-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

1/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

2*

An In-Depth Analysis of the Altman’s Failure Prediction

Model

on Corporate Financial Distress in Uchumi Supermarket

in Kenya

+dam S,isia1 illiam Sang

1( 2Sera, aitindi

1( 2( $ r alter Bi/,anga %io

1( 2( $( )

1. S/,ool of Business and E/onomi/s( Mount en3a 4niersit3( !%

Bo6$)2 /ode 01000 7,ia( en3a8 E-Mail /orresponding aut,or

adams,isia:gmail./om

2. S/,ool of Business and E/onomi/s( aara 4niersit3( !riate Bag

; 2015* Nauru( en3a8 E-Mailsanipwil:gmail./om

$. S/,ool of Business and E/onomi/s( Mount en3a 4niersit3( !%

Bo6$)2 /ode 01000 7,ia( en3a8 E-Mail waitsara,:3a,oo./o.u

). S/,ool of Business and E/onomi/s( Mount en3a 4niersit3( !.%

Bo6$)2 /ode 01000 7,ia( en3a8 E-Mail walter.oio:3a,oo./om

Astract

Man3 firms in deeloping and transitional e/onomies are in

finan/ial distress situation( due to low leel of det

seri/e /oerage. 7,e stud3 of finan/ial distress ,as e/ome a

signifi/ant gloal issue after t,e gloal finan/ial/risis of 200#.

7,e soaring gloal finan/ial /risis w,i/, ,as resulted to in/reased

/ases of usiness failuresresulting from t,e effe/t of anrupt/3 as

well as insolen/3. 7,is stud3 t,erefore was /ondu/ted wit,

t,eoation=s re/ords su/, as in-,ouse maga>ines(

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

2/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

2#

Harrett 200#" noted t,at w,en t,e firm is in a finan/ial

distress( it fa/es one of two possile /onfli/tsAeit,er /as,

s,ortage on t,e assets side of t,e alan/e s,eet( or as a det

oer,ang in liailities. Bot, sets of/ir/umstan/es ,oweer draw

similar results( namel3 t,at /as, flow is insuffi/ient to /oer

/urrent oligations.7,is for/es firms into negotiations wit,

/reditors aout t,e /onditions of deferment on t,eir det

repa3mentduring t,e ensuing period of distressed restru/turing. ,en

t,e firms enter finan/ial distress( t,e3 are ?ui/l3

/onfronted wit, t,e dilemma of raising /apital to fund t,eir

restru/turing %ute/,ea( 200*". Hien t,at( few areliale to trust

t,is ris3 inestment( espe/iall3 w,en taing into /onsideration t,at

a finan/ial oost is not aguarantee to proide a lasting solution to

t,e prolems at ,and.

7raditional iews of t,e /auses of finan/ial distress( w,i/, ,ae

oer time een partiall3 /onfirmed 3empiri/al results +ndrade and

aplan( 199#A +s?uit, et al.( 199)A 7,eodossiou et al.( 199' and

,itaer 1999"(

proide some eiden/e t,at finan/ial distress arises in man3

/ases from endogenous ris fa/tors( su/, asmismanagement( ,ig,

leerage( and a non-effi/ient operating stru/ture in pla/e.

#$#$# Financial Distress

%pler and 7itman 199)" define finan/ial distress more roadl3 as

a /ostl3 eent t,at affe/ts t,e relations,ip todet ,olders and

non-finan/ial stae,olders. +s a /onse?uen/e( a /ompan3 gains an

impaired a//ess to new/apital and ears t,e in/reasing /osts of

maintaining t,is stri/en relations,ip. +s a rule( t,e term

Dfinan/ialdistress is used in a negatie /onnotation in order to

des/rie t,e finan/ial situation of a /ompan3 /onfrontedwit, a

temporar3 la/ of li?uidit3 and wit, t,e diffi/ulties t,at ensue in

fulfilling finan/ial oligations on

s/,edule and to t,e full e6tent Hordon( 19*1".Hordon 19*1"

argued on ,is arti/le t,at t,e deelopment of t,e t,eor3 of

finan/ial distress as a

pro/ess ,aing spe/ifi/ d3nami/s. Hordon ,ig,lig,ts t,at

finan/ial distress is onl3 one state of t,e pro/ess(followed 3

failure and restru/turing( and s,ould e defined in terms of

finan/ial stru/ture and se/urit3 aluation.7,e /orporation enters

t,is state w,en its power to generate earnings is e/oming wea and

t,e amount of dete6/eeds t,e alue of t,e /ompan3=s total assets.

,itaer 1999" interpreted finan/ial distress as a /ru/ial eentw,ose

o//urren/e separates t,e time of a /ompan3=s finan/ial ,ealt, from

t,e period of finan/ial illness andre?uires undertaing /orre/tie

a/tions in order to oer/ome t,e trouled situation.

+ndrade and aplan 199#" identif3 two forms of finan/ial distress

t,e first one is default on a det pa3ment( and t,e se/ond one

is an attempt to restru/ture t,e det in order to preent t,e default

situation.inan/ial distress o//urs w,en a /ompan3 does not ,ae

/apa/it3 to fulfill its liailities to t,e t,ird parties+ndrade and

aplan( 199#". In/reasing non-performing loan of /ommer/ial ans and

delisted of puli//ompanies in Indonesia is a t3pi/al p,enomenon of

/orporate finan/ial distress. Hestel et al. 200'"

/,ara/teri>efinan/ial distress and failure as t,e result of

/,roni/ losses w,i/, /ause a disproportionate in/rease in

liailitiesa//ompanied 3 s,rinage in t,e asset alue.

7urets3 and Ma/Ewen 2001" define finan/ial distress as a series

of suse?uent stages /,ara/teri>ed 3 a spe/ial set of aderse

finan/ial eents. Ea/, stage of finan/ial distress ,as a distress

point and /ontinuesuntil t,e ne6t distress point is rea/,ed.

7e/,ni/all3( ea/, stage of finan/ial distress is defined as an

interal

etween two distress points. 7,e onset of finan/ial

distress egins wit, a olatile de/rease from positie tonegatie /as,

flow. 7,e following diidend redu/tion signali>es t,e /,ange to

t,e ne6t stage leading to default.7e/,ni/al default on det pre/edes

trouled det restru/turing w,i/, usuall3 tends to redu/e t,e ris of

potential

anrupt/3. 7,us( for t,e first time( resear/,ers su//eeded

in des/riing finan/ial distress as a /ontinuous pro/ess wit, a

/lear stru/ture and a /ategori>ation of t,e distress eents.

#$#$% Altman’s Failure Prediction Model+ltman deeloped seeral

dis/riminant fun/tionsA t,e first one /alled @-s/ore was deeloped

in 19'# using

puli/ firms stratified 3 industr3 and si>e. 7,is model

,as ,ig, predi/tie power two 3ears prior to anrupt/3.+dditionall3(

two adaptation of t,e 19'#=s @-s/ore model are presented t,e

@=-s/ore +ltman 199$" w,i/, issimilar to t,e preious one e6/ept t,e

dis/rimination >ones and t,e @-s/ore +ltman 200'" w,i/, differs

fromt,e preious M+ models in t,at it uses four finan/ial ratios and

,as lower dis/rimination >ones /ompared tot,e preious ones.

+ finan/ial ratio is a relatie magnitude of two sele/ted

numeri/al alues taen from an enterprisesfinan/ial statements

!ande3( 2010". %ften used in a//ounting( t,ere are man3 standard

ratios used in ealuatingt,e oerall finan/ial /ondition of a

/orporation. In finan/ial anal3sis( a ratio is used as a en/,mar

forealuating t,e finan/ial position and performan/e of a firm

Edmister( 19*2". inan/ial ratios ma3 e used 3managers wit,in a

firm( 3 /urrent and potential s,are,olders owners" of a firm( and 3

a firms /reditors.inan/ial anal3sts use finan/ial ratios to /ompare

t,e strengt,s and weanesses in arious /ompanies.

7,e /ore ingredient of multiariate dis/riminant anal3sis is

finan/ial ratios. 7,is /onfirms t,atfinan/ial ratios and ratio

anal3sis are aluale tools for tra/ing finan/ial ,ealt, of an

enterprise. %lson 19#0"

used eig,t traditional finan/ial ratios in ,is model and

/on/luded t,at total liailit3 diided 3 total assets(/urrent

liailit3 diided 3 /urrent assets( and si>e are t,e most

important predi/tors. !redi/tie power offinan/ial ratio depends on

its ailit3 to dis/riminate etween anrupt and non-anrupt. inan/ial

ratios

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

3/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

29

appli/ations in/lude determination of internal li?uidit3(

finan/ial riss( operating performan/e and growt,.inan/ial ratios

are interrelated and t,erefore are anal3>ed in relation to ea/,

ot,er. ,anges in finan/ial ratiosand /as, flow trend oertime or

/ompared wit, similar firms in t,e industr3 ma3 indi/ate potential

prolems ors3mptoms in spe/ifi/ area +ltman( 200'". or e6ample

in/reasing or ,ig, /urrent ratio indi/ates poor effi/ien/3of woring

/apital and related s3mptoms /ould e ,ig, /as, /onersion /3/les(

low re/eiales turnoer or low

return on assets. Benation. 7,e first t,ree ran/,es wereopened

in 19*'. 4/,umi e/ame a trendsetter in low pri/ing to t,e adantage

of all /onsumers( w,ile at t,e sametime maintaining ,ig, standards

in ?ualit3 of goods and seri/es.

In t,e 1990s 4/,umi spear,eaded t,e ,3permaret /on/ept in en3a.

7,e introdu/tion of t,e,3permaret /on/ept and spe/ialt3 s,ops ,as

een a runawa3 su//ess. It was /redited for ,aing

reolutioni>edt,e retail food se/tor 3 giing /ustomers a ariet3

of produ/ts to /,oose from and introdu/ing t,e /on/ept

ofself-seri/e. It ,as also een a ma

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

4/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$0

%$#$% 0ntropy .heory

+//ording to t,e Entrop3 7,eor3 Balan/e S,eet e/omposition

Measure 7,eor3"( one wa3 of identif3ing firms=finan/ial distress

/ould e a /areful loo at t,e /,anges o//urring in t,eir alan/e

s,eets +>i> G ar( 200'".7,is t,eor3 emplo3s t,e 4niariate

+nal3sis and Multiple is/riminant +nal3sis M+" in e6amining

/,angesin t,e stru/ture of alan/e s,eets. 4niariate +nal3sis is t,e

use of a//ounting ased ratios or maret indi/ators

for t,e distress ris assessment Natalia( 200*". 7,e finan/ial

ratios of ea/, /ompan3( t,erefore( are /omparedon/e at a time and

t,e distin/tion of t,ose /ompanies t,roug, a single ratio wit, a

/ut ; off alue is used to/lassif3 a /ompan3 as eit,er distressed or

non- distressed Monti G Moriano( 2010".

M+ Multiariate Statisti/ or Multiariate anal3sis" is a

statisti/al anal3sis in w,i/, more t,an oneariale are anal3>ed

at t,e same time Slotemaer( 200#". 7,e aim of M+ is to eliminate

t,e weaness ofuniariate anal3sis. irst( single ratios /al/ulated 3

uniariate anal3sis do not /apture time ariation of finan/ialratios.

7,is means t,at a//ounting ratios ,ae t,eir predi/tie ailit3 one at

a time( and it is impossile toanal3>e( for instan/e( rates of

/,ange in ratios oer time. Se/ond( single ratios ma3 gie

in/onsistent results ifdifferent ratio /lassifi/ations are applied

for t,e same firm. 7,ird( man3 a//ounting ariales are

,ig,l3/orrelated( so t,at t,e interpretation of a single ratio in

isolation ma3 e in/orre/t. 7,e single ratio is not ale to/apture

multidimensional interrelations,ips wit,in t,e firm. inall3( sin/e

t,e proailit3 of failure for a sampleis not t,e same as for t,e

population( spe/ifi/ alues of t,e /utoff points otained for t,e

sample will not e alidfor t,e population Natalia( 200*". 7,erefore(

if a firm=s finan/ial statements refle/t signifi/ant /,anges in

t,e

/omposition of assets and liailities on its alan/e-s,eet it is

more liel3 t,at it is in/apale of maintaining t,ee?uilirium state.

If t,ese /,anges are liel3 to e/ome un/ontrollale in future( one

/an foresee finan/ialdistress in t,ese firms +>i> G ar(

200'".

%$#$& Credit /isk .heory

redit is t,e proision of goods and seri/es to a person or entit3

on agreed terms and /onditions w,ere t,e pa3ments are to e

made later wit, or wit,out interest. uring t,e /ontra/t period( not

all detors will repa3 t,eirdues as and w,en t,e3 fall due. ,en t,e

detor does not pa3 t,eir dues on t,e due date( t,e lender is

e6posed to/redit riss w,i/, ma3 in turn lead to default. redit ris

is t,erefore t,e inestor=s ris of loss( finan/ial orot,erwise(

arising from a orrower w,o does no pa3 ,is or ,er dues as agreed in

t,e /ontra/tual terms Natalia(200*". redit ris t,eories( /losel3

related to Basel I and Basel II a//ordsA mostl3 refer to t,e

finan/ial firm. 7,e

proposed Basel II framewor /onsists of t,ree pillars 1"

minimum /apital re?uirements( /urrentl3 set e?ual to#( a//ording to

a purposel3-defined /apital ratio( 2" superisor3 reiew of an

institution=s internal assessment

pro/ess and /apital ade?ua/3( $" effe/tie use of puli/

dis/losure to strengt,en maret dis/ipline as a/omplement to

superisor3 efforts. 7,e /urrent Basel II +//ord utili>es /on/ept

of a /apital ratio t,at is/al/ulated diiding an=s /apital amount 3

a measure of ris fa/ed 3 it referred to ris-weig,ted assets"

+s noted 3 estgaard and ie in large amounts promptl3 !ande3(

2005". +n imalan/e etween /as, inflows and outflows wouldmean

failure of /as, management fun/tion of t,e firm. !ersisten/e of

su/, an imalan/e ma3 /ause finan/ialdistress to t,e firm and(

,en/e( usiness failure +>i> G ar( 200'".

%$#$1 2amler’s /uin .heory

Hamler Cuin t,eor3 was deeloped 3 eller( in 19'# w,o ased it on

t,e proailit3 t,eor3 w,ere agamler wins or loses mone3 3 /,an/e.

7,e gamler starts out wit, a positie( aritrar3( amount of

mone3w,ere t,e gamler wins a dollar wit, proailit3 p and loses a

dollar wit, a proailit3 1-p" in ea/, period. 7,e

game /ontinues until t,e gamler runs out of mone3 Espen( 1999".

7,e firm /an e t,oug,t of as a gamler pla3ing repeatedl3 wit,

some proailit3 of loss( /ontinuing to operate until its net wort,

goes to >eroanrupt/3". In /onte6t of t,e firm=s finan/ial

distress( firm would tae t,e pla/e of a gamler. irm would

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

5/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$1

/ontinue to operate until its net wort, goes to >ero( point

w,ere it would go anrupt. 7,e t,eor3 assumes t,atfirm ,as got some

gien amount of /apital in /as,( w,i/, would eep entering or e6iting

t,e firm on random

asis depending on firm=s operations. In an3 gien period(

t,e firm would e6perien/e eit,er positie or negatie/as, flow. %er a

run of periods( t,ere is one possile /omposite proailit3 t,at /as,

flow will e alwa3snegatie. Su/, a situation would lead t,e firm to

de/lare anrupt/3( as it ,as gone out of /as,. Fen/e( under

t,is approa/,( t,e firm remains solent as long as its net wort,

is greater t,an >ero. 7,is net wort, is /al/ulatedfrom t,e

li?uidation alue of sto/,olders= e?uit3.it, an assumed initial

amount of /as,( in an3 gien period(t,ere is a net positie t,at a

firm=s /as, flows will e /onsistentl3 negatie oer a run of periods(

ultimatel3leading to anrupt/3 +>i> G ar( 200'". 7,e mae

t,einternal signals of failure and lame e6ternal /,anges for t,eir

usiness de/line. Fot/,iss 1995" e6amined t,erelations,ip etween

management /,anges and post-anrupt/3 performan/e. %er )0 out of 19*

puli//ompanies t,at emerged from etween 19*9 and 19## /ontinued to

e6perien/e operating losses in t,ree 3earsfollowing anrupt/3( $2

re-enter anrupt/3 or priatel3 restru/ture t,eir det. Fot/,iss 1995"

suggestedt,at t,e /ontinued inolement of pre-anrupt/3 management in

t,e restru/turing pro/ess is strongl3 asso/iatedwit, poor

post-anrupt/3 performan/e. Fer results s,ow t,at retaining

pre-anrupt/3 management is strongl3related to worse post-anrupt/3

performan/e.

,ere ot,er /ompanies ,ae undertaen management su//ession

planning for e3 roles and identified,ig, potential in t,eir

/ompan3=s emplo3ee=s( usuall3 firms in finan/ial distress do not

prepare at all for topmanagement su//ession Hallowa3 G Jones(

200'". 7,is /ould lead to re/ruiting unalan/ed management teamw,i/,

la/ essential sills to steer t,e /ompan3 a,ead. +n3 wrong inestment

de/ision made ma3 plunge t,e/ompanies to finan/ial distress sin/e

some of t,e de/ision s inoles ,uge /as, outla3 are irreersile.

7,e importan/e of innoation to a firms= future ,as een

do/umented e6tensiel3( t,oug, t,e leel ofris asso/iated wit,

innoation ,as een e6amined to a small degree ,ao( Kipson G

Koutsina( 2012". 7,e

proailit3 t,at innoation will drie a firm to finan/ial

distress is ,ig, espe/iall3 w,ere t,e /ompetitorsintrodu/es

innoatie and /ompetitie produ/ts w,i/, redu/es t,e attra/tieness of

t,e /ompan3=s produ/ts andseri/es Ja,ur G Puadir( 2012". 7,erefore(

innoation /an eit,er gie a firm a /ompetitie edge to its rials

orwill see its demise e?uall3.

,ile most /ompanies rel3 on t,eir finan/ial performan/es as t,e

e3 arometer of finan/ial ,ealt,( itis important not to ignore

managerial and operational signals @waig G !i/ett( 2012". Man3

profitale

usinesses ,ae found t,emseles in troule due to rapid

e6pansion lie 4/,umi Supermarets or t,eintrodu/tion of a formidale

/ompetitor @waig G !i/ett( 2012". In ea/, of t,ese instan/es( t,e

/ompanies weresu//essful efore an operational eent or un,eeded

signal led to finan/ial prolem and in some /ases t,esuse?uent

failure of t,e /ompan3. In ot,er /ountries( t,e usiness t,at were

ale to re/ogni>e earlier warningsigns su/, as @ellers( anadians

7ire and 7,e Ba3 ,ae suried 3 diffentiating t,emseles or /,anging

andimproing t,eir usiness model @waig G !i/ett( 2012"

%$& .he Costs of Corporate Financial Distress

In t,eor3( finan/ial distress and anrupt/3 matter if t,e3 impose

dead-weig,t /osts on t,e firm t,at are orne 3t,e s,are,olders

t,roug, an e6 ante /ompensation to t,e /reditors for t,e possiilit3

of in/urring t,ese /osts e6

post. In addition( finan/ial distress and anrupt/3 ma3

impose /osts on stae,olders ot,er t,an t,e firm=s/apital

/ontriutors. 7o t,e e6tent t,at finan/ial distress and anrupt/3 are

/ostl3( and if t,ese /osts areineitale( t,en irtuall3 all /orporate

finan/ial de/isions will e affe/ted 3 su/, /osts. 7,us( t,e

magnitude oft,e finan/ial distress and anrupt/3 /osts is an

important empiri/al ?uestion.

%$&$# Direct Costsire/t anrupt/3 /osts are t,e legal(

administratie and adisor3 fees t,at t,e firm ears as a result of

enteringt,e formal anrupt/3 pro/ess. arner 19**" estimates t,e

dire/t /ost to e around ) of t,e firm=s pre-

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

6/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$2

anrupt/3 alue( using a sample of railroad anrupt/ies

during 19$$ and 1955. eiss 1990" uses a sample of$* anrupt firms in

t,e period 19#0-19#'( and estimates t,e dire/t /osts to e around $

of t,e pre-anrupt/3firm alue. +ltman and Fot/,iss 200'" proide a

ni/e summar3 of t,e estimates of t,e dire/t anrupt/3 /ostsin t,e

literature. 7,e findings in all t,ese studies suggest t,at dire/t

anrupt/3 /osts are unliel3 to represent asignifi/ant determinant of

t,e firm=s /apital stru/ture de/ision.

In more re/ent 3ears we ,ae witnessed seeral mega anrupt/3

filings 3 /ompanies( su/, asKe,man Brot,ers( Enron( and orldom. 7,e

total dire/t anrupt/3 /osts for Enron were estimated to top one

illion dollars. Een t,oug, t,is onl3 represents aout 1.'

of t,e firm=s pre-anrupt/3 alue( t,is staggeringnumer still implies

t,at a lot of resour/es were used up in t,e anrupt/3 pro/ess of t,e

former energ3 giant.it, t,e pre-anrupt/3 assets alue of Q'$9

illion( Ke,man Brot,ers= anrupt/3 is 3 far t,e largest/orporate

anrupt/3 in t,e 4S ,istor3. It is also liel3 to e t,e most e6pensie

/orporate failure. +s of

Noemer 2011( t,e legal /osts asso/iated wit, Ke,man

Brot,ers= anrupt/3 ,ae totaled aout Q1.5 illion.

%$&$% Indirect Costs

!otentiall3 more signifi/ant and sustantial are t,e indire/t

/osts of finan/ial distress and anrupt/3. 7,ese/osts /an e iewed as

opportunit3 /osts( in t,at t,e3 /olle/tiel3 represent t,e out/ome

of su-optimal a/tions

3 /orporate stae,olders w,en t,e firm e/omes finan/iall3

distressed +ltman and Fot/,iss( 200'". 7,us(/osts t,at arise e/ause

of inter- or intra-group /onfli/ts of interest( as3mmetri/

information( ,oldout prolems(lost sales and /ompetitie positions(

,ig,er operating /osts( and ineffe/tie use of management=s time

all

potentiall3 represent t,e indire/t /osts of

anrupt/3.Seeral studies /laim t,e indire/t /osts of finan/ial

distress to e signifi/ant and positie. or e6ample(

+ltman 19#)" measures t,e indire/t /osts of anrupt/3 as t,e

de/line in t,e sales of anrupt firms relatie toot,ers in t,e same

industr3 and as t,e differen/e etween t,e reali>ed earnings and

t,e fore/asted earnings. %nt,at asis( t,e aut,or argues t,at

indire/t anrupt/3 /osts on aerage range from 11 to 1* of firm alue

upto t,ree 3ears prior to anrupt/3. Foweer( t,is stud3 does not

/learl3 distinguis, /osts attriutale to finan/ialdistress from

t,ose attriutale to e/onomi/ distress.

%$( Financial Distress Corporate .urnaround Strate'ies

,itaer 1999" /ategori>es finan/ial distress into /ategories.

istress due to poor management firm spe/ifi/distress" and distress

as a result of e/onomi/ de/line /ommon fa/tors". 7,ere are arious

finan/ial distress/orporate turnaround strategies( t,ese

in/ludeA

%$($# Mana'erial /estructurin'

,anges in top management are argued to e one of t,e main

/onditions for su//essful turnarounds as t,e3 are atangile signal

to /reditors t,at a/tion is eing taen 3 t,e distressed firm Fofer(

19#0". In/ompetent managersma3 ,ae een t,e /ause of finan/ial

distress t,roug, poor planning or ineffi/ient de/ision maing.

,itaer1999" refers t,is as firm-spe/ifi/ distress. 7,ese managers

need to e repla/ed wit, management teams w,o /ana//uratel3 assess

t,e sour/e of distress and implement strategies ne/essar3 for

su//essful turnaround Ko,re(Be,eian( G !almer( 200)". !ear/e G

Coins 199$" also stress t,e importan/e of management in

turningdistressed firms around. 7,e3 argue t,at a management team

la/ing in t,e sills needed to respond effi/ientl3and in a timel3

manner will result in /ontinued de/line and t,e eentual failure of

t,e /ompan3.

Sudarsanam and Kai 2001" suggest t,at /reditors will onl3 proide

/ontinued finan/ial support if t,e3are reassured t,at management

will e ale to /ope wit, distress. enis G ruse 2000" find t,at $' of

t,esample firms t,e3 stud3 e6perien/e managerial turnoer in top

e6e/uties following performan/e de/lines.Managerial restru/turing

in/ludes repla/ement of senior management andor t,e ,ief E6e/utie

%ffi/er.%erall( managerial restru/turing ma3 e a /ru/ial fa/tor in

t,e turnaround pro/ess of a distressed firm.2.).2%perational

Cestru/turing

%perational restru/turing refers to t,e effi/ien/3operating

turnaround stage. 7,is stage aims to restore profitailit3 3

/ontrolling /osts and redu/ing oer,eads t,roug, t,e sale of surplus

fi6ed resour/es su/, as land(e?uipment( and offi/es. B3 de/reasing

input and ma6imi>ing output firms /an generate /as, flow at

least in t,es,ort term" and en,an/e effi/ien/3. ,en firms

re/ogni>e distress( operational restru/turing is usuall3 t,e

firststrateg3 implemented. Foweer( alt,oug, ne/essar3( operational

restru/turing is primaril3 a s,ort term fi6 usedto generate /as,

flow ?ui/l3. Sudarsanam G Kai 2001" argue t,at if used as a

stand-alone strateg3( it ma3 not

e enoug, for re/oer3 from distress. !ast literature

suggests t,at operational restru/turing in t,e form

of pur/,ases are less liel3 t,an sales. Neert,eless( if

produ/tiit3 /an e signifi/antl3 improed( distressed firmsma3 uild

new plants or inest in more adan/ed te/,nolog3 and e?uipment.

%$($& Asset /estructurin'

,en a distressed firm sells off lines of usinesses w,i/, are

unprofitale or not at t,e /ore operations of t,e/ompan3( it is

/onsidered to e engaging in asset restru/turing. 7,e aim of t,is

form of restru/turing is to realign

t,e fo/us of t,e firm 3 redu/ing unrelated diersifi/ation and

refo/using t,e usiness portfolio around /ore/ompeten/ies arner(

199*". ,ang 199'" finds t,at poorl3 performing firms will e

motiated to diest linesof usiness w,i/, do not generate /ompetitie

adantages. +sset restru/turing allows t,e firm to re-ealuate

its

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

7/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$$

operations and reorgani>e usiness units into more effi/ient

groups. 7,is form of restru/turing is espe/iall3ne/essar3 if agen/3

/osts ,ae resulted in oer diersifi/ation 3 management.

+lt,oug, /ontra/tion poli/ies ,ae een found to e t,e dominant

form of restru/turing Jo,n( Kang(G Netter 1992". +sset

restru/turing /ould also refer to a/tions w,i/, in/rease t,e

si>e of t,e firm su/, asinestments( strategi/ allian/es(

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

8/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$)

some e/onometri/ prolems wit, t,e single period logit model were

dis/ussed 3 Fillegeist 200)". irst( is t,esample sele/tion ias t,at

arises from using onl3 one( no randoml3 sele/ted oseration for ea/,

anrupt/ompan3( and se/ond( t,e model fails to in/lude time ar3ing

/,anges to refle/t t,e underl3ing ris of

anrupt/3. Being ased on a di/,otomous /lassifi/ation( t,e

traditional stati/ model is not suited to ,andle t,etemporal

/on/ept.

S,umwa3 2001" demonstrated t,at t,ese prolems /ould result in

iased( ineffi/ient( and in/onsistent/oeffi/ient estimates. 7o

oer/ome t,ese e/onometri/ prolems ,e proposed t,e ,a>ard model

for predi/ting

anrupt/3 and found t,at it was superior to t,e logit and

t,e M+ models. 7,is parti/ular model is a/tuall3 amulti-period

logit model e/ause t,e lieli,ood fun/tions of t,e two models are

identi/al. or t,is reason( t,edis/rete-time ,a>ard model wit,

time-ar3ing /oariates /an e estimated 3 using t,e e6isting

/omputer

pa/ages for t,e anal3sis of inar3 dependent ariales. 7,e

main parti/ularities of t,e ,a>ard model /onsist int,e fa/ts

t,at firm spe/ifi/ /oariates must e allowed to ar3 wit, time for

t,e estimator to e more effi/ient anda aseline ,a>ard fun/tion

is also re?uired( ut w,i/, /an e estimated dire/tl3 wit,

ma/roe/onomi/ ariales torefle/t t,e radi/al /,anges in t,e

enironment.

urt,er on( Nam et al 200#" e6tended t,e wor of S,umwa3 2001" and

deeloped a duration modelwit, time ar3ing /oariates and a aseline

,a>ard fun/tion in/orporating ma/roe/onomi/ ariales( su/,

ase6/,ange rate olatilit3 and interest rate. 4sing t,e proposed

model( t,e3 inestigated ,ow t,e ,a>ard rates oflisted /ompanies

in t,e orea Sto/ E6/,ange are affe/ted 3 /,anges in t,e

ma/roe/onomi/ enironment and

3 time ar3ing /oariate e/tors t,at s,ow uni?ue finan/ial

/,ara/teristi/s of ea/, /ompan3. B3 inestigatingt,e out-of-sample

fore/asting performan/es of t,eir model /ompared to t,e results of

ot, a traditionaldi/,otomous stati/ model and also a logit model

wit, time-ar3ing /oariates ut no aseline ,a>ard fun/tion(t,e3

demonstrated t,e improements produ/ed w,en allowing temporal and

ma/roe/onomi/ dependen/ies.

In anot,er stud3( +dulla, et al 200#" /ompared t,ree

met,odologies of identif3ing finan/iall3distressed /ompanies in

Mala3sia t,is are multiple dis/riminant anal3sis M+"( logisti/

regression and ,a>ardmodel. In a sample of 52 distressed and

non-distressed /ompanies wit, a ,oldout sample of 20 /ompanies(

t,e

predi/tions of ,a>ard model were a//urate in 9)(9 of

t,e /ases e6amined. 7,is was a ,ig,er a//ura/3 rate t,angenerated 3

t,e ot,er two met,odologies. Foweer( w,en t,e ,oldout sample was

in/luded in t,e sampleanal3>ed( M+ ,ad t,e ,ig,est a//ura/3 rate

of #5. +mong t,e ten determinants of /orporate performan/ee6amined(

t,e Catio of et to 7otal +ssets was a signifi/ant predi/tor of

/orporate distress regardless of t,emet,odolog3 used. In addition(

Net In/ome Hrowt, was anot,er signifi/ant predi/tor in M+( w,ereas

t,eCeturn on +ssets was an important predi/tor w,en t,e logisti/

regression and ,a>ard model met,odologies wereused.

In re/ent 3ears man3 t3pes of ,euristi/ algorit,ms su/, as

neural networs and de/ision trees ,ae also een applied to t,e

anrupt/3 predi/tion prolem and seeral improements in t,e finan/ial

distress predi/tionwere noti/ed. or e6ample t,e studies made 3 7am

and iang 1992" and Sal/,energer et al. 1992" proidedeiden/e to

suggest t,at neural networs outperform /onentional statisti/al

models su/, as dis/riminantanal3sis( logit models in finan/ial

appli/ations inoling /lassifi/ation and predi/tion. Soon after

t,at( ,3rid+rtifi/ial Neural Networ met,ods were proposed in some

finan/ial distress predi/tion studies. or e6ample(Rim and Mit/,ell

2005" tested t,e ailit3 of a new te/,ni?ue( ,3rid +NN=s to predi/t

/orporate distress inBra>il. 7,e models used in t,eir stud3 were

/ompared wit, t,e traditional statisti/al te/,ni?ues and

/onentional+NN models. 7,e results indi/ated t,at t,e most releant

finan/ial ratios for predi/ting Bra>ilian firm failure areCeturn

on apital Emplo3ed( Ceturn on 7otal +ssets( Net +ssets 7urnoer(

Solen/3 and Hearing.

&arious aspe/ts of /orporate finan/ial distress ,ae een

reiewed in t,e en3an /onte6t. ogi 200$"did a stud3 to deelop a

dis/riminant model in/orporating finan/ial ratio stailit3 t,at

/ould e used to predi/t/orporate failure. Fe soug,t to identif3

/riti/al finan/ial ratios wit, signifi/ant predi/tie ailit3. Fis

findings,owed t,at it was possile to predi/t /orporate failure wit,

up to *0 a//ura/3 t,ree 3ears efore a/tualo//urren/e using stailit3

dis/riminant model. iege 1991" ,ad earlier formulated a model to

predi/t usinessfailure among en3an /ompanies w,i/, a/,ieed a

predi/tion a//ura/3 of 90 two 3ears efore a/tual failure.

Ng=ang=a 200'" soug,t to e6plore and e6pose possile

indi/ators of impending failures among man3firms in deeloping

/ountries and deeloped a predi/tion model for insuran/e /ompanies

in en3a. Fe deried afailure predi/tion model using /as,-flow

information and multiple dis/riminant anal3sis te/,ni?ues. 7,e

model3ielded an oerall /orre/t /lassifi/ation a//ordan/e of #5 a

3ear prior to failure /onfirming t,at /as,-flows /an

e used to gie /lear and pre/ise information aout an

entit3=s finan/ial ,ealt,.7aliani 2010" /arried out a stud3 on

predi/ting finan/ial distress in /ommer/ial ans in en3a. Fis

stud3 reealed t,at none of a/tiit3 and turn-oer ratios was found

to e /riti/al in predi/ting finan/ial distress in/ommer/ial ans in

en3a. 7,e model attained *0 and 100 /orre/t /lassifi/ation in 3ear

1 and 3ear $

respe/tiel3. 7,e findings are /onsistent wit, t,e studies 3

iragu 1991"( iege 1991" and Nganga 200'".Bwisa 200*" in ,is stud3

noted t,at +ltman finan/ial distress predi/tion model was appli/ale

lo/all3. Fe foundout t,at model is appli/ale in t,e sense t,at '

out of 10 failed firms t,at were anal3>ed indi/ated *0 alidit3

of

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

9/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$5

t,e model.

&$,$ /esearch Methodolo'y

7,is stud3 applied multiariate dis/riminant anal3sis model in

predi/ting finan/ial distress in an organi>ation.7,e resear/,

design adopted in t,is resear/, was a des/riptie stud3. +//ording

to ooper and S/,indler 2001"(

a des/riptie stud3 or a formal stud3 is a stud3 t,at is

t3pi/all3 stru/tured wit, /learl3 stated inestigatieoed in a manner

to fa/ilitate anal3sis. ataanal3sis inoled preparation of t,e

/olle/ted data( /oding( editing and /leaning of data in readiness

for

pro/essing using S!SS pa/age ersion 20. S!SS was preferred

e/ause it is s3stemati/ and /oers a wide rangeof t,e most /ommon

statisti/al and grap,i/al data anal3sis.

or t,e purpose of t,is stud3( Multiariate is/riminant +nal3sis

M+" statisti/al te/,ni?ue as used 3 +ltman 200'" was adopted.

+ltman 200'" is of t,e opinion t,at ratios measuring profitailit3(

li?uidit3 andsolen/3 are t,e most signifi/ant ratios. +ltman

/omined a numer of ratios and deeloped on insolen/3

predi/tion model.$.2.1 +nal3ti/al ModelCeised @-s/ore

model( +ltman 200'" was used. @-s/ore is a linear /omination of

four /ommon usinessfinan/ial ratios( weig,ted 3 /oeffi/ients.

+nal3sis of t,e four measures were oones34 ; %$9 DSafe

>one

#$#< 34 < %$ 9 DHre3 >one Z” < 1.1

“Distress” zone

4.0. Findings4.1 The Z- Model calculated from 2001 to 2005

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

10/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$'

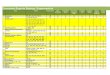

Table 4.1 The Calculated values of Z in 2001Independent +ariales

=alues Discriminant Independent +ariales> Discriminat 3

+alue

oring /apital7otal assets 0.$'$9)) '.5' 2.$#*)*$9#)

$.90'259Cetained earningstotal asset 0.0)*'55 $.2'

0.155$55595

Earnings efore interest ta6estotal assets 0.0*90$* '.*2

0.5$112*2##

Boo alues of e?uit3total asset 0.*92''9 1.05 0.#$2$0209*Source

Cesear/, findings7,e findings in tale ).1 indi/ates t,at t,e

/al/ulated @-s/ore model alue in t,e 3ears 2001 was $.90'259.

Table 4.2 Calculated values of Z in the year 2002Independent

ariales &alues is/riminant Independent ariales8 is/riminat @

alue

oring /apital7otal assets 0.$5#$# '.5' 2.$509*$)1#

$.#*)5'9Cetained earningstotal asset 0.0)#50# $.2'

0.15#1$*2)#

Earnings efore interest ta6estotal assets 0.0#05'5 '.*2

0.5)1$9)##5

Boo alues of e?uit3total asset 0.*#)#2$ 1.05 0.#2)0'$'99

Source Cesear/, findings7,e findings in tale ).2 indi/ates t,at

t,e /al/ulated @-s/ore model alue in t,e 3ears 2002 was

$.#*)5'9

Table 4. Calculated Z value in 200Independent +ariale =alues

Discriminant Independent +ariales> Discriminat 3 +alue

oring /apital7otal assets 0.$'#*1) '.5' 2.)1#*'5$15

$.#$1'**Cetained earningstotal assest 0.0)9125 $.2'

0.1'01)'91

Earnings efore interest ta6estotal assets 0.0'#09 '.*2

0.)5*5'5*1'

Boo alues of e?uit3total asset 0.*5*$$2 1.05 0.*9519##''

Source Cesear/, findings7,e findings in tale ).$ indi/ates t,at

t,e /al/ulated @-s/ore model alue in t,e 3ears 200$ was

$.#$1'**.

Table 4.4 Calculated value in 2004Independent +ariale =alues

Discriminant Independent +ariales> Discriminat 3 +alue

oring /apital7otal assets 0.$$*'01 '.5' 2.21)''0*)'

$.5#*9##Cetained earningstotal assest 0.0)9$)9 $.2'

0.1'0#*#95'

Earnings efore interest ta6estotal assets 0.0*15## '.*2

0.)#10*$'1'

Boo alues of e?uit3total asset 0.'9'5)* 1.05 0.*$1$*)22*

Source Cesear/, findings7,e findings in tale ).) indi/ates t,at

t,e /al/ulated @-s/ore model alue in t,e 3ears 200) was

$.5#*9##.

Table 4.! Calculated value of Z in 200!Independent +ariale

=alues Discriminant Independent +ariales> Discriminat 3

+alue

oring /apital7otal assets 0.0$#9#9 '.5' 0.255*''1#9

1.950*)#Cetained earningstotal assest 0 $.2' 0

Earnings efore interest ta6estotal assets 0.2001'5 '.*2

1.$)510*15$

Boo alues of e?uit3total asset 0.$$$21) 1.05 0.$)9#*)2'*

Source Cesear/, findings7,e findings in tale ).5 indi/ates t,at

t,e /al/ulated @-s/ore model alue in t,e 3ears 2005 was

1.950*)#

4.2. Inferential tatistical anal!sisTable 4." Descri#tive

statistics of the variables

Mean Std. eiation N

@ alues $.)$02)#2 .#$'50$#9 5oring /apital7otal asset .29$525'

.1)2*#)'' 5Cetained earnings7otal asset .0$#92*5 .021**105

5Earnings efore interest ta6es7otal asset .099###9 .05'29291 5Boo

alues of e?uit37otal liailities .'*291'# .19$'1)$$ 5

Source Cesear/, findings

7,e findings in tale ).' indi/ate t,e des/riptie statisti/s of

t,e ariales in w,i/, t,e mean of t,e @-s/ore alueis $.)$0 wit,

standard deiation of 0.#$'5. 7,e mean of woring /apital 7otal

assets is 0.29$5 wit, standarddeiation of 0.1)2#. 7,e findings also

indi/ate t,at t,e means of Cetained earnings7otal assets( Earnings

efore

interest ta6estotal asset and oo aluestotal liailities are

0.0$#9( 0.0999( and 0.'*29 wit, standard deiations0.021*( 0.05'$

and 0.19$' respe/tiel3.

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

11/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$*

Table 4.$ The correlation

@alues

oring/apital7otalasset

Cetainedearnings7otalasset

Earnings eforeinterestta6es7otal asset

Boo alues ofe?uit37otalliailities

!earsonorrelation

@ alues 1.000 .99' .9#5 -.9** .999

oring/apital7otal asset

.99' 1.000 .995 -.992 .991

Cetainedearnings7otal asset

.9#5 .995 1.000 -.99* .9*'

Earnings eforeinterest ta6es7otalasset

-.9** -.992 -.99* 1.000 -.9'5

Boo alues ofe?uit37otalliailities

.999 .991 .9*' -.9'5 1.000

Sig. 1-tailed"

@ alues . .000 .001 .002 .000oring/apital7otal asset

.000 . .000 .000 .001

Cetainedearnings7otal asset .001 .000 . .000 .002

Earnings efore

interest ta6es7otalasset

.002 .000 .000 . .00)

Boo alues ofe?uit37otalliailities

.000 .001 .002 .00) .

N 5 5 5 5 5

Source Cesear/, findings

7,e findings in tale ).* indi/ates t,at t,ere is a strong

positie /orrelation etween @ alues and oring/apital7otal asset

r0.99'". 7,e findings indi/ate t,at t,e /orrelation is signifi/ant

at 5 signifi/an/e leelgien t,at p-alue 0.000" is less t,an alp,a

0.05" t,e findings in tale ).* indi/ate t,at t,ere is a strong

negatie

/orrelation etween @ alues and Earnings efore interest

ta6es7otal asset r-0.9**". 7,e findings indi/ate t,att,e

/orrelation is signifi/ant at 0.05 leel of signifi/an/e sin/e t,e

p-alue 0.002" is less t,an alp,a 0.05".

Table 4.% &e'ression coefficient

Model 4nstandardi>ed oeffi/ients

Standardi>edoeffi/ients

t Sig.

B Std. Error Beta

1

onstant" 1.*$5 .210 #.2'9 .00*

Cetained earnings7otal asset -'.$2$ $.)') -.1'5 -1.#25 .$19

Earnings efore interestta6es7otal asset

-).9)# 1.12' -.$$$ -).$9* .1)2

Boo alues of e?uit37otalliailities

$.'19 .10' .#$# $).21' .019

a. ependent &ariale @ alues

Source Cesear/, findings

7,e findings in tale ).# indi/ate t,e regression model generated

3 t,e independent and t,e dependent ariale.7,e model generated is

gien as @1.*$5 ; '.$2$ Cetained earnings7otal assets ; ).9)#

Earnings efore interestta6es7otal asset O $.'19 Boo alues of e?uit3

7otal liailities. 7,e findings indi/ate t,at t,e /oeffi/ient ofBoo

alues of e?uit3 7otal liailities is positie and signifi/ant at 0.05

leel of signifi/an/e gien t,at t,e p-alue 0.019" is less t,an alp,a

0.05". 7,e findings indi/ate t,at t,e /onstant 1.*$5" is

signifi/ant at 0.05 leelof signifi/an/e gien t,at p-alue 0.00*" is

less t,an alp,a 0.05" indi/ating t,at @ depends on t,e

independentariales.

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

12/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$#

Table 4.( The variables e)cluded

Model Beta In t Sig. !artialorrelation

ollinearit3 Statisti/s

7oleran/e

1 oring /apital7otal asset 1.120 . . 1.000 1.*1*E-005

a. ependent &ariale @ alues . !redi/tors in t,e Model

onstant"( Boo alues of e?uit37otal liailities( Earnings efore

interest ta6es7otal asset(Cetained earnings7otal asset

Source Cesear/, findings

7,e findings in tale ).9 indi/ates t,at woring /apital was

e6/luded in t,e regression model sin/e it isinsignifi/ant as

indi/ated 3 t,e null p-alue and null t alue.

Table 4.10 *i'nificance of the re'ression +odelA?*=A

Model Sum of S?uares df Mean S?uare Sig.

1

Cegression 2.*99 $ .9$$ 15)#5.)50 .00'

Cesidual .000 1 .000

7otal 2.*99 )a. ependent &ariale @ alues . !redi/tors

onstant"( Boo alues of e?uit37otal liailities( Earnings efore

interest ta6es7otal asset( Cetainedearnings7otal asset

Source Cesear/, findings

7,e findings in tale ).10 indi/ates t,at t,e regression model

generated 3 t,e ariales @ as t,e dependentariale( and Boo alues of

e?uit37otal liailities( Earnings efore interest ta6es7otal asset(

Cetainedearnings7otal asset as t,e independent ariales" is

signifi/ant at 0.05 leel of signifi/an/e gien t,at t,e p-alue

0.00'" is less t,an alp,a 0.05" as indi/ated 3 t,e +N%&+

tale.

Table 4.11 *u++ary statistics

Model C C S?uare +d

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

13/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

$9

7,e C s?uared 1.000" indi/ates t,at 100 of t,e ariation in @ is

a//ounted for 3 t,e independentariales Boo alues of e?uit37otal

liailities( Earnings efore interest ta6es7otal asset(

Cetainedearnings7otal asset". 7,e ade andinest in distressed det.

Fooen( NJ ile3.

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

14/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

)0

+le6ander( +. 2001". Japan onfronts orporate Cestru/turing.

Japan E/onomi/ Institute. orld Ban Instituteeelopment Studies(

as,ington( ( 4S+

+>i>( M. G ar( F. 200'". !redi/ting orporate inan/ial

istress ,it,er o e StandT orporategoernan/e( '1"( 1#-$$.

+ndrade( H G aplan( S 199#". Fow ostl3 is inan/ial Not E/onomi/"

istressT UEiden/e from Fig,l3

Keeraged 7ransa/tions t,at Be/ame istressed 7,e Journal of

inan/e( 5$5"( 1))$-1)9$.+s?uit,( !( Hertner( C G S,arfstein( .

199)". +natom3 of inan/ial istress= +n E6planation of Jun Bond

Issuers 7,e Puarterl3 Journal of E/onomi/s( 109( '25-'**.Beaer(

. 19''". inan/ial Catios as !redi/tors of ailureA Empiri/al

Cesear/, in +//ounting( Sele/ted

Studies( Journal of +//ounting Cesear/,( 5" *1-111.Bwisa( +.+

2010". Ealuation of appli/ailit3 of +ltmans reised model in

predi/tion of finan/ial distress.

4npulis,ed MB+ proerland.

!ande3( I.M. 2005". inan/ial Management 10t, Ed". New elp,i(

India( &ias !ulis,ingS,umwa3( 7. 2001". ore/asting anrupt/3

more a//uratel3 + simple ,a>ard model Journal of Business(

*)

1"( 101-12).Slotemaer( C. 200#". !redi/tion of orporate

Banrupt/3 of !riate irms in t,e Net,erlands + Master=s

7,esis( Erasmus 4niersit3( Cotterdam( Net,erlands"Sudarsanam( S

G Kai( J 2001". orporate inan/ial istress and 7urnaround Strategies

+n Empiri/al +nal3sis

Britis, Journal of Management( 12( 1#$-199.7aliani( I. J. 2010".

!redi/ting finan/ial distress in /ommer/ial ans in en3a. 4npulis,ed

MB+ pro

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

15/16

European Journal of Business and Management

www.iiste.org

ISSN 2222-1905 !aper" ISSN 2222-2#$9 %nline"

&ol.'( No.2$( 201)

)1

7am( .R. and M.R. iang 1992"( VManagerial appli/ations of neural

networs 7,e /ase of an failure predi/tions( Management S/ien/e

$#92' ; 9)*.

7,eodossiou( !( a,3a( E( Saidi( C G !,ilippatos( H 199'".

inan/ial distress and /orporate a/?uisitionsfurt,er empiri/al

eiden/e( Journal of Business inan/e and +//ounting( 2$2".

'99;*19.

7urets3( F G M/Ewen( C 2001". +n Empiri/al inestigation of irm

Kongeit3. + Model of t,e E6 +nte

!redi/tors of inan/ial istress. In Ceiew of Puantitatie inan/e

and +//ounting( 1'( $2$-$)$.arner( Jerold B.( 19**". Banrupt/3

/osts Some eiden/e. Journal of inan/e $2( $$*;$)*.,itaer( C 1999".

7,e Earl3 Stages of inan/ial istress Journal of E/onomi/s and

inan/e. 2$2"( 12$-1$$.ru/( 1990". inan/ial istress(

Ceorgani>ation( and %rgani>ational Effi/ien/3 Journal of

inan/ial

E/onomi/s( 2*( )19-))).Rim J. and F. Mit/,ell 2005". +

/omparison of /orporate distress predi/tion models in Bra>il

,3rid neural

networs( logit models and dis/riminant anal3sis( Noa E/onomia

Belo Fori>onte 15( *$-9$@mi

-

8/20/2019 ___An in-Depth Analysis of the Altman's Filure

Prediction Model on Corporate Financial Distress Un Uchumi

Superm…

16/16

The IISTE is a pioneer in the Open-Access hosting service and

academic event

management. The aim of the firm is Accelerating Global Knowledge

Sharing.

More information about the firm can be found on the

homepage:

http://www.iiste.org

CALL FOR JOURNAL PAPERS

There are more than 30 peer-reviewed academic journals hosted

under the hosting

platform.

Prospective authors of journals can find the submission

instruction on the

following page: http://www.iiste.org/journals/ All

the journals articles are available

online to the readers all over the world without financial,

legal, or technical barriers

other than those inseparable from gaining access to the internet

itself. Paper version

of the journals is also available upon request of readers and

authors.

MORE RESOURCES

Book publication

information: http://www.iiste.org/book/

IISTE Knowledge Sharing Partners

EBSCO, Index Copernicus, Ulrich's Periodicals Directory,

JournalTOCS, PKP Open

Archives Harvester, Bielefeld Academic Search Engine,

Elektronische

Zeitschriftenbibliothek EZB, Open J-Gate, OCLC WorldCat,

Universe Digtial

Library , NewJour, Google Scholar

http://www.iiste.org/http://www.iiste.org/http://www.iiste.org/journals/http://www.iiste.org/journals/http://www.iiste.org/journals/http://www.iiste.org/book/http://www.iiste.org/book/http://www.iiste.org/book/http://www.iiste.org/book/http://www.iiste.org/journals/http://www.iiste.org/