Embed Size (px)

Citation preview

ANNUAL ACCOUNTING & BUSINESS CONFERENCE

An independent member of UHY International

OPENING COMMENTARY

Scott MillerPartnerUHY LLP

Welcome to our ninth annual Accounting & Business Conference!

ATTENDEE CHECKLIST

CPE materials

Feedback• Tear out form in back of attendee booklet

Questions

Keep a look out for a post-event email• Download a copy of the PowerPoint presentation

Pre-register for 2017

ABOUT OUR FIRM

LOCAL

• Nearly 50 years of experience

• Ranked 5th largest accounting firm in Southeast Michigan by Crain's Detroit Business

• Over 330 employees in Detroit, Farmington Hills and Sterling Heights

• Largest accounting firm presence in Macomb County

NATIONAL

• Named one of IPA’s Top 10 Fastest Growing Accounting Firms of 2016

• 14 offices across the US

• PCAOB registered

• Most recent peer review resulted in a Pass opinion, the highest possible result

INTERNATIONAL

• Member firms in 320 business centers across 92 countries

• Over 7,600 professionals

• 16th largest international accounting and consultancy network

• Member of the Forum of Firms

US LOCATIONS

GLOBAL NETWORKAMERICAS

Argentina

Bahamas

Brazil

Canada

Chile

Colombia

Costa Rica

Dominican Republic

Ecuador

Honduras

Jamaica

Guatemala

Mexico

Panama

Peru

Puerto Rico

United States

Uruguay

Venezuela

ASIA-PACIFIC

Australia

Bangladesh

China (incl. Hong Kong)

India

Indonesia

Japan

Kazakhstan

Korea (Rep. of)

Malaysia

New Zealand

Pakistan

Philippines

Qatar

Saudi Arabia

Singapore

Taiwan

Thailand

Uzbekistan

Vietnam

EUROPE

Albania

Austria

Belarus

Belgium

Bulgaria

Czech Republic

Croatia

Cyprus

Denmark

Finland

France

Georgia

Germany

Greece

Guernsey

Hungary

Ireland

Isle of Man

Italy

Luxembourg

Malta

Montenegro

Netherlands

Norway

Poland

Portugal

Romania

Russian Federation

Serbia

Slovakia

Slovenia

Spain

Sweden

Switzerland

Turkey

Ukraine

United Kingdom

MIDDLE EAST & AFRICA

Angola

Azerbaijan

Egypt

Ghana

Israel

Jordan

Kenya

Republic of Kuwait

Lebanon

Mauritius

Morocco

Nigeria

South Africa

Tunisia

UAE

Uganda

Zambia

SELECT SERVICE OFFERINGS

AUDIT & ASSURANCE

• Audits, reviews and compilations of financial statements

• Audits of financial statements of employee benefit plans and pensions

• Financial forecasts and projections

• Attestation services including agreed-upon procedures reports and service auditor reports (SSAE 16)

• Financial reporting assistance

• Due diligence

• Audit committee advice

TAX PLANNING & COMPLIANCE

• Federal income tax planning and compliance

• Business formation and entity structuring

• State and local taxes and incentives

• Unclaimed property

• Executive tax and financial planning

• International tax compliance

• Transfer pricing

• Research and development credits

• Cost segregation

• Estate and succession planning

ADVISORY

• Internal audit, risk and compliance services

• Management and technology consulting

• Transaction services

• Resource solutions

• Employee benefits consulting

FORENSIC, LITIGATION & VALUATION

• Commercial litigation and financial damage analysis

• Expert witness testimony

• Business valuation

• Financial fraud examinations and investigations

• Business insurance claims measurement and consulting

• Accountant malpractice claims

• Family law and divorce consulting

TODAY’S SCHEDULE OF EVENTS

8:45AM–9:45AM Survival of the fittest:Sustainability through OPMS™Cindy Hannafey, UHY Advisors

9:45AM–10:00AM Break

10:00AM–12:00PM SEC accounting and legal update Marc Lichtman, UHY LLPCarrie Leahy, Bodman PLC

12:00PM–1:00PM Lunch

1:00PM–2:00PM 831(b) micro captives panel discussion Scott Miller, UHY LLPKevin Bates, Cambridge Consulting GroupRandy O’Brien, Corporate & Endowment Solutions, Inc. Jeremy Huish, Artex Risk Solutions, Inc.

2:00PM–2:15PM Break

2:15PM–3:15PM Tax update Pat Gregory, UHY LLP

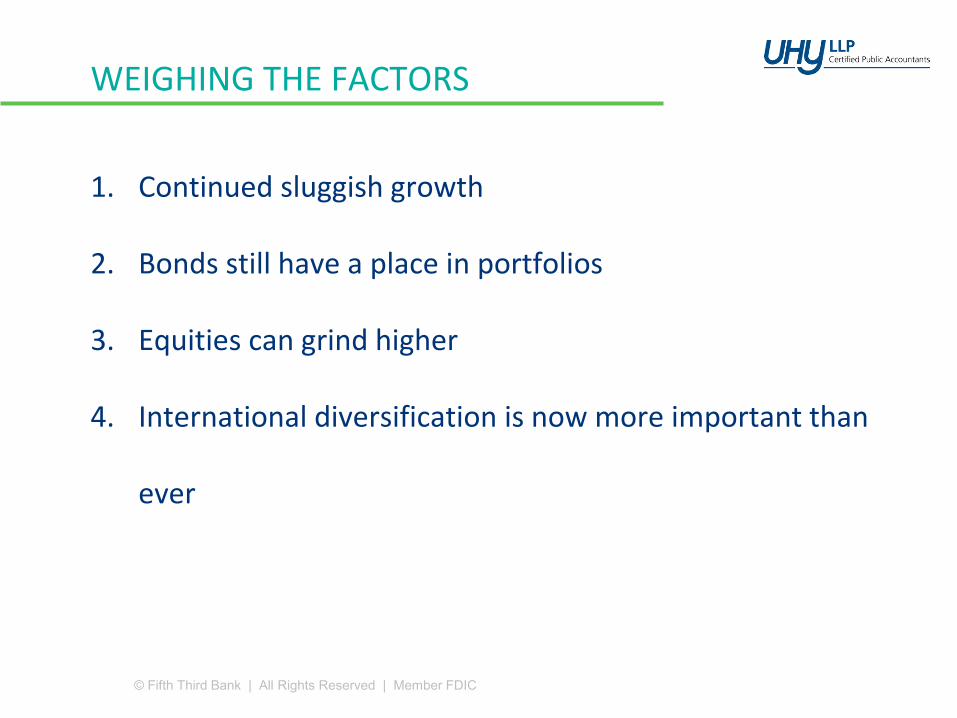

3:15PM–4:15PM US economic and market outlook: Bulls and bears and swans! Oh my! Greg Curvall, Fifth Third Bank

4:15PM–6:00PM Cocktail reception

SURVIVAL OF THE FITTESTSUSTAINABILITY THROUGH OPMS™

Cindy HannafeyPrincipalUHY Advisors

CORPORATE LANDSCAPE

• Uncertainty is prevalent after elections, regardless of party affiliations

• Presidential election cycles correlate with stock market returns

• New policies, procedures and laws

• The stock market has, for the most part, ebbed and flowed with the four-year election cycle for the past 182 years

“Survival of the Fittest”

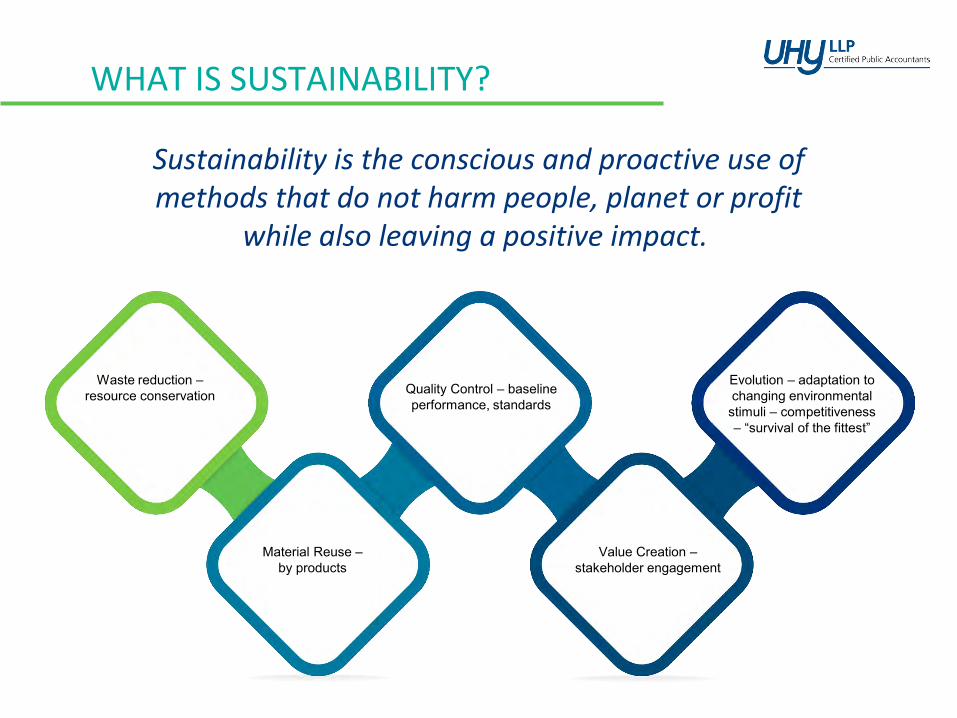

WHAT IS SUSTAINABILITY?

Sustainability is the conscious and proactive use of methods that do not harm people, planet or profit

while also leaving a positive impact.

Evolution – adaptation to changing environmental stimuli – competitiveness – “survival of the fittest”

Waste reduction –resource conservation

Material Reuse –by products

Quality Control – baseline performance, standards

Value Creation –stakeholder engagement

SUSTAINABILITY – VIDEO

THE VICIOUS PROCESS CYCLE

EmployeesEmployees

desire to do a good job!

ComplexityIncreased complexity leads employees to

create “work-arounds”

Sub-Optimal ProcessesWork-arounds lead

to sub-optimal processes and

reduce the focus on the customer

Normal Routines

Over time, these sub-optimal processes

become “normal” and lead to the dreaded

statement:

“This is the way we’ve always

done it!”

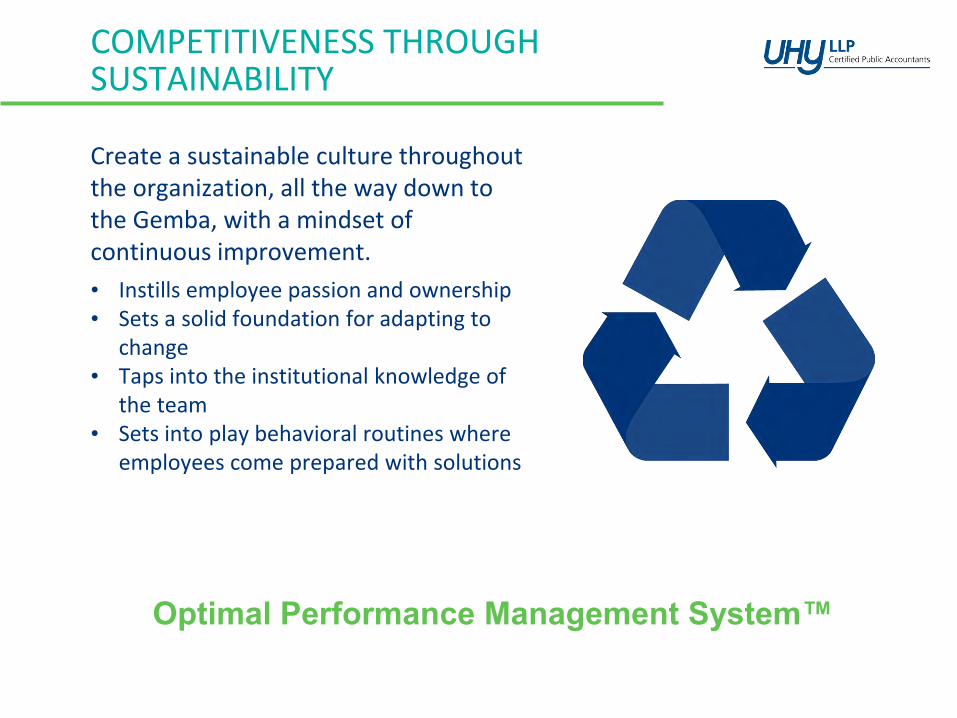

COMPETITIVENESS THROUGH SUSTAINABILITY

Create a sustainable culture throughout the organization, all the way down to the Gemba, with a mindset of continuous improvement.

• Instills employee passion and ownership• Sets a solid foundation for adapting to

change• Taps into the institutional knowledge of

the team• Sets into play behavioral routines where

employees come prepared with solutions

Optimal Performance Management System™

OPTIMAL PERFORMANCE MANAGEMENT SYSTEM™

Top Five Steps to Build OPMS™ for Your Organization

Competitive Landscape

Corporate Strategy

Optimal Performance Management

System

STEP ONE

Measure

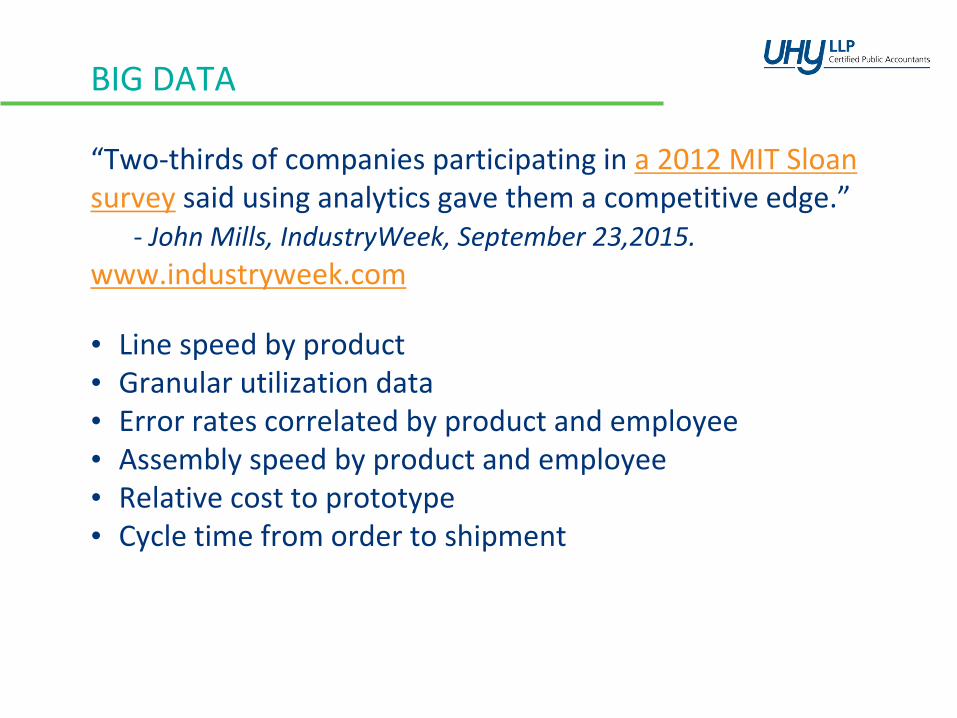

BIG DATA

“Two-thirds of companies participating in a 2012 MIT Sloan survey said using analytics gave them a competitive edge.”

- John Mills, IndustryWeek, September 23,2015.

www.industryweek.com

• Line speed by product• Granular utilization data• Error rates correlated by product and employee• Assembly speed by product and employee• Relative cost to prototype• Cycle time from order to shipment

STEP TWO

Measure Empower

Corporate Strategy

Competitive Landscape

Optimal Performance Management

System

EMPOWER – VIDEO

EMPOWER

Culture of Empowerment

Focus on Operations

Data for actual use, not simply

for records

Agreement on what is important

Employees own the data

Employee process

ownershipCustomer

first

STEP THREE

Measure Empower

Publish

Corporate Strategy

Competitive Landscape

Optimal Performance Management

System

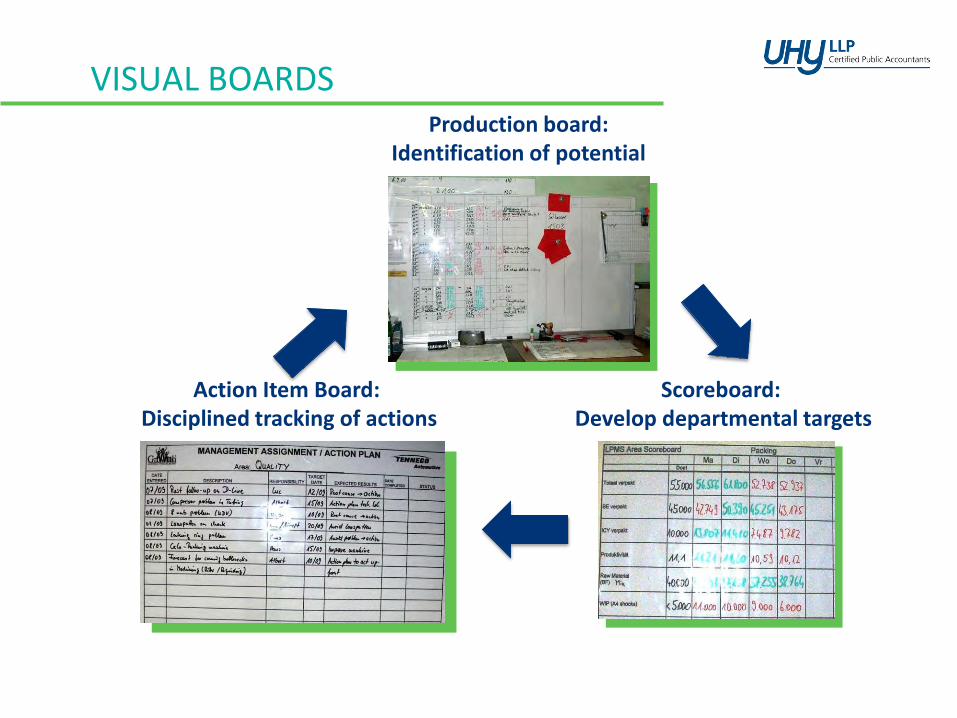

VISUAL BOARDS

Action Item Board: Disciplined tracking of actions

Production board: Identification of potential

Scoreboard: Develop departmental targets

Measure Empower

Publish

STEP FOUR

Communicate

Corporate Strategy

Competitive Landscape

Optimal Performance Management

System

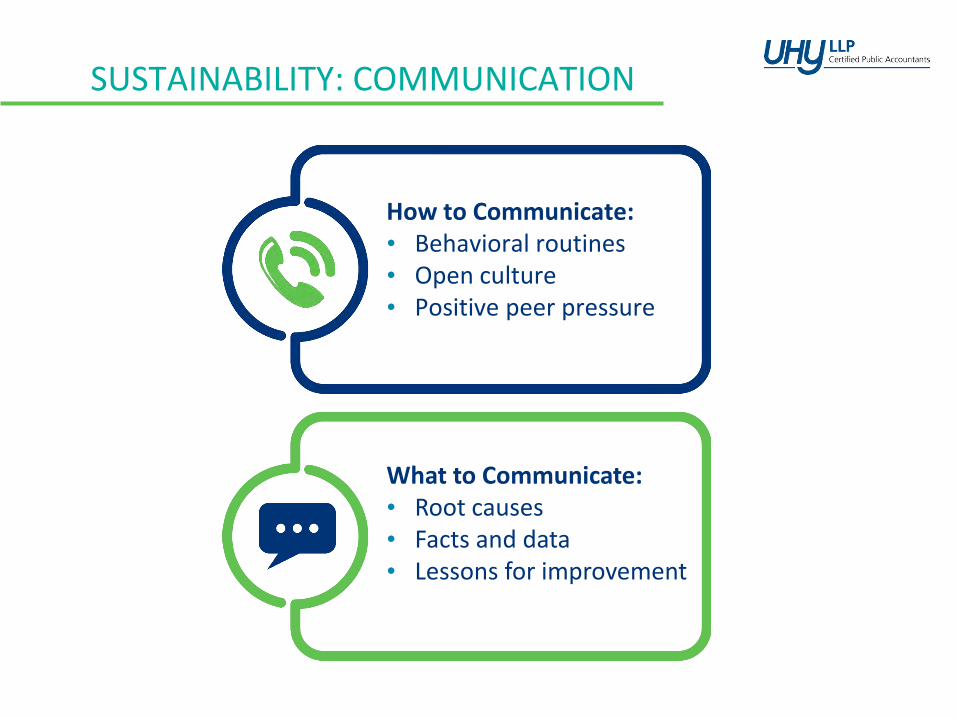

SUSTAINABILITY: COMMUNICATION

How to Communicate:• Behavioral routines• Open culture• Positive peer pressure

What to Communicate:• Root causes• Facts and data• Lessons for improvement

STEP FIVE

Measure Empower

Publish

Communicate

Celebrate

Corporate Strategy

Competitive Landscape

Optimal Performance Management

System

SUSTAINABILITY: CELEBRATION

Employee Appreciation

“Magic Wand”Empowerment

and Peer Recognition

“Go Forth”

NEXT STEPS

• Optimal Performance Management System empowers employees and fosters a culture where employees think like owners

• When employees think like owners, productivity improves, waste declines, and complexity is kept to a minimum via continuous monitoring

• These improvements are noticeable and contribute significantly to the bottom line

• When incorporated into business strategy, the employees themselves become a competitive advantage in the marketplace

REFRESHMENT BREAK

We will reconvene in fifteen minutes

ACCOUNTING STANDARDS UPDATE

Marc LichtmanPartnerUHY LLP

ACCOUNTING STANDARDS UPDATES

ACCOUNTING STANDARDS UPDATES

ASU 2014-15 – Presentation of Financial Statements—Going Concern (Topic 205-40)

• Under U.S. GAAP, financial statements are prepared under the presumption that the entity will continue to operate as a going concern.

• Currently, GAAP lacks guidance about management’s responsibility to evaluate the going concern assumption or provide disclosures.

• This ASU is intended to define management’s responsibility to evaluate whether there is substantial doubt about an entity’s ability to continue as a going concern and to provide related disclosures.

ACCOUNTING STANDARDS UPDATES

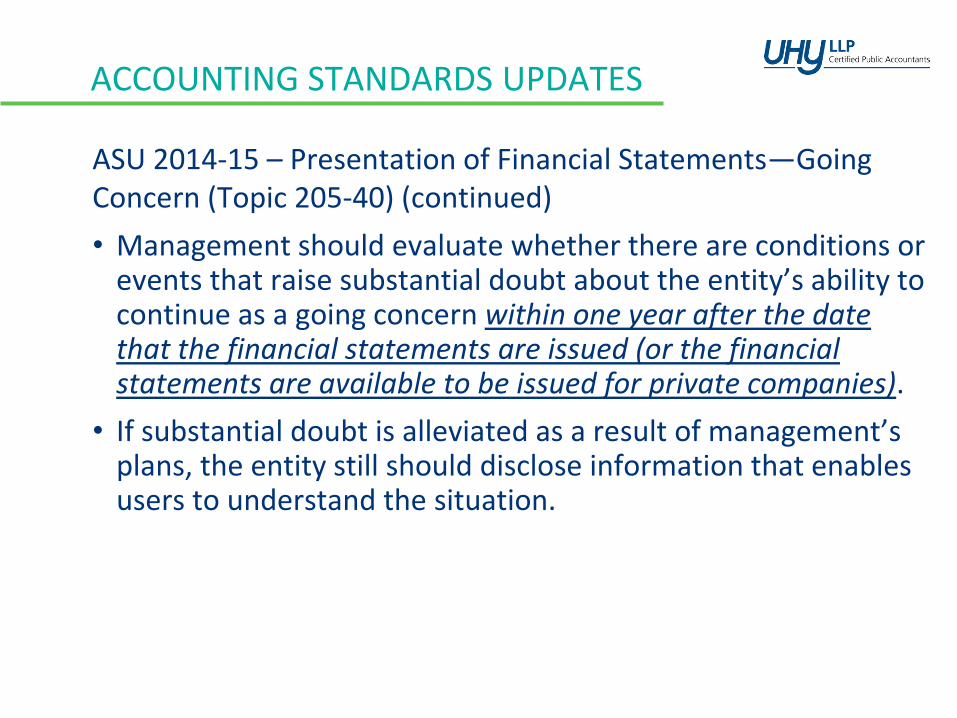

ASU 2014-15 – Presentation of Financial Statements—Going Concern (Topic 205-40) (continued)

• Management should evaluate whether there are conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern within one year after the date that the financial statements are issued (or the financial statements are available to be issued for private companies).

• If substantial doubt is alleviated as a result of management’s plans, the entity still should disclose information that enables users to understand the situation.

ACCOUNTING STANDARDS UPDATES

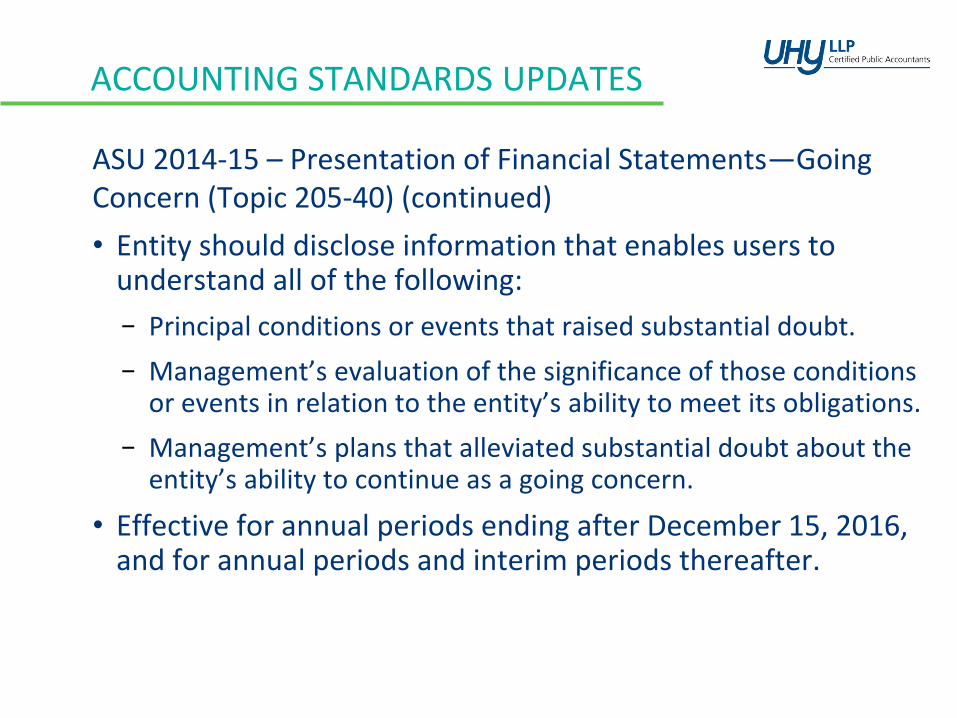

ASU 2014-15 – Presentation of Financial Statements—Going Concern (Topic 205-40) (continued)

• Entity should disclose information that enables users to understand all of the following:

− Principal conditions or events that raised substantial doubt.

− Management’s evaluation of the significance of those conditions or events in relation to the entity’s ability to meet its obligations.

− Management’s plans that alleviated substantial doubt about the entity’s ability to continue as a going concern.

• Effective for annual periods ending after December 15, 2016, and for annual periods and interim periods thereafter.

ACCOUNTING STANDARDS UPDATES

• Requires that debt issuance costs related to recognized debt be presented in the balance sheet as a direct deduction from the carrying amount of that debt, consistent with debt discounts.

• When debt issuance costs relate to a line-of-credit agreement, the issuance costs related to lines of credit may be presented as a deferred charge.

ASU 2015-03 – Interest (Subtopic 835-30)

ACCOUNTING STANDARDS UPDATES

• For public entities, effective for fiscal years beginning after December 15, 2015, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2015, and interim periods within fiscal years beginning after December 15, 2016.

• An entity should apply the new guidance on a retrospective basis.

• Upon transition an entity is required to comply with the applicable disclosures for a change in an accounting principle.

ASU 2015-03 – Interest (Subtopic 835-30) (continued)

ACCOUNTING STANDARDS UPDATES

• Requires that deferred tax liabilities and assets be classified as noncurrent in the balance sheet.

• The current requirement that deferred tax liabilities and assets of a tax-paying component of an entity be offset and presented as a single amount is not affected by this ASU.

• Upon transition an entity is required to comply with the applicable disclosures for a change in an accounting principle.

ASU 2015-17 – Income Taxes (Topic 740) – Balance Sheet Classification of Deferred Taxes

ACCOUNTING STANDARDS UPDATES

• For public entities, effective for annual periods beginning after December 15, 2016, and interim periods within those years.

• For all other entities, effective for annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018.

• Earlier application is permitted for all entities as of the beginning of an interim or annual reporting period.

• May be applied either prospectively to all deferred tax liabilities and assets or retrospectively to all periods presented.

ASU 2015-17 – Income Taxes (Topic 740) – Balance Sheet Classification of Deferred Taxes (continued)

ACCOUNTING STANDARDS UPDATES

• Intended to improve the recognition, measurement and disclosure of financial instruments.

• Requires equity investments (except those under the equity method of accounting) to be measured at fair value with changes in fair value recognized in net income.

• Eliminates the requirement to disclose the fair value of financial instruments measured at amortized cost for entities that are not public entities.

• Eliminates the requirement for public entities to disclose the method and assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost.

ASU 2016-01: Financial Instruments—Overall (Subtopic 825-10)

ACCOUNTING STANDARDS UPDATES

• Requires public entities to use the exit price notion when measuring the fair value of financial instruments for disclosure.

• Requires separate presentation of financial assets and financial liabilities by measurement category and form of financial asset (i.e., securities or loans and receivables) on the balance sheet or accompanying notes.

ASU 2016-01: Financial Instruments—Overall (Subtopic 825-10) (continued)

ACCOUNTING STANDARDS UPDATES

• Effective for public entities for fiscal years beginning after December 15, 2017, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019.

• Adopted on a modified retrospective basis.

• Earlier application is permitted for non-public entities on the public entity dates.

ASU 2016-01: Financial Instruments—Overall (Subtopic 825-10) (continued)

ACCOUNTING STANDARDS UPDATES

• Requires that a lessee should recognize a liability to make lease payments and an asset representing its right to use the underlying asset for the lease term.

• Lessee accounting and disclosures are significantly changed.

• Lessor accounting and disclosures are largely unchanged except to align lessor guidance with revenue standards under ASC 606 (new revenue standard).

• Only applies to the leases of property, plant, and equipment.

• Fewer lease origination costs will be capitalizable for lessors and lessees.

ASU 2016-02: Leases (Topic 842)

ACCOUNTING STANDARDS UPDATES

For lease terms of 12 months or less –

• A lessee may elect not to recognize lease assets and liabilities by class of asset.

• Lease expense will be recognized on a straight-line basis.

• Lessee must consider options to extend the lease when considering this election (may not have a short-term lease).

ASU 2016-02: Leases (Topic 842) (continued)

ACCOUNTING STANDARDS UPDATES

Current Lease Accounting

New Lease Model

Lessee accounting Leases are either:• Operating leases (off

balance sheet)• Capital leases

• All leases recorded on balance sheet (except short-term)

• Two income statement presentations

• Operating lease• Finance lease

Lessor accounting • Operating leases• Sales-type or direct

finance leases• Leveraged leases

• Operating leases• Sales-type/direct finance

leases• No more leveraged leases

ASU 2016-02: Leases (Topic 842) (continued)

ACCOUNTING STANDARDS UPDATES

• Finance leases˗ Most existing capital/finance leases will be “finance” leases.

˗ Record amortization expense for the asset and interest expense on the liability (expense is greater in early years).

˗ Classify payments of principal as financing cash flows and payments of interest and variable lease payments as operating cash flows.

• Operating leases˗ Most existing operating leases will be “operating” leases.

˗ Record amortization and interest expense together as a single cost in SG&A (rent expense) on a straight-line basis.

˗ Cash payments classified as operating cash flows.

ASU 2016-02: Leases (Topic 842) (continued)

ACCOUNTING STANDARDS UPDATES

Lease is a finance lease if any of the following criteria are met at lease commencement:

• Lease transfers ownership at end of lease term.

• Lease grants lessee an option to purchase the asset that lessee is reasonably certain to exercise.

• Lease term is for a major part of remaining economic life of asset.

• Present value of lease payments and any residual value guarantee equals or exceeds substantially all of the fair value of the asset.

• Asset is of such a specialized nature that it is expect to have no alternative future use to the lessor at end of lease term.

ASU 2016-02: Leases (Topic 842) (continued)

ACCOUNTING STANDARDS UPDATES

• Payments related to optional periods should be included only if lessee is reasonably certain to exercise the option.

• Similarly, purchase options for the underlying asset should be included only if lessee is reasonably certain to exercise.

• Reasonably certain is a high degree of confidence that future event will occur based on all economic factors relevant to that assessment. See ASC 842-10-55-26 for guidance.

• Variable lease payments are excluded unless they are dependent on an index or rate.

ASU 2016-02: Leases (Topic 842) (continued)

ACCOUNTING STANDARDS UPDATES

• ASU defines a lease as a contract, or part of a contract, that conveys the right to control the use of the identified asset for a period of time in exchange for consideration.

• Control the use of the identified asset means that customer has both:

1) The right to obtain substantially all of the economic benefit from the use of the asset.

2) The right to direct the use of the asset.

ASU 2016-02: Leases (Topic 842) (continued)

ACCOUNTING STANDARDS UPDATES

• Effective for public entities for fiscal years beginning after December 15, 2018, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020.

• Lessees and lessors are required to recognize and measure leases at the beginning of the earliest period presented using a modified retrospective approach.

• Earlier application is permitted.

ASU 2016-02: Leases (Topic 842) (continued)

ACCOUNTING STANDARDS UPDATES

Several optional practical expedients are available:

Must be elected as a package at the adoption date

An entity may elect not to reassess:

• If expired or existing contracts contain leases under the new definition of a lease

• Classification for expired or existing leases

• If previously capitalized initial direct costs would qualify for capitalization under the new standard

May be elected individually or with the other practical expedients

• May use hindsight in determining the leaseterm (e.g., evaluating options to extend or terminate or to purchase ROU assets) and in assessing impairment of ROU assets

ACCOUNTING STANDARDS UPDATES

• Permits private companies that elect to adopt for the first time one of the accounting alternatives covered in this ASU after their effective dates to forgo having to assess whether the accounting alternative is preferable.

• Any subsequent change to an accounting policy election requires justification that the change is preferable.

• The ASU is effective immediately.

ASU 2016-03: Intangibles – Goodwill and Other (Topic 350); Business Combinations (Topic 805); Consolidation (Topic 810); Derivatives and Hedging (Topic 815)

ACCOUNTING STANDARDS UPDATES

• Requires breakage for liabilities related to the sale of prepaid stored-value products be accounted for consistent with the breakage guidance in Topic 606.

• Applies to prepaid gift and phone cards and traveler’s checks.

• Topic 606 contains specific breakage guidance but excludes financial liabilities.

ASU 2016-04: Intangibles – Liabilities —Extinguishments of Liabilities (Subtopic 405-20)

ACCOUNTING STANDARDS UPDATES

• Effective for public entities for fiscal years beginning after December 15, 2017, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019.

• Entity can elect to adopt the amendment using a modified retrospective approach or retrospectively.

• Earlier application is permitted.

ASU 2016-04: Intangibles – Liabilities —Extinguishments of Liabilities (Subtopic 405-20) (continued)

ACCOUNTING STANDARDS UPDATES

• Novations of derivative instruments may occur for various reasons including mergers, intercompany transactions, compliance with laws, etc.

• Clarifies that a change in the counterparty to a derivative instrument that has been designated as the hedging instrument does not, in and of itself, require dedesignation of that hedging relationship provided that all other hedge accounting criteria continue to be met.

ASU 2016-05: Derivatives and Hedging (Topic 815)

ACCOUNTING STANDARDS UPDATES

• Effective for public entities for fiscal years beginning after December 15, 2016, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018.

• Entity can elect to adopt the amendment prospectively, on a modified retrospective approach, or retrospectively.

• Earlier application is permitted.

ASU 2016-05: Derivatives and Hedging (Topic 815) (continued)

ACCOUNTING STANDARDS UPDATES

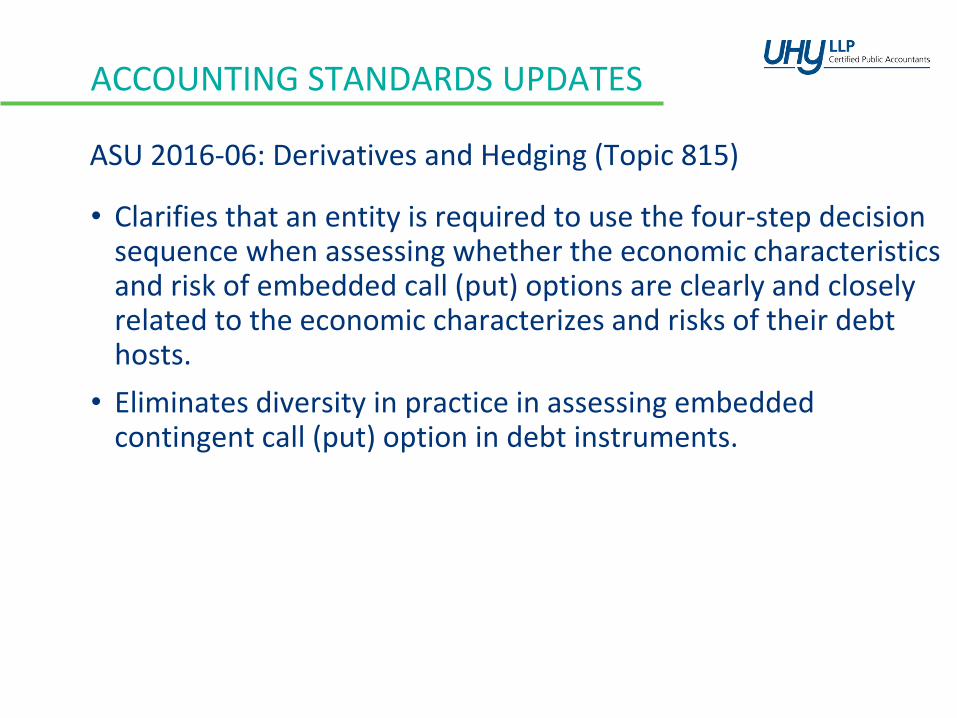

• Clarifies that an entity is required to use the four-step decision sequence when assessing whether the economic characteristics and risk of embedded call (put) options are clearly and closely related to the economic characterizes and risks of their debt hosts.

• Eliminates diversity in practice in assessing embedded contingent call (put) option in debt instruments.

ASU 2016-06: Derivatives and Hedging (Topic 815)

ACCOUNTING STANDARDS UPDATES

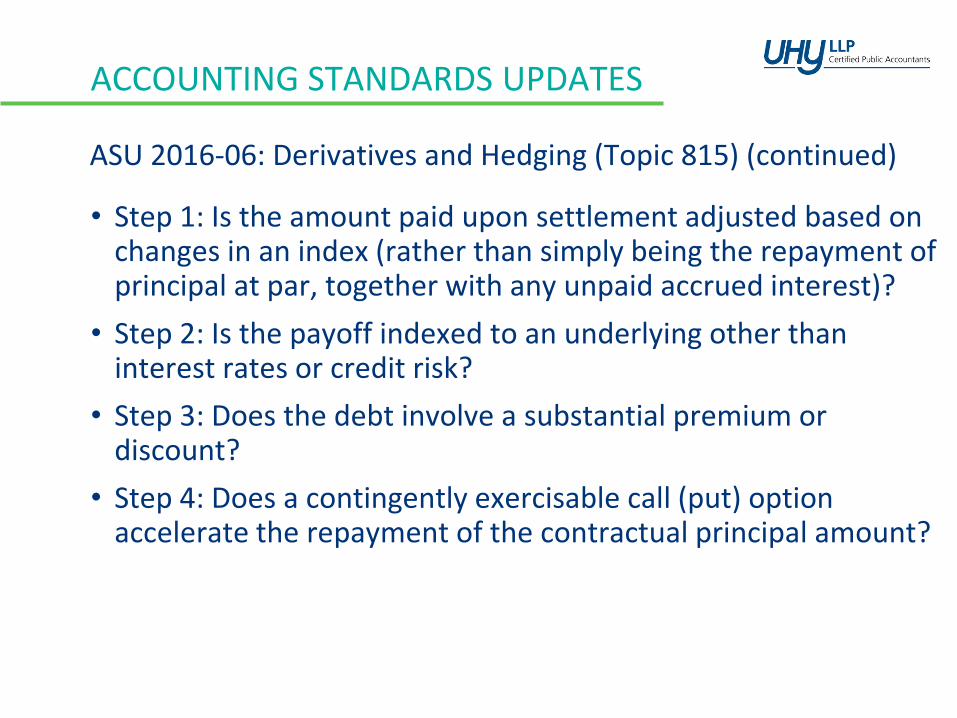

• Step 1: Is the amount paid upon settlement adjusted based on changes in an index (rather than simply being the repayment of principal at par, together with any unpaid accrued interest)?

• Step 2: Is the payoff indexed to an underlying other than interest rates or credit risk?

• Step 3: Does the debt involve a substantial premium or discount?

• Step 4: Does a contingently exercisable call (put) option accelerate the repayment of the contractual principal amount?

ASU 2016-06: Derivatives and Hedging (Topic 815) (continued)

ACCOUNTING STANDARDS UPDATES

• Effective for public entities for fiscal years beginning after December 15, 2016, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018.

• Entity should apply the amendment on a modified retrospective basis to existing debt instruments.

• Earlier application is permitted.

ASU 2016-06: Derivatives and Hedging (Topic 815) (continued)

ACCOUNTING STANDARDS UPDATES

• Eliminates the requirement to retroactively adjust the investment and net income as if the equity method had been applied during all prior periods when an investment qualifies for the equity method as a result of an increase in the level of ownership interest or degree of influence.

• Add the cost of acquiring the additional interest to the current basis of the previously held interest and adopt the equity method of accounting as of that date.

• Requires that unrealized holding gains or losses be recognized in earnings when an available-for-sale equity security becomes qualified for the equity method of accounting.

ASU 2016-07: Investments —Equity Method and Joint Ventures (Topic 323)

ACCOUNTING STANDARDS UPDATES

• For all entities, effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016.

• Entity should adopt the amendment prospectively.

• Earlier application is permitted.

ASU 2016-07: Investments —Equity Method and Joint Ventures (Topic 323) (continued)

ACCOUNTING STANDARDS UPDATES

• Simplifies several aspects of the accounting for share-based payments.

• Some of areas of simplification apply only to nonpublic entities.

• Accounting for income taxes

˗ All excess tax benefits and tax deficiencies (including tax benefits of dividends on share-based payment awards) should be recognized as income tax expense or benefit in the income statement.

˗ Tax effects of exercised or vested awards should be treated as discrete items in the reporting period in which they occur.

˗ An entity also should recognize excess tax benefits regardless of whether the benefit reduces taxes payable in the current period.

ASU 2016-09: Compensation —Stock Compensation (Topic 718)

ACCOUNTING STANDARDS UPDATES

• Classification of excess tax benefits on statement of cash flows˗ Excess tax benefits should be classified along with other income tax

cash flows as an operating activity.

• Forfeitures˗ An entity can make an entity-wide accounting policy election to either

estimate the number of awards that are expected to vest (current GAAP) or account for forfeitures when they occur.

• Minimum statutory tax withholding requirements˗ The threshold to qualify for equity classification permits withholding

up to the maximum statutory tax rates in the applicable jurisdictions (previously limited to employer’s minimum statutory rates).

ASU 2016-09: Compensation —Stock Compensation (Topic 718) (continued)

ACCOUNTING STANDARDS UPDATES

• Classification of employee taxes paid on statement of cash flows when employer withholds shares for tax-withholding

˗ Cash paid by an employer when directly withholding shares for tax withholding purposes should be classified as a financing activity.

• Practical Expedient – Expected Term˗ A nonpublic entity can elect to apply a practical expedient to estimate

the expected term for all awards with performance or service conditions that meet certain conditions.

• Intrinsic Value˗ A nonpublic entity can make a one-time accounting policy election to

switch from measuring all liability-classified awards at fair value to intrinsic value.

ASU 2016-09: Compensation —Stock Compensation (Topic 718) (continued)

ACCOUNTING STANDARDS UPDATES

• Effective for public entities for fiscal years beginning after December 15, 2016, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018.

• See ASU for details on how each amendment should be applied.

• Earlier application is permitted, but an entity must adopt all amendments in the same period.

ASU 2016-09: Compensation —Stock Compensation (Topic 718) (continued)

ACCOUNTING STANDARDS UPDATES

• Rescinds the following SEC Staff Observer comments upon adoption of Topic 606:

a. Revenue and Expense Recognition for Freight Services in Process, which is codified in paragraph 605-20-S99-2

b. Accounting for Shipping and Handling Fees and Costs, which is codified in paragraph 605-45-S99-1

c. Accounting for Consideration Given by a Vendor to a Customer (including Reseller of the Vendor’s Products), which is codified in paragraph 605-50-S99-1

d. Accounting for Gas-Balancing Arrangements (that is, use of the “entitlements method”), which is codified in paragraph932-10-S99-5.

ASU 2016-11: Revenue Recognition (Topic 605) and Derivatives and Hedging (Topic 815)

ACCOUNTING STANDARDS UPDATES

• Replaces the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a boarder range of reasonable and supportable information to inform credit loss estimates.

• Objective is to provide more useful information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity.

• Affects entities holding financial assets and net investment in leases that are not accounted for at fair value through net income.

ASU 2016-13: Credit Losses (Topic 326)

ACCOUNTING STANDARDS UPDATES

• Affects loans, debt securities, trade receivables, net investments in leases, off-balance-sheet credit exposures, reinsurance receivables, and any other financial assets not excluded from the scope that have the contractual right to receive cash.

• The main provisions of the ASU affect the following areas:

˗ Assets measured at amortized cost

˗ Available-for-sale debt securities

ASU 2016-13: Credit Losses (Topic 326) (continued)

ACCOUNTING STANDARDS UPDATES

• Assets measured at amortized cost

˗ Financial assets measured at amortized cost are required to be presented at the net amount expected to be collected.

˗ Income statement should reflect the measurement of credit losses for newly recognized financial assets, as well as the expected increases or decreases of expected credit losses that have taken place during the period.

˗ Expected credit losses are to be based on relevant information about past events, including historical experience, current conditions, and reasonable and supportable forecasts that affect collectability.

ASU 2016-13: Credit Losses (Topic 326) (continued)

ACCOUNTING STANDARDS UPDATES

• Available-for-sale debt securities

˗ Credit losses should be recorded through an allowance.

˗ Allowance for credit losses is limited to the amount by which fair value is below amortized cost.

• For purchased assets with a more-than-insignificant amount of credit deterioration since origination, the initial allowance for credit losses is added to the purchase price rather than reported as a credit loss expense. Only subsequent changes in the allowance for credit losses are recorded in credit loss expense.

ASU 2016-13: Credit Losses (Topic 326) (continued)

ACCOUNTING STANDARDS UPDATES

• Effective for public entities for fiscal years beginning after December 15, 2019, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2020, and interim periods within fiscal years beginning after December 15, 2021.

• See ASU for details on how the amendment should be applied.

• Earlier application is permitted for fiscal years beginning after December 15, 2018, and interim periods within those years.

ASU 2016-13: Credit Losses (Topic 326) (continued)

ACCOUNTING STANDARDS UPDATES

• Amends financial statement requirements to improve the current net asset classification requirements and information presented in the financial statements and notes about an entity’s liquidity, financial performance, and cash flows.

• Main provisions are as follows:

˗ Present on the face of the statement of financial position two classes of net assets rather than the currently required three classes —

1) net assets with donor restrictions

2) net assets without donor restrictions

ASU 2016-14: Not-for-Profit Entities (Topic 958)

ACCOUNTING STANDARDS UPDATES

˗ Present on the face of the statement of activities the amount of the change in each of the two classes of net assets rather than the currently required three classes.

˗ No longer requires the presentation or disclosure of the indirect method if using the direct method.

˗ Requires several new and enhanced disclosures.

˗ Report investment return net of external and direct internal investment expenses (no longer disclose of netted expenses).

˗ Absent explicit donor stipulations, use the placed-in-service approach for reporting expirations of restrictions on gifts of cash or other assets to be used to acquire or construct a long-lived asset.

ASU 2016-14: Not-for-Profit Entities (Topic 958) (continued)

ACCOUNTING STANDARDS UPDATES

• Effective for fiscal years beginning after December 15, 2017, and interim periods within fiscal years beginning after December 15, 2018.

• Application to interim financial statements is permitted but not required in the initial year of application.

• In the period of adoption, an NFP should disclose the nature of any reclassifications or restatements and their effects, if any, on changes in the net asset classes for each period presented.

• Entity should adopt the amendment retrospectively.

• Earlier application is permitted.

ASU 2016-14: Not-for-Profit Entities (Topic 958) (continued)

ACCOUNTING STANDARDS UPDATES

Provides guidance on eight specific cash flow issues:

• Debt prepayment or debt extinguishment costs

˗ Cash payments for debt prepayment or debt extinguishment costs should be classified as cash outflows for financing activities.

• Settlement of zero-coupon debt instruments or other debt with coupon interest rates that are insignificant in relation to the effective interest rate of the borrowing

˗ Classify the portion of the cash payment attributable to the accreted interest from the debt discount as cash outflows for operating activities, and the portion of the cash payment attributable to the principal as cash outflows for financing activities.

ASU 2016-15: Statement of Cash Flows (Topic 230)

ACCOUNTING STANDARDS UPDATES

• Contingent consideration payments made after a business combination

˗ Cash payments not made soon after the acquisition date should be separated and classified as cash outflows for financing activities and operating activities.

˗ Cash payments up to the amount of the contingent consideration liability recognized at the acquisition date (including measurement-period adjustments) should be classified as financing activities; any excess should be classified as operating activities.

˗ Cash payments made soon after the acquisition date should be classified as cash outflows for investing activities.

ASU 2016-15: Statement of Cash Flows (Topic 230) (continued)

ACCOUNTING STANDARDS UPDATES

• Proceeds from the settlement of insurance claims

˗ Cash proceeds received from insurance claims should be classified based on the related coverage (that is, the nature of the loss).

˗ For proceeds received in a lump sum, classify based on the nature of each loss included in the settlement.

• Proceeds from the settlement of corporate-owned life insurance policies, including bank-owned life insurance policies

˗ Cash proceeds received from corporate-owned life insurance policies should be classified as cash inflows from investing activities.

˗ Cash payments for premiums on corporate-owned policies may be classified as cash outflows for investing activities, operating activities, or a combination of investing and operating activities.

ASU 2016-15: Statement of Cash Flows (Topic 230) (continued)

ACCOUNTING STANDARDS UPDATES

• Distributions received from equity method investees

˗ In applying the equity method, entities should make an election to classify distributions received using either of the following:

Cumulative earnings approach

Nature of the distribution approach

• Beneficial interests in securitization transactions

˗ A transferor’s beneficial interest obtained in a securitization should be disclosed as a noncash activity, and cash receipts from payments on a transferor’s beneficial interests in securitized trade receivables should be classified as cash inflows from investing activities.

ASU 2016-15: Statement of Cash Flows (Topic 230) (continued)

ACCOUNTING STANDARDS UPDATES

• Separately identifiable cash flows and application of the predominance principle

˗ Classification of receipts and payments that have aspects of more than one class of cash flows should be determined first by applying specific guidance in GAAP.

˗ In the absence of specific guidance, an entity should determine each separately identifiable source or use based on the nature of the underlying cash flows and classify accordingly.

˗ When receipts and payments have aspects of more than one class of cash flows and cannot be separated by source or use, the appropriate classification should depend on the activity that is likely to be the predominant source or use of cash flows for the item.

ASU 2016-15: Statement of Cash Flows (Topic 230) (continued)

ACCOUNTING STANDARDS UPDATES

• Effective for public entities for fiscal years beginning after December 15, 2017, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019.

• Entities should adopt the amendment retrospectively.

• Earlier application is permitted.

ASU 2016-15: Statement of Cash Flows (Topic 230) (continued)

ACCOUNTING STANDARDS UPDATES

• Requires an entity to recognize income tax consequences of an intra-entity transfer of an asset other than inventory when the transfer occurs (eliminates current exception).

• Aligns the recognition policy with IFRS.

• Effective for public entities for fiscal years beginning after December 15, 2017, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019.

• Adopt the amendment on a modified retrospective basis.

• Earlier application is permitted.

ASU 2016-16: Income Taxes (Topic 740)

ACCOUNTING STANDARDS UPDATES

• In a VIE model, the company has a controlling financial interest when it has:

˗ The power to direct the activities that most significantly affect the economic performance of the entity; and

˗ The obligation to absorb losses or the right to receive benefits of the entity that could be potentially significant to the entity.

• This ASU requires that the reporting entity that is a single decision maker of a VIE, in determining if it satisfies the second characteristic of a primary beneficiary, to include all of its direct variable interests and, on a proportionate basis, its indirect variable interests.

ASU 2016-17: Consolidation (Topic 810)

ACCOUNTING STANDARDS UPDATES

• If, after the assessment, an entity does not have the characteristics of a primary beneficiary, then it must evaluate whether it and a related party under common control, as a group, have the characteristics of a primary beneficiary.

• Effective for public entities for fiscal years beginning after December 15, 2016, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017.

• Early adoption is permitted.

• See ASU for details on how amendment should be adopted.

ASU 2016-17: Consolidation (Topic 810) (continued)

ACCOUNTING STANDARDS UPDATES

• Requires that restricted cash and restricted cash equivalents be included with cash and cash equivalents on the statement of cash flows.

• Effective for public entities for fiscal years beginning after December 15, 2017, and interim periods within those years.

• For all other entities, effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019.

• Early adoption is permitted.

• Should be adopted using a retrospective transition method.

ASU 2016-18: Statement of Cash Flows (Topic 230)

REVENUE FROM CONTRACTSWITH CUSTOMERS

CORE PRINCIPLES

Current GAAP New Standard

Recognize revenue when it is earned and realizable

• Persuasive evidence of an arrangement exists

• Delivery has occurred or services have been rendered

• Price is fixed or determinable

• Collectability is reasonably assured

Application of criteria is subject to industry specific guidance; including construction-and-production type contracts, software, real estate, etc.

Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

Application of criteria is based on the terms of the contract with the customer.

OLD GAAP VS. NEW GAAP

Current GAAP New Standard

Numerous requirements for recognizing revenue, including industry-specific guidance

Consistent principles for recognizing revenue, regardless of industry

Limited informative disclosure Broad disclosure about an organization’s contracts and customers

Many goods and services not treated as distinct revenue-generating transactions even though they may represent separate performance obligations

Revenue is recognized as performance obligations are satisfied

Amount of consideration allocated to an element is limited to the amount not contingent on delivering future goods or services

The transaction price is allocated to each performance obligation based on relative standalone selling price

Accounting for variable consideration differs greatly from industry to industry

A single model for considering variableconsideration (including rebates, discounts, bonuses, right of return)

STEPS TO RECOGNIZE REVENUE

#1• Identify the contract(s) with a customer

#2• Identify the performance obligations

#3• Determine the transaction price

#4• Allocate the transaction price to the

performance obligations

#5• Recognize revenue when (or as) performance

obligations are satisfied

STEP 1: IDENTIFY CONTRACT(S)

Applies to a contract if all of the following criteria are met:

• Parties have approved the contract and are committed

• Rights of the parties can be identified

• Payment terms can be identified

• Contract has commercial substance

• It is probable that the entity will collect the consideration to which it will be entitled in exchange for the goods or services that will be transferred to the customer

ASU 2016-12 clarifies guidance in assessing collectability:

• Clarifies that the objective of the collectability criterion is to determine whether the contract is valid and represents a substantive transaction on the basis of whether the customer has the ability and intention to pay promised consideration.

• If a contract fails Step 1, an entity should recognize revenue in the amount of consideration received when:

˗ the entity has transferred control of the goods or services

˗ the entity has stopped transferring goods or services (if applicable) and has no obligation under the contract to transfer additional goods or services; and

˗ the consideration received from the customer is nonrefundable.

STEP 1: IDENTIFY CONTRACT(S)

STEP 1: IDENTIFY CONTRACT(S)

Some contracts must be combined as one contract:

• Entered into at or near the same time

• Negotiated as a package with a single objective

• Consideration is interdependent

• Promise is a single performance obligation

IDENTIFY CONTRACTS: EXAMPLE 1A

• Real estate developer enters into a contract with a customer for the sale of a $1 million building.

• Customer intends to use the space for a restaurant.

• Area has a high level of competition in the restaurant business.

• Customer has no prior experience in the industry and has no other income or assets.

• Customer paid an upfront, nonrefundable fee of $50,000 and financed the remaining 95% on a long-term basis with the real estate developer (nonrecourse loan).

• The customer will obtain control of the building at the contract inception.

• The customer intends to repay the loan primarily from income derived from the restaurant.

Has the contract met all the necessary criteria of the standard?

IDENTIFY CONTRACTS: EXAMPLE 1A

• Entity concludes that the criterion of collectability is not met because it is not probable that it will collect substantially all of the consideration to which it is entitled.

• Nonrefundable fee cannot be initially recognized as revenue.

• This conclusion is based on the following factors:˗ Customer intends to repay the loan primarily from the income

of the restaurant in which they have little experience and there is heavy competition.

˗ Customer has no other means to repay the loan should the restaurant fail.

˗ As the loan is a nonrecourse loan, the customer has limited liability in the event of default.

IDENTIFY CONTRACTS: EXAMPLE 1B

• A service provider enters into a three-year service contract with a new customer of low credit quality.

• Transaction price of the contract is $720, and $20 is due at the end of each month (standalone monthly selling price is $20).

• Entity’s history with this class of customer indicates it is not probable the customer will pay the transaction price of $720, and the customer is expected to make the payments required for at least 9 months.

• If the customer stops making the required payments, the entity’s customary business practice is to limit its credit risk by not transferring further services to the customer and to pursue collection for the unpaid services.

Has the contract met all the necessary criteria of the standard?

IDENTIFY CONTRACTS: EXAMPLE 1B

• It is not probable the entire transaction price ($720) will be collected because of the customer’s low credit rating.

• However, exposure to credit risk is mitigated because the entity has the ability and intent (as evidenced by its customary business practice) to stop providing services if the customer does not pay the promised consideration for services provided.

• Therefore, the entity concludes that the contract meets the collectability criterion because it is probable that the customer will pay substantially all of the consideration to which the entity is entitled for the services the entity will transfer to the customer.

STEP 2: IDENTIFY THE PERFORMANCE OBLIGATIONS

• A performance obligation is a promise in a contract with a customer to transfer to the customer either:

˗ A good or service (or a bundle of goods or services) that is distinct; or

˗ A series of distinct goods and services that are substantially the same and that have the same pattern of transfer to the customer.

• A good or service is distinct if both:

˗ Customer can benefit from the good or service on its own or together with other readily available resources; and

˗ Good or service is separately identifiable from other promises in the contract.

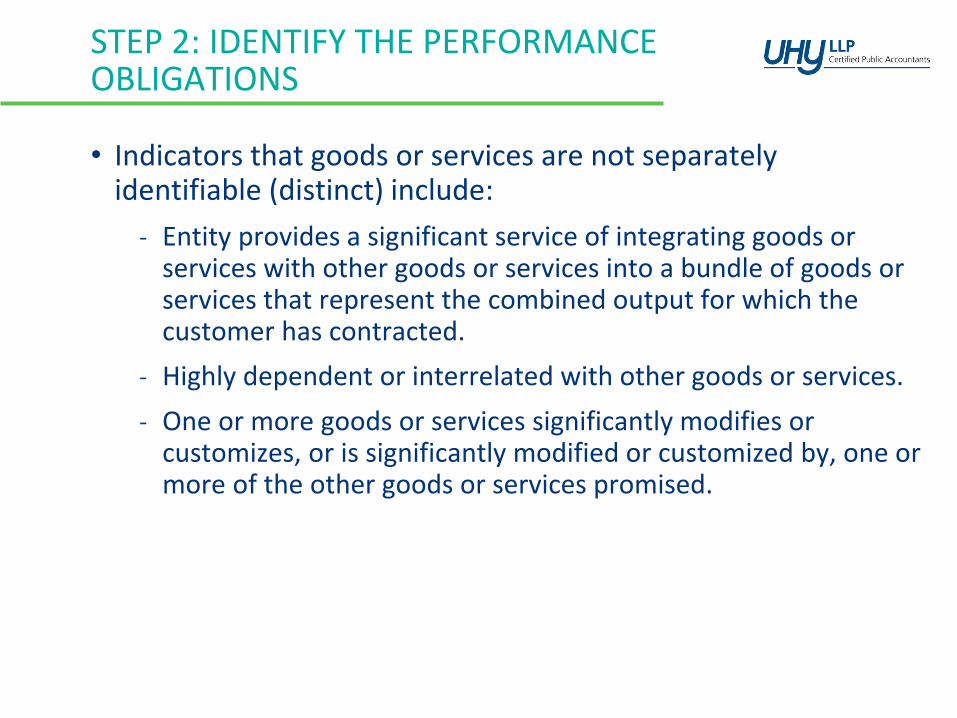

STEP 2: IDENTIFY THE PERFORMANCE OBLIGATIONS

• Indicators that goods or services are not separately identifiable (distinct) include:

˗ Entity provides a significant service of integrating goods or services with other goods or services into a bundle of goods or services that represent the combined output for which the customer has contracted.

˗ Highly dependent or interrelated with other goods or services.

˗ One or more goods or services significantly modifies or customizes, or is significantly modified or customized by, one or more of the other goods or services promised.

STEP 2: IDENTIFY THE PERFORMANCE OBLIGATIONS

Immaterial promised goods and services

• Not required to assess whether promised goods or services are performance obligations if they are immaterial in the context of the contract.

• If the revenue related to a performance obligation that includes goods or services that are immaterial in the context of the contract is recognized before those immaterial goods or services are transferred to the customer, then the related costs to transfer those goods or services shall be accrued.

STEP 2: IDENTIFY THE PERFORMANCE OBLIGATIONS

Shipping and Handling Activities

• If shipping and handling activities are performed before the customer obtains control of the good, then the shipping and handling activities are not a promised service but are activities to fulfill the promise to transfer the good.

• If shipping and handling activities are performed after a customer obtains control of the good, then an entity may elect to account for shipping and handling as activities to fulfill the promise to transfer the good.

IDENTIFY PERFORMANCE OBLIGATIONS – EXAMPLE 10C

• An entity grants a customer a three-year license to anti-virus software and promises to provide when-and-if available updates during the license period.

• The entity frequently provides updates that are critical to the continued utility of the software.

• Without the updates, the customer’s ability to benefit from the software would decline significantly during the three-year arrangement.

IDENTIFY PERFORMANCE OBLIGATIONS – EXAMPLE 10C

• The entity concludes that the software and the updates are each promised goods or services in the contract and are each capable of being distinct; however,

the entity concludes that its promises to transfer the software license and provide updates, when-and-if available, are not separately identifiable.

• The updates significantly modify the functionality of the software and are integral to maintaining the utility of the software.

• The license and the updates are, in effect, inputs to a combined item (anti-virus protection) and fulfill a single promise to the customer to provide protection from computer viruses for three years (a single performance obligation).

IDENTIFY PERFORMANCE OBLIGATIONS – EXAMPLE 11A

• A software developer enters into a contract to:

˗ Transfer a software license

˗ Perform installation services

˗ Provide unspecified software updates and technical support for two years

• Additional facts:

˗ Entity sells the license, installation service, and technical support separately

˗ Installation services are routinely performed by other entities and does not significantly modify the software

˗ Software remains functional without the updates and technical support.

IDENTIFY PERFORMANCE OBLIGATIONS – EXAMPLE 11A

• Four performance obligations exist:

˗ Software license - Software updates

˗ Installation service - Technical support

• Software is delivered before the other goods and services and remains functional without the updates and support.

• Installation services are routine and can be obtained from alternate providers.

• Customer can benefit from the updates together with the software license transferred at the outset of the contract.

• Customer can benefit from each of the goods and services either on their own or together with the other goods and services that are readily available.

IDENTIFY PERFORMANCE OBLIGATIONS – EXAMPLE 11E

• An entity enters into a contract with a customer to provide a piece of off-the-shelf equipment (operational without any significant customization or modification) and to provide specialized consumables for use in the equipment at predetermined intervals over the next three years.

• The consumables are produced only by the entity, but are sold separately by the entity.

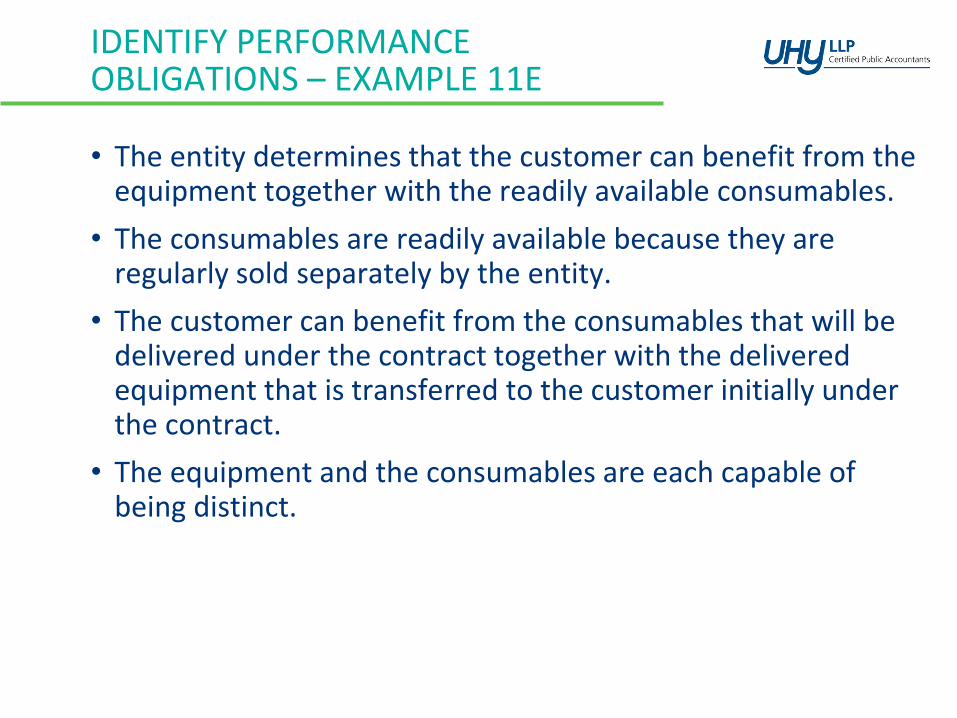

IDENTIFY PERFORMANCE OBLIGATIONS – EXAMPLE 11E

• The entity determines that the customer can benefit from the equipment together with the readily available consumables.

• The consumables are readily available because they are regularly sold separately by the entity.

• The customer can benefit from the consumables that will be delivered under the contract together with the delivered equipment that is transferred to the customer initially under the contract.

• The equipment and the consumables are each capable of being distinct.

IDENTIFY PERFORMANCE OBLIGATIONS – EXAMPLE 11E

• The entity determines that its promises to transfer the equipment and to provide consumables over a three-year period are each separately identifiable.

• The entity it is not providing a significant integration service that transforms the equipment and consumables into a combined output.

• Neither the equipment nor the consumables are significantly customized or modified by the other.

• The equipment and the consumables are not highly interdependent or highly interrelated because they do not significantly affect each other. The entity would be able to fulfill each of its promises in the contract independently of the other.

STEP 3: DETERMINE THE TRANSACTION PRICE

• Transaction price is the amount of consideration to which the entity expects to be entitled.

• Can be fixed amount or include variable consideration (e.g., discounts, rebates, refunds, price concessions, incentives, performance bonuses, penalties, etc.)

• Estimating variable consideration will require significant judgment.

• An entity may make an accounting policy election to exclude amounts collected from customers for all sales and similar taxes from the transaction price.

STEP 3: DETERMINE THE TRANSACTION PRICE

• Estimate variable consideration based on:

˗ Expected-value method (probability-weighted range), or

˗ Most likely amount

˗ Use whichever is most predictive of the amount to which the entity will be entitled

• Variable consideration constraint:

˗ Include variable consideration in the transaction price only to the extent it is probable that subsequent changes in the estimate will not result in a significant reversal of revenue.

• Applies only to variability resulting from reasons other than the form of the consideration.

STEP 3: DETERMINE THE TRANSACTION PRICE

• In evaluating variable consideration, consider:

˗ Susceptibility of consideration to factors outside the entity’s influence

˗ Uncertainty about consideration is not resolved for a long period of time

˗ If entity’s experience is limited or not predictive

˗ If entity has a practice of offering a broad range of price concessions or changing payment terms and conditions

˗ If contract has a large number and broad range of consideration

STEP 3: DETERMINE THE TRANSACTION PRICE

• Other matters to consider in determining the price:

˗ Significant financing components

˗ Noncash consideration

˗ Consideration payable to the customer

STEP 3: DETERMINE THE TRANSACTION PRICE

Significant Financing Component

• Adjust price for the time value of money if the timing of payments provides a significant financing benefit.

− Objective is to adjust the consideration to the amount that would have been paid if the customer had paid in cash

− One year practical expedient

• Don’t adjust consideration if difference between cash selling price and consideration are for reasons other than financing.

• Discount rate should reflect the rate in a separate financial transaction between parties.

• Discount rate should reflect credit characteristics of receiving party.

STEP 3: DETERMINE THE TRANSACTION PRICE

Noncash consideration

• Measured at fair value; or

• If fair value is not reasonably measurable, refer to standalone selling price.

• If assets are contributed towards fulfillment of the contract, assess control of the contributed assets.

• Measurement date is contract inception.

STEP 3: DETERMINE THE TRANSACTION PRICE

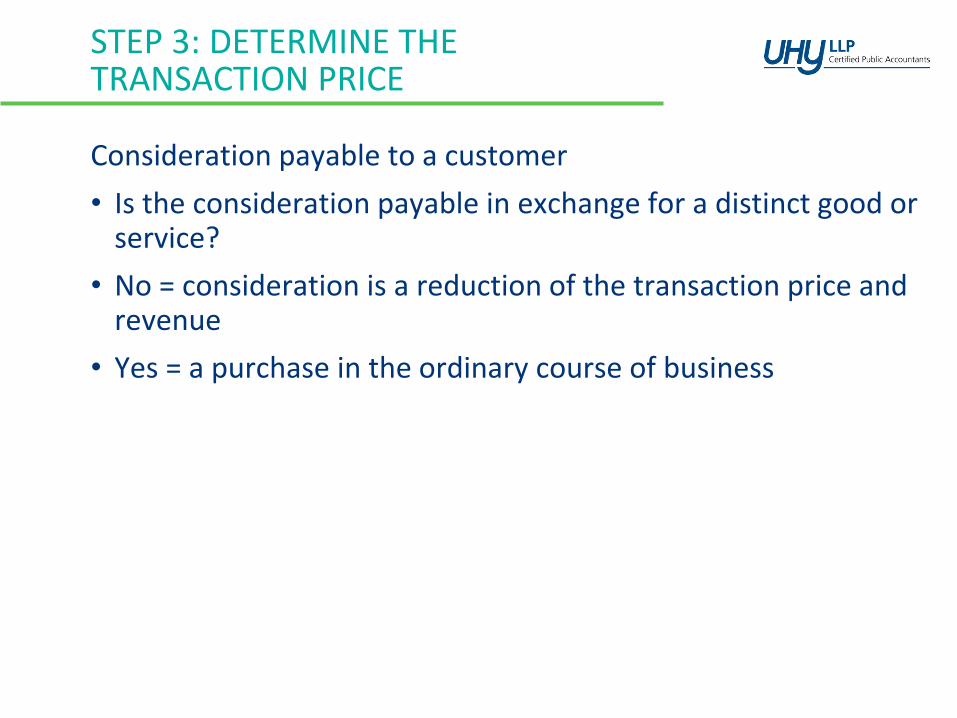

Consideration payable to a customer

• Is the consideration payable in exchange for a distinct good or service?

• No = consideration is a reduction of the transaction price and revenue

• Yes = a purchase in the ordinary course of business

DETERMINE THE TRANSACTION PRICE – EXAMPLE 22

Right of Return

• Entity enters into 100 contracts with customers to provide one product each for $100.

• Entity’s customary business practice is to allow returns within30 days for a full refund.

• Each product costs the company $60 to produce.

• Using the expected-value method, the entity estimates that 3 products will be returned based on significant experience.

DETERMINE THE TRANSACTION PRICE – EXAMPLE 22

• Entity first concludes that it can treat contracts as a portfolio because treating them individually is not materially different.

• Because the contract allows the product to be returned, the consideration is variable and subject to constraint.

• Although returns are outside their influence, entity has significant experience in estimating returns for this product and customer class.

• Uncertainty will be resolved within a short time frame.

• Entity concludes it is probable that a significant reversal in the cumulative amount of revenue recognized ($9,700) will not occur during the resolution of the uncertainty over the return period.

DETERMINE THE TRANSACTION PRICE – EXAMPLE 22

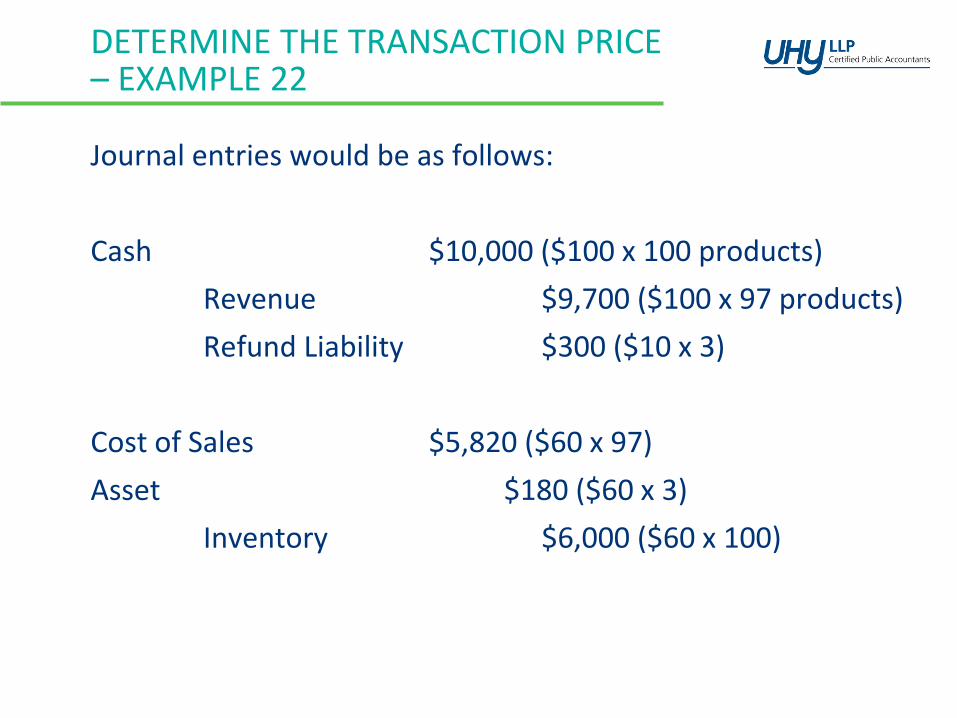

Journal entries would be as follows:

Cash $10,000 ($100 x 100 products)

Revenue $9,700 ($100 x 97 products)

Refund Liability $300 ($10 x 3)

Cost of Sales $5,820 ($60 x 97)

Asset $180 ($60 x 3)

Inventory $6,000 ($60 x 100)

DETERMINE THE TRANSACTION PRICE – EXAMPLE 26

Significant Financing Component and Right of Return

• An entity sells a new product to a customer for $121.

• Product can be returned within 90 days.

• Consideration is payable 24 months after delivery.

• Customer obtains control of the product at contract inception.

• Entity has no relevant historical evidence of product returns or other available market evidence (new product).

• Cash selling price is $100 if paid upon delivery for same product under otherwise identical terms and conditions.

• The entity’s cost of the product is $80.

DETERMINE THE TRANSACTION PRICE – EXAMPLE 26

• Due to a lack of history of returns, the entity cannot conclude that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur.

• Therefore, the entity would not recognize revenue when control of the product transfers to the customer.

• Revenue is recognized after 90 days when right of return lapses.

• Includes a significant financing component as the difference between the promised consideration of $121 and the cash selling price of $100.

• Implicit interest is 10%, which the entity determines is commensurate with the rate in a separate financing transaction.

DETERMINE THE TRANSACTION PRICE – EXAMPLE 26

• When product is transferred to customer —

Asset for right to product $80

Inventory $80

• When right of return lapses —

Receivables $100

Revenue $100

Cost of sales $80

Asset for right to product $80

• Interest would be accreted from the time the right of return lapsed until customer payment.

STEP 4: ALLOCATE THETRANSACTION PRICE

• Allocate transaction price to each performance obligation on the basis of standalone selling price

• Standalone selling price:

− Determine at inception of the contract

− Applied to goods and services underlying each separate performance obligation

− Price used is the price when sold separately

− Best evidence of standalone selling price:

Observable price

Price estimated using observable inputs

STEP 4: ALLOCATE THETRANSACTION PRICE

When estimating price use an approach that maximizes observable inputs:

• Adjusted market assessment

• Expected cost plus margin

• Residual approach (if standalone price is highly variable or uncertain)

STEP 4: ALLOCATE THETRANSACTION PRICE

Exceptions to allocating selling price:

• If sum of standalone selling prices exceed the transaction price, allocate the discount to separate obligations based on standalone selling price EXCEPT:

An entity must allocate a discount entirely to one or more separate performance obligation(s) if:

− Regularly sell each good or service on a standalone basis, and

− Observable selling prices provide evidence to where the entire discount should be allocated

STEP 4: ALLOCATE THETRANSACTION PRICE

Exceptions to allocating selling price:

• If the transaction price includes contingent consideration, apply contingent consideration entirely to a distinct good or service if:

− Contingent payment relates directly to the efforts to transfer that good or service, and

− Allocation to that distinct good or service is consistent with expectations

• An entity can allocate contingent consideration to more than one distinct good or service in a contract.

STEP 4: ALLOCATE THETRANSACTION PRICE

Changes to transaction price:

• Changes should be allocated to separate performance obligations consistent with initial allocation at inception.

• Amounts allocated should be recognized as revenue or a reduction of revenue in the period of change.

• An entity must allocate a change entirely to one or more distinct goods or services if:

− Contingent terms relate specifically to efforts to transfer that good or service, and

− Allocation is consistent with expectations

STEP 5: RECOGNIZE REVENUE

• Performance obligation is satisfied when customer obtains control of the good or service.

• Control is the ability to direct the use of and obtain substantially all of the remaining benefits from the asset.

• For each performance obligation, a determination must be made as to whether control is transferred over time or at a point in time.

STEP 5: RECOGNIZE REVENUE

Obtaining Control:

• Transfer of control is determined on the basis of indicators.

• Benefits of an asset are the potential cash flows that can be obtained directly or indirectly.

• Control includes the ability to prevent other entities from directing the use of and obtaining the benefits from the asset.

STEP 5: RECOGNIZE REVENUE

Indicators that control has transferred to the customer

• Entity has a present right to payment for the asset

• Customer has legal title to the asset

• Entity has transferred physical possession of the asset

• Customer has the significant risks and rewards of ownership of the asset

• Customer has accepted the asset

STEP 5: RECOGNIZE REVENUE

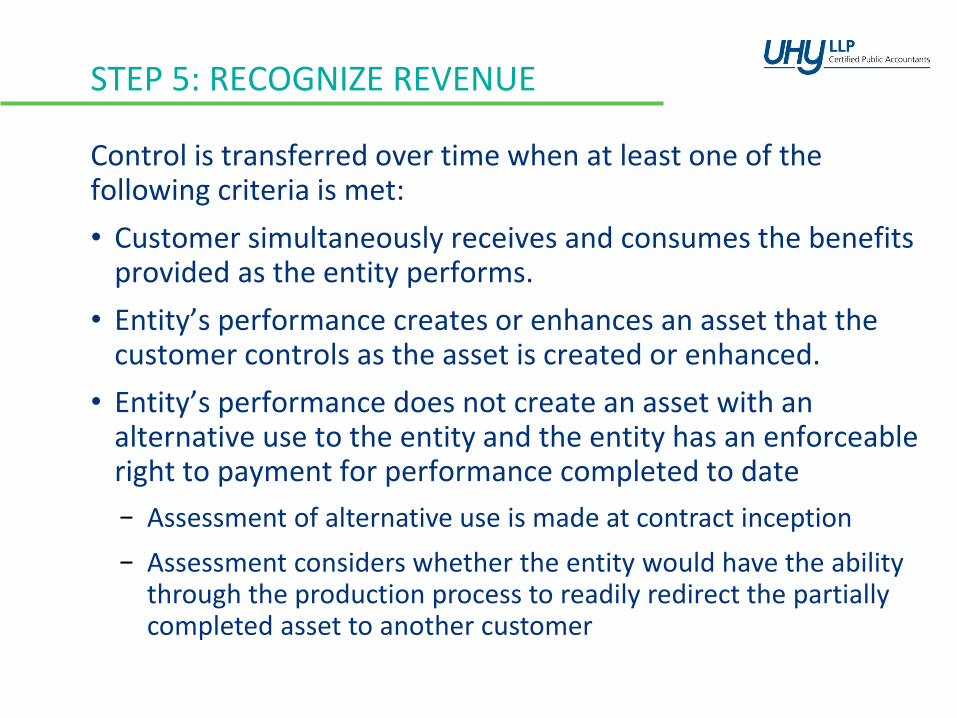

Control is transferred over time when at least one of the following criteria is met:

• Customer simultaneously receives and consumes the benefits provided as the entity performs.

• Entity’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced.

• Entity’s performance does not create an asset with an alternative use to the entity and the entity has an enforceable right to payment for performance completed to date

− Assessment of alternative use is made at contract inception

− Assessment considers whether the entity would have the ability through the production process to readily redirect the partially completed asset to another customer

STEP 5: RECOGNIZE REVENUE

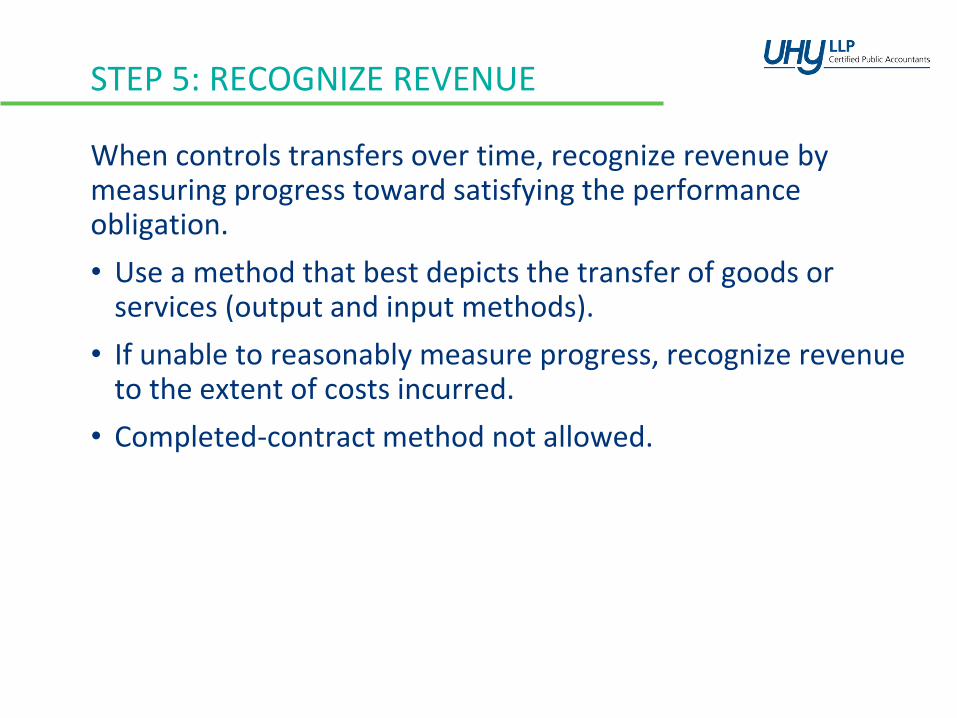

When controls transfers over time, recognize revenue by measuring progress toward satisfying the performance obligation.

• Use a method that best depicts the transfer of goods or services (output and input methods).

• If unable to reasonably measure progress, recognize revenue to the extent of costs incurred.

• Completed-contract method not allowed.

STEP 5: RECOGNIZE REVENUE –EXAMPLE 17

Satisfy obligation at a point in time or over time —

• An entity is developing a multi-unit residential complex.

• Customer enters into a contract for a specified unit under construction.

• Each unit is similar in size and floor plan but other attributes are different.

• Customer pays a deposit at contract inception, which is refundable only if the entity fails to complete construction in accordance with the contract.

• Remainder of the contract price is payable when the customer obtains possession of the unit.

• If customer defaults, entity only has the right to the deposit.

STEP 5: RECOGNIZE REVENUE –EXAMPLE 17

• Because the entity does not have a right to payment for work completed to date, the entity’s performance obligation is not satisfied over time.

• Instead, the entity would account for the sale of the unit as a performance obligation satisfied at a point in time when the unit is transferred.

CONTROL-BASED MODEL

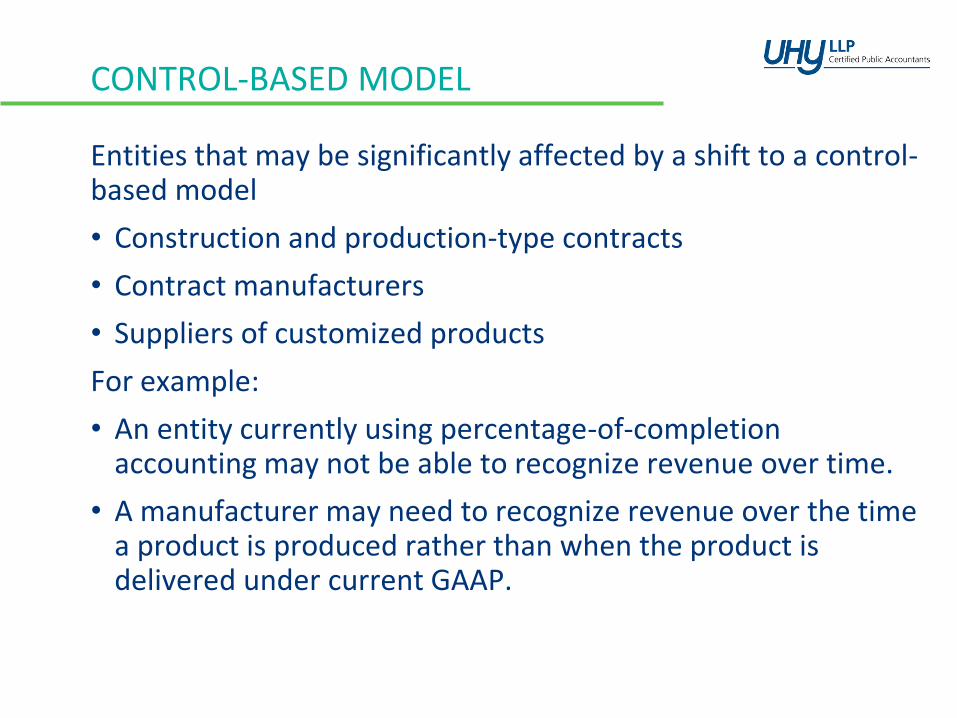

Entities that may be significantly affected by a shift to a control-based model

• Construction and production-type contracts

• Contract manufacturers

• Suppliers of customized products

For example:

• An entity currently using percentage-of-completion accounting may not be able to recognize revenue over time.

• A manufacturer may need to recognize revenue over the time a product is produced rather than when the product is delivered under current GAAP.

CONTRACT MODIFICATIONS

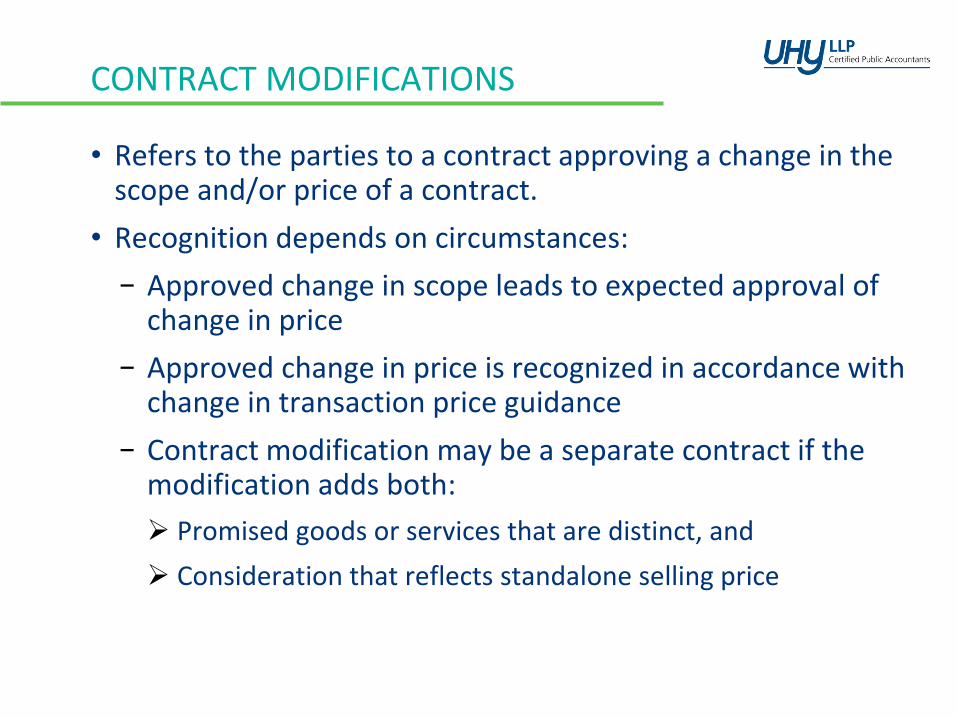

• Refers to the parties to a contract approving a change in the scope and/or price of a contract.

• Recognition depends on circumstances:

− Approved change in scope leads to expected approval of change in price

− Approved change in price is recognized in accordance with change in transaction price guidance

− Contract modification may be a separate contract if the modification adds both:

Promised goods or services that are distinct, and

Consideration that reflects standalone selling price

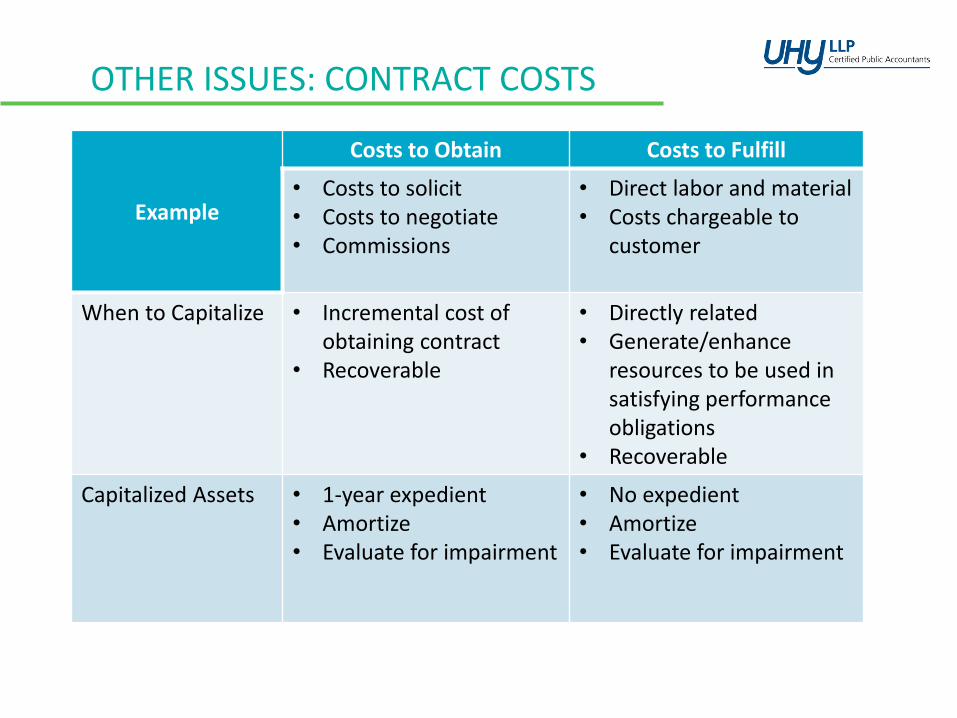

OTHER ISSUES: CONTRACT COSTS

Example

Costs to Obtain Costs to Fulfill

• Costs to solicit• Costs to negotiate• Commissions

• Direct labor and material• Costs chargeable to

customer

When to Capitalize • Incremental cost of obtaining contract

• Recoverable

• Directly related• Generate/enhance

resources to be used in satisfying performance obligations

• Recoverable

Capitalized Assets • 1-year expedient• Amortize• Evaluate for impairment

• No expedient• Amortize• Evaluate for impairment

OTHER ISSUES: WARRANTIES

• Use cost accrual method for warranty obligations (same as current GAAP).

• Warranties providing a service beyond ensuring that the goods or service complies with agreed-upon specifications are separate performance obligations.

• If there is an option to purchase the warranty separately, it is a separate performance obligation.

• If no option to purchase warranty separately, it is a separate performance obligation if any part of the warranty provides an additional service in addition to assurance the goods or services comply with specs.

OTHER ISSUES: LICENSES

Licenses for intellectual property (e.g. technology, motion pictures, music, franchises, patents, trademarks, copyrights):

• Recognize revenue as of a point in time for “functional IP” (intellectual property as it exists when the license is granted)

• Recognize revenue over time for “symbolic IP” intellectual property as it exists throughout the license period)

Significant change from current GAAP

OTHER ISSUES: LICENSES

• Functional intellectual property includes software, biological compounds or drug formulas, and completed media content (for example: films, television shows, or music).

• Symbolic intellectual property includes supporting or maintaining that intellectual property during the license period.

• Symbolic intellectual property includes brands, team or trade names, logos, and franchise rights.

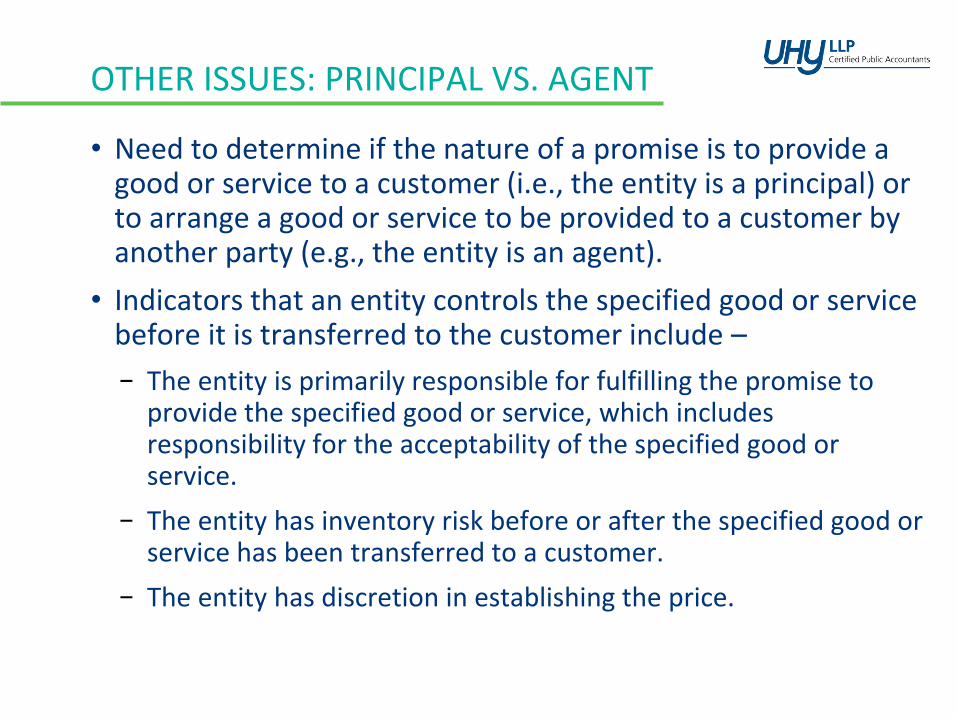

OTHER ISSUES: PRINCIPAL VS. AGENT

• Need to determine if the nature of a promise is to provide a good or service to a customer (i.e., the entity is a principal) or to arrange a good or service to be provided to a customer by another party (e.g., the entity is an agent).

• Indicators that an entity controls the specified good or service before it is transferred to the customer include –

− The entity is primarily responsible for fulfilling the promise to provide the specified good or service, which includes responsibility for the acceptability of the specified good or service.

− The entity has inventory risk before or after the specified good or service has been transferred to a customer.

− The entity has discretion in establishing the price.

LEGAL UPDATE

Carrie LeahyMemberBodman PLC – Ann Arbor

INTRASTATE OFFERINGS

• Rule 147:˗ Facilitates offerings relying on intrastate crowd-funding exemptions.

• Rule 147A:˗ Allows for out-of-state participants.

˗ Allows for companies to be incorporated out-of-state.

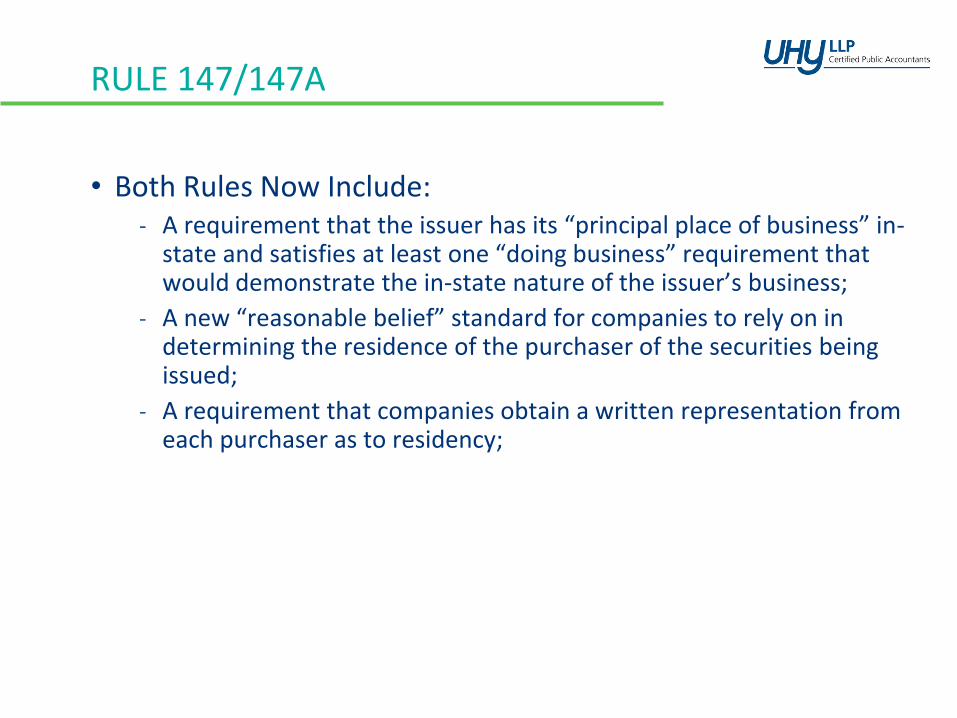

RULE 147/147A

• Both Rules Now Include:˗ A requirement that the issuer has its “principal place of business” in-

state and satisfies at least one “doing business” requirement that would demonstrate the in-state nature of the issuer’s business;

˗ A new “reasonable belief” standard for companies to rely on in determining the residence of the purchaser of the securities being issued;

˗ A requirement that companies obtain a written representation from each purchaser as to residency;

RULE 147/147A

• Both Rules Now Include (continued):˗ A limit on resales to persons residing within the state or territory of

the offering for a period of 6 months from the date of the sale by the company to the purchaser;

˗ An integration safe harbor that would include any prior offerings or sales of securities by the issuer made under another provision; and

˗ Legend requirements to offerees and purchaser about the limitations on resales.

REGULATION D

• Amendments to Rule 504:˗ Increase amount of securities sold in a 12-month period from $1m to

$5m.

˗ Disqualifies “bad actors” from participating.

˗ Repeal of Rule 505.

• Current status of definition of “Accredited Investor”?

MICHIGAN UNIFORM SECURITIES ACT

• New proposed rules were published in September 2016.˗ Regulatory gap on “finders.”

˗ Potentially adverse impact on private funds.

˗ Multiple changes for registered investment advisors.

LUNCH

We will reconvene in one hour

Scott MillerPartnerUHY LLP

Kevin BatesPartnerCambridge Consulting Group

831(B) MICRO CAPTIVES PANEL DISCUSSION

Randy O’BrienFounder, CEO and managing partnerCorporate & Endowment Solutions, Inc.

Jeremy HuishDirector of business developmentArtex Risk Solutions, Inc.

AGENDA

• Introductions

• Background on captive insurance companies

• Provide understanding of captive strategies and identify potential

solutions

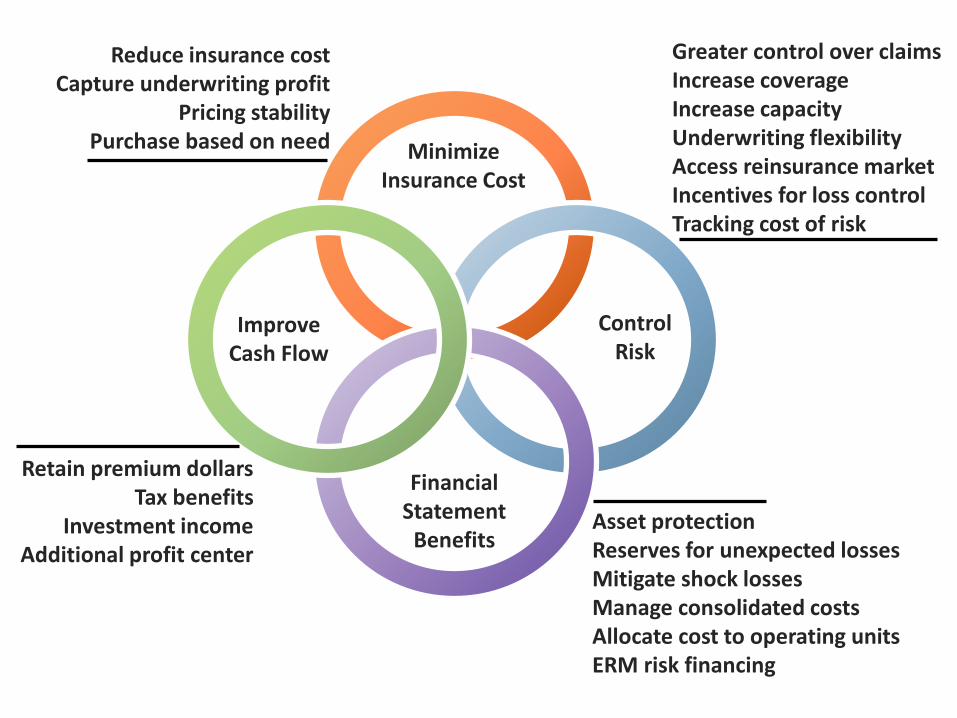

Retain premium dollarsTax benefits

Investment incomeAdditional profit center

Greater control over claimsIncrease coverageIncrease capacityUnderwriting flexibilityAccess reinsurance marketIncentives for loss controlTracking cost of risk

Minimize Insurance Cost

Control Risk

Financial Statement

Benefits

Improve Cash Flow

Reduce insurance costCapture underwriting profit

Pricing stabilityPurchase based on need

Asset protectionReserves for unexpected lossesMitigate shock lossesManage consolidated costsAllocate cost to operating unitsERM risk financing

CAPTIVE INSURANCETHE MIDDLE MARKET SOLUTION

A captive is an insurance company that insures the risks of its owner, affiliates, or a group of companies. It issues policies, collects premiums, and pays claims.

Shareholders

CaptiveBusiness

Basic Captive Diagram

Insurance Premiums

Insurance Coverage

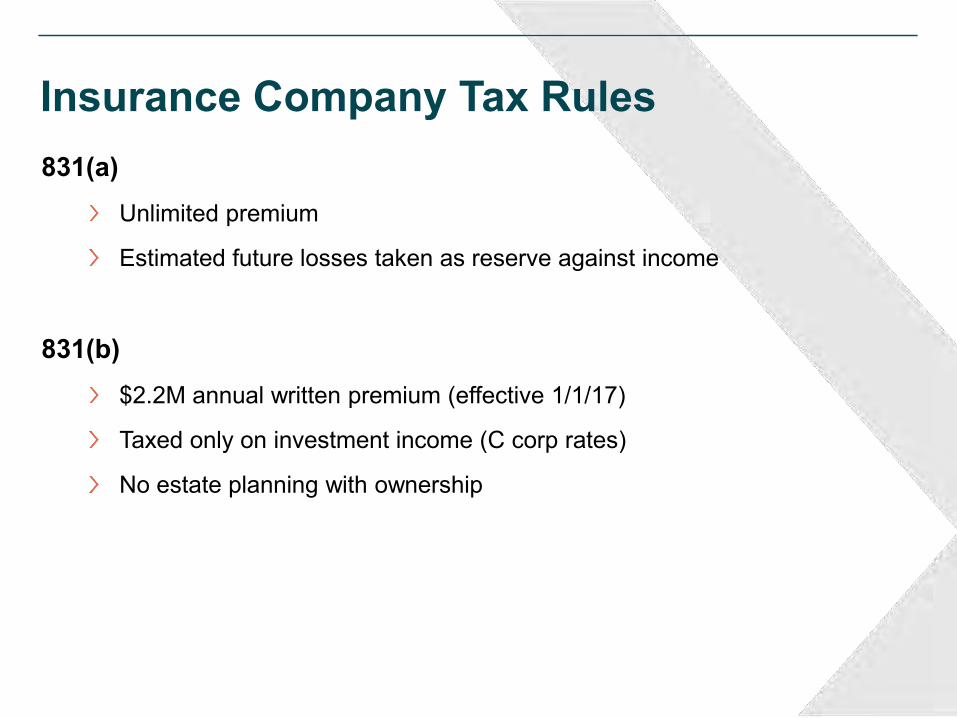

Insurance Company Tax Rules831(a)

Unlimited premium

Estimated future losses taken as reserve against income

831(b)$2.2M annual written premium (effective 1/1/17)

Taxed only on investment income (C corp rates)

No estate planning with ownership

Uses of Captive Assets

Business Other Insurance CompanyCaptive

Invest Assets

Shareholder

DividendsSalary Liquidation

ReinsurancePay losses

Stocks Bonds Other

Ownership Options

Captive

Shareholders Key EmployeesParentCompany

Estate planning restriction: No spouse or children may own more of the captive than such person owns of the insured business.

156

Who is a Candidate?

Business with:

$30M+ annual Gross Revenues

or

$200K+ annual P&C expense

or

$100K+ annual self-insured losses

Key Industries:Real Estate Developers / Builders

Manufacturers

Professional Services Firms

Franchisees

Restaurant / Hotel Chains

Physicians / Groups

Standard Insurance MarketWork Comp General Liability Auto Property Umbrella

Captive Policies

Deductibles

Work CompGeneral LiabilityProfessional LiabilityAutoCyber LiabilityProperty

Typically Uninsured Risk

ExclusionsCyber LiabilityWarrantyCollection RiskD&O/E&OMold & PollutionConstruction Defect

Typically Unavailable for Middle Markets Businesses

Regulatory ChangeAdministrative ActionsLitigation ExpensesBusiness Interruption DICReputational RiskLoss of Key EmployeeRework Expenses

New Tax Code

Section 831 Language

• The changes take effect Jan. 1, 2017 (for tax years after Dec. 31, 2016).

• The $2.2 Million threshold will be adjusted for inflation in $50,000 increments (rounding down).

$1.2m

2016

$2.2m

2017

$2.2m

2018

$2.25m

2019*

$2.25m

2020*

EFFECTIVE DATE AND ANNUAL INCREASES

* Showing possible adjustments due to possible inflation

NEW RISK DIVERSIFICATION REQUIREMENT

The 831(b) election will now require the insurance company to satisfy a diversification requirement, which can be met by either:

• Option 1 – no more than 20% of net written premiums from any one policyholder(i.e., The 80% Unrelated Risk Test),

OR

• Option 2 – The business owner’s spouse or descendants may not own more of the captive than they do of the business owner’s business(i.e., Family Ownership Test).

Child’s ownership in Captive

Child’s ownership in

Business +2%

* The test is more complex than shown here. Please refer to the actual language for specifics. For example the rules that apply to children also apply to a spouse.

FAMILY OWNERSHIP TEST*

Significant IRS Initiatives• 1977-1991: IRS Doctrine of “Economic Family” (Although Rejected by Courts) Prevails

– Resolution: taxpayers won several court cases rejecting the economic family doctrine and setting up the IRS safe harbors (Rev. Ruls. 2002-89, -90 -91).

• 2002: IRS designated PORCs (auto dealer owned reinsurance companies) as Listed Transactions and labeled as tax shelters

– Resolution: in 2004, PORCs were removed from the Listed Transaction list. Thousands of PORCs are used by auto dealers today.

• 2003: IRS audited large numbers of non-profit captives making the IRC 501(c)(15) election. – Resolution: Congress changed the law for this election, limiting its use. 501(c)(15)s are

still valid today, but limited to $600,000 of total income. • 2007: IRS proposed regulations to deny the reserve deduction for large captives.

– Resolution: US Senators got involved and the IRS revoked its changes.• 2009: IRS audits offshore insurance companies for the Federal Excise Tax (FET). This tax

does not apply to domestic captives or foreign captives making the 953(d) election. – Resolution: court case in 2014 held for the taxpayer and limited some of this tax.

• 2014-2015: Tax court cases focusing on large captives and insurance companies. – Resolution: 3 taxpayer victories: Rent-A-Center, Securitas, Residual Value Insurance

Recent IRS Activity

• 2013: IRS increases audit activity on 831(b) electing captives and captive managers

• 2015: IR-2015-19. IRS “Dirty Dozen” list references certain trust and captive arrangement

• 2015-2016: Tax Court cases awaiting decision: Avrahami

• 2016: Notice 2016-66

A VALID CAPTIVE REQUIRES“RISK DISTRIBUTION”

Risk distribution is a spreading of risk that allows the insurer to reduce the possibility that a single costly claim will exceed the amount available to the insurer for the payment of such a claim.

Related principles:

“The Law of Large Numbers”

Risk Sharing

Multiple Subsidiaries Unrelated Risk

Sub

Sub

Sub Sub

Sub

Sub

Sub

Sub

Sub

Sub Sub Sub