Embed Size (px)

Citation preview

Saïd Business School

Research Papers

Saïd Business School RP 2015-2

The Saïd Business School’s working paper series aims to provide early access to high-quality and rigorous academic research. The Shool’s working papers reflect a commitment to excellence, and an interdisciplinary scope that is appropriate to a business school embedded in one of the world’s major research universities. This paper is authorised or co-authored by Saïd Business School faculty. It is circulated for comment and discussion only. Contents should be considered preliminary, and are not to be quoted or reproduced without the author’s permission.

Angels and Venture Capitalists: Substitutes or

Complements?

Thomas Hellman Saïd Business School, University of Oxford; Sauder School of Business, University of British Columbia

Paul Schure University of Victoria

Dan Vo Sauder School of Business, University of British Columbia

February 2015

Electronic copy available at: http://ssrn.com/abstract=2602739

1

Angels and Venture Capitalists:

Substitutes or Complements?

Thomas F. Hellmann *

Said School of Business, Oxford University and NBER

Paul H. Schure

University of Victoria, Department of Economics

Dan H. Vo

Sauder School of Business, University of British Columbia

February 2015

We would like to thank the Investment Capital Branch of the Government of the Province of British

Columbia, and in particular Todd Tessier and Clint Megaffin, for allowing us to analyze the BCICP

data. We are grateful for the comments we received from Ajay Agrawal, Pascal Courty, Jean de

Bettignies, Josh Lerner, Antoinette Schoar, Veikko Thiele, Rick Townsend, seminar participants at

Oxford University, Queens University and the University of Victoria, and conference participants at

the 2012 and 2013 NBER Conferences on Changing Financing Market for Innovation and

Entrepreneurship (Boston, MA and Half Moon Bay, CA) and the 2013 Conference of the Canadian

Council for Small Business and Entrepreneurship, and the First European Workshop on

Entrepreneurship Economics (2013, CEPR, Amsterdam). A special thank you goes to Dylan Callow,

Aydin Culhaci, Arif Khimani, Karen Robinson-Rafuse for their immense energy in helping us with

the data and managing teams of students at the University of British Columbia and the University of

Victoria. Hellmann and Schure are grateful for the financial support of the Social Sciences and

Humanities Research Council (SSHRC). Schure thanks the Netherlands Institute of Advanced Studies

in the Humanities and Social Sciences (NIAS) for their generous support and facilities during his

fellowship in fall 2014. All errors are ours. Updated versions are available at

http://www.sbs.ox.ac.uk/community/people/thomas-hellmann.

* Corresponding author.

Electronic copy available at: http://ssrn.com/abstract=2602739

2

1. INTRODUCTION

Equity financing of entrepreneurial start-ups has traditionally been equated with venture

capital (VC henceforth), but the importance of angel investors is increasingly recognized. An

OECD report from 2011 notes that “While VC tends to attract the bulk of the attention from

policy makers, the primary source of external seed and early-stage equity financing in many

countries is angel financing not VC” (OECD 2011, p.10). This same report estimates that the

total angel market is approximately the same size as the VC market, an estimate in line with

earlier studies (e.g. Mason and Harrison, 2002; Sohl, 2003).

How does angel financing interact with VC financing? Two opposing points of view

seem to have emerged among practitioners. The first view sees angels and VCs as synergistic

members of a common financing ecosystem. They have different skills and networks, not to

mention different levels of amounts to invest. Companies benefit from the combination of

these attributes. Marc Andreessen, venture capitalist and founder of Netscape, for example

notes that “[…] to get the best introductions to the A stage venture firms is to work through

the seed investors […]” (Sanghvi, 2014). A common view is that angel financing is a

“stepping stone” to obtaining venture capital. Benjamin and Margulis (2000) note: “Angel

investment runs the critical first leg of the relay race, passing the baton to VC only after a

company has begun to find its stride.” The examples of Google and Facebook powerfully

illustrate this stepping stone logic.

The second view sees angels and VCs as alternative financing modes that do not mix

well. They are competing approaches for financing companies, where companies that obtain

funding from one type of investor are more likely to stick to that investor type. This could be

because certain company attributes lend themselves to one type of financing, and/or because

investors guide their companies towards staying within their investor type. Michael

Arrington, founder of Tech Crunch, notes in a blog entitled “VCs and Super Angels: The War

3

For The Entrepreneur”: “Pick the wrong investor and you’ve closed the door on others.

You’ll never even know why it happened, but it will.” (Arrington, 2010)

In this paper we empirically examine the relationship between angel investors and

venture capitalists (VCs). Our research question concerns the dynamic investment pattern of

start-ups, and we ask whether companies that obtained angel financing are subsequently more

or less likely to obtain VC funding, and vice versa. We specifically test the “complements

hypothesis”, which suggests positive dynamic interactions between angel and VC financing,

against the “substitutes hypothesis”, which suggests a negative dynamic relationship.

The biggest obstacle to researching angel investments has been access to credible and

systematic data. We collect data related to a government program in British Columbia,

Canada (BC), where tax credits are available not only to VC firms but also to angel investors

(Government of British Columbia, 2014; Hellmann and Schure, 2010). The regulatory filings

under BC’s Investment Capital Program offer a unique opportunity to obtain systematic and

detailed data on both angel and VC investments. A useful feature of this dataset is the

availability of documents that list all the companies’ shareholders over time, which allows us

to construct detailed and comprehensive financing histories of start-ups. Our data includes

469 starts-up that were funded over the period 1995-2009.

Our analysis utilizes the dynamics in the data, asking specifically how prior

investments relate to subsequent investment choices. Our regressions contain a rich set of

controls, including company characteristics and a variety of time clocks. First, we find strong

evidence for dynamic persistence within investor types. A company that already obtained

funding from one particular type of investor is likely to raise more funding from investors of

the same type. This effect is not driven by repeat investments of existing investors, which are

deliberately removed from the analysis. Second, we find significant negative dynamic effects

between angel and VC financing. Companies that obtained more angel financing in the past

4

are less likely to subsequently obtain VC funding; and vice versa. These main findings are

robust to multiple model specifications.

The observed pattern of dynamic substitutes could be due to selection or treatment

effects, both of which have interesting economic interpretations. We think of selection effects

as a manifestation of a “company-led logic”, where companies have unobservable

characteristics that make them better suited for one type of investor over the other. We think

of treatment effects as a manifestation of an “investor-led logic”, where investors influence

companies raising more funding from their own type. To empirically separate selection and

treatment explanations we exploit exogenous variation in the tax credit program that affects

the relative availability of angel and VC financing. Our IV estimations suggest that both

company-led and investor-led effects contribute to the dynamic substitutes pattern.

Specifically, we find that exogenous increases in the availability of angel financing lead to

less subsequent VC financing. However, exogenous increases in the availability of VC

financing do not lead to less subsequent angel financing.

A potential concern about the substitutes pattern we find is that it is generated by poorly

performing companies that initially raise angel financing, and then continue to rely on further

angel financing, because they are not good enough to ‘graduate’ to the VC stage. Under this

view the stepping stone logic only applies to the best companies (the ‘Googles and

Facebooks’), and not the potentially much larger set of struggling companies. To empirically

test this more refined version of the stepping stone hypothesis we examine how the dynamic

substitutes pattern varies with company performance. Measuring performance in private

companies is always challenging. We follow the prior literature by focusing on exit

outcomes, that is, whether companies eventually had a successful exit (IPO or acquisition),

stayed alive, or failed (e.g. Phalippou and Gottschalg, 2009). We find that VC funding is

associated with better exit outcomes. However, the negative effect between angels and VC

5

funding does not change across the three performance categories, which is inconsistent with

the stepping stone hypothesis and its refined version.

A unique strength of our data is that it allows us to distinguish between different types

of angels. We classify angels into three types, ‘casual angels’ who only invest in a single

company; ‘serial angels’ who invest in multiple companies and are likely to be more

committed to angel investing; and ‘angel funds’ that combine the funding of multiple angels

into an investment vehicle. We find that the negative interaction pattern between angels and

VCs applies to casual angels and angel funds, but not to serial angels. This suggests, first of

all, that heterogeneity within the angel community matters, and, secondly, that serial angels

are less disconnected from the VC community than other types of angels.

The academic literature on angel financing remains underdeveloped. The paper closest

to our is Goldfarb et al. (2012), who make use of a unique dataset from a bankrupt law firm

that contained term sheets from client firms, some of which obtained angel and/or VC

financing. They show that VCs obtain more aggressive control rights than angel investors.1

They find a negative performance effect of mixing angel and VC funding, and argue that this

is driven by split control rights, where neither angels nor VCs have firm control over the

companies’ board of directors. Our analysis complements the work of Goldfarb et al. (2012)

in several important ways. For each company they only have a single snapshot of one

financing round and therefore mainly consider syndicated investment where angels and VCs

invest in the same round.2 We examine the full dynamic relationship between angel and VC

funding. We also exploit exogenous variation in tax credits to address identification issues,

and we are able to make finer distinctions amongst different types of angel investors.

1 This finding is consistent with what we know about VCs (e.g. Kaplan and Strömberg, 2003) and other research

on angel investors (Van Osnabrugge and Robinson (2000) and Wong (2010)).

2 Interestingly, our data also suggests that syndicated angel-VC investments are somewhat rare. In our sample

only 7% of all financing rounds involve syndication between angels and VCs.

6

Kerr et al. (2014) examine data from two angel funds that keep track of which

companies presented in front of the group, and which companies actually received funding.

Using a regression discontinuity approach, they find evidence that obtaining angel funding

affects the companies’ growth and survival rates. While they have more detailed evidence on

the investment decisions of angel investors, they can only look at a specific part of the angel

community, namely those associated with angel networks. They also do not consider the

interrelationships between angels and VCs. In a related vein, Bernstein, Korteweg and Law

(2014) perform some randomized online experiments on Angellist, an electronic investment

platform, showing that inexperienced angel investors react differently to information than

more experienced angel investors.

Hellmann and Thiele (2014) provide a theory that explicitly models the interaction

between angels and VCs. In their model companies want to proceed from angel to VC

funding. VCs may use their market power to squeeze out angel investors, which in turn

encourages angels to seek out alternative exit routes. A key insight from the theory is that the

bargaining dynamics between angels and VCs may determine whether the relationship is one

of complements or substitutes.

Two more papers provide further useful theoretical foundations for comparing angels

and VCs. Chemmanur and Chen (2006) assume that VCs add value but angels do not. Their

model explains why entrepreneurs might want to first obtain angel financing before switching

to VC. Schwienbacher (2009) assume that both angels and VCs can add value, but that only

VCs have enough money to refinance a deal. Under his set-up, angels endogenously provide

more value-adding effort, because of the need to attract outside capital at the later stage.

The VC literature is much larger than that on angel investors. Da Rin, Hellmann and

Puri (2012) provide a comprehensive survey of that literature. Closest to this paper are the

literatures on staged financing (Gompers, 1995; Tian, 2011) and independent versus

7

corporate venture capital (Chemmanur, Loutskina and Tian, 2014; Fulghieri and Sevilir,

2009; Hellmann, Lindsey and Puri, 2008). Furthermore, our work is related to Ozmel,

Robinson and Stuart (2013), who examine the dynamic interactions between VC financing

and strategic alliances.

The remainder of this paper is structured as follows. Section 2 discusses data sources

and variable definitions. Section 3 examines the main model of the dynamic financing

patterns across different investor types. Section 4 examines several empirical extensions. It is

followed by a brief conclusion.

2. DATA AND VARIABLES

2.1. Data sources

Our primary data source is the Government of British Columbia, who administers the British

Columbia Investment Capital Program (henceforth BCICP). The core of the program is a

30% tax credit for direct or indirect investments in eligible BC entrepreneurial companies

(details in the next subsection). Our analysis hinges on a unique feature of the BCICP that

this 30% tax credit applies to investments by both angel investors and venture capitalists.

Sandler (2004) shows that most North-American public policy initiatives target formal

venture capital, rather than the angel segment of the market.

Our BCICP dataset contains detailed company and investment activity information. Of

particular importance for our analysis are the companies’ share registries, which contain the

entire history of the individual share purchases in the company. The share registry data

contains both investments supported by the BCICP and those that are not.

We augmented the BCICP data using several additional data sources. First, these

sources helped us classify investors into types. Investors do not only include angels and

venture capitalists, but also other financial parties, corporations, and smaller groups such as

universities, charitable organizations, etc. Details will be given later on. Secondly, as we are

8

interested in how companies evolve and perform after their initial registration with the

program, we collected company exit and survival data from several additional data sources:

the BC company registry; the federal company registry (“Corporations Canada”); Capital IQ;

ThomsonOne (VentureXpert, SDC Global New Issues and SDC Mergers and Acquisitions);

Bureau Van Dijk (a data provider that collects private company data – for Canada, the main

source of the Bureau Van Dijk data comes from Dunn and Bradstreet); SEDAR, which

contains the record of filings with the Canadian Securities Administrators of public

companies and investment funds; EDGAR (filings with the SEC); and the Internet (using

mostly Google searches and an internet archive called the Wayback Machine

(http://archive.org/web).

2.2. The British Columbia Investment Capital Program (BCICP)3

The core of the BCICP was established in 1985 under the Small Business Venture Capital

Act of British Columbia. By the end of our sample period in 2009, the BCICP has four

segments that all offer a 30% tax credit for BC investors that invest in eligible entrepreneurial

companies. Eligible companies are BC-based companies that, at the moment of registration

and together with affiliate companies, if any, no more than 100 employees; pay at least 75%

of the wages and salaries to BC employees; and operate in an eligible industry.

Two segments of the BCICP primarily target angel investors. The first consists of tax

credits for investments in funds called VCCs, for Venture Capital Corporations, as the

program requires the investment vehicles to be structured as corporations.4 VCCs can only

invest in eligible small businesses and can only raise money from BC-based “eligible

3 Section contains a selective summary of the program. Further detail can be found in Hellmann and Schure

(2010), Lerner et al. (2012), and Government of British Columbia (2014).

4 The name ‘Venture Capital Corporation’ is slightly misleading, as these funds are not open to institutional

investors, but instead are only meant for private individuals. Consequently they should be thought of as angel funds. Note, however, that there are also different types of VCCs that are explicitly structured as venture capital funds for retail investors. As discussed below, we classified those as (government) venture capital funds.

9

investors”. For individual investors this means they need to satisfy some qualified investor

criterion (based on wealth, earnings, or “sophistication”), or else demonstrate to have a prior

acquaintance with the VCC fund managers (either based on a family relationship or

professional contacts.)

The second segment of the program is called the EBC program which was introduced

in 2003. It consists of tax credits for direct investments of BC-based eligible investors into

entrepreneurial companies called Eligible Business Corporations. This program is

administratively much simpler for angels than the VCC program since there is no need to set

up an investment vehicle. Indeed, the EBC program was intended to reach out to a wider set

of angels. Eligible investors, including angels, can simply claim the 30% tax credit on the

basis of an investment in an EBC.

The other two segments of the BCICP promote venture capital investments made by

what we call retail funds. The two retail fund programs are very similar. Retail funds have the

permission to approach investors from the general public. Individual investors receive again a

30% tax credit for investments into retail funds. The retail funds have an obligation to invest

the funds they attract within a specific time frame. The two retail fund programs differ in how

they are funded. In the so-called Labour-sponsored venture capital program, the BC and

federal governments equally share the costs, while in the so-called provincial retail venture

capital program the BC Government fully funds the tax credits.

2.3. Companies and investment rounds

Our analysis focuses on the time period of Jan 1995 to March 2009 and we have information

on all companies that registered under the BCICP in this period. Given our interest in

dynamic investment patterns we use financing rounds as our fundamental unit of analysis.

Below we first describe how we obtained our investment transactions and how we define

10

what constitutes a financing round. We will then present some descriptive statistics on the

company sample.

There are three sources for our transactions data. Our most important source is the

collection of share registries that give the histories of all share purchases in the company.

These transactions include investments supported by the BCICP, but also many non-BCICP

supported ones. We often have complete transaction data for the share-registry data (date,

type of share, investor, quantity, price), although at times we miss share prices. The other

sources for our transactions are the BCICP database and Venture Xpert, which we use to

augment the share-registry data in case they cover additional time periods not covered by the

share registries. For the BCICP database we have full transaction data if investments are

made by individual investors, and we have invested amounts in case investments are made by

vehicles (VCCs).5 Transactions found in Venture Xpert can cover both BCICP and non-

BCICP supported investments by mainly venture capitalists. For the Venture Xpert data we

only observe the identity of the investor and the invested amount.

As part of compensation, founders and other company insiders sometimes receive the

opportunity to purchase shares in their companies at deeply discounted values (“sweat

equity”). Investors can also buy shares at discounted prices, possibly because they may have

acquired warrants. Our analysis aims to detect the dynamic logic behind investments in

companies, rather than compensation issues. We therefore remove all sweat equity

transactions. Specifically, we remove all transactions in which shares were acquired for $0.01

or less, as well as those for which we observed the shares were acquired for 10% or less of

the share price paid by other investors in the same round.

5 For investments that are only covered by the BCICP database we miss out on investments made by out-of

province investors as well as BC investors that do not take advantage of the tax credits, either because they don’t want them, or because they already received tax credit up the maximum allowance under the program.

11

We assume that all investments made in the same quarter are part of the same financing

round. When companies raise funds during a time span that crosses two or more quarter

boundaries, we adopted the following rule regarding the definition and timing of the

financing round. The time-stamp on a round is the quarter in which the first of a series of

investments takes place. Subsequent investments are considered to be part of the same round

if they take place within ninety days of a prior one.

Our empirical analysis focuses on investment dynamics, so we require a company to

receive a minimum of two financing rounds. The procedure described above yielded 18,925

investments made by 9424 unique investors in 469 companies. The investments comprise

2168 financing rounds. All 469 companies attracted at least some funds supported by the

BCICP in one of their financing rounds.

2.4. Investors

There is no universally accepted definition for what exactly an angel investor is, and how it is

different from VC.6 Conceptually we adopt the following approach: an angel investor invests

his/her own (family’s) wealth, whereas a VC invests on behalf of other fund providers. This

definition is based on a fundamental economic distinction between direct versus

intermediated financing. From a theoretical point of view, one would expect that investors

investing their own money face different incentives and constraints than investors who are

intermediaries that act on behalf of others.7 In the data we have one interesting borderline

case, namely “angel funds”. They are normally thought of as a form of angel investing,

because they aggregate the monies of private individuals. However, they also involve some

financial intermediation, in the sense they delegate the investment functions of screening

projects and negotiating terms to a small management team of lead angels. In our data the

6 This is further discussed also OECD (2011) and Goldfarb, Hoberg, Kirsch, and Triantis (2012)

7 See also Diamond (1984) and Axelson, Strömberg and Weisbach (2009).

12

funding and management structures of these angel funds are clearly distinct from those of

venture capital funds, making the empirical distinction easy. We also adhere to the received

wisdom of classifying angel funds under the angel category. Beyond angel investors and

VCs, we also identify a variety of other investors in our data set, most notably corporations

(including institutions), as well as company founders and their families.

Too classify our 9,424 investors into investor types we adopted a two-step approach. In

step 1 we separated investors into two groups, namely humans (7,823 investors) and vehicles

(1,601). Human investors are identified by having only a first and last name (i.e. there are no

additions like “Inc.”, “Company”, “Trust”, etc); vehicle investors are the remaining ones. In

Step 2 we performed several name-based matches with other data sources to classify the

investors into several investor type categories. Our principal categorization distinguishes

Angels, VCs, and Other Investors. In the tables of the paper we abbreviate these investors

types as AN, VC, and OI, respectively. For some of the analysis in this paper we use a more

granular categorization. Specifically, we subdivide the angel investor category into three

types, namely casual angels who in our dataset invest in just a single company, albeit

possibly in multiple rounds (“AN - CASU” in our tables); ‘serial’ angels who in our dataset

invest in more than one company (“AN – SERI”); and ‘angel funds’, representing investment

vehicles that are owned by more than one angel (“AN – FUND”). We subcategorize VCs into

Private VCs (“VC – PRIV”) and Government VCs (“VC – GOVT”). Finally, the Other

Investors are a diverse group, consisting on the one hand of founders, key company

employees and their family members (“OI – FOFA”), and on the other hand a wide variety of

corporate entities (“OI – CORP”). Appendix A describes the details of Step 2, in which we

mapped human and vehicle investors into the investor categories.

2.5. Descriptive statistics

13

The variable description for all tables is provided in Table 1. Table 2 reports descriptive

statistics at the financing round level (Panels A-C) and the company level (Panel D). Panel A

shows that of the 2,184 financing rounds 1,491 involved one or more angels, 690 one or more

VCs, and 798 one or more Other Investors. Panel A further provides information of the sector

and region of the companies that received the funding in the rounds. We obtained this table

after manually classifying our 469 companies into industries. Our industry classification

focuses on innovative companies and is loosely based on NAICS codes. We obtained the

information on the companies’ activities from their business plans, their BCICP registration

applications, as well as internet searches. We observe that most of the BCICP companies are

active in the software industry (30%), Hi-tech manufacturing (18%) or biotech (14%). Taken

together, high-tech companies account for 80% of the companies in our data, while the other

20% of companies focus on Art, Recreation and Tourism (“Tourism”) or Agriculture,

Forestry, Fishery, Mining, Construction, or Non-high-tech manufacturing (designated for

export) (“Other”). These last two categories are eligible under the BCICP because they are

also deemed to further its main objective, namely to “enhance and diversify the BC

economy” (Government of British Columbia, 2014).

Company location is usually available through the BCICP data (from business plans,

the registration application, and/or annual filings) and we used internet searches for the

occasional company for which these documents failed us (e.g. because they reported the

accountant’s address). Our companies are concentrated in and around Vancouver – 73% of

them are located in the Greater Vancouver Regional District.8 The two smaller hubs for

innovative activities are BC’s Capital Region District (“Greater Victoria”, so to speak), and,

in the East of BC, the adjacent areas of the Okanagan and the Thompson River Valley.

8 For simplicity we also include in our GVRD definition nine companies that were located in the “Lower

Mainland”, which is the valley extending inland from Vancouver.

14

Panel B shows that the average company is 2.4 years old at the time of their first

financing round and 4.9 years old across all rounds.9 Company age for rounds in which at

least one angel (VC, Other Investor) invested is found in the second (third, fourth) column.

These age statistics are roughly similar to the all-round numbers. Panels B also provides

descriptive statistics on round amounts. For example, the all-rounds column shows that

angels, VCs, and Other Investors invested $240,000, $1,080,000 and $210,000 in an average

round in our dataset. This made the round amount close to $1.5M. The next three numbers

show that the vast majority of the dollars invested were from investors which had not

invested in any previous round. The second (third, fourth) column shows these per-round

funding averages across rounds where at least one one angel (VC, Other Investor) invested.

What stands out from these numbers is the not so surprising fact that VCs injected very

substantial amounts in the rounds in which they were active. They are by far the largest

investor category in our data, investing more than four times the amount that the more

numerous angel investors invested. The data show that co-investments happen in substantial

amounts. For example, in rounds in which at least one VC is active, angels and Other

Investors still invest on average $220,000 and $300,000 respectively.

Panel C provides data on the company’s exit status in May 2014. Using SDC Mergers

and Acquisitions, SEDAR, CapitalIQ, LexisNexis and internet searches we checked whether

companies were involved in IPOs or acquisitions. We also consulted the BC and Canadian

corporate registries to learn the status of the remaining companies. The corporate registries

are quite reliable as companies are required to submit documentation annually. Panel C of

Table 2 shows that 17% of the companies in our dataset had exited through either an IPO or

an acquisition and 35% of the them had failed. The remaining 48% of the companies in our

dataset were still active by May 2014.

9 We observe companies’ financing history for an average of 3.8 years after their first round. Companies are

hence on average 2.4+3.8=6.2 years old at the time of the last financing round we observe.

15

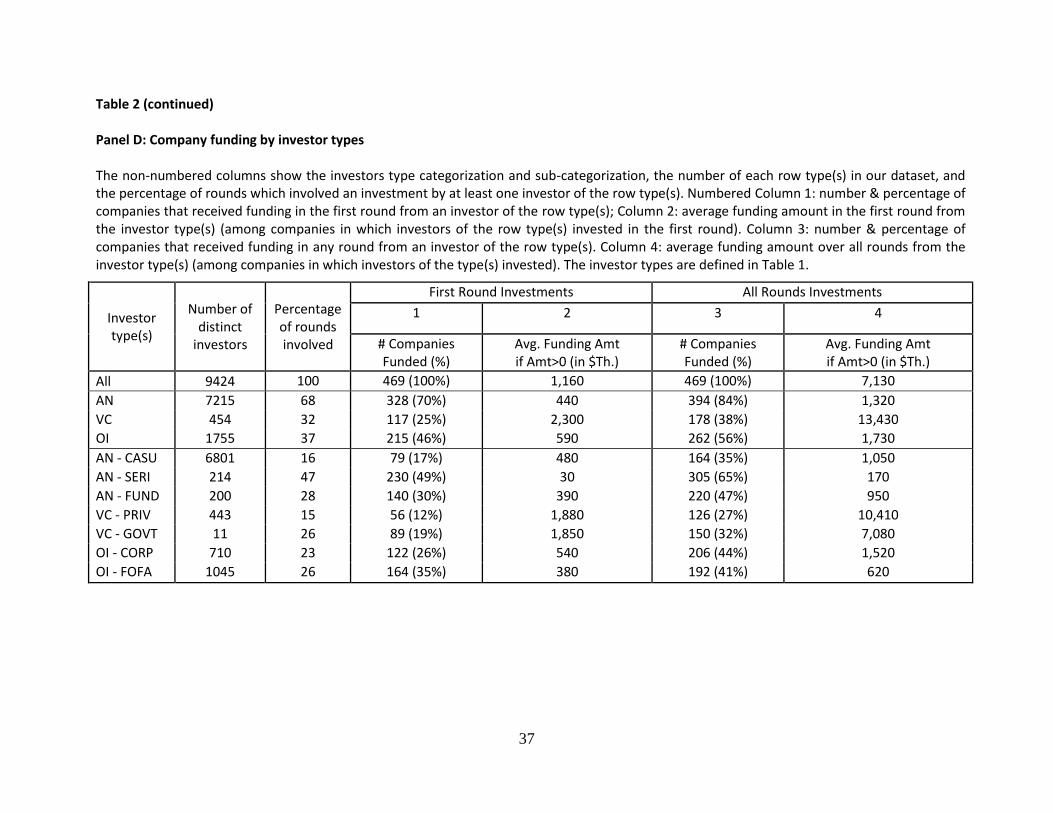

Panel D shows data about the investor type categorization in the three non-numbered

columns, and draws the link between investor types and funding at the company level in

Columns 1-5. The investor type categorization shows that our 9,424 unique investors consist

of 7215 Angels, 454 VCs and 1755 Other Investors. It also shows the numbers for the

subcategories, where it stands out that the bulk of the angels in our dataset are casual angels

that invest in just a single company. The third non-numbered column shows the percentage of

rounds in which at least one investor of the investor type is involved. We see that 68% of the

investment rounds involve at least one Angel Investor, 32% of the rounds one or more VCs,

and 37% of the round at least one Other Investor.

Columns 1 and 2 of Panel D reflect the first financing round of our 469 companies. We

note that 70% of the first rounds involved one or more angels, compared to 25% and 46% for

VCs and Other Investors. However, in Column 2 it becomes clear that if VCs were involved

in the first round, then they bring in an amount of $2.3M per company, much more than

Angels ($440,000) and Other Investors ($590,000). Our sub-categorization numbers show,

perhaps somewhat surprisingly, that despite their vast number, casual angels are involved in

the first rounds of merely 17% of the 469 companies, a substantially lower percentage than

for the serial angels (49%) and the angel funds (30%).

Columns 3 and 4 show the number of companies and amounts when aggregating over

all the investment rounds. Per-company average investment amounts were $7.13M. The data

confirms what we saw at the first-round level. The per-company average funding from VCs

($13.43M) is much higher than the corresponding amounts from Angels ($1.32M) and Other

Investors ($1.73M).

3. DYNAMIC FUNDING PATTERNS

3.1. Empirical specification

16

Our study of the dynamics of funding focuses on the relationship between the amount

companies receive in the current round, and the funding amount received in all rounds prior

to the current round. Thus, our unit of observation is the financing round (denoted by the

subscript r), and we follow our sample companies from their first to their last investment.

Clearly in the first financing round of a company (r=1) the prior amount received is not

meaningfully defined, so that our sample effectively begins with the second round.

Our main regression model is as follows:

Jikr = α+ βk Iik,r-1 + γ Xi + δ Xir + ηt + εikr

The dependent variable, Jikr, is the amount of funding that a company i obtains from

new investors of type k, in round r. We deliberately exclude from Jikr any funding received

from investors who already invested in a prior round. This is because we believe that our

results on the dynamic investment pattern of companies are most convincing when focusing

only on amounts invested by new investors. Existing investors who may decide to make

follow-on investments face a different decision problem than new investors. Observe also

that our regression specification does not reflect a single equation, but rather of a collection

of k equations. At the highest level of aggregation we consider the case of k=3, for Angel

investors, VCs and other investors. For example, in our main table, Table 3, Columns 1-3

reflect dollar amounts from new angel investors (AN), VCs (VC) and other investors (OI),

respectively. Column 4 considers the total funding amounts by new investors in the current

round. In section 4.3 we also consider specifications with higher values of k, disaggregating

the investor categories.

The most important independent variables are Iik,r-1, which measure the cumulative

amount of funding that company i received from investors of type k, up to round r-1. For this

we use the total amount of funding received from both new and existing investors.

17

In terms of controls, Xi is the set of variables that measure all time-invariant company

characteristics, namely: company age at the time of the first round, industry and location. We

report those controls in Table 3, but omit them in all subsequent tables to save space.

Moreover, Xir is a set of variables that measure all time-variant company characteristics.

These include (i) the amount raised in the previous round, (ii) the time since the first round

(measured non-parametrically with a complete set of dummies for each quarter, starting with

the quarter when the first round occurs), (iii) the time since the last round (measured non-

parametrically with a complete set of dummies for each quarter, restarting the counter every

time a new round occurs), and (iv) a dummy control for whether the round data was obtained

from the company’s share registry (dummy = 1) or from the BCICP database and Venture

Xpert (dummy = 0). Our non-parametric time-controls are included to capture possible

independent time-varying factors, allowing us to isolate the relationship between prior and

current funding choices.10

Finally ηt are a complete set of calendar-time fixed effects. These

control for any seasonal effects, any business cycles effects, or indeed any other calendar

time effects. All our regression models use these controls, but for the sake of brevity they

remain unreported in the results tables.

Throughout the paper we use OLS regressions with robust standard errors, clustered at

the company level, and we denote these by εikr. Of course we recognize the possibility that

unobserved heterogeneity creates a possible correlation between the error term and the

dependent variable, which is commonly referred to as an endogeneity problem. In section 3.2

we first report the results without any endogeneity correction. Section 3.3 then explicitly

focuses on issue of unobserved heterogeneity.

10

Note that our specification implicitly takes care of company age, since we control for both the age at the time of first round, and a clock for time since the first round. Using a clock for company age, instead of a clock for the time since the first round, yields very similar results.

18

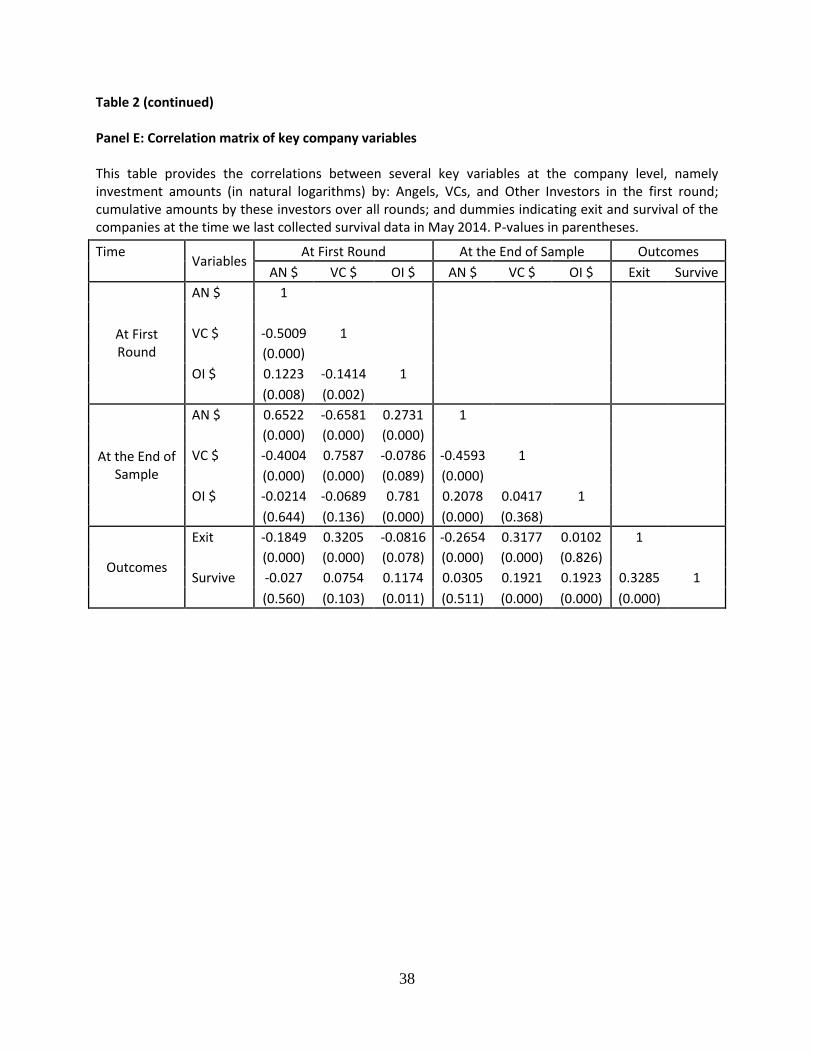

Panel E of table 2 reports pairwise correlation coefficients between some of the main

variables of interest at the company level. Foreshadowing the regression analysis we find

negative correlations between the various measures of angel and venture capital funding.

3.2. Results from the base model

Table 3 shows the estimation results of our base model. Columns 1-3 report the main results

concerning the relationships between investor types. We first note that the coefficients on the

main diagonal (i.e., the effect of prior financing by type k on current financing by type k) are

always positive and strongly significant at the 1% level. This suggests that companies that

have already received funding from one type of investor are likely to receive further funding

from that same investor type. Importantly, this result is not driven by repeat investors, since

our dependent variable only measures investments from new investors.

Probably the most important finding concerns the negative relationship between angel

and VC funding. If a company received more prior VC funding, it will raise less angel

funding. Conversely, if company received more prior angel funding, it will raise less VC

funding. Both these off-diagonal coefficients are statistically significant at the 1% level. This

finding suggests the existence of a separate angel and VC “tracks” in the financial ecosystem.

It is consistent with a dynamic financing pattern of ‘substitutes’ not ‘complements’.

Column 4 examines the relationship between prior funding and all new current funding.

It shows that more prior VC funding is associated with more total new funding, but that more

prior angel funding (as well as prior funding from other investors) is associated with less total

new funding. Table 3 also shows that more prior OI funding is associated with less current

VC funding, and more prior AN funding is associated with less current OI funding. Finally,

Table 3 shows some interesting and intuitive patterns for the control variables. For example,

there is less VC funding outside of the main urban centres of BC, and in certain industries

19

such as high tech services or tourism. We also find that larger prior round amounts predict

less new angel, but more new VC funding, which is in tune with the results from column 4.

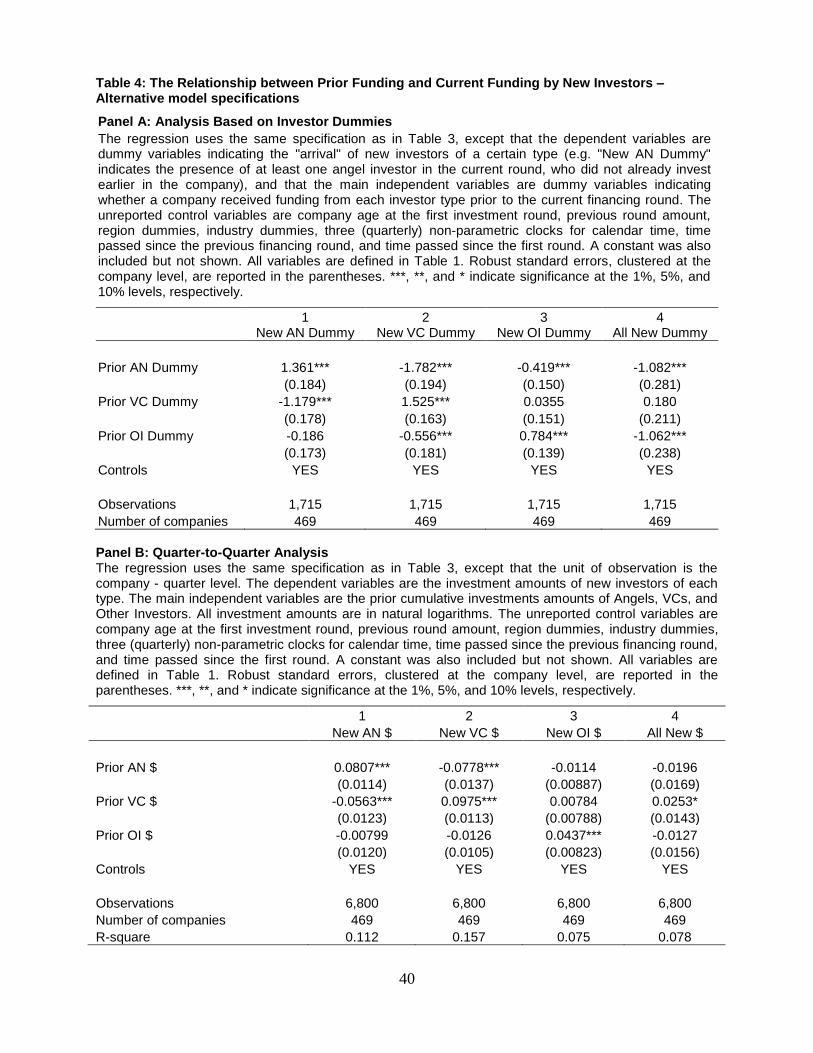

We considered many permutations of the base model, and report two of the most

important ones in Table 4. First, in Table 3 the focus is on funding amounts, but we may also

be interested in the mere presence or absence of certain investor types. Such estimates are

similar in spirit to estimating transition probabilities. Panel A of Table 4 therefore estimates

the same model as Table 3, but replaces investment amounts with dummy variables

indicating presence of investor types, both for the dependent and independent variables. The

pattern of results is very similar to that of Table 3, thus indicating that the main results about

investment amounts also carry over to the presence or absence of investor types.

Second, our basic unit of analysis of investment rounds implicitly requires a company

to be raising some funding. We may also ask whether the prior presence of investors

influences the likelihood of raising new money in the first place. We therefore consider a

time-based unit of observation that also allows us to observe the absence of financing rounds.

Specifically, in Panel B of Table 4 we re-estimate the base model using company-quarters as

our unit of analysis. Note this gives us many more observations, namely the quarters in which

companies did not raise funding. Nevertheless, while some of the results for other investors

now become insignificant, our core results about the substitutes patterns between angel and

VC financing remain significant at the 1% level.11

3.3. Unobserved heterogeneity

We may ask to what extent the results so far are driven by unobserved heterogeneity. In the

introduction we mentioned two alternative explanations for a substitution pattern. One is a

company-based ‘selection logic’ where there are unobserved company characteristics that

11

As a robustness check we also reran the regression models from Table 3 and 4 using as a dependent variable the total investment amount, instead of just using the investment amounts of new investors. The results were very similar, suggesting that the inclusion of old investor amounts does not affect our main insights.

20

affect matches between companies and investors. The other is an investor-based ‘treatment

logic’ where existing investors influence the subsequent choice of investor types. We believe

that both selection and treatment constitute interesting and economically meaningful findings,

and point out that the two effects may also coexist.

The empirical challenge is to find some exogenous variation in the data that separates

these two effects. We first note that it would not be enough to consider shocks to the overall

funding availability in the market, because our research question pertains to choices across

different investors within the market. Instead we need to look for exogenous shifts in the

relative availability of alternative financing types. In an ideal scenario the government would

have differentially changed the rates at which tax credits are made available to angels and VC

investments. Unfortunately for us the rate remained fixed at 30% over time for all investors.

However, the provincial government did shift substantial amounts of tax credits across the

different program segments over the years. A noteworthy example is the introduction of the

EBC program in 2003 (see Section 2.2). We thus take an instrumental variable specification

that exploits the historic variation in the amounts of tax credit across different program

segments.

As described in Section 2.2, the BC tax credit program consists of the EBC, VCC and

Retail fund segments. The EBC segment focuses on individual angel investors, which we

abbreviate by ANI. The VCC segment focuses on angel funds, and we use the abbreviation

ANF. The Retail fund segment targets venture capital. For each of these program categories,

RVC, ANF and ANI, we observe the annual amount of tax credits disbursed.

The variable that we want to instrument for is the prior cumulative amount of funding

obtained from a particular investor type. The idea for the instrument is that the prior amount

in companies is influenced by the past availability of tax credits. Since this effect occurs over

time, we use a weighted average of our tax credits measure. Because the relevant time

21

periods are those when the company was actually fundraising, we use the company’s relative

investment amounts as weights.

Conceptually our instrument has strengths and weaknesses. It has clear theoretical

foundations, since differential access to tax credits should clearly have a direct effect on the

amount of funding provided by the alternative investor types. Empirically we benefit from the

fact that the BC tax credit involves considerable variation in the relative availability of angel

versus VC financing.

One possible concern is that the variation in the program budgets is not entirely

random. Indeed, budget changes are likely to be driven by local political considerations.

However, what matters for econometric identification is only that the variation in budget

changes is independent of companies’ expectations of future financing sources. Our

identification strategy would only be problematic if government would allocate tax credits

with an explicit intent on influencing not the current funding environment, but the future

funding possibilities that result from today’s funding choices. We submit that such foresight

would seem highly improbable, and that policies only react to current and past funding

conditions, which is consistent with our instrumentation strategy.

One potential weakness of our approach is that we can only measure the amount of tax

credit actually used by market participants. This measure is jointly determined by the amount

of tax credit offered under program, as well as the amount of tax credits that investors ask for

based on their investment decisions. Our measure may therefore incorporate not only the

supply shock that can be directly traced back to the tax credit policy, but also a broader

supply shock for the market availability of each type of financing. Following the seminal

work of Berger et al. (2005), measures of market availability are commonly used as

instruments in the corporate finance literature. This means that, even though our measure

22

combines two types of supply shocks, both of them are suitable for identifying exogenous

changes in the availability of investments across different investor types.

Panel A of Table 5 reports a typical first-stage regression, which gives an idea of the

strength of our instrument.12

It shows that an increase in the tax credits in the RVC program

is associated with significantly more VC funding, and significantly less Angel and Other

Investor funding. More tax credits in the ANF or ANI budgets, by contrast, are associated

with significantly higher Angel investments. More ANF funding is also associated with lower

VC investment amounts. To assess to overall strength of our instruments in Panel A, we

perform an F-test for the joint significance of the instruments. The instruments are jointly

significant at the 1% level for Column 1 (Angels) and Column 2 (VCs). Interestingly, they

are insignificant for Column 3 (Other Investors), which is consistent with the fact that many

of these Other Investors are not eligible for tax credits.

Panel B shows the results of the second stage regressions. The evidence suggests the

presence of both selection and treatment effects. First note that the coefficients on the main

diagonal are all smaller, and all insignificant. This suggests that there are unobserved

company characteristics that make different companies more suitable to match with different

investor types. It explains why companies repeatedly return to the same type of investor, even

when raising money from new investors. Secondly note that the coefficient for the effect of

prior VC funding on angel financing is now negative but insignificant. The economic

interpretation is that randomly adding more venture capital funding does not affect the

(already low) probability of companies returning to the angel market. Third, we find that the

effect of prior angel funding on VC remains significant and negative. This suggests that in

addition to the company-led (selection) effects, there also are some investor-led (treatment)

effects. Specifically, if a company was exposed to a positive supply shock of angel funding in

12

We report the first-stage regression for the estimation of the current angel amounts, but the results are very similar for the regressions for the VC and Other Investor amounts.

23

the past, then the company becomes less likely to raise VC financing. This finding is

consistent with the notion that angels can guide companies away from VC funding.

4. EXTENSIONS

4.1. Does the stepping stone hypothesis still apply to the best companies?

In this section we consider several extensions of the main empirical analysis. We begin by

examining whether the substitutes patterns observed in section 3 can be explained by

company performance. One might argue that the reason why many companies fail to progress

from angel financing to VC is that their underlying performance doesn’t warrant it. Put

differently, the stepping stone logic would argue that only the best companies ‘graduate’ from

angel funding to VC funding, and that the remaining ones are stuck with angels. To

empirically evaluate this possibility we ask whether the negative relationship between angel

and VC funding holds true across the performance spectrum.

An empirical challenge is that performance is hard to observe in privately-held

companies. Within our data constraints the most credible proxy for performance is the

realization of final outcomes. While this proxy does not reflect the evolution of performance

over time, it classifies companies into three distinct categories: those that ultimately

experienced a successful exit event, as measured by an acquisition or IPO; those that are still

alive by the end of the sample period; and those companies that failed.

A necessary requirement for the stepping stone hypothesis is that VCs invest in

companies that are more likely to exit. But this is not enough: under the stepping stone

hypothesis the observed negative relationship between prior angel and current VC funding

has to also turn positive for those companies that are more likely to have a successful exit.

We test both of these conditions.

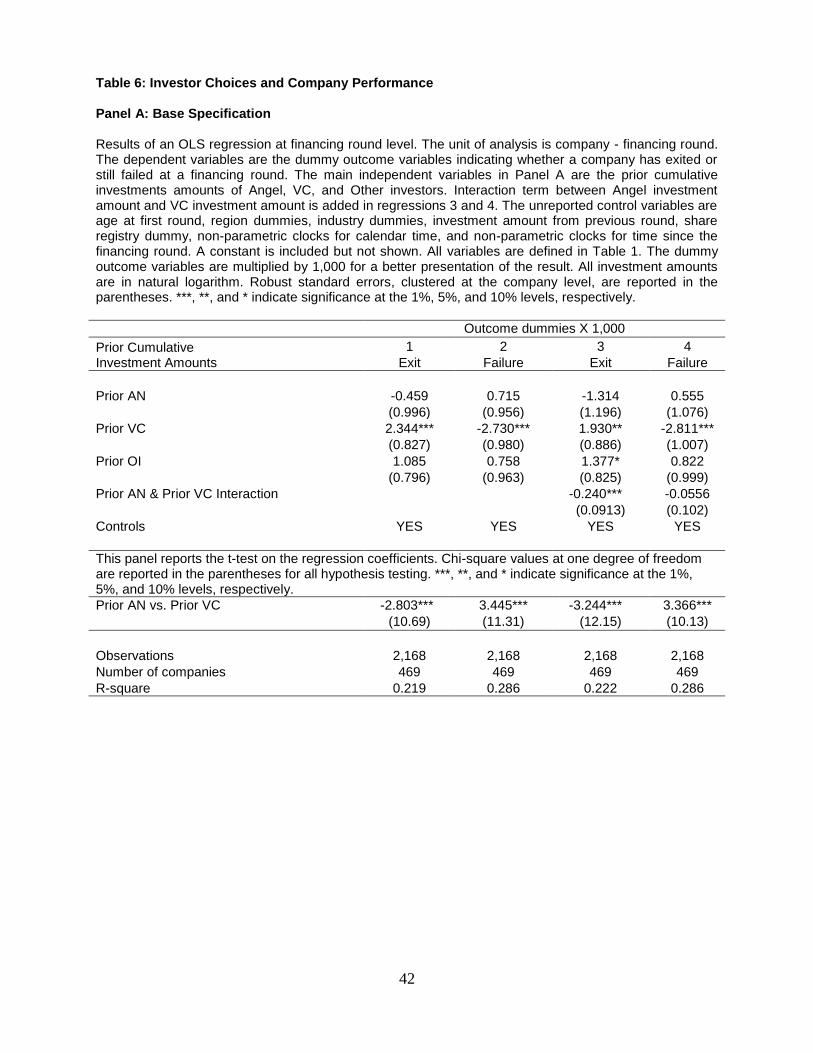

To test the necessary condition that VCs invest in better companies, we regress final

outcomes on prior funding types. As before, our unit of analysis is the investment round, but

24

we augment the sample with one round that captures the final outcome. Panel A of Table 6

reports the results from linear probability models for Exit and Failure, where the independent

variables are the same as in our main model (Table 3).13

In Column 1, the dependent variable

measures whether or not the company experienced a successful exit, in Column 2 the

dependent variable measures whether the company failed or not. The central findings are that

VC financing is associated with more exits, and fewer failures. Neither the amount of funding

from angel investors, nor from other investors, is significantly correlated with exits or

failures. These findings are consistent with prior research on VC (see Da Rin, Hellmann and

Puri 2012). In columns 3 and 4 we add an interaction term between the amounts of VC and

angel financing. We find that this does not affect the main coefficients of interest. As for the

interaction term, we note that it is negative and significant at 1% for exits, and insignificant

for failures. This result is broadly consistent with the analysis of Goldfarb et al. (2012), who

find that VCs tend to do best when investing on their own.

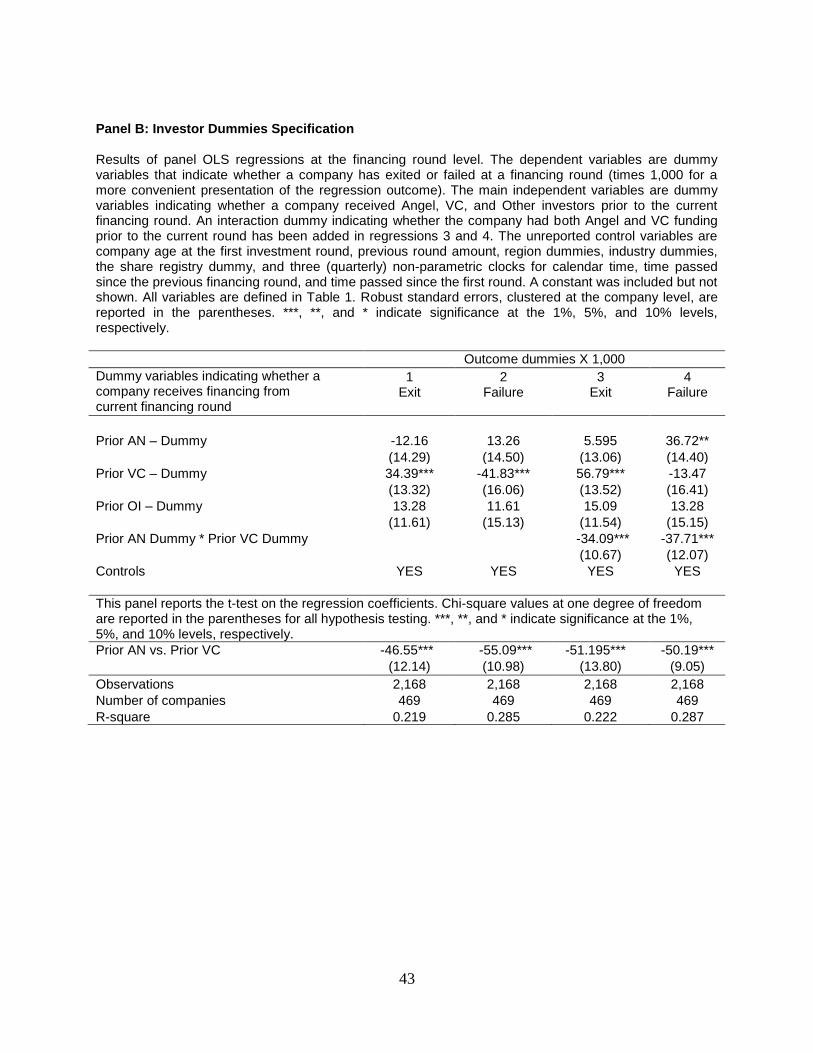

Panel B of Table 6 uses a similar structure as Panel A, but instead of using the

continuous amount variables for the three investor types, we now use the categorical

variables which measure the presence or absence of an investor type (previously used in

Table 4A). We find very similar results for columns (1) – (3). In column (4) we also find that

companies funded only by angels have a higher failure rate, but this does not apply to those

that also attract VC.14

15

13

We refrain from using non-linear Probit or Logit models, because the large number of fixed effects in our specifications creates an incidental parameter problem (see Angrist and Pischke, 2009).

14 Specifically, we find a positive and significant coefficient for the presence of angels, a negative and

insignificant coefficient for the presence of VC, and a negative and significant coefficient for the presence of both angels and VCs. We note that the positive coefficient for the interaction effect is of a very similar magnitude as the negative coefficient for the angel dummy.

15 In addition to running a round-to-exit panel model, we also considered a simple cross-section, where the

dependent variable is simply the final company outcome (exit, alive or failed), and where the independent variable of interest is either the cumulative investment amount of the different investor types at the end of the sample (cf. Table 6A); or the presence or absence of the different investor types at the end of the sample (Table 6B). The results were in line with those of Table 6.

25

Let us collect the insights from both panels of Table 6. First, the results from columns

(1) and (2) suggest that VC backed companies do achieve better outcomes, which is

necessary for the stepping stone hypothesis. Second, the results from both columns (3) shed

some doubt on the stepping stone hypothesis, as they show that the most successful

companies do not mix angel and VC funding. Finally, the results from both columns (4) are

mixed. While there is some evidence in Panel B (but not in Panel A) that mixing of angel and

VC funding might be associated with better outcomes, this only occurs for poorly performing

companies, and not for the best companies, as conjectured by the stepping stone hypothesis.

The results from Table 6 only measure correlation, and make no claims about the

direction of causality. A large prior literature tries to disentangle selection and treatment

effect for the effect of investors on performance (see Da Rin et al. 2012 for a detailed

discussion). While not central to the analysis of the stepping stone hypothesis, we nonetheless

reran the regressions of Table 6 using an instrumentation strategy based on the analysis of

Table 5. In unreported regressions we found that none of the investor type coefficients are

statistically significant. This suggests that selection effects explain most for the relationship

between investor types and performance.

Next we consider the second condition of the stepping stone hypothesis, namely that

the observed negative relationship between prior angel and current VC funding applies to

poorly performing, but not to high-performing companies. Table 7 examines how the

dynamic relationship between angels and VCs differs across the performance range. We

interact our investor type variables with two sets of dummy variables that measure eventual

company outcomes. The first four columns of Table 7 report the same regressions as in Table

3, yet augmented by controls for Exit and Failure. They show that the main coefficients are

very similar to before. The last four columns of Table 7 then report the interaction effects of

financing type with eventual company outcomes. We find that almost all interaction

26

coefficients are statistically insignificant.16

Most importantly, we do not find that the negative

relationship between prior angel funding and current VC funding is weaker for companies

that eventually have a successful exit. This finding is inconsistent with the central argument

of the stepping stone hypothesis.

4.2. Do funding needs affect transitions across investor types?

The analysis of section 4.1 suggests that the negative dynamic relationship between angel and

VC funding applies across the performance range. In this section we ask how it might vary

across the range of funding needs. This question is motivated by Table 2 which shows that

VC rounds tend to be considerably larger than angel rounds. Our simple conjectures are that

(i) the negative relationship of going from angel to VC funding should weaken for larger

deals, and that (ii) the negative relationship of going from VC to angel funding should

weaken for small deals. These conjectures are driven by the basic observation that angels

tend to invest smaller amounts than VCs. In fact, the most relevant empirical question is

maybe not whether these conjectures are true, but whether the substitutes pattern survives

after controlling for these portfolio size effects.

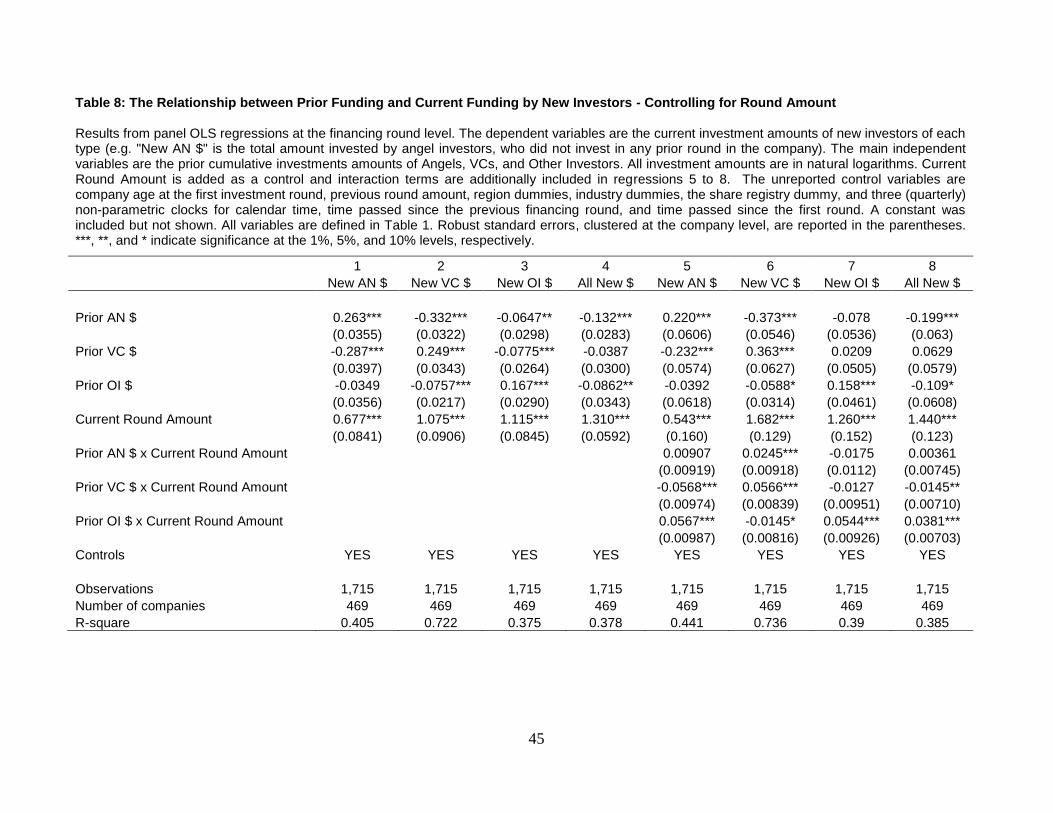

Table 8 reports results from a regression that is similar to Table 7, but in which we

interact the investor type variables with the amount of funding raised in the current round.

The main finding is that the conjectures above are strongly confirmed in the data. In Column

2 we find that the negative effect of prior angel financing on VC is attenuated in larger

rounds. The interaction effect is positive and significant at the 1% level. Moreover, in

Column 1 we find that the negative effect of prior VC financing on angels is stronger in

larger rounds. The interaction effect is negative and significant at the 1% level. We also find

16

The only significant interaction effects occur for exited companies on the main diagonal. Specifically, angel backed companies that eventually exit, are more likely to continue raising more angel investing. The same is true for other investors, but not for VCs.

27

that the persistence of investor types for VCs and Other Investors is stronger in larger deals,

as reflected by the positive and significant interaction effects on the main diagonal.

The finding that larger round size attenuates the negative effect of angel funding on

VC, but accentuates the negative effect of VC on angel funding, is reassuring. It confirms that

the dynamic funding relationship is affected by important economic variables, such as the

financing needs of the company at the time of financing. Yet, probably the most important

finding is that the basic substitutes patterns between angel and VC financing is unaffected

after controlling for these portfolio size effects. Indeed, both the size and the statistical

significance of the main coefficients are hardly affected by the additional controls.

4.3. Does the dynamic financing pattern vary across investor subtypes?

Our analysis so far uses aggregate categories for angels, VC and other investor. In this

section we disaggregate those categories to obtain a deeper understanding of the

interrelationship between different investor types. The more granular categorization allows us

to (i) gauge the dynamic financing patterns within investor types, and to (ii) examine how

cross-investor effects vary by subcategories. Indeed, the biggest question is whether the

negative relationship between angels and VCs applies uniformly across angel types.

In section 2 we discussed our decomposition of angel investors into three types: casual

angels, serial angels, and angel funds. A natural interpretation is that serial angels are likely

to be more experienced and committed to angel investing in the long term than casual angels.

For example, it is likely that our casual angel category includes ‘friends’ who invest in a

single company on the basis of personal relationships, but have no intention to systematically

engage in angel investing. Angel funds may behave differently from both casual and serial

angels. Prowse (1998) distinguishes between “active” and “passive” angels within angel

funds. He argues that active angels are delegated monitors for the passive angels, and may

develop relevant skills and networks in this position. In addition we note that angel funds are

28

likely to have deeper pockets than individual angels, and may therefore become a viable

alternative to VC funding for companies that require large investment amounts.

The theoretical predictions as to the substitutes pattern between VCs and any of these

angel subcategories are often ambiguous. For example, on the one hand one may conjecture

that serial angels are a stronger substitute to VCs than casual angels because the former are

more willing to fund companies on their own. However, on the other hand, VCs may find it

easier to develop long-term relationships with the serial angels, which would suggest a

stronger substitutes pattern for the casual angels than for the angel funds. Similarly angel

funds may exhibit a relatively weak substitutes pattern with VCs as they appear to be the

most akin to VCs and should hence select into similar firms and/or be able to work together

productively. But angel funds may also exhibit strong substitutes patterns with VCs as they

may offer a viable alternative funding system due to their expertise and size.

Table 9 shows the results for decomposing investor types. Concerning relationships

within investor types we again note positive (and mostly significant) relationships on the

main diagonal. Consider next the interactions amongst different types of angel investors,

shown in columns 1-3. We find a two-way negative relationship between casual angels and

angel funds. We also find a positive and significant relationship between prior casual angel

funding and current serial angel funding. However, this effect goes only one way, i.e., there is

no effect between prior serial angel funding and current casual angel funding. Within the

venture capital subcategories we also find an interesting asymmetry, namely that prior

funding from private VCs is associated with greater current government VC funding

amounts, but not vice versa.

Turning next to the breakout across investor types, we find a negative effect of prior

angel financing on (both types of) VC for two out of three angel subcategories, namely casual

angels and angel funds. However, the coefficients for serial angels are insignificant (and even

29

have a positive sign). This suggests that serial angels stand less apart from the VC community

than casual angels or angel funds. Looking at the reverse relationship of prior VC on angel

investing we notice a somewhat similar pattern for government VCs: more prior government

VC funding predicts less current funding from casual angels and angel funds, but it has no

significant effect on current funding from serial angels. For private VCs, however, more prior

funding always predicts less angel funding, irrespective of the specific angel subcategory.

Finally, there are some interesting patterns between angels and Other Investors. Prior

funding from angel funds is negatively related to current funding from Other Investors. This

is not the case for prior funding from casual or serial angels. As for the breakout within Other

Investors, the most interesting result is that prior funding from corporations is associated with

greater private VC funding. Prior funding from founders and family is not associated with

greater private VC funding.

Overall we note that the analysis of subcategories reveals several interesting insights,

the most interesting one being that there are significant differences in the dynamic investment

patterns of casual angels, serial angels, and angel funds.

5. CONCLUSION

This paper examines the dynamic interactions between different types of investors, focusing

in particular on the interactions between angels and VCs. Using detailed data from British

Columbia, Canada, we find considerable support for the hypothesis that angel investors and

VCs are dynamic substitutes. Companies that obtain VC funding are less likely to obtain

subsequent angel funding, and vice versa. The results are robust across a wide range of

econometric specifications. The substitutes effect is stronger for casual angels and angel

funds than for serial angels.

Our analysis suggests several avenues for future research. First, a natural next step

would be to obtain a deeper understanding of the reasons behind the observed substitutes

30

pattern. Do angels and VCs have different networks? Do they have incompatible governance

systems? Or do disagreements about valuations drive the substitutes result? Second, while we

obtain unique data on angels and VCs in British Columbia, Canada, it would be interesting to

see to what extent the results continue to hold in other environments. For example, does the

substitutes result also hold in large start-up ecosystems such as Silicon Valley? And how

about in significantly less developed start-up ecosystems than British Columbia? Third, an

interesting line of research is to examine whether the substitutes pattern continues to apply

after recent developments in angel markets, most notably the rise of electronic investment

platforms, such as Angellist and equity crowdfunding platforms. Finally, there is an

important research agenda in understanding public policy implications. Government policies

traditionally focused on (formal) venture capital as the main path to improving the financing

environment of start-ups. Yet our central finding challenges that approach, suggesting that

government policies towards angel investors would reach a different set of entrepreneurial

companies that develop outside of the reach of venture capitalists.

31

REFERENCES.

Angrist, J. and J. Pischke. 2009. Mostly harmless econometrics. Princeton, NJ: Princeton

University Press.

Arrington, Michael. 2010. VCs and super angels: The war for the entrepreneur. Retrieved

from http://techcrunch.com/2010/08/15/venture-capital-super-angel-war-

entrepreneur/

Axelson, Ulf, Per Strömberg and Michael Weisbach. 2009. Why are buyouts leveraged? The

financial structure of private equity funds. Journal of Finance 64-4: 1549-1582.

Benjamin, G. A., & J. Margulis. 2001. The angel investor’s handbooks. How to profit from

early-stage investing. Princeton, NJ: Bloomberg Press.

Berger, A., N. Miller, M. Petersen, R. Rajan, and J. Stein. 2005. Does function follow

organizational form? Evidence from the lending practices of large and small banks.

Journal of Financial Economics 76: 237–269.

Bernstein, Shai, Arthur Korteweg, and Kevin Law. 2014. Attracting early stage investors:

Evidence from a randomized field experiment. Mimeo Stanford University.

Brander, James, Qianqian Du and Thomas Hellmann. 2013. The effects of government-

sponsored VC: international evidence. Working Paper, University of British

Columbia.

Chemmanur, T. and Z. Chen. 2006. VCs versus angels: the dynamics of private firm

financing contracts. Unpublished working paper.

Chemmanur, Thomas, Elena Loutskina and Xuan Tian. 2014. Corporate venture capital,

value creation, and innovation. Review of Financial Studies 27 (8): 2434-2473.

Da Rin, Marco, Thomas Hellmann and Manju Puri. 2012. A survey of VC research. In

Handbook of the Economics of Finance, Vol. 2, ed. George Constantinides, Milton

Harris, and René Stulz. Amsterdam, North Holland.

Diamond, Douglas. 1984. Financial intermediation and delegated monitoring. The Review of

Economic Studies 51: 393–414.

Fulghieri, Paolo and Merih Sevilir. 2009. Organization and financing of innovation, and the

choice between corporate and independent venture capital. Journal of Financial and

Quantitative Analysis 44 (n.6): 1291-1321.

Goldfarb, B., G. Hoberg, D. Kirsch and A. Triantis. 2012. Does angel participation matter?

An analysis of early venture financing. Unpublished working paper.

Gompers, Paul. 1995. Optimal investment, monitoring, and the staging of venture capital.

Journal of Finance 50: 1461-1489.

32

Government of British Columbia. 2014. Investment capital. Government of British Columbia,

Ministry of International Trade and Responsible for Asia Pacific Strategy and

Multiculturalism. Retrieved from http://www.mit.gov.bc.ca/icp/

Hellmann, T., L., Lindsey, and M. Puri. 2008. Building relationships early: banks in venture

capital. Review of Financial Studies 21, 513-541.

Hellmann, Thomas and Paul Schure. 2010. An evaluation of the VC program in British

Columbia. Report prepared for the BC Ministry of Small Business, Technology and

Economic Development.

Hellmann, Thomas and Veikko Thiele. 2014. Friends or foes? The interrelationship between

angel and venture capital markets". Journal of Financial Economics, forthcoming.

Kaplan, Steven and Per Strömberg. 2003. Financial contracting theory meets the real world:

Evidence from VC contracts. Review of Economic Studies 70, 281–315.

Kerr, W., J. Lerner, and A. Schoar. 2014. The consequences of entrepreneurial finance: a

regression discontinuity analysis. Review of Financial Studies, 27:1, 20-55.

Lerner, Josh, Thomas Hellmann and Ilkin Ilyaszade. 2012. Angels in British Columbia.

Harvard Business School Case Study 9 – 811 – 100.

Mason, Colin, and Richard Harrison. 2002. Barriers to investment in the informal VC sector.

Entrepreneurship and Regional Development 14 , 271-287.

OECD. 2011. Financing high-growth firms: The role of angel investors. OECD Publishing,

http://dx.doi.org/10.1787/9789264118782-en.

Ozmel, Umut, David T. Robinson and Toby Stuart. 2013. Strategic alliances, venture capital,

and the going public decision. Journal of Financial Economics 107(3): 655-670.

Phalippou, L. and O. Gottschalg. 2009. The performance of private equity funds. Review of

Financial Studies 22: 1747-1776.

Prowse, Stephen. 1998. Angel investors and the market for angel investments. Journal of

Banking & Finance 22: 785–792.

Sandler, Daniel. 2004. VC and tax incentives: A comparative study of Canada and the United

States. Toronto, ON: Canadian Tax Foundation.

Sanghvi, Rajen. 2014. 17 quotes from Marc Andreessen & Ron Conway on how to raise

money. From how to start a start-up – Lecture 9. Retrieved from

https://medium.com/how-to-start-a-startup/17-quotes-from-marc-andreessen-ron-

conway-on-how-to-raise-money-d0b710f115f1.

Schwienbacher, A. 2009. Financing commitments and investors incentives in entrepreneurial

firms. Unpublished working paper.

33

Sohl, Jeffrey E. 2003. The U.S. angel and VC Market: Recent trends and developments. The

Journal of Private Equity 6-2: 7-18.

Tian, Xuan. 2011. The causes and consequences of venture capital stage financing. Journal of

Financial Economics 101 (1): 132-159.

Van Osnabrugge, Mark and Robert J. Robinson. 2000. Angel investing: Matching start-up

funds with start-up companies. San Francisco, CA: Jossey-Bass.

Wong, Andrew. 2010. Angel finance: The other VC. In VC: Investment Strategies,

Structures, and Policies, ed. Douglas Cumming. Hoboken, NJ: John Wiley & Sons.

34

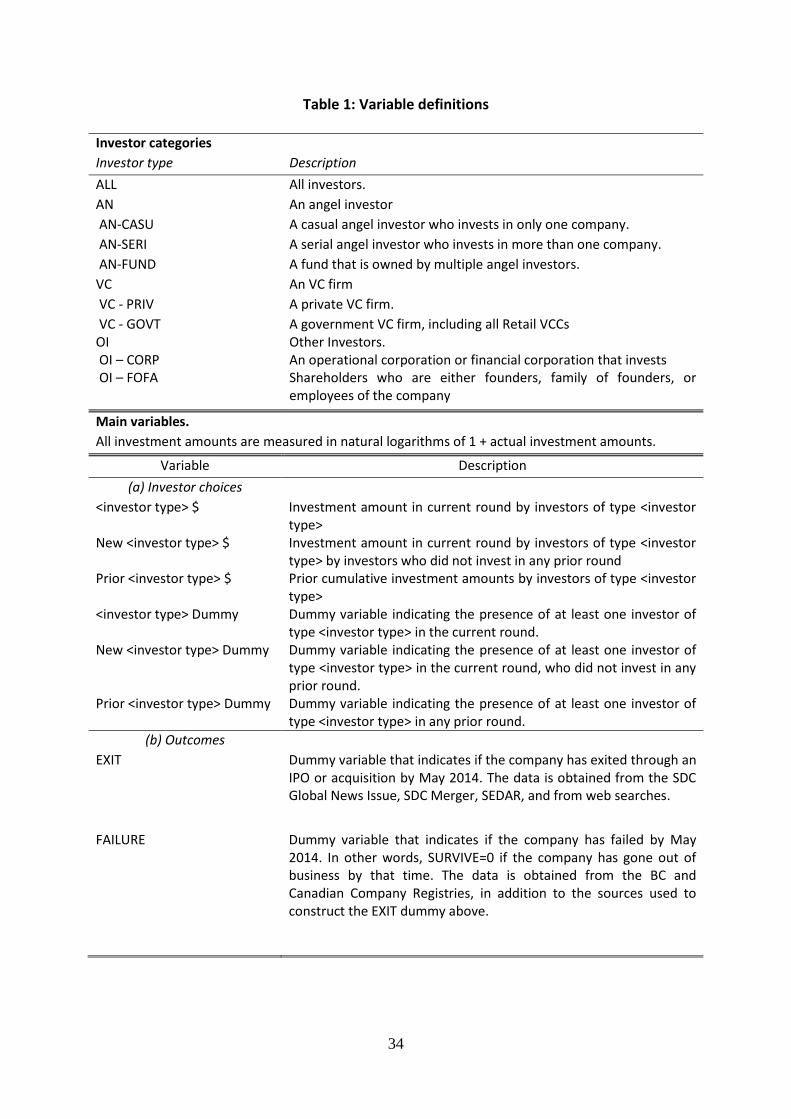

Table 1: Variable definitions

Investor categories

Investor type Description

ALL All investors.

AN An angel investor

AN-CASU A casual angel investor who invests in only one company.

AN-SERI A serial angel investor who invests in more than one company.

AN-FUND A fund that is owned by multiple angel investors.

VC An VC firm

VC - PRIV A private VC firm.

VC - GOVT A government VC firm, including all Retail VCCs OI OI – CORP

Other Investors. An operational corporation or financial corporation that invests

OI – FOFA Shareholders who are either founders, family of founders, or employees of the company

Main variables.

All investment amounts are measured in natural logarithms of 1 + actual investment amounts.

Variable Description

(a) Investor choices

<investor type> $ Investment amount in current round by investors of type <investor type>

New <investor type> $ Investment amount in current round by investors of type <investor type> by investors who did not invest in any prior round

Prior <investor type> $ Prior cumulative investment amounts by investors of type <investor type>

<investor type> Dummy Dummy variable indicating the presence of at least one investor of type <investor type> in the current round.

New <investor type> Dummy Dummy variable indicating the presence of at least one investor of type <investor type> in the current round, who did not invest in any prior round.

Prior <investor type> Dummy Dummy variable indicating the presence of at least one investor of type <investor type> in any prior round.

(b) Outcomes

EXIT Dummy variable that indicates if the company has exited through an IPO or acquisition by May 2014. The data is obtained from the SDC Global News Issue, SDC Merger, SEDAR, and from web searches.

FAILURE Dummy variable that indicates if the company has failed by May 2014. In other words, SURVIVE=0 if the company has gone out of business by that time. The data is obtained from the BC and Canadian Company Registries, in addition to the sources used to construct the EXIT dummy above.

35

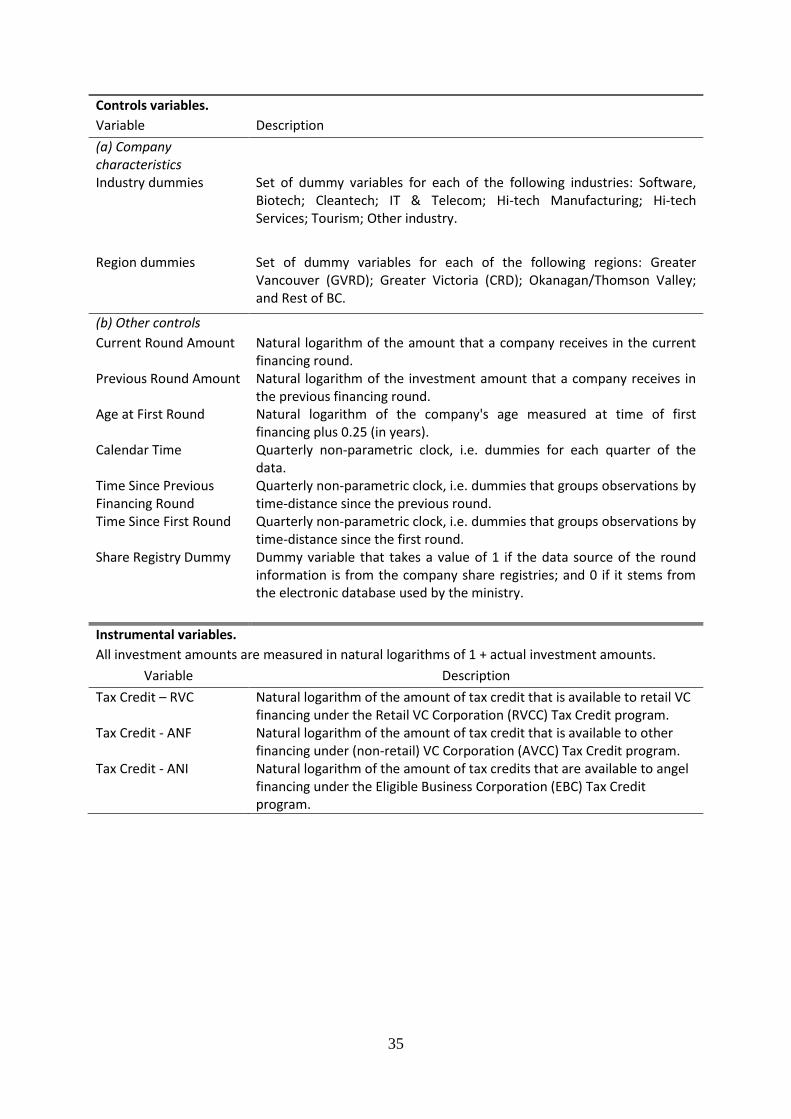

Controls variables.

Variable Description

(a) Company characteristics

Industry dummies Set of dummy variables for each of the following industries: Software, Biotech; Cleantech; IT & Telecom; Hi-tech Manufacturing; Hi-tech Services; Tourism; Other industry.

Region dummies Set of dummy variables for each of the following regions: Greater Vancouver (GVRD); Greater Victoria (CRD); Okanagan/Thomson Valley; and Rest of BC.

(b) Other controls

Current Round Amount Natural logarithm of the amount that a company receives in the current financing round.

Previous Round Amount Natural logarithm of the investment amount that a company receives in the previous financing round.

Age at First Round Natural logarithm of the company's age measured at time of first financing plus 0.25 (in years).

Calendar Time Quarterly non-parametric clock, i.e. dummies for each quarter of the data.

Time Since Previous Financing Round

Quarterly non-parametric clock, i.e. dummies that groups observations by time-distance since the previous round.

Time Since First Round Quarterly non-parametric clock, i.e. dummies that groups observations by time-distance since the first round.

Share Registry Dummy Dummy variable that takes a value of 1 if the data source of the round information is from the company share registries; and 0 if it stems from the electronic database used by the ministry.

Instrumental variables.

All investment amounts are measured in natural logarithms of 1 + actual investment amounts.

Variable Description

Tax Credit – RVC Natural logarithm of the amount of tax credit that is available to retail VC financing under the Retail VC Corporation (RVCC) Tax Credit program.

Tax Credit - ANF Natural logarithm of the amount of tax credit that is available to other financing under (non-retail) VC Corporation (AVCC) Tax Credit program.

Tax Credit - ANI Natural logarithm of the amount of tax credits that are available to angel financing under the Eligible Business Corporation (EBC) Tax Credit program.

36

Table 2: Descriptive Statistics

Panel A: Company sectors and regions GVRD = Greater Vancouver Region District. CRD = Capital Region District (Greater Victoria).

Variable All rounds (n=2,184 )

AN Rounds (n=1,491)

VC Rounds (n=690)

OI Rounds (n=798)

Industry (% of all rounds)

Software 30 28 34 35

Biotech 14 11 23 16

Cleantech 4 5 3 5

IT & Communication 7 5 9 6

Hi-tech Manufacturing 18 19 19 20

Hi-tech Service 6 7 3 5

Tourism 6 7 1 6

Other 14 17 7 8

Location (% of all rounds)

GVRD (Vancouver) 73 70 81 75

CRD (Victoria) 9 8 11 8

Okanagan & Thompson River 5 6 4 6

Rest of BC 12 16 4 12

Panel B: Company age and investment amounts

Variable All rounds (n=2,184 )

AN Rounds (n=1,491)

VC Rounds (n=690)

OI Rounds (n=798)

Company Age at 1st Round (yrs) 2.4 2.3 2.7 2.2