Embed Size (px)

Citation preview

Analy&cs & Decision Making -‐ Way Forward Aneesh Bhatnagar Director – Product Management MetricStream

Sriraghavan Rajamannar r SVP – Integrated Risk – Risk Analy&cs Bank Danamon Indonesia

Analy&cs Agenda

2

• Analy&cs – What? Why? Stages & Catalysts • Infrastructure the Most Neglected • Analy&c Building Blocks • Analy&c Applica&ons

• PorJolio Management • Risk Applica&ons

• Tracking Analy&cs

Key Aspects

3

• Clarity on what business needs now and in future

• Avoid Silos. Need to Standardize.

• Central repository of Process, Risk and Control data.

• Cri&cal importance of quality data

• Capturing and managing accurate, &mely and relevant data is vital

• Building an effec&ve data analy&cs infrastructure

Key Aspects

4

• Flexible repor&ng framework

• Remember: Analy&cs is Big Data

• Automate and avoid manual errors

• All the above needs investment in systems, soUware and automa&on

• Select the appropriate tools for your requirements

• Have the best skilled people for Analy&cs

5

Analy&cs – What? Why? Stages & Catalysts

What is Analy&cs

6

“Analytics is all about deriving insights from relevant data to support fact-based decision-making”

“Analytics helps improve Top-line and Bottom-line

The Essence of Research has Shifted from Information Capture to its Transformation into Knowledge”

“In an uncertain world, one factor sets successful enterprises

apart: Intelligence”

“Intelligent enterprises apply data and process insights to make technology work smarter for them”

Why Analy&cs

7

• Targeted acquisi&on – booking quality vs. booking quan&ty • Drive growth in saturated market – need to look inwards – x-‐

sell, up-‐sell and deep sell • Supports proac&ve ac&ons – no more reac&ve (prescrip&ve) • Drive customer sa&sfac&on, loyalty and value • Maximize value crea&on over the product lifecycle • Correlate product offers to customer life cycle events • Results in value crea&on and aids growth of the Bank • Adds to the boYom-‐line

Op&mizing risk -‐ response through analy&c based targeted marke&ng strategies – a direct impact to the boYom line

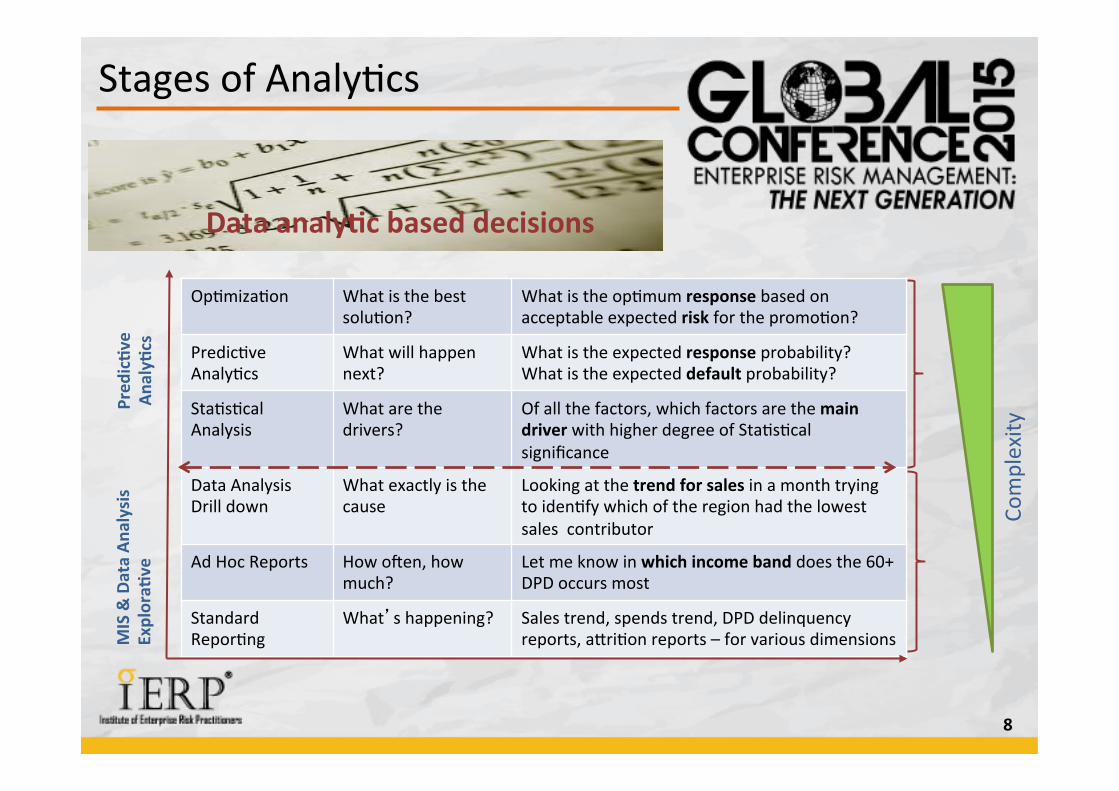

Stages of Analy&cs

8

Op&miza&on What is the best solu&on?

What is the op&mum response based on acceptable expected risk for the promo&on?

Predic&ve Analy&cs

What will happen next?

What is the expected response probability? What is the expected default probability?

Sta&s&cal Analysis

What are the drivers?

Of all the factors, which factors are the main driver with higher degree of Sta&s&cal significance

Data Analysis Drill down

What exactly is the cause

Looking at the trend for sales in a month trying to iden&fy which of the region had the lowest sales contributor

Ad Hoc Reports How oUen, how much?

Let me know in which income band does the 60+ DPD occurs most

Standard Repor&ng

What’s happening? Sales trend, spends trend, DPD delinquency reports, aYri&on reports – for various dimensions

Pred

ic>v

e

Analy>

cs

MIS & Data An

alysis

Explora>

ve

Complexity

Data analy>c based decisions

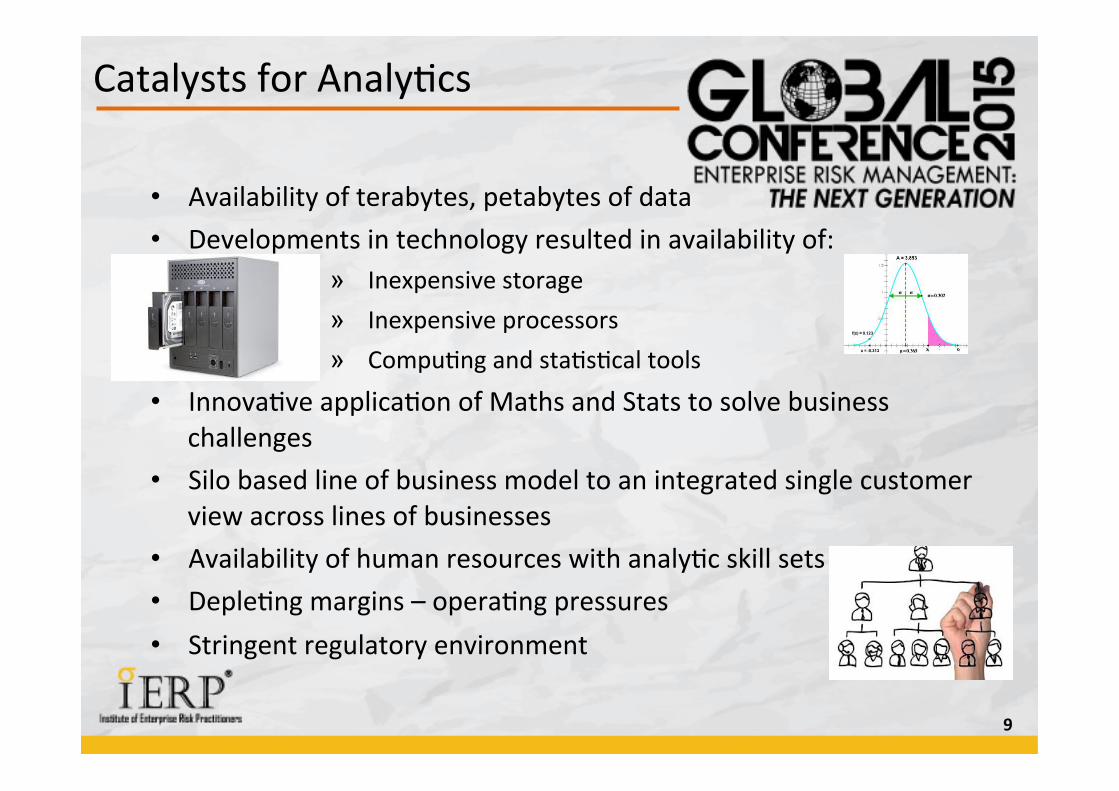

Catalysts for Analy&cs

9

• Availability of terabytes, petabytes of data • Developments in technology resulted in availability of:

» Inexpensive storage » Inexpensive processors » Compu&ng and sta&s&cal tools

• Innova&ve applica&on of Maths and Stats to solve business challenges

• Silo based line of business model to an integrated single customer view across lines of businesses

• Availability of human resources with analy&c skill sets • Deple&ng margins – opera&ng pressures • Stringent regulatory environment

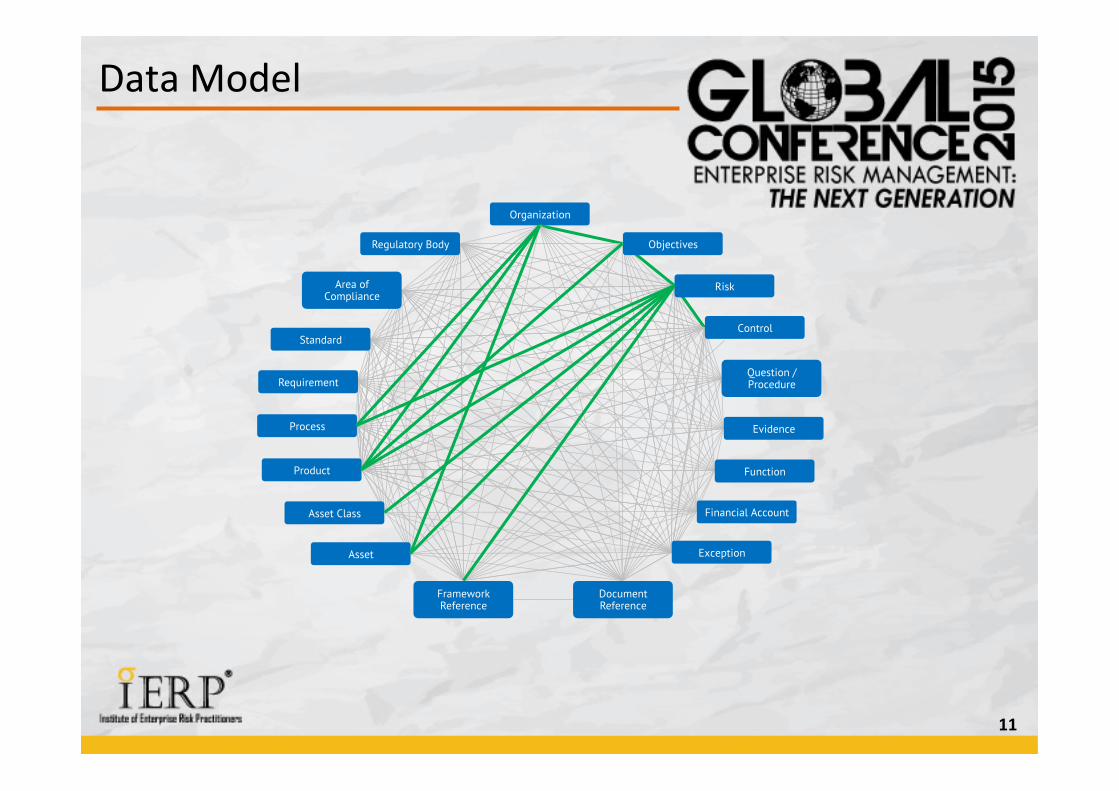

Data Model

10

Organization

Objectives

Risk

Control

Question / Procedure

Evidence

Function

Financial Account

Exception Asset

Asset Class

Product

Process

Requirement

Standard

Area of Compliance

Regulatory Body

Framework Reference

Document Reference

Data Model

11

Organization

Objectives

Risk

Control

Question / Procedure

Evidence

Function

Financial Account

Exception Asset

Asset Class

Product

Process

Requirement

Standard

Area of Compliance

Regulatory Body

Framework Reference

Document Reference

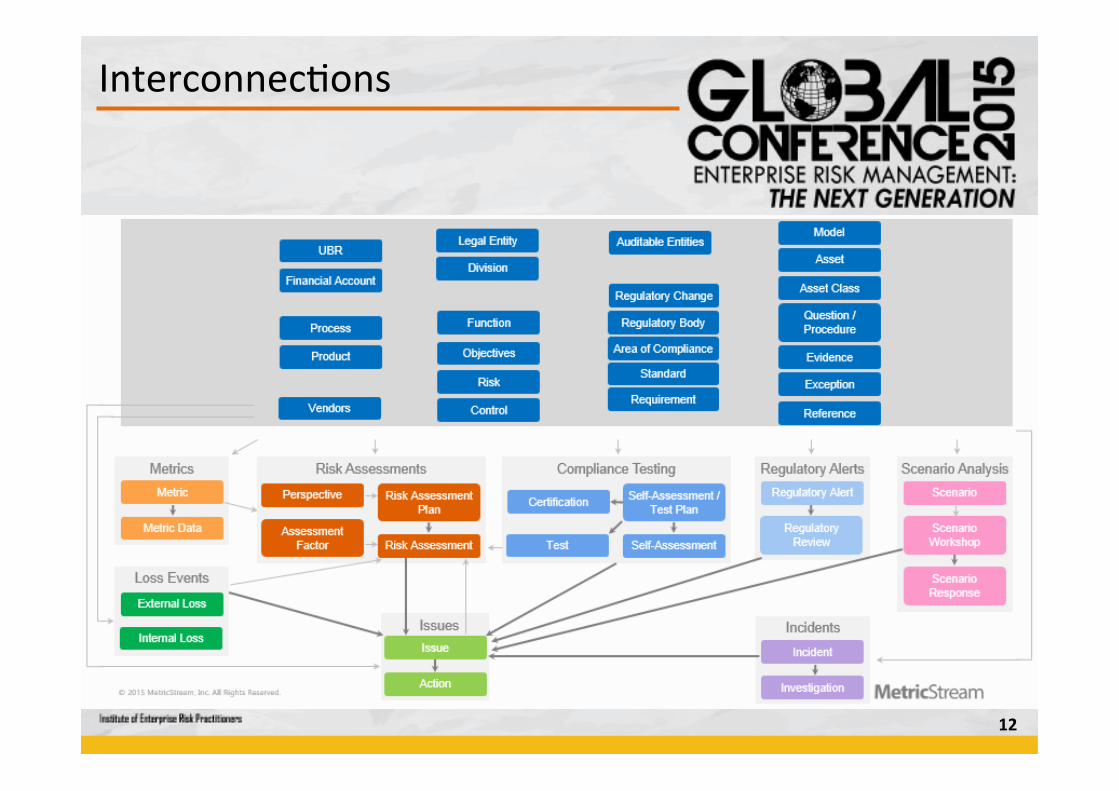

Interconnec&ons

12

Interac&ve Business Intelligence The advantages are clear

13

+40%

Organiza&onal Collabora&on

+50%

Speed of decision making

+60%

Trust in underlying data

Source: Aberdeen Group, April 2014

14

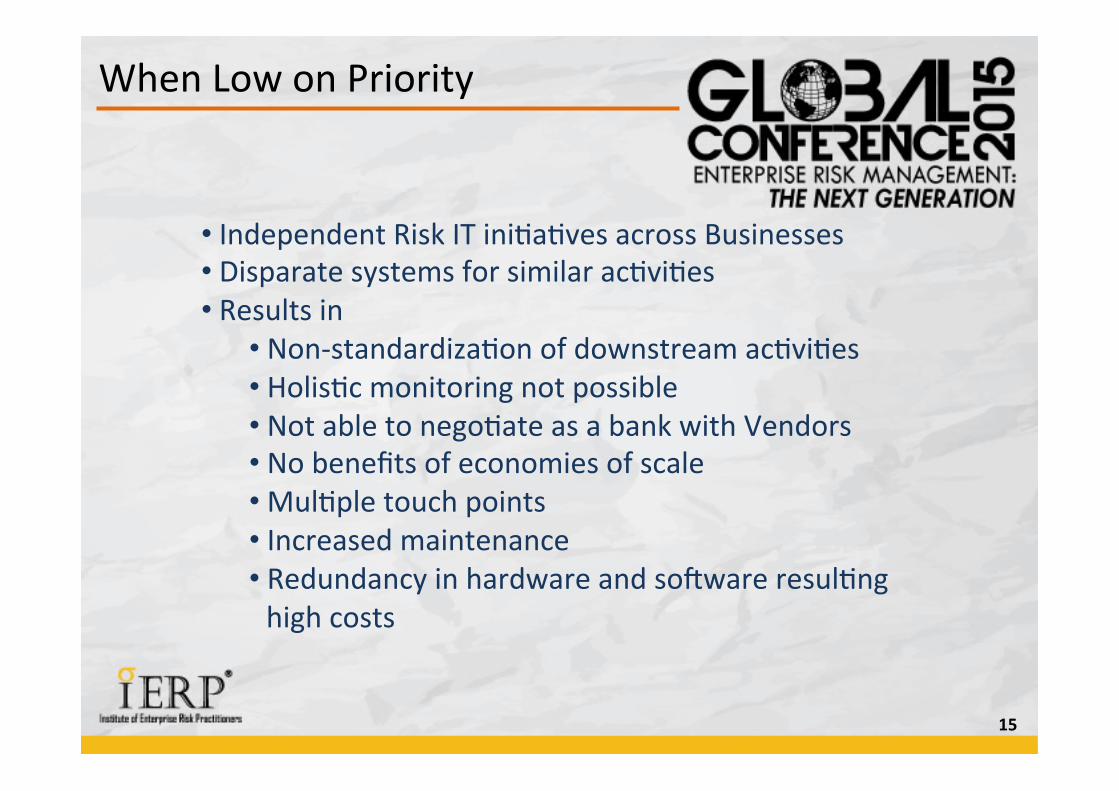

Infrastructure The Most Neglected

15

When Low on Priority

• Independent Risk IT ini&a&ves across Businesses • Disparate systems for similar ac&vi&es • Results in

• Non-‐standardiza&on of downstream ac&vi&es • Holis&c monitoring not possible • Not able to nego&ate as a bank with Vendors • No benefits of economies of scale • Mul&ple touch points • Increased maintenance • Redundancy in hardware and soUware resul&ng high costs

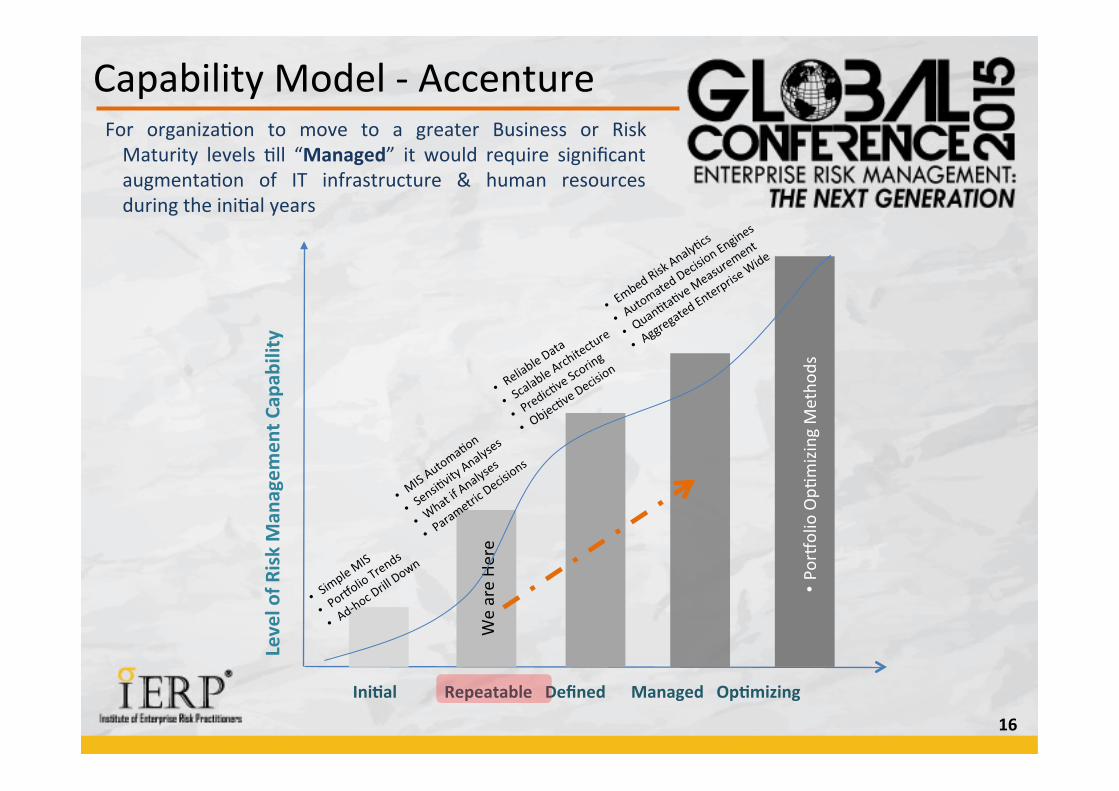

Capability Model -‐ Accenture

16

We are He

re

Level of R

isk Man

agem

ent C

apab

ility

Ini>al Repeatable Defined Managed Op>mizing

• PorJo

lio Op&

mizing M

etho

ds

For organiza&on to move to a greater Business or Risk Maturity levels &ll “Managed” it would require significant augmenta&on of IT infrastructure & human resources during the ini&al years

17

Analy&cs Building Blocks

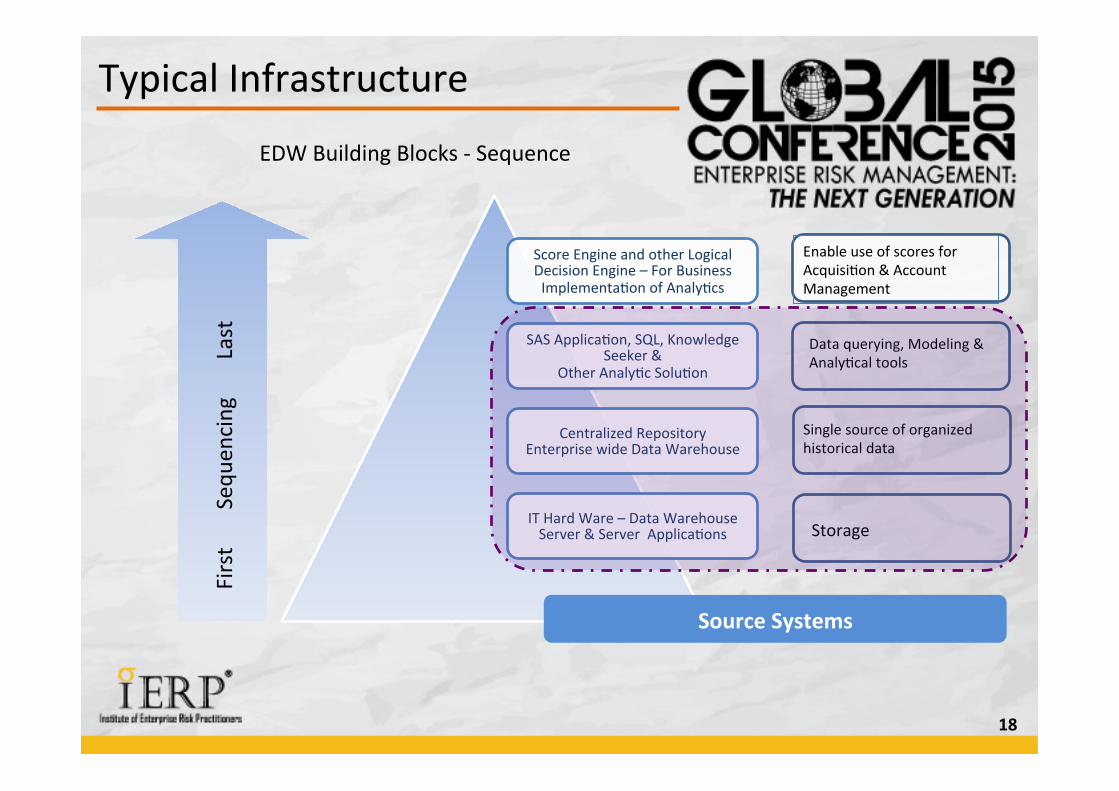

Typical Infrastructure

18

Enable use of scores for Acquisi&on & Account Management

Score Engine and other Logical Decision Engine – For Business Implementa&on of Analy&cs

SAS Applica&on, SQL, Knowledge Seeker &

Other Analy&c Solu&on

Centralized Repository Enterprise wide Data Warehouse

IT Hard Ware – Data Warehouse Server & Server Applica&ons

First Seq

uencing Last

Single source of organized historical data

Data querying, Modeling & Analy&cal tools

Storage

Source Systems

EDW Building Blocks -‐ Sequence

19

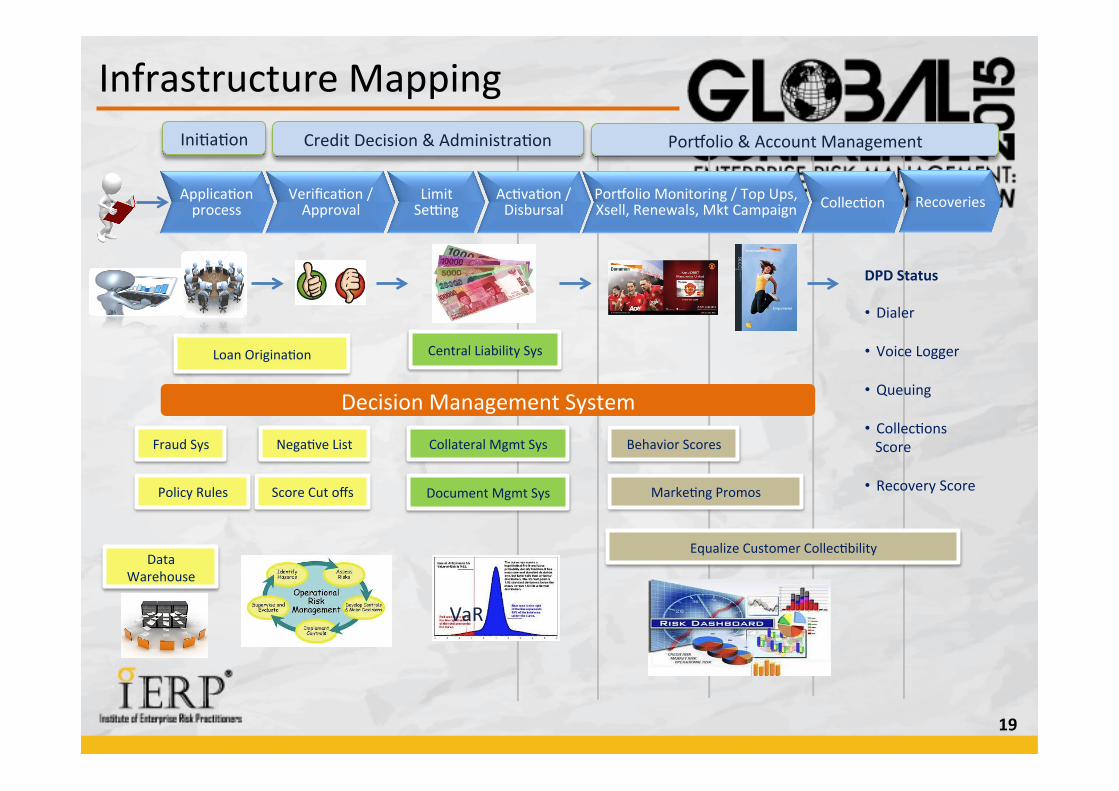

Infrastructure Mapping

Score Cut offs

Loan Origina&on

PorJolio & Account Management Credit Decision & Administra&on Ini&a&on

Applica&on process

Verifica&on / Approval

Limit Seeng

Ac&va&on / Disbursal

PorJolio Monitoring / Top Ups, Xsell, Renewals, Mkt Campaign Collec&on

Nega&ve List

Data Warehouse

Fraud Sys

Central Liability Sys

Equalize Customer Collec&bility

DPD Status • Dialer

• Voice Logger

• Queuing

• Collec&ons Score

• Recovery Score

Recoveries

Decision Management System

Document Mgmt Sys Policy Rules

Collateral Mgmt Sys Behavior Scores

VaR

Marke&ng Promos

Investments in Decision Engine

20

Decision Engine – Central Nervous System of the Organiza&on

• Faster Turn Around Time (TAT) • Improved efficiency • Enables the embedding of Policy Rules & Credit Scores – (App. & Beh.) for Approval and PorJolio Ac&ons

• Automa&on reduces errors in interpreta&on and implementa&on of the credit policy parameters due to lesser human interface / interference

• Interface with digital imaging system • Holis&c Credit Proposal Work Flow • Automated Nega&ve List de dupe (internal Bureau checking)

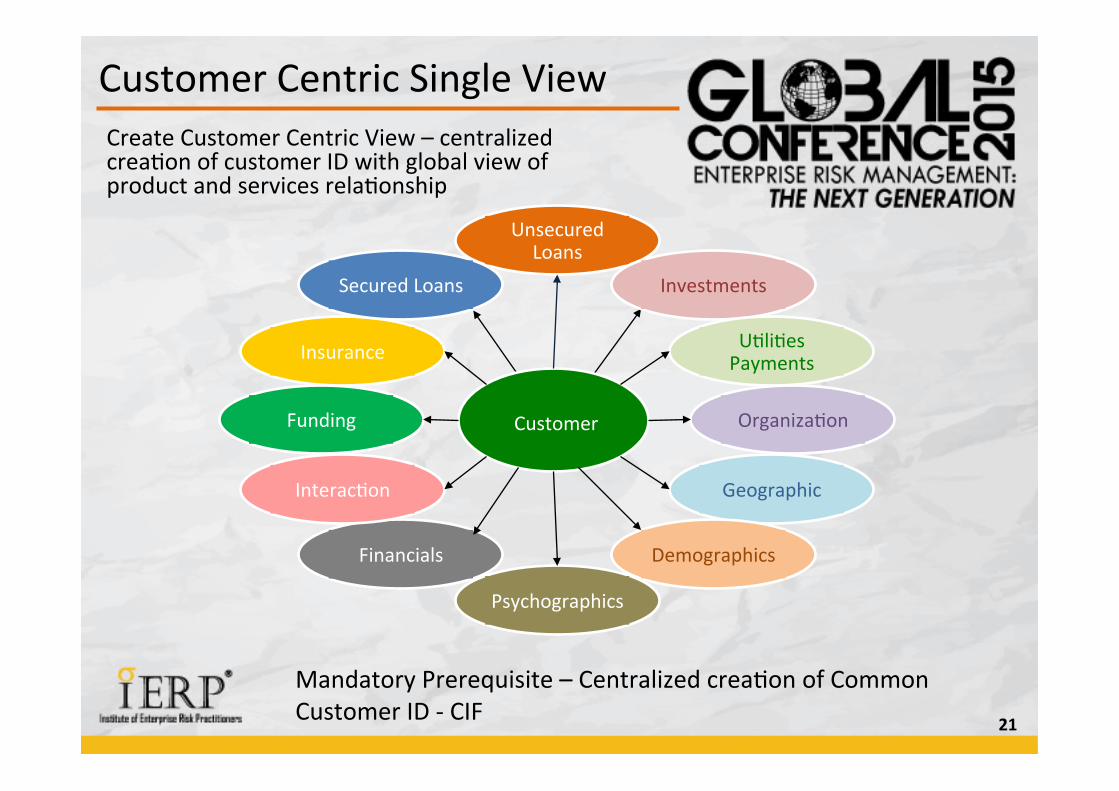

Customer Centric Single View

21

Create Customer Centric View – centralized crea&on of customer ID with global view of product and services rela&onship

Mandatory Prerequisite – Centralized crea&on of Common Customer ID -‐ CIF

Unsecured Loans

Investments

U&li&es Payments

Organiza&on

Geographic

Demographics

Psychographics

Financials

Interac&on

Funding

Insurance

Secured Loans

Customer

Analy&c Center of Excellence

22

Silo based Analy>c approach and Organiza>onal Concerns: Lack of understanding on how to use analy&cs to improve the business

––Disconnected projects causing silos of data to develop in pockets across the enterprise

––Weak or poorly understood business analy&cs strategy and roadmap • Projects that are misaligned with business needs, are compe&ng for priority

or lack execu&ve sponsorship and support • Lack of skills internally in the line of business

–– A lack of training and support to ensure that tools are used effec&vely, mee&ng ease of use and response &me expecta&ons

• Best prac&ces and standards that are not shared and applied consistently, affec&ng the efficiency of Finance, IT and user communi&es

Work towards an Analy&cs Center of Excellence (CoE) – move from silo to centralized organiza&on structure to enable the big picture view for the bank

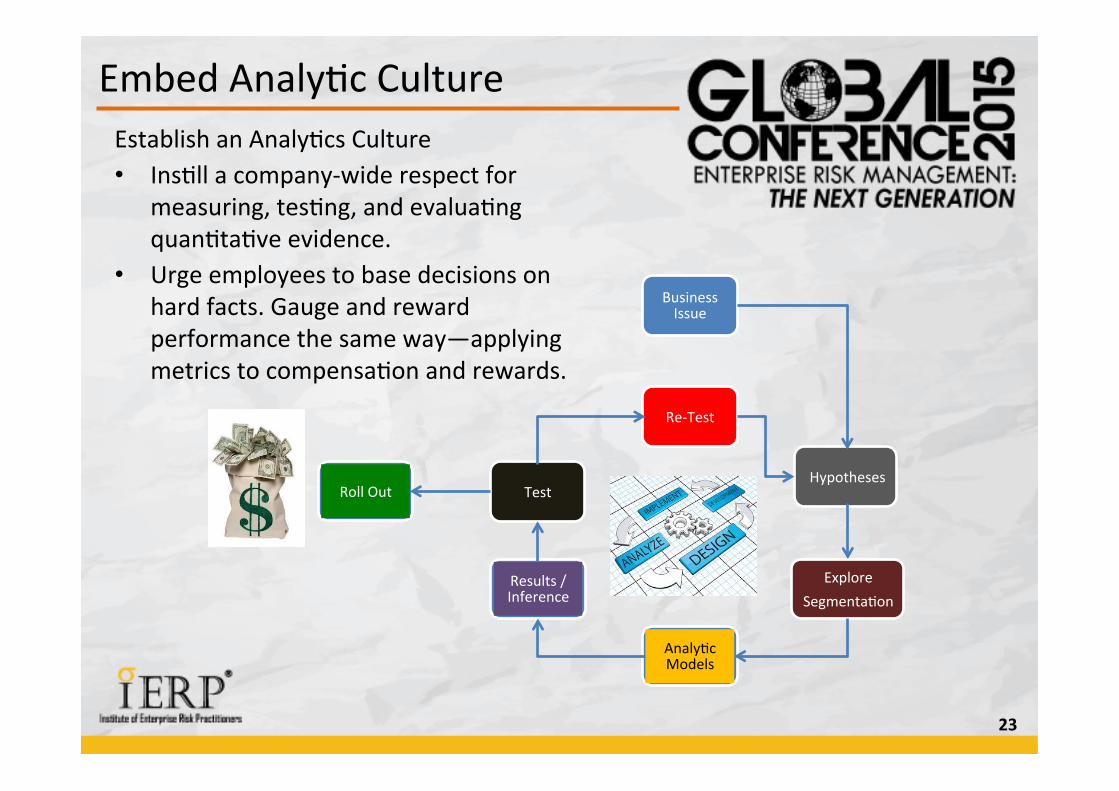

Embed Analy&c Culture

23

Establish an Analy&cs Culture • Ins&ll a company-‐wide respect for

measuring, tes&ng, and evalua&ng quan&ta&ve evidence.

• Urge employees to base decisions on hard facts. Gauge and reward performance the same way—applying metrics to compensa&on and rewards.

Business Issue

Hypotheses

Explore Segmenta&on

Analy&c Models

Results / Inference

Test Roll Out

Re-‐Test

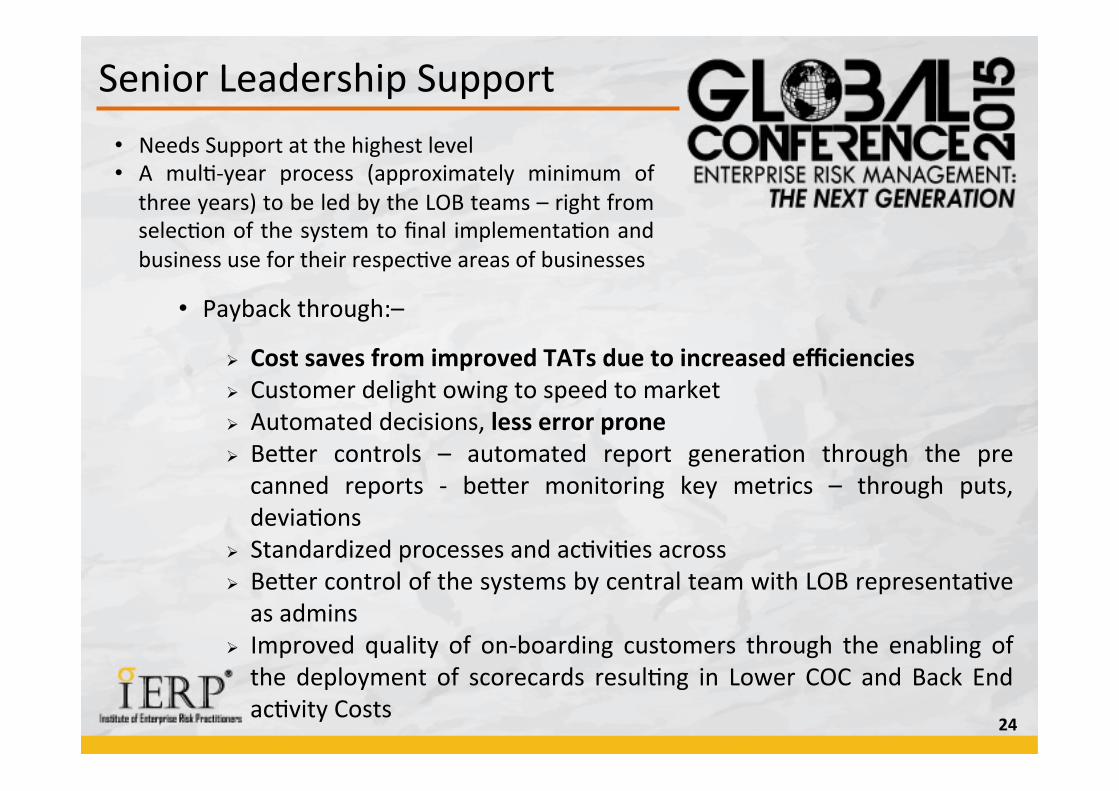

Senior Leadership Support

24

• Payback through:–

Ø Cost saves from improved TATs due to increased efficiencies Ø Customer delight owing to speed to market Ø Automated decisions, less error prone Ø BeYer controls – automated report genera&on through the pre canned reports -‐ beYer monitoring key metrics – through puts, devia&ons

Ø Standardized processes and ac&vi&es across Ø BeYer control of the systems by central team with LOB representa&ve as admins

Ø Improved quality of on-‐boarding customers through the enabling of the deployment of scorecards resul&ng in Lower COC and Back End ac&vity Costs

• Needs Support at the highest level • A mul&-‐year process (approximately minimum of three years) to be led by the LOB teams – right from selec&on of the system to final implementa&on and business use for their respec&ve areas of businesses

25

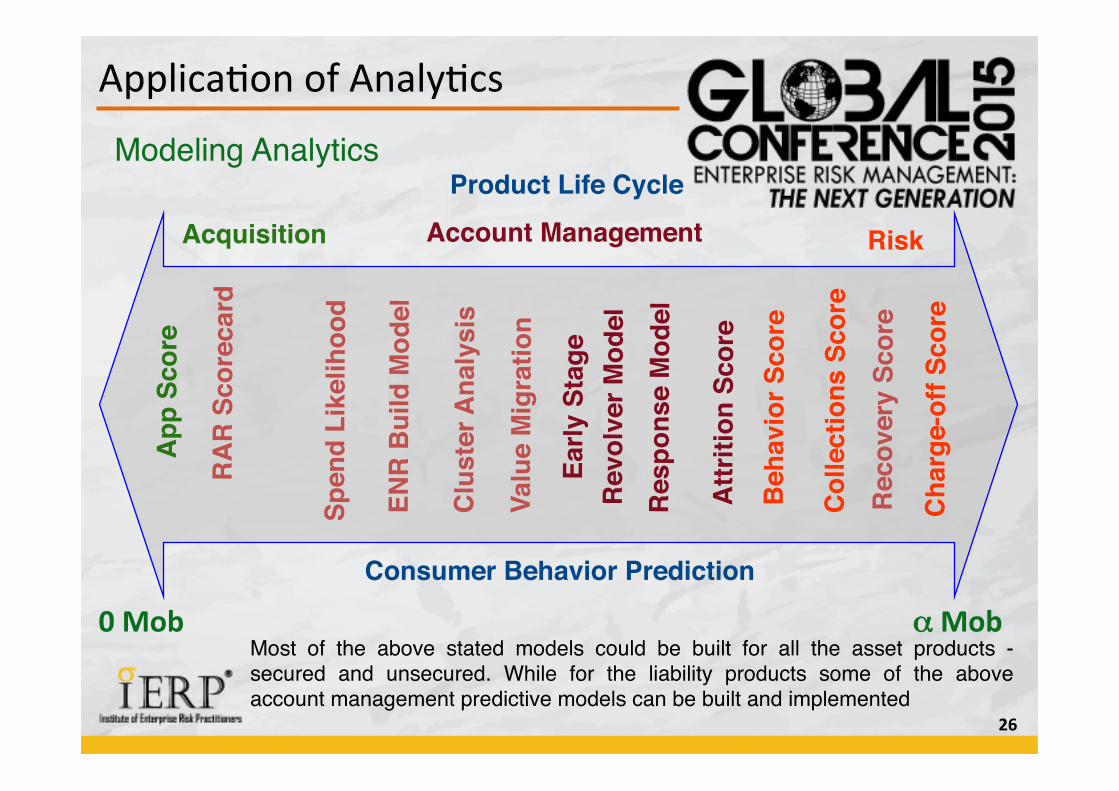

Analy&c Business Applica&ons

Applica&on of Analy&cs

26

App

Sco

re!

Attr

ition

Sco

re!

ENR

Bui

ld M

odel!

Early

Sta

ge !

!

Rev

olve

r Mod

el!

Res

pons

e M

odel!

Valu

e M

igra

tion!

Spen

d Li

kelih

ood!

Cha

rge-

off S

core!

Col

lect

ions

Sco

re!

Beh

avio

r Sco

re!

Rec

over

y Sc

ore!

Product Life Cycle!

Consumer Behavior Prediction!

Modeling Analytics

Acquisition! Account Management! Risk!

0 Mob α Mob Most of the above stated models could be built for all the asset products - secured and unsecured. While for the liability products some of the above account management predictive models can be built and implemented "

Clu

ster

Ana

lysi

s!

RA

R S

core

card!

Product Life Cycle Analy&cs

27

n Best Product n Limit Seeng

n Limit Mgmt. -‐ increase / decrease / freeze

n Renewals

n Pricing

n Risk Ranking n Objec&ve standardized outcomes

n Auto Approval Decision

n Selec&ve Verifica&ons

n Segmenta&on n Ac&va&on

n AYri&on Mgmt.

n Response predic&on

n Cross-‐sell / up sell

n Product & campaign design

n PorJolio mix op&miza&on

n Loss forecas&ng

n Dynamic reserving

n Policy revision

n Targeted balance build

n Priori&zing coll & Rec Ac&vity

n Queuing, contact method, and frequency

n Debt -‐ Sell / hold decisions

Under Wri>ng Limit SeWng Marke>ng Ac>vi>es

PorXolio Monitoring

Collec>ons & Recoveries

App Scores Behavior Scores Collns & Reco

Scores

Gain compe&&ve advantage vis a vis compe&tors

28

Analy&cs Risk Applica&ons

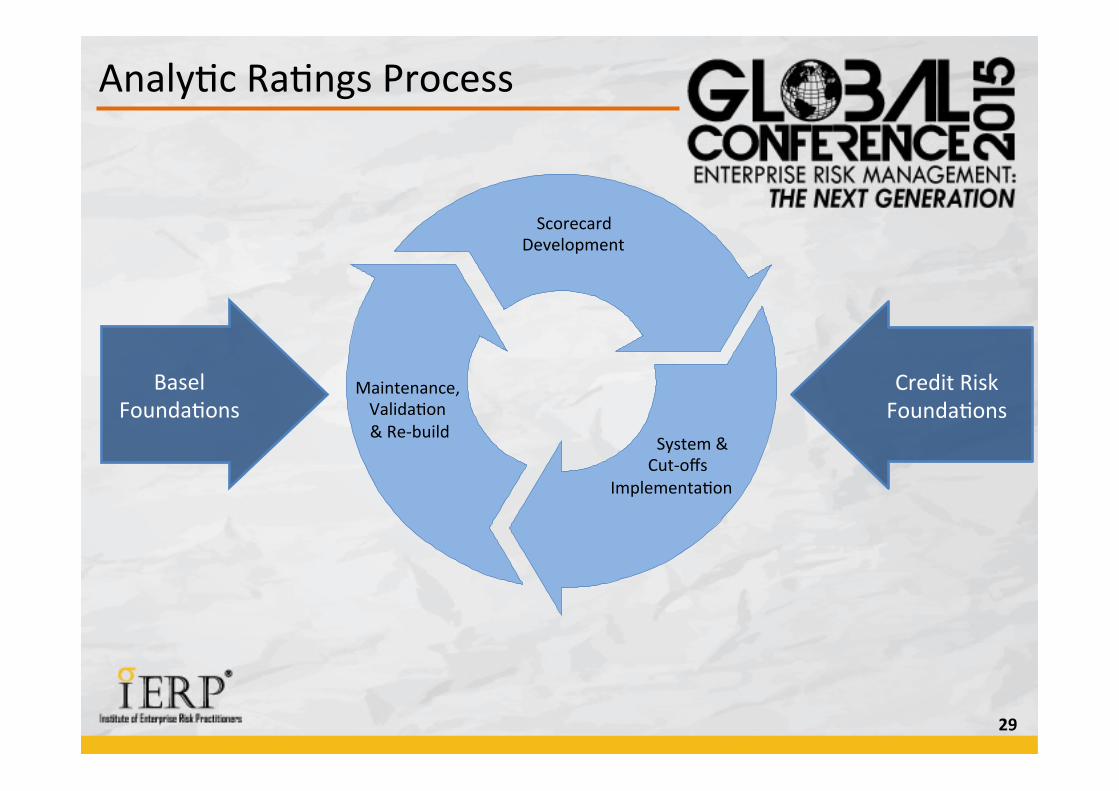

Analy&c Ra&ngs Process

29

Scorecard Development

System & Cut-‐offs

Implementa&on

Maintenance, Valida&on & Re-‐build

Basel Founda&ons

Credit Risk Founda&ons

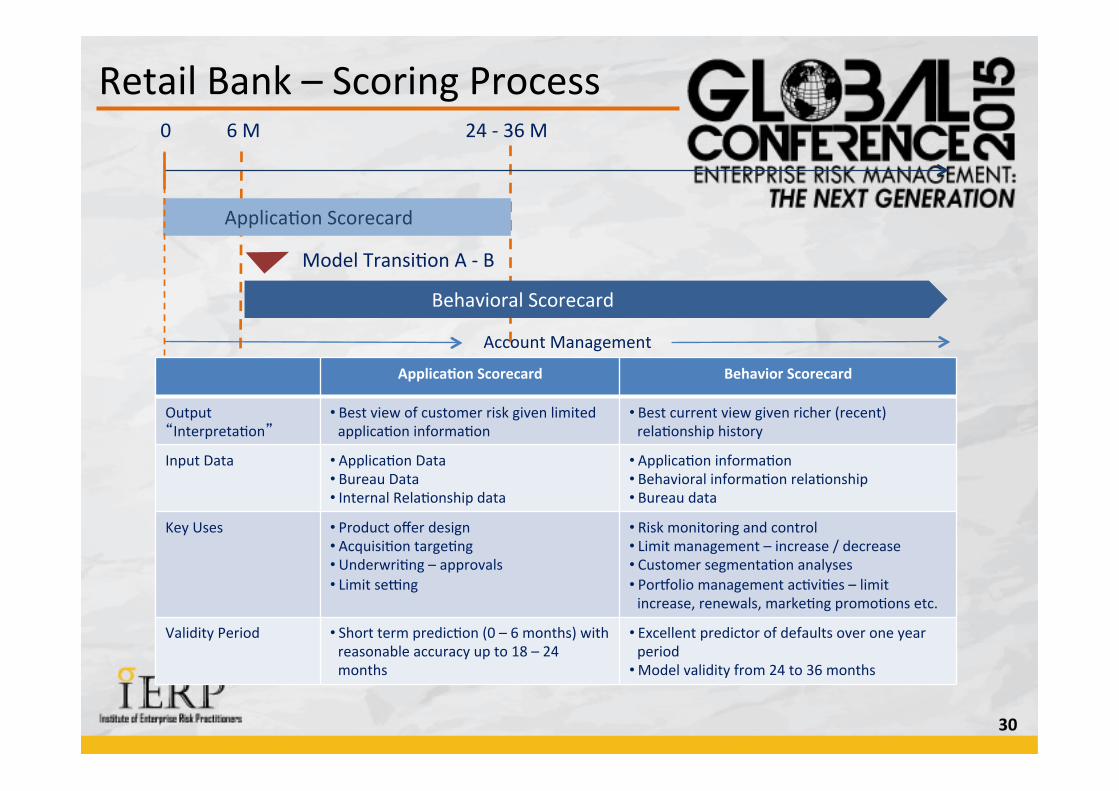

Retail Bank – Scoring Process

30

Applica>on Scorecard Behavior Scorecard

Output “Interpreta&on”

• Best view of customer risk given limited applica&on informa&on

• Best current view given richer (recent) rela&onship history

Input Data • Applica&on Data • Bureau Data • Internal Rela&onship data

• Applica&on informa&on • Behavioral informa&on rela&onship • Bureau data

Key Uses • Product offer design • Acquisi&on targe&ng • Underwri&ng – approvals • Limit seeng

• Risk monitoring and control • Limit management – increase / decrease • Customer segmenta&on analyses • PorJolio management ac&vi&es – limit increase, renewals, marke&ng promo&ons etc.

Validity Period • Short term predic&on (0 – 6 months) with reasonable accuracy up to 18 – 24 months

• Excellent predictor of defaults over one year period

• Model validity from 24 to 36 months

0 6 M 24 -‐ 36 M

Model Transi&on A -‐ B

Applica&on Scorecard

Behavioral Scorecard

Account Management

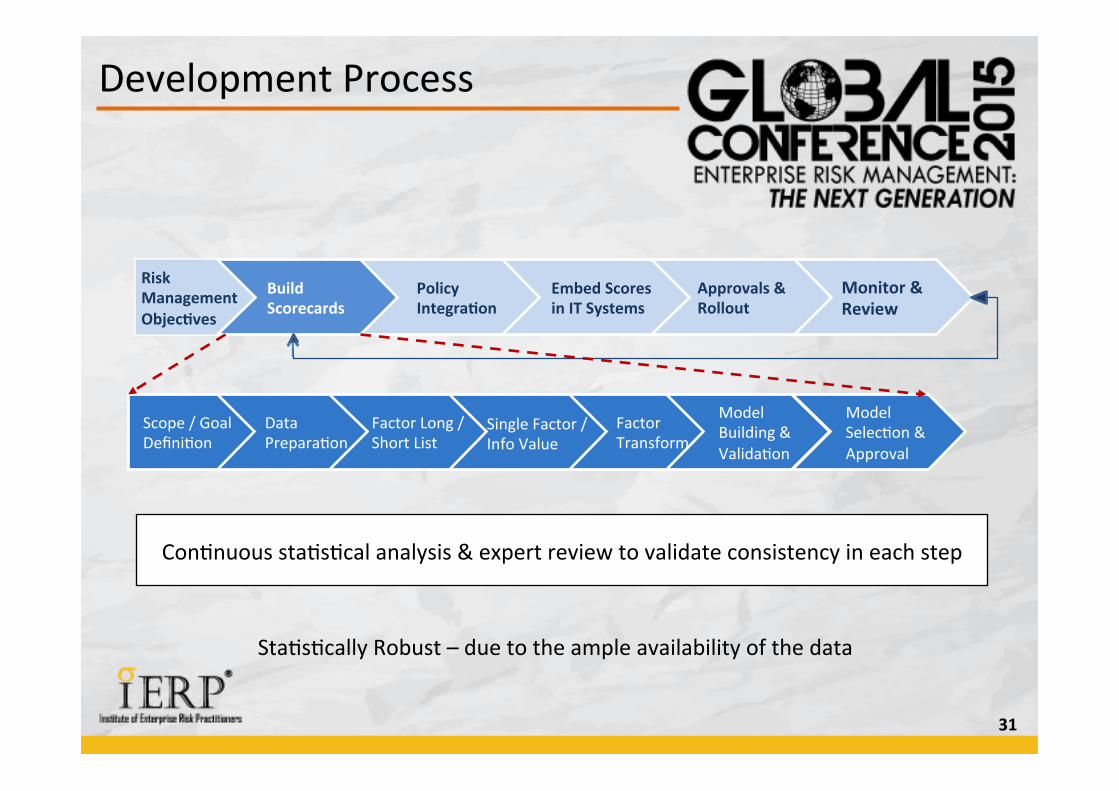

Development Process

31

Risk Management Objec>ves

Build Scorecards

Policy Integra>on

Embed Scores in IT Systems

Approvals & Rollout

Monitor & Review

Scope / Goal Defini&on

Data Prepara&on

Factor Long / Short List

Single Factor / Info Value

Factor Transform

Model Selec&on & Approval

Model Building & Valida&on

Con&nuous sta&s&cal analysis & expert review to validate consistency in each step

Sta&s&cally Robust – due to the ample availability of the data

32

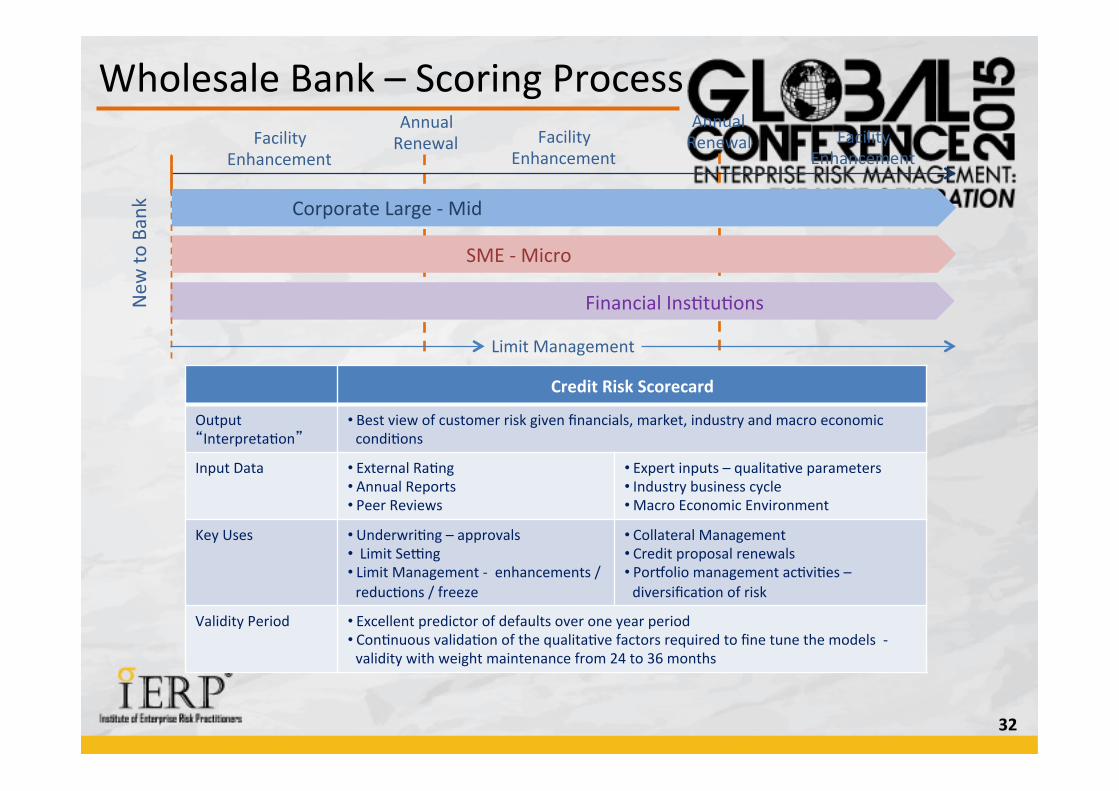

Credit Risk Scorecard

Output “Interpreta&on”

• Best view of customer risk given financials, market, industry and macro economic condi&ons

Input Data • External Ra&ng • Annual Reports • Peer Reviews

• Expert inputs – qualita&ve parameters • Industry business cycle • Macro Economic Environment

Key Uses • Underwri&ng – approvals • Limit Seeng • Limit Management -‐ enhancements / reduc&ons / freeze

• Collateral Management • Credit proposal renewals • PorJolio management ac&vi&es – diversifica&on of risk

Validity Period • Excellent predictor of defaults over one year period • Con&nuous valida&on of the qualita&ve factors required to fine tune the models -‐ validity with weight maintenance from 24 to 36 months

New

to Bank

Annual Renewal

Corporate Large -‐ Mid

SME -‐ Micro

Financial Ins&tu&ons

Facility Enhancement

Facility Enhancement

Facility Enhancement

Annual Renewal

Limit Management

Wholesale Bank – Scoring Process

33

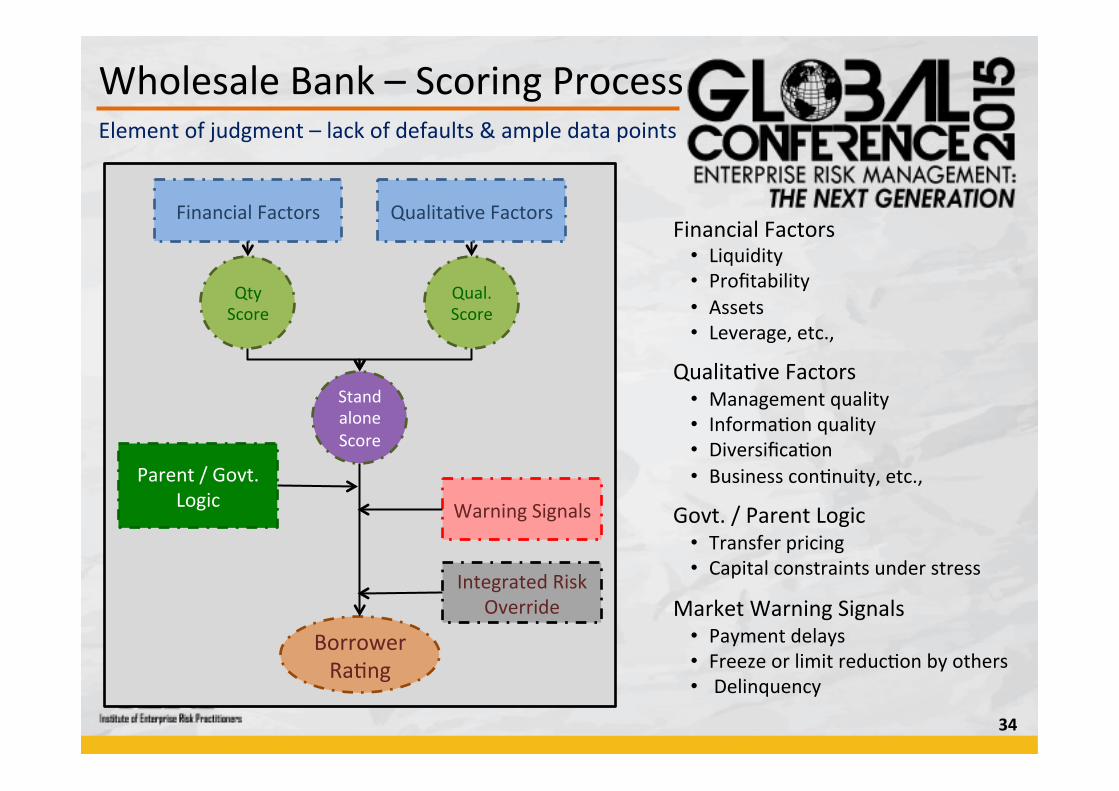

Tracking Analy&cs

34

Financial Factors Qualita&ve Factors

Warning Signals

Qty Score

Qual. Score

Standalone Score

Integrated Risk Override

Borrower Ra&ng

Parent / Govt. Logic

Financial Factors • Liquidity • Profitability • Assets • Leverage, etc.,

Qualita&ve Factors • Management quality • Informa&on quality • Diversifica&on • Business con&nuity, etc.,

Govt. / Parent Logic • Transfer pricing • Capital constraints under stress

Market Warning Signals • Payment delays • Freeze or limit reduc&on by others • Delinquency

Element of judgment – lack of defaults & ample data points

Wholesale Bank – Scoring Process

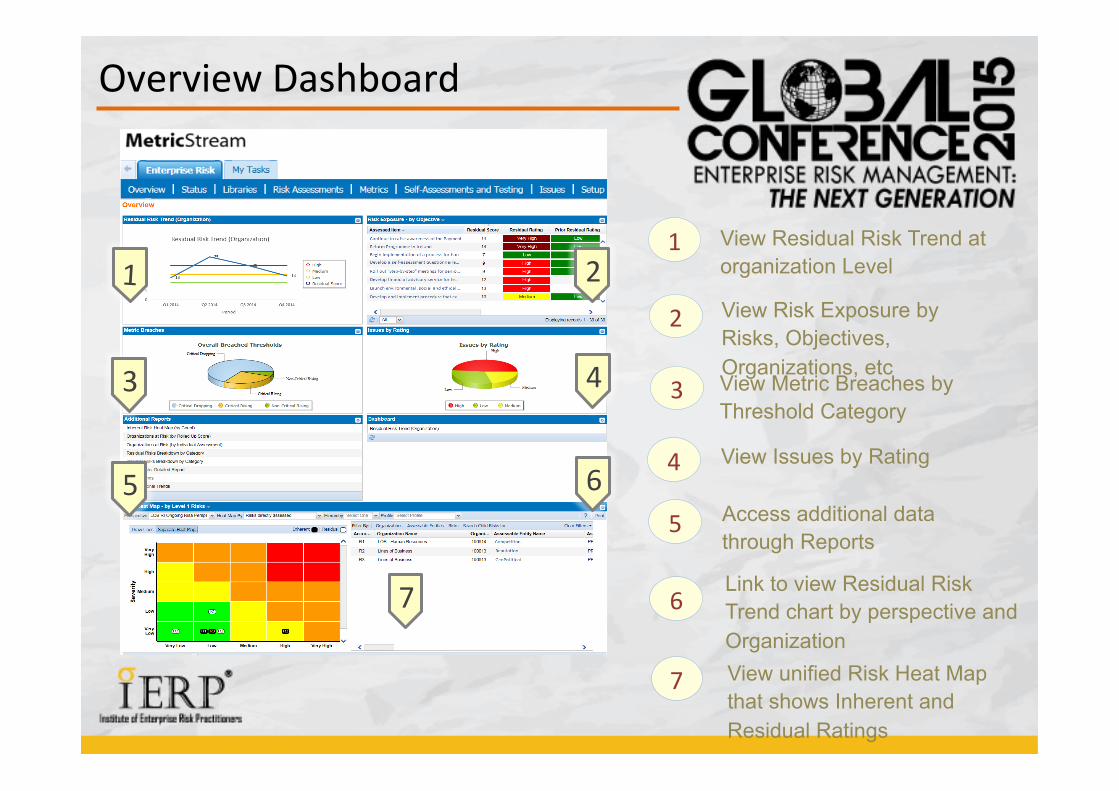

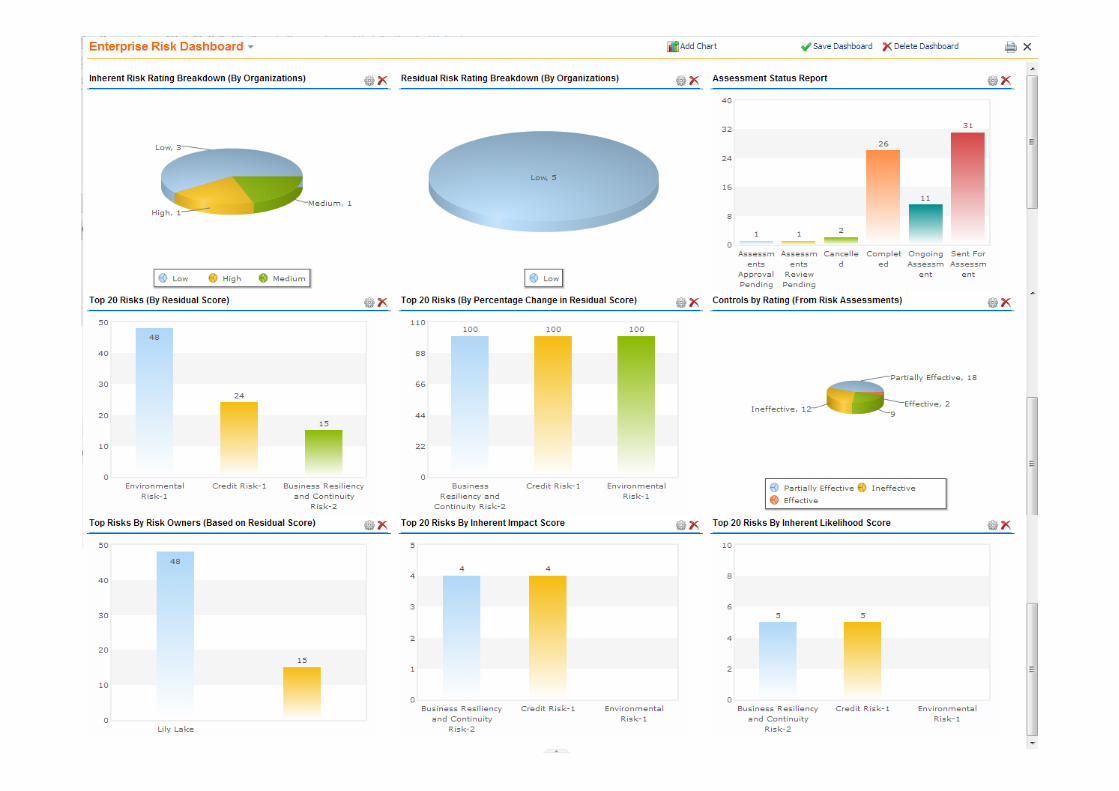

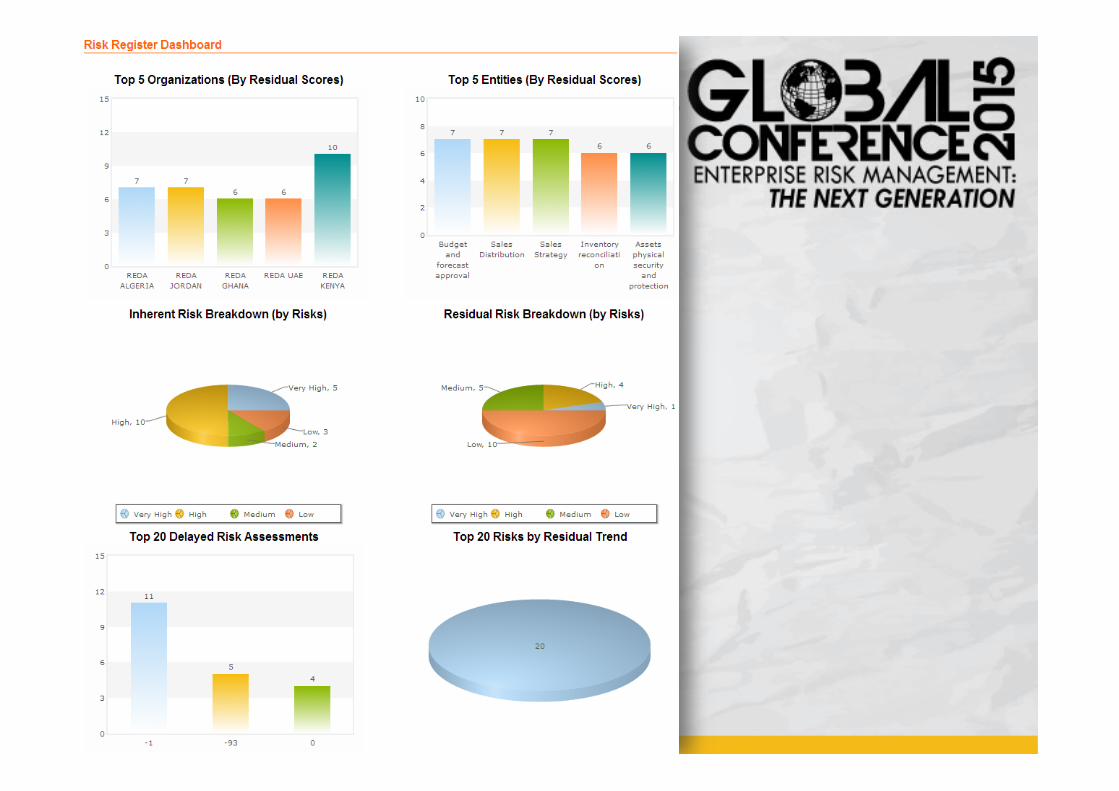

Overview Dashboard

1 2

3 4

5

1 View Residual Risk Trend at organization Level

2 View Risk Exposure by Risks, Objectives, Organizations, etc

3

4

View Metric Breaches by Threshold Category

5

View Issues by Rating

6

Access additional data through Reports

6

7 Link to view Residual Risk Trend chart by perspective and Organization

7 View unified Risk Heat Map that shows Inherent and Residual Ratings

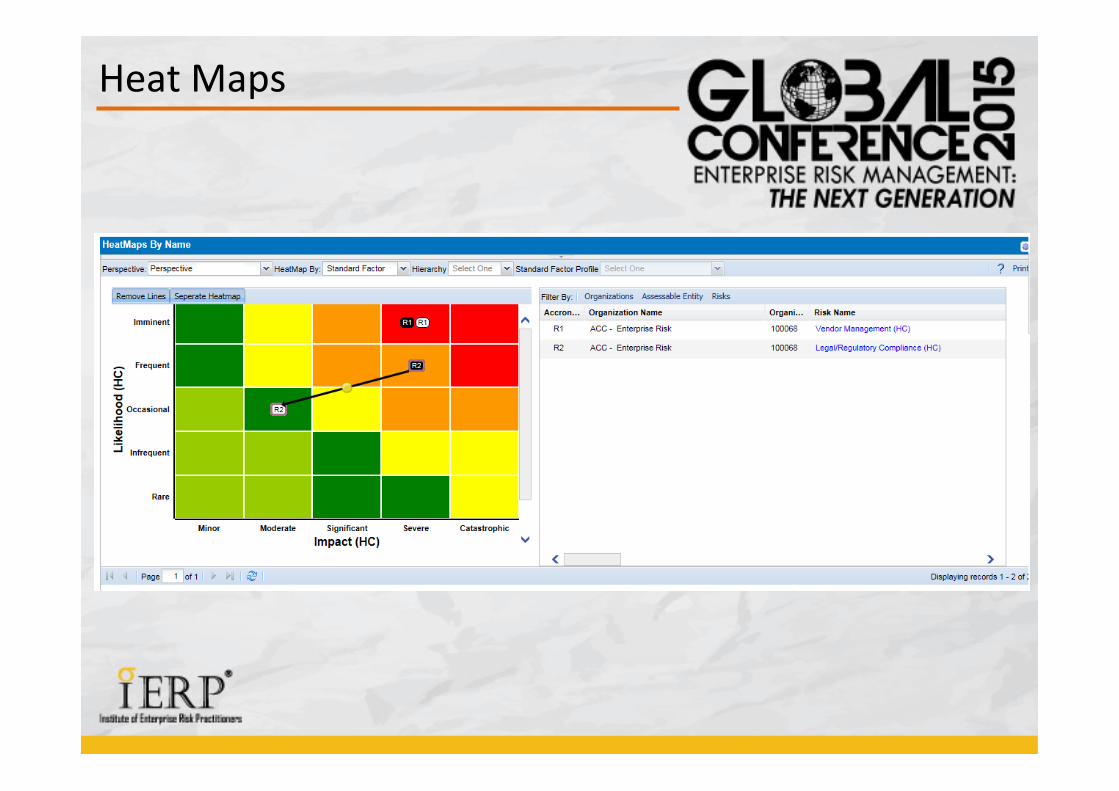

Heat Maps

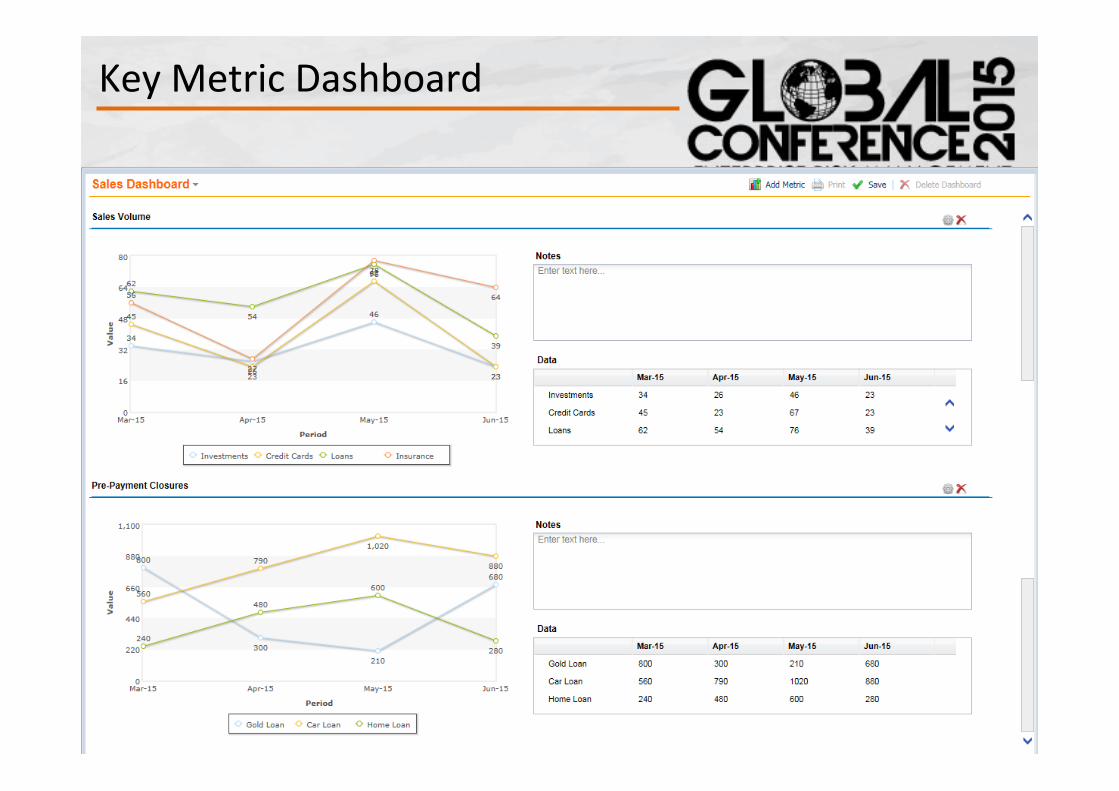

Key Metric Dashboard

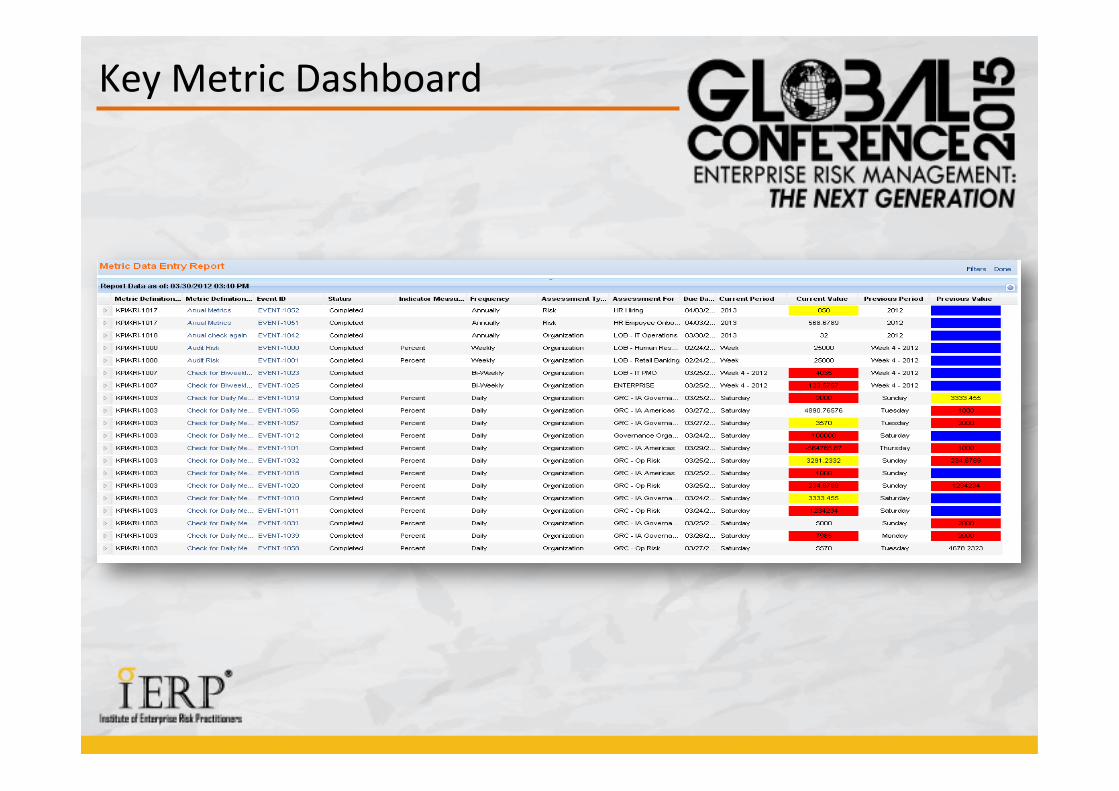

Key Metric Dashboard

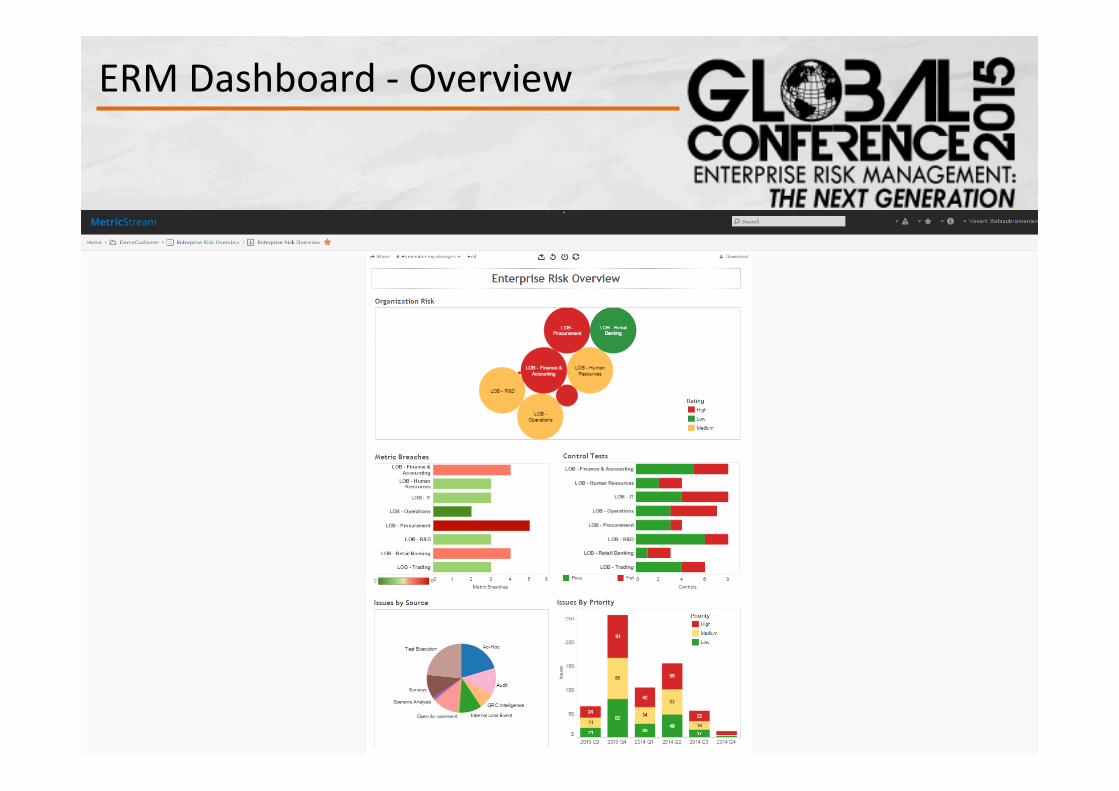

ERM Dashboard -‐ Overview

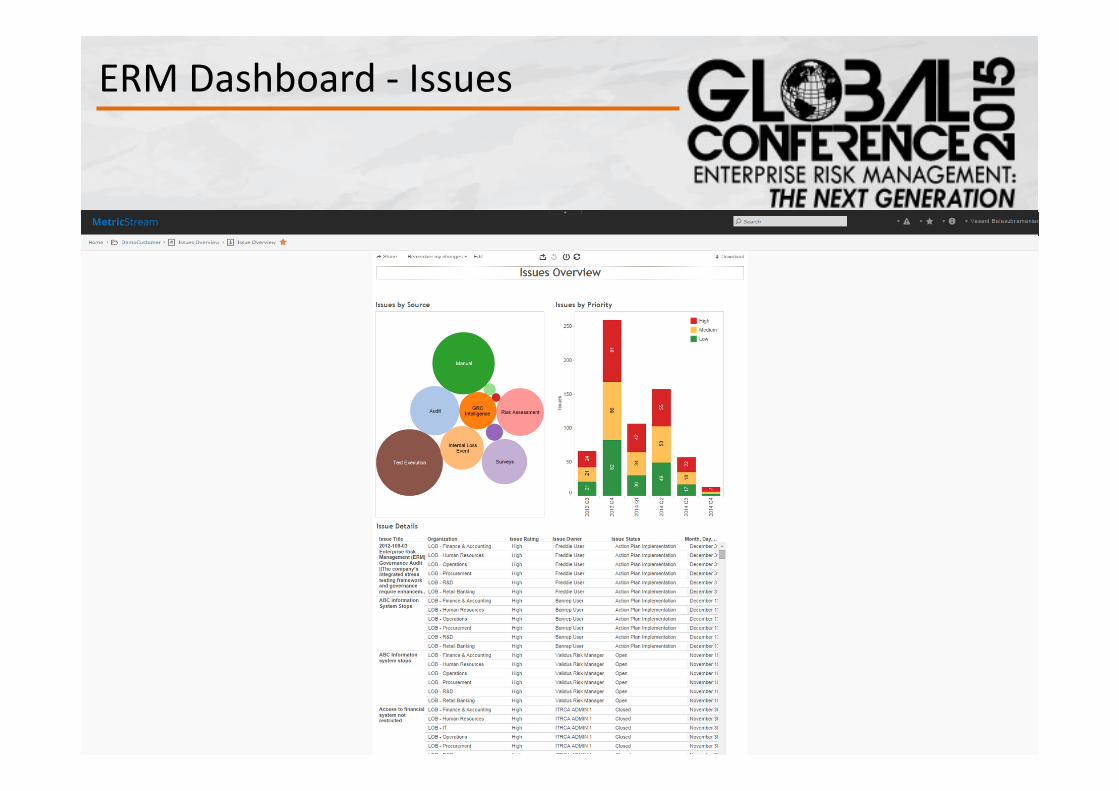

ERM Dashboard -‐ Issues

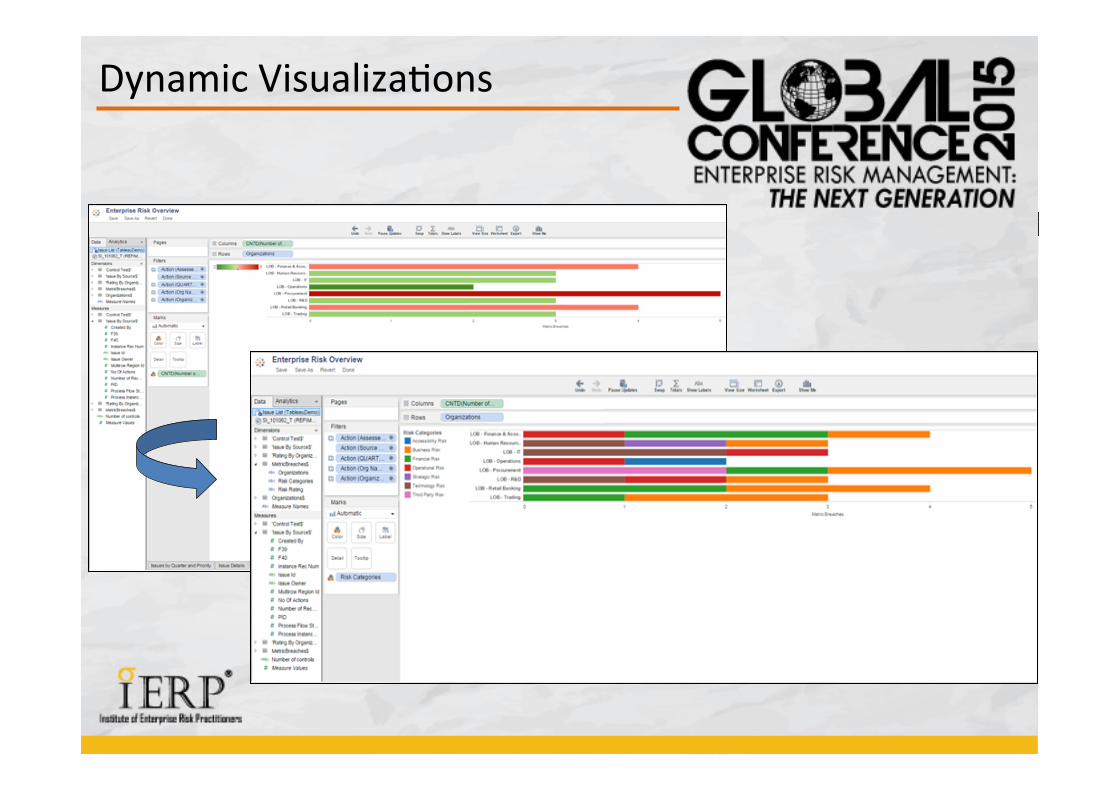

Dynamic Visualiza&ons

Dynamic Visualiza&ons

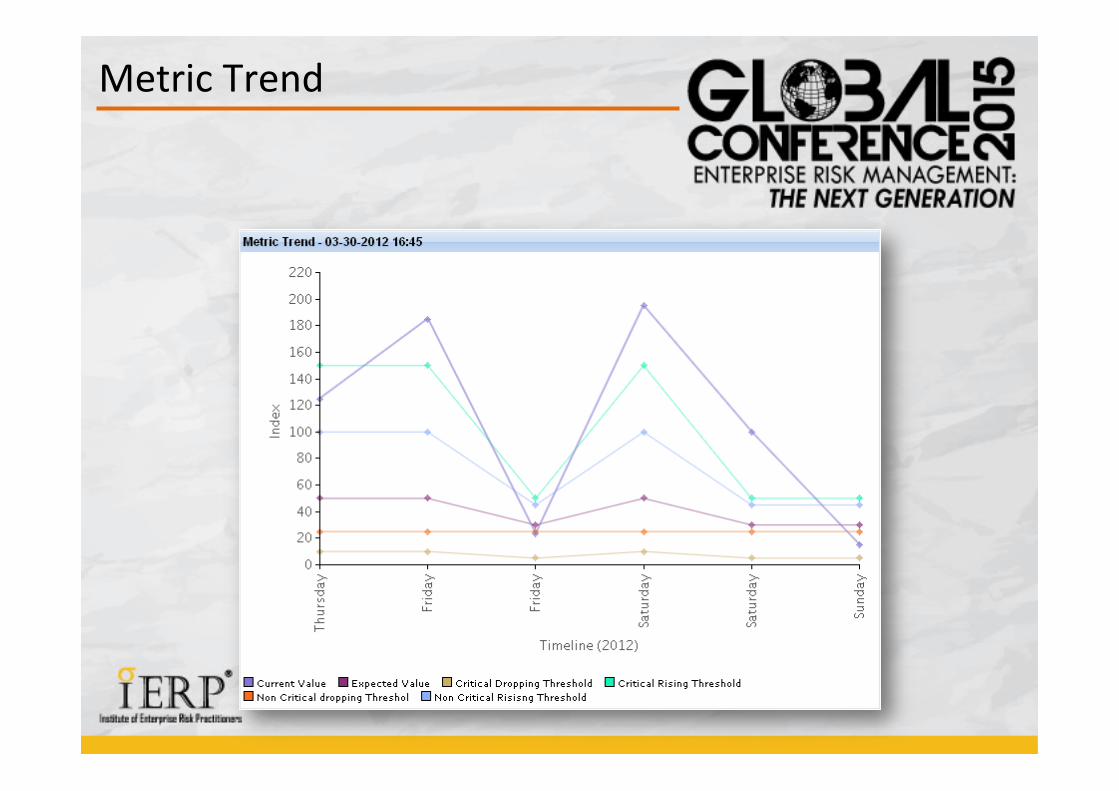

Metric Trend

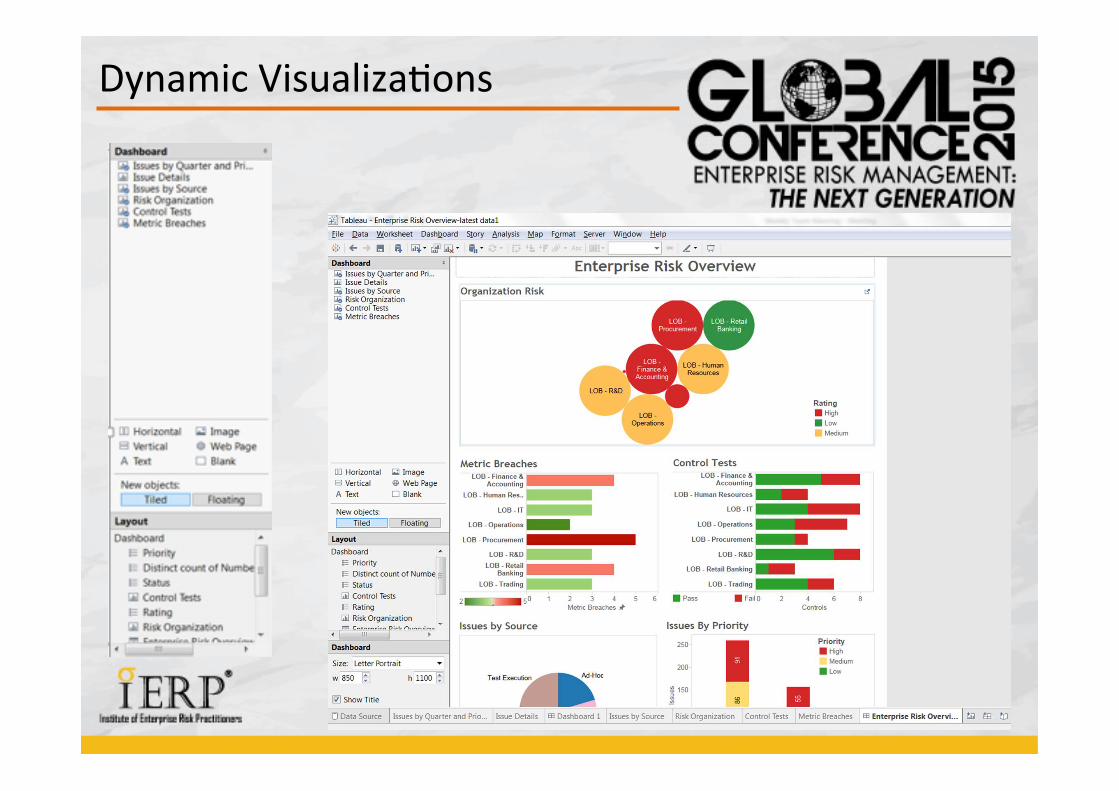

Dynamic Visualiza&ons

Dynamic Visualiza&ons

Benefits & Value Adds

46

Ø Enables Regulatory compliance in terms of iden&fica&on, measurement, mi&ga&on and management of risk

Ø Brining in process efficiencies, improved SLA and turn around &mes Ø Targeted ac&ons – in acquisi&ons or marke&ng promo&ons or risk mi&ga&on

ac&vi&es Ø Ability to make more accurate provisions to safe guard the capital Ø Improvement in overall quality of customers – resul&ng in lower cost of credit and

higher margins net of risk Ø Enables differen&a&on – whom to target, which customers, what products, pricing,

limits etc Ø Speed to market and ability to calibrate products and offerings in a nimble way Ø More transparent decision – to stakeholders, customers and staff Ø Predic&ve forward looking analy&c solu&ons enable management from taking

Reac&ve to a Proac&ve decision