Embed Size (px)

Citation preview

Accounting and Assurance Update

A RealisticApproach Seminars Conference Presentation

Annual Accounting Standards Update

A RealisticApproach Seminars Conference Presentation

FASB – Accounting Standard Updates

A RealisticApproach Seminars Conference Presentation

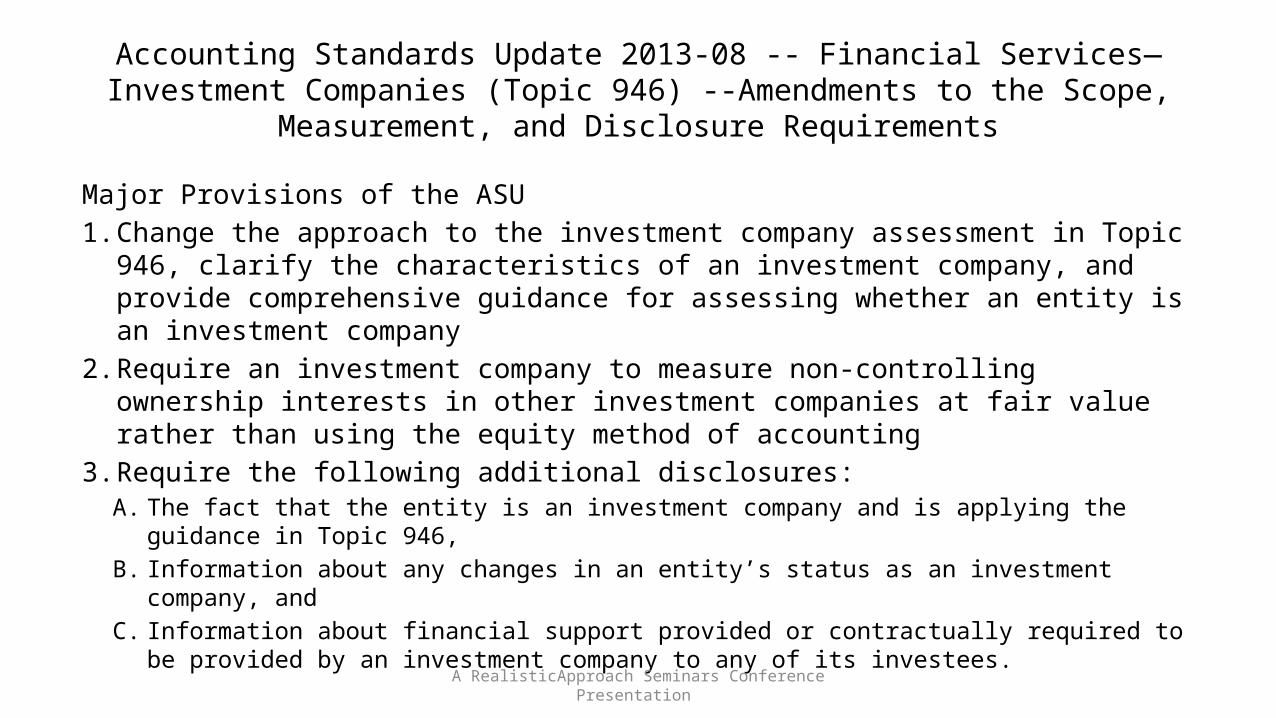

Accounting Standards Update 2013-08 -- Financial Services—Investment Companies (Topic 946) --Amendments to the Scope, Measurement, and Disclosure Requirements

Major Provisions of the ASU1. Change the approach to the investment company assessment in Topic 946, clarify

the characteristics of an investment company, and provide comprehensive guidance for assessing whether an entity is an investment company

2. Require an investment company to measure non-controlling ownership interests in other investment companies at fair value rather than using the equity method of accounting

3. Require the following additional disclosures: A. The fact that the entity is an investment company and is applying the guidance in Topic

946, B. Information about any changes in an entity’s status as an investment company, and C. Information about financial support provided or contractually required to be provided by

an investment company to any of its investees.A RealisticApproach Seminars Conference Presentation

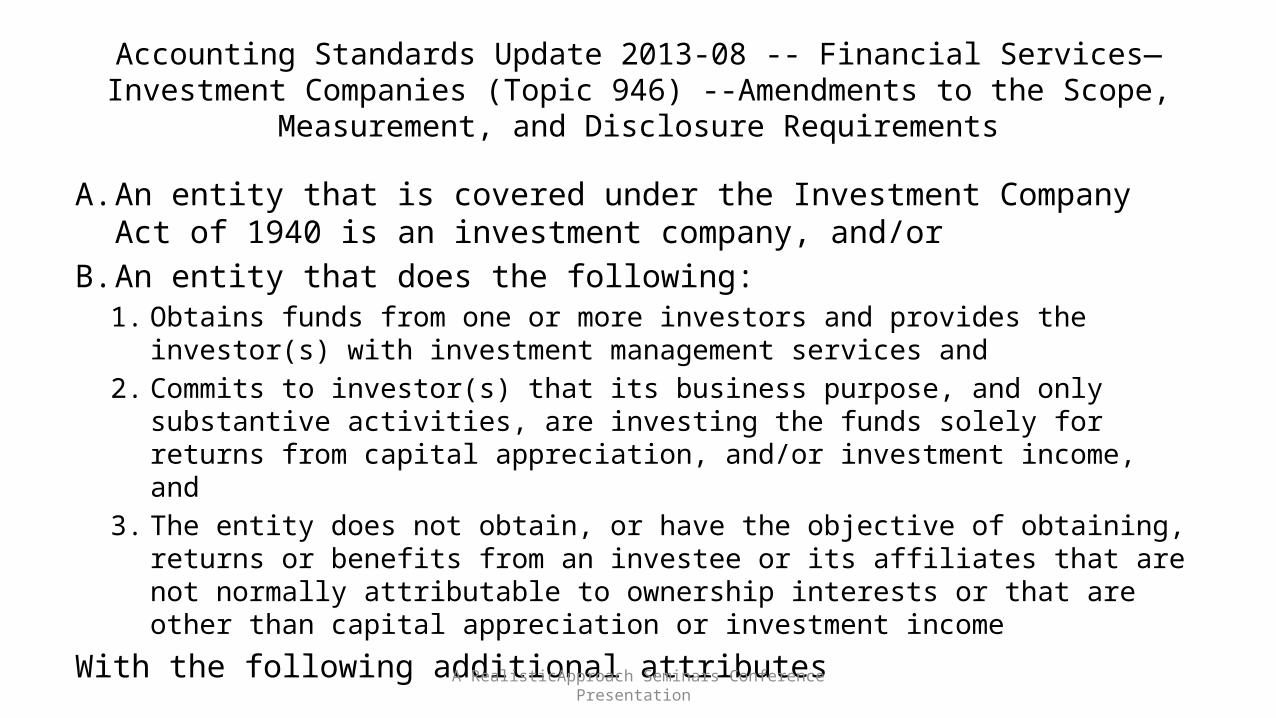

Accounting Standards Update 2013-08 -- Financial Services—Investment Companies (Topic 946) --Amendments to the Scope, Measurement, and Disclosure Requirements

A. An entity that is covered under the Investment Company Act of 1940 is an investment company, and/or

B. An entity that does the following:1. Obtains funds from one or more investors and provides the investor(s) with

investment management services and2. Commits to investor(s) that its business purpose, and only substantive activities,

are investing the funds solely for returns from capital appreciation, and/or investment income, and

3. The entity does not obtain, or have the objective of obtaining, returns or benefits from an investee or its affiliates that are not normally attributable to ownership interests or that are other than capital appreciation or investment income

With the following additional attributesA RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2013-08 -- Financial Services—Investment Companies (Topic 946) --Amendments to the Scope, Measurement, and

Disclosure Requirements

It has1. More than one investment.2. More than one investor.3. Investors that are not related parties of the parent or the investment

manager.4. Ownership interests in the form of equity or partnership interests.5. Historically managed substantially all of its investments on a fair value

basis. The provisions of this Update are effective for an entity’s interim and annual reporting periods in fiscal years that begin after December 15, 2013. Earlier application is prohibited.A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2013-09 --Fair Value Measurement (Topic 820) Deferral of the Effective Date of Certain Disclosures for Nonpublic Employee Benefit Plans in

Update No. 2011-04

This Update defers, indefinitely, the effective date of certain required disclosures in Update 2011-04 (Topic 820) of quantitative information about the significant unobservable inputs used in Level 3 fair value measurements for investments held by a nonpublic employee benefit plan in its plan sponsor’s own nonpublic entity equity securities, including equity securities of its plan sponsor’s nonpublic affiliated entities. The amendments in this Update do not defer the effective date for those certain quantitative disclosures for other nonpublic entity equity securities held in the nonpublic employee benefit plan or any qualitative disclosures. This amendment is effective upon issuance for financial statements that have not been issued.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2013-10 --Derivatives and Hedging (Topic 815)Inclusion of the Fed Funds Effective Swap Rate (or Overnight Index Swap Rate) as a

Benchmark Interest Rate for Hedge Accounting Purposes

The amendments in this Update permit the Fed Funds Effective Swap Rate to be used as a U.S. benchmark interest rate for hedge accounting purposes under Topic 815, in addition to UST and LIBOR. The amendments also remove the restriction on using different benchmark rates for similar hedges.

The provisions of this ASU are effective prospectively for qualifying new or re-designated hedging relationships entered into on or after July 17, 2013.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2013-11 -- Income Taxes (Topic 740) Presentation of an Unrecognized Tax Benefit When a Net Operating Loss

Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists An unrecognized tax benefit, or a portion of an unrecognized tax benefit, should be presented in the financial statements as a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss, or a tax credit carryforward, except as follows. To the extent a net operating loss carryforward, a similar tax loss, or a tax credit carryforward is not available at the reporting date under the tax law of the applicable jurisdiction to settle any additional income taxes that would result from the disallowance of a tax position or the tax law of the applicable jurisdiction does not require the entity to use, and the entity does not intend to use, the deferred tax asset for such purpose, the unrecognized tax benefit should be presented in the financial statements as a liability and should not be combined with deferred tax assets. The assessment of whether a deferred tax asset is available is based on the unrecognized tax benefit and deferred tax asset that exist at the reporting date and should be made presuming disallowance of the tax position at the reporting date. For example, an entity should not evaluate whether the deferred tax asset expires before the statute of limitations on the tax position or whether the deferred tax asset may be used prior to the unrecognized tax benefit being settled.The amendments in this Update do not require new recurring disclosuresA RealisticApproach Seminars Conference Presentation

Accounting Standards Update2013-11 -- Income Taxes (Topic 740) Presentation of an Unrecognized Tax Benefit When a Net Operating Loss

Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists

The provisions of this ASU are effective for fiscal years, and interim periods within those years, beginning after December 15, 2013. For nonpublic entities, the amendments are effective for fiscal years, and interim periods within those years, beginning after December 15, 2014.Early adoption is permitted.The amendments should be applied prospectively to all unrecognized tax benefits that exist at the effective date. Retrospective application is permitted.

A RealisticApproach Seminars Conference Presentation

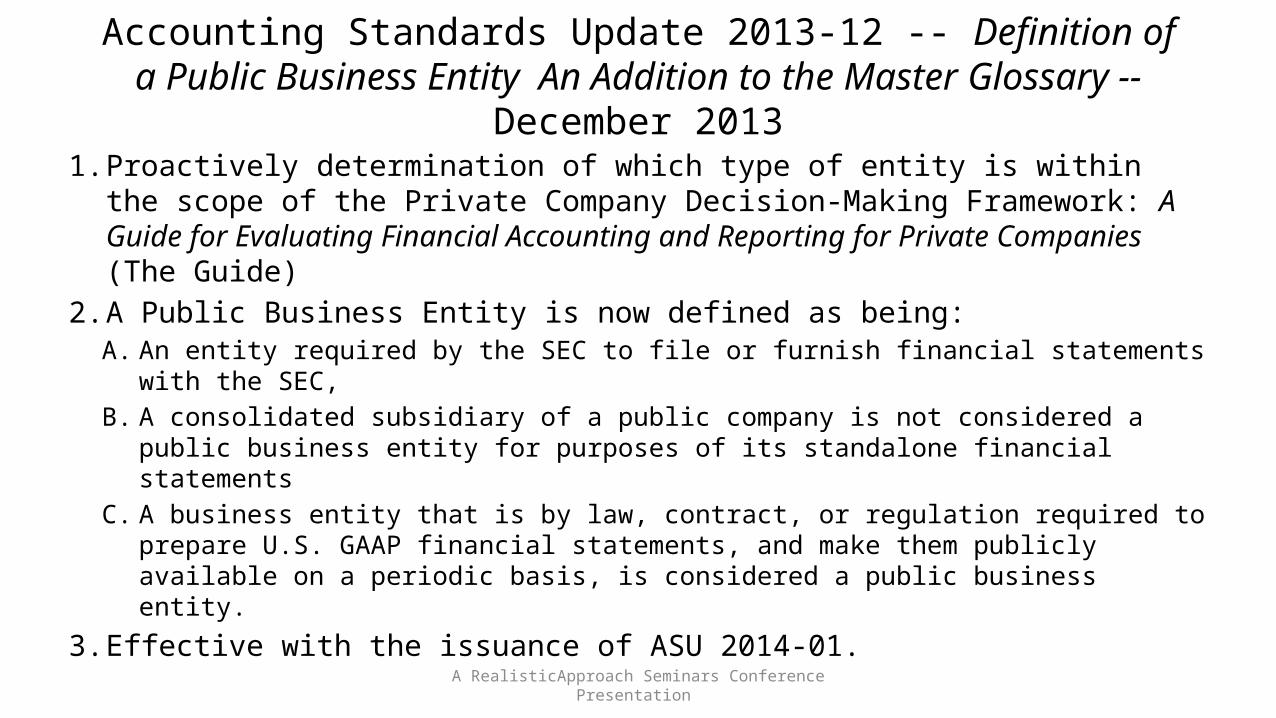

Accounting Standards Update 2013-12 -- Definition of a Public Business Entity An Addition to the Master Glossary -- December 2013

1. Proactively determination of which type of entity is within the scope of the Private Company Decision-Making Framework: A Guide for Evaluating Financial Accounting and Reporting for Private Companies (The Guide)

2. A Public Business Entity is now defined as being: A. An entity required by the SEC to file or furnish financial statements with the SEC, B. A consolidated subsidiary of a public company is not considered a public

business entity for purposes of its standalone financial statements C. A business entity that is by law, contract, or regulation required to prepare U.S.

GAAP financial statements, and make them publicly available on a periodic basis, is considered a public business entity.

3. Effective with the issuance of ASU 2014-01.A RealisticApproach Seminars Conference Presentation

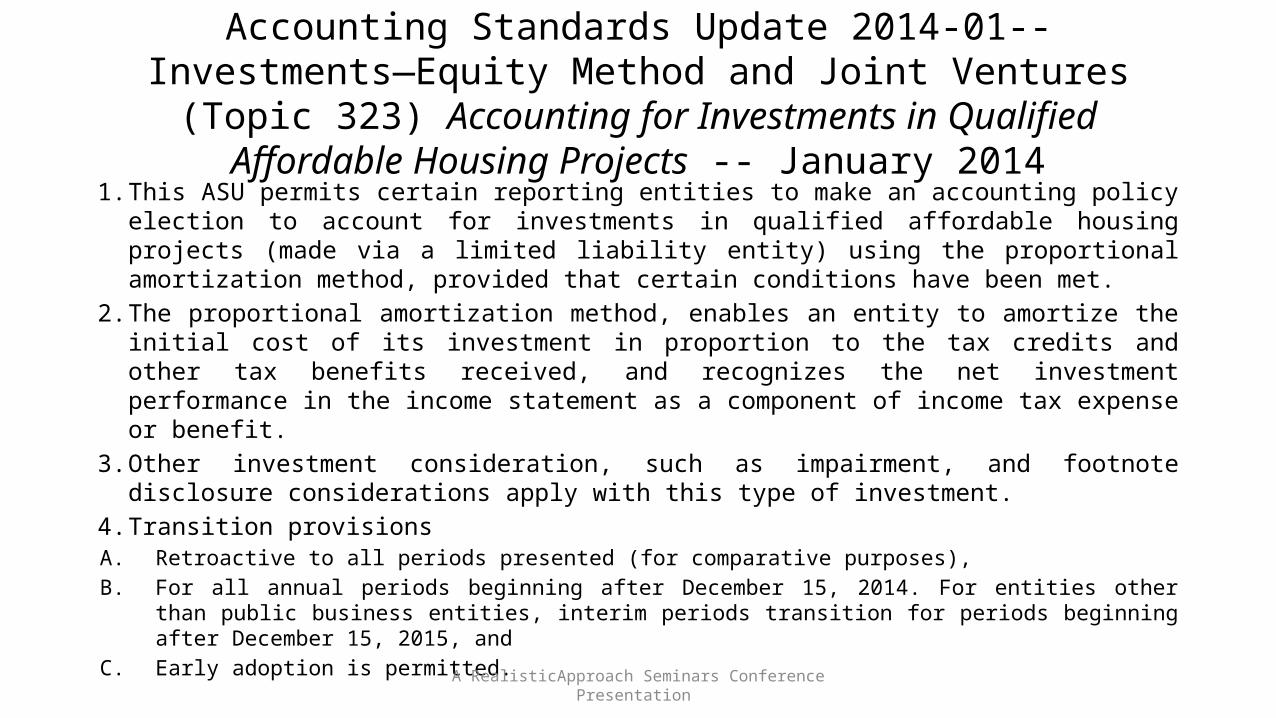

Accounting Standards Update 2014-01-- Investments—Equity Method and Joint Ventures (Topic 323) Accounting for Investments in Qualified

Affordable Housing Projects -- January 20141. This ASU permits certain reporting entities to make an accounting policy election to

account for investments in qualified affordable housing projects (made via a limited liability entity) using the proportional amortization method, provided that certain conditions have been met.

2. The proportional amortization method, enables an entity to amortize the initial cost of its investment in proportion to the tax credits and other tax benefits received, and recognizes the net investment performance in the income statement as a component of income tax expense or benefit.

3. Other investment consideration, such as impairment, and footnote disclosure considerations apply with this type of investment.

4. Transition provisions A. Retroactive to all periods presented (for comparative purposes), B. For all annual periods beginning after December 15, 2014. For entities other than public business

entities, interim periods transition for periods beginning after December 15, 2015, and C. Early adoption is permitted. A RealisticApproach Seminars Conference Presentation

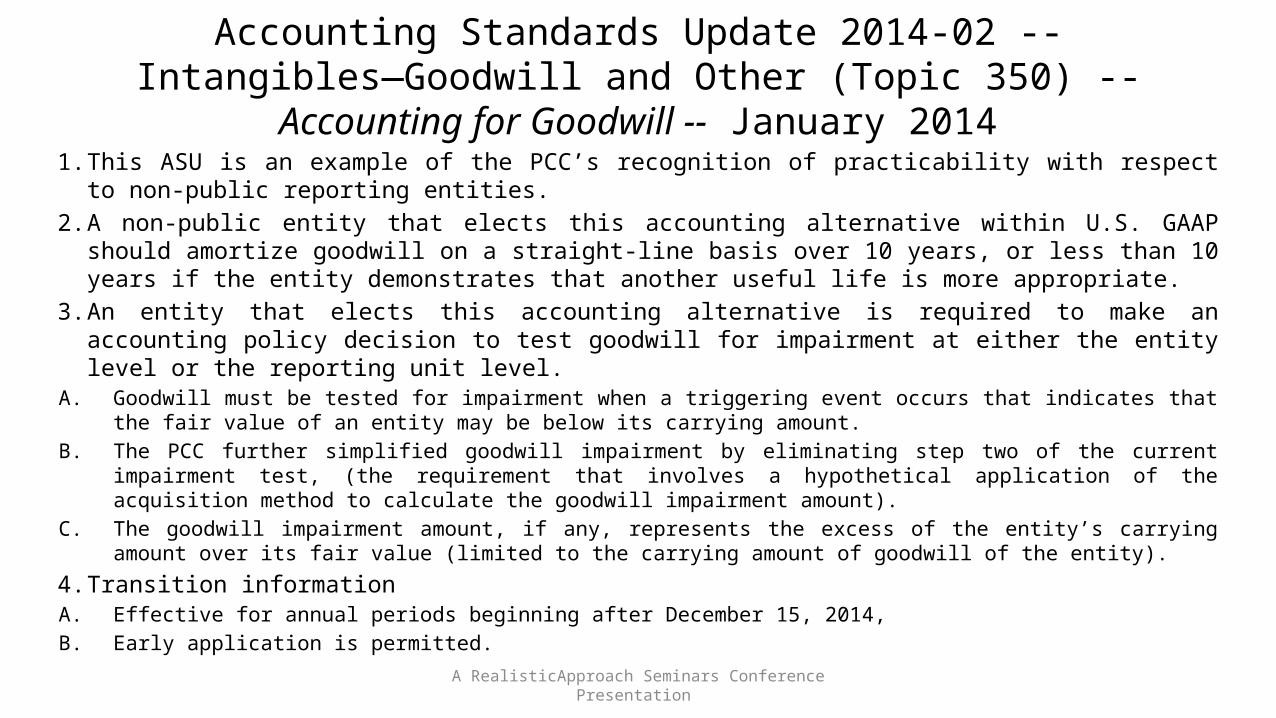

Accounting Standards Update 2014-02 -- Intangibles—Goodwill and Other (Topic 350) -- Accounting for Goodwill -- January 2014

1. This ASU is an example of the PCC’s recognition of practicability with respect to non-public reporting entities.

2. A non-public entity that elects this accounting alternative within U.S. GAAP should amortize goodwill on a straight-line basis over 10 years, or less than 10 years if the entity demonstrates that another useful life is more appropriate.

3. An entity that elects this accounting alternative is required to make an accounting policy decision to test goodwill for impairment at either the entity level or the reporting unit level.

A. Goodwill must be tested for impairment when a triggering event occurs that indicates that the fair value of an entity may be below its carrying amount.

B. The PCC further simplified goodwill impairment by eliminating step two of the current impairment test, (the requirement that involves a hypothetical application of the acquisition method to calculate the goodwill impairment amount).

C. The goodwill impairment amount, if any, represents the excess of the entity’s carrying amount over its fair value (limited to the carrying amount of goodwill of the entity).

4. Transition information A. Effective for annual periods beginning after December 15, 2014, B. Early application is permitted. A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-03 -- Derivatives and Hedging (Topic 815) -- Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified

Hedge Accounting Approach --January 2014

1. Another example of an accommodation to non-public entities regarding accounting for a particular type of hedging transaction. (A particular type of “cash-flow” hedge)

2. The hedging transaction in question involves offsetting the effect of variable-rate debt such that it appears to be a fixed-rate instrument. Hedged risk is increase in interest rate.

3. ASU allows for the non-consideration of non-performance risk – a presumption of 100 percent efficiency of the hedge instrument.

4. Transition information A. Effective for annual periods beginning after December 15, 2014, B. Early application is permitted. A RealisticApproach Seminars Conference Presentation

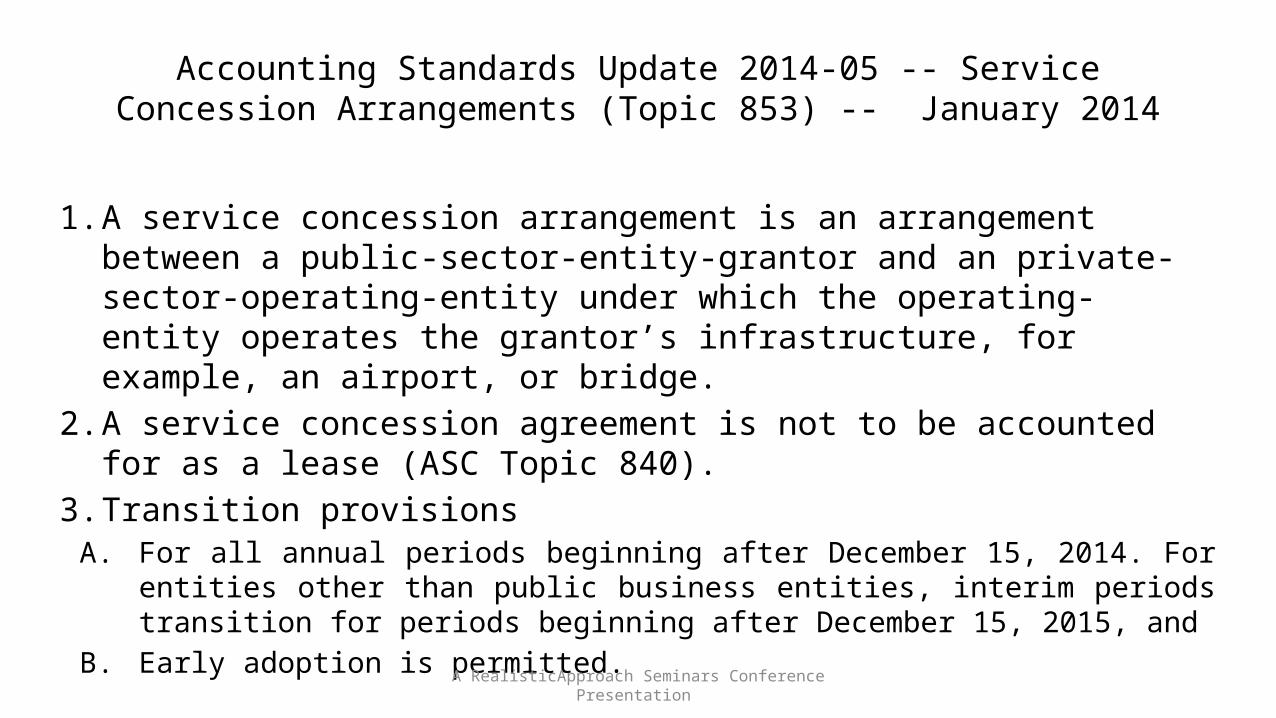

Accounting Standards Update 2014-05 -- Service Concession Arrangements (Topic 853) -- January 2014

1. A service concession arrangement is an arrangement between a public-sector-entity-grantor and an private-sector-operating-entity under which the operating-entity operates the grantor’s infrastructure, for example, an airport, or bridge.

2. A service concession agreement is not to be accounted for as a lease (ASC Topic 840).

3. Transition provisions A. For all annual periods beginning after December 15, 2014. For entities other

than public business entities, interim periods transition for periods beginning after December 15, 2015, and

B. Early adoption is permitted. A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-06 -- Technical Corrections and Improvements Related to Glossary Terms -- March 2014

1. This is an update of terms addressed in the Master Glossary section of the Accounting Standards Codification. There are numerous deletions of terminology that the FASB has determined will not be used in the codification.

2. Transition guidance – Changes in terminology were effective upon issuance of the ASU.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-07 -- Consolidation (Topic 810) -- Applying Variable Interest Entities Guidance to Common Control Leasing

Arrangements -- March 2014

1. Private company financial statement users noted that, in instances in which a lessor entity is consolidated by a private company lessee on the basis of VIE guidance, most users of the private company lessee entity’s financial statements stated that the consolidated financial statements are not relevant to them because users focus on cash flows and tangible worth of the lessee entity, rather than on consolidated cash flows of the consolidated entity as presented under current U.S. generally accepted accounting principles.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-07 -- Consolidation (Topic 810) -- Applying Variable Interest Entities Guidance to Common Control Leasing

Arrangements -- March 2014

2. This ASU permits a private company lessee to elect an alternative to not apply VIE guidance to a lessor entity if

A. The lessee and the lessor entity are under common control, B. The lessee has a lease arrangement with the lessor entity, C. Substantially all of the activities between the private lessee and the lessor are

related to leasing activities including support of leasing activities between the two entities, and

D. If the lessee explicitly guarantees or provides collateral for any obligation of the lessor entity related to the asset leased by the lessee, the principal amount of the obligation, at the inception of such guarantee or collateral arrangement, does not exceed the value of the leased asset.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-07 -- Consolidation (Topic 810) -- Applying Variable Interest Entities Guidance to Common Control Leasing

Arrangements -- March 2014

3. The accounting policy election, once made, should be applied by a private company lessee to all current and future lessor entities under common control that meet the criteria for applying this approach.

4. An electing lessee is not required to make VIE disclosures regarding the lessor entity.

5. Electing lessees are, however, required to make the following disclosures regarding the relationship

A. Amount(s) and key terms of liabilities recognized by the lessor that expose the lessee to a potential obligation to provide financial support to the lessor, and

B. A description of qualitative circumstances, not recognized in the financial statements of the lessor, that may expose the lessee to having to provide financial support to the lessor. A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-07 -- Consolidation (Topic 810) -- Applying Variable Interest Entities Guidance to Common Control Leasing

Arrangements -- March 2014

6. Transition provisions A. For all annual periods beginning after December 15, 2014. For

entities other than public business entities, interim periods transition for periods beginning after December 15, 2015, and

B. Early adoption is permitted.

A RealisticApproach Seminars Conference Presentation

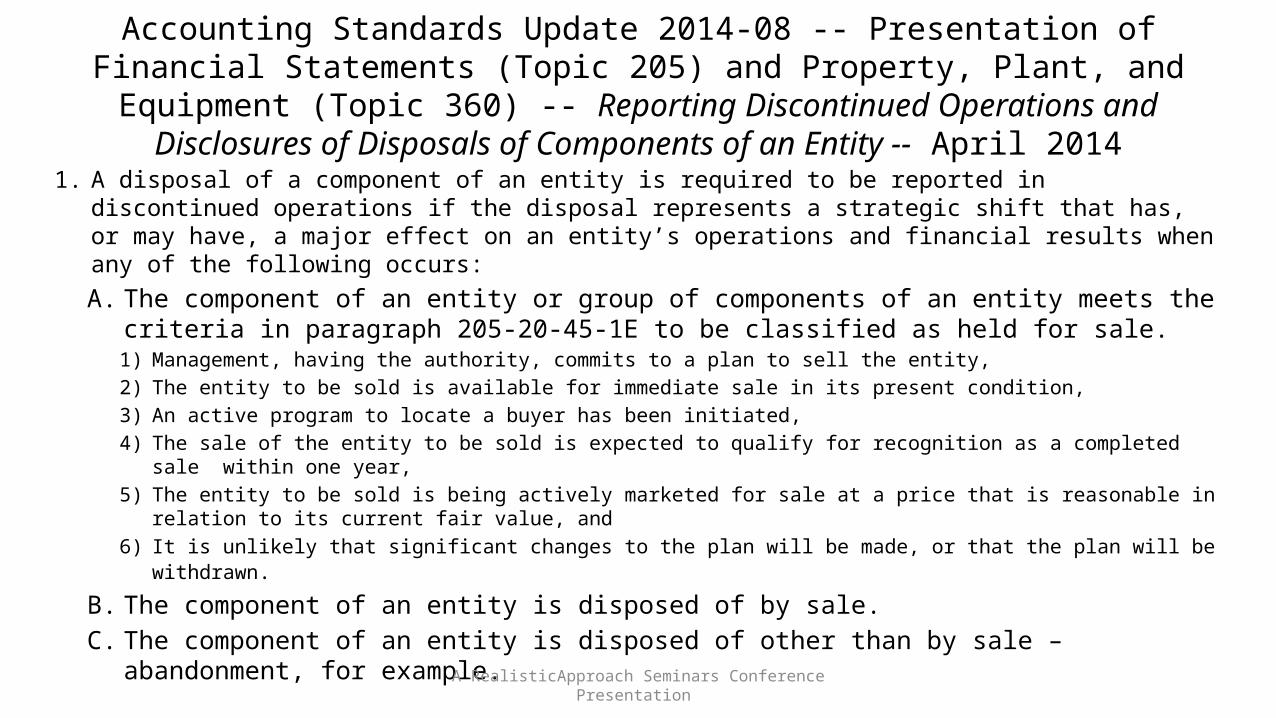

Accounting Standards Update 2014-08 -- Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360) -- Reporting Discontinued Operations and

Disclosures of Disposals of Components of an Entity -- April 2014

1. A disposal of a component of an entity is required to be reported in discontinued operations if the disposal represents a strategic shift that has, or may have, a major effect on an entity’s operations and financial results when any of the following occurs:A. The component of an entity or group of components of an entity meets the criteria in

paragraph 205-20-45-1E to be classified as held for sale. 1) Management, having the authority, commits to a plan to sell the entity, 2) The entity to be sold is available for immediate sale in its present condition, 3) An active program to locate a buyer has been initiated, 4) The sale of the entity to be sold is expected to qualify for recognition as a completed sale within one year, 5) The entity to be sold is being actively marketed for sale at a price that is reasonable in relation to its current

fair value, and 6) It is unlikely that significant changes to the plan will be made, or that the plan will be withdrawn .

B. The component of an entity is disposed of by sale. C. The component of an entity is disposed of other than by sale – abandonment, for

example. A RealisticApproach Seminars Conference Presentation

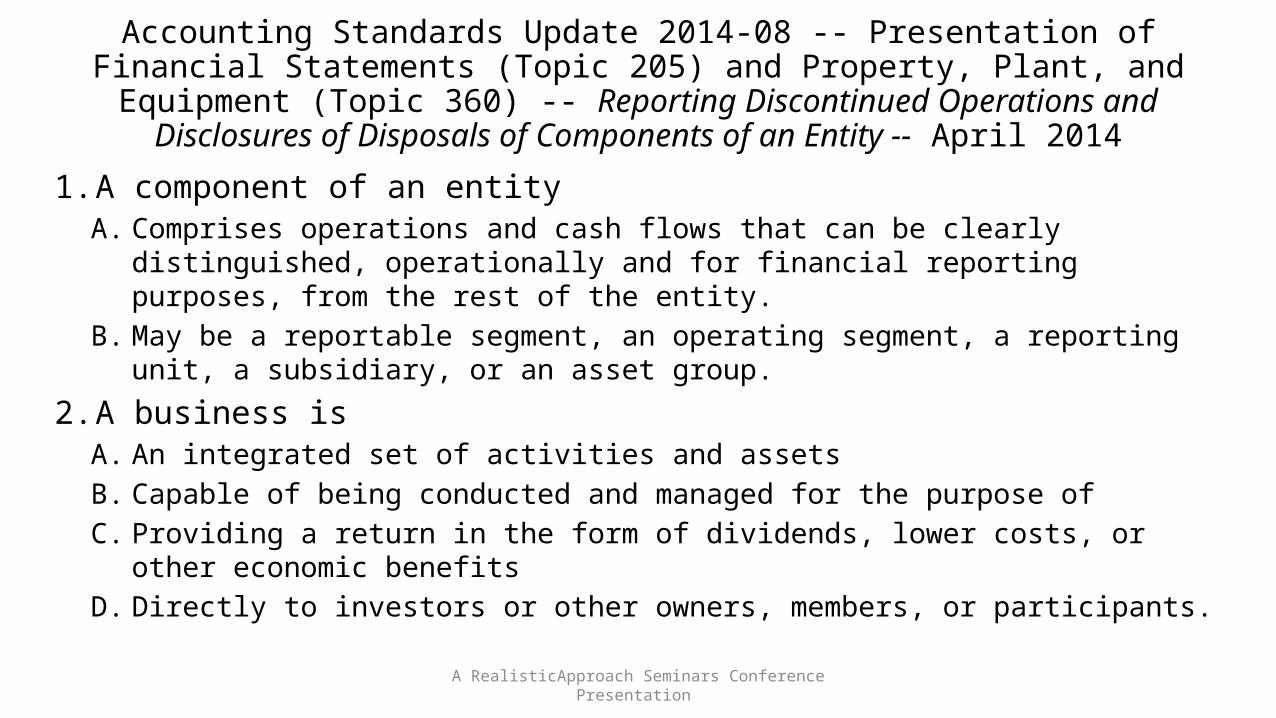

1. A component of an entity A. Comprises operations and cash flows that can be clearly distinguished,

operationally and for financial reporting purposes, from the rest of the entity. B. May be a reportable segment, an operating segment, a reporting unit, a

subsidiary, or an asset group.

2. A business is A. An integrated set of activities and assets B. Capable of being conducted and managed for the purpose of C. Providing a return in the form of dividends, lower costs, or other economic

benefits D. Directly to investors or other owners, members, or participants.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-08 -- Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360) -- Reporting Discontinued Operations and

Disclosures of Disposals of Components of an Entity -- April 2014

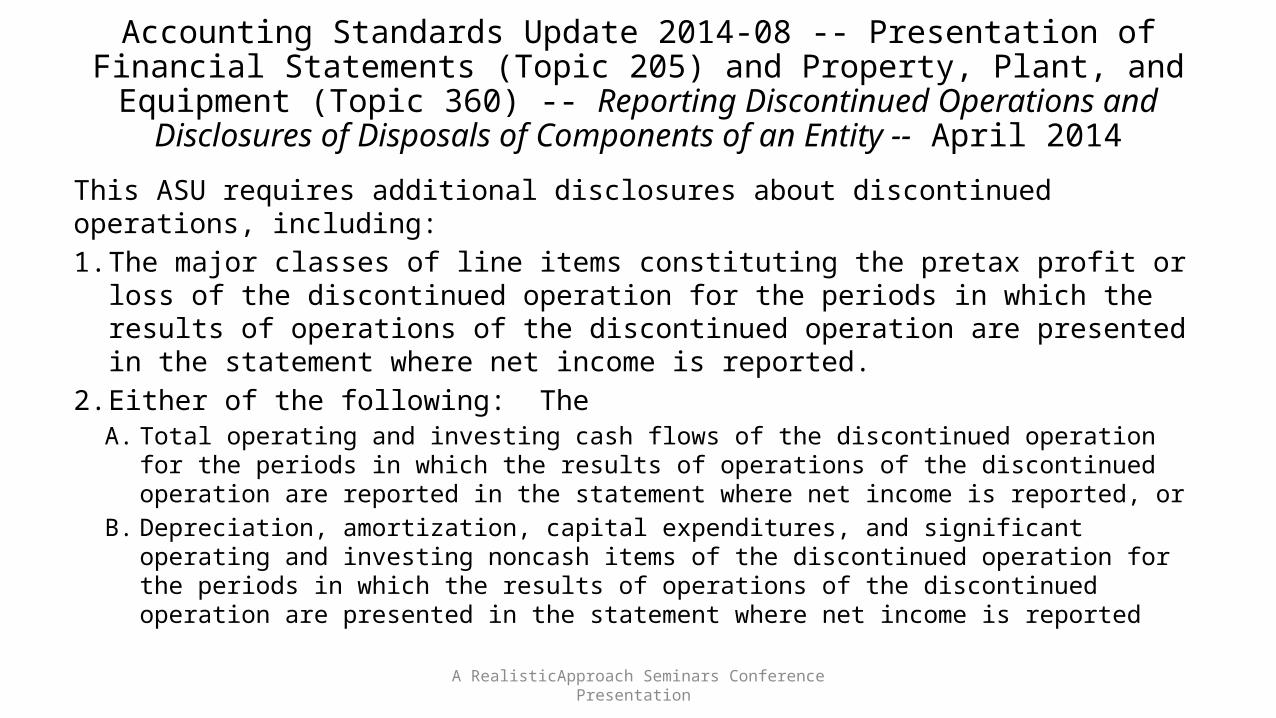

This ASU requires additional disclosures about discontinued operations, including:1. The major classes of line items constituting the pretax profit or loss of the

discontinued operation for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported.

2. Either of the following: TheA. Total operating and investing cash flows of the discontinued operation for the periods in

which the results of operations of the discontinued operation are reported in the statement where net income is reported, or

B. Depreciation, amortization, capital expenditures, and significant operating and investing noncash items of the discontinued operation for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-08 -- Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360) -- Reporting Discontinued Operations and

Disclosures of Disposals of Components of an Entity -- April 2014

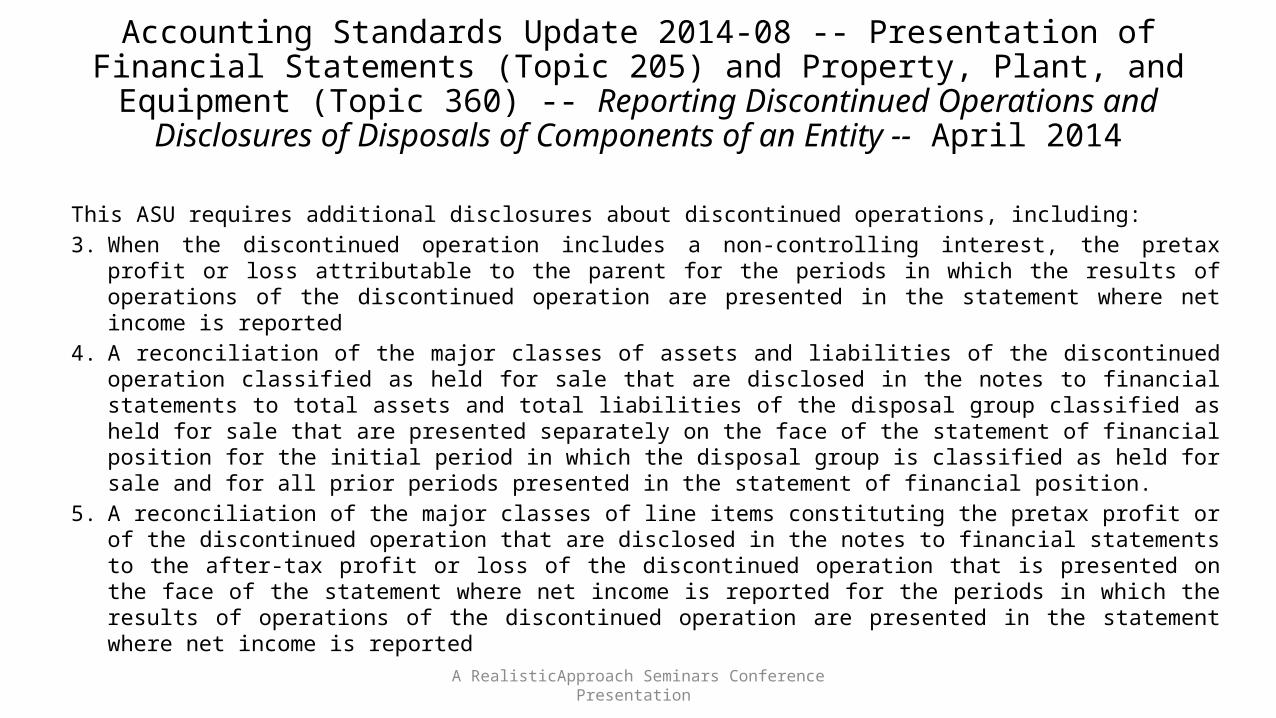

This ASU requires additional disclosures about discontinued operations, including:3. When the discontinued operation includes a non-controlling interest, the pretax profit or loss

attributable to the parent for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported

4. A reconciliation of the major classes of assets and liabilities of the discontinued operation classified as held for sale that are disclosed in the notes to financial statements to total assets and total liabilities of the disposal group classified as held for sale that are presented separately on the face of the statement of financial position for the initial period in which the disposal group is classified as held for sale and for all prior periods presented in the statement of financial position.

5. A reconciliation of the major classes of line items constituting the pretax profit or of the discontinued operation that are disclosed in the notes to financial statements to the after-tax profit or loss of the discontinued operation that is presented on the face of the statement where net income is reported for the periods in which the results of operations of the discontinued operation are presented in the statement where net income is reported

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-08 -- Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360) -- Reporting Discontinued Operations and

Disclosures of Disposals of Components of an Entity -- April 2014

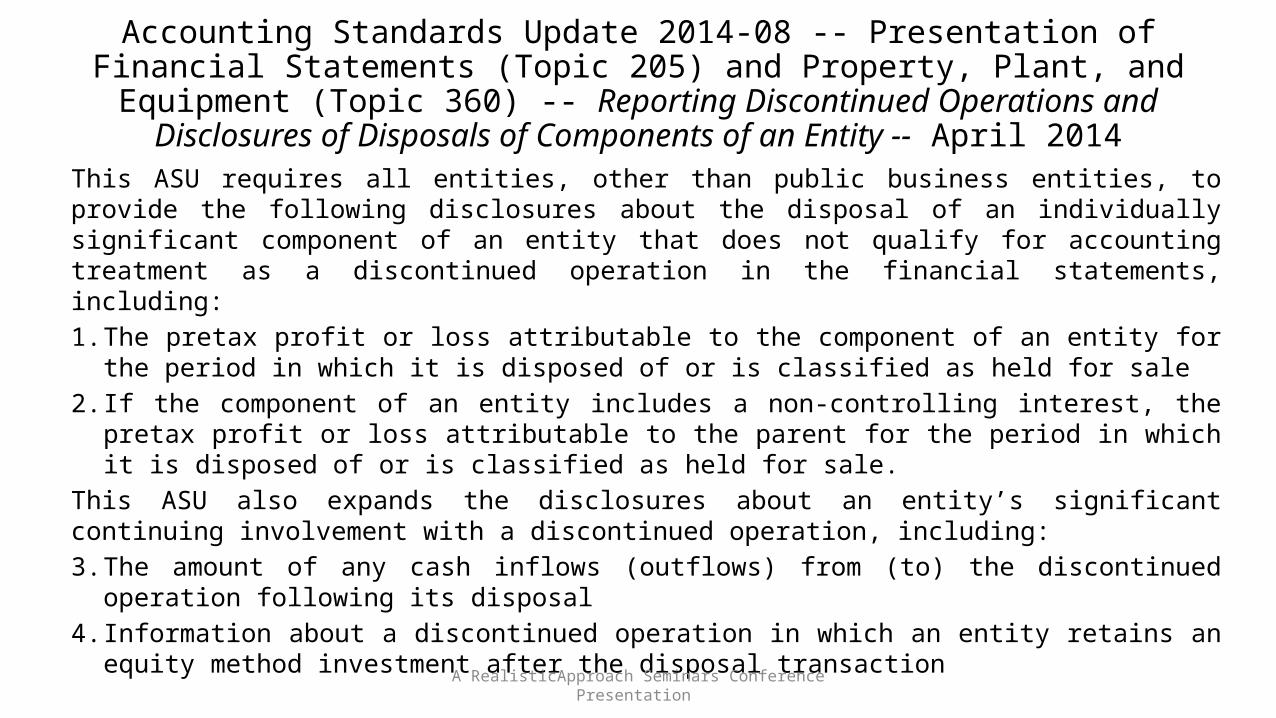

This ASU requires all entities, other than public business entities, to provide the following disclosures about the disposal of an individually significant component of an entity that does not qualify for accounting treatment as a discontinued operation in the financial statements, including:1. The pretax profit or loss attributable to the component of an entity for the period in which it is

disposed of or is classified as held for sale 2. If the component of an entity includes a non-controlling interest, the pretax profit or loss

attributable to the parent for the period in which it is disposed of or is classified as held for sale.

This ASU also expands the disclosures about an entity’s significant continuing involvement with a discontinued operation, including:3. The amount of any cash inflows (outflows) from (to) the discontinued operation following its

disposal4. Information about a discontinued operation in which an entity retains an equity method

investment after the disposal transactionA RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-08 -- Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360) -- Reporting Discontinued Operations and

Disclosures of Disposals of Components of an Entity -- April 2014

Transition -- All entities, other than public business entities, should apply the amendments in this ASU prospectively to each of the following:1. All disposals of components of an entity that occur within annual periods

beginning on or after December 15, 2014, and interim periods within annual periods beginning on or after December 15, 2015

2. All businesses activities that, upon acquisition, are classified as held for sale that occur within annual periods beginning on or after December 15, 2014, and interim periods within annual periods beginning on or after December 15, 2015.

3. Early adoption is permitted, but only for disposals, or classifications as held for sale, that have not been reported in financial statements previously issued or available for issuance.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-08 -- Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360) -- Reporting Discontinued Operations and

Disclosures of Disposals of Components of an Entity -- April 2014

Accounting Standards Update 2014-09 -- Revenue from Contracts with Customers (Topic 606) -- May 2014

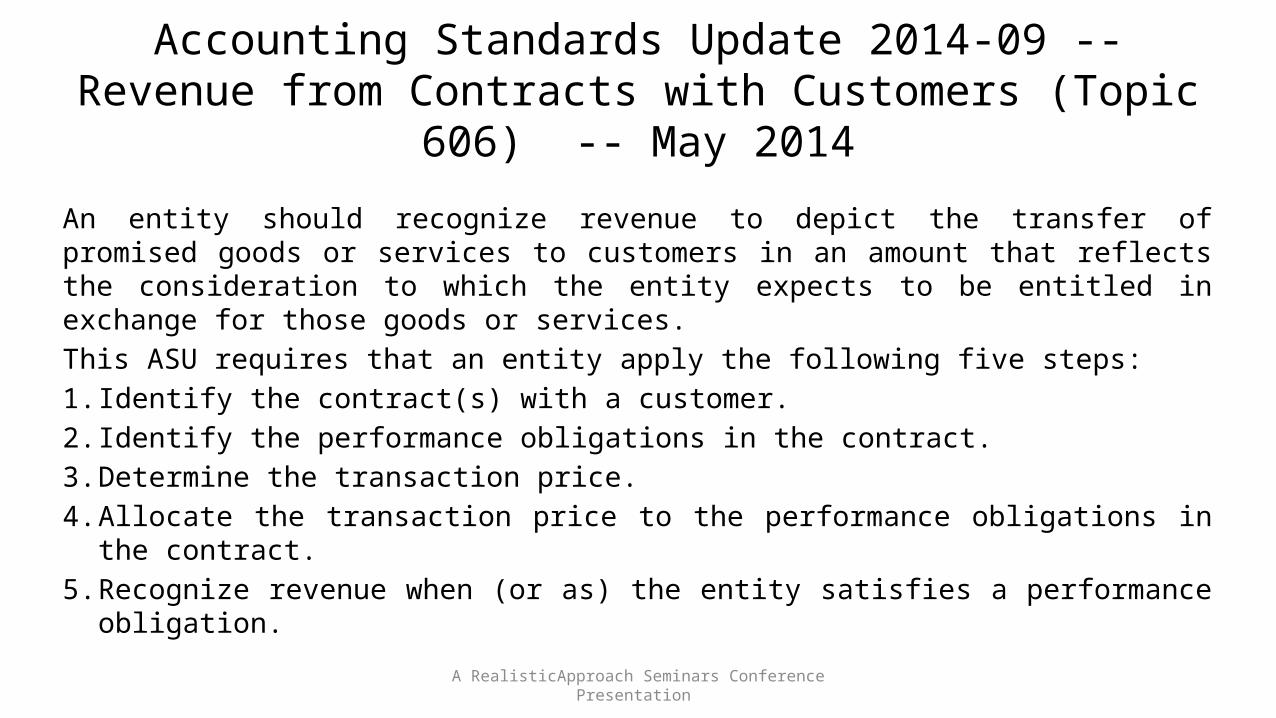

An entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. This ASU requires that an entity apply the following five steps:1. Identify the contract(s) with a customer.2. Identify the performance obligations in the contract.3. Determine the transaction price.4. Allocate the transaction price to the performance obligations in the contract.5. Recognize revenue when (or as) the entity satisfies a performance

obligation.A RealisticApproach Seminars Conference Presentation

Regarding step 1, this ASU applies to each contract that meets the following criteria:1. Approval and commitment of the parties2. Identification of the rights of the parties3. Identification of the payment terms4. The contract has commercial substance5. It is probable that the entity will collect the consideration to

which it will be entitled in exchange for the goods or services that will be transferred to the customer

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-09 -- Revenue from Contracts with Customers (Topic 606) -- May 2014

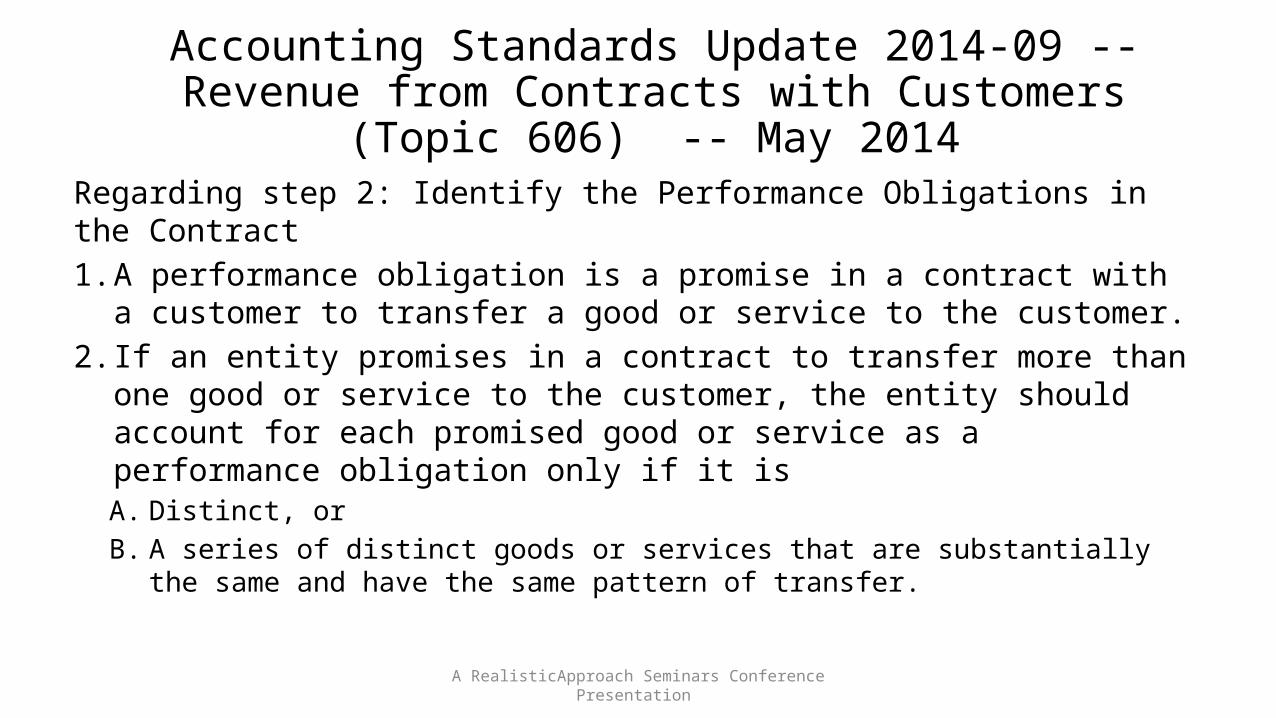

Regarding step 2: Identify the Performance Obligations in the Contract1. A performance obligation is a promise in a contract with a customer

to transfer a good or service to the customer. 2. If an entity promises in a contract to transfer more than one good

or service to the customer, the entity should account for each promised good or service as a performance obligation only if it is A. Distinct, or B. A series of distinct goods or services that are substantially the same and

have the same pattern of transfer.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-09 -- Revenue from Contracts with Customers (Topic 606) -- May 2014

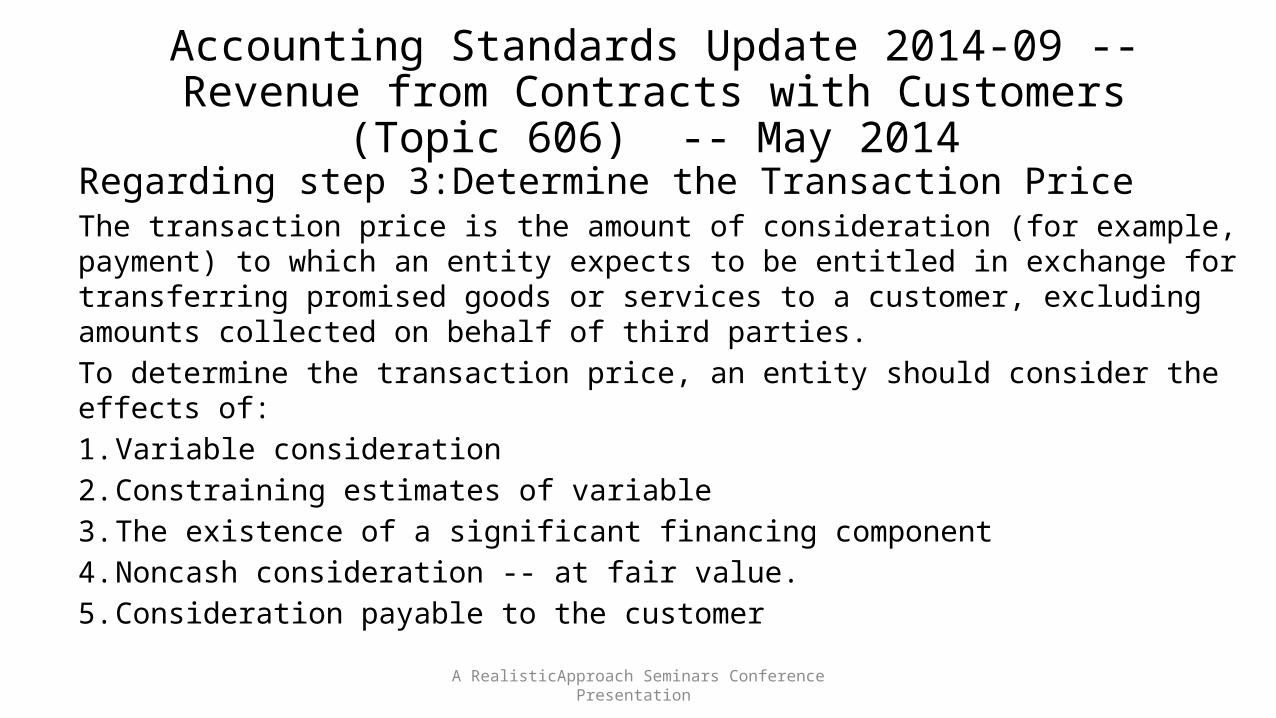

Regarding step 3:Determine the Transaction Price The transaction price is the amount of consideration (for example, payment) to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties. To determine the transaction price, an entity should consider the effects of:1. Variable consideration 2. Constraining estimates of variable 3. The existence of a significant financing component 4. Noncash consideration -- at fair value. 5. Consideration payable to the customer

A RealisticApproach Seminars Conference Presentation

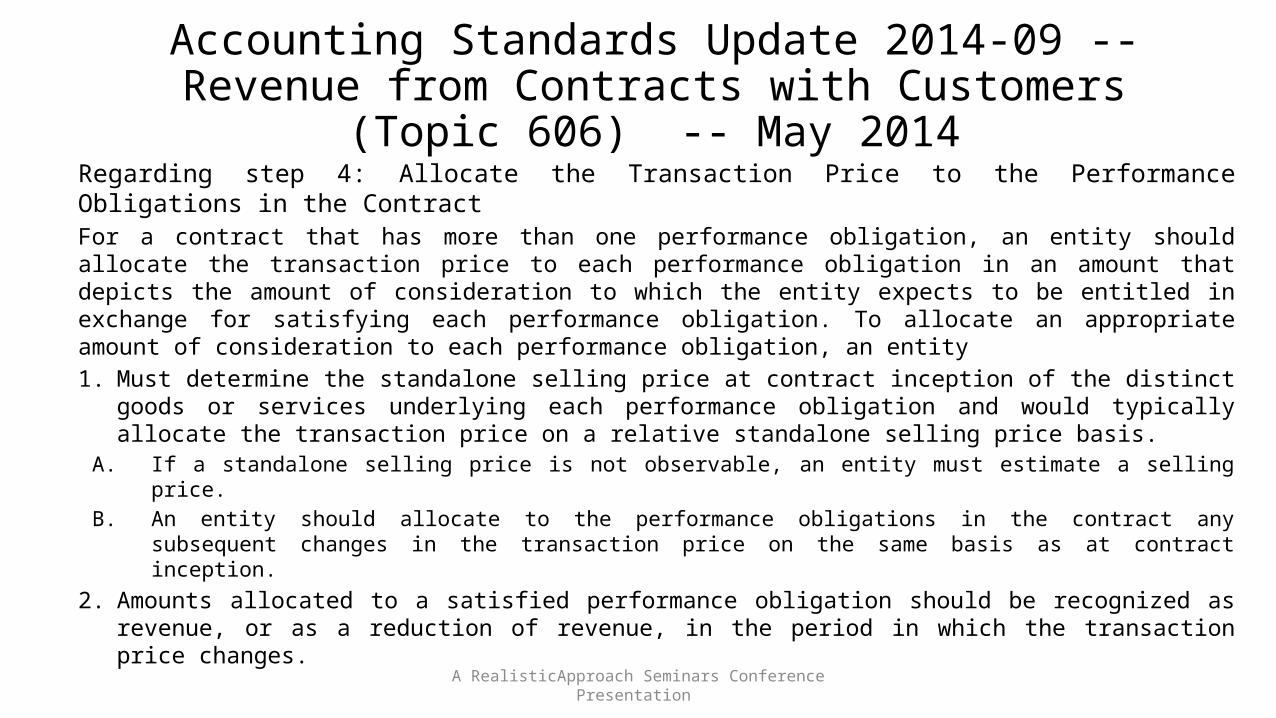

Accounting Standards Update 2014-09 -- Revenue from Contracts with Customers (Topic 606) -- May 2014

Regarding step 4: Allocate the Transaction Price to the Performance Obligations in the ContractFor a contract that has more than one performance obligation, an entity should allocate the transaction price to each performance obligation in an amount that depicts the amount of consideration to which the entity expects to be entitled in exchange for satisfying each performance obligation. To allocate an appropriate amount of consideration to each performance obligation, an entity 1. Must determine the standalone selling price at contract inception of the distinct goods or services

underlying each performance obligation and would typically allocate the transaction price on a relative standalone selling price basis.

A. If a standalone selling price is not observable, an entity must estimate a selling price. B. An entity should allocate to the performance obligations in the contract any subsequent changes in the

transaction price on the same basis as at contract inception. 2. Amounts allocated to a satisfied performance obligation should be recognized as revenue, or as a

reduction of revenue, in the period in which the transaction price changes.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-09 -- Revenue from Contracts with Customers (Topic 606) -- May 2014

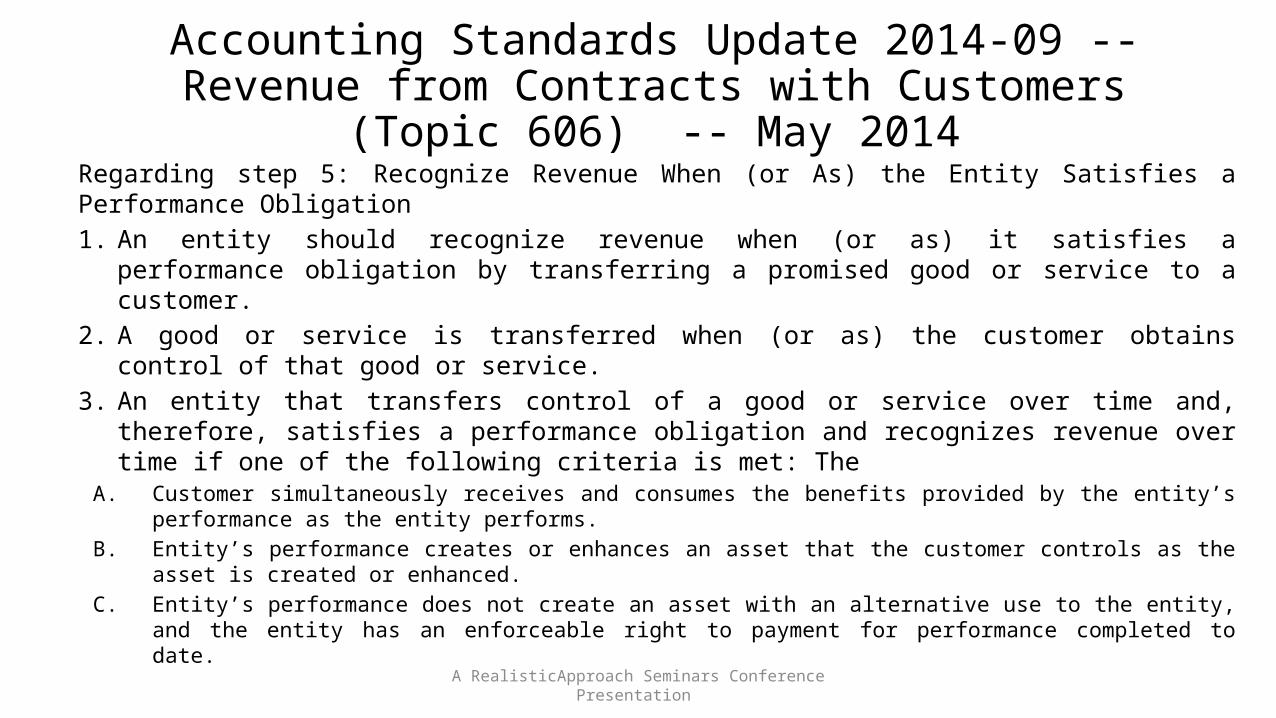

Regarding step 5: Recognize Revenue When (or As) the Entity Satisfies a Performance Obligation 1. An entity should recognize revenue when (or as) it satisfies a performance obligation by

transferring a promised good or service to a customer. 2. A good or service is transferred when (or as) the customer obtains control of that good or

service. 3. An entity that transfers control of a good or service over time and, therefore, satisfies a

performance obligation and recognizes revenue over time if one of the following criteria is met: The

A. Customer simultaneously receives and consumes the benefits provided by the entity’s performance as the entity performs.

B. Entity’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced.

C. Entity’s performance does not create an asset with an alternative use to the entity, and the entity has an enforceable right to payment for performance completed to date.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-09 -- Revenue from Contracts with Customers (Topic 606) -- May 2014

Regarding step 5: Recognize Revenue When (or As) the Entity Satisfies a Performance Obligation 4. If a performance obligation is not satisfied over time, an entity satisfies the

performance obligation at a point in time. To determine the point in time at which a customer obtains control of a promised asset and an entity satisfies a performance obligation, the entity would consider indicators of the transfer of control, which include, but are not limited to, the following: The1. Entity has a present right to payment for the asset.2. Customer has legal title to the asset.3. Entity has transferred physical possession of the asset. 4. Customer has the significant risks and rewards of ownership of the asset.5. Customer has accepted the asset.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-09 -- Revenue from Contracts with Customers (Topic 606) -- May 2014

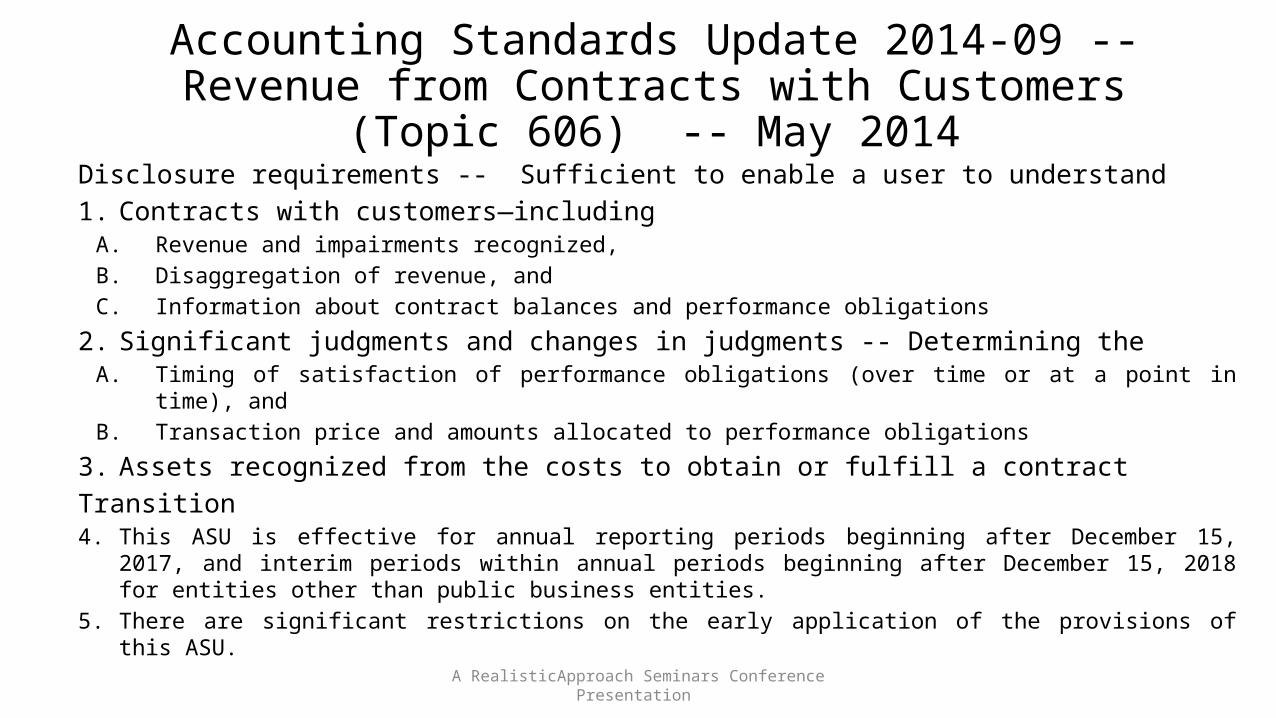

Disclosure requirements -- Sufficient to enable a user to understand1. Contracts with customers—including

A. Revenue and impairments recognized, B. Disaggregation of revenue, and C. Information about contract balances and performance obligations

2. Significant judgments and changes in judgments -- Determining the A. Timing of satisfaction of performance obligations (over time or at a point in time), and B. Transaction price and amounts allocated to performance obligations

3. Assets recognized from the costs to obtain or fulfill a contract Transition 4. This ASU is effective for annual reporting periods beginning after December 15, 2017, and interim

periods within annual periods beginning after December 15, 2018 for entities other than public business entities.

5. There are significant restrictions on the early application of the provisions of this ASU.A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-09 -- Revenue from Contracts with Customers (Topic 606) -- May 2014

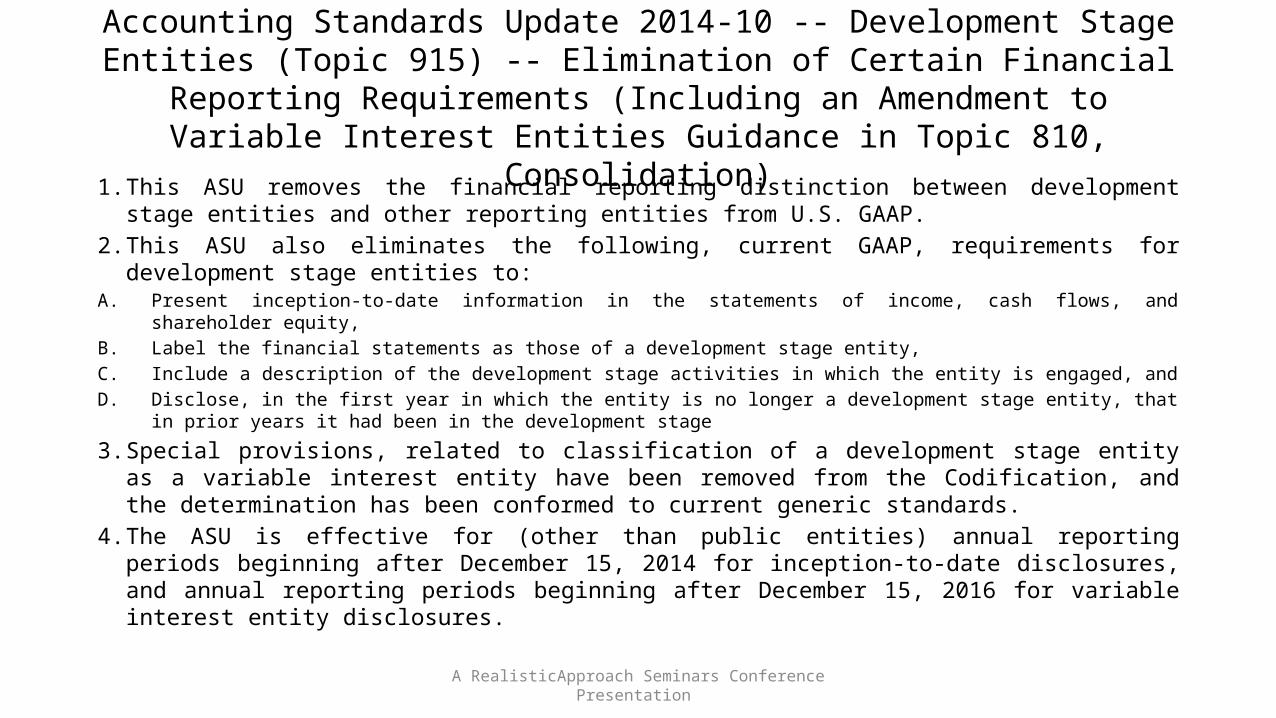

Accounting Standards Update 2014-10 -- Development Stage Entities (Topic 915) -- Elimination of Certain Financial Reporting Requirements (Including an Amendment

to Variable Interest Entities Guidance in Topic 810, Consolidation)

1. This ASU removes the financial reporting distinction between development stage entities and other reporting entities from U.S. GAAP.

2. This ASU also eliminates the following, current GAAP, requirements for development stage entities to:

A. Present inception-to-date information in the statements of income, cash flows, and shareholder equity, B. Label the financial statements as those of a development stage entity, C. Include a description of the development stage activities in which the entity is engaged, and D. Disclose, in the first year in which the entity is no longer a development stage entity, that in prior years it had

been in the development stage

3. Special provisions, related to classification of a development stage entity as a variable interest entity have been removed from the Codification, and the determination has been conformed to current generic standards.

4. The ASU is effective for (other than public entities) annual reporting periods beginning after December 15, 2014 for inception-to-date disclosures, and annual reporting periods beginning after December 15, 2016 for variable interest entity disclosures.

A RealisticApproach Seminars Conference Presentation

Accounting Standards Update 2014-11 -- Transfers and Servicing (Topic 860): Repurchase-to-Maturity Transactions, Repurchase Financings, and Disclosures

1. The ASU states that repurchase-to-maturity transactions are to be accounted for as secured borrowing transactions (as opposed to purchase/sale transactions), and

2. Secured Borrowing Accounting requires a separate accounting for transfer of an asset and movement of cash.

A RealisticApproach Seminars Conference Presentation

The provisions of this ASU relate to a particular type of (typically) short-term investment of funds – normally a component of a cash-management effort – wherein an entity “purchases” a portfolio of securities, with an explicit understanding that the selling organization will re-purchase that portfolio at a specified future date. A. This ASU addresses those circumstances where the securities in question will actually mature during the holding

period of the investor. B. Additionally, the ASU addresses disclosures for repurchase-financing-agreement type arrangements. This is a two-

step process wherein1. Entity A sells a financial instrument to Entity B, and then 2. Entity A “purchases” that same financial instrument from Entity B in a classic repurchase agreement, and 3. Entity B repurchases the financial instrument from Entity A – and closes out the cycle.

Accounting Standards Update 2014-11 -- Transfers and Servicing (Topic 860): Repurchase-to-Maturity Transactions, Repurchase Financings, and Disclosures

3. The ASU states that repurchase-financing arrangements that are open at a particular reporting date include the following disclosures: The

A. Carrying amount of assets de-recognized as of the date of de-recognition, B. Amount of gross proceeds received by the transferor at the time of de-recognition for the assets derecognized C. Information about the transferor’s ongoing exposure to the economic return on the transferred financial assets, and D. Amounts reported in the statement of financial position arising from the transaction.

A RealisticApproach Seminars Conference Presentation

The provisions of this ASU relate to a particular type of (typically) short-term investment of funds – normally a component of a cash-management effort – wherein an entity “purchases” a portfolio of securities, with an explicit understanding that the selling organization will re-purchase that portfolio at a specified future date. A. This ASU addresses those circumstances where the securities in question will actually mature during the holding

period of the investor. B. Additionally, the ASU addresses disclosures for repurchase-financing-agreement type arrangements. This is a two-

step process wherein1. Entity A sells a financial instrument to Entity B, and then 2. Entity A “purchases” that same financial instrument from Entity B in a classic repurchase agreement, and 3. Entity B repurchases the financial instrument from Entity A – and closes out the cycle.

Accounting Standards Update 2014-11 -- Transfers and Servicing (Topic 860): Repurchase-to-Maturity Transactions, Repurchase Financings, and Disclosures

4. Additionally, the ASU states that the following three disclosures should be made for all repurchase arrangements: A. A disaggregation of the gross obligation by the class of collateral pledged, B. The remaining contractual period of the agreement(s), and C. A discussion of the potential risks associated with the

1) Agreement, and 2) The related collateral pledged, including obligations arising from a decline in the fair value of the collateral pledged and 3) How risks are managed.

5. The accounting changes are effective for annual periods beginning after December 15, 2014.

A RealisticApproach Seminars Conference Presentation

The provisions of this ASU relate to a particular type of (typically) short-term investment of funds – normally a component of a cash-management effort – wherein an entity “purchases” a portfolio of securities, with an explicit understanding that the selling organization will re-purchase that portfolio at a specified future date. A. This ASU addresses those circumstances where the securities in question will actually mature during the holding

period of the investor. B. Additionally, the ASU addresses disclosures for repurchase-financing-agreement type arrangements. This is a two-

step process wherein1. Entity A sells a financial instrument to Entity B, and then 2. Entity A “purchases” that same financial instrument from Entity B in a classic repurchase agreement, and 3. Entity B repurchases the financial instrument from Entity A – and closes out the cycle.

Accounting Standards Update 2014-12 -- Compensation (Topic 718): Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance

Target Could Be Achieved after the Requisite Service Period (a consensus of the FASB Emerging Issues Task Force)

The ASU requires that a performance target that affects 1. Vesting, and 2. Could be achieved after the requisite service period be treated as a performance condition.

A performance condition is a matter that affects vesting, exercisability, or other factors considered in determining the fair value of a stock-based compensation award that affects each of the following elements: 3. Employee rendering of service for a specified period of time, and 4. Achievement of a specified performance target, as defined by the employer

Effective for annual periods beginning after December 15, 2015. Earlier adoption is permitted.

A RealisticApproach Seminars Conference Presentation

Matters in Exposure

1. Proposed Statement of Financial Accounting Concepts—Conceptual Framework for Financial Reporting: Chapter 8: Notes to Financial Statements – Comment period ends July 14, 2014.

2. Proposed Accounting Standards Update, Leases (Topic 842): a revision of the 2010 proposed Accounting Standards Update, Leases (Topic 840).

A RealisticApproach Seminars Conference Presentation

Recent ASU Issuances1. ASU No. 2014-13—Consolidation (Topic 810): Measuring the Financial Assets and the Financial

Liabilities of a Consolidated Collateralized Financing Entity (a consensus of the FASB Emerging Issues Task Force)

2. ASU No. 2014-14—Receivables—Troubled Debt Restructurings by Creditors (Subtopic 310-40): Classification of Certain Government-Guaranteed Mortgage Loans upon Foreclosure (a consensus of the FASB Emerging Issues Task Force)

3. ASU No. 2014-15—Presentation of Financial Statements—Going Concern (Subtopic 205-40): Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

4. Update No. 2014-16—Derivatives and Hedging (Topic 815): Determining Whether the Host Contract in a Hybrid Financial Instrument Issued in the Form of a Share Is More Akin to Debt or to Equity (a consensus of the FASB Emerging Issues Task Force)

5. ASU No. 2014-17—Business Combinations (Topic 805): Pushdown Accounting (a consensus of the FASB Emerging Issues Task Force)

A RealisticApproach Seminars Conference Presentation

Annual Auditing Standards Update

A RealisticApproach Seminars Conference Presentation

Recently Issued Statements on Auditing Standards

A RealisticApproach Seminars Conference Presentation

Accessing Recently Issued Statements on Auditing Standards

A RealisticApproach Seminars Conference Presentation

Alert That Restricts the Use of the Auditor's Written Communication

1. Prior to the clarity project, this topic was known of as restricted-distribution reporting. 2. This Statement on Auditing Standards (SAS) became effective for

A. The auditor's written communications related to audits of financial statements for periods ending on or after December 15, 2012.

B. For all other engagements (other than audits) conducted in accordance with GAAS, this SAS is effective for the auditor's written communications issued on or after December 15, 2012.

3. Objective of SAS is to provide a tool whereby an auditor can restrict the distribution (use) of a written communication.

4. There are three categories where restricted distribution is called for by professional standards:

A. Measurement and/or disclosure matters are such that the auditor believes that there a limited number of users adequately informed regarding such matters, or

B. Measurement and/or disclosure criteria are, in fact, only available to certain parties, or C. The communication is a “by-product” report.

A RealisticApproach Seminars Conference Presentation

Alert That Restricts the Use of the Auditor's Written Communication

5. Elements of the restricted distribution paragraph A. A statement that the written communication is intended solely for the identified parties, B. Identification of the specified parties, and C. A statement that the communication is not intended to be, and should not be, used by anyone other than

the specified parties.

6. The SAS contains example wording, such as This communication is intended solely for the information and use of management, others

within the organization, and [identify any other parties] and is not intended to be, and should not be, used by anyone other than these specified parties.

7. Additional parties may be added to the restricted distribution, provided that the auditor obtains a representation from the additional parties addressing the following matters: Familiarity with the

A. Nature of the engagement, B. Measurement and/or disclosure criteria, and C. Auditor’s written communication (report)

8. There is separate guidance for this type of report when the engagement is conducted in accordance with Government Auditing Standards (Yellow Book)

A RealisticApproach Seminars Conference Presentation

Alert That Restricts the Use of the Auditor's Written Communication

9. Following is a listing of situations, currently addressed in auditing standards, that may result in a restricted distribution report: A. The Auditor's Communication With Those Charged With GovernanceB. Communicating Internal Control Related Matters Identified in an Audit C. Supplementary Information in Relation to the Financial Statements as a WholeD. Special Considerations—Audits of Financial Statements Prepared in Accordance

With Special Purpose FrameworksE. Reporting on Compliance With Aspects of Contractual Agreements or Regulatory

Requirements in Connection With Audited Financial StatementsF. Reports on Application of Requirements of an Applicable Financial Reporting

FrameworkG. Letters for Underwriters and Certain Other Requesting PartiesH. Compliance Audits

A RealisticApproach Seminars Conference Presentation

The Auditor's Consideration of an Entity's Ability to Continue as a Going Concern

1. This SAS is a re-drafting of rules-based SAS 59 into principles-based requirements. There does not appear to be any significant change in audit requirements set forth in this document.

2. Objectives stated in SAS No. 126 A. Evaluate and conclude, based on the audit evidence obtained,

1) Whether there is substantial doubt about the entity's ability to continue as a going concern 2) For a reasonable period of time

B. Identify and assess (risk surrounding) the possible financial statement effects (includes disclosure) regarding uncertainty(ies) about the entity's ability to continue as a going concern for a reasonable period of time, and

C. Ascertain the effect, if any, on the auditor’s report.

A RealisticApproach Seminars Conference Presentation

The Auditor's Consideration of an Entity's Ability to Continue as a Going Concern

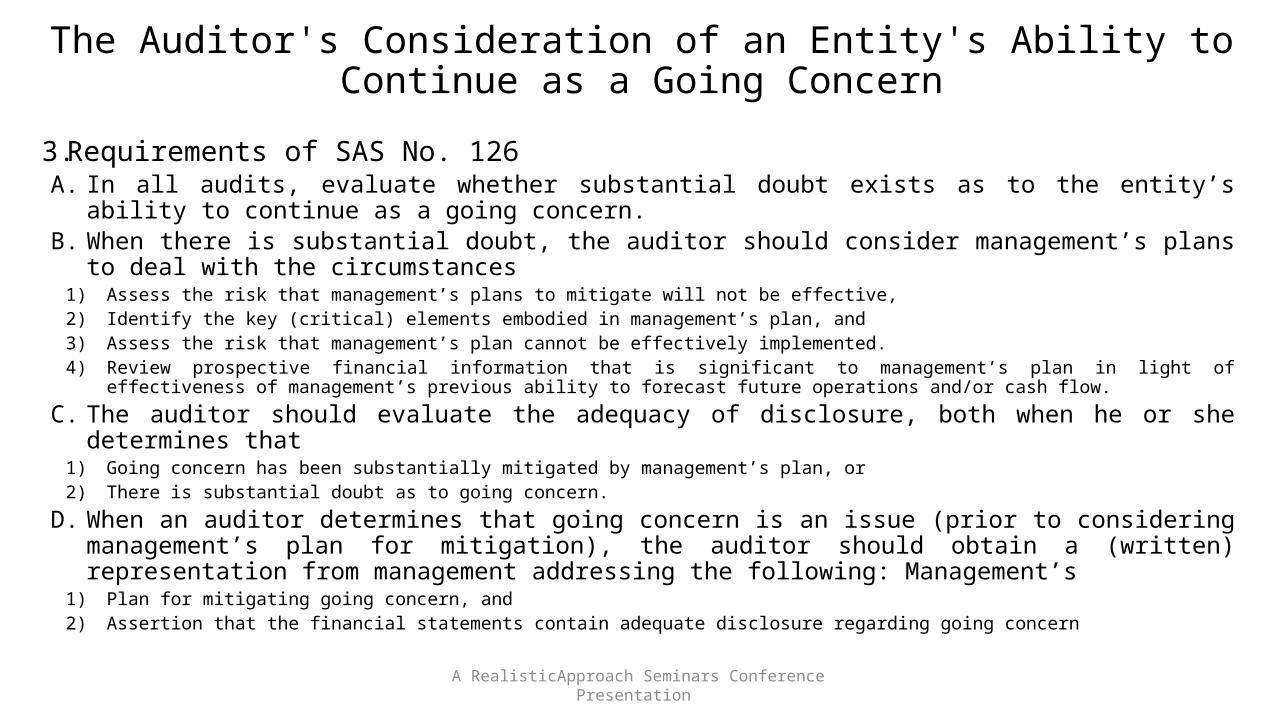

3. Requirements of SAS No. 126 A. In all audits, evaluate whether substantial doubt exists as to the entity’s ability to continue as a going

concern. B. When there is substantial doubt, the auditor should consider management’s plans to deal with the

circumstances 1) Assess the risk that management’s plans to mitigate will not be effective, 2) Identify the key (critical) elements embodied in management’s plan, and 3) Assess the risk that management’s plan cannot be effectively implemented. 4) Review prospective financial information that is significant to management’s plan in light of effectiveness of management’s previous ability

to forecast future operations and/or cash flow.

C. The auditor should evaluate the adequacy of disclosure, both when he or she determines that 1) Going concern has been substantially mitigated by management’s plan, or 2) There is substantial doubt as to going concern.

D. When an auditor determines that going concern is an issue (prior to considering management’s plan for mitigation), the auditor should obtain a (written) representation from management addressing the following: Management’s

1) Plan for mitigating going concern, and 2) Assertion that the financial statements contain adequate disclosure regarding going concern

A RealisticApproach Seminars Conference Presentation

The Auditor's Consideration of an Entity's Ability to Continue as a Going Concern

3. Requirements of SAS No. 126 E. Consider the effects on the auditor’s report

1) Requires the inclusion of an emphasis-of-a-matter paragraph in the auditor’s report.2) Emphasis paragraph should include the wording substantial doubt and going concern, 3) If the auditor believes that disclosure regarding going concern is inadequate – the auditor’s report should be

modified 4) If an auditor is not certain regarding going concern, the auditor is not precluded from disclaiming an opinion.

F. Communication with those charged with governance 1) Made when an auditor believes that going concern is an issue, 2) Should address the following areas: The

a. Nature of the concern for going concern, b. Possible effect on amounts in the financial statements, c. Possible effects on disclosures in the financial statements, and d. Effect on the auditor’s report

G. If an auditor reported on going concern in a prior period, presented for comparative purposes, the emphasis-of-a-matter paragraph should not be repeated.

A RealisticApproach Seminars Conference Presentation

The Auditor's Consideration of an Entity's Ability to Continue as a Going Concern

3.Requirements of SAS No. 126 H.Documentation requirements

1) The specific conditions or events that led the auditor to believe that there is substantial doubt about the entity's ability to continue as a going concern.

2) Management's plans, considered by the auditor to be particularly significant in overcoming the adverse effects of conditions or events.

3) Those audit procedures performed to evaluate the significant elements of management's plans as well as evidence obtained.

4) The auditor's conclusion as to whether substantial doubt about the entity's ability to continue as a going concern for a reasonable period of time, and

5) The auditor's conclusion as to the effects, if any, on the auditor's report.

A RealisticApproach Seminars Conference Presentation

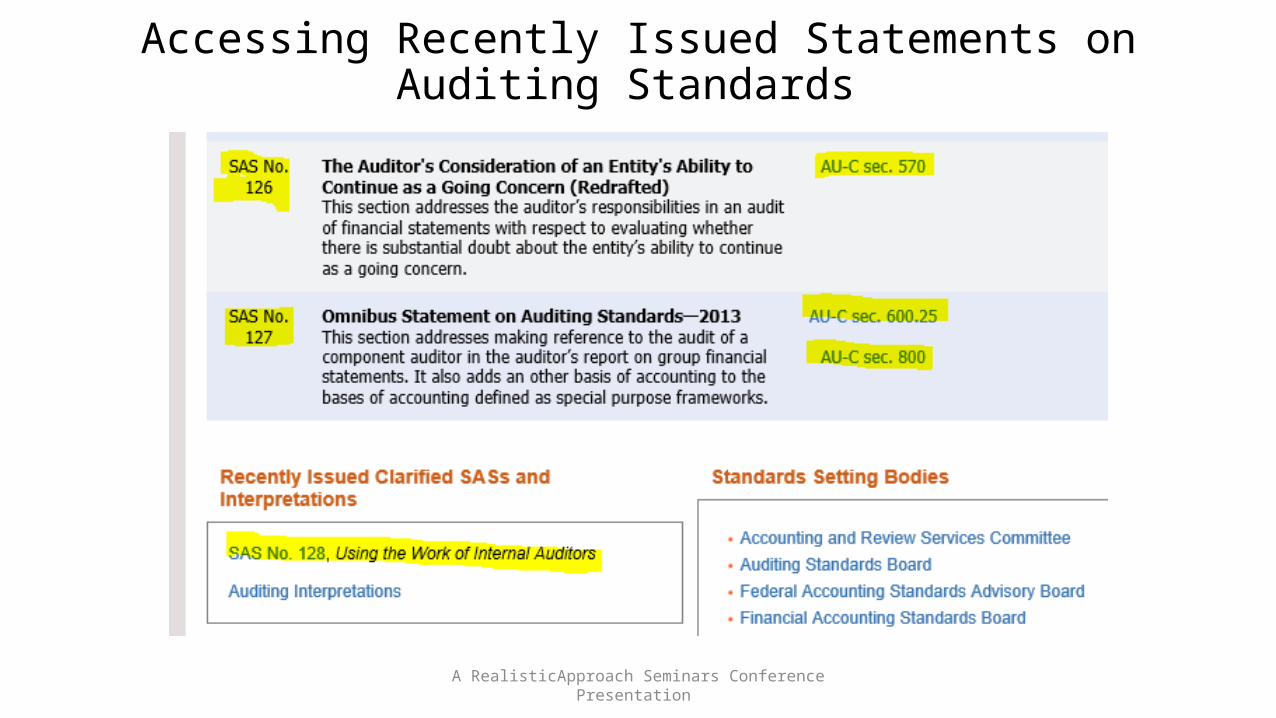

SAS No. 127 -- Omnibus

This omnibus SAS addresses two areas:

1. SAS No. 122, Statements on Auditing Standards: Clarification and Recodification, section 600, “Special Considerations—Audits of Group Financial Statements (Including the Work of Component Auditors), and

2. SAS No. 122 section 800, “Special Considerations -- Audits of Financial Statements Prepared in Accordance With Special Purpose Frameworks

A. Addresses the subject of Special Purpose Frameworks 1) Cash 2) Income tax 3) Regulatory, and 4) Contractual

B. Broadens the principles-based rule that would include frameworks (basis) that use logical, reasonable criteria. Ostensibly, meeting the criteria for being regarded as a financial reporting framework.

1) Measurement, 2) Recognition, 3) Presentation, and 4) Disclosure

3. Effective for periods ending on or after December 15, 2012.

A RealisticApproach Seminars Conference Presentation

The Document – (COSO Report)Internal Control — Integrated Framework 2013

A RealisticApproach Seminars Conference Presentation

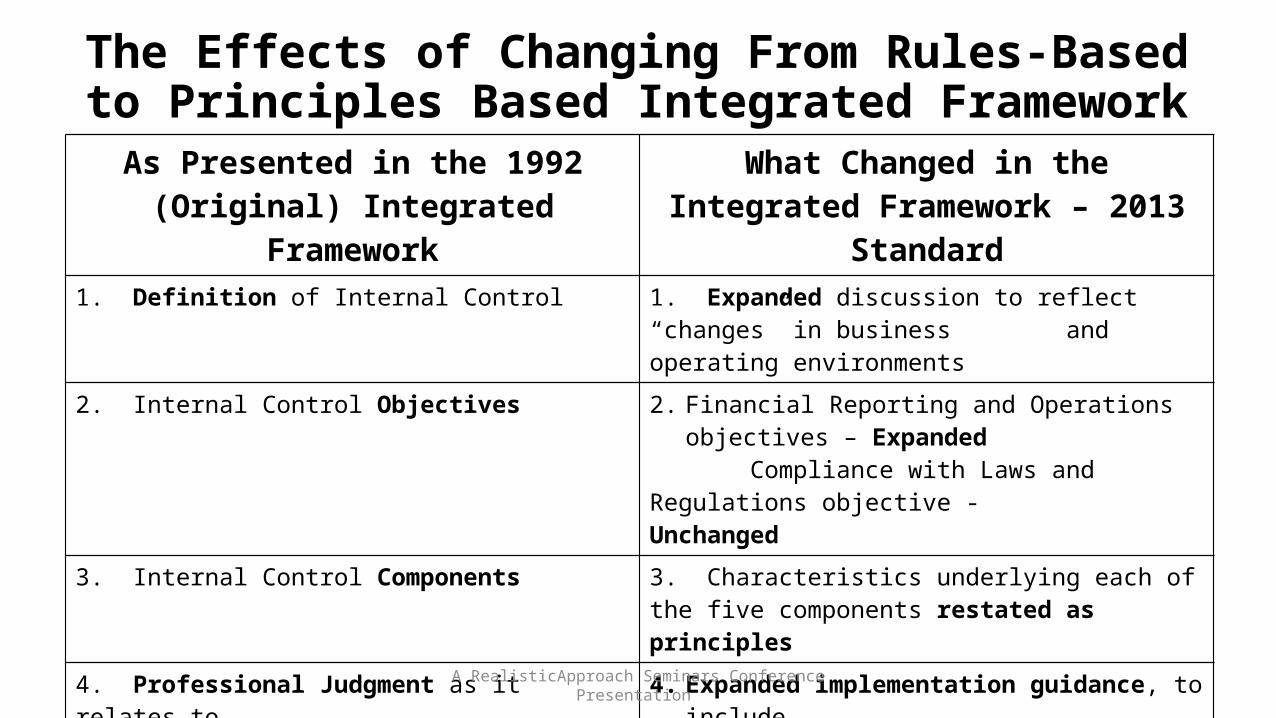

The Effects of Changing From Rules-Based to Principles Based Integrated Framework

As Presented in the 1992 (Original) Integrated Framework

What Changed in the Integrated Framework – 2013 Standard

1. Definition of Internal Control 1. Expanded discussion to reflect “changes” in business and operating environments

2. Internal Control Objectives 2. Financial Reporting and Operations objectives – Expanded

Compliance with Laws and Regulations objective - Unchanged

3. Internal Control Components 3. Characteristics underlying each of the five components restated as principles

4. Professional Judgment as it relates to A. Design B. Implementation C. Conduct, and D. Assessment of Operational Effectiveness

4. Expanded implementation guidance, to include A. Compliance with laws and regulations, and B. Non-financial reporting

A RealisticApproach Seminars Conference Presentation

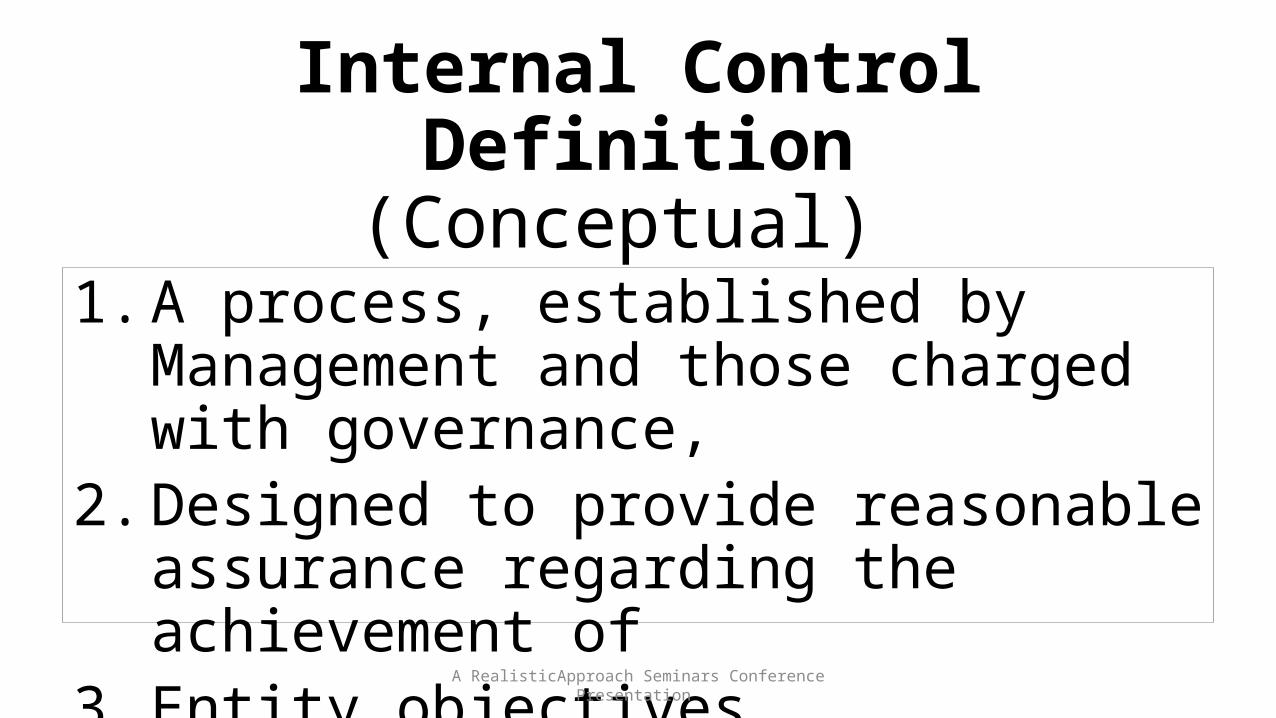

Internal Control Definition

(Conceptual) 1. A process, established by Management and

those charged with governance, 2. Designed to provide reasonable assurance

regarding the achievement of3. Entity objectives.

A RealisticApproach Seminars Conference Presentation

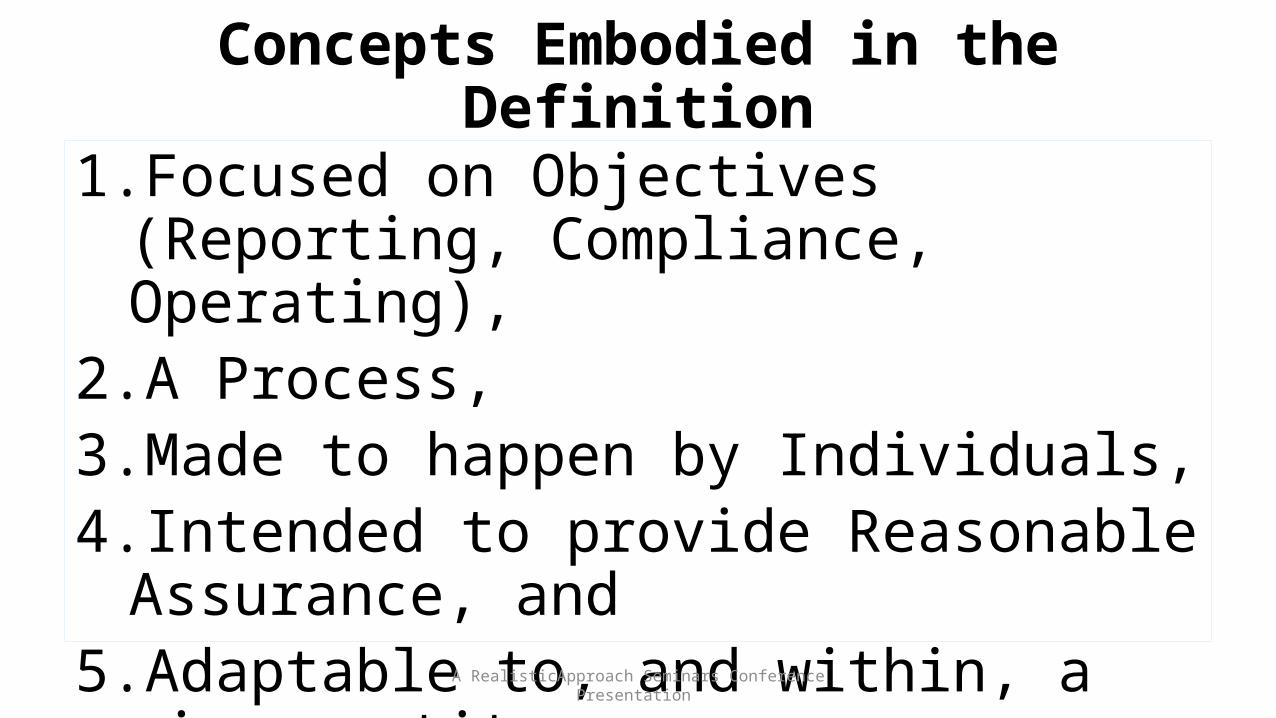

Concepts Embodied in the Definition

1. Focused on Objectives (Reporting, Compliance, Operating),

2. A Process, 3. Made to happen by Individuals, 4. Intended to provide Reasonable Assurance,

and 5. Adaptable to, and within, a given entity.

A RealisticApproach Seminars Conference Presentation

Internal Control Definition

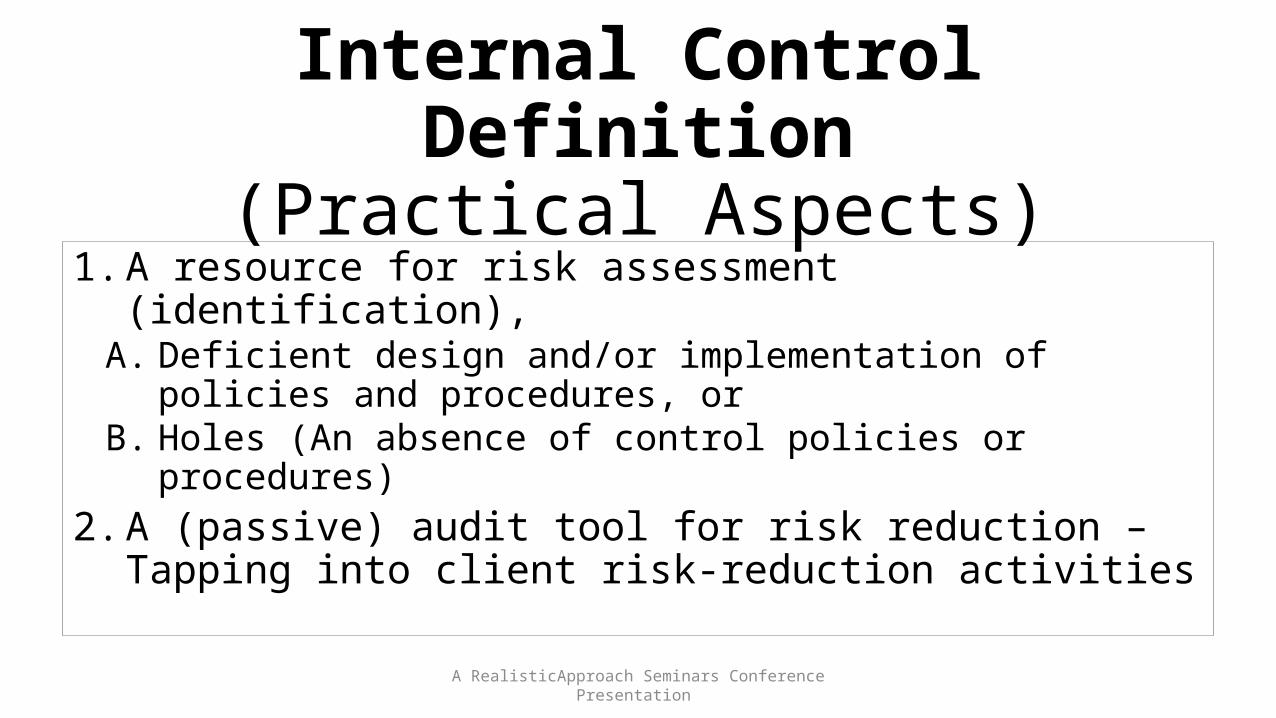

(Practical Aspects) 1. A resource for risk assessment (identification),

A. Deficient design and/or implementation of policies and procedures, or

B. Holes (An absence of control policies or procedures)2. A (passive) audit tool for risk reduction – Tapping

into client risk-reduction activities

A RealisticApproach Seminars Conference Presentation

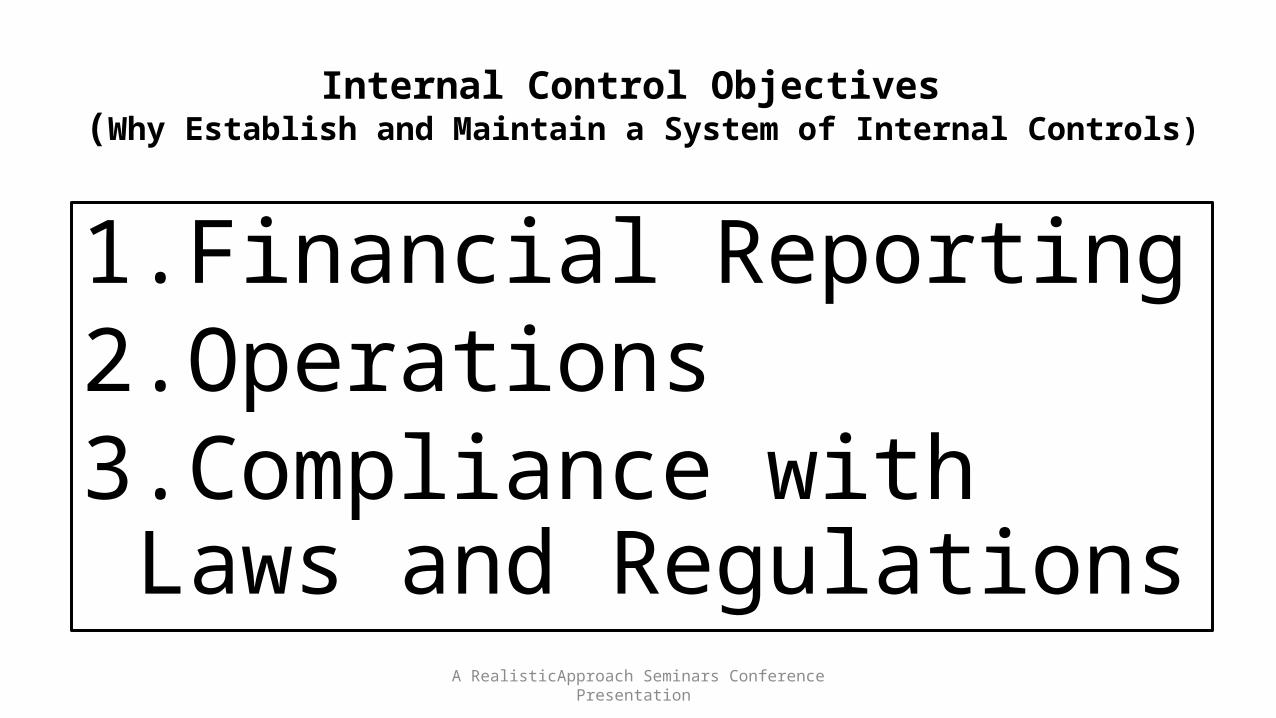

Internal Control Objectives (Why Establish and Maintain a System of Internal Controls)

1.Financial Reporting2.Operations3.Compliance with Laws and

Regulations A RealisticApproach Seminars Conference Presentation

Control Environment

Risk Assessment

Control Activities

Information & Communication

Monitoring Activities

Updated Integrated Framework Articulates 17 Principles of Effective Internal Control, by

Component

1.Demonstrates commitment to integrity and ethical values2.Exercises oversight responsibility3.Establishes structure, authority and responsibility4.Demonstrates commitment to competence5.Enforces accountability

6.Specifies suitable objectives7.Identifies and analyzes risk8.Assesses fraud risk9.Identifies and analyzes significant change

10.Selects and develops control activities11. Selects and develops general controls over technology12.Deploys through policies and procedures

13.Uses relevant information14.Communicates internally15.Communicates externally

16.Conducts ongoing and/or separate evaluations17.Evaluates and communicates deficiencies

Internal Control Components Principles of Effective Control

Internal Control Components

1. Control Environment Principles1. Commitment to integrity and ethical values,2. Performance of Oversight Responsibility,3. Establishment of organizational structure, authority,

and responsibility, 4. Organizational commitment to competence,5. Enforcement of accountability.

A RealisticApproach Seminars Conference Presentation

Internal Control Component – Control Environment

Associated Risk From Absence or Deficiency

A RealisticApproach Seminars Conference Presentation

1.Demonstrates commitment to integrity and ethical values

2.Exercises oversight responsibility

3.Establishes structure, authority and responsibility

4.Demonstrates commitment to competence

5.Enforces accountability

1.Permissive Atmosphere 2.Basis for Rationalization

3.Nobody’s looking – anything goes

4.No central source of answers to questions, 5.Incompatible functions “assumed” by individuals

6. Fosters a “compliance” mentality – What’s the least I have to do? 7. Potential for deficient monitoring and review 8. Possible lack of knowledge of current professional/legal requirements

9. Attitude of no-price to be paid for non-compliance with policies/procedures 10. Uncorrected deficiencies present the potential for blind-siding risk.

Principles of Effective Control

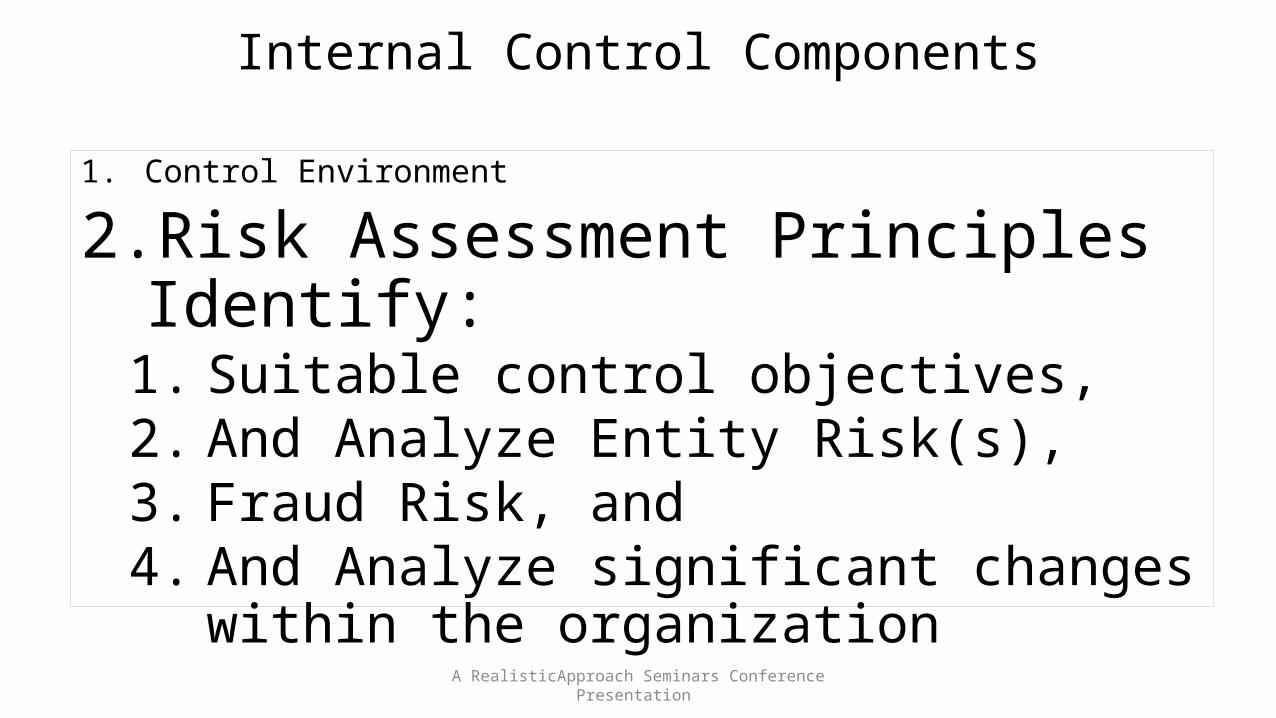

Internal Control Components

1. Control Environment

2. Risk Assessment Principles Identify:1. Suitable control objectives, 2. And Analyze Entity Risk(s), 3. Fraud Risk, and 4. And Analyze significant changes within the

organization

A RealisticApproach Seminars Conference Presentation

Internal Control Component – Risk Assessment

Associated Risk From Absence or Deficiency

A RealisticApproach Seminars Conference Presentation

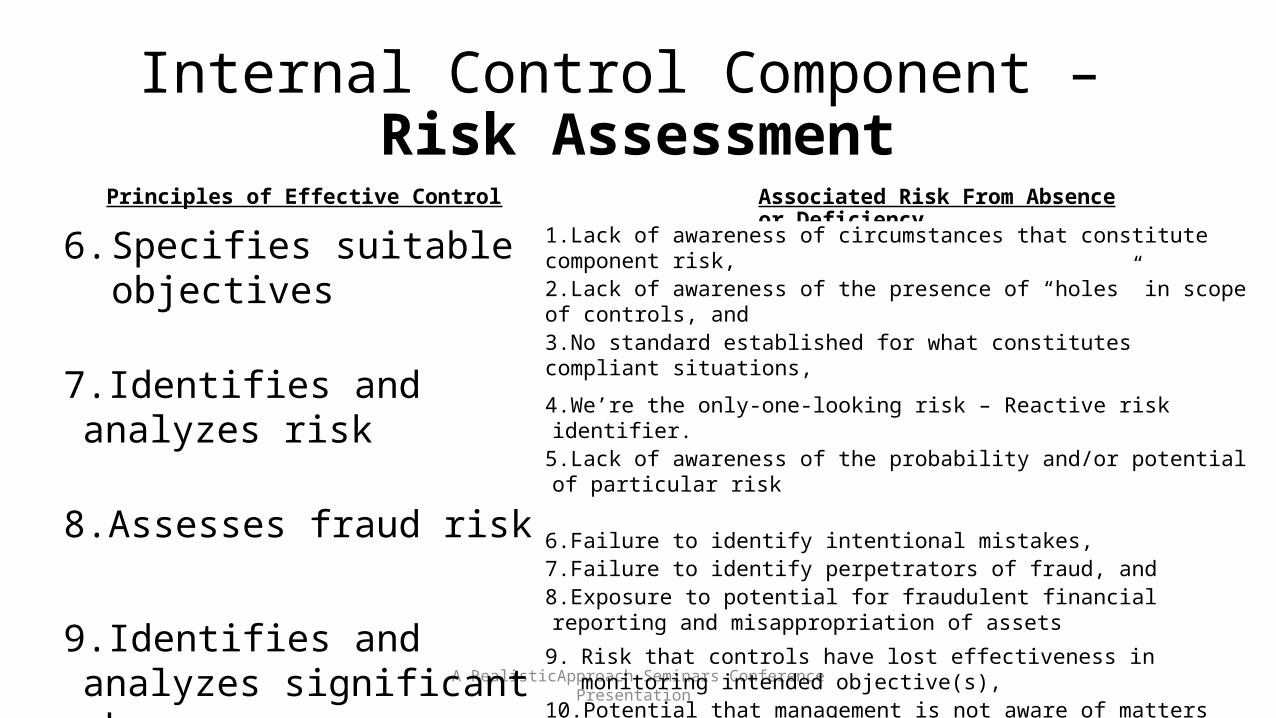

6. Specifies suitable objectives

7.Identifies and analyzes risk

8.Assesses fraud risk

9.Identifies and analyzes significant change

1.Lack of awareness of circumstances that constitute component risk, 2.Lack of awareness of the presence of “holes” in scope of controls, and3.No standard established for what constitutes compliant situations,

4.We’re the only-one-looking risk – Reactive risk identifier.5.Lack of awareness of the probability and/or potential of particular risk

6.Failure to identify intentional mistakes, 7.Failure to identify perpetrators of fraud, and 8.Exposure to potential for fraudulent financial reporting and misappropriation of assets

9. Risk that controls have lost effectiveness in monitoring intended objective(s), 10. Potential that management is not aware of matters that could indicate an

evolving deficiency, 11. Reactive attitude toward risk identification (only-one-looking risk).

Principles of Effective Control

Internal Control Components1. Control Environment2. Risk Assessment

3. Control Activities – Principles1. Select and Develop control activities

(Policies and/or Procedures) 2. Select and Develop General Controls over

Technology, and 3. Deploy Selected Control Activities

A RealisticApproach Seminars Conference Presentation

Internal Control Component – Control Activities

Associated Risk From Absence or Deficiency

A RealisticApproach Seminars Conference Presentation

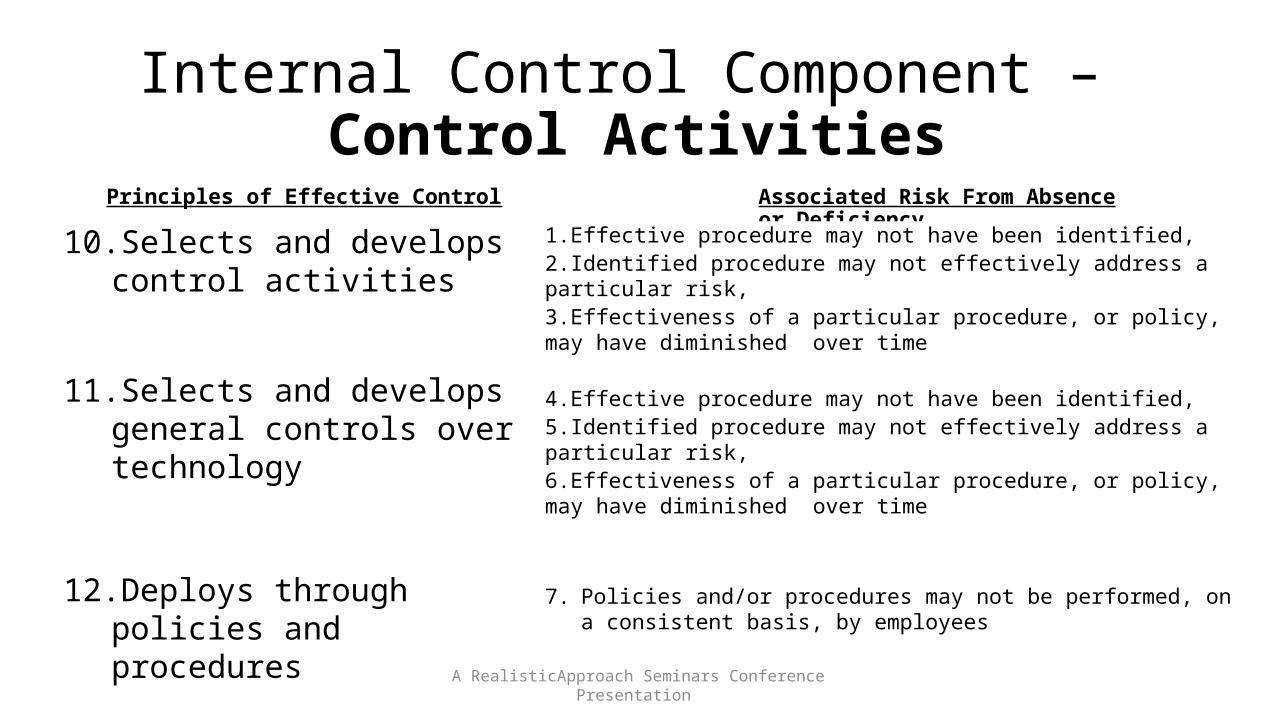

10. Selects and develops control activities

11. Selects and develops general controls over technology

12. Deploys through policies and procedures

1.Effective procedure may not have been identified, 2.Identified procedure may not effectively address a particular risk, 3.Effectiveness of a particular procedure, or policy, may have diminished over time

4.Effective procedure may not have been identified, 5.Identified procedure may not effectively address a particular risk, 6.Effectiveness of a particular procedure, or policy, may have diminished over time

7. Policies and/or procedures may not be performed, on a consistent basis, by employees

Principles of Effective Control

Internal Control Components

1. Control Environment2. Risk Assessment

3. Control Activities are Client Policies and/or Procedures that Establish and/or Monitor

1. Checks and/or Edits 2. Authorization 3. Segregation of Duties 4. Restrictions regarding Access to Assets and Accounting Records5. A Document Trail

A RealisticApproach Seminars Conference Presentation

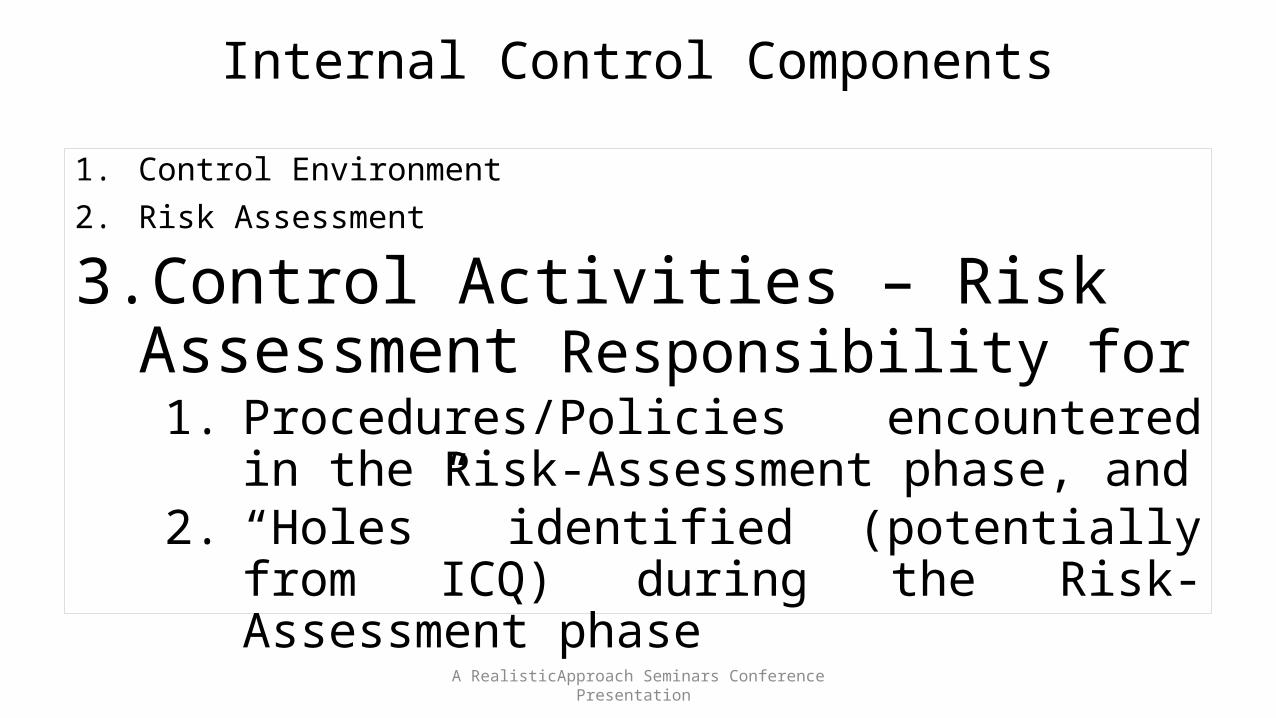

Internal Control Components

1. Control Environment2. Risk Assessment

3. Control Activities – Risk Assessment Responsibility for

1. Procedures/Policies encountered in the Risk-Assessment phase, and

2. “Holes” identified (potentially from ICQ) during the Risk-Assessment phase

A RealisticApproach Seminars Conference Presentation

Internal Control Components

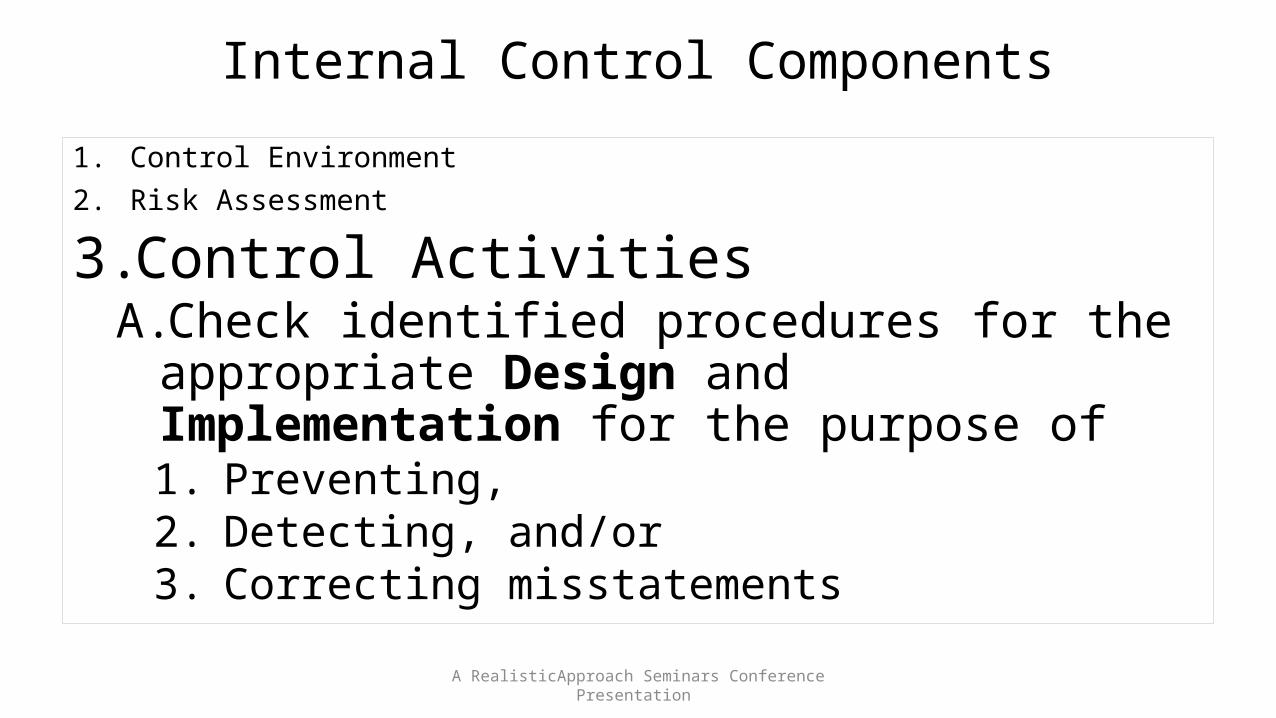

1. Control Environment2. Risk Assessment

3. Control Activities A.Check identified procedures for the appropriate

Design and Implementation for the purpose of1. Preventing, 2. Detecting, and/or3. Correcting misstatements

A RealisticApproach Seminars Conference Presentation

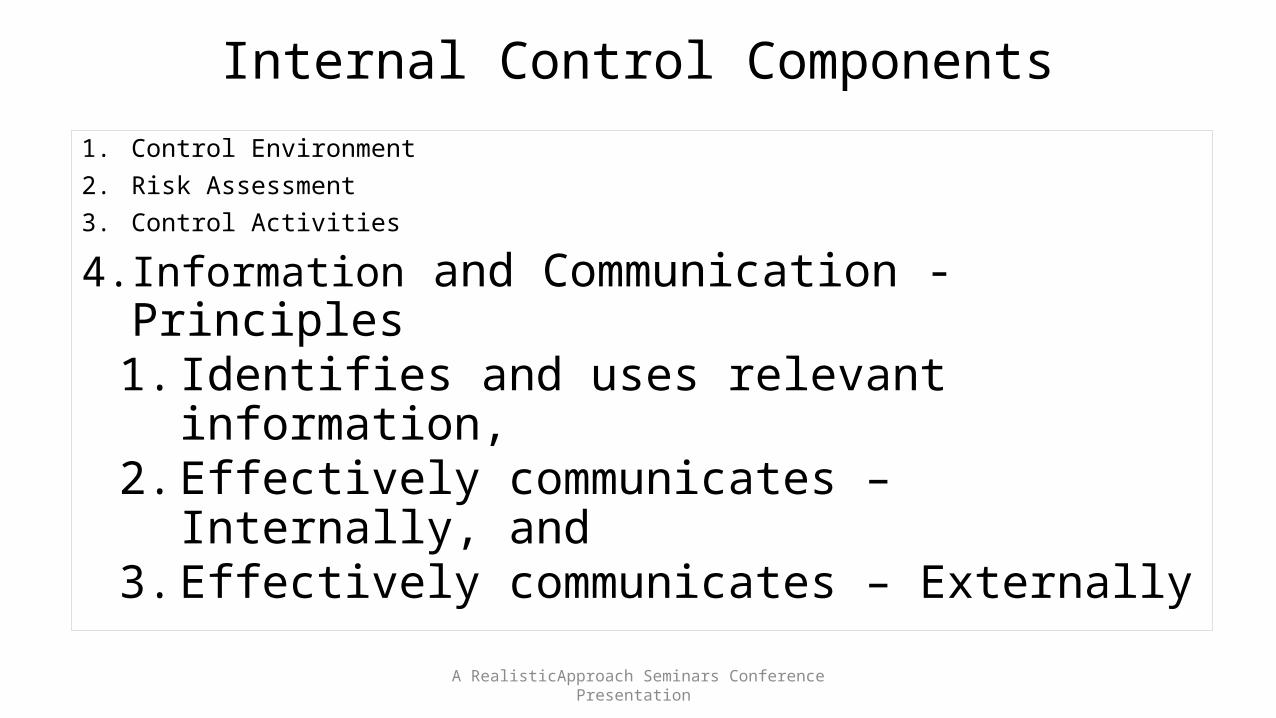

Internal Control Components

1. Control Environment2. Risk Assessment3. Control Activities

4. Information and Communication - Principles 1. Identifies and uses relevant information, 2. Effectively communicates – Internally, and 3. Effectively communicates – Externally

A RealisticApproach Seminars Conference Presentation

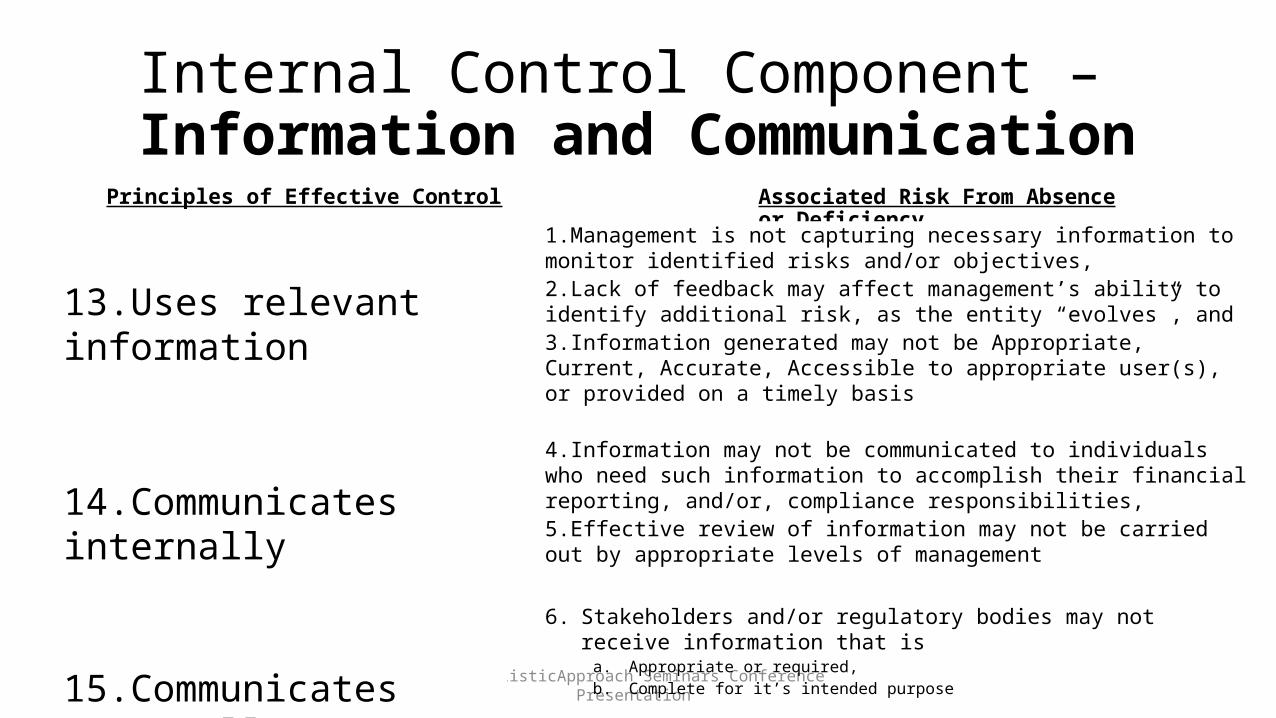

Internal Control Component – Information and Communication

Associated Risk From Absence or Deficiency

A RealisticApproach Seminars Conference Presentation

1.Management is not capturing necessary information to monitor identified risks and/or objectives,2.Lack of feedback may affect management’s ability to identify additional risk, as the entity “evolves”, and 3.Information generated may not be Appropriate, Current, Accurate, Accessible to appropriate user(s), or provided on a timely basis

4.Information may not be communicated to individuals who need such information to accomplish their financial reporting, and/or, compliance responsibilities, 5.Effective review of information may not be carried out by appropriate levels of management

6. Stakeholders and/or regulatory bodies may not receive information that is a. Appropriate or required, b. Complete for it’s intended purpose

Principles of Effective Control

13.Uses relevant information

14.Communicates internally

15.Communicates externally

Internal Control Components1. Control Environment2. Risk Assessment3. Control Activities

4. Information and Communication addresses Risk as it relates to

1. Significant classes of transactions 2. How transactions are initiated, authorized, recorded,

processed and reported 3. Accounting records reflecting transactions4. Information system processing5. Reporting process to include estimation

A RealisticApproach Seminars Conference Presentation

Internal Control Components

1. Information and Communication addresses Risk as it relates to

Procedures to prepare financial statements 1. How summarized totals migrate to general ledger (G/L)2. Initiation, authorization, recording, and processing of journal

entries to G/L 3. Summarization of G/L amounts, and 4. Preparation of financial statements

A RealisticApproach Seminars Conference Presentation

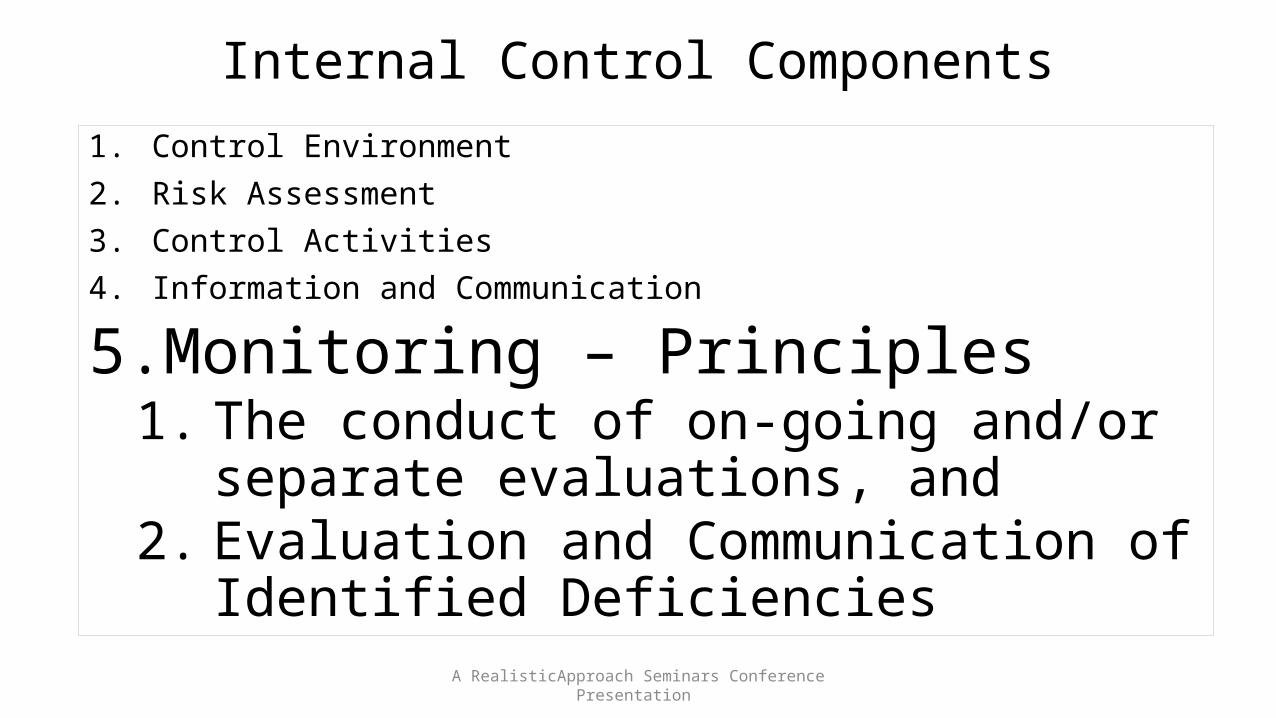

Internal Control Components

1. Control Environment2. Risk Assessment3. Control Activities4. Information and Communication

5. Monitoring – Principles 1. The conduct of on-going and/or separate

evaluations, and 2. Evaluation and Communication of Identified

DeficienciesA RealisticApproach Seminars Conference Presentation

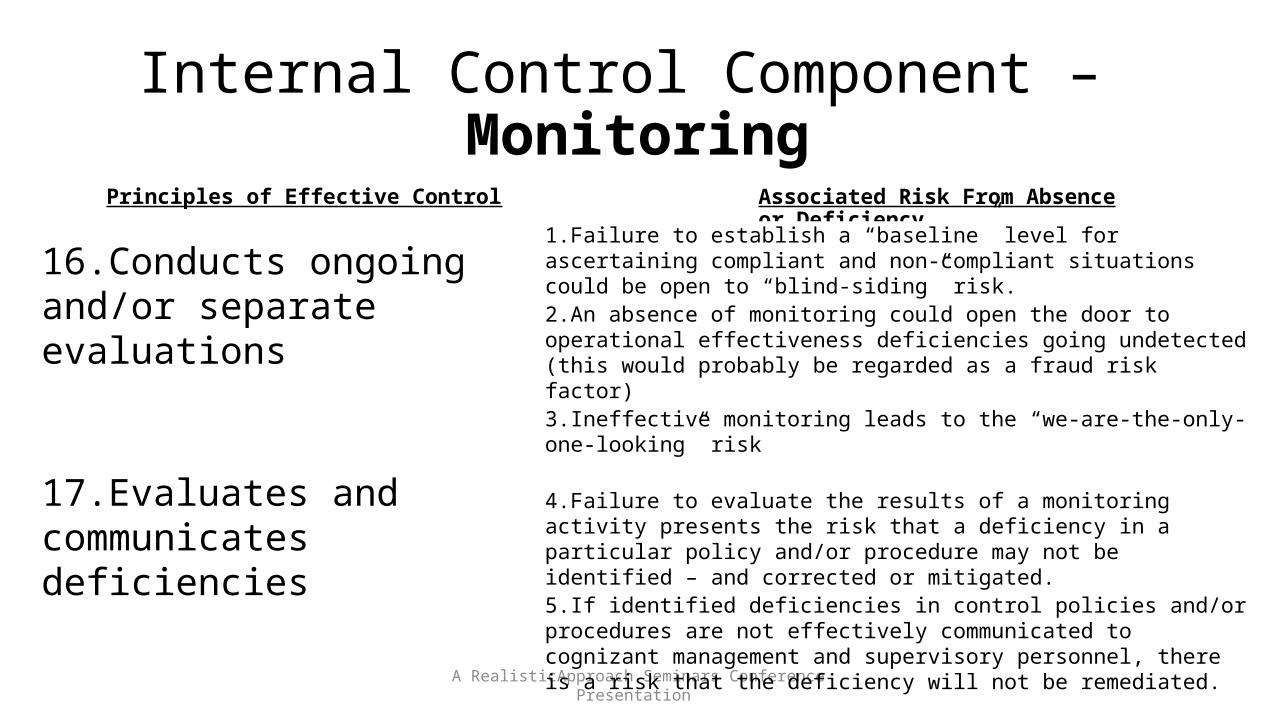

Internal Control Component – Monitoring

Associated Risk From Absence or Deficiency

A RealisticApproach Seminars Conference Presentation

1.Failure to establish a “baseline” level for ascertaining compliant and non-compliant situations could be open to “blind-siding” risk.2.An absence of monitoring could open the door to operational effectiveness deficiencies going undetected (this would probably be regarded as a fraud risk factor) 3.Ineffective monitoring leads to the “we-are-the-only-one-looking” risk

4.Failure to evaluate the results of a monitoring activity presents the risk that a deficiency in a particular policy and/or procedure may not be identified – and corrected or mitigated. 5.If identified deficiencies in control policies and/or procedures are not effectively communicated to cognizant management and supervisory personnel, there is a risk that the deficiency will not be remediated.

Principles of Effective Control

16.Conducts ongoing and/or separate evaluations

17.Evaluates and communicates deficiencies

Essential Elements of an Effective System of Internal Control

Effective internal control provides reasonable assurance regarding the achievement of objectives and requires that:1. The five components operate together -- in an integrated manner 2. Each component and each relevant principle is present and functioning, when

A. Each principle is suitable to all entities; B. All principles are presumed relevant except in rare situations where management

determines that a principle is not relevant to a componentC. Components operate together if

1) All components are present and functioning and 2) Internal control deficiencies aggregated across components do not result in one

or more major deficiencies3. A major internal control deficiency represents an internal control deficiency, or

combination of deficiencies, that severely reduces the likelihood that an entity can achieve its objectives

A RealisticApproach Seminars Conference Presentation

Transitioning to the 2013 Integrated Framework

1. Reporting Entities (and third-party Accountants) are encouraged to transition to the updated Framework as soon as feasible,

2. The 2013 Integrated Framework will supersede original Framework at the end of the transition period (i.e., December 15, 2014) A. During the transition period, external reporting of internal control

related matters should disclose whether the original or updated version of the Framework was used

B. Impact of adopting the updated Framework will vary by organization

A RealisticApproach Seminars Conference Presentation