Embed Size (px)

Citation preview

Advanced Taxation Republic of Ireland

Sample Paper 1

Questions & Suggested Solutions

Page 2 of 32

Sample Paper 1

NOTES TO USERS ABOUT SAMPLE PAPERS

Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance

to students and their teachers regarding the style and type of question, and their suggested solutions, in

our examinations. They are not intended to provide an exhaustive list of all possible questions that may

be asked and both students and teachers alike are reminded to consult our published syllabus (see

www.AccountingTechniciansIreland.ie) for a comprehensive list of examinable topics.

There are often many possible approaches to the solution of questions in professional examinations. It

should not be assumed that the approach adopted in these solutions is the only correct approach,

particularly with discursive answers. Alternative answers will be marked on their own merits.

This publication is copyright 2016 and may not be reproduced without permission of Accounting

Technicians Ireland.

© Accounting Technicians Ireland, 2061.

Page 3 of 32

Sample Paper 1

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY

SECTION A

Answer Question 1, 2, 3 in this section. ALL QUESTIONS ARE

COMPULSORY

SECTION B

Answer any TWO of the four questions in this section

Page 4 of 32

Sample Paper 1

SECTION A

Answer Question 1, 2, 3 in this section. All questions are compulsory.

QUESTION 1 Compulsory

David and Susan Brady have been married for ten years. They have opted for joint assessment and David

is the assessable person.

David runs his own legal practice; he set this up many years ago. His tax adjusted profits before capital

allowances for the last two years were as follows:-

Year ended 30th

June 2016 € 90,000.

Year ended 30th

June 2017 €100,000.

His capital allowances are:-

2015 ........................ €6,000

2016 ........................ €8,000

David is 44 years of age and has decided to set up a retirement annuity in 2016. He paid his first premium

of €10,000 in May 2016.

He inherited a warehouse from his father in September 2016. He let it out on a ten year on lease on 1st

November 2016 at a yearly rental income of €24,000 and a premium of €40,000.

His only other income was deposit interest from the Allied Irish Bank. He opened the account in May

2016. He received interest of €2,360 net of D.I.R.T.

Susan stays at home to look after their three children. She has a part time job and earns €5,000 in 2016.

P.A.Y.E deducted was €950. She also received a dividend of €2,560 from an Irish company in November

2016. David and Susan have the following outgoings in 2016.

1. College fees for Susan for an approved part time course €2,200.

2. David paid permanent health insurance of €850.

Page 5 of 32

Sample Paper 1

QUESTION 1 (Cont’d)

Requirement

(i) Calculate David and Susan’s Income tax liability for 2016.

15 Marks (ii) Calculate David’s PRSI, and Universal Social Charge for 2016. 3 Marks

(iii) What is the payment date for David’s preliminary tax for 2016? 1 Mark

(iv) What is the filing date for David’s Form II for 2016? 1 Mark

Total 20 Marks

Page 6 of 32

Sample Paper 1

QUESTION 2 Compulsory

Blayney Limited is an Irish resident company. It is not a close company. Its year end is the 30th

September each year. The profit and loss account for the year ended 30th

September 2016 is set out

below:-

Notes € €

Sales .................................................................. 1,200,000

Cost of Sales ...................................................... 680,550

Gross Profit........................................................ 519,450

Other Income ..................................................... 1 120,000

Less: Expenses

Wages & Salaries .............................................. 280,480

Directors remuneration ..................................... 80,000

Depreciation ..................................................... 10,510

Legal Fees.......................................................... 2 6,500

Bad Debts .......................................................... 3 3,800

Entertainment .................................................... 4 5,000

Motor Expenses and Lease Rental ..................... 5 17,400

Audit Fee ........................................................... 3,625

Insurance ........................................................... 4,150

Interest on Late Payment of Corporation Tax1,510

Telephone, Light, Heat ...................................... 6,500 419,475

Net Profit .......................................................... 219,975

NOTES

(1) Other Income €

Bank interest received gross ................ 10,000

Gain on sale of warehouse ....... 90,500

Irish dividends received 19,500

............................................................. 120,000

The company sold the warehouse in May 2016 for €350,000. Legal fees on disposal were €3,800. The

company purchased this warehouse in March 1998 for €255,700.

(2) Legal Fees €

Parking fines ........................................ 450

Defending title to stock........................ 1,200

Disposal of warehouse ......................... 3,800

Recovery of Bad Debts ........................ 1,050

............................................................. 6,500

Page 7 of 32

Sample Paper 1

QUESTION 2 (Cont’d)

(3) The bad debts account is as follows:-

€

Increase in general provision 800

Increase in specific provision 1,100

Bad debts written off 2,550

Bad debts recovered (650)

3,800

(4) The entertainment expenses include €1,580 for the staff Christmas party. The balance was

incurred entertaining customers and potential customers.

(5) Motor Expenses and Lease rental

Vehicle Cost/List Price

Emissions

Running

Expenses €

Lease Rental

€

Van €26,000 130g/km 3,800 -

Car for Managing

Director €32,000 175g/km 4,100 5,100

Car for Sales

Director €27,500 135g/km 4,400 -

12,300 5,100

All vehicles were acquired in August 2015.

(6) Trading Loss

The company has an allowable trading loss of €10,000 brought forward from 30th

September 2015.

(7) Fixed Assets

Machinery Car Van

€ € €

TWDV – 1/10/2015 12,750 21,000 22,750

The machine was purchased in August 2014 for €18,000. A grant of €1,000 was received.

Page 8 of 32

Sample Paper 1

QUESTION 2 (Cont’d)

Requirement:

In respect of the accounting period ended 30th

September 2016 for Blayney Limited:-

(i) Prepare the adjusted Case I trading profits before capital allowances.

10 Marks

(ii) Prepare the capital allowances computation. Show the tax written down value at 30th

September

2016.

4 Marks

(iii) Prepare the corporation tax liability computation. Show clearly the appropriate schedule each

category of income is assessed under and show the amount for ‘Total Income’ and ‘Total

Profits’ as calculated for corporation tax purposes.

6 Marks

Total 20 Marks

Page 9 of 32

Sample Paper 1

QUESTION 3 Compulsory

Note this question has two parts. Both parts must be answered

Part A

(a) State the factors which a trader should take into account in deciding whether to register for V.A.T.

5 Marks

(b) Explain the two-thirds rule.

3 Marks

(c) Explain briefly the V.A.T. treatment of suppliers making exempt supplies. 2 Marks

Part B

Aíne Taylor has been carrying on in business for many years. She accounts for V.A.T. on the sales basis.

Details of her sales, receipt and payments for the two month period March/April 2016 were as follows:-

€

Sales exclusive of V.A.T at 23% 300,000

Cash receipts exclusive of V.A.T. at 23% 295,000

Expenses inclusive of V.A.T. at 23%

Goods for re-sale 184,500

Entertaining customers 615

Petrol 968

Diesel 1,107

Telephone 492

Expenses inclusive of V.A.T at 13.5%

Electricity 681

Requirement:

(i) Compute Aíne’s V.A.T. liability for the two-month period March/April 2016.

8 Marks

(ii) State the date by which the V.A.T. liability should have been paid.

2 Marks

Total 20 Marks

Page 10 of 32

Sample Paper 1

SECTION B

Answer any TWO of the four questions in this section

QUESTION 4

Gary and his wife Sandra are resident and domiciled in Ireland. During 2016 they had the following

disposals:-

(i) In June 2016, Gary sold 10,000 shares in Delta Limited for €35,000. Details of Gary’s

acquisitions are as follows:-

Date of Purchase Number of Shares Cost

€

1st March 1999 5,000 8,400

15th

September 2002 12,000 25,500

(ii) In August 2016, Sandra sold a painting her husband had given to her in October 2000 for

€10,000. The market value of the painting in October 2000 was €4,000. Gary had originally

purchased the painting in May 1980 for €800 at a car boot sale.

(iii) Gary inherited 50 acres of farm land from his father in January 1988. Its market value at that

date was €21,000. His father had originally purchased the 50 acres in January 1980 for €5,000.

In October 2016, Gary sold 10 acres for €8,000. The market value of the 40 acres remaining is

€45,000.

(iv) Gary and Sandra sold a house they owned jointly for €300,000 net of disposal costs in

November 2016. This house was not their principal private residence. They had originally

purchased the house in March 1998 for €56,500. Legal costs of acquisition were €4,000. They

spent €40,000 on an extension in August 2001. In February 2002, they spent €5,000 on

repairing the roof.

Requirement

a) You are required to calculate Gary and Sandra’s capital gains tax for 2016.

18 Marks

b) State the date(s) by which any capital gains tax is payable.

2 Marks

Total 20 Marks

Page 11 of 32

Sample Paper 1

QUESTION 5

a) Sarah Murray commenced as a florist on 1st June 2014. Her tax adjusted profits for her first three

years are as follows:-

Year ended 31st May 2015 €9,600

Year ended 31st May 2016 €6,000

Year ended 31st May 2017 €12,000

Requirement

You are required to calculate Sarah’s Case I Income for her first three tax years exercising any

options available to her.

10 Marks

b) John White has been in business for many years. His year end is September each year. His tax

written down value at 1st January 2016 is as follows:-

Machinery €11,250

Motor Car €18,000

The machine was purchased in May 2014 for €15,000. The car was purchased in March 2014 for

€30,000. John uses the car 25% for private use. The emissions for this car were 140g/km.

During his year ended 30th

September 2016, John had the following transactions with regard to

his fixed assets:-

Date Transaction Cost/Sales Proceeds Grant Received

1/11/2015 Purchase of Machine €10,000 €1,000

10/07/2016 Sale of Car €19,200 -

10/07/2016 Purchase of new car €35,000 -

The emissions of the new car purchased on the 10th

July 2016 are 165 g/km. The private use by

John White remains at 25%.

Requirement

You are required to calculate John White’s capital allowances for 2016.

10 Marks

Total 20 Marks

Page 12 of 32

Sample Paper 1

QUESTION 6

The following multiple choice questions consist of TEN parts, each of which is followed by four possible

answers. There is only one correct answer.

Requirement

Indicate the correct answer to each of the following TEN parts.

[1] Green Ltd provides Mark with a company car on 1st October 2014. The car cost Green Ltd €20,000.

Its original market value was €26,000. Mark travels 26,500 business kilometres in 2016 and

reimburses his employer €1,000 in 2016 for the use of the car. What is Mark’s taxable Benefit–in–

Kind for 2016:

a) €6,000

b) €5,000

c) €6,240

d) €5,240

[2] Mark Byrne ceased business on the 30th

June 2016. He made up accounts to

30th

June each year. Profits as adjusted for tax purposes were as follows:-

Year ended 30th

June 2015 €10,000

Year ended 30th

June 2016 €12,000

The Schedule D, Case I profit assessed for 2016 is:-

a) €12,000

b) €10,000

c) € 6,000

d) €11,000

[3] Josie is single. In 2016 she paid €8,000 to her widowed mother, aged 68 under a Deed of Covenant.

She paid a further €4,000 in favour of her permanently incapacitated niece aged 9, under a separate

Deed of Covenant. In 2016 details of Josie’s income are as follows:

Gross Income €140,000

Total Income €100,000.

The amount of tax relief available to Josie in respect of payments under Deed of Covenants is:

a) €11,000

b) €9,000

c) €12,000

d) €5,000

[4] Seamus owns his own business. He is registered for V.A.T. He supplies goods to a registered trader

on 18th

June 2016. He must issue a V.A.T. invoice to the registered trader by: -

a) 10th

July 2016

b) 19th

July 2016

c) 15th

July 2016

d) 30th

June 2016

Page 13 of 32

Sample Paper 1

QUESTION 6 (Cont’d)

[5] Wise Limited had an accounting period year ended 31st October 2016. The company paid a dividend

to its shareholders on 18th

June 2016. Dividend withholding tax must be paid by Wise Limited by: -

a) 23rd

September 2016

b) 31st December 2016

c) 23rd

July 2016

d) 14th

July 2016

[6] To account for V.A.T. on a cash receipts basis you must supply 90% of your turnover to a non-

registered person or your annual turnover must be below: -

a) € 37,500

b) € 75,000

c) €2,000,000

d) €1,250,000

[7] Lorraine borrowed €100,000 from her employer on 1st July 2016. She used the money to purchase her

main residence. Her employer charged her interest of 3.25%. What is Lorraine’s Benefit-in-Kind for

2016: -

a) € 875

b) €1,750

c) € 375

d) € 750

[8] Susan a single person purchased a house for €50,000 on 1st July 200. On 1

st July 2016 she sold the

house for €350,000. Susan lived in this house as her principal private residence for the period 1st July

2002 to 30th June 2008. She made no other disposals in 2016. Her capital gains tax for 2016 and her

payment date for this gain is: -

a) €49,095 15th

December 2016

b) €48,676 31st October 2017

c) €52,441 15th

December 2016

d) €48,676 15th

December 2016

[9] Joe sold a painting for €10,000 in May 2016. He was given the painting by his Aunt in July 1999 for

€1,000. The market value of the painting in July 1999 was €2,200. Joe’s chargeable capital gain

before annual exemption is: -

a) Nil as exempt

b) €9,000

c) €8,807

d) €7,375

Page 14 of 32

Sample Paper 1

QUESTION 6 (Cont’d)

[10] Acorn Ltd commenced trading on 1st July 2015 and incurred a trade loss of €10,000 in the year

ended 30th

June 2016. Acorn Ltd. also had the following income during the year ended 30th

June

2016:

Rental Income €6,000

Capital Gain - Adjusted for corporation tax €4,000

Calculate Acorn Limited’s corporation tax for the accounting period 30th

June 2016 assuming

maximum loss relief was claimed by Acorn Ltd.

a) Nil

b) €2,000

c) € 750

d) €1,250 Total 20 Marks

Page 15 of 32

Sample Paper 1

QUESTION 7

(a) List the six badges of trade which were identified by the Royal Commission of Taxation in 1954 and

write a brief note on each.

10 Marks

(b) Spruce Limited has prepared accounts for the 18-month accounting period ended 31st December

2016.

Details of the company’s income is as follows:

€

Case I adjusted income before capital allowances 25,000

Case III foreign interest 2,500

On 1st December 2015, Spruce Limited purchased plant and machinery for €20,000. The company did

not own any other plant and machinery.

Requirement:

Calculate the corporation tax due by Jupiter Limited for all accounting periods covered by Spruce

Limited’s 18 month accounting period to the 31st December 2016.

You may assume all income accrued evenly throughout the 18-month period.

10 Marks

Total 20 Marks

Page 16 of 32

Sample Paper 1

Advanced Taxation (Republic of Ireland)

Sample Paper 1 – Suggested Solutions

Page 17 of 32

Sample Paper 1

Solution 1

David and Susan

Income Tax Liability 2016

(i)

Notes €

Schedule D – Case II (H) 1 82,000

Schedule D – Case IV (H)

€2,360 x 100 4,000

[100-41]

Schedule D – Case V (H) 2 36,800

Schedule E (W) 5,000

Schedule F (W)

€2,560 x 100 3,200

80

131,000

Less: Charges

Retirement Annuity 3 (10,000)

Statutory Income 121,000

Allowances

Permanent Health Insurance 4 (850)

Taxable Income 120,150

€ 51,000 at 20% = €10,200 (Note 5)

€ 4,000 at 41% = € 1,640 (Note 6)

€ 65,150 at 40% = €26,060

€ 120,150 €37,900

Page 18 of 32

Sample Paper 1

Solution 1 (Cont’d)

Less: Non Refundable Tax Credits

Married €3,300

P.A.Y.E. (Note 7) €1,000

Earned Income € 550

Carers (Note 8 and note 5) Nil

DIRT €4,000 at 41% €1,640

College Fees (Note 9) € 140 € 6,630

Tax Liability €31,270

Less: Refundable Tax Credits

P.A.Y.E. Paid € 950

DWT €3,200 at 20% € 640 € 1,590

€29,680

(ii)

David Total Income €

Schedule D – Case I 82,000

Schedule D – Case IV 4,000

Schedule D – Case V 36,800

122,800

P.R.S.I and Universal Social Charge

PRSI €122,800 at 4% = €4,912

Universal Social Charge - David Only

Schedule D – Case I 82,000

Schedule D – Case IV exempt

Schedule D – Case V 36,800

118,800

€12,012 at 1% = € 120.12

€ 6,656 at 3% = € 199.68

€51,376 at 5.5% = €2,825.68

€29,956 at 8% = €2,396.48

€18,800 at 11%1 = €2,068.00

€118,800 €7,609

1 A 3% surcharge applies to USC for non-PAYE income in excess of €100,000

Page 19 of 32

Sample Paper 1

Solution 1 (Cont’d)

(iii)

The payment date for David’s preliminary tax for 2016 is 31st October 2016.

(iv)

The filing date for David’s form 11 for 2016 is 31st October 2017.

Notes

1. Schedule D – Case II

As David is not in commencement or cessation the basis of assessment is current year.

2016 c/y 30th June 2016 €90,000

Less capital allowances € 8,000

Schedule D – Case II €82,000

2. Schedule D – Case V

Rent 24,000 x 2/12 = €4,000

(Nov-Dec)

Premium

€40,000 X (51-10) = €32,800

50

Schedule D – Case V €36,800

3. Retirement Annuity

Schedule D – Case II €82,000

Maximum tax relief

€82,000 x 25% = €20,500

Relief restricted to amount paid €10,000

Page 20 of 32

Sample Paper 1

Solution 1 (Cont’d)

4. Permanent Health Insurance

Maximum 10% of Statutory Income

Case I + Case IV + Case V – Retirement annuity

€82,000 + €4,000 + €36,800 - €10,000 = €112,800 at 10% = €11,280

Limited to premium paid of €850.

5. The married band for one income is €42,800, this will be increased by Susan’s income of €8,200. This

gives a married band of €51,000.

6. The maximum tax that deposit interest is assessed on is 41%.

7. The P.A.Y.E credit is restricted as Susan’s Schedule E income is only €5,000. Therefore, the P.A.Y.E.

credit is limited to €5,000 x 20% = €1,000.

8. The carer’s credit does not apply as Susan’s income exceeds €6,700 and the increased band was claimed.

9. College fees €2,200 - €1,500 = €700 at 20% = €140.

Solution 2

(a)

Blayney Limited

Case I Computation

Year ended 30th

September 2016

Notes € €

Net profit

219,975

Add Backs

Depreciation 10,510

Interest on late payment of corporation tax

1,510

Legal Fees (1) 4,250

Increase in general provision for bad debts 800

Entertainment (€5,000 – €1,580) 3,420

Motor expenses and lease rental (2) 3.188 23,678

243,653

Deductions

Other income (120,000)

Case 1 Excluding capital allowances 123,653

NOTES

(1) Legal Fees €

Parking Fines 450

Disposal of warehouse 3,800

4,250

(2) Motor expenses and lease rental.

There is no addback for expenses only lease rental for cars as any personal usage will be dealt

with through the PAYE system.

Car for managing director is category D

Disallow

€5,100 X [(€32,000-€12,000)/€32,000] = €3,188

Page 22 of 32

Sample Paper 1

Solution 2 (Cont’d)

(b) Blayney Limited

Capital Allowances computation

Machinery Car Van

€ € €

TWDV 1 October 2015 12,750 21,000 22,750

W&T Note 1 (2,125) (3,000) (3,250)

TWDV 30 September 2016 10,625 18,000 19,500

Note 1

Wear and Tear

Machine

Cost 18,000

Less: grant 1,000

17,000 at 12 ½ % = €2,125

Car 27,500

Limit 24,000 at 12 ½ % = €3,000

Van (no limit) 26,000 at 12 ½% = €3,250

€8,375

(c)

Blayney Limited

Corporation Tax Computation

Year ended 30th

September 2016

Notes €

Schedule D Case I

€123,653 - €8,375 = 115,278

Less: Trade loss carried forward (10,000)

105,278

Schedule D Case III 10,000

Income 115,278

Gain 2 82,310

Profits 197,588

Corporation Tax Case I €105,278 at 12 ½% = €13,160

Case III € 10,000 at 25% = € 2,500

Gain € 82,310 at 12 ½% = €10,289

€25,949

Page 23 of 32

Sample Paper 1

Solution 2 (Cont’d)

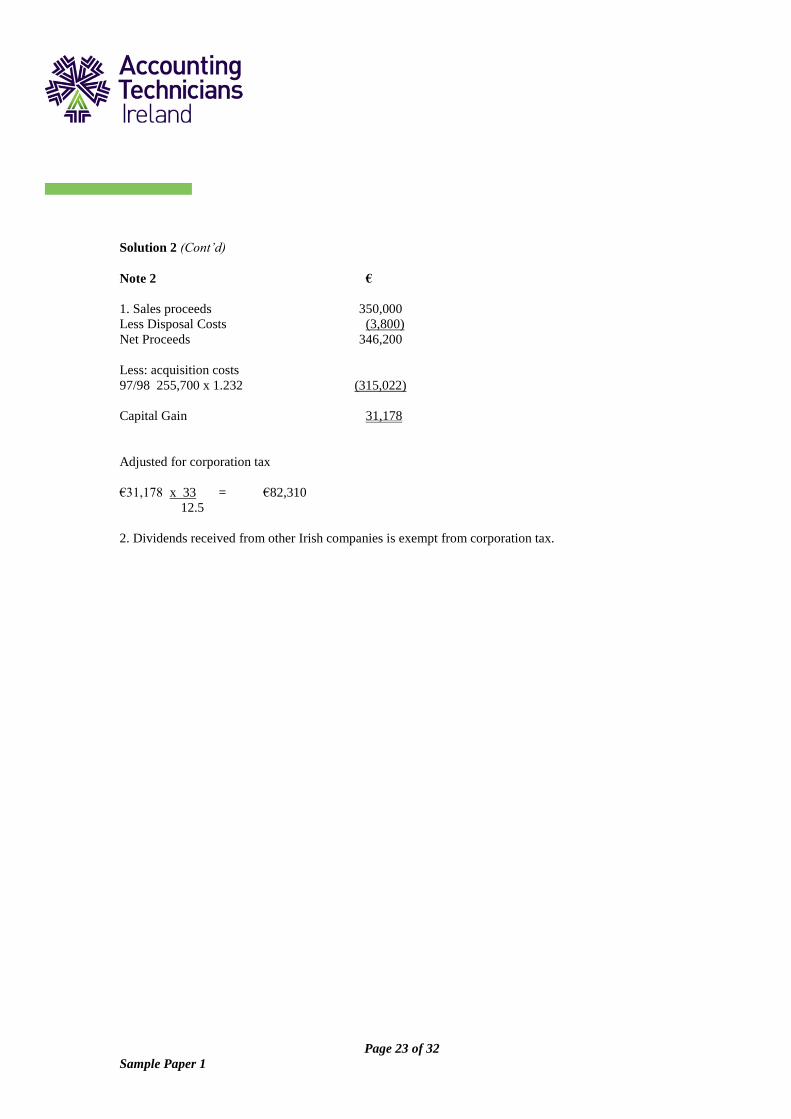

Note 2 €

1. Sales proceeds 350,000

Less Disposal Costs (3,800)

Net Proceeds 346,200

Less: acquisition costs

97/98 255,700 x 1.232 (315,022)

Capital Gain 31,178

Adjusted for corporation tax

€31,178 x 33 = €82,310

12.5

2. Dividends received from other Irish companies is exempt from corporation tax.

Page 24 of 32

Sample Paper 1

Solution 3

Part A

(a) Where there is no obligation on a person to register for V.A.T., the issues to be considered are as

follows:

(i) The percentage of the customers or potential customers who are registered or likely

to be registered for V.A.T.

(ii) Whether the V.A.T element of the purchase/input costs are significant.

(iii) The additional work involved in having to issue V.A.T. invoices and lodging of

V.A.T. returns with the revenue.

(iv) The possibility of a V.A.T audit and the danger of penalty/interest exposures if the

V.A.T. returns are not correct and/or V.A.T. due for a period is not paid on time.

(b) The rate of V.A.T. applying to a service which is supplied with goods is dependent on the ⅔ rule. This

is a rule, which provides that a transaction is liable for V.A.T. as a sale of goods at the rate of V.A.T.

applicable to the goods supplied, and not at a rate applicable to the service if the value of goods used

in providing the service exceeds two thirds of the consideration charged to the customer.

(c) Where a supply is made of an exempt item it is not regarded as a taxable supply for V.A.T. purposes

and the trader therefore cannot register for VAT or obtain credit in respect of input V.A.T.

Part B

(i)

Aíne Taylor

V.A.T. Computation - March/April 2016

V.A.T. on sales € €

€300,000 at 23% 69,000

V.A.T. on expenses

Goods for resale

184,500 x 23 (34,500)

123

Entertaining customer Not allowed

Petrol Not allowed

Diesel

1107 x 23 (207)

123

Telephone

492 x 23 (92)

123

Electricity

681 x 13.5 (81) (34,880)

113.5 V.A.T. Due 34,120

(ii) The V.A.T. due must be paid on or before 23rd

of May 2016.

Page 25 of 32

Sample Paper 1

Solution 4

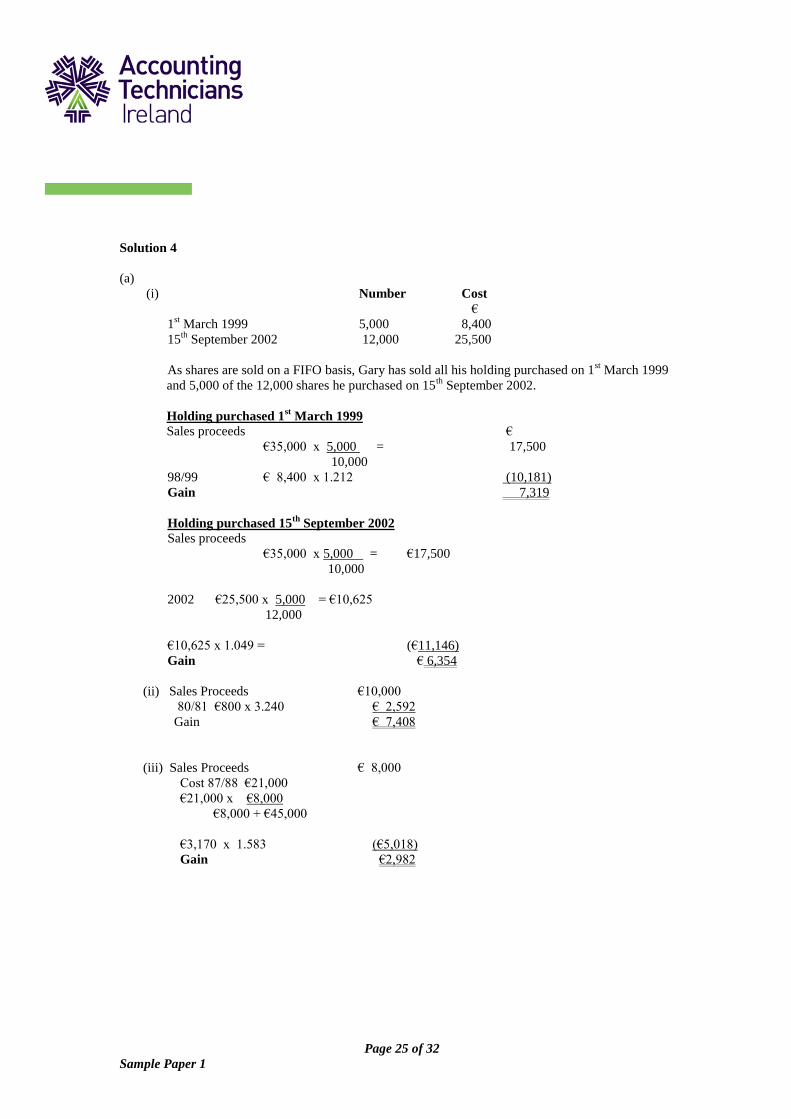

(a)

(i) Number Cost

€

1st March 1999 5,000 8,400

15th

September 2002 12,000 25,500

As shares are sold on a FIFO basis, Gary has sold all his holding purchased on 1st March 1999

and 5,000 of the 12,000 shares he purchased on 15th

September 2002.

Holding purchased 1st March 1999

Sales proceeds €

€35,000 x 5,000 = 17,500

10,000

98/99 € 8,400 x 1.212 (10,181)

Gain 7,319

Holding purchased 15th

September 2002

Sales proceeds

€35,000 x 5,000 = €17,500

10,000

2002 €25,500 x 5,000 = €10,625

12,000

€10,625 x 1.049 = (€11,146)

Gain € 6,354

(ii) Sales Proceeds €10,000

80/81 €800 x 3.240 € 2,592

Gain € 7,408

(iii) Sales Proceeds € 8,000

Cost 87/88 €21,000

€21,000 x €8,000

€8,000 + €45,000

€3,170 x 1.583 (€5,018)

Gain €2,982

Page 26 of 32

Sample Paper 1

Solution 4 (Cont’d)

( iv) Sales Proceeds €300,000

Cost 97/98 €56,500

Add: acquisition costs €4,000

€60,500

€60,500 x 1.232 (€74,536)

Enhancement expenditure

2001 €40,000 x 1.087 (€43,480)

Gain €181,984

The repairs are not allowed in capital gains tax as they are not capital expenditure.

Gary and Sandra

Capital Gains Tax Computation – 2016

(Note-Separate calculation of gain shown for each)

Gary Sandra

€ €

(i) €7,319 + €6,354 13,673

(ii) 7,408

(iii) 2,982

(iv) 181,984 / 2 90,992 90,992

107,647 98,400

Less: annual exemption (1,270) (1,270)

106,377 97,130

Capital Gains Tax at 33% 35,104 32,053

Total Capital Gains Tax for 2016

€35,104 + €32,053 = €67,157.

(b) The tax on the sale of the shares, painting and the land must be paid by 15th

December 2016, as

these gains arise in the initial period.

The tax on the sale of the house must be paid by the 31st January 2017 as that gain arises in the

later period.

Page 27 of 32

Sample Paper 1

Solution 5

(a) Tax year Basis of Assessment Amount

2014 Actual

1st June 2014 to 31

st December 2014

€9,600 x 7/12 €5,600

2015 12 months ended 31st May 2015 €9,600

2016 12 months ended 31st May 2016 €6,000

Section 66 TCA 1997

This option is available in the third year.

Original assessment for year 2

€9,600

Actual for year 2 – 2015

1st January 2015 to 31

st December 2015

€9,600 x 5/12 = €4,000

€6,000 x 7/12 = €3,500 €7,500

Excess €2,100 *

Adjustment in Year 3 2016 original assessment €6,000

Less: Section 66 (€2,100) *

Final assessment €3,900

Final Assessments

2014 €5,600

2015 €9,600

2016 €3,900 (as revised)

Page 28 of 32

Sample Paper 1

Solution 5 (Cont’d)

(b) John White

Capital Allowances Computation – 2016

Machinery Motor Car

€ €

TWDV – 1st January 2016 11,250 18,000

Disposal (18,000)

Additions 9,000 12,000 Note 1

20,250 12,000

Wear and Tear (3,000) Note 2 (1,500)

TWDV – 31st December 2016 17,250 10,500

Balancing charge / allowance computation

Sales Proceeds €19,200 x €24,000 = €15,360

€30,000

TWDV €18,000

Balancing allowance €2,640

Restricted to business use

€2,640 x 75% = €1,980

Summary € €

Wear and Tear

Machinery 3,000

Car €1,500 x 75% 1,125 4,125

Balancing allowance 1,980

Total Capital allowances for 2016 6,105

NOTES

1. As the car’s emissions are 165g/km, the cost of the car (for capital allowances) is restricted to the lower

of:-

(i) €35,000 x 50% = €17,500

or

(ii) €24,000 x 50% = €12,000

2. Wear and Tear for Machinery

€

Opening cost 15,000

Cost of addition less grant 9,000

24,000

Wear and Tear at 12 ½ % = 3,000

Page 29 of 32

Sample Paper 1

Solution 6

(1) – (d) €26,000 x 24% = €6,240 - €1,000 = €5,240

(2) – (c) Actual 1/1/2015 to 30/06/2015

€12,000 x 6/12 = €6,000

(3) – (b) No restriction on payment in respect of permanently incapacitated child so full €4,000

allowed.Payment in respect of adult aged over 65 restricted to 5% of total income so relief restricted to

(€100,000 @ 5%) €5,000.

Relief die (€4,000 +€5,000) = €9,000.

(4) – (c)

(5) – (d)

(6) – (c)

(7) – (c) €100,000 x (4 % - 3 ¼ %) = €750

€750 x 6/12 = €375

(8) – (d) Sales proceeds €350,000

2002

€50,000 x 1.049 € 52,450

€297,550

Total ownership

1/7/2002 to 1/7/2016 = 14 years

Non occupation

1/7/2009 to 1/7/2016 = 7 years

Last 12 months of ownership (1/7/2015- 1/7/2016) is deemed occupation.

€297,550 x 7/14 = €148,775

Less: annual exemption € 1,270

€147,505

Tax 33% € 48,676

Sold in July 2016: Payment date 15th

December 2016

(9) – (d) Sales proceeds €10,000

99/00

€2,200 x 1.193 € 2,625

Gain € 7,375

Page 30 of 32

Sample Paper 1

Solution 6 (Cont’d)

(10) – (c) Acorn Ltd

Corporation Tax Computation

Schedule D – Case I Nil

Schedule D – Case V € 6,000

Income € 6,000

Gain € 4,000

Profits €10,000

Corporation tax

€6,000 x 25% = € 1,500

€4,000 x 12 ½ % = € 500

€ 2,000

Less: Trade loss

€10,000 x 12 ½ % = (€1,250)

€750

Page 31 of 32

Sample Paper 1

Solution 7

(a) The six badges of trade as identified by the Royal Commission of Taxation in 1954 were as follows:

1. Subject matter;

2. Frequency of transactions;

3. Length of ownership;

4. Supplementary work and marketing;

5. Circumstances in which the asset is realised;

6. Profit motive.

1. Subject Matter

The question as to whether a person is trading or not sometimes can be decided by examining the subject

matter of the transaction under review. Assets, such as painting are quite often held as an investment for

their intrinsic value. Consequently, a subsequent disposal at a profit may produce a gain of a capital

nature rather than a trading profit. On the other hand, a profit arising from the sale of articles such as

clothing stock, cosmetics and so forth are more likely classified as a trading profit.

2. Frequency of Transactions

A gain arising from a once off transaction could indicate that it is of a capital rather than a trading nature.

Whereas, gain/profit arising from the frequent sale of assets would indicate a trading profit.

3. Length of ownership

Here, the courts infer that the sale of items shortly after their purchase indicate an adventure in the nature

of a trade.

4. Supplementary work and marketing

In a case where work is done to convert, or create an asset, rather than simply making it more marketable,

the courts will almost certainly ascribe a trading motive.

5. Circumstances in which the asset is realised

Where a taxpayer can show that the reason why the asset was sold was in response to an emergency or a

sudden opportunity to realise a windfall gain, rather than as part of an organised scheme for making

profit, he could go a long way to establishing that the gain was capital rather than trading in nature.

6. Profit Motive

While the absence of a profit motive does not necessarily mean that a trade was not carried on and indeed

there is abundance of case law to prove this point, it is nevertheless a strong indication that trading is

carried on.

Page 32 of 32

Sample Paper 1

Solution 7 (Cont’d)

(b) Spruce Limited

12 months to 6 months to

30-Jun-16 31-Dec-16

€ €

Profits (25,000 X 12/18) 16,667

(25,000 X 6/18) 8,333

Capital allowances (20,000 @ 12.5%) (2,500)*

20,000 @ 12.5% X 6/12 (1,250) **

Case I 14,167 7,083

Case III 1,667 833

Total Income 15,834 7,916

Taxed as Follows

Case 1@ 12.5% 1,770 885

Passive Income @ 25% 417 208

Tax Due 2,187 1,093

* As accounts are for 12 months 12 months capital allowances due

** As accounts are only for 6 months only 6 months capital allowances due.