Embed Size (px)

Citation preview

Home of the South African farmer | Ikhaya lomlimi waseNingizimu Africa | Tuiste van die Suid-Afrikaanse boer | Lehae la balimi ba Africa Borwa

Agri SA’s comments on Eskom’s Regulatory

Clearing Account (RCA) Application

MYPD3 Year 1 (2013/14)

4 February 2016

Thabi Nkosi: Senior Economist- Agri SA

Agri SA is a federation of agricultural organisations comprising of nine provincial

agricultural unions and 24 commodity organisations.

We promote, on behalf of our members:

• development

• profitability

• stability

• sustainability

of agriculture in South Africa by means of our involvement and input on national

and international policy level. Through our affiliations, we represent a diverse group

of farmers irrespective of gender, colour or creed.

Agri SA is also a member of Business Unity South Africa (BUSA) and thus also

engages with other sectors of the economy on matters of transversal importance

such as energy.

Who we are

© 2015 Agri SA 2

1. Context and background

• Impact of the drought on agriculture and South Africa

• Effect on irrigation farmers

2. General comments on Eskom’s submission

• Application of the MYPD methodology

• Economic assumptions

• Reliability of information

• Load shedding

• Power buy-backs and inflation adjustments

3. General recommendations

Content

© 2015 Agri SA 3

Context and background

© 2015 Agri SA 4

• As SA faces possible recession and the agricultural sector has been the worst

performing

• Agricultural production and farm incomes of both small- and large-scale farmers

have been severely affected by drought conditions.

Agricultural sector contracted by :

• 19.7% in Q2 2015

• 12.6% in Q3 2015

A further double digit contraction is expected to be reported in relation to the

last quarter of 2015

SA in the midst of the worst drought in decades

© 2015 Agri SA 5

Maize

• Estimated that 2016/17 maize harvest will amount to approximately 5 million

tons, down from an average annual harvest of 11 million tons

• Loss of revenue by maize farmers of at least R15 billion in 2015/16

Sugar

• Drought-induced revenue losses in the 2015/16 season have been

estimated to reach over R1.1 billion.

Livestock

• Thousands of livestock losses have been

reported, leading to revenue losses that are

yet to be estimated.

Estimated losses for farmers

© 2015 Agri SA 6

© 2015 Agri SA 7

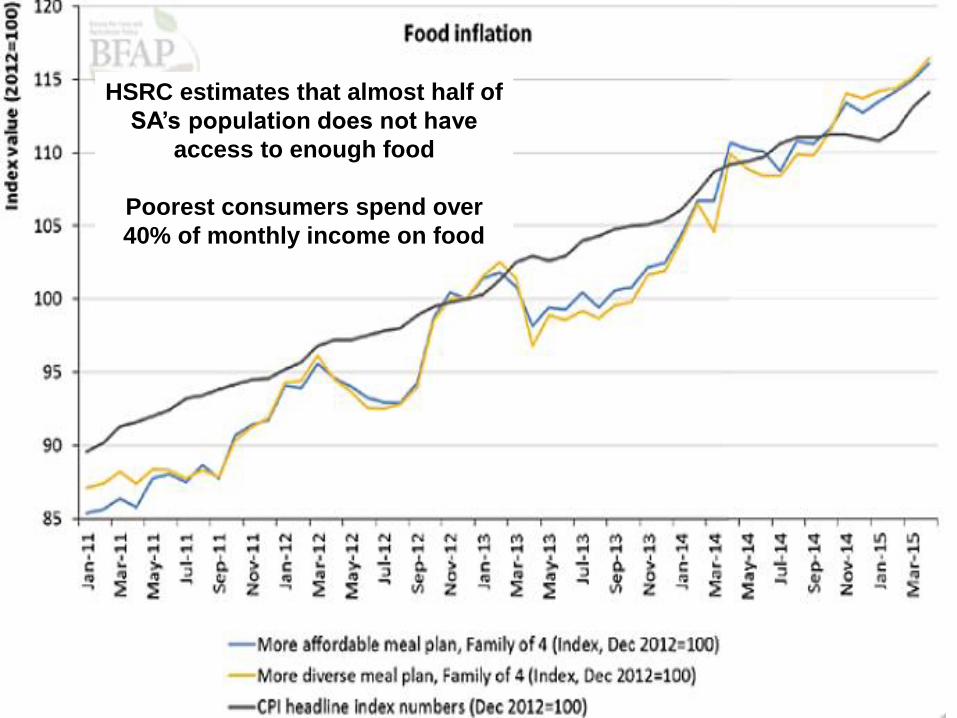

Source: BFAP

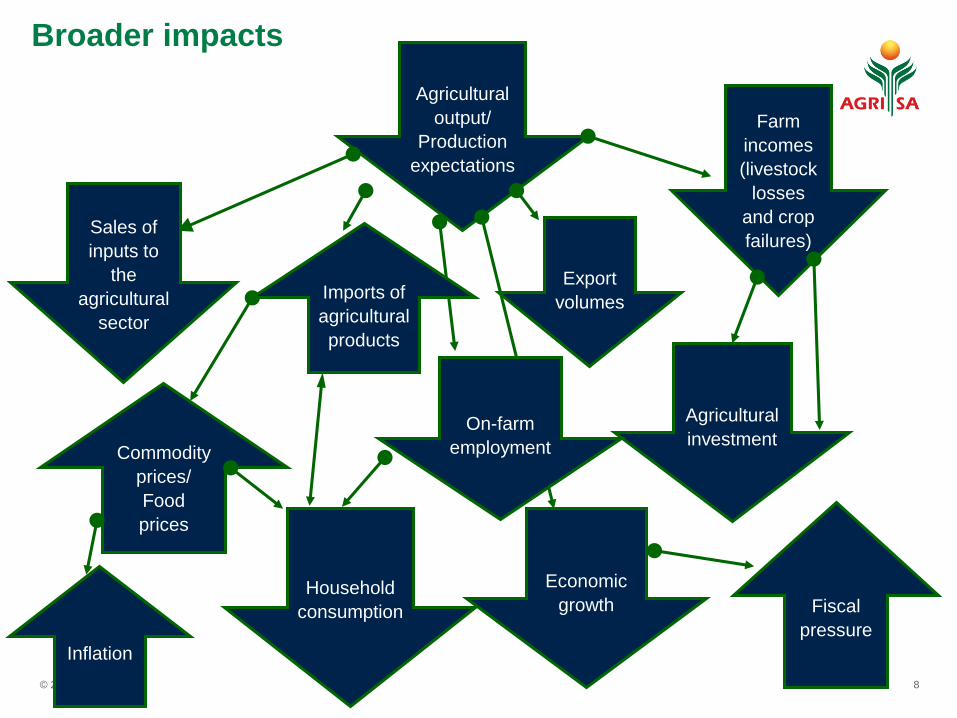

Broader impacts

© 2015 Agri SA 8

Agricultural

output/

Production

expectations

Sales of

inputs to

the

agricultural

sector

Export

volumes

Agricultural

investment

Farm

incomes

(livestock

losses

and crop

failures)

Commodity

prices/

Food

prices

Household

consumption

Economic

growth Fiscal

pressure

Inflation

On-farm

employment

Imports of

agricultural

products

• All farmers are users of electricity to varying degrees and are thus all sensitive to increases

in the price of electricity

Effect on irrigation farmers

© 2015 Agri SA 9

Irrigation farmers most

acutely affected by NERSA’s

RCA decision

17% of South Africa’s

maize production is under irrigation

47% of wheat is produced

on irrigated land

30% of sugar is produced

on irrigated lands

25% of the country’s food

is produced by irrigation-reliant and

energy-intensive industries

10%Contribution of

electricity costs to an average

producer’s total variable cost

Electricity costs constitute the second and fourth largest cost components

in the production of wheat and maize under irrigation respectively.

Undoubtedly, tariff hikes significantly in excess of the 8% communicated in

the original MYPD3 decision will place tremendous liquidity pressure on any

enterprise, especially if electricity constitutes a large proportion of variable

costs as in the case of irrigation-reliant agricultural industries

© 2015 Agri SA 10

© 2015 Agri SA 11

1 300

1 500

1 700

1 900

2 100

2 300

2 500

2 700

2 900

3 100

3 300

3 500

3 700

3 900

4 100

4 300

4 500

4 700

4 900

5 100

5 30015

-Fe

b-1

3

17

-Mar-

13

16

-Apr-

13

16

-May-1

3

15

-Jun

-13

15

-Jul-

13

14

-Aug

-13

13

-Sep

-13

13

-Oct-

13

12

-Nov-1

3

12

-Dec-1

3

11

-Jan

-14

10

-Fe

b-1

4

12

-Mar-

14

11

-Apr-

14

11

-May-1

4

10

-Jun

-14

10

-Jul-

14

9-A

ug-1

4

8-S

ep-1

4

8-O

ct-

14

7-N

ov-1

4

7-D

ec-1

4

6-J

an-1

5

5-F

eb

-15

7-M

ar-

15

6-A

pr-

15

6-M

ay-1

5

5-J

un-1

5

5-J

ul-1

5

4-A

ug-1

5

3-S

ep-1

5

3-O

ct-

15

2-N

ov-1

5

2-D

ec-1

5

1-J

an-1

6

R/ton

Date

PRICES OF USA WHITE MAIZE DELIVERED IN RANDFONTEIN

USA Import Parity

USA Export Parity

Safex WM

© 2015 Agri SA 12

HSRC estimates that almost half of

SA’s population does not have

access to enough food

Poorest consumers spend over

40% of monthly income on food

General comments

© 2015 Agri SA 13

Application of the MYPD methodology

© 2015 Agri SA 14

We acknowledge need for Eskom to maintain a healthy financial position and to advocate for full cost recovery BUT the downstream effects of substantial tariff hikes on sectors cannot be

ignored

We have supported the adoption of the MYPD methodology as a mechanism of bringing certainty and ensuring Eskom’s financial

viability

However, given the fragile state of the country’s key sectors and the economy at large a blind application of the methodology at this stage would be inappropriate and would

exacerbate economic difficulties

We urge NERSA to give greater consideration to the ability of customers to absorb cost increases and to the likely impact that further tariff increases will have on future demand and further revenue

variances which will give rise to further hefty RCA applications

(Vicious cycle)

We agree with Eskom that high electricity prices have unfavourably affected the demand for electricity, contributing to the unfavourable

revenue variance

Further price increases will almost certainly lead to reduced electricity consumption, continuing an unsustainable cycle of under-recovery and

unfavourable revenue variances

NOTE: Unlike the economy at large, the demand for electricity in the agricultural sector is relatively inelastic in the short term despite current efforts

to move to renewable sources of energy.

Economic assumptions

© 2015 Agri SA 15

• We recognise that the economic growth assumptions on which the original MYPD3

decision was based were concluded at a time when the economic outlook was slightly

more positive.

• We are however concerned that it appears that Eskom had missed an opportunity to

update the growth and sales assumptions made in their MYPD3 submission, to reflect

a more realistic view of the future prior to submitting to NERSA.

• The current RCA application indicates on page 42 that the sales forecast was finalised

on 14 September 2011, over a year prior to the submission of the MYPD3 application

to NERSA.

• We recommend that in future, a requirement to update economic assumptions in

line with the latest available information be imposed as far as is feasible to allow

for more realistic outlooks and projections.

• We further recommend that in future MYPD applications, the relationship

between economic growth and electricity sales to the various sectors be

relooked given the trend that most rapid growth has been observed in less

energy intensive sectors.

Reliability of information

© 2015 Agri SA

We are concerned about the number of errors being

reported by Eskom in the application:

• creates confusion

• erodes the confidence of industries in the

submissions made by Eskom and the decisions

taken by NERSA.

1. The first of these errors relates to a failure to add

the environmental levy to the total primary energy

costs in 2013/14.

2. The second error relates to the pricing applicable

to NPA customers and ultimately the allowed

revenue in the original MYPD3 decision.

Given the avoidable nature of these errors made

by either the regulator or Eskom, they should not

be laid at the doorstep of the consumer and thus

request that any contribution of such errors to the

RCA variance be disregarded 16

Load shedding

© 2015 Agri SA 17

• We are concerned with the manner in

which Eskom has accounted for load-

shedding in the RCA application

• Of the view that the information

provided is inadequate and does not

allow for informed comment.

• Concerned that this type of reporting,

caused by a lack of data collection,

sets an unfavourable precedent for

future RCA applications particularly

given the significance of load

shedding in 2014/15 and 2015/16.

Power buy backs

• Concerning to us that an unfavourable variance as a result of Power Buy Backs

has been included as part of the RCA application given that the resultant

decrease in sales was initiated and incentivised by Eskom.

• It is our view that the contribution of the PBB scheme to the reported variance be

disregarded.

Inflation Adjustment

• It is our understanding that over-expenditure on operating costs cannot be

included in an RCA application.

• For the purposes of the application, it would thus also be inappropriate to apply

an inflation adjustment on the operating cost over-expenditure of R10 billion.

• From Eskom’s submission, it is not clear whether inflation adjustments on this

over-expenditure were excluded.

Power Buy Backs and inflation adjustment

© 2015 Agri SA 18

General

recommendations

© 2015 Agri SA 19

Recommendations

20

Essentially, Eskom is a state-owned

utility and a supplier of a critical input

in the South African economy. Given

the impact of the organisation’s

operations on the cost of doing

business in South Africa, greater

transparency is required regarding

the methodologies applied to

calculate costs and determine

efficiency and prudency of

expenditure.

• Given the current fragile position of the South

African economy, consideration should be

given to recovering the approved RCA

balance over an extended period of time, as

allowable in the MYPD methodology.

• If the full RCA balance of R22.8 billion as

requested by Eskom were to be recovered in

the current period, an increase of

approximately 16% to the tariff may be likely.

• This would be destructive to the economy and

the agricultural sector in particular. It is

recognised that the EBITDA and EBIT ratios

are at such low levels that they may be

negatively considered by rating agencies. A

rigid phasing-in schedule for RCA should

however contribute towards alleviating this

position.

Thank you

© 2015 Agri SA 21