Embed Size (px)

Citation preview

06/01/2010

1

Euro-Mediterranean Energy Market Integration Project

Germany

France

Lebanon

Belgium

Dr. Albrecht KauppTeam Leader

Solar Electricity for Regional Consumption or Export:

Which way to lean?

This project is funded by the European UnionThis project is funded by the European Union

Team Leader

“The contents of this publication are the sole responsibility of the author and can in no way be taken to reflect the views of the

European Union”.

1

We support all colors of energy in the region such as solar, wind, hydro, coal, oil shale, gas and energy

This project is funded by the European Union

2

, g gyefficiency.

06/01/2010

2

Support for the enhanced integration and the improved security of the

Euro-Mediterranean energy market

This project is funded by the European Union

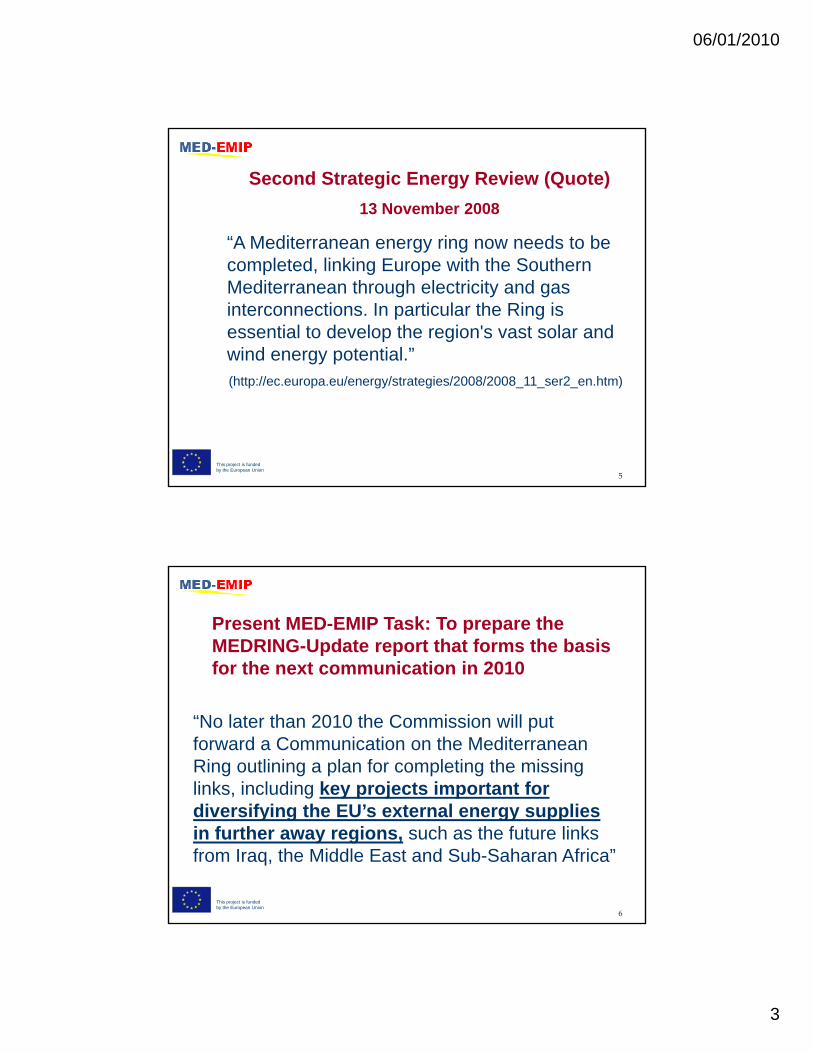

Natural Gas Facts and Figures 2008

EWell price in MENA region $1 - $ 3 per Million BTU Explanation

Henry Hub USA gas price $5 - $8 per Million BTU

Gas from Russia to Europe $ 13 per Million BTU

equivalent to $ 370 /per 1000 m3 (2008)

1 ft3 natural gas = 1000 BTU and 1000 ft3 = 28 m3

1 normal cubic meter gas = GCV 39 MJ = 10 8 kWh

06.01.2010 Seite 4Page 4 4

ns1 normal cubic meter gas = GCV 39 MJ = 10.8 kWh

06/01/2010

3

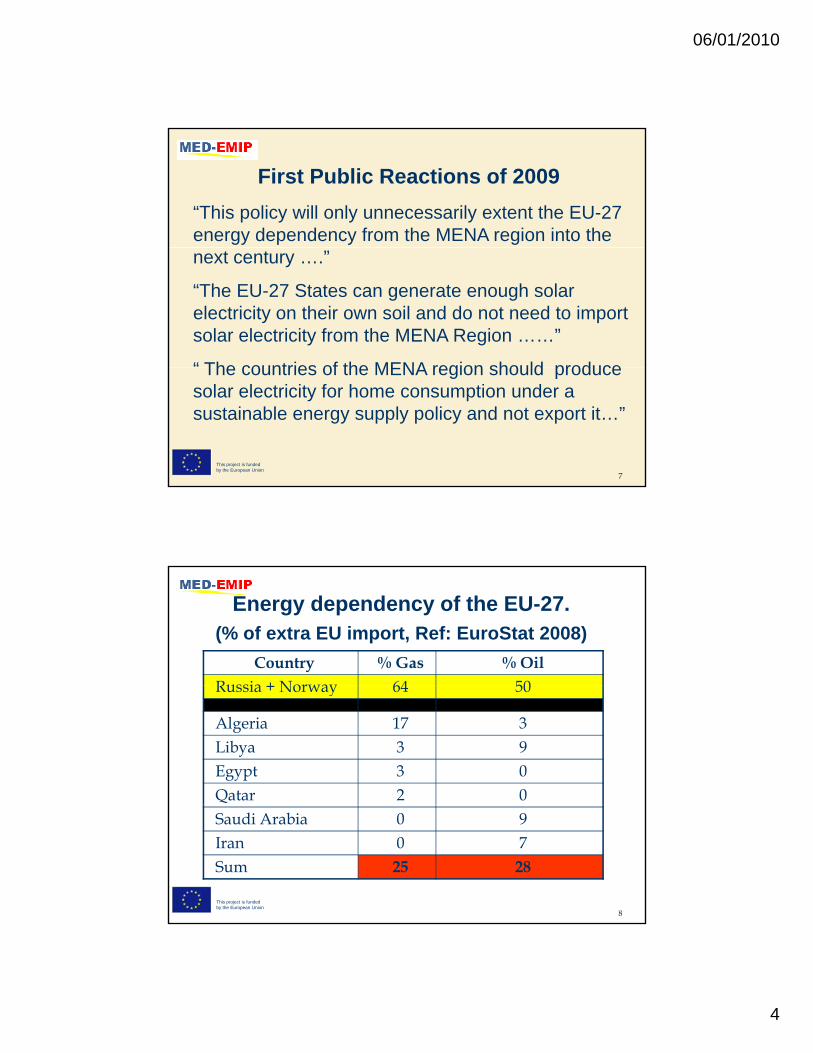

Second Strategic Energy Review (Quote)13 November 2008

“A Mediterranean energy ring now needs to beA Mediterranean energy ring now needs to be completed, linking Europe with the Southern Mediterranean through electricity and gas interconnections. In particular the Ring is essential to develop the region's vast solar and wind energy potential.”

This project is funded by the European Union

5

(http://ec.europa.eu/energy/strategies/2008/2008_11_ser2_en.htm)

Present MED-EMIP Task: To prepare the MEDRING-Update report that forms the basis for the next communication in 2010

“No later than 2010 the Commission will put forward a Communication on the Mediterranean Ring outlining a plan for completing the missing links, including key projects important for di if i th EU’ t l li

This project is funded by the European Union

6

diversifying the EU’s external energy supplies in further away regions, such as the future links from Iraq, the Middle East and Sub-Saharan Africa”

06/01/2010

4

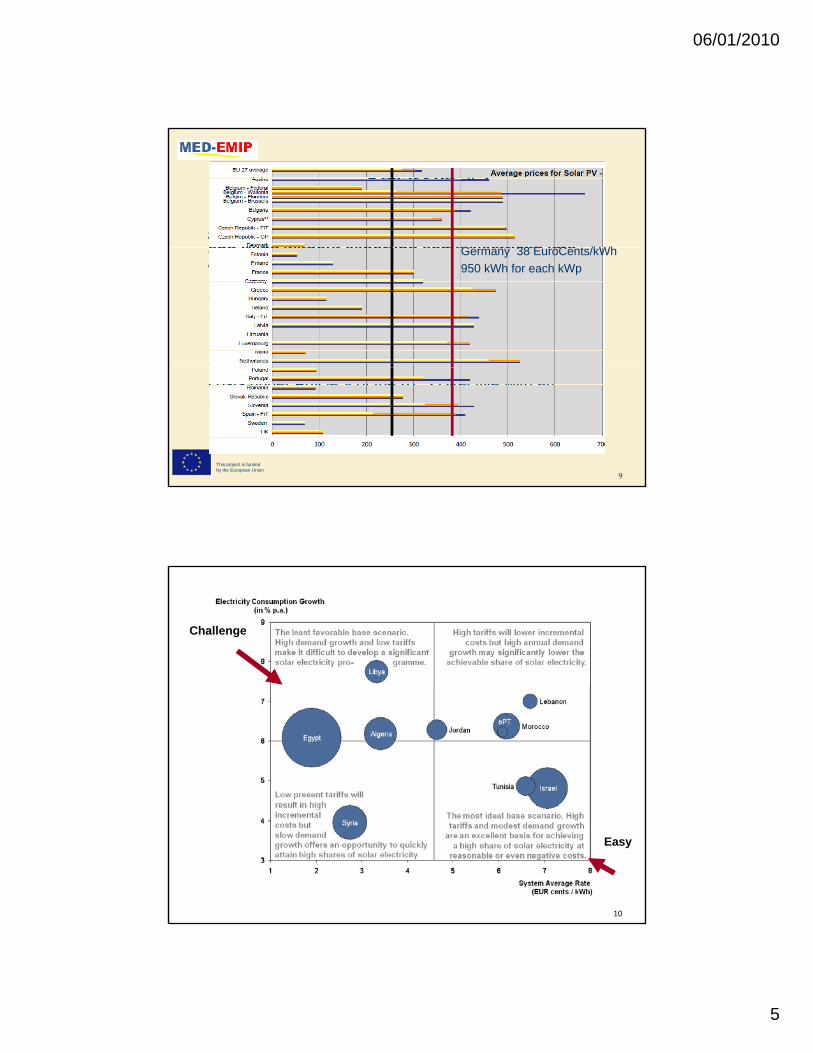

First Public Reactions of 2009“This policy will only unnecessarily extent the EU-27 energy dependency from the MENA region into the next century ….”

“The EU-27 States can generate enough solar electricity on their own soil and do not need to import solar electricity from the MENA Region ……”

“ The countries of the MENA region should produce

This project is funded by the European Union

7

The countries of the MENA region should produce solar electricity for home consumption under a sustainable energy supply policy and not export it…”

Energy dependency of the EU-27.(% of extra EU import, Ref: EuroStat 2008)

Country % Gas % OilRussia + Norway 64 50Russia + Norway 64 50

Algeria 17 3Libya 3 9Egypt 3 0Qatar 2 0

This project is funded by the European Union

8

Saudi Arabia 0 9Iran 0 7Sum 25 28

06/01/2010

5

Key-Issue # 1 Is it possible to built a significant and economically attractive RE based power industry with PV, CSP and Wind without exporting some electricity intoG 38 E C t /kWhand Wind without exporting some electricity into well paying EU markets ?

• Significant is defined as 30% of the electricity generation in 2030 is based on PV, CSP and Wind in a Country of the MENA region .

•Well paying is defined as full cost recovery of supply

Germany 38 EuroCents/kWh950 kWh for each kWp

This project is funded by the European Union

9

Well paying is defined as full cost recovery of supply costs under Article 9 of the RES Directive with an orientation on various feed-in-tariff schemes.

Challenge

10

Easy

06/01/2010

6

Variables and Constants

11

14

16SAR (€¢ / kWh)

CSP, PV, EU 27 Residential

System Average Rates (2008)

Large range of 3 $Cents/ kWh to 10 $Cents/ kWh

4,64

6,086,176,596,69

7,07

6

8

10

12

Wind

EU 27 Industry

g g $ $

1,912,74

3,323,42

0

2

4

LYDZJOoPTMATNMediterranean Partner Countries

EGSYLBIL

Note: Assumed US$-EUR exchange rate: 1.4

06/01/2010

7

AIC (€ million)

-400

400

0

AAIC (€ million)

-4,000

4,000

0

-4,000

4,000

0

AIC (€ million)

-400

400

0

AAIC (€ million)

Favourable scenario Unfavourable scenario

Targ

et

10%

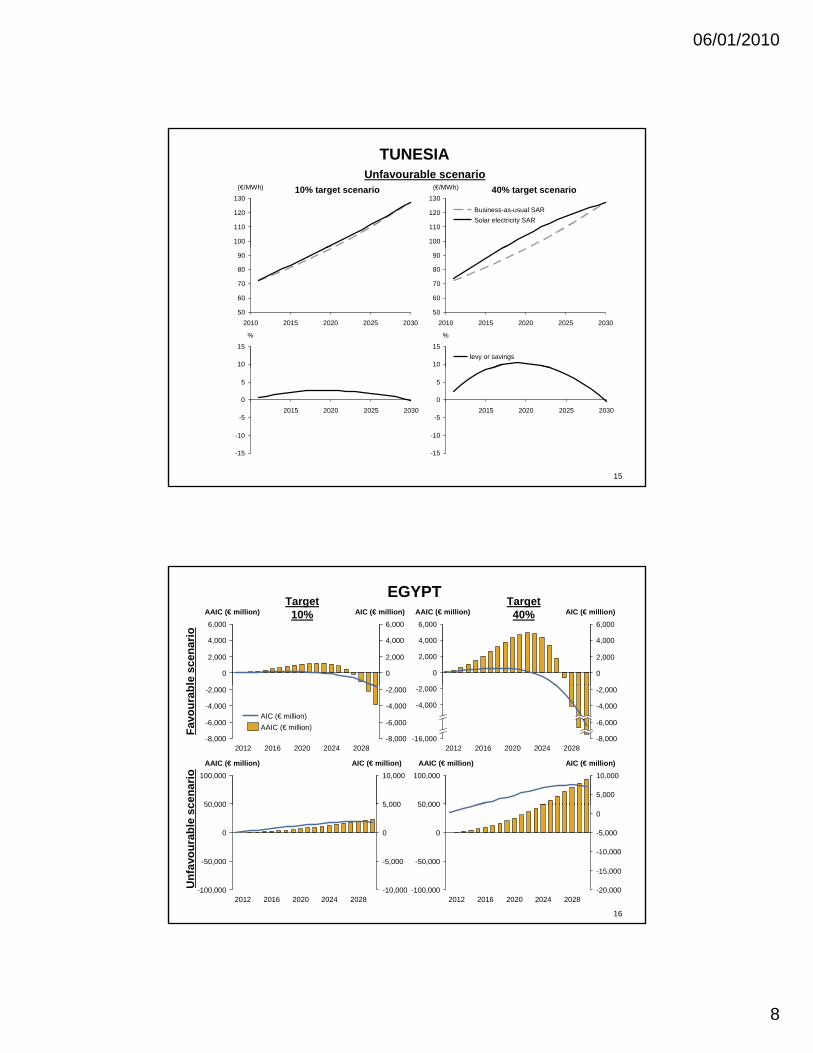

TUNESIA

-800

-1,200

-8,000

-12,00020282024202020162012

-8,000

-12,00020282024202020162012

-800

-1,200AAIC (€ million)AIC (€ million)

AAIC (€ million)AIC (€ million)

AIC (€ million)400

0

AAIC (€ million)4,000

0 0

4,000

AIC (€ million)400

0

AAIC (€ million)

rget

0%

13

-1,200

-800

-400

-8,000

-4,000

-12,00020282024202020162012 2012 2016 2024

-800

-400

2020-1,200

-8,000

-4,000

2028-12,000

Ta 40

AAIC (€ million)AIC (€ million)

AAIC (€ million)AIC (€ million)

TUNESIA

40% target scenario

100

110

120

130(€/MWh)

Solar electricity SARBusiness-as-usual SAR

10% target scenarioFavourable scenario

100

110

120

130(€/MWh)

50

60

70

80

90

202520202015 20302010

10

15%

levy or savings

50

60

70

80

90

202520202015 20302010

10

15%

14

-30

-25

-20

-15

-10

-5

0

5

202520202015 2030

-15

-10

-5

0

5

10

202520202015 2030

06/01/2010

8

TUNESIA

40% target scenario

100

110

120

130(€/MWh)

Solar electricity SARBusiness-as-usual SAR

10% target scenarioUnfavourable scenario

100

110

120

130(€/MWh)

50

60

70

80

90

202520202015 20302010

10

15%

levy or savings

50

60

70

80

90

202520202015 20302010

10

15%

15

-15

-10

-5

0

5

202520202015 2030

-15

-10

-5

0

5

202520202015 2030

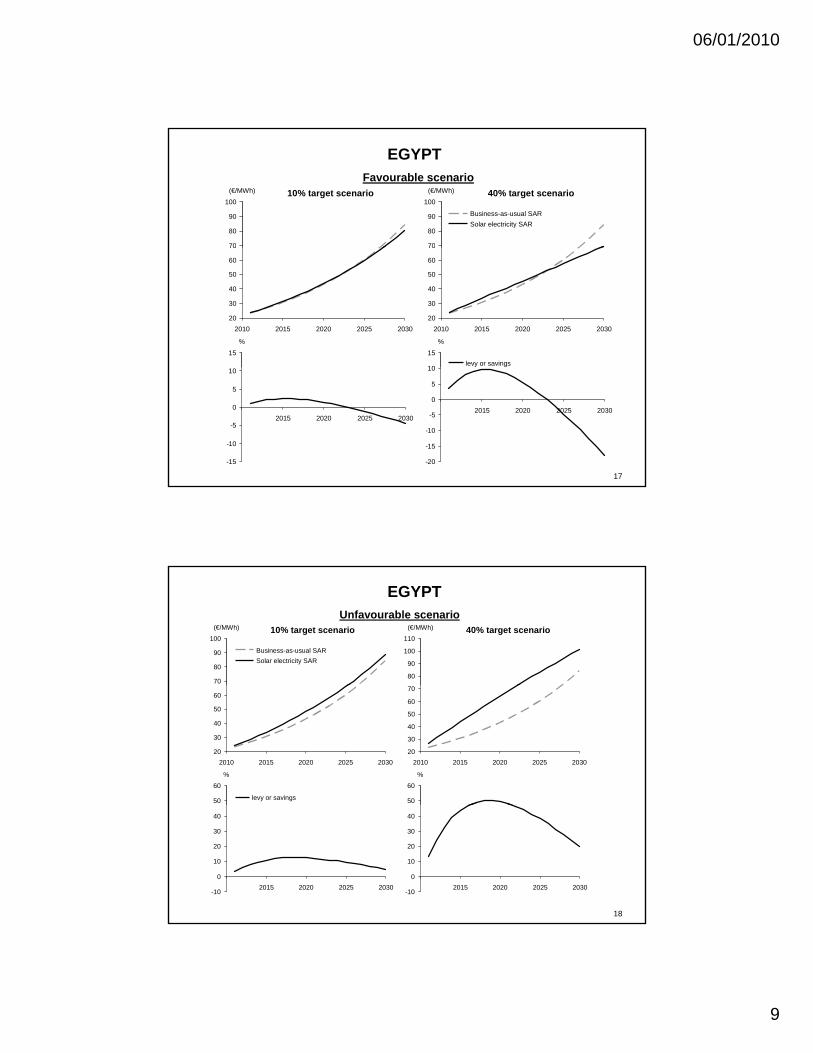

EGYPT

0

AIC (€ million)

0

2,000

4,000

6,000

2,000

4,000

AAIC (€ million)6,000

le s

cena

rio

Target 40%

Target 10%

0

2,000

0

AAIC (€ million) AIC (€ million)

2,000

4,000

6,000

4,000

6,000

2016 20282020 20242012

-2,000

-4,000

-8,000

-6,000

-8,000

-6,000

-4,000

-2,000

AIC (€ million)100,000

5 00050 000

10,000

AAIC (€ million)

AIC (€ million)AAIC (€ million)Fa

vour

ab

100,000

5,00050 000

AAIC (€ million)10,000

AIC (€ million)

-4,000

-16,000

-2,000-2,000

-8,000

-6,000

2020

-4,000

2024 20282012 2016

cena

rio

16

20242016 2020

0

2012 2028

0

-5,000

5,00050,000

-50,000

-100,000 -10,0002016 20242020 20282012

0

-15,000

50,000

-100,000 -20,000

-10,000-50,000

0

-5,000

Unf

avou

rabl

e sc

06/01/2010

9

EGYPT

40% target scenario

70

80

90

100(€/MWh)

Solar electricity SARBusiness-as-usual SAR

10% target scenarioFavourable scenario

70

80

90

100(€/MWh)

20

30

40

50

60

70

202520202015 20302010

10

15%

levy or savings

20

30

40

50

60

70

202520202015 20302010

15%

17

-20

-15

-10

-5

0

5

10

202520202015 2030

-15

-10

-5

0

5

10

202520202015 2030

EGYPT

40% target scenario

80

90

100

110(€/MWh)

Solar electricity SARBusiness-as-usual SAR

10% target scenarioUnfavourable scenario

70

80

90

100(€/MWh)

20

30

40

50

60

70

202520202015 20302010

50

60%

levy or savings

20

30

40

50

60

202520202015 20302010

50

60%

18

-10

0

10

20

30

40

202520202015 2030-10

0

10

20

30

40

202520202015 2030

06/01/2010

10

Key-Issue # 2

Is it technically feasible to run submarine power transmission lines across the M dit S ?Mediterranean Sea ?

YES, but best from Algeria, Morocco, Tunisia and Libya! Egypt is uncertain.

…and at what approximate wheeling

This project is funded by the European Union

19

pp gcosts ?

Costs will be around 1- 2 $Cents/kWh

Technically feasible corridorsRed areas are deeper than 2000 m,

This project is funded by the European Union

20

06/01/2010

11

This project is funded by the European Union

21

This project is funded by the European Union

22

06/01/2010

12

Sending electricity around the Mediterranean Basin may not be the best option

This project is funded by the European Union

23

There are difficulties to achieve 100% AC synchronization and dedicated HVDC lines may be necessary as well

Key-Issue # 3

Are there commercially attractive scenarios for interstate import and export of electricity for the region. ?

Yes in terms of security of supply and increased opportunities to reduce own

l t f t i

This project is funded by the European Union

24

supply costs for some countries

06/01/2010

13

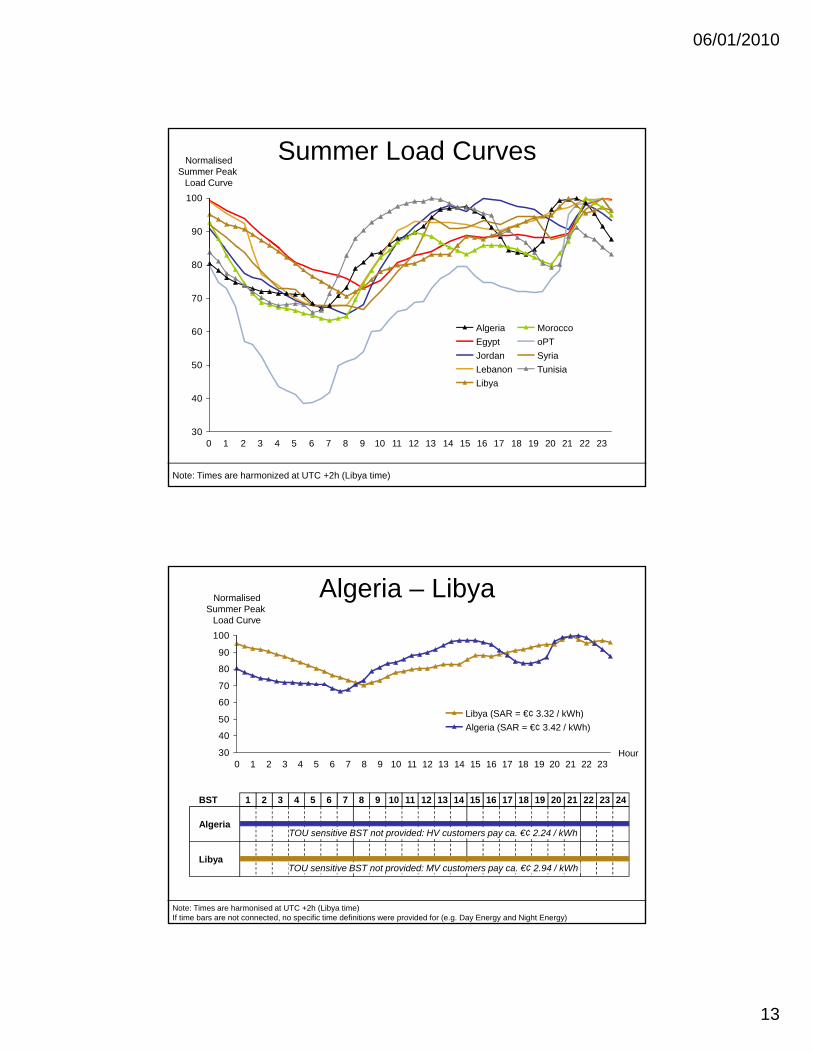

Summer Load Curves

90

100

NormalisedSummer Peak

Load Curve

50

60

70

80

T i iSyriaoPTMorocco

L bJordanEgyptAlgeria

Note: Times are harmonized at UTC +2h (Libya time)

30

40

50

23222120191817161514131211109876543210

TunisiaLibyaLebanon

Algeria – Libya

70

80

90

100

NormalisedSummer Peak

Load Curve

30

40

50

60

70

Hour23222120191817161514131211109876543210

Algeria (SAR = €¢ 3.42 / kWh)Libya (SAR = €¢ 3.32 / kWh)

242322212019181611 12 13 15 171410987654321BST

Note: Times are harmonised at UTC +2h (Libya time)If time bars are not connected, no specific time definitions were provided for (e.g. Day Energy and Night Energy)

TOU sensitive BST not provided: MV customers pay ca. €¢ 2.94 / kWh Libya

AlgeriaTOU sensitive BST not provided: HV customers pay ca. €¢ 2.24 / kWh

06/01/2010

14

The unpleasant news

All countries except for two have moved in the last 4 years into low to very low operational reserve margins because of fast increasing demand and too little capacity addition.

There is little electricity to exchange or to

27

export and it would be also appropriate to invest in demand side management strategies.

28

06/01/2010

15

“Everything should be made as simple as possible, but p p ,

not simpler”(ALBERT EINSTEIN)

THE END

This project is funded by the European Union

29

THE END