Embed Size (px)

Citation preview

August 2002

Advancing wealth management capability, reach and scale

Disclaimer

The material contained in the following presentation is intended to be general background information on Westpac Banking Corporation and its activities as at 26 August 2002.

The information is supplied in summary form and is therefore not necessarily complete. Also, it is not intended that it be relied upon as advice to investors or potential investors, who should consider seeking independent professional advice depending upon their specific investment objectives, financial situation or particular needs.

2.

Agenda

David MorganØ Strategic rationale Ø Deal summary

David ClarkeØ Combined strengths Ø Business model & integration

Rob CoombeØ The BT business

Philip ChronicanØ Financial impact

3.

Strategy

Broaden customer relationships

Improve wealth management position

Drive operational efficiency

Embed a high performance culture

Build corporate reputation

4.

Enhancing our growth trajectory

• Changing our business mix

• Without compromising returns

• Rothschild acquisition• Hastings acquisition

• AGC Sale

Invest in growth Manage for growth

5.

Corporate Super

Life

New Zealand Wrap

Margin Lending

Retail

Select investment management capabilities

BT brand

BT Acquisition

• Consideration $900 million

• Cash EPS positive by end 2004

6.

A new wealth management force

• Platform capabilitiesØ Best-in-class wrap platformØ Leading corporate superannuation platform

• Enhanced distribution reachØ Product relationships with 15,000 EFAsØ Platform relationships with 2,000 EFAs

• Critical mass and scale efficienciesØ 4th largest retail fund managerØ 2nd largest wrap/master trust providerØ Margin lending market share from 6% to 17%Ø 6th largest corporate super provider

7.

Rounding out our franchise –market share

Sourcesa. Reported customer numbers b. KPMG FIPS NZ 2002, AC Nielson, Greenwichc. Greenwich Associatesd. Corporate transactional business – Greenwich Associatese. Greenwich large corporate banking survey (9/01)f. Retail funds under management ASSIRT June 2002g. Melville Jessup Weaver, Investment Survey, March 2002

9g5fWealth management (before)

5g4fWealth management (after)

2e1dCorporate banking

2b2cBusiness banking

1b2aConsumer banking

New ZealandAustralia

8.

Consistent with disciplined acquisition criteria

Strategically aligned

Shareholder value accretive

Not unduly diverting

P

P

P

9.

Realigned executive team

David MorganChief Executive Officer

David ClarkeWealth Management

Phil CoffeyInstitutional Bank

Michael CoomerBusiness & Technology

Solutions & Service

Philip ChronicanChief Financial Officer

Ann SherryPeople & Performance

Mike PrattBusiness & Consumer Banking

10.

Agenda

David MorganØ Strategic rationale Ø Deal summary

David ClarkeØ Combined strengths Ø Business model & integration

Rob CoombeØ The BT business

Philip ChronicanØ Financial impact

12.

BT Financial Group overview

Strategic position• 450,000 Australian and New Zealand investors

• Strong brand and relationships but weathered some damage

• 1,300 experienced employees

$6.5bnFunds under wrap administration

$1.0 bnMargin lending

$1.2bnCorporate super

$11.4bnRetail funds under management

+ 2,000Wrap advisors

+15,000External financial advisors

Market position

13.

Increased scale – retail FUM

Source: ASSIRT, Market Share Report, June Quarter 2002

17

11 11 107

48

3429 28

22

05

101520253035404550

CBA / Colo

nial

Nation

al / M

LC AMP

Westpa

c/BT ING

Westpa

c

Macqu

arie BT

AXA

Perpe

tual

$ bi

llion

68% increase in retail funds under management

14.

Increased scale – wrap/master trust

Source: Plan for Life, March Quarter 2002Notes: NAB/MLC includes FUM in Masterkey balanced FUM

BT includes BT Wrap + retail super products classified as master trusts.

10 97

53

1010

1417

28

0

5

10

15

20

25

30

Nation

al / M

LC

Wes

tpac /

BT CBA

AMP BT

St Geo

rge

Norwich

Union

Westpa

c INGAXA

$ b

illio

nFrom 7th to 2nd in master trust/wrap funds under administration

15.

New Zealand – increased FUM

Source: Melville Jessup Weaver, Investment Survey, March 2002

3.83.1

2.3 2.3 1.9

4.24.24.35.7

10.3

0

2

4

6

8

10

12

AMP INGRSA

Tower

Westpa

cTru

st / B

T

CBA / Sov

ereign AXA

BNZ BT

Westpa

cTru

st

$ N

Z b

illio

n

Doubled funds under management to 5th largest player

16.

End to end capabilities

•JP Morgan relationship

•Service Centre

•Scale

•Growth style

•Ext ratings

•Extensive range

•Online platform access

•Wrap

•Corporate super

•15,000 EFA relationships

•2,000 EFA’son wrap

•Additional 450,000 customers

•RBC relationship

•Value style

•Ext ratings

•International alliances

•Development & execution excellence

•1,000 Premier planners

•Servicing platform

•80,000 customers

•Internal service centre

•True to label

•Core style

•Solid product range

•Structured investments

•Master trust

•Individually managed accounts

•700 internal planners & advisors

•7.4 million customers

•CRM capabilityW

estp

acR

oth

sch

ildB

T

Customers Distribution & Advice

BundlingPlatform

ProductManufacture

InvestmentManagement

BackOffice

17.

Wealth management structure

Rothschild Westpac Fin Services

BT Financial GroupSagitta

Asset Accumulation

InvestmentManagement Life New

Zealand

Integration

18.

Customers

Business Model

Westpac FP&A

External Advisers

&Distributors

Business Advisers

Distribution & Advice

BundlingPlatform

ProductManufacture

InvestmentManagement

Westpac Customers

EFA Customers

Business Customers

PP

S M

aster T

rust

Dealer M

aster T

rusts

“Wrap

” Platfo

rm

Corp Super

Su

per

Pen

sion

Investm

ent

Risk

Clien

t Services an

d A

dm

inistratio

n

Putnam

BlackRock

AEW

TAA

Value

Core

Growth

Back O

ffice

Margin Lending

Principal

Grosvenor

BackOffice

19.

Integration plans The current integration of Rothschild/Westpac Financial Services

will continue and then be merged with the BT integrationR

oth

sch

ild

Stage 1 - Priority

•Merge investment mgt, margin lending, Group Services

•Wrap/corporate super to bank channels

•Stabilise funds managementBT

Fin

anci

al

Stage 2 - Continuing

•Finalise structure & resourcing

•Single ‘on-sale’ product set

•Quick wins

Stage 1 - Completed

•Merge investment mgt

•Executive team in place

•Sagitta brand launched

Stage 2

• Integrate distribution models •Single ‘on-sale’ product set •Consolidate admin services

Westpac Financial Services

20.

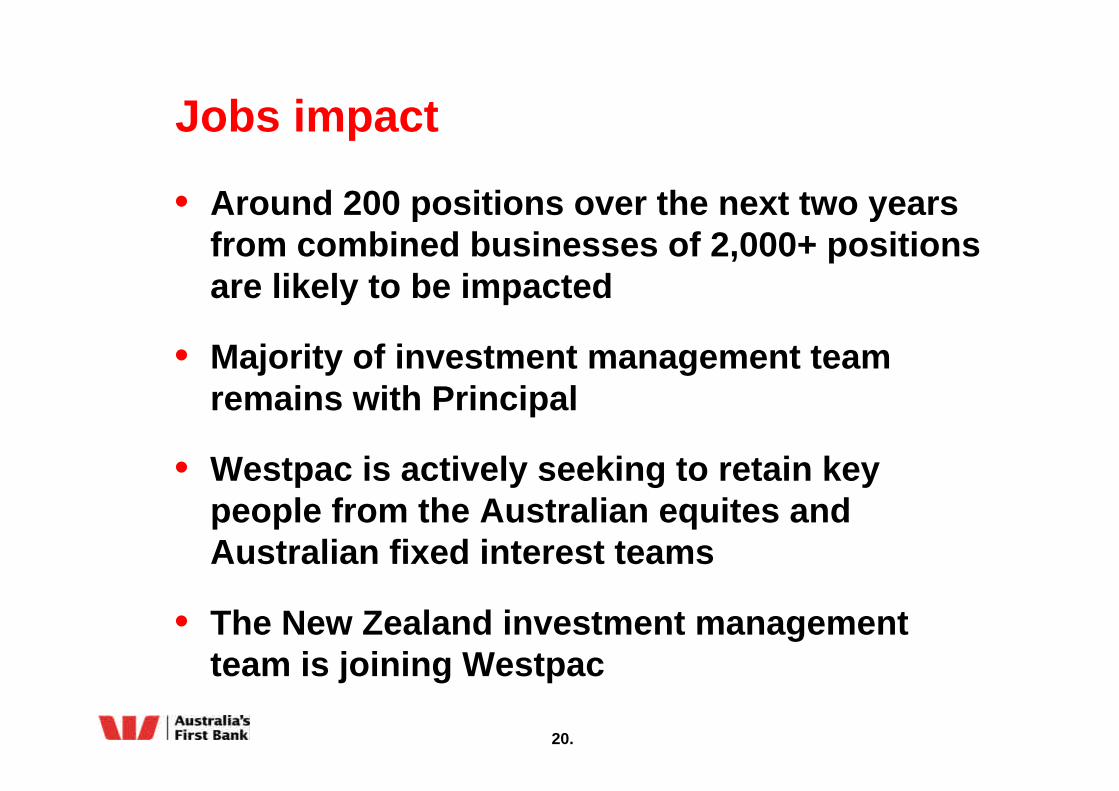

Jobs impact

• Around 200 positions over the next two years from combined businesses of 2,000+ positions are likely to be impacted

• Majority of investment management team remains with Principal

• Westpac is actively seeking to retain key people from the Australian equites and Australian fixed interest teams

• The New Zealand investment management team is joining Westpac

21.

The international equities management transition

Current BT team, process and philosophy to continue

Additional processes and controls including Principal US oversight

Key business continuity plans in place

22.

Agenda

David MorganØ Strategic rationale Ø Deal summary

David ClarkeØ Combined strengths Ø Business model & integration

Rob CoombeØ The BT business

Philip ChronicanØ Financial impact

23.

BT Financial Group

$6.5bnFunds under wrap administration

$1.0bnMargin lending

$1.2bnCorporate super

$11.4bnRetail funds under management

+ 2,000Wrap advisors

+15,000External financial advisors

Market position

24.

2001 ASSIRT survey results

Ù

Ù

Ù

Ù

Ù

Ù

Overall marketing support

Overall administration support

Ease of doing business with the firm

Effectiveness of communication

Overall technical services

Quality of asset management

IndustryAverage

Low High

Ù Position of BT on survey scale

25.

Retail funds – decline in FUM over past 18 months

•Outsource international equities

•Researcher perception of international equities

•Broaden product range & move to open architecture

•Poor absolute performance

•Out of favour growth style

SolutionIssue

26.

Top1 seven wrap badges

1. Top 7 Badges by funds under administration and approximate number of registered advisers

200Associated Planners

90Investor Group

120The Money Managers

20Investar Portfolio Management

35Tynan Mackenzie

600Zurich

750Count Financial Limited

Approx No. of registered advisers

Badge

27.

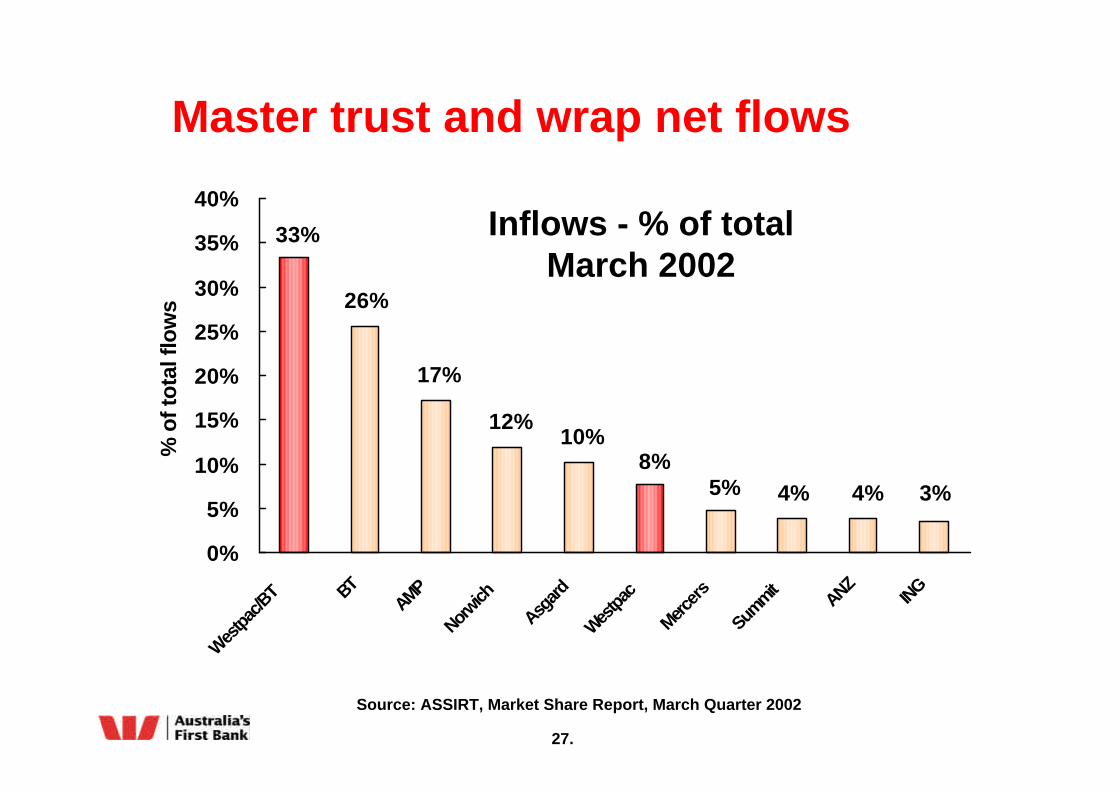

Master trust and wrap net flows

Source: ASSIRT, Market Share Report, March Quarter 2002

3%4%4%5%8%

33%

26%

17%

12%10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Wes

tpac/B

T BTAMP

Norwich

Asgard

Westpa

c

Mercers

Summit

ANZING

% o

f tot

al fl

ows

Inflows - % of totalMarch 2002

28.

Corporate Super - BT Lifetime Super – Employer Plan

• Recognised as a leading productØ “Without doubt, one of the two best products

for the up to $50m market”Warren Chant – Chant West Financial Services – Aug 2002

Ø Top rated product by Ausuper

• Scaleable administration

• Dedicated sales, service, education and technology

• Full featured plans

30.

Agenda

David MorganØ Strategic rationale Ø Deal summary

David ClarkeØ Combined strengths Ø Business model & integration

Rob CoombeØ The BT business

Philip ChronicanØ Financial impact

31.

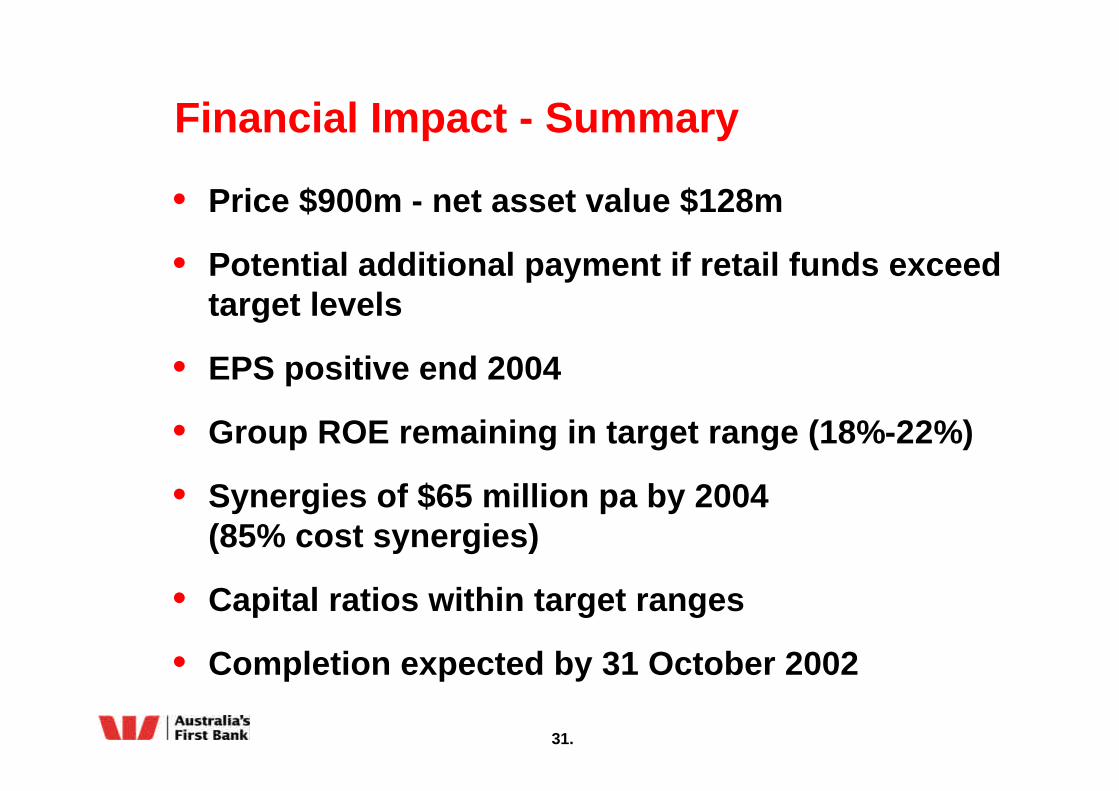

Financial Impact - Summary

• Price $900m - net asset value $128m

• Potential additional payment if retail funds exceed target levels

• EPS positive end 2004

• Group ROE remaining in target range (18%-22%)

• Synergies of $65 million pa by 2004 (85% cost synergies)

• Capital ratios within target ranges

• Completion expected by 31 October 2002

32.

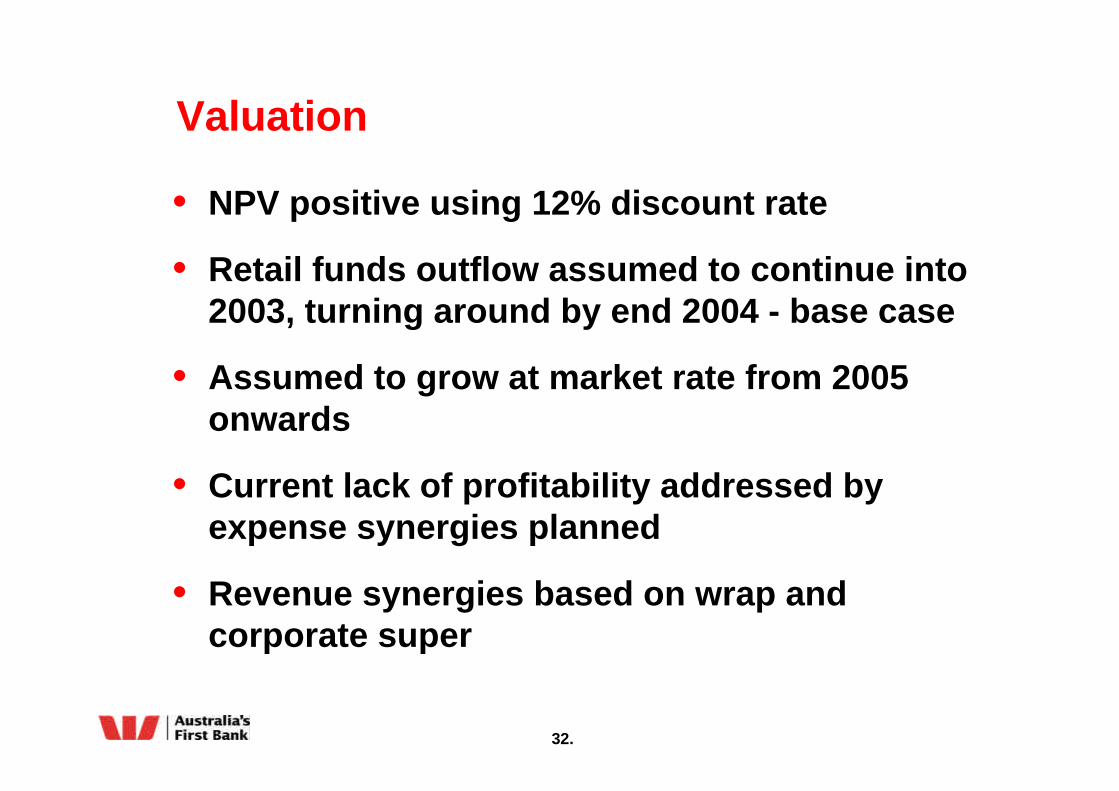

Valuation

• NPV positive using 12% discount rate

• Retail funds outflow assumed to continue into 2003, turning around by end 2004 - base case

• Assumed to grow at market rate from 2005 onwards

• Current lack of profitability addressed by expense synergies planned

• Revenue synergies based on wrap and corporate super

33.

Valuation

36%

15%

1%

16%

4%

SynergiesAllocated

64%

5%

4%

25%

30%

Standalone

34%Portfolio services–Wrap & Corp Super

Total

Total

100%

20%

5%

41%

Margin lending and other

New Zealand

Retail product and distribution

• Valuation above price sees all revenue benefits and 25% of cost synergies retained

• Synergies allow for $100m of integration and transition expenses

34.

• Merge client services and administration

• Rationalise systems

• Merge product sets

• Integrate group services

Ongoing synergies $65 million pa to be achieved by end 2004

Cost Synergies and revenue benefits

• Wrap service across Westpac FP&A network

• Corporate super to Westpac business customers

• Increased sales through broader distribution footprint

Cost synergies Revenue benefits

85% 15%

35.

Potential additional payment

• Deferred contingent payment of up to $150 million

• Contingent on achieving above target retail funds under management by Dec 2004

• If trigger reached, further value accrues to both Westpac and Principal equally up to level of cap

36.

Projected financial outcomes

0.5%0.3%(0.3)%(1.0)%Cash EPS accretion/dilution

197(11)(18)Incremental cash earnings

45454545Funding cost2

64523427Additional earnings1,3

2006200520042003$ million

• Group ROE remains in target range 18% - 22%

1. BT net profit plus cost synergies and revenue benefits2. $900 million @ 7% pre tax3. Assumed integration costs expensed in 2002

37.

Funding plan

• Capital resources sufficient to fund internally

• Current buy-back not to be re-activated

• Continue to maintain capital ratios in target ranges

• Investigate opportunities to optimise capital mix:Ø Hybrid equityØ Other capital management initiatives Ø Outcomes will be presented at full year earnings

announcement

38.

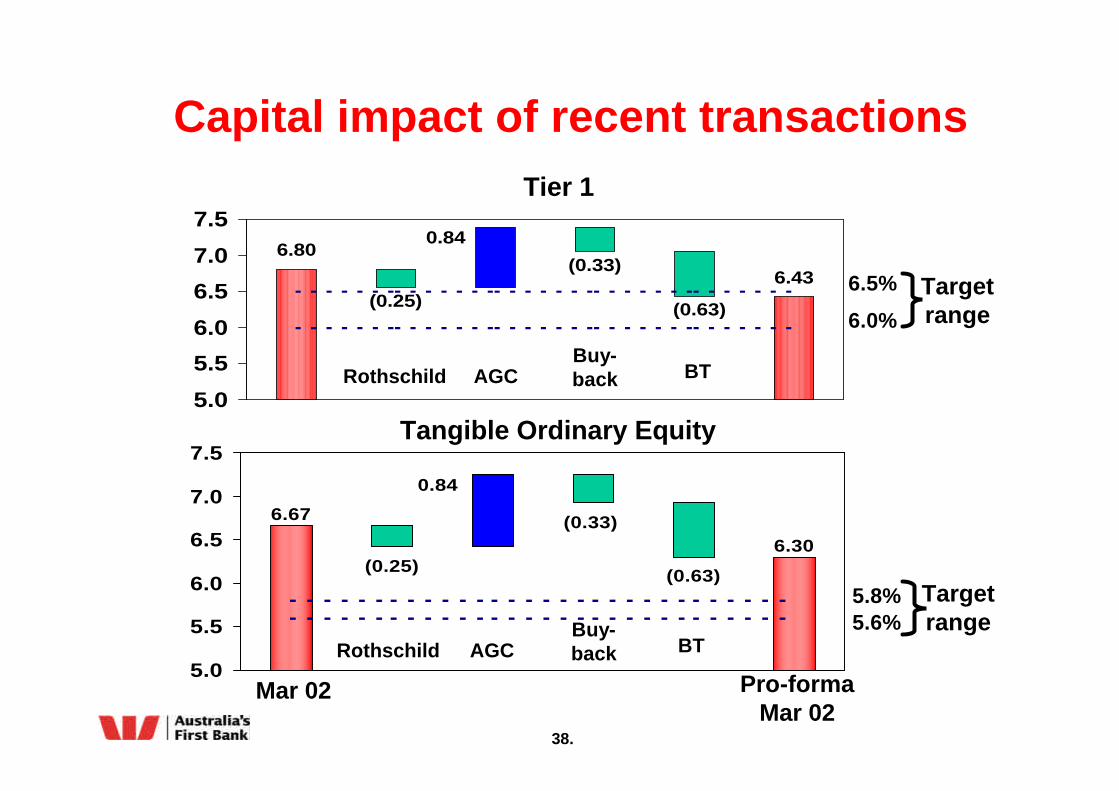

6.30

6.67

(0.25)

0.84

(0.33)

(0.63)

5.0

5.5

6.0

6.5

7.0

7.5

6.43

6.80

(0.63)

(0.33)

0.84

(0.25)

5.0

5.5

6.0

6.5

7.0

7.5Tier 1

Tangible Ordinary Equity

Mar 02 Pro-formaMar 02

Rothschild AGCBuy-back

6.5%

6.0%

5.8%5.6%

Targetrange

Targetrange

Capital impact of recent transactions

BT

Rothschild AGCBuy-back BT

39.

Accounting treatment • Different valuation basis for wealth

management operations

Ø Rothschild planned to be carried at purchase price in the life company

Ø Embedded value used for revenue recognition in part of Westpac’s existing businesses

• BT acquisition further complicates treatment

• Undertaking a comprehensive analysis of wealth management structure

Ø Trade-off income volatility and goodwill perspectives

Ø Prefer common accounting treatment for all wealth management businesses

40.

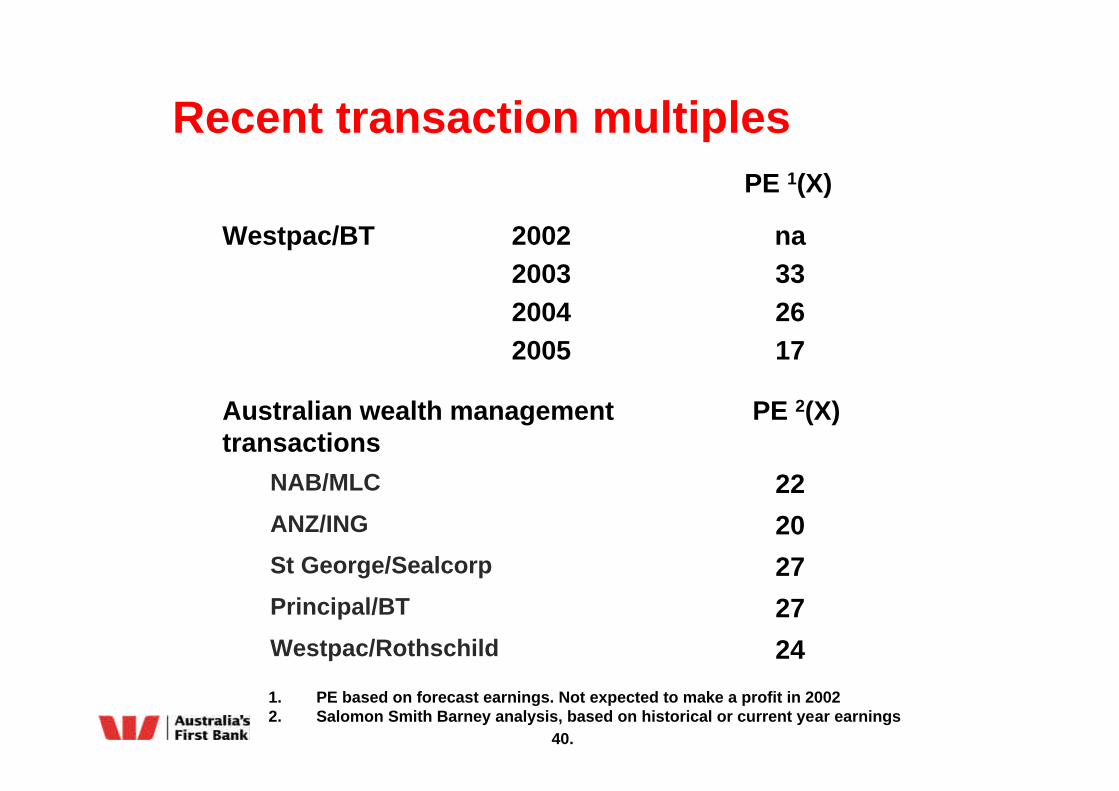

Recent transaction multiples

1. PE based on forecast earnings. Not expected to make a profit in 20022. Salomon Smith Barney analysis, based on historical or current year earnings

24Westpac/Rothschild

27Principal/BT

27St George/Sealcorp

20ANZ/ING

22NAB/MLC

Australian wealth management PE 2(X)transactions

na332617

Westpac/BT 2002200320042005

PE 1(X)

41.

Recent transaction multiples

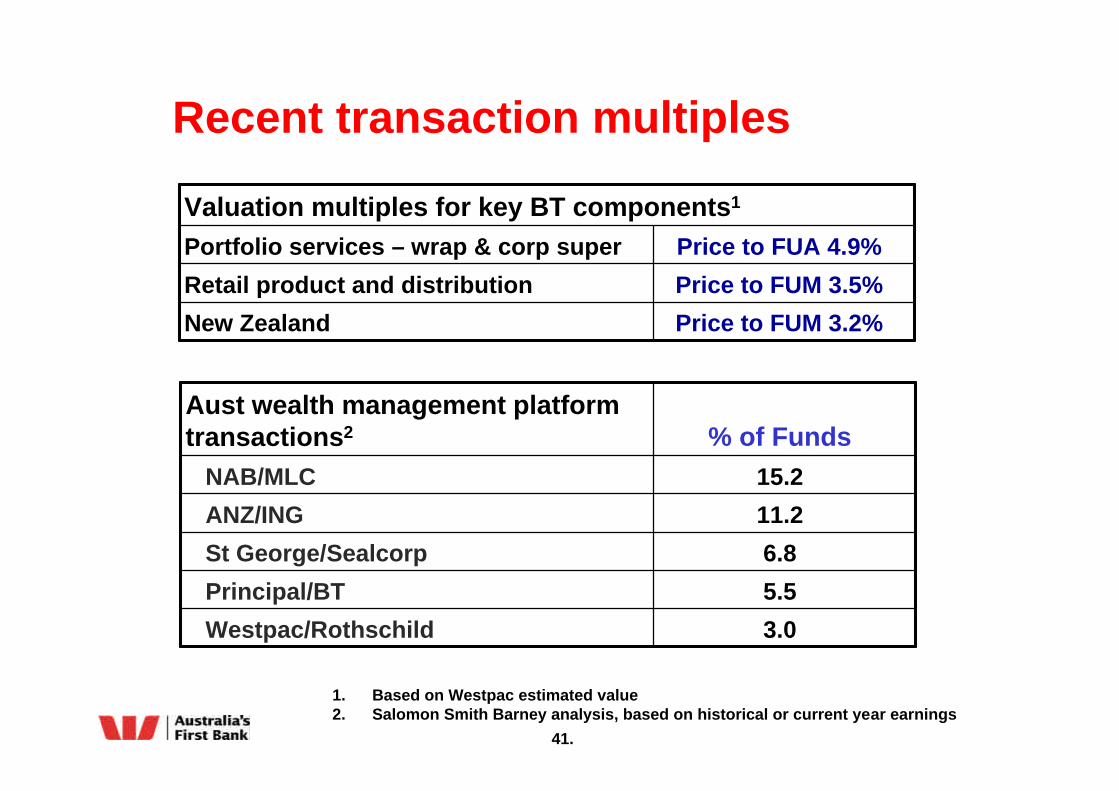

1. Based on Westpac estimated value 2. Salomon Smith Barney analysis, based on historical or current year earnings

% of FundsAust wealth management platform transactions2

3.0Westpac/Rothschild

5.5Principal/BT

6.8St George/Sealcorp

11.2ANZ/ING

15.2NAB/MLC

Price to FUA 4.9%Portfolio services – wrap & corp super

Valuation multiples for key BT components1

Price to FUM 3.2%

Price to FUM 3.5%

New Zealand

Retail product and distribution

42.

Gaining the scale, capability and reach in wealth management

Inside valuation criteria

Maintain strong financial position

Enhanced medium term growth prospects

44.

45.

Pro-forma P&L – Wealth ManagementProforma Profit & Loss Statement for Combined Wealth Management Businesses

WFS RAAM BT BT Synergies

2002 2002 2003 2003

$m

Operating income 395 120 255 3Expenses (168) (96) (262) 43Underlying profit 227 24 (7) 46Bad debts - - - - NPBT 227 24 (7) 46Tax expense (43) (6) 2 (14)NPAT 184 18 (5) 32

Note 1 Note 2 Note 3 Note 4

Note 1: WFS based on September 2002 full year forecast. Income includes $53m EV uplift (pre-tax)

Note 2: RAAM based on September 2002 full year forecast extrapolated for a full year ownership

Note 3: BT based on the acquired businesses for full year 2003

Note 4: Synergies as identified in BT acquisition valuation