Embed Size (px)

Citation preview

October 22, 2013

An Insiders Look at M&A

Overview

• Health Care Industry Trends

• Health Care M&A

• Strategic Alternatives

Health Care Industry Trends

3

Healthcare Providers

PPACA

Consumerism

Physician Shortages

Increased Payor

Leverage

Risk Assumption & Population Management

Limited Access to Capital

Competitor Consolidation

Value Based Purchasing of

Care

Health Care Industry Trends Pressure on Providers

Increased M&A Activity

4

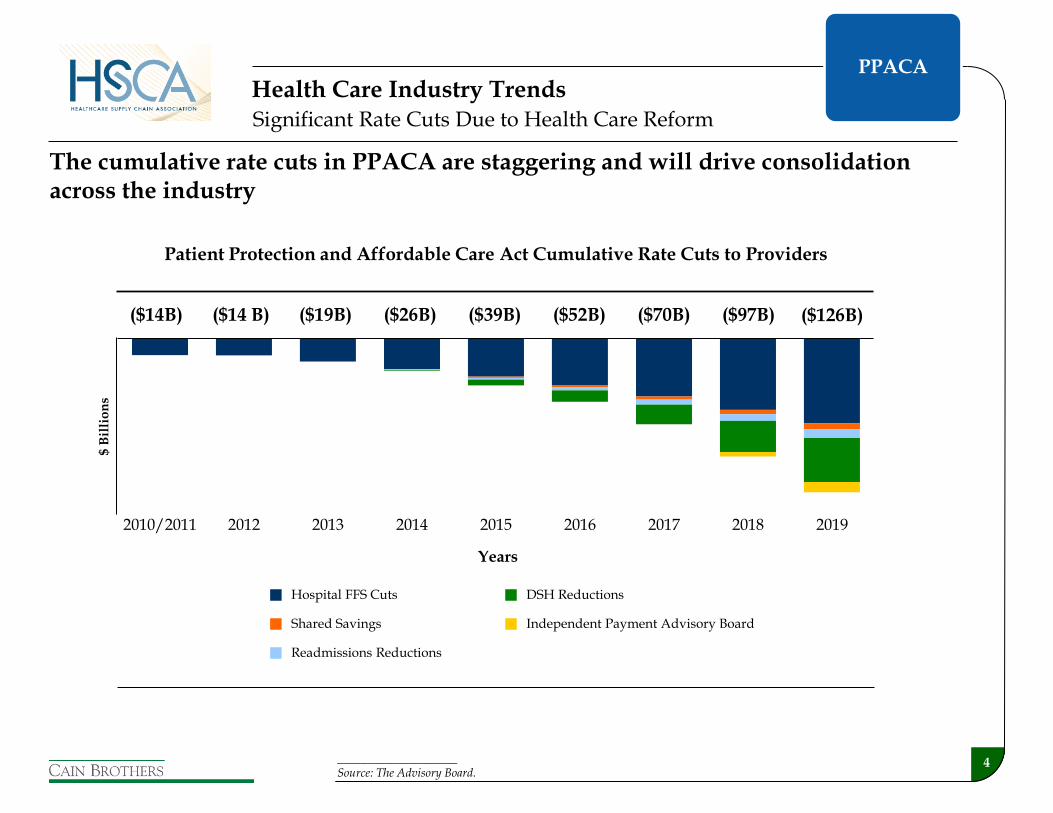

Patient Protection and Affordable Care Act Cumulative Rate Cuts to Providers

($14B) ($26B) ($39B) ($52B) ($70B) ($97B) ($126B) ($14 B) ($19B)

2010/2011 2012 2013 2014 2015 2016 2017 2018 2019

____________________ Source: The Advisory Board.

$ B

illi

on

s

Years

Hospital FFS Cuts

Shared Savings

Readmissions Reductions

DSH Reductions

Independent Payment Advisory Board

The cumulative rate cuts in PPACA are staggering and will drive consolidation across the industry

Significant Rate Cuts Due to Health Care Reform

Health Care Industry Trends PPACA

5

0%

5%

10%

15%

20%

25%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

196

0

1964

196

8

1972

197

6

1980

198

4

198

8

199

2

199

6

200

0

200

4

200

8

201

2P

201

6P

202

0P

% o

f GD

P

$ B

illi

on

s

Expenditures ($ in billions) Expenditures as % of GDP

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

196

0

196

4

1968

197

2

197

6

198

0

198

4

1988

199

2

199

6

200

0

200

4

200

8

2012

P

201

6P

202

0P

Per Capita Expenditures

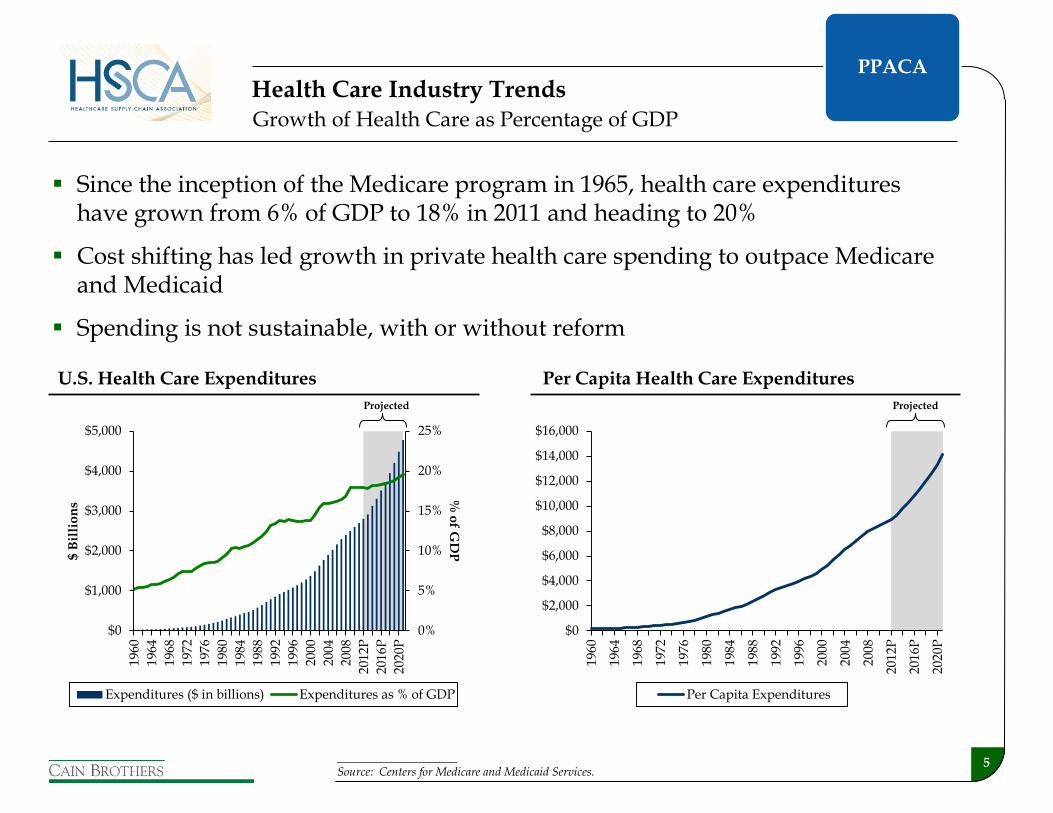

Since the inception of the Medicare program in 1965, health care expenditures have grown from 6% of GDP to 18% in 2011 and heading to 20%

Cost shifting has led growth in private health care spending to outpace Medicare and Medicaid

Spending is not sustainable, with or without reform

____________________ Source: Centers for Medicare and Medicaid Services.

Projected Projected

Growth of Health Care as Percentage of GDP

Health Care Industry Trends

U.S. Health Care Expenditures Per Capita Health Care Expenditures

PPACA

6

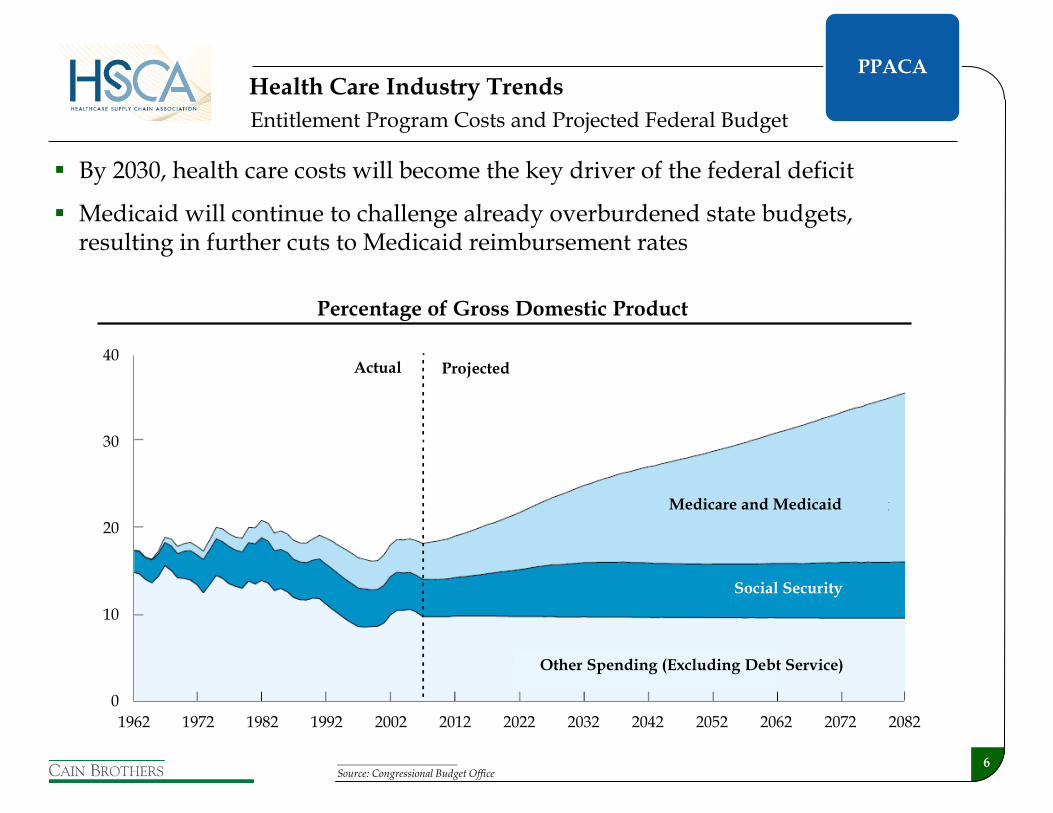

Entitlement Program Costs and Projected Federal Budget

By 2030, health care costs will become the key driver of the federal deficit

Medicaid will continue to challenge already overburdened state budgets, resulting in further cuts to Medicaid reimbursement rates

Health Care Industry Trends

____________________ Source: Congressional Budget Office

0

10

20

30

40

1962 1972 1982 1992 2002 2012 2022 2032 2042 2052 2062 2072 2082

Other Spending (Excluding Debt Service)

Projected Actual

Percentage of Gross Domestic Product

Medicare and Medicaid

Social Security

PPACA

7

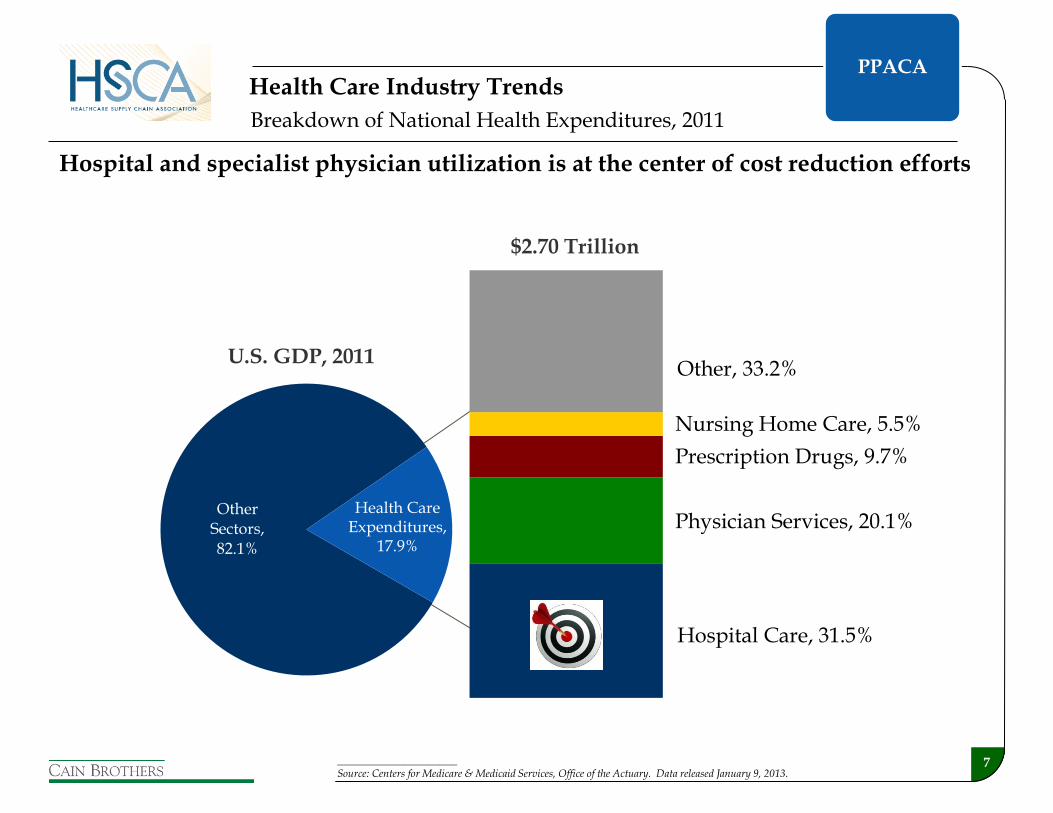

Health Care

Expenditure

s, 17.9%

$2.70 Trillion

Nursing Home Care, 5.5%

Physician Services, 20.1%

Other, 33.2%

Prescription Drugs, 9.7%

Hospital Care, 31.5%

Other Sectors, 82.1%

U.S. GDP, 2011

Health Care Expenditures,

17.9%

Breakdown of National Health Expenditures, 2011

____________________ Source: Centers for Medicare & Medicaid Services, Office of the Actuary. Data released January 9, 2013.

Hospital and specialist physician utilization is at the center of cost reduction efforts

Health Care Industry Trends PPACA

8

Health Care Industry Trends Consumerism

8

Traditional fee-for-service insured and

managed care

Consumerism

9 ____________________ Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits

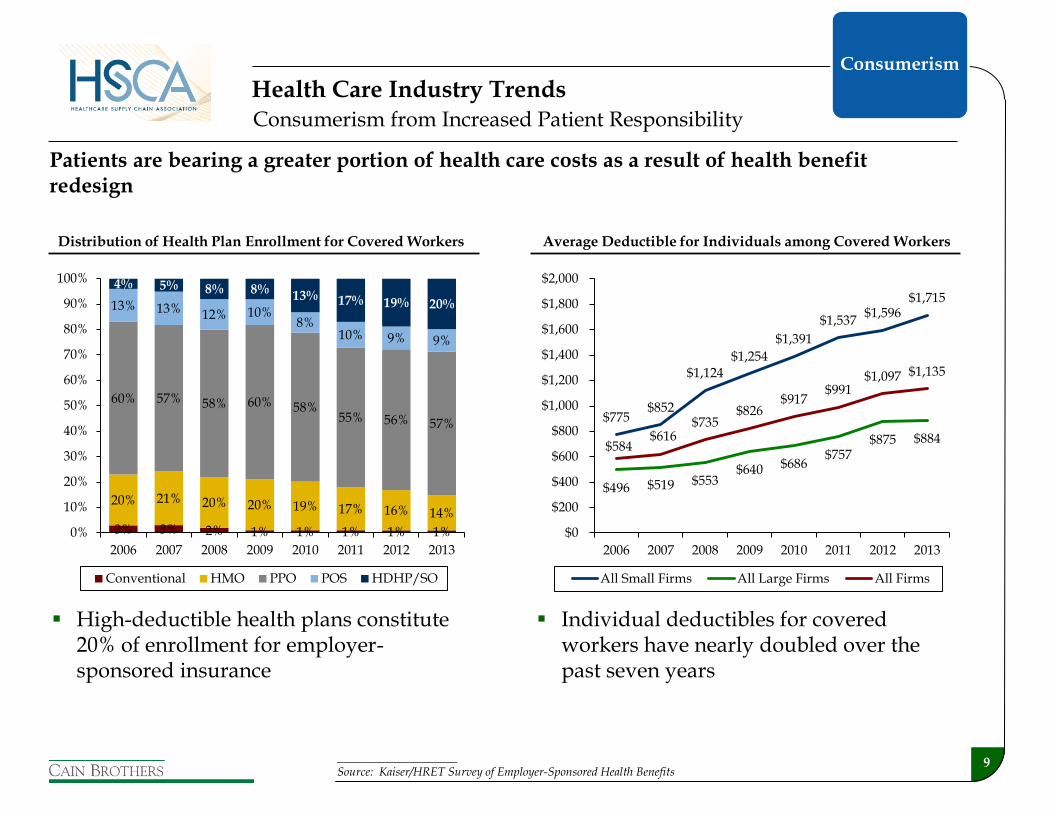

Consumerism from Increased Patient Responsibility

Health Care Industry Trends

Distribution of Health Plan Enrollment for Covered Workers Average Deductible for Individuals among Covered Workers

3% 3% 2% 1% 1% 1% 1% 1%

20% 21% 20% 20% 19% 17% 16% 14%

60% 57% 58% 60% 58%55% 56% 57%

13% 13% 12% 10%8%

10% 9% 9%

4% 5% 8% 8% 13% 17% 19% 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013

Conventional HMO PPO POS HDHP/SO

$775 $852

$1,124 $1,254

$1,391

$1,537 $1,596

$1,715

$496 $519 $553 $640 $686

$757 $875 $884

$584 $616

$735 $826

$917 $991

$1,097 $1,135

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2006 2007 2008 2009 2010 2011 2012 2013

All Small Firms All Large Firms All Firms

High-deductible health plans constitute 20% of enrollment for employer-sponsored insurance

Individual deductibles for covered workers have nearly doubled over the past seven years

Patients are bearing a greater portion of health care costs as a result of health benefit redesign

Consumerism

10

Year-over-Year Same-Store Adjusted Admissions Trends for Publicly Traded Hospital Management Companies

2.6% 3.0%

2.3%

1.1% 1.5%

0.0%

0.6%

1.4%

(0.3%)

1.0%

0.5%

1.9%

0.4%

(0.2%)

1.9%

(3.2%)

(0.8%)

(4.0%)

(3.0%)

(2.0%)

(1.0%)

0.0%

1.0%

2.0%

3.0%

4.0%

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2009 2010 2011 2012 2013

____________________ Source: UBS – “Q2 Recap, Expectations Low for 2H” – August 23, 2013. Results are based upon an average for the seven publicly traded hospital management companies.

Patient volumes are down, driven by many factors, including the economy, technology, beginnings of PPACA implementation and shift toward higher deductible health plans

Flat to Declining Patient Volumes

Health Care Industry Trends Consumerism

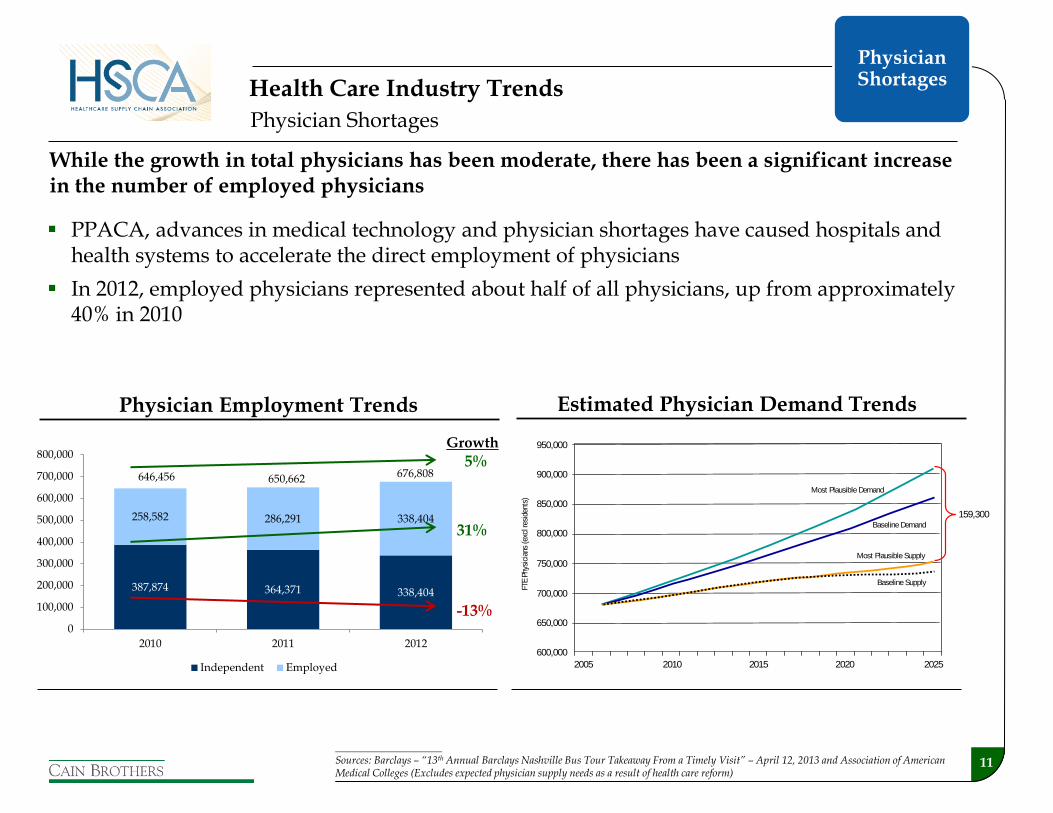

11 ____________________ Sources: Barclays – “13th Annual Barclays Nashville Bus Tour Takeaway From a Timely Visit” – April 12, 2013 and Association of American Medical Colleges (Excludes expected physician supply needs as a result of health care reform)

Physician Employment Trends

While the growth in total physicians has been moderate, there has been a significant increase in the number of employed physicians

PPACA, advances in medical technology and physician shortages have caused hospitals and health systems to accelerate the direct employment of physicians

In 2012, employed physicians represented about half of all physicians, up from approximately 40% in 2010

387,874 364,371 338,404

258,582 286,291 338,404

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2010 2011 2012

Independent Employed

646,456 650,662 676,8085%

31%

-13%

Growth

Physician Shortages

950,000

900,000

850,000

800,000

750,000

700,000

650,000

600,000

FTE

Phy

sici

ans

(exc

l res

iden

ts)

2005 2010 2015 2020 2025

159,300

Baseline Supply

Most Plausible Supply

Baseline Demand

Most Plausible Demand

Estimated Physician Demand Trends

Health Care Industry Trends

Physician Shortages

12

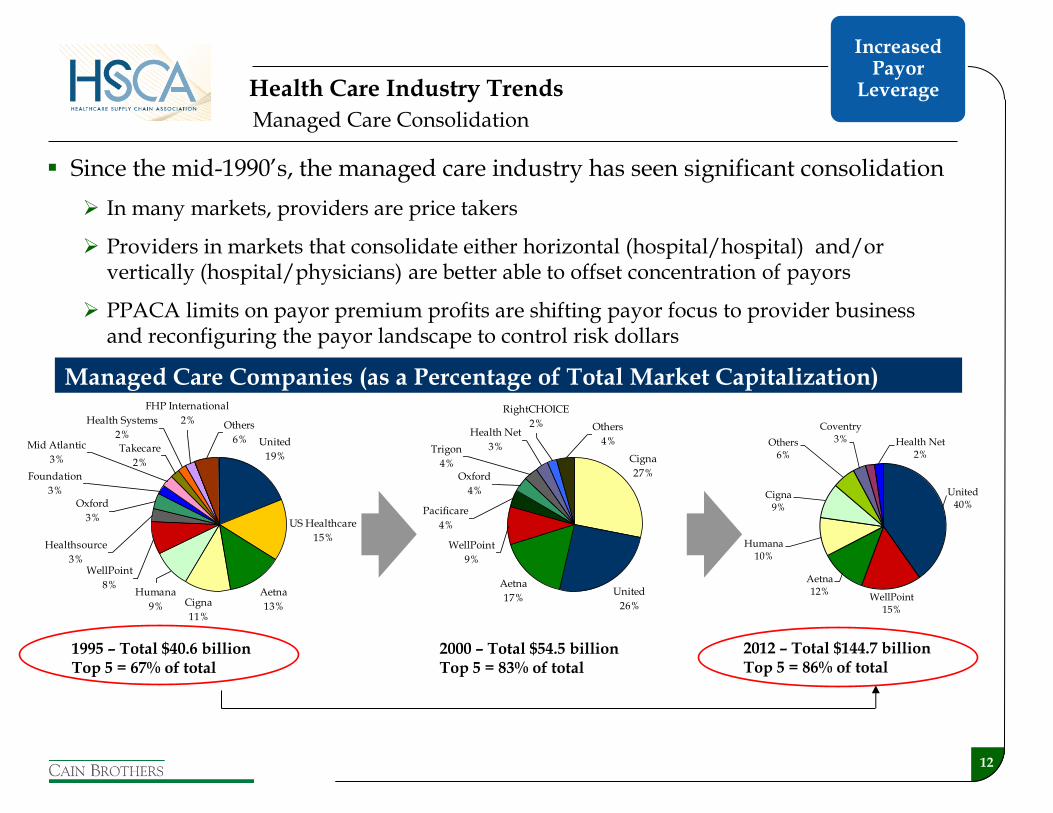

Since the mid-1990’s, the managed care industry has seen significant consolidation

In many markets, providers are price takers

Providers in markets that consolidate either horizontal (hospital/hospital) and/or vertically (hospital/physicians) are better able to offset concentration of payors

PPACA limits on payor premium profits are shifting payor focus to provider business and reconfiguring the payor landscape to control risk dollars

Managed Care Consolidation

Managed Care Companies (as a Percentage of Total Market Capitalization)

United

19%

US Healthcare

15%

Aetna

13%Cigna

11%

Takecare

2%

Health Systems

2%

FHP International

2% Others

6%

Foundation

3%

Mid Atlantic

3%

Oxford

3%

Healthsource

3%WellPoint

8%Humana

9%

1995 – Total $40.6 billion Top 5 = 67% of total

Cigna

27%

Aetna

17%

WellPoint

9%

Oxford

4%

Health Net

3%

RightCHOICE

2% Others

4%Trigon

4%

Pacificare

4%

United

26%

2000 – Total $54.5 billion Top 5 = 83% of total

2012 – Total $144.7 billion Top 5 = 86% of total

United40%

WellPoint15%

Aetna12%

Humana10%

Cigna9%

Others6%

Coventry3% Health Net

2%

Health Care Industry Trends

Increased Payor

Leverage

13

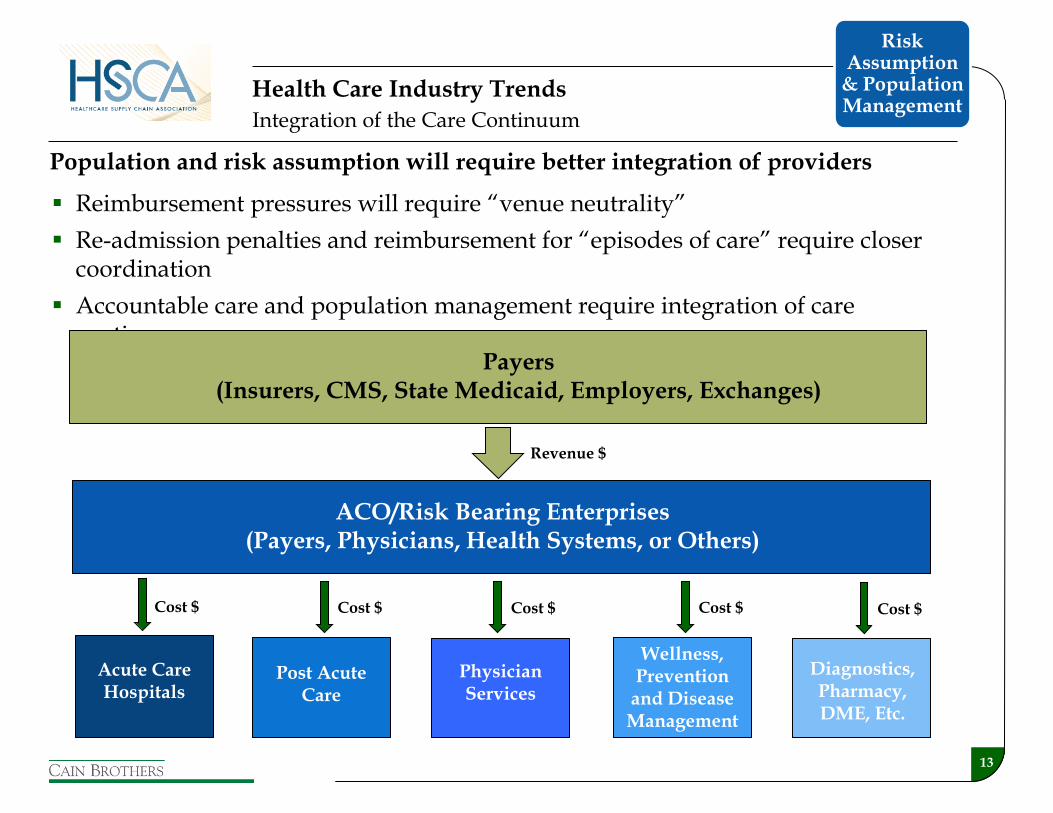

Population and risk assumption will require better integration of providers

Reimbursement pressures will require “venue neutrality”

Re-admission penalties and reimbursement for “episodes of care” require closer coordination

Accountable care and population management require integration of care continuum

Integration of the Care Continuum

Acute Care Hospitals

Post Acute Care

Physician Services

Wellness, Prevention

and Disease Management

Diagnostics, Pharmacy, DME, Etc.

ACO/Risk Bearing Enterprises (Payers, Physicians, Health Systems, or Others)

Payers (Insurers, CMS, State Medicaid, Employers, Exchanges)

Revenue $

Cost $ Cost $ Cost $ Cost $ Cost $

Health Care Industry Trends

Risk Assumption

& Population Management

14

Care Delivery Ecosystem

Physicians / Clinicians Managed

Care

Key Constituents of the Delivery Ecosystem

Providers in care delivery ecosystem have different incentives

FFS mechanisms incentivize admissions

Care of a patient is not tracked among providers

Bundled payments and ACO structures will drive coordination

Cost and outcomes will define where patients and $’s will go

Physicians/clinicians and managed care will all fight for a leading role

The Key Question Who will control the ultimate economics of the system?

Hospital

ALOS: 5.4 days Ave Cost Per Day: $1,752

LTAC

ALOS: 26.6 days Ave Cost Per Day: $1,451

IRF

ALOS: 13.1 days Ave Cost Per Day: $1.344

Skilled Nursing

ALOS: 27.1 days Ave Cost Per Day: $398

Home Health

VPPS: 36.7 visits Ave Cost Per Visit: $154

Hospital / Health System

Health Care Industry Trends

Risk Assumption

& Population Management

15

Nonprofits’ credit strength is driven by cash and leverage

Capital deployed has changed from PP&E to physician integration, IT and risk resources

Traditional tax-exempt capital is not effective for funding new needs

Hospital Sector Update: Size Matters

____________________ Source: S&P – “U.S. Not-For-Profit Health Care System: Stability in 2011 Fives Providers a Grim foundation to Face Industry Challenges ” Information as of 8/13/2012

S&P Not-For-Profit Health Care Ratings Distribution

Larger systems continue to benefit from a broader revenue base, economies of scale, and stronger operating margins

Health Care Industry Trends

18%

23%

20%

17%

12%

6%

1% 1% 2%3%

5%

14% 14%15% 15%

12%11%

10%

0%

5%

10%

15%

20%

25%

AA+/AA AA- A+ A A- BBB+ BBB BBB- SpeculativeGrade

Systems Stand-Alones

Limited Access to Capital

16

University of Michigan

Health System (“UMHS”)

Duke LifePoint Health Care

(“DLP”)

Strategic Alliance

• UMHS get minority equity

ownership in MMH

• 2 seats on MMH’s board

• U-M’s block “M” brand on

MMH’s logo and the expertise of

UMHS

• UMHS’s equity has the potential

to increasing to as much as 20%.

• LifePoint is a 97% owner of JV

• LifePoint provides access to

capital and operations resources

• Duke will enhance and develop

needed clinical services

• Duke provides access to highly

specialized medical services

• Long-term relationship to evolve

over time

• JV vehicle for acquisitions

• Cleveland Clinic and CHS will

remain independent

organizations

• Expands access and enhances the

level of care provided in the

multi-county region served by

MMH

• Expands UMHS’s presence

within the state of Michigan

• Provides LifePoint with scale

and strong brand recognition

• Makes LifePoint a more

palpable partner for not-for-

profit hospitals

• Duke will have no significant

capital exposure but share in

referral base without acquiring

hospitals and physician groups

• CCF extends its reach and

quality initiatives into new

regions served by CHS’s

network of 135 hospitals

• CHS will advance its clinical

programs through access to

CCF’s expertise in medical

specialties, best practices and

innovation in patient care

Transaction Summary

Transaction Rationale

Health Care Industry Trends Recent Partnerships

Limited Access to Capital

17

2,400

2,500

2,600

2,700

2,800

2,900

3,000

3,100

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Ho

spit

als

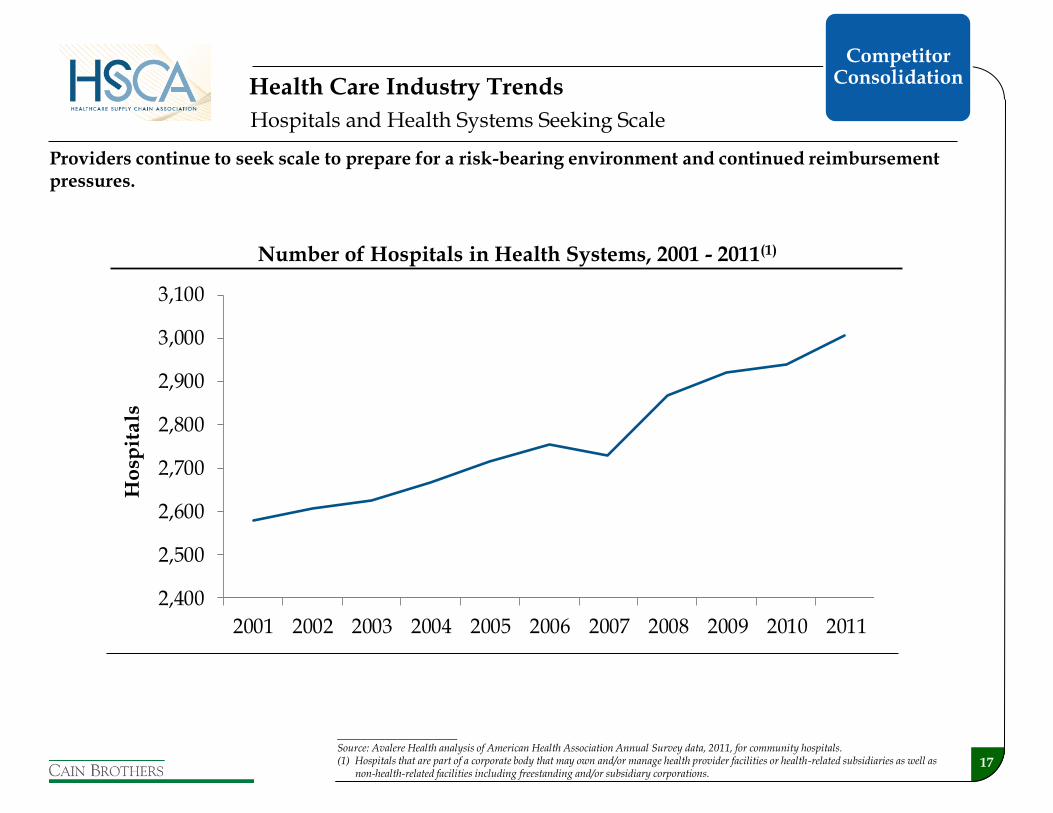

Hospitals and Health Systems Seeking Scale

Health Care Industry Trends

Number of Hospitals in Health Systems, 2001 - 2011(1)

____________________ Source: Avalere Health analysis of American Health Association Annual Survey data, 2011, for community hospitals. (1) Hospitals that are part of a corporate body that may own and/or manage health provider facilities or health-related subsidiaries as well as

non-health-related facilities including freestanding and/or subsidiary corporations.

Providers continue to seek scale to prepare for a risk-bearing environment and continued reimbursement pressures.

Competitor Consolidation

18

Increased transparency and regulation is driving industry towards commoditization

Convergence of Price and Quality:

Market Average Past Future

Health Care Industry Trends

Value Based Purchasing

of Care

19

Increasing focus on interrelationships across all points in the care continuum drives M&A

Pharmacy/ Dispensing

Radiology

Nursing

ICU/CCU

Psych. Lab

MDs

Cardiology

ED

+

Acute Care Value Pyramid

Value

Population Management + Reduced Reimbursement+ Market Characteristics

Clinical Outcomes

Cost Management

Infrastructure Development

Benchmarking / Decision Support

The “Integration” Mandate

Health Care M&A

Value Based Purchasing

of Care

Health Care M&A

21

IT systems

Purchasing

Back office

Human resources

Compliance

+ + + + Economies

of Scale

Human Capital and

Expertise

Risk Management

Capital Formation

Payor Contracting

Physician engagement

Recruiting

Quality and clinical protocols

Standardization

Best practice deployment

Reserves

Revenue, payor, and geographical diversification

Population health capabilities

Improved access to debt capital

Lower debt costs

Investment flexibility

Access to lives

Preferred provider arrangements

Ability to assume greater risk (and related rewards)

Most M&A activity is being driven by an attempt to realize the benefits of scale and to create coordinated care networks to manage population health

The Benefit of Scale

Foundation for Creating an Integrated and Coordinated System of Care

Health Care M&A

22

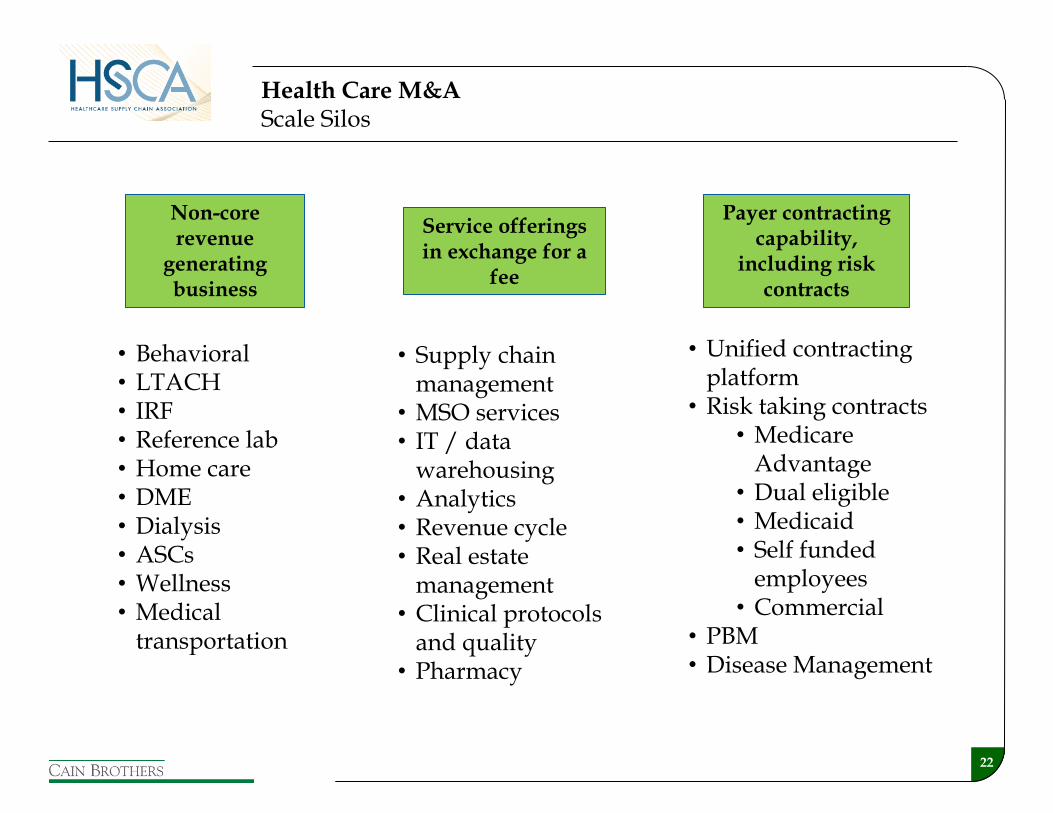

Non-core revenue

generating business

Service offerings in exchange for a

fee

Payer contracting capability,

including risk contracts

Health Care M&A Scale Silos

• Behavioral • LTACH • IRF • Reference lab • Home care • DME • Dialysis • ASCs • Wellness • Medical

transportation

• Supply chain management

• MSO services • IT / data

warehousing • Analytics • Revenue cycle • Real estate

management • Clinical protocols

and quality • Pharmacy

• Unified contracting platform

• Risk taking contracts • Medicare

Advantage • Dual eligible • Medicaid • Self funded

employees • Commercial

• PBM • Disease Management

23

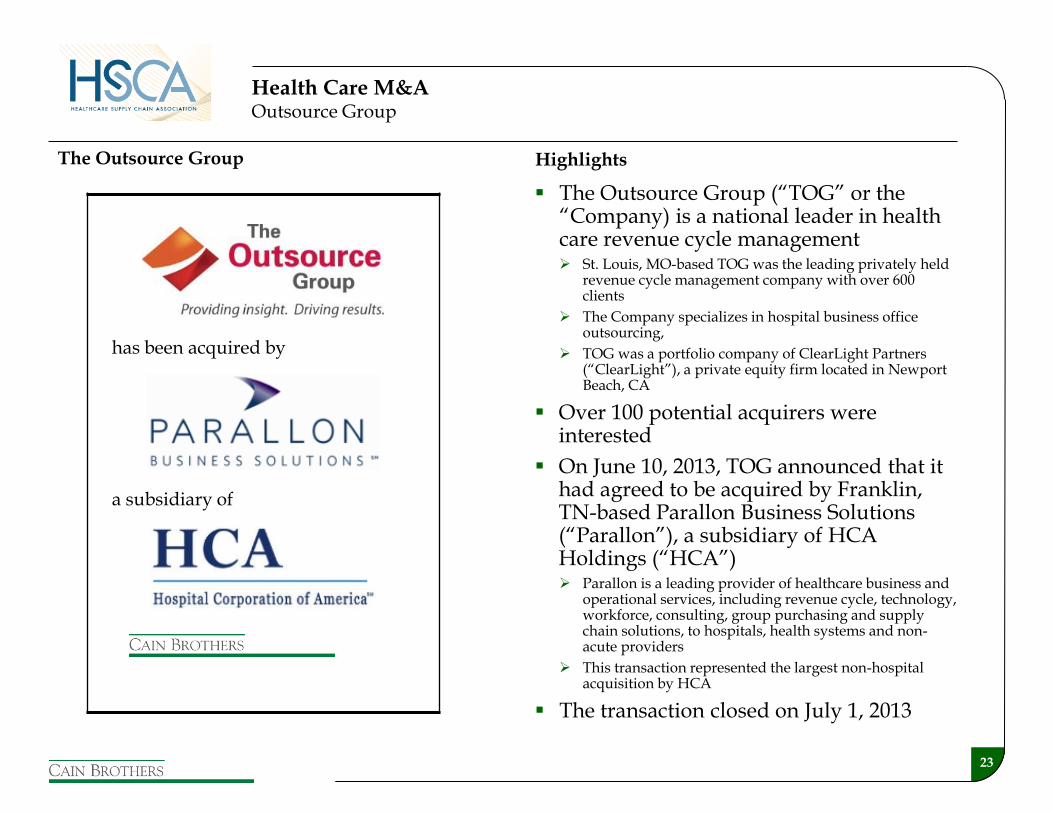

Highlights The Outsource Group

Health Care M&A Outsource Group

a subsidiary of

The Outsource Group (“TOG” or the “Company) is a national leader in health care revenue cycle management St. Louis, MO-based TOG was the leading privately held

revenue cycle management company with over 600 clients

The Company specializes in hospital business office outsourcing,

TOG was a portfolio company of ClearLight Partners (“ClearLight”), a private equity firm located in Newport Beach, CA

Over 100 potential acquirers were interested

On June 10, 2013, TOG announced that it had agreed to be acquired by Franklin, TN-based Parallon Business Solutions (“Parallon”), a subsidiary of HCA Holdings (“HCA”) Parallon is a leading provider of healthcare business and

operational services, including revenue cycle, technology, workforce, consulting, group purchasing and supply chain solutions, to hospitals, health systems and non-acute providers

This transaction represented the largest non-hospital acquisition by HCA

The transaction closed on July 1, 2013

has been acquired by

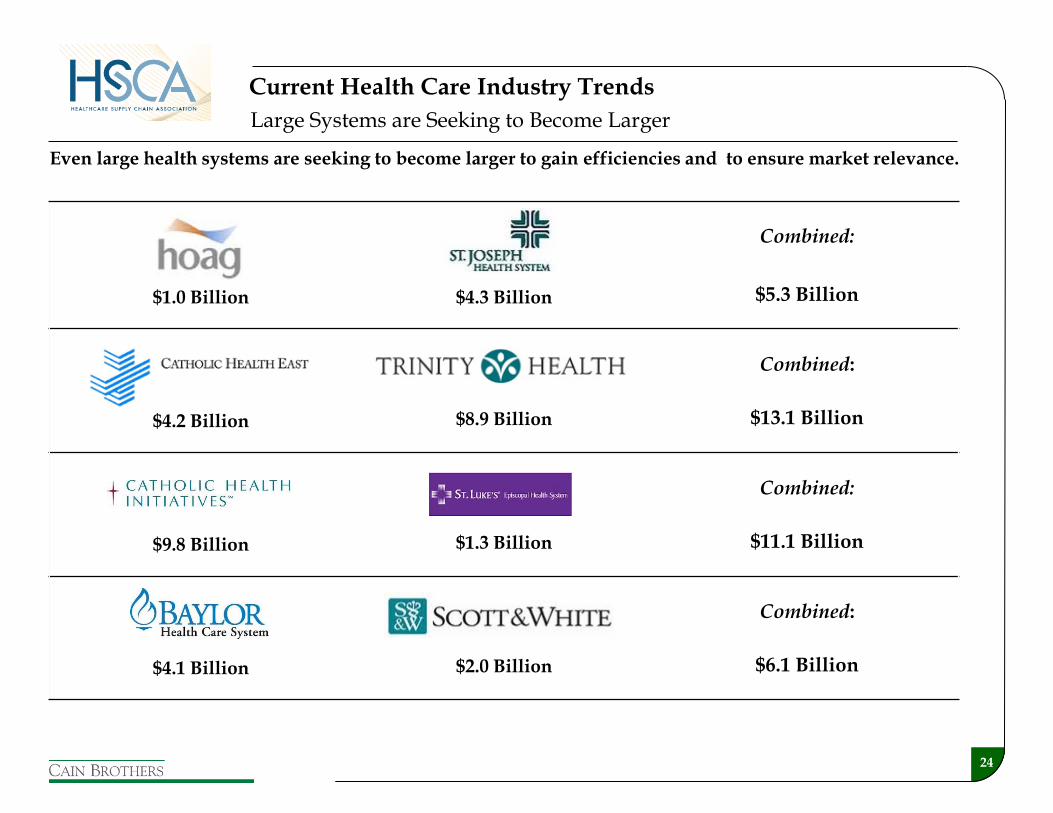

24

$1.0 Billion

$4.3 Billion

Combined:

$5.3 Billion

$4.2 Billion

$8.9 Billion

Combined:

$13.1 Billion

$9.8 Billion

$1.3 Billion

Combined:

$11.1 Billion

$4.1 Billion

$2.0 Billion

Combined:

$6.1 Billion

Large Systems are Seeking to Become Larger

Current Health Care Industry Trends

Even large health systems are seeking to become larger to gain efficiencies and to ensure market relevance.

25

$2.2 Billion

$4.5 Billion

Combined:

$6.7 Billion

Large Systems are Seeking to Become Larger

Current Health Care Industry Trends

Unsuccessful transactions can result from a myriad of issues.

Unclear objectives

Process failure

Poor management and communication with key constituents (particularly physicians)

Inflexibility

Regulatory process

Lack of imagination

Lack of cultural fit

Due diligence results

Economic changes

Material adverse changes due to internal or external factors

Competitor actions

26

M&A Activity Is Accelerating

Hospital transaction volume has been strong over the last three years

Booz & Company predicts that the number of independent hospitals will decrease from 5,000 to 4,000 over the next five to seven years due to consolidation

Affordable Care Act expectations will continue to drive consolidation over the next several years

Noteworthy recent transactions include:

Community Health Systems’ pending acquisition of Health Management Associates

Tenet’s pending acquisition of Vanguard Health Systems

Recently completed merger of Trinity Health and Catholic Health East

Merger of Scott & White Healthcare and Baylor Health Care System (Cain Brothers client)

Duke LifePoint’s acquisition of Marquette General Hospital

Health Care M&A Volume (# of Deals and Hospitals)(1)

Number of Acute Care Hospital Beds Acquired(1)

____________________ Sources: Irving Levin Associates, Inc. and Cain Brothers. (1) YTD statistics are as of June 30, 2013.

60 6053

7386

75

57

153

78

57

198

129

215

106

0

50

100

150

200

250

'07 '08 '09 '10 '11 '12 YTD

Deals Hospitals

22,010

5,282

10,668

19,030

23,527

41,344

21,193

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

'07 '08 '09 '10 '11 '12 YTD

Health Care M&A

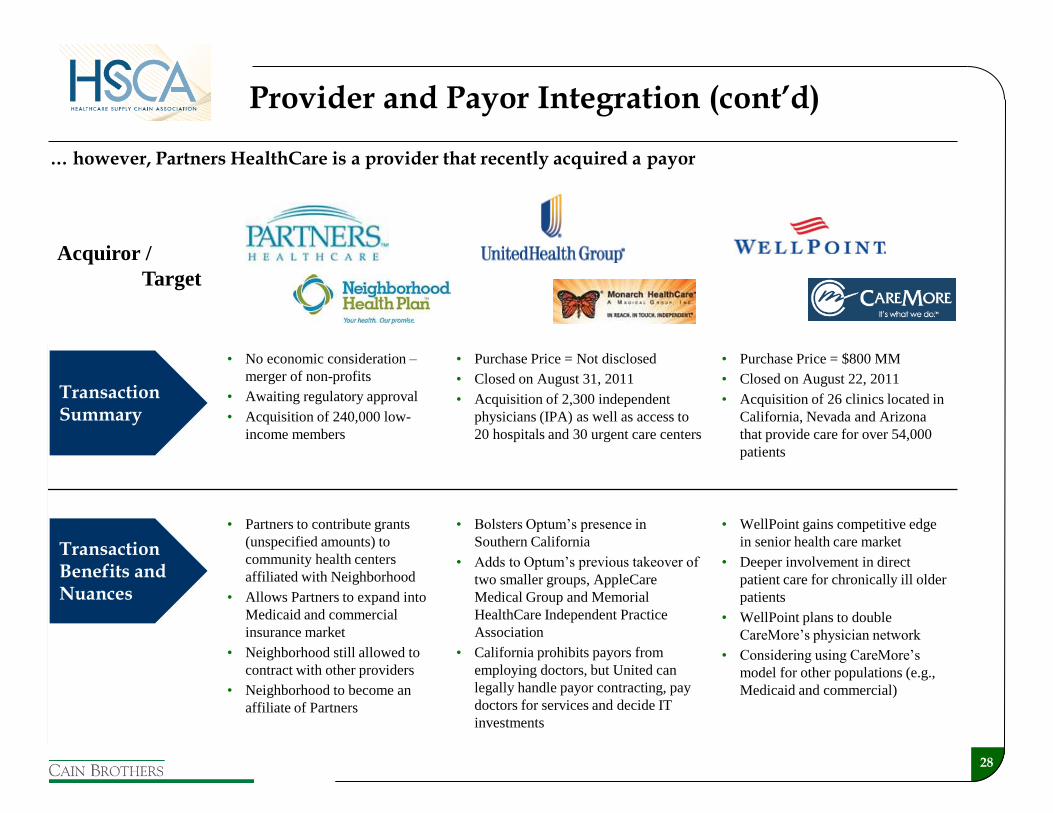

27 ____________________ (1) Relationship consists of a risk-sharing agreement. Not an acquisition by Aetna.

Recent consolidation activity has been oriented to payor acquisitions of providers…

Acquiror /

Target

• Risk-sharing agreement

• Announced on November 21, 2011

• Affiliation with more than 2,000

employed and affiliated physicians

• Purchase Price = $475 MM

• Awaiting regulatory approval

• Acquisition of six 100+ bed

hospitals and related ancillary

businesses, which admit more than

79,000 patients

• Purchase Price = $790 MM

• Closed on December 21, 2010

• Acquisition of 300 medical

centers in 42 states

• Risk-sharing agreement will

compensate Banner on quality,

efficiency, and patient satisfaction

measures

• Members will pay less out of

pocket, receive more coordinated

care and have increased focus on

wellness

• Highmark to focus on quality and

efficient service, rather than revenue

growth

• Allows West Penn to keep open

West Penn Hospital (otherwise

slated to close)

• Maintains provider choice in region

• Driven by local market dynamics –

competitor is an integrated

provider/payor (UPMC)

• Will help Humana reduce costs

and enhance wellness programs

• Primary goal for Humana was to

obtain a physician-management

platform for occupational health

• Concentra has blue-chip work-

site clients: Hewlett Packard;

Whole Foods Market; and Hobby

Lobby

Transaction Summary

Transaction Rationale

(1)

Provider and Payor Integration

28

… however, Partners HealthCare is a provider that recently acquired a payor

Acquiror /

Target

• No economic consideration –

merger of non-profits

• Awaiting regulatory approval

• Acquisition of 240,000 low-

income members

• Purchase Price = Not disclosed

• Closed on August 31, 2011

• Acquisition of 2,300 independent

physicians (IPA) as well as access to

20 hospitals and 30 urgent care centers

• Purchase Price = $800 MM

• Closed on August 22, 2011

• Acquisition of 26 clinics located in

California, Nevada and Arizona

that provide care for over 54,000

patients

• Partners to contribute grants

(unspecified amounts) to

community health centers

affiliated with Neighborhood

• Allows Partners to expand into

Medicaid and commercial

insurance market

• Neighborhood still allowed to

contract with other providers

• Neighborhood to become an

affiliate of Partners

• Bolsters Optum’s presence in

Southern California

• Adds to Optum’s previous takeover of

two smaller groups, AppleCare

Medical Group and Memorial

HealthCare Independent Practice

Association

• California prohibits payors from

employing doctors, but United can

legally handle payor contracting, pay

doctors for services and decide IT

investments

• WellPoint gains competitive edge

in senior health care market

• Deeper involvement in direct

patient care for chronically ill older

patients

• WellPoint plans to double

CareMore’s physician network

• Considering using CareMore’s

model for other populations (e.g.,

Medicaid and commercial)

Transaction Summary

Transaction Benefits and Nuances

Provider and Payor Integration (cont’d)

Strategic Alternatives

30

Strategic Framework

Strategic Evaluation

• Define vision, mission and strategic

objectives

• Understand organizational risk

tolerance

• Understand environment

Internal

External

• Evaluate key activities

Hospital operations

Physician operations

Non-core operations

• Understand the tradeoffs in defending

and extending market share

• Obtain and quantify competitor

intelligence

• Formulate potential strategic

alternatives

• Develop financial forecasts to support

analyses of strategic alternatives

Every situation is different and

health care is still local

Funding Assessment

• Estimate funding requirements for

strategic alternatives considered

• Determine enterprise valuations and

business unit valuations

• Evaluate and prioritize funding options

to meet capital needs

Ability to generate cash from

operations

Debt capacity based on risk

thresholds

Ability to generate philanthropic

giving

Value from non-core asset sales

Value from joint ventures and other

contractual arrangements

Outright sale or merger

• Prioritize strategies based on accretive

opportunities, risk tolerance and

availability and cost of capital

Capital demands to pursue strategies

often exceed capital available thereby

creating a funding gap

Potential Strategic Responses

• Engage in operational improvement

initiatives

Cost efficiencies

Program realignment

Revenue cycle

• Adjust capital plans

Ensure hurdle rate discipline

• Consider acquisition/development

strategies

Hospitals

Outpatient facilities

Physician practices

Other

• Issue debt

• Enter into joint ventures

• Sell non-core operations

Real estate assets

• Pursue other affiliations

• Sell/merge

Balance strategies that can be

financed with strategies that achieve

organizational objectives

Strategic Alternatives

31

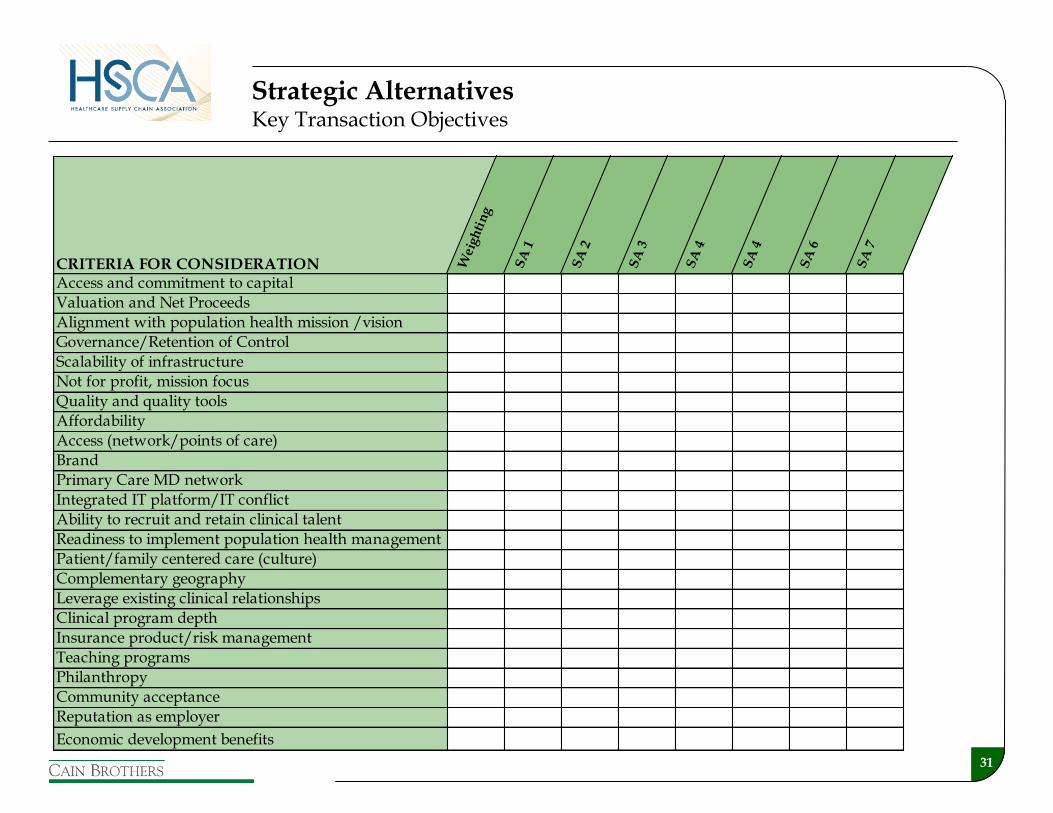

Strategic Alternatives Key Transaction Objectives

CRITERIA FOR CONSIDERATION Wei

ghti

ng

SA

1

SA

2

SA

3

SA

4

SA

4

SA

6

SA

7

Access and commitment to capital

Valuation and Net Proceeds

Alignment with population health mission /vision

Governance/Retention of Control

Scalability of infrastructure

Not for profit, mission focus

Quality and quality tools

Affordability

Access (network/points of care)

Brand

Primary Care MD network

Integrated IT platform/IT conflict

Ability to recruit and retain clinical talent

Readiness to implement population health management

Patient/family centered care (culture)

Complementary geography

Leverage existing clinical relationships

Clinical program depth

Insurance product/risk management

Teaching programs

Philanthropy

Community acceptance

Reputation as employer

Economic development benefits

32

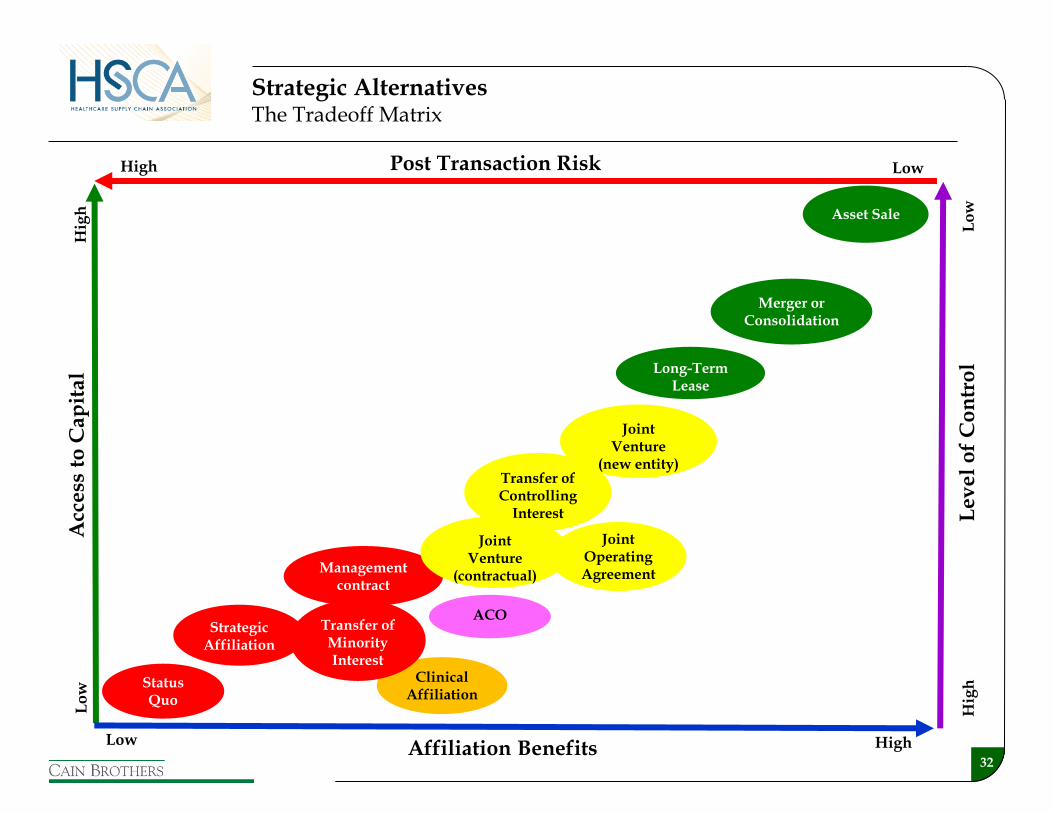

Post Transaction Risk

High Low

Lo

w

Hig

h

Hig

h

Lo

w

Acc

ess

to

Ca

pit

al

High Low

Joint Operating Agreement

Status Quo

Joint Venture

(new entity)

Management contract

Merger or Consolidation

Clinical Affiliation

Asset Sale

Affiliation Benefits

Le

ve

l o

f C

on

tro

l

Strategic Alternatives The Tradeoff Matrix

Strategic Affiliation

Long-Term Lease

Transfer of Controlling

Interest

Joint Venture

(contractual)

Transfer of Minority Interest

ACO

33

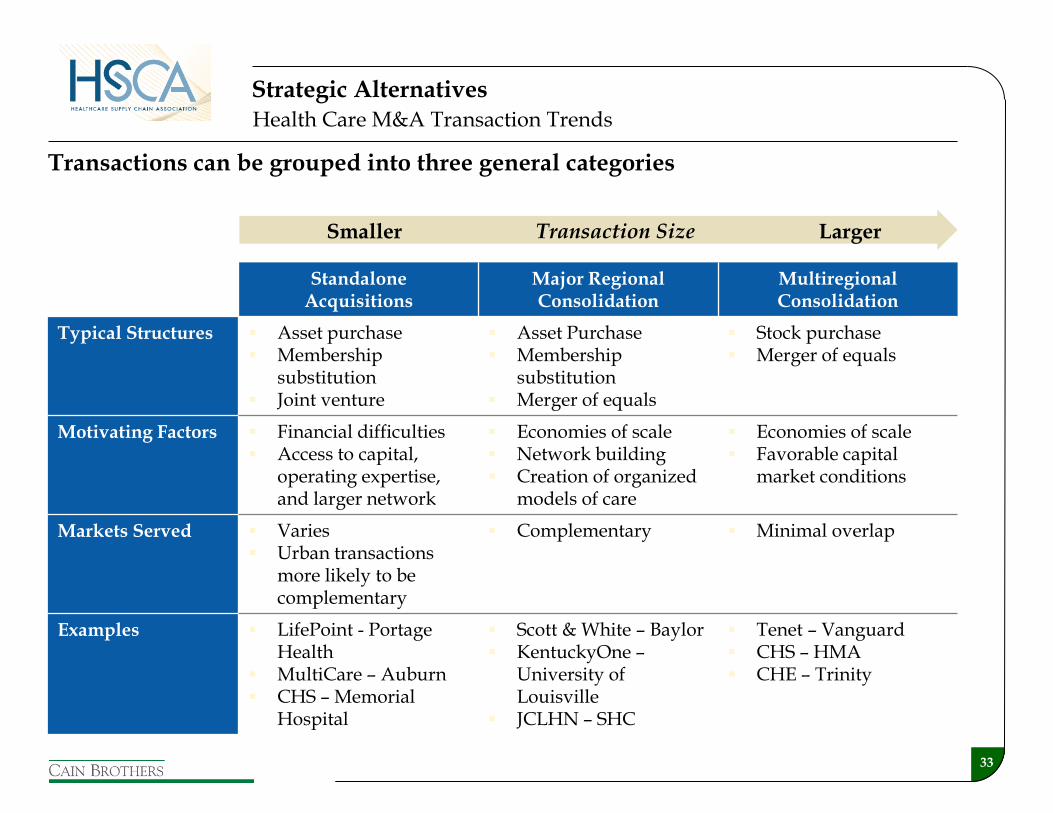

Transactions can be grouped into three general categories

Standalone Acquisitions

Major Regional Consolidation

Multiregional Consolidation

Typical Structures Asset purchase Membership

substitution Joint venture

Asset Purchase Membership

substitution Merger of equals

Stock purchase Merger of equals

Motivating Factors Financial difficulties Access to capital,

operating expertise, and larger network

Economies of scale Network building Creation of organized

models of care

Economies of scale Favorable capital

market conditions

Markets Served Varies Urban transactions

more likely to be complementary

Complementary Minimal overlap

Examples LifePoint - Portage Health

MultiCare – Auburn CHS – Memorial

Hospital

Scott & White – Baylor KentuckyOne –

University of Louisville

JCLHN – SHC

Tenet – Vanguard CHS – HMA CHE – Trinity

Health Care M&A Transaction Trends

Smaller Larger Transaction Size

Strategic Alternatives

34

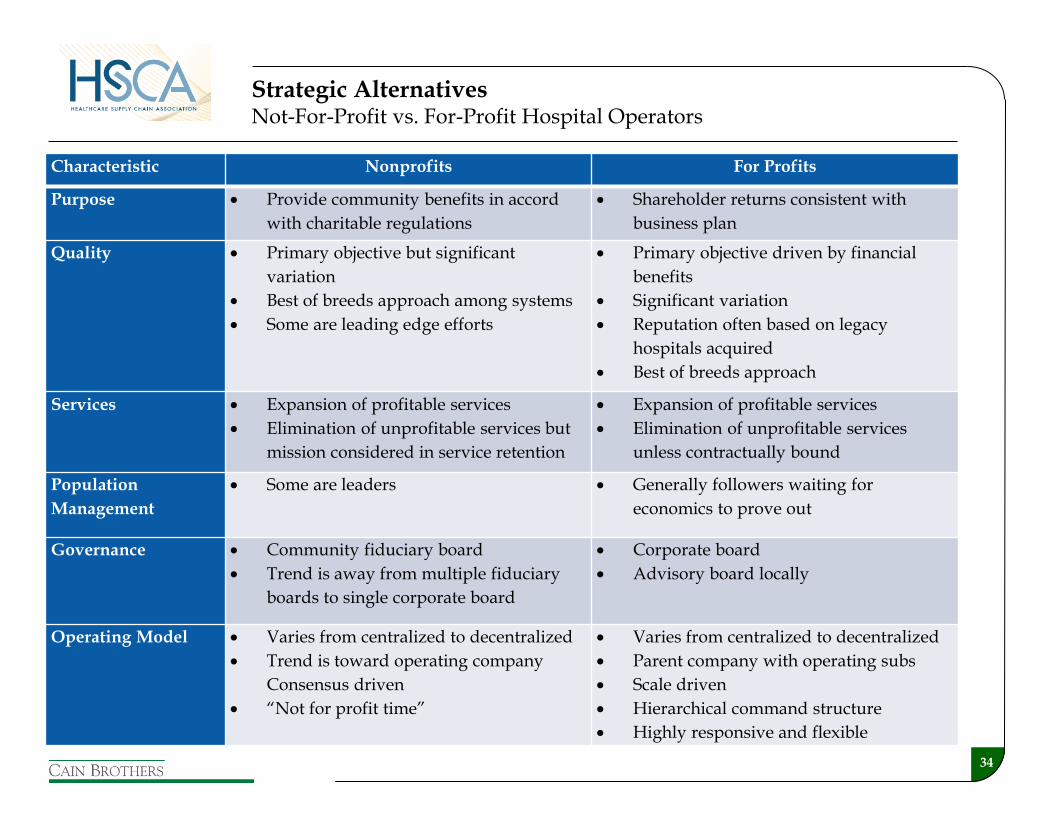

Characteristic Nonprofits For Profits

Purpose Provide community benefits in accord

with charitable regulations

Shareholder returns consistent with

business plan

Quality Primary objective but significant

variation

Best of breeds approach among systems

Some are leading edge efforts

Primary objective driven by financial

benefits

Significant variation

Reputation often based on legacy

hospitals acquired

Best of breeds approach

Services Expansion of profitable services

Elimination of unprofitable services but

mission considered in service retention

Expansion of profitable services

Elimination of unprofitable services

unless contractually bound

Population

Management

Some are leaders Generally followers waiting for

economics to prove out

Governance Community fiduciary board

Trend is away from multiple fiduciary

boards to single corporate board

Corporate board

Advisory board locally

Operating Model Varies from centralized to decentralized

Trend is toward operating company

Consensus driven

“Not for profit time”

Varies from centralized to decentralized

Parent company with operating subs

Scale driven

Hierarchical command structure

Highly responsive and flexible

Strategic Alternatives Not-For-Profit vs. For-Profit Hospital Operators

35

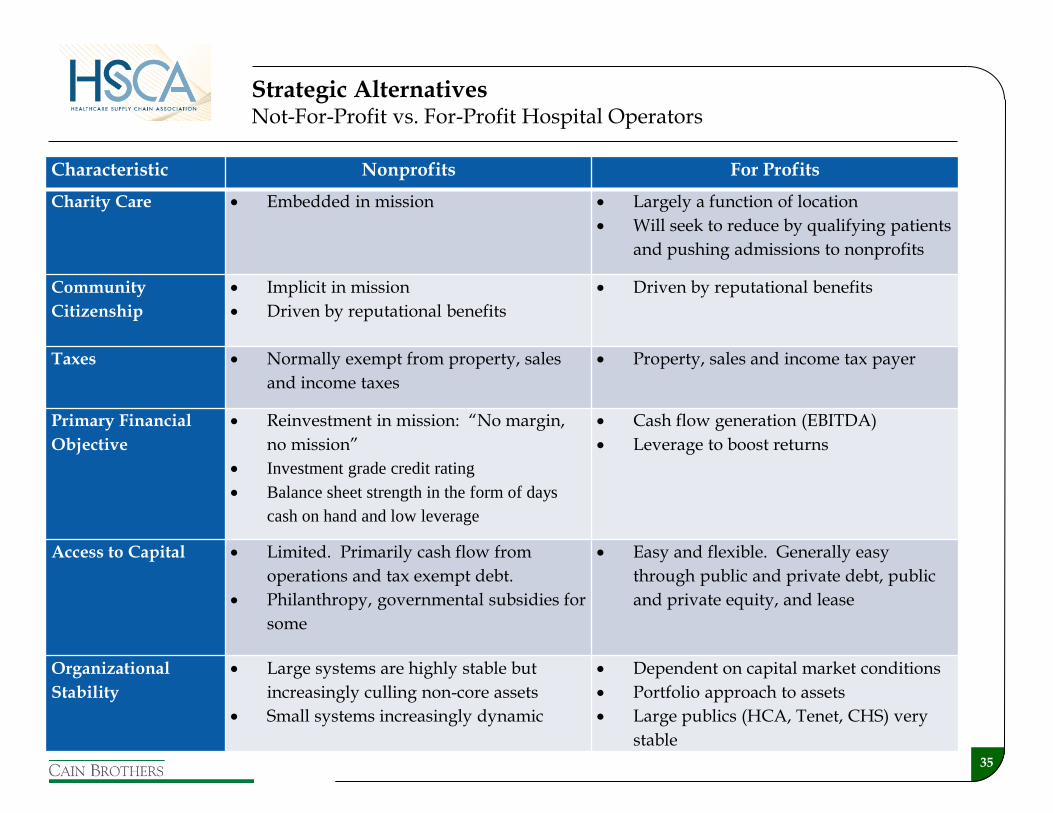

Characteristic Nonprofits For Profits

Charity Care Embedded in mission Largely a function of location

Will seek to reduce by qualifying patients

and pushing admissions to nonprofits

Community

Citizenship

Implicit in mission

Driven by reputational benefits

Driven by reputational benefits

Taxes Normally exempt from property, sales

and income taxes

Property, sales and income tax payer

Primary Financial

Objective

Reinvestment in mission: “No margin,

no mission”

Investment grade credit rating

Balance sheet strength in the form of days

cash on hand and low leverage

Cash flow generation (EBITDA)

Leverage to boost returns

Access to Capital Limited. Primarily cash flow from

operations and tax exempt debt.

Philanthropy, governmental subsidies for

some

Easy and flexible. Generally easy

through public and private debt, public

and private equity, and lease

Organizational

Stability

Large systems are highly stable but

increasingly culling non-core assets

Small systems increasingly dynamic

Dependent on capital market conditions

Portfolio approach to assets

Large publics (HCA, Tenet, CHS) very

stable

Strategic Alternatives Not-For-Profit vs. For-Profit Hospital Operators

36

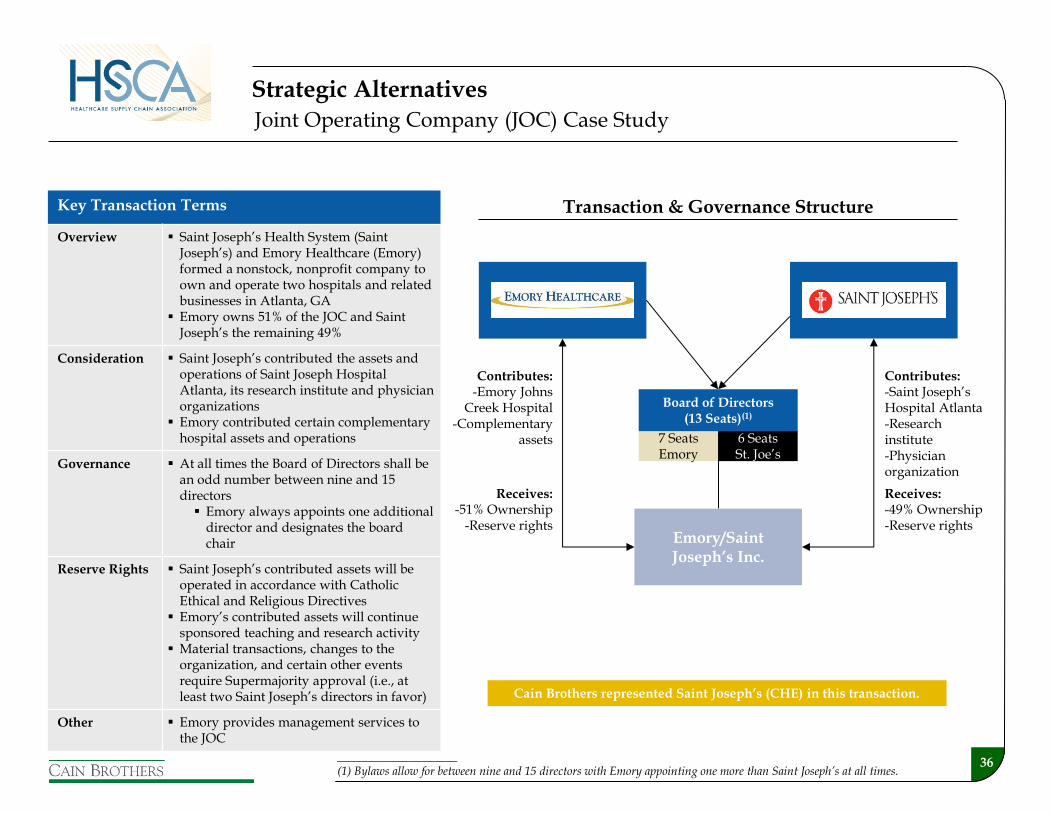

Strategic Alternatives

Joint Operating Company (JOC) Case Study

Key Transaction Terms

Overview Saint Joseph’s Health System (Saint Joseph’s) and Emory Healthcare (Emory) formed a nonstock, nonprofit company to own and operate two hospitals and related businesses in Atlanta, GA

Emory owns 51% of the JOC and Saint Joseph’s the remaining 49%

Consideration Saint Joseph’s contributed the assets and operations of Saint Joseph Hospital Atlanta, its research institute and physician organizations

Emory contributed certain complementary hospital assets and operations

Governance At all times the Board of Directors shall be an odd number between nine and 15 directors Emory always appoints one additional

director and designates the board chair

Reserve Rights Saint Joseph’s contributed assets will be operated in accordance with Catholic Ethical and Religious Directives

Emory’s contributed assets will continue sponsored teaching and research activity

Material transactions, changes to the organization, and certain other events require Supermajority approval (i.e., at least two Saint Joseph’s directors in favor)

Other Emory provides management services to the JOC

Contributes: -Emory Johns

Creek Hospital -Complementary

assets

Emory/Saint Joseph’s Inc.

Contributes: -Saint Joseph’s Hospital Atlanta -Research institute -Physician organization

7 Seats Emory

6 Seats St. Joe’s

Board of Directors (13 Seats)(1)

Receives: -49% Ownership -Reserve rights

Receives: -51% Ownership

-Reserve rights

Transaction & Governance Structure

____________________ (1) Bylaws allow for between nine and 15 directors with Emory appointing one more than Saint Joseph’s at all times.

Cain Brothers represented Saint Joseph’s (CHE) in this transaction.

37

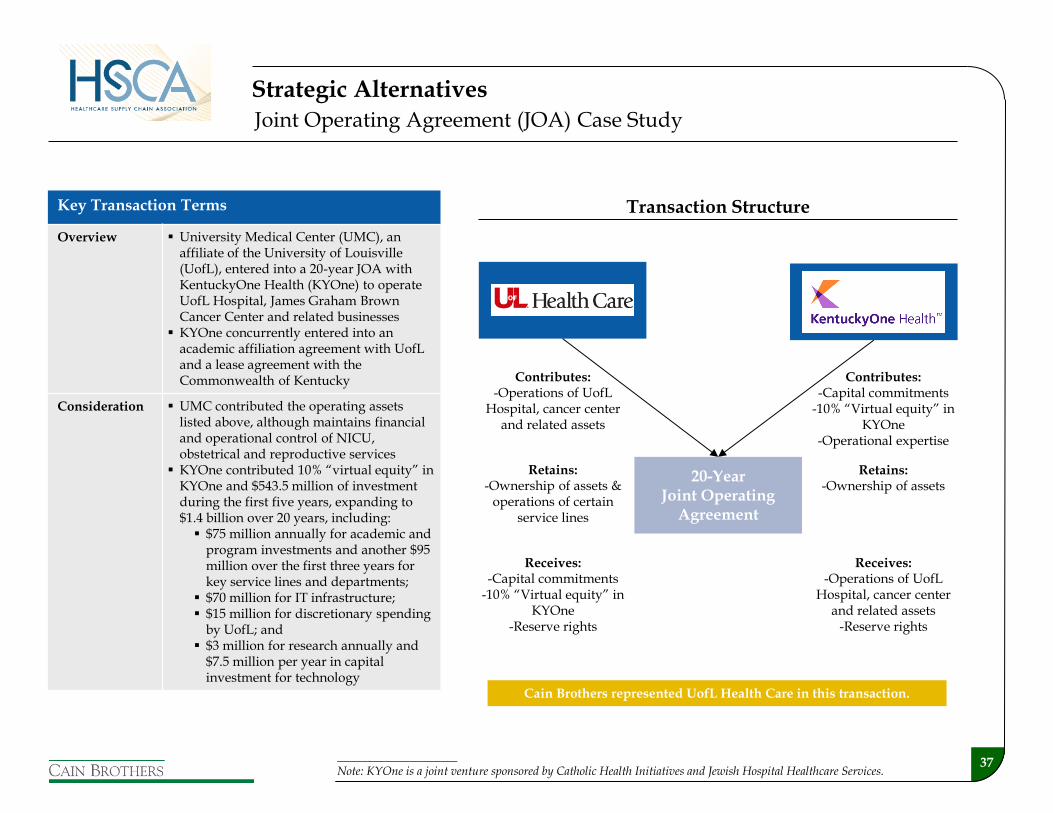

Strategic Alternatives Joint Operating Agreement (JOA) Case Study

Key Transaction Terms

Overview University Medical Center (UMC), an affiliate of the University of Louisville (UofL), entered into a 20-year JOA with KentuckyOne Health (KYOne) to operate UofL Hospital, James Graham Brown Cancer Center and related businesses

KYOne concurrently entered into an academic affiliation agreement with UofL and a lease agreement with the Commonwealth of Kentucky

Consideration UMC contributed the operating assets listed above, although maintains financial and operational control of NICU, obstetrical and reproductive services

KYOne contributed 10% “virtual equity” in KYOne and $543.5 million of investment during the first five years, expanding to $1.4 billion over 20 years, including: $75 million annually for academic and

program investments and another $95 million over the first three years for key service lines and departments;

$70 million for IT infrastructure; $15 million for discretionary spending

by UofL; and $3 million for research annually and

$7.5 million per year in capital investment for technology

Contributes: -Operations of UofL

Hospital, cancer center and related assets

20-Year Joint Operating

Agreement

Receives: -Capital commitments

-10% “Virtual equity” in KYOne

-Reserve rights

Transaction Structure

Retains: -Ownership of assets &

operations of certain service lines

Contributes: -Capital commitments

-10% “Virtual equity” in KYOne

-Operational expertise

Receives: -Operations of UofL

Hospital, cancer center and related assets

-Reserve rights

Retains: -Ownership of assets

____________________ Note: KYOne is a joint venture sponsored by Catholic Health Initiatives and Jewish Hospital Healthcare Services.

Cain Brothers represented UofL Health Care in this transaction.

38

Strategic Alternatives

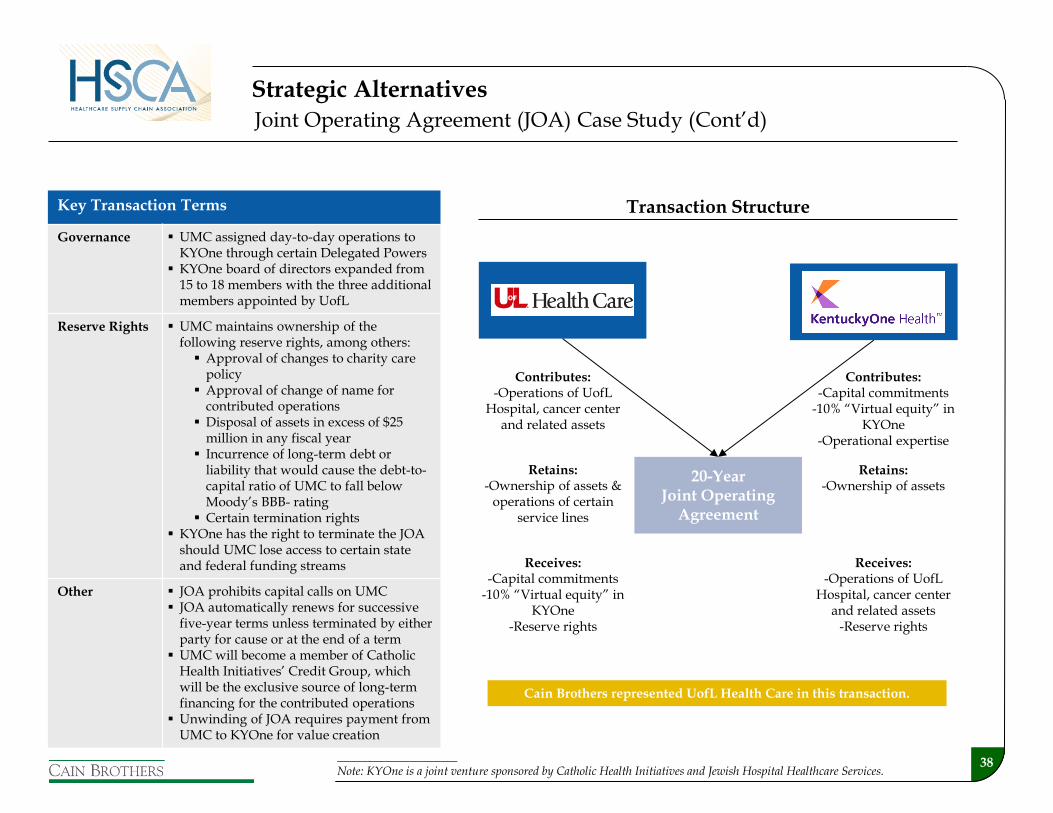

Joint Operating Agreement (JOA) Case Study (Cont’d)

Key Transaction Terms

Governance UMC assigned day-to-day operations to KYOne through certain Delegated Powers

KYOne board of directors expanded from 15 to 18 members with the three additional members appointed by UofL

Reserve Rights UMC maintains ownership of the following reserve rights, among others: Approval of changes to charity care

policy Approval of change of name for

contributed operations Disposal of assets in excess of $25

million in any fiscal year Incurrence of long-term debt or

liability that would cause the debt-to-capital ratio of UMC to fall below Moody’s BBB- rating

Certain termination rights KYOne has the right to terminate the JOA

should UMC lose access to certain state and federal funding streams

Other JOA prohibits capital calls on UMC JOA automatically renews for successive

five-year terms unless terminated by either party for cause or at the end of a term

UMC will become a member of Catholic Health Initiatives’ Credit Group, which will be the exclusive source of long-term financing for the contributed operations

Unwinding of JOA requires payment from UMC to KYOne for value creation

Contributes: -Operations of UofL

Hospital, cancer center and related assets

20-Year Joint Operating

Agreement

Receives: -Capital commitments

-10% “Virtual equity” in KYOne

-Reserve rights

Transaction Structure

Retains: -Ownership of assets &

operations of certain service lines

Contributes: -Capital commitments

-10% “Virtual equity” in KYOne

-Operational expertise

Receives: -Operations of UofL

Hospital, cancer center and related assets

-Reserve rights

Retains: -Ownership of assets

____________________ Note: KYOne is a joint venture sponsored by Catholic Health Initiatives and Jewish Hospital Healthcare Services.

Cain Brothers represented UofL Health Care in this transaction.

39

-Ownership

Strategic Alternatives

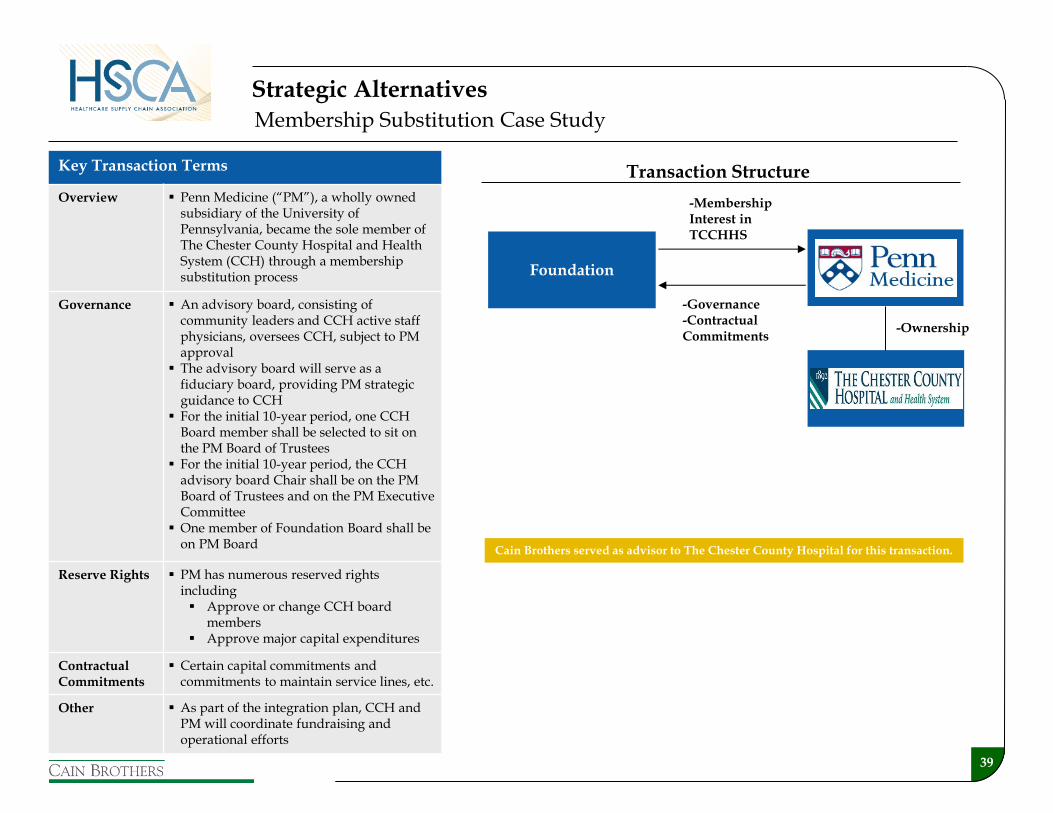

Membership Substitution Case Study

Key Transaction Terms

Overview Penn Medicine (“PM”), a wholly owned subsidiary of the University of Pennsylvania, became the sole member of The Chester County Hospital and Health System (CCH) through a membership substitution process

Governance An advisory board, consisting of community leaders and CCH active staff physicians, oversees CCH, subject to PM approval

The advisory board will serve as a fiduciary board, providing PM strategic guidance to CCH

For the initial 10-year period, one CCH Board member shall be selected to sit on the PM Board of Trustees

For the initial 10-year period, the CCH advisory board Chair shall be on the PM Board of Trustees and on the PM Executive Committee

One member of Foundation Board shall be on PM Board

Reserve Rights PM has numerous reserved rights including Approve or change CCH board

members Approve major capital expenditures

Contractual Commitments

Certain capital commitments and commitments to maintain service lines, etc.

Other As part of the integration plan, CCH and PM will coordinate fundraising and operational efforts

Transaction Structure

Cain Brothers served as advisor to The Chester County Hospital for this transaction.

Foundation

-Membership Interest in TCCHHS

-Governance -Contractual Commitments

40

Strategic Alternatives

Clinical Affiliation Case Study

Key Transaction Terms

Overview Through a Joint Powers Affiliation Agreement and related contracts, UC San Diego (UCSD) transferred virtually all of its pediatric operations to Children’s Hospital and Health Center (CHHC)

Consideration CHHC established an Academic Fund to replace the financial support traditionally provided by the UCSD Medical Center to the UCSD School of Medicine for peds

CHHC provided facilities to house UCSD personnel and a $5 million commitment for the construction of a research building

A new leadership position of Physician-In-Chief was established to guide the vision of creating a world-class academic children’s health center

Governance CHHC increased the size of its Board from 15 to 18 Trustees, of which a third of the positions are to be held by UCSD

Similar amendments were made to Children’s Hospital, San Diego’s Board

Reserve Rights CHHC’s governing documents were amended to include the clinical, research, and academic missions of UCSD Health Services as a purpose of the corporation

Other CHHC became the primary pediatric teaching and research site for UCSD

Pediatric specialty physicians of UCSD Medical Group became members of Children’s Specialists of San Diego

Transaction Structure

Cain Brothers represented UC San Diego in this transaction.

UCSD Pediatric

Operations

UCSD Pediatric

Operations

Contributes: -Pediatric operations

Receives: -Ongoing academic support payments -Governance rights

Contributes: -Ongoing academic support payments -Governance rights

Receives: -UCSD pediatric

operations