Embed Size (px)

Citation preview

ALTERNATIVE FINANCING MODELS

COUNTRY EXPERIENCES –SRI LANKA

November 2014

Regulator-Central Bank of Sri LankaTwo types of Banking Licenses

1. Licensed Commercial (24 Banks)

2. Licensed Specialized (9 Banks)Non-Banking Financial Institutions

1. Finance Companies

2. Leasing CompaniesUnit TrustsVenture Capital CompaniesSuperannuation Funds Insurance Funds

FINANCIAL SECTOR LANDSCAPE

DFCC Bank

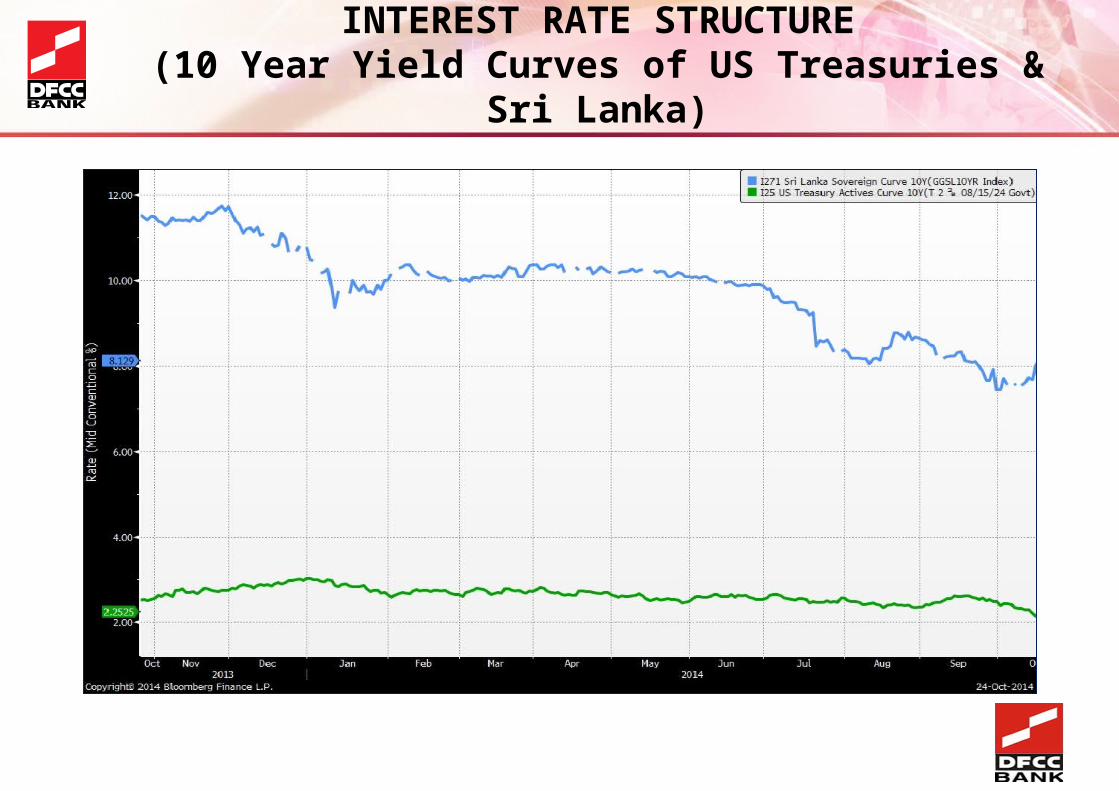

INTEREST RATE STRUCTURE(10 Year Yield Curves of US Treasuries & Sri Lanka)

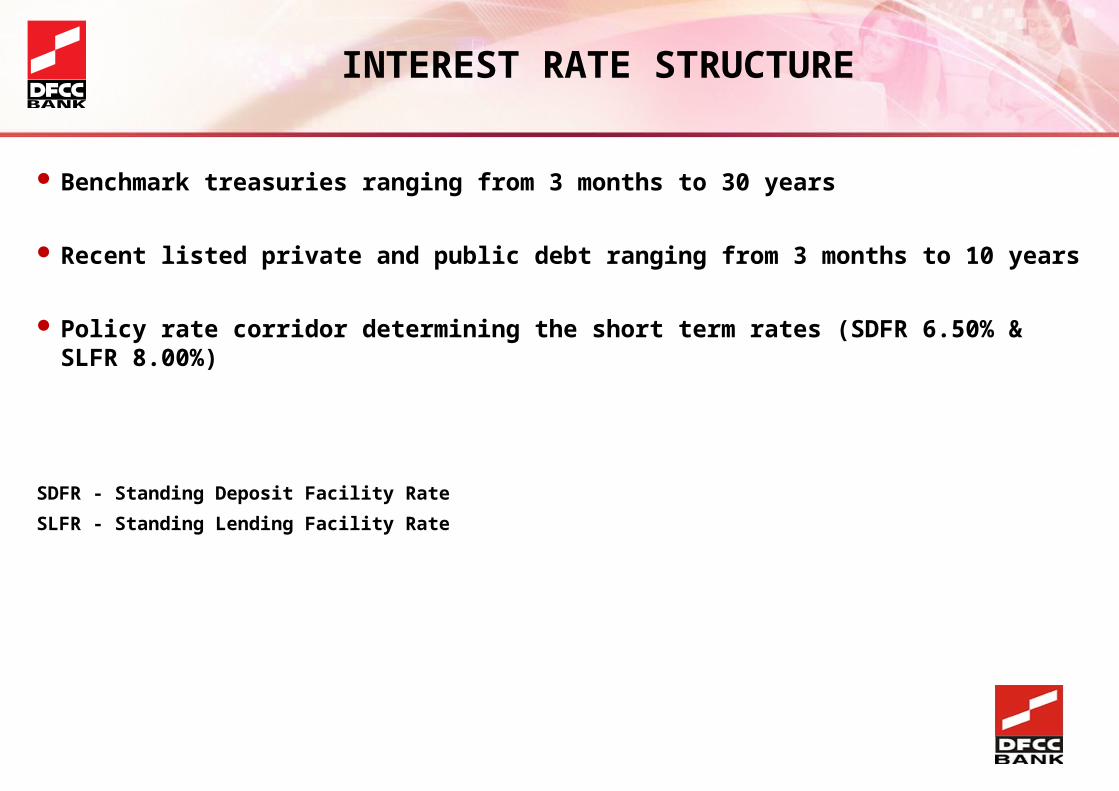

Benchmark treasuries ranging from 3 months to 30 years

Recent listed private and public debt ranging from 3 months to 10 years

Policy rate corridor determining the short term rates (SDFR 6.50% & SLFR 8.00%)

SDFR - Standing Deposit Facility Rate

SLFR - Standing Lending Facility Rate

INTEREST RATE STRUCTURE

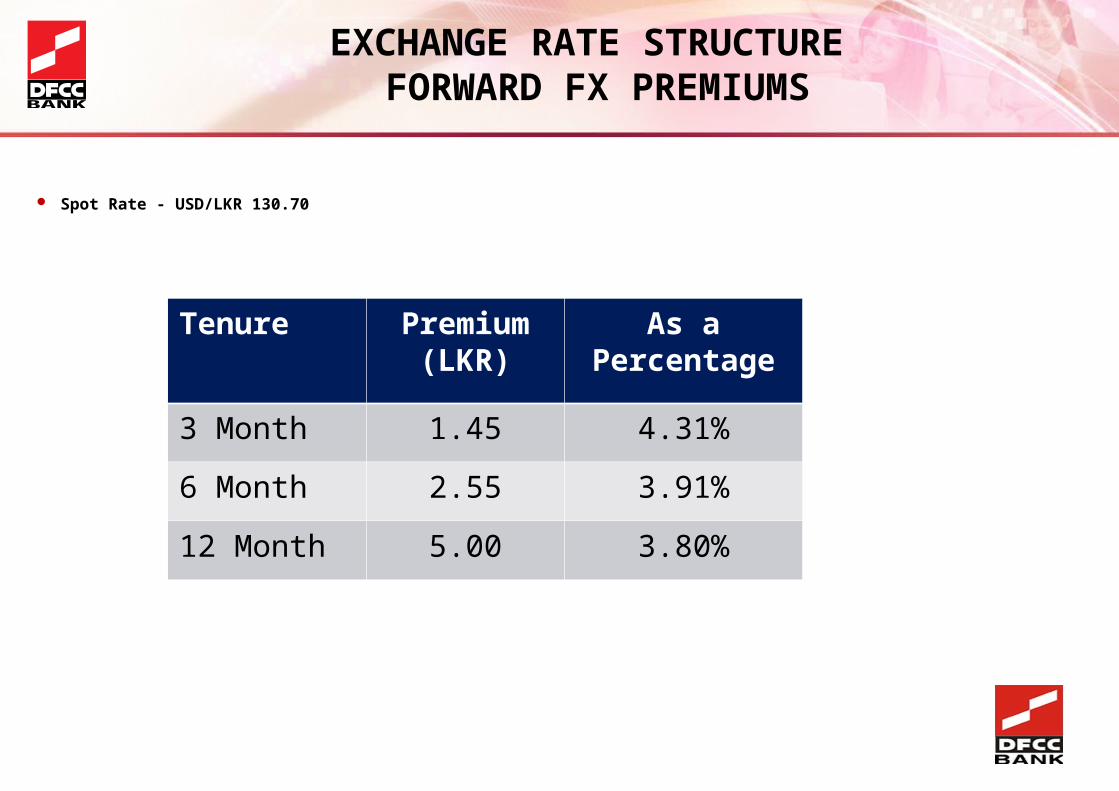

Spot Rate - USD/LKR 130.70

EXCHANGE RATE STRUCTURE FORWARD FX PREMIUMS

Tenure Premium (LKR)

As a Percentage

3 Month 1.45 4.31%

6 Month 2.55 3.91%

12 Month 5.00 3.80%

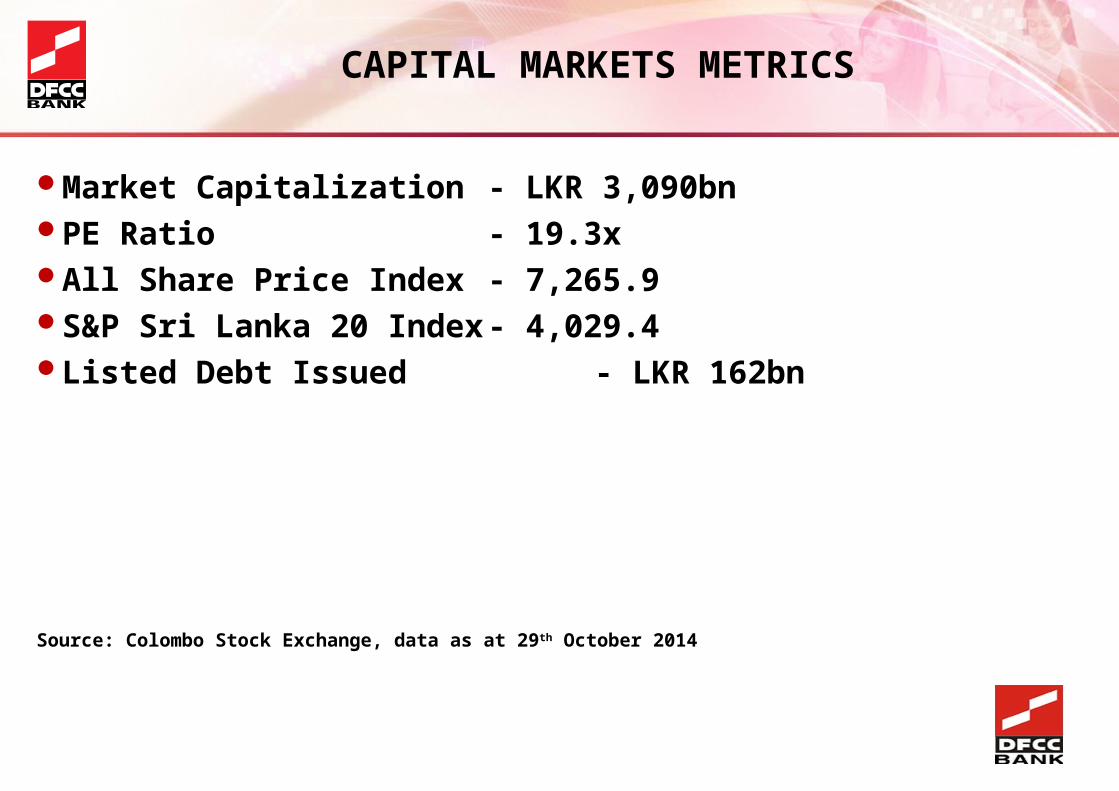

Market Capitalization - LKR 3,090bnPE Ratio - 19.3xAll Share Price Index- 7,265.9S&P Sri Lanka 20 Index - 4,029.4Listed Debt Issued - LKR 162bn

Source: Colombo Stock Exchange, data as at 29th October 2014

CAPITAL MARKETS METRICS

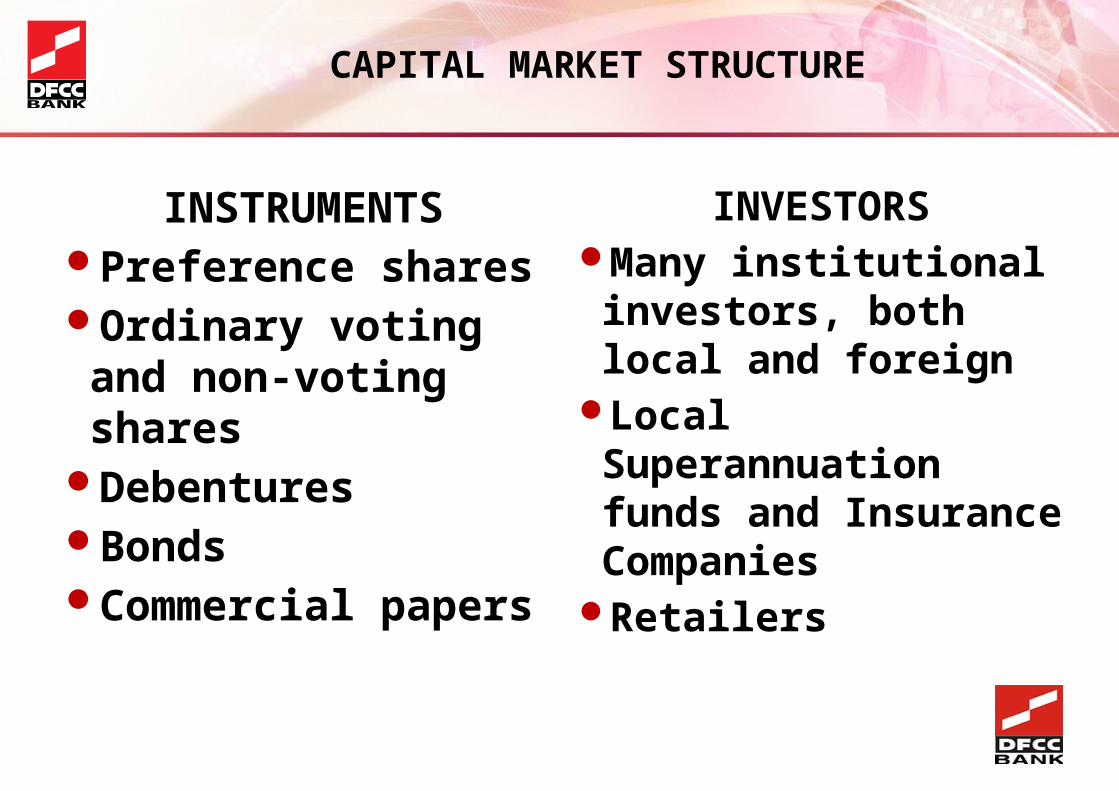

INSTRUMENTSPreference sharesOrdinary voting and

non-voting sharesDebenturesBondsCommercial papers

INVESTORSMany institutional

investors, both local and foreign

Local Superannuation funds and Insurance Companies

Retailers

CAPITAL MARKET STRUCTURE

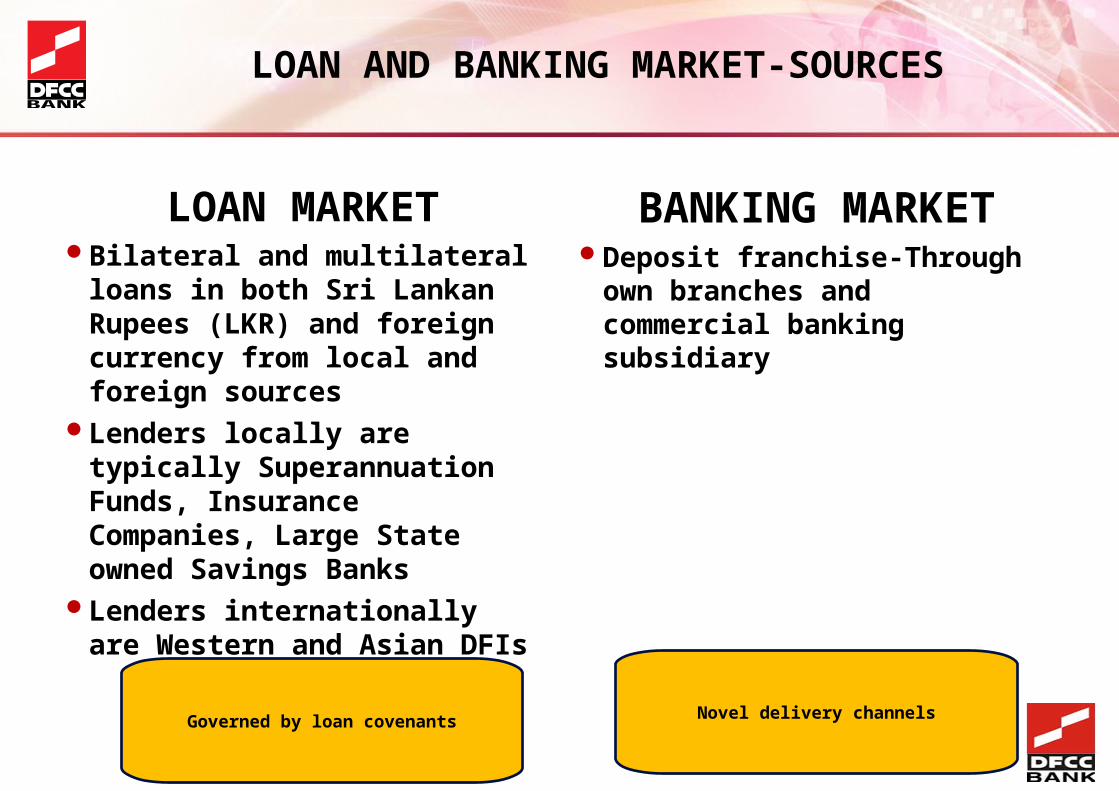

LOAN MARKETBilateral and multilateral loans

in both Sri Lankan Rupees (LKR) and foreign currency from local and foreign sources

Lenders locally are typically Superannuation Funds, Insurance Companies, Large State owned Savings Banks

Lenders internationally are Western and Asian DFIs

BANKING MARKETDeposit franchise-Through own

branches and commercial banking subsidiary

LOAN AND BANKING MARKET-SOURCES

Governed by loan covenants Novel delivery channels

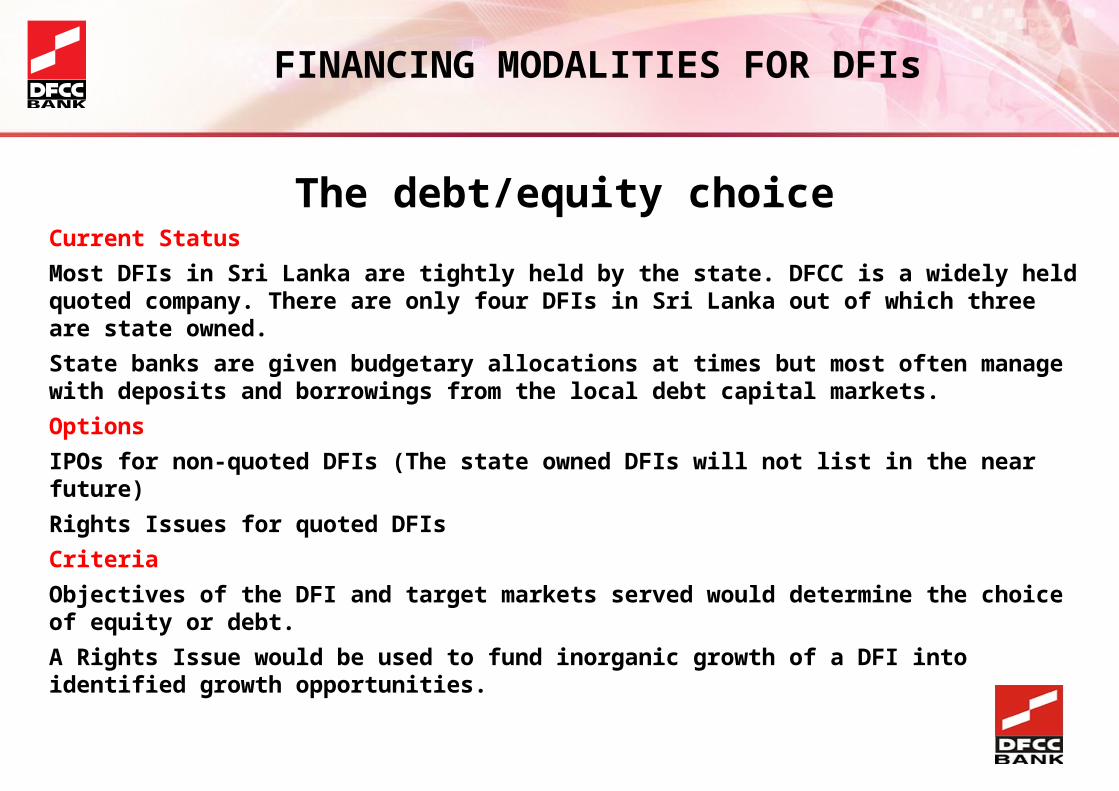

The debt/equity choiceCurrent Status

Most DFIs in Sri Lanka are tightly held by the state. DFCC is a widely held quoted company. There are only four DFIs in Sri Lanka out of which three are state owned.

State banks are given budgetary allocations at times but most often manage with deposits and borrowings from the local debt capital markets.

Options

IPOs for non-quoted DFIs (The state owned DFIs will not list in the near future)

Rights Issues for quoted DFIs

Criteria

Objectives of the DFI and target markets served would determine the choice of equity or debt.

A Rights Issue would be used to fund inorganic growth of a DFI into identified growth opportunities.

FINANCING MODALITIES FOR DFIs

FINANCIAL MARKET FUND MOBILISATION

A popular mode of fund raising which currently yields tax benefits to investors

Private placements vis-à-vis Public Issues

A fair selection of Investment Bankers to structure transactions

A wide institutional investor pool and developing retail pool

FINANCING MODALITIES FOR DFIs

Deposit Taking

CompetitionNine LSBs including 3 dedicated savings banks, 24 LCBs, 48 LFCs SLCs, Unit Trusts, Rural Banks, Thrift and Credit Cooperative Societies and Insurance Funds

Financial InclusionMobile banking as opposed to branch banking with over 100% mobile telephony penetration in Sri Lanka

LSB – Licensed Specialized Bank

LCB – Licensed Commercial Bank

LFC – Licensed Finance Company

SLC – Specialized Leasing Company

FINANCING MODALITIES FOR DFIs

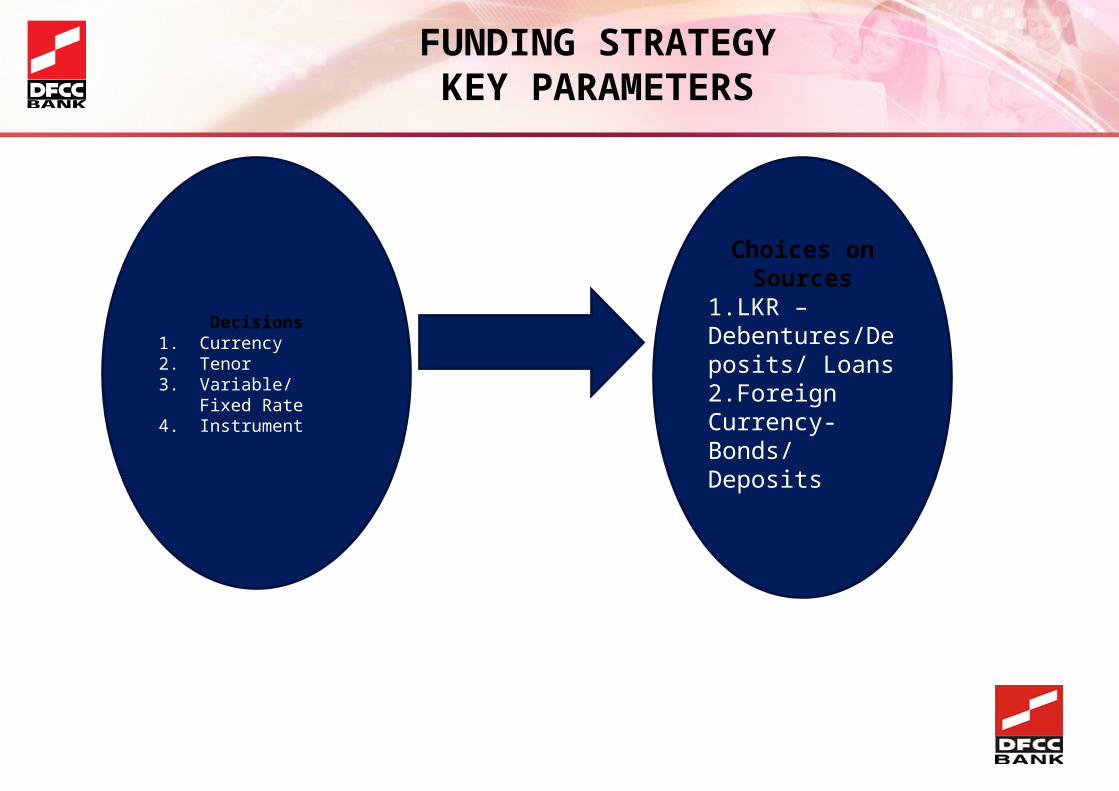

FUNDING STRATEGYKEY PARAMETERS

Decisions1. Currency2. Tenor3. Variable/ Fixed

Rate4. Instrument

Choices on Sources

1.LKR –Debentures/Deposits/ Loans2.Foreign Currency-Bonds/ Deposits

13

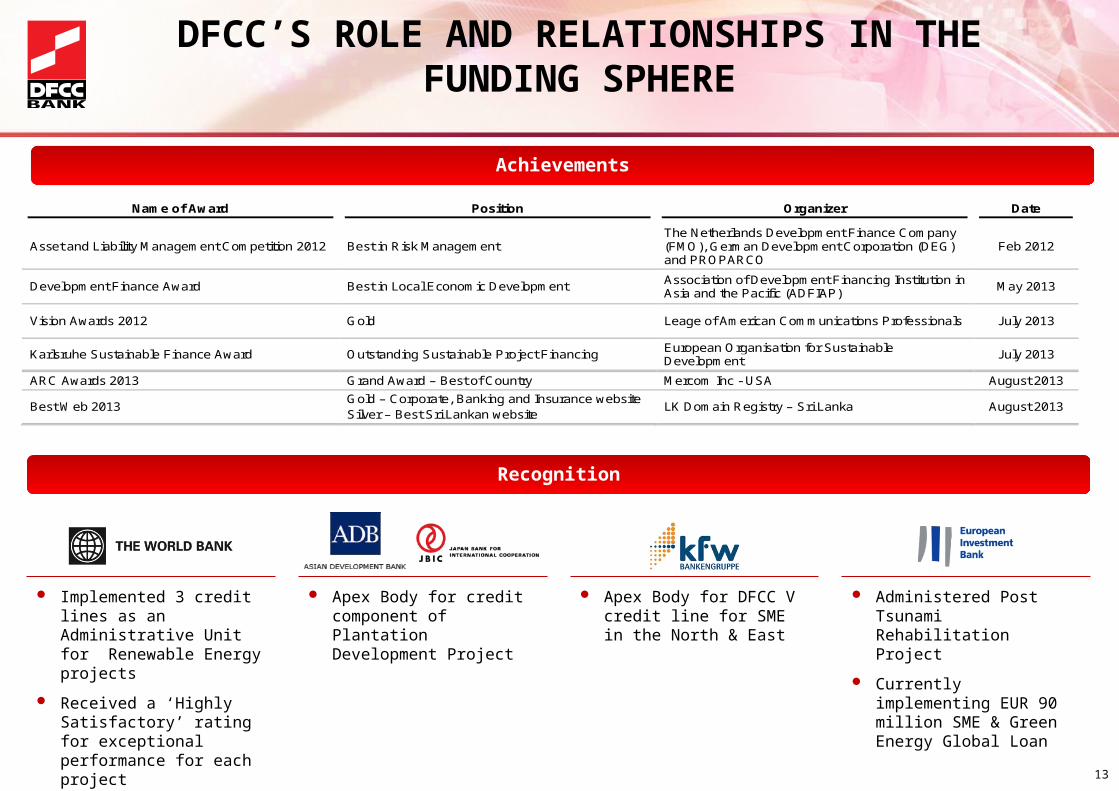

Recognition

Implemented 3 credit lines as an Administrative Unit for Renewable Energy projects

Received a ‘Highly Satisfactory’ rating for exceptional performance for each project

Apex Body for credit component of Plantation Development Project

Apex Body for DFCC V credit line for SME in the North & East

Administered Post Tsunami Rehabilitation Project

Currently implementing EUR 90 million SME & Green Energy Global Loan

DFCC’S ROLE AND RELATIONSHIPS IN THE FUNDING SPHERE

Name of Award Position Organizer Date

Asset and Liability Management Competition 2012 Best in Risk Management The Netherlands Development Finance Company (FMO), German Development Corporation (DEG) and PROPARCO

Feb 2012

Development Finance Award Best in Local Economic Development Association of Development Financing Institution in Asia and the Pacific (ADFIAP)

May 2013

Vision Awards 2012 Gold Leage of American Communications Professionals July 2013

Karlsruhe Sustainable Finance Award Outstanding Sustainable Project Financing European Organisation for Sustainable Development

July 2013

ARC Awards 2013 Grand Award – Best of Country Mercom Inc - USA August 2013

Best Web 2013 Gold – Corporate, Banking and Insurance website Silver – Best Sri Lankan website

LK Domain Registry – Sri Lanka August 2013

Achievements

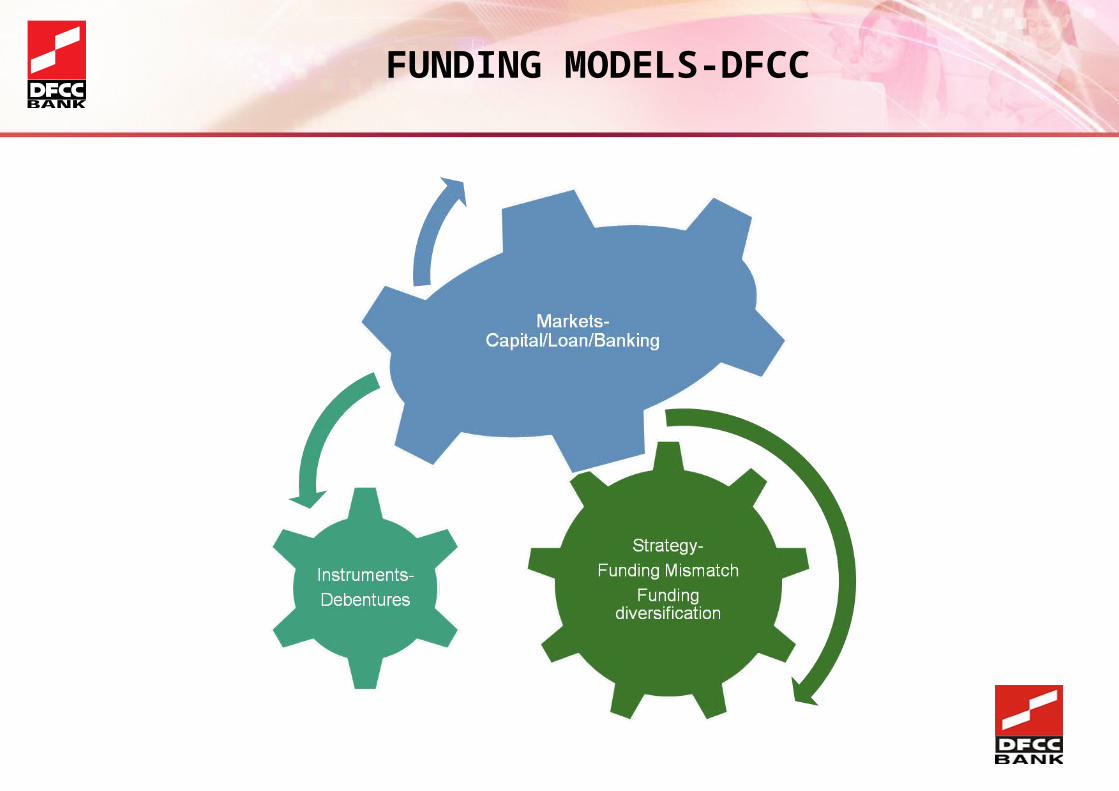

FUNDING MODELS-DFCC

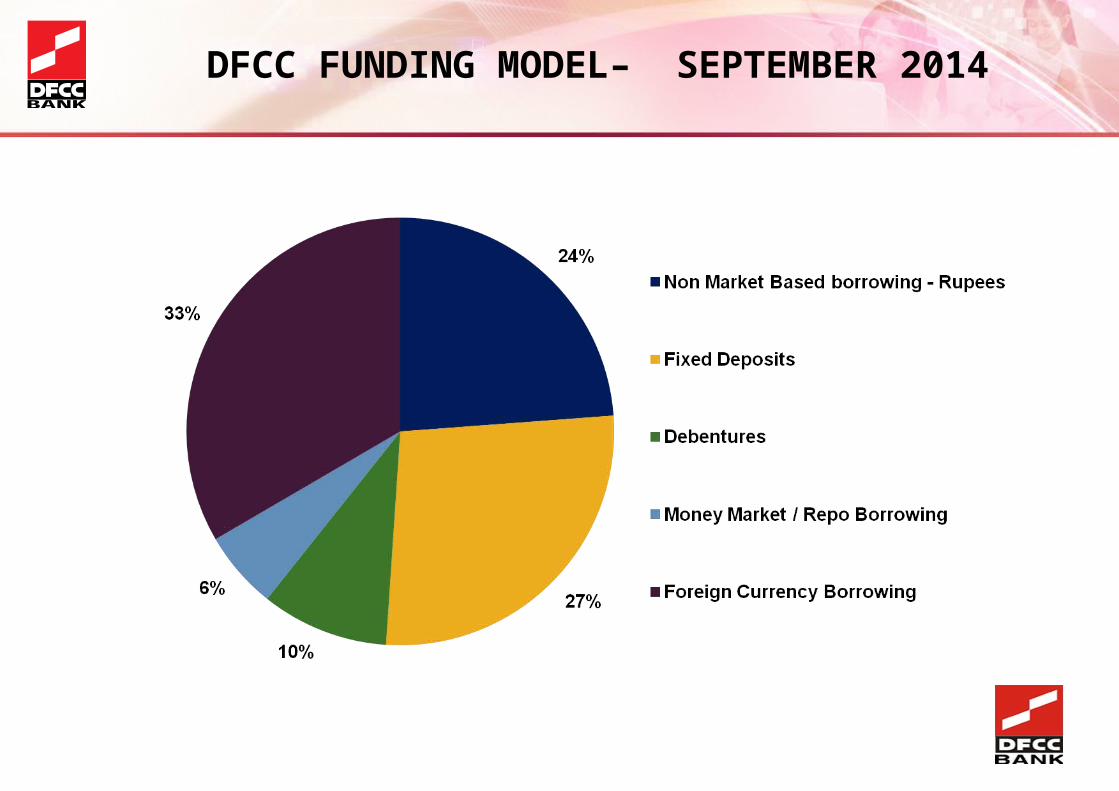

DFCC FUNDING MODEL– SEPTEMBER 2014

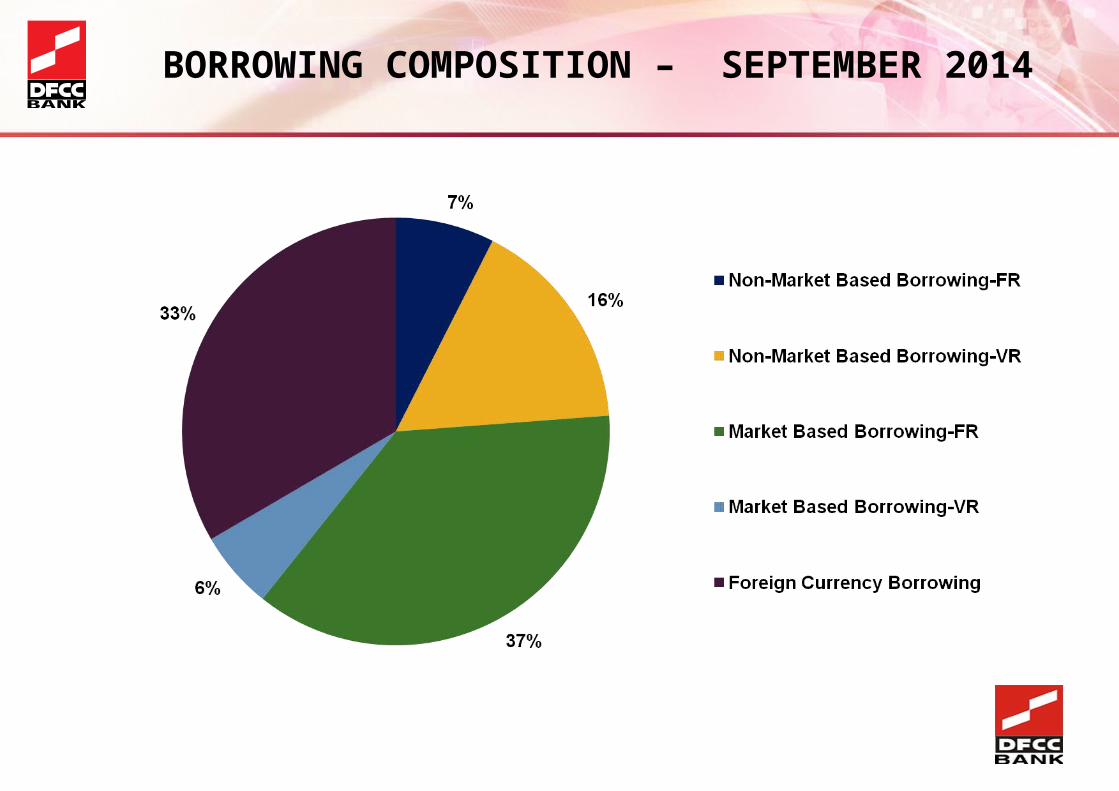

BORROWING COMPOSITION – SEPTEMBER 2014

Credit lines (either bilateral or multilateral) targeted for specific sectors such as renewable energy and SME

Sector identification and floating of specialized funds to cater to priority sectors

Securitization of loan receivables due to exposure limits

ALTERNATE FUNDING MODELS

Growth strategy in line with government’s five hub focus in terms of being in the forefront of related

capital asset funding

Funding strategy based on the three pillars of deposit and loan markets, financial markets and

specialized funds

Negotiation of specific state guidance in funding priority sectors

COUNTRY DFI STRTATEGY

Footnote

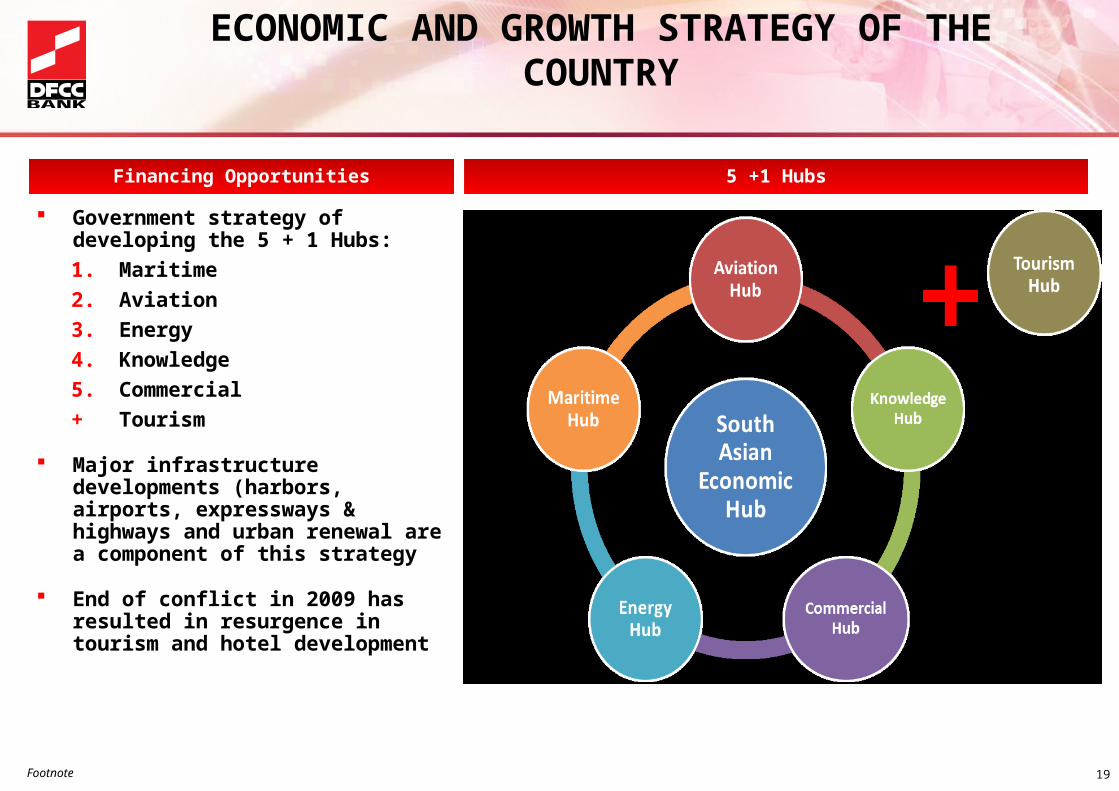

ECONOMIC AND GROWTH STRATEGY OF THE COUNTRY

19

Financing Opportunities 5 +1 Hubs

Government strategy of developing the 5 + 1 Hubs:

1. Maritime

2. Aviation

3. Energy

4. Knowledge

5. Commercial

+ Tourism

Major infrastructure developments (harbors, airports, expressways & highways and urban renewal are a component of this strategy

End of conflict in 2009 has resulted in resurgence in tourism and hotel development

Partnerships with established and emerging DFI giants in sourcing direct business

opportunities

Innovative financing through facilitated funding models such as equipment leasing

Usage of vehicles such as Private Equity funds with reasonable exit mechanisms

Actively seek local currency funding guaranteed by leading global DFIs

FUNDING MODELS -WAY FORWARD

Sector composition a trade off between country strategy alignment and risk

Specialised lending as a competitive advantage

Development portfolio management skills in infrastructure and other emerging sectors

Migration of best practice in the region through training and resource sharing

arrangements

GOALS OF SRI LANKAN DFIs-2020

22

Thank You