Embed Size (px)

Citation preview

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Alaska

October 19, 2011

[email protected] 808-524-6239

[email protected] 818-707-8376

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 2

Workers Compensation Environment

The State of the Economy

State of the Industry

Alaska Workers Compensation System Overview

Claim Frequency

Medical Severity

Prescription Drug Study 2011 Update

Indemnity Severity

Workers Compensation and an Aging Workforce: Is 35 the New ―Older‖ Worker?

The Residual Market in Alaska

NCCI Initiatives

Alaska Workers Compensation State Advisory Forum

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Workers Compensation Environment

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 4

Five workers compensation bills were introduced

• Issues included:

−Presumption of compensability for firefighters

−Mediation and collective bargaining in workers compensation

−Establishing a Workers Compensation Advisory Council

• One workers compensation bill was passed:

−HB 13 establishes parameters for a medical fee schedule

Alaska Legislature—2011

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 5

• State budget issues continue to dominate

• Regulatory turnover continues

• Some states have enacted system reforms

• Misclassification of employees/independent contractors is an ongoing concern

Countrywide Legislative Environment

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 6

Federal Insurance Office (FIO) • Within the Treasury Department

• Michael McRaith has been selected as Director of the Federal Insurance Office (FIO)

• Study of state regulation and recommendations are due January 2012

• Office will monitor the insurance industry to gain expertise

• No supervisory or regulatory authority over ―the business of insurance‖

Insurance Advisory Committee • Created by Treasury to advise FIO and Treasury

• 15 members, including insurers, regulators, public advocates, and others

Wall Street Reform and Consumer Protection Act

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 7

Medicare

• Medicare Secondary Payment (MSP) Act Reporting

• Recent changes in physician fee schedules

Social Security

• The Government Accountability Office (GAO) study on the impact of state workers compensation benefits on the Social Security Disability Insurance (SSDI) program

Reverse offset provisions

Should be completed by the end of 2011

• Administration could require insurance companies to report, so that SSDI could recoup possible overpayments

State Workers Compensation Benefits and Federal Programs

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

The State of the Economy ―Son, this ain’t a dream no more, it’s the real thing‖

Bob Dylan, Street Legal

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 9

Severity of Recession: Output The 2007 Recession Was the Most Severe Post-War Contraction

Severity is measured as the maximum cumulative percentage decline from the onset of the recession (peak of economic activity, as defined by the NBER); output is measured as Real GDP, billions of chained 2000 dollars, seasonally adjusted Recessions are identified by the calendar year in which they started Frequency of observation: quarterly; latest data point available for consideration: Q2/2011 Sources: BEA, www.bea.gov; NBER, www.nber.org/cycles.html

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 10

Severity of Recession: Employment The 2007 Recession Caused Severe Job Losses

Severity is measured as the maximum cumulative percentage decline from the onset of the recession (peak of economic activity, as defined by the NBER); employment is measured as Total Nonfarm, Current Employment Statistics Survey, seasonally adjusted Recessions are identified by the calendar year in which they started Frequency of observation: monthly; latest data point available for consideration: August 2011 Sources: US Bureau of Labor Statistics (BLS), www.bls.gov; NBER, www.nber.org/cycles.html

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 11

The chart shows the number of states for which the one-month change in the coincidence index of economic activity indicates an expansion; this index summarizes the state of the economy in a single statistic, using nonfarm payroll employment, average hours worked in manufacturing, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (US city average); frequency of observation: monthly; latest observation: August 2011; does not include District of Columbia Source: FRB of Philadelphia, www.philadelphiafed.org/research-and-data/regional-economy/indexes/coincident

Number of States Expanding There Is an Elevated Risk of the Current Soft Patch Giving Way to Recession

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 12

Unemployment: Official Rate and U-6 The Unemployment Rate Is More Persistent Than in Past Recoveries

U-6 measures the number of the unemployed and the marginally attached for economic reasons as a percentage of the labor force plus marginally attached; official unemployment rate and U-6 are seasonally adjusted; prior to 1994, U-6 unemployment are estimates from Moody's Analytics Frequency of observation: monthly; latest available data point: August 2011 Sources: Moody’s Analytics, www.economy.com; US Bureau of Labor Statistics (BLS), www.bls.gov

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 13

Employment by Industry Several Sectors Have Added Jobs Since the Onset of the Recovery

Percentage change since the onset of the recovery (trough of economic activity, June 2009) Seasonally adjusted; frequency of observation: monthly; latest observed data point: August 2011 Note that the public school system is part of Government; Educational and Health Services consists primarily of healthcare and social assistance Source: US Bureau of Labor Statistics (BLS): Current Employment Statistics (CES), www.bls.gov/ces

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 14

Employment by Industry Employment Has Yet to Recover From the Recession in Most Industries

Percentage change since the onset of the recession (peak of economic activity, December 2007) Seasonally adjusted; frequency of observation: monthly; latest observed data point: August 2011 Note that the public school system is part of Government; Educational and Health Services consists primarily of healthcare and social assistance Source: US Bureau of Labor Statistics (BLS): Current Employment Statistics (CES), www.bls.gov/ces

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 15

Nonfarm Employment, seasonally adjusted Monthly employment shown for the period November 2001 through August 2011 Sources: FRED, www.research.stlouisfed.org/fred2; US Bureau of Labor Statistics (BLS), www.bls.gov

The Industrial Structure Is Changing Recession as a Catalyst for Change in Employment

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 16

Frequency and Economic Structure The Frequency Decline Is Primarily Due to Workplaces Getting

Safer by Design

Injury and Illnesses Cases per 100 Full-Time Equivalent Workers, Total Recordable Cases, All Private Industry Frequency of observation: annual; latest available data point: 2009; no data points are available for 2001 and 2002 due to changes in industry classification; tick marks indicate beginning of year; data points are mid-year Sources: Bureau of Economic Analysis (BEA), www.bea.gov; US Bureau of Labor Statistics (BLS), www.bls.gov/iif

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 17

Workplace Injuries and Job Tenure Short-Tenured Employees Are Overrepresented Among the Injured

Workplace injuries represent nonfatal injuries and illnesses involving days away from work; short job tenure means 11 months or less (workplace injuries) or 12 months or less (employment); intermediate length of service means 1 to 5 years and 13 months to 4 years, respectively; long length of service means more than 5 years or 5 years or more, respectively; percentages for workplace injuries do not account for a small ―residual category‖; job tenure information for employment is available bi-annually (for January only); percentages may not add to 100 due to rounding Source: US Bureau of Labor Statistics, www.bls.gov

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 18

• During recessions, there are many establishments cutting

jobs (job destruction) and only a few adding jobs (job

creation).

• Job creation means adding employees, who are typically inexperienced in the new job. Because employees with short tenure are overrepresented among the injured, faster job creation (as is observed during economic recoveries) causes frequency to drop less than it would drop otherwise, or even causes frequency to rise temporarily.

• During recessions, the impact of slowing job creation more than offsets the opportunistic filing of workers compensation claims following layoffs.

Frequency and the Business Cycle The Business Cycle Behavior of Frequency Is Driven by Job Creation

For an empirical study on the link between frequency and the business cycle see Schmid, Frank A. (2009) Job Flows and Workplace Injuries, www.ncci.com/Documents/WorkplaceInjuries-0709.pdf

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 19

Labor Force Participation by Age Group

The Labor Force Participation Rate is the share of the population 16 years and older working or seeking work; the population is defined as noninstitutionalized civilian; persons seeking work are defined as those who have actively looked for work in the past four weeks; baby boomers are defined as persons born in the years 1946 through 1964 Frequency of observation: annual; latest available data point: 2010 Source: US Bureau of Labor Statistics (BLS), www.bls.gov

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 20

Labor Force Participation and Job Tenure Changing Participation Patterns Contribute to a Lengthening of Job Tenure

The Labor Force Participation Rate is the share of the population 16 years and older working or seeking work; the population is defined as noninstitutionalized civilian; persons seeking work are defined as those who have actively looked for work in the past four weeks Median job tenure is available for even calendar years only, and only for January; for some age groups, median job tenure was obtained by taking the mean across two or more age sub-groups; frequency of observation: annual (participation rate) and bi-annual (job tenure), January; latest available data point: 2010 Source: US Bureau of Labor Statistics (BLS), www.bls.gov/cps

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 21

Median Unemployment Duration Half of the Unemployed Have Been Out of Work for More Than Five Months

The median unemployment duration is based on seasonally adjusted data Frequency of observation: monthly; latest available data point: August 2011 Source: US Bureau of Labor Statistics (BLS), www.bls.gov

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 22

Alaska Employment Increased During the Past Three Recessions

Percentage change from the onset of the recession (peak of economic activity, as defined by the NBER) to the onset of the recovery (trough of economic activity); Current Employment Statistics Survey, seasonally adjusted Frequency of observation: monthly; range of US states includes District of Columbia Source: US Bureau of Labor Statistics (BLS), www.bls.gov/ces

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 23

Alaska Employment Growth Is More Robust Than Most of the United States

Nonfarm Employment, seasonally adjusted Frequency of observation: monthly; latest available data point: August 2011; range of US states includes District of Columbia Tick marks indicate beginning of year Source: US Bureau of Labor Statistics (BLS), www.bls.gov

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 24

Alaska Many Sectors Have Added Jobs Since the Onset of the Recovery

Percentage change since the onset of the recovery (trough of economic activity, June 2009); Current Employment Statistics Survey, seasonally adjusted; frequency of observation: monthly; latest observed data point: August 2011 Source: US Bureau of Labor Statistics (BLS), www.bls.gov/ces

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 25

Alaska Employment Is Above Pre-Recession Level in Most Industries

Percentage change since the onset of the recession (peak of economic activity, December 2007); Current Employment Statistics Survey, seasonally adjusted; frequency of observation: monthly; latest observed data point: August 2011 Source: US Bureau of Labor Statistics (BLS), www.bls.gov/ces

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 26

Alaska The Change in Industrial Structure Is Comparably Mild

Nonfarm Employment, seasonally adjusted Monthly employment shown for the period November 2001 through August 2011 Sources: US Bureau of Labor Statistics (BLS), www.bls.gov; Moody’s Economy.com

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 27

Alaska The Unemployment Rate Is Well Below the National Average

Unemployment rate, seasonally adjusted; range of US states includes District of Columbia Frequency of observation: monthly; latest available data point: August 2011 Source: US Bureau of Labor Statistics (BLS), www.bls.gov

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 28

Alaska The Private Sector BLS Injury and Illness Rate Is Above Average

Injury and Illnesses Cases per 100 Full-Time Equivalent Workers, Total Recordable Cases, All Private Industry Frequency of observation: annual; latest available data point: 2009 Range of US states includes District of Columbia Source: US Bureau of Labor Statistics (BLS), www.bls.gov/iif

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 29

• For the nation, economic growth is slow and is likely to remain sub-par for several years into the future

– Job creation is tepid (and is likely to remain so)

– As a consequence, upward pressure on frequency is limited

– Alaska is an exception—although growth slowed during the 2007 recession, the economy showed little signs of contracting

• Inflationary forces are weak, due to significant excess industrial capacity and high unemployment

– Medical care price inflation and wage inflation are likely to be muted

Implications for Workers Compensation

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 30

• Prior to the recession, economic growth was fueled to a large extent by a continually decreasing personal saving rate

– Private household deleveraging and the ensuing sluggish consumption growth portends a slow pace of economic expansion

• High government debt may depress economic growth

– Households anticipate tax increases and cutbacks in entitlements, which gives them an incentive to increase the saving rate, which places additional drag on consumption growth

– Businesses anticipate tax increases

• The financial crises raised government debt levels in many developed countries

– There is a non-negligible risk of sovereign default (and a potential replay of the 2007–2008 financial crisis)

Challenges for the US Economy

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

State of the Industry

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 32

• Calendar year and accident year combined ratios continue to deteriorate

• Decline in lost-time claim frequency stopped in 2010

• More increases proposed in latest NCCI filing cycle

• Impact of healthcare reform and federal involvement in insurance remains uncertain

State of the Workers Compensation Market

―Deteriorating‖

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 33

Workers Compensation Premium Decline Moderates

Net Written Premium

26.1 29.2

31.1

34.7 37.8 38.6 37.6

33.8

30.3 29.9

32.1

37.7

42.3

46.5 47.8

46.5 44.3

39.3

34.6 33.8

4.1 4.1 4.2 4.5 4.7 5.0 5.3 5.4 5.1 5.2

0

5

10

15

20

0

10

20

30

40

50

60

70

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

State Funds ($ B)

Private Carriers ($ B)

Private Non-Farm Wages and Salaries

Premium

$ Billions

Calendar Year p Preliminary Sources: 2001–2009 Private Carriers, Annual Statement data; 2010p, NCCI 2001–2010p State Funds: AZ, CA, CO, HI, ID, KY, LA, MD, MO, MT, NM, OK, OR, RI, TX, UT Annual Statements

Wages

$ Trillions

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 34

Countrywide Impact of Discounting on Workers Compensation Premium

NCCI States—Private Carriers

-7.1 -7.4 -7.1 -8.5

-10.5

-14.6

-17.7

-22.6 -23.2

-19.2

-14.3

-4.0 -1.7

2.1 0.7

-2.2

-4.7 -7.4 -8.2 -9.2

-25

-20

-15

-10

-5

0

5

10

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Rate/Loss Cost DepartureSchedule RatingDividends

Policy Year p Preliminary Dividend ratios are based on calendar year statistics NCCI benchmark level does not include an underwriting contingency provision Based on data through 12/31/2010 for the states where NCCI provides ratemaking services

Percent

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 35

Countrywide Average Approved Bureau Rates/Loss Costs

History of Average WC Bureau Rate/Loss Cost Level Changes

* Preliminary Countrywide approved changes in advisory rates, loss costs, and assigned risk rates as filed by the applicable rating organization

12.1

7.4

10.0

2.9

-6.4

-3.2

-6.0

-8.0

-5.4

-2.6

3.5

1.2

4.9

6.6

-6.0 -5.1

-5.7 -6.6

-3.1 -2.0

-1.1

0.2

-10

-5

0

5

10

15

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Percent

Calendar Year

Cumulative 1994–1999

–27.8%

Cumulative

1990–1993

+36.3%

Cumulative 2000–2003

+17.1%

Cumulative 2004–2010

–26.2%

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 36

Status of NCCI Filing Activity Voluntary Market Filings

30 28

21

7

1 0 0 0

5

8

16 17

0

5

10

15

20

25

30

2008/2009 Season 2009/2010 Season 2010/2011 Season 2011/2012 Season

Nu

mb

er

of

Sta

tes

Less than 0% No Filing 0% and greater

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 37

-9.8

-8.1

-7.5

-5.8

-5.6

-4.5

-3.9

-3.7

-3.7

-3.0

-2.6

-1.8

-1.7

0.6

1.2

3.6

3.7

4.2

4.4

5.2

6.2

7.4

-9.3

-3.2

-0.3

1.4

1.5

1.6

1.7

2.3

2.7

3.5

3.7

4.5

5.2

6.7

8.9

10.5

-25

-20

-15

-10

-5

0

5

10

15

MS AL WVKY AR MT NE NV GA SC MEMO VT OROK TX NC SDMD UT TN KS IN AK IL RI CO ID LA IA CT AZ HI DC NHNM FL VA

Approved Pending

Current NCCI Voluntary Market Filed Rate/Loss Cost Changes

Excludes Law-Only Filings

Percent

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 38

New Mexico 1/1/12 +7.4%

Arizona 1/1/12 +5.2%

Hawaii * 1/1/12 +5.2%

Colorado* 1/1/12 +3.7%

Idaho 1/1/11 +3.7%

Alaska* 1/1/12 +2.7%

Utah* 12/1/11 +1.5%

California 1/1/11 0.0%

Oregon 1/1/11 -1.8%

Nevada 3/1/11 -3.9%

Montana 7/1/11 -5.6%

State Voluntary Market Filed Rates/Loss Costs

Western NAIC Zone

* Pending

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 39

Alaska* 1/1/12 +2.9%

Nevada 3/1/11 -2.2%

Oregon 1/1/11 -1.8%

New Mexico 1/1/12 -5.0%

Residual Market Filings Western NAIC Zone

* Pending

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 40

-10.9

-4.8

-2.9

-10.3

-2.5

2.7

-13.7

-5.2

-2.9

-9.9

-0.4

2.9

-15

-10

-5

0

5

10

1/1/2008 1/1/2009 5/1/2009 1/1/2010 1/1/2011 1/1/2012Pending

Pe

rce

nt

Effective Date

Voluntary Assigned Risk

Alaska’s Filing Activity

Voluntary Loss Cost and Assigned Risk Rate Changes

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 41

Alaska January 1, 2012 Filing Average Changes by Industry Group

Manufacturing

+2.8%

Contracting

-0.1%

Office & Clerical

+4.3%

Goods & Services

+4.3%

Miscellaneous

+2.9%

Oil & Gas

-1.8%

OVERALL +2.7%

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 42

157

216 242

302

337 347 333

285

256 235

7.6 8.0 8.3 8.8 9.3 9.9 10.6 11.3 11.5 11.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

0

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Written Premium

Private Non-FarmWages and Salaries

Alaska’s Workers Compensation Premium Volume

Direct Written Premium

Premium

$ Millions

p Preliminary Source: NAIC Annual Statement data Bureau of Economic Analysis

Calendar Year

Wages

$ Billions

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 43

-26.4

-7.0 -11.0

2.0

11.1 14.0 14.7 9.2 5.1

-0.2

0.3

-0.2

-30

-20

-10

0

10

20

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Pe

rce

nt

Policy Year

Rate/Loss Cost Departure Schedule Rating Dividends

The Impact on Premium of Rate/Loss Cost Departures, Schedule Rating, and

Dividends in Alaska

Based on data through 12/31/2010 Dividend ratios are based on calendar year statistics

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 44

Current Average Voluntary Pure Loss Costs Using Alaska’s

Payroll Distribution

2.11

1.58 1.52

0

1

2

3

AK REG CW

Pu

re L

os

s C

os

t—A

ll C

las

se

s

State

Regional states are AZ, MT, NM, and OR Based on the latest NCCI approved rates and loss costs in the various states

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 45

1.020

3.100

3.330

0.0

1.0

2.0

3.0

4.0

5.0

6.0

ND IN AR DC VA CO UT MA KS MD OR FL HI AZ WY IA WV DE MO NM MS NE ID RI SD WA LA GA NC MI NV TN WI VT OH MN KY PA NY SC TX AL NH ME NJ CT CA OK IL AK MT

Workers Compensation Premium Rate Ranking

Premium Rate Index per $100 of Payroll

Source: 2010 Oregon Workers’ Compensation Premium Rate Ranking Summary Indexes based on rates in effect on January 1, 2010

AK Ranking

50th (out of 51).

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 46

0.649

1.088

1.688

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

ND AL WY NY FL KS MS MN NM GA MT AR UT NJ IN MO TN CA SC AZ WV LA NH OR CO OK NC SD NE MD MI ME OH ID AK HI VA KY TX DE WI WA VT CT IA IL PA RI NV MA

Average Statutory Benefit Provisions

(Indemnity only; as of 1/1/2008)

1.0 represents countrywide average cost

per case (indemnity only). All states

indexed to countrywide average.

AK Ranking

35th (out of 50).

All states based

on rates in effect

on 1/1/2008.

Source: Workers Compensation State Rankings, Manufacturing Industry Costs, and Statutory Benefit Provisions, 2008 Ed., Prepared by Actuarial & Technical Solutions, Inc.

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 47

$85

$342

$457

$0

$100

$200

$300

$400

$500

$600

IN AR AZ UT DC TX FL AL VA KS WI SD NE NH KY MS ID MO NM MI OR TN CO IA MN MD HI GA MA ME LA CA SC NC NJ DE VT RI PA MT NY AK NV CT IL OK

Actual Average Indemnity Benefits per Employee per Year

(Cost spread over all employees whether or not injured)

AK Ranking

42nd (out of 46).

Source: NCCI’s Statistical Plan data at first report for policies effective in 2006 and 2007

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 48

$109

$679

$1,007

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$1,100

DC MA RI NY HI MI AR IN NC CO TX MD SC GA VA MO ME IA NM KS OR FL WI ID UT NE LA PA MS AZ TN NV NJ CT OK IL VT KY MN AL NH SD CA DE AK MT

Actual Average Medical Benefits per Employee per Year

(Cost spread over all employees whether or not injured)

AK Ranking

45th (out of 46).

Source: NCCI’s Statistical Plan data at first report for policies effective in 2006 and 2007

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 49

$226

$1,021

$1,334

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

DC IN AR TX VA MA MI UT AZ FL KS HI MO WI CO NE NM MD ID MS GA IA OR RI NC SC ME KY AL TN NY NH LA SD MN NJ PA VT NV CT IL CA OK DE AK MT

Actual Average Total Benefits per Employee per Year

(Cost spread over all employees whether or not injured)

AK Ranking

45th (out of 46).

Source: NCCI’s Statistical Plan data at first report for policies effective in 2006 and 2007

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 50

Alaska Policy Year Combined Ratios

95%

103% 108%

117%

144%

155% 151%

130%

106%

100%

84%

70% 73%

81% 85%

60%

80%

100%

120%

140%

160%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Co

mb

ine

d R

ati

o

Policy Year

Source: NCCI financial data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 51

Alaska Accident Year Combined Ratios

80%

66%

78%

84% 83%

0%

20%

40%

60%

80%

100%

2005 2006 2007 2008 2009

Co

mb

ine

d R

ati

o

Accident Year Sources: NCCI financial data, NAIC Annual Statement data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 52

Countrywide WC Calendar Year Combined Ratio Continues to Deteriorate

Private Carriers

117 123 121

109

102 97 100 101

107

115 118

122

111 110 107 103

93

101 101

110 115

0

20

40

60

80

100

120

140

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Dividends Underwriting Expense LAE Loss

Percent

Calendar Year

p Preliminary Source: 1990–2009, Annual Statement Data; 2010p, NCCI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 53

Countrywide Accident Year Combined Ratios

Workers Compensation Calendar Year vs. Ultimate Accident Year Private Carriers

122

111 110 107

103

93

101 101

110

115

125

106

97

88 87 86

98

104

109

114

80

90

100

110

120

130

140

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Calendar Year Accident Year

Percent

p Preliminary Accident Year data is evaluated as of 12/31/2010 and developed to ultimate Sources: Calendar Years 2001–2009, Annual Statement data; Calendar Year 2010p and Accident Years 2001–2010, NCCI analysis based on Annual Statement data Includes dividends to policyholders

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 54

83

126

0

20

40

60

80

100

120

140

AK TX AR,DC

HI,MO

KS,NM

AL,NE

MS IN,VA

NV ME,SD,VT

SC LA,NC,TN

UT MT,OK

ID,IA

FL KY IL AZ,MD

NH CT,GA

CO OR RI

Results Vary From State to State

Accident Year 2009 Combined Ratios

Data is evaluated as of 12/31/2009

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Alaska Workers Compensation

System Overview

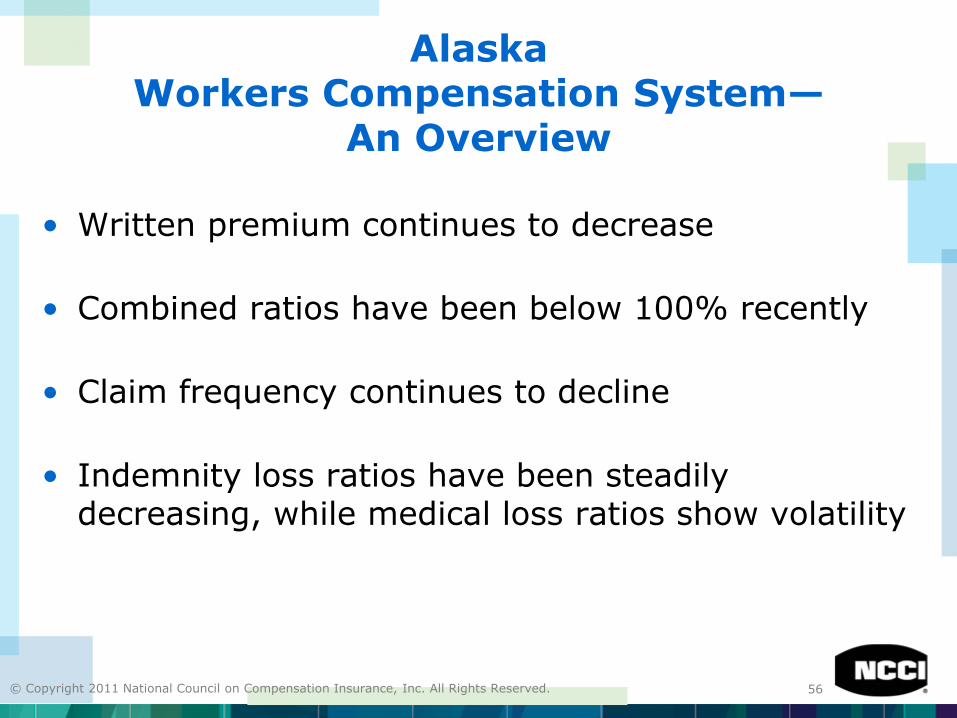

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 56

• Written premium continues to decrease

• Combined ratios have been below 100% recently

• Claim frequency continues to decline

• Indemnity loss ratios have been steadily decreasing, while medical loss ratios show volatility

Alaska Workers Compensation System—

An Overview

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 57

0.62 0.62 0.56

0.60 0.63 0.69

0.61

0.47 0.45 0.40

0.30 0.38 0.35

0.30 0.28

0.71 0.68 0.68

0.81 0.86

0.92 0.93

0.83 0.90

0.78

0.68

0.84 0.81

0.76 0.73

0.0

0.2

0.4

0.6

0.8

1.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Lo

ss

Rati

o

Policy Year

Indemnity Medical

Alaska’s Indemnity and Medical Loss Ratios

Based on NCCI’s financial data at current benefit level and developed to ultimate

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Claim Frequency

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 59

-4.2 -4.4

-9.2

0.3

-6.5

-4.5

0.5

-3.9

-2.3

-4.5

-6.9

-4.5 -4.1

-3.7

-6.6

-4.5

-2.1

-4.1

-5.5

3.0

-10

-8

-6

-4

-2

0

2

4

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Percent Change

Accident Year

Countrywide Workers Compensation Lost-Time Claim Frequency

Increased in 2010

Lost-Time Claims

Cumulative Change of –56.4%

(1991–2009)

2010p: Preliminary based on data valued as of 12/31/2010 1991–2009: Based on data through 12/31/2009, developed to ultimate Based on the states where NCCI provides ratemaking services, including state funds; excludes high deductible policies Frequency is the number of lost-time claims per $1M wage-adjusted pure premium at current voluntary level Frequency changes are adjusted for payroll audits

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 60

Alaska Claim Frequency

30

16

10

15

20

25

30

35

40

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Fre

qu

en

cy p

er

Mil

lio

n

of

On

-Le

ve

led

Pre

miu

m

Policy Year

Based on NCCI’s financial data Frequency of lost-time claims

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 61

18

15

22

19

14

16

18

20

22

24

2005 2006 2007 2008 2009

Fre

qu

en

cy p

er

$1

M

Pu

re P

rem

ium

Accident Year

Alaska Countrywide

Alaska vs. Countrywide Claim Frequency

Frequency of lost-time claims Source: NCCI financial data

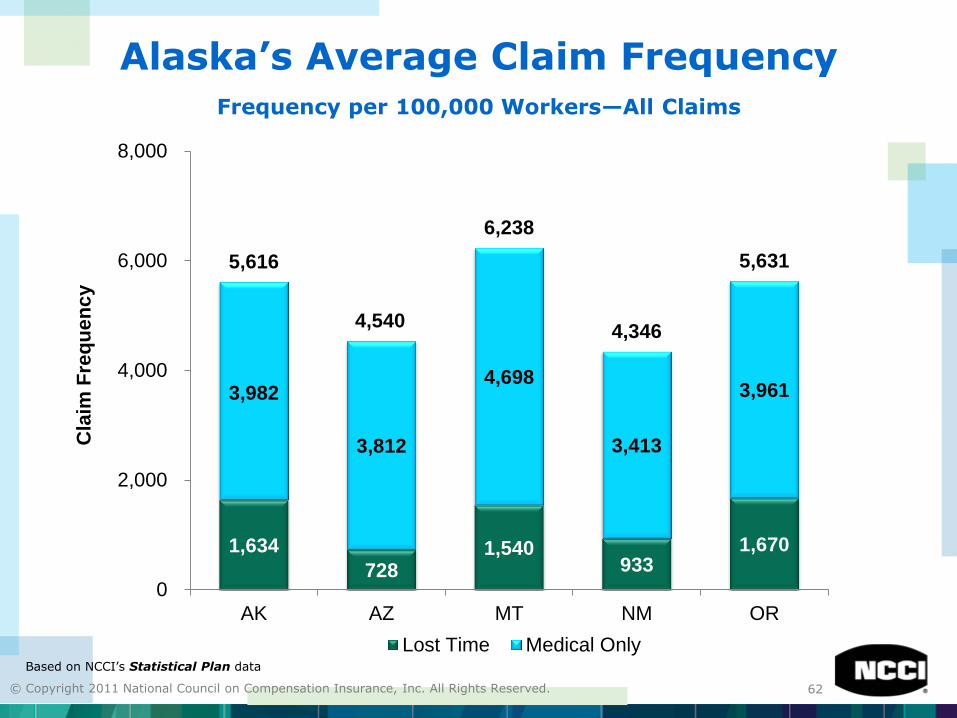

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 62

Alaska’s Average Claim Frequency

Frequency per 100,000 Workers—All Claims

1,634

728 1,540

933 1,670

3,982

3,812

4,698

3,413

3,961

5,616

4,540

6,238

4,346

5,631

0

2,000

4,000

6,000

8,000

AK AZ MT NM OR

Cla

im F

req

ue

nc

y

Lost Time Medical OnlyBased on NCCI’s Statistical Plan data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 63

Alaska’s Distribution of Claims by Injury Type

70.9%

20.4%

8.6% 0.1%

76.4%

14.6%

8.8% 0.2%

Alaska

Temporary Total Permanent Partial Permanent Total/Fatal Medical Only

76.5%

14.5%

8.9% 0.1%

Regional Average Countrywide

Regional states are AZ, MT, NM, and OR Based on NCCI’s Statistical Plan data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 64

Percent of Lost-time Claims Closed

At First Report

74.8%

62.6%

55%

60%

65%

70%

75%

80%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

% C

laim

s C

los

ed

Policy Year

Based on NCCI’s financial data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 65

04/03 - 03/04 04/04 - 03/05 04/05 - 03/06 04/06 - 03/07 04/07 - 03/08

Permanent Total/Fatal 0.5% 0.4% 0.4% 0.7% 0.5%

Permanent Partial 21.9% 24.4% 27.7% 30.1% 29.5%

Temporary Total 77.7% 75.2% 71.9% 69.2% 70.0%

0%

20%

40%

60%

80%

100%

Pe

rce

nt

Policy Period

Alaska’s Distribution of Lost-Time Claims by Injury Type Over Time

Source: NCCI’s 2011 Annual Statistical Bulletin Based on NCCI’s Statistical Plan data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Medical Severity

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 67

Medical/Indemnity Cost Distribution Comparison

76%

25%

Indemnity Medical

66%

34%

59%

41%

Regional Average Countrywide

Alaska

Regional states are AZ, MT, NM, and OR

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 68

$8

.2

$8

.4

$8

.2

$8

.9

$9

.4

$1

0.1

$11

.1

$1

2.0

$1

3.3

$1

4.2

$1

6.2

$1

7.6

$1

8.9

$2

0.0

$2

1.8

$2

3.1

$2

4.5

$2

5.7

$2

7.1

$2

7.7

+6.8% +1.3% -2.1% +9.0% +5.1%

+7.4% +10.1%

+8.3% +10.6%

+7.3%

+13.5% +8.8%

+7.7% +5.4%

+9.1% +6.1%

+6.1% +5.0%

+5.4% +2%

5

10

15

20

25

30

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Accident Year

Accident Year

Annual Change 1991–1993: +1.9%

Annual Change 1994–2001: +8.9%

Annual Change 2002–2009: +6.7%

Medical

Claim Cost

($ '000s)

2010p: Preliminary based on data valued as of 12/31/2010 1991–2009: Based on data through 12/31/2009, developed to ultimate Based on the states where NCCI provides ratemaking services, including state funds Excludes high deductible policies

Countrywide Workers Compensation Medical Claim Cost Trends

Average Medical Cost per Lost-Time Claim

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 69

Countrywide Workers Compensation Medical Severity Lags Medical Inflation

Average Medical Cost per Lost-Time Claim

5.1

7.4

10.1

8.3

10.6

7.3

13.5

8.8

7.7

5.4

9.1

6.1 6.1

5.0 5.4

2

4.5

3.5

2.8 3.2 3.5

4.1 4.6 4.7

4.0 4.4 4.2 4.0

4.4 3.7

3.2 3.4

0

2

4

6

8

10

12

14

16

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Change in Medical Cost per Lost-Time Claim

Change in Medical CPI

Year

Based on the states where NCCI provides ratemaking services, including state funds; excludes high deductible policies Sources: Medical CPI—All states, Moody’s Economy.com; Accident year medical severity—NCCI states, NCCI

Percent Change

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 70

Alaska’s Average Medical Severity

16.1

25.2

15.4

4

9

14

19

24

29

34

39

44

49

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Me

dic

al A

ve

rag

e

Cla

im S

eve

rity

($

'0

00

s)

Policy Year

Adjusted to Current Wage Level Actual

Based on NCCI’s financial data for lost-time claims at current benefit level and developed to ultimate

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 71

31

47

23

28

15

20

25

30

35

40

45

50

2006 2007 2008 2009 2010*

Co

st

pe

r C

as

e (

$ '0

00

s)

Accident Year

Alaska Countrywide

Alaska vs. Countrywide Average Medical Claim Severity

* Countrywide figure is preliminary Source: NCCI financial data valued as of 12/31/2010

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 72

Alaska’s Medical Loss Distribution by Injury Type

10.9%

17.0%

72.1%

0.0%

12.7%

14.9%

57.1%

15.3%

Alaska

Temporary Total Permanent Partial Permanent Total/Fatal Medical Only

11.9%

17.4%

59.1%

11.6%

Regional Average Countrywide

Regional states are AZ, MT, NM, and OR Based on NCCI’s Statistical Plan data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 73

04/03 - 03/04 04/04 - 03/05 04/05 - 03/06 04/06 - 03/07 04/07 - 03/08

Medical Only 9.0% 10.9% 8.1% 8.7% 10.9%

Permanent Total/Fatal 16.9% 1.2% 23.2% 17.0% 0.0%

Permanent Partial 53.9% 66.0% 52.4% 59.3% 72.1%

Temporary Total 20.2% 21.9% 16.3% 15.1% 17.0%

0%

20%

40%

60%

80%

100%

Pe

rce

nt

Policy Period

Alaska’s Distribution of Medical Losses by Injury Type Over Time

Source: NCCI’s 2011 Annual Statistical Bulletin Based on NCCI’s Statistical Plan data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Prescription Drug Study 2011 Update

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 75

• The indicated Rx share of total medical is 19%; this is slightly higher than the estimate given in our 2010 update

• Recent overall cost increases are driven more by utilization increases than by price increases

• Physician dispensing continues to increase in Service Year 2009 in almost every state

• Increased physician dispensing is associated with

increased drug costs per claim

Key Findings

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 76

The Indicated Rx Share of Total Medical Is Slightly Elevated From the Last Study

18% 19% 19%

14.1% 14.2% 14.2%

18% 18%

13% 13%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Es

tim

ate

d R

x S

ha

re o

f

To

tal M

ed

ica

l a

t U

ltim

ate

Injury Year

Best Estimate(Current Study)

Not Trended(Current Study)

Best Estimate(Prior Study)

Not Trended(Prior Study)

Source: Derived from sample data provided by carriers Aggregation of states where NCCI provides ratemaking services, excludes WV, plus CA, DE, MA, MI, MN, NJ, NY, PA, and WI Prior Study: Workers Compensation Prescription Drug Study—2008 Update, available at ncci.com

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 77

Top Drugs for Service Year 2009

Rank Based on Total Dollars Paid in Workers Compensation

Paid Share

Service Year

2009 Drug Name Service Year

2009 2008 2007

6.1% OXYCONTIN® 1 3 8

5.2% LIDODERM® 2 2 2

5.1% HYDROCODONE-ACETAMINOPHEN 3 1 1

4.4% LYRICA® 4 4 4

3.7% CELEBREX® 5 5 3

3.4% GABAPENTIN 6 6 5

2.8% SKELAXIN® 7 7 7

2.7% CYMBALTA® 8 8 13

2.3% MELOXICAM 9 11 15

2.3% CYCLOBENZAPRINE HCL 10 9 9

2.1% TRAMADOL HCL 11 10 10

2.0% OMEPRAZOLE 12 15 18

1.8% FENTANYL 13 12 14

1.5% FLECTOR® 14 28 >1000

1.4% OXYCODONE HCL 15 13 6

Source: Derived from sample data provided by carriers Aggregation of states where NCCI provides ratemaking services, excludes WV, plus CA, DE, MA, MI, MN, NJ, NY, PA, and WI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 78

Utilization Continues to Be a Major Cost Driver

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2000-2001

2001-2002

2002-2003

2003-2004

2004-2005

2005-2006

2006-2007

2007-2008

2008-2009p

Pe

rce

nta

ge

Ch

an

ge

Service Year

Price Utilization Total Cost

Source: Derived from sample data provided by carriers Aggregation of states where NCCI provides ratemaking services, excludes WV, plus CA, DE, MA, MI, MN, NJ, NY, PA, and WI 2009p = Preliminary

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Physician-Dispensed and Repackaged Drugs in

Workers Compensation

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 80

Physician Dispensing Increased in Service Year 2009

16% 17%

18% 19% 19%

23%

28%

9% 10% 10% 10%

12%

18%

23%

0%

5%

10%

15%

20%

25%

30%

2003 2004 2005 2006 2007 2008 2009

Ph

ys

icia

n-D

isp

en

se

d R

x

Do

lla

r S

ha

re o

f A

ll R

x

Service Year

Including California With California Removed

Source: Derived from sample data provided by carriers 1st through 10th relative service year Average cost per claim with physician-dispensed drugs Aggregation of states where NCCI provides ratemaking services, excludes WV, plus CA, DE, MA, MI, MN, NJ, NY, PA, and WI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 81

Many States Have Substantial Physician Dispensing

> 15.5%

≤ 15.5% AND ≥ 10.5%

< 10.5%

OR

MT

KS

NE

OK

LA

MS

KY

TN

FL

WI

IN

GA

MN

TX

CO

ID

UT

AR

AL

SC

VA

NC

AZ

IL

MI

IA

MO

CA

NH

MA

CT

MD

PA

DE

NM

NV

AK

VT

HI

NJ

NY

ME

RI

SD

Source: Derived from sample data provided by carriers 1st through 10th relative service year Statistics are based on at least $150,000 paid Rx for each state service year combination

Physician-Dispensed Rx Dollar Share of All Rx Service Year 2009

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 82

Physician Dispensing on the Rise in Most States

0%

10%

20%

30%

40%

50%

FL CA GA MD PA IL DE AZ CO MI SC TN AL IN IA LA AK CT MO HI KS NM MS VT NY OK VA DC NJ NC

Ph

ys

icia

n-D

isp

en

se

d R

x

Do

lla

r S

hare

of

All

Rx

State

SY 2007 SY 2008 SY 2009

States With Physician Dispensing in 2009 ≥ 15.5%

Source: Derived from sample data provided by carriers 1st through 10th relative service year Statistics are based on at least $150,000 paid Rx for each state service year combination

ALASKA

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 83

• This update shows that physician dispensing continued to increase in 2009. The update also points toward new evidence that physician dispensing increases drug costs on claims. The update also looks into the drivers of state differences in per-claim Rx costs.

• NCCI will continue to look for other drivers of per-

claim Rx costs and will continue to monitor and report on prescription drugs and other important issues that affect the workers compensation industry.

Prescription Drug Study Summary

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Indemnity Severity

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 85

Countrywide Workers Compensation Indemnity Claim Costs Decline in 2010

Average Indemnity Cost per Lost-Time Claim

$1

0.0

$9

.7

$9

.5

$9

.9

$1

0.1

$1

0.7

$11

.5

$1

2.5

$1

3.8

$1

5.2

$1

6.6

$1

7.1

$1

7.9

$1

8.2

$1

8.8

$1

9.9

$2

1.1

$2

2.8

$2

3.0

$2

2.3

+1.0% -3.1% -2.8% +4.9% +1.7%

+5.9% +7.7%

+9.0%

+10.1%

+10.1% +9.2%

+3.1% +4.6% +1.6%

+3.4% +5.6%

+5.9%

+8.2% +0.8% -3%

5

10

15

20

25

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Accident Year

Accident Year 2010p: Preliminary based on data valued as of 12/31/2010 1991–2009: Based on data through 12/31/2009, developed to ultimate Based on the states where NCCI provides ratemaking services, including state funds Excludes high deductible policies

Annual Change 1991–1993: –1.7%

Annual Change 1994–2001: +7.3%

Annual Change 2002–2009: +4.1%

Indemnity

Claim Cost

($ '000s)

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 86

Countrywide WC Indemnity Severity Declines in Spite of Wage Recovery

Average Indemnity Cost per Lost-Time Claim

1.7

5.9

7.7

9.0

10.1 10.1

9.2

3.1

4.6

1.6

3.4

5.6 5.9

8.2

0.8

-3

3.6 4.2

5.2 5.6

4.7

6.3

2.3

1.1

2.7

4.3

3.5

4.7 4.6

2.3

-0.6

2

-4

-2

0

2

4

6

8

10

12

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

Change in Indemnity Cost per Lost-Time Claim

Change in Average Weekly Wage

Year Based on the states where NCCI provides ratemaking services, including state funds; excludes high deductible policies Sources: Average Weekly Wage 1995–2009: Quarterly Census of Employment and Wages, Moody’s Economy.com; 2010p, NCCI Accident year indemnity severity—NCCI states, NCCI

Percent Change

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 87

Alaska’s Average Indemnity Severity

20.7

17.7

13.5

4

9

14

19

24

29

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Ind

em

nit

y A

ve

rag

e

Cla

im S

eve

rity

($

'0

00

s)

Policy Year

Adjusted to Current Wage Level Actual

Based on NCCI’s financial data for lost-time claims at current benefit level and developed to ultimate

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 88

15 18

20 22

0

5

10

15

20

25

30

35

2006 2007 2008 2009 2010*

Co

st

pe

r C

as

e (

$ '0

00

s)

Accident Year

Alaska Countrywide

Alaska vs. Countrywide Average Indemnity Claim Severity

* Countrywide figure is preliminary Source: NCCI financial data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 89

Alaska’s Indemnity Loss Distribution by Injury Type

Temporary Total Permanent Partial Permanent Total/Fatal

14.0%

70.4%

15.6%

12.3%

73.6%

14.1% 13.9%

78.2%

7.9%

Regional Average Countrywide

Alaska

Regional states are AZ, MT, NM, and OR Based on NCCI’s Statistical Plan data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 90

04/03 - 03/04 04/04 - 03/05 04/05 - 03/06 04/06 - 03/07 04/07 - 03/08

Permanent Total/Fatal 9.9% 7.6% 8.0% 17.4% 15.6%

Permanent Partial 67.5% 71.9% 74.7% 68.1% 70.4%

Temporary Total 22.6% 20.5% 17.4% 14.5% 14.0%

0%

20%

40%

60%

80%

100%

Pe

rce

nt

Policy Period

Alaska’s Distribution of Indemnity Losses by Injury Type Over Time

Source: NCCI’s 2011 Annual Statistical Bulletin Based on NCCI’s Statistical Plan data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Workers Compensation and an Aging Workforce:

Is 35 the New ―Older‖ Worker?

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 92

Workers Compensation and an Aging Workforce

• An Aging Workforce

• Frequency—Steady Declines

• Medical and Indemnity Severity—Steady Increases

– Types of Injuries

– Wage Rates

• Loss Costs—Flat to Up Moderately

– Remarkably Similar for Workers 35 and Older

Overview

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 93

Alaska Population Distribution

Source: US Census Bureau

0%

5%

10%

15%

20%

25%

30%

<15 15-19 20-24 25-34 35-44 45-54 55-64 65-74 75-84 85<

Pe

rce

nta

ge

of

To

tal P

op

ula

tio

n

1990 Census 2000 Census 2010 Census

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 94

0%

5%

10%

15%

20%

25%

30%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Calendar Year

15–19 20–24 25–34 35–44 45–54 55–64 65+

Workers 45 and Older Account for an Increasing Share of the US Workforce

Derived Labor Force Share

Source: Based on labor force participation rates from the Bureau of Labor Statistics and forecasts of population from Moody’s Economy.com

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 95

0%

5%

10%

15%

20%

25%

30%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Calendar Year

15–19 20–24 25–34 35–44 45–54 55–64 65+

And Younger Workers Make Up a Declining Share of the US Workforce

Derived Labor Force Share

Source: Based on labor force participation rates from the Bureau of Labor Statistics and forecasts of population from Moody’s Economy.com

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 96

50

100

150

200

250

300

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Inci

de

nce

Rat

e

Calendar Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Frequency Has Fallen Consistently Across Prime Age Groups

Derived Injury and Illness Incidence Rates Involving Days Away From Work per 10,000 FTE Workers

FTE = Full-Time Equivalent Source: Derived by NCCI using data from the Bureau of Labor Statistics

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 97

50

75

100

125

150

2006 2007 2008 2009

Inci

de

nce

Rat

e

Calendar Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Differences in Frequency Now Modest Across Prime Age Groups

Injury and Illness Incidence Rates Involving Days Away From Work per 10,000 FTE Workers

FTE = Full-Time Equivalent Source: Bureau of Labor Statistics

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 98

$0

$5,000

$10,000

$15,000

$20,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Accident Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Indemnity Severity Increases by Age Have Continued

Average Paid Plus Case Indemnity Severities Reported at 18 Months

Source: NCCI’s Detailed Claim Information data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 99

$0

$5,000

$10,000

$15,000

$20,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Accident Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Indemnity Severity Increases by Age Have Continued

Average Paid Plus Case Indemnity Severities Reported at 18 Months

Source: NCCI’s Detailed Claim Information data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 100

$0

$5,000

$10,000

$15,000

$20,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Accident Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Medical Severity Increases by Age Have Continued

Average Paid Plus Case Medical Severities on Lost-Time Claims Reported at 18 Months

Source: NCCI’s Detailed Claim Information data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 101

$0

$5,000

$10,000

$15,000

$20,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Accident Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Medical Severity Increases by Age Have Continued

Average Paid Plus Case Medical Severities on Lost-Time Claims Reported at 18 Months

Source: NCCI’s Detailed Claim Information data

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 102

Differences in the Mix of Diagnoses Top 10 Claim Diagnoses for Lost-Time Claims With Temporary Payments

That Closed Within 24 Months of Date of Injury, Accident Years 1996–2007, NCCI States

Ages 20–34 Ages 45–64

Diagnosis and Indemnity Severity Index Diagnosis and Indemnity Severity Index

1 Sprain Lumbar Region 0.53 Sprain Rotator Cuff 2.04

2 Lower Leg Injury, not otherwise specified 0.95 Unilateral Inguinal Hernia 0.67

3 Sprain of Ankle, not otherwise specified 0.46 Carpal Tunnel Syndrome 1.06

4 Unilateral Inguinal Hernia 0.84 Tear Medial Cartilage/Meniscus of Knee 1.28

5 Cervicalgia 1.45 Lower Leg Injury, not otherwise specified 0.88

6 Lumbar Disc Displacement 2.43 Sprain Lumbar Region 0.42

7 Carpal Tunnel Syndrome 1.55 Cervicalgia 1.34

8 Lumbago 0.73 Rotator Cuff Syndrome, unspecified 1.68

9 Sprain Lumbosacral 0.47 Lumbar Disc Displacement 1.80

10 Sprain of Neck 0.68 Lumbosacral Neuritis, not otherwise

specified 1.54

The severity index is the ratio of paid temporary indemnity severity for that diagnosis to average paid temporary indemnity severity for all claims for the relevant experience period Source: NCCI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 103

0

10

20

30

40

50

60

70

80

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Du

rati

on

in D

ays

Accident Year

20–34 45–64

Average Temporary Duration 1996–2007 =

57 for the 20–34 age cohort, and

61 for the 45–64 age cohort

A 7% difference (after controlling for mix)

Average Duration for Temporary Payments After Controlling for the

Difference in Injury Mix

Lost-Time Claims With Temporary Payments Closed Within 24 Months of Date of Injury, NCCI States

Source: NCCI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 104

0

10

20

30

40

50

60

70

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Nu

mb

er

of

Tre

atm

en

ts p

er

Cla

im

Accident Year

20–34 45–64

Average Treatments per Claim 1996–2007 =

48 for the 20–34 age cohort, and

54 for the 45–64 age cohort

A 14% difference (after controlling for mix)

Average Number of Treatments per Claim After Controlling for the Difference in Injury Mix

Lost-Time Claims With Temporary Payments Closed Within 24 Months of Date of Injury, NCCI States

Source: NCCI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 105

$0

$100

$200

$300

$400

$500

$600

$700

$800

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Accident Year

20–34 45–64

Average Weekly Wages 1996–2007 =

$485 for the 20–34 age cohort, and

$633 for the 45–64 age cohort

A 31% difference (not controlling for mix)

Average Weekly Wages as Reported

Lost-Time Claims With Temporary Payments Closed Within 24 Months of Date of Injury, NCCI States

Source: NCCI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 106

$0

$10

$20

$30

$40

$50

$60

$70

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Accident Year

20–34 45–64

Average Temporary Benefits Paid per Day 1996–2007 =

$43 for the 20–34 age cohort, and

$52 for the 45–64 age cohort

A 21% difference (after controlling for mix)

Average Temporary Benefits Paid per Day After Controlling for Mix

Lost-Time Claims With Temporary Payments Closed Within 24 Months of Date of Injury, NCCI States

Source: NCCI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 107

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Accident Year

20–34 45–64

Average Price per Treatment 1996–2007 =

$117 for the 20–34 age cohort, and

$126 for the 45–64 age cohort

An 8% difference (after controlling for mix)

Average Price per Treatment After Controlling for Mix

Lost-Time Claims With Temporary Payments Closed Within 24 Months of Date of Injury, NCCI States

Source: NCCI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 108

Contribution of Differences in Mix, Quantity, and Price to Differences in

Indemnity and Medical Severity by Age Modest Impact

Paid Temporary Indemnity Severities and Paid Medical Severities on Claims With Temporary Payments

Lost-Time Claims Closed Within 24 Months of Date of Injury, Accident Years 1996–2007, NCCI States

Indemnity

45–64 vs. 20–34

Medical

45–64 vs. 20–34

Difference Share Difference Share

Total 56% 100% 51% 100%

Due to Diagnosis Mix 26% 46% 28% 55%

Due to Number of Treatments or

Duration 8% 14% 15% 29%

Due to Price and Other Factors 22% 39% 8% 16%

Source: NCCI

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 109

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Calendar/Accident Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

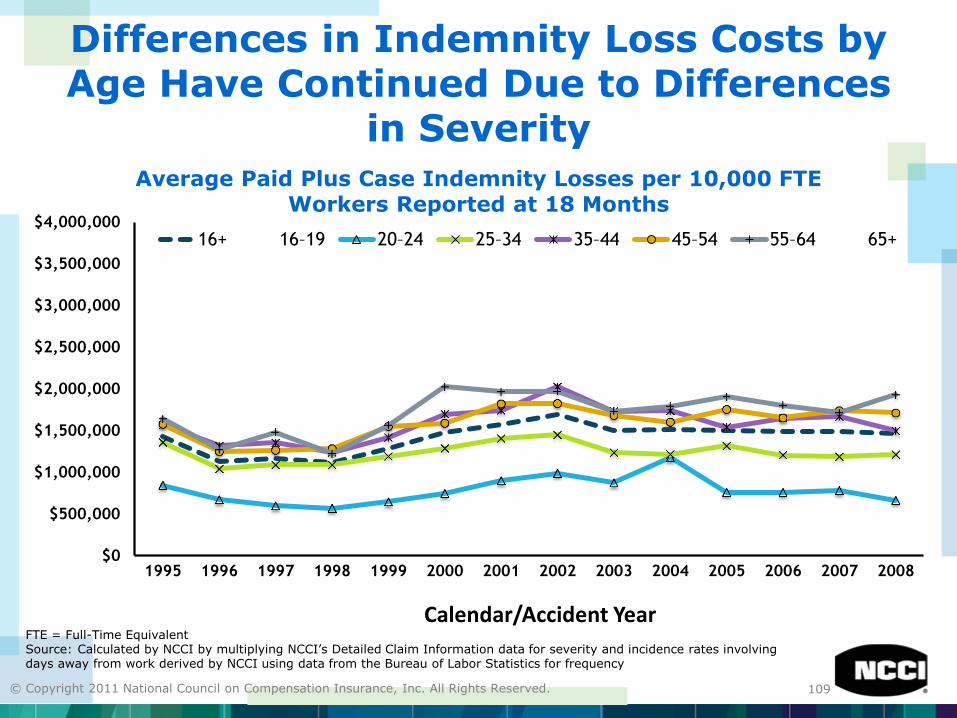

Differences in Indemnity Loss Costs by Age Have Continued Due to Differences

in Severity

Average Paid Plus Case Indemnity Losses per 10,000 FTE Workers Reported at 18 Months

FTE = Full-Time Equivalent Source: Calculated by NCCI by multiplying NCCI’s Detailed Claim Information data for severity and incidence rates involving days away from work derived by NCCI using data from the Bureau of Labor Statistics for frequency

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 110

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Calendar/Accident Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Differences in Medical Loss Costs by Age Have Continued Due to

Differences in Severity

Average Paid Plus Case Medical Losses per 10,000 FTE Workers Reported at 18 Months

FTE = Full-Time Equivalent Source: Calculated by NCCI by multiplying NCCI’s Detailed Claim Information data for severity and incidence rates involving days away from work derived by NCCI using data from the Bureau of Labor Statistics for frequency

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 111

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Calendar/Accident Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Differences in Total Loss Costs by Age Have Continued Due to

Differences in Severity

Average Paid Plus Case Total Losses per 10,000 FTE Workers Reported at 18 Months

FTE = Full-Time Equivalent Source: Calculated by NCCI by multiplying NCCI’s Detailed Claim Information data for severity and incidence rates involving days away from work derived by NCCI using data from the Bureau of Labor Statistics for frequency

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 112

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Calendar/Accident Year

16+ 16–19 20–24 25–34 35–44 45–54 55–64 65+

Differences in Total Loss Costs by Age Have Continued Due to

Differences in Severity

Average Paid Plus Case Total Losses per 10,000 FTE Workers Reported at 18 Months

FTE = Full-Time Equivalent Source: Calculated by NCCI by multiplying NCCI’s Detailed Claim Information data for severity and incidence rates involving days away from work derived by NCCI using data from the Bureau of Labor Statistics for frequency

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 113

• Workers Aged 35 to 64 Appear to Have Similar Costs per Worker

• Workers Aged 20 to 24 Appear to Have Markedly Lower Severities and Loss Costs

• Workers Aged 25 to 34 Fall in the Middle

• Differences Primarily Reflect Differences in Severities

– Claims of Older Workers 50% More Costly

– Differences in Leading Types of Injuries a Major Factor

o Rotator Cuff, Knee vs. Back and Ankle Sprains

• Indemnity Severity—Higher Wages a Key Factor

• Medical Severity—More Treatments per Claim a Material Factor

Summary

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

The Residual Market in Alaska

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 115

68.8

56.4

44.9 49.8

$199M

$153M $127M $136M

0

100

200

300

400

500

2007 2008 2009 2010

0

20

40

60

80

100

Calendar Year

Total New Applications Total New Premium

Total Residual Market New Applications and Premium Assigned in All Plan States

# Thousands $ Millions

$ Premium (Millions) # Applications (‘000s)

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 116

1,998 1,869 1,687 1,774

$8M $7M

$5M $5M

0

5

10

15

2007 2008 2009 2010

0

500

1,000

1,500

2,000

2,500

3,000

Calendar Year

Total New Applications Total New Premium

Total Residual Market New Applications and

Premium Assigned in Alaska

# Count $ Millions

$ Premium (Millions) # Applications

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 117

Alaska’s Total Residual Market Plan Policy Count

8,357

8,178

8,024

7,866

7,500

8,000

8,500

2007 2008 2009 2010

Nu

mb

er

of

Po

lic

ies

Policy Year

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 118

Alaska’s Total Residual Market Plan Premium Volume

$39.0

$32.1

$26.4

$23.6

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2007 2008 2009 2010

Pre

miu

m (

in M

illi

on

s)

Policy Year

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 119

Alaska Residual Market Plan 2009 vs. 2010 Total

Policy Size Comparison

Premium Size

2009 2010

# of Policies Premium # of Policies Premium

$0–$2,499 5,741 $5,200,352 5,717 $5,136,025

$2,500–$4,999 1,169 $4,099,513 1,127 $3,922,425

$5,000–$9,999 593 $4,166,854 557 $3,892,024

$10,000–$19,999 318 $4,378,907 290 $3,962,139

$20,000–$49,999 162 $4,715,822 149 $4,485,611

$50,000–$99,999 34 $2,341,684 21 $1,408,031

$100,000–$199,999 4 $473,543 4 $533,723

$200,000 and greater 3 $1,057,157 1 $212,626

TOTAL 8,024 $26,433,832 7,866 $23,552,604

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 120

Comparison of the Estimated Market Share for Alaska’s

Residual Market by Total Policy Count and Written Premium

Market share as a percentage of residual market total written premium/policies in force

2010 numbers are preliminary

13.8% 12.0%

55.7% 53.2%

0%

10%

20%

30%

40%

50%

60%

2007 2008 2009 2010

Pe

rce

nta

ge

of

Ma

rke

t

Year

Premium Policies

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 121

National

5645—Carpentry (5.3%)

5551—Roofing (3.6%)

7228—Trucking, Local (3.0%)

8835—Nursing, Home Health (2.5%)

5474—Painting (2.1%)

Alaska’s Top Five Class Codes Based on Residual Market

Plan Total Written Premium

Alaska

5645—Carpentry (5.1%)

9094—Outdoor Guide Service (5.0%)

8832—Physician (4.9%)

8017—Retail Store NOC (4.0%)

8824—Retirement Living Centers (2.9%)

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 122

• Elimination of Premium Discounts

• Surcharge

• Take-Out Credit (TOC) Program

• Safe Workplace Incentive Program

• Voluntary Coverage Assistance Program (VCAP® Service)

Alaska Assigned Risk Programs

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

NCCI Initiatives

123

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 124

• Increase the split point

• Index the split point so future increases are automatic

• Revise the maximum modification formula/cap so the maximum mod is not less than 1.10

• Experience rating changes will be premium- neutral statewide

Experience Rating Plan Update

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 125

• The split point separates losses into primary and excess components. It is currently 5,000.

• If the split point is not indexed for claim cost inflation, a greater proportion of losses fall into the excess category as time goes on.

• Since excess losses receive less weight than primary losses in the experience rating formula, the plan becomes less responsive.

• Indications are that the split point should be increased to 15,000. This is not surprising since the average cost of a claim has tripled since the last split point update (20 years ago).

Experience Rating Plan Split Point Review

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 126

• NCCI plans to institute a transition program that increases the split point most of the way initially and phases in the rest of the change

– The split point will initially be increased to 10k

– The next effective year filing will further increase the split point to 13.5k

– The third effective year filing will further increase the split point all the way to the indicated split point of 15k trended two years forward (rounded to the nearest 500)

• Subsequent effective year filings will increase the split point as indicated

Experience Rating Plan Split Point Review

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 127

Experience Rating Plan Update

Projected timeline:

• Filed August 2, 2011

• Effective on the loss cost effective date beginning with 1/1/2013 filings

• NCCI will pursue a six-month approval lead time (e.g., approval by 6/30/2012 in states with 1/1/2013 loss cost filings)

An on-demand webinar is currently available on ncci.com

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Q & A

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Closing Remarks

Thank You!

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Glossary

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 131

• Assigned Risk Adjustment Program (ARAP)—An assigned risk market program that surcharges residual market risks based on the magnitude of their experience rating modification.

• Calendar Year (CY)—Experience of earned premium and loss transactions occurring within the calendar year beginning January 1, irrespective of the contractual dates of the policies to which the transactions relate and the dates of the accidents.

• Calendar-Accident Year (AY)—The accumulation of loss data on all accidents with the date of occurrence falling within a given calendar year. The premium figure is the same as that used in calendar year experience.

• Claim Frequency—The number of claims per unit of exposure; for example, the number of claims per million dollars of premium or per 100 workers.

Glossary

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 132

• Claim Severity—The average cost of a claim. Severity is calculated by dividing total losses by the total number of claims.

• Combined Ratio—The sum of the (i) loss ratio, (ii) expense ratio, and (iii) dividend ratio for a given time period.

• Detailed Claim Information (DCI)—An NCCI call that collects detailed information on an individual workers compensation lost-time claim basis, such as type of injury, whether or not an attorney was involved, timing of the claim’s report to the carrier, etc.

• Direct Written Premium (DWP)—The gross premium income adjusted for additional or return premiums, but excluding any reinsurance premiums.

Glossary

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 133

• Indemnity Benefits—Payments by an insurance company to cover an injured worker's time lost from work. These benefits are also referred to as ―wage replacement‖ benefits.

• Loss Ratio—The ratio of losses to premium for a given time period.

• Lost-Time (LT) Claims—Claims resulting in indemnity benefits (and usually medical benefits) being paid to or on behalf of the injured worker for time lost from work.

• Medical-Only Claims—Claims resulting in only medical benefits being paid on behalf of an injured worker.

• Net Written Premium (NWP)—The gross premium income adjusted for additional or return premiums and including any additions for reinsurance assumed and any deductions for reinsurance ceded.

Glossary

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 134

• Permanent Partial (PP)—Disability that prevents the insured from working at their own (and sometimes any) occupation. A disability is considered to result in partial permanent loss of earning power.

• Policy Year (PY)—Premium and loss data on business for a 12-month period for policies with inception dates within the 12-month period.

• Schedule Rating—A debit and credit plan that recognizes variations in the hazard-causing features of an individual risk.

• Take-Out Credit Program—An assigned risk program that encourages carriers to write current residual market risks in the competitive voluntary marketplace.

• Temporary Total (TT)—A disability that totally disables a worker for a temporary period of time.

Glossary

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved.

Appendix

© Copyright 2011 National Council on Compensation Insurance, Inc. All Rights Reserved. 136

• Financial Aggregate Calls

– Used for aggregate ratemaking

• Statistical Plan for Workers Compensation and Employers Liability Insurance (Statistical Plan)

– Used for class ratemaking

• Detailed Claim Information

– In-depth sample of lost-time claims

• Policy Data

– Policy declaration page information

NCCI Workers Compensation Resources