Embed Size (px)

Citation preview

1

R/Rmetrics

Diethelm Würtz

ITP ETH Zürich

Meielisalp Workshop, July 8th - 12th

(c) 2007www.rmetrics.org | www.finance.ch

An Educational Environment for Teaching Financial Engineering and Computational Finance

2

--- Part I ---Financial Engineering and Computational FinanceRapid Model PrototypingS, R and Rmetrics …Rmetrics Software Environment

--- Part II ---Rmetrics Selected Topics

Explorative Data AnalysisVolatility ForecastingHedging with FuturesExtremal EventsCopulaeOption ValuationTerm Structure ModelingPortfolio OptimizationTime and Date

3

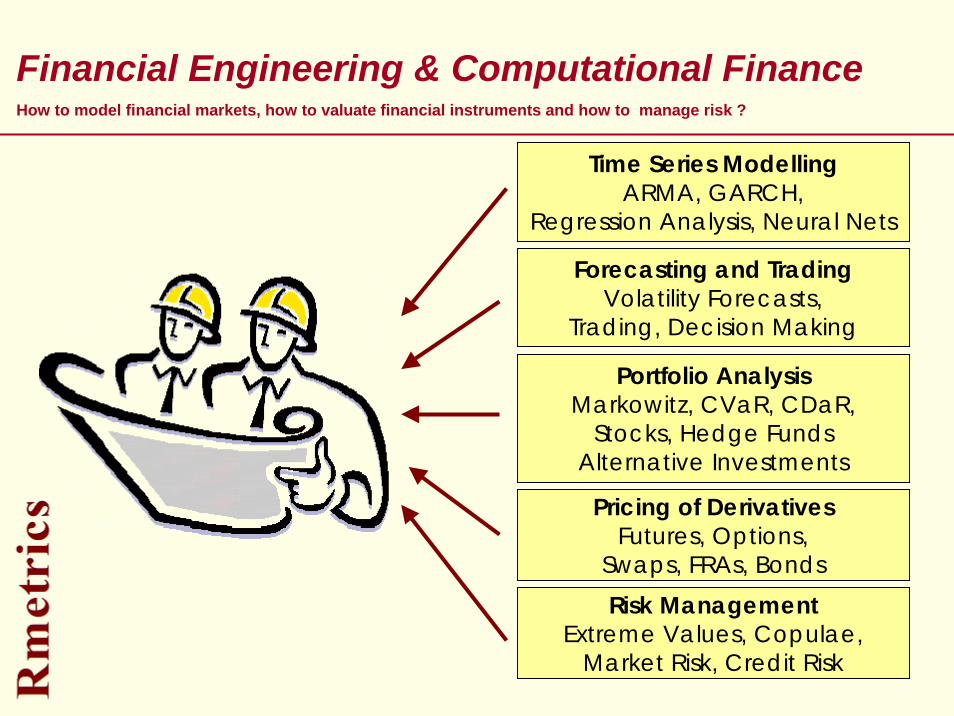

Financial Engineering & Computational Finance

FinancialEngineering

Portfolio AnalysisMarkowitz, CVaR, CDaR,

Stocks, Hedge FundsAlternative Investments

Forecasting and TradingVolatility Forecasts,

Trading, Decision Making

Pricing of DerivativesFutures, Options,

Swaps, FRAs, Bonds

Time Series ModellingARMA, GARCH,

Regression Analysis, Neural Nets

Risk ManagementExtreme Values, Copulae,

Market Risk, Credit Risk

How to model financial markets, how to valuate financial instruments and how to manage risk ?

4

Teaching and “Rapid Model Prototyping”

Initial versions of an implementation of “Models” into software are called “Model Prototypes” …

are the starting point in most financial analysis processes. Teaching and learning mean not only to explain and to understand the theoretical concepts and algorithms behind these models, but also

to demonstrate algorithmic concepts,

to try out model design concepts,

to find out more about the problem and possible solutions, and

to compare models and algorithms.

Models

Furthermore, “Rapid” Model Prototyping can be considered as a tool to see the feasibility and usefulness of the implemented model in an efficient way.

5

Pillars of a RMP Environment for Teaching

RMP Systems are build on three main pillars …

Pillar I:

An RMP must allow an interactive usageAn RMP must support powerful data types and structuresAn RMP must provide powerful mathematical and statistical functions

Pillar II:

An RMP must provide powerful plot toolsAn RMP must provide device drivers and controls

Pillar III:

An RMP must be programmable through a powerful languageThe language must offer to write user defined functionsThe language must offer OO Programming

6

RMP and “Requirement Risk”

RMP generates model prototypes which can be used to give in a very short time a concrete impression of the model’s capabilities.

RMP favors techniques which pay much attention to speed of delivery rather than performance and maintainability of an implemented model.

RMP is the best-way approach to try-out several requirements before agreeing in a final model and its implementation.

RMP supports efficiently requirements validation: Prototypes can reveal errors and omissions in the specifications.

RMP can be even used for the implementation of models where thespecification cannot be definitely developed in advance.

RMP can be considered as a risk reduction activity which reduces “Requirement Risks” …

7

Scripting Environments as Ideal RMP Systems

R, S-Plus and Matlab are well known scripting languages for scientific modeling, diagnostic analysis and testing.

A transparent interface to compiled libraries (C++, C, Java, Fortran) offers additional flexibility to scripting based RMP environments.

Additional requirements of RMP Systems include:Interactive Usage and Batch Job SubmissionAdvanced Graphical Tools, Graphics Devices, Bitmaps, Postscript, PDFAdvanced Reporting Tools, HTML Interface and XML/XLS Parser/GeneratorMS Excel Interface, DCOM InterfaceData Base Management Interfaces, Data Feed Interfaces Web Server Interface

Scripting Languages are the Basis for Software Prototyping …

8

S and R are an Ideal RMP System !

R providesan environment for interactive computing with dataan OO language based on functions and function callsboth traditional and trellis graphics, and a OpenGL rendering backendseveral graphical device drivers and controlsinterfaces for C++, C, Java and Fortran

R allows users to transition easily into programmers.

Design Goals ..

S and R are a Language and Computing Environment …

The S language was developed by John Chambers at Bell LaboratoriesS builds today the de facto standard in statistics researchR is the Open Source project implementation of SR runs on MS Windows, Linux/Unix, and also on the Mac

What is S and R it ?

9

What is R ?

Building aRapid Model Prototyping System

“R is a free software environment for statistical computing and graphics. It compiles and runs on a wide variety of UNIX platforms, Windows and MacOS.” [CRAN Server]

R fulfills the requirements for

for teaching “Computational Finance and Financial Engineering”

10

What is R/Rmetrics ?

Rmetrics is the premier open source solution for financial market analysis and the

valuation of financial instruments.

Rmetrics combines explorative data analysis and statistical modeling with

object oriented rapid prototyping.

Rmetrics creates especially for students and researchers in the third world a first class system for applications in finance.

Rmetrics can be considered as a unique platform ideally suited for RMP in financial engineering and

computational finance.

Rmetrics allows to study all the source code, so she or he can find out precisely

which variation of the algorithm or method has been implemented.

Rmetrics comes with hundreds of function build on modern and

powerful methods.Example: Exponential Brownian MotionPricing Path Dependent Options

Rmetrics is a “Rapid Model Prototyping” System for Teaching in Finance

11

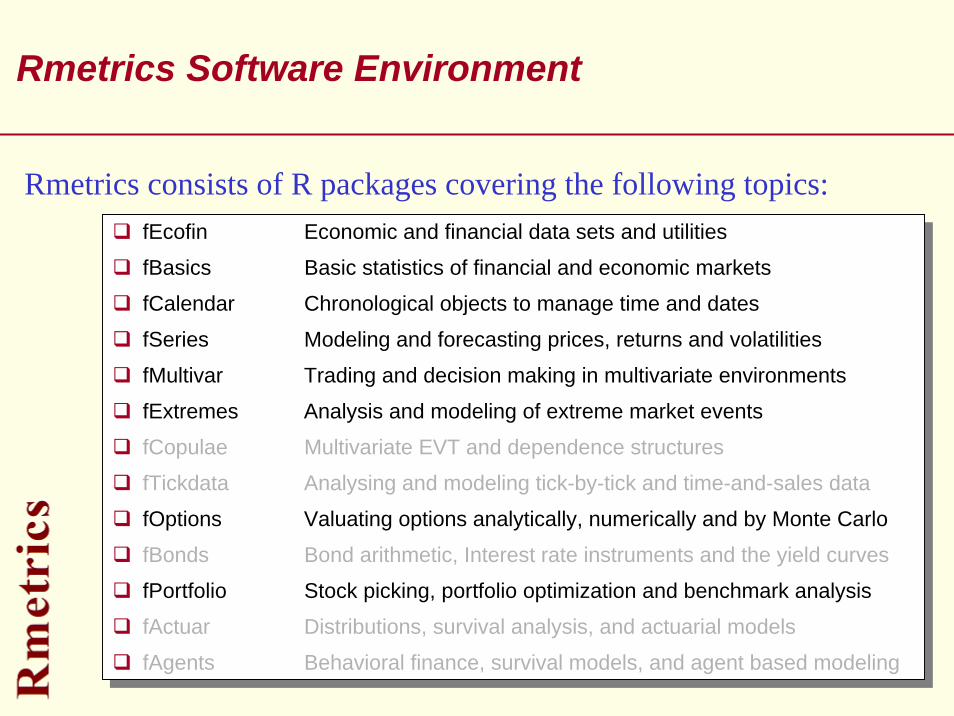

fEcofin Economic and financial data sets and utilities

fBasics Basic statistics of financial and economic markets

fCalendar Chronological objects to manage time and dates

fSeries Modeling and forecasting prices, returns and volatilities

fMultivar Trading and decision making in multivariate environments

fExtremes Analysis and modeling of extreme market events

fCopulae Multivariate EVT and dependence structures

fTickdata Analysing and modeling tick-by-tick and time-and-sales data

fOptions Valuating options analytically, numerically and by Monte Carlo

fBonds Bond arithmetic, Interest rate instruments and the yield curves

fPortfolio Stock picking, portfolio optimization and benchmark analysis

fActuar Distributions, survival analysis, and actuarial models

fAgents Behavioral finance, survival models, and agent based modeling

fEcofin Economic and financial data sets and utilities

fBasics Basic statistics of financial and economic markets

fCalendar Chronological objects to manage time and dates

fSeries Modeling and forecasting prices, returns and volatilities

fMultivar Trading and decision making in multivariate environments

fExtremes Analysis and modeling of extreme market events

fCopulae Multivariate EVT and dependence structures

fTickdata Analysing and modeling tick-by-tick and time-and-sales data

fOptions Valuating options analytically, numerically and by Monte Carlo

fBonds Bond arithmetic, Interest rate instruments and the yield curves

fPortfolio Stock picking, portfolio optimization and benchmark analysis

fActuar Distributions, survival analysis, and actuarial models

fAgents Behavioral finance, survival models, and agent based modeling

Rmetrics Software Environment

Rmetrics consists of R packages covering the following topics:

12

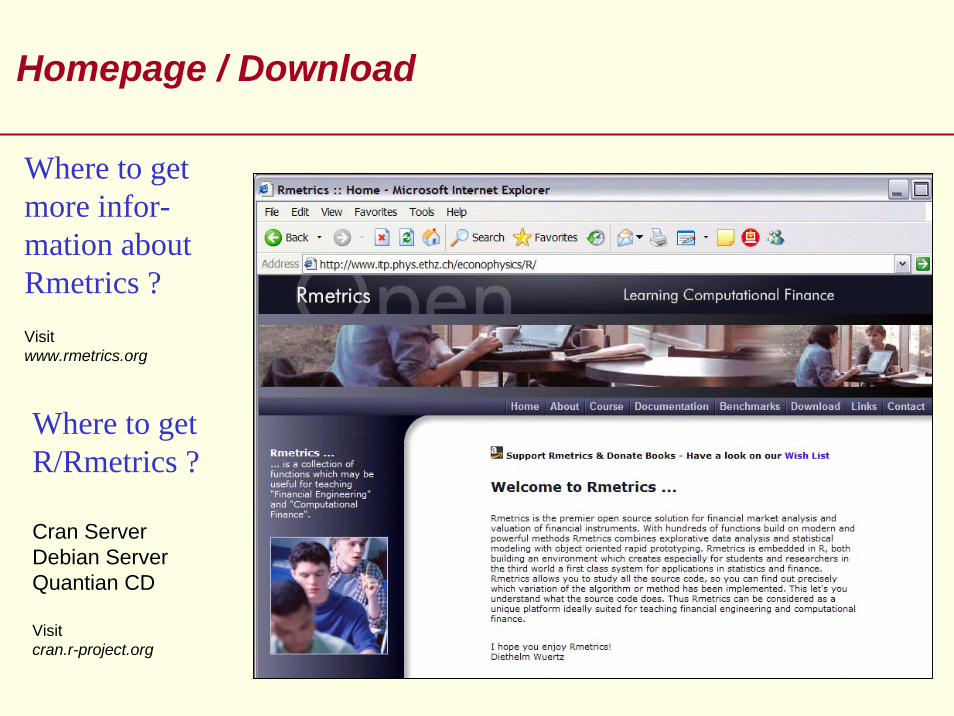

Homepage / Download

Where to get more infor-mation about Rmetrics ?Visit www.rmetrics.org

Where to get R/Rmetrics ?

Cran ServerDebian ServerQuantian CD

Visitcran.r-project.org

13

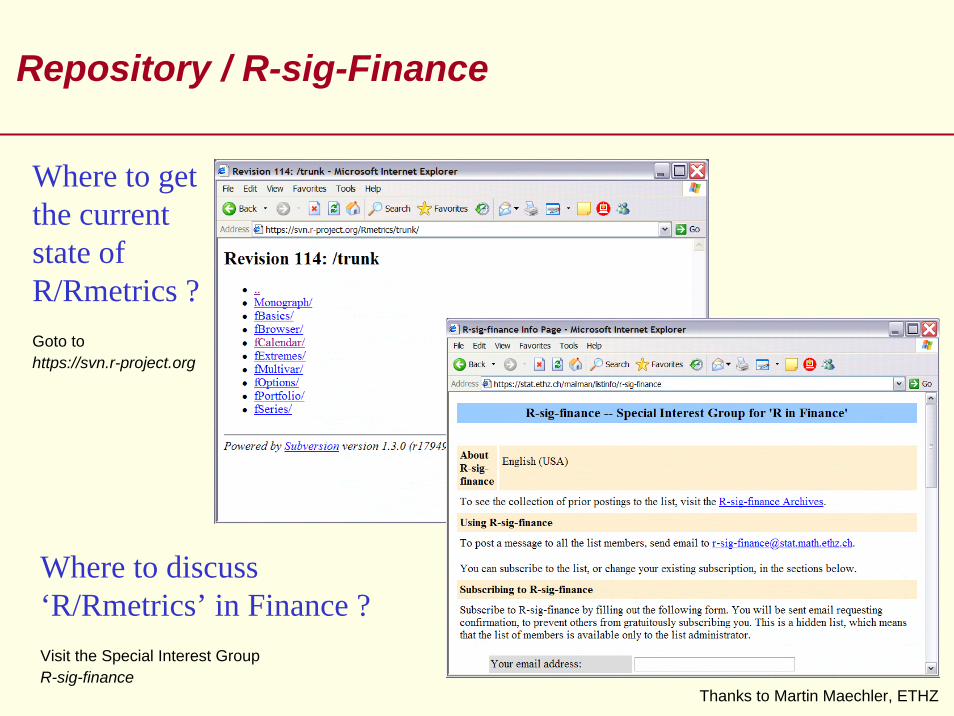

Repository / R-sig-Finance

Where to discuss ‘R/Rmetrics’ in Finance ?Visit the Special Interest GroupR-sig-finance

Where to get the current state of R/Rmetrics ?Goto to https://svn.r-project.org

Thanks to Martin Maechler, ETHZ

14

--- Part II ---

Selected Topics

• Explorative Data Analysis• Volatility Forecasting• Hedging with Futures• Extremal Events• Copulae• Option Valuation• Term Structure Modeling• Portfolio Optimization• Time and Date

The Diamonds in R/Rmetrics

15

Explorative

Data AnalysisAll Around – Wassily Kandinski

16

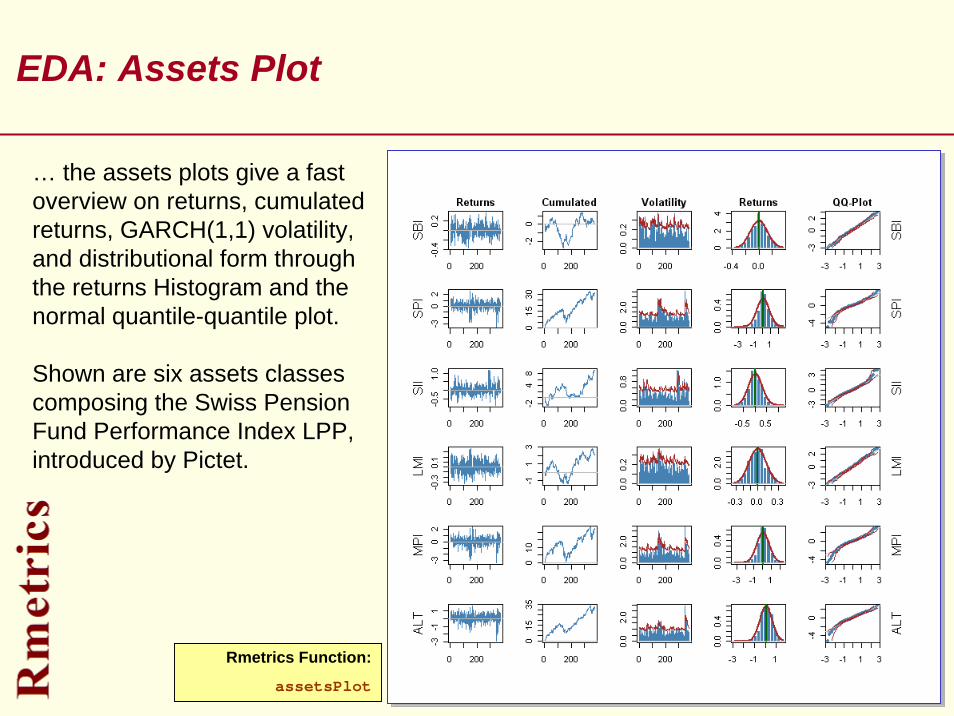

EDA: Assets Plot

… the assets plots give a fast overview on returns, cumulatedreturns, GARCH(1,1) volatility,and distributional form throughthe returns Histogram and thenormal quantile-quantile plot.

Shown are six assets classescomposing the Swiss PensionFund Performance Index LPP,introduced by Pictet.

Rmetrics Function:

assetsPlot

17

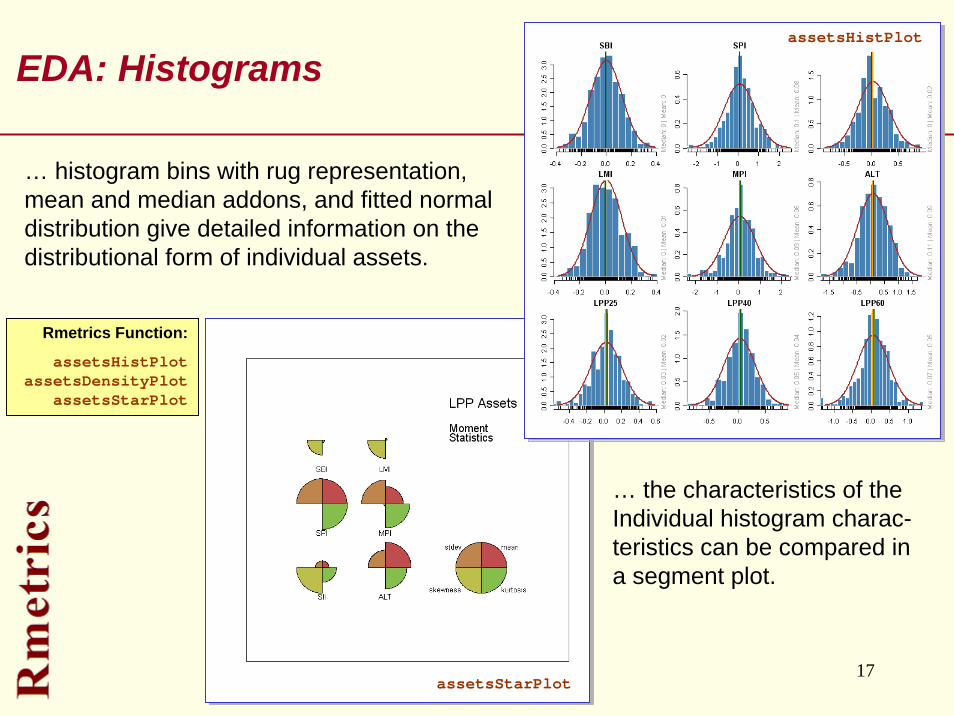

EDA: Histograms

Rmetrics Function:

assetsHistPlotassetsDensityPlot

assetsStarPlot

… histogram bins with rug representation, mean and median addons, and fitted normal distribution give detailed information on the distributional form of individual assets.

… the characteristics of theIndividual histogram charac-teristics can be compared ina segment plot.

assetsStarPlot

assetsHistPlot

18

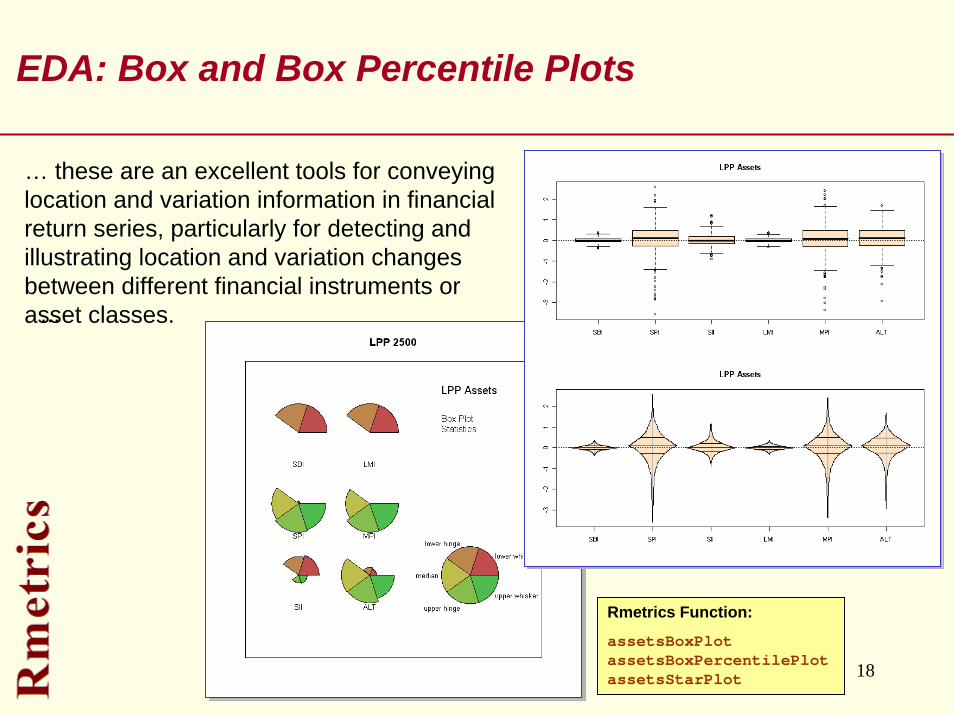

EDA: Box and Box Percentile Plots

… these are an excellent tools for conveying location and variation information in financial return series, particularly for detecting and illustrating location and variation changes between different financial instruments or asset classes. ...

Rmetrics Function:

assetsBoxPlotassetsBoxPercentilePlotassetsStarPlot

19

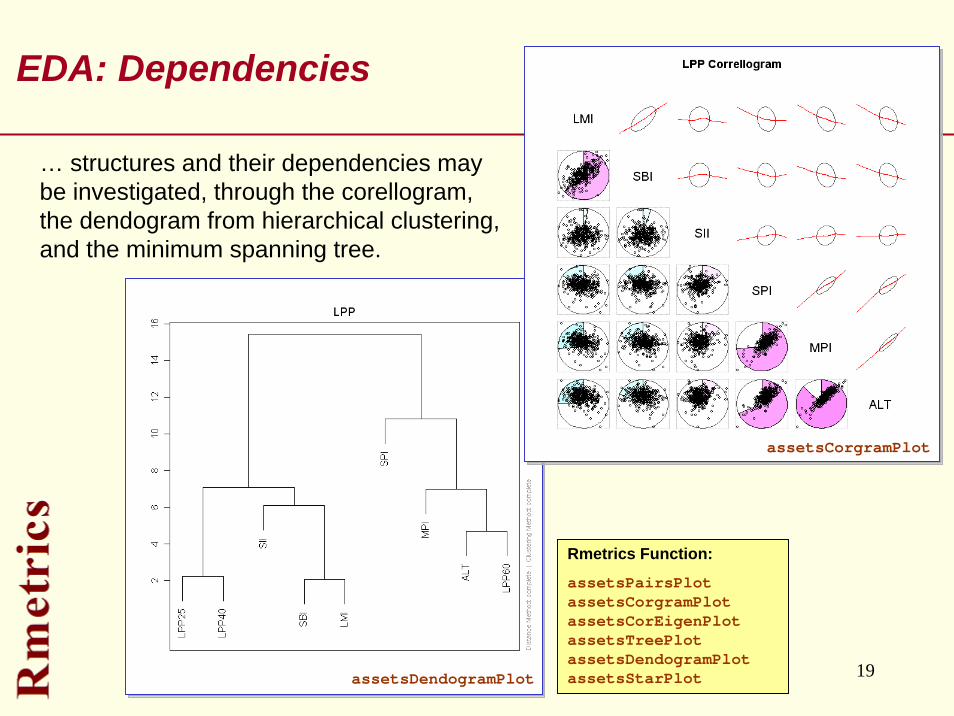

EDA: Dependencies

… structures and their dependencies maybe investigated, through the corellogram,the dendogram from hierarchical clustering,and the minimum spanning tree.

Rmetrics Function:

assetsPairsPlotassetsCorgramPlotassetsCorEigenPlotassetsTreePlotassetsDendogramPlotassetsStarPlot

assetsCorgramPlot

assetsDendogramPlot

20

Rmetrics Functions

Bivariate Binning:squareBinning

hexagonalBinning

fEcofin fBasics fPortfolio

Time Series Plots:seriesPlot

histPlotdensityPlotqqnormPlotqqnigPlot

Extremal Index:exindexPlot

exindexesPlot

fExtremes

Assets Plots:assetsPlot

assetsSeriesPlotassetsHistPlot

assetsDensityPlotassetsQQNormPlot

Tables:characterTable

symbolTablecolorTable

Time Series Plots:emdPlot

qqparetoPlotmePlot

recordsPlotmsratioPlot

sllnPlotlilPlot

xacfPlotAssets Box Plots:assetsBoxPlot

assetsBoxPerc*Plot

Assets PairsPlots:assetsPairsPlot

assetsCorgramPlotassetsCorTestPlot

Assets Multiv. Plots:assetsCorEigenPlot

assetsTreePlotassetsDendogramPlot

assetsStarsPlot

Stylized Facts:

taylorPlotlmacfPlot

logpdfPlotscalinglawPlot

Explorative Data Analysis

21

Volatility Forecasting

Beruhigt – Wassily Kandinski

22

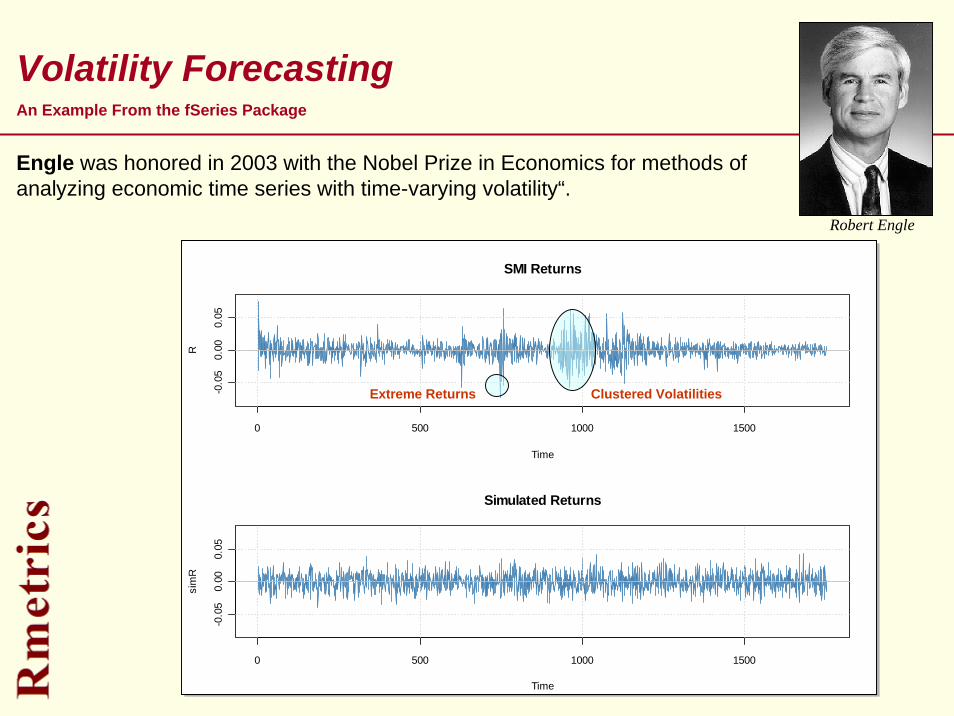

Volatility Forecasting

SMI Returns

Time

R

0 500 1000 1500

-0.0

50.

000.

05

Simulated Returns

Time

sim

R

0 500 1000 1500

-0.0

50.

000.

05

Extreme Returns Clustered Volatilities

Robert Engle

Engle was honored in 2003 with the Nobel Prize in Economics for methods of analyzing economic time series with time-varying volatility“.

An Example From the fSeries Package

23

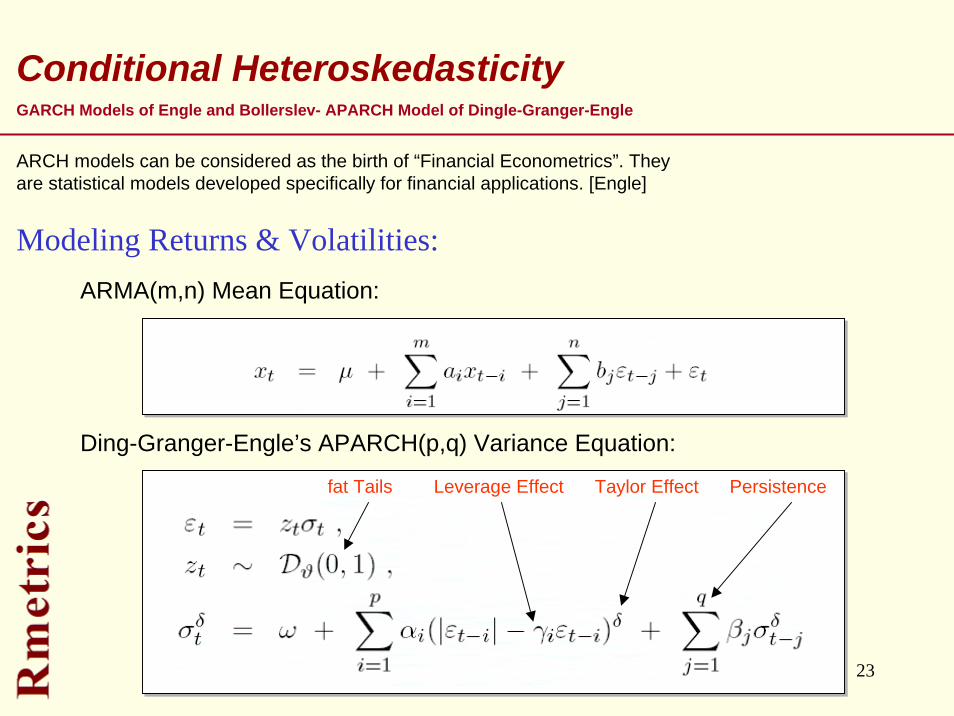

Conditional HeteroskedasticityGARCH Models of Engle and Bollerslev- APARCH Model of Dingle-Granger-Engle

ARCH models can be considered as the birth of “Financial Econometrics”. They are statistical models developed specifically for financial applications. [Engle]

Ding-Granger-Engle’s APARCH(p,q) Variance Equation:

fat Tails Leverage Effect Taylor Effect Persistence

ARMA(m,n) Mean Equation:

Modeling Returns & Volatilities:

24

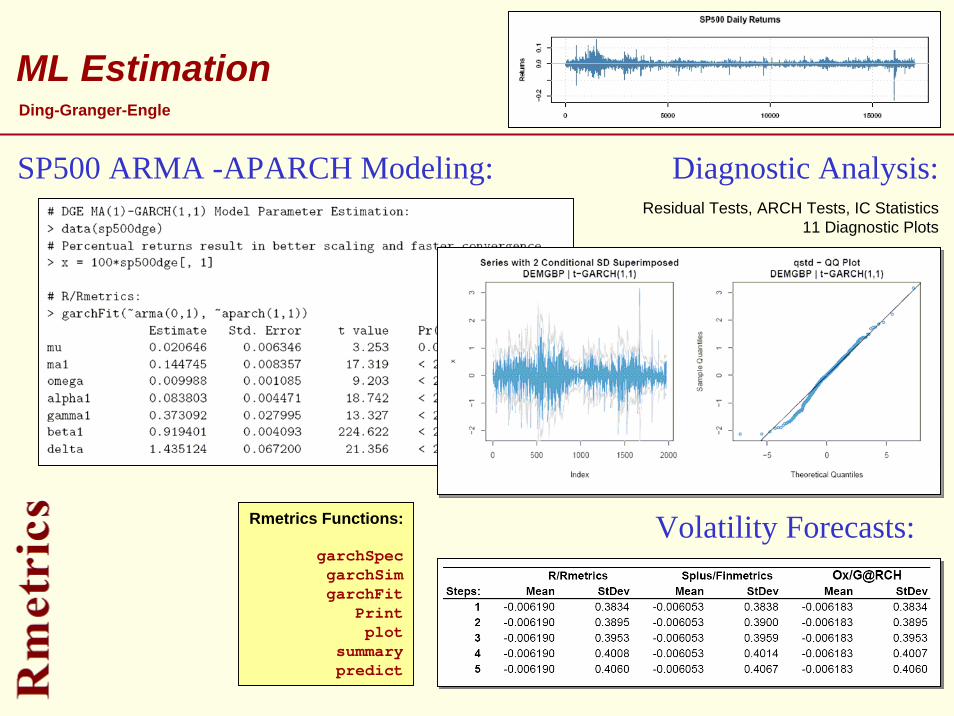

ML Estimation Ding-Granger-Engle

SP500 ARMA -APARCH Modeling:

Rmetrics Functions:

garchSpecgarchSimgarchFit

Printplot

summarypredict

Diagnostic Analysis:

Volatility Forecasts:

Residual Tests, ARCH Tests, IC Statistics11 Diagnostic Plots

25

Hedging With Futures

Mit und Gegen – Wassily Kandinski

26

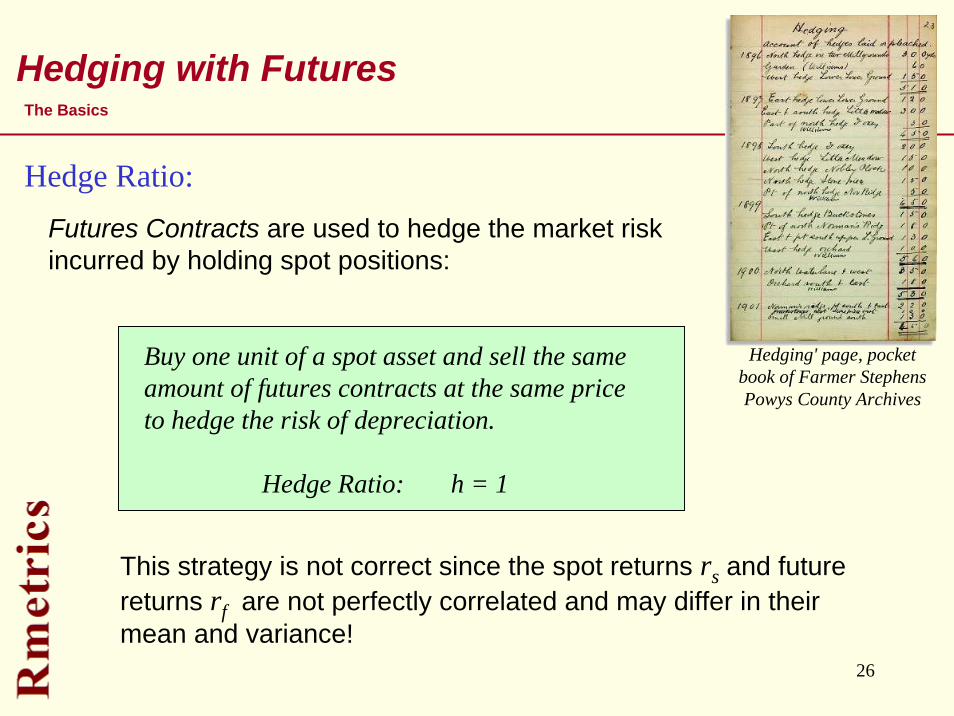

Hedging with FuturesThe Basics

Hedging' page, pocket book of Farmer Stephens Powys County Archives

Hedge Ratio:

This strategy is not correct since the spot returns rs and future returns rf are not perfectly correlated and may differ in their mean and variance!

Futures Contracts are used to hedge the market risk incurred by holding spot positions:

Buy one unit of a spot asset and sell the same amount of futures contracts at the same price to hedge the risk of depreciation.

Hedge Ratio: h = 1

27

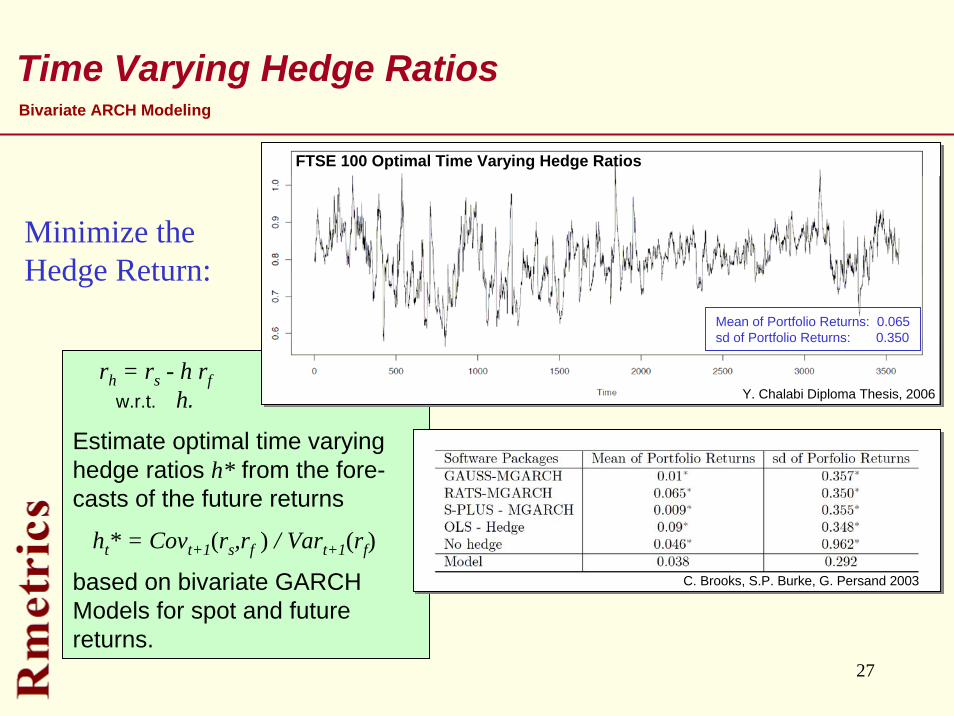

rh = rs - h rfw.r.t. h.

Estimate optimal time varying hedge ratios h* from the fore-casts of the future returns

ht* = Covt+1(rs,rf ) / Vart+1(rf)

based on bivariate GARCH Models for spot and future returns.

Time Varying Hedge RatiosBivariate ARCH Modeling

Minimize the Hedge Return:

FTSE 100 Optimal Time Varying Hedge Ratios

Y. Chalabi Diploma Thesis, 2006

C. Brooks, S.P. Burke, G. Persand 2003

Mean of Portfolio Returns: 0.065sd of Portfolio Returns: 0.350

28

Rmetrics Functions

Interfaces:

garchOxFitgarchSPlusFit

Parameter Estimation:

*Fit

GARCH Modeling Distributions

GARCH Modeling:

"fGARCH" ClassgarchSimgarchFit

printsummarypredict

Distributions:

[dpqr]norm[dpqr]snorm

[dpqr]std[dpqr]sstd[dpqr]ged

[dpqr]sged[dpqr]ghyp[dpqr]nig

29

ExtremalEvents

Intensita – Claudia Raimondi

30

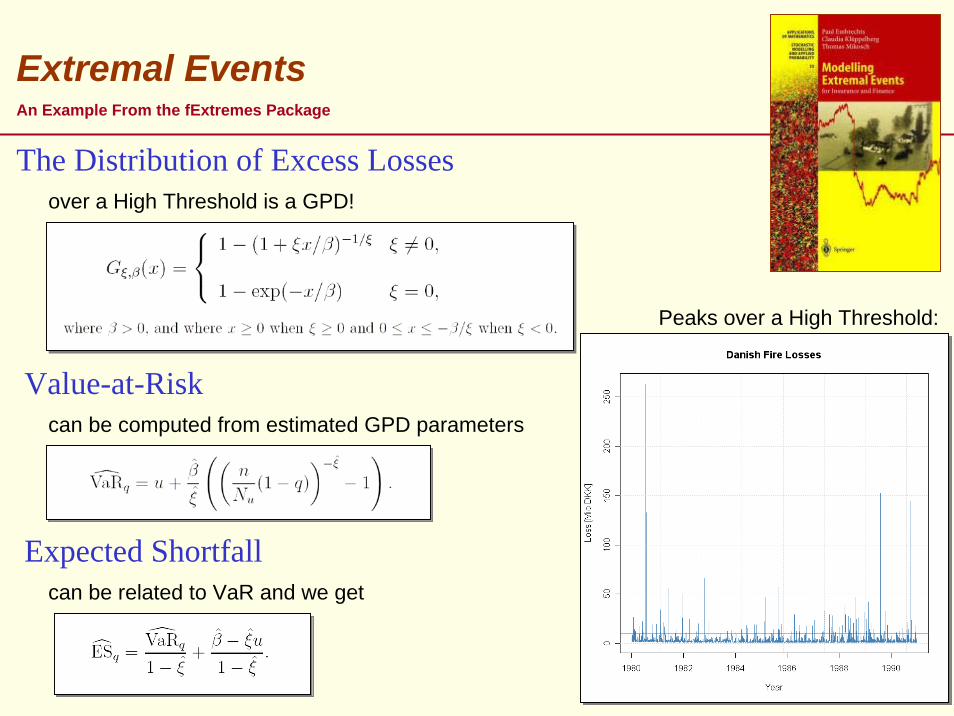

Extremal Events

The Distribution of Excess Losses

An Example From the fExtremes Package

can be computed from estimated GPD parameters

can be related to VaR and we get

Value-at-Risk

Expected Shortfall

over a High Threshold is a GPD!

Peaks over a High Threshold:

31

Insurance Risk

# GPD Parameter Estimation

> require(fExtremes)> data(danish)> fit = gpdFit(danish, threshold = 10) > fit

Call:gpdFit(x = danish, threshold = 10)

Estimation Type: gpd ml

Estimated Parameters:xi beta

0.4968062 6.9745523

# GPD Risk Measures

> gpdRiskMeasures(fit)

p quantile sfall1 0.9900 27.28488 58.210912 0.9950 40.16160 83.800913 0.9990 94.28956 191.369724 0.9995 134.71099 271.699485 0.9999 304.62448 609.36958

McNeil, Estimating the tails of loss severitydistributions using extreme value theory (1966)

Resnick, Discussion of the Danish data onlarge fire insurance losses (2000)

Danish Fire Losses:

32

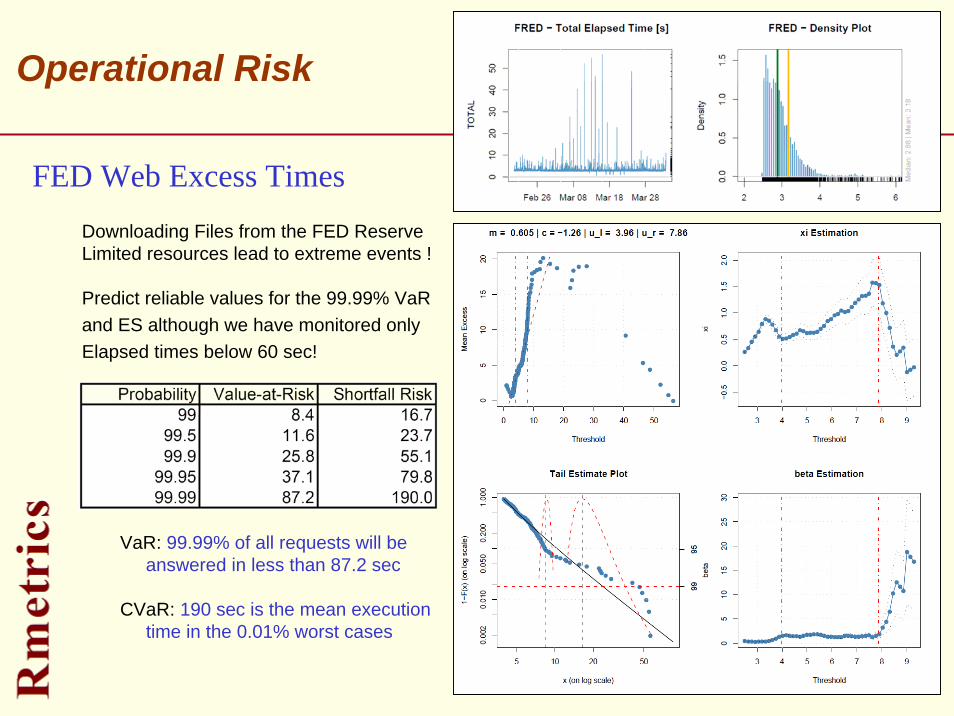

Operational Risk

VaR: 99.99% of all requests will be answered in less than 87.2 sec

CVaR: 190 sec is the mean execution time in the 0.01% worst cases

Downloading Files from the FED ReserveLimited resources lead to extreme events !

Predict reliable values for the 99.99% VaR and ES although we have monitored only Elapsed times below 60 sec!

FED Web Excess Times

33

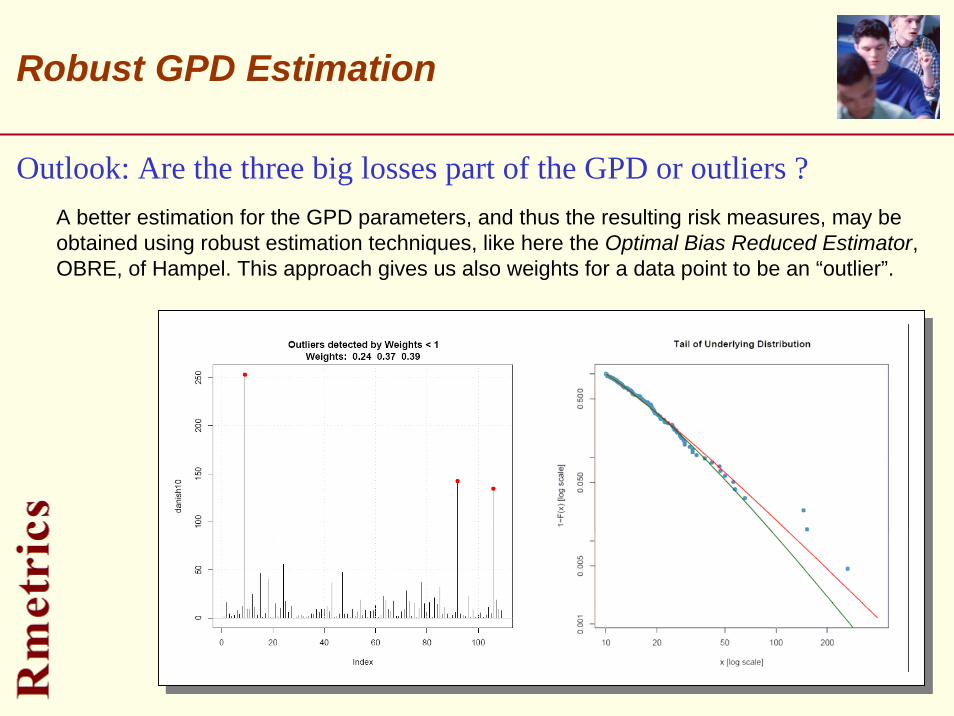

Robust GPD Estimation

Outlook: Are the three big losses part of the GPD or outliers ?A better estimation for the GPD parameters, and thus the resulting risk measures, may be obtained using robust estimation techniques, like here the Optimal Bias Reduced Estimator, OBRE, of Hampel. This approach gives us also weights for a data point to be an “outlier”.

34

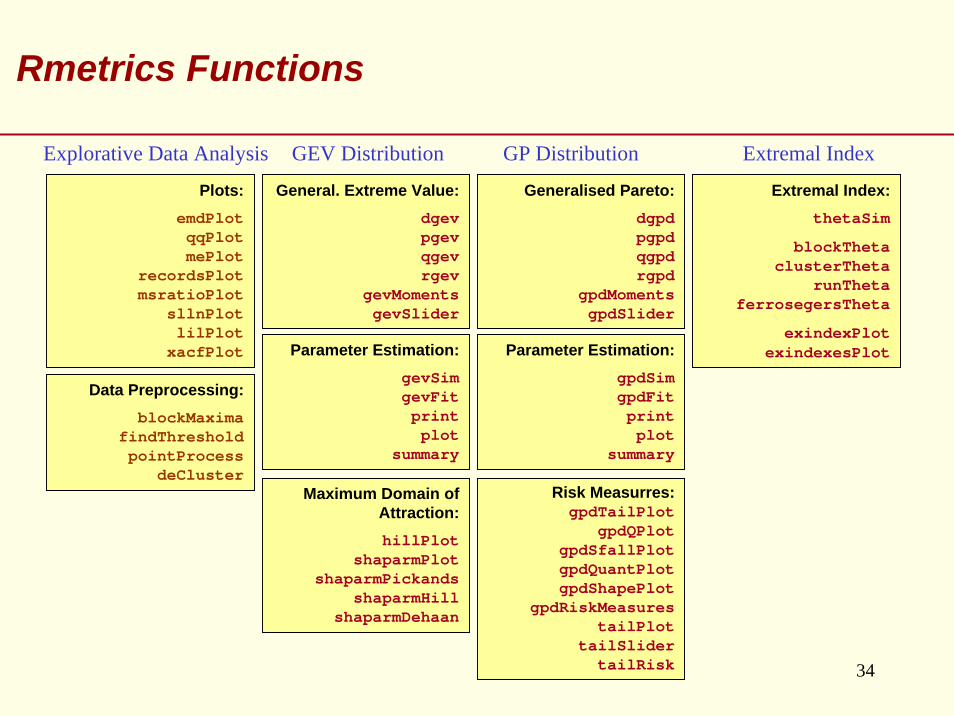

Rmetrics Functions

Data Preprocessing:blockMaxima

findThresholdpointProcess

deCluster

Explorative Data Analysis GEV Distribution Extremal Index

Plots:emdPlotqqPlotmePlot

recordsPlotmsratioPlot

sllnPlotlilPlot

xacfPlot

General. Extreme Value:dgevpgevqgevrgev

gevMomentsgevSlider

Generalised Pareto:dgpdpgpdqgpdrgpd

gpdMomentsgpdSlider

Extremal Index:thetaSim

blockThetaclusterTheta

runThetaferrosegersTheta

exindexPlotexindexesPlot

GP Distribution

Parameter Estimation:gevSimgevFitprintplot

summary

Maximum Domain of Attraction:hillPlot

shaparmPlotshaparmPickands

shaparmHillshaparmDehaan

Parameter Estimation:gpdSimgpdFitprintplot

summary

Risk Measurres:gpdTailPlot

gpdQPlotgpdSfallPlotgpdQuantPlotgpdShapePlot

gpdRiskMeasurestailPlot

tailSlidertailRisk

35

Copulae

Solar Heights – Nadja Neiler Ugo

36

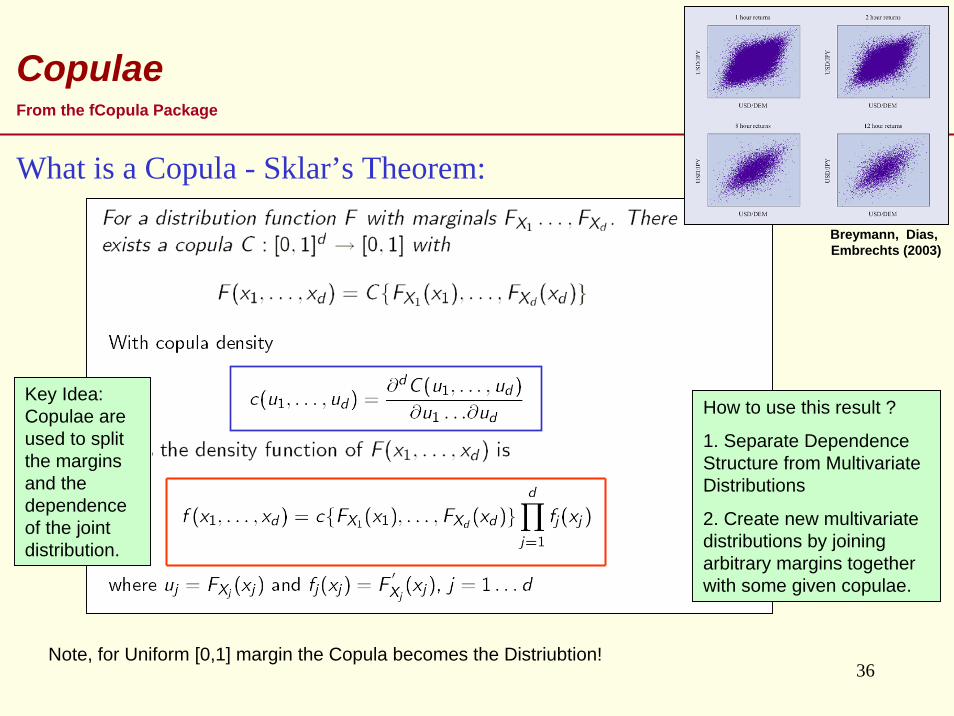

Copulae

Key Idea: Copulae are used to split the margins and thedependence of the joint distribution.

How to use this result ?

1. Separate DependenceStructure from MultivariateDistributions

2. Create new multivariate distributions by joining arbitrary margins together with some given copulae.

What is a Copula - Sklar’s Theorem:

Note, for Uniform [0,1] margin the Copula becomes the Distriubtion!

From the fCopula Package

Breymann, Dias, Embrechts (2003)

37

Applications

Finance:– Stress testing – Credit Risk Management– Risk Management Basle II– Pricing/Hedging basket

derivatives

Insurance:– Life (multi-life products)– Non-Life, multi-line covers– Risk Management,

Solvency 2– Dynamic Financial Analysis,

ALM

Density

Random Variates

Fitting

38

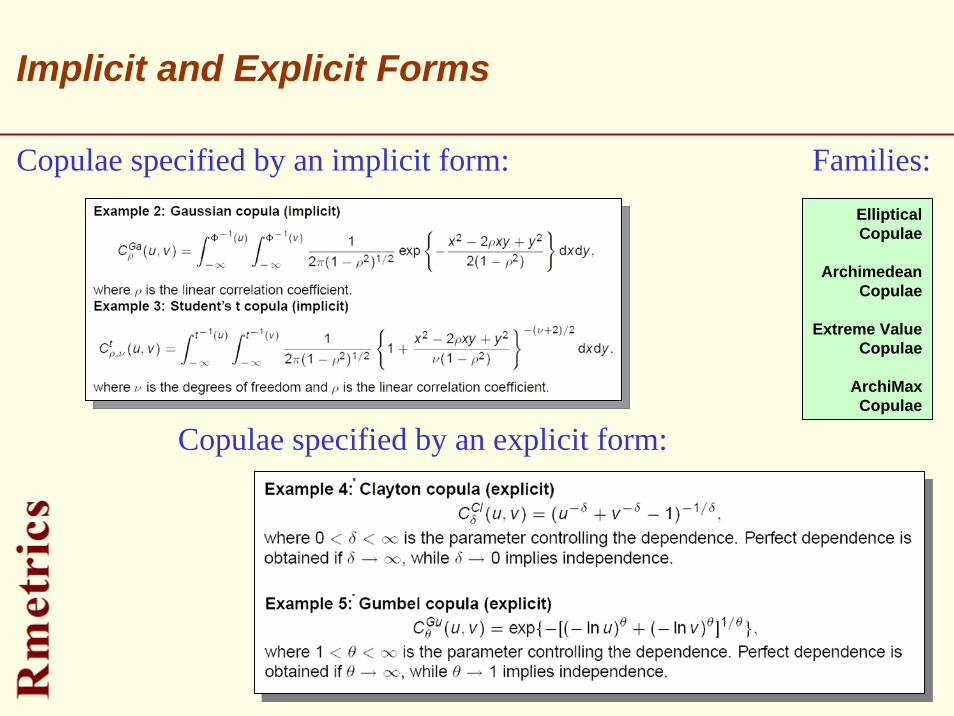

Implicit and Explicit Forms

Copulae specified by an implicit form:

Copulae specified by an explicit form:

EllipticalCopulae

ArchimedeanCopulae

Extreme ValueCopulae

ArchiMaxCopulae

Families:

39

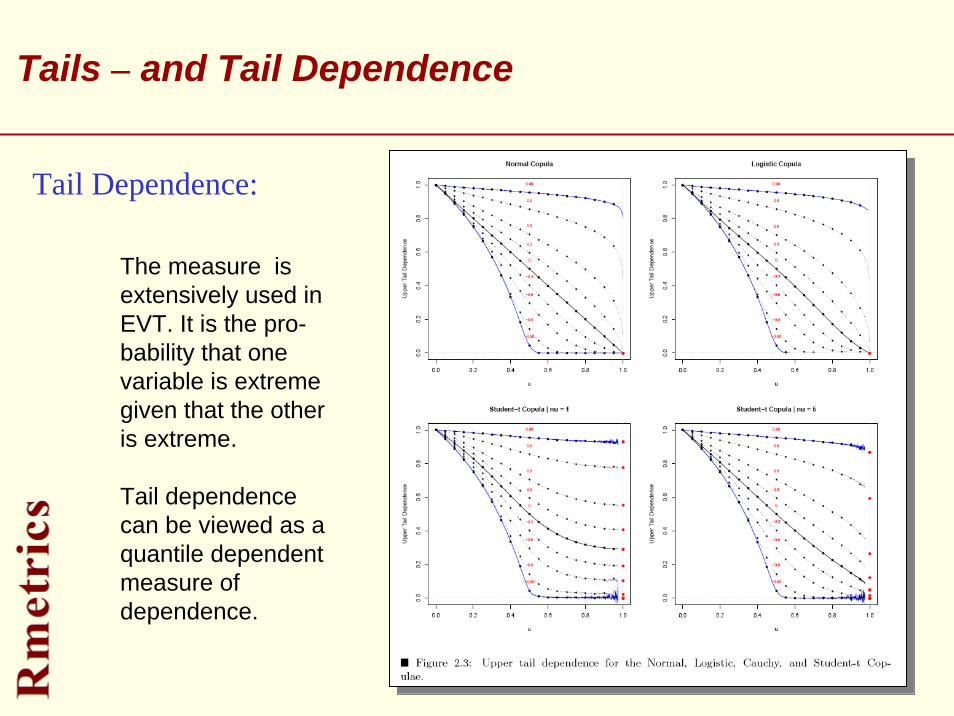

Tails – and Tail Dependence

Tail Dependence:

The measure is extensively used in EVT. It is the pro-bability that one variable is extreme given that the other is extreme.

Tail dependence can be viewed as a quantile dependent measure of dependence.

40

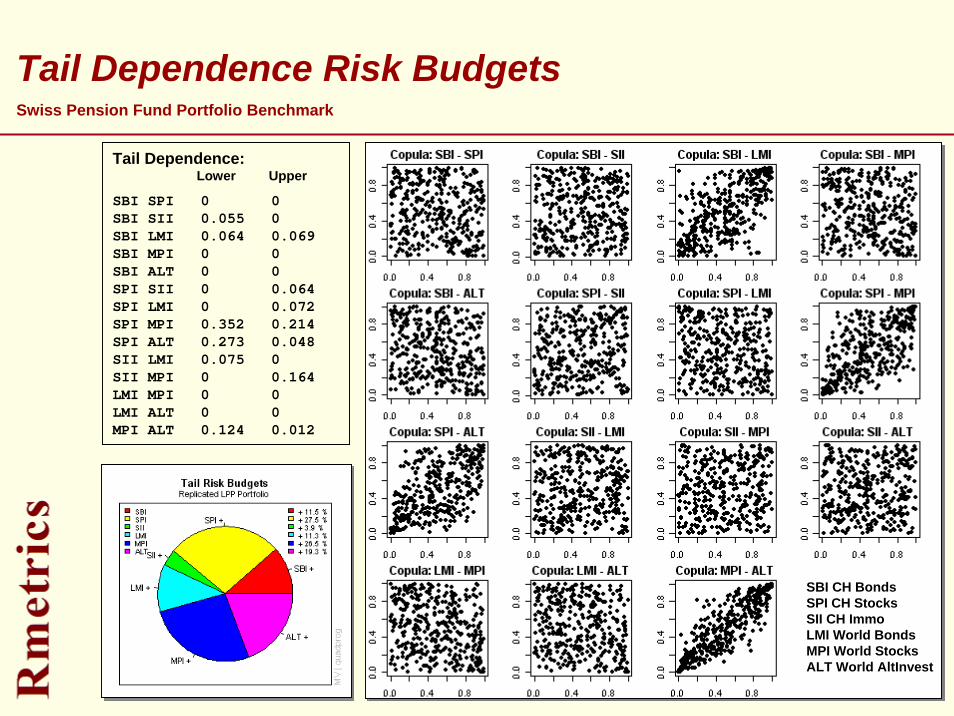

Tail Dependence Risk Budgets

Tail Dependence:Lower Upper

SBI SPI 0 0 SBI SII 0.055 0 SBI LMI 0.064 0.069 SBI MPI 0 0 SBI ALT 0 0 SPI SII 0 0.064 SPI LMI 0 0.072 SPI MPI 0.352 0.214 SPI ALT 0.273 0.048 SII LMI 0.075 0 SII MPI 0 0.164 LMI MPI 0 0 LMI ALT 0 0 MPI ALT 0.124 0.012

SBI CH BondsSPI CH StocksSII CH ImmoLMI World BondsMPI World StocksALT World AltInvest

Swiss Pension Fund Portfolio Benchmark

41

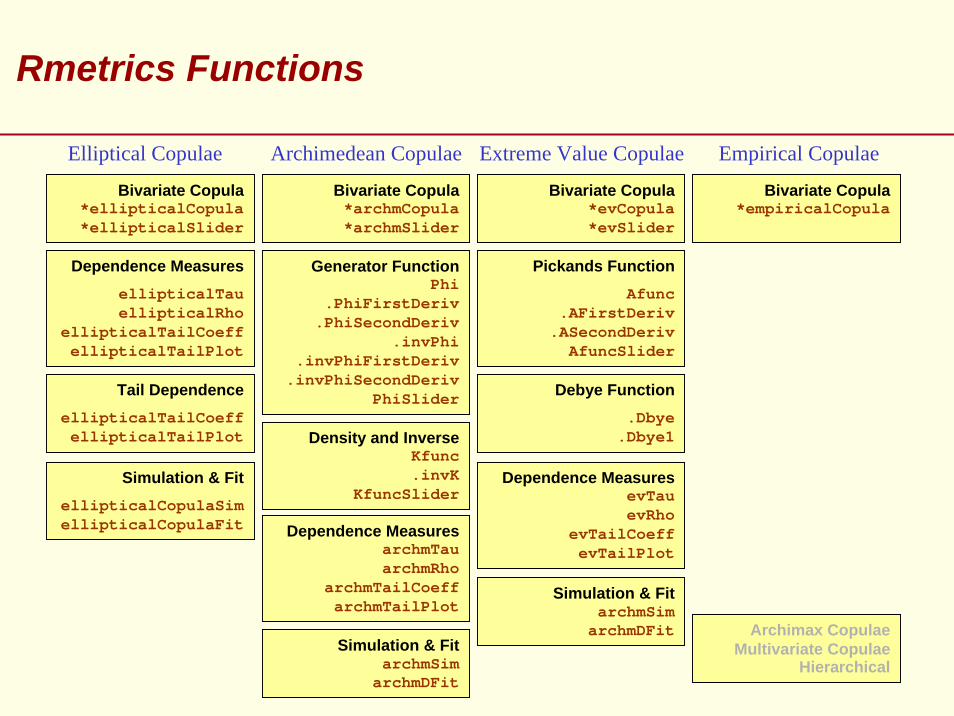

Rmetrics Functions

Dependence MeasuresellipticalTau ellipticalRho

ellipticalTailCoeffellipticalTailPlot

Simulation & FitellipticalCopulaSimellipticalCopulaFit

Tail DependenceellipticalTailCoeffellipticalTailPlot

Generator FunctionPhi

.PhiFirstDeriv.PhiSecondDeriv

.invPhi.invPhiFirstDeriv

.invPhiSecondDerivPhiSlider

Density and InverseKfunc.invK

KfuncSlider

Dependence MeasuresarchmTauarchmRho

archmTailCoeffarchmTailPlot

Elliptical Copulae Archimedean Copulae Extreme Value Copulae Empirical Copulae

Pickands FunctionAfunc

.AFirstDeriv.ASecondDeriv

AfuncSlider

Debye Function.Dbye

.Dbye1

Bivariate Copula*ellipticalCopula*ellipticalSlider

Bivariate Copula*archmCopula*archmSlider

Bivariate Copula*evCopula*evSlider

Simulation & FitarchmSim

archmDFit

Bivariate Copula*empiricalCopula

Archimax CopulaeMultivariate Copulae

Hierarchical

Simulation & FitarchmSim

archmDFit

Dependence MeasuresevTauevRho

evTailCoeffevTailPlot

42

Options

The Tree of Life – Gustav Klimt

43

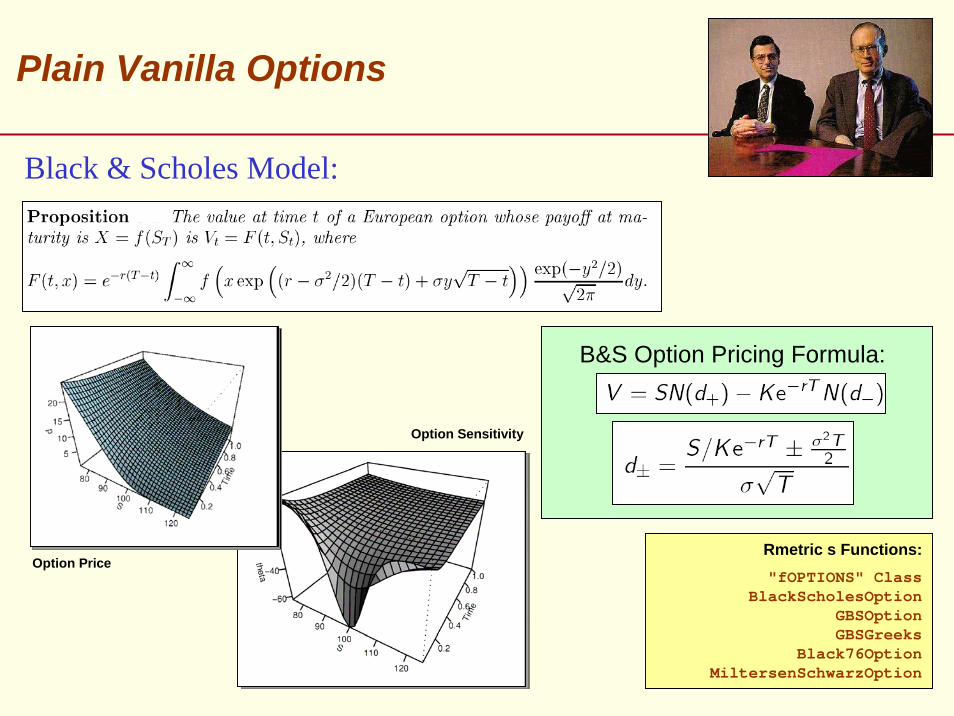

B&S Option Pricing Formula:

Black & Scholes Model:

Plain Vanilla Options

Rmetric s Functions:"fOPTIONS" Class

BlackScholesOptionGBSOptionGBSGreeks

Black76OptionMiltersenSchwarzOption

Option Price

Option Sensitivity

44

Exotic OptionsRmetrics Functions:

ExecutiveStockOptionForwardStartOption

RatchetOptionTimeSwitchOption

SimpleChooserOptionComplexChooserOption

OptionOnOption

HolderExtendibleOptionWriterExtendibleOption

TwoAssetCorrelationOptionExchangeOneForAnotherOption

ExchangeOnExchangeOptionEuropeanExchangeOption

AmericanExchangeOptionFloatingStrikeLookbackOption

FixedStrikeLookbackOptioPTFloatingStrikeLookbackOption

PTFixedStrikeLookbackOption

StandardBarrierOptionDoubleBarrierOption

PTSingleAssetBarrierOptionTwoAssetBarrierOption

PTTwoAssetBarrierOptionLookBarrierOption

DiscreteBarrierOptionSoftBarrierOption

GapOptionCashOrNothingOption

TwoAssetCashOrNothingOptionAssetOrNothingOption

SuperShareOptionBinaryBarrierOption

GeometricAverageAsianOptionTurnbullWakemanAsianApproxOption

LevyAsianApproxOptionFEInDomesticFXOptionEquityLinkedFXOption

TakeoverFXOption

Exotic Options

Rmetrics has implemented several functions to price (beside plain vanilla, options) many types of exotic options.

An Exotic Option breaks at least one of the standard contract terms of a traditional option. They can be manipulated according to the following categories:

Options with Contract VariationsPath-Dependent OptionsLimit-Dependent OptionsMulti-Factor Options

An Example From the fOptions Package

45

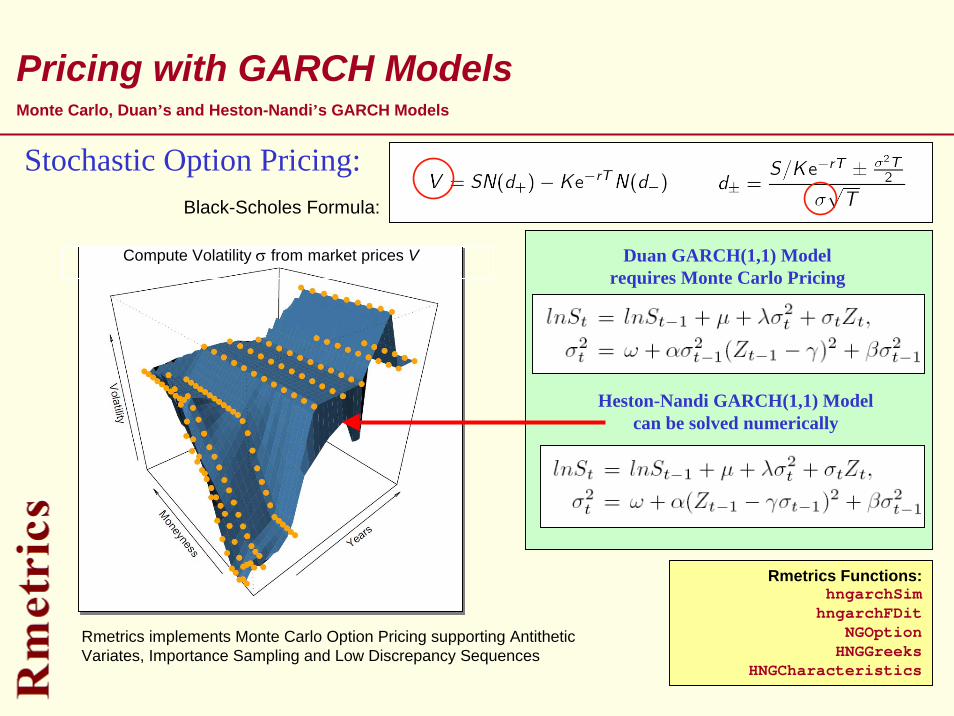

Pricing with GARCH ModelsMonte Carlo, Duan’s and Heston-Nandi’s GARCH Models

Duan GARCH(1,1) Modelrequires Monte Carlo Pricing

Heston-Nandi GARCH(1,1) Modelcan be solved numerically

Compute Volatility σ from market prices V

Stochastic Option Pricing:Black-Scholes Formula:

Rmetrics Functions:hngarchSim

hngarchFDitNGOption

HNGGreeks HNGCharacteristics

Rmetrics implements Monte Carlo Option Pricing supporting Antithetic Variates, Importance Sampling and Low Discrepancy Sequences

46

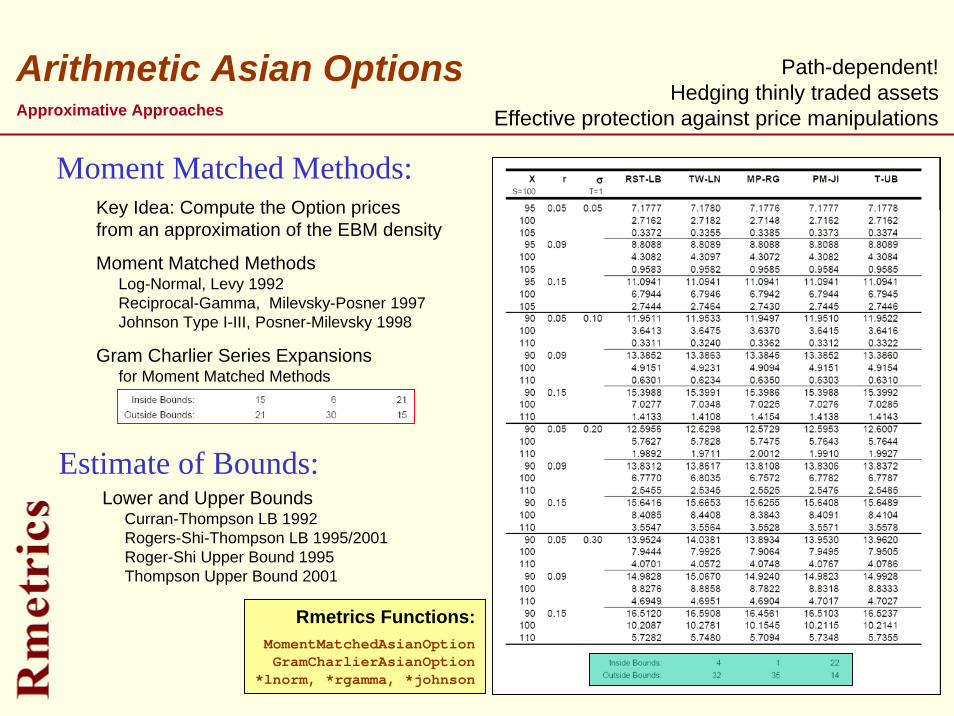

Arithmetic Asian Options

Key Idea: Compute the Option pricesfrom an approximation of the EBM density

Moment Matched MethodsLog-Normal, Levy 1992Reciprocal-Gamma, Milevsky-Posner 1997Johnson Type I-III, Posner-Milevsky 1998

Gram Charlier Series Expansionsfor Moment Matched Methods

Moment Matched Methods:

Rmetrics Functions:MomentMatchedAsianOptionGramCharlierAsianOption

*lnorm, *rgamma, *johnson

Lower and Upper BoundsCurran-Thompson LB 1992Rogers-Shi-Thompson LB 1995/2001Roger-Shi Upper Bound 1995Thompson Upper Bound 2001

Estimate of Bounds:

Approximative Approaches

Path-dependent!Hedging thinly traded assets

Effective protection against price manipulations

47

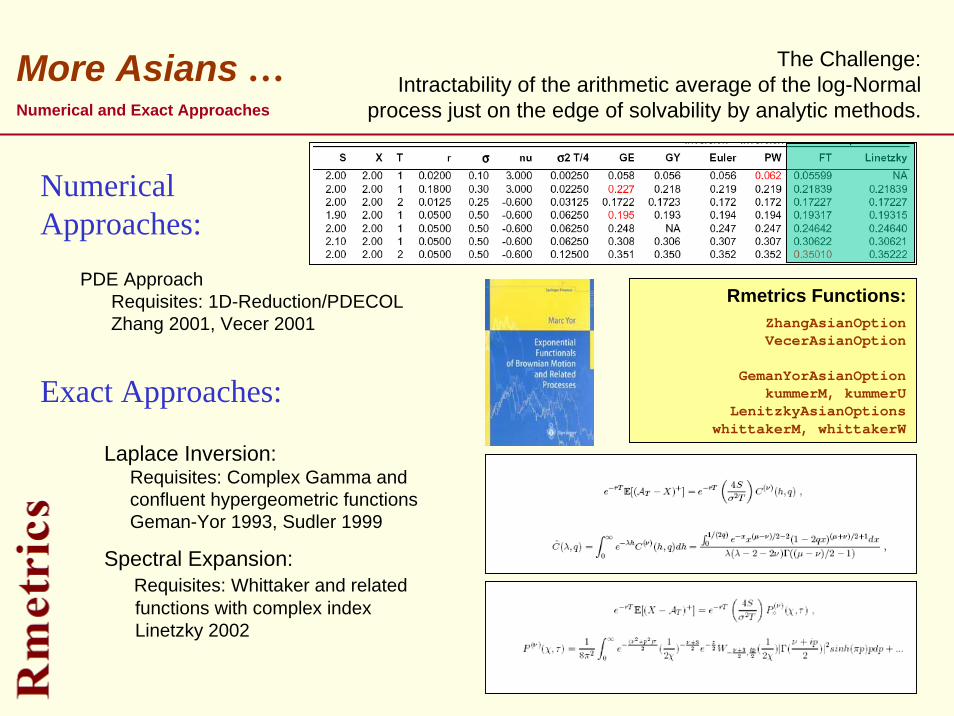

More Asians …

Laplace Inversion:Requisites: Complex Gamma andconfluent hypergeometric functionsGeman-Yor 1993, Sudler 1999

Spectral Expansion:Requisites: Whittaker and relatedfunctions with complex indexLinetzky 2002

PDE ApproachRequisites: 1D-Reduction/PDECOLZhang 2001, Vecer 2001

Numerical Approaches:

Exact Approaches:

Rmetrics Functions:ZhangAsianOptionVecerAsianOption

GemanYorAsianOptionkummerM, kummerU

LenitzkyAsianOptionswhittakerM, whittakerW

Numerical and Exact Approaches

The Challenge:Intractability of the arithmetic average of the log-Normal

process just on the edge of solvability by analytic methods.

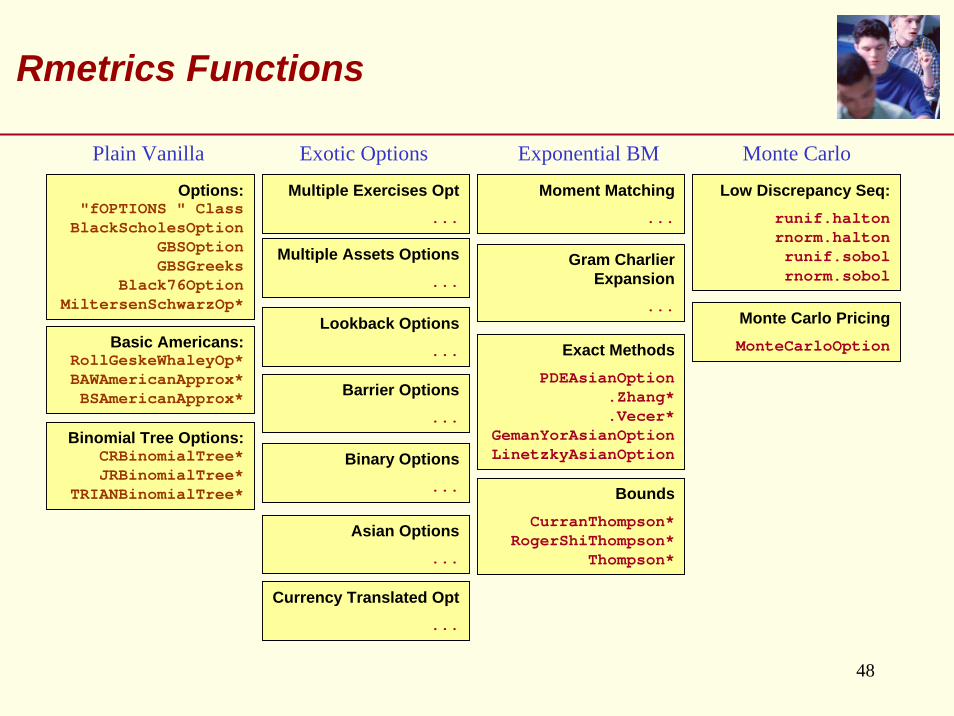

48

Rmetrics Functions

Basic Americans:RollGeskeWhaleyOp*BAWAmericanApprox*BSAmericanApprox*

Plain Vanilla Exotic Options Monte Carlo

Options:"fOPTIONS " Class

BlackScholesOptionGBSOptionGBSGreeks

Black76OptionMiltersenSchwarzOp*

Multiple Exercises Opt...

Moment Matching...

Low Discrepancy Seq:runif.haltonrnorm.haltonrunif.sobolrnorm.sobol

Exponential BM

Multiple Assets Options...

Binomial Tree Options: CRBinomialTree*JRBinomialTree*

TRIANBinomialTree*

Lookback Options...

Barrier Options...

Binary Options...

Asian Options...

Currency Translated Opt...

Gram CharlierExpansion

...

Exact MethodsPDEAsianOption

.Zhang*

.Vecer*GemanYorAsianOptionLinetzkyAsianOption

BoundsCurranThompson*

RogerShiThompson*Thompson*

Monte Carlo PricingMonteCarloOption

49

Term Structure Modelling

Structure Joyeuse – Wassily Kandinski

50

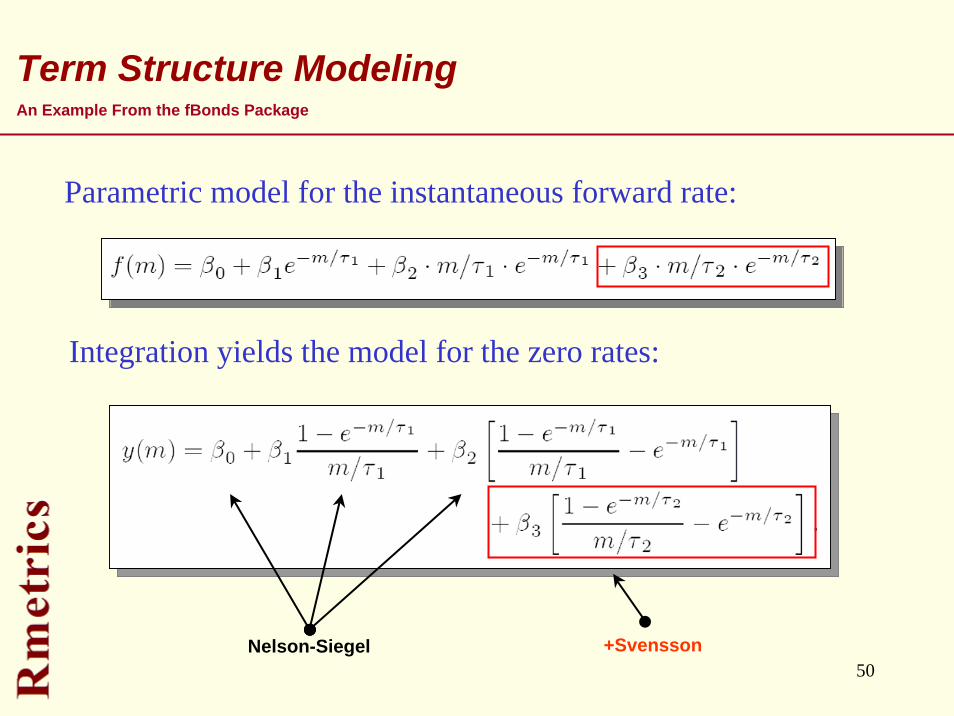

Term Structure Modeling

Parametric model for the instantaneous forward rate:

Integration yields the model for the zero rates:

Nelson-Siegel +Svensson

An Example From the fBonds Package

51

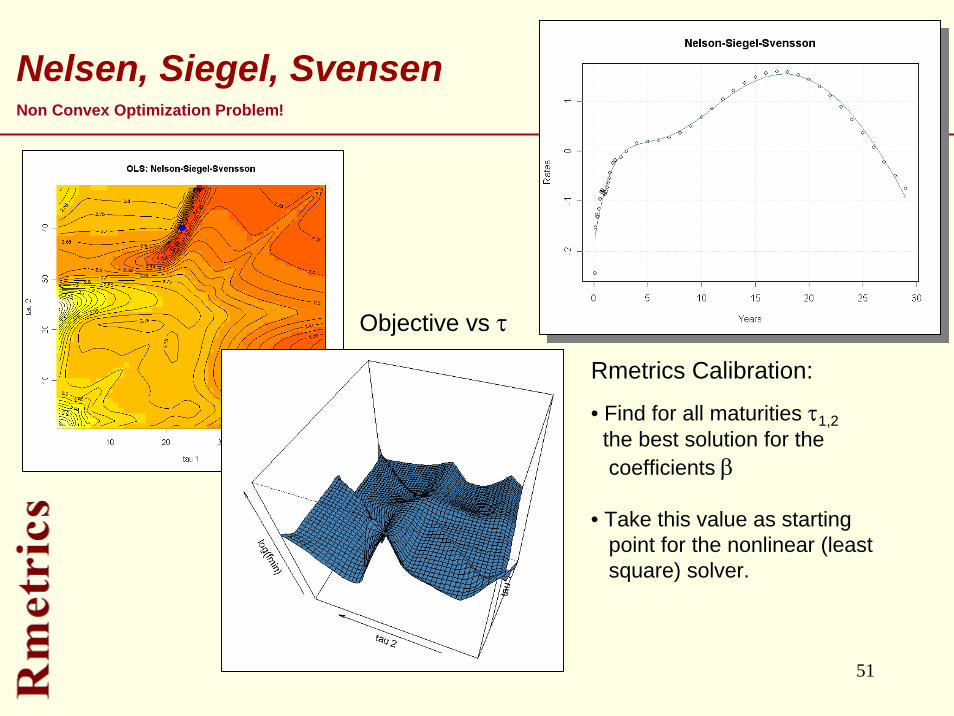

Nelsen, Siegel, Svensen

Rmetrics Calibration:

• Find for all maturities τ1,2the best solution for the coefficients β

• Take this value as starting point for the nonlinear (leastsquare) solver.

Objective vs τ

Non Convex Optimization Problem!

52

PortfolioSelection and Optimization

Circ

les

in a

Circ

le –

Was

sily

Kan

dins

ki

53

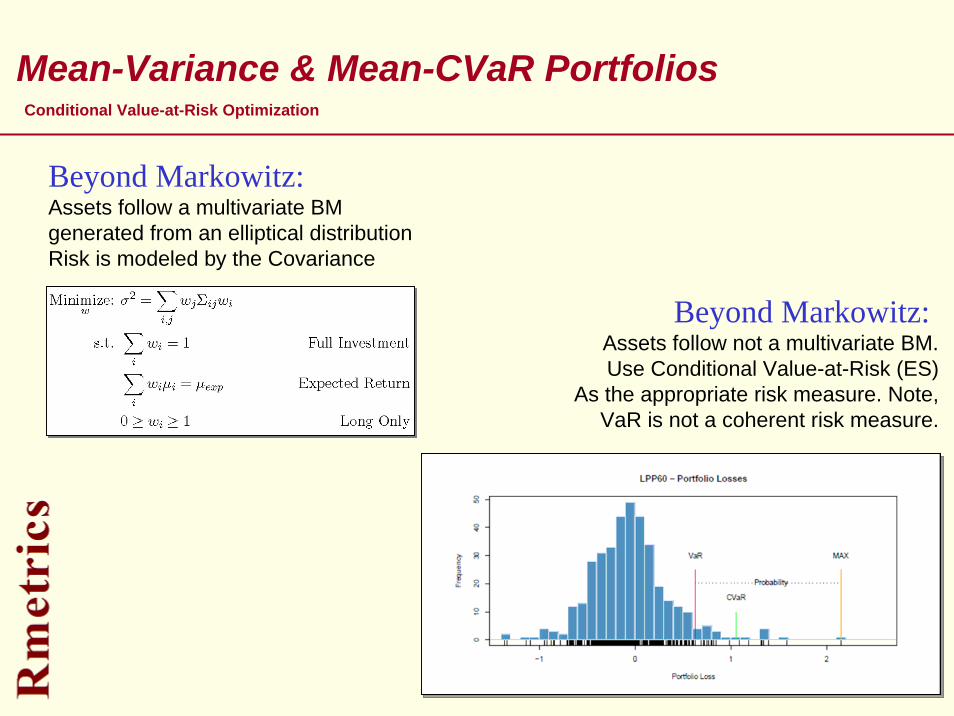

Beyond Markowitz:Assets follow not a multivariate BM.Use Conditional Value-at-Risk (ES)

As the appropriate risk measure. Note,VaR is not a coherent risk measure.

Mean-Variance & Mean-CVaR PortfoliosConditional Value-at-Risk Optimization

Beyond Markowitz:Assets follow a multivariate BMgenerated from an elliptical distributionRisk is modeled by the Covariance

54

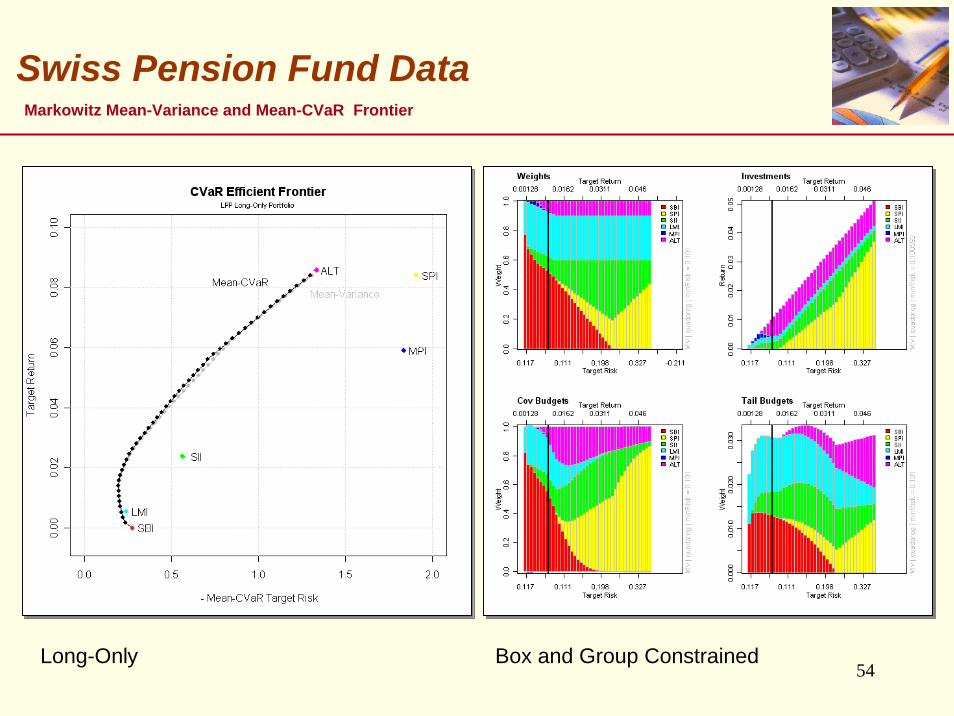

Swiss Pension Fund DataMarkowitz Mean-Variance and Mean-CVaR Frontier

Long-Only Box and Group Constrained

55

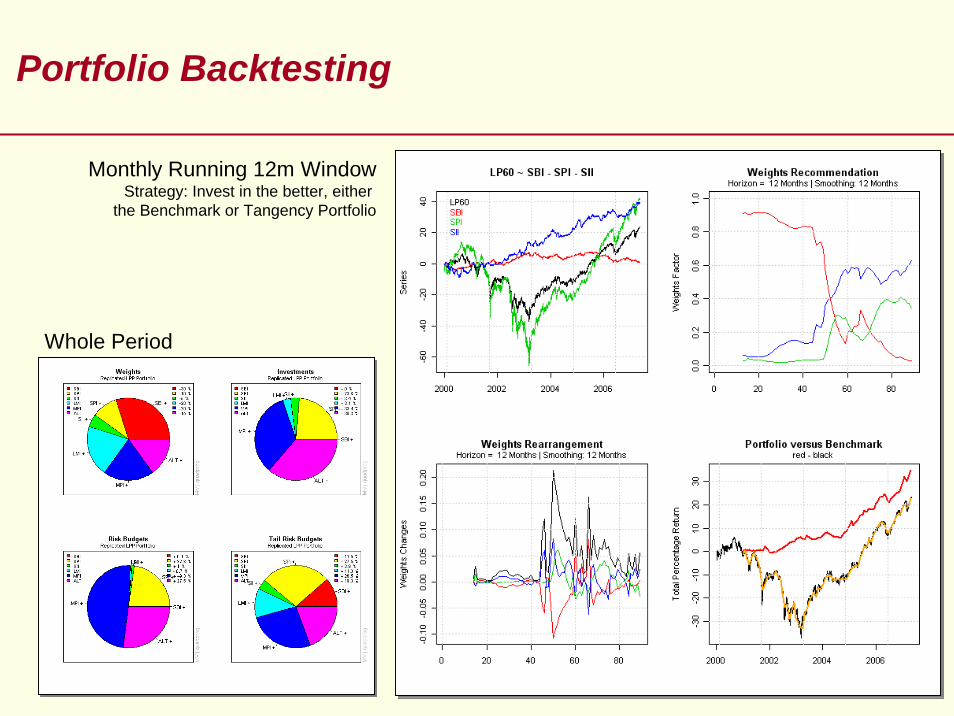

Portfolio Backtesting

Whole Period

Monthly Running 12m WindowStrategy: Invest in the better, either

the Benchmark or Tangency Portfolio

56

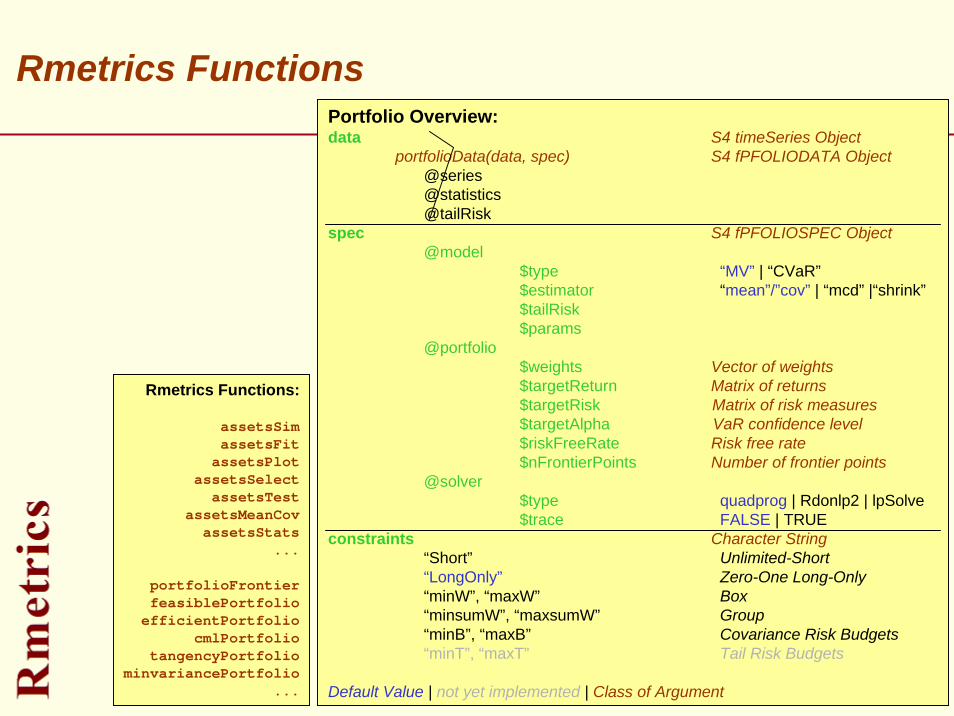

Portfolio Overview:data S4 timeSeries Object

portfolioData(data, spec) S4 fPFOLIODATA Object@series@statistics@tailRisk

spec S4 fPFOLIOSPEC Object@model

$type “MV” | “CVaR”$estimator “mean”/”cov” | “mcd” |“shrink”$tailRisk$params

@portfolio$weights Vector of weights$targetReturn Matrix of returns$targetRisk Matrix of risk measures$targetAlpha VaR confidence level$riskFreeRate Risk free rate$nFrontierPoints Number of frontier points

@solver$type quadprog | Rdonlp2 | lpSolve$trace FALSE | TRUE

constraints Character String“Short” Unlimited-Short“LongOnly” Zero-One Long-Only“minW”, “maxW” Box“minsumW”, “maxsumW” Group“minB”, “maxB” Covariance Risk Budgets“minT”, “maxT” Tail Risk Budgets

Default Value | not yet implemented | Class of Argument

Rmetrics Functions

Rmetrics Functions:

assetsSimassetsFit

assetsPlotassetsSelect

assetsTestassetsMeanCov

assetsStats...

portfolioFrontierfeasiblePortfolio

efficientPortfoliocmlPortfolio

tangencyPortfoliominvariancePortfolio

...

57

timeDatetimeSeries

Raum und Zeit – Timothy Baar

58

timeDate & time Series Class

setClass("timeDate", representation(

Data = "POSIXct",Dim = "character",format = "character", FinCenter = "character",

))

setClass("timeDate", representation(

Data = "POSIXct",Dim = "character",format = "character", FinCenter = "character",

))

“GMT” POSIXct Object Number of Date ElementsPosix Format SpecificationName of Financial Center

Class Representation:

setClass("timeSeries", representation(

Data = "matrix",positions = "character",format = "character", FinCenter = "character", units = "character",recordIDs = "data.frame", title = "character",documentation = "character"

))

setClass("timeSeries", representation(

Data = "matrix",positions = "character",format = "character", FinCenter = "character", units = "character",recordIDs = "data.frame", title = "character",documentation = "character"

))

Numeric Matrix of InstrumentsCommon Time/Date StampsPosix Date FormatName of Financial CenterNames of Financial Instruments

Optional Record IdentifiersGives a Title to the Time Series Briefly Describes the Time Series

Provides Splus Compatibility

59

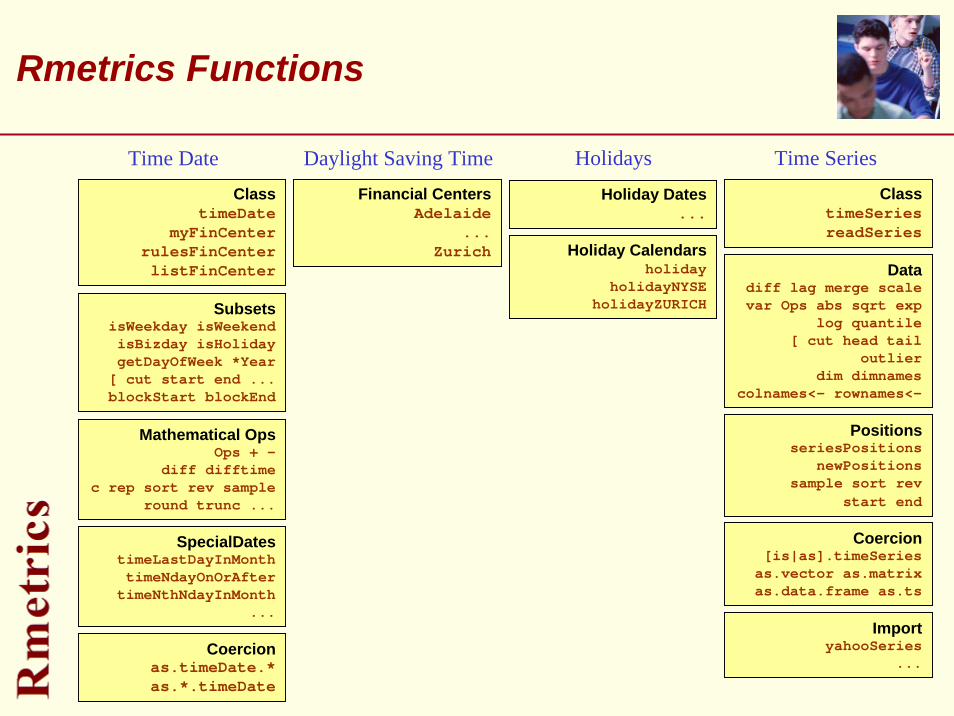

Rmetrics Functions

SubsetsisWeekday isWeekendisBizday isHoliday getDayOfWeek *Year

[ cut start end ...blockStart blockEnd

Mathematical OpsOps + -

diff difftimec rep sort rev sample

round trunc ...

SpecialDatestimeLastDayInMonth timeNdayOnOrAfter

timeNthNdayInMonth...

Daylight Saving TimeTime Date Time SeriesHolidays

Datadiff lag merge scale var Ops abs sqrt exp

log quantile[ cut head tail

outlierdim dimnames

colnames<- rownames<-

PositionsseriesPositions

newPositionssample sort rev

start end

Financial CentersAdelaide

...Zurich

ClasstimeDate

myFinCenter rulesFinCenterlistFinCenter

ClasstimeSeriesreadSeries

Coercionas.timeDate.*as.*.timeDate

Coercion [is|as].timeSeries

as.vector as.matrix as.data.frame as.ts

Holiday Dates...

ImportyahooSeries

...

Holiday Calendarsholiday

holidayNYSEholidayZURICH

60

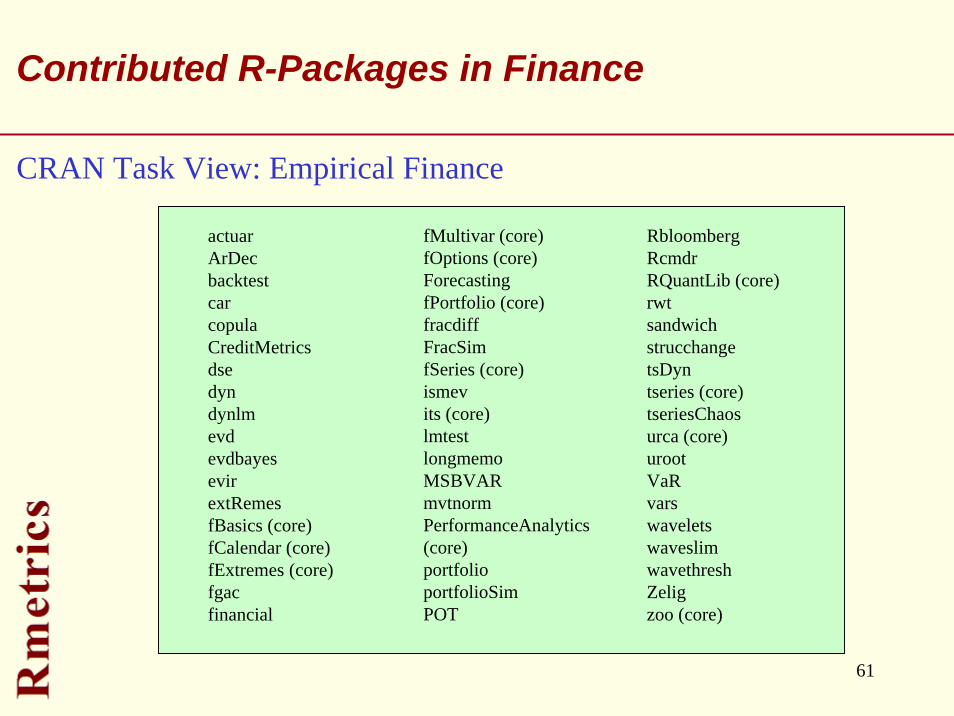

CRAN Task ViewFinance

Raum und Zeit – Timothy Baar

61

Contributed R-Packages in Finance

actuarArDecbacktestcarcopulaCreditMetricsdsedyndynlmevdevdbayesevirextRemesfBasics (core)fCalendar (core)fExtremes (core)fgacfinancial

RbloombergRcmdrRQuantLib (core)rwtsandwichstrucchangetsDyntseries (core)tseriesChaosurca (core)urootVaRvarswaveletswaveslimwavethreshZeligzoo (core)

fMultivar (core)fOptions (core)ForecastingfPortfolio (core)fracdiffFracSimfSeries (core)ismevits (core)lmtestlongmemoMSBVARmvtnormPerformanceAnalytics(core)portfolioportfolioSimPOT

CRAN Task View: Empirical Finance

62(c) 2007 Diethelm Würtz

www.itp.phys.ethz.ch | www.rmetrics.org | www.finance.ch

Thanks to CRAN and Kurt Hornik, …Thanks to R-sig-finance and Martin Mächler, …Thanks to Rmetrics on Debian and Dirk Eddelbüttel, …Thanks to all who have contributed to Rmetrics, …

Thank you for Your Attention