Embed Size (px)

Citation preview

WORLD ANTIMONY FORUM

ANTIMONY RESOURCES

IN AUSTRALIATSX // MND

Andre Booyzen, GM Australasian Operations,

Mandalay Resources

Changsha, China

May 20 – 21, 2015

2

1. Mandalay Resources

2. Antimony in Australia

3. Costerfield Mine

Antimony in Australia

This presentation contains "forward-looking statements" within the meaning of applicable securities laws, including statements relating to life of

mine production plans, exploration plans and the growth and strategy of Mandalay. Actual results and developments may differ materially from

those contemplated by these statements depending on, among other things: exploration results or production results not meeting management’s

expectations; capital, production and operating cost results not meeting current plans; and changes in commodity prices and general market and

economic conditions. The factors identified above are not intended to represent a complete list of the factors that could affect Mandalay. A

description of additional risks that could result in actual results and developments differing from those contemplated by forward looking

statements in this news release can be found under the heading “Risk Factors” in Mandalay’s annual information form dated March 31, 2015 and

in its final prospectus dated September 2, 2014, copies of which are available under Mandalay's profile at www.sedar.com. Although Mandalay

has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-

looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be

no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those

anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

Quality Control and AssuranceQuality control and assurance programs are implemented in line with the standards of National Instrument 43-101.

The exploration program at Costerfield is supervised by Chris Gregory (Member, Australian Institute of Geoscientists accredited Chartered

Professional (Mining)), General Manager of Australasian Business Development for Mandalay and a Qualified Person as defined under National

Instrument 43-101. Mr. Gregory regularly visits Costerfield, supervises the collection and interpretation of scientific and technical information

contained in this presentation.

The exploration programs on the Cerro Bayo project is supervised by Ronald Luethe (Member: American Institute of Professional Geologists and

an Idaho Registered Professional Geologist), General Manager of Mandalay Chile Ltda. and a Qualified Person as defined under National

Instrument 43-101. Mr. Luethe visits the Cerro Bayo project often, supervises the collection and interpretation of scientific and technical

information contained in this presentation.

Dr. Mark Sander (Member: AusIMM), President of Mandalay, has visited the Costerfield, Cerro Bayo, Challacollo, and Björkdal and has

supervised the preparation of this presentation.

All currency references in US$ unless otherwise indicated

Forward-looking Statements

3

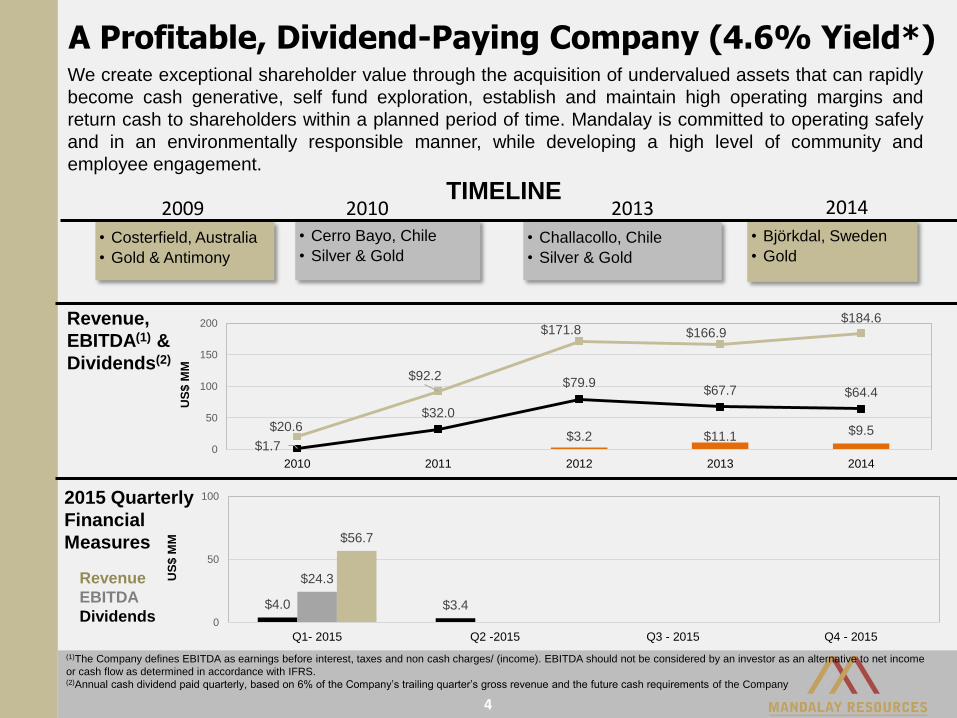

2009

• Costerfield, Australia

• Gold & Antimony

2010• Cerro Bayo, Chile

• Silver & Gold

2013

• Challacollo, Chile

• Silver & Gold

2014

• Björkdal, Sweden

• Gold

$3.2 $11.1 $9.5$20.6

$92.2

$171.8 $166.9$184.6

$1.7

$32.0

$79.9$67.7 $64.4

0

50

100

150

200

2010 2011 2012 2013 2014

US

$ M

M

A Profitable, Dividend-Paying Company (4.6% Yield*)

4

We create exceptional shareholder value through the acquisition of undervalued assets that can rapidly

become cash generative, self fund exploration, establish and maintain high operating margins and

return cash to shareholders within a planned period of time. Mandalay is committed to operating safely

and in an environmentally responsible manner, while developing a high level of community and

employee engagement.

(1)The Company defines EBITDA as earnings before interest, taxes and non cash charges/ (income). EBITDA should not be considered by an investor as an alternative to net income

or cash flow as determined in accordance with IFRS.(2)Annual cash dividend paid quarterly, based on 6% of the Company’s trailing quarter’s gross revenue and the future cash requirements of the Company

TIMELINE

2015 Quarterly

Financial

Measures

Revenue,

EBITDA(1) &

Dividends(2)

Revenue

EBITDA

Dividends$4.0 $3.4

$24.3

$56.7

0

50

100

Q1- 2015 Q2 -2015 Q3 - 2015 Q4 - 2015

US

$ M

M

5

Mining friendly operational jurisdictions with strong and diversified customer base

Operational Locations and Tradeflows

6

15,854 63,351

107,941 126,908

253,796

520,175 633,000

771,500

1,123,367

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

0

50,000

100,000

150,000

200,000

250,000

300,000

2010 2011 2012 2013 2014 2015

Oz A

u E

q.

Ye

ar-

En

d

Res

erv

es

Oz A

u E

q.

An

nu

al

P

rod

uc

tio

n

6

Reserves

Production

154,810

167,000 –

185,000 EGrowing Production and Reserves

Costerfield M&I Resource Additions & Depletion (Au Eq oz)

Bjorkdal M&I Resource Additions & Depletion (Au oz) Cerro Bayo M&I Resource Additions & Depletion (Ag oz)

Challacollo M&I Resource Additions & Depletion (Ag oz)

Financial Performance

7

Operational Performance

Q1, 2015 2014YE Q1, 2014 2013YE

Saleable Silver oz produced 590,755 3,329,519 743,569 3,145,537

Saleable Gold oz produced 27,740 77,900 13,105 50,240

Saleable Antimony t produced 969 3,639 858 3,275

Q1, 2015 2014YE Q1, 2014 2013YE

Net Cash/All-in cost/oz Ag at Cerro Bayo, $ 10.09 / 17.61 5.30 / 11.36 5.81 /11.31 6.84 / 12.07

Net Cash/All-in cost/oz Au Eq. at

Costerfield, $

566 / 744 771 / 1,035 800 / 1,052 819 / 1,062

Net Cash/All-in cost/oz Au Eq. at

Björkdal, $(1)

797 / 940 870 / 1,023 -(1) -(1)

EBITDA, $ million 24.3 64.4 16.0 67.7

Net Income, $ million 12.5 17.2 5.7 29.4

Cash and cash equiv., $ million 51.9 49.0 20.0 33.5

Q1 2015 Mandalay Performance

(1) Björkdal Acquired September 10, 2014

Site all-in costs include total cash operating costs, royalty expense, depletion, depreciation, accretion and write-off of exploration and evaluation.

8

Total Cerro Bayo Costerfield Björkdal

Saleable gold

production (oz)

101,000 – 116,000 23,000 – 27,000 32,000 – 37,000 46,000 – 52,000

Saleable silver

production (million oz)

2.7 – 3.1 2.7 – 3.1 -- --

Saleable antimony

production (t)

3,200 – 3,500 -- 3,200 – 3,500 --

Gold equivalent

production (oz)

167,000 – 185,000 -- -- --

Cash cost $/oz silver

net by-product

-- 6.00 – 8.00 -- --

Cash cost $/oz gold or

gold equivalent

-- -- 625 – 750 850 – 950

Capital expenditures

($ million)

38 – 44 12 – 14 16 – 18 10 – 12

Exploration ($ million) 7 3 1 3

Mandalay 2015 Full Year Production and Cost Guidance

9

1. Mandalay Resources

2. Antimony in Australia

3. Costerfield Mine

Antimony in Australia

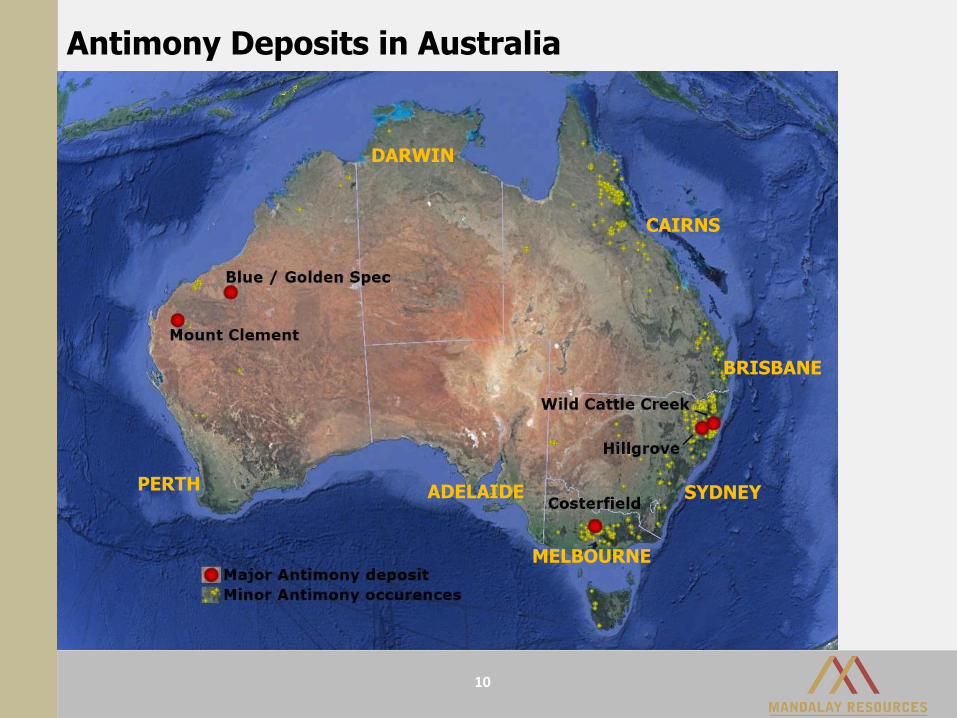

Antimony Deposits in Australia

MELBOURNE

PERTH SYDNEY

BRISBANE

DARWIN

CAIRNS

ADELAIDE

10

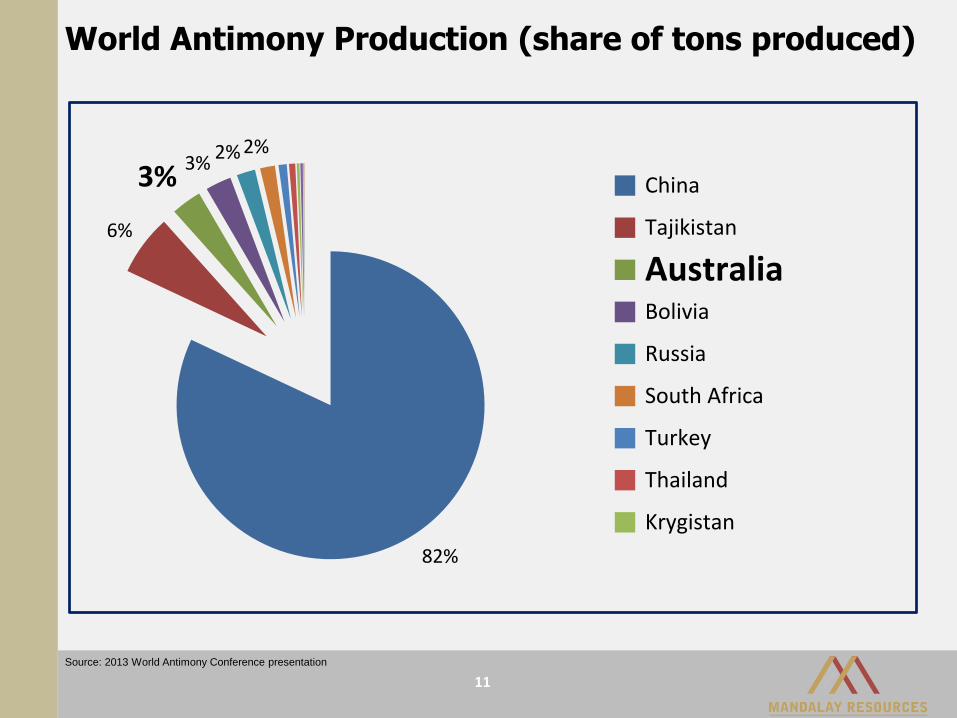

World Antimony Production (share of tons produced)

11

82%

6%

3%3%

2% 2%

China

Tajikistan

AustraliaBolivia

Russia

South Africa

Turkey

Thailand

Krygistan

Source: 2013 World Antimony Conference presentation

World Antimony Reserves (metal tonnes)

12

2,400,000

450,000

370,000

320,000

300,000

200,000

150,000

90,000 330,000China

Thailand

Russia

Bolivia

AustraliaSouth Africa

Tajikistan

USA

Other countries

Source: 2013 World Antimony Conference presentation

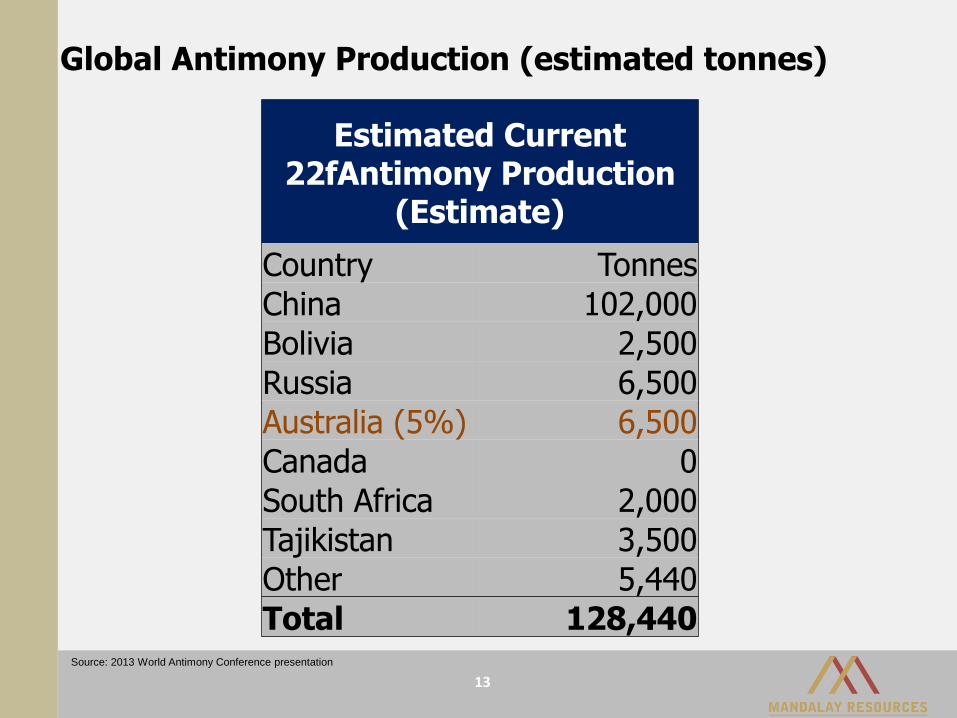

Global Antimony Production (estimated tonnes)

13

Estimated Current 22fAntimony Production

(Estimate)

Country Tonnes

China 102,000

Bolivia 2,500

Russia 6,500

Australia (5%) 6,500

Canada 0

South Africa 2,000

Tajikistan 3,500

Other 5,440

Total 128,440Source: 2013 World Antimony Conference presentation

Antimony Imports to China

14

Sb Ores/Concs Import (DMT) by China

2011 2012 2013 2014

Russia 10,702 18,851 20,761 16,055

Tajikistan 13,812 13,865 9,727 14,361

Australia (21%) 5,629 6,968 9,820 12,329

Myanmar 6,228 7,876 9,291 3,917

Kazakhstan 1,354 1,261 1,711 1,538

Bolivia 386 875 1,600 1,516

Thailand 7,989 6,059 5,238 1,490

Mexico 1,542 1,374 4 1,302

Laos 574 1,743 1,956 1,020

Peru 48 41 71 819

Zimbabwe 148 95 640 651

Turkey 0 0 646 611

Honduras 100 139 77 394

Iran 220 447 331 337

Kyrgyzstan 0 0 0 95

India 0 0 0 70

Morocco 22 0 0 69

Ecuador 0 0 0 23

South Africa 375 103 259 23

Indonesia 0 0 0 20

North Korea 22 40 50 10

Canada 9,574 6,811 1,237 0

Pakistan 58 516 1,004 0

Nigeria 0 0 72 0

Guatemala 0 0 18 0

Albania 0 956 0 0

Japan 128 43 0 0

Vietnam 1,012 515 0 0

Chile 39 0 0 0

TOTAL 59,961 68,580 64,515 56,649

Source: 2013 World Antimony Conference presentation

Antimony Resources in Australia

15

• Major deposits around Costerfield region. Long history of 150 years of

mining antimony.

• Deposits in Western Australia likely require substantially higher

antimony and/or gold prices.

• Hillgrove is understood to be ramping-up production, but not a public

company so current scale unconfirmed.

• Capital constraints exist for antimony exploration – funding today is

from active mine production.

• Unlikely to see new antimony ore producers from Australia in the near

future.

Costerfield is Australian antimony mining success story.

16

Future of Antimony Mining in Australia

17

1. Mandalay Resources

2. Antimony in Australia

3. Costerfield Mine

Antimony in Australia

Costerfield Gold-Antimony Mine: Overview

18

2015 Planned Exploration

Budget $1 million

Land package 1,293 hectares

Ownership 100%

2014 gold production 35,751 oz

2014 antimony production 3,639 t

2015E gold production 32,000 – 37,000 oz

2015E antimony production 3,200 – 3,500 t

P&P Reserves(1) 430,000 tonnes @ 8.1 g/t Au; 3.6% Sb

Current throughput 400 tpd

Plant recoveries (Q1 2015) Au: 89.9%, Sb: 95.0%

2015E Cash cost/oz Au Eq. / 2014A $625 - $750 / $771

(1) Refer to notes on reserves in the Appendix

Augusta Mine Site

19

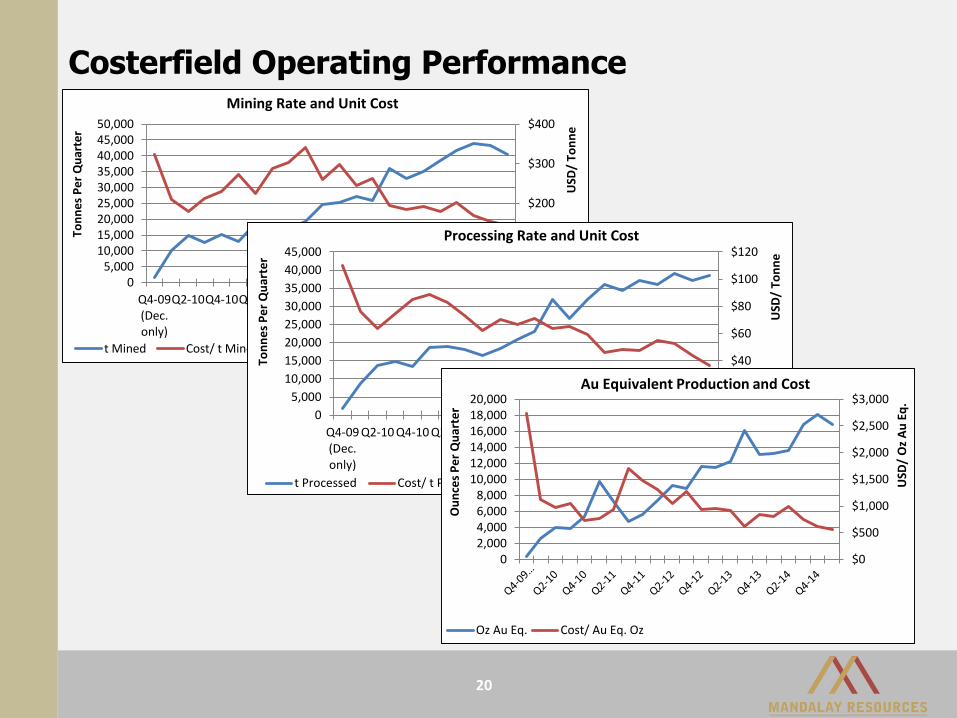

Costerfield Operating Performance

20

$0

$100

$200

$300

$400

05,000

10,00015,00020,00025,00030,00035,00040,00045,00050,000

Q4-09(Dec.only)

Q2-10Q4-10Q2-11Q4-11Q2-12Q4-12Q2-13Q4-13Q2-14Q4-14

USD

/ To

nn

e

Ton

nes

Pe

r Q

uar

ter

Mining Rate and Unit Cost

t Mined Cost/ t Mined

$0

$20

$40

$60

$80

$100

$120

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Q4-09(Dec.only)

Q2-10 Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-13 Q4-13 Q2-14 Q4-14

USD

/ To

nn

e

Ton

ne

s P

er

Qu

arte

r

Processing Rate and Unit Cost

t Processed Cost/ t Processed

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

USD

/ O

z A

u E

q.

Ou

nce

s P

er

Qu

arte

r

Au Equivalent Production and Cost

Oz Au Eq. Cost/ Au Eq. Oz

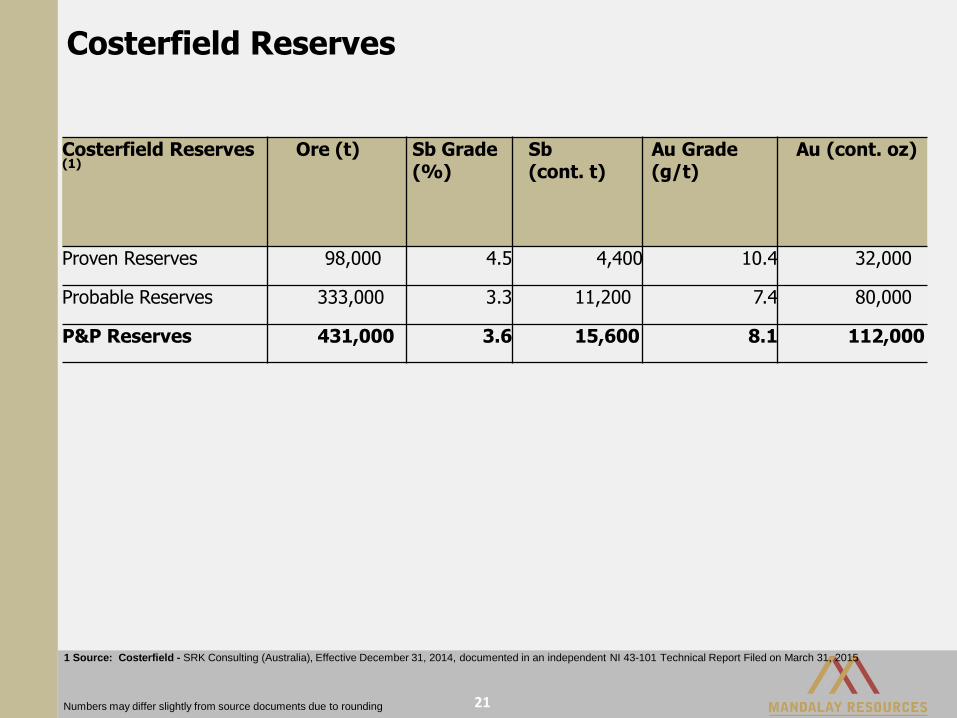

Numbers may differ slightly from source documents due to rounding 21

1 Source: Costerfield - SRK Consulting (Australia), Effective December 31, 2014, documented in an independent NI 43-101 Technical Report Filed on March 31, 2015

Costerfield Reserves(1)

Ore (t) Sb Grade(%)

Sb (cont. t)

Au Grade(g/t)

Au (cont. oz)

Proven Reserves 98,000 4.5 4,400 10.4 32,000

Probable Reserves 333,000 3.3 11,200 7.4 80,000

P&P Reserves 431,000 3.6 15,600 8.1 112,000

Costerfield Reserves

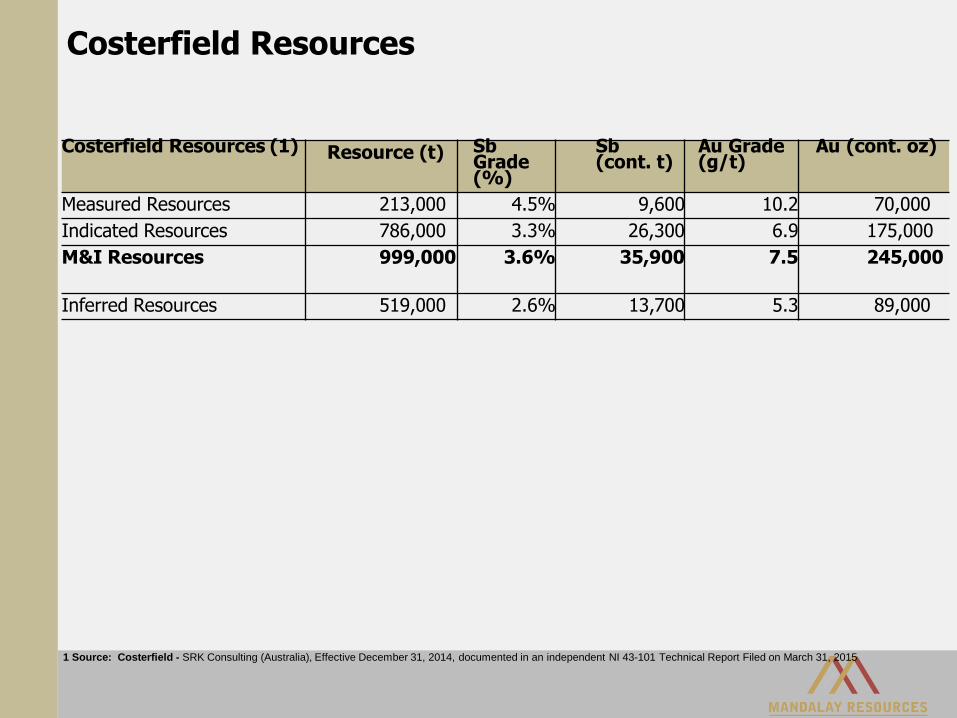

1 Source: Costerfield - SRK Consulting (Australia), Effective December 31, 2014, documented in an independent NI 43-101 Technical Report Filed on March 31, 2015

Costerfield Resources (1) Resource (t) Sb Grade (%)

Sb (cont. t)

Au Grade (g/t)

Au (cont. oz)

Measured Resources 213,000 4.5% 9,600 10.2 70,000

Indicated Resources 786,000 3.3% 26,300 6.9 175,000

M&I Resources 999,000 3.6% 35,900 7.5 245,000

Inferred Resources 519,000 2.6% 13,700 5.3 89,000

Costerfield Resources

Costerfield Operations

• Area first mined in mid-1800’s - Augusta Mine operating since 2005

• Employ almost 200 people – mostly from local area

• Has seen growth and prosperity in local area over the last 3 years

• Spend almost $60 million per annum in local economy

• Strong exploration & capital program to increase mine life

• Gold & antimony

• Ore widths average 300mm.

• Gold grades range from 8-20g/t

• Antimony grades range from 3-5% Sb.

• High confidence mine life of approximately four years

• Currently processing over 13,000 tonnes per month

• Cost reduction efforts paying off with less than $800/ Au Equivalent Ounce

23

Costerfield Challenges in 2010 – now overcome

• Safety was unacceptable

• Staff morale poor – ineffective workforce

• Land acquisition – infrastructure and water disposal challenging

• Lack of cash – not making money

• Political and regulatory support

• High and rising costs

• Skills shortage in many areas

• Ground conditions

• Specialised narrow vein mine – labour intensive

• Operating restrictions – noise and zero discharge

• Electrical power required for growth

• Inefficient operations

24

Highlights

25

• From 2010 to 2014 – Increases in:

• Saleable Sb tonnes produced from 1,106 to over 3,639

• Saleable Au oz. produced from 7,661 to 35,751

• Revenue from $22m to $78m

• Earnings (EBITDA) from $5.4m to $29m

• Capital spend from $2.8m to $7.8m

• Opex spend from $16.5m to $32m

• Safety - 80% improvement in safety – LTI and MTI

• Low staff turnover – from 72% per annum to less than 8%

• Culture of continuous improvement

• Incremental improvements across mining operations

• Empowered staff to realise cost savings in their own areas

• Improvement ongoing to drive bottom line and revenue growth

• Simple key indicators to manage the mine

• Management and supervisors enrolled in the culture

26

Mandalay Culture

Questions?

For more information, please contact:

Greg DiTomaso

Director, Investor Relations

Tel: 647.260.1566

Email: [email protected]

Company Website: www.mandalayresources.com

Twitter: @MandalayAuAg