Embed Size (px)

Citation preview

An Overview of the Financial SystemMoney and Banking

Cesar E. TamayoDepartment of Economics, Rutgers University

July 12, 2011

C.E. Tamayo () Econ - 301 July 12, 2011 1 / 18

Program

ReCap

Structure and key concepts (cont.)

Financial intermediaries

Regulation and intervention

C.E. Tamayo () Econ - 301 July 12, 2011 2 / 18

ReCap

Financial markets (fundamental) role: channel funds fromunproductive to productive use (e.g., consumption smoothing,investment in R&D, etc).

Funds are the relevant quantities and interest rates are the relevantprices.

Financial institutions are the key players: banks are the oldest but notthe only ones.

Direct and indirect finance.

Financial instruments: borrower/lender contracts, bonds, stocks andcurrencies.

Term structure: maturity of financial instruments.

C.E. Tamayo () Econ - 301 July 12, 2011 3 / 18

ReCap

Financial markets (fundamental) role: channel funds fromunproductive to productive use (e.g., consumption smoothing,investment in R&D, etc).

Funds are the relevant quantities and interest rates are the relevantprices.

Financial institutions are the key players: banks are the oldest but notthe only ones.

Direct and indirect finance.

Financial instruments: borrower/lender contracts, bonds, stocks andcurrencies.

Term structure: maturity of financial instruments.

C.E. Tamayo () Econ - 301 July 12, 2011 3 / 18

ReCap

Financial markets (fundamental) role: channel funds fromunproductive to productive use (e.g., consumption smoothing,investment in R&D, etc).

Funds are the relevant quantities and interest rates are the relevantprices.

Financial institutions are the key players: banks are the oldest but notthe only ones.

Direct and indirect finance.

Financial instruments: borrower/lender contracts, bonds, stocks andcurrencies.

Term structure: maturity of financial instruments.

C.E. Tamayo () Econ - 301 July 12, 2011 3 / 18

ReCap

Financial markets (fundamental) role: channel funds fromunproductive to productive use (e.g., consumption smoothing,investment in R&D, etc).

Funds are the relevant quantities and interest rates are the relevantprices.

Financial institutions are the key players: banks are the oldest but notthe only ones.

Direct and indirect finance.

Financial instruments: borrower/lender contracts, bonds, stocks andcurrencies.

Term structure: maturity of financial instruments.

C.E. Tamayo () Econ - 301 July 12, 2011 3 / 18

ReCap

Financial markets (fundamental) role: channel funds fromunproductive to productive use (e.g., consumption smoothing,investment in R&D, etc).

Funds are the relevant quantities and interest rates are the relevantprices.

Financial institutions are the key players: banks are the oldest but notthe only ones.

Direct and indirect finance.

Financial instruments: borrower/lender contracts, bonds, stocks andcurrencies.

Term structure: maturity of financial instruments.

C.E. Tamayo () Econ - 301 July 12, 2011 3 / 18

ReCap

Financial markets (fundamental) role: channel funds fromunproductive to productive use (e.g., consumption smoothing,investment in R&D, etc).

Funds are the relevant quantities and interest rates are the relevantprices.

Financial institutions are the key players: banks are the oldest but notthe only ones.

Direct and indirect finance.

Financial instruments: borrower/lender contracts, bonds, stocks andcurrencies.

Term structure: maturity of financial instruments.

C.E. Tamayo () Econ - 301 July 12, 2011 3 / 18

Structure and key concepts (cont.)

Financial intermediaries help reduce transaction costs: time andmoney spent on carrying out transactions.

ExampleSuppose you have $100k to spare. Finding out a potential borrower forthat kind of money will cost you time and money. That is, for the actualtransaction (loan) to take place you will have to use some resources.

Financial intermediaries provide liquidity services

ExampleChecking accounts provide you with funds whenever you need them;simply write a check to play your bills instantly..

Risk and risk sharing: uncertainty about your investment.and itsreturn.Portfolio diversification: use a collection of different assets whosereturns do not move closely together in order to reduce overall risk.

C.E. Tamayo () Econ - 301 July 12, 2011 4 / 18

Structure and key concepts (cont.)

Financial intermediaries help reduce transaction costs: time andmoney spent on carrying out transactions.

ExampleSuppose you have $100k to spare. Finding out a potential borrower forthat kind of money will cost you time and money. That is, for the actualtransaction (loan) to take place you will have to use some resources.

Financial intermediaries provide liquidity services

ExampleChecking accounts provide you with funds whenever you need them;simply write a check to play your bills instantly..

Risk and risk sharing: uncertainty about your investment.and itsreturn.Portfolio diversification: use a collection of different assets whosereturns do not move closely together in order to reduce overall risk.

C.E. Tamayo () Econ - 301 July 12, 2011 4 / 18

Structure and key concepts (cont.)

Financial intermediaries help reduce transaction costs: time andmoney spent on carrying out transactions.

ExampleSuppose you have $100k to spare. Finding out a potential borrower forthat kind of money will cost you time and money. That is, for the actualtransaction (loan) to take place you will have to use some resources.

Financial intermediaries provide liquidity services

ExampleChecking accounts provide you with funds whenever you need them;simply write a check to play your bills instantly..

Risk and risk sharing: uncertainty about your investment.and itsreturn.Portfolio diversification: use a collection of different assets whosereturns do not move closely together in order to reduce overall risk.

C.E. Tamayo () Econ - 301 July 12, 2011 4 / 18

Structure and key concepts (cont.)

Financial intermediaries help reduce transaction costs: time andmoney spent on carrying out transactions.

ExampleSuppose you have $100k to spare. Finding out a potential borrower forthat kind of money will cost you time and money. That is, for the actualtransaction (loan) to take place you will have to use some resources.

Financial intermediaries provide liquidity services

ExampleChecking accounts provide you with funds whenever you need them;simply write a check to play your bills instantly..

Risk and risk sharing: uncertainty about your investment.and itsreturn.Portfolio diversification: use a collection of different assets whosereturns do not move closely together in order to reduce overall risk.

C.E. Tamayo () Econ - 301 July 12, 2011 4 / 18

Structure and key concepts (cont.)

Financial intermediaries help reduce transaction costs: time andmoney spent on carrying out transactions.

ExampleSuppose you have $100k to spare. Finding out a potential borrower forthat kind of money will cost you time and money. That is, for the actualtransaction (loan) to take place you will have to use some resources.

Financial intermediaries provide liquidity services

ExampleChecking accounts provide you with funds whenever you need them;simply write a check to play your bills instantly..

Risk and risk sharing: uncertainty about your investment.and itsreturn.

Portfolio diversification: use a collection of different assets whosereturns do not move closely together in order to reduce overall risk.

C.E. Tamayo () Econ - 301 July 12, 2011 4 / 18

Structure and key concepts (cont.)

Financial intermediaries help reduce transaction costs: time andmoney spent on carrying out transactions.

ExampleSuppose you have $100k to spare. Finding out a potential borrower forthat kind of money will cost you time and money. That is, for the actualtransaction (loan) to take place you will have to use some resources.

Financial intermediaries provide liquidity services

ExampleChecking accounts provide you with funds whenever you need them;simply write a check to play your bills instantly..

Risk and risk sharing: uncertainty about your investment.and itsreturn.Portfolio diversification: use a collection of different assets whosereturns do not move closely together in order to reduce overall risk.C.E. Tamayo () Econ - 301 July 12, 2011 4 / 18

Structure and key concepts (cont.)

Portfolio diversification: where would you rather be?

C.E. Tamayo () Econ - 301 July 12, 2011 5 / 18

Structure and key concepts (cont.)

Primary market: where investors purchase securities directly fromthe issuer

The process of selling new issues to investors is called underwriting(investment banks).

In the case of a new stock issue, this sale is an initial public offering(IPO).

Secondary market: where investors buy securities from otherinvestors.

The stock exchanges and over-the-counter markets are the mostprominent examples secondary markets.

C.E. Tamayo () Econ - 301 July 12, 2011 6 / 18

Structure and key concepts (cont.)

Primary market: where investors purchase securities directly fromthe issuer

The process of selling new issues to investors is called underwriting(investment banks).

In the case of a new stock issue, this sale is an initial public offering(IPO).

Secondary market: where investors buy securities from otherinvestors.

The stock exchanges and over-the-counter markets are the mostprominent examples secondary markets.

C.E. Tamayo () Econ - 301 July 12, 2011 6 / 18

Structure and key concepts (cont.)

Primary market: where investors purchase securities directly fromthe issuer

The process of selling new issues to investors is called underwriting(investment banks).

In the case of a new stock issue, this sale is an initial public offering(IPO).

Secondary market: where investors buy securities from otherinvestors.

The stock exchanges and over-the-counter markets are the mostprominent examples secondary markets.

C.E. Tamayo () Econ - 301 July 12, 2011 6 / 18

Structure and key concepts (cont.)

Primary market: where investors purchase securities directly fromthe issuer

The process of selling new issues to investors is called underwriting(investment banks).

In the case of a new stock issue, this sale is an initial public offering(IPO).

Secondary market: where investors buy securities from otherinvestors.

The stock exchanges and over-the-counter markets are the mostprominent examples secondary markets.

C.E. Tamayo () Econ - 301 July 12, 2011 6 / 18

Structure and key concepts (cont.)

Primary market: where investors purchase securities directly fromthe issuer

The process of selling new issues to investors is called underwriting(investment banks).

In the case of a new stock issue, this sale is an initial public offering(IPO).

Secondary market: where investors buy securities from otherinvestors.

The stock exchanges and over-the-counter markets are the mostprominent examples secondary markets.

C.E. Tamayo () Econ - 301 July 12, 2011 6 / 18

Structure and key concepts (cont.)

Money market: where short term debt instruments are traded.

Money market rates:

Prime rate: interest on corporate bank loansFed funds rate: overnight loans in the FF market (bank-to-bank loans)T-bill rate: interest on US short term bonds ("treasury bills")

Capital market: where long term debt and equity instruments aretraded

Examples of instruments traded in CM are corporate stocks,mortgages, long-term corporate and government bonds

C.E. Tamayo () Econ - 301 July 12, 2011 7 / 18

Structure and key concepts (cont.)

Money market: where short term debt instruments are traded.

Money market rates:

Prime rate: interest on corporate bank loansFed funds rate: overnight loans in the FF market (bank-to-bank loans)T-bill rate: interest on US short term bonds ("treasury bills")

Capital market: where long term debt and equity instruments aretraded

Examples of instruments traded in CM are corporate stocks,mortgages, long-term corporate and government bonds

C.E. Tamayo () Econ - 301 July 12, 2011 7 / 18

Structure and key concepts (cont.)

Money market: where short term debt instruments are traded.

Money market rates:

Prime rate: interest on corporate bank loans

Fed funds rate: overnight loans in the FF market (bank-to-bank loans)T-bill rate: interest on US short term bonds ("treasury bills")

Capital market: where long term debt and equity instruments aretraded

Examples of instruments traded in CM are corporate stocks,mortgages, long-term corporate and government bonds

C.E. Tamayo () Econ - 301 July 12, 2011 7 / 18

Structure and key concepts (cont.)

Money market: where short term debt instruments are traded.

Money market rates:

Prime rate: interest on corporate bank loansFed funds rate: overnight loans in the FF market (bank-to-bank loans)

T-bill rate: interest on US short term bonds ("treasury bills")

Capital market: where long term debt and equity instruments aretraded

Examples of instruments traded in CM are corporate stocks,mortgages, long-term corporate and government bonds

C.E. Tamayo () Econ - 301 July 12, 2011 7 / 18

Structure and key concepts (cont.)

Money market: where short term debt instruments are traded.

Money market rates:

Prime rate: interest on corporate bank loansFed funds rate: overnight loans in the FF market (bank-to-bank loans)T-bill rate: interest on US short term bonds ("treasury bills")

Capital market: where long term debt and equity instruments aretraded

Examples of instruments traded in CM are corporate stocks,mortgages, long-term corporate and government bonds

C.E. Tamayo () Econ - 301 July 12, 2011 7 / 18

Structure and key concepts (cont.)

Money market: where short term debt instruments are traded.

Money market rates:

Prime rate: interest on corporate bank loansFed funds rate: overnight loans in the FF market (bank-to-bank loans)T-bill rate: interest on US short term bonds ("treasury bills")

Capital market: where long term debt and equity instruments aretraded

Examples of instruments traded in CM are corporate stocks,mortgages, long-term corporate and government bonds

C.E. Tamayo () Econ - 301 July 12, 2011 7 / 18

Structure and key concepts (cont.)

Money market: where short term debt instruments are traded.

Money market rates:

Prime rate: interest on corporate bank loansFed funds rate: overnight loans in the FF market (bank-to-bank loans)T-bill rate: interest on US short term bonds ("treasury bills")

Capital market: where long term debt and equity instruments aretraded

Examples of instruments traded in CM are corporate stocks,mortgages, long-term corporate and government bonds

C.E. Tamayo () Econ - 301 July 12, 2011 7 / 18

Structure and key concepts (cont.)

Over-the-counter (OTC): individual dealers contact each other withbuy/sell offers

Stock markets: everyone comes to the same "place" to trade.(e.g.NYSE, LSE)

Indexes: group large sets of assets into a representative measure ofthe performance of the individual assets.

Examples are:

DJI: how 30 large, publicly owned companies based in the US havetraded during a standard trading session NYSE.S&P500: 500 large-cap common stocks trading on either NYSE orNasdaqNikkei: 225 stocks of the first section of the Tokyo Stock Exchange

C.E. Tamayo () Econ - 301 July 12, 2011 8 / 18

Structure and key concepts (cont.)

Over-the-counter (OTC): individual dealers contact each other withbuy/sell offers

Stock markets: everyone comes to the same "place" to trade.(e.g.NYSE, LSE)

Indexes: group large sets of assets into a representative measure ofthe performance of the individual assets.

Examples are:

DJI: how 30 large, publicly owned companies based in the US havetraded during a standard trading session NYSE.S&P500: 500 large-cap common stocks trading on either NYSE orNasdaqNikkei: 225 stocks of the first section of the Tokyo Stock Exchange

C.E. Tamayo () Econ - 301 July 12, 2011 8 / 18

Structure and key concepts (cont.)

Over-the-counter (OTC): individual dealers contact each other withbuy/sell offers

Stock markets: everyone comes to the same "place" to trade.(e.g.NYSE, LSE)

Indexes: group large sets of assets into a representative measure ofthe performance of the individual assets.

Examples are:

DJI: how 30 large, publicly owned companies based in the US havetraded during a standard trading session NYSE.S&P500: 500 large-cap common stocks trading on either NYSE orNasdaqNikkei: 225 stocks of the first section of the Tokyo Stock Exchange

C.E. Tamayo () Econ - 301 July 12, 2011 8 / 18

Structure and key concepts (cont.)

Over-the-counter (OTC): individual dealers contact each other withbuy/sell offers

Stock markets: everyone comes to the same "place" to trade.(e.g.NYSE, LSE)

Indexes: group large sets of assets into a representative measure ofthe performance of the individual assets.

Examples are:

DJI: how 30 large, publicly owned companies based in the US havetraded during a standard trading session NYSE.S&P500: 500 large-cap common stocks trading on either NYSE orNasdaqNikkei: 225 stocks of the first section of the Tokyo Stock Exchange

C.E. Tamayo () Econ - 301 July 12, 2011 8 / 18

Structure and key concepts (cont.)

Over-the-counter (OTC): individual dealers contact each other withbuy/sell offers

Stock markets: everyone comes to the same "place" to trade.(e.g.NYSE, LSE)

Indexes: group large sets of assets into a representative measure ofthe performance of the individual assets.

Examples are:

DJI: how 30 large, publicly owned companies based in the US havetraded during a standard trading session NYSE.

S&P500: 500 large-cap common stocks trading on either NYSE orNasdaqNikkei: 225 stocks of the first section of the Tokyo Stock Exchange

C.E. Tamayo () Econ - 301 July 12, 2011 8 / 18

Structure and key concepts (cont.)

Over-the-counter (OTC): individual dealers contact each other withbuy/sell offers

Stock markets: everyone comes to the same "place" to trade.(e.g.NYSE, LSE)

Indexes: group large sets of assets into a representative measure ofthe performance of the individual assets.

Examples are:

DJI: how 30 large, publicly owned companies based in the US havetraded during a standard trading session NYSE.S&P500: 500 large-cap common stocks trading on either NYSE orNasdaq

Nikkei: 225 stocks of the first section of the Tokyo Stock Exchange

C.E. Tamayo () Econ - 301 July 12, 2011 8 / 18

Structure and key concepts (cont.)

Over-the-counter (OTC): individual dealers contact each other withbuy/sell offers

Stock markets: everyone comes to the same "place" to trade.(e.g.NYSE, LSE)

Indexes: group large sets of assets into a representative measure ofthe performance of the individual assets.

Examples are:

DJI: how 30 large, publicly owned companies based in the US havetraded during a standard trading session NYSE.S&P500: 500 large-cap common stocks trading on either NYSE orNasdaqNikkei: 225 stocks of the first section of the Tokyo Stock Exchange

C.E. Tamayo () Econ - 301 July 12, 2011 8 / 18

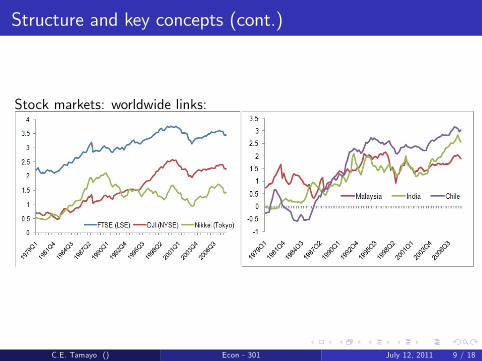

Structure and key concepts (cont.)

Stock markets: worldwide links:

C.E. Tamayo () Econ - 301 July 12, 2011 9 / 18

Financial intermediaries: Depository institutions

Comercial banks: checkable, savings and time deposits, make loans(comercial, consumer and mortgage) and invest on federal and stategovernment bonds.

Thrift institutions (S&Ls): similar to comercial banks but heavilyfocused on mortgage finance

Credit unions: small cooperative S&L institutions whose customersare usually members of a union or an employee association. Heavilyfocused on consumer loans.

C.E. Tamayo () Econ - 301 July 12, 2011 10 / 18

Financial intermediaries: Depository institutions

Comercial banks: checkable, savings and time deposits, make loans(comercial, consumer and mortgage) and invest on federal and stategovernment bonds.

Thrift institutions (S&Ls): similar to comercial banks but heavilyfocused on mortgage finance

Credit unions: small cooperative S&L institutions whose customersare usually members of a union or an employee association. Heavilyfocused on consumer loans.

C.E. Tamayo () Econ - 301 July 12, 2011 10 / 18

Financial intermediaries: Depository institutions

Comercial banks: checkable, savings and time deposits, make loans(comercial, consumer and mortgage) and invest on federal and stategovernment bonds.

Thrift institutions (S&Ls): similar to comercial banks but heavilyfocused on mortgage finance

Credit unions: small cooperative S&L institutions whose customersare usually members of a union or an employee association. Heavilyfocused on consumer loans.

C.E. Tamayo () Econ - 301 July 12, 2011 10 / 18

Financial intermediaries: Contractual savings institutions

Insurance companies: offer coverage against financial loss followingdifferent catastrophic events. They collect premiums and bear the riskof loss.

Pension and retirement funds: collect periodic contributions fromlong-term savers towards retirement benefits.

Finance companies: GE Financial or GM financial/Americredit

Mutual funds: sell shares to investors and use the proceedings topurchase diversified portfolios.

C.E. Tamayo () Econ - 301 July 12, 2011 11 / 18

Financial intermediaries: Contractual savings institutions

Insurance companies: offer coverage against financial loss followingdifferent catastrophic events. They collect premiums and bear the riskof loss.

Pension and retirement funds: collect periodic contributions fromlong-term savers towards retirement benefits.

Finance companies: GE Financial or GM financial/Americredit

Mutual funds: sell shares to investors and use the proceedings topurchase diversified portfolios.

C.E. Tamayo () Econ - 301 July 12, 2011 11 / 18

Financial intermediaries: Contractual savings institutions

Insurance companies: offer coverage against financial loss followingdifferent catastrophic events. They collect premiums and bear the riskof loss.

Pension and retirement funds: collect periodic contributions fromlong-term savers towards retirement benefits.

Finance companies: GE Financial or GM financial/Americredit

Mutual funds: sell shares to investors and use the proceedings topurchase diversified portfolios.

C.E. Tamayo () Econ - 301 July 12, 2011 11 / 18

Financial intermediaries: Contractual savings institutions

Insurance companies: offer coverage against financial loss followingdifferent catastrophic events. They collect premiums and bear the riskof loss.

Pension and retirement funds: collect periodic contributions fromlong-term savers towards retirement benefits.

Finance companies: GE Financial or GM financial/Americredit

Mutual funds: sell shares to investors and use the proceedings topurchase diversified portfolios.

C.E. Tamayo () Econ - 301 July 12, 2011 11 / 18

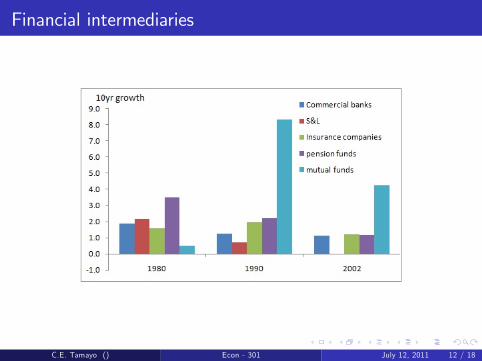

Financial intermediaries

C.E. Tamayo () Econ - 301 July 12, 2011 12 / 18

Regulation and intervention: key ideas

Because some transaction costs are fixed (e.g. setting up anelectronic payment system) and do not depend on the quantitiestraded, financial institutions have incentives to expand theiroperations to exploit economies of scale.

This creates the possibility of concentration (i.e. monopoly power)and so called "too big to fail".

Asymmetric information: in any given transaction, different partiesmay have different information regarding risk and return ofinvestments.

This creates, for instance, the possibility of a bank run; since saversdon’t know precisely the creditworthiness of the financial institution,they may be subject to financial panic and "run" to pull their funds.

C.E. Tamayo () Econ - 301 July 12, 2011 13 / 18

Regulation and intervention: key ideas

Because some transaction costs are fixed (e.g. setting up anelectronic payment system) and do not depend on the quantitiestraded, financial institutions have incentives to expand theiroperations to exploit economies of scale.

This creates the possibility of concentration (i.e. monopoly power)and so called "too big to fail".

Asymmetric information: in any given transaction, different partiesmay have different information regarding risk and return ofinvestments.

This creates, for instance, the possibility of a bank run; since saversdon’t know precisely the creditworthiness of the financial institution,they may be subject to financial panic and "run" to pull their funds.

C.E. Tamayo () Econ - 301 July 12, 2011 13 / 18

Regulation and intervention: key ideas

Because some transaction costs are fixed (e.g. setting up anelectronic payment system) and do not depend on the quantitiestraded, financial institutions have incentives to expand theiroperations to exploit economies of scale.

This creates the possibility of concentration (i.e. monopoly power)and so called "too big to fail".

Asymmetric information: in any given transaction, different partiesmay have different information regarding risk and return ofinvestments.

This creates, for instance, the possibility of a bank run; since saversdon’t know precisely the creditworthiness of the financial institution,they may be subject to financial panic and "run" to pull their funds.

C.E. Tamayo () Econ - 301 July 12, 2011 13 / 18

Regulation and intervention: key ideas

Because some transaction costs are fixed (e.g. setting up anelectronic payment system) and do not depend on the quantitiestraded, financial institutions have incentives to expand theiroperations to exploit economies of scale.

This creates the possibility of concentration (i.e. monopoly power)and so called "too big to fail".

Asymmetric information: in any given transaction, different partiesmay have different information regarding risk and return ofinvestments.

This creates, for instance, the possibility of a bank run; since saversdon’t know precisely the creditworthiness of the financial institution,they may be subject to financial panic and "run" to pull their funds.

C.E. Tamayo () Econ - 301 July 12, 2011 13 / 18

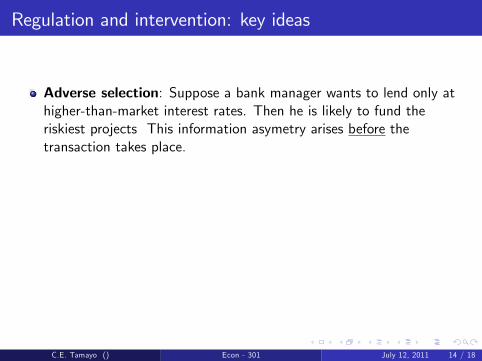

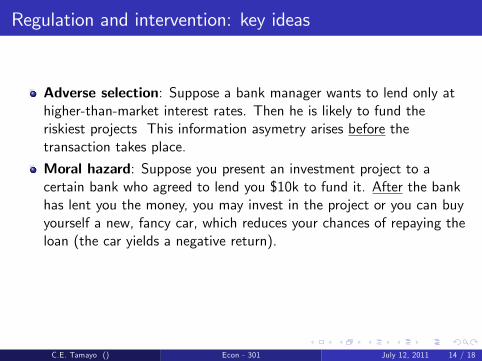

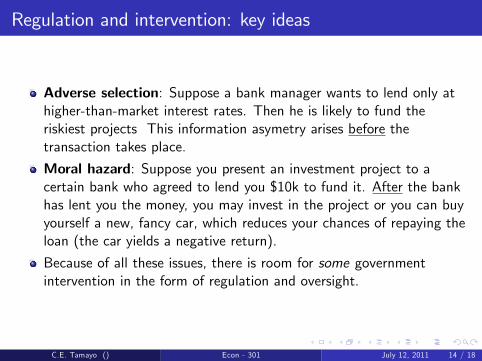

Regulation and intervention: key ideas

Adverse selection: Suppose a bank manager wants to lend only athigher-than-market interest rates. Then he is likely to fund theriskiest projects This information asymetry arises before thetransaction takes place.

Moral hazard: Suppose you present an investment project to acertain bank who agreed to lend you $10k to fund it. After the bankhas lent you the money, you may invest in the project or you can buyyourself a new, fancy car, which reduces your chances of repaying theloan (the car yields a negative return).

Because of all these issues, there is room for some governmentintervention in the form of regulation and oversight.

C.E. Tamayo () Econ - 301 July 12, 2011 14 / 18

Regulation and intervention: key ideas

Adverse selection: Suppose a bank manager wants to lend only athigher-than-market interest rates. Then he is likely to fund theriskiest projects This information asymetry arises before thetransaction takes place.

Moral hazard: Suppose you present an investment project to acertain bank who agreed to lend you $10k to fund it. After the bankhas lent you the money, you may invest in the project or you can buyyourself a new, fancy car, which reduces your chances of repaying theloan (the car yields a negative return).

Because of all these issues, there is room for some governmentintervention in the form of regulation and oversight.

C.E. Tamayo () Econ - 301 July 12, 2011 14 / 18

Regulation and intervention: key ideas

Adverse selection: Suppose a bank manager wants to lend only athigher-than-market interest rates. Then he is likely to fund theriskiest projects This information asymetry arises before thetransaction takes place.

Moral hazard: Suppose you present an investment project to acertain bank who agreed to lend you $10k to fund it. After the bankhas lent you the money, you may invest in the project or you can buyyourself a new, fancy car, which reduces your chances of repaying theloan (the car yields a negative return).

Because of all these issues, there is room for some governmentintervention in the form of regulation and oversight.

C.E. Tamayo () Econ - 301 July 12, 2011 14 / 18

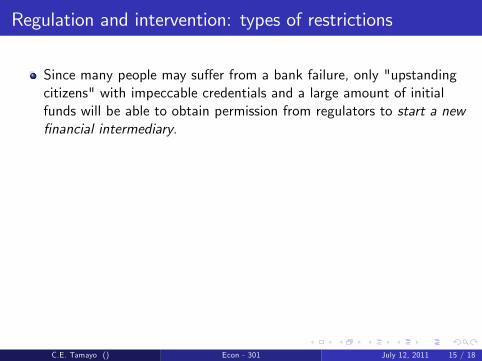

Regulation and intervention: types of restrictions

Since many people may suffer from a bank failure, only "upstandingcitizens" with impeccable credentials and a large amount of initialfunds will be able to obtain permission from regulators to start a newfinancial intermediary.

This results in limits to competition and may create monopoly power.

Thus, in some countries regulators declare upper limits (ceilings) oninterest rates that financial intermediaries can charge.

However, some regulators have also introduced lower limits oninterest rates that intermediaries pay on deposits, further reducing(price) competition.

Because some financial intermediaries hold people’s money, regulatorsthink it wise to impose restrictions on the kind of assets (i.e. on theamount of risk) that can be purchased with people’s money

C.E. Tamayo () Econ - 301 July 12, 2011 15 / 18

Regulation and intervention: types of restrictions

Since many people may suffer from a bank failure, only "upstandingcitizens" with impeccable credentials and a large amount of initialfunds will be able to obtain permission from regulators to start a newfinancial intermediary.

This results in limits to competition and may create monopoly power.

Thus, in some countries regulators declare upper limits (ceilings) oninterest rates that financial intermediaries can charge.

However, some regulators have also introduced lower limits oninterest rates that intermediaries pay on deposits, further reducing(price) competition.

Because some financial intermediaries hold people’s money, regulatorsthink it wise to impose restrictions on the kind of assets (i.e. on theamount of risk) that can be purchased with people’s money

C.E. Tamayo () Econ - 301 July 12, 2011 15 / 18

Regulation and intervention: types of restrictions

Since many people may suffer from a bank failure, only "upstandingcitizens" with impeccable credentials and a large amount of initialfunds will be able to obtain permission from regulators to start a newfinancial intermediary.

This results in limits to competition and may create monopoly power.

Thus, in some countries regulators declare upper limits (ceilings) oninterest rates that financial intermediaries can charge.

However, some regulators have also introduced lower limits oninterest rates that intermediaries pay on deposits, further reducing(price) competition.

Because some financial intermediaries hold people’s money, regulatorsthink it wise to impose restrictions on the kind of assets (i.e. on theamount of risk) that can be purchased with people’s money

C.E. Tamayo () Econ - 301 July 12, 2011 15 / 18

Regulation and intervention: types of restrictions

Since many people may suffer from a bank failure, only "upstandingcitizens" with impeccable credentials and a large amount of initialfunds will be able to obtain permission from regulators to start a newfinancial intermediary.

This results in limits to competition and may create monopoly power.

Thus, in some countries regulators declare upper limits (ceilings) oninterest rates that financial intermediaries can charge.

However, some regulators have also introduced lower limits oninterest rates that intermediaries pay on deposits, further reducing(price) competition.

Because some financial intermediaries hold people’s money, regulatorsthink it wise to impose restrictions on the kind of assets (i.e. on theamount of risk) that can be purchased with people’s money

C.E. Tamayo () Econ - 301 July 12, 2011 15 / 18

Regulation and intervention: types of restrictions

Since many people may suffer from a bank failure, only "upstandingcitizens" with impeccable credentials and a large amount of initialfunds will be able to obtain permission from regulators to start a newfinancial intermediary.

This results in limits to competition and may create monopoly power.

Thus, in some countries regulators declare upper limits (ceilings) oninterest rates that financial intermediaries can charge.

However, some regulators have also introduced lower limits oninterest rates that intermediaries pay on deposits, further reducing(price) competition.

Because some financial intermediaries hold people’s money, regulatorsthink it wise to impose restrictions on the kind of assets (i.e. on theamount of risk) that can be purchased with people’s money

C.E. Tamayo () Econ - 301 July 12, 2011 15 / 18

Regulation and intervention

Disclosure: in an effort to reduce the degree of informationasymmetry.regulators have imposed stringent reporting requirementsfor financial intermediaries; they must follow standardized accountingpractices and must make some information available for the public.

Deposit insurance: The government offers some form of insurance tomost deposits we hold in financial institutions. The most importantsource of insurance being the Federal Deposit Insurance Corporation.This a somewhat recent feature; prior to 1934 most deposits were notinsured and people’s savings were usually lost when banks failed.

C.E. Tamayo () Econ - 301 July 12, 2011 16 / 18

Regulation and intervention

Disclosure: in an effort to reduce the degree of informationasymmetry.regulators have imposed stringent reporting requirementsfor financial intermediaries; they must follow standardized accountingpractices and must make some information available for the public.

Deposit insurance: The government offers some form of insurance tomost deposits we hold in financial institutions. The most importantsource of insurance being the Federal Deposit Insurance Corporation.This a somewhat recent feature; prior to 1934 most deposits were notinsured and people’s savings were usually lost when banks failed.

C.E. Tamayo () Econ - 301 July 12, 2011 16 / 18

Regulation and intervention

C.E. Tamayo () Econ - 301 July 12, 2011 17 / 18

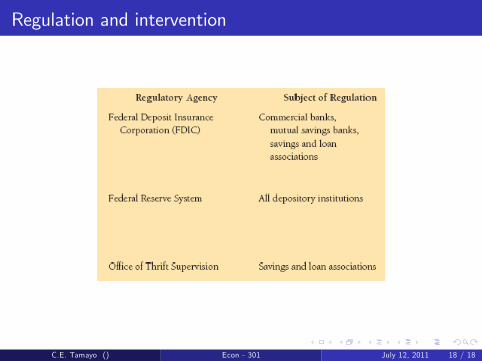

Regulation and intervention

C.E. Tamayo () Econ - 301 July 12, 2011 18 / 18

![Assessing central bank credibility during the ERM crises ...econweb.rutgers.edu/mizrach/pubs/[26]-2006_JFS.pdf · Assessing central bank credibility during the ... rates provide useful](https://img.pdfslide.us/doc/110x75/5aa343c77f8b9ac67a8e2663/assessing-central-bank-credibility-during-the-erm-crises-26-2006jfspdfassessing.jpg)