Embed Size (px)

DESCRIPTION

AGROBANCO, RURAL DEVELOPMENT BANK. Contents. - Strategic Planning - Participation and Portfolio Growth - Term of Placements - Growth of our Clients - Portfolio Quality - Potential Demand - National Coverage - Financial Products - Major Crops Financed - Financial Results - ANNEXES - PowerPoint PPT Presentation

Citation preview

AGROBANCO, RURAL DEVELOPMENT BANK

Contents

- Strategic Planning- Participation and Portfolio Growth- Term of Placements- Growth of our Clients- Portfolio Quality- Potential Demand- National Coverage- Financial Products- Major Crops Financed- Financial Results- ANNEXES - Human Resources and Business Managers - Other Services - Other Variables

Section OneStrategic Planning

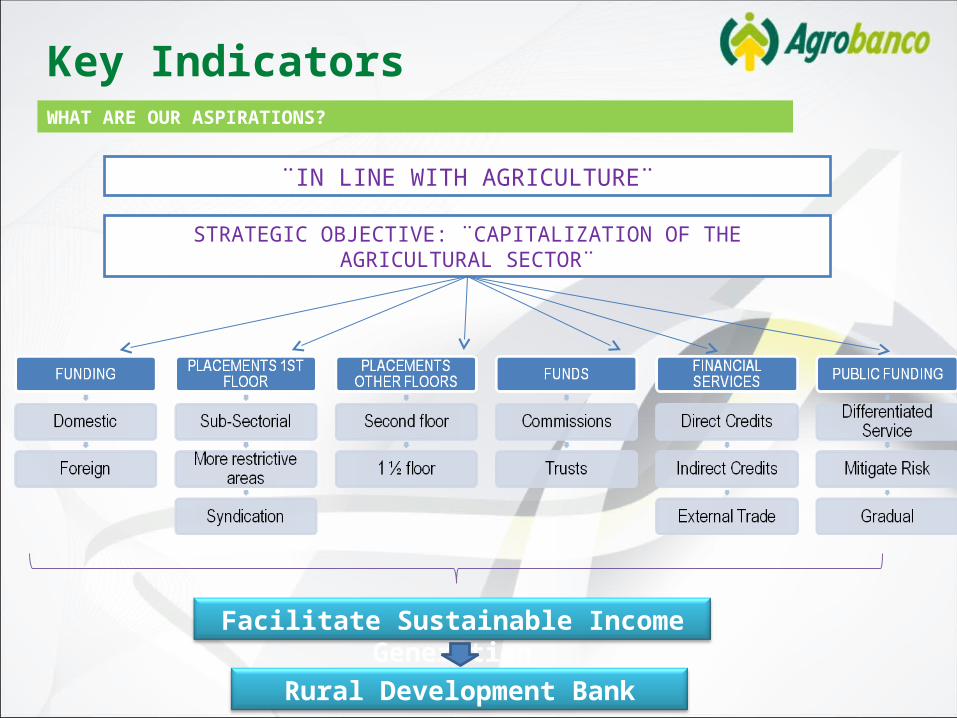

WHAT ARE OUR ASPIRATIONS?

Key Indicators

¨IN LINE WITH AGRICULTURE¨

Facilitate Sustainable Income Generation

STRATEGIC OBJECTIVE: ¨CAPITALIZATION OF THE AGRICULTURAL SECTOR¨

Rural Development Bank

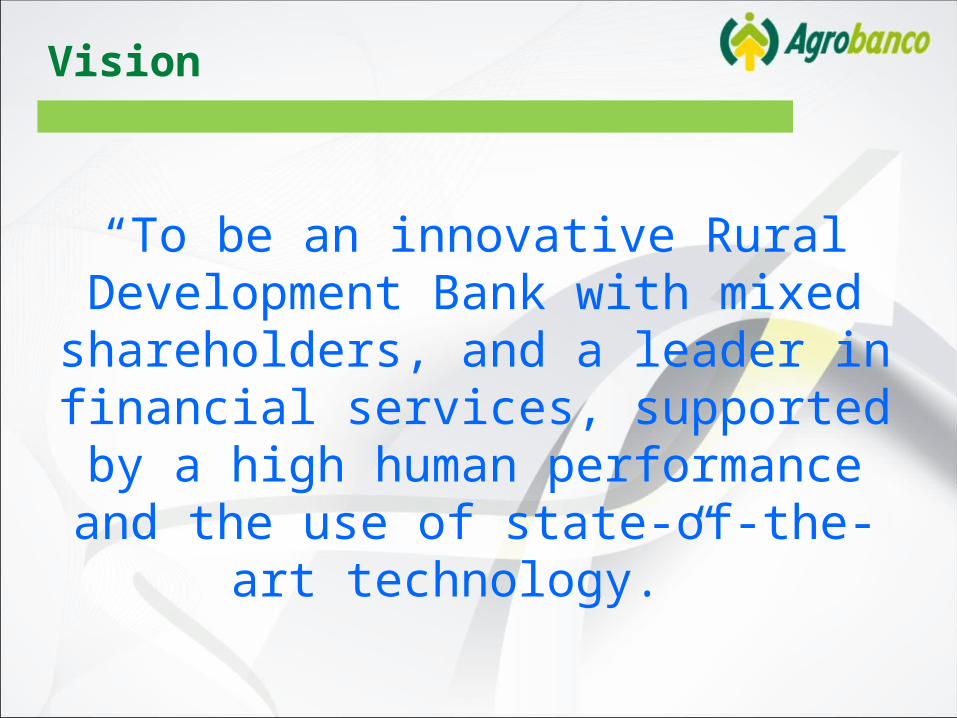

Vision

“To be an innovative Rural Development Bank with mixed shareholders, and a leader in financial

services, supported by a high human performance and the use of state-of-the-art

technology.”

Mission

“To provide financial products and services in promotion of rural savings and accompany the

development of production, agricultural businesses and complementary activities in the rural areas, focused on the financial inclusion of

people in poverty and/or other limitations.”

Section TwoParticipation and Portfolio Growth

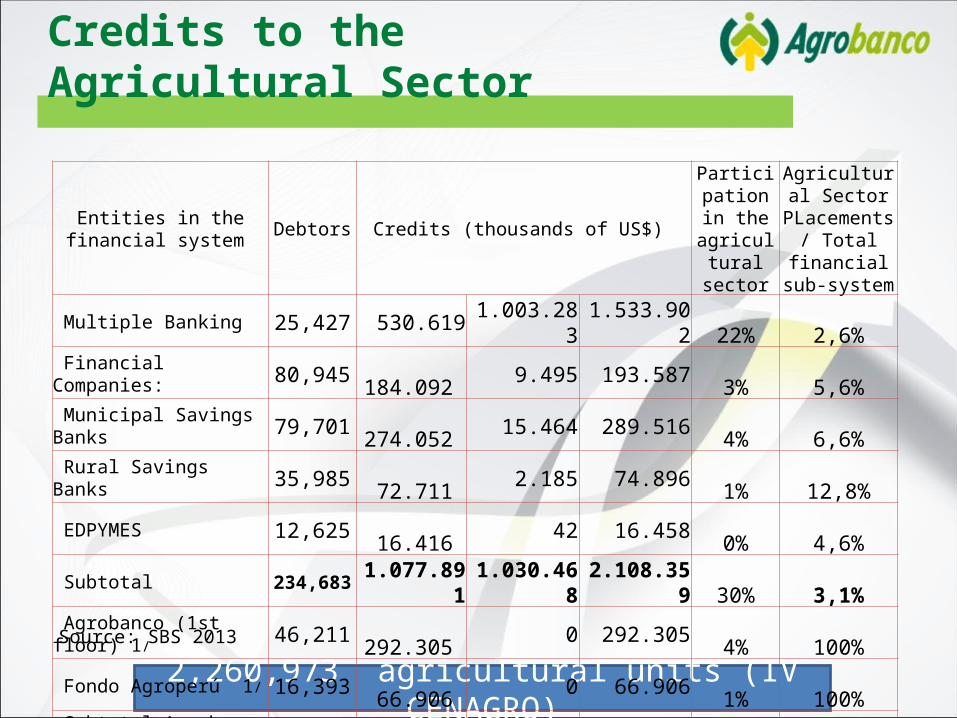

2,260,973 agricultural units (IV CENAGRO)

Credits to the Agricultural Sector

Entities in the financial system Debtors Credits (thousands of US$)

Participation in the

agricultural sector

Agricultural Sector

PLacements / Total financial

sub-system Multiple Banking 25,427 530.619 1.003.283 1.533.902 22% 2,6% Financial Companies: 80,945 184.092 9.495 193.587 3% 5,6% Municipal Savings Banks 79,701 274.052 15.464 289.516 4% 6,6% Rural Savings Banks 35,985 72.711 2.185 74.896 1% 12,8% EDPYMES 12,625 16.416 42 16.458 0% 4,6% Subtotal 234,683 1.077.891 1.030.468 2.108.359 30% 3,1% Agrobanco (1st floor) 1/ 46,211 292.305 0 292.305 4% 100% Fondo Agroperú 1/ 16,393 66.906 0 66.906 1% 100% Subtotal Agrobanco 62,604 359.211 0 359.211 5% 100% Total 297,287 1.437.102 1.030.468 2.467.570 35% 3,6% Agrobanco (2nd floor) 1/ 7,966 9.043 0 9.043 0% Total AGROBANCO 70,570 368.254 0 368.254 5% 1/ Placements December 2013

Source: SBS 2013

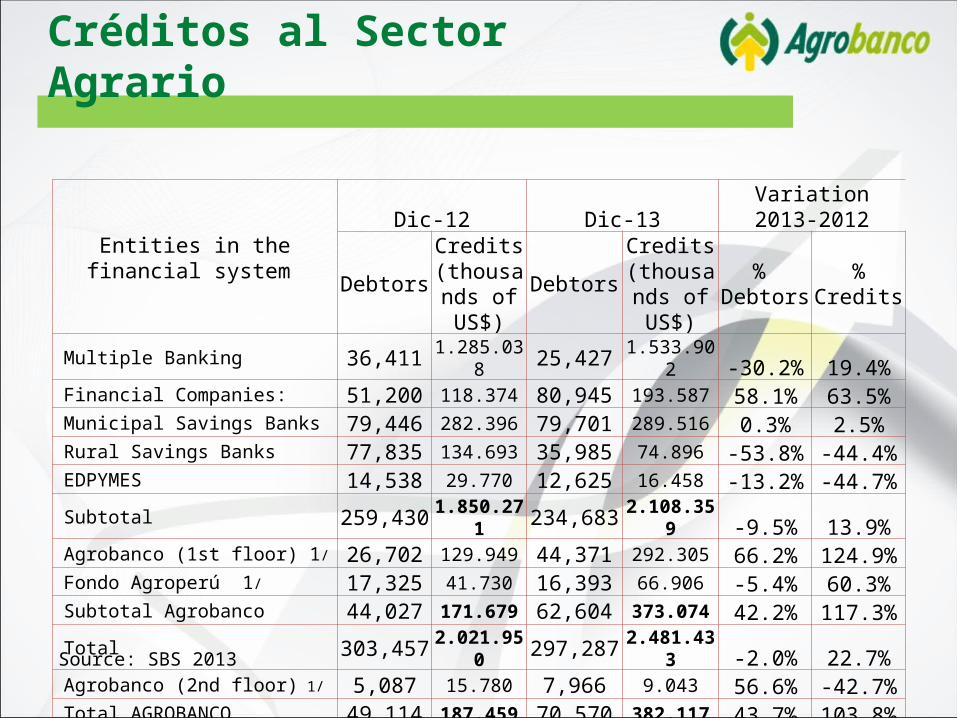

Créditos al Sector Agrario

Entities in the financial system

Dic-12 Dic-13 Variation 2013-2012

DebtorsCredits

(thousands of US$)

DebtorsCredits

(thousands of US$)

% Debtors

%Credits

Multiple Banking 36,411 1.285.038 25,427 1.533.902 -30.2% 19.4% Financial Companies: 51,200 118.374 80,945 193.587 58.1% 63.5% Municipal Savings Banks 79,446 282.396 79,701 289.516 0.3% 2.5% Rural Savings Banks 77,835 134.693 35,985 74.896 -53.8% -44.4% EDPYMES 14,538 29.770 12,625 16.458 -13.2% -44.7% Subtotal 259,430 1.850.271 234,683 2.108.359 -9.5% 13.9% Agrobanco (1st floor) 1/ 26,702 129.949 44,371 292.305 66.2% 124.9% Fondo Agroperú 1/ 17,325 41.730 16,393 66.906 -5.4% 60.3% Subtotal Agrobanco 44,027 171.679 62,604 373.074 42.2% 117.3% Total 303,457 2.021.950 297,287 2.481.433 -2.0% 22.7% Agrobanco (2nd floor) 1/ 5,087 15.780 7,966 9.043 56.6% -42.7% Total AGROBANCO 49,114 187.459 70,570 382.117 43.7% 103.8%

Source: SBS 2013

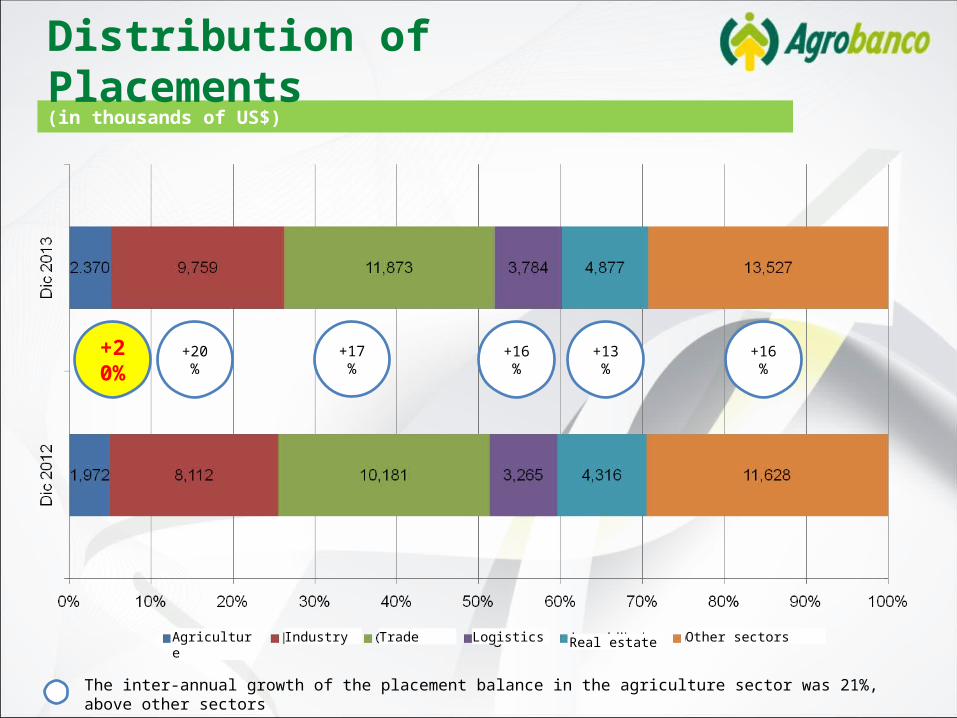

(in thousands of US$)

Distribution of Placements

+20%

+20% +17% +16% +13% +16%

The inter-annual growth of the placement balance in the agriculture sector was 21%, above other sectors

Agriculture Industry Trade Logistics Real estate Other sectors

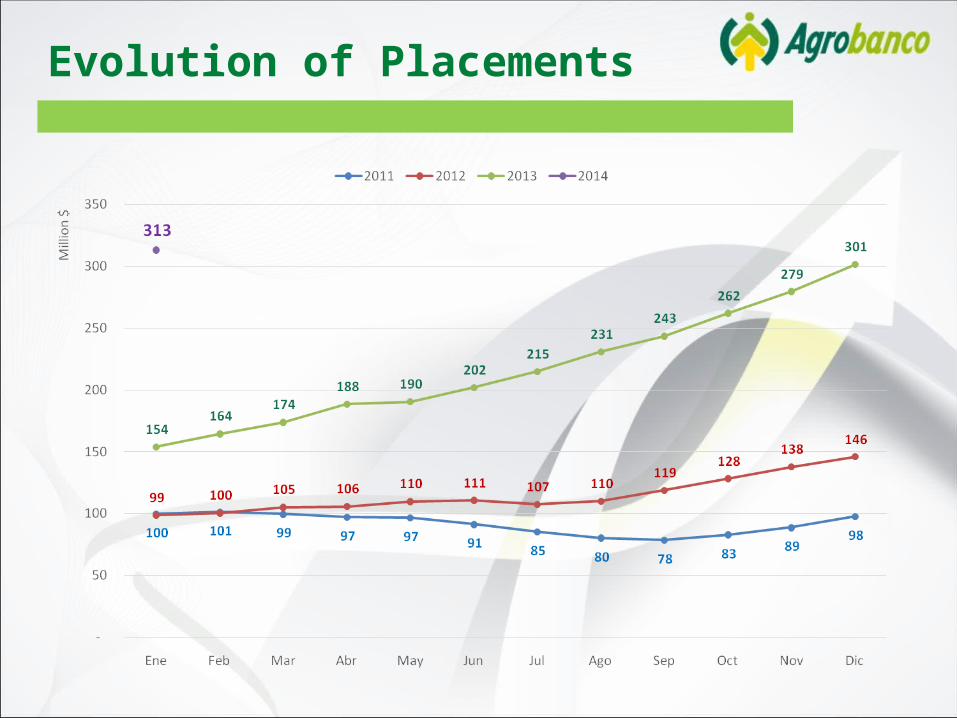

Evolution of Placements

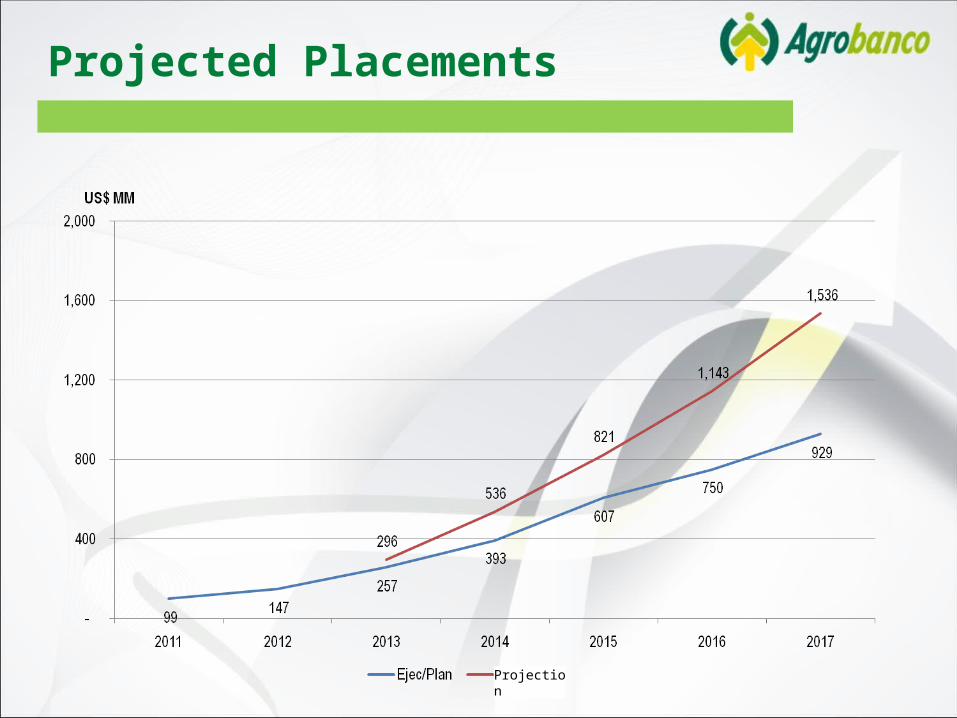

Projected Placements

Projection

+ 94%

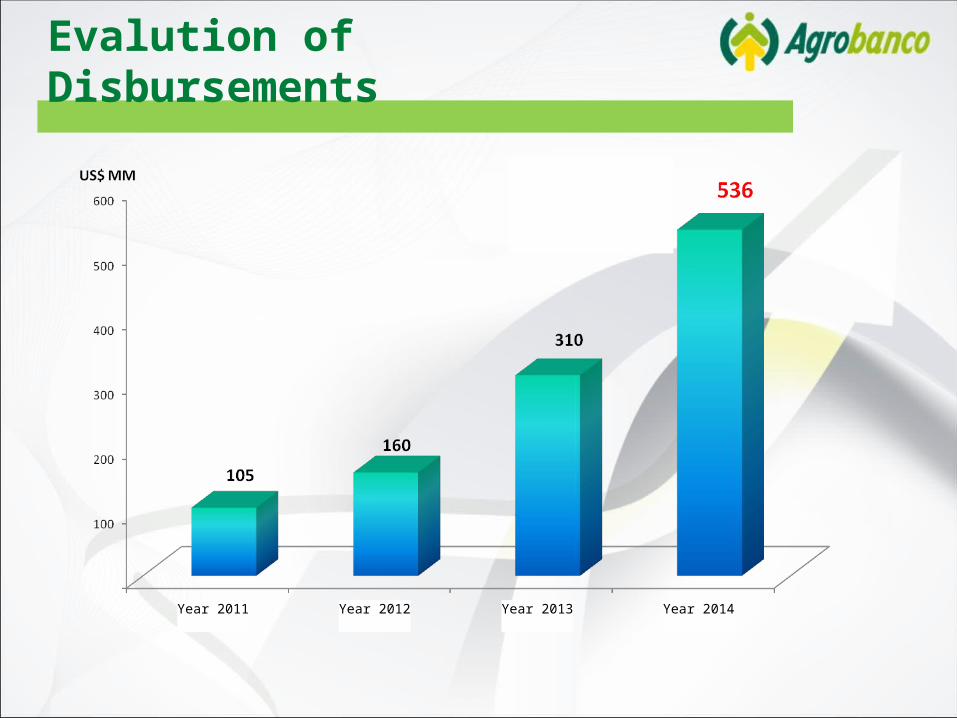

Evalution of Disbursements

Year 2011 Year 2012 Year 2013 Year 2014

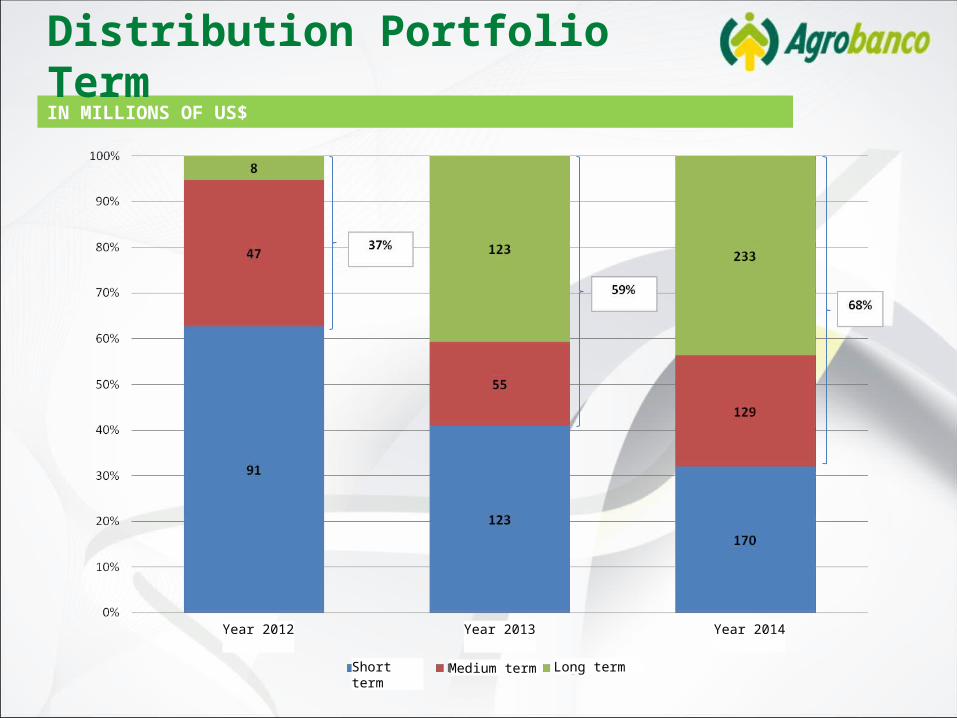

Section ThreeTerm of Placements

IN MILLIONS OF US$

Distribution Portfolio Term

Year 2012 Year 2013 Year 2014

Short term Medium term Long term

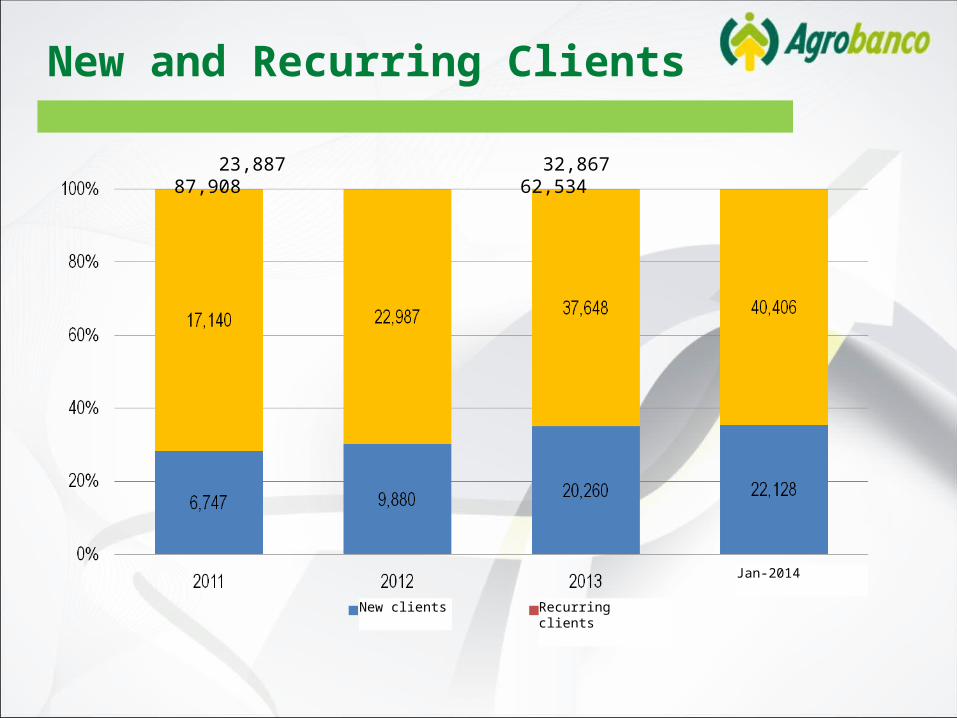

Section FourGrowth of our Clients

New and Recurring Clients

23,887 32,867 87,908 62,534

New clients Recurring clients

Jan-2014

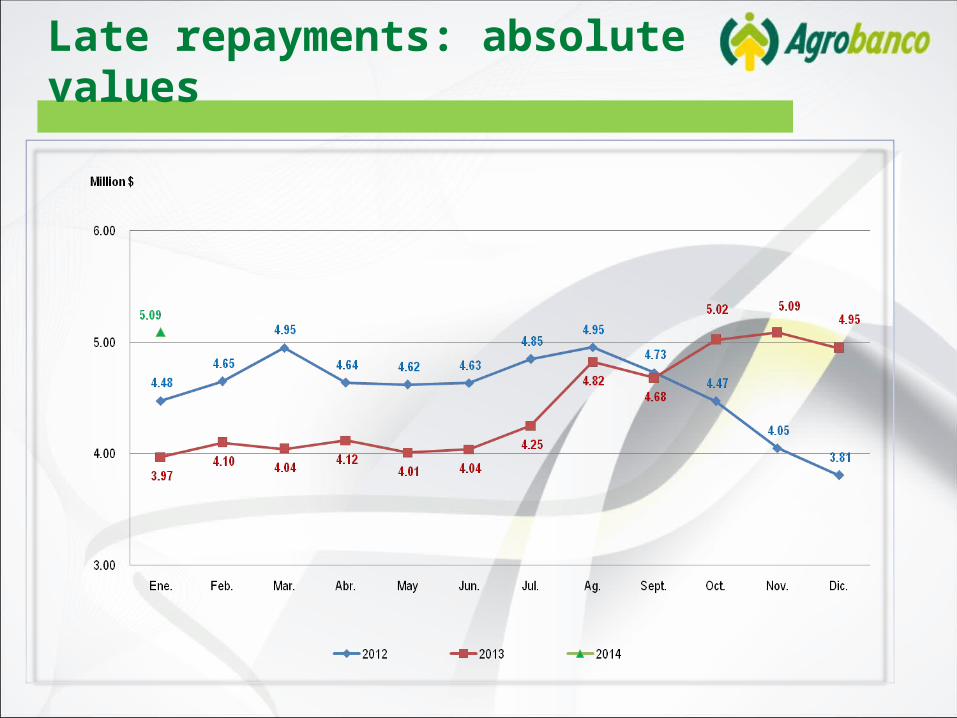

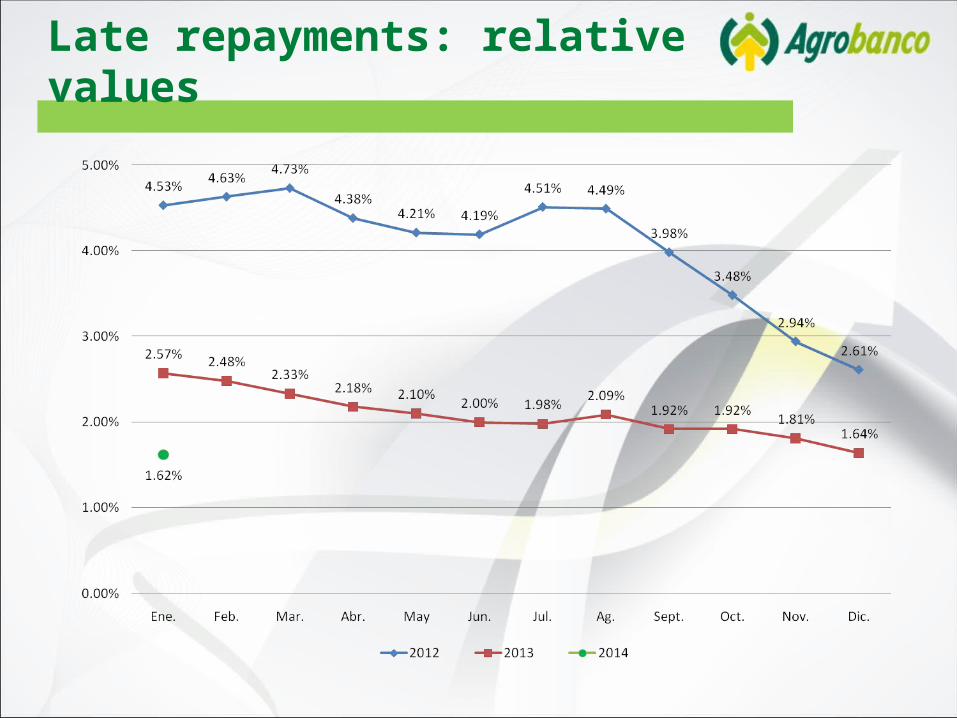

Section Five Portfolio Quality

Late repayments: absolute values

Late repayments: relative values

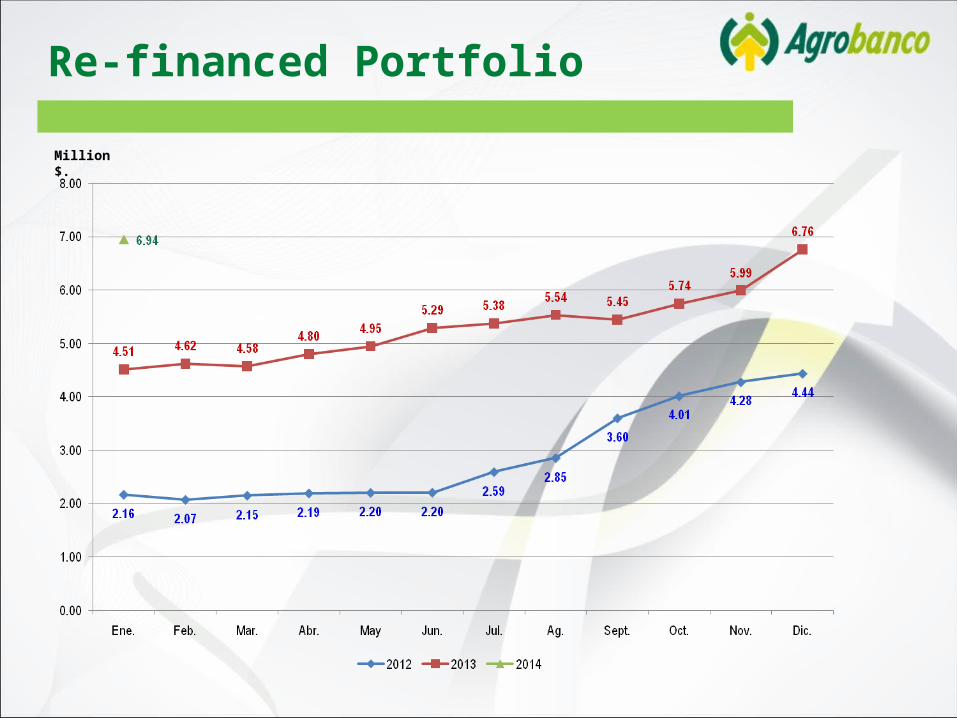

Re-financed Portfolio

Million $.

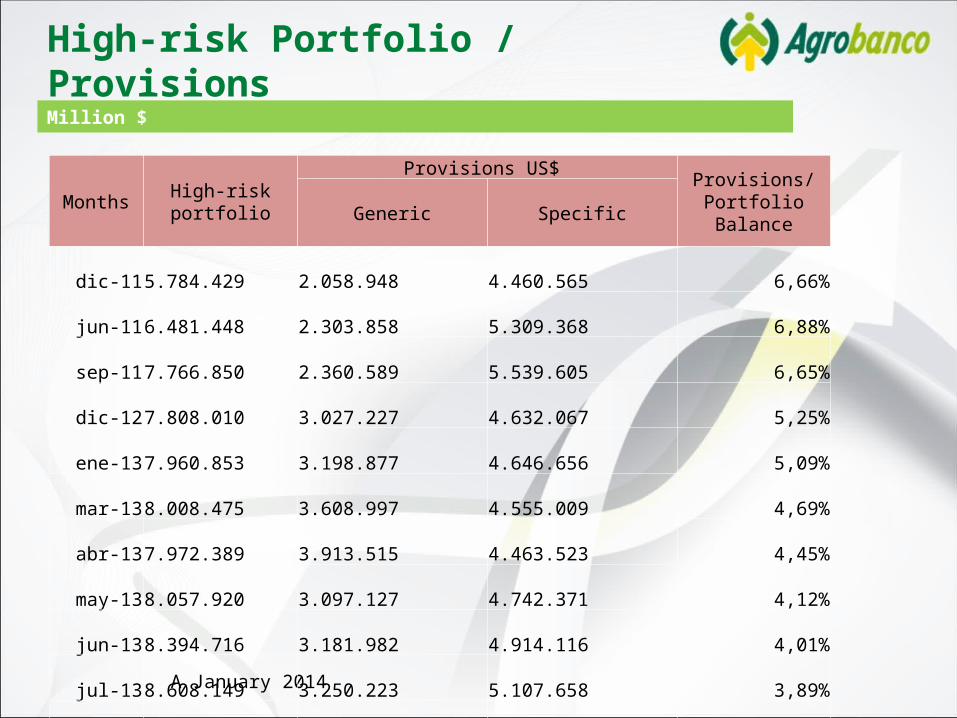

High-risk Portfolio

Million $.

Million $

High-risk Portfolio / Provisions

A January 2014

Months High-risk portfolioProvisions US$

Provisions/Portfolio BalanceGeneric Specific

dic-11 5.784.429 2.058.948 4.460.565 6,66%jun-11 6.481.448 2.303.858 5.309.368 6,88%sep-11 7.766.850 2.360.589 5.539.605 6,65%dic-12 7.808.010 3.027.227 4.632.067 5,25%

ene-13 7.960.853 3.198.877 4.646.656 5,09%mar-13 8.008.475 3.608.997 4.555.009 4,69%abr-13 7.972.389 3.913.515 4.463.523 4,45%

may-13 8.057.920 3.097.127 4.742.371 4,12%jun-13 8.394.716 3.181.982 4.914.116 4,01%jul-13 8.608.149 3.250.223 5.107.658 3,89%

ago-13 9.036.674 3.484.977 5.265.334 3,79%sep-13 8.857.597 3.469.146 5.048.104 3,50%oct-13 9.283.495 3.740.113 5.049.874 3,36%nov-13 9.691.040 3.964.911 5.422.109 3,34%dic-13 10.400.234 4.292.820 5.590.890 3,28%

ene-14 9.201.281 4.466.594 5.806.671 3,28%

Economic losses: penalties

Year 2011 2012 2013 Jan-14

Amount Capital Penalty US$ 2.298.337 1.026.534 1.377.254 0

Equity US$ 99.298.883 124.485.024 150.111.682 150.896.033

Disbursements US$ 104.745.938 158.744.572 312.009.553 40.832.074

Economic Loss % 2.3% 0.8% 0.9% 0.0%

Section SixPotential Demand

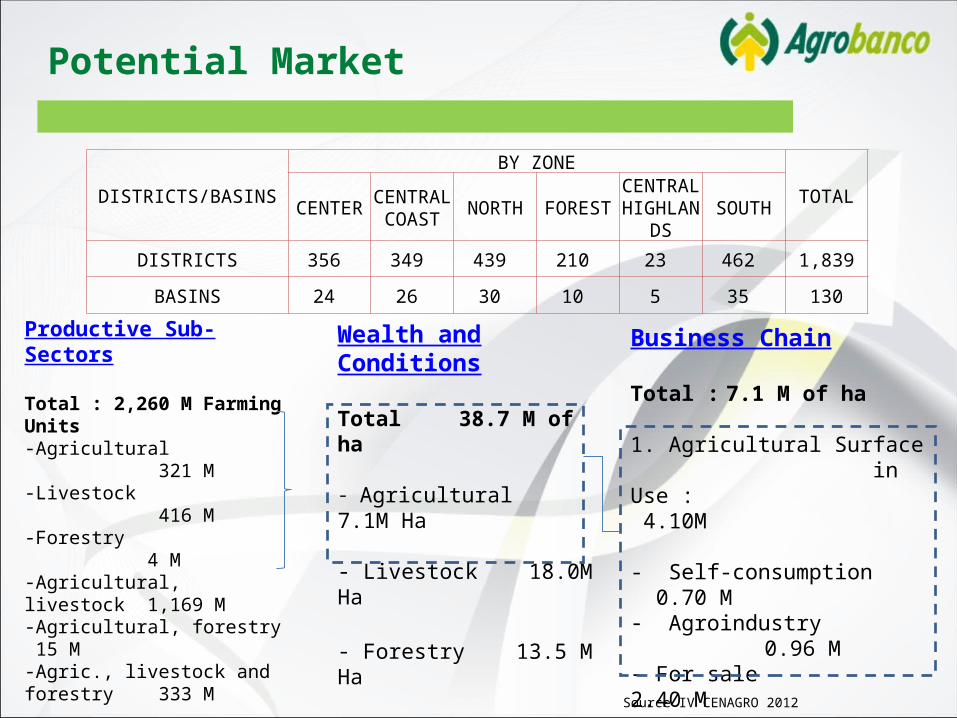

Productive Sub-Sectors

Total : 2,260 M Farming Units-Agricultural 321 M-Livestock 416 M -Forestry 4 M -Agricultural, livestock 1,169 M-Agricultural, forestry 15 M -Agric., livestock and forestry 333 M

Property and conditionIrrigation and basinsEnergy supplyAltitudinal tiers

Wealth and Conditions

Total 38.7 M of ha

- Agricultural 7.1M Ha - Livestock 18.0M Ha

- Forestry 13.5 M Ha

Business Chain

Total : 7.1 M of ha

1. Agricultural Surface in Use : 4.10M

- Self-consumption 0.70 M- Agroindustry 0.96 M- For sale 2.40 M

2. Agricultural Surface in Development: 3.00 M

DISTRICTS/BASINS

BY ZONE

TOTALCENTER CENTRAL

COAST NORTH FORESTCENTRAL HIGHLAN

DSSOUTH

DISTRICTS 356 349 439 210 23 462 1,839

BASINS 24 26 30 10 5 35 130

Source IV CENAGRO 2012

Potential Market

Potential Market

North AreaPotential debtors 189,371Agrobanco debtors 7,142Agricultural sector debtors 92,269

Agrobanco participation 8%

Central Coast AreaPotential debtors 30,213Agrobanco debtors 3,576Agricultural sector debtors 52,496

Agrobanco participation 7%

Rainforest AreaPotential debtors 41,304Agrobanco debtors 5,716Agricultural sector debtors 34,546

Agrobanco participation 17%

Central AreaPotential debtors 29,685Agrobanco debtors 5,908Agricultural sector debtors 42,093

Agrobanco participation 14%

South AreaPotential debtors 34,916Agrobanco debtors 8,725Agricultural sector debtors 80,762

Agrobanco participation 11%

15

18

10

10

17

DomesticPotential debtors 325,489Agrobanco debtors 31,067Agricultural sector debtors 302,166

Agrobanco participation 10%

Number of points of sale (Dec. 13)AGROBANCO

458

507 385

113

111

Number of points of sale (Dec. 13)Financial System

Source: National Agricultural Sector 2012 – INEI; SBS (2012)

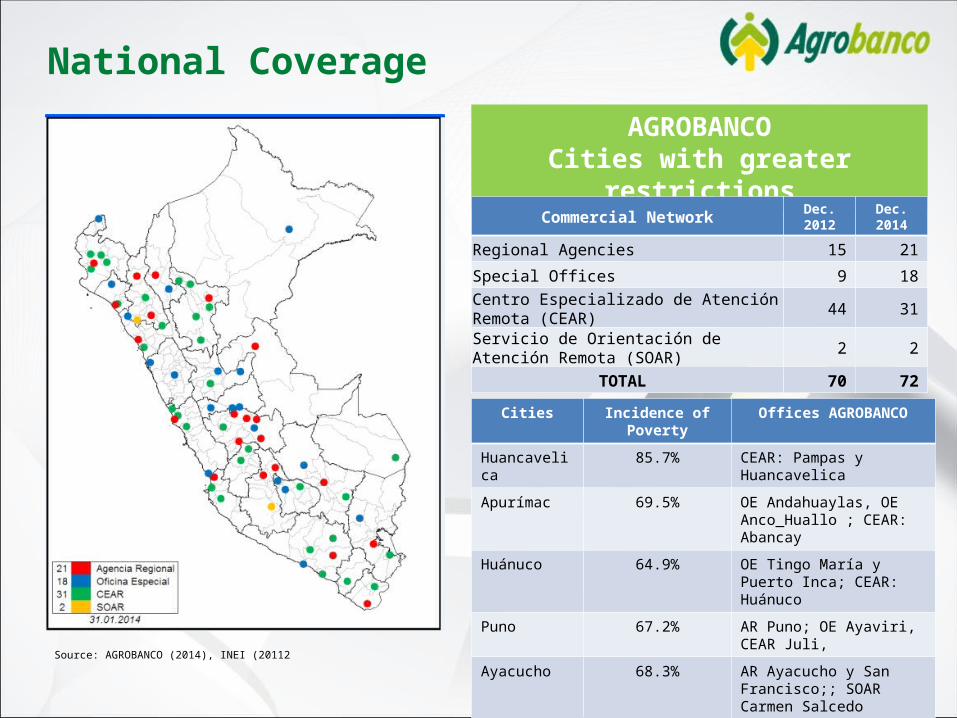

Section SevenNational Coverage

National Coverage

AGROBANCOCities with greater restrictions

Source: AGROBANCO (2014), INEI (20112

Cities Incidence of Poverty Offices AGROBANCO

Huancavelica 85.7% CEAR: Pampas y Huancavelica

Apurímac 69.5% OE Andahuaylas, OE Anco_Huallo ; CEAR: Abancay

Huánuco 64.9% OE Tingo María y Puerto Inca; CEAR: Huánuco

Puno 67.2% AR Puno; OE Ayaviri, CEAR Juli,

Ayacucho 68.3% AR Ayacucho y San Francisco;; SOAR Carmen Salcedo

TOTAL

03 Agencia Regional05 Oficina Especial

05 CEARs01 SOAR

Commercial Network Dec. 2012 Dec. 2014

Regional Agencies 15 21

Special Offices 9 18Centro Especializado de Atención Remota (CEAR) 44 31

Servicio de Orientación de Atención Remota (SOAR) 2 2

TOTAL 70 72

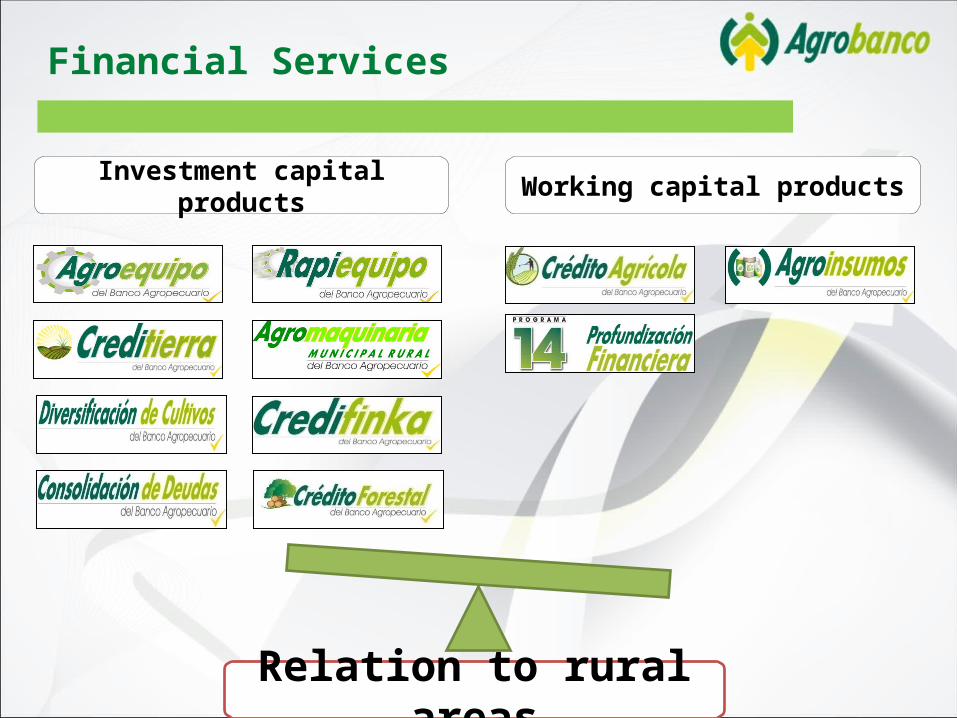

Section EightFinancial Products

Investment capital products Working capital products

Relation to rural areas

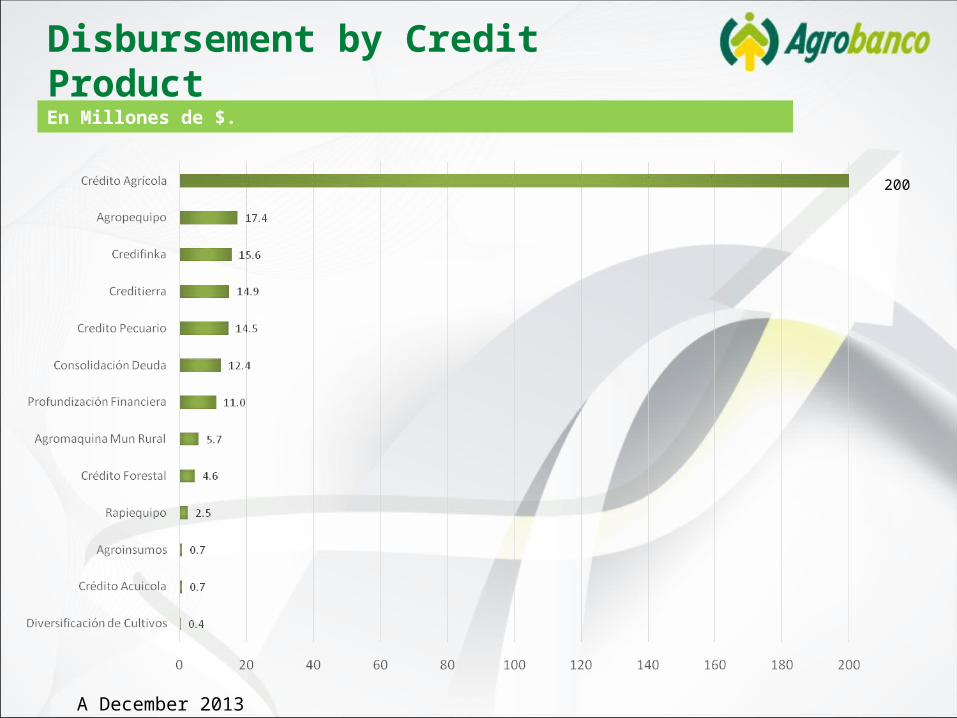

Financial Services

En Millones de $.

Disbursement by Credit Product

A December 2013

200

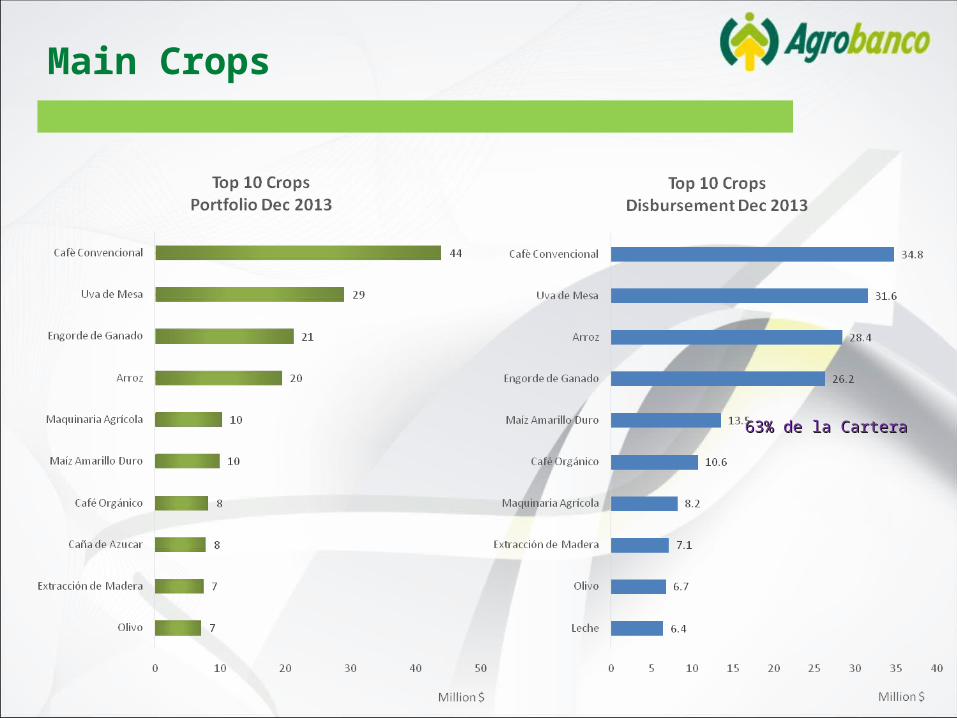

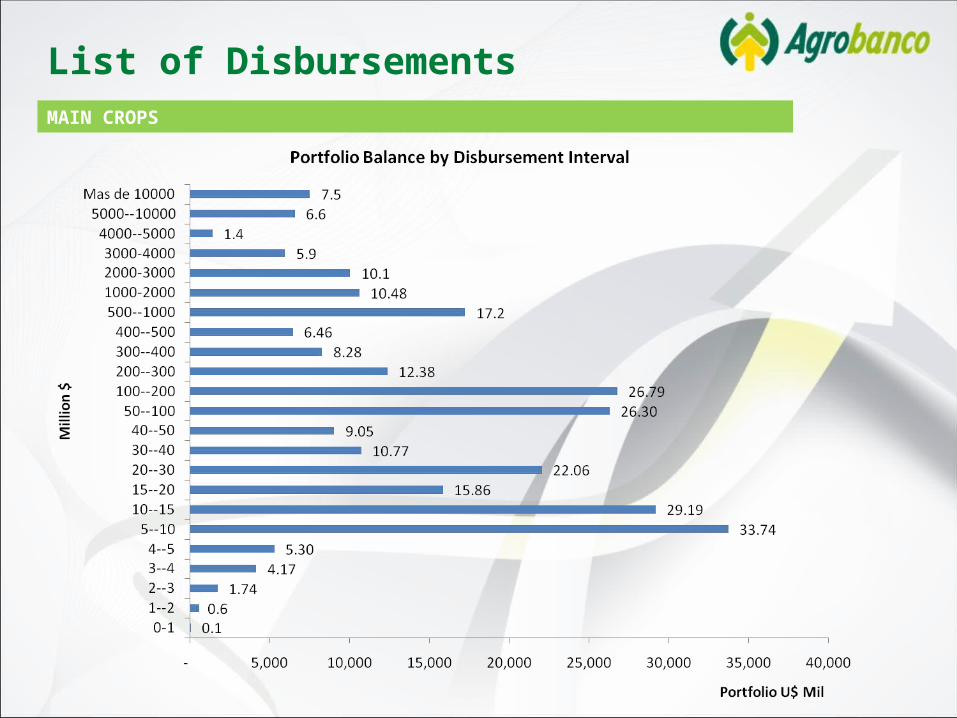

Section NineMajor Crops Financed

63% de la Cartera63% de la Cartera

Main Crops

MAIN CROPS

List of Disbursements

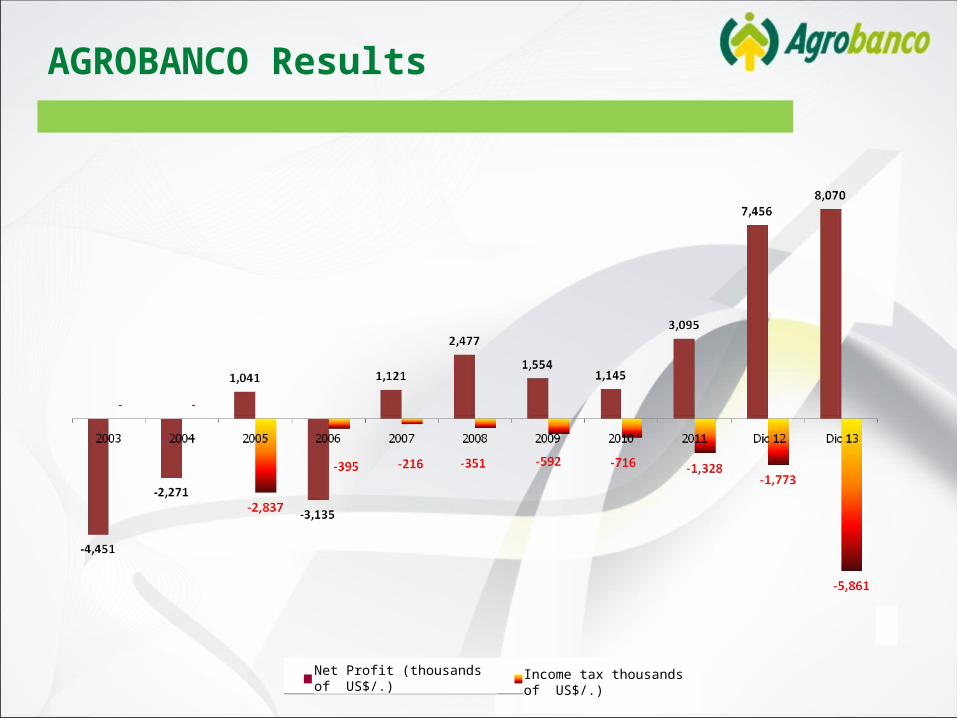

Section TenFinancial Results

AGROBANCO Results

Net Profit (thousands of US$/.) Income tax thousands of US$/.)

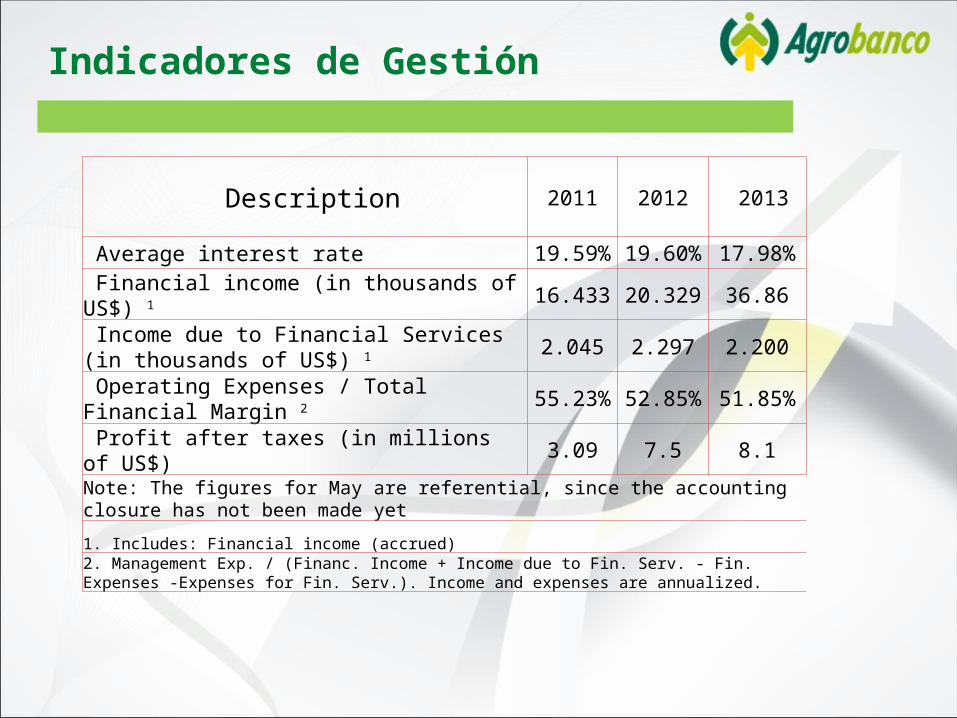

Indicadores de Gestión

Description 2011 2012 2013

Average interest rate 19.59% 19.60% 17.98%

Financial income (in thousands of US$) 1 16.433 20.329 36.86 Income due to Financial Services (in thousands of US$) 1

2.045 2.297 2.200

Operating Expenses / Total Financial Margin 2 55.23% 52.85% 51.85%

Profit after taxes (in millions of US$) 3.09 7.5 8.1Note: The figures for May are referential, since the accounting closure has not been made yet

1. Includes: Financial income (accrued)2. Management Exp. / (Financ. Income + Income due to Fin. Serv. - Fin. Expenses -Expenses for Fin. Serv.). Income and expenses are annualized.

INVESTMENT GRADE

International Rating

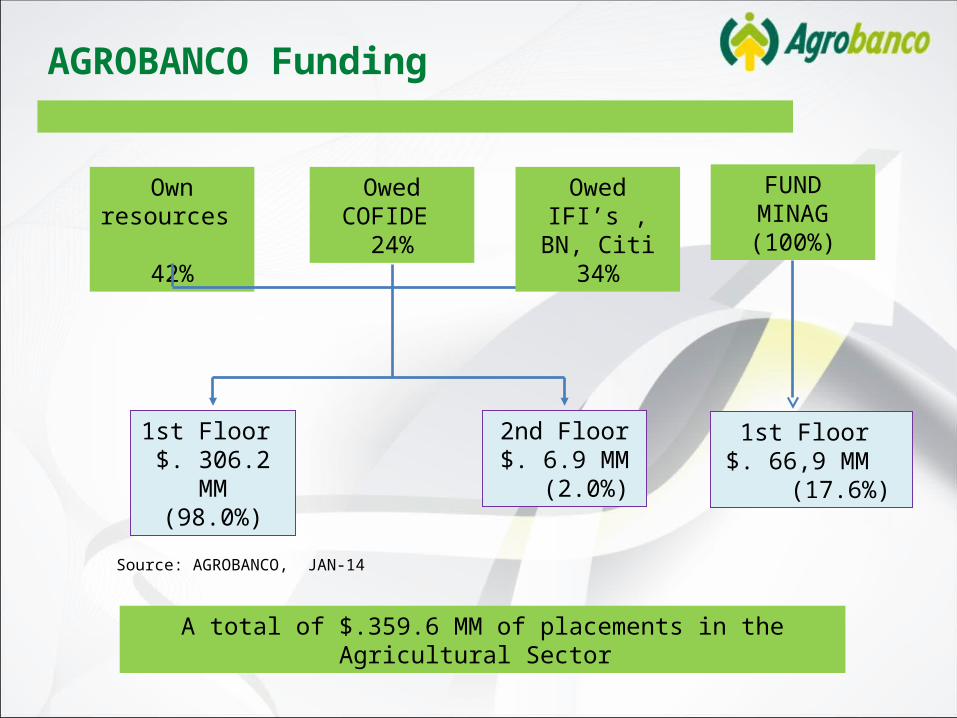

Own resources

42%

OwedCOFIDE

24%

A total of $.359.6 MM of placements in the Agricultural Sector

Source: AGROBANCO, JAN-14

1st Floor $. 306.2 MM

(98.0%)

2nd Floor$. 6.9 MM (2.0%)

OwedIFI’s , BN, Citi

34%

FUNDMINAG(100%)

1st Floor $. 66,9 MM

(17.6%)

AGROBANCO Funding

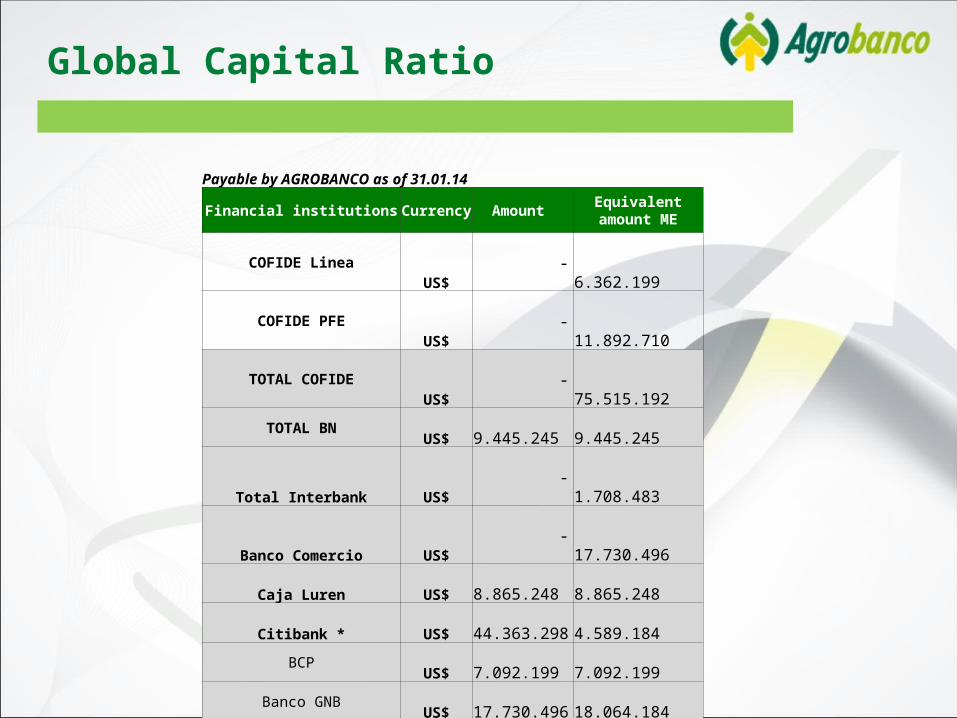

Global Capital Ratio

Payable by AGROBANCO as of 31.01.14

Financial institutions Currency Amount Equivalent amount ME

COFIDE Linea US$ - 6.362.199 COFIDE PFE US$ - 11.892.710

TOTAL COFIDEUS$ - 75.515.192

TOTAL BN US$ 9.445.245 9.445.245 Total Interbank US$ - 1.708.483

Banco Comercio US$ - 17.730.496

Caja Luren US$ 8.865.248 8.865.248 Citibank * US$ 44.363.298 4.589.184

BCP US$ 7.092.199 7.092.199 Banco GNB US$ 17.730.496 18.064.184

TOTAL - 182.450.658

COFIDE 75.515.192

Loans from third parties 106.935.466

Funding 182.450.658

Section ElevenANNEXES

Section ElevenHuman Resources and Business Managers

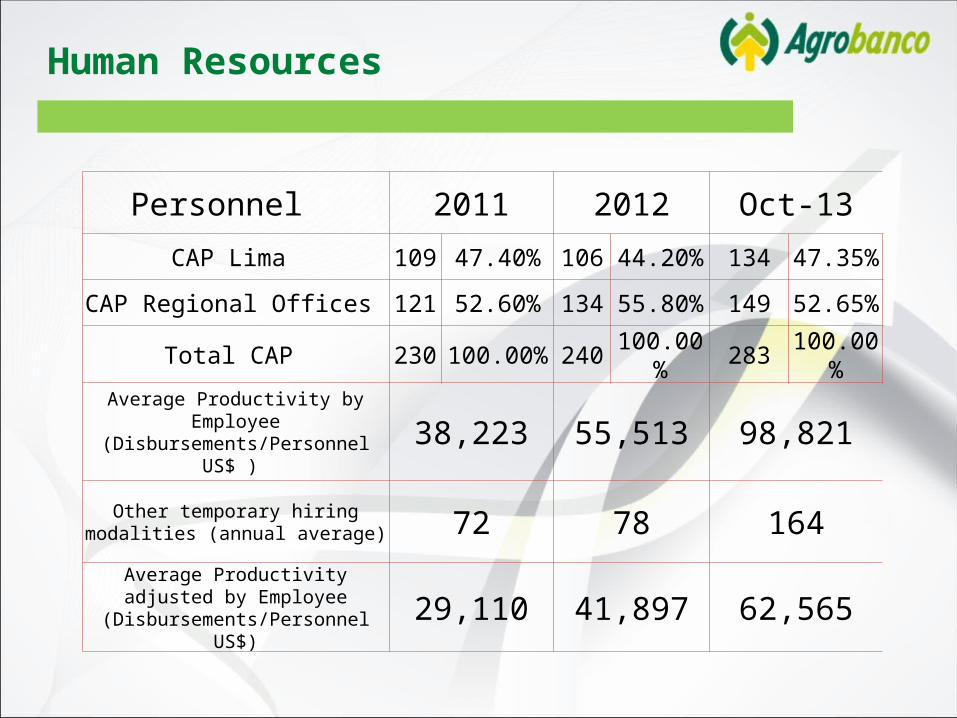

Human Resources

Personnel 2011 2012 Oct-13

CAP Lima 109 47.40% 106 44.20% 134 47.35%

CAP Regional Offices 121 52.60% 134 55.80% 149 52.65%

Total CAP 230 100.00% 240 100.00% 283 100.00%

Average Productivity by Employee (Disbursements/Personnel US$ ) 38,223 55,513 98,821

Other temporary hiring modalities (annual average) 72 78 164

Average Productivity adjusted by Employee (Disbursements/Personnel

US$)29,110 41,897 62,565

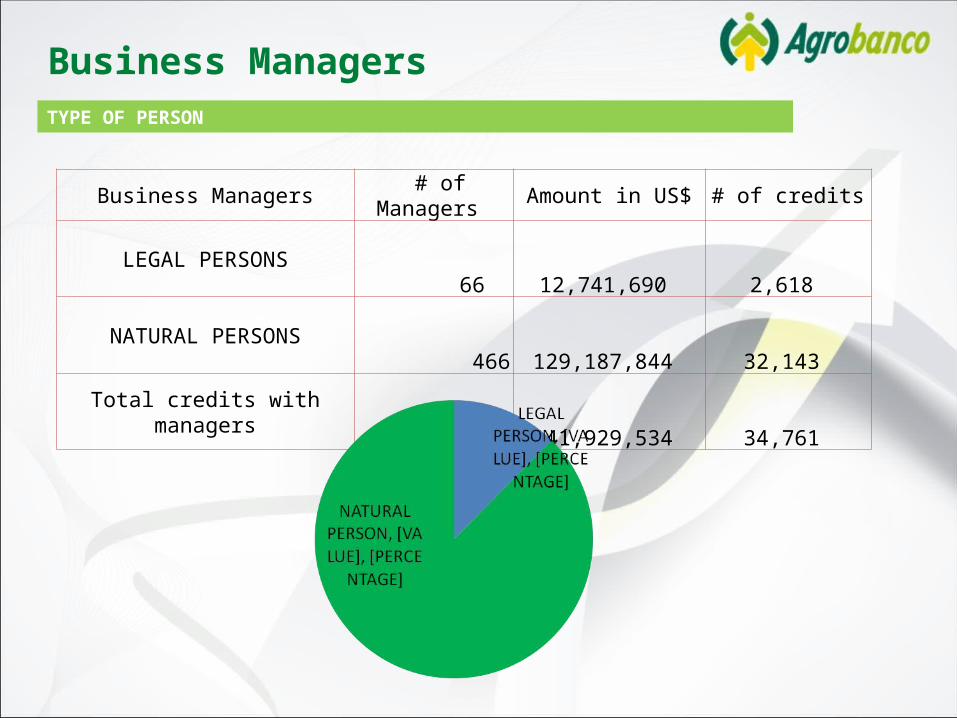

Business Managers # of Managers Amount in US$ # of credits

LEGAL PERSONS 66 12,741,690

2,618

NATURAL PERSONS 466 129,187,844

32,143

Total credits with managers 532 141,929,534

34,761

TYPE OF PERSON

Business Managers

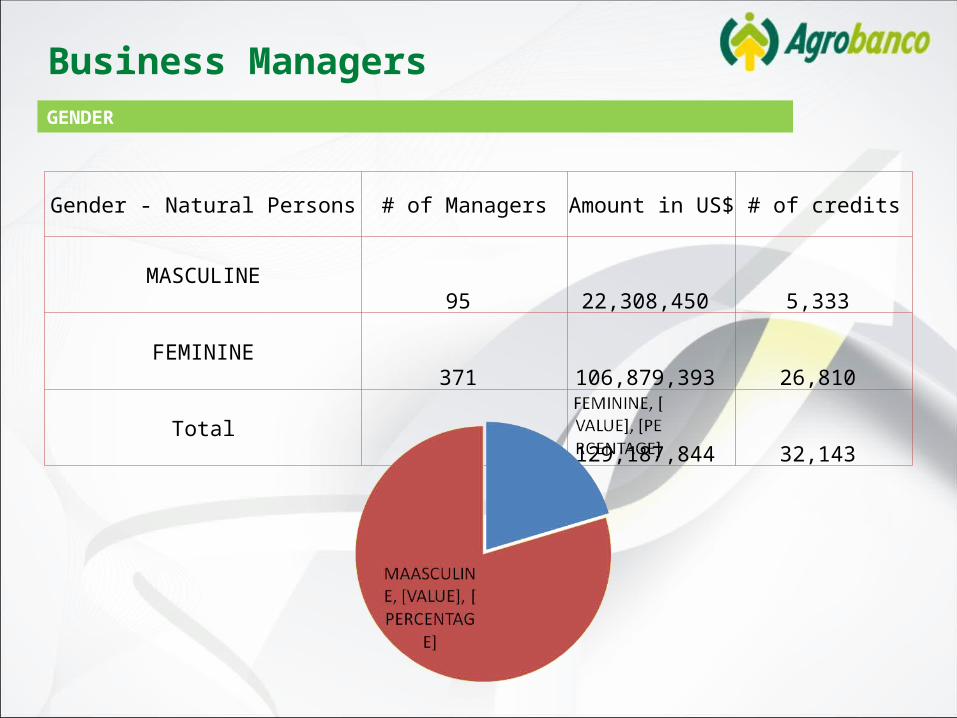

Gender - Natural Persons # of Managers Amount in US$ # of credits

MASCULINE 95 22,308,450 5,333

FEMININE 371 106,879,393 26,810

Total466 129,187,844 32,143

GENDER

Business Managers

Section ElevenOther Services

II International Seminar on Rural Financial ServicesBREAKING PARADIGMS

• Held on November 11• Speakers: Peruvian and international professionals will share their

experience in rural financial services for the agricultural sector.

http://www.agrobanco.com.pe/index.php?id=ii-seminario-internacional&lang=es

Objectives of the Seminar:• Contributing to a better understanding of the rural agricultural sector. • Promoting growth and development of a bank industry for the agricultural

sector. • Placing financial services as factors for social inclusion, growth and

development of the banking industry in the sector.

Statistical Maps

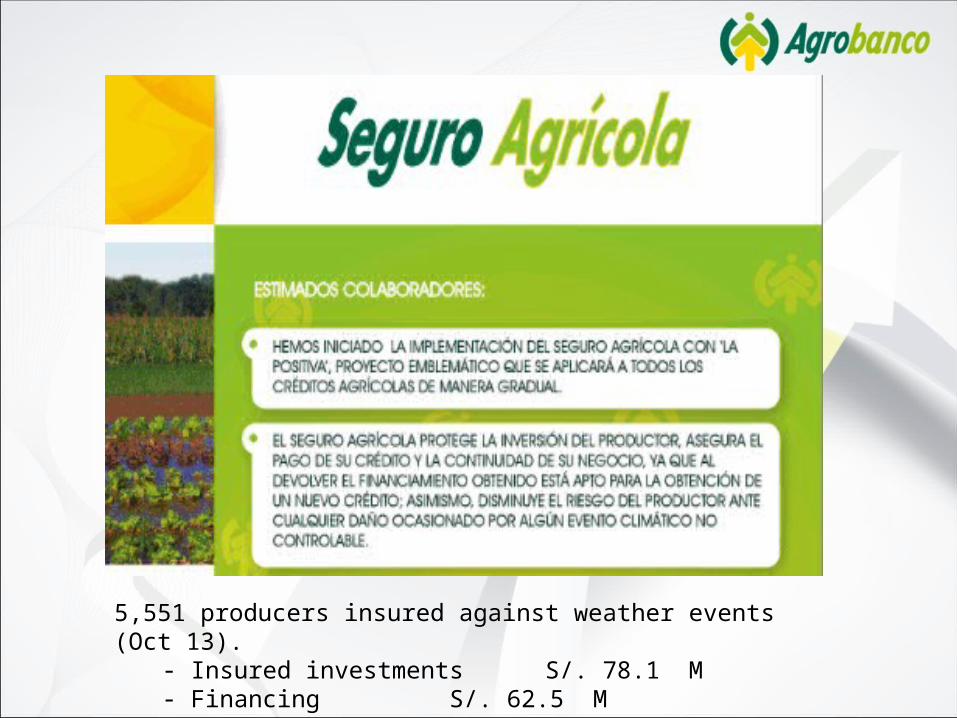

Non-Financial Serv. Platform

5,551 producers insured against weather events (Oct 13).- Insured investments S/. 78.1 M- Financing S/. 62.5 M

Section ElevenOther Variables

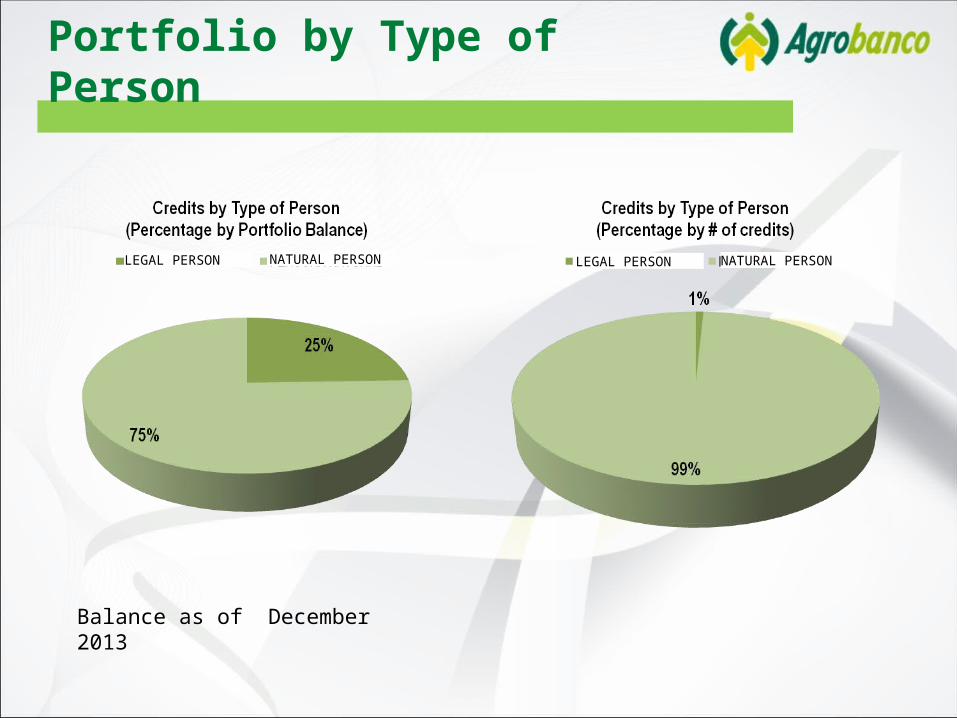

Portfolio by Type of Person

Balance as of December 2013

LEGAL PERSON NATURAL PERSON LEGAL PERSON NATURAL PERSON

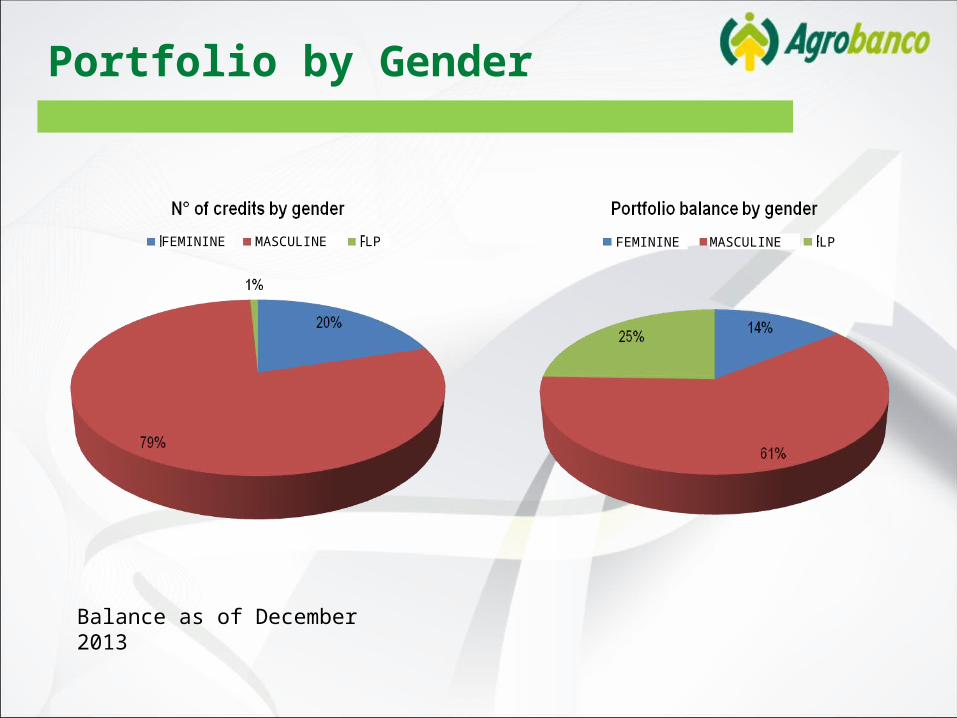

Portfolio by Gender

Balance as of December 2013

FEMININE MASCULINE LP FEMININE MASCULINE LP

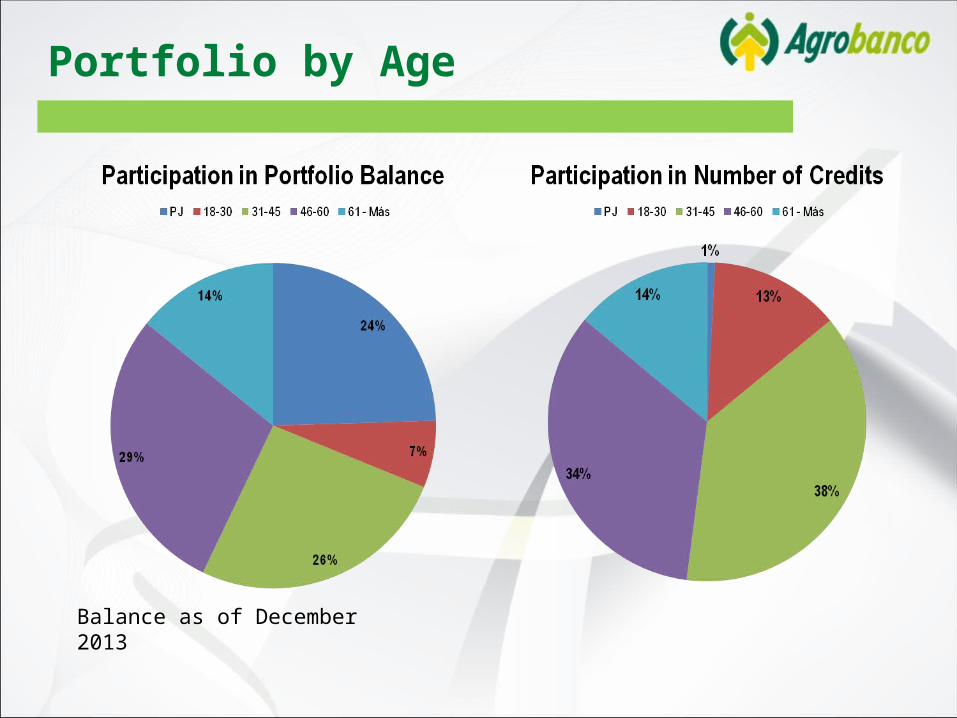

Portfolio by Age

Balance as of December 2013