Embed Size (px)

Citation preview

Investor Presentation

Bharti Airtel LimitedMarch 2009

DisclaimerThe information contained in this presentation is only current as of its date. All actions and statements made herein or otherwise shall be subject to the applicable laws and regulations as amended from time to time. There is no representation that all information relating to the context has been taken care off in the presentation and neither we undertake any obligation as to the regular updating of the information as a result of new information, future events or otherwise. We will accept no liability whatsoever for any loss arising directly or indirectly from the use of, reliance of any information contained in this presentation or for any omission of the information. The information shall not be distributed or used by any person or entity in any jurisdiction or countries were such distribution or use would be contrary to the applicable laws or Regulations. It is advised that prior to acting upon this presentation independent consultation / advise may be obtained and necessary due diligence, investigation etc may be done at your end. You may also contact us directly for any questions or clarifications at our end.

This presentation contain certain statements of future expectations and other forward-looking statements, including those relating to our general business plans and strategy, our future financial condition and growth prospects, and future developments in our industry and our competitive and regulatory environment. In addition to statements which are forward looking by reason of context, the words ‘may, will, should, expects, plans, intends, anticipates, believes, estimates, predicts, potential or continue’ and similar expressions identify forward looking statements.

Actual results, performances or events may differ materially from these forward-looking statements including the plans, objectives, expectations, estimates and intentions expressed in forward looking statements due to a number of factors, including without limitation future changes or developments in our business, our competitive environment, telecommunications technology and application, and political, economic, legal and social conditions in India. It is cautioned that the foregoing list is not exhaustive

This presentation is not being used in connection with any invitation of an offer or an offer of securities and should not be used as a basis for any investment decision.

Investor Relations :- http://www.bhartiairtel.inFor any queries, write to: [email protected]

“The information contained herein does not constitute an offer of securities for sale in the United States. Securities may not be sold in the United States absent registration or an exemption from registration under the U.S. Securities Act of 1933, as amended. Any public offering of securities to be made in the United States will be made by means of a prospectus and will contain detailed information about the Company and its management, as well as financial statements. No money, securities or other consideration is being solicited, and, if sent in response to the information contained herein, will not be accepted.”

3

Mobile Services Telemedia Services Enterprise Services

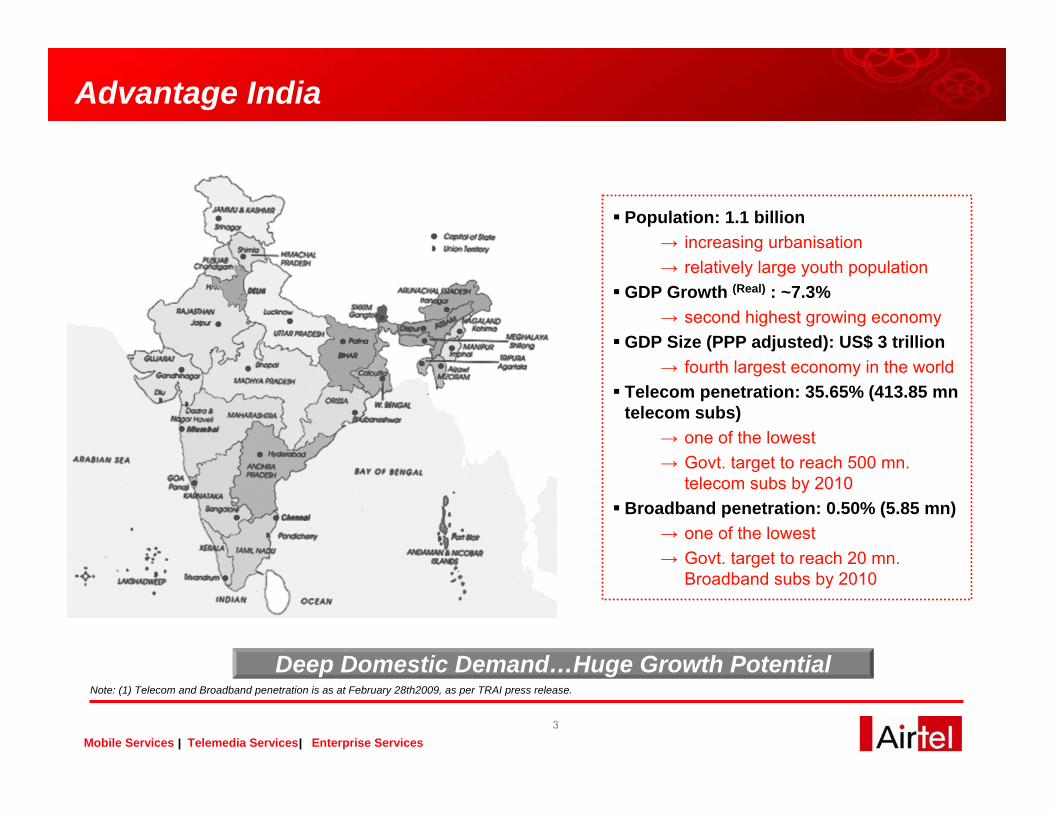

Advantage India

Deep Domestic Demand…Huge Growth Potential

Population: 1.1 billion→ increasing urbanisation→ relatively large youth population

GDP Growth (Real) : ~7.3%→ second highest growing economy

GDP Size (PPP adjusted): US$ 3 trillion→ fourth largest economy in the world

Telecom penetration: 35.65% (413.85 mntelecom subs)

→ one of the lowest→ Govt. target to reach 500 mn.

telecom subs by 2010Broadband penetration: 0.50% (5.85 mn)

→ one of the lowest→ Govt. target to reach 20 mn.

Broadband subs by 2010

Note: (1) Telecom and Broadband penetration is as at February 28th2009, as per TRAI press release.

4

Mobile Services Telemedia Services Enterprise Services

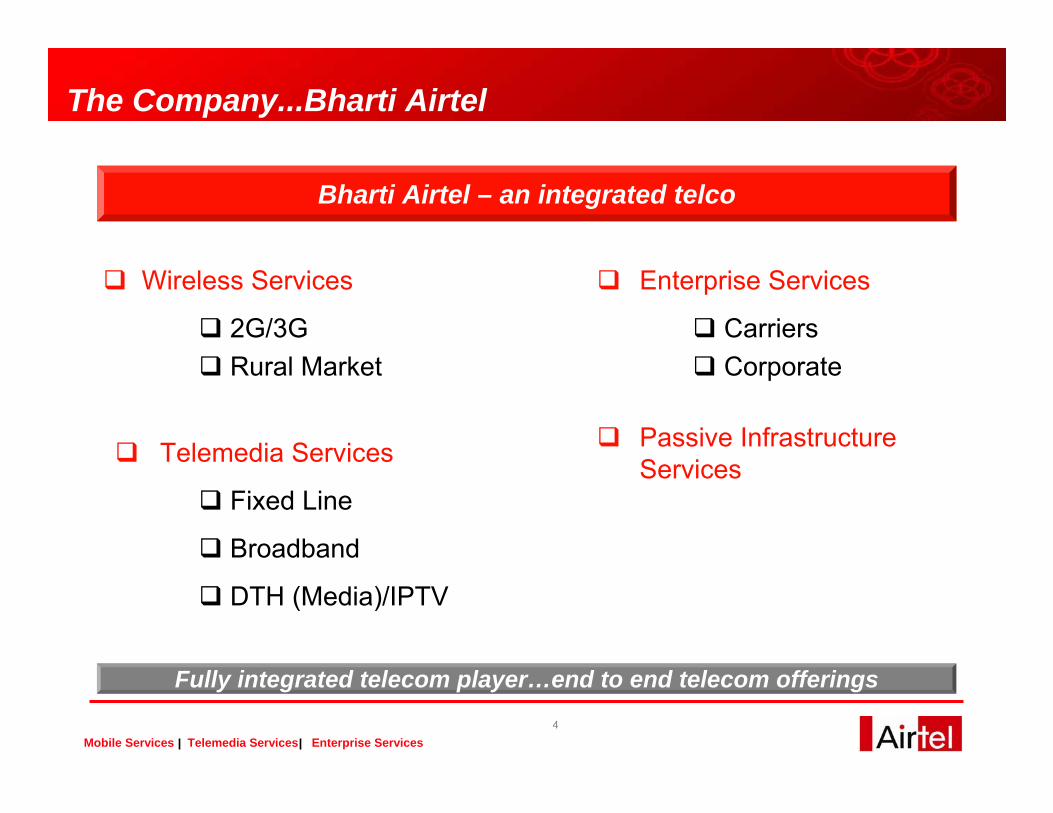

The Company...Bharti Airtel

Bharti Airtel – an integrated telco

Wireless Services

2G/3GRural Market

Telemedia Services

Fixed Line

Broadband

DTH (Media)/IPTV

Enterprise Services

CarriersCorporate

Passive Infrastructure Services

Fully integrated telecom player…end to end telecom offerings

5

Mobile Services Telemedia Services Enterprise Services

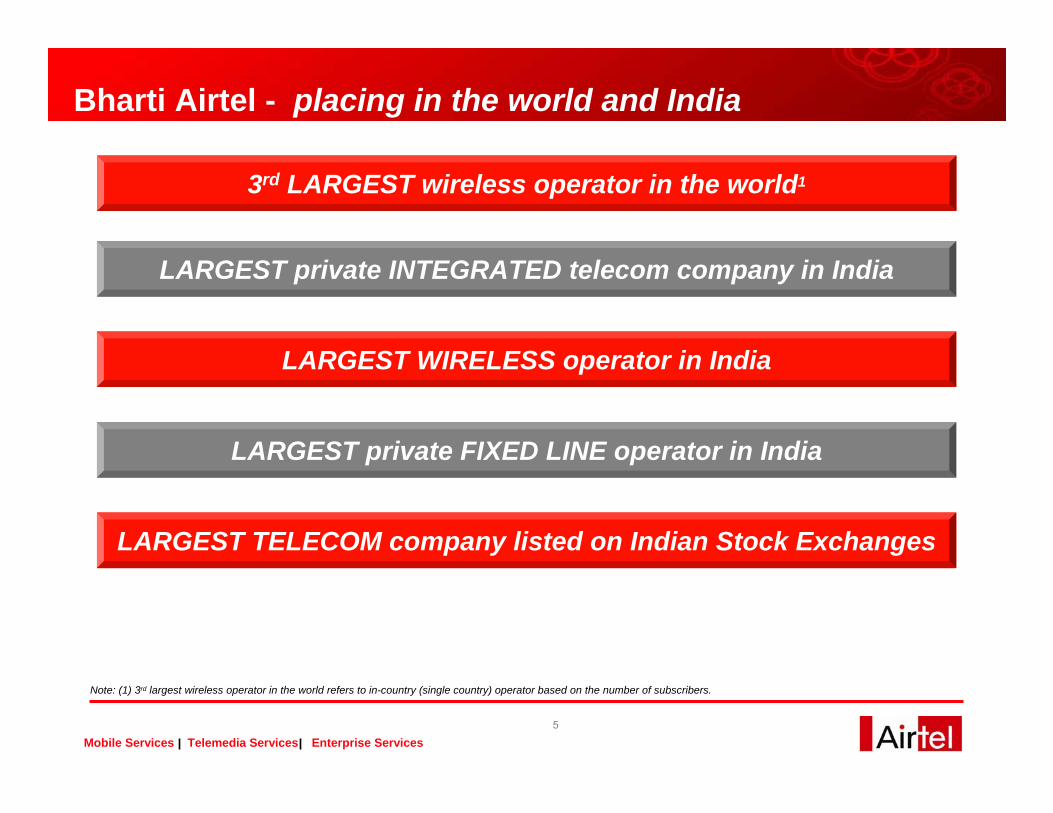

3rd LARGEST wireless operator in the world1

LARGEST TELECOM company listed on Indian Stock Exchanges

Bharti Airtel - placing in the world and India

LARGEST private INTEGRATED telecom company in India

LARGEST WIRELESS operator in India

LARGEST private FIXED LINE operator in India

Note: (1) 3rd largest wireless operator in the world refers to in-country (single country) operator based on the number of subscribers.

6

Mobile Services Telemedia Services Enterprise Services

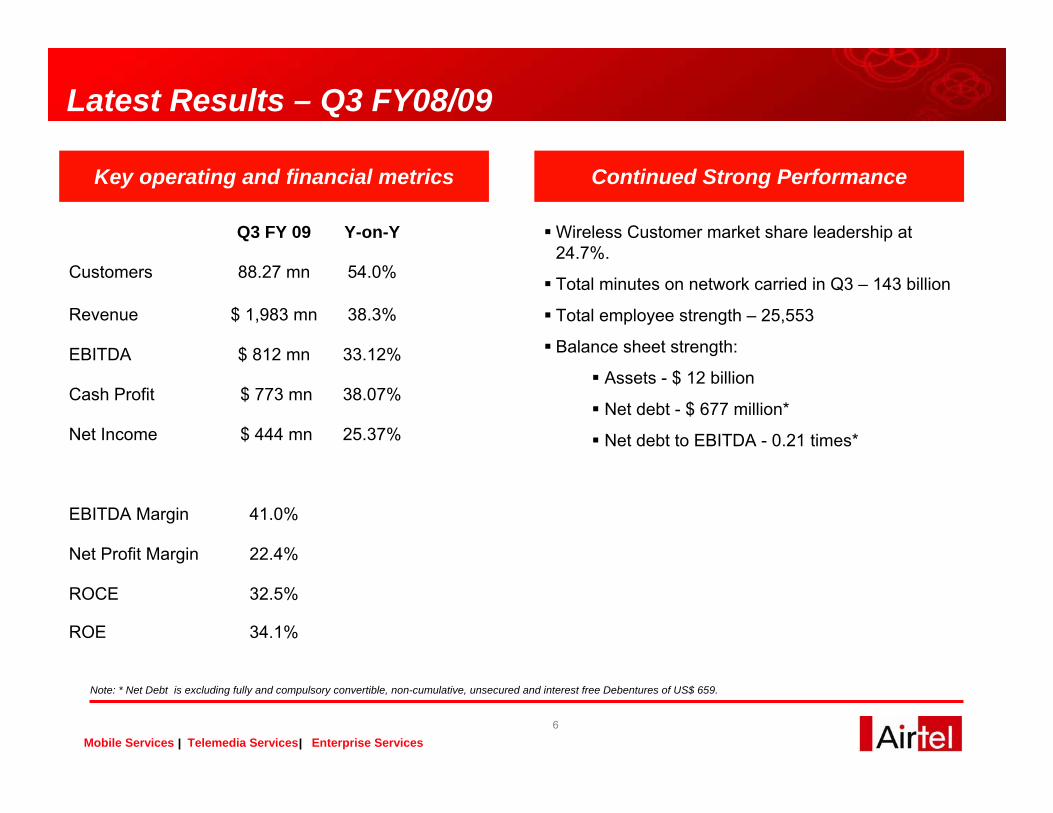

Latest Results – Q3 FY08/09

Key operating and financial metrics

34.1%ROE

32.5%ROCE

22.4%Net Profit Margin

41.0%EBITDA Margin

25.37%$ 444 mnNet Income

38.07%$ 773 mnCash Profit

33.12%$ 812 mnEBITDA

38.3%$ 1,983 mnRevenue

54.0%88.27 mnCustomers

Y-on-YQ3 FY 09

Continued Strong Performance

Wireless Customer market share leadership at 24.7%.

Total minutes on network carried in Q3 – 143 billion

Total employee strength – 25,553

Balance sheet strength:

Assets - $ 12 billion

Net debt - $ 677 million*

Net debt to EBITDA - 0.21 times*

Note: * Net Debt is excluding fully and compulsory convertible, non-cumulative, unsecured and interest free Debentures of US$ 659.

7

Mobile Services Telemedia Services Enterprise Services

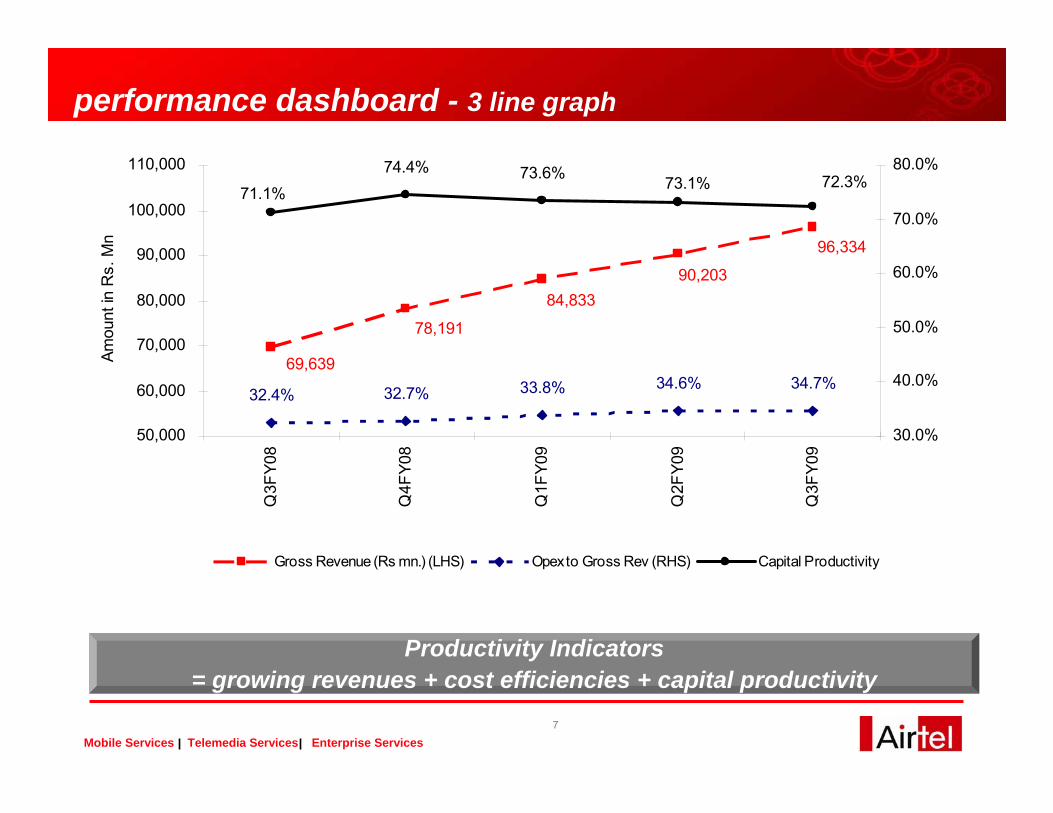

performance dashboard - 3 line graph

Productivity Indicators = growing revenues + cost efficiencies + capital productivity

96,334

90,20384,833

78,191

69,639

32.4% 32.7% 33.8% 34.6% 34.7%

71.1%74.4% 73.6% 73.1% 72.3%

50,000

60,000

70,000

80,000

90,000

100,000

110,000

Q3F

Y08

Q4F

Y08

Q1F

Y09

Q2F

Y09

Q3F

Y09

Amou

nt in

Rs.

Mn

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Gross Revenue (Rs mn.) (LHS) Opex to Gross Rev (RHS) Capital Productivity

8

Mobile Services Telemedia Services Enterprise Services

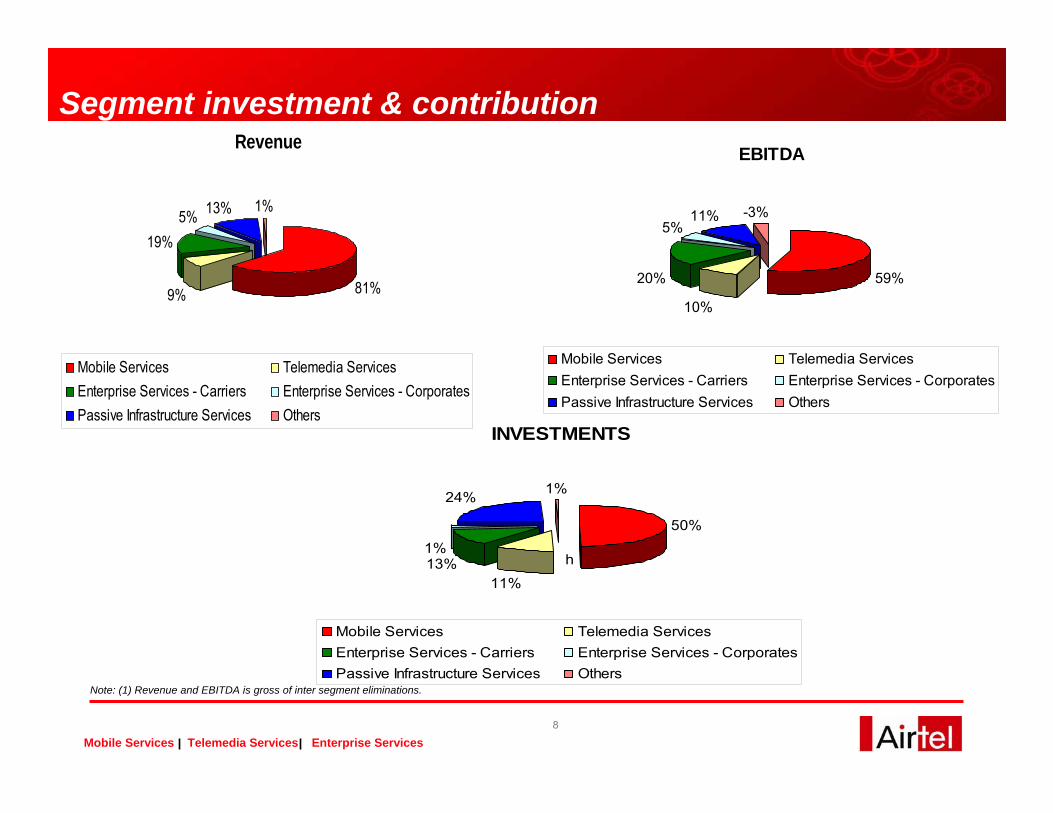

Segment investment & contribution

Note: (1) Revenue and EBITDA is gross of inter segment eliminations.

Revenue

81%9%

19%5% 13% 1%

Mobile Services Telemedia ServicesEnterprise Services - Carriers Enterprise Services - CorporatesPassive Infrastructure Services Others

EBITDA

59%

10%

20%

5%11% -3%

Mobile Services Telemedia ServicesEnterprise Services - Carriers Enterprise Services - CorporatesPassive Infrastructure Services Others

INVESTMENTS

50%

11%13%1%

24% 1%

Mobile Services Telemedia ServicesEnterprise Services - Carriers Enterprise Services - CorporatesPassive Infrastructure Services Others

h

few recent recognitionsBharti Airtel top honors at the 7th edition of the Frost & Sullivan ICT awards 2008 in the categories of Large Enterprise Telecom Services, Wholesale Data Services and Mobile Service.

Bharti Airtel and IFFCO joint venture recently bagged the ‘Best Content Service’award and the Gujarat E-GRAM project executed by Bharti Airtel has won ‘Best Project Management’ award at the World Communications Awards held at London

Bharti Airtel was voted as India’s most innovative company in a survey conducted by The Wall Street Journal.

Airtel won the Platinum Trusted Brand Award in the Mobile Service Provider Category in the Reader’s Digest Asia Trusted Brand’s Survey.

Airtel was chosen as the 2nd most trusted service brand in India in the ‘Most Trusted Brands 2008 Survey’ conducted by the Economic Times - Brand Equity

Awarded with top honors at the GSMA Mobile World Congress Conference 2008 in Barcelona for the category “Best Billing/ Customer Care solution.”

Adjudged as the ‘Best Carrier India‘ at the Telecom Asia Award 2008

Sunil Bharti Mittal, Chairman & Group CEO

GSM Association Chairman’s Award 2008

Chosen for Padma Bhushan Awards in 2007

Sarvjit Dhillon, Group Director

Best Performing CFO in Telecommunications Sector by CNBC-TV18 in March 2009

10

Mobile Services Telemedia Services Enterprise Services

Wireless Services

11

Mobile Services Telemedia Services Enterprise Services

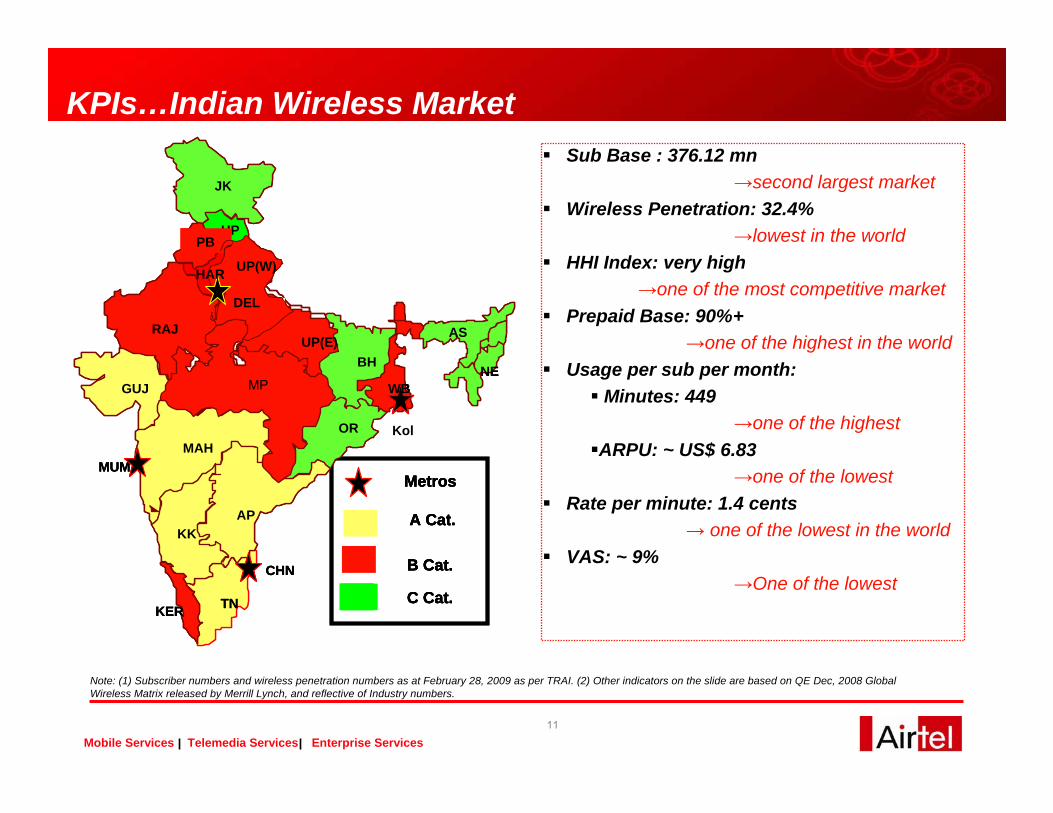

Sub Base : 376.12 mn→second largest market

Wireless Penetration: 32.4%→lowest in the world

HHI Index: very high→one of the most competitive market

Prepaid Base: 90%+→one of the highest in the world

Usage per sub per month:Minutes: 449

→one of the highestARPU: ~ US$ 6.83

→one of the lowestRate per minute: 1.4 cents

→ one of the lowest in the worldVAS: ~ 9%

→One of the lowest

KPIs…Indian Wireless Market

MUM

HP

DELHI

AP

CHN

MADHYA PRADESH`

TNKER

PB

DEL

UP(W)

MP

RAJUP(E)

KK

OR

HAR

JK

BH

WBGUJ

MAH

AS

NE

Metros

A Cat.

B Cat.

C Cat.

MUM

HP

DELHI

AP

CHN

MADHYA PRADESH`

TNKER

PB

DEL

UP(W)

MP

RAJUP(E)

KK

OR

HAR

JK

BH

WBGUJ

MAH

AS

NE

Metros

A Cat.

B Cat.

C Cat.

MUM

HP

DELHI

AP

CHN

MADHYA PRADESH`

TNKER

PB

DEL

UP(W)

MP

RAJUP(E)

KK

OR

HAR

JK

BH

WBGUJ

MAH

AS

NE

Metros

A Cat.

B Cat.

C Cat.

Metros

A Cat.

B Cat.

C Cat.

Kol

Note: (1) Subscriber numbers and wireless penetration numbers as at February 28, 2009 as per TRAI. (2) Other indicators on the slide are based on QE Dec, 2008 Global Wireless Matrix released by Merrill Lynch, and reflective of Industry numbers.

12

Mobile Services Telemedia Services Enterprise Services

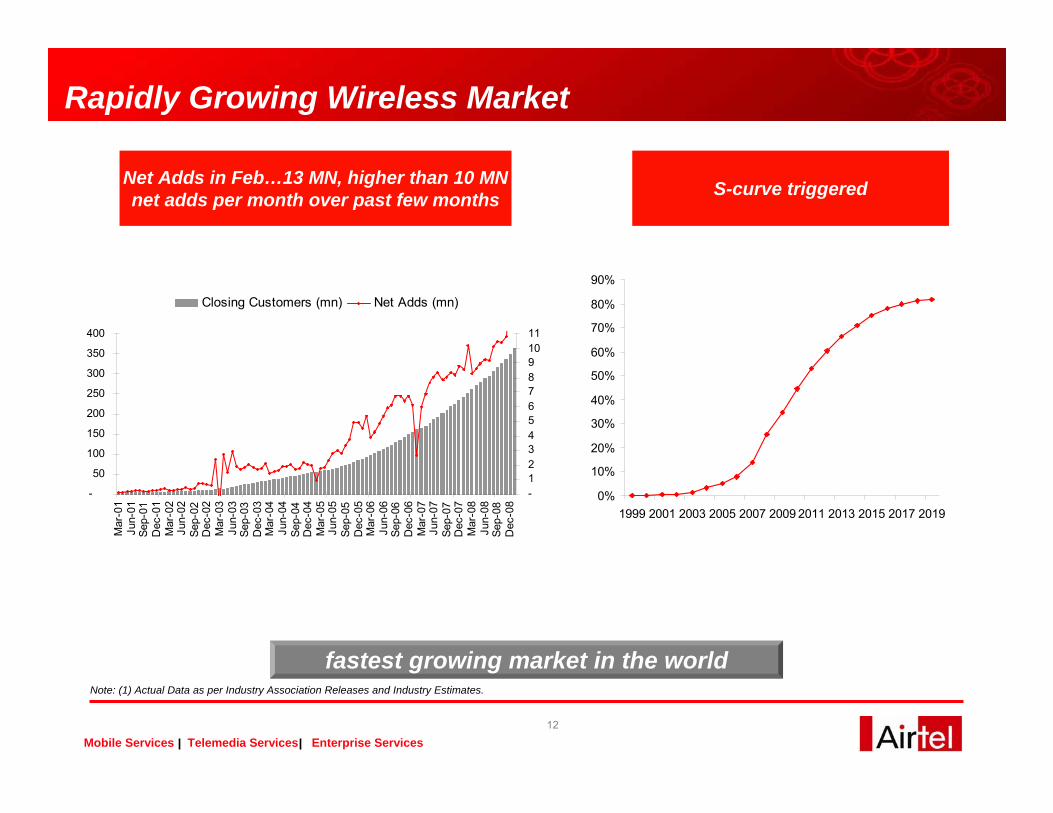

Net Adds in Feb…13 MN, higher than 10 MN net adds per month over past few months S-curve triggered

Rapidly Growing Wireless Market

Note: (1) Actual Data as per Industry Association Releases and Industry Estimates.

fastest growing market in the world

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

-

50

100

150

200

250

300

350

400

Mar

-01

Jun-

01Se

p-01

Dec

-01

Mar

-02

Jun-

02Se

p-02

Dec

-02

Mar

-03

Jun-

03Se

p-03

Dec

-03

Mar

-04

Jun-

04Se

p-04

Dec

-04

Mar

-05

Jun-

05Se

p-05

Dec

-05

Mar

-06

Jun-

06Se

p-06

Dec

-06

Mar

-07

Jun-

07Se

p-07

Dec

-07

Mar

-08

Jun-

08Se

p-08

Dec

-08

-1234567891011

Closing Customers (mn) Net Adds (mn)

13

Mobile Services Telemedia Services Enterprise Services

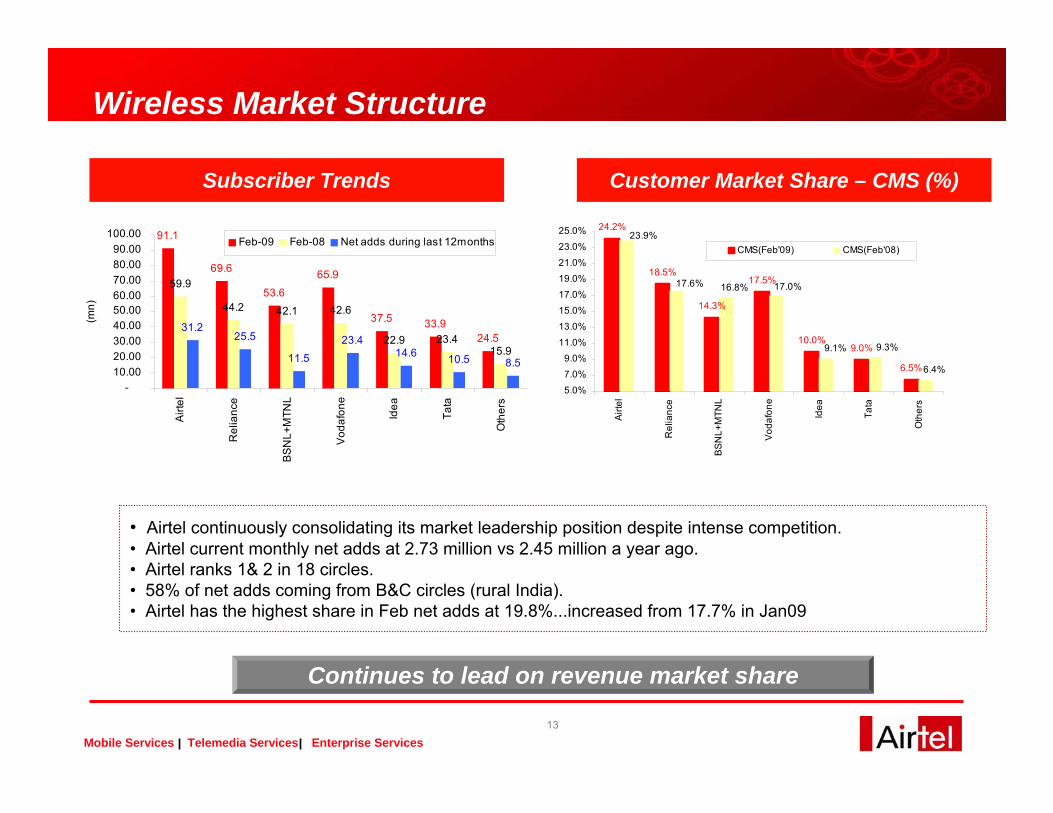

Wireless Market Structure

• Airtel continuously consolidating its market leadership position despite intense competition.• Airtel current monthly net adds at 2.73 million vs 2.45 million a year ago.• Airtel ranks 1& 2 in 18 circles.• 58% of net adds coming from B&C circles (rural India).• Airtel has the highest share in Feb net adds at 19.8%...increased from 17.7% in Jan09

Continues to lead on revenue market share

Subscriber Trends Customer Market Share – CMS (%)

91.1

69.6

53.6

65.9

37.5 33.924.5

59.9

44.2 42.1 42.6

22.9 23.415.9

31.225.5

11.5

23.414.6 10.5 8.5

-10.0020.0030.0040.0050.0060.0070.0080.0090.00

100.00

Airt

el

Rel

ianc

e

BSN

L+M

TNL

Vod

afon

e

Idea

Tata

Oth

ers

(mn)

Feb-09 Feb-08 Net adds during last 12months24.2%

18.5%

14.3%

17.5%

10.0%9.0%

6.5%6.4%

9.3%9.1%

17.0%16.8%17.6%

23.9%

5.0%

7.0%

9.0%11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

23.0%

25.0%

Airt

el

Rel

ianc

e

BS

NL+

MTN

L

Vod

afon

e

Idea

Tata

Oth

ers

CMS(Feb'09) CMS(Feb'08)

14

Mobile Services Telemedia Services Enterprise Services

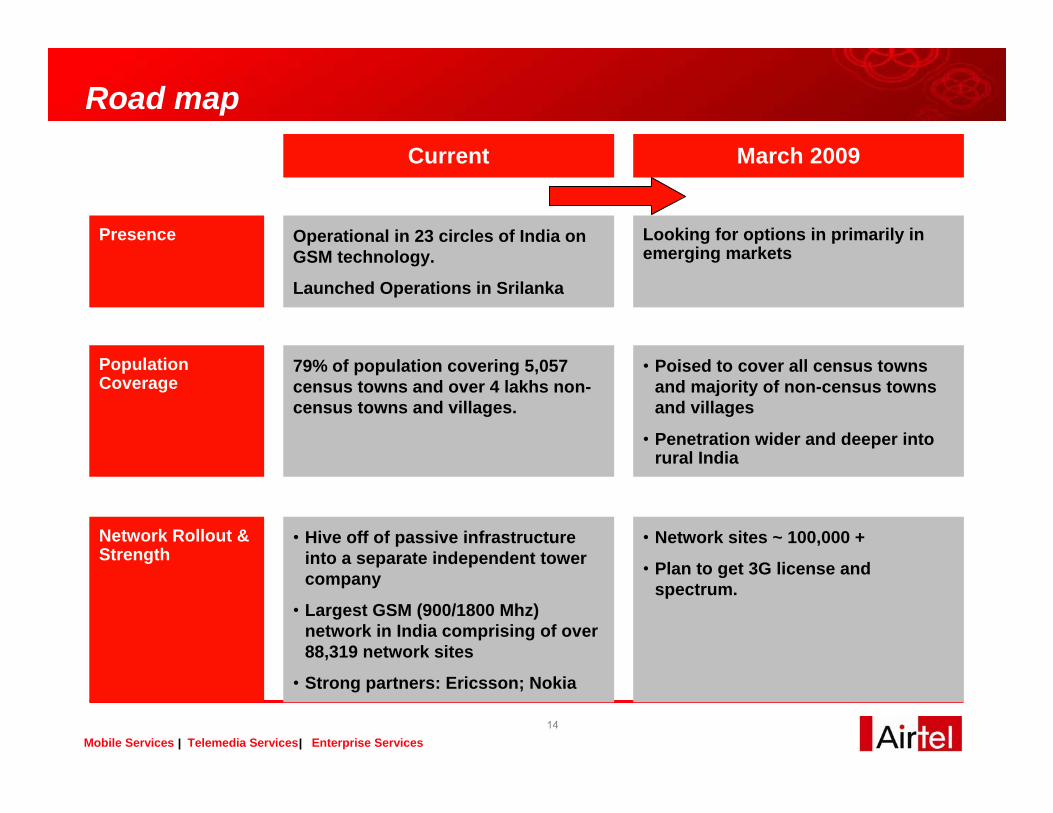

Looking for options in primarily in emerging markets

Operational in 23 circles of India on GSM technology.

Launched Operations in Srilanka

Presence

• Network sites ~ 100,000 +

• Plan to get 3G license and spectrum.

• Hive off of passive infrastructure into a separate independent tower company

• Largest GSM (900/1800 Mhz) network in India comprising of over 88,319 network sites

• Strong partners: Ericsson; Nokia

Network Rollout & Strength

• Poised to cover all census towns and majority of non-census towns and villages

• Penetration wider and deeper into rural India

79% of population covering 5,057 census towns and over 4 lakhs non-census towns and villages.

Population Coverage

March 2009Current

Road map

15

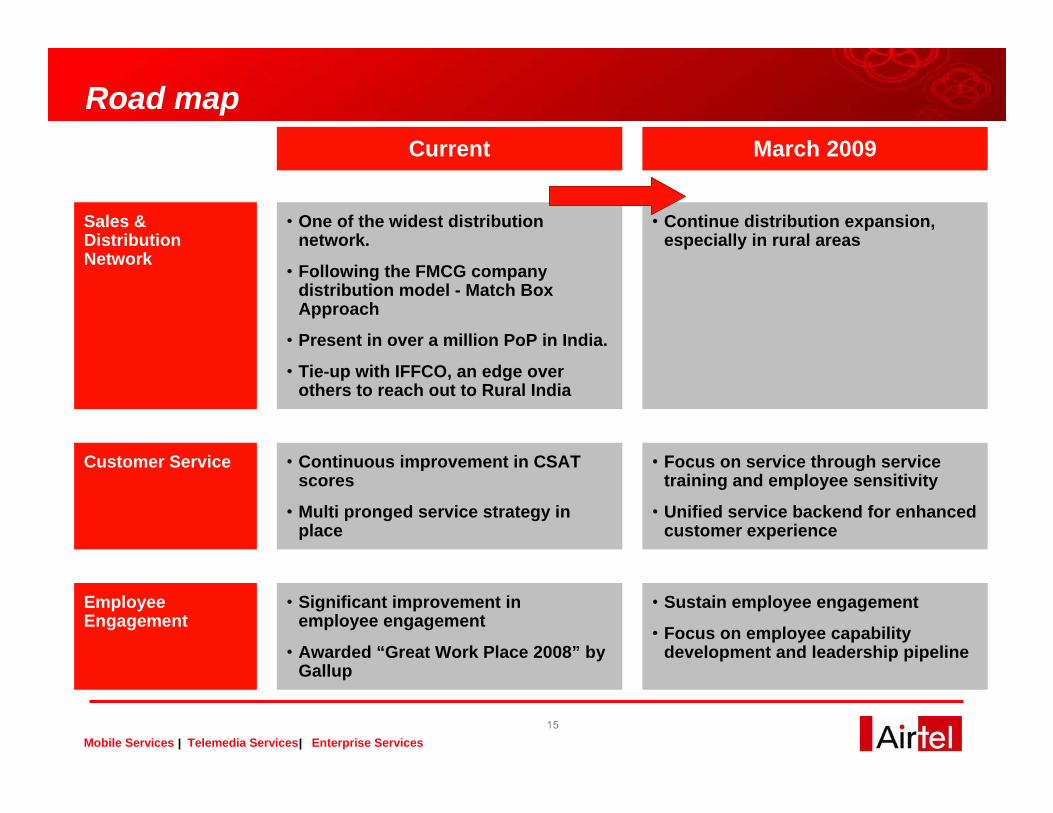

Mobile Services Telemedia Services Enterprise Services

• Focus on service through service training and employee sensitivity

• Unified service backend for enhanced customer experience

• Continuous improvement in CSAT scores

• Multi pronged service strategy in place

Customer Service

• Sustain employee engagement

• Focus on employee capability development and leadership pipeline

• Significant improvement in employee engagement

• Awarded “Great Work Place 2008” by Gallup

Employee Engagement

• Continue distribution expansion, especially in rural areas

• One of the widest distribution network.

• Following the FMCG company distribution model - Match Box Approach

• Present in over a million PoP in India.

• Tie-up with IFFCO, an edge over others to reach out to Rural India

Sales & Distribution Network

March 2009Current

Road map

16

Mobile Services Telemedia Services Enterprise Services16

Hello Tunes(Ring Back

Tones)

Portfolio Manager(Stock Tracker)

Blackberry

Airtel Live(Portal)

first mover advantage/ product innovations

Life time validity product

Electronic Recharge /

Micro Prepaid

focus on product innovations

Easy Music

Song Catcher

Call Home Service

Money Transfers

Music on Demand

Google search

M Commerce

iPhone

17

Mobile Services Telemedia Services Enterprise Services

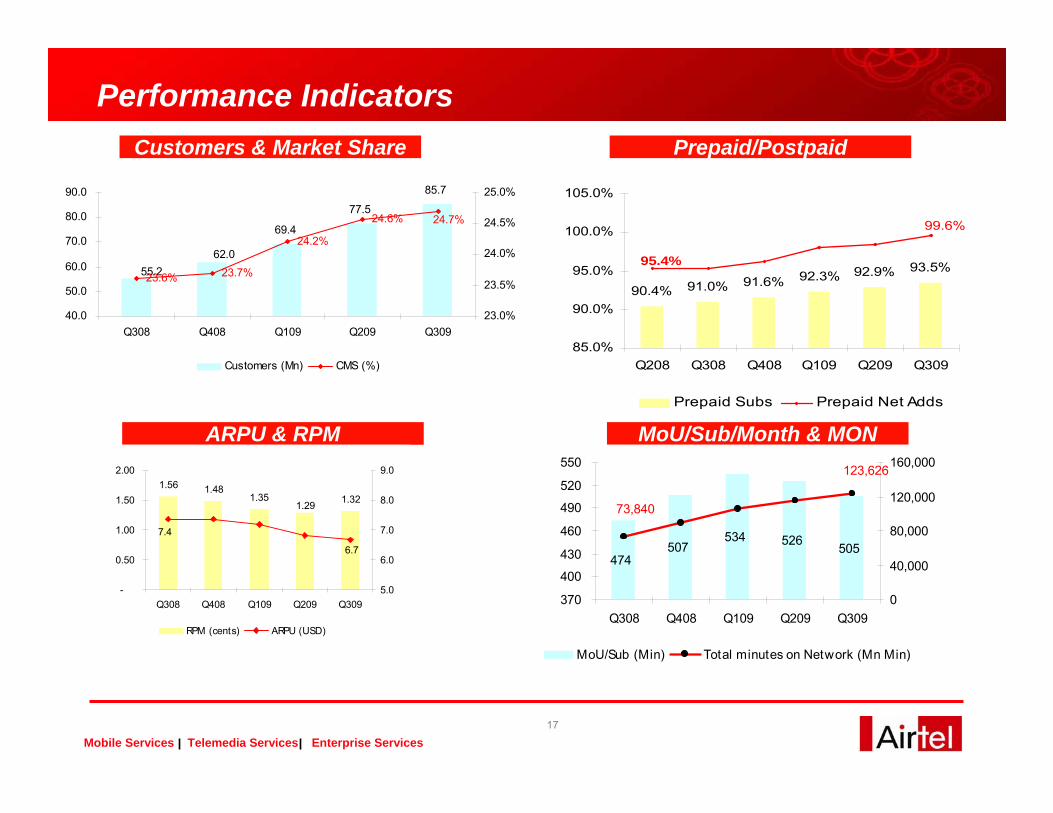

Performance IndicatorsCustomers & Market Share Prepaid/Postpaid

MoU/Sub/Month & MONARPU & RPM

90.4% 91.0% 91.6% 92.3% 92.9% 93.5%

99.6%

95.4%

85.0%

90.0%

95.0%

100.0%

105.0%

Q208 Q308 Q408 Q109 Q209 Q309

Prepaid Subs Prepaid Net Adds

69.4

77.5

85.7

55.262.0

23.6% 23.7%

24.2%

24.6% 24.7%

40.0

50.0

60.0

70.0

80.0

90.0

Q308 Q408 Q109 Q209 Q30923.0%

23.5%

24.0%

24.5%

25.0%

Customers (Mn) CMS (%)

1.56 1.481.35 1.321.29

7.4

6.7

-

0.50

1.00

1.50

2.00

Q308 Q408 Q109 Q209 Q3095.0

6.0

7.0

8.0

9.0

RPM (cents) ARPU (USD)

474505507

534 526

123,626

73,840

370

400

430

460

490

520

550

Q308 Q408 Q109 Q209 Q3090

40,000

80,000

120,000

160,000

MoU/Sub (Min) Total minutes on Network (Mn Min)

18

Mobile Services Telemedia Services Enterprise Services

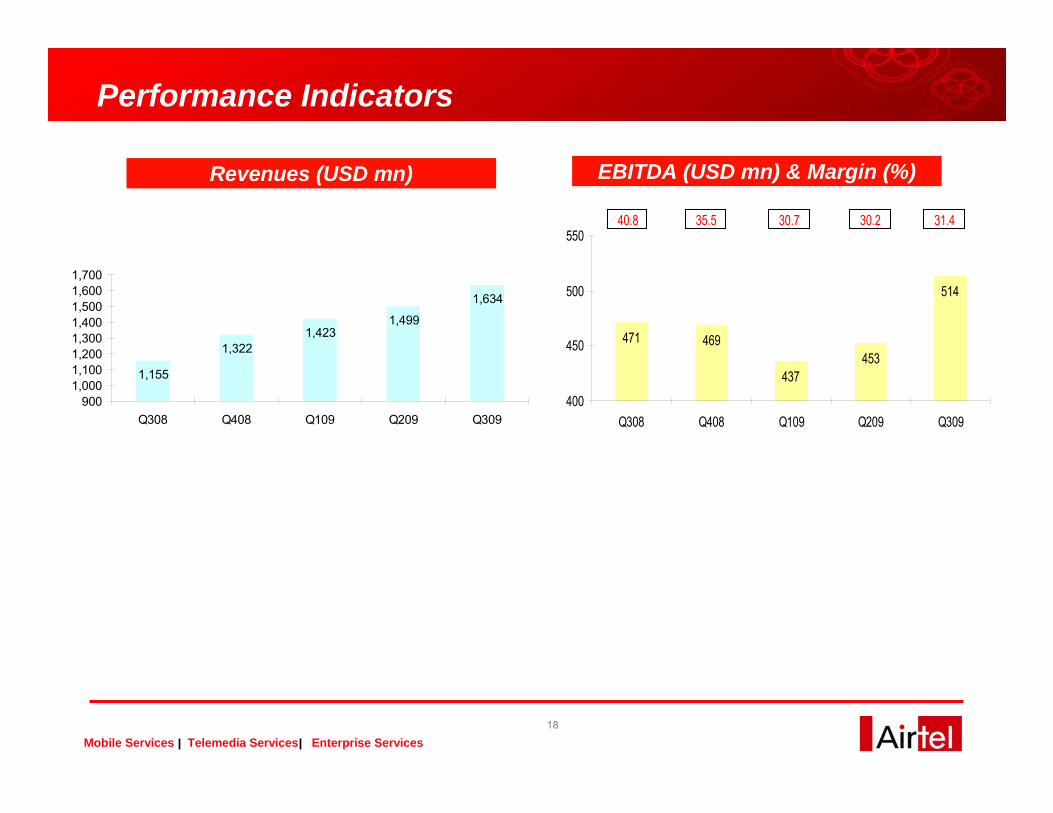

Performance Indicators

EBITDA (USD mn) & Margin (%)Revenues (USD mn)

1,155

1,3221,423

1,499

1,634

9001,0001,1001,2001,3001,4001,5001,6001,700

Q308 Q408 Q109 Q209 Q309

471 469

437453

514

400

450

500

550

Q308 Q408 Q109 Q209 Q309

40.8 35.5 30.7 30.2 31.4

19

Mobile Services Telemedia Services Enterprise Services

Telemedia Services

20

Mobile Services Telemedia Services Enterprise Services

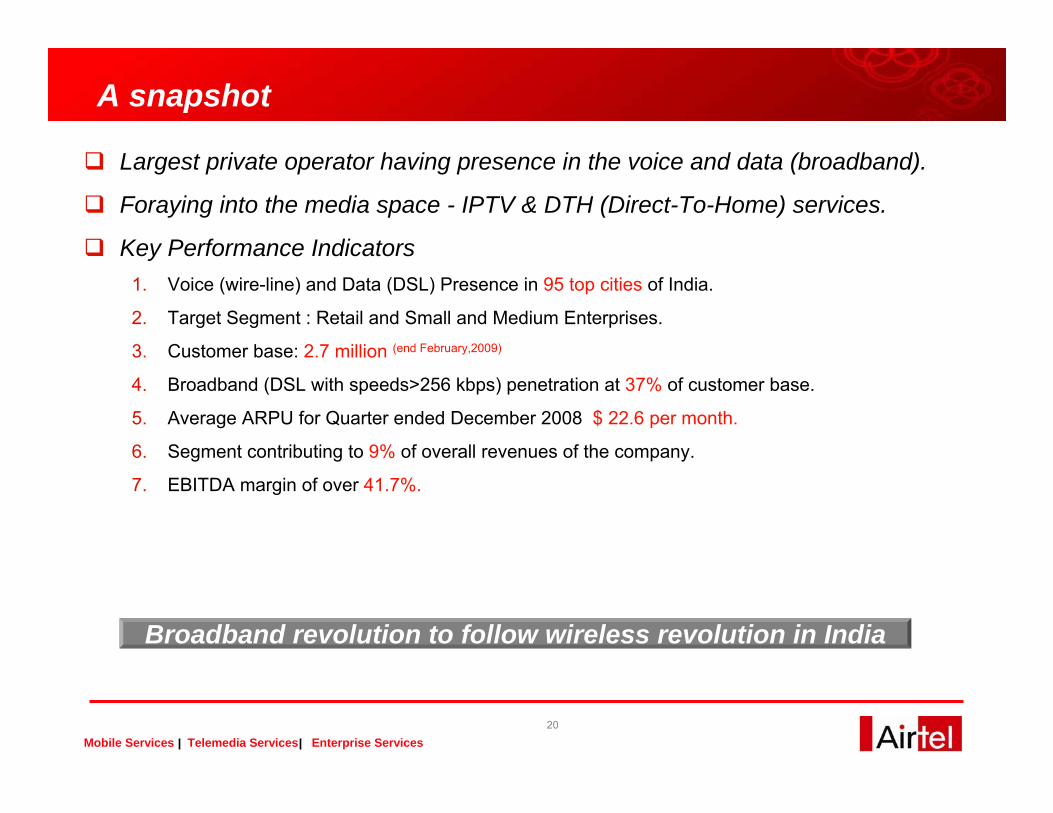

A snapshot

Largest private operator having presence in the voice and data (broadband).

Foraying into the media space - IPTV & DTH (Direct-To-Home) services.

Key Performance Indicators 1. Voice (wire-line) and Data (DSL) Presence in 95 top cities of India.

2. Target Segment : Retail and Small and Medium Enterprises.

3. Customer base: 2.7 million (end February,2009)

4. Broadband (DSL with speeds>256 kbps) penetration at 37% of customer base.

5. Average ARPU for Quarter ended December 2008 $ 22.6 per month.

6. Segment contributing to 9% of overall revenues of the company.

7. EBITDA margin of over 41.7%.

Broadband revolution to follow wireless revolution in India

21

Mobile Services Telemedia Services Enterprise Services

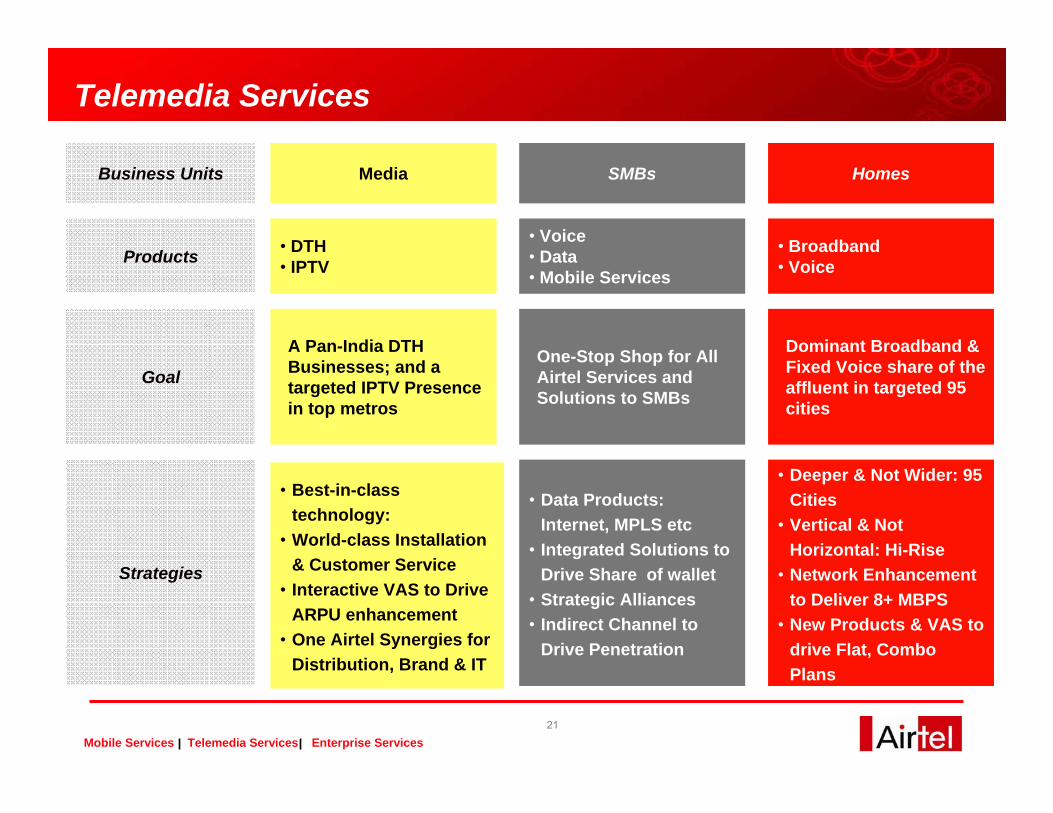

Telemedia Services

Business Units Media SMBs Homes

Products • DTH• IPTV

• Voice• Data• Mobile Services

• Broadband• Voice

Goal

A Pan-India DTH Businesses; and a targeted IPTV Presence in top metros

One-Stop Shop for All Airtel Services and Solutions to SMBs

Dominant Broadband & Fixed Voice share of the affluent in targeted 95 cities

Strategies

• Best-in-class technology:

• World-class Installation & Customer Service

• Interactive VAS to Drive ARPU enhancement

• One Airtel Synergies for Distribution, Brand & IT

• Data Products: Internet, MPLS etc

• Integrated Solutions to Drive Share of wallet

• Strategic Alliances• Indirect Channel to

Drive Penetration

• Deeper & Not Wider: 95 Cities

• Vertical & Not Horizontal: Hi-Rise

• Network Enhancement to Deliver 8+ MBPS

• New Products & VAS to drive Flat, Combo Plans

22

Mobile Services Telemedia Services Enterprise Services

Product Portfolio

Our Media Play

23

Mobile Services Telemedia Services Enterprise Services

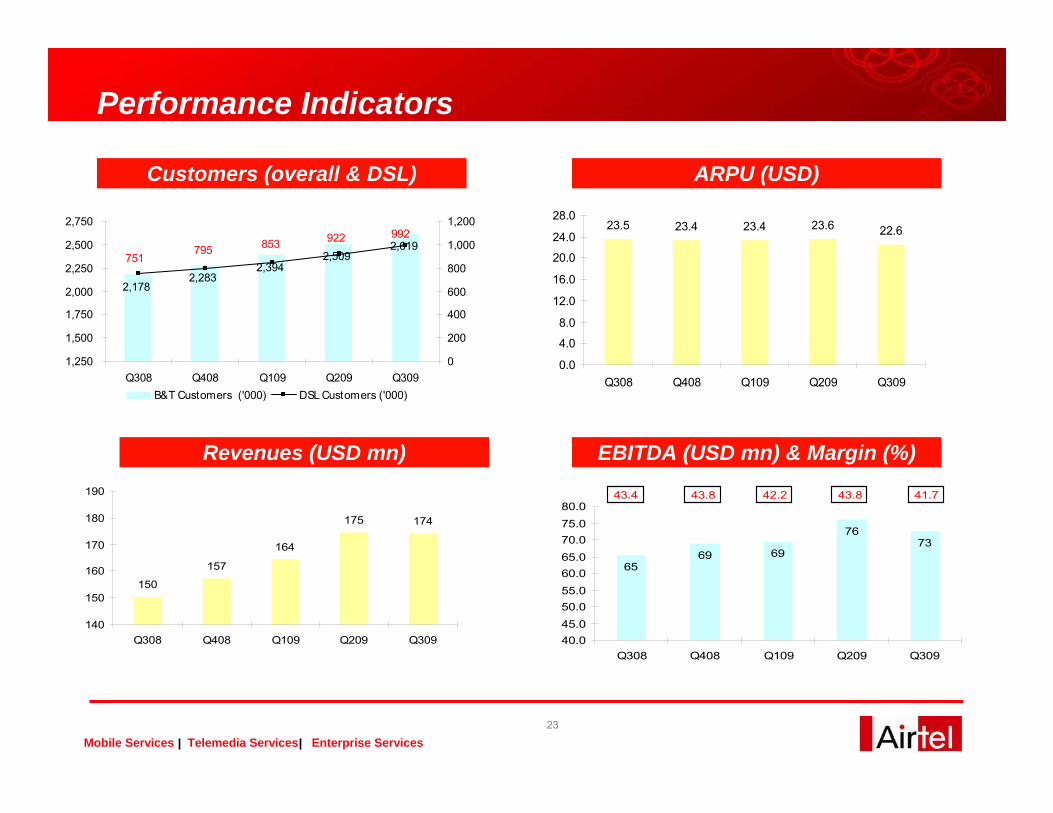

Performance Indicators

Customers (overall & DSL) ARPU (USD)

Revenues (USD mn) EBITDA (USD mn) & Margin (%)

2,2832,394

2,5092,619

2,178

992922853795751

1,250

1,500

1,750

2,000

2,250

2,500

2,750

Q308 Q408 Q109 Q209 Q3090

200

400

600

800

1,000

1,200

B&T Customers ('000) DSL Customers ('000)

23.5 23.4 23.4 23.6 22.6

0.0

4.0

8.0

12.0

16.0

20.0

24.0

28.0

Q308 Q408 Q109 Q209 Q309

150

157

164

175 174

140

150

160

170

180

190

Q308 Q408 Q109 Q209 Q309

6569 69

7673

40.045.050.055.060.065.070.075.080.0

Q308 Q408 Q109 Q209 Q309

43.4 43.8 42.2 43.8 41.7

24

Mobile Services Telemedia Services Enterprise Services

Enterprise Services

25

Mobile Services Telemedia Services Enterprise Services

A snapshotCarrier: - one of the largest carriers of voice and data, both domestic and international.

Corporate: - providing end to end telecom solutions to large corporate and Small & Medium Businesses.

Present Competition: National Long Distance: BSNL; Reliance; VSNL; Vodafone; Tata

International Long Distance: VSNL, Bharti, Reliance, BSNL

26

Mobile Services Telemedia Services Enterprise Services

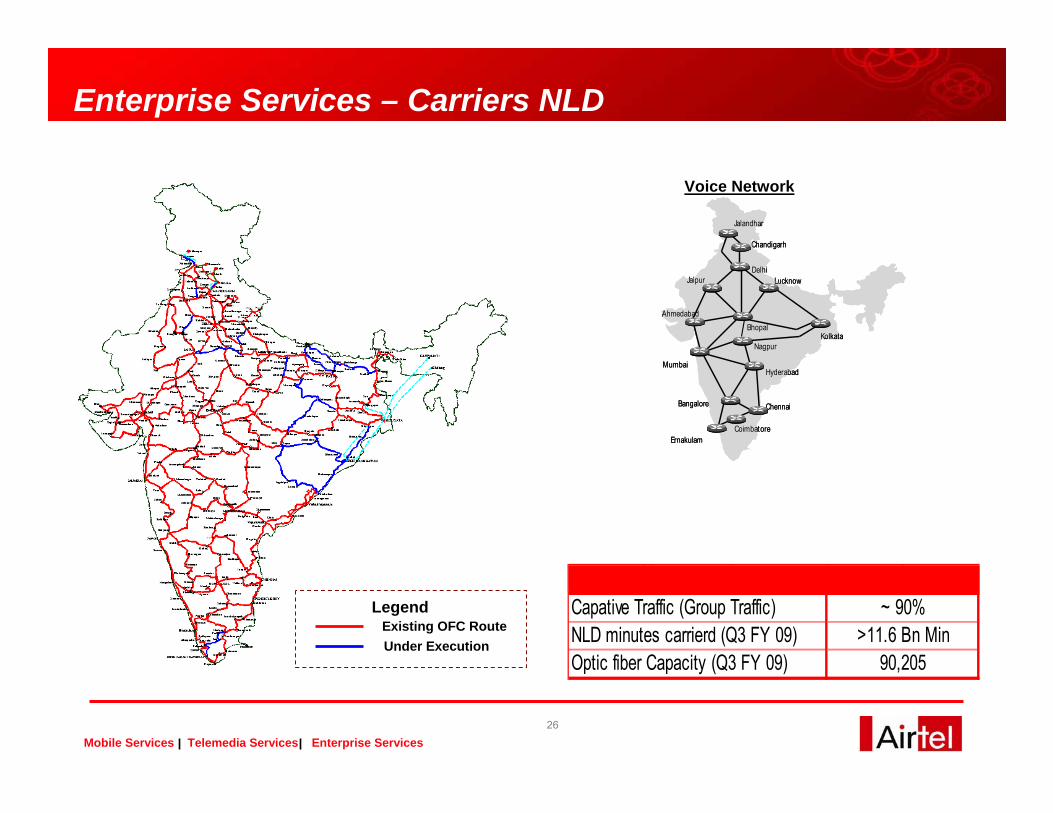

Enterprise Services – Carriers NLD

LegendExisting OFC RouteUnder Execution

Kolkata

Mumbai

Chennai

Hyderabad

Bangalore

Jaipur

Ahmedabad Bhopal

Chandigarh

Delhi

Nagpur

Lucknow

Jalandhar

ErnakulamCoimbatore

Kolkata

Mumbai

Chennai

Hyderabad

Bangalore

Jaipur

Ahmedabad Bhopal

Chandigarh

Delhi

Nagpur

Lucknow

Jalandhar

ErnakulamCoimbatore

Voice Network

Capative Traffic (Group Traffic)NLD minutes carrierd (Q3 FY 09)Optic fiber Capacity (Q3 FY 09)

~ 90%>11.6 Bn Min

90,205

27

Mobile Services Telemedia Services Enterprise Services

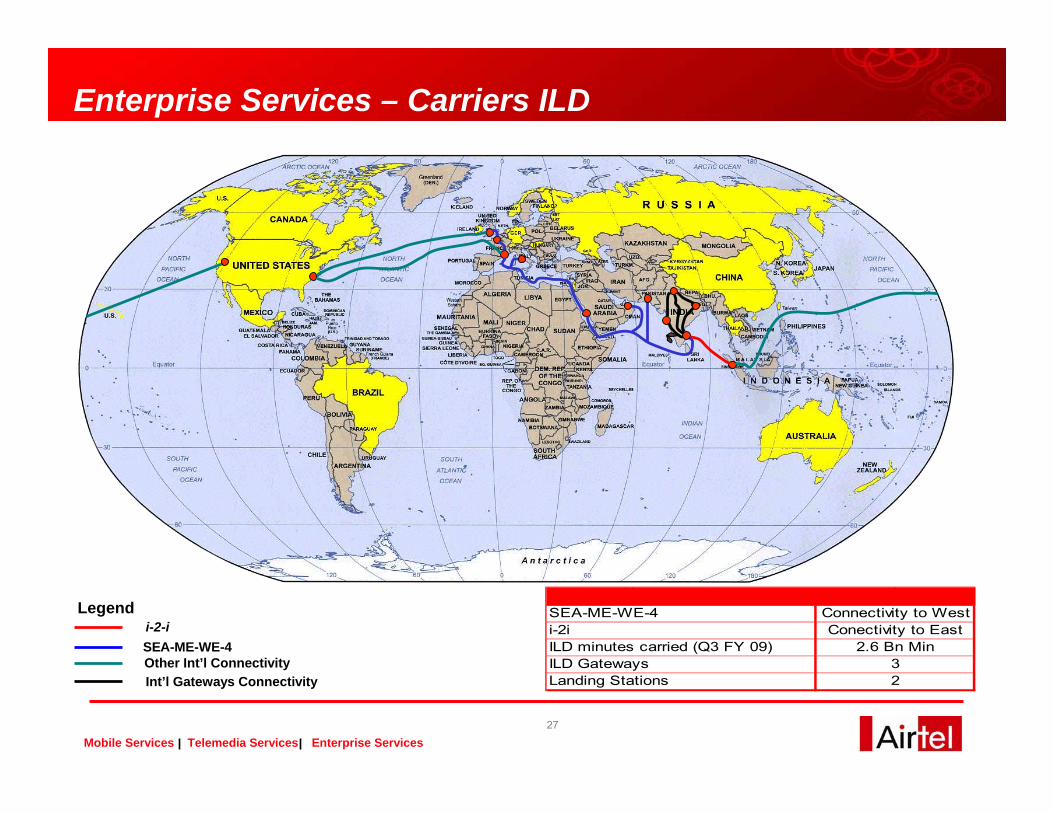

Enterprise Services – Carriers ILD

Legendi-2-iSEA-ME-WE-4Other Int’l ConnectivityInt’l Gateways Connectivity

SEA-ME-WE-4i-2i ILD minutes carried (Q3 FY 09)ILD GatewaysLanding Stations

Connectivity to West

32

Conectivity to East2.6 Bn Min

28

Mobile Services Telemedia Services Enterprise Services

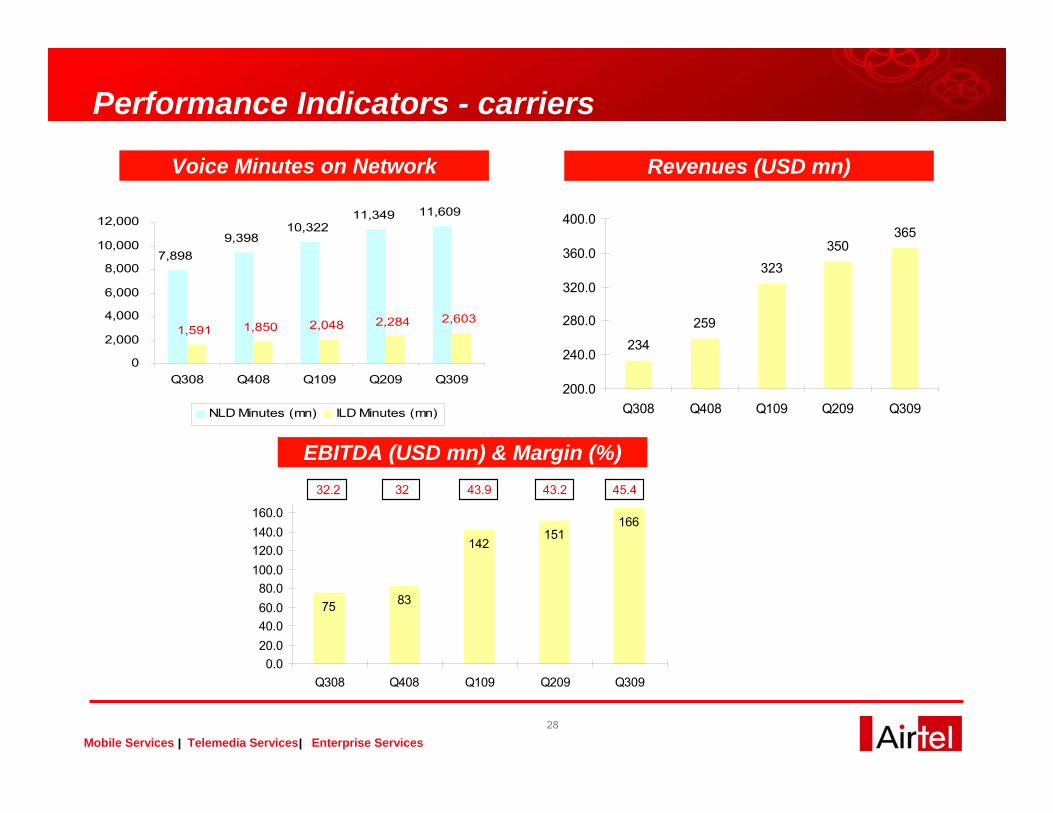

Performance Indicators - carriers

Voice Minutes on Network Revenues (USD mn)

EBITDA (USD mn) & Margin (%)

7,8989,398

10,32211,349 11,609

1,591 1,850 2,048 2,284 2,603

0

2,000

4,000

6,000

8,000

10,000

12,000

Q308 Q408 Q109 Q209 Q309

NLD Minutes (mn) ILD Minutes (mn)

234259

323350

365

200.0

240.0

280.0

320.0

360.0

400.0

Q308 Q408 Q109 Q209 Q309

75 83

142151

166

0.020.040.060.080.0

100.0120.0140.0160.0

Q308 Q408 Q109 Q209 Q309

32.2 32 43.9 43.2 45.4

29

Mobile Services Telemedia Services Enterprise Services

Enterprise Services - Corporates

Voice services

Satellite services Managed data & Internet services

Managed e -business services

Managed customized integrated solutions

Mobile services

competition limitedsegment one stop telecom solutiontarget 2,000 top large corporatesleveraging integrated play

30

Mobile Services Telemedia Services Enterprise Services

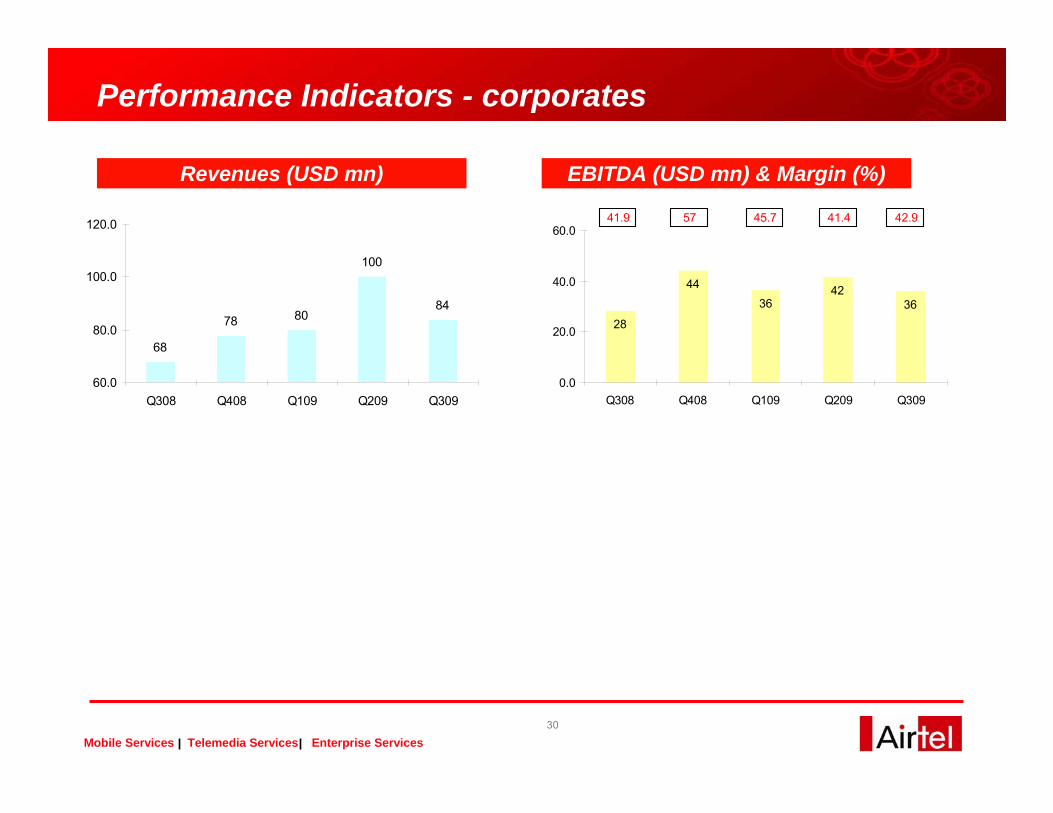

Performance Indicators - corporates

Revenues (USD mn) EBITDA (USD mn) & Margin (%)

68

78 80

100

84

60.0

80.0

100.0

120.0

Q308 Q408 Q109 Q209 Q309

28

4436

4236

0.0

20.0

40.0

60.0

Q308 Q408 Q109 Q209 Q309

41.9 57 45.7 41.4 42.9

31

Mobile Services Telemedia Services Enterprise Services

Passive Infrastructure Services

32

Mobile Services Telemedia Services Enterprise Services

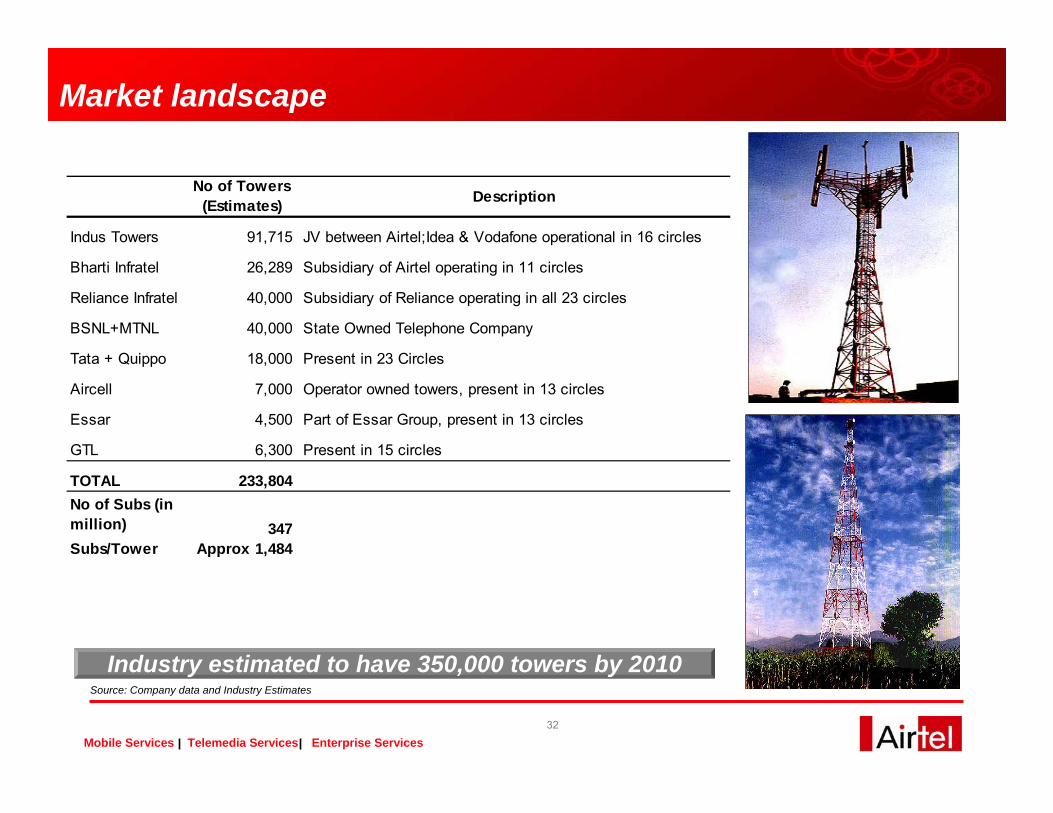

Market landscape

Industry estimated to have 350,000 towers by 2010Source: Company data and Industry Estimates

No of Towers (Estimates) Description

Indus Towers 91,715 JV between Airtel;Idea & Vodafone operational in 16 circles

Bharti Infratel 26,289 Subsidiary of Airtel operating in 11 circles

Reliance Infratel 40,000 Subsidiary of Reliance operating in all 23 circles

BSNL+MTNL 40,000 State Owned Telephone Company

Tata + Quippo 18,000 Present in 23 Circles

Aircell 7,000 Operator owned towers, present in 13 circles

Essar 4,500 Part of Essar Group, present in 13 circles

GTL 6,300 Present in 15 circles

TOTAL 233,804 No of Subs (in million) 347 Subs/Tower Approx 1,484

33

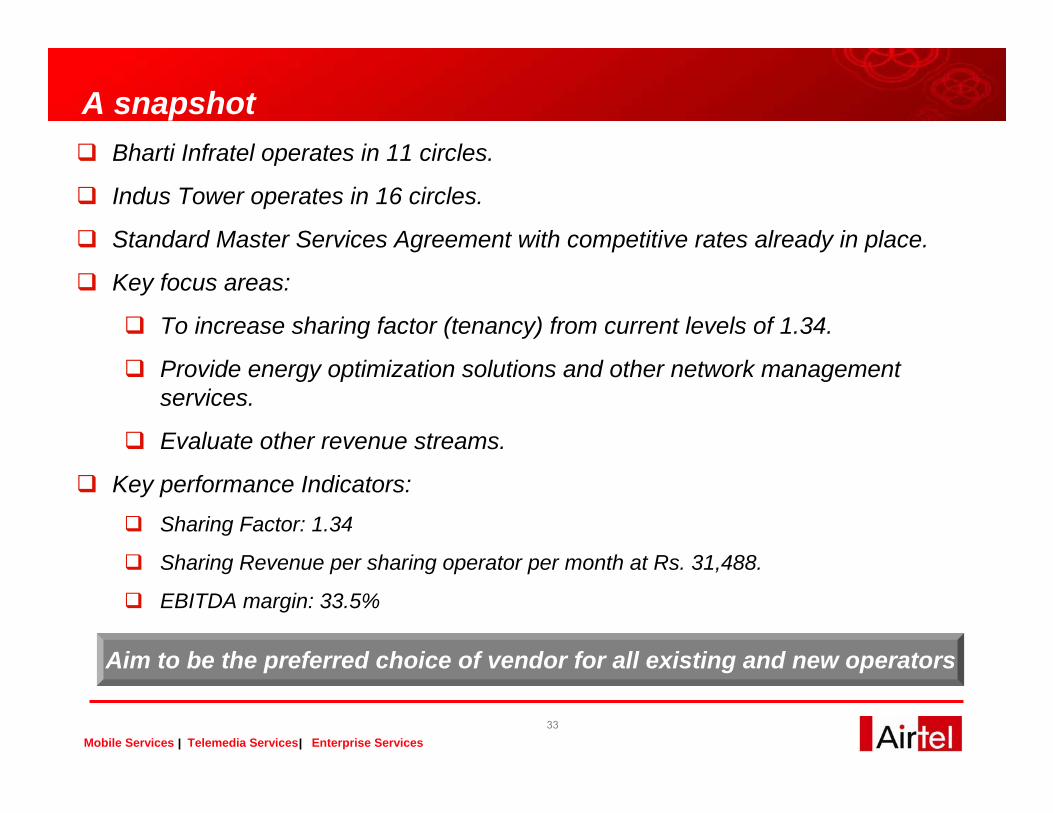

Mobile Services Telemedia Services Enterprise Services

A snapshotBharti Infratel operates in 11 circles.

Indus Tower operates in 16 circles.

Standard Master Services Agreement with competitive rates already in place.

Key focus areas:

To increase sharing factor (tenancy) from current levels of 1.34.

Provide energy optimization solutions and other network management services.

Evaluate other revenue streams.

Key performance Indicators:Sharing Factor: 1.34

Sharing Revenue per sharing operator per month at Rs. 31,488.

EBITDA margin: 33.5%

Aim to be the preferred choice of vendor for all existing and new operators

34

Mobile Services Telemedia Services Enterprise Services

To conclude

35

Mobile Services Telemedia Services Enterprise Services

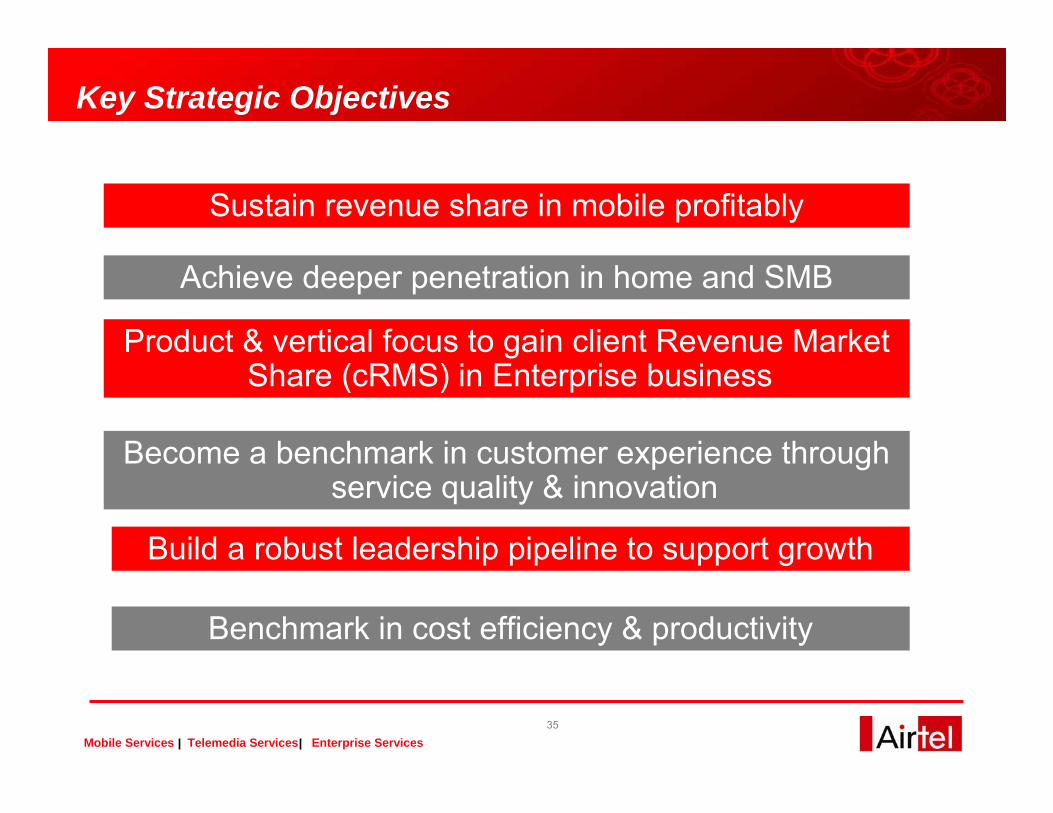

Key Strategic Objectives

Sustain revenue share in mobile profitably

Achieve deeper penetration in home and SMB

Product & vertical focus to gain client Revenue Market Share (cRMS) in Enterprise business

Become a benchmark in customer experience through service quality & innovation

Build a robust leadership pipeline to support growth

Benchmark in cost efficiency & productivity

DisclaimerThe information contained in this presentation is only current as of its date. All actions and statements made herein or otherwise shall be subject to the applicable laws and regulations as amended from time to time. There is no representation that all information relating to the context has been taken care off in the presentation and neither we undertake any obligation as to the regular updating of the information as a result of new information, future events or otherwise. We will accept no liability whatsoever for any loss arising directly or indirectly from the use of, reliance of any information contained in this presentation or for any omission of the information. The information shall not be distributed or used by any person or entity in any jurisdiction or countries were such distribution or use would be contrary to the applicable laws or Regulations. It is advised that prior to acting upon this presentation independent consultation / advise may be obtained and necessary due diligence, investigation etc may be done at your end. You may also contact us directly for any questions or clarifications at our end.

This presentation contain certain statements of future expectations and other forward-looking statements, including those relating to our general business plans and strategy, our future financial condition and growth prospects, and future developments in our industry and our competitive and regulatory environment. In addition to statements which are forward looking by reason of context, the words ‘may, will, should, expects, plans, intends, anticipates, believes, estimates, predicts, potential or continue’ and similar expressions identify forward looking statements.

Actual results, performances or events may differ materially from these forward-looking statements including the plans, objectives, expectations, estimates and intentions expressed in forward looking statements due to a number of factors, including without limitation future changes or developments in our business, our competitive environment, telecommunications technology and application, and political, economic, legal and social conditions in India. It is cautioned that the foregoing list is not exhaustive

This presentation is not being used in connection with any invitation of an offer or an offer of securities and should not be used as a basis for any investment decision.

Investor Relations :- http://www.bhartiairtel.inFor any queries, write to: [email protected]

“The information contained herein does not constitute an offer of securities for sale in the United States. Securities may not be sold in the United States absent registration or an exemption from registration under the U.S. Securities Act of 1933, as amended. Any public offering of securities to be made in the United States will be made by means of a prospectus and will contain detailed information about the Company and its management, as well as financial statements. No money, securities or other consideration is being solicited, and, if sent in response to the information contained herein, will not be accepted.”