Embed Size (px)

Citation preview

American Economic Association

Ambiguity Aversion and Incompleteness of Contractual FormAuthor(s): Sujoy MukerjiSource: The American Economic Review, Vol. 88, No. 5 (Dec., 1998), pp. 1207-1231Published by: American Economic AssociationStable URL: http://www.jstor.org/stable/116867Accessed: 31/03/2009 09:05

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available athttp://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unlessyou have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and youmay use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained athttp://www.jstor.org/action/showPublisher?publisherCode=aea.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printedpage of such transmission.

JSTOR is a not-for-profit organization founded in 1995 to build trusted digital archives for scholarship. We work with thescholarly community to preserve their work and the materials they rely upon, and to build a common research platform thatpromotes the discovery and use of these resources. For more information about JSTOR, please contact [email protected].

American Economic Association is collaborating with JSTOR to digitize, preserve and extend access to TheAmerican Economic Review.

http://www.jstor.org

Ambiguity Aversion and Incompleteness of Contractual Form

By SUJOY MUKERJI*

Subjective uncertainty is characterized by ambiguity if the decision maker has an imprecise knowledge of the probabilities of payoff-relevant events. In such an instance, subjective beliefs are better represented by a set of probability functions than by a unique probability function. An ambiguity-averse decision maker ad- justs his choice on the side of caution in response to his imprecise knowledge of the odds. This paper shows that ambiguity aversion can explain the existence of incomplete contracts. The contextual setting is the investment hold-up model which has been the focus of much of the research on incomplete contracts. (JEL D23, D8, L22)

State-contingent contracts record agree- ments about rights and obligations of contract- ing parties at uncertain future scenarios: descriptions of possible future events are listed and the action to be taken by each party on the realization of each listed contingency is spec- ified. Casual empiricism suggests that a real- world contract is very often incomplete in the sense that it may not include any instruction for some possible events. The actual actions to be taken in such events are thus left to ex post negotiation. The fact that real-world contracts are incomplete explains the working of many economic institutions [see surveys by Jean Tirole (1994), Oliver D. Hart (1995), and James M. Malcomson (1997)]. Take for in- stance the institution of the business firm. What determines whether all stages of produc- tion will take place within a single firm or will

be coordinated through markets? In a world of complete contingent contracts there is no ben- efit from integrating activities within a single firm as opposed to transacting via the market. However, contractual incompleteness can ex- plain why integration might be desirable and more generally why the allocation of authority and of ownership rights matters. This insight developed by Ronald H. Coase (1937), Herbert A. Simon (1951), Benjamin Klein et al. (1978), Oliver E. Williamson (1985), and Sanford J. Grossman and Hart (1986), among others, underscores the importance of under- standing what reasons explain why and in what circumstances contracts are left incomplete.

Traditionally, incompleteness of contracts has been explained by appealing to a combi- nation of transactions costs (e.g., Williamson, 1985) and bounded rationality (e.g., Barton L. Lipman, 1992; Luca Anderlini and Leonardo Felli, 1994). These rationalizations validate the incompleteness as an economizing action on the hypothesis that including more detail in a coniract involves direct costs. This paper will provide an alternative explanation based on the hypothesis that decision behavior under subjective uncertainty is affected by ambiguity aversion. Indeed, it will be assumed through- out that there is no direct cost to introducing a marginal contingent instruction into a contract.

Suppose an agent's subjective knowledge about the likelihood of contingent events is consistent with more than one probability dis- tribut:ion, and further that what the agent

* Department of Economics, University of Southamp- ton, Southampton S017 1BJ, U.K. (e-mail: sm5@ soton.ac.uk). The paper has benefited very substantially from the many constructive suggestions of the two anon- ymous referees. Their efforts went much beyond the call of duty and I remain very grateful. Jim Malcomson's painstaking scrutiny of an earlier draft made possible the much-needed expositional improvements. I also thank Dieter Balkenborg, Jacques Cramer, David Kelsey, Fahad Khalil, Peter Klibanoff, Andrew Mountford, David Pearce, R. Edward Ray, Gerd Weinrich, and seminar members at various universities and conferences (espe- cially the audience at the Conference on Decision Making Under Uncertainty held at Saarbruicken [Germany], Uni- versity of Saarland) for helpful discussions and comments.

1207

1208 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

knows does not inform him of a precise (second-order) probability distribution over the set of "possible" probabilities. We say then that the agent's beliefs about contingent events are characterized by ambiguity. If am- biguous,1 the agent's beliefs are captured not by a unique probability distribution in the stan- dard Bayesian fashion but instead by a set of probabilities, any one of which could be the "true" distribution. Thus not only is the par- ticular outcome of an act uncertain but also the expected payoff of the action, since the payoff may be measured with respect to more than one probability. An ambiguity-averse de- cision maker evaluates an act by the minimum expected value that may be associated with it. Thus the decision rule is to compute all pos- sible expected values for each action and then choose the act which has the best minimum expected outcome. The idea being, the more an act is affected adversely by the ambiguity the less its appeal to the ambiguity-averse de- cision maker. The formal analysis in this paper basically involves a reconsideration of the ca- nonical model of a vertical relationship be- tween two contracting firms under the assumption that the agents' common infor- mation about the contingent events is ambig- uous and that the agents are ambiguity averse. Next, I preview this exercise with a simple example.

Consider two vertically related risk-neutral firms, B and S. B is an automobile manufac- turer planning to introduce a new line of mod- els. B wishes to purchase a consignment of car bodies (tailor-made for the new models) from S. The firms may sign a contract at some initial date 0 specifying the terms of trade of the sale at date 2; that is, whether trade takes place and

at what price. The gains from trade are contin- gent upon the state of nature realized in date 1. There are three possible contingencies, w0, Wb, wg, with corresponding tradeable surpluses SO, Sb, SS- After date 0 but before date 1, S invests in research for a die that will efficiently cast car bodies required for the new model while B invests effort to put together an ap- propriate marketing campaign for the new model. The investments affect the likelihood of realizing a particular state of nature. Each firm may choose between a low and a high level of investment effort. The investments are not contractible per se but the terms of trade specification may be made as contingency spe- cific as required. In the case that the contract is incomplete and an "unmentioned" event arises with sure potential for surplus, it is com- monly anticipated by the parties that trade will be negotiated ex post and the surplus split evenly. Consider the two possibilities X and Y: X -there is a longer list of reservations for the new model than for comparable makes and at a price higher than those for comparable makes; Y -the variable cost of production of car bodies is low. The state of the world w0 is characterized by the fact that both the state- ments are false. At Wb, X iS true but not Y; conversely, at wg, X is false but Y holds.2 Cor- respondingly suppose so < Sb = s,. The com- mon belief about the likelihood of Wb is at the margin affected (positively) more by B choos- ing the high investment effort over low effort than by S doing the same, while the opposite is true of ws. As is customary, we define a (first-best) efficient investment profile as one that would be chosen if investment effort were verifiable and contractible.

Bear in mind the allowance of being able to write complete contingent contracts and the institutional setting of a vertical interfirm relationship. As will be formally argued in a subsequent section, given all this and that decision makers are subjective expected util- ity (henceforth, SEU) maximizers, the non- verifiability of investment will not impede efficiency. In our example for instance, a

' To preempt misunderstandings it is emphasized that the term "ambiguity," as used in this paper, refers purely to the fuzzy perception of the likelihood subjectively as- sociated with an event (e.g., when asked about his subjec- tive estimate of the probability of an event, the agent replies, "It is between 50 and 60 percent."). It does not refer to a lack of clarity in the description of contingent events and actions. Also note, some authors and research- ers refer to ambiguity as "Knightian Uncertainty" or even simply as "uncertainty." As it is used in this paper, the word "uncertainty" is simply the defining characteristic of any environment where the consequence of at least one action is not known for certain.

2 The reader is assured that the example is essentially unaffected by also having a state in which both the state- ments are true.

VOL. 88 NO. S MUKERJI: AMBIGUITY AVERSION AND INCOMPLETE CONTRACTS 1209

contract which distinguishes the three con- tingencies and sets prices that reward B sufficiently higher at Wb than at other contin- gencies (and similarly reward S at wg) will enforce the first-best effort profile. The gen- eral conclusion is that if agents are SEU maximizers then an incomplete contract which implements an inefficient profile can- not be rationalized. Such a contract can never be the optimal because it will be pos- sible to find a complete contract that domi- nates it (i.e., a contract that obtains higher ex ante payoffs for both parties). However, this conclusion is overturned if agents are ambiguity averse. The logic of this may be seen by reevaluating the above example with the sole amendment that agents are ambi- guity averse. To provide sufficient incentive to take the efficient investment, the ex post payoffs in the contract have to treat the two firms asymmetrically at Wb and ws; for B the payoff is higher at wb than at ws, while it is the other way around for S. This implies that the firms must use different probability dis- tributions to evaluate their expected payoffs. From the set of probabilities embodying the firms' symmetric information, B measures its payoffs using a probability distribution that puts a relatively higher weight on ws than the distribution S thinks prudent to check its payoff against. Consequently, the sum of the expected payoffs will fall short of the expected total surplus-there is a "virtual loss" of the expected surplus. It fol- lows that if this "loss" is large enough the participation constraints will break, thereby making such a contract impossible. An in- complete contract, say the null contract (one that leaves all allocation of contingent sur- plus to ex post negotiation), is not similarly vulnerable to ambiguity aversion. Such a contract will lead to a proportionate division of surplus at each contingency, implying that each firm will use the same probability to evaluate its payoffs. Additivity of the stan- dard expectation operator then ensures that no "virtual loss" occurs. It will be shown that from all this it follows that there will be parametric configurations for which an in- complete contract, even though only imple- menting an inefficient investment profile, is not dominated by any other contract. Under

such circumstances the market transaction, if maintained, may justifiably be conducted with an "inefficient" incomplete contract. The "inefficiency" of the market transac- tion would also explain why it might be abandoned in favor of vertical integration.

Why might an explanation like the one given above be of interest? The final section of the paper will discuss historic instances of vertical mergers and empirical regularities about supply contracts that are understandable on the basis of ambiguity aversion, but are not well explained by "physical" transactions costs of writing contingent details into con- tracts. A recurrent claim amrong business peo- ple is that they integrate verticaily because of uncertainty in input supply. This idea has al- ways caused difficulties for economists (see, for instance, Dennis W. Carlton, 1979) who have been unable to rationalize it and have generally regarded it as misguided (see, how- ever, George Baker et al., 1997). The analysis in the present paper explains how the idea of ambiguity aversion provides one precise un- derstanding of the link between uncertainty and vertical integration.3 Moreover, since vi- olations of SEU in generai, and evidence of ambiguity aversion in particular, have long been noted in laboratory settings, it is worth uncovering what implications such "patholo- gies" have for "real-world" economics out- side the laboratory. The exercise in this paper is at least partly inspired by this thought. Fi- nally, at a more abstract level, a significant in- sight obtained is that even if there were no direct cost to conditioning contractual terms on "finely described" events, one may well end up with only "coarse" arrangements be- cause the value of fine-tuning is not robust to the agents' misgivings that they have only a vague assessment of the likelihoods of the rel- evant "fine" events.

The rest of the paper is organized as fol- lows: Section I introduces the framework of the formal decision model and its underlying motivation; Section II analyses the hold-up model under the assumption of ambiguity

: The author remains most grateful to the two anony- mous referees for drawing his attention to this point.

1210 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

aversion; Section III concludes the paper with a discussion of the empirical signifi- cance of the results. The Appendix contains the formal proofs. Those eager for a first pass at the arithmetic of the main result may wish to look at Example 2 (which basically fleshes out the above example) in Section II

I. An Introduction to the Model of Decision- Making by Ambiguity-Averse Agents

It is often the case that a decision maker's (DM) perception of the uncertain environment is ambiguous in the sense that his knowledge is consistent with more than one probability function. The theory of ambiguity aversion is inspired by two simple hypotheses about decision-making in such situations. First, that behavior is influenced by ambiguity: i.e., DM's behavior actually reflects the fact that his guess about a likelihood may be given by a probability interval. By presumption agents do not necessarily behave as if they have re- duced all their ambiguity to a belief consistent with a unique probability using a "second- order" probability over the different proba- bility distributions consistent with their knowledge. Second, that agents are ambiguity averse. That is, ceteris paribus, the more am- biguous their knowledge of the uncertainty the more conservative is their choice. David Schmeidler (1989) pioneered an axiomatic derivation of a model of DMs with preferences incorporating ambiguity aversion. This paper uses Schmeidler's model, termed the Choquet expected utility (CEU) model, in the formal arguments.

The DM's domain of uncertainty is the finite state space Q = { wi I =. The DM chooses between acts whose payoffs are state contingent: e.g., an act f, f: Q -- R. In the CEU model an ambiguity-averse DM's sub- jective belief is represented by a convex non- additive probability function, w. Like a standard probability function it assigns to each event a number between 0 and 1, and it is also true that, (i) w(0) 0 O and (ii) w(Q) = 1. Where a convex nonadditive probability func- tion differs from a standard probability is in the third property, (iii) wr(X U Y/) ? w(X) + 7ry U- 7rf X nyMA for all X, Y C Q. By this

third property4 the measure of the union of two disjoint events may be greater than the sum of the measure of each individual event. A con- vex nonadditive probability function is actu- ally a parsimonious representation of the full range of probabilities compatible with the DM's knowledge. ir(X) is interpreted as the minimum possible probability of X. This is readily seen from the fact that a given convex nonadditive probability ir corresponds to a unique convex set of probability functions identified by the core5 of ir, denoted by FI( r) [notation: A(Q) is the set of all additive prob- ability measures on Q]:

H(ir) - {1rj E A(Q)j1r1(X)

2 ir(X), for allXC Q}.

Hence, 7r(X) = min71j 1 (X). The convex nonadditive probability representation enables us to express the notion of ambiguity precisely. We say ir is ambiguous if there are two events X, Y such that axiom (iii) holds with a strict inequality; 7r is unambiguous if axiom (iii) holds as an equality everywhere. (A DM with unam- biguous belief is a SEU maximizer.) The am- biguity' of the belief about an event X is measured by the expression A(ir(X)) 1 - ir(X) - r(XC). The relation between 7r and

4 In general, a nonadditive probability (or capacity) 7r obeys the axioms (i), (ii), and the condition that X 2 Y X

7(X) 2 7( Y). The axiom (iii) applies to the special case of a convex nonadditive probability. The term "convex" points to the requirement that the nonadditive probability of a set is (weakly) greater than the sum of the nonadditive probabilities of the cells of a partition of the set. Presumably, the analogy is to the property of any increasing convex function, say 4): R+ - R, that 4(x) + 4(y) c 4(x + y). It is when the nonadditive probability is convex that the CEU decision rule corresponds to ambiguity aversion.

'This follows from the celebrated theorem in Lloyd S. Shapley (1965) which asserts the existence of a core allo- cation corresponding to any convex characteristic value func- tion defined on possible coalitions in a cooperative game.

6 Peter C. Fishburn ( 1993) provides a axiomatic justi- fication of this definition of ambiguity and Mukerji ( 1997) demonstrates its equivalence to a more primitive and ep- istemic notion of ambiguity (expressed in terms of the DM's knowledge of the state space). Massimo M. Marinacci (1995) applies the idea to game theory, while David Kelsey and Shasikanta Nandeibam's (1996) anal- ysis explains why this definition is sometimes interpreted as a measure of "uncertainty aversion."

VOL. 88 NO. S MUKERJI: AMBIGUITY AVERSION AND INCOMPLETE CONTRACTS 1211

11(w) shows that the -A is indeed a measure of the "fuzziness" of the belief, since, A4(w(X)) =

max7,j . n (r) 1rj(X) - min7j C n(7,) 1j](X). The DM evaluates Choquet expectation of

each act with respect to the nonadditive prob- ability, and chooses the act with the highest evaluation. Given a convex nonadditive prob- ability w, the Choquet expectation7 of an act is simply the minimum of all possible "stan- dard" expected values obtained by measuring acts with respect to each of the additive prob- abilities in 11(r), the core of w:

CE(f) =min{ I f(wi)wi(wi)}i 7rjrl(7r ) wiCG

The Choquet expectation of an act is just its standard expectation calculated with respect to a "minimizing probability" corresponding to this act. Hence, in the Choquet method the DM's appraisal is not only informed by his knowledge of the odds but is also automati- cally adjusted downwards to the extent it may be affected by the imprecision of his knowl- edge. The fact that the same additive proba- bility (in the core of relevant nonadditive probability) will not in general "minimize'' the expectation for two different acts, explains why the Choquet expectations operator, unlike the standard operator, is not additive:

PROPERTY: For any two actsf, g: CE (f ) + CE(g) c CE(f + g).

Two acts are comonotonic if their outcomes are monotonic across the state space in the same way: i.e., the acts f and g are comono-

7 The Choquet expectation operator may be directly de- fined with respect to a nonadditive probability. Label wi such thatf(w1 ) c * *f(wN). Then,

N

CCE,r(f f f(wi,) + E, [ f(wui) f f(wi -X)] i =2

X ir( { Wi, WN})

N- I

= f(w)i ( {(vi, WN})

W + l *-- .N})] + f (WN)({wN} )

tonic if for every w, w' -E Q, (f (w) -

f(w'))(g(w) - g(w')) O 0. Clearly, for com- onotonic acts the "minimizing probability" will be the same. Hence, the Choquet expec- tations operator is assuredly additive if the acts being considered are cornonotonic, but not otherwise. The first example explains how noncomonotonicity may lead to the failure of additivity.

Example 1: Two agents, B and S, are consid- ering their respective payoff from an agree- ment for sharing a contingent "surplus." Table 1 indicates the (nonadditive) probability describing the common information about the uncertainty, the contingent surpluses, and the division of the surplus specified in the agreement.

Given w(*), B's expected payoff is obtained by taking expectations with respect to the rel- evant minimizing probability in the core of

C CE(b) = 0.7 x 40 + 0.3 x 60 = 46. Similarly, S's expected payoff CE(s) = 0.4 X 60 + 0.6 X 40 = 48. Finally, the expectation of the total surplus CE(b + s) = 100.

Clearly, CE(b) + CE(s) = 94 < CE(b + s). Note that the payoff vectors chosen for B and S are noncomonotonic. This is responsible for the fact that (given 1r) the minimizing probability corresponding to B's payoffs (0.7; 0.3) is different from that corresponding to S's payoffs (0.4; 0.6)-hence the evident failure of additivity. Notice how b and s mutually "hedge" against the ambiguity. This is the "economic" intuition of why "integrated" payoffs given by (b + s) is relatively robust (in the sense that its expected payoff is less affected by the possible mistake about the ac- tual probability) to ambiguity aversion.8

In the example, the Choquet operator cal- culates expectations using the nonadditive probability directly by multiplying the non- additive probability of each wi with the payoff at the respective wi and then multiplying the "residual" [X({Ws, Wbl) - w(Ws) - )(Wb)] with minimum outcome of the act across the two states. Thus,

8 For a fuller review of the arithmetic of the Choquet expectation operator, see Example Al in the Appendix.

1212 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

TABLE 1-RELEVANT DETAILS ABOUT THE CONTINGENT STATES

Possible states

as WI,b

Nonadditive probability of the state 7r(w,) = 0.4 7r(wlb) = 0.3

Total surplus in the state 100 100

Surplus designated for B in the state 40 60

Surplus designated for S in the state 60 40

CE(b) = 40 X w(w,) + 60 X 7f(Wb)

+min{40,60} X [X( {w,w)b I

-w(ws) -w(b) ]

=0.4X40+0.3 X60+40 X0.3

= 46.

In general, the operator will associate the "re- sidual" in an event with the worst outcome in the event. See Example Al for further clarification.

A convex nonadditive probability function expresses the idea that an agent's knowledge of the true likelihood of an event E, is less vague than his knowledge of the likelihood of a cell in a "fine" partition of E.9 It is common experience that the evidence and received knowledge that informs one of the likelihood of a "large" event does not readily break down to give similar information about the "finer" constituent events. While it is routine to work out an "objective" next-day forecast of the probability of rain in the New York area, the same analytics generally would not yield a similar forecast for a particular borough in New York. Beliefs are not built "bottom up": one typically does not figure out the belief about a "large" event by putting together the

beliefs about all possible subevents. This ra- tionale for nonadditive probabilities is formal- ized in Paolo Ghirardato (1994) and Mukerji (1997). These papers also point out how a similar rationale explains why the DM's awareness that the precise implication of some contingencies is inevitably left unforeseen will typically lead to beliefs that have nonadditive representation. The papers explain the Cho- quet decision rule as a "procedurally rational" agent's means of "handicapping" the evalu- ation of an act to the extent the estimate of its "expected performance" is adversely affected by his imprecise knowledge of the odds.

There is considerable experimental evi- dence (see Colin F. Camerer and Martin Weber, 1992) demonstrating that DMs' choices are influenced by ambiguity and also that aversion to the perceived ambiguity is typ- ical. The classic experiment, due to Daniel Ellsberg (1961), runs as follows:

There are two urns each containing one hundred balls. Each ball is either red or black. The subjects are told of the fact that there are fifty balls of each color in urn I. But no information is provided about the proportion of red and black balls in urn II. One ball is chosen at ran- dom from each urn. There are four events, denoted IR, IB, IIR, IIB, where IR denotes the event that the ball chosen from urn I is red, etc. On each of the events a bet is offered: $100 if the event occurs and $0 if it does not.

The modal response is for a subject to prefer every bet from urn I (IR or IB) to every bet

9 This is technically evident from the fact that if { X, y I is a partition of the set TE, then convexity of the belief (on TE) implies,

A(,x(X) + A(x Y1 )/r 11

A( x(E) tF

VOL. 88 NO. 5 MUKERJI: AMBIGUITY AVERSION AND INCOMPLETE CONTRACTS 1213

from urn II (IIR or IIB). That is, the typical revealed preference is IB > IIB and IR > IIR. (The preferences are strict.) The DM's beliefs about the likelihood of the events, as revealed in the preferences, cannot be described by a unique probability distribution. The story goes: People dislike the ambiguity that comes with choice under uncertainty; they dislike the possibility that they may have the odds wrong and so make a wrong choice (ex ante). Hence they go with the gamble where they know the odds -betting from urn I. It is straightforward to check that the choice is consistent with con- vex nonadditive probabilities: For instance, let w(IR) = w(JB) and w(IR) + w(JB) = w(IR U IB) = 1; also let w(IIR) = w(IJJB), but allow ir(IIR) + w(IIB) < w(IIR U IIB) = 1. It follows that the expected payoff from bet- ting on IR CE(IR) CE(IB) = 50; and, CE(IIR) = CE(IIB) =r(IIR) X 100 w(IJB) X 100 < 50.

The theory of ambiguity aversion lends fresh insight into the analysis of important economic problems. Despite the relative novelty of the the- ory, there is already convincing evidence of this. Interesting applications in the area of finance in- clude James P. Dow and Sergio R. Werlang (1992), Larry G. Epstein and Tan Wang (1994, 1995), and Jean-Marc Tallon (1998). Specific applications to strategic interaction include Dow and Werlang (1994), Mukerji (1995), Jurgen Eichberger and David Kelsey (1996), and Kin Chung Lo (1998).

II. Ambiguous Beliefs, Investment Holdup and Incomplete Contracts-A Formal Analysis

Consider a (downstream) buyer B who wishes to purchase a unit of a homogeneous input from an (upstream) seller S. B and S, who are assumed to be risk neutral, may sign a contract at an initial date 0. The contract will specify the terms of trade at date 2, which is when 0 or 1 unit of the input may be produced and traded. After date 0 but before date 1, B and S make relation-specific sunk investments

? E { OH, fL I and a E { UH, UL } respectively. Investments are like effort, in the sense of hav- ing an unverifiable component; and so it is supposed that O3 and a are not contractible. The buyer's valuation, v, and the seller's produc- tion costs, c, are contingent on state of the

world wi realized at date 1; wi is drawn from a finite set Q = { wi }I = 1, and v = v(i ), c - c(wi). The (contingent) surplus at wi is s ()i v (w)i -c (wi). The contingencies are indexed such that s ( w) is (weakly) increasing in i. The vector of joint investments deter- mines the belief (common information to B and S) about the likelihood of each contingent event, represented by a (possibly nonadditive and convex) probability distribution over 252. x(E?1,/, a) is the probability that the event E s Q is realized when the investment profile is (/3, a). hB(f3), hs(u) denote the respective (private) costs of the actions /3 and a. Since investment of one party may affect the likeli- hood of the ex post surplus and hence the ex- pected gains from trade of the other party, there is a potential problem of untapped exter- nalities, and therein lies the genesis of the hold- up problem. The primitives of the model are then described by a tuple (r( 1,6, a), hB(-), hs(), v ( ), c( )). If f: Q -+ R, then f denotes the vector [f(w), ,f (wN)]; a(fi, c) denotes the vector [ir(w11/3, a), ...-, W(W)NI, C)]. Given a contingency wi, let X( wi ) denote the event {Xc QI w E X tj 2 i}. The following as- sumptions on the specification of the model are maintained throughout.

ASSUMPTION 1: hB(/BH) > hB(/3) > 0, hs (UH) > hB (UL) > 0.

ASSUMPTION 2a: wX(X(wi ) 1H, C) ?

1r(X(Wi) I/L, a) for all i E {1, ..., N} and there is an w1n with the property thatS (wn) >

s (wn -1), where the above inequality holds strictly.

ASSUMPTION 2b: wX(X(wi )I1, cH) 2

ir(X(w i ) 3 UL) for all i E {1, ..., N } and there is an wJn with the property that s (W. *) > S (wn* - - ) where the above inequal- ity holds strictly.

The first assumption has it that "H" actions are costlier than "L" actions. Assumption 2a(b) simply says that f6H(cH) stochastically dominates /3(JUL) in the first-order sense.'0

10 Usually stochastic dominance is defined with respect

1214 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

ES (,/, a), defined below, is understood to be the expected net surplus under vertical in- tegration when the profile (,/, a) is chosen:

(1) ES (,l, a) 5E(max{s(wi), O}I , a)

- hB(f3)-hs(f),

(IE denotes the standard expectations operator when -r is additive and the Choquet expecta- tions operator if w is nonadditive.) The ex- pression E&(,/, a) provides a natural way to rank profiles (,/, ar) as first best, " second best, and so on. For instance, (,/*, a*) is afirst-best profile if

(/3*, a*) = arg max { ES (,6, a) .

To keep matters interesting I will restrict at- tention to parameter configurations which en- sure that the expected net surplus from a second-best profile is nonnegative.

It is assumed that parties can write contracts as contingency specific as they choose; i.e., parties may make prices and delivery contin- gent on events in Q in any way they wish.12 A contingent price p (wi ) is the payment by B to S subject to the realization of wi. The price may take a negative value; one may informally interpret the price p (wi ) < 0 as a fine paid by S to B. A contingent delivery rule is a function

: Q -{ O, 1 }, where 6(wi ) = 1 (or 0) indi- cates an agreement for contingent delivery13 (or nondelivery) on date 2. A contract is a list of contingent instructions { (p (wi ),

6 (wM)) }i E { IN } A given contract will im- ply a particular allocation of the surplus be- tween the buyer and seller at each contingency. Correspondingly, a contingent transfer t(wi) p(wi) c(wj)6((w), is S's ex post payoff at wg; the complement s (w)i ) 6 (Oi )-t (i ) goes to B. A contract im- plements an action profile (/6, a) if for all fE {f&3H, fL} and S E {fTH, OJL} the conditions ICB, PCB, ICs, PCS stated below are satisfied.

(2) E(v (wi )6(w) - p(w)i ) 16 )

EWW(iMw(li) - p(avi) Ifi a)

2 hB(3) -hB()

(3) E(v(wj )6(w ) - p(wi) Io a )

- hB(3) 2 0

(4) E(p(wi) - c(wj)6(wj)I/3, a)

-E(p(wi) - c(wj)6(wj)j/3, 5)

2 hs(f)-hs(f-

(5) E(p(wi) - c(wj)6(w(j)I8, cr)

- hs(cr) ? 0.

The conditions ensure that payments obtained in the contract meet the incentive and partici- pation constraints of the buyer and seller, so that they choose ,6 and v. A contract is deemed incomplete if it fails to include instructions for the value of p (wi ) or of 6 (wi ) for at least one contingency wi. The null contract is an ex- treme example of an incomplete contract. It is a contract which does not specify instructions about the terms of trade to be observed in any contingency (or whether any trade is to be conducted at all). It is assumed that if a con- tingency promising positive gains from trade is reached parties engage in trade in spite of

to the payoff or the outcome space. As stated here, instead the reference is to the underlying contingency space. Thus we have to suitably amend the usual definition to accom- modate the fact that contiguous contingencies may yield the same outcome, i.e., the same surplus.

" The reader will observe that this notion of the first best is "vindicated" by the fact that this is the profile that will be chosen if the investment effort were contractible.

2 In particular, this allows for terms of trade being con- tingent on realizations of v ( ) and c ( ) by the simple ex- pedient of making the terms contingent on events such as E(V; C) {wi C QIv(wv ) = Vandc(w) = C}.

'" By taking 6 as a mapping into { 0, I I ex post ran- domization is ruled out. This follows the dominant tradi- tion in the literature on incomplete contracting, see e.g., Hart anid John P4H Moore ( 19QX)-

VOL. 88 NO. 5 MUKERJI: AMBIGUITYAVERSIONAND INCOMPLETE CONTRACTS 1215

the absence of instructions. In such an instance the terms of trade are negotiated ex post. It will be taken as given that any instance of ex post bargaining results in a X (to B), 1 - X (to S) proportional division of the surplus arising from trade. It is assumed that the value of A is commonly known to both parties at date 0.

Consider a contract C and let t&() be the associated transfer rule [where t&( )is suitably extended in accordance with our assumption about the division of surplus at unwritten con- tingencies ]. Denote 1(C) to be the set of pro- files that can be implemented by C. Then the expected payoff from C is:

max { E(s(wi )6(w ) - tc(w)i 1p3, a) (3,a) E 1(C)

+ E(tc(wSi)I/, a) }

[In the above maximand, E(s(wi )6(w6 ) tc(wi)) is B's expected payoff and E(tc(wi)) is S's expected payoff.] I define optimal con- tracts to be Pareto optimal (ex ante). Hence a contract is optimal if there does not exist an- other contract with a greater expected payoff.

The point of writing a contingent contract in this setting is to make payoffs contingent on events in a way that ensures that parties have the right incentives for undertaking the requi- site actions. In other words, the contingent events serve as proxies for the actual (noncon- tractible) actions. Hence, for the exercise to be meaningful at all, the contingency space has to be minimally informative. Condition 1 be- low ensures that there are contingencies which are differentially informative of agents' ac- tions. In other words, for any action there is at least one contingency whose likelihood is dif- ferently affected (at the margin) by this action than by any other. If this were not to hold, contingent events would be completely unin- formative about the actions taken by the par- ties and writing contingent contracts would not be a meaningful exercise. Henceforth, a con- vex nonadditive probability ir( 1I3, ar) will be referred to as an inforned belief if it satisfies Condition 1.

ConditionI (Informnativeness): Let l(ir( I1p, a)) denote the set of additive probability mea- sures in the core of the convex nonadditive

probability function -rr 13,6c a). Suppose lRm

and 7r,, are probability functions in n(irQ 1 H, UH)), -rr is any member of fl(-r(- 136, UH)), and 7rq is any member of I1(i7r( 1i3H, CL)). Then there exists at least one pair of contin- gencies Wk and w1, such that the vectors

(lrm (Wk) - (rr(Wk), lrm(WI) - 7rr( wI) ) and

(lrn (Wk) - 1q( Wk), -r. (WI) -lfq( w1q ) )

are linearly independent. The condition as stated above applies to any

convex nonadditive probability, which in- cludes as a special case the instance when be- liefs are additive (i.e., they are trivially nonadditive). The technical import of the con- dition is simpler to grasp if we were to focus on this special case. In the special case, the condition requires independence between the vectors indicating the marginal effect of 1 and a on the unique probability describing the un- certainty. In general, the condition requires the same of every distribution in the set of prob- abilities consistent with the nonadditive prob- ability that might describe the uncertainty. The condition ensures that there are at least two contingencies whose likelihoods (as described by any of the probability functions consistent with the DM's knowledge) are differently af- fected at the margin by 13H and 0H. The fol- lowing lemma assures us that Condition 1 does the job required of it: if the condition is sat- isfied, then there exist ways of conditioning payments to meet the incentive compatibility requirements of implementing the first best.

LEMMA 1: Suppose wrQ 13,, a) is an in- formed convex nonadditive probability func- tion and that (/3H, UH) is the first-best action profile. Then there will always be a bounded transfer rule, t, which satisfies the incentive compatibility conditions ICB, ICs:

(ICB) E(max {s (wi ), O } - t(wi ) 1l3H, UH)

- E(max{ s(wi), O}

- t(wi ) I 3L, O4-)

2 hB (1H) - hB (3L)

1216 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

(ICs) E(}(wJi ) 16H, H) - EG((wi ) 16H, UL)

2 hs(?H) - hs(cL).

The first proposition proves that if agents' beliefs are not ambiguous, then informative- ness of the contingency space guarantees the existence of a contract that implements the first best. The result is not really new; Steven R. Williams and Roy Radner (1988) and Patrick Legros and Hitoshi Matsushima (1991), for example, arrive at a similar conclusion.

PROPOSITION 1: Suppose ir( 1|, a) is un- ambiguous and informed. Let (13H, cH) be the first-best action profile. Then there exists a contract with an associated bounded transfer rule, t, that implements the first best.

The formal proof appears in the Appendix but the basic argument is straightforward: if, at the margin, the effect of B's action on the likelihood of event I Wk } is greater than its ef- fect on the likelihood of event { w1 } (and the converse is true for S's action vis-'a-vis events { Wk } and { w1 }), then a unit of the contingent surplus assigned to B in the event { Wk I has a relatively greater impact on B's decisions than a unit of contingent surplus assigned to it in the event I w, }; a parallel argument works for S and the events { w, } and { Wk }I. Hence ade- quate incentives can be put in place by re- warding B sufficiently higher at { Wk } than at { w, }, and by rewarding S higher at { w1 } than at { Wk }. Since the expectation operator is ad- ditive, the sum of the agents' expected pay- ments would equal to the net surplus obtainable under vertical integration. Thus the participation constraints may be satisfied by appropriate ex ante transfers. Indeed, Williams and Radner (1988) demonstrate that generi- cally, in the space of probability distributions, there exist contingent transfers that would en- force efficient implementation. In other words, a condition such as 1 will hold generically in the data of the model. An argument invoking mathematical genericity is not necessarily compelling though, since the data of the model is not necessarily generated by "random sam- pling." Arguably, the parameter values are likely to be specific to the institutional setting.

However, bear in mind the relevant institu- tional setting is one of a vertical relationship between two firms operating distinct (even though, complementary) production pro- cesses. As such it is only reasonable to assume that events such as { w1 } and { WI } are bound to exist. (In Example 2, and its verbal descrip- tion in Section I, {I WU} and { us } are such events.) Therefore, Proposition 1 gives us compelling reason to conclude that at least as far as vertical relationships between firms are concerned, if agents' common beliefs were un- ambiguous and there were no direct cost to drafting contingent payments, contracts can achieve efficient implementation. Clearly then, in such a world, mergers cannot better what can be achieved with contracts and fur- thermore, an incomplete contract that does not implement efficiently cannot be the best pos- sible contract. The following Corollaries 1 and 2 summarize these conclusions.

COROLLARY 1: Suppose i(r 1|6, a) is un- ambiguous and informed. Then any contract that does not implement the first best is not an optimal contract.

COROLLARY 2: Suppose ir( 1 6, a) is un- ambiguous and informed. Then the maximum net expected surplus under vertical integration max{ES(/3, ac)}, is no greater than the ex- pected payoff obtainable from an optimal contract.

The next and key proposition shows that contrary to the first result, even if informative events exist, ambiguity-averse agents may not be able to draft contracts that implement the first best. Proposition 2 says that provided the convex nonadditive probability ir is ambigu- ous and satisfies two conditions, there exists a nonempty set of cost and value functions such that the efficient investment cannot be imple- mented with a contract-and this in spite of there being sufficiently informative contracti- ble events. The first of these two conditions, encapsulated in Conditions 2a and 2b, essen- tially rules out cases where the contingency space (labelled according to increasing sur- plus) may be partitioned into two cells, one of which is such that its likelihood is affected (at

VOL. 88 NO. S MUKERJI: AMBIGUITY AVERSION AND INCOMPLETE CONTRACTS 1217

the margin) by only one party (B or S, not both). The final condition, Condition 3, may be interpreted to mean that the belief about any event consisting of two contiguous contingen- cies is ambiguous.14 The role played by the two conditions is explained along with the general intuition for the proof, after the state- ment of the proposition.

A precise statement of Condition 2 and the details of the proof are especially facilitated if we were to define a concept of the "social ben- efit of an action." Define the Social Benefit of the action /3H over the action 13L [denoted SocBen(/3H/fJL)] as E(max { s(w1), O} If H, JH) - E(max{s(w ), O}I,QL, UH). Analo- gously, SocBen(UcH/ICL) E(max { s(wi), O}I /3H, (H) - E(max{s(wi), O} |/3H, CL). Define

'r(XI,8/0, a) 7 (XI 0, a)

- r(XI/#, a), and

7r(XI/0, c/') -r(XI/, a) - r(X1f, 6).

Condition 2a: There does not exist an i Ee {1, ... N} such that

Y S(wk) [ I(X(wk) 1/3H//L, CH) N> k2 i*

- ir(X(wJk +I) I/H//3L, cH)]

+ S(WN)lr( {fwN} I/3HI/L, JH)

= SocBen(/3H/I,L) and

S(wk) [7r(X(wk) I|H, UcHIcL) 0<k<i*

- r(X(wk k+ l)LIQH, cHIcL)]

- SocBen(o-H/IUL).

Condition 2b: There does not exist aj* e {1, N} such that

Y S(wk) [r(X(wk) IPH cYHI cL) N> k j*

- lr (X(wk + 1) H, cHHI/cL)]

+ S(WN)lr( {W)N I 1H1 cYHI cL)

- SocBen(JHIJL) and

Y S(wk) [r(X(Jk) 13H/f3L, JH)

0 < k <1i*

- lr(X(wk+ I ) I/3H//L , UH) ]

-SocBen(/3H//3L).

Condition 3: lr({Wk+1, k}k I k ) >

r(Wk ?. 1 113, c) + r(wk 1 f, a) for all k E 1, ..., N - 11 and for all 13 E {3H, 13L}, of E { 0H, s L } .

PROPOSITION 2: Suppose ir(' 13H, cH),

7r( I/3H, 0L), 7rQ 1I/h, JH), 7r(Q I/L, cL) are informed and ambiguous beliefs, and let (/3H, cH) be the first-best profile. Provided the be- liefs also satisfy Conditions 2a, 2b, and 3, there exist investment cost functions hB (), hs ), and value and cost functions v( ( ) and c (), such that no contract may implement (/3H, cH).

The proposition follows immediately from Lemmas Al, A2, and A3 proved in the Ap- pendix. The simple intuition inspiring the for- mal proof may be stated as follows: If contingent payments are comonotonic (for ex- ample, a proportional split of the surplus) then

14 It seems a reasonable conjecture that Conditions 2 and 3 are generic. If, for instance, Condition 2 fails to hold, even the slightest perturbation of beliefs should restore the condition. A similar understanding can be suggested for Condition 3. In a suitably rich space of measures that in- cludes all convex nonadditive measures, the subspace of beliefs that are strictly additive (over at least some events) would appear to be nongeneric. (N.B., the parametric specification in Example 2 satisfies Conditions 1, 2a, 2b, and 3.)

1218 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

the full incremental social benefit of an agent's action does not get passed on to the agent. Hence, the agent's individual incentive to take the first-best action will be lower than the full marginal benefit of the action. So if the mar- ginal cost of the first-best action is high enough, only noncomonotonic contingent pay- ments could satisfy the relevant incentive con- straints. But with noncomonotonic payments, given Condition 3, the sum of the individual expected payoffs is bound to be less than the expected surplus under vertical integration. Therefore, if the marginal cost of the first-best action is high enough, one may not find con- tingent payments that satisfy both the incentive and participation constraints. How- ever, if Condition 2 were not to hold then it would be possible to design comonotonic con- tingent payoffs that enforce the efficient in- vestment. Basically, such a payoff scheme would partition Q into two cells { w1, ... , w*i and {Wi*+ 1, ..., wNI}: all the surplus in {w1 *.. Wi * } will go to one party and all the incre- mental surplus in the complementary cell [i.e., s(wi*+ 1) - S(Wi*), S(Wi*+2) - s(w1*), ...]

will go to the other party. The argument in Proposition 2 suggests

why incomplete contracts may not be a para- dox in a world with ambiguity aversion since their inefficiency will not be "readily fixa- ble" -complete contracts do not help very much. Proposition 3 shows that the same conditions as in Proposition 2 also imply that there will exist cost and value functions cor- responding to which the null contract is an optimal contract, even though it implements a less than first-best profile. This shows for- mally that ambiguity aversion can rational- ize an "inefficient" incomplete contract even when there exist sufficiently informative events for conditioning contractual pay- ments. As is known from Corollary 1, this is impossible without ambiguity aversion. Be- fore stating the formal result, we look at an example. It will illustrate the arithmetic of how because of ambiguity aversion, a null incomplete contract that can at best imple- ment an inefficient profile can dominate a contract which satisfies the incentive con- straints for implementing the first-best pro- file. (A verbal description of the example appeared in the introduction.)

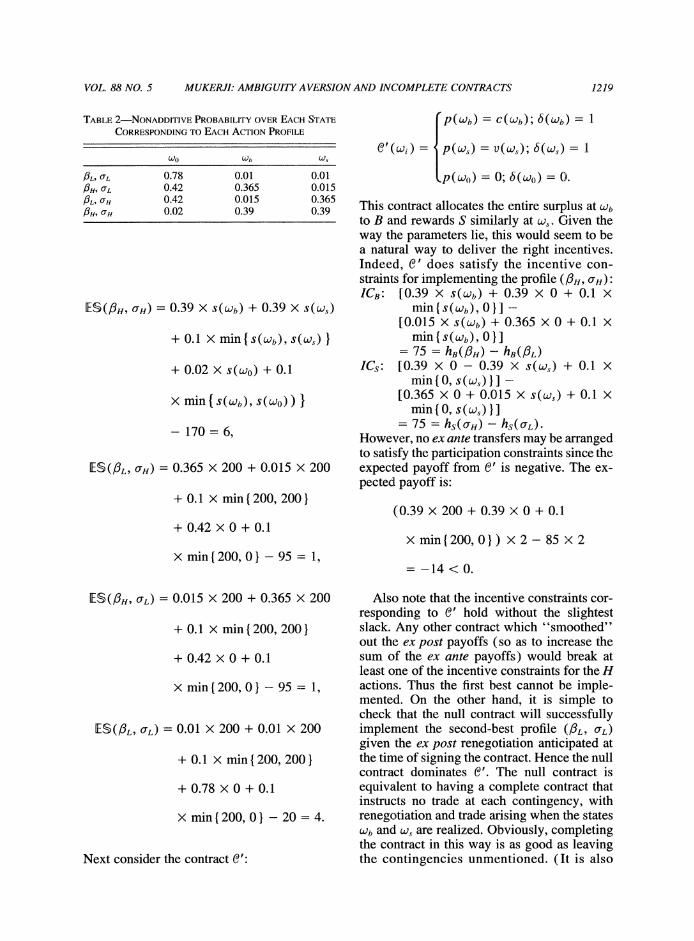

Example 2: Consider two vertically related firms B and S. Q = { go, Wb, w( }; the values of other parameters are as follows:

s(wO) = 0, S(Wb) = s(wU) = 200;

hB(/3L) = 10; hs(cL) = 10, hM(/PH) = 85,

hs(JH) = 85;

T(1L, 07L) = (0.78, 0.01, 0.01),

1T(IH, CrH) = (0.02, 0.39, 0.39);

(fPH, OL) = (0.42, 0.365, 0.015);

T(PL, UH) = (0.42, 0.015, 0.365);

r ({wJb, wJ }I I, ) -r( { b }I/ )

- 7r( [Li, (Us }, a) 0 .1,

7r( { O, wb }I 0,3) ir ( {w O }I/,)

7r( {wb} II/,9) = 0.1,

7f {so, US} I IP, a) - 7(f Wo}s a)

i7r( {w}I IolC) = 0

7r(QIi3, a) = 1; A = 0.5.

The first point to observe is that the essen- tial effect of B's taking the H action is to "shift likelihood" from the low surplus state w0 to the high surplus state (W)b Symmetri- cally, S's H action would "shift likelihood" from the low surplus state w0 to the high sur- plus state w,. This information is summa- rized in Table 2. (N.B., the actions do not affect the "residual probability" over any event; for the events { W,, w, } and { W0, Wb

the residual is constant at 0.1 while it is 0 for two, wU }.)

B and S have a "comparative advantage" in making Wb and wg, respectively, more likely at the margin, as it were. Next note that (63H,

cH) is the first best, and (63L, CL) is the second- best action profile. To confirm this, compare the expected net surplus from the possible ac- tion profiles:

VOL 88 NO. S MUKERJI: AMBIGUITY AVERSION AND INCOMPLETE CONTRACTS 1219

TABLE 2-NONADDITIVE PROBABILITY OVER EACH STATE

CORRESPONDING TO EACH ACTION PROFILE

w0 Wb Ws

f3L, ?L 0.78 0.01 0.01 f3H, aL 0.42 0.365 0.015 f3L, aH 0.42 0.015 0.365 f3H, UH 0.02 0.39 0.39

ES(/3H, UH) = 0.39 X S(Wb) + 0.39 X s(w,)

+ 0.1 X min{S(Wb), s(W) }

+ 0.02 X s(wo) + 0.1

X min {S( Wb), S(WO)) }

- 170 = 6,

IES(/3L, OH) = 0.365 x 200 + 0.015 x 200

+ 0.1 x min{200, 2001

+ 0.42 x 0 + 0.1

X min{200, 01 -95 = 1,

ES(?8H, CL) = 0.015 x 200 + 0.365 x 200

+ 0.1 X min{200, 2001

+ 0.42 X 0 + 0.1

X min{200, 01 -95 = 1,

ES(L, CL) 0.01 X 200 + 0.01 X 200

+ 0.1 X min{200, 2001

+ 0.78 X 0 + 0.1

X min{200, 01 -20 = 4.

Next consider the contract C':

p(Wb) = C(wb); 6(Wb) 1

C'(wi) = p(W,) = v(W); 6(w,) =

p(Wo) = 0; 8(wo) = 0.

This contract allocates the entire surplus at Wb

to B and rewards S similarly at w,. Given the way the parameters lie, this would seem to be a natural way to deliver the right incentives. Indeed, e' does satisfy the incentive con- straints for implementing the profile (f3H, cH):

ICB: [0.39 X S(Wb) + 0.39 X 0 + 0.1 X min{s(Wb), 0}] -

[0.015 X S(Wb) + 0.365 x 0 + 0.1 x min{s(wb), 0}]

= 75 = hB(#H) -- hB(BL)

ICs: [0.39 X 0 - 0.39 X s(w,) - 0.1 X min{0, s(ws)}] --

[0.365 X 0 + 0.015 X s(w,) + 0.1 X min{0, s(w) }]

= 75 = hs(rH) - hs(oL) However, no ex ante transfers may be arranged to satisfy the participation constraints since the expected payoff from e' is negative. The ex- pected payoff is:

(0.39 x 200 + 0.39 x 0 + 0.1

X min{200, 01) X 2- 85 X 2

- -14 < 0.

Also note that the incentive constraints cor- responding to C' hold without the slightest slack. Any other contract which "smoothed" out the ex post payoffs (so as to increase the sum of the ex ante payoffs) would break at least one of the incentive constraints for the H actions. Thus the first best cannot be imple- mented. On the other hand, it is simple to check that the null contract will successfully implement the second-best profile (/6L, TL)

given the ex post renegotiation anticipated at the time of signing the contract. Hence the null contract dominates C'. The null contract is equivalent to having a complete contract that instructs no trade at each contingency, with renegotiation and trade arising when the states Wb and w, are realized. Obviously, completing the contract in this way is as good as leaving the contingencies unmentioned. (It is also

1220 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

possible to mimic the null contract with a com- plete contract by actually instructing formally in the contract an equal split of the surplus and full delivery at all contingencies.)

The following lemma, which is used in proving Proposition 3, shows how incom- plete contracts (especially null contracts) are relatively "robust" to ambiguity aver- sion. Such contracts actually entail a com- onotonic (ex post) payoff scheme across the set of contingencies where the contract (by its silence) leaves payoffs to be determined by ex post negotiation. Compared to con- tracts with noncomonotonic payoffs, these contracts are robust in the sense that the sum of the value of a contract to B and to S is relatively less adversely affected by ambi- guity. Thus if the contingent payoffs from a null contract can satisfy individual incentive constraints and the aggregate participation constraint for a particular profile, it can nec- essarily implement the profile.

LEMMA 2: Suppose the following inequali- ties hold and the expectations are evaluated with respect to a nonadditive probability:

( 6 ) A [E ((max { s (wi ), } | ,

- E(max Is(wi), 0 1 1A, a5)]

2 hB(4) - hB(/3)

(7) (I 1-) [ E (max I s(wi ), ? } 1 a)

-E(max{s(wi), }01, 1]) I

2 hs(&) - hs(oT)

(8) E(max { s(wi ), O} a,)

2 hs(&) + hB(4).

Then a contract will implement the profile (,, a) if it specifies an allocation of ex post surplus in accordance with the uncontingent transfer rulet() t .

PROPOSITION 3: Let (wr*(| I/OH, UH),

1r*(. 16H, OL), 7r ( 16L, UH), 7*(. 16L, CL) be a tuple of ambiguous and informed beliefs that satisfy Conditions 2a, 2b, and 3. Then for each such tuple there exist investment cost functions h*(*), hs( ), and value and cost functions v*( ) and c*(.), such that the null contract is an optimal contract, even though the null contract does not implement the first- best profile.

A gist of the proof would run as follows: By Proposition 2 we are assured that correspond- ing to any belief satisfying Conditions 2 and 3, there is a set of parametric configurations for which there are no contracts that imple- ment the first best. Then it can be shown that for a nonempty subset of the set of such para- metric configurations a null contract will sat- isfy the necessary incentive constraints for implementing a second-best profile. By Lemma 2 it then follows that the null contract will actually implement the second-best pro- file. Since the first-best profile cannot be im- plemented by any contract, the null contract in such cases must be the optimal contract. Since this is true even in the case of an informed belief, the result stands in stark contrast to Cor- ollary 1. It is important to clarify the sense in which this reasoning "predicts" incomplete contracts. Formally, the incomplete contract corresponds to the parties knowing that they will split the surplus ex post according to a state-independent sharing rule. But they could write a complete contract that calls for this ex- plicitly. Hence the argument per se does not show that ambiguity aversion can imply that the optimal contract must be incomplete. Nev- ertheless, the argument does imply that even the smallest transactions costs would make the incomplete contract (strictly) preferable.

Proposition 3 also suggests a rationalization of the elusive connection between supply un- certainty and vertical integration mentioned in the introductory section. Suppose, as seems natural, we interpret "supply uncertainty" to mean the uncertainty about the (realized) price and delivery associated with a supply contract. Could there be circumstances wherein the supply uncertainty accompanying any contract with sufficient incentives for the efficient action is more than what the trans-

VOL. 88 NO. 5 MUKERJI: AMBIG UITY AVERSION AND INCOMPLETE CONTRACTS 1221

acting parties want to bear? In such cases ver- tical integration as a institutional form would have the potential of generating strictly greater value than a contractual transaction. Corollary 2 rules out such circumstances if the agents' beliefs about the uncertainty is unambiguous. However, Proposition 3 allows us to infer that such cases do exist under ambiguity aversion, as Corollary 3 below records. Thus it is the possible ambiguity aversion associated with supply uncertainty which provides the logical link to vertical integration. To see the point a little differently, given that agents perceive the uncertainty to be ambiguous and are ambiguity averse, an "efficient" contractual relationship (because of the "high-powered" nature of the incentive scheme it must embody) would only exacerbate the adverse effect of the uncer- tainty. This "loss of surplus" is avoided by integrating. By monitoring via an administra- tive hierarchy integration makes it possible to deliver adequate incentives without involving contingent payments. Obviously, integration would be the preferred alternative only if the costs of "physical" monitoring is less than the "loss of surplus" that accompanies the use of "financial" monitoring via a contract.

COROLLARY 3: Let { r( 1,6, a) } be a tuple of informed and ambiguous beliefs that satisfy Conditions 2a, 2b, and 3. Then for each such tuple there exist investment costfunctions and value and cost functions such that the maxi- mum expected net surplus under vertical in- tegration, max I ES (/3, aT) }, is strictly greater than the expected payoff obtainable from an optimal contract.

III. Concluding Discussion

The incomplete contracts literature focusing on investment holdup has for the most part maintained the salience of transactions costs in providing the empirical cornerstone for the theory. Since the effect of ambiguity aversion is essentially to reduce the marginal gains from including more details in a contract, under am- biguity aversion even small transactions costs may result in incompleteness. But there is rea- son to think that the role of ambiguity aversion is not merely supplementary to transactions

costs. It is crucial to take into account the na- ture of the uncertainty characterizing the de- cision environment in order to explain the empirical realities about contractual forms and vertical relationships. It is a fact that detailed contingent contracts successfully underpin many business relationships. Where contracts fail or exist as incompletely specified arrange- ments, are situations where uncertainty is rife. Paul L. Joskow ( 1985) notes examples of last- ing long-term contractual relationships be- tween electricity generating plants and mine-mouth coal suppliers. The story of the merger between Fisher Body and GM is an oft- cited example in the incomplete contracts/ver- tical integration literature. It is worth remembering that Fisher and GM did actually successfully transact business via a contract for almost ten years before the merger oc- curred. The reason for the collapse of the con- tract, as explained by Klein et al. ( 1978), was the unprecedented and dramatic demand un- certainty faced by the automobile market in the 1920's. The transactions-cost paradigm cannot explain why detailed, long-term contin- gent contracts thrive in a relatively stable world like that of the coal-electrical utility nexus but not in the more complex uncertain environments. Ambiguity aversion on the other hand would explain this in more intuitive terms.'5'6 Ambiguity aversion also explains

5 A referee has remarked, "the claim ... that [a] trans- actions cost argument cannot rationalize the use of long- term contracts in stable environments but not in highly uncertain ones is debatable ... if the greater uncertainty means more contingencies that must be foreseen, de- scribed, bargained over, and ultimately recognized ...." While admittedly debatable, the claim is definitely defen- sible. It is certainly intuitive to posit a link between the nature of the incumbent uncertainty and the extent of transactions costs. But one is yet to see a formal clarifi- cation of such a story. For instance, it is hard to figure precisely what primitives and principles imply that "greater uncertainty means more contingencies that must be foreseen (etc)." The point is, while ambiguity aversion does manage to convey a precise and coherent account of a link between uncertainty and contracting costs, the trans- actions-costs paradigm is yet to find one.

16 James M. Malcomson and W. Bentley McLeod (1993) explains Joskow contracts by essentially arguing that in such contexts conditioning instructions over a coarse partition of the contingency space is sufficient. This explanation is very consistent with the ambiguity aversion

1222 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

why long-term vertical relationships exist when the input supplied is "standard equip- ment," whereas R&D intensive inputs are typ- ically integrated within the firm. While it may appear that the last observation is fully ex- plained by the notion of "transaction-specific assets," there is reason to think otherwise. Scott E. Masten et al. (1989) report evidence regarding the relative influence of transaction- specific investments in physical and human capital on the pattern of vertical integration us- ing data obtained directly from U.S. auto man- ufacturers. Their results support the propositions that investments in specialized technical know-how have a stronger influence than those in specialized physical capital on the decision to integrate production within the firm. It is well known that government/ defense procurement contracts are typically incompletely specified and prone to renegoti- ation when R&D is a significant component of the good being supplied. But complicated con- tracts running to several thousand pages are quite common with "large" orders of goods not involving significant R&D. That we in- habit a world of incomplete contracts is not necessarily because agents are constrained from conditioning contractual instructions on "finely" described events by the direct costs of envisaging and/or writing down the rele- vant details. Rather, it could simply be because DMs perceive that they have very vague ideas about the likelihood of such events. The un- derstanding that how well the DM thinks he knows the relevant likelihoods explains what events are used to condition contractual in- structions is a novel contribution of the theory of ambiguity aversion to the debate about the foundations of incomplete contracts. The un- derstanding is indeed novel since to a SEU maximizer the quality or accuracy of his belief does not matter.

The explanation of contractual incomplete- ness advanced in this paper turns on the as- sumption that the specific investments are not contractible. At least as long as value and cost are simply functions of the realized contingency (i.e., v = v(w) and c = c(w)], and contingencies

are "informative," the fact that investments are not contractible would not of itself allow "in- efficient" incomplete contracts to be optimal contracts. Further, the requisite "informative- ness" is an empirically valid assumption in the relevant economic context. Suppose instead, that the value and cost are not just functions of the realized contingency, but say, v = v(w; q) and c = c(w; q), where q is a variable measuring the quality or quantity of the input traded. Then it is possible that contractual incompleteness (in the sense of not mentioning trade prices for some events) can arise as a strategic imperative as long as q is also not contractible. This result is demonstrated in B. Douglas Bernheim and Michael D. Whinston (1997). One contribution of the present paper lies in demonstrating how it is possible to rationalize incompleteness even if q were degenerate.

The model presented in this paper assumes firms are risk neutral. There is a dominant tra- dition in economics of modelling firms as such. For the typical "big" firm, pervasive risk spreading ensures that the ownership of the firm's returns is sufficiently diffuse. Thus a firm may act as if its utility is linear in profits; i.e., it only cares about expected profits and may ignore risk completely. When analyzing contractual incompleteness in interfirm rela- tionships, the challenge thus is to explain with- out invoking risk aversion-hence, the assumption of risk neutrality. Notice though that the arguments used to urge the analyst to ignore risk would not work to rule out the ef- fect of ambiguity. While risk spreading en- sures that firms behave as if their utility functions are linear, as we have observed, am- biguity aversion bites in spite of linear utilities.

Finally, I turn my attention to some general theoretical issues raised by the analysis. We have obtained at least a preliminary under- standing of the role of ambiguity aversion in the design of optimal contracts. For instance, we have been alerted to the fact that the trade- off between exacerbating the effect of ambi- guity and the provision of incentives may make it optimal to ignore "information-rich" signals. This is very analogous to the well- researched trade-offs between risk and incentives and between "information rent" and incentives. One suspects that the trade-off associated with ambiguity aversion will have

story: as has been observed earlier (footnote 9), the coarser the partition the less the bite from ambiguity.

VOL. 88 NO. S MUKERJI: AMBIGUITY AVERSION AND INCOMPLETE CONTRACTS 1223

~E ; iQE) ==0.8 1Ec;xEC)=02

El; x(EI) 0.5 E2; x(E2) =S; ( 0 = 0.

~El, ;i1 (E;l) = 0.1 E12 .E2) =0.2

Payoff of actf at E1 f (E12) = 20 f (E2) = 5 TEf (EC) = 0

=f(El)= 10

FIGURE Al. THE SPACE OF EVENTS AND OUTCOMES OFf

as wide-ranging and significant implications as these other trade-offs. For example, the above analysis prompts the question: Can ambiguity aversion force contracts in models of double- sided moral hazard to have linear or even ap- proximately linear sharing rules? This is one open question to be dealt with in future re- search, along with the broader issue of obtain- ing a complete characterization of optimal contracts under ambiguity aversion.

APPENDIX

Example Al: Let the universe Q consist of two complementary events CE and EC. E, in turn, consists of two subevents El and E2 E1 is fur- ther partitioned into E11 and E12. The nonaddi- tive probability function ir which describes the DM's belief is: 7r(cEl) = 0.1; 7r(E12) - 0.2;

r( El) = 0.5; 7r(E2) = 0.2; ir(E) = 0.8; 7r(EC) = 0.2; 7r(cEll U X) = 7r(cEll) + 7r(X) whereXE {IE2 EC, E2U EC};r(E12UX) = rr(E12) + 7r(X) where XE { E2, Ec, T2 U EC}; rr(E1 U CE C } = r(CE1) + r(ME C); ir(E2 U

EC) = ir(E2) + ir(EC); 7r(Q) = 1. The payoffs of the act f are as indicated in Figure Al.

CE,(f ) = f (EC) [r(Q) - ir(E)] + f(E2) [ 7r(E) - 7r(EI)] + f(E11) [7r(EI) -

ir(E12)] + f( E12)1 r(E12) = 8.5. It is instructive to note that an equivalent

computation is:

CE,(f) r( El I )f ( E1 1) 4- ir( E12)f (E12)

+ 7r(E2)f(T2) + 7r(Ec)f(Ec)

+ [ 7r(EI) - {7r(El)

+ ir(E12) I ] min{ f (El,), f (E12) }

+ [ir(E) - ir(cE1) + 7r(E2) }]

X min {f(El1), f(TE12), f(E2) I

= 8.5.

The second computation shows that the Cho- quet method evaluates an act in much the same way as the usual expectation operator, with the amendment that the "residual" measure (viz., the residual at El is [7r(E2) - {ir(TEl) + ir(E12) }]) in any subset of contingencies is

1224 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

"attached" to the contingency bearing the worst consequence of the act in that subset.

PROOF OF LEMMA 1: First I establish some notation. Given a con-

vex nonadditive probability ir( 1,6, a) let H(ir(- 1,6, a)) denote the set of additive prob- abilities in the "core" of 7r( Io,/ u), i.e.,

n (7r( 07s) I {7r A(Q) I *(X)

2: -(XI,8, VX E=2" 1 o

Note that if rx( 1,6, au) is additive then H(7rQ 1/,6, u)) is a singleton, the only element being wr( 16, a) itself. Next, given a payoff function f, f: Q -* R, define the set w( f; /, a) as follows:

7r( f ; /, a)

G~ ~~~~~~w Ti (7 l,9 If(i)*

That is, evaluating the Choquet expectation of f with respect to the nonadditive probability wrQ 1/6, a) is equivalent to evaluating the ex- pectation of f with respect to any additive probability in wr( f; /3, a).

Now, t will solve ICB and ICs if there exists a Xb(Wi I/3 u) e (s6 - t; /3, a) and also a

s (U)i 1u8, a) e w(t; , ca), such that the follow- ing inequalities (Al) and (A2) are satisfied:

(Al) I [VTrb(wi OH, UH) wi C Q2

-'rb(W(i 1/3L, UH) ] [S(wi )6(Li)

t(wi) ] 2 hB(fH)- hB(/3L)

(A2) I Hrs(Wi IP/H, 9 H) wi C Q

-r5s (wi I PH, UL) ] [t(Wi) ]

2 h( UH) - hs ( cL)

Suppose ,(w) I /3, a) E ir(s; /3, a). Since (/3H, CH) is the first best, the inequalities (A3) and (A4) must be true:

(A3) I TO(a)i I OH, CH) (max Is s(i), O }

- hB(fH) hs(CH)

2 T O(Wi /3IL, CH)

x (max{s(wi),} )

hB(f3L)- hs(oH)

(A4) I 'JCO(wi 13H, cH)(max { s(wi), O})

hB (/3H)- hs (UH)

2 :? ko(Li 1O/H9 CL) Wi c Q2

x (max { s(wi), O})

hB(f3H)- hs(o-L)-

Setting 6(-) such that 6(wi) > 0 4 s(wi) 0, and rearranging terms (A3) yields (A5), and (A4) yields (A6):

(AS) I ko JiI E lHQ UH)

-o (w)i If3L, UH) )(s(wGJi )6(wJi ))

2 hB(/3H) - hB(/L)

(A6) M (Wr(i I PH, U7H) wCE Q

- oW(i I /3H, UL) )(S(Wi )6(W ) )

2 hs (9ci) - hs(UL) -

Hence solutions to (Al) and (A2) will exist if we find t that solves (A7) and (A8):

VOL 88 NO. 5 MUKERJI: AMBIGUITY AVERSION AND INCOMPLETE CONTRACTS 1225

(A7) X [ b ((W I OH, UH) - rb (W I L, aH) ]

X [s (wi)6(wi) - t(ii)]

X r ((i I (I/3H, UH)

-o (i 1I/3L, UH) ) (s(w)6(wO ))

(A8) I Ls (wi I /3H, cH) wi C Q2

-S (i I 1fH, UL) ] [t(wi)]

X (Or,(w(i 3H,oJH) wi C Q2

-r (i fOH, JL) ) (S(wi )6(w ) )

Using matrix notation the inequalities (A7) and (A8) may be replaced by (A9):

(A9)

[- bh(Wi IH, OH) + *b(Wi 113L, UH) r 1 (i Nl H H) (H) -((Wi Nl H L) )L)(|(L6-w)

Consider the case where w(- 1,6, a-) is un- ambiguous. It is possible to find a (bounded) t if the vectors- *7b(PH, cTH ) + f,b (13L, cTH)

and*s (PH, C1H) - *s( iH, 1rL) are indepen- dent, which in turn is ensured by Condition 1. Thus the proof is complete for this case.

However, in general, the fact that the sys- tem in (A9) has a bounded solution does not immediately follow from our assumption on independence. The reason is that, when the core of Th(he, cr) is a nonsingleton set, the vectors - (b(H, 0rH) + *b +BL, 0rH) and *s(PH, H) - *s(PBH, cL) are not completely

''exogenous" to the system; they are "en- dogenous" in so far as they depend on t. However, Condition 1 applied in conjunc- tion with a standard fixed-point argument shows that (A9) indeed has a bounded solution.

To proceed with the fixed-point argument I first construct an appropriate mapping in the following three steps.

Step 1: Pick any two elements from fl(w( IH3H, cxH)) and an element each from f(r(e IO3H, UL)) and fl(r( I/3L, UH)). Denote them as ir, ir2, *3, 74, respectively.

Step 2: Consider the solution set to the sys- tem given by (A1O):

(AIO)

[ (ii(w, I/3H,,,H) -o(Wi V13L H) )(s(wi)6(w)) *2 7eET3

E (TO(w,) I13H, UH) - i(wi) l113H, CL) )(s(w, )6(w ) )

Let r = {tlt solves (A10)}. Recall the role of contingencies Wk and w1 as_stated in Con- dition 1. Make a selection t from r such that-(i) = 0, if i * k or i * 1. It follows from Condition 1 that such a selection exists and is unique. Furthermore, t is bounded.

Step 3: Finally consider a set { rI-, t, Wt,

w-xt I where 7l, Ity e_ Er(t; f3H, UH), ir E wr(t; fH9 c(L), r4t E w(t; fL, cH).

Steps 1 and 2 together define a continuous function

"1D: w(r( If3H, JH) ) X rl(wr( If3H, (H))

X H((r I|/3H, JL) )

X H(Or( I /3L, UH) ) -RN

while Step 3 defines a convex-valued upper hemicontinuous correspondence

1226 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

X H(w( I/3H, UH)) X H((- I|/3H, UL))

x H(( 1f1, (H))-

Hence the composition D, - =2 o (I defines a convex-valued upper hemicontinuous cor- respondence from the convex domain

fl(( If3H, UH) ) X H((- I|/3H, (H))

X H((- If3H, (L) ) X H(w(- If3L, (H))

into itself. Kakutani's fixed-point theorem ensures that 4 has a fixed point. Let { w17rI, 7r2t*, r3t*, 7r4t* } be a fixed point of 4. If t* solves (All), then clearly t* satisfies con- ditions required of the transfert [in (Al ) and (A2) ]:

(All)

-7Tj* +4 ] [t(41)

1

*2t* ?*3t )

E I10g;l/H, UH) -W(i If3p, UH) )(s(w)6()() 1

E i(w,(g l13H, 6TH) -o( w, |3H, CL) )(s(w )6(wi) ) J

PROOF OF PROPOSITION 1: Lemma 1 proves that a (bounded) t exists

which satisfies the incentive constraints rele- vant to implementing the first best. Given such a t the expected payoffs to B and S are

E(s(wj)6(wj)- t(Wi) O/H, 90H) hB(OH)

and E(t(Wi ) OpH 90H) hs((JH),

respectively. Since the expectations operator is additive, the sum of the expected payoffs to the two parties is

E(s(wj)6(wj) 3H, UH) hB(lH)- hs(UH)-

(f3H, (UH) is the first best, implying E(s(wi)6(wi)l8H, UH) - hB (f3)- hs(oH) ?::) 0. Hence participation constraints can be taken

care of by a transfer Tr e R transacted when the contract is signed, so long as r satisfies the following conditions:

(PC* ) E(s(wj)6(wj) t(Wi) I#/H (JH) r

-hB (fH) 2 0

(PC*) E(t(wi) If3H, cH) + T- hs(cYH) O0

LEMMA Al: Given that f: Q - R',g:- Q R8 and that w is a convex nonadditive proba- bility function, w: 2-+ [0, 1]; and the label- ling of the state space Q = { wI } N is such thatf(m) > g(wn) =* m > n.

(a) If f and g are comonotonic then E1r(f+ g) = E1r(f) + E1j(g).

(b) Let f and f + g be comonotonic, and suppose that there is Wk + 1, Wk such that (i) and (ii) holds:

(i) g(wk+ l) < g(wk); (ii) W( {W k + I 1) + 7( {W k } ) < lr( { Jk + 1,

Wk 1) -

Then E1(f+ g)> E,(f) + Ej(g).

PROOF: The proof is straightforward and hence

omitted.

LEMMA A2: Assume 1(- I ) satisfies Conditions 2a, 2b, and that (f3h, ch) is thefirst- best action profile. Then there exist hB(.), hs(.) such that for any t which satisfies the incentive compatibility conditions ICB, ICs in Lemma 1, t and the vector [max{s(), O} -t( )] are not comonotonic.

PROOF: The strategy of the proof will be to choose

hs (.) such that hs (oH)-hs ((L,) = SocBen(o-H/ (JL) and then show that if t and s - t are corn- onotonic, B's marginal private benefit from choosing f3H (i.e., E(s - ti PH, UH) - E(s ti 3L, 9H) falls short of SocBen(/H/ /3L). Hence we can choose hB() with the difference hB(fH) -hB(fL) large enough [but less than SocBen(/3H1/3L)IJ, so that if t, s - t are to satisfy (ICB), (ICs), then it must be that t and s - t are not comonotonic.

VOL. 88 NO. 5 MUKERJI: AMBIGUITY AVERSION AND INCOMPLETE CONTRACTS 1227

Fix s( ) such tiat SocBen(aH/aL) > 0 and SocBen(fH/fL) > 0 and consider hs(.) and hB(*) such that (13H, CH) is the first-best action profile. Choose hs(.) such that hs(OH) - hs(crL) =

SocBen(UH/UL). Choose t such that s, t and s -

t are comonotonic and t satisfies ICs. Let is be the smallest value of the contingent

state index i, such that

1l (X(2i + I) )|H. OrH/L) > ?.

Similarly, let is be the highest index i such that

7r (X(Wi ) I,6Hq O'HIUL) :> ?-

Note, Assumption 2b guarantees that the set { wi E Q I is ? i ? is} is not a singleton set.

Claim Al: s(wi) - t(wi ) is the same for all i satisfying the condition is ' i ' is.

PROOF: Since for all i s is, 7r(X(w(i ) I ,H, T'HIL)=

0, it follows that

(A12) 7r (X(WS) |1,6H, O'HIL)

- 7r(X(w!S?+ I) I PH, HI(L) < 0

Since for all i > iS, 7r(X(w )If3H, UH/aL) =

0, it follows that

(A13 ) 7r (X(w --) | ,6Hq U7HIUL)

- 7r(X(w'S-+.) I )JH, 0H/I0L) > 0.

At this point it is useful to recall that E (s -

t1,6, a) may be written as

N-I

? [s(wA) t ) ] X [7r (X(w 1)|6, a)

- ir(X(wi+ 1) ,1, a)]

+ [S(coN) - t(wN) ]7r(wNI,6, a).

Suppose the claim is false. That is, s(wi) - t(wi) is not constant when i varies in the inter- val [is, is]. By comonotonicity of s and s - t, s(wi) - t(wi) is weakly increasing in wi for i such that is ? i ? [S. Hence it must be that s(w)s) - 't(wiS) < s(w)-) -t(- -) Next notice,

(A14) E(s- tI3H, OH) -- E(s- t'IPH, OrL)

is

- , [S(Wi )-t((Ai )] = 1s

X [7r(X(Wi ) |13H, H)

-7T (X(W}i + I ) | PH, UH)]

= 2; [s(wi)-t(wi)]

I =l

i=j5

X [ 7r (X(Wi ) 16H,o /L)

7r (AX(i + IE) (s- I L) )

iS

I [S((Ai) )-i(Ai )] i =!:S

X [ 7T (X(wni ) 1,6Hq UHIUL)

- 7r (X(Wvi + I ) |P UHI U/L ) I

By inspecting the final expression (A14) above, it may be checked that

(A15) E (s- i ,PH Ul)

- E(s s-t |& H, L ) > 0.

To see this, first note that for any i = Z,

N-1

7r ( X( W) 1I6 U f) I [r (X(Wi ) 1,69 )

i z

-7r (X(Si + ) 1,6, 0') I + 7r(WNI f)-

Hence, the Assumption 2b (7r(X(wt ) I PH, Uhl

a,) 2: O) implies

1228 THE AMERICAN ECONOMIC REVIEW DECEMBER 1998

-7r(X((Ai + 1) 1,H, O'HIOL)]2 0-

Then, (A 15) finally follows from the fact that s(wi) - t(wi) is weakly increasing in wi, (A16), (A12), (A13) and that s(w,,) -

t(wis) < s(?i-;-) t(oi5).

But (A15) in turn implies

(A17) E(ti |H, JH)- E(t |PH, OL)

< SocBen(OH/IOL) .

Hence, given that we chose t which satisfies ICs we have arrived at a contradiction.

Claim A2: E(s - tI IH, 0H) - E(s - t6L, (0H) < SocBen (16H/1L).

PROOF: Suppose not, i.e., E(s - tIl6H, CH) - E(s -

tI[AL, (H) = SocBen (/3H/16L). Then by an ar- gument as in Claim Al, one may show that there must be a set of contiguous contingencies {W? ..., wz} where t(wi) is constant when i varies in the closed interval [iB, iB]. Further, Condition 2 (a and b taken together) ensures that the intervals [is, i'] and [iB, iB] overlap; i.e., iB < i and is 'B. Since it has already been established that s(wi - t(w ) is constant when i E is, is , the fact that t(wi) is constant for i E [iB, iB] therefore implies that both s (wi)- t(wz) and t(wi) are constant when i E_[i,_i], where i -min iB, is } and i max { iB, is Thus we are left with the contradictory conclusion that SocBen(16H/16L) = 0 = SocBen(OH/L).

With Claim A2 we have established that if t and s - t are comonotonic, and if hs(OH) -

hs(oL) = SocBen(UH/IL), then we can find hB(.) such that s - t will not satisfy (ICB) if t satisfies (ICs).