Embed Size (px)

Citation preview

2012 Client Seminars

ANAO Client Webinar 16 March 2015 9:30-11:00 AM

Your presenter: Alastair Higham Senior Director Reporting Frameworks

2012 Client Seminars

Up and coming changes to

Accounting Standards

Agenda

Responses to Webinar Feedback Financial instruments Leases Revenue from contracts with customers Related parties Disclosure initiative Emerging trends in accounting standards

Responses to Webinar Feedback

Thank you for the feedback from the last ANAO Webinar – very encouraging.

Our response:

Slides focused on key points relevant to audience – give participants visual context and guidance.

Introduced “key points” slides prior to complex/ detailed issues to direct participants on where to focus in subsequent slides.

Purpose

Broad understanding of key elements, accounting principles and framework changes.

Opportunity for entities to consider systems issues, operational impact and options.

Foundation to start the conversation – auditors, staff, senior executives and audit committee.

We will revisit detailed application closer to implementation dates.

2012 Client Seminars

Financial Instruments “It is not life [simplification] as we know it or understand it.”

[Spock]

AASB 9 Financial Instruments

Applicable for annual reporting periods beginning on or after 1 January 2018.

Replaces AASB 139 Financial Instruments: Recognition and Measurement.

Associated amendments to AASB 7: Financial Instruments: Disclosures.

AASB 9 Financial Instruments

Brings together classification, measurement, impairment and hedge accounting.

Moves away from an “instrument” based approach.

2012 Client Seminars

What is the entity’s business model for managing financial assets?

How does the entity intend to obtain benefit from the financial asset (use cash flows / sale)?

Financial assets – key points

AASB 9 – Recognition of Financial Assets

Recognise when entity becomes party to the contractual provisions.

De-recognise when contractual rights to cash flows expire or transfer.

AASB 9 – Initial Recognition of Financial Assets

Initial recognition at fair value plus or minus transaction costs directly attributable.

If fair value differs from transaction price:

Quoted price in active market or valuation technique using only observable market data – difference recognised as gain or loss.

Otherwise defer difference.

AASB 9 – Subsequent Measurement of Financial Assets

Subsequent measurement of financial assets is based on:

The entity’s business model for managing the financial assets (collect cash flows, sale or mix), and

The financial asset’s contractual cash flow characteristics.

AASB 9 – Financial Asset Measurement Models

Financial assets to be measured at either:

Amortised cost

Fair value through OCI

Fair value through profit or loss, or

Can designate at fair value through OCI.

AASB 9 – Amortised Cost

Measured using amortised cost if:

Business model objective is to hold financial asset to collect contractual cash flows

Financial asset is managed and performance evaluated by KMP on a contractual yield basis, and

Contractual terms give rise on specified dates to cash flows that are solely payments of principal, and interest on outstanding principal.

AASB 9 – Fair Value through OCI

Measured using fair value through OCI if:

Business model objective is to both hold the financial asset to collect contractual cash flows and sell the financial asset, and

Contractual terms give rise on specified dates to cash flows that are solely payments of principal, and interest on principal amount outstanding.

AASB 9 – Fair Value through Profit or Loss

Measured using fair value through profit or loss when not at:

Amortised cost

Fair value through OCI, or

Designated at fair value through OCI.

2012 Client Seminars

Expected credit losses:

Separation of expected credit losses from other changes in value.

Expected credit loss is the change in credit risk from initial recognition.

Impairment – key points

AASB 9 – Impairment

At each reporting date assess:

Whether credit risk has increased significantly since initial recognition - probability-weighted amount (based on range of possible outcomes).

Must consider reasonable and supportable information that is available without undue cost or effort.

When information not available, entity may use past due information.

There is a rebuttable presumption that credit risk has increased significantly if 30 days past due.

AASB 9 – Simplified Impairment

Simplified approach available for:

Trade receivables and contract assets that result from transactions within scope of AASB 15 Revenue from Contracts with Customers, and

Lease receivables within scope of AASB 117 Leases.

Entity to measure expected credit loss allowance at an amount equal to lifetime expected credit losses.

Practical expedient – can use provision matrix to estimate expected lifetime expected credit losses.

AASB 9 – Write-offs

Directly reduce carrying amount where no reasonable expectation of recovering a financial asset (entirety or proportion).

There is a rebuttable presumption that entity’s should not set a default greater than 90 days without reasonable and supportable evidence for the alternative.

AASB 9 – Financial Liabilities

All financial liabilities to be measured at amortised cost using the effective interest method except for:

Financial liabilities designated at fair value through profit of loss

Financial liabilities that arise when a transfer of a financial asset does not qualify for de-recognition or when continuing involvement approach applies

Financial guarantee contracts, and

Commitments to provide a loan at below-market interest rate.

AASB 9 – Reclassification

Financial assets may be reclassified when an entity changes its business model.

Financial liabilities cannot be reclassified.

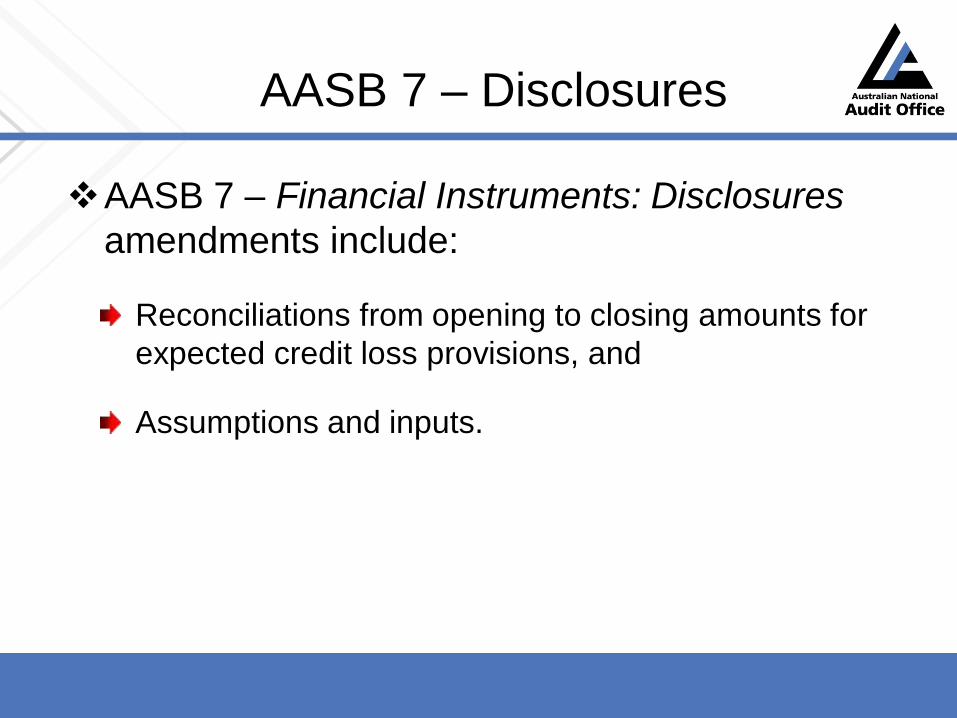

AASB 7 – Disclosures

AASB 7 – Financial Instruments: Disclosures amendments include:

Reconciliations from opening to closing amounts for expected credit loss provisions, and

Assumptions and inputs.

AASB 9 – Transition

Full retrospective classification – restatement of comparative periods.

Not applied to items already de-recognised at the date of initial application.

Must reclassify all financial instruments (retrospective).

Must revoke previous designations that don’t meet designation provisions for AASB 9.

May designate if meet provisions of AASB 9.

Pragmatic - comparatives not required to be restated.

AASB 9 – Please consider…

‘Models’ – Does your entity have a model? Does your entity need more than one model?

Opportunity to simplify; complex arrangements = detailed accounting.

Review all current and ongoing contracts; classification and business model (internal performance/evaluation).

Trade receivables (AASB 15) - use of simplified approach.

Rebuttable presumptions (30 day and 90 day).

Initial credit risk and subsequent impairment.

Same financial asset may have different classification.

2012 Client Seminars

Leases “One of my great ambitions before I die is to fly

in an aircraft that is on an airline’s balance sheet.” [Sir David Tweedie]

AASB 17 Leases

Expected new Standard for release by AASB in late 2015:

IAS 17 expected to be released Q3 2015.

AASB 17 Leases

Lease defined as “a contract that conveys the right to use an asset for a period in exchange for consideration.”

No distinction between operating and financing leases.

AASB 17 - Exceptions

Exemptions for short-term leases of 12 months or less.

Considering an exemption for small assets (e.g. laptops and office furniture).

Can use a portfolio approach for similar assets.

2012 Client Seminars

There must be an identified asset.

Control is determined by:

Right of use (economic benefit),and

Right to direct use (purpose).

Each right of use is a potential lease.

Leases – key points

AASB 17 – No Identified Asset

No identified asset if supplier has:

Right to substitute without customer consent

No barriers (economic or otherwise), and

Ability to benefit from the substitution.

AASB 17 – Initial Recognition

Right-of-use asset (RoUA) and lease liability:

Present value of the future lease payments (plus direct costs of entering into the lease).

Effective interest rate – rate lessor charges or lessees incremental rate of borrowing.

Excludes most variable payments and optional payments.

AASB 17 – Subsequently…

RoUA amortised on a straight line basis over the life of the agreement.

Lease repayments split between principal and interest expense (unwinding of discount).

Cash flow;

Principal portion of lease liability – financing activity.

Interest portion – in accordance with requirements relating to other interest paid.

AASB 17 - Example

Assumptions: 3 year lease.

Lease payments $50,000 p.a.

Effective interest rate 6%.

Lease payments made at end of period.

AASB 17 – Example (cont.)

At start - RoUA and lease liability $133,651.

At the end of each period - RoUA amortisation $44,550.

For each lease payment - cash $50,000 and;

Year 1; Interest expense $8,019 & principal repayment $41,981.

Year 2; Interest expense $5,500 & principal repayment $44,500.

Year 3; Interest expense $2,830 & principal repayment $47,170.

AASB 17 – Multi Lease Contracts

Must consider that each RoUA is a separate lease component.

Allocate consideration to each separate lease component:

Recognise a separate lease for each lease component with an observable stand alone price.

Where no observable stand alone price, bundle and recognise components as a single lease component.

AASB 17 – Lessor Accounting

Accounting largely unchanged – likely to be substantial additional disclosures.

Assumptions.

Judgements.

Income.

AASB 17 – Still to be decided

Lessee disclosures.

Transition arrangements.

Effective date.

AASB 17 – Please consider…

Identify operating leases likely to be recognised in balance sheet.

Model impact of taking up operating leases.

Review leases contracts with both service and lease components.

Review lease contracts with multiple RoUA (determine basis for attribution of contribution – standalone price).

Review control principles (direct purpose and obtain benefit).

Present value calculations - determine effective interest rate (may differ between leases for similar or like assets).

2012 Client Seminars

Revenue from Contracts with Customers

“One Ring to rule them all, One ring to find them; One ring to bring them all and in the darkness bind them.”

[The Fellowship of the Ring]

AASB 15 Revenue from Contracts with Customers

Effective for annual reporting periods beginning on or after 1 January 2017.

Applies to all exchange transactions.

AASB 1004 Contributions will apply to non-exchange transactions until not-for-profit version of AASB 15 completed (TBA).

AASB 15 - Recognition

Revenue is determined as the consideration the entity expects to receive in exchange for providing goods or services.

Revenue is recognised when a customer obtains control of goods or services.

2012 Client Seminars

Control determined by who has:

Right of use (economic benefit); and

Right to direct use (purpose).

Customers are defined.

Contract is a set of performance obligations.

Transaction price – standalone selling price.

Revenue from contracts – key points

AASB 15 – Key Features

Replaces AASB 118 Revenue and AASB 111 Construction Contracts.

Scope exclusions:

Financial instruments

Leases

Insurance contracts

Certain guarantee contracts

Certain non-monetary exchange contracts, and

Contracts with elements in multiple standards.

AASB 15 – 5 Steps

5 Steps:

Step 1: Identify the contract/s with a customer.

Step 2: Identify the performance obligations.

Step 3: Determine the transaction price.

Step 4: Allocate the transaction price to the performance obligations.

Step 5: Recognise revenue when (or as) the entity satisfies the performance obligations.

AASB 15 – Step 1

Identify the contract/s with a customer;

Agreement provides parties with enforceable rights and obligations (written, oral or otherwise).

It is probable that the entity will collect consideration (price in contract may be different).

AASB 15 – Step 2

Identify the performance obligations:

Identify as a performance obligation, each distinct promise to transfer goods or services (or a bundle of goods or services) to a customer.

Separation criteria:

Customer can benefit from good or service either on its own or with other resources that are readily available, and

Good or service is separable from other promises.

AASB 15 – Step 3

Determine the transaction price:

The amount of consideration to which an entity expects to be entitled in exchange for transferring the goods or services:

Relative standalone selling price

Non-cash consideration measured at fair value

Consideration paid or expected to be paid to customer will reduce transaction price

Adjust for significant financing benefit to customer, and

Estimate of variable consideration.

AASB 15 – Step 3 (cont.)

Relative standalone selling price:

Price an entity would charge a customer on a standalone basis.

If no standalone selling price must estimate (maximise the use of observable inputs):

Expected cost plus reasonable margin

Market prices adjusted for similar goods or services, and

Residual approach (total transaction price less the sum of the observable standalone selling price of other goods and services promised in the contract).

AASB 15 – Step 4

Allocate transaction price to performance obligations:

Where multiple performance obligations in a single arrangement - allocate the consideration to each of those performance obligations based on relative standalone selling price.

AASB 15 – Step 5

Recognise revenue when (or as) the entity satisfies a performance obligation:

Over time (evaluate first) – recognise revenue based on pattern of transfer to the customer, or

Point in time – recognise revenue when control transfers.

AASB 15 – Step 5 (cont.)

Revenue is recognised over time when:

Customer simultaneously receives and consumes all of the benefits as the entity performs obligations (traditional service arrangements e.g. cleaning and security services).

Performance creates or enhances an asset that the customer controls (e.g. construction contracts where the customer controls the work-in-progress throughout the arrangement).

Performance does not create an asset with an alternate use and entity has enforceable right to payment for performance to date (e.g. legal services – payment reflects work performed including a reasonable profit margin).

AASB 15 – Step 5 (cont.)

Revenue is recognised at a point in time when:

Performance obligations not satisfied over time.

Considered to be transferred when:

Customer has legal title to the asset.

Customer has physical possession of the asset (right of use / direct use).

Customer exposed to significant risks and rewards of ownership of the asset.

Customer has accepted the asset.

AASB 15 – Licence of Intellectual Property

Right of use – right to use entity’s IP as it exists when licence is granted:

Recognise as point in time.

Right of access – right to use entity’s IP as it exists during licence period:

Recognise over time.

AASB 15 – Disclosures

Key qualitative and quantitative disclosures:

Contract balances

Disaggregation of revenue

Costs to obtain or fulfil contracts

Remaining performance obligations, and

Significant judgments and changes in judgments.

AASB 15 – Transition

Retrospectively with some relief:

Full retrospective application, and

Hindsight allowed for variable consideration of completed contracts.

Practical expedient:

Apply to all existing contracts as of effective date and to contracts entered into subsequently.

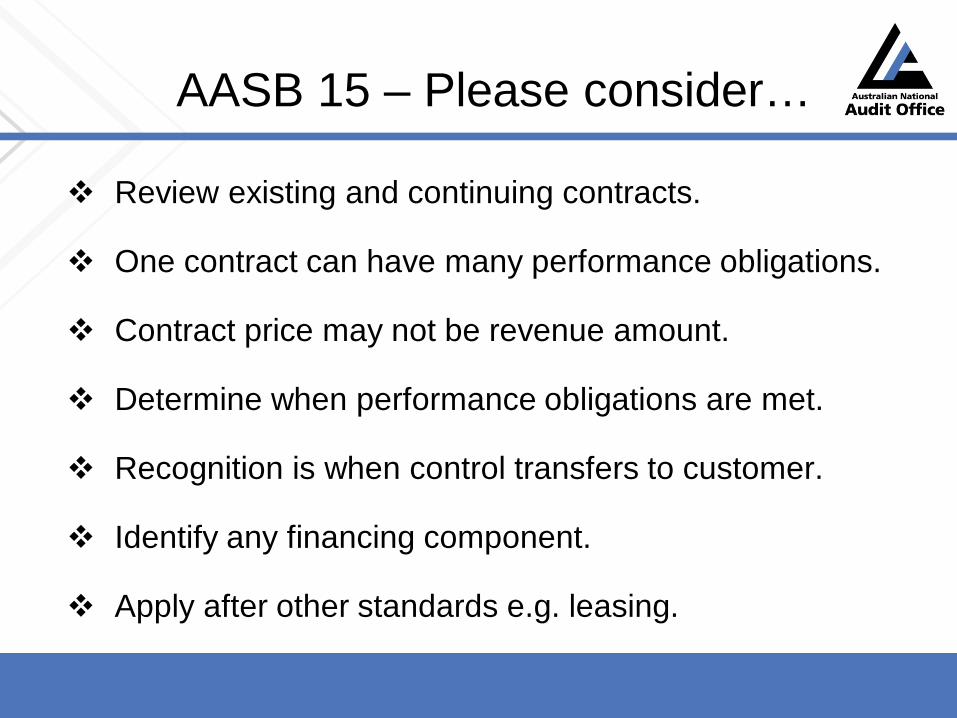

AASB 15 – Please consider…

Review existing and continuing contracts.

One contract can have many performance obligations.

Contract price may not be revenue amount.

Determine when performance obligations are met.

Recognition is when control transfers to customer.

Identify any financing component.

Apply after other standards e.g. leasing.

Income from Transaction of Not-for-Profit Entities

To be based on AASB 15.

Expected ED was Q1 2015 now TBD.

Replace income recognition components of AASB 1004 Contributions.

2012 Client Seminars

Related Parties “Society does not consist of individuals but expresses the sum of interrelations,

the relations within which these individuals stand.” [Karl Marx]

AASB 124 Related Parties Disclosures

Amendment to existing standard:

Effective for annual reporting periods beginning on or after 1 July 2016.

No prior year comparatives required for first year.

Amending standard to be issued by end March 2015.

AASB 124 - Related Parties

Removal of scope exemption for not-for-profit public sector (NFP) entities.

NFP entities will need to:

Identify related parties

Identify related party transactions, and

Make required disclosures.

AASB 124 - Related Parties

For a typical NFP Australian government entity, related parties would be expected to include:

Every entity controlled, jointly controlled or significantly influenced by your entity.

Every entity controlled, jointly controlled or significantly influenced by the Australian government.

Key management personnel of your entity and entities that control your entity including their close family members as well as any entities they control or jointly control and their superannuation plans.

Note: simplified disclosures apply for related party transactions between government-related entities.

AASB 124 – Disclosures

Disclose related party transactions separately for the following categories:

Parent.

Entities with control or significant influence over the entity.

Subsidiaries.

Associates.

Joint ventures in which the entity is a venturer.

KMP of the entity or its parent.

Any other related parties.

AASB 124 – Disclosures (cont.)

For each related party, disclose:

Nature of relationship.

Amount of transactions and outstanding balances (terms and conditions, security etc.).

Provisions for doubtful debts and any bad debts written off.

Aggregate of KMP compensation split into specified categories.

AASB 124 – KMP Disclosures

KMP compensation disclosure requirements:

Short-term employee benefits

Post-employment benefits

Other long-term benefits

Termination benefits, and

Share-based payments.

AASB 124 – Simplified Government-related Entities Disclosures

Simplified disclosure for government-related entities:

The name of the government and the nature of its relationship with the entity

The nature and amount of each individually significant transaction, and

For other transactions that are collectively, but not individually significant, a qualitative or quantitative indication of their extent.

AASB 124 – Please consider…

Time consuming – identify and document all related party relationships.

Advise key related parties that information will be required and transactions may be disclosed.

Review likely classes of transactions and identify which ones need to be reported.

Consider how to capture related party information for Ministers and their immediate family.

AASB 124 – Relief for Ministers as KMP

Possible relief from individual reporting requirements for Ministers as KMP under ‘management entity’ amendments to AASB 124

Exempt KMP compensation disclosure where services from ‘management entity’.

Still disclose amounts incurred by the entity for the provision of ‘management entity’ KMP services.

2012 Client Seminars

AASB Disclosure Initiative “Less is more.” [Ludwig Mies]

AASB 2015-2 Disclosure Initiative

Effective date is reporting periods beginning on or after 1 January 2016.

Aimed at clarifying existing requirements.

Does not affect recognition or measurement.

Places emphasis on professional judgment and materiality.

AASB 2015-2 Disclosure Initiative

Disclose only material information.

Do not obscure useful information with immaterial information.

Use professional judgment to determine what information is disclosed and the order in which that information is disclosed.

Clarifies need to identify significant accounting policies.

Do not have to comply with AAS if information is not material – “as a minimum” does not mean must.

2012 Client Seminars

Emerging Trends in Accounting Standards…

“By failing to prepare, you are preparing to fail.” [Benjamin Franklin]

Emerging Trends in Accounting Standards…

Follow the standards is being replaced with obligation to disclose.

Control is ability to direct purpose and benefit from use.

Disaggregate complex contracts and arrangements.

Simplification is an entity’s responsibility.

Guidance replaced with examples.

Emerging Trends in Accounting Standards…(cont.)

New key terms:

Significant – make a judgment.

Probable – recognise what is probable.

Use of observable standalone prices – fair value by another name?

Estimation – disclose risks, variables and judgments.

External disclosures based on information used by entity decision makers.

That’s all Folks! [Mel Blanc]

AASB 124 - Related Parties

A party is related to an entity if the party:

a) Directly, or indirectly:

i. Controls, is controlled by, or is under the common control of another entity

ii. Has an interest in the entity that gives it significant influence over the entity, or

iii. Has joint control over the entity.

b) Is an associate of the entity

c) Is a joint venture in which entity is a venturer

d) Is a member of key management personnel (KMP) of the entity or its parent

AASB 124 - Related Parties

A party is related to an entity if (cont.):

e) Is a close member of the family of an individual referred to in (a) or (d)

f) Is an entity that is controlled, jointly controlled or significantly influenced by, or for which significant voting power in such entity resides with, directly or indirectly, any individual referred to in (d) or (e), or

g) Is a post-employment benefit plan for the benefit of the entity’s employees, or of any entity that is a related party of the entity.

AASB 124 - Related Parties

A related party transaction is a transfer of resources, services or obligations between related parties, regardless of whether a price is charged.

Key management personnel (KMP) are those persons having authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly.

Close members of the family of an individual are the family members who are expected to influence, or be influenced by, that individual in their dealings with the entity.

AASB 124 - Related Parties

The following are not related parties:

Entities simply because they have common directors or KMP

Venturers simply because they share joint control over a joint venture

Entities where relationship is based on normal dealings with the entity e.g. trade unions, public utilities and providers of finance, and

Customers, suppliers etc. even when the relationship results in economic dependence.

AASB 124 – Example Transactions

Examples of related party transactions:

Purchases or sales of goods.

Purchases or sales of property and other assets.

Rendering or receiving of services.

Leases.

Transfers of research and development.

Transfers under licence agreements.

Transfers under finance arrangements.

Provisions of guarantees or collateral.

Commitments to do something if a particular event occurs or does not occur.

Settlement of liabilities.

![How marketers can leverage Ektron DXH's Exact Target for better client engagement [Webinar]](https://img.pdfslide.us/doc/110x75/554bb254b4c905ae618b5995/how-marketers-can-leverage-ektron-dxhs-exact-target-for-better-client-engagement-webinar.jpg)