Embed Size (px)

Citation preview

©Amit DEV, director & Expert team at CMAI Assn of India; September 2012

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 2014 2015

$351 B $373 B $389 B $406 B $423 B $443 B

GLOBAL OUTSOURCING MARKET SIZE

FY 2012

Middle East &Africa

Central & LatinAmerica

Asia Pacific

WesternEurope

North America

REGIONAL GROWTH OF GLOBAL IT-SERVICES

Manufacturing 28.8%

Energy 15.7%

Government 15.4%

Consumers 11.9%

BFSI 11.1%

Telecom 7.2%

Education 1.5%

Healthcare 1.0%

Retail 0.4%

Others 7.0%

25.1%

20.6%

17.5%

17.5%

17.5%

17.5%

14.4%

12.7%

12.4%

16% Total

Consumers

Telecom

Healthcare

Government

Retail

Education

BFSI

Manufacturing

Energy

ITO-BPO SPENDING / GROWTH IN VERTICALS

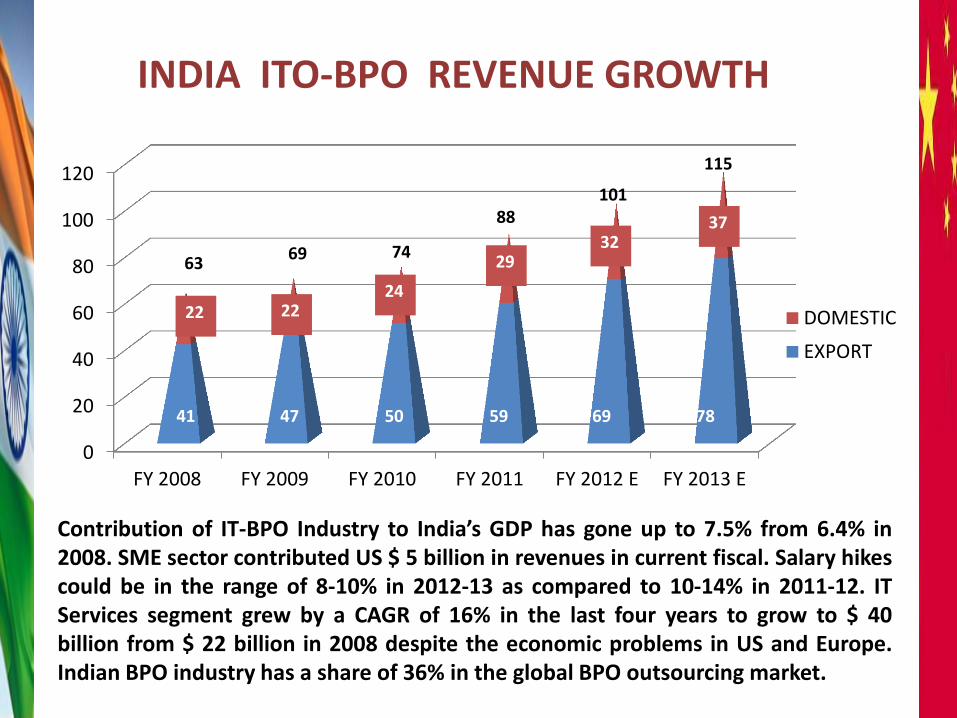

0

20

40

60

80

100

120

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 E FY 2013 E

DOMESTIC

EXPORT

63 69 74

88 101

115

41 47 50 59 69 78

22 22 24

29 32

37

Contribution of IT-BPO Industry to India’s GDP has gone up to 7.5% from 6.4% in 2008. SME sector contributed US $ 5 billion in revenues in current fiscal. Salary hikes could be in the range of 8-10% in 2012-13 as compared to 10-14% in 2011-12. IT Services segment grew by a CAGR of 16% in the last four years to grow to $ 40 billion from $ 22 billion in 2008 despite the economic problems in US and Europe. Indian BPO industry has a share of 36% in the global BPO outsourcing market.

INDIA ITO-BPO REVENUE GROWTH

[

OUTSOURCING SERVICE GIANTS, INDIA

Process consolidation

Remote support Reduction of

manual processes Transformational

outsourcing

Citizen-centric services

Focus on integrated solutions

Enablement of core processes through IT

Discounted Licensed software

Business process automation

Outsourcing of non-core processes

Services and support focus

Social connectivity

Converged solutions

Quality products

Quick and robust service support

EXPECTATIONS OF GLOBAL CUSTOMERS

Clearly, the future of technology services industry is beyond services – it will be a combination of services, solutions and platforms. Indian IT organizations are investing in building platforms to drive future growth opportunities. These domain solutions and technology platforms will offer improved revenue leverage versus talent employed in the industry and will also significantly increase the intellectual property base of the Indian IT industry. The industry can take clue from the fact that public cloud services spending is expected to outpace growth of the overall IT spend by about four times between 2012 and 2015.

With the outsourcing industry emerging from the aftermath of the global

recession, there are a number of trends that give us a glimpse of the future:

Analysts are predicting that the industry will continue to fight short-term

cost pressures, and that there will be pressure on service providers for

more flexible pricing contracts.

Buyers will seek more standardized solutions from their outsourcing

engagements, so they will have to differentiate themselves through

performance rather than pricing.

Many small alliances, focused on increased operational efficiencies,

better quality control and reduced back-office costs, are being set up.

Shared and common services were always considered a threat to

outsourcing, but the trend is changing. Sharing critical business and IT

services has been proven to cut costs, reduce errors and improve

productivity.

Brazil and Russia will make their presence felt in the global outsourcing

market and China will continue to move ahead.

FUTURE OUTSOURCING TRENDS

EXPERTISE FOR GLOBAL DELIVERY

WICS-SERVICES STRATEGY MATRIX

[

ADVISORY SERVICE INSTANCE CLIENTELE

WICS-ADVISORY: TCS AMERICA-DEAL

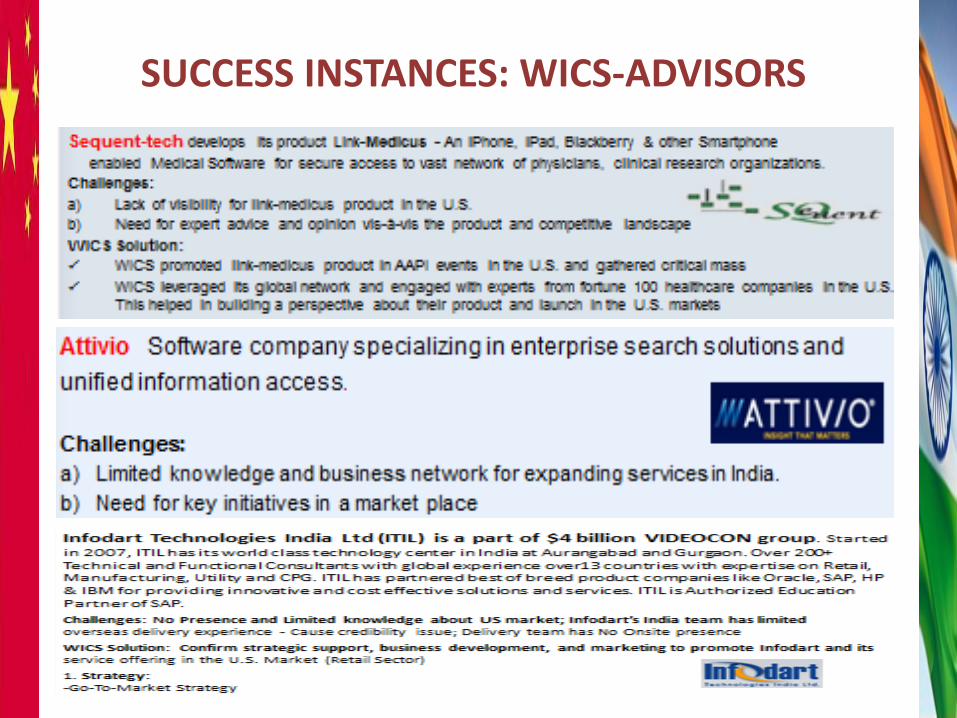

SUCCESS INSTANCES: WICS-ADVISORS

WICS-EXPERT SERVICES SPECTRUM

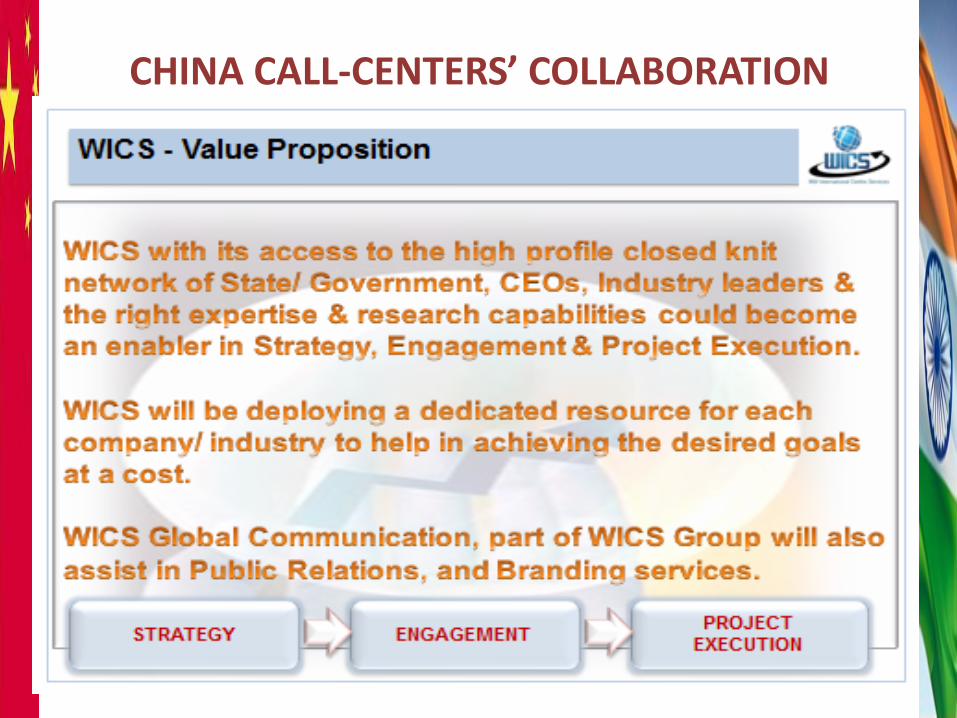

CHINA CALL-CENTERS’ COLLABORATION