Embed Size (px)

Citation preview

Alternatives for Going Public: Evidence from Reverse Takeovers, Self-Underwritten IPOs, and Traditional IPOs∗

This draft: September 25, 2004 Very Preliminary Comments Welcome Kimberly C. Gleason Florida Atlantic University [email protected] Ravi Jain Temple University [email protected] Leonard Rosenthal Bentley College [email protected]

∗ The authors would like to thank the Securities and Exchange Commission’s Division of Corporate Finance (Small Business Policy), Tim Halter of Halter Financial Group, Paul Enright of JOMY Safety Products, Joe Prang of Mentor Capital., Bob Rader of Capital West Securities, the Pink Sheets™ LLC, and Stacy Swanstrum of the National Association of Securities Dealers for their valuable information, experiences, and insights.

Alternatives for Going Public: Evidence from Reverse Takeovers, Self-Underwritten IPOs, and Traditional IPOs

ABSTRACT

We examine the characteristics of firms using reverse takeovers and self-underwritten IPOs as an alternative to the traditional underwritten IPO. We find that at the time they go public, firms that use alternative mechanisms tend to be less profitable than contemporaneously issued IPO firms of comparable size in the same 3 digit SIC code, but they do not exhibit significantly lower balance sheet liquidity or significantly higher distress. However, by two years post going public, they have significantly increased debt and experience declines in profitability and balance sheet liquidity. Furthermore, we find that RT and SU firms are characterized by lower levels of trading liquidity and significantly higher volatility, as measured by the standard deviation of returns. While the combined sample of RT and SU firms have comparable institutional ownership post going public to their control IPO firms, RT firms are characterized by statistically lower institutional ownership than their matches, and while IPO firms experience significant increases in institutional support, those using RTs and SUs experience declines. We also find evidence that firms utilizing alternative going public mechanisms outperform their matched traditional IPO counterparts over longer horizons as indicated by mean and median tests of Sharpe ratios; however, the results for buy and hold returns are mixed.

1

Alternatives for Going Public: Evidence from Reverse Takeovers, Self-Underwritten IPOs, and Traditional IPOs

1. Introduction.

Hundreds of scholarly papers and practitioner articles have examined the issues

surrounding initial public offerings (IPOs), the performance of IPOs, and the governance of IPO

firms. Academic research has uncovered that underwriter reputation matters, that firms leave

money on the table, that IPO firms exhibit poor performance in the longer term, and that

conflicts of interest between investment banking, sell side, and underwriting functions

contributed to the crash of the technology stocks in early 2000. A casual perusal of the academic

literature would lead the reader to believe that an underwritten IPO is the only mechanism

available for going public.

The recent Google IPO, which utilized a Dutch Auction initial public offering, renewed

interest in alternative going-public mechanisms, and has led many in the industry to question

whether the traditional underwritten IPO is the only game in town. Because of the size and

established reputation of Google, its relatively novel variation on the traditional IPO has

generated a great deal of publicity. However, it is common knowledge in the small cap equity

sector that Google is not alone in utilizing a nontraditional approach to going public. What has

been less investigated in the academic literature are alternatives to the traditional IPO process

used by many public firms. Contrary to popular belief, it is not necessary to hire an investment

bank and have the issue underwritten in order to become publicly traded. Firms can, and do,

acquire a public firm in order to go public through a technique known as a “reverse takeover”, or

manage the underwriting of their own IPOs, called a “self-underwritten IPO”.

2

In this paper, we examine the characteristics of firms that use reverse takeovers and self-

underwritten IPOs, and the performance implications of alternative going public strategies

relative to a control sample of traditional underwritten IPOs.

2. Going Public

2.1. Traditional Underwritten IPOs

A great deal is known about the traditional underwritten IPO from both a practitioner and

academic perspective (see, e.g., the comprehensive Ritter and Welch, 2002 review paper).

Generally speaking, the process takes between six months and a year and a half, from the time

that the firm obtains an underwriter(s) and appropriate legal counsel, submits the registration

statement with the SEC (S-1), receives feedback from the SEC following a typical 30 day

review, files amendments to its S-1, carries on with the roadshow, prepares a “litigation proof”

prospectus, and files the prospectus and documents with the SEC and the exchange where the

shares will be listed. Firms choose an investment bank, arguably the one with the best reputation

that they can afford (or which is willing)1, to handle the pricing and marketing of the issue, in the

hopes that they will obtain the best possible price for their shares, get research coverage with a

favorable rating2, observe a consistent increase in trading volume and liquidity, and perform well

post-IPO. The process is time-consuming, sensitive to changes in industry and market-wide

conditions, and financially costly. If market conditions are not appropriate, the IPO may be

postponed or withdrawn. Prior to July 2003, a quiet period of 25 days was required before an 1 Firms doing an IPO should choose bankers who can match the kinds of investors the firm wants to place its shares with rather than just going with a marquis banker. In some cases, choosing a strong regional banker as a lead or co-lead may result in a more successful IPO, whereas using a marquis banker may result in less experienced bankers taking the firm public. 2 Under the Global Brokerage Settlement reached in April 2003, it is now illegal for investment banks to promise research coverage as a quid pro quo for getting the deal. However, some people believe that this practice is now continuing with a wink and a nod (see “Wall Street On the Run: Stock Analysts Are Facing a Far Graver Threat Than New York Attorney General,” Fortune, June 14, 2004).

3

analyst working for an investment bank that managed or co-managed the IPO could issue a

report on the company. The quiet period was extended to 40 days for leads and co-leads and a

25 day quiet period was established for other bankers involved in the deal (see SEC Release No.

34-48252; File No. SR-NASD-2002-154; SR-NYSE-2002-49, July 29, 2003).

The process has been extensively criticized for potential conflicts of interest with

underwriters, allocation of shares to “cronies” of the underwriter, and for the extent to which

money is left on the table. The media frenzy surrounding the recent Google IPO indicated that

many market participants are frustrated with the traditional IPO, but the Google experience also

indicates that the market may not view even minor deviations from tradition favorably.

2.2. Reverse Takeovers

The best known American reverse takeover (RT) was conducted by the now-infamous

corporate offender Bernie Ebbers, who, along with three other investors, formed Long Distance

Discount Service (LDDS) in September of 1983. In May of 1989, LDDS was acquired by

Addvantage Companies (NASDAQ: ADCO) through a reverse takeover to become listed on the

NASDAQ, and, after a protracted acquisition binge, Bernie Ebbers renamed the firm Worldcom.

While not the image that M&A advisors specializing in reverse takeovers like to put forth, like

SUs, many reverse takeovers have a reputation for low quality, or as being “crash and burn”

stocks3. Others, such as Hayes Microcomputer Products, which did an RT in 1997 with

3 Among the 10 largest RT firms in our sample, Struthers Industries Inc. (now Global Marines, Ltd.) personifies the stereotypical RT firm. Even though its stock is virtually worthless, its investor relations website expresses hope: “The shareholders of Struthers, Inc. have suffered mightily over the past few years, both financially and emotionally, yet somehow still clinging to the dream that there were fortunes to be made; while helplessly watching the share price sink to $.0001 and the company itself nearly destroyed. On October 28, 2003 all of that changed...when we decided to take charge of the situation and control our own destiny.” http://www.struthers-inc.com/index.html

4

NASDAQ-listed Access Beyond to go public, were fallen angels that once led their respective

industries; in the late 1970s, Hayes introduced the first PC modem4.

A reverse takeover is a technique that allows a privately held company to obtain a listing

on a public exchange without doing an IPO. The private firm (called the target) is acquired by a

publicly traded firm, referred to as the vehicle, or the “acquirer”, or the shell5. Following the

acquisition, the management of the privately held firm replaces the management of the vehicle,

and the surviving entity is the newly public, previously private “target”. While the target is now

public, it does not raise new equity capital through the transaction, unlike a firm doing an IPO,

whether self-underwritten or not. The motive is only to go public, and to obtain the benefits of

being public.

Thus, the reverse takeover process is a corporate combination (i.e., an acquisition) rather

than an IPO. The private firm management seeks an appropriate public vehicle, arranges for the

public vehicle to make a bid where payment is in stock or cash and stock, completes the

transaction, and files the appropriate forms for a corporate combination with the SEC, as in any

other acquisition. The process typically takes anywhere from a month to six months. The short

completion time relative to the traditional IPO is often mentioned as a motive for using the

reverse takeover. For instance, the Global Sources Investor Relations website provides

information on the reasons for the RT: “In March 2000, Global Sources exchanged 100 percent

of its shares for a 95 percent stake in Fairchild (Bermuda) Ltd. Through this deal, Global Sources

sought a public listing in order to provide an additional source of funds to expand its Internet 4 At the time, the deal was shopped around as though management was doing a favor for the investing public rather than providing a last chance for Hayes following its Chapter 11 reorganization. As stated by Jim Jones, Hayes’ CFO, "This will be a tremendous opportunity for people who have wanted to invest in Hayes" (Atlanta Journal/Constitution, 1997/Troubled Company Reporter http://bankrupt.com/TCR_Public/971229.MBX). Despite the optimism, Hayes Corp. filed Chapter 11 slightly over a year after going public, in large part because of a toxic private placement of preferred stock in a PIPE issue. 5 The term “shell” typically refers to a publicly traded firm that has ceased operations, but that has been “cleaned” of any potential legal liabilities.

5

business. If Global Sources had proceeded with the traditional Initial Public Offering, it would

have taken 2-3 years longer to go public. The reverse merger was the quickest and simplest way

for a public listing.” Managers of reverse takeover firms also have the advantage of knowing

exactly what the valuation will be prior to the going-public transaction.

Many boutique “shell brokers”, who are generally small investment advisors, can be

found that arrange reverse takeovers. They argue that the merits of RTs are that they allow the

firm attempting to go public to avoid the costs of having an investment bank underwrite the

issue, and that firms that use RTs to go public avoid depending on the vagaries of market

sentiment. Evidence also suggests that perhaps the RT process involves less SEC scrutiny than

the IPO process, (and hence, allows less reputable firms to go public). While firms who do RTs

are required to provide financial statements within two weeks of the transaction, they often

simply file an “inability to file” form instead, citing the difficulties of obtaining a comprehensive

set of financial statements so soon after the merger. Indeed, in April of 2004, the SEC voted to

increase supervision and regulation of reverse takeovers, and of requiring private firms using

RTs to go public to provide more extensive financial information than had been required

previously. In doing so, the SEC cited schemes involving insider sales to unsuspecting outside

shareholders (Burns, 2004).

Following reverse takeovers, the managers of the newly public firms often take steps to

“morph” into new corporate entities through repeated acquisitions, product line modifications,

and name changes. For example, one of the firms in our sample, Strategic Solutions, was the

intermediary product in a chain of RTs. The firm began as Trans Am Capital Corp, a small

financial services firms, which morphed into Pacific Animated Imaging Corp, which changed its

name to Strategic Solutions Inc. SSI merged with US Technologies. Strategic Solutions later

6

changed its name to US Technologies, and later to Digital Chainsaw. Digital Chainsaw merged

with both E2Enet and YAZAM and later changed its name back to US Technologies; thus, over

the course of a decade, the firm went from document processing to e-business. Another reverse

takeover combined a mushroom spawn farm (Urbani Truffels) with a satellite components

manufacturer (Sattel Global Networks) to form an exotic foods holding company (Urbani

Holdings).

Unlike an IPO, firms that use reverse takeovers are, in some ways, able to evade the

disclosure requirements and uncertainty of completion inherent in the IPO process. Furthermore,

very little information must be provided about the private firm prior to the acquisition; it is up to

the public vehicle shareholders to decide if they will vote for the combination. Ritter (1987) ties

stock price volatility post-going public to uncertainty about the market value of the firm prior to

going public. Thus, there should be greater uncertainty, and post going public volatility, of

reverse takeover firms than IPOs, whose prospectuses and registration statements require them to

provide comprehensive information.

Only one academic study examines reverse takeovers. In an exploratory study, Gleason et

al (2004) examine a sample of 121 reverse takeovers listed on the New York Stock Exchange

and NASDAQ-AMEX. They find that reverse takeover firms are small, unprofitable, and likely

to fail within 2 years of going public, though announcement returns to the acquirer vehicle firm

are significantly positive. However, they do not examine first day or long run returns from the

perspective of the shareholder of the private firm that uses the reverse takeover to go public, nor

do they compare the performance or characteristics of reverse takeover firms to IPO firms. In a

loosely related study, Brown et. al. (2004) finds that “rollup” IPOs (where several firms in an

7

industry combine into a single entity and go public) underperform as well, and attribute poor

performance to agency problems.

2.3. Self-Underwritten IPOs

Self-underwritten IPOs (SUs) are initial public offerings (typically best-efforts, though a

handful are all-or-none offerings) where the firm doing the issue underwrites its own shares.

While typically associated with Small Corporate Offering Registration (SCOR) offerings, which

are limited to under $1 million, or with unregistered Rule 504 offerings, self-underwritten IPOs

are registered equity securities that are not limited to qualified institutional buyers for purchase.

Like traditional IPO firms, SU companies can list on the Pink Sheets ™, the OTCBB, the

NASDAQ-AMEX, or the NYSE6. Though most end up on the Pink Sheets™ or the OTCBB,

several have successfully listed their stock on the NASDAQ. Some start off trading on the less

liquid platforms, with the hopes of moving up to the NASDAQ. Like self-underwritten IPOs,

some seasoned offerings, known as “Direct Public Offerings” are also not underwritten by an

investment bank, but unlike the firms in the sample, the DPO issuers are not listed on any

exchange; management of the firm markets the newly issued stock directly to private investors,

typically with the intention of later listing the stock if the equity investment pays off7.

In a true self-underwritten issue, firms do not have an investment bank manage the new

issue; the firm’s management acts as broker-dealer for the IPO itself, and often holds roadshows

6 At one point in the “internet revolution”, it was thought that improvements in information technology might lead to changes in the entire securities issuance process that would improve efficiency and accessibility to a broader base of investors. To that end, web-based, nontraditional lead-manager systems were developed by W.R. Hambrecht and E*Offering (which later became Wit). However, few IPOs were ever brought forward through these mechanisms, with the best-known offering being Peet’s Coffee and Tea (Lewis, 2001). 7 One such firm is JOMY, a Colorado safety equipment firm that raised $1 million through a direct public offering in 2003, which was widely followed by the local Boulder business press. The issue, which offered 27% of the company for outside ownership, was marketed by the CEO to the local community and was oversubscribed at $1 per share.

8

on the company’s premises8. Managers determine the value of the company within limits, and

potential investors decide if the price is acceptable. The tradeoffs involved are clear; the firm

does not get the benefit of underwriter marketing to institutional investors, aftermarket

stabilization, or certification, as described by Gompers and Lerner (1999), but the firm avoids

many of the costs and the uncertainty inherent in obtaining a firm commitment from an

investment bank as in a traditional underwritten issue9.

The opportunity costs of having management market the issue rather than an investment

bank are nontrivial. A tremendous amount of managerial resources must be dedicated to

obtaining retail buyer interest (though management may be able to obtain a higher valuation than

what would be possible with an issue aggressively marketed to more sophisticated institutional

investors). As described by Lipman (2001), some SU firms are able to interest local and regional

broker-dealers in providing IPO marketing services to assist managers, but investment banks

typically do not provide marketing services unless they handle the entire underwriting process.

8 The executives of the firm must meet certain qualifications in order to act as broker-dealer (though many appear to obtain exemptions), as described in Corporate RoadShow Dot Com’s 424A: “Mr. Ferraro, the CEO, will be the person responsible for the sales of securities on behalf of CRS and that he will rely on the safe harbor from broker dealer registration set out in Rule 3a4-1 under the Securities Exchange Act of 1934. Mr. Ferraro meets each of the qualifications set forth in such rule as follows: (i) he is not subject to any statutory disqualification; (ii) he is not compensated in connection with his participation by the payment of commissions or other remuneration based either directly or indirectly on transactions in securities; (iii) he is not at the time of his participation an associated person of a broker or dealer; and (iv) he will restrict his participation with respect to such sales to the following activities: (A) preparing any written communication or delivering such communication through the mails or other means that does not involve oral solicitation by the associated person of a potential purchaser; provided, however, that the content of such communication is approved by a partner, officer or director of the issuer; (B) responding to inquiries of a potential purchaser in a communication initiated by the potential purchaser; provided, however, that the content of such responses are limited to information contained in a registration statement filed under the Securities Act of 1933 or other offering document; or (C) Performing ministerial and clerical work involved in effecting any transaction.” 9 Firms going public through SUs still pay underwriting and registration fees, they simply do not pay them to an investment bank (and often who exactly such fees are paid to is not addressed in the prospectus). For example, SmartMetric Inc. issued its prospectus on 9/8/2004, and its SB-2 indicates that its fees associated with issuance and distribution of the new securities amounted to $147,927.43, including legal and accounting costs, printing and engraving, blue sky qualification fees, and transfer agent fees. It also reports underwriting costs ranging between $222,957 and $747,957. Many SU firms report having no underwriting expenses whatsoever.

9

SUs are not uncommon in practitioner circles, but have not been addressed in the

academic literature, with one exception: Muscarella and Vetsuypens (1989), examine a small

subsample of self-underwritten IPOs with a sample ending in the 1980s, where a “self-

underwritten” deal is defined as one where firms go public with or without the support of

investment banks in valuing and marketing the issues, but which have no underwriter.

Muscarella and Vetsuypens (1989) examine only investment bank IPOs; they find that self-

underwritten investment bank IPOs significantly underperform a control sample of investment

bank IPOs underwritten by an outside group. While not a study of self-underwritten IPOs per se,

Chen and Lin (1996) find similar results, using a sample of investment companies whose

underwriters own at least 3% of the firm’s stock at the time of the IPO. These results suggest the

outside certification involved in the IPO process is important.

Despite lacking investment bank/underwriter certification, self-underwritten IPOs are still

required to file all necessary documentation that any ordinary IPO would, including a prospectus.

Like ordinary IPOs, they are subject to listing and disclosure requirements, lockup period

constraints on insider sales, and corporate governance requirements of their respective

exchanges. However, as noted in the “Risk Factors” section of the Friday Night Entertainment

Corporation 2004 Prospectus, asymmetric information is likely to be higher for SUs than IPOs:

“…This offering is being self-underwritten by our officers and directors, and potential investors

should give careful consideration to all aspects of this offering before any investment is made. In

the absence of an underwriter, no due diligence examination has been performed in conjunction

with this offering such as would have been performed in an underwritten offering.”

In the popular press, SUs are considered speculative. For example, a Wall Street Journal

article notes that SUs “stand a good chance of never seeing the light of day” (Hennessey,

10

2004)10. They are generally viewed as firms that would not be able to get an investment bank to

underwrite the issue (though anecdotal evidence from the 1990’s IPO market suggests that by

and large, firms that wanted to go public were able to find underwriters). Indeed, many firms

who file prospectuses cannot realistically expect to ever meet the listing and disclosure

requirements of even the Bulletin Board, and their prospectuses list risk factors such as

management’s and accountant’s doubts about the firms’ prospects as a going concern, the fact

that the CEO may have to resign pending the outcome of an SEC investigation for securities

fraud11, the problem of the firm having no employees, doubts that a product will ever result from

R&D, no operating history, and the fact that the executive responsible for sales has no industry

experience whatsoever12.

The lack of a minimum number of shares that must be sold in SU offerings, as opposed to

the traditional IPO, makes them risky for investors as well. Managers who potentially have

conflicts of interest in marketing the shares can simply offer the shares, take the funds, and

obtain personal rents by claiming that sufficient funds were not raised to operationalize the

10 SUs often appear in the popular press as the butt of jokes as “do-it-yourself” IPOs done by bogus companies. See, e.g., the satire website http://www.anvari.org/fortune/Humorix_Stories/1745.html. 11 As stated in Human Biosystem’s 6/25/2003 prospectus: “Primarily as a result of these recurring losses, our independent certified public accountants modified their report on our December 31, 2002 financial statements to include an uncertainty paragraph wherein they expressed substantial doubt about our ability to continue as a going concern.” The next risk factor described in the prospectus involves securities fraud charges against the CEO: “On August 7, 2002, the United States Attorney for the Eastern District of New York and the Securities and Exchange Commission announced that they were bringing securities fraud charges against Harry Masuda, our Chief Executive Officer, for allegedly paying an unregistered broker an undisclosed commission in a 1999 and 2000 private placement. The allegations generally charge Mr. Masuda with the failure to adequately disclose to investors in this private placement a commission agreement with Larry Bryant, an unlicensed broker-dealer. Remedies sought in these proceedings include criminal penalties and a bar from service as an officer or director of a publicly-traded company … there can be no assurance that Mr. Masuda will be able to continue to serve as our Chief Executive Officer in the event that the Securities and Exchange Commission receives the remedies that it seeks.” 12 As stated in Coffee Pacifica’s August 8, 2003 424b2, “Our ability to implement the marketing and sales strategy is partially dependent on our employee, Brooks Farrell's, ability to increase awareness and recognition of Papua New Guinea grown green bean coffee in United States. Brooks Farrell lacks coffee industry experience and may have difficulty selling the Papua New Guinea grown green bean coffee.” Similar concerns are expressed in Grafix2Go’s 6/25/2003 prospectus: “We will rely heavily on Brandon Stillman and Jared Stillman to develop our business. While Jared and Brandon have some limited experience in computer programming and graphics, they have virtually no business and sales experience. This lack of experience further increases the risk that they will be unable to successfully develop our business.”

11

business plan outlined in the prospectus. As indicated in Coffee Pacifica’s August 8, 2003

424b2, “There is no minimum number of shares that must be sold in this offering, even if we

raise a nominal amount of money. Any money we receive will be immediately available for use

by us. We may not raise enough money to implement our business plan. No money will be

refunded to investors under any circumstances. As a result, investors may lose their entire

investment.”

At one time, during the IPO wave of the 1990s, self-underwritten IPOs were considered

the wave of the future. Interest reached a peak in 1999, when the relatively well-known firm

LinuxOne planned to do a self-underwritten IPO onto the NASDAQ, but ended up hiring an

investment bank, Capital West Securities, to underwrite the issue13.

In a sense, SUs provide a natural laboratory for investigating whether underwriters make

a difference. We examine whether SUs are, in fact, different in terms of operating characteristics

from firms whose IPOs are underwritten. We anticipate finding that self-underwritten IPOs face

higher volatility and lower performance outcomes than underwritten IPOs.

3. Post-IPO Performance

A great deal of evidence exists demonstrating that firms underperform following an IPO,

using a variety of measurement techniques (see, e.g., Ritter, 1991; Loughran and Ritter, 1995;

Gompers and Lerner, 2003; Levis, 1993; Lee, Taylor, and Walter, 1999; Keloharju, 1993). Ritter

(1991) finds that IPO firms significantly underperform non-IPO firms post IPO, and studies of

13 Both the decision to do the self-underwritten IPO and the decision to employ Capital West Securities baffled the investment community. Red Hat, a firm in the same industry, had hired prestigious Goldman Sachs to underwrite its IPO, indicating that LinuxOne could have hired a higher profile investment bank with more experience than Capital West, which had only underwritten 10 previous IPOs.

12

internet IPOs (see, e.g., Ljungqvist and Wilhelm, 2003) provide an even more blistering critique

of long horizon performance in the late 1990s.

However, whether poor post-IPO performance is merely an artifact of the broader issue

of low returns to small, low book to market firms, the use of buy and hold rather than calendar

time returns, or a function of the particular returns generating process used in the analysis, is a

matter of ongoing empirical debate (see, e.g., Brav and Gompers, 1997; Brav, Gzecy, and

Gompers, 2000). Furthermore, Purnanandam and Swaminathan (2004) argue that the evidence

from analysis of multiples indicates that high offer price-to-value IPOs experience greater price

declines than peers; the market seems to get carried away with overly optimistic growth

forecasts, and engages in systematic misvaluation.

If IPO firms do underperform post-IPO, then sentiment and market timing models stand

ready to explain the performance (see, e.g., Ritter, 1991; Loughran and Ritter, 2000; Hirshleifer,

2001; Baker and Wurgler, 2000; Ljungqvist, Nanda, and Singh, 2002; and Loughran, Ritter, and

Rydqvist, 1994). Carter et. al. (1998) indicates that underwriter reputation is a significant

determinant of long run performance post IPO. Furthermore, investors time their purchases to

coincide with periods of optimism, which bids up the price of the newly public firms, but which

results in sell-offs when the street becomes disenfranchised. Ben Dor (2004) argues that

institutional investor involvement in new IPOs is a leading indicator of market enfranchisement,

and, having better information than uninformed individual investors, institutions should

anticipate investor sentiment and capitalize on it. Consistent with this hypothesis, he shows that

higher institutional investor ownership shortly after the IPO is associated with higher subsequent

returns.

13

If traditional underwritten IPOs underperform, despite efforts by underwriters to properly

price and market the security issue (for which they are usually paid, approximately, 7% of the

proceeds), then what might one expect from the performance of firms using alternative

techniques to go public? At first glance, it might appear that it would be more difficult for

reverse takeover and self-underwritten IPOs to obtain institutional support or analyst coverage,

given that there is no underwriter to promote the issue. It may be the case that such firms are

poor performers who could not get an investment bank to risk reputational capital by

underwriting their offerings. Anecdotally, it appears to be the case that the scrutiny of the IPO

process is more extensive than for corporate combinations. If so, one would expect the popular

conception of reverse takeovers to be true, that they may turn out to be shareholder rip-offs. Self-

underwritten IPOs may save the 7% required for underwriting, but they also would be expected

to suffer from the consequences of not having the marketing backup provided by the underwriter,

and from the overextension of managerial resources involved in marketing the stock to retail

buyers. Both self-underwritten IPOs and RTs face the disadvantage of not obtaining the publicity

and visibility inherent in underwritten IPOs. RTs also differ from SUs and traditional IPOs in

that if the shares are determined to be marginable, shares of RTs can be shorted without lockup

period constraints, whereas the shares of SUs and traditional underwritten IPOs cannot be.

We first attempt to examine whether firms that use nontraditional going public

mechanisms differ from those that choose the traditional underwritten IPO. We then examine the

first day returns, long-term performance, volatility, and liquidity of firms that use nontraditional

approaches following their going public transactions to see whether they over or underperform

traditional IPOs. We document the ability of RTs and SUs to obtain institutional investor

14

support after they go public. Finally, we examine the factors that affect 12 month control-

adjusted buy and hold returns for firms using RTs or SUs to go public.

4. Data

Our data collection efforts were extremely intensive because it involved obtaining a

sample of transactions that are not widely or accurately covered by traditional data vendors. We

obtained our initial sample of reverse takeovers from Securities Data Corporation’s (SDC)

International Mergers and Acquisition files. However, in the process of examining the proxy

statements of firms reported to be reverse takeover firms, we found that SDC often incorrectly

categorizes rollups and other forms of industry consolidation as RTs, and improperly categorizes

many ordinary IPOs as RTs. Hence, we engaged in an extensive search for other firms that had

gone public using reverse takeovers. Our final sample includes 127 confirmed reverse takeovers

to go public and which were initially listed on the New York, American, or NASDAQ stock

exchanges between 1986 and 2002. All transactions were confirmed through Lexis Nexis

searches as well as the financial statements of the public and private firms involved in the deals.

Self-underwritten IPOs were even more difficult to track down and verify. Unlike

traditional underwritten IPOs, Securities Data Corporation does not cover SUs. Hence, we

utilized word searches in Edgar Online and online news searches to identify self-underwritten

IPOs involving public offerings registered with the SEC, which were listed on the New York,

American, or NASDAQ stock exchanges. The exchange listing screen removed firms that did

Direct Public Offers over the internet (such as Spring Street Brewing Company), Rule 506

offerings only available to qualified institutional buyers, and Regulation A and Public Rule

504/SCOR offerings resulting in a bulletin board listing for which no Compustat data was

15

available14. While these issues are not covered by traditional data sources, such as SDC, the SEC

and Edgar’s IPO Express track them. After obtaining the initial sample, we verified that the IPOs

were self-underwritten from their registration statements and from personal contact with the

SEC. Our final sample consists of 53 self-underwritten IPOs, which traded on the NASDAQ-

AMEX or NYSE between 1991 and 2003; however, we have CRSP data for only 22 firms.

Finally, we obtained our control sample of traditional underwritten IPOs from Securities

Data Corporation’s Global New Issues. We obtained all original IPOs in the 12-month period

prior to the reverse takeover or self underwriting, and selected the closest match on industry and

assets.

Our sample period covers 1986 to 2003. Sample breakdown by year and industry is

shown in Table 1.

[Table 1 About Here]

We obtained stock price, returns, and volume data from CRSP and accounting data from

Standard and Poor’s Compustat Research Insights. We obtained institutional ownership data for

all firms from CDA/Spectrum. Finally, we obtained characteristics on the transactions from the

proxy statements for the reverse takeovers, the registration statements for the self-underwritten

IPOs, and SDC Global New Issues database for the underwritten IPO control sample.

5. Methodology

We examine the characteristics of firms selecting into either an RT or SU (=1), or a

traditional underwritten IPO (=0) using a logit regression analysis:

14 Given the size of the issues, it is possible that some of the sample SUs would have preferred to use the Regulation A offering, except that development stage firms with no business plans are prohibited under Reg A, as are felons, under the Rule 262 “bad boy” provision.

16

p(RT or SU) = α + β1SIZE + β2Z + β3CASH + β4PROFIT + β5LEVERAGE (1)

where SIZE is proxied by the log of assets (or sales) at the time of the going public transaction,

Altman’s Z is a distress proxy, CASH, a proxy for balance sheet liquidity, is the ratio of cash and

equivalents to total asset, PROFIT, a profitability measure, is proxied by ROA or ROE in

different specifications, and LEVERAGE is the ratio of debt to total assets.

We also examine the long run performance of firms utilizing self-underwritten IPOs and

reverse takeovers relative to a control sample of traditional underwritten IPOs. We calculate

buy-and-hold returns (BHRs) for the sample RT and SU firms and for the matched IPO firms

using daily returns starting the day after the RT or SU event date until the end of the holding

period (which is either 6, 12, 18, 24, or 36 months) or the delisting date, whichever is earlier.

The buy-and-hold abnormal return (BHAR) is calculated as the difference between the buy-and-

hold return of the RT or SU firm and the buy-and-hold return of the matched IPO firm.

We use both equal-weighted and value-weighted (the firms’ market capitalization at the

time of the RT or SU event are used as weights) average holding period buy and hold returns to

compare the long-run performance of the RT and SU sample relative to the control sample of

IPOs. The average holding period buy and hold return across a sample of N firms is calculated

as:

17

earlier is whicheverdate, delisting or the istock for period holding theof endday tover istock return to the

return periodholding average theformingin weight si'stock

)2(1001)1(21

===

⎥⎥⎦

⎤

⎢⎢⎣

⎡−+= ∏∑

==

i

it

i

Ti

tit

N

ii

TR

where

XRBHR

ω

ω

As an alternative to the BHR approach, we also examine the performance of RTs and

SUs relative to their matched IPOs by using Sharpe Ratios computed over the corresponding 6,

12, 18, 24, and 36 month period post going public.

Following Ben Dor (2004), we examine whether institutional investor participation

predicts returns after controlling for important firm characteristics:

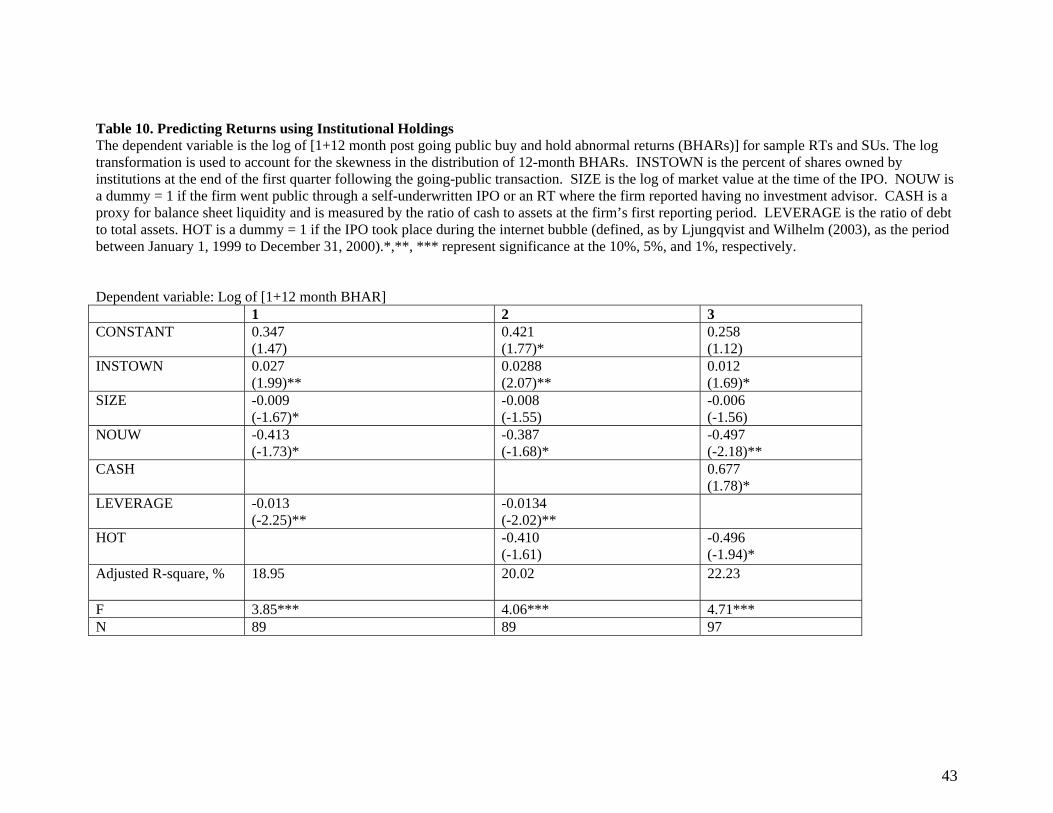

Log (1 + BHAR12) = α + β1 INSTOWN + β2 SIZE + β3 NOUW + β4 CASH

+ β5 LEVERAGE + β6 HOT (3)

The log transformation is used to account for the skewness in the distribution of 12-month

BHARs. INSTOWN is the percent of shares owned by institutions at the end of the first quarter

following the going-public transaction. SIZE is the log of market value at the time of the IPO.

NOUW is a dummy = 1 if the firm went public through a self-underwritten IPO or an RT where

the firm reported having no investment advisor. CASH is a proxy for balance sheet liquidity and

is measured by the ratio of cash to assets at the firm’s first reporting period. LEVERAGE is the

ratio of debt to total assets. HOT is a dummy = 1 if the IPO took place during the internet bubble

(defined, as by Ljungqvist and Wilhelm (2003), as the period between January 1, 1999 to

December 31, 2000). All specifications incorporate White’s correction for heteroscedasticity.

18

6. Results

6.1. Do Firms Using Alternatives to IPOs Differ from IPOs?

6.1.1. Univariate Statistics

We first examine whether the characteristics of RT, SU, and matched IPO firms differ

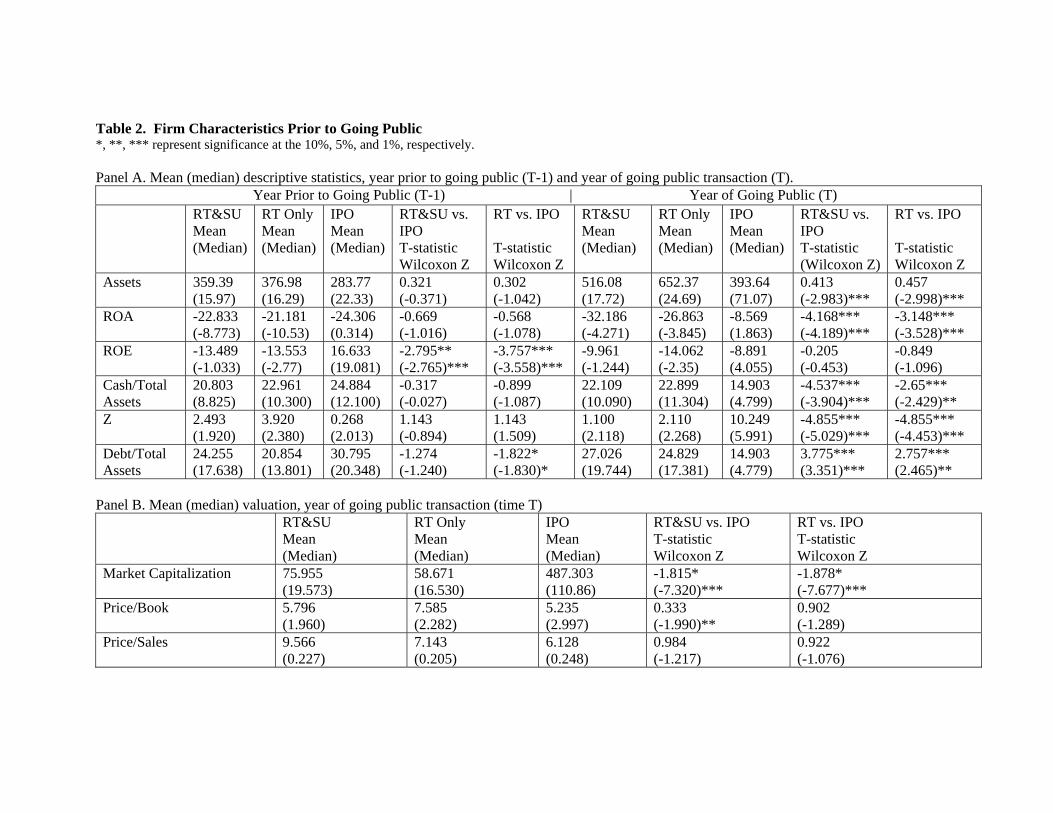

significantly the year prior to the IPO. The results of univariate tests are shown in Table 2.

[Table 2 About Here]

Panel A provides mean and median values for the operating characteristics of RT, SU,

and IPO firms, for the year prior to going public15, and for the year of the going private

transaction. Anecdotal evidence suggests that firms that use alternatives to the traditional

underwritten IPO do so because they are so small, or that their operating characteristics are so

poor that either the firm cannot afford to have an investment bank underwrite the issue, or the

firm cannot find an investment bank to underwrite the issue at all. Table 2, which presents tests

of differences in means and medians, indicates that operationally, firms using RTs or SUs to go

public do not differ significantly from their IPO matches the year prior to going private16. All

three sets of firms are small, with mean (median) assets of $359.39 ($15.97) million for RTs and

SUs, and $282.77 ($22.33) million for IPOs. IPOs were size matched to RTs and SUs for the

year prior to the transaction, so it is not surprising that the mean size is not significantly

different.

Similarly, RT and SU firms do not, by and large, appear to differ from matched IPO

firms in terms of profitability, as measured by ROA and ROE, in the year prior to going public.

15 For RT firms, the year prior data is provided for the private firm that goes public via a reverse takeover. 16 Nonparametric Kolmogorov-Smirnov tests indicate that assets, ROA, ROE, Cash to Assets, Debt to Assets, and Altman’s Z are not normally distributed. Hence, we provide nonparametric as well as parametric tests throughout the paper. In most cases, the results of the nonparametric tests support the results of the parametric tests.

19

Mean figures illustrate that all three groups are unprofitable from an accounting perspective, as

indicated by negative ROA and ROE. Statistically, only RTs appear to be significantly less

profitable in terms of mean and median ROE than their control IPOs. Significant differences

appear in the year of the going private transaction, however, and firms using RTs and SUs

exhibit significantly lower profitability ratios in the years they go public.

Table 2 also provides proxies for leverage (debt/total assets), liquidity (cash and

equivalents/total assets), and distress (Altman’s Z). While RTs and SUs have cash and

equivalents comparable to their IPO matches in the year prior to going public, they exhibit

significantly lower balance sheet liquidity in the year that they go public. Furthermore, RT and

SU firms have higher leverage and are significantly more distressed (as indicated by lower

Altman’s Zs) than control IPOs the year they go public.

Table 2, Panel B provides information on market value and relative valuation in the year

of the going public transaction. We find that at the time they go public, RT and SU firms have

significantly lower market capitalization than control firms. However, their price to book and

price to sales multiples are comparable to control IPOs.

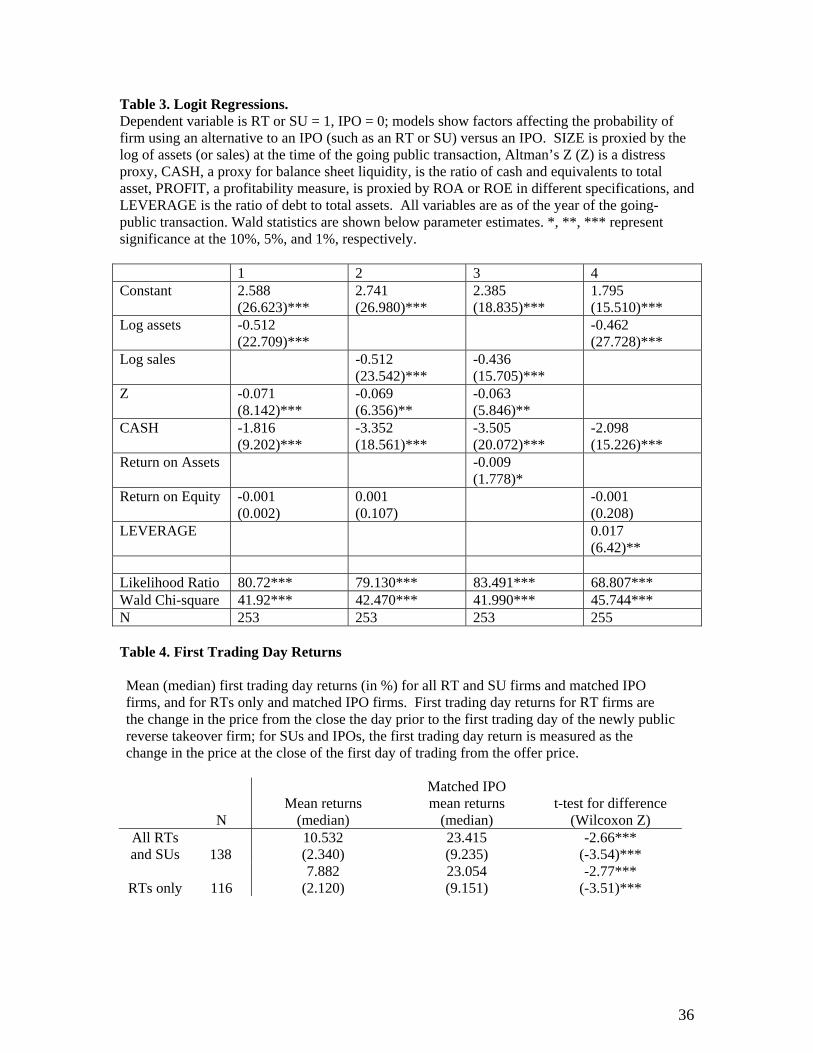

6.1.2. Logit Analysis

We next examine differences in characteristics of firms using SUs and RTs in a

multivariate framework. Table 3 provides the results of logit regressions, where the dependent

variable = 1 if the firm utilized an SU or RT to go public. We examine whether firms using

alternatives to IPOs differed from IPOs in terms of leverage, balance sheet liquidity, profitability,

and size (log of assets or sales).

[Table 3 About Here]

20

Table 3 confirms the results shown in Table 2 in a multivariate framework. Firms that use

RTs or SUs rather than IPOs tend to be smaller (as indicated by the significance of the negative

coefficient of the log of assets or sales). They also tend to exhibit higher distress, as proxied by

Altman’s Z; firms with higher Zs experience lower levels of distress, and the negative coefficient

of Altman’s Z indicates that firms with lower levels of distress are less likely to do RTs or SUs

than IPOs. The negative coefficient on the profitability measures, ROA and ROE, indicate that

more profitable firms are more likely to use IPOs than alternative measures. Finally, RTs and

SUs are associated with significantly higher levels of debt.

6.2. Do Firms Using Alternatives to Traditional IPOs Underperform Traditional IPOs?

6.2.1. First Trading Day Returns

In order to get an idea of investor sentiment and underpricing, we examine first trading

day returns. First trading day returns for RT firms are the change in the price from the close the

day prior to the first trading day of the newly public reverse takeover firm; for SUs and IPOs, the

first trading day return is measured as the change in the price at the close of the first day of

trading from the offer price. Table 4 provides first day trading returns for sample and control

firms.

[Table 4 About Here]

The mean (median) first trading day return for the combined RT and SU sample is

10.532% (2.340%), and for the RT sample is 7.882% (2.120%). By contrast, the matched

underwritten IPO firms corresponding to these two samples have a mean (median) first trading

day return of 23.415% (9.235%) and 23.054% (9.151%), respectively. The test statistics indicate

21

that the first trading day returns for both the combined RT and SU sample and for the RT only

sample are significantly lower than for their matched underwritten IPO counterparts.

It appears that market sentiment favored the underwritten IPO sample, or alternatively,

that the underwritten IPO sample experienced greater underpricing. Also, on average, SU firms

realize higher first trading day returns than RT firms as can be inferred from the larger first

trading day return for the combined RT and SU sample relative to the RT only sample. Two

factors may account for the difference in first trading returns for RTs and SUs. First, the RT is

an anticipated event. Part of the first day return may be captured in the return to the public

vehicle firm when the announcement of the merger is made to the public. Gleason et. al. (2004)

find that the (-1,0) mean (median) announcement returns to the shareholders of the public vehicle

are 15.60% (13.02%). Hence, the cash flow implications may have been partly impounded into

the price before the merger was actually completed and the private firm began trading.

Secondly, from the investor’s perspective, there is more certainty involved with the reverse

takeover than with the IPO. The value of the acquisition is known in advance in the case of the

RT, whereas for the IPO firms, the offer price is not known until the day of trading.

6.2.2. Market Performance

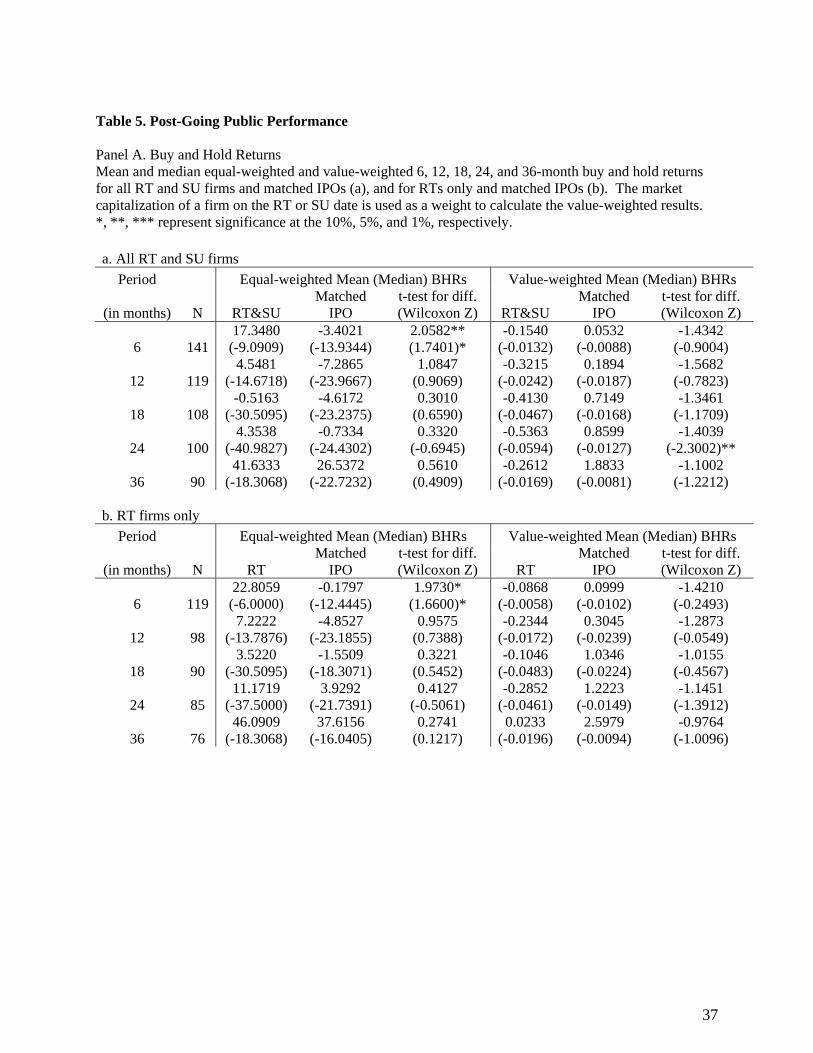

Table 5 provides buy and hold returns and Sharpe ratios for sample and control firms for

the 6, 12, 18, 24, and 36 month periods following their going private transactions.

[Table 5 About Here]

In general, the results in panel A suggest that long-run equal-weighted and value-

weighted average BHRs for the sample RT and SU firms are similar to the corresponding

average BHRs for matched IPO firms. We also compare median BHRs of the two samples

22

because the distribution of BHRs for both the RT and SU firms and the matched IPOs is

characterized by skewness (other studies, such as Purnandam and Swaminathan, 2004, have also

documented that long-run IPO returns are not normally distributed).

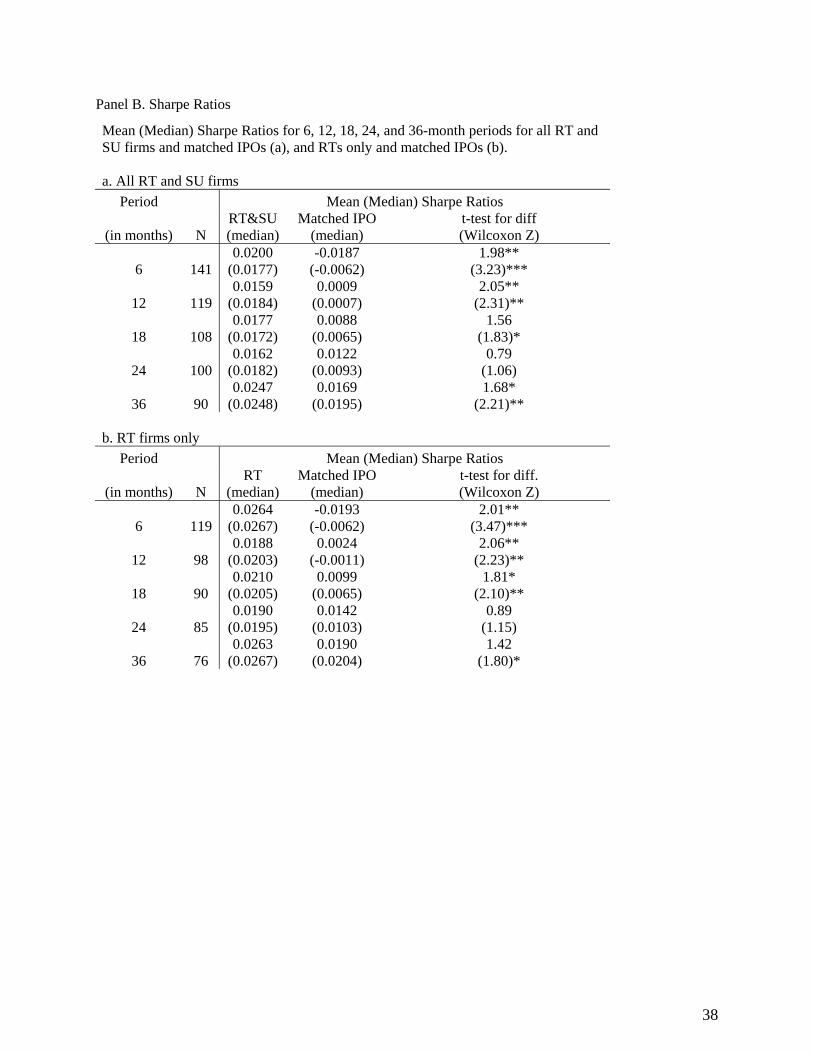

In contrast to the results above, a comparison of the Sharpe ratios of the sample firms

with the matched firms indicates that the stocks of RTs and SUs exhibit better performance, on

average, than their IPO counterparts (see panel B) over the 6, 12, 18, 24, and 36 months

following their going-public transactions.

6.2.3. Accounting Performance

To provide a broader illustration of post going public performance, Table 6 presents

changes in balance sheet profitability, liquidity, leverage, and distress variables, as well as price

to book and price to sales ratios, for the first and second full reporting years as public companies.

The table also tests if the change in the value of these variables for RT and SU firms is

significantly different from the change in the value of these variables for the matched IPO firms.

[Table 6 About Here]

The results in table 6 indicate that the profitability (ROA and ROE) of RT and SU firms

decline following the going public transaction but the decline is not statistically significant.

However, when compared with their IPO counterparts, RT and SU firms show a significantly

larger decline in ROA over the second year after they go public, and in ROE over the first year

after they go public.

Table 6 also indicates that balance sheet liquidity, proxied by cash/assets, declines

significantly for RT and SU firms over the two years after they go public. Furthermore, the

decline in the cash to assets ratio for RT and SU firms is significantly greater than that for their

23

matched IPO controls. The leverage increases significantly for sample firms over the first and

second full trading years. However, sample firms did not experience a greater increase in

leverage than control firms did. The results for Altman’s Z are mixed; while sample firms

experience a significantly larger decline in distress (increase in Z) over the first year than control

firms, distress appears to increase significantly (decline in Z) for the combined RT and SU

sample over the second year.

Finally, Table 6, Panel B provides evidence suggesting that market value multiples (price

to book and price to sales) decline during the first and second reporting years as a public

company for sample firms, though the decline is not greater than that experienced by control IPO

firms. Both the combined RT and SU sample and the RT sample exhibit an insignificant decline

in price to book. Price to sales, however, declines significantly for the combined RT and SU

sample and the RT firms alone.

Taken together, the results in Table 6 indicate that RT and SU firms experience a decline

in liquidity and an increase in leverage after they go public but these changes are not

significantly different from the corresponding changes shown by control underwritten IPO firms.

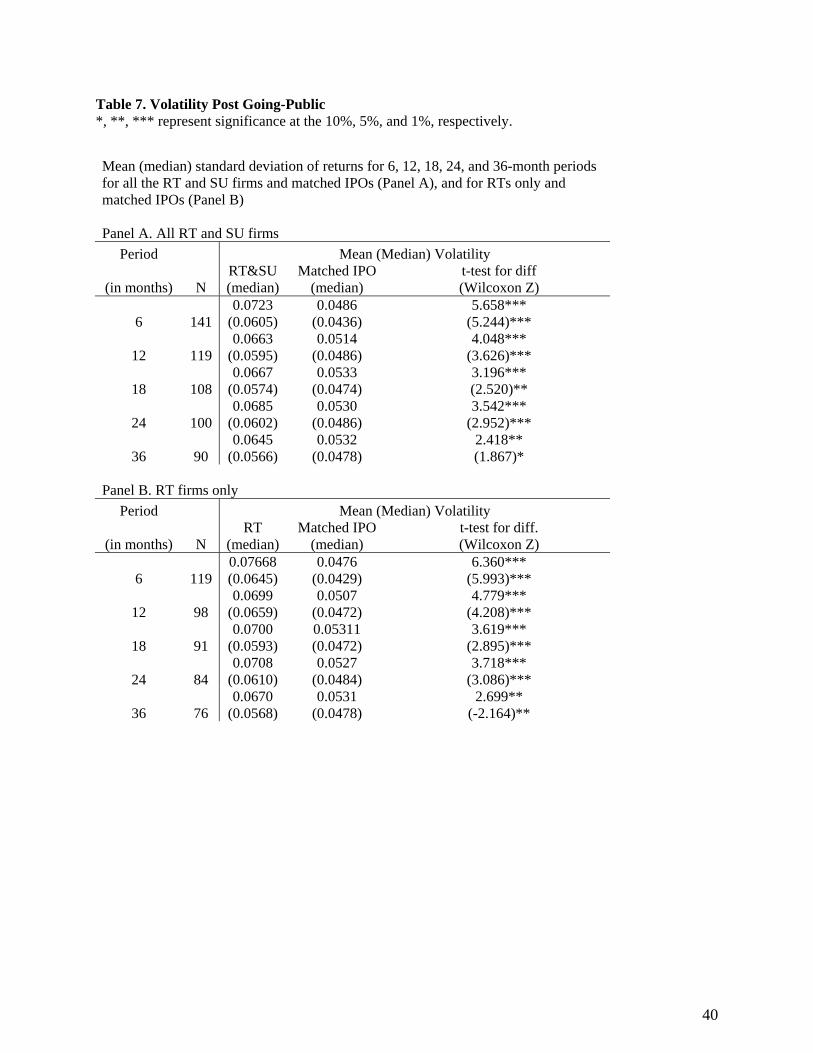

6.2.4. Volatility and Trading Liquidity

We investigate volatility and trading liquidity of sample and control firms following the

inception of trading. The popular perception of RTs and SUs is that they are less liquid, more

volatile, and generally riskier than IPOs. Also, RT and SU firms do not benefit from the

stabilization efforts of an IPO underwriter. Table 7 provides data on volatility, as measured by

the standard deviation of returns, over the 6, 12, 18, 24, and 36 months following the going-

public transaction.

24

[Table 7 About Here]

Table 7, Panel A shows that the stocks of RT and SU firms are significantly more volatile

than the stocks of matched IPO firms over each time interval. Similar results are obtained if the

comparison is done for the sample of RT firms only and their matched IPO firms (see Panel B).

Table 8 provides the results of an analysis of liquidity of RT and SU firms over the first,

second, and third year following their going-public transactions.

[Table 8 About Here]

Panel A documents that the RT and SU firms are less liquid than their IPO counterparts

in each of the three years following the RT or SU event date. Similar results are obtained when

the comparison is done for the sample of RT firms only and their IPO counterparts (see Panel B).

These results are consistent with those in Eckbo and Norli (2001), which finds that IPOs are

more liquid than size-matched seasoned firms. We measure liquidity by turnover, which is

volume divided by number of shares outstanding. Liquidity is measured beginning from the

second month after the event date (i.e. date of reverse takeover or self-underwritten offering),

and is measured as daily averages for each of the first three years. In each year, an RT and SU

firm is included in the sample if it and its matched IPO (in the case of Panels A and B) have a

minimum of 200 observations for which daily turnover can be calculated.

Unlike SUs and IPOs, RTs involve a previously existing and trading public firm. So in

Panel C we examine if the liquidity of the public firm is affected by the reverse takeover. We

find that there is no statistically significant change in the liquidity of the public firm because of

the reverse takeover, as the liquidity of the pre-existing public firm in the year prior to the

reverse takeover is not statistically different from the liquidity in the year after the reverse

takeover. This result suggests that while the shareholders of the private firm experience a

25

significant improvement in their liquidity position as a result of going public, the shareholders of

the former vehicle firm who remain as shareholders of the newly public firm do not.

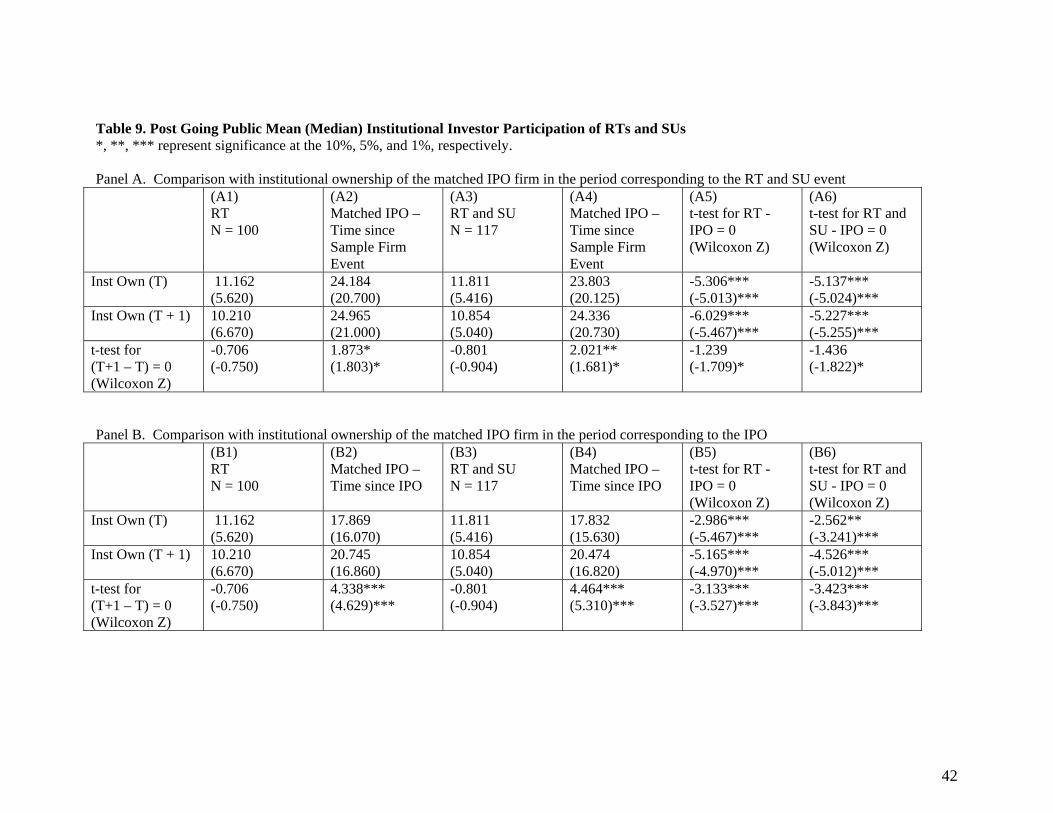

6.2.5. Ability to Attract Institutional Ownership

In Table 9, we compare the institutional ownership of the combined RT and SU sample

and the RT only sample with the institutional ownership of the matched IPO sample during the

quarter of the event (i.e. reverse takeover or self-underwritten offering) and the following quarter

(see Panel A). We also do this comparison for the period corresponding to the matched firm’s

IPO (see Panel B). Finally, we examine if there is a change in the institutional ownership for

sample and control firms in the quarter after they go public.

[Table 9 About Here]

To illustrate the contents of Table 9, we provide the following example. Hayes Corp went

public through an RT on 7/30/1997. Its control firm, Ciena Corp, did an IPO on 2/7/1997. Table

9 column A1, shows the percent institutional ownership for RT firms at the end of the quarter in

which they went public (i.e., for Hayes, the quarter including 7/30/1997) and the quarter after.

Column A3 provides the same information for the combined RT and SU sample. Column A2

(A4) shows the institutional ownership of the matched IPO firm at the time the RT (RTSU) firm

went public (i.e., institutional ownership is reported for Ciena for the quarter including

7/30/1997, which is the quarter that the sample firm Hayes went public, and the quarter after).

Columns A5 and A6 provide t-statistics and Wilcoxon Z statistics for difference in mean and

medians between the RT sample and control IPO firms and between the full RTSU sample and

matched control firms, respectively.

26

The information for the RT sample and the combined RTSU sample remains the same in

Panel B. What differs in Panel B is the time measurement for control sample comparison

purposes. Column B2 (B4) provides the percent institutional ownership for the IPO control firms

for the RT (RTSU) sample for the quarter during which the control firm went public and the

quarter after (i.e., Ciena’s institutional ownership the quarter of 2/7/1997, when Ciena went

public, and the quarter after). In using both time measurements, we take into account market

conditions that might affect institutional ownership decisions as well as the decisions of

institutions to hold stock involving the “trading age” of the firm, or the time since the firm went

public.

Table 9 shows that at the end of the first reporting quarter, RTs and the combined RT and

SU sample exhibit significantly lower levels of institutional ownership relative to the control IPO

sample (a mean of 11.162% for RTs and 11.811% for the combined RT and SU sample, vs.

23.803% for matched IPO firms in the same period, and 17.832% for IPO firms in the period

when the IPO firm went public. Similarly, in the quarter following the going public transaction,

institutional ownership is significantly lower for RT firms and for RT and SU firms than for the

matched sample IPOs.

The last row in Table 9 indicates that while institutional ownership for the RT sample and

the combined RT and SU sample declined significantly between the quarter they went public and

the following quarter, institutional ownership rose significantly for control IPO firms.

Taken together, these results suggest that the IPO process provides benefits to IPO firms

in terms of obtaining institutional support for their clients. While clients pay for these services,

they appear more difficult to achieve without the help of all that is involved in the IPO process,

from the roadshow to aftermarket stabilization. The marketing function performed by the lead

27

manager appears to be more effective than that of the merger advisor in the case of the RT or the

management of the company in the case of the SU in attracting institutional support.

6.3. Post Going-Public Return Predictability

We next examine the factors that influence the long horizon performance of firms using

RTs and SUs to go public. Table 10 provides the results of regressions for three model

specifications where the dependent variable is 12 month buy and hold abnormal returns

(BHARs) of RT and SU firms.

[Table 10 About Here]

All three model specifications indicate that institutional ownership at the end of the first

quarter is a significant determinant of superior post going-public performance. This supports the

notion that institutional owners mitigate agency conflicts and provide monitoring for newly

public firms. The market capitalization of the RT or SU firms is negatively related to 12-month

BHARs but its coefficient is significant (at the 10% level) in only one specification. The

negative and significant coefficient on the HOT dummy variable in Model 3 indicates that firms

that engage in RTs or SUs during hot IPO markets (defined as per Ljungqvist and Wilhelm

(2004) and Loughran and Ritter (2004) as the period corresponding to the “internet bubble” in

1999 and 2000) perform poorly, consistent with other IPO studies.17 However, the negative

coefficient on the HOT dummy variable is insignificant in Model 2. Models 1 and 2 indicate that

higher leverage (proxied by the ratio of debt to total assets) is detrimental to long term

performance of RT and SU firms, while Model 3 indicates that higher balance sheet liquidity –

proxied by cash and equivalents to total assets – is positively and significantly related to

17 Ofek and Richardson (2003) use the 1998 – 2000 time period to represent the “internet bubble”. Our results are robust to this definition of hot market as well.

28

performance. The significance of both leverage and liquidity indicate that firms need to take

actions to reduce leverage and manage cash flow from the time they go public, and this would be

particularly true for firms in industries with high “burn rates” or for firms that would find

accessing the capital markets through a secondary offering prohibitively costly.

We also investigate whether having outside valuation assistance facilitates better post-

valuation performance. We include NOUW, a dummy variable, which is equal to 1 if the firm is

either an SU (with no underwriter) or an RT with no investment advisor18. Having no investment

advisor or underwriter (i.e., truly a “do it yourself” deal) is significantly and negatively related to

12 month performance in all three model specifications. This is consistent with comments made

by Capital West Securities banker Bob Rader, in explaining why self-managed going public

transactions often fail: “As a manager, you need to dedicate your time to running the firm, rather

than going out and trying to find people interested in your stock.”19 While not necessarily a

strong indicator of the role performed by the underwriter in a traditional IPO, this result is

consistent with the conjecture that managerial resources can become overextended if the firm

does not seek outside assistance with the going public transaction, and with the idea that an

outside financial valuation group provides certification of value.

7. Conclusions

In this paper, we examine the characteristics of firms using reverse takeovers and self-

underwritten IPOs as an alternative to the traditional underwritten IPO. We find that firms that

use alternative mechanisms tend to be less profitable than IPO firms of comparable size in the

same 3 digit SIC code. At the time that they go public, they do not exhibit significantly lower

18 Some reverse takeover firms report hiring a financial advisor to assist with the deal. However, about a third report “no investment advisor” in their pre-merger financial statements. 19 Personal interview with Bob Rader of Capital West Securities, 7/30/2004.

29

balance sheet liquidity or significantly higher distress. However, by two years post going public,

they have significantly higher debt and experience declines in profitability and balance sheet

liquidity.

We also examine post going public liquidity, volatility, institutional ownership, and post

IPO performance. We find that RT and SU firms are characterized by lower levels of liquidity

and significantly higher volatility, as measured by the standard deviation of returns. While the

combined sample of RT and SU firms have comparable institutional ownership post going public

to their control IPO firms, RT firms are characterized by statistically lower institutional

ownership than their matches, and while IPO firms experience significant increases in

institutional support, those using RTs and SUs experience declines. We also find evidence that

firms utilizing alternative going public mechanisms outperform their matched traditional IPO

counterparts over longer horizons as indicated by mean and median tests of Sharpe ratios;

however, the returns for buy and hold returns are mixed.

Our results have important implications for managers – namely, that the traditional

underwritten IPO is not the only game in town, and that firms can avoid the costs of the

traditional IPO without experiencing substantially lower performance by some measures.

However, investors should consider that firms using RTs and SUs experience lower institutional

ownership participation, lower liquidity, and higher volatility. Finally, having no investment

advisor at all when arranging a going public transaction appears to be negatively correlated with

long run performance.

30

References Baker, M. and J. Wurgler, 2000, The equity share in new issues and aggregate stock returns, The Journal of Finance 55, 2219-2257. Ben Dor, A., 2004, Sentiment, Long Run Performance, and the Cross Section of Institutional Ownership in IPOs, unpublished working paper, Northwestern University. Brav, A., C. Geczy, and P. A. Gompers, 2000, Is The Abnormal Return Following Equity Issuances Anomalous? Journal of Financial Economics, 56, 209-250. Brav, A. and P. A. Gompers, 1997, Myth or reality? The long-run underperformance of initial public offerings: Evidence from venture and nonventure capital-backed companies, Journal of Finance 52, 1791-1821. Brown, K., A. Dittmar, and H. Servaes, 2004, “Roll-ups: Performance and Incentives for Industry Consolidating IPOs,” Review of Financial Studies, forthcoming. Burns, J., April 14, 2004, SEC May Impose Stricter Rules on Behavior of Shell Companies, Dow Jones Newswires. Carter, R. B. and Dark, F. H., 1993, Underwriter reputation and initial public offerings: The detrimental effects of flippers, Financial Review, 28, 2, 279-301. Carter, R. B., F. H. Dark and A. K. Singh, 1998, Underwriter reputation, initial returns, and the long-run performance of IPO stocks, Journal of Finance 53, 285-311. Chen, C. and Lin, T. H., 1996, The information content of self-underwritten IPOs.” In Empirical Issues in Raising Equity Capital. Edited by Mario Levis. Elsevier Science B.V. Amsterdam, the Netherlands. Chen, Hsuan-Chi and Ritter, Jay R. (2000). “The Seven Percent Solution.” The Journal of Finance, 55, 1105-1131. Eckbo, Espen, and Orvind Norli, 2001, Leverage, liquidity, and long-run IPO returns, unpublished Dartmouth University working paper. Gleason, K., L. Rosenthal, and R. Wiggins, 2004, Reverse takeovers: Backing into being public, Journal of Corporate Finance, forthcoming. Gompers, P., and J. Lerner, 1999, Conflict of Interest and Reputation in the Issuance of Public Securities: Evidence from Venture Capital, Journal of Law and Economics, 42, 53-80

Gompers, P., and J. Lerner, 2003, The really long-term performance of initial public offerings: The pre-Nasdaq evidence, Journal of Finance, 58, 1355-1392.

31

Hennessey, R., 2004, Mum is the Word on Where IPOs Will Call Home, Wall Street Journal, June 7, 2004, page c4. Hirshleifer, D., 2001, Investor Psychology and Asset Pricing, Journal of Finance, 56, 1533-1598. Keloharju, M., 1993, The winner's curse, legal liability, and the long-run price performance of initial public offerings in Finland, Journal of Financial Economics 34, 251-277 Lee, P. J., S. L. Taylor and T. S. Walter, 1999, IPO underpricing explanations: Implications from investor application and allocation schedules, Journal of Financial and Quantitative Analysis 34, 425-444. Levis, M., 1993, The Long-Run Performance of Initial Public Offerings: The UK Experience 1980-1988, Financial Management, 22, 28-41. Lewis, M., 2001, Online IPO Revolution Postponed, Forbes.com, http://www.forbes.com/2001/03/14/0314banks.html. Lipman, F., 2001, The Complete Going Public Handbook. Prima Publishing, Roseville, CA. Ljungqvist, A., V. Nanda, and R. Singh, 2002, Hot markets, investor sentiment, and IPO pricing, unpublished NYU working paper. Ljungqvist, A. and Wilhelm, W.J., 2003, IPO pricing in the dot-com bubble, Journal of Finance, 58, 723-752. Loughran, T. and J. R. Ritter, 1995, The new issues puzzle, Journal of Finance 50, 23-51. Loughran, T., and J. R. Ritter, 2000, Uniformly least powerful tests of market efficiency, Journal of Financial Economics, 55, 361-389. Loughran, T., and J. R. Ritter, 2004, Why Has IPO Underpricing Increased Over Time? Financial Management, 33, 5-37. Loughran, T., J.R. Ritter and K. Rydqvist, 1994, Initial public offerings: International insights, Pacific-Basin Finance Journal 2, 165-199. Muscarella, C. J. and Vetsuypens, M. R., 1989, A simple test of Baron's model of IPO underpricing. Journal of Financial Economics, 24, 125-136. Ofek, E., and M. Richardson, 2003, DotCom Mania: The rise and fall of internet stock prices, Journal of Finance, 58, 1113-1138. Purnanandam, A. K., and B. Swaminathan, 2004, Are IPOs underpriced? Review of Financial Studies, forthcoming.

32

Ritter, J. R., 1987, The Costs of Going Public, Journal of Financial Economics, 19, 269-281.

Ritter, J. R., 1991, The long run performance of initial public offerings, Journal of Finance, 46, 3-27. Ritter, J. R., and I. Welch, 2002, A review of IPO activity, pricing, and allocations, Journal of Finance, 57, 1795-1828.

33

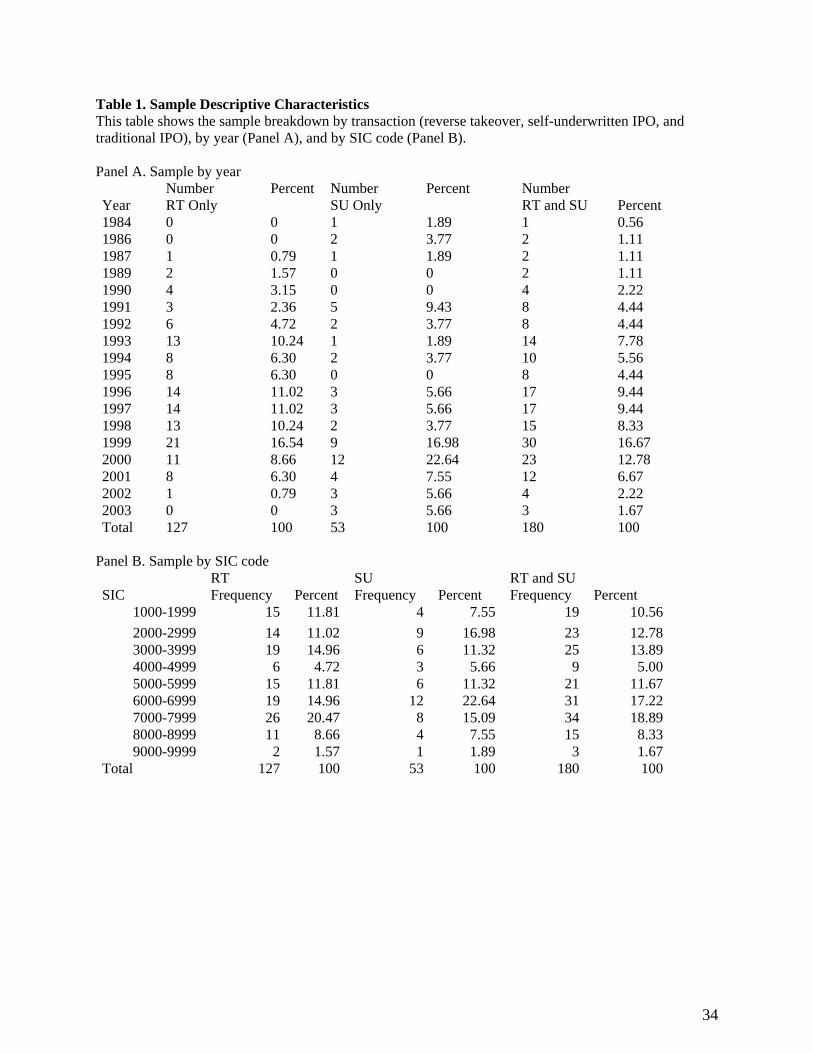

Table 1. Sample Descriptive Characteristics This table shows the sample breakdown by transaction (reverse takeover, self-underwritten IPO, and traditional IPO), by year (Panel A), and by SIC code (Panel B). Panel A. Sample by year

Year Number RT Only

Percent Number SU Only

Percent Number RT and SU Percent

1984 0 0 1 1.89 1 0.56 1986 0 0 2 3.77 2 1.11 1987 1 0.79 1 1.89 2 1.11 1989 2 1.57 0 0 2 1.11 1990 4 3.15 0 0 4 2.22 1991 3 2.36 5 9.43 8 4.44 1992 6 4.72 2 3.77 8 4.44 1993 13 10.24 1 1.89 14 7.78 1994 8 6.30 2 3.77 10 5.56 1995 8 6.30 0 0 8 4.44 1996 14 11.02 3 5.66 17 9.44 1997 14 11.02 3 5.66 17 9.44 1998 13 10.24 2 3.77 15 8.33 1999 21 16.54 9 16.98 30 16.67 2000 11 8.66 12 22.64 23 12.78 2001 8 6.30 4 7.55 12 6.67 2002 1 0.79 3 5.66 4 2.22 2003 0 0 3 5.66 3 1.67 Total 127 100 53 100 180 100

Panel B. Sample by SIC code RT SU RT and SU SIC Frequency Percent Frequency Percent Frequency Percent

1000-1999 15 11.81 4 7.55 19 10.562000-2999 14 11.02 9 16.98 23 12.783000-3999 19 14.96 6 11.32 25 13.894000-4999 6 4.72 3 5.66 9 5.005000-5999 15 11.81 6 11.32 21 11.676000-6999 19 14.96 12 22.64 31 17.227000-7999 26 20.47 8 15.09 34 18.898000-8999 11 8.66 4 7.55 15 8.339000-9999 2 1.57 1 1.89 3 1.67

Total 127 100 53 100 180 100

34

Table 2. Firm Characteristics Prior to Going Public *, **, *** represent significance at the 10%, 5%, and 1%, respectively. Panel A. Mean (median) descriptive statistics, year prior to going public (T-1) and year of going public transaction (T). Year Prior to Going Public (T-1) | Year of Going Public (T) RT&SU RT Only

Mean (Median)

Mean (Median)

IPO Mean (Median)

RT&SU vs. IPO T-statistic Wilcoxon Z

RT vs. IPO T-statistic Wilcoxon Z

RT&SU Mean (Median)

RT Only Mean (Median)

IPO Mean (Median)

RT&SU vs. IPO T-statistic (Wilcoxon Z)

RT vs. IPO T-statistic Wilcoxon Z

Assets 359.39 376.98 (15.97) (16.29)

283.77 (22.33)

0.321 (-0.371)

0.302 (-1.042)

516.08 (17.72)

652.37 (24.69)

393.64 (71.07)

0.413 (-2.983)***

0.457 (-2.998)***

ROA -22.833 -21.181 (-8.773) (-10.53)

-24.306 (0.314)

-0.669 (-1.016)

-0.568 (-1.078)

-32.186 (-4.271)

-26.863 (-3.845)

-8.569 (1.863)

-4.168*** (-4.189)***

-3.148*** (-3.528)***

ROE -13.489 -13.553 (-1.033) (-2.77)

16.633 (19.081)

-2.795** (-2.765)***

-3.757*** (-3.558)***

-9.961 (-1.244)

-14.062 (-2.35)

-8.891 (4.055)

-0.205 (-0.453)

-0.849 (-1.096)

Cash/Total Assets

20.803 (8.825)

22.961 (10.300)

24.884 (12.100)

-0.317 (-0.027)

-0.899 (-1.087)

22.109 (10.090)

22.899 (11.304)

14.903 (4.799)

-4.537*** (-3.904)***

-2.65*** (-2.429)**

Z 2.493 3.920 (1.920) (2.380)

0.268 (2.013)

1.143 (-0.894)

1.143 (1.509)

1.100 (2.118)

2.110 (2.268)

10.249 (5.991)

-4.855*** (-5.029)***

-4.855*** (-4.453)***

Debt/Total Assets

24.255 (17.638)

20.854 (13.801)

30.795 (20.348)

-1.274 (-1.240)

-1.822* (-1.830)*

27.026 (19.744)

24.829 (17.381)

14.903 (4.779)

3.775*** (3.351)***

2.757*** (2.465)**

Panel B. Mean (median) valuation, year of going public transaction (time T) RT&SU RT Only

Mean (Median)

Mean (Median)

IPO Mean (Median)

RT&SU vs. IPO T-statistic Wilcoxon Z

RT vs. IPO T-statistic Wilcoxon Z

Market Capitalization 75.955 (19.573)

58.671 (16.530)

487.303 (110.86)

-1.815* (-7.320)***

-1.878* (-7.677)***

Price/Book

5.796 (1.960)

7.585 (2.282)

5.235 (2.997)

0.333 (-1.990)**

0.902 (-1.289)

Price/Sales

9.566 (0.227)

7.143 (0.205)

6.128 (0.248)

0.984 (-1.217)

0.922 (-1.076)

Table 3. Logit Regressions. Dependent variable is RT or SU = 1, IPO = 0; models show factors affecting the probability of firm using an alternative to an IPO (such as an RT or SU) versus an IPO. SIZE is proxied by the log of assets (or sales) at the time of the going public transaction, Altman’s Z (Z) is a distress proxy, CASH, a proxy for balance sheet liquidity, is the ratio of cash and equivalents to total asset, PROFIT, a profitability measure, is proxied by ROA or ROE in different specifications, and LEVERAGE is the ratio of debt to total assets. All variables are as of the year of the going-public transaction. Wald statistics are shown below parameter estimates. *, **, *** represent significance at the 10%, 5%, and 1%, respectively. 1 2 3 4 Constant 2.588

(26.623)*** 2.741 (26.980)***

2.385 (18.835)***

1.795 (15.510)***

Log assets -0.512 (22.709)***

-0.462 (27.728)***

Log sales -0.512 (23.542)***

-0.436 (15.705)***

Z -0.071 (8.142)***

-0.069 (6.356)**

-0.063 (5.846)**

CASH -1.816 (9.202)***

-3.352 (18.561)***

-3.505 (20.072)***

-2.098 (15.226)***

Return on Assets -0.009 (1.778)*

Return on Equity -0.001 (0.002)

0.001 (0.107)

-0.001 (0.208)

LEVERAGE

0.017 (6.42)**

Likelihood Ratio 80.72*** 79.130*** 83.491*** 68.807*** Wald Chi-square 41.92*** 42.470*** 41.990*** 45.744*** N 253 253 253 255 Table 4. First Trading Day Returns Mean (median) first trading day returns (in %) for all RT and SU firms and matched IPO firms, and for RTs only and matched IPO firms. First trading day returns for RT firms are the change in the price from the close the day prior to the first trading day of the newly public reverse takeover firm; for SUs and IPOs, the first trading day return is measured as the change in the price at the close of the first day of trading from the offer price.

N Mean returns

(median)

Matched IPO mean returns

(median) t-test for difference

(Wilcoxon Z) All RTs and SUs 138

10.532 (2.340)

23.415 (9.235)

-2.66*** (-3.54)***

RTs only 116 7.882

(2.120) 23.054 (9.151)

-2.77*** (-3.51)***

36

Table 5. Post-Going Public Performance Panel A. Buy and Hold Returns Mean and median equal-weighted and value-weighted 6, 12, 18, 24, and 36-month buy and hold returns for all RT and SU firms and matched IPOs (a), and for RTs only and matched IPOs (b). The market capitalization of a firm on the RT or SU date is used as a weight to calculate the value-weighted results. *, **, *** represent significance at the 10%, 5%, and 1%, respectively. a. All RT and SU firms

Period Equal-weighted Mean (Median) BHRs Value-weighted Mean (Median) BHRs

(in months) N RT&SU Matched

IPO t-test for diff. (Wilcoxon Z) RT&SU

Matched IPO

t-test for diff. (Wilcoxon Z)

6 141 17.3480

(-9.0909) -3.4021

(-13.9344) 2.0582** (1.7401)*

-0.1540 (-0.0132)

0.0532 (-0.0088)

-1.4342 (-0.9004)

12 119 4.5481

(-14.6718) -7.2865

(-23.9667) 1.0847

(0.9069) -0.3215

(-0.0242) 0.1894

(-0.0187) -1.5682

(-0.7823)

18 108 -0.5163

(-30.5095) -4.6172

(-23.2375) 0.3010

(0.6590) -0.4130

(-0.0467) 0.7149

(-0.0168) -1.3461

(-1.1709)

24 100 4.3538

(-40.9827) -0.7334

(-24.4302) 0.3320

(-0.6945) -0.5363

(-0.0594) 0.8599

(-0.0127) -1.4039

(-2.3002)**

36 90 41.6333

(-18.3068) 26.5372

(-22.7232) 0.5610

(0.4909) -0.2612

(-0.0169) 1.8833

(-0.0081) -1.1002

(-1.2212) b. RT firms only

Period Equal-weighted Mean (Median) BHRs Value-weighted Mean (Median) BHRs

(in months) N RT Matched

IPO t-test for diff. (Wilcoxon Z) RT

Matched IPO

t-test for diff. (Wilcoxon Z)

6 119 22.8059

(-6.0000) -0.1797

(-12.4445) 1.9730*

(1.6600)* -0.0868

(-0.0058) 0.0999

(-0.0102) -1.4210

(-0.2493)

12 98 7.2222

(-13.7876) -4.8527

(-23.1855) 0.9575

(0.7388) -0.2344

(-0.0172) 0.3045

(-0.0239) -1.2873

(-0.0549)

18 90 3.5220

(-30.5095) -1.5509

(-18.3071) 0.3221

(0.5452) -0.1046

(-0.0483) 1.0346

(-0.0224) -1.0155

(-0.4567)

24 85 11.1719

(-37.5000) 3.9292

(-21.7391) 0.4127

(-0.5061) -0.2852

(-0.0461) 1.2223

(-0.0149) -1.1451

(-1.3912)

36 76 46.0909

(-18.3068) 37.6156

(-16.0405) 0.2741

(0.1217) 0.0233

(-0.0196) 2.5979

(-0.0094) -0.9764

(-1.0096)

37

Panel B. Sharpe Ratios

Mean (Median) Sharpe Ratios for 6, 12, 18, 24, and 36-month periods for all RT and SU firms and matched IPOs (a), and RTs only and matched IPOs (b). a. All RT and SU firms

Period Mean (Median) Sharpe Ratios

(in months) N RT&SU (median)

Matched IPO (median)

t-test for diff (Wilcoxon Z)

6 141 0.0200

(0.0177) -0.0187

(-0.0062) 1.98**

(3.23)***

12 119 0.0159

(0.0184) 0.0009

(0.0007) 2.05**

(2.31)**

18 108 0.0177

(0.0172) 0.0088

(0.0065) 1.56

(1.83)*

24 100 0.0162

(0.0182) 0.0122

(0.0093) 0.79

(1.06)

36 90 0.0247

(0.0248) 0.0169

(0.0195) 1.68*

(2.21)** b. RT firms only

Period Mean (Median) Sharpe Ratios

(in months) N RT

(median) Matched IPO

(median) t-test for diff. (Wilcoxon Z)

6 119 0.0264

(0.0267) -0.0193

(-0.0062) 2.01**

(3.47)***

12 98 0.0188

(0.0203) 0.0024

(-0.0011) 2.06**

(2.23)**

18 90 0.0210

(0.0205) 0.0099

(0.0065) 1.81*

(2.10)**

24 85 0.0190

(0.0195) 0.0142

(0.0103) 0.89

(1.15)

36 76 0.0263

(0.0267) 0.0190

(0.0204) 1.42

(1.80)*

38