Embed Size (px)

DESCRIPTION

An overview of fiscal decentralisation : theory and practice. Harmonisation, Decentralisation and Local Governance. Session overview. Understanding the context of fiscal decentralisation Assigning expenditure responsibilities Instruments for financing local government - PowerPoint PPT Presentation

Citation preview

Harmonisation, Decentralisation and Local Governance

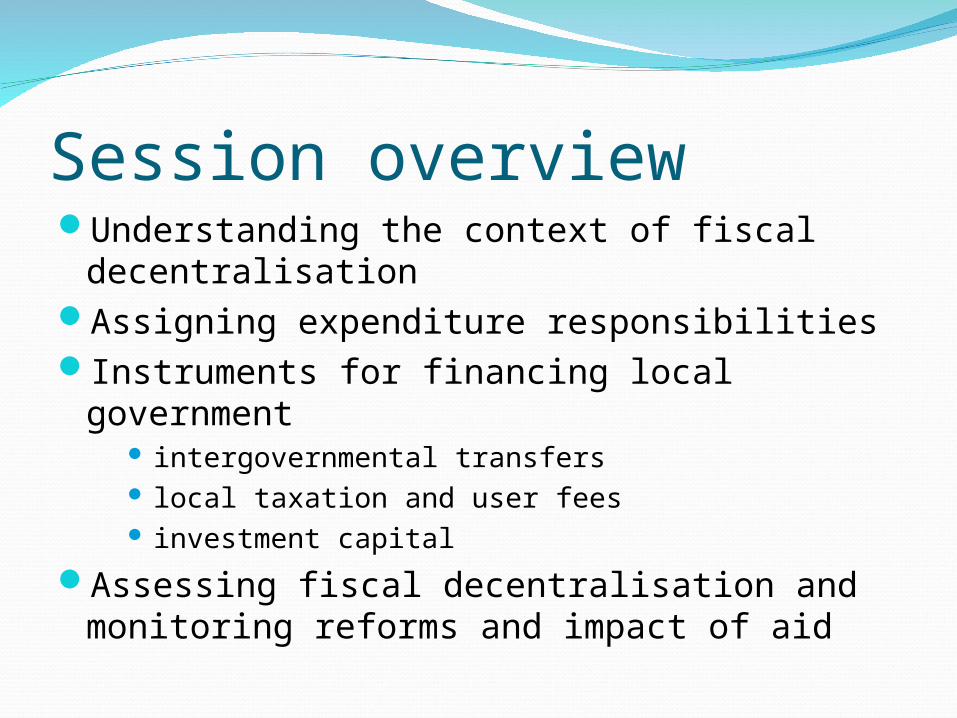

Session overviewUnderstanding the context of fiscal

decentralisationAssigning expenditure responsibilitiesInstruments for financing local government

intergovernmental transfers local taxation and user fees investment capital

Assessing fiscal decentralisation and monitoring reforms and impact of aid

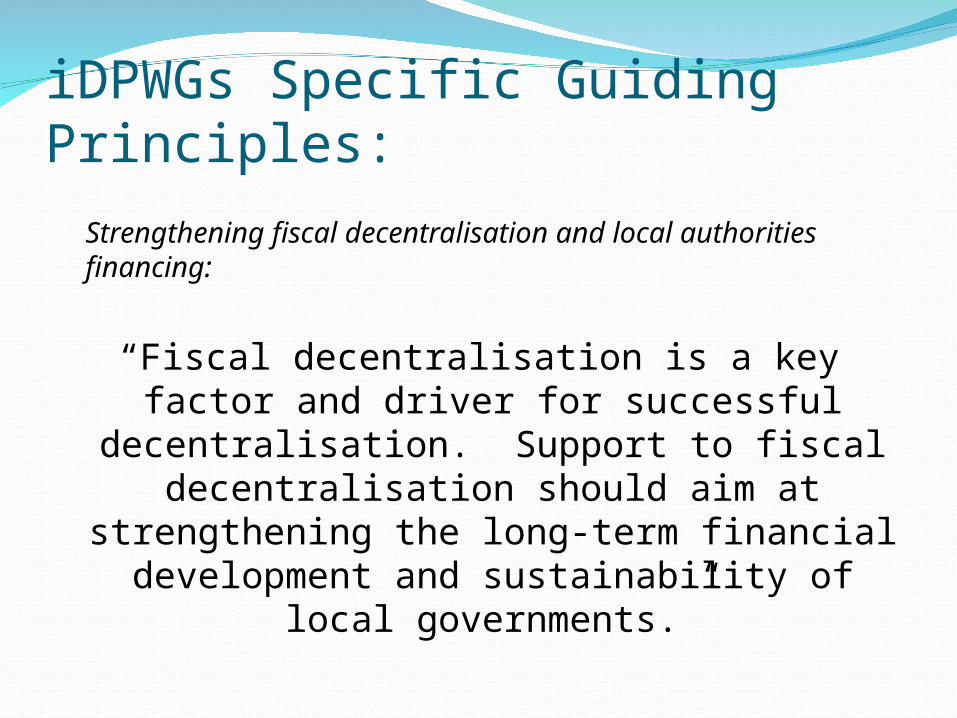

iDPWGs Specific Guiding Principles:Strengthening fiscal decentralisation and local authorities financing:

“Fiscal decentralisation is a key factor and driver for successful decentralisation.

Support to fiscal decentralisation should aim at strengthening the long-term

financial development and sustainability of local governments.”

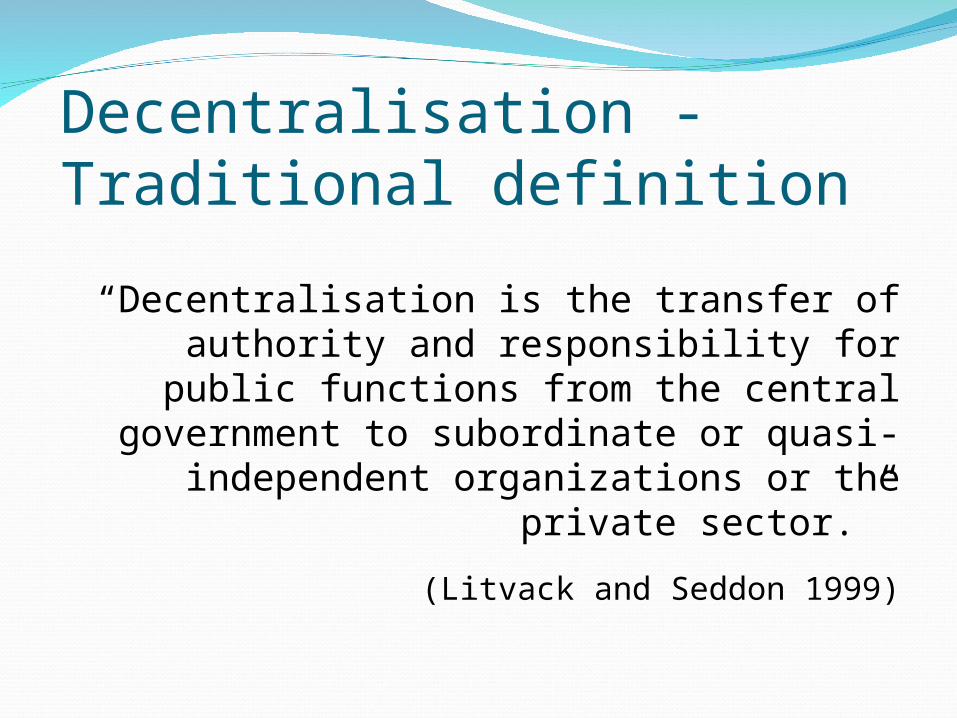

Decentralisation - Traditional definition

“Decentralisation is the transfer of authority and responsibility for public

functions from the central government to subordinate or quasi-independent

organizations or the private sector.”

(Litvack and Seddon 1999)

Why (fiscal) decentralisation?Inefficient centralisation (largely theoretical)

Unable to accommodate differences in local needs and preferences

Inefficient taxation: poor match between government services and tax costs

Excessive centralisation inhibits growth

Improve public services, reduce poverty and encourage economic development

Local governments have better info on local needs / incentives for more responsive government

Fiscal incentives for regional development

Why (fiscal) decentralization? (Continued)Governance-driven decentralization: Greater

accountability at the local government level to provide

Local governments have grown up

Politically driven decentralization: Autonomy versus dissolution

Some observations about fiscal decentralisation around the worldIt is often history and politics -not economics-

that determines subnational government structure and drives fiscal decentralisation reforms

Many fiscal decentralisation reforms shifted the financial resources to the local government level, but failed to decentralise the discretion to manage these resources

In developing and transition countries, over-fragmentation of subnational government structure has been a common occurrence

New “consensus” on decentralisation

“(Fiscal) decentralization is the empowerment of people by the (fiscal) empowerment of

their local governments.” (Roy Bahl, 2005)

Implications of new definition (1)Recognition that fiscal decentralisation

requires more than just a ‘pushing down’ of financial resources – control over these financial resources matters just as much

Decentralisation is tied much more closely to governance and poverty reduction (empowerment)

Implications of new definition (2)In order to achieve the benefits of fiscal

decentralisation, ‘institutions matter’The quality of the design of intergovernmental

fiscal systems matters a great deal to achieve efficient and equitable outcomes

Decentralised political systems matter (local politicians should serve the community)

Local officials should have control over the local public service (hiring and firing)

Local corruption exists. Achieving local accountability is complex but possible (and easier than fighting central corruption)

Revisiting the “Wall of wonders”The system of intergovernmental fiscal

relations should be well-designed in its own right

The fiscal, political and administrative dimensions of decentralisation should be properly aligned

For every element of decentralisation (including fiscal decentralisation), there is a need to balance discretion with accountability

Intergovernmental finance: Four pillars

Intergovernmental finance: Four pillarsThe assignment of expenditure

responsibilities The assignment of revenue sources to

subnational governmentsThe allocation of intergovernmental fiscal

transfers or grantsRules on subnational budget deficits and the

incurrence of subnational debt

‘The first pillar of intergovernmental finance’

The assignment of expenditure responsibilitiesWhat functions and expenditure

responsibilities are (or should be) assigned to each level of government?

Subsidiarity principle Multi-dimensional nature of functions Accountability mechanisms in place

The Subsidiarity PrincipleGovernment services should be provided at

the lowest level of government that can do so efficiently.

Generally this means that public services should be provided at the level of government compatible with the “benefit area” of the service. If the benefits area is smaller (or greater) than

the jurisdiction, the provision choice will be inefficient.

But, it’s not all or nothing: expenditure responsibilities are multi-dimensionalWithin a certain sector or function,

responsibility can be assigned separately for:Policy and regulation FinancingProvision (responsibility) of the serviceProduction (delivery) of the service.

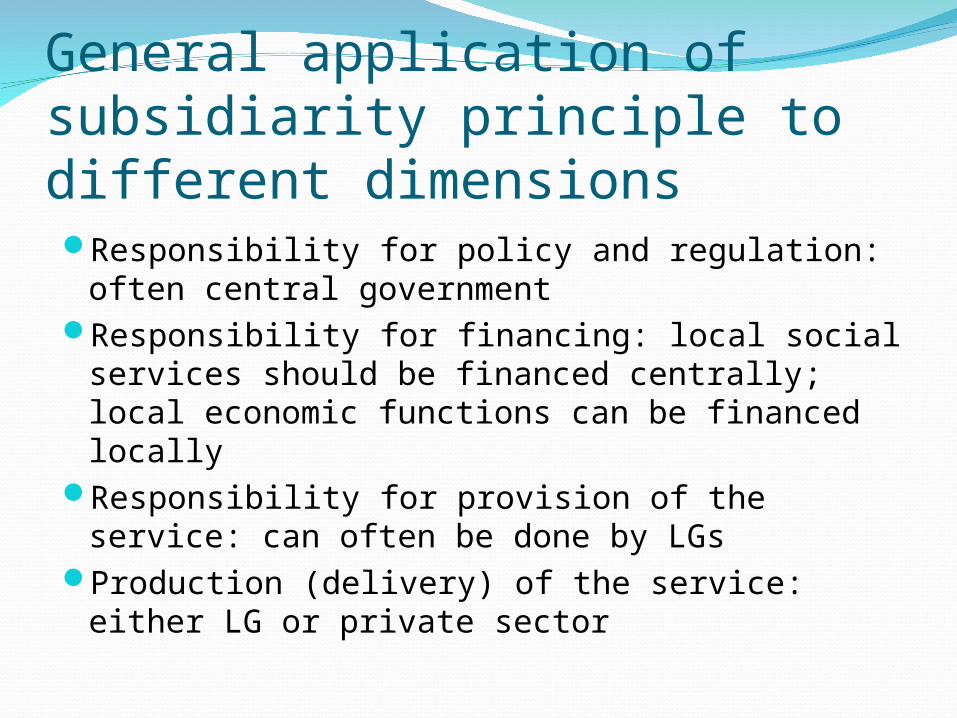

General application of subsidiarity principle to different dimensionsResponsibility for policy and regulation: often

central governmentResponsibility for financing: local social

services should be financed centrally; local economic functions can be financed locally

Responsibility for provision of the service: can often be done by LGs

Production (delivery) of the service: either LG or private sector

Further stipulations to the subsidiarity principle Local ability to efficiently provide public

services further requires:Elected local government: Appropriate,

participatory and accountable local governance structures

Locally appointed officials and local human resource capability to deliver adequate public services

Adequate local financial management systems to assure transparency and sound PFM

Different countries have ended up with widely different practices

Functions typically devolved to the local government level:

Basic education, basic health services, agricultural extension, (rural) water supply, local roads

Urban services (public utilities, roads, sanitation)

Note that many of these functions are closely related to achieving the MDGs !

In general…It is important to have a clear and stable

assignment, but there is no single ”best” assignment of expenditure responsibilities that applies to all conditions….

Open invitation: To what extent has real authority been

decentralised to the local level in your country of work?

But in reality....Decentralisation reforms most often go

wrong in expenditure assignments, since the willingness across key stakeholders to decentralise real authority to the local level is often missing.

Local taxation and user feesIntergovernmental transfers

Financing capital investments

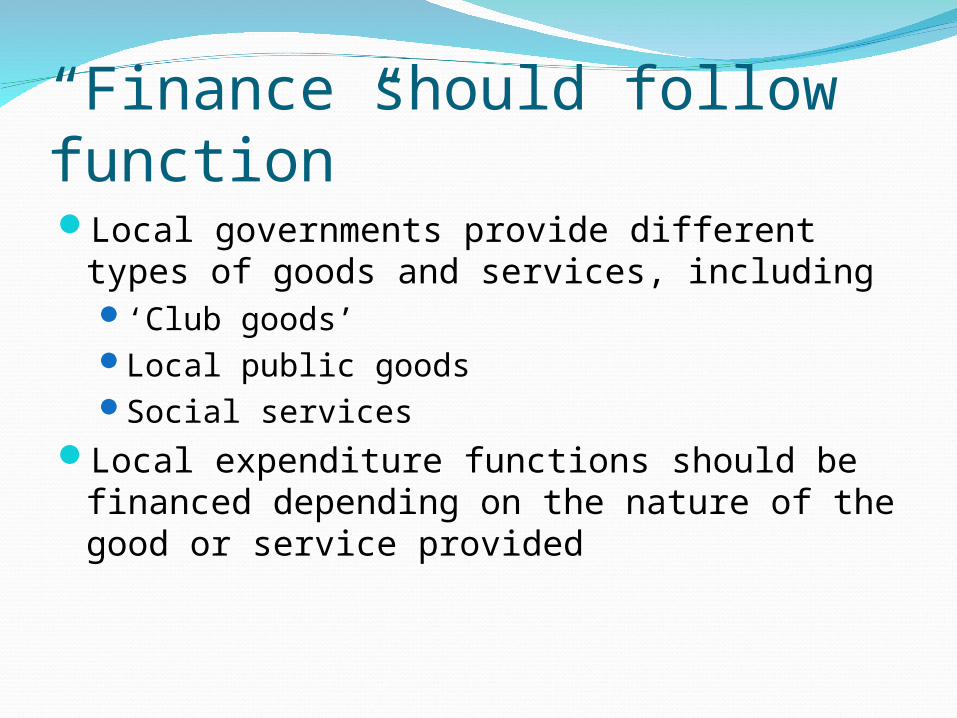

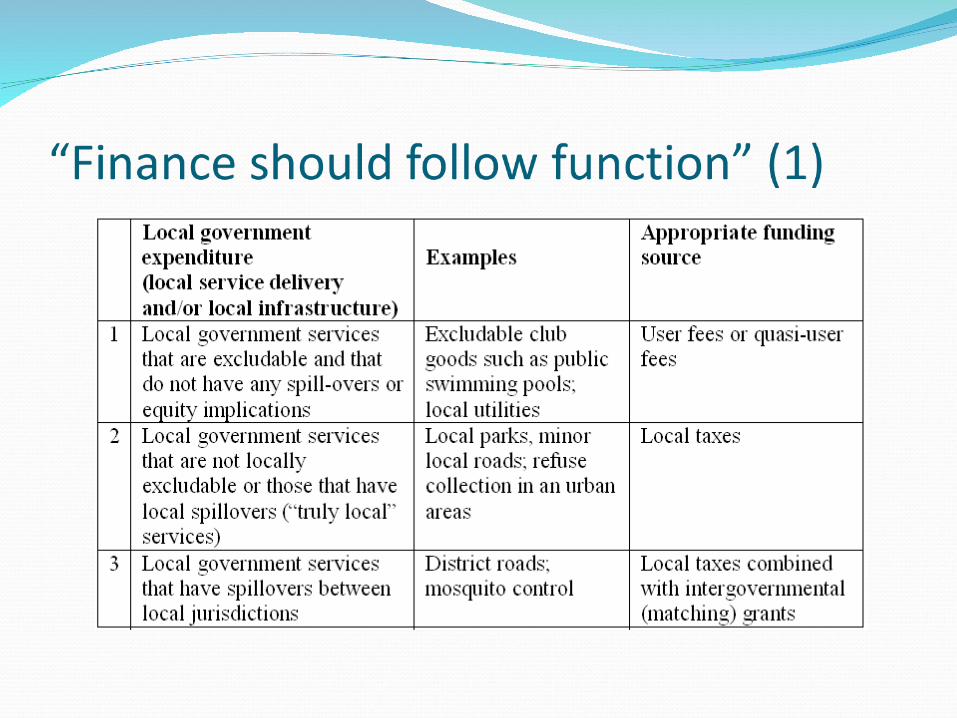

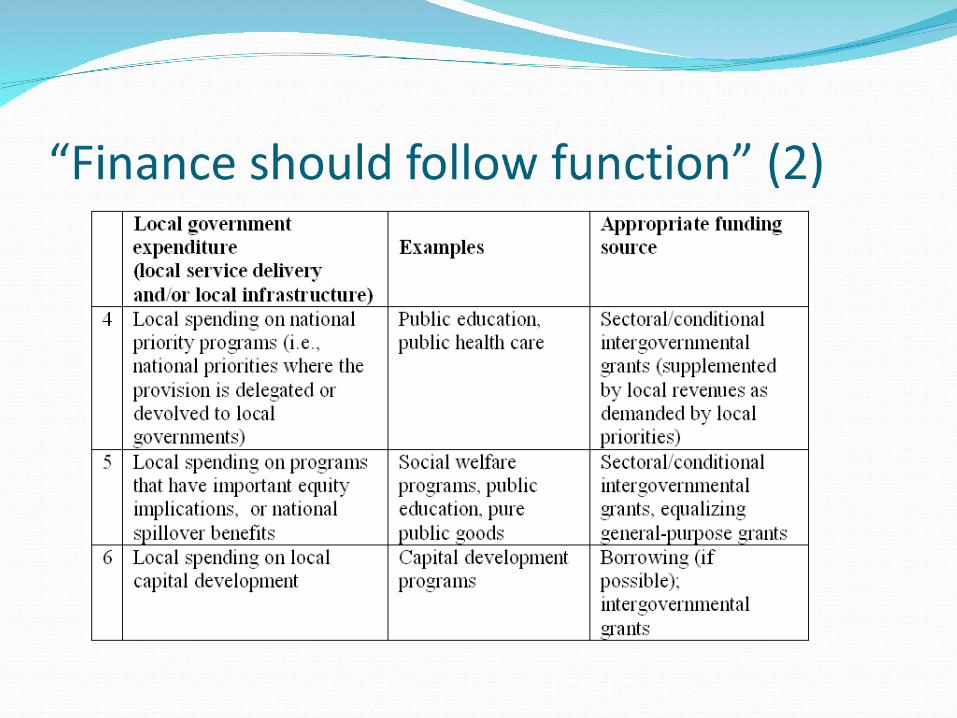

“Finance should follow function”Local governments provide different types of

goods and services, including‘Club goods’Local public goodsSocial services

Local expenditure functions should be financed depending on the nature of the good or service provided

The revenue assignment question (second pillar)Which tax sources or non-tax revenue

sources (including fee revenues) will be made available to subnational governments in order to provide them with revenue sources?

The assignment of own revenue sources is considered the second ‘pillar’ of intergovernmental finance

Why have sub-national taxation?Sub-national governments are often more

accountable for controlling spending if they are also responsible for revenues

Reduces excessive demand by sub-national governments for transfers from the center

Allows tax policy (tax levels and structure) to be tailored to the conditions and preferences of sub-national governments

Allows decentralised tax administration (when local governments are in a better position to collect)

Features of an ‘ideal’ local revenue sourceSubnational governments should be assigned

taxes that achieve a ‘correspondence’ between the tax and the benefits from local goverment services

Relatively easy to administerShould not be easy to give ‘perverse

incentives’ to taxpayers

Suitable local revenue sourcesProperty taxesMarket fees and other local user fees

But also…A ‘piggy-back’ personal income taxLocal business fees (but not CIT)Sales taxes (but not VAT)Motor vehicle taxes

Conclusions on fiscal decentralisation and local revenuesLocal revenues should be an important part of a

well-functioning intergovernmental fiscal system, both for economic and accountability reasons

But, raising more local revenues is only efficient if the revenues are well-spent, and

Neither central politicians nor local politicians have a strong incentive to rely heavily on local government revenues

As a result, local revenues are often an under-emphasised part of fiscal decentralisation

Intergovernmental fiscal transfers (the third pillar)

Since own source revenues are (almost) never enough to covers local expenditure responsibilities, central (or regional) governments may provide local governments with additional resources through a system of intergovernmental fiscal transfers, such as revenue-sharing or grants

In most countries, transfers are (by far) the main funding source for local government, esp. for social sector services

But transfers do not have same accountability benefits as own source revenues

Sound reasons for intergovernmental fiscal transfersImproving the vertical fiscal balance of the

system of intergovernmental relationsImproving the horizontal fiscal balance of the

system of intergovernmental relations (in other words, equalisation).

Compensating for the presence of spillovers or “externalities” between jurisdictions

Funding national priorities or “merit goods”

Dimensions of intergovernmental transfer mechanismsDefine the purposeDetermine size of the transfer pool‘Horizontal’ allocation of transfers between

government unitsConditional (specific / earmarked), sectoral,

or unconditional transfersNature of transfer: matching grant or lump

sum (block) grant

Finally, the fourth pillar of subnational finance: deficits and debtIf subnational governments do not carefully

balance their annual expenditures with revenues and transfers, this will result in subnational deficits and the incurrence of subnational debt.

In many developed economies, local borrowing is an appropriate way for local governments to fund capital infrastructure, since (i) it corrects the inter-temporal mismatch between costs and benefits, and (ii) there are numerous mechanisms that assure responsible borrowing.

Local capital financeIn many LDCs, the absence of market-based

mechanisms to enforce a ‘hard budget constraint’ requires restricting local borrowing:

Rules-based restrictions Permission required Local government bank / loan fund No borrowing allowed

Instead, capital grants are often relied on to fund local capital development.

Useful source of information:World Bank: Fiscal decentralisation indicators

(derived from the IMFs Governance Finance Statistics (GFS)). The GFS covers 149 countries on a yearly basis and

is the only data source with such comprehensive coverage, although the number of countries with sub-national data is reduced by about two thirds.

It has more than 50 variables for each government tier allowing fairly detailed analysis of fiscal flows..

Cautioning note: standardisation inevitably leads to a loss of detail and data richness that must be kept in mind when using GFS data to assess decentralization.