used inCompilation and Review Services

2. Identification of the Applicable Financial Reporting Framework -- A Primary responsibility of management and/or those charged with governance.

3. Meaning of Financial Statement or Financial InformationA. Includes

A. Complete set of financial statements, orB. Subset of a complete set of financial statements

B. Individual FRF determines components of a complete set of financial statements

C. Estimation in financial statements is made in the context of the AFRF. A RealisticApproach Seminar Presentation 21

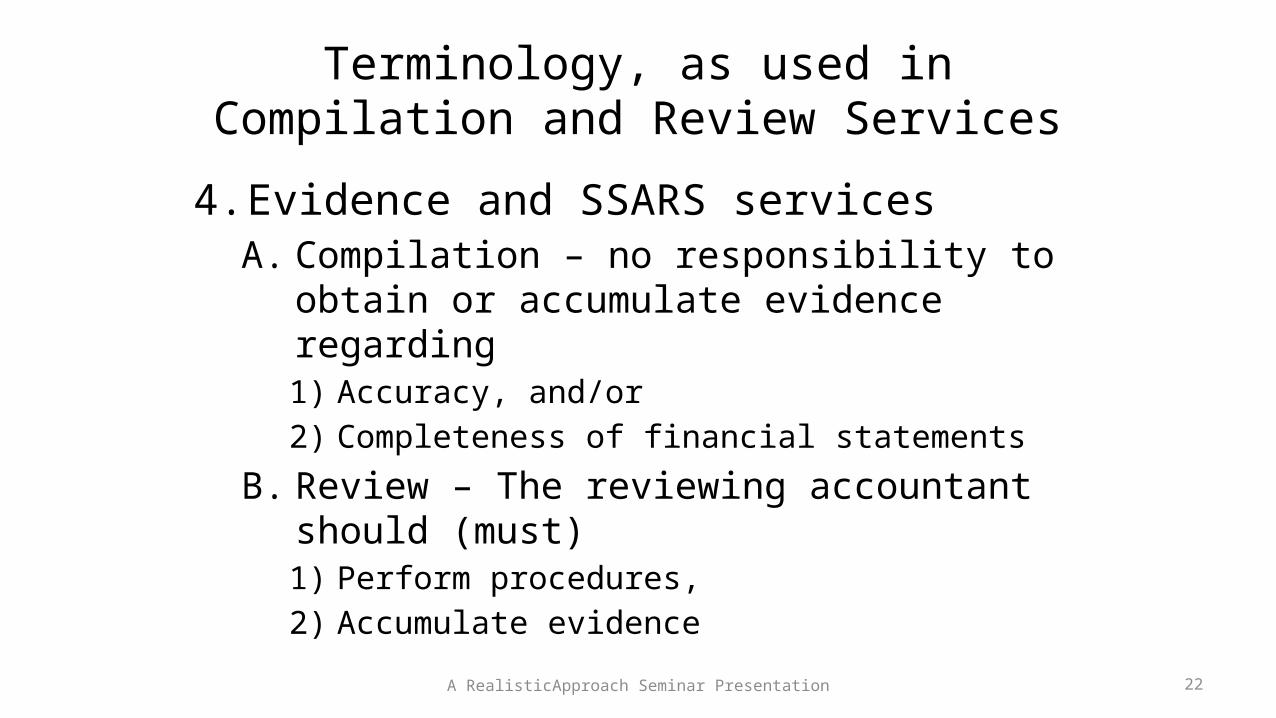

Terminology, as used inCompilation and Review Services

4. Evidence and SSARS services A. Compilation – no responsibility to obtain or

accumulate evidence regarding1) Accuracy, and/or2) Completeness of financial statements

B. Review – The reviewing accountant should (must)1) Perform procedures, 2) Accumulate evidence

A RealisticApproach Seminar Presentation 22

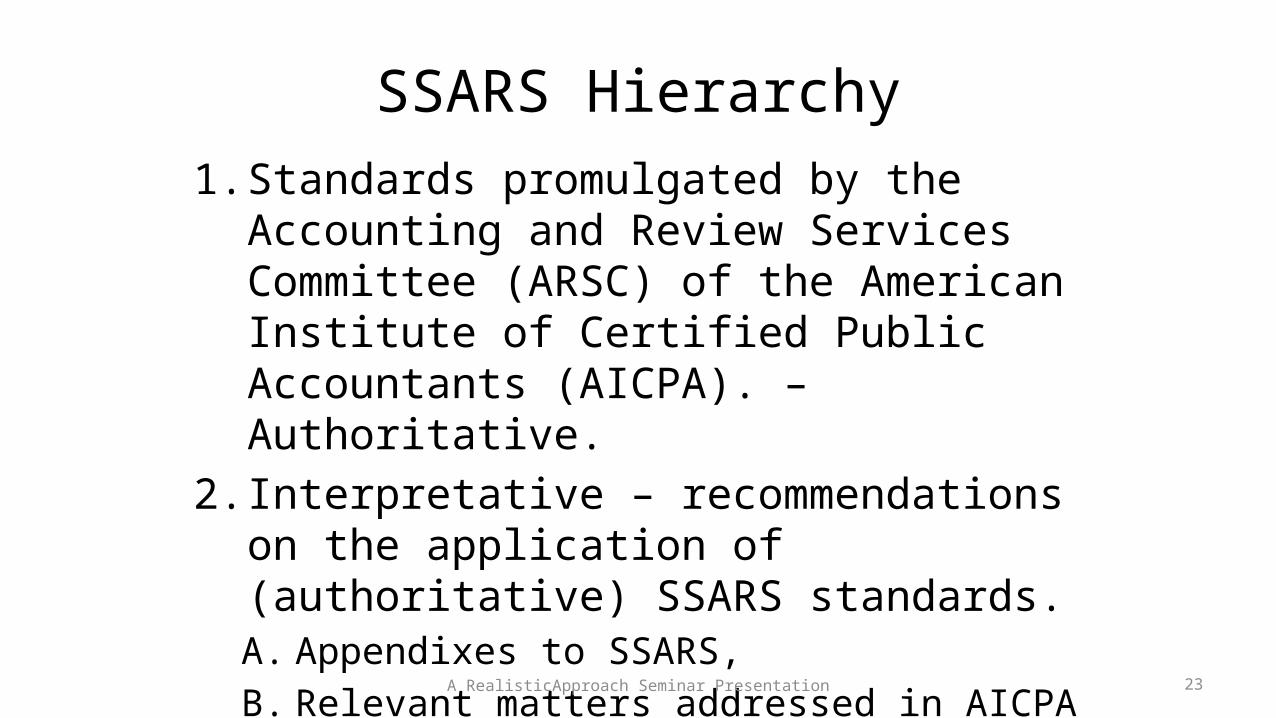

SSARS Hierarchy1. Standards promulgated by the Accounting and

Review Services Committee (ARSC) of the American Institute of Certified Public Accountants (AICPA). – Authoritative.

2. Interpretative – recommendations on the application of (authoritative) SSARS standards. A. Appendixes to SSARS, B. Relevant matters addressed in AICPA Audit and

Accounting Guides, andC. AICPA Statements of Position

A RealisticApproach Seminar Presentation 23

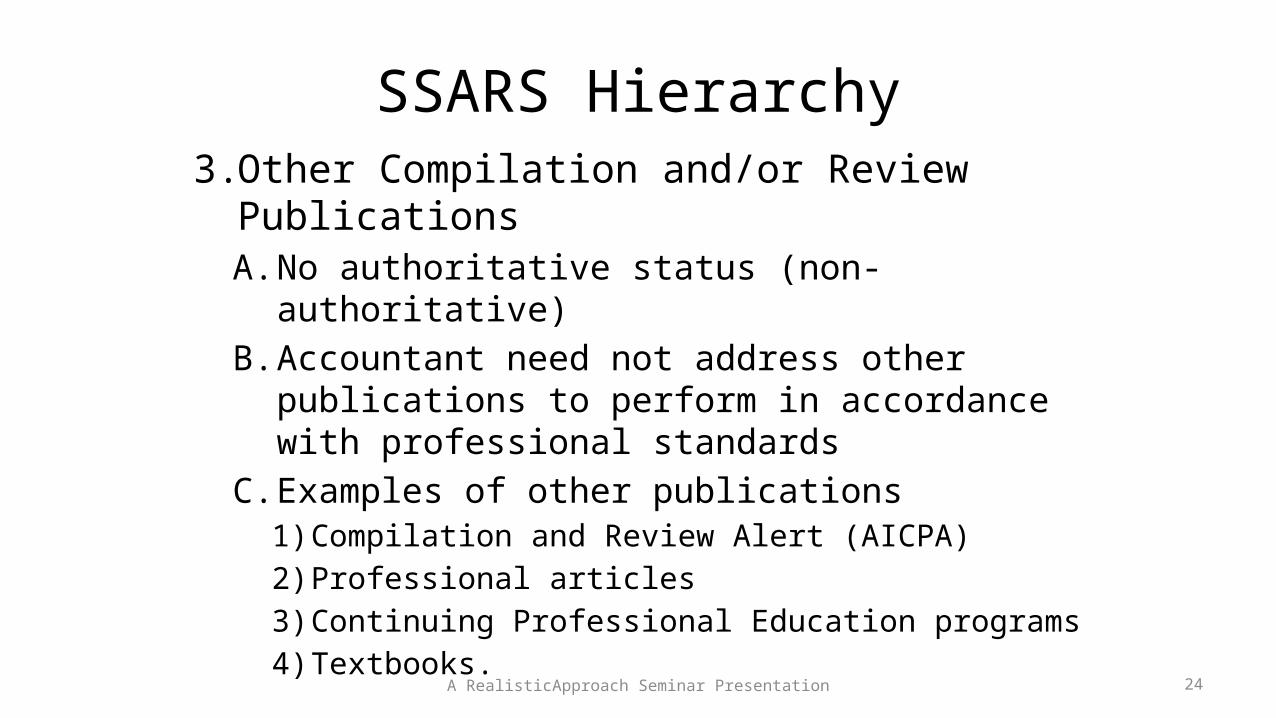

SSARS Hierarchy3. Other Compilation and/or Review

Publications A. No authoritative status (non-authoritative) B. Accountant need not address other publications

to perform in accordance with professional standards

C. Examples of other publications1) Compilation and Review Alert (AICPA)2) Professional articles 3) Continuing Professional Education programs 4) Textbooks. A RealisticApproach Seminar Presentation 24

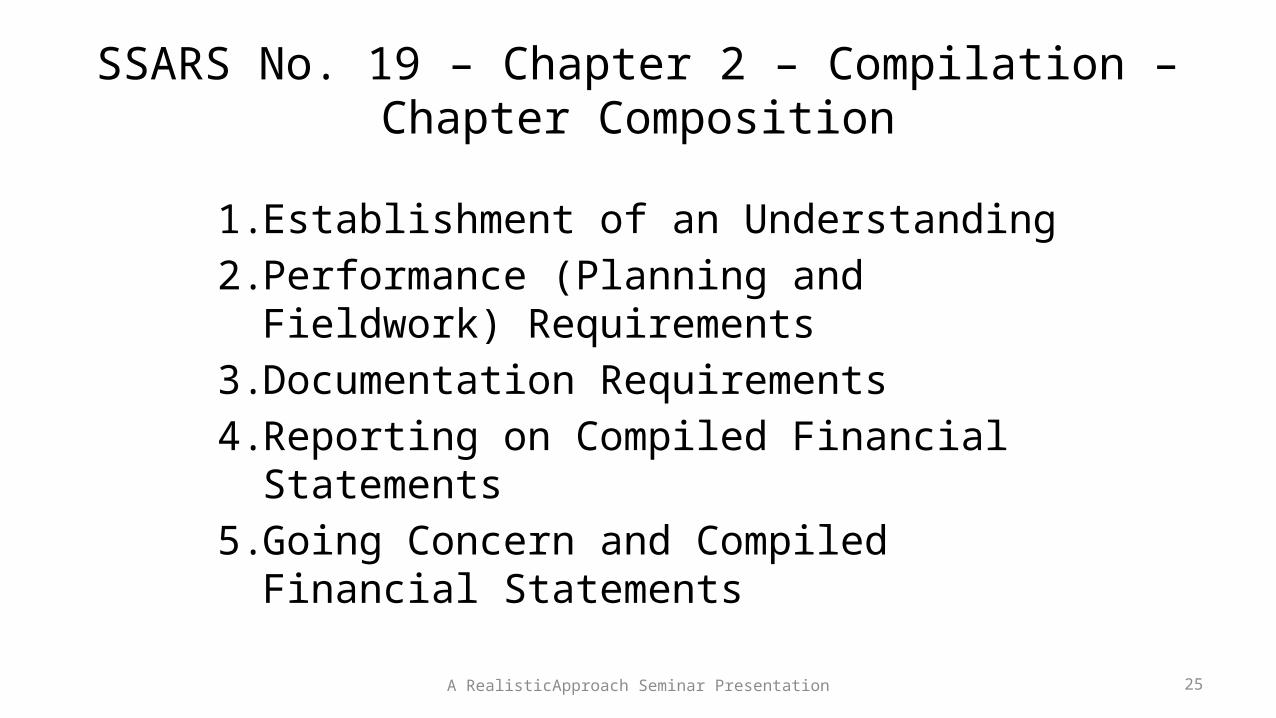

SSARS No. 19 – Chapter 2 – Compilation – Chapter Composition

1. Establishment of an Understanding 2. Performance (Planning and Fieldwork)

Requirements 3. Documentation Requirements 4. Reporting on Compiled Financial

Statements 5. Going Concern and Compiled Financial

Statements A RealisticApproach Seminar Presentation 25

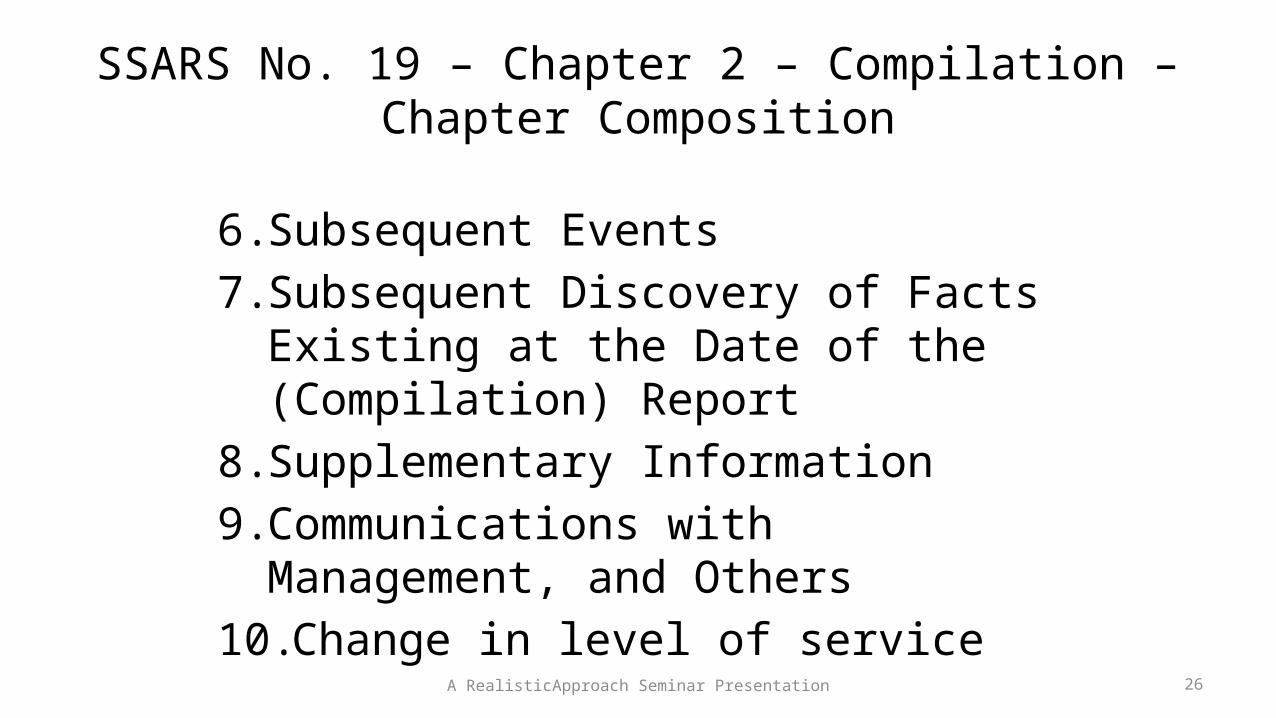

SSARS No. 19 – Chapter 2 – Compilation – Chapter Composition

6. Subsequent Events 7. Subsequent Discovery of Facts Existing

at the Date of the (Compilation) Report 8. Supplementary Information 9. Communications with Management,

and Others 10.Change in level of service

A RealisticApproach Seminar Presentation 26

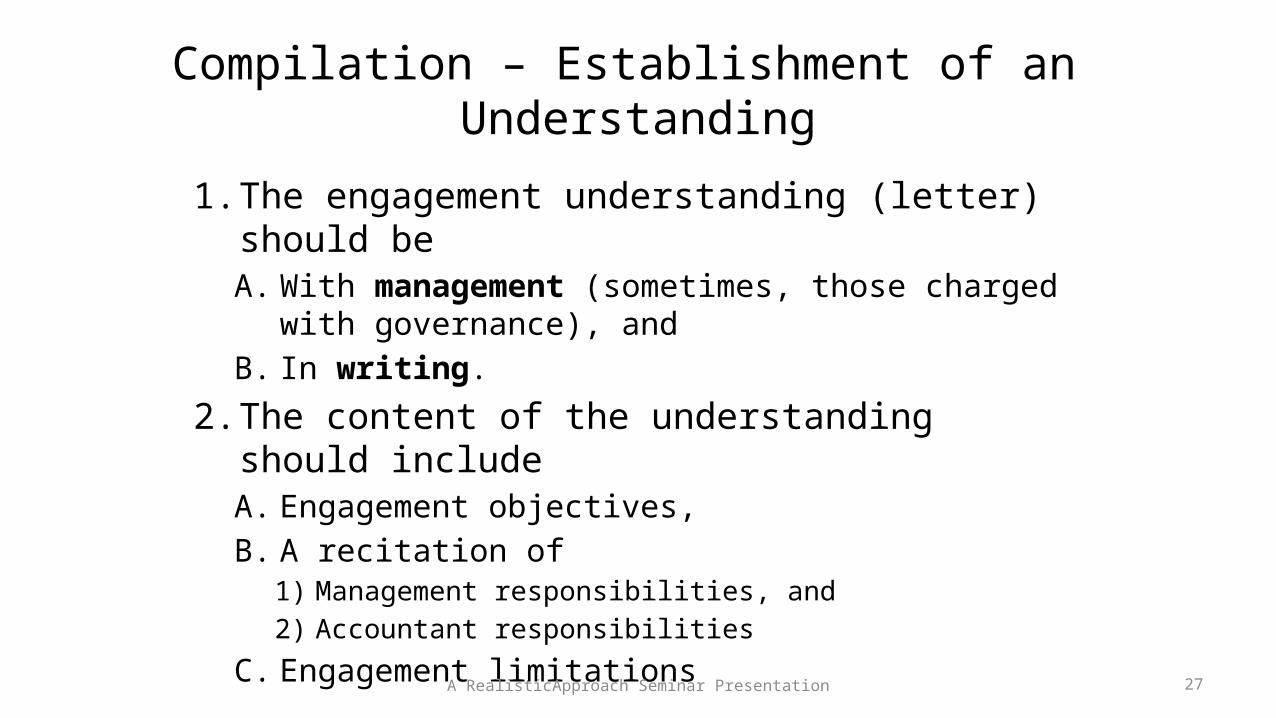

Compilation – Establishment of an Understanding

1. The engagement understanding (letter) should beA. With management (sometimes, those charged with

governance), and B. In writing.

2. The content of the understanding should includeA. Engagement objectives, B. A recitation of

1) Management responsibilities, and2) Accountant responsibilities

C. Engagement limitations A RealisticApproach Seminar Presentation 27

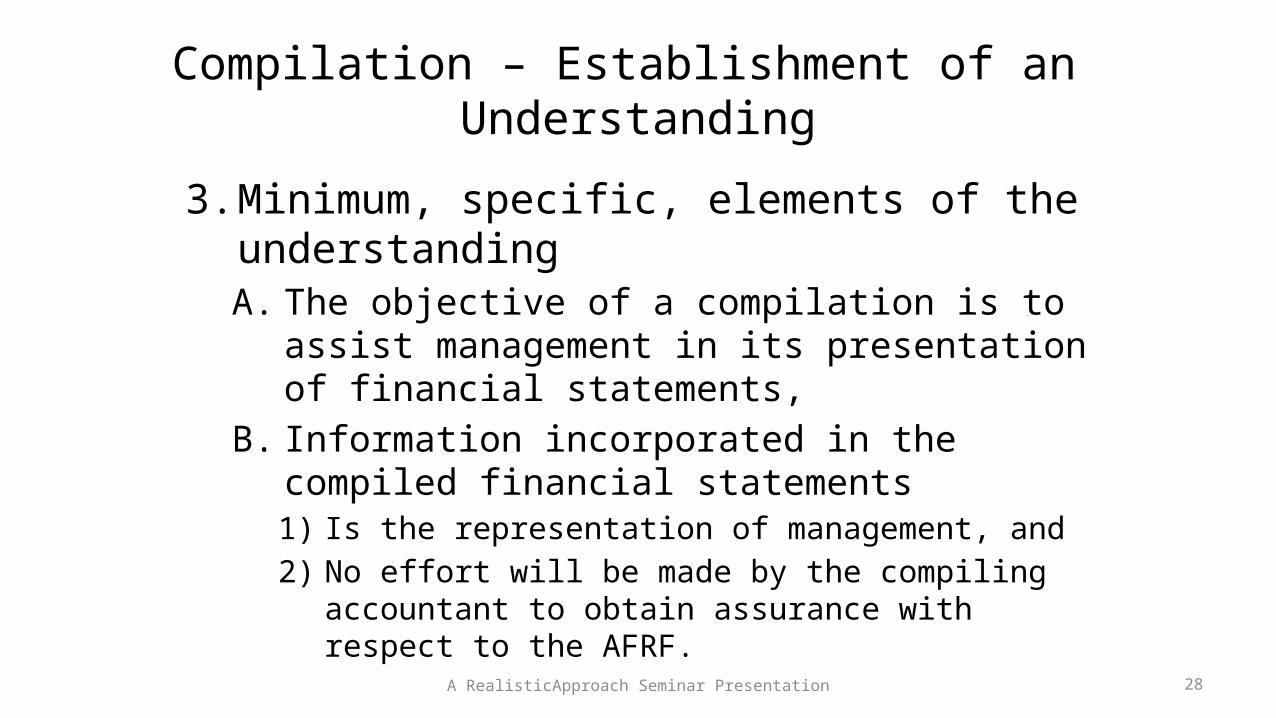

Compilation – Establishment of an Understanding

3. Minimum, specific, elements of the understanding A. The objective of a compilation is to assist

management in its presentation of financial statements,

B. Information incorporated in the compiled financial statements 1) Is the representation of management, and 2) No effort will be made by the compiling accountant to

obtain assurance with respect to the AFRF.

A RealisticApproach Seminar Presentation 28

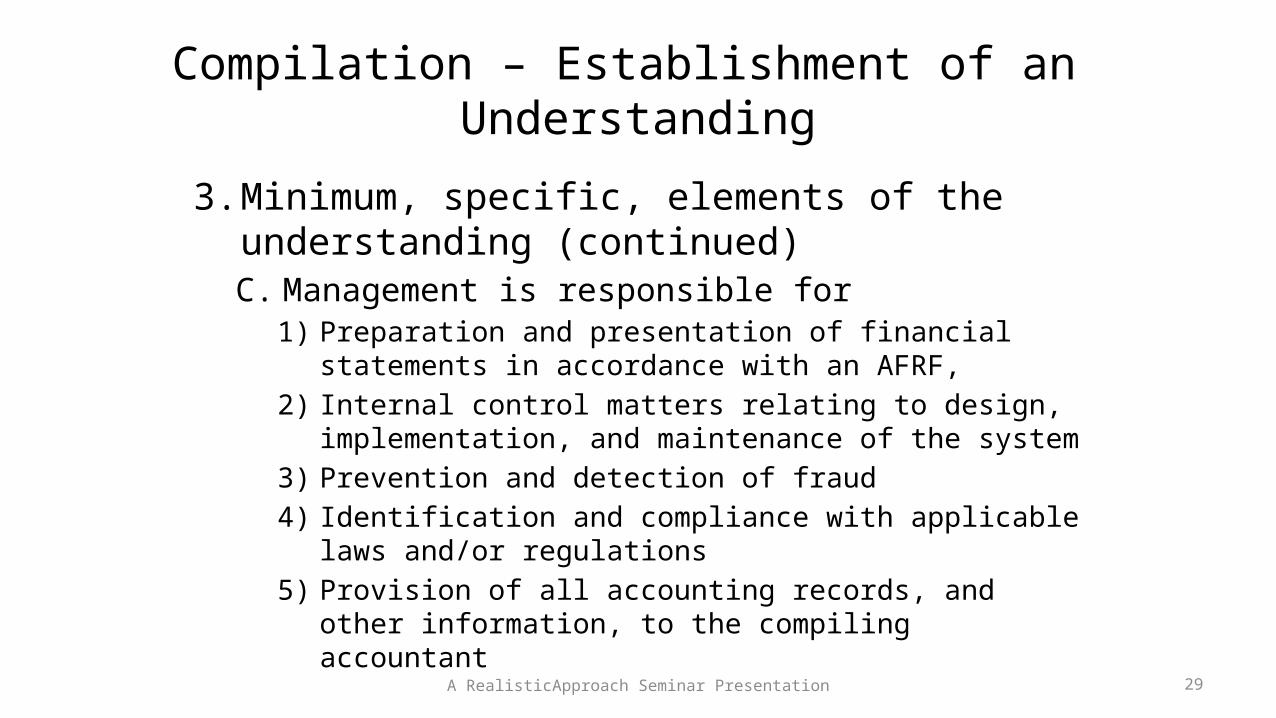

Compilation – Establishment of an Understanding

3. Minimum, specific, elements of the understanding (continued)C. Management is responsible for

1) Preparation and presentation of financial statements in accordance with an AFRF,

2) Internal control matters relating to design, implementation, and maintenance of the system

3) Prevention and detection of fraud 4) Identification and compliance with applicable laws

and/or regulations 5) Provision of all accounting records, and other

information, to the compiling accountantA RealisticApproach Seminar Presentation 29

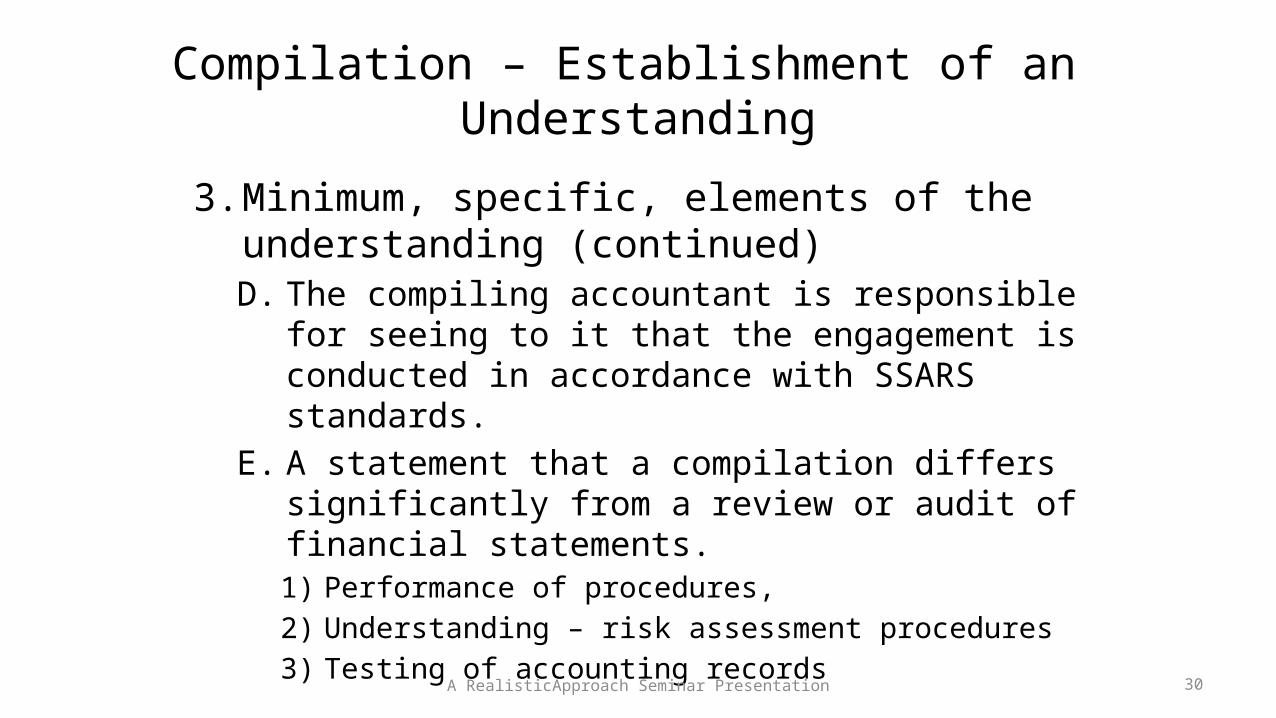

Compilation – Establishment of an Understanding

3. Minimum, specific, elements of the understanding (continued)D. The compiling accountant is responsible for seeing

to it that the engagement is conducted in accordance with SSARS standards.

E. A statement that a compilation differs significantly from a review or audit of financial statements.1) Performance of procedures, 2) Understanding – risk assessment procedures 3) Testing of accounting records

A RealisticApproach Seminar Presentation 30

Compilation – Establishment of an Understanding

3. Minimum, specific, elements of the understanding (continued)F. A compilation engagement cannot be relied upon to disclose

1) Fraud, and/or 2) Illegal acts.

G. The accountant will inform an appropriate level of management (or those charged with governance) of identified1) Material errors, 2) Evidence of fraud, or 3) Matters that may constitute an illegal act

H. Matters related to (anticipated/identified) independence impairment A RealisticApproach Seminar Presentation 31

Compilation – Establishment of an Understanding

3. Minimum, specific, elements of the understanding (continued)I. Other matters, as applicable, to a particular

compilation engagement 1) When financial statements are for management use only

(old SSARS 8) -- Management’s representation of its understanding, and agreement that the financial statements will not be used by any third party

2) Material departures from the AFRF may be identified, but the effect(s) not quantified

3) OSAD option, and/or4) Supplementary information will accompany the basic

financial statements A RealisticApproach Seminar Presentation 32

Compilation – Performance (Planning & Fieldwork) Requirements

1. Compiling accountants should understand the industry in which their client operatesA. Sufficient to be aware of the proper form of

financial statements in that industry B. Such knowledge may be obtained from sources

such as1) Prior experience, 2) AICPA Guides, 3) Industry publications, 4) Financial statements of others in the same industry, or 5) Continuing Professional EducationA RealisticApproach Seminar Presentation 33

Compilation – Performance (Planning & Fieldwork) Requirements

2. Compiling accountants should possess knowledge regarding their client in the following areas:A. Client business practices and/or policies

(normally obtained through inquiry and experience), and 1) Organization 2) Operating characteristics, 3) Assets, Liabilities, revenues, and expenses

A RealisticApproach Seminar Presentation 34

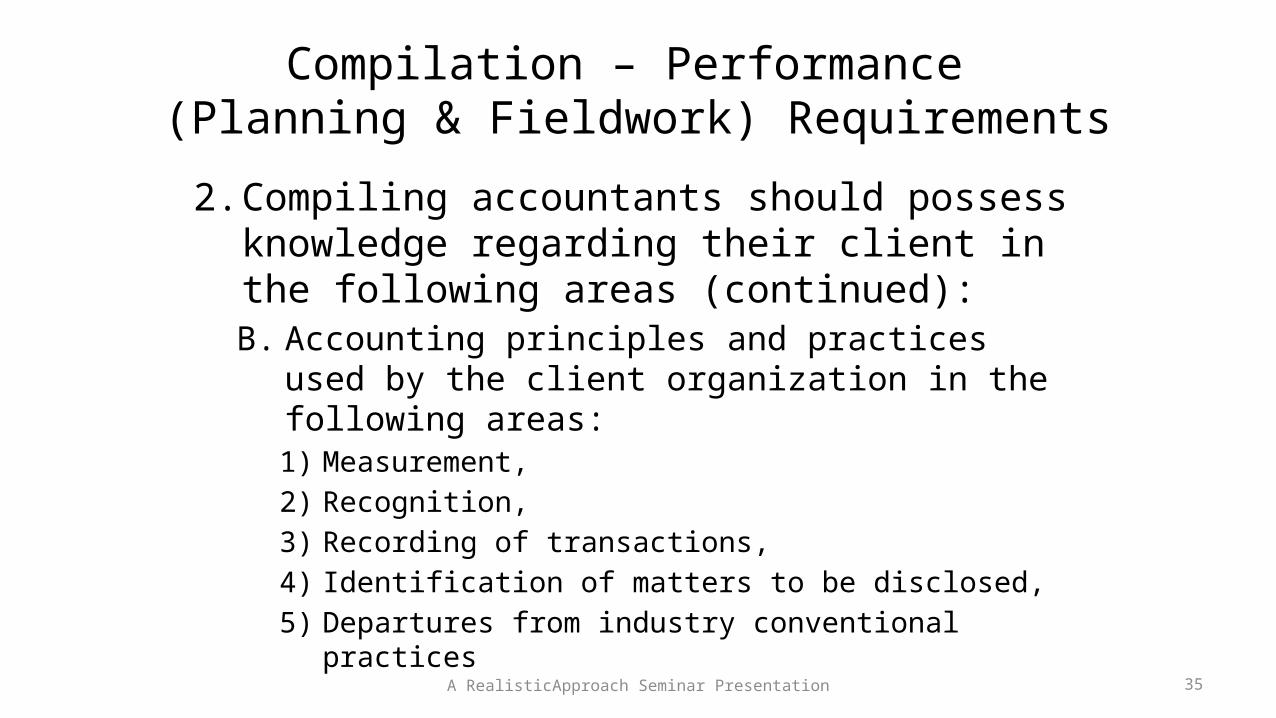

Compilation – Performance (Planning & Fieldwork) Requirements

2. Compiling accountants should possess knowledge regarding their client in the following areas (continued):B. Accounting principles and practices used by the

client organization in the following areas: 1) Measurement, 2) Recognition, 3) Recording of transactions, 4) Identification of matters to be disclosed, 5) Departures from industry conventional practices

A RealisticApproach Seminar Presentation 35

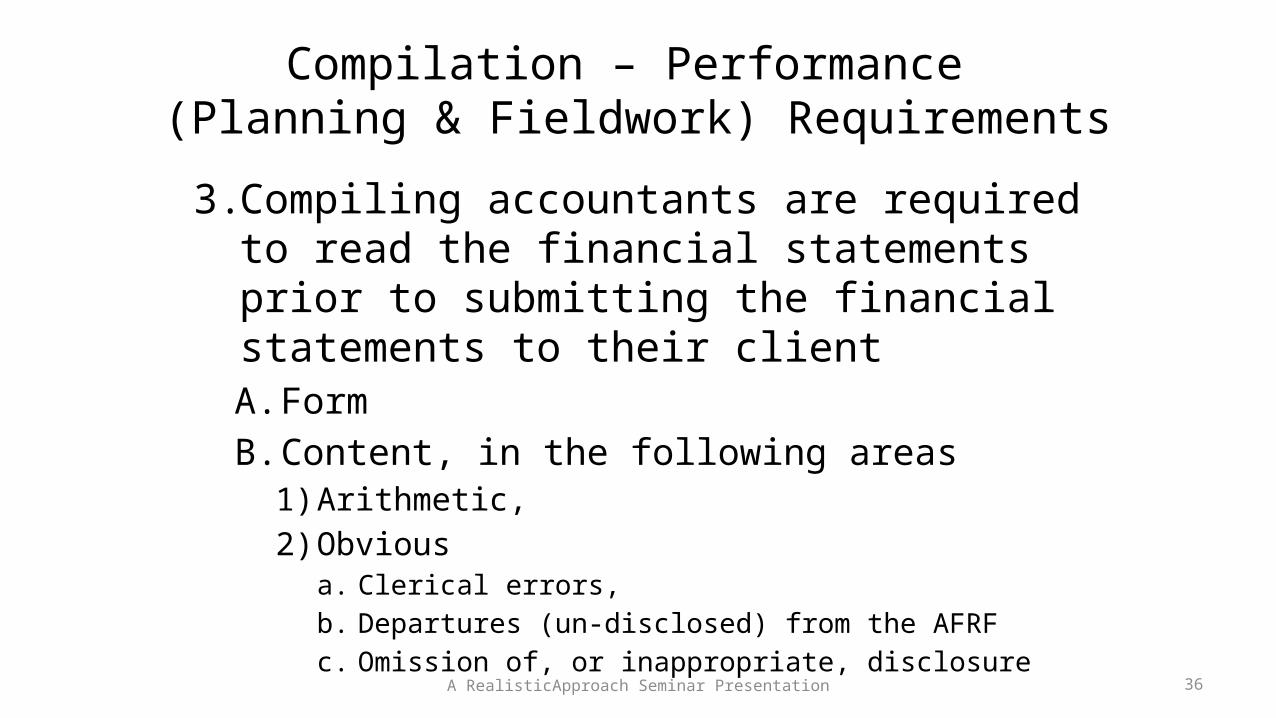

Compilation – Performance (Planning & Fieldwork) Requirements

3. Compiling accountants are required to read the financial statements prior to submitting the financial statements to their clientA. FormB. Content, in the following areas

1) Arithmetic, 2) Obvious

a. Clerical errors, b. Departures (un-disclosed) from the AFRF c. Omission of, or inappropriate, disclosure A RealisticApproach Seminar Presentation 36

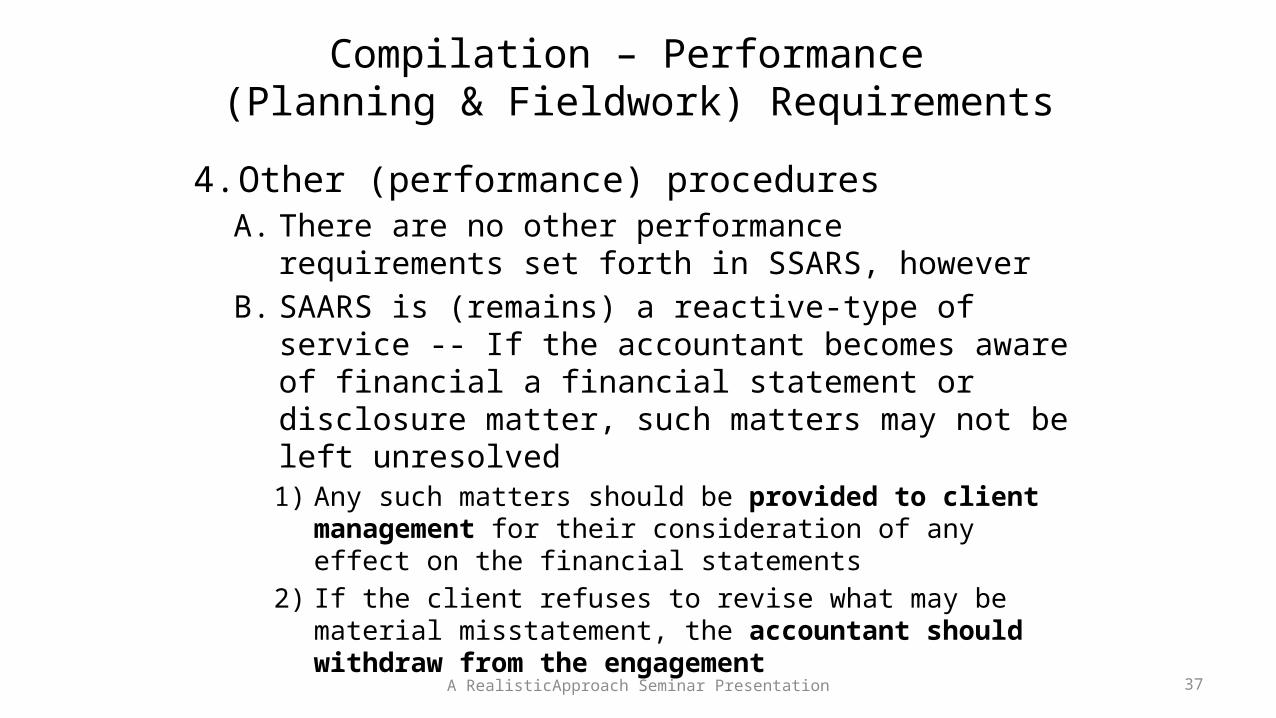

Compilation – Performance (Planning & Fieldwork) Requirements

4. Other (performance) proceduresA. There are no other performance requirements set

forth in SSARS, howeverB. SAARS is (remains) a reactive-type of service -- If the

accountant becomes aware of financial a financial statement or disclosure matter, such matters may not be left unresolved1) Any such matters should be provided to client

management for their consideration of any effect on the financial statements

2) If the client refuses to revise what may be material misstatement, the accountant should withdraw from the engagement A RealisticApproach Seminar Presentation 37

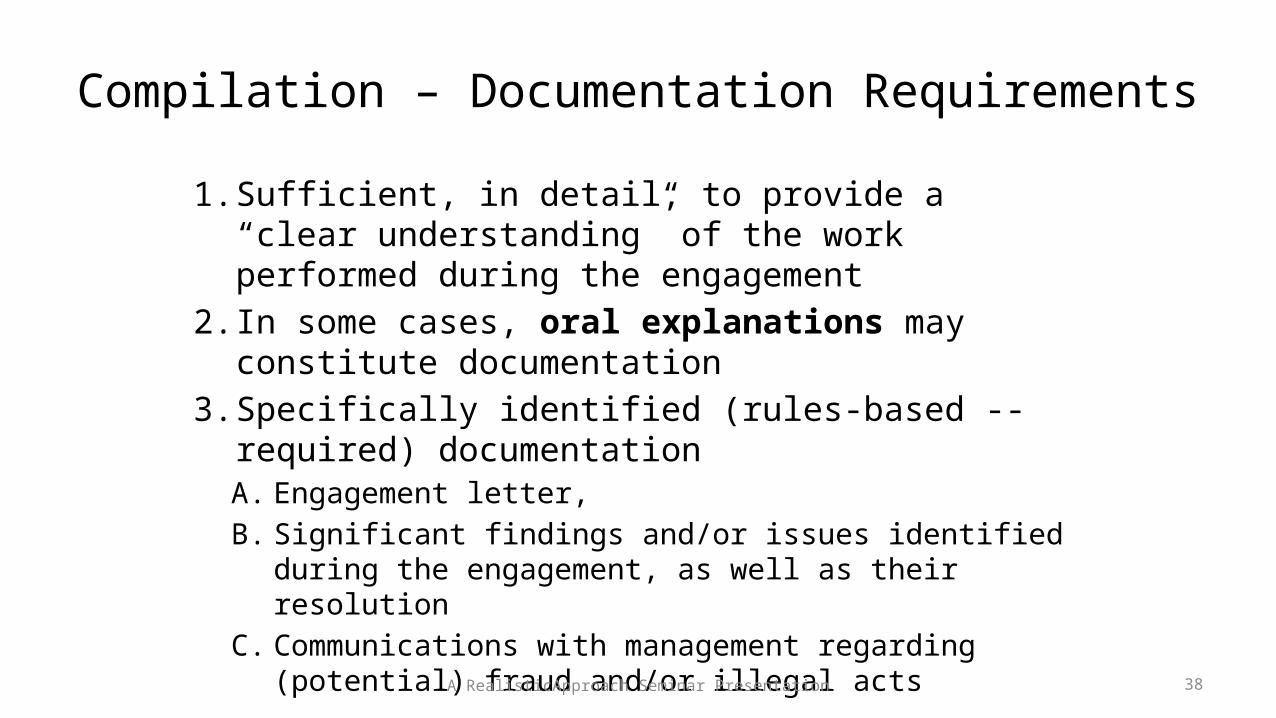

Compilation – Documentation Requirements

1. Sufficient, in detail, to provide a “clear understanding” of the work performed during the engagement

2. In some cases, oral explanations may constitute documentation

3. Specifically identified (rules-based -- required) documentation A. Engagement letter, B. Significant findings and/or issues identified during the

engagement, as well as their resolution C. Communications with management regarding (potential)

fraud and/or illegal acts A RealisticApproach Seminar Presentation 38

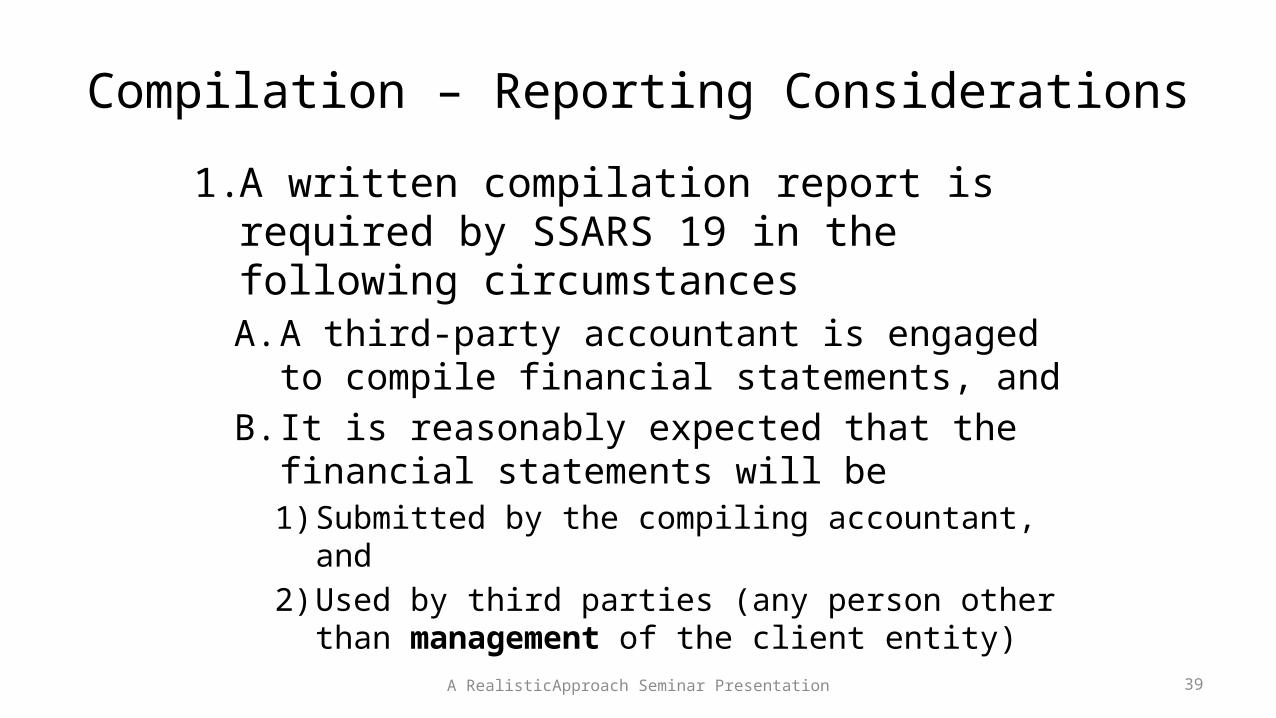

Compilation – Reporting Considerations

1. A written compilation report is required by SSARS 19 in the following circumstancesA. A third-party accountant is engaged to

compile financial statements, and B. It is reasonably expected that the financial

statements will be 1) Submitted by the compiling accountant, and 2) Used by third parties (any person other than

management of the client entity)

A RealisticApproach Seminar Presentation 39

Compilation – Reporting Considerations

Example Components of the Standard Accountants’

Compilation Report

A RealisticApproach Seminar Presentation 40

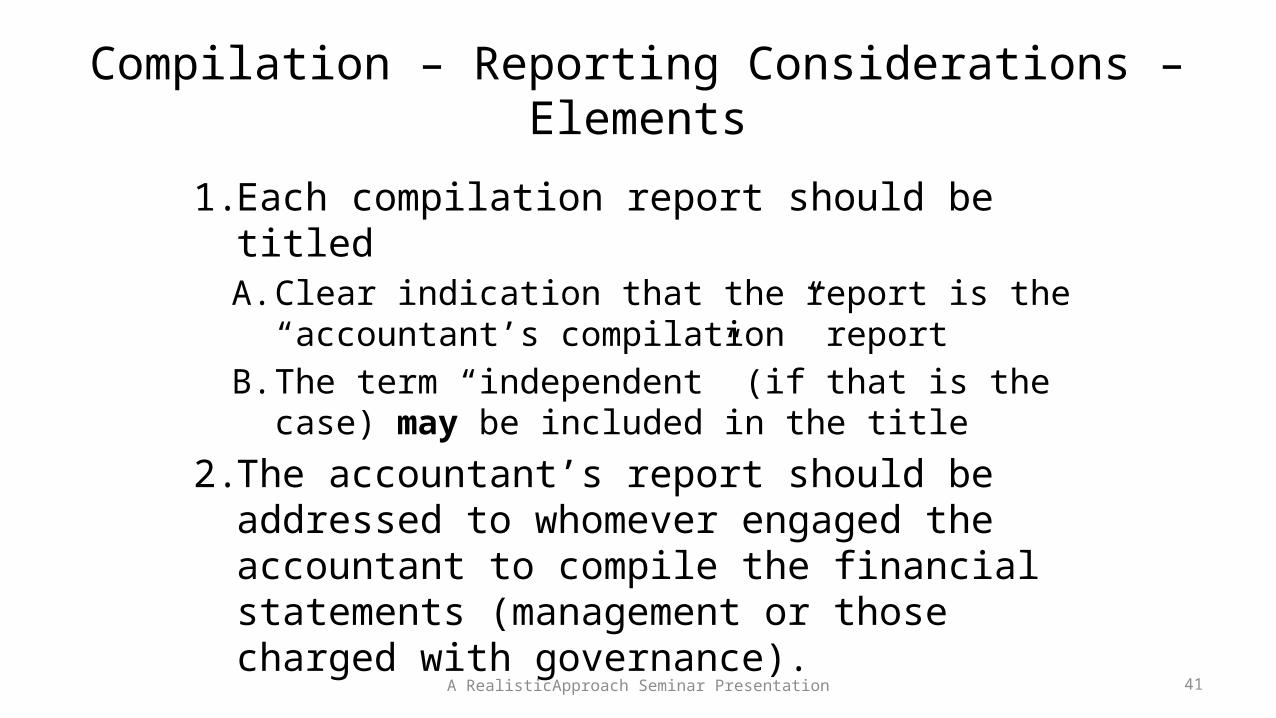

Compilation – Reporting Considerations – Elements

1. Each compilation report should be titledA. Clear indication that the report is the

“accountant’s compilation” reportB. The term “independent” (if that is the case) may

be included in the title

2. The accountant’s report should be addressed to whomever engaged the accountant to compile the financial statements (management or those charged with governance). A RealisticApproach Seminar Presentation 41

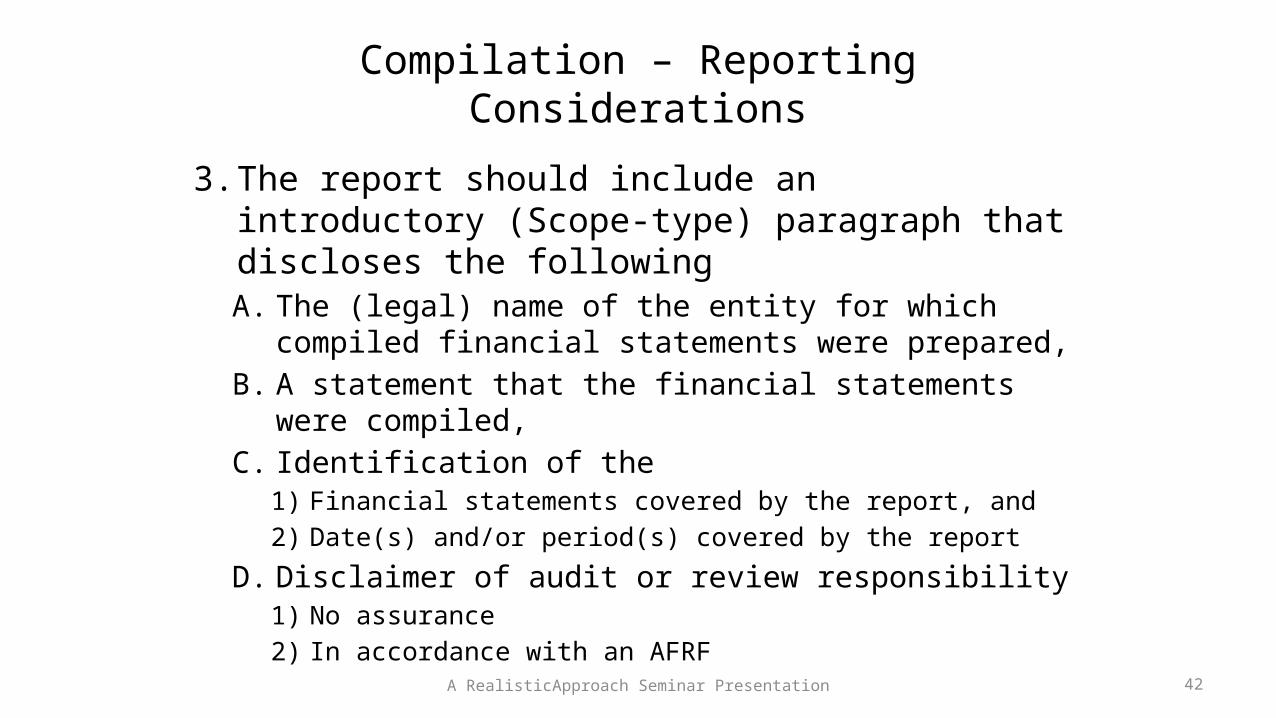

Compilation – Reporting Considerations

3. The report should include an introductory (Scope-type) paragraph that discloses the followingA. The (legal) name of the entity for which compiled

financial statements were prepared, B. A statement that the financial statements were

compiled, C. Identification of the

1) Financial statements covered by the report, and 2) Date(s) and/or period(s) covered by the report

D. Disclaimer of audit or review responsibility1) No assurance 2) In accordance with an AFRF A RealisticApproach Seminar Presentation 42

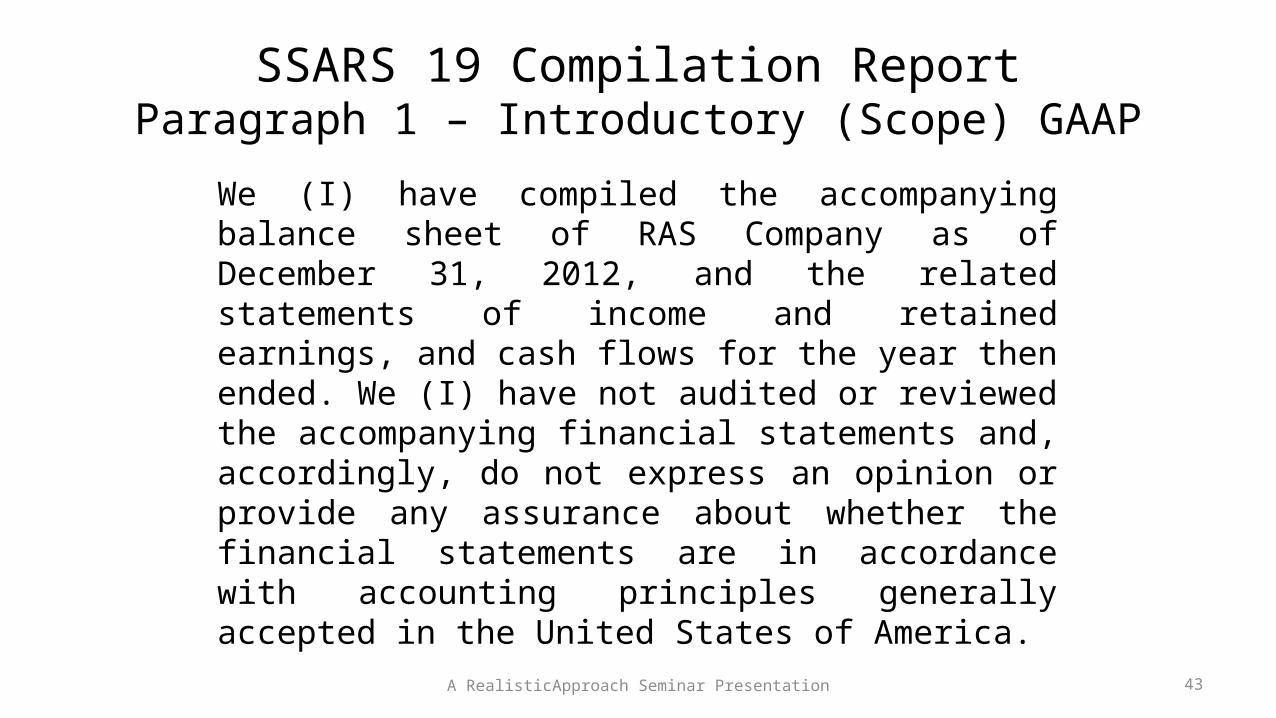

SSARS 19 Compilation ReportParagraph 1 – Introductory (Scope) GAAP

We (I) have compiled the accompanying balance sheet of RAS Company as of December 31, 2012, and the related statements of income and retained earnings, and cash flows for the year then ended. We (I) have not audited or reviewed the accompanying financial statements and, accordingly, do not express an opinion or provide any assurance about whether the financial statements are in accordance with accounting principles generally accepted in the United States of America. A RealisticApproach Seminar Presentation 43

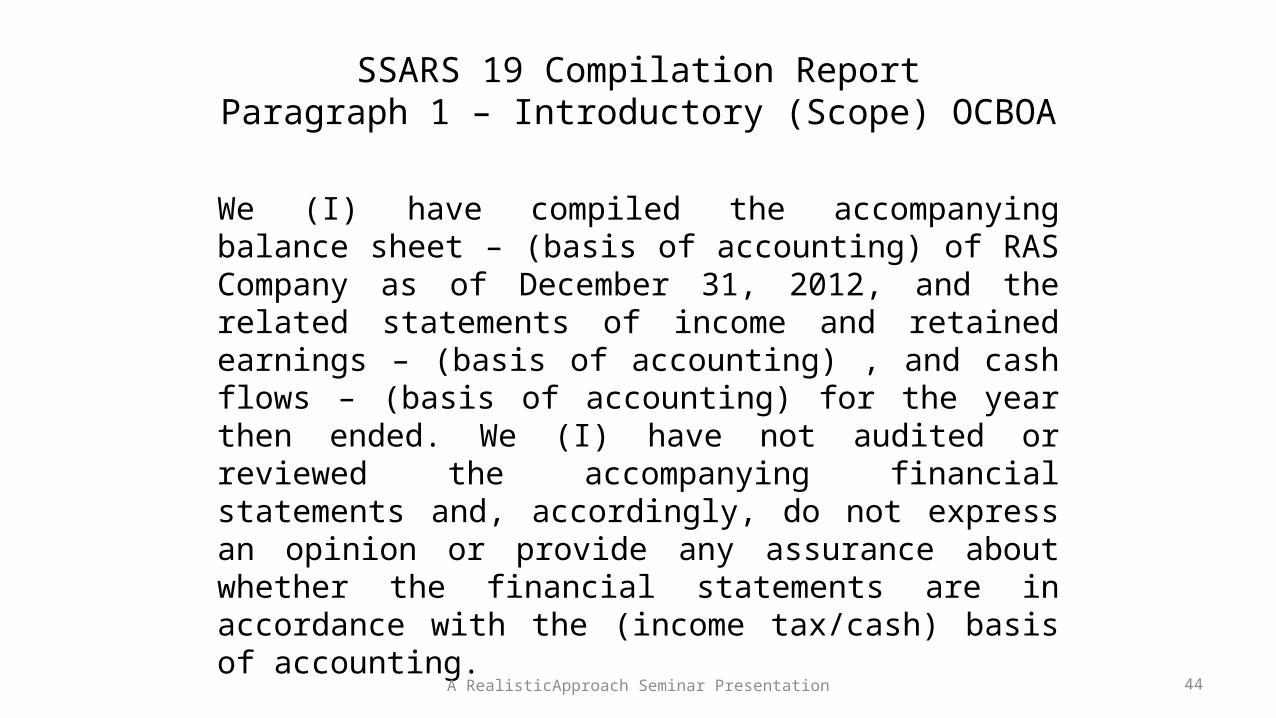

SSARS 19 Compilation ReportParagraph 1 – Introductory (Scope) OCBOA

We (I) have compiled the accompanying balance sheet – (basis of accounting) of RAS Company as of December 31, 2012, and the related statements of income and retained earnings – (basis of accounting) , and cash flows – (basis of accounting) for the year then ended. We (I) have not audited or reviewed the accompanying financial statements and, accordingly, do not express an opinion or provide any assurance about whether the financial statements are in accordance with the (income tax/cash) basis of accounting. A RealisticApproach Seminar Presentation 44

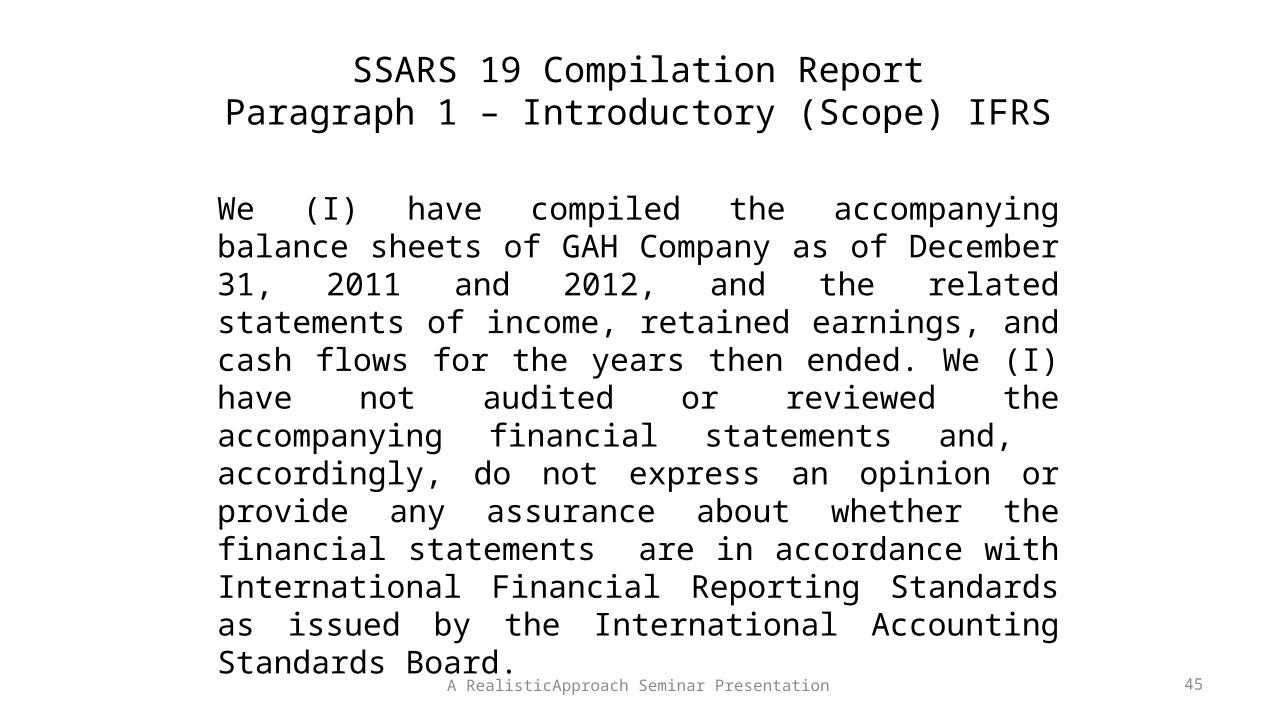

SSARS 19 Compilation ReportParagraph 1 – Introductory (Scope) IFRS

We (I) have compiled the accompanying balance sheets of GAH Company as of December 31, 2011 and 2012, and the related statements of income, retained earnings, and cash flows for the years then ended. We (I) have not audited or reviewed the accompanying financial statements and, accordingly, do not express an opinion or provide any assurance about whether the financial statements are in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board. A RealisticApproach Seminar Presentation 45

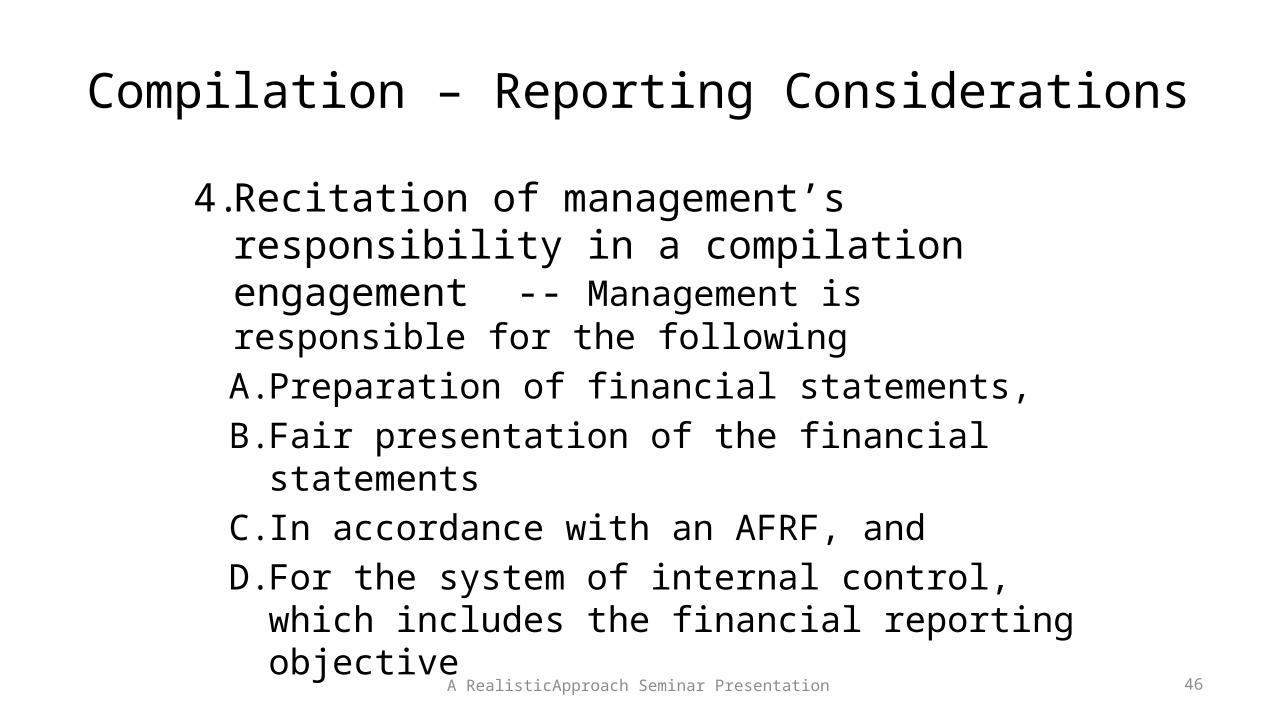

Compilation – Reporting Considerations

4. Recitation of management’s responsibility in a compilation engagement -- Management is responsible for the followingA. Preparation of financial statements, B. Fair presentation of the financial statements C. In accordance with an AFRF, andD. For the system of internal control, which

includes the financial reporting objective

A RealisticApproach Seminar Presentation 46

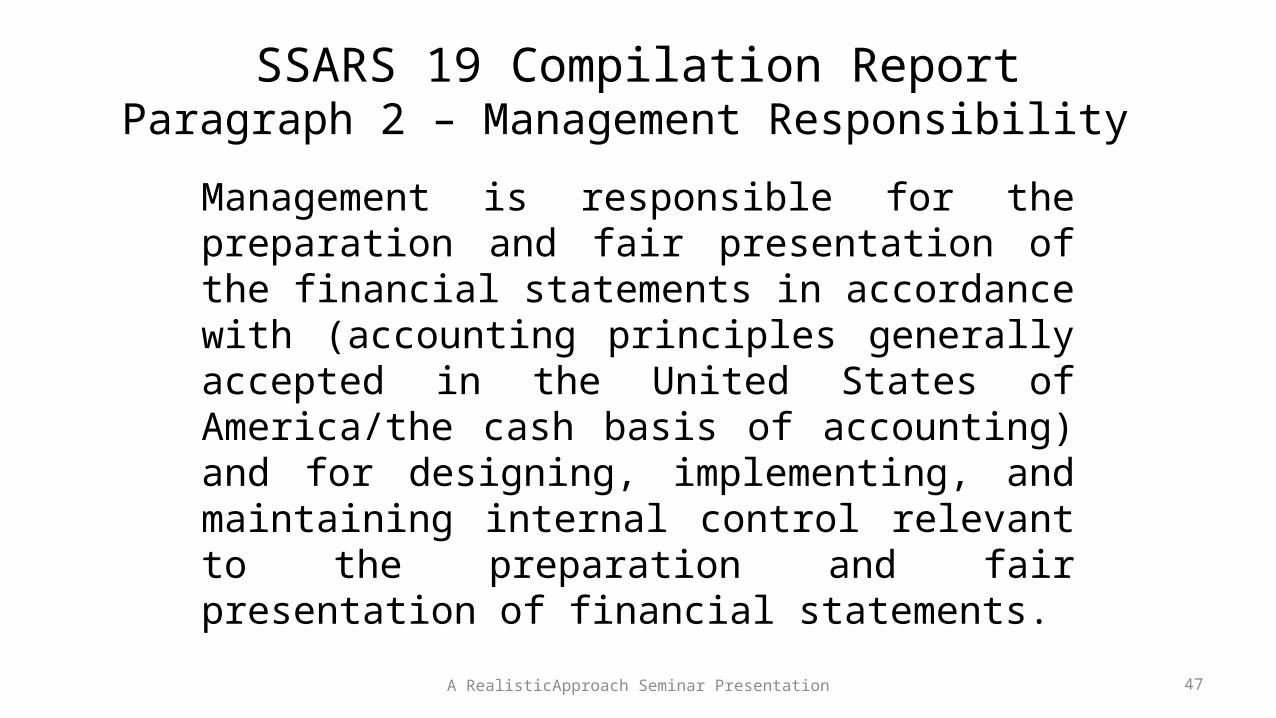

SSARS 19 Compilation ReportParagraph 2 – Management Responsibility

Management is responsible for the preparation and fair presentation of the financial statements in accordance with (accounting principles generally accepted in the United States of America/the cash basis of accounting) and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of financial statements.

A RealisticApproach Seminar Presentation 47

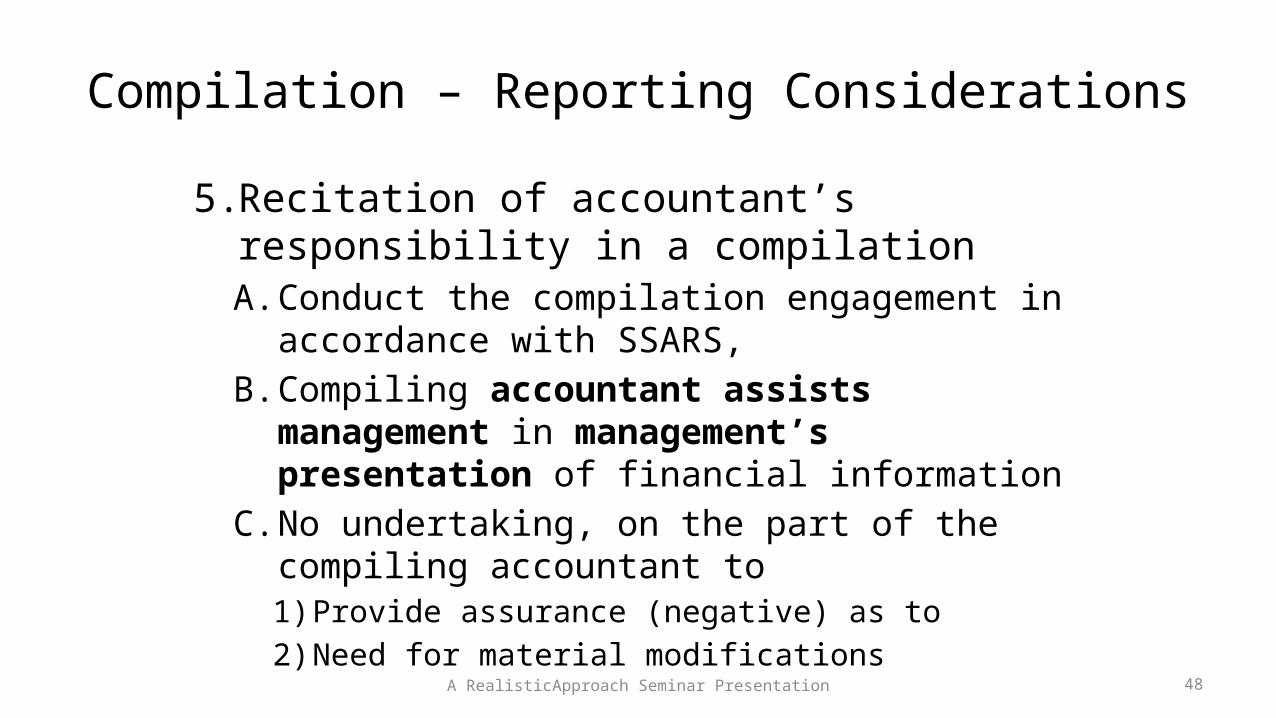

Compilation – Reporting Considerations

5. Recitation of accountant’s responsibility in a compilation A. Conduct the compilation engagement in accordance

with SSARS, B. Compiling accountant assists management in

management’s presentation of financial information C. No undertaking, on the part of the compiling

accountant to 1) Provide assurance (negative) as to 2) Need for material modifications

A RealisticApproach Seminar Presentation 48

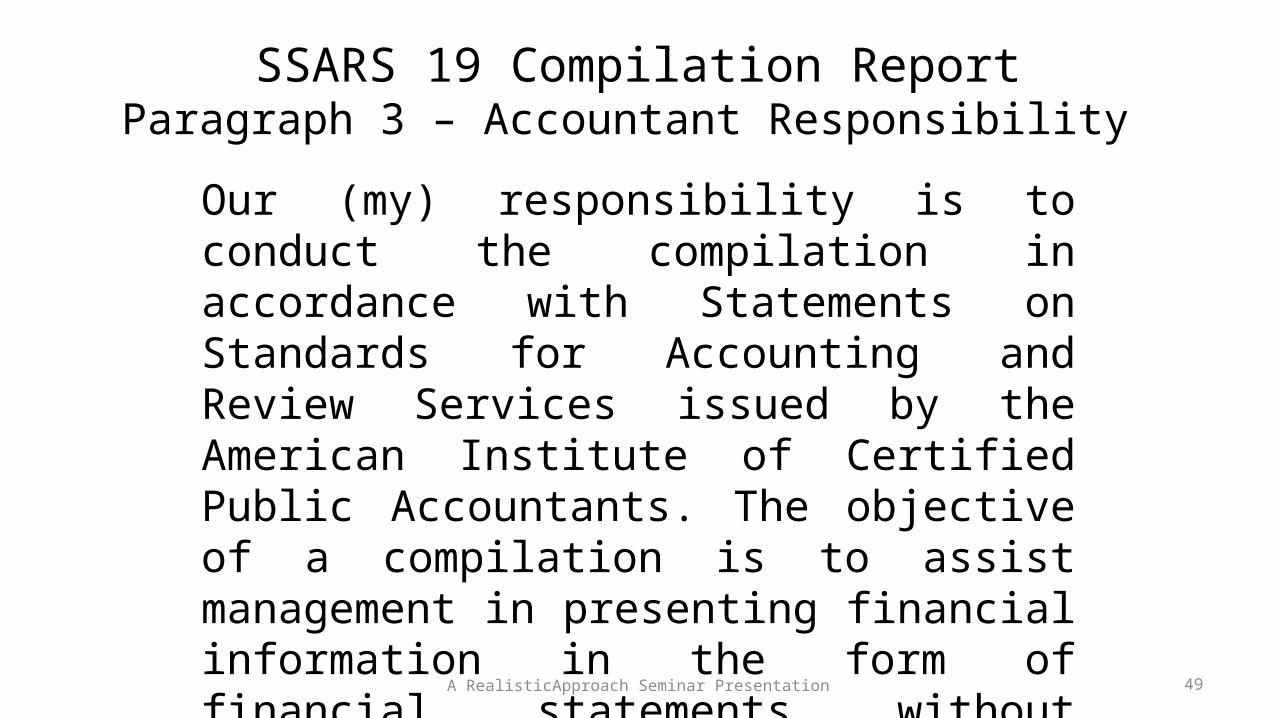

SSARS 19 Compilation ReportParagraph 3 – Accountant Responsibility

Our (my) responsibility is to conduct the compilation in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. The objective of a compilation is to assist management in presenting financial information in the form of financial statements without undertaking to obtain or provide any assurance that there are no material modifications that should be made to the financial statements.

A RealisticApproach Seminar Presentation 49

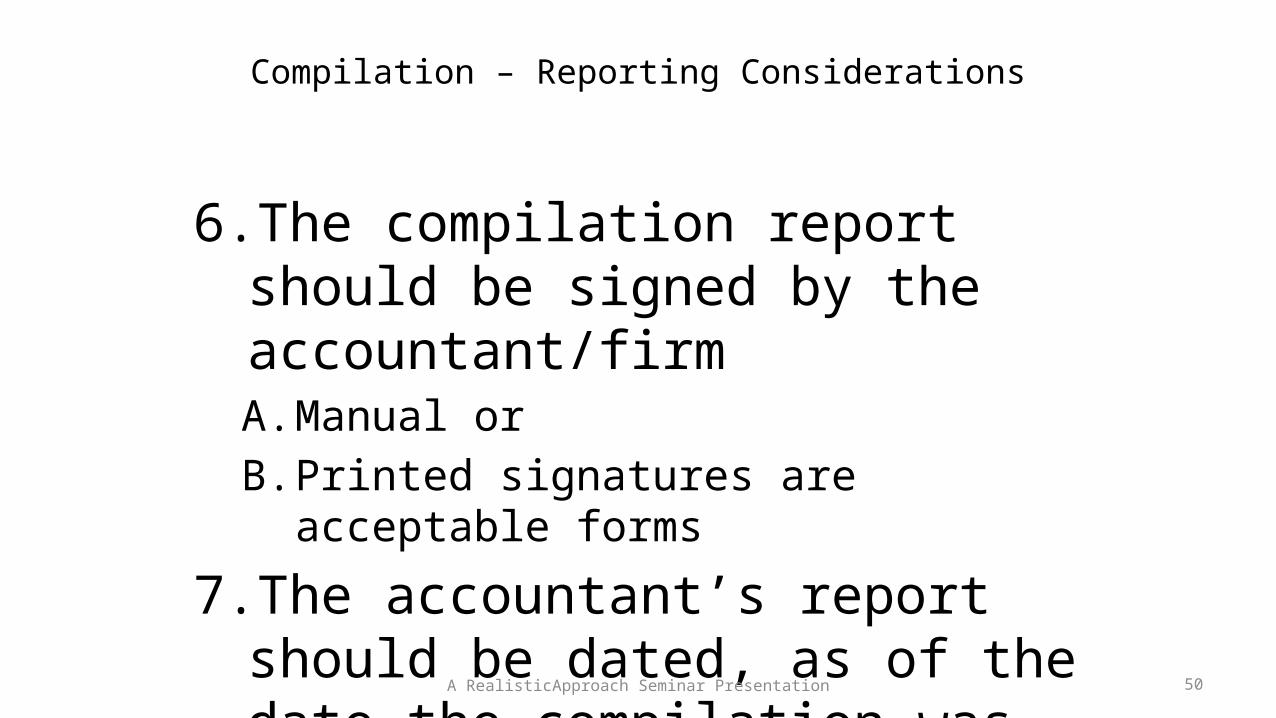

Compilation – Reporting Considerations

6. The compilation report should be signed by the accountant/firm A. Manual orB. Printed signatures are acceptable forms

7. The accountant’s report should be dated, as of the date the compilation was completed.

A RealisticApproach Seminar Presentation 50

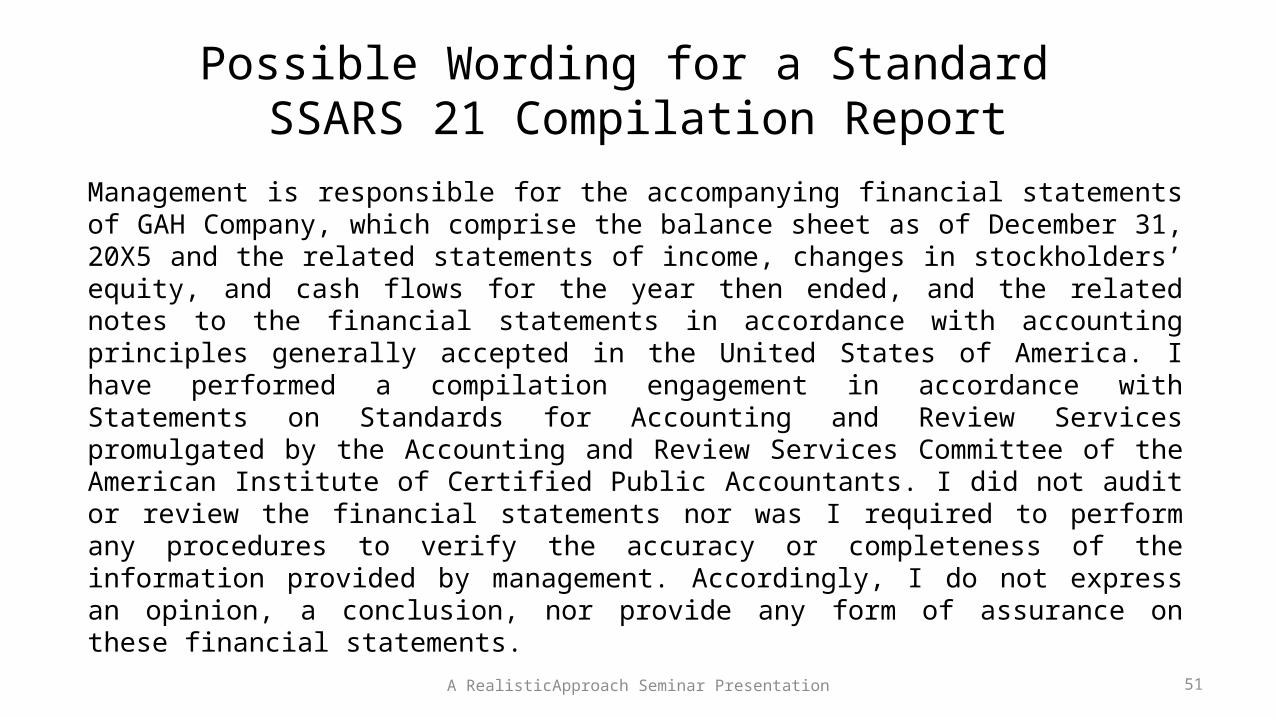

Possible Wording for a Standard SSARS 21 Compilation Report

Management is responsible for the accompanying financial statements of GAH Company, which comprise the balance sheet as of December 31, 20X5 and the related statements of income, changes in stockholders’ equity, and cash flows for the year then ended, and the related notes to the financial statements in accordance with accounting principles generally accepted in the United States of America. I have performed a compilation engagement in accordance with Statements on Standards for Accounting and Review Services promulgated by the Accounting and Review Services Committee of the American Institute of Certified Public Accountants. I did not audit or review the financial statements nor was I required to perform any procedures to verify the accuracy or completeness of the information provided by management. Accordingly, I do not express an opinion, a conclusion, nor provide any form of assurance on these financial statements.

A RealisticApproach Seminar Presentation 51

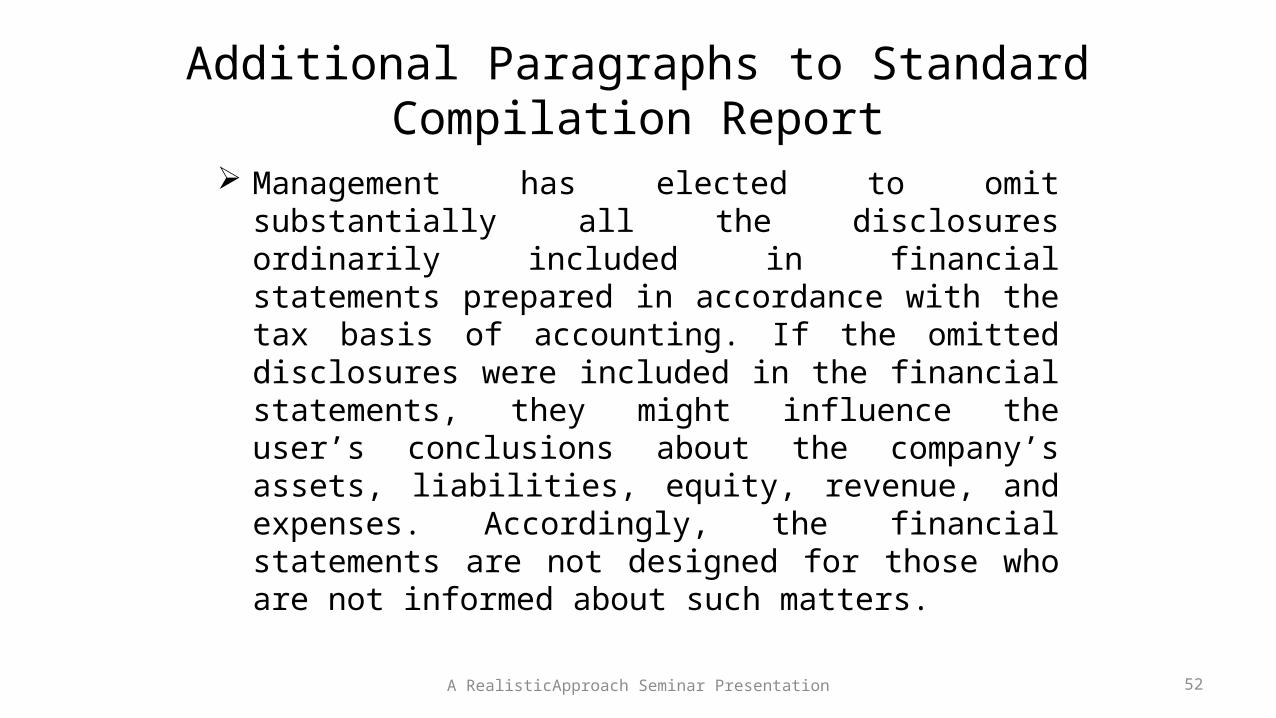

Additional Paragraphs to Standard Compilation Report

Management has elected to omit substantially all the disclosures ordinarily included in financial statements prepared in accordance with the tax basis of accounting. If the omitted disclosures were included in the financial statements, they might influence the user’s conclusions about the company’s assets, liabilities, equity, revenue, and expenses. Accordingly, the financial statements are not designed for those who are not informed about such matters.

A RealisticApproach Seminar Presentation 52

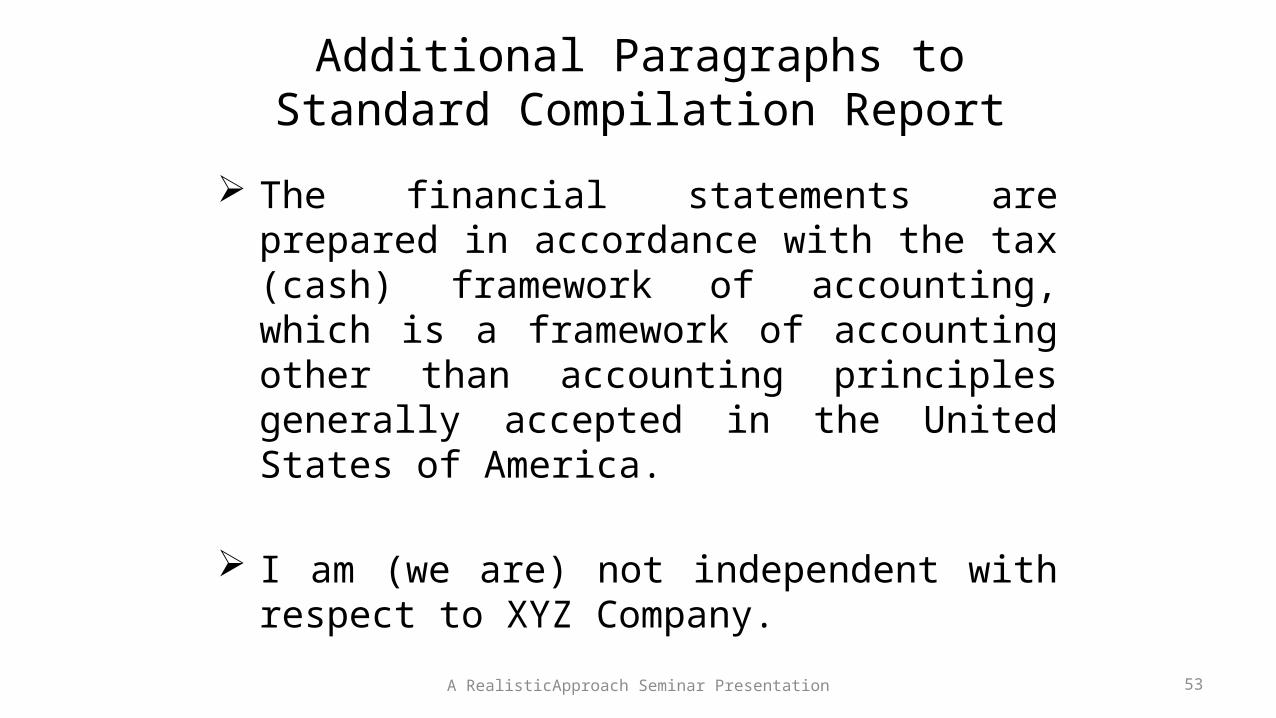

Additional Paragraphs to Standard Compilation Report

The financial statements are prepared in accordance with the tax (cash) framework of accounting, which is a framework of accounting other than accounting principles generally accepted in the United States of America.

I am (we are) not independent with respect to XYZ Company.

A RealisticApproach Seminar Presentation 53

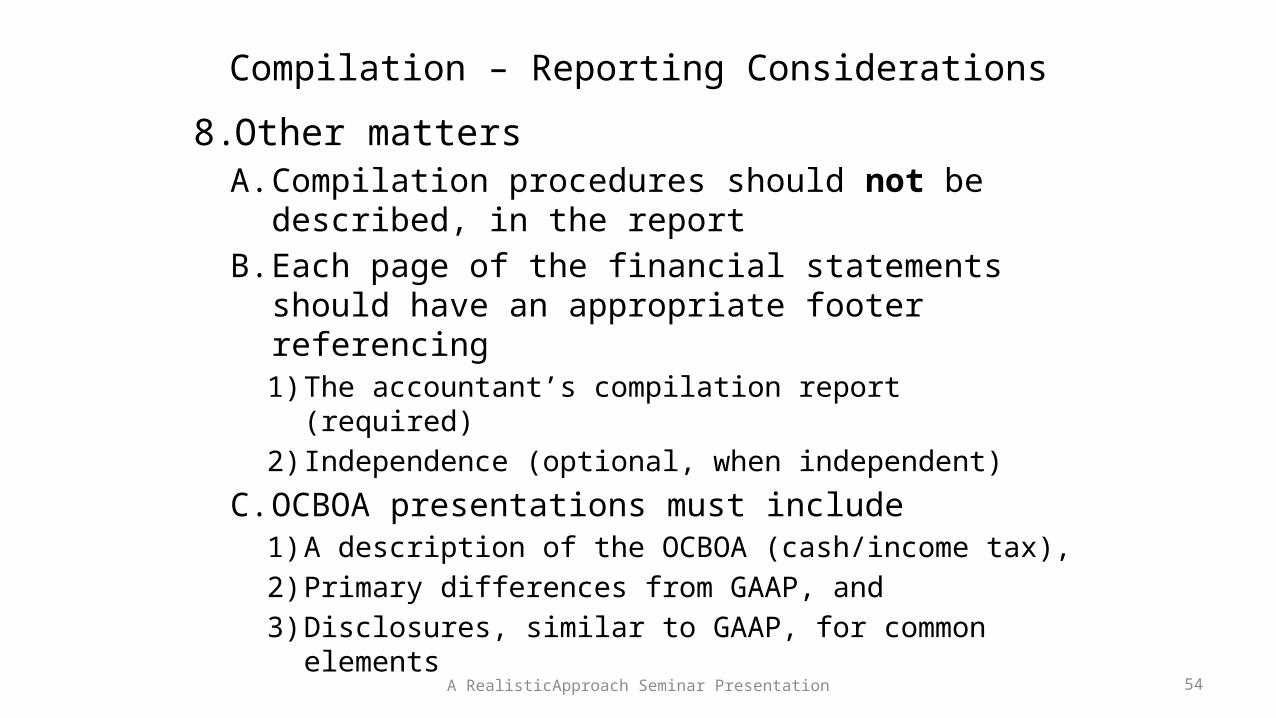

Compilation – Reporting Considerations8. Other matters

A. Compilation procedures should not be described, in the report

B. Each page of the financial statements should have an appropriate footer referencing1) The accountant’s compilation report (required) 2) Independence (optional, when independent)

C. OCBOA presentations must include1) A description of the OCBOA (cash/income tax), 2) Primary differences from GAAP, and3) Disclosures, similar to GAAP, for common elements

A RealisticApproach Seminar Presentation 54

Compilation – Reporting Considerations9. Omission of Substantially All Disclosures (OSAD)

A. A client request (as opposed to a client-directive) B. That may be acceded to by the compiling

accountant if the request is1) Related to expediency, and the intended users are

already familiar with such matters, and 2) Not an attempt to mislead through omission

C. Requires an additional paragraph, stating1) Management has elected to omit the disclosures, 2) If the disclosures were included, they might influence,

and3) Are not designed for users who are not already informed

A RealisticApproach Seminar Presentation 55

Compilation – Reporting Considerations9. Omission of Substantially All Disclosures (OSAD)

D. There are times when certain disclosures, but not all disclosures, are included in financial statements. 1) The decision to include “selected Information” is made

by management, but the need may come from a. Management, b. Client, or c. Compiling accountant inputs

2) Requires the standard (appropriate) OSAD paragraph in the accountant’s report, plus

3) Notation on pages where disclosure(s) are made – “Selected Information – Substantially All Disclosures Required by (insert AFRF) Are Not Included”

A RealisticApproach Seminar Presentation 56

Compilation – Reporting Considerations

10. Independence reporting considerations A. If a compiling accountant is not independent, the

accountant’s report must be modified to disclose the lack of independence (This is the “final paragraph” of the report.)

B. The disclosure of a lack of independence should be styled – “ I am (We are) not independent with respect to (name the client entity).

C. Compiling accountant may disclose reason(s) for the lack of independence

1) Optional – not required, and2) In for a penny, in for a pound -- All reasons for the lack of

independence must be disclosed A RealisticApproach Seminar Presentation 57

Compilation – Other Matters2. Known AFRF deficiencies – If the compiling

accountant becomes aware of a deficiency, the accountant has two choices A. Add an additional paragraph to the compilation

report that discloses the following1) Nature of the departure, and 2) If already determined by management, the effect, or3) A statement that the effect has not been determined

B. Request/require that management “cure” the deficiency in the financial statements 1) Approach taken when disclosure, alone, is not sufficient 2) Accountant should withdraw from the engagement if

management will not cure the deficiencyA RealisticApproach Seminar Presentation 58

Compilation – Other Matters3. Additional information in the accountant’s

compilation reportA. The compiling accountant may, but is not required

to, add additional information in the report to emphasize matters already disclosed in the body of the financial statements

B. Examples of matters that an accountant may wish to emphasize include 1) Uncertainties 2) Related party dealings 3) Other matters of significance – already within the body

of the financial statements. A RealisticApproach Seminar Presentation 59

Compilation and Going Concern

1. Compiling accountants have no pro-active responsibility to consider possibility of going concern (reactive responsibility, only)

2. If going concern, within a one-year period (the definitional “reasonable period of time”) from the financial statement date, appears to be an (a potential) issue, the compiling accountant should A. Refer the matter to management for its

consideration and conclusion regarding the matter B. Consider the reasonableness of management’s

response.A RealisticApproach Seminar Presentation 60

Compilation and Going Concern

3. If, in the compiling accountant’s opinion, management’s conclusions are not reasonable, or accurate, the accountant should handle the matter as a departure from an AFRF

4. While there is no requirement to do so in SSARS, a compiling accountant may wish to add an emphasis paragraph to his or her report.A. This option supposes that going concern is a

disclosure made within the financial statementsB. It is not appropriate to use the wording provided in

auditing standards guidanceA RealisticApproach Seminar Presentation 61

Compilation and Going Concern

4. Interpretation No. 12, Reporting on an Uncertainty, Including an Uncertainty About an Entity’s Ability to Continue as a Going Concern, provides suggested wording:

As discussed in Note X, certain conditions indicate that the Company may be unable to continue as a going concern. The accompanying financial statements do not include any adjustments that might be necessary should the Company be unable to continue as a going concern.

A RealisticApproach Seminar Presentation 62

Compilation – Subsequent Events1. A compiling accountant has a reactive

responsibility with respect to each type of subsequent event A. Alpha (estimation refinement) event, and B. Beta (event occurs post-financial-statement-date)

2. Accountant may become aware of a subsequent event eitherA. In the course of performing the engagement, orB. After the completion of the engagement, but before

the financial statements are issued

A RealisticApproach Seminar Presentation 63

Compilation – Subsequent Events3. The compiling accountant should refer identified

subsequent events to management, for management’s considerationA. Of potential adjustment of the financial statements and/orB. Adequacy of disclosure regarding the event

4. If the compiling accountant believes that the subsequent event is not adequately reflected and/or disclosed, the matter should be treated as a departure from the AFRF

5. Subsequent events may be the subject of an emphasis paragraph in the accountant’s report, provided the matter is (already) disclosed in the body of the financial statements

A RealisticApproach Seminar Presentation 64

Compilation – Subsequent Discovery of Facts Existing at the Date of the Report

1. A compiling accountant has no responsibility, subsequent to the date of the accountant’s report, to perform additional compilation procedures. However, if an accountant does become aware of additional matters he or she must follow up on those matters.

2. The accountant has a duty to investigate the matter for the purpose of A. Ascertaining the credibility of the information, andB. Determining whether that information would have

significantly changed the1) Content of the financial statements, and/or 2) The accountant’s report.A RealisticApproach Seminar Presentation 65

Compilation – Subsequent Discovery of Facts Existing at the Date of the Report

3. The matter(s) should be discussed with an appropriate level of client management and/or those charged with governance to enlist their assistance with the investigation of the matter(s).

4. The accountant should take additional steps if A. His or her report would have been different if the

information had been known at the report date, and B. It is likely that users

1) Are (still) using the financial statements, and 2) The new information would be significant to those users

A RealisticApproach Seminar Presentation 66

Compilation – Subsequent Discovery of Facts Existing at the Date of the Report

5. When the accountant determines that disclosure of the matter should be made, it should be done in a manner such asA. When issuance of subsequent financial statements is

imminent, the disclosure of the matter can be made in those financial statements,

B. When revised financial statements are appropriate the financial statements should include1) Footnote disclosure of the reason for the revision, 2) The accountant may, but is not required to, add an

emphasis paragraph to the (revised) compilation reportA RealisticApproach Seminar Presentation 67

Compilation – Subsequent Discovery of Facts Existing at the Date of the Report

5. When the accountant determines that disclosure of the matter should be made, it should be done in a manner such asC. When the effect on the financial statements cannot

be determined without additional effort, and issuance of revised financial statements is not imminent 1) Users should be notified, by the client, that revised

financial statements will be issued as soon as open items can be resolved, and

2) When applicable, a revised compilation report will be issued, as well. A RealisticApproach Seminar Presentation 68

Compilation – Subsequent Discovery of Facts Existing at the Date of the Report

6. If a client refuses to disclose matters considered significant by the compiling accountant by means of one of the methods described above A. The accountant should communicate the refusal to those

charged with governance, and B. If the client does not make appropriate disclosure, the

accountant should (subject to advice from counsel) notify 1) The client that the report must not be associated with the

financial statements, 2) Each of the following parties that the accountants report

should no longer be useda. Any regulatory agencies that are usersb. Other users (financial statements and accountant’s report)A RealisticApproach Seminar Presentation 69

Compilation – Subsequent Discovery of Facts Existing at the Date of the Report

6. If a client refuses to disclose matters considered significant by the compiling accountant by means of one of the methods described above C. Disclosure of such matters should be as precise and

objective as necessary to communicate the matter to the parties and, at a minimum, include1) A description of the subsequently identified information 2) The effect on the financial statements 3) An Indication that the client has not assisted in validation

of the disclosure (if that is the case), and 4) If the matter is valid, the accountant’s report should no

longer be associated with the financial statementsA RealisticApproach Seminar Presentation 70

Compilation – Subsequent Discovery of Facts Existing at the Date of the Report

6. If a client refuses to disclose matters considered significant by the compiling accountant by means of one of the methods described above D. No disclosure is necessary regarding

subsequently identified matters unless the accountant believes that the1) Financial statements may be misleading, and2) Accountants report should no longer be associated

with the financial statements because of a lack of disclosure of the identified matter A RealisticApproach Seminar Presentation 71

Compilation – Supplementary Information

1. When supplementary information is included with compiled financial statements, the compiling accountant has a reporting obligation.

2. When a combined report is used, a statement such as “The (identify the accompanying information) is presented for purposes of additional analysis and is not a required part of the basic financial statements.” should be added to the first paragraph of the compilation report.

A RealisticApproach Seminar Presentation 72

Compilation – Supplementary Information

3. If the compiling accountant elects to use the two-report approach for reporting on supplementary information, that report should include the following elements A. A statement that the supplementary information is

presented for purposes of additional analysis B. Supplementary information has been compiled from

information represented by management, and C. The accountant has/does not

1) Audited or Reviewed the supplementary information and2) Express an opinion or any assurance on the supplementary

information A RealisticApproach Seminar Presentation 73

Compilation – Matters to be Communicated to Management and Others

1. Compiling accountants have a communication obligation when, and if, they become aware of matters that indicate the potential that fraud or illegal acts may have occurred.

2. The communication should be made to an appropriate level of management and/or those charged with governance.

3. The communication may be made A. Orally, and documented in the working papers, orB. In writing to the client and memorialized in the

working papers A RealisticApproach Seminar Presentation 74

Compilation – Matters to be Communicated to Management and Others

4. Reporting line when senior officials of the client may be involved -- If the fraud or illegal act involves A. Senior management, the accountant should

communicate with management at least one level higher than the (potential) perpetrator, or a member of those charged with governance

B. The/an owner of the client entity, the accountant should consider resigning the engagement. A RealisticApproach Seminar Presentation 75

Compilation – Matters to be Communicated to Management and Others

1. Disclosure of any client information, without client permission to do so, is generally, prohibited. However, there may be times when matters related to fraud or illegal acts may be required to be disclosed to certain third parties without client permission to do so.A. In response to legal and/or regulatory

requirements, B. To a successor accountant, in response to a

predecessor accountant’s request, and C. In response to a (valid) subpoena.A RealisticApproach Seminar Presentation 76

Thank You For Attending Today’s Session!

If you have questions and/or comments

A RealisticApproach Seminar Presentation 77