Embed Size (px)

Citation preview

An Introduction to Structured Investments

March 2012

AGENDA

Who are Catley Lakeman?

Structured Investments Overview & Composition

Overview

Composition: How is a Structured Investment put together?

Structured Investments Pricing & Risks

Pricing: Volatility

Pricing: Counterparty Credit

Pricing: Overview

Pricing: Structured Investment Pendulum

Risks: What are the risks associated with Structured Investments?

CATLEY LAKEMAN SECURITIES

WHO ARE CATLEY LAKEMAN?

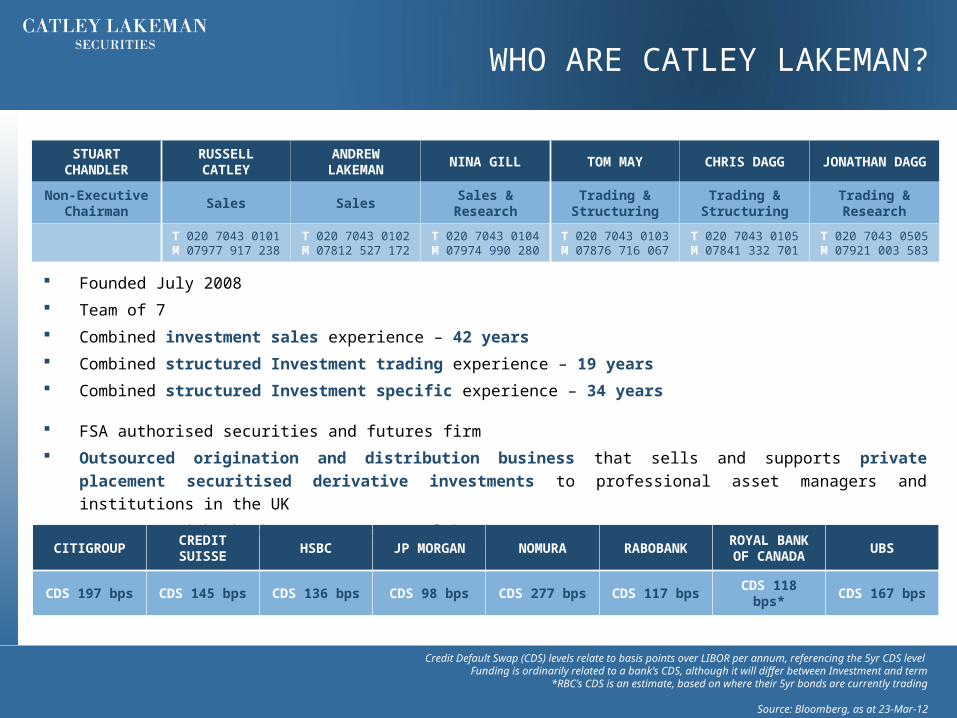

Founded July 2008

Team of 7

Combined investment sales experience – 42 years

Combined structured Investment trading experience – 19 years

Combined structured Investment specific experience – 34 years

FSA authorised securities and futures firm

Outsourced origination and distribution business that sells and supports private placement securitised

derivative investments to professional asset managers and institutions in the UK

Represent eight banks on a contractual basis

STUART CHANDLER

RUSSELL CATLEY

ANDREW LAKEMAN

NINA GILL TOM MAY CHRIS DAGGJONATHAN

DAGG

Non-Executive Chairman

Sales SalesSales &

ResearchTrading &

StructuringTrading &

StructuringTrading & Research

T 020 7043 0101M 07977 917 238

T 020 7043 0102M 07812 527 172

T 020 7043 0104M 07974 990 280

T 020 7043 0103M 07876 716 067

T 020 7043 0105M 07841 332 701

T 020 7043 0505M 07921 003 583

CITIGROUPCREDIT SUISSE

HSBC JP MORGAN NOMURA RABOBANKROYAL BANK OF CANADA

UBS

CDS 197 bps CDS 145 bps CDS 136 bps CDS 98 bps CDS 277 bps CDS 117 bps CDS 118 bps* CDS 167 bps

Credit Default Swap (CDS) levels relate to basis points over LIBOR per annum, referencing the 5yr CDS level Funding is ordinarily related to a bank’s CDS, although it will differ between Investment and term

*RBC’s CDS is an estimate, based on where their 5yr bonds are currently trading

Source: Bloomberg, as at 23-Mar-12

STRUCTURED INVESTMENTS OVERVIEW & COMPOSITION

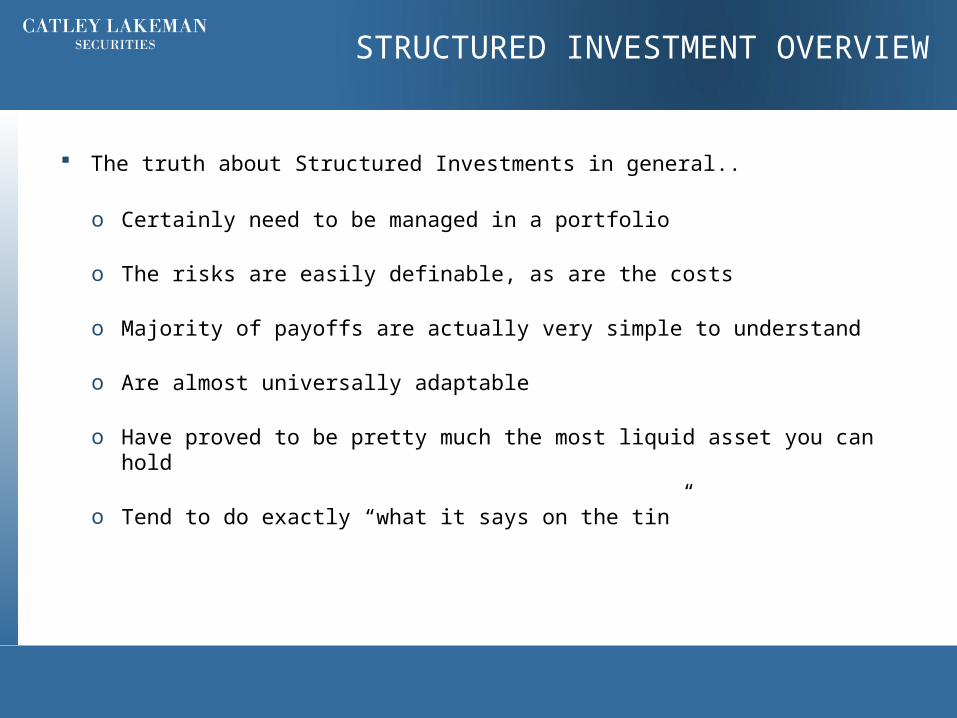

The truth about Structured Investments in general..

o Certainly need to be managed in a portfolio

o The risks are easily definable, as are the costs

o Majority of payoffs are actually very simple to understand

o Are almost universally adaptable

o Have proved to be pretty much the most liquid asset you can hold

o Tend to do exactly “what it says on the tin”

STRUCTURED INVESTMENT OVERVIEW

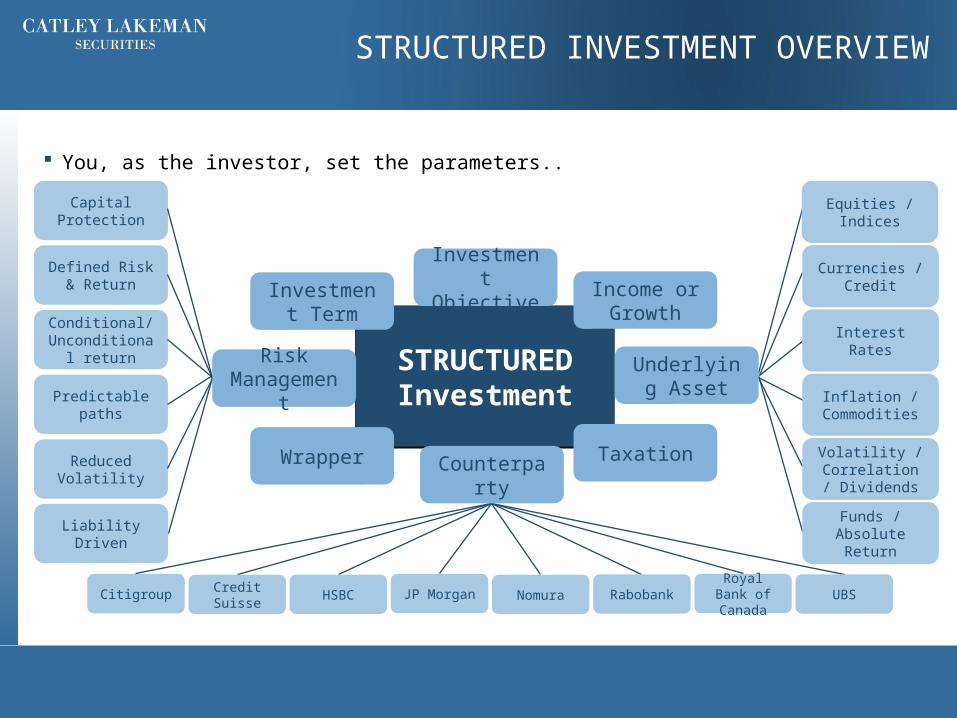

You, as the investor, set the parameters..

STRUCTURED INVESTMENT OVERVIEW

Funds / Absolute Return

Volatility / Correlation / Dividends

Inflation / Commodities

Interest Rates

Currencies / Credit

Equities / Indices

Predictable paths

Conditional/ Unconditional

return

Defined Risk & Return

Reduced Volatility

Capital Protection

Liability Driven

JP Morgan Nomura RabobankRoyal Bank of Canada

UBSHSBCCredit Suisse

Citigroup

STRUCTURED Investment

STRUCTURED Investment

Income or Growth

Underlying Asset

Investment Objective

Wrapper Taxation

Investment Term

Counterparty

Risk Management

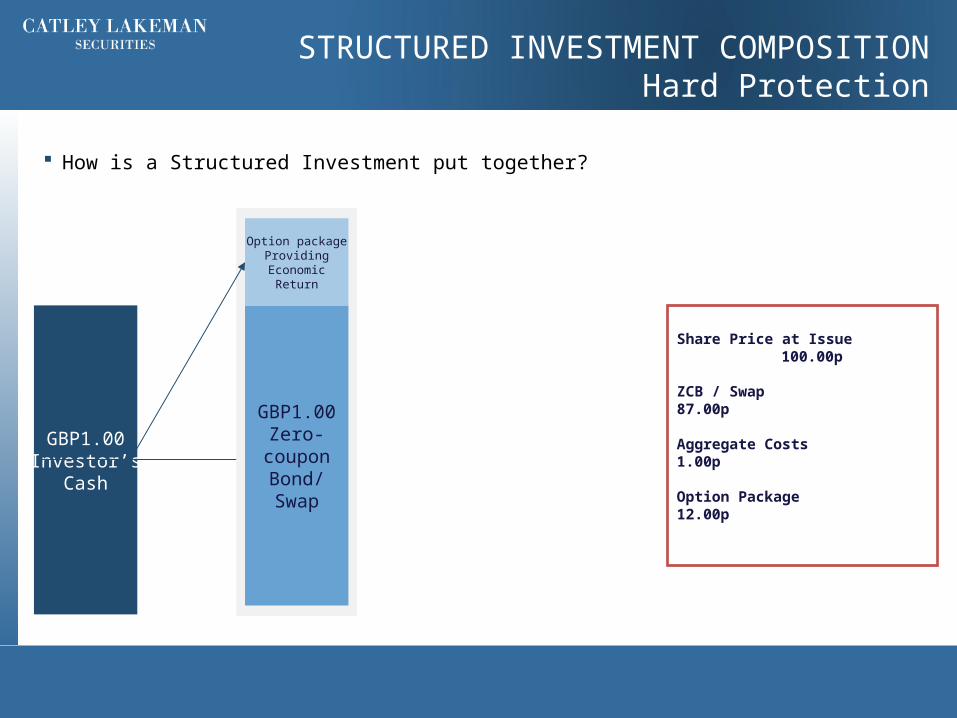

How is a Structured Investment put together?

Share Price at Issue 100.00p

ZCB / Swap 87.00p

Aggregate Costs 1.00p

Option Package 12.00p

STRUCTURED INVESTMENT COMPOSITIONHard Protection

GBP1.00Investor’s

Cash

GBP1.00Zero-

couponBond/Swap

Option packageProvidingEconomic

Return

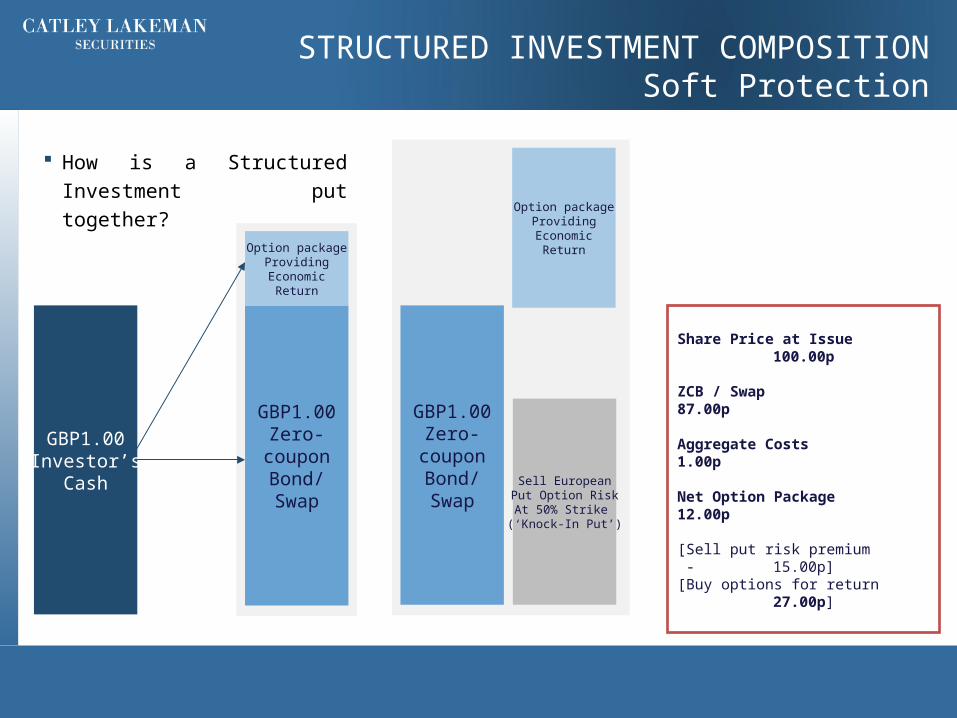

How is a Structured Investment

put together?

Share Price at Issue 100.00p

ZCB / Swap 87.00p

Aggregate Costs 1.00p

Net Option Package 12.00p

[Sell put risk premium - 15.00p][Buy options for return 27.00p]

Option packageProvidingEconomic

Return

Sell EuropeanPut Option RiskAt 50% Strike (‘Knock-In Put’)

GBP1.00Investor’s

Cash

GBP1.00Zero-

couponBond/Swap

Option packageProvidingEconomic

Return

GBP1.00Zero-

couponBond/Swap

STRUCTURED INVESTMENT COMPOSITIONSoft Protection

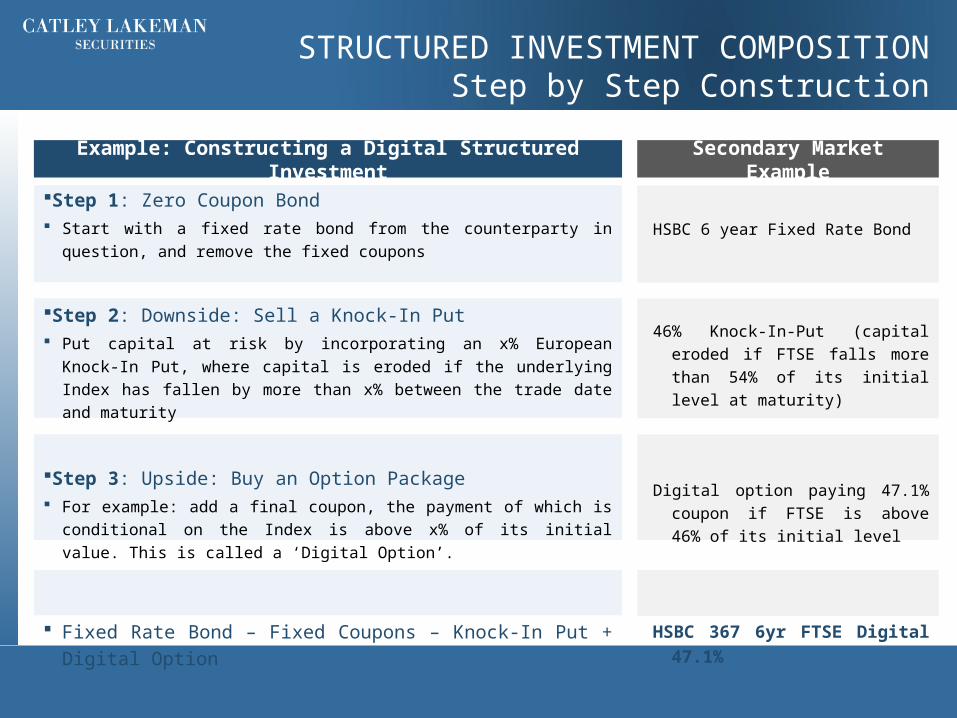

HSBC 6 year Fixed Rate Bond

46% Knock-In-Put (capital eroded if

FTSE falls more than 54% of its

initial level at maturity)

Digital option paying 47.1% coupon if

FTSE is above 46% of its initial

level

HSBC 367 6yr FTSE Digital 47.1%

Step 1: Zero Coupon Bond Start with a fixed rate bond from the counterparty in question, and remove the

fixed coupons

Step 2: Downside: Sell a Knock-In Put Put capital at risk by incorporating an x% European Knock-In Put, where

capital is eroded if the underlying Index has fallen by more than x% between

the trade date and maturity

Step 3: Upside: Buy an Option Package For example: add a final coupon, the payment of which is conditional on the

Index is above x% of its initial value. This is called a ‘Digital Option’.

Fixed Rate Bond – Fixed Coupons – Knock-In Put + Digital Option

Example: Constructing a Digital Structured Investment Secondary Market Example

STRUCTURED INVESTMENT COMPOSITIONStep by Step Construction

STRUCTURED INVESTMENT PRICING & RISKS

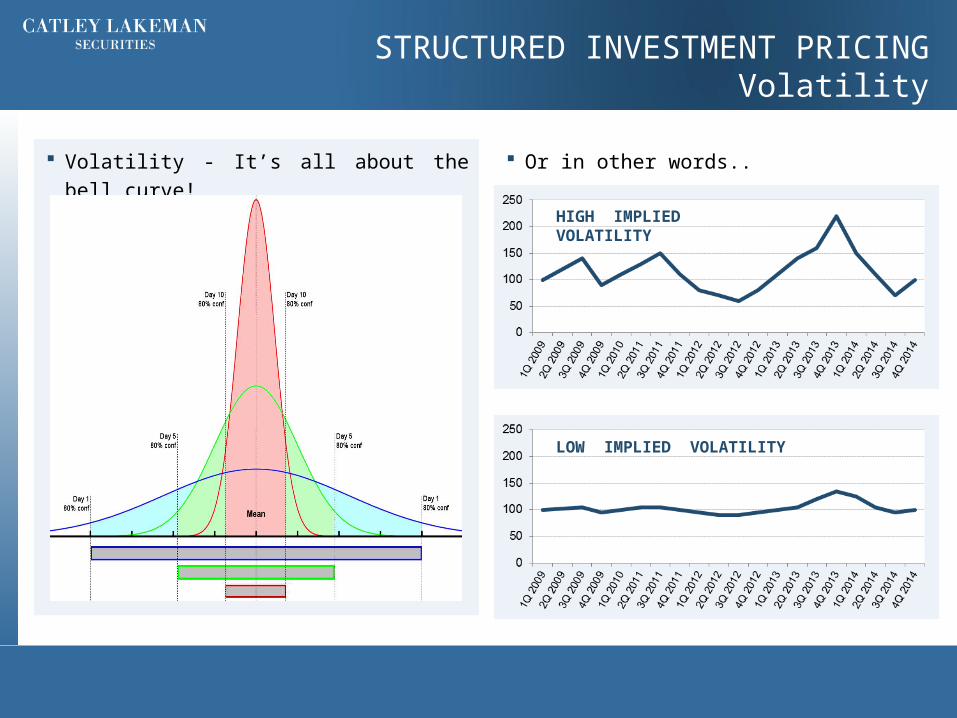

Or in other words.. Volatility - It’s all about the bell curve!

STRUCTURED INVESTMENT PRICINGVolatility

HIGH IMPLIED VOLATILITY

LOW IMPLIED VOLATILITY

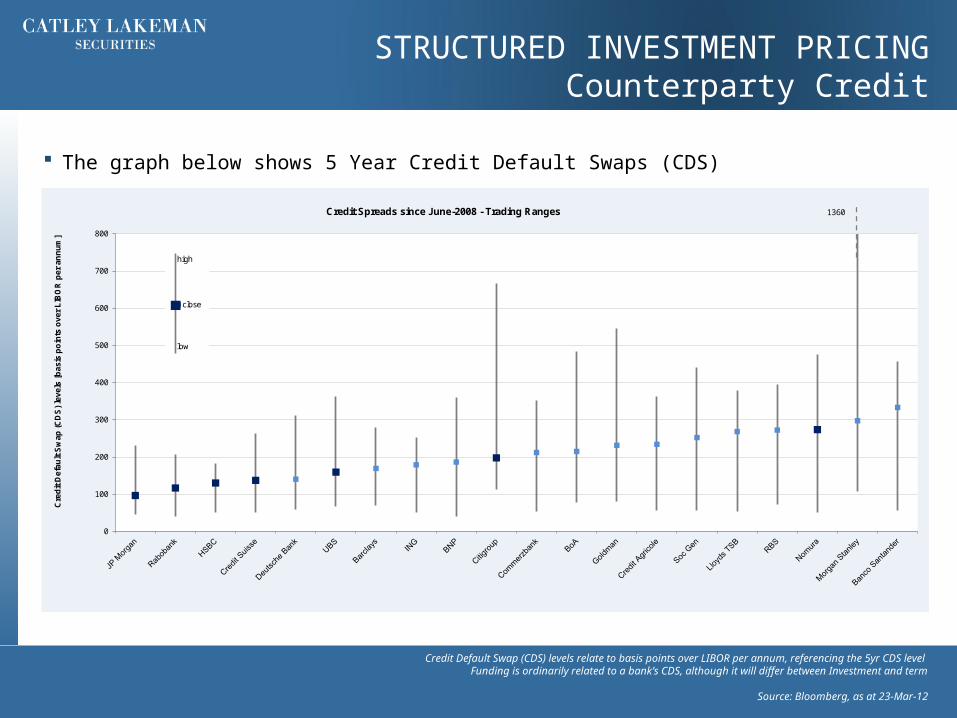

The graph below shows 5 Year Credit Default Swaps (CDS)

Credit Default Swap (CDS) levels relate to basis points over LIBOR per annum, referencing the 5yr CDS level Funding is ordinarily related to a bank’s CDS, although it will differ between Investment and term

Source: Bloomberg, as at 23-Mar-12

STRUCTURED INVESTMENT PRICINGCounterparty Credit

0

100

200

300

400

500

600

700

800

Cre

dit

De

fau

lt S

wa

p (

CD

S)

leve

ls [

ba

sis

po

ints

ove

r L

IBO

R p

er

an

nu

m]

Credit Spreads since June-2008 - Trading Ranges

close

1360

high

low

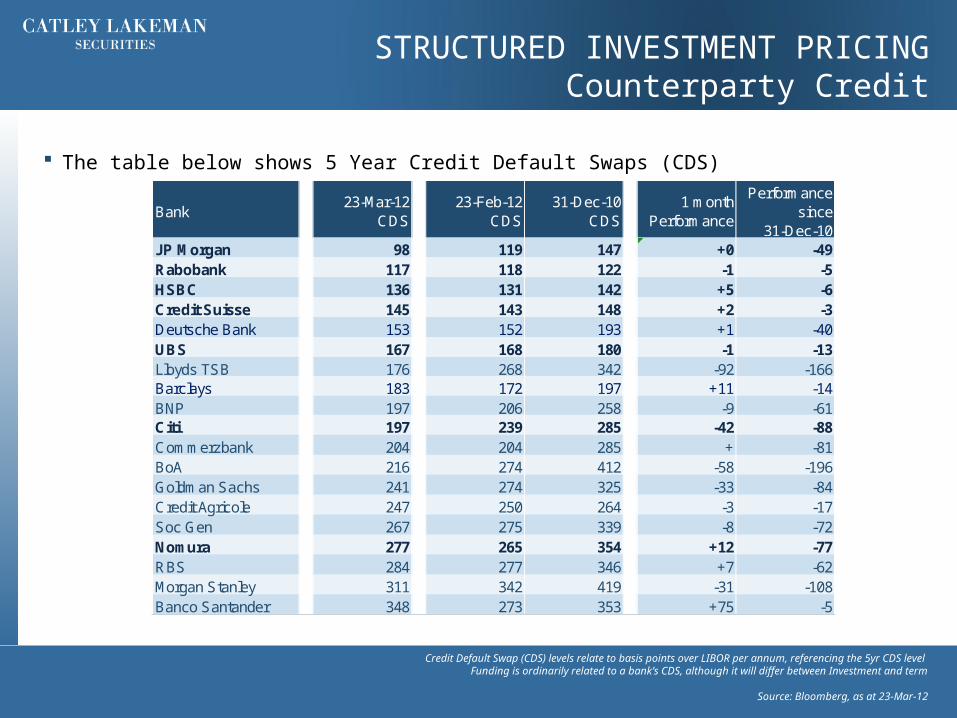

The table below shows 5 Year Credit Default Swaps (CDS)

Credit Default Swap (CDS) levels relate to basis points over LIBOR per annum, referencing the 5yr CDS level Funding is ordinarily related to a bank’s CDS, although it will differ between Investment and term

Source: Bloomberg, as at 23-Mar-12

STRUCTURED INVESTMENT PRICINGCounterparty Credit

Bank23-Mar-12

CDS23-Feb-12

CDS31-Dec-10

CDS1 month

Performance

Performance since

31-Dec-10JP Morgan 98 119 147 +0 -49Rabobank 117 118 122 -1 -5HSBC 136 131 142 +5 -6Credit Suisse 145 143 148 +2 -3Deutsche Bank 153 152 193 +1 -40UBS 167 168 180 -1 -13Lloyds TSB 176 268 342 -92 -166Barclays 183 172 197 +11 -14BNP 197 206 258 -9 -61Citi 197 239 285 -42 -88Commerzbank 204 204 285 + -81BoA 216 274 412 -58 -196Goldman Sachs 241 274 325 -33 -84Credit Agricole 247 250 264 -3 -17Soc Gen 267 275 339 -8 -72Nomura 277 265 354 +12 -77RBS 284 277 346 +7 -62Morgan Stanley 311 342 419 -31 -108Banco Santander 348 273 353 +75 -5

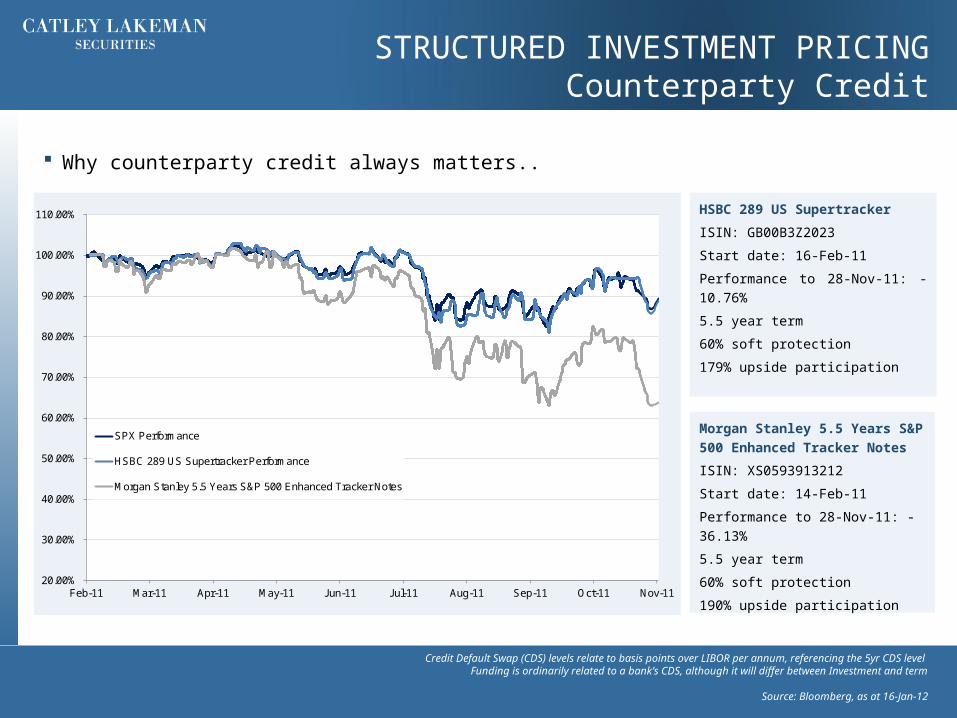

Why counterparty credit always matters..

Credit Default Swap (CDS) levels relate to basis points over LIBOR per annum, referencing the 5yr CDS level Funding is ordinarily related to a bank’s CDS, although it will differ between Investment and term

Source: Bloomberg, as at 16-Jan-12

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

110.00%

Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11

SPX Performance

HSBC 289 US Supertracker Performance

Morgan Stanley 5.5 Years S&P 500 Enhanced Tracker Notes

HSBC 289 US Supertracker

ISIN: GB00B3Z2023

Start date: 16-Feb-11

Performance to 28-Nov-11: -10.76%

5.5 year term

60% soft protection

179% upside participation

Morgan Stanley 5.5 Years S&P 500

Enhanced Tracker Notes

ISIN: XS0593913212

Start date: 14-Feb-11

Performance to 28-Nov-11: -36.13%

5.5 year term

60% soft protection

190% upside participation

STRUCTURED INVESTMENT PRICINGCounterparty Credit

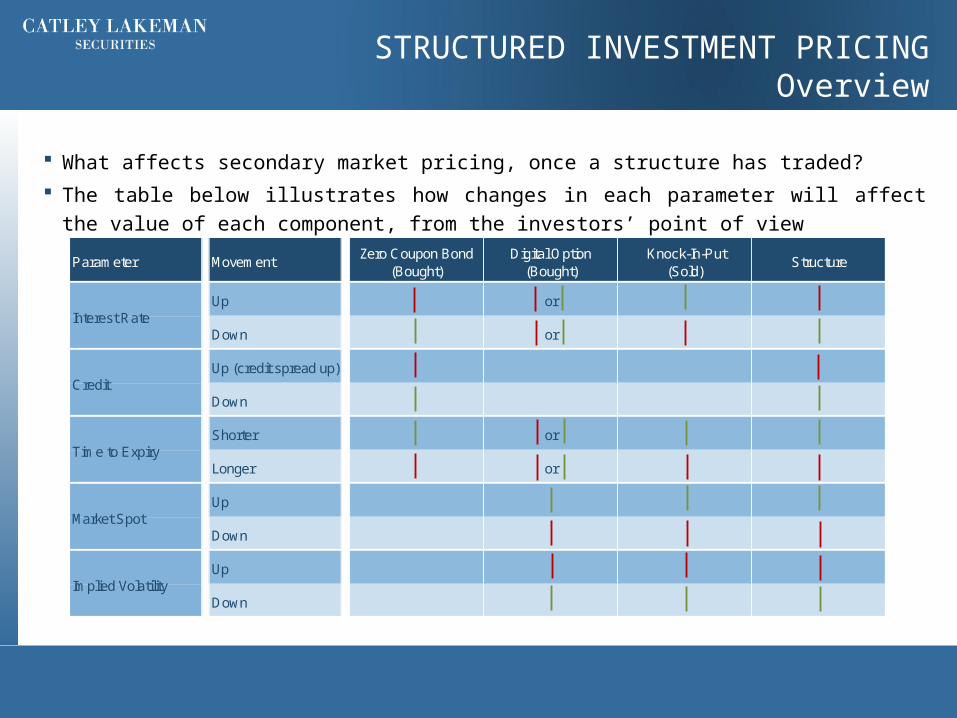

What affects secondary market pricing, once a structure has traded?

The table below illustrates how changes in each parameter will affect the value of each

component, from the investors’ point of view

STRUCTURED INVESTMENT PRICINGOverview

Parameter MovementZero Coupon Bond

(Bought)Digital Option

(Bought) Knock-In-Put

(Sold)Structure

Up or

Down or

Up (credit spread up)

Down

Shorter or

Longer or

Up

Down

Up

Down

Interest Rate

Credit

Time to Expiry

Market Spot

Implied Volatility

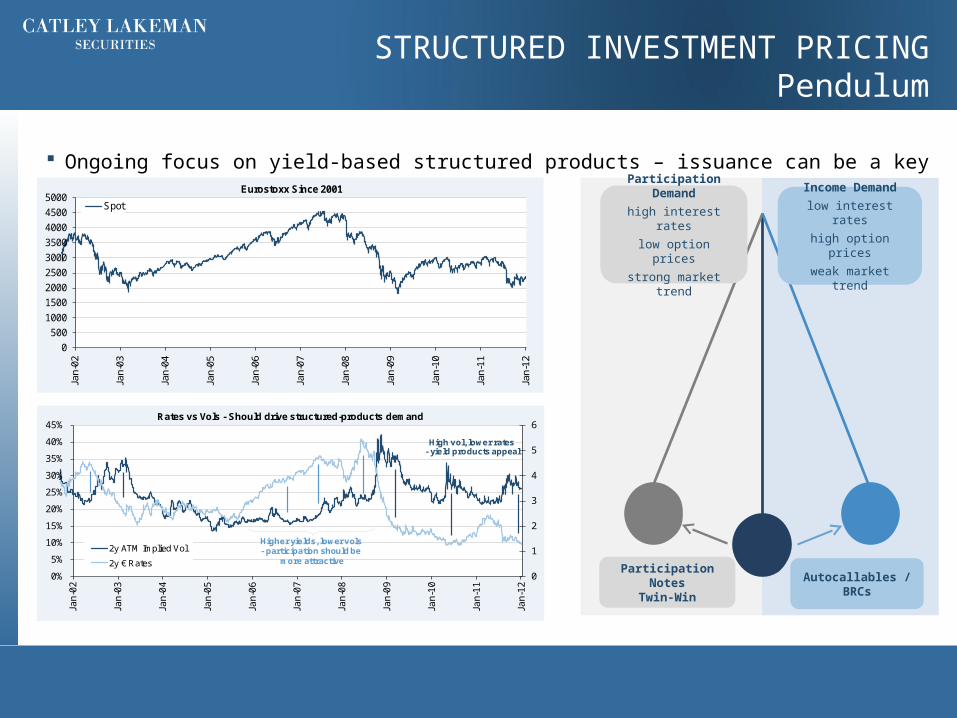

Ongoing focus on yield-based structured products – issuance can be a key driver for long-end

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Eurostoxx Since 2001

Spot

0

1

2

3

4

5

6

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Rates vs Vols - Should drive structured-products demand

2y ATM Implied Vol

2y € Rates

Higher yields, lower vols - participation should be

more attractive

High vol, lower rates- yield products appeal

Sources: UBS Equity Derivatives Strategy, Bloomberg, Jan 2012

Participation Demand

high interest rates

low option prices

strong market trend

Income Demand

low interest rates

high option prices

weak market trend

Participation NotesTwin-Win

Autocallables / BRCs

STRUCTURED INVESTMENT PRICINGPendulum

What are the risks associated with Structured Investments?

1.Market Risk Self evident and common across all risk investment vehicles

2. Credit Risk The investor is reliant on each individual bank being in a position to repay each structure at maturity. As a general

rule, the lower-rated the issuer, the more funding they will pay you within the pricing of the structure.

The 5yr Credit Default Swap (CDS) is often used as an indication of credit risk and is essentially the rate at which

institutions insure credit risk against each other (see appendix)

3. Liquidity / Mark-to-Market Risk If structured correctly, there will be full intra-day liquidity, proven in extremis Intra-day “live” prices available on websites, Bloomberg, Reuters Very easy to trade through Crest/Euroclear by DFM trading teams Accurate modeling and scenario analysis is used to assess the mark-to-market risks before issuance

STRUCTURED INVESTMENT RISKS

The information in this document is derived from sources believed to be reliable but which have not been independently verified. Catley Lakeman Securities makes no

guarantee of its accuracy and completeness and is not responsible for errors of transmission of factual or analytical data, nor is it liable for damages arising out of any

person’s reliance upon this information. All charts and graphs are from publicly available sources or proprietary data. The opinions in this document constitute the

present judgment of Catley Lakeman Securities, which is subject to change without notice. This document is neither an offer to sell, purchase or subscribe for any

investment nor a solicitation of such an offer. This document is intended for the use of institutional and professional customers and is not intended for the use of

private customers. This document is not intended for distribution in the United States of America or to US persons. This document is intended to be distributed in its

entirety. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient.

Catley Lakeman Securities is a LLP registered in England and Wales, Registered Office : One Eleven Edmund Street, Birmingham, B3 2HJ. Registration

Number: OC336585, FSA Reference: 484826

DISCLAIMER