Embed Size (px)

Citation preview

Allianz –an opportunity!

Oliver Schmidt, Head of Investor Relations

UniCreditGerman Investment Conference,Munich, September 2011

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

2

OutlookD

Sovereign debt exposureC

1H 2011B

Allianz at a glanceAAgenda

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

3

1) 12/20102) 06/20113) Relation of positive parts of operating profit

P/C

Allianz at a glance

EUR 106bn total revenues1

EUR 1,508bn total AuM2

EUR 8.2bn operating profit1

180% solvency ratio2

EUR 43bn S/H equity2

EUR 44bn market cap2

More than 76mn customers1

Segments1,3

Operating profit in %Regions1,3

Operating profit in %

AM

L/H WesternEurope

GermanyGrowth markets

Specialty insurance

Broker markets US, UK, AUS

31%

22%

47%

5%12%

32%28%

23%

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

4

Leading P/C insurer globally1

Top 5 in Life business globally

Top 5 asset manager globally

Largest global assistance provider

Worldwide leader in credit insurance

One of the leading industrial insurers globally

Building the leading global automotive

provider

1) All rankings mentioned on the slide based on 2009 or 2010 data

Strong market positions and brands 1Successfactor

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

5

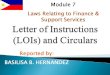

8.2

7.2

7.4

10.9

10.4

7.7

6.9

4.0

n.a.

4.5

4.1

3.5

5.5

3.8

2.0

1.8

1.5

We delivered in tough environment …

… thanks todiversification

Operating profit1 (EUR bn) and DPS (EUR)

2003

2004

2005

2006

2007

2008

2009

2010

Operating profit by business segment in %2

26

-53

-8

9

11

12

7

60

58

54

54

55

73

49

47

45

23

21

21

22

26

15

34

31

31

16

12

14

12

12

12

17

22

240

0

0

0

1) Historical reported figures2) Based on historical reported figures

excluding Corporate segment and consolidation

1H 2011

Operating profitDividend per share P/C

L/HAM

Bank

8.0 ± 0.5

Balanced business portfolio2Successfactor

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

6

EUR 448.4bn

AAA 45%

AA 14%A 25%BBB 10%

Not rated3 4%

Cash / Other 2%EUR 6.8bn

Real estate 2%EUR 8.6bn

Equities 7%EUR 33.4bn

Debt instruments 89%EUR 399.6bn

Rating profile2

1) 1H 2011, based on consolidated insurance portfolios (P/C, L/H), Corporate and other2) Excluding self-originated German private retail mortgage loans3) Mostly policyholder loans and registered debentures, all of investment grade quality

Non-investment grade 2%

High-quality investment portfolio

Conservative asset allocation1 High-quality fixed income portfolio

3Success factor

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

7

Shareholders’ equity1

(EUR mn)

1) Excluding non-controlling interests (31.12.10: EUR 2,071mn, 31.03.11: EUR 2,055mn, 30.06.11: EUR 2,074mn)

2) Including F/X3) After non-controlling interests, policyholder participation and tax4) Including derivatives

31.12.10 31.03.11 30.06.11

43,560

28,685

4,000

10,875

-2.2%

44,491

28,685

10,749

5,057

Paid-in capital

Unrealizedgains/losses

Retainedearnings2

Equity markets -30%4

Interest rate +100bps

Interest rate -100bps

Credit loss/migration5

Credit spread6

Interest rate +100bps/equity markets -30%4

Estimation of stress impact on IFRS equity3 (EUR bn)

-4.4

+3.7

-2.1

-2.6

-3.2

-1.1

5) Credit loss/migration (Corporate and ABS portfolio): scenario based on probabilities of default as in 1932, migrations adjusted to mimic recession and assumed recovery rate of 30%

6) Credit spread: 100bps increase in the credit spreads across allrating classes (Corporate and ABS bond portfolio)

28,685

42,615

9,649

4,281

-7.6

F/X USD -10%

4Successfactor

Strong capital position (1)

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

8

Conglomerate solvency1

(EUR bn)

Solvency ratio

+0%-p

173%

31.12.10 30.06.11

41.3

22.9

31.03.11

22.9

39.6

Available fundsRequirement

Conglomerate solvency ratio2

Target range: 150% – 170%

Ratio as of 30.06.11

Equity markets -30%3

Interest rate +100bps

Interest rate -100bps

Credit loss/migration4

NatCat6

Credit spread5

180%

181%

176%

175%

180%

175%

167%

Interest rate +100bps/equity markets -30%3 168%

100%

4) Corporate credit loss/ migration: scenario based on probabilities of default as in 1932, migrations adjusted to mimic recession and assumed recovery rate of 30%

5) Credit spread: 100bps increase in the credit spreads across allrating classes (Corporate and ABS bond portfolio)

6) NatCat: loss due to Cat events, both natural and man-made,leading to claims of EUR 1.5bn. Applies to P/C business only

1) Including off-balance sheet reserves (31.12.10: EUR 2.1bn, 31.03.11:EUR 2.1bn, 30.06.2011: 2.1bn) pro forma. The solvency ratio excludingoff-balance sheet reserves would be 164% as of 31.12.10, 171%as of 31.03.11 and 171% as of 30.06.11

2) After non-controlling interests, policyholder participation and tax3) Including derivatives

180% 180%

41.4

23.0

F/X USD -10% 179%

4Successfactor

Strong capital position (2)

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

9

30.06.1131.03.11

177%

54.6

30.8

+7%-p

Economic solvency1

(EUR bn)

Economic solvency ratioRisk bearing fundsRisk capital

Stress impact2

Ratio as of 30.06.11

Interest rate +100bps

Interest rate -100bps

Equity markets -30%

Equity markets +30%

F/X USD -10%

1) Internal risk capital is calculated at 99.97% confidence level. At the local OE-level we are capitalizing at 99.93% confidence level. Risk bearing funds reflect yield curves and liquidity premium for valuation purposes in line with the current proposal of the European Insurance and Occupational Pensions Authority ("EIOPA") for L/H segment. Before non-controlling interests

2) Estimated solvency ratio changes in case of stress scenarios (stress applied on both risk bearing funds and risk capital)

184%

165%

195%

171%

196%

181%

184%

56.2

30.6

Interest rate -100bps/equity markets -30% 154%

4Successfactor

Strong capital position (3)

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

10

OutlookD

Sovereign debt exposureC

1H 2011B

Allianz at a glanceAAgenda

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

11

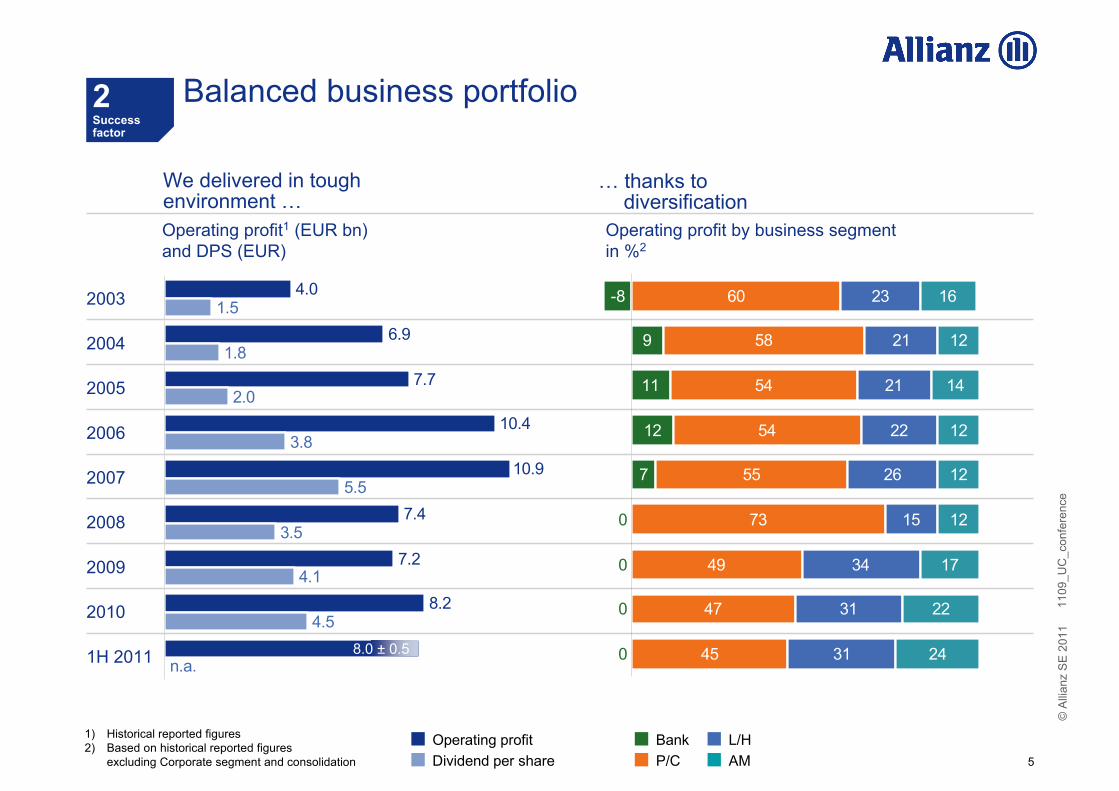

Key developments in 1H 2011

Strong operating profit despite crisis, slightly below previous year due to high NatCat and negative F/X impact

Total revenues EUR 54.5bn (-2.6%)

1H Operating profit EUR 4.0bn (-1.8%)

Shareholders’ equity EUR 42.6bn (-4.2%)

Net income EUR 2.0bn (-28.0%)

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

12

Net income(EUR mn)

Operating profit(EUR mn)

Total revenues(EUR bn)

Quarterly results overview

22.0

-3.2%1

22.225.5

30.625.4

29.9

4Q 1Q2Q 3Q 4Q 1Q 2Q 3Q

2,0551,762 2,009 1,960 1,732

2,302

-0.1%

1,660

1,268

1,8721,390

1,0331,603

1,157

-7.4%

915

2,154

1,181

1) Internal growth -0.9%, adjusted for F/X and consolidation effects

2Q

24.6

2,300

1,071

2009 2010 2011

26.024.5

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

13

P/C 1H 2011: operating profit up 7%

Comments Growth driven by positive volume and

price effects

Operating profit up due to improvement in France, Italy, credit insurance and AGCS

NatCat still at high level (EUR 910mn / 4.7%-p CR)

Accident year loss ratio excluding NatCat steadily improving (<70%)

Operating investment income grew, driven by higher asset base

Positive price effect of 1.0% on our renewed business (+1.5% excluding credit insurance)

Revenues(EUR bn)

Operating profit(EUR mn)

1H 10 1H 11

+2.1%

23.9 24.4

1H 10 1H 11

+7.2%

1,8591,992

98.4 98.1

Combined ratio in %

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

14

Revenues(EUR bn)

L/H 1H 2011: operating profit suffered from impairments

Comments Revenue development impacted by

positive one-offs in 1H 10

Operating asset base up 2%, net inflows EUR 2.1bn

Stable value creation from new business (NBM 2.4%)

Operating profit suffered from impairments on Greek sovereign bonds (EUR 76mn)

Operating profit(EUR mn)

1H 10 1H 11

-7.6%

29.527.2

1H 10 1H 11

-16.8%

1,659

1,381

2.5% 2.4%

Operating asset base (EUR bn)

414 423

New business margin

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

15

3rd party AuM(EUR bn)

1H 10 1H 11

AM 1H 2011: strong contribution to Group performance

Comments Growing AuM drive revenues and

operating profit

Total AuM internal growth of 11.1%

Strong net inflows despite difficult market environment

Share of outperforming assets further increased to outstanding 94% (fixed income) and 65% (equities)

Shift to higher margin products increases AuM driven margin to 40.3bps from 39.1bps

Operating profit(EUR mn)

+1.1%

1,139 1,151

1H 10 1H 11

+7.5%

9821,056

57.4 59.0

Cost-income ratio in %

60.0 33.6

Net inflows (EUR bn)

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

16

OutlookD

Sovereign debt exposureC

1H 2011B

Allianz at a glanceAAgenda

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

17

Greek sovereign bond portfolio impaired to market values 30.6.2011 (EUR mn)

Gross impairments on sovereign bonds

Net income effect from impairments(a/php1, a/tax, b/min)

644 48596

326 41285

AllianzGroup

P/C L/H AllianzGroup

P/C L/H

Operating profit effect from impairments (a/php1)

L/HP/CAllianzGroup

7676 0

Special effectsGreece EUR 92mnFrance EUR 135mn

1) After policyholder participation

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

18

Remaining exposure to peripheral sovereign bonds marked-to-market …

1.8%

Spain1.2%

Total fixed income portfolio1

100% = EUR 399.6bnGreece

0.2%

Portugal0.2%

Ireland0.2%

35%

26%19%

10%

10%

-236

-102

-58

-4

-72

Unrealized loss (net)2

-7267,285Total

-245780Portugal

-195646Ireland

-6782Greece3

-2805,077Spain

Unrealized loss (gross)

Carrying value

Gross exposure (EUR mn)

1) As of June 30, 2011, portfolio discussion is based on consolidated insurance portfolios (P/C, L/H, Corporate and Other, does not include Banking operations)2) After policyholder participation and taxes; based on June 30, 2011 balance sheet figures reflected in accumulated other comprehensive income3) After impairments

Government

OtherBanksCorporateCovered bonds

Government bonds

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

19

Absolute exposure

100% 100% 100%

Carrying value in %

of total investments

Unrealized loss (gross) in % of shareholders'

equity2

Unrealized loss(gross) in % ofrequired FCD solvency cap.2

-1,44436,442Total

-71829,157Italy

-7267,285Sub-total

-2805,077Spain

-6782Greece

-245780Portugal

-195646Ireland

Unrealized loss (gross)Carrying valueEUR mn

1H 2011

Relative exposure1

1.6%

8.1%

1.7%3.4% 3.2%

6.3%All ratios

before phpand tax!

1) Light grey ratios refer to total exposure (peripherals plus Italy)2) Ratios slightly overstated, because net unrealized losses are already deducted from S/H equity

… and low

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

20

OutlookD

Sovereign debt exposureC

1H 2011B

Allianz at a glanceAAgenda

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

21

Our strategy for the next five years:keep proven business model – just get better …

Dimension

Capital efficiency

Growth

External

Internal

External

Internal

Solvency II, rating, market volatility

Discipline, cash flow, dividends, risk management

GDP, demography, emerging markets

Distribution, Global Lines, self-retention

Main levers Mid-term trend

ComplexityExternal

Internal

Transaction opportunities

Disposals, streamlining, Global Lines

ProfitabilityExternal

Internal

Cycle, interest rates, growth, competition, NatCat

Structures, processes, products, channels

1

+One

3

2

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

22

Revenues at EUR 27bn EUR 2.1bn net inflows

EUR 34bn net inflows CIR 59.0%

Please mind the seasonality of the business and our disclaimer1!

Exceptionally high NatCat CR 98.1%

As expected

Total

L/H

AM

Co

P/C 2.04.2 – 4.8

1.42.2 – 2.8

1.1

-0.4

4.0

EUR 7.5 – 8.5bn operating profit expected in 2011

Operating profit (EUR bn)

-0.9 – -1.1

1) Disclaimer: Impact from NatCat, financial markets and global economic development not predictable!

1H 2011 Outlook published 02/11 1H 2011

8.57.5

8.0

1.8 – 2.2

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

23

Summary: Allianz well positioned

Resilient and well diversified business model

High-quality investment portfolio

Strong capital base

Balanced growth opportunities

EUR 7.5bn – 8.5bn operating profit expected in 2011

Well positioned for the

“New Normal”

Appendix

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

25

Investor Relations contacts

Oliver SchmidtHead of Investor Relations

Phone +49 89 [email protected]

Peter Hardy

Phone +49 89 [email protected]

Holger Klotz

Phone +49 89 [email protected]

Reinhard Lahusen

Phone +49 89 [email protected]

Christian Lamprecht

Phone +49 89 [email protected]

Stephanie AldagIR Events

Phone +49 89 [email protected]

Investor Relations

Fax +49 89 [email protected]

Internet

(English): www.allianz.com/investor-relations(German): www.allianz.com/ir

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

26

Financial calendar

November 11, 2011 3rd quarter results 2011

February 23, 2012 Financial press conference for the 2011 fiscal year

February 24, 2012 Analysts’ conference for the 2011 fiscal year

March 23, 2012 Annual Report 2011

May 9, 2012 Annual General Meeting

May 15, 2012 Interim Report 1st quarter 2012

August 3, 2012 Interim Report 2nd quarter 2012

November 9, 2012 Interim Report 3rd quarter 2012

The German Securities Trading Act ("Wertpapierhandelsgesetz") obliges issuers to announce immediately any information which may have a substantial price impact, irrespective of the communicated schedules. Therefore we cannot exclude that we have to announce key figures of quarterly and fiscal year results ahead of the dates mentioned above. As we can never rule out changes of dates, we recommend checking them on the Internet at www.allianz.com/financialcalendar.

1109

_UC

_con

fere

nce

© A

llian

z S

E 2

011

27

Disclaimer

These assessments are, as always, subject to the disclaimer provided below.

Cautionary Note Regarding Forward-Looking StatementsThe statements contained herein may include statements of future

expectations and other forward-looking statements that are based

on management’s current views and assumptions and involve known

and unknown risks and uncertainties that could cause actual results,

performance or events to differ materially from those expressed or

implied in such statements. In addition to statements which are forward-

looking by reason of context, the words “may”, “will”, “should”, “expects”,

“plans”, “intends”, “anticipates”, “believes”, “estimates”, “predicts”,

“potential”, or “continue” and similar expressions identify forward-looking

statements. Actual results, performance or events may differ materially

from those in such statements due to, without limitation, (i) general economic

conditions, including in particular economic conditions in the Allianz Group’s

core business and core markets, (ii) performance of financial markets,

including emerging markets, and including market volatility, liquidity and

credit events (iii) the frequency and severity of insured loss events,

including from natural catastrophes and including the development of loss

expenses, (iv) mortality and morbidity levels and trends, (v) persistency

levels, (vi) the extent of credit defaults, (vii) interest rate levels, (viii) currency

exchange rates including the Euro/U.S. Dollar exchange rate, (ix) changing

levels of competition, (x) changes in laws and regulations, including monetary

convergence and the European Monetary Union, (xi) changes in the policies

of central banks and/ or foreign governments, (xii) the impact of acquisitions,

including related integration issues, (xiii) reorganization measures, and (xiv)

general competitive factors, in each case on a local, regional, national and/ or

global basis. Many of these factors may be more likely to occur, or more

pronounced, as a result of terrorist activities and their consequences. The

company assumes no obligation to update any forward-looking statement.

No duty to updateThe company assumes no obligation to update any information

contained herein.