Embed Size (px)

Citation preview

Please do not quote!

Advanced Econometrics 1

and

Theoretical Econometrics

Lecture Notes

Laszlo Matyas

2020

1

Topics : 1− 2

Short Introduction to Identificationand Asymptotics

2

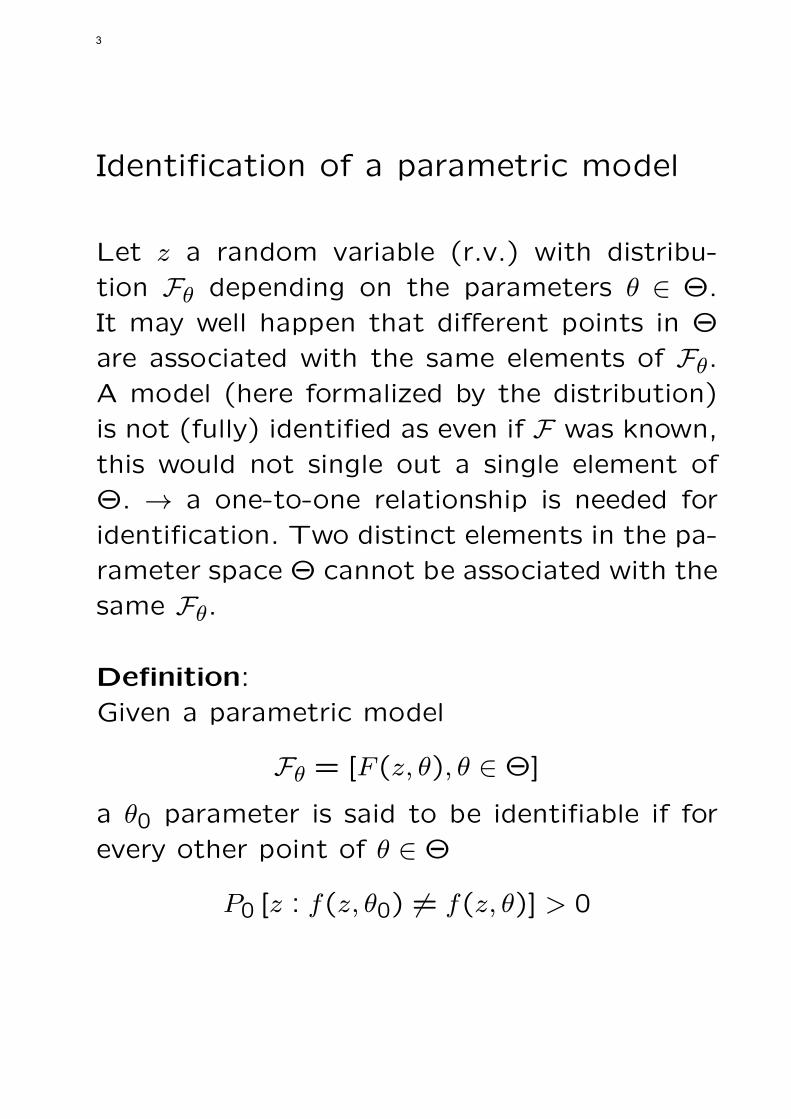

Identification of a parametric model

Let z a random variable (r.v.) with distribu-

tion Fθ depending on the parameters θ ∈ Θ.

It may well happen that different points in Θ

are associated with the same elements of Fθ.

A model (here formalized by the distribution)

is not (fully) identified as even if F was known,

this would not single out a single element of

Θ. → a one-to-one relationship is needed for

identification. Two distinct elements in the pa-

rameter space Θ cannot be associated with the

same Fθ.

Definition:

Given a parametric model

Fθ = [F (z, θ), θ ∈ Θ]

a θ0 parameter is said to be identifiable if for

every other point of θ ∈ Θ

P0 [z : f(z, θ0) = f(z, θ)] > 0

3

where P0 denotes the probability with respect

to the density f(z, θ0). A model is (fully) iden-

tified if it is identified in all its parameter points

∈ Θ.

Partial identification → identification in a re-

stricted parameter space. E.g., Local identifi-

cation → “around”, in the “neighbourhood” of

a parameter value.

Asymptotic identification → when the model is

identified in large samples (sample size → ∞).

EXAMPLE:

Let Fθ the parametric model generated by r.v.

u ∼ N2(0, I2) (2D normal r.v.) through the

transformation g(u) = Γu, where Γ is a (2×2)

matrix.

This model is NOT identified as, for example,

Γ0 =

(2 11 2

), Γ1 =

( √5 0

4/√5 3/

√5

)

4

are associated with the same N2(0, σ):

Σ = Γ0Γ′0 = Γ1Γ

′1 =

(5 44 5

).

Elements of asymptotic theory(Detailed theory in lecture READER 1!)

Definition: Limit of a deterministic sequence (or

convergnece)

Series xn, n = 1, . . . converges to a constant c

if for any ε > 0 there is an n ≥ N such that

|xn − c| < ε, then limn→∞xn = c .

Definition: Limit of a random sequence

Series of random variables xn converges to con-

stant c if

limn→∞Prob [(|xn − c|) > ε] = 0, for any ε > 0.

5

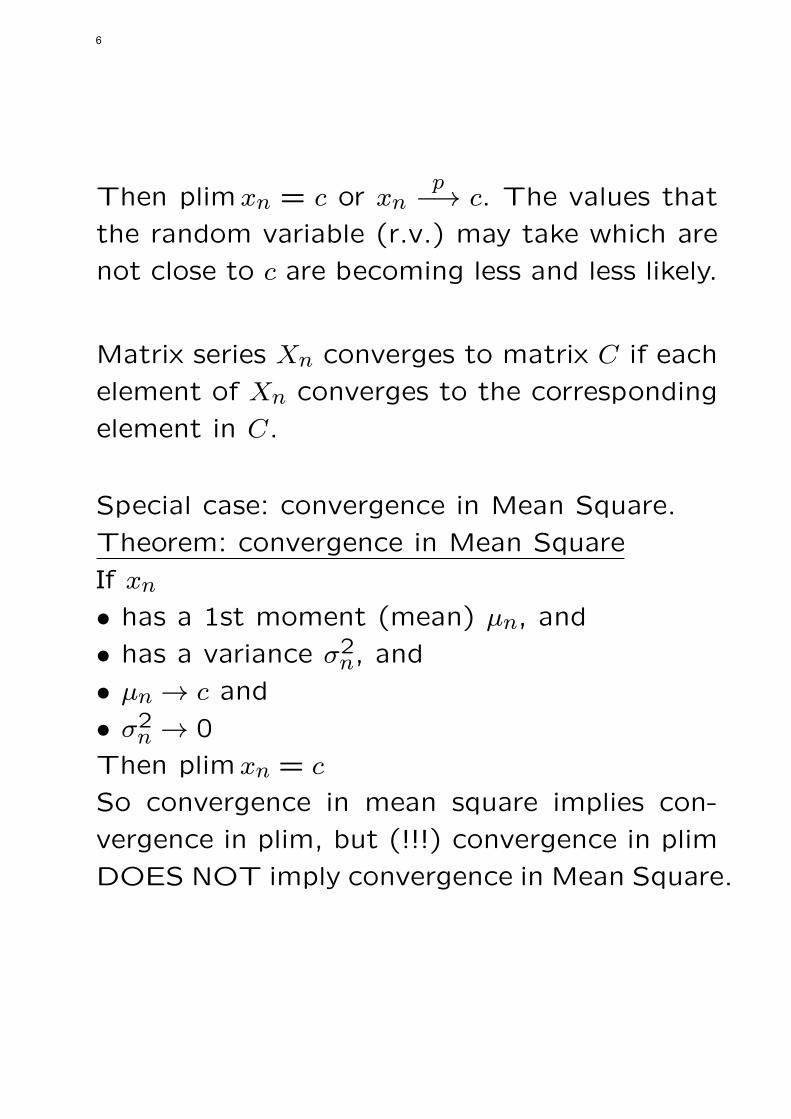

Then plimxn = c or xnp−→ c. The values that

the random variable (r.v.) may take which are

not close to c are becoming less and less likely.

Matrix series Xn converges to matrix C if each

element of Xn converges to the corresponding

element in C.

Special case: convergence in Mean Square.

Theorem: convergence in Mean Square

If xn

• has a 1st moment (mean) µn, and

• has a variance σ2n, and

• µn → c and

• σ2n → 0

Then plimxn = c

So convergence in mean square implies con-

vergence in plim, but (!!!) convergence in plim

DOES NOT imply convergence in Mean Square.

6

Slutsky theoremFor a continous function g(xn), which is not afunction of n

plim g(xn) = g(plimxn) .

Properties of the plim

If plimxn = c and plim yn = d, then:plim(xn + yn) = c+ d

plimxnyn = c d

plim xnyn

= cd, d = 0 .

If XN is an invertible random matrix,then plimXn = Ω implies plimX−1

n = Ω−1.

Uniform convergence in probabilitySeries of r.v. xn(θ) (r.v. x depends on θ) con-verges uniformly to the constant c(θ) in prob-ability on the parameter space Ω if

limn→∞P (sup

θ∈Ω|xn(θ)− c(θ)| < ξ) = 1 ∀ξ > 0

7

Some laws of large numbersGeneric Weak Law of Large Numbers - WLLN

Let xn be a series of r.v. on n = 1, . . . , N , with

E(xn) = µ If some regularity conditions are

met, then

xn =

∑Nn=1 xn

N

p−→ µ .

Some “applications” of this.

WLLN for iid series

Let xn be a series of r.v. on n = 1, . . . , N , with

E(xn) = µ and the same variance σ2 = E(xn−µ)2, then

xn =

∑xn

N

p−→ µ .

WLLN for non iid series

Let xn be a series of i.i.d. r.v. on n = 1, . . . , N ,

with E(xn) = µ and different variances σ2n =

E(xn − µ)2. If V ar(xn) → 0, then

xnp−→ µ .

8

Distributions

Definition: Convergence in distribution

Let xn series of r.v. with cdf Fn(x), then xn

converges in distribution to a r.v x with cdf

F (x) if

limn→∞ |Fn(x)− F (x)| = 0

at all points of F (x): xnd−→ x. This called the

Limiting Distribution.

Convergence in distribution DOES NOT mean

convergence in plim! Let us see an example!

Let r.v xn have the following distribution:

Prob(xn = 1) =1

2+

1

n+1

Prob(xn = 2) =1

2−

1

n+1

Now

xnd−→ f(x) =

P (x = 1) = 1/2

P (x = 2) = 1/2

9

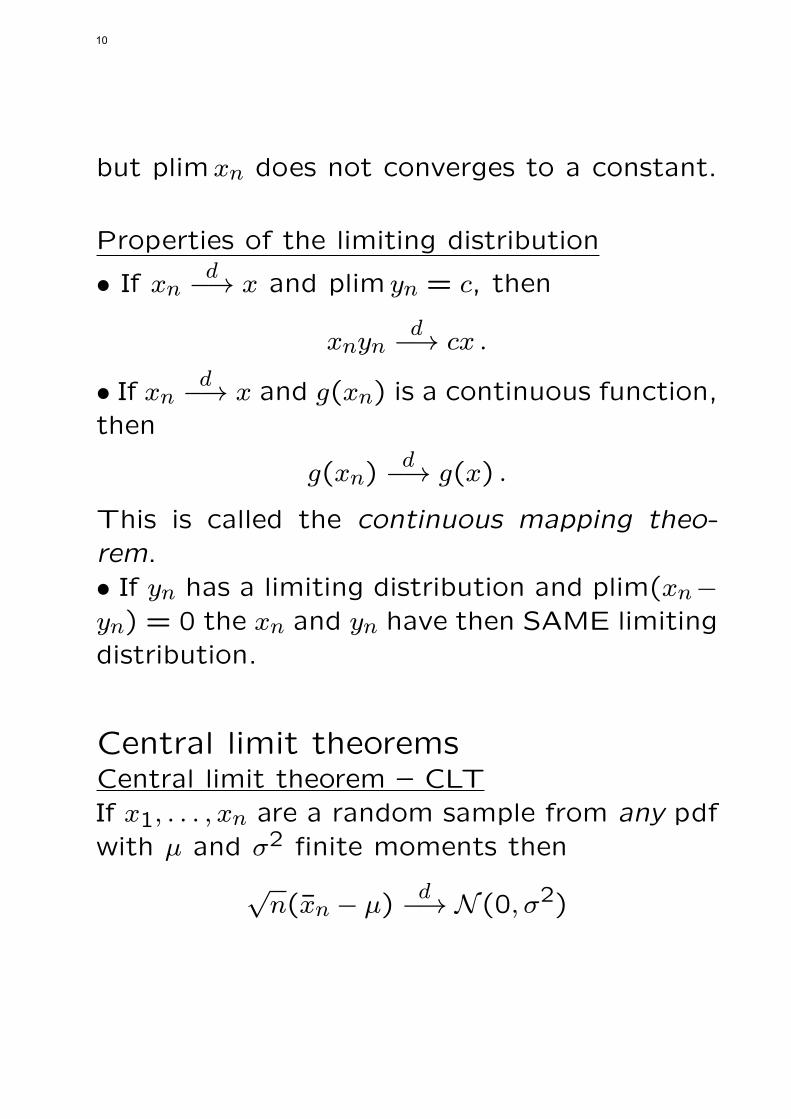

but plimxn does not converges to a constant.

Properties of the limiting distribution

• If xnd−→ x and plim yn = c, then

xnynd−→ cx .

• If xnd−→ x and g(xn) is a continuous function,

then

g(xn)d−→ g(x) .

This is called the continuous mapping theo-rem.• If yn has a limiting distribution and plim(xn−yn) = 0 the xn and yn have then SAME limitingdistribution.

Central limit theoremsCentral limit theorem – CLTIf x1, . . . , xn are a random sample from any pdfwith µ and σ2 finite moments then

√n(xn − µ)

d−→ N (0, σ2)

10

Lindberg – Levy CLTIf x1, . . . , xn are a random sample from a mul-tivariate distribution (random vectors) with fi-nite moment µ and Q covariance matrix, then

√n(xn − µ)

d−→ N (0, Q)

Lindberg – Feller CLTIf x1, . . . , xn are a random sample from a multi-variate distribution with finite moment E(xi) =µi, it’s demeaned version E(xi − µi) = 0 ∀i,V ar(xi) = Qi,

Qn =

∑iQi

n, lim Qn = Q pos. definite ∀n

and some regularity conditions are satisfied,then

√n(xn − µn)

d−→ N (0, Q)

with µn = 1n

∑i µi.

Definition: Asymptotic DistributionIt is a distribution to approximate the (often

11

unknown) distribution of a random variable.

Example:

If√n(xn − µ)

σ

d−→ N (0,1)

then we say that xn asymptotic distribution is

xnd−→ N (µ, σ2) or

A∼

Definition: Limiting Distribution

It is the Asymptotic distribution WITHOUT

normalising and de-meaning. In the above ex-

ample the limiting distribution is

xnd−→ N (µ,

σ2

n) .

[Comment: as we will see later on, for a con-

sistent estimator the variance of the limiting

distribution is always 0, while, in most of the

cases, the variance of the asymptotic distribu-

tion is finite, non-zero!]

12

Rates of convergence – Order notation

Definition: Same Order

A deterministic sequence θT is O(T k) (of the

order T k) if: for some M > 0, there exists some

number K such that∣∣∣∣T−kθT

∣∣∣∣ < M

for all T > K.

This definition states that θT is O(T k) if T−kθTbecomes bounded as T → ∞. Notice it must

hold for some M , not all M . If the definition

held for all M then T−kθT would converge to

zero.

Example 1:

If

θT = T2,

then θT = O(T2) since T−2θT = 1 for all T ,

and hence is bounded for all T .

13

Example 2: (a bit more challenging)If

θT =T∑

t=1

t,

then θT = O(T2).

Definition: Smaller/Lower OrderA deterministic sequence θT is o(T k) if: forall ϵ > 0, there exists some number K suchthat ∣∣∣∣T−kθT

∣∣∣∣ < ϵ

for all T > K.That is, if θT = o(T k) then

T−kθT → 0.

This notation is used most commonly as “θT =op(1)”, to state that θT → 0.Example:

θT =T∑

t=1

t then θT = o(T3) .

14

Operations with orders:

O(np)±O(nq) = O(nmax(p,q))

o(np)± o(nq) = o(nmax(p,q))

O(np)± o(nq) = O(np) if p ≥ q

O(np)± o(nq) = o(nq) if p < q

O(np)O(nq) = O(n(p+q))

o(np)o(nq) = o(n(p+q))

O(np)o(nq) = o(n(p+q))

Example: xt has µ as a first moment, and the

CLT applies to it, then

n∑t=1

xt = O(n) if µ = 0

and in the de-meaned casen∑

t=1

(xt − µ) = O(n1/2) .

15

Applying asymptotics to the linear re-gression model

y = Xβ + u

and the “usual” assumptions apply. Further,

we also assume that

limn→∞

1

nX ′X = Q positive definite

then

plim βOLS = β +plim(1

nX ′X)−1 (

1

nX ′u)

= β +Q−1 plim(1

nX ′u)

From the Mean Square Convergence, we need

lim1

nX ′uu′X

1

n=

σ2

n

X ′X

n

limσ2/n = 0, limX ′X/n = 0

so plim 1nX

′u = 0, i.e., the OLS is consistent.

16

Now let us see the asymptotic distribution of

the OLS. We are interested in

√n(β − β) =

(X ′X

n

)−1 1√nX ′u

and we need the limiting distribution of 1√nX ′u.

Using the Lindberg–Feller CLT we get

1√nX ′u d−→ N (0, σ2Q)

which implies that

√n(β − β)

A∼ N (0, σ2Q−1) .

17

Topic : 3

Maximum Likelihood Estimation

18

Inverse Function

For scalars:

y = f(x)

where f(.) is strictly monotonic, there is aninverse function such as

x = f−1(y)

Example:

y = a+ bx

x = −a

b+

1

by

where

d x

d y=

d f−1(y)

d y

is the Jacobian of the transformation, here 1b .

For vectors:

y = f(x) , J =∂x

∂y′

19

is the Jacobian matrix,∂x1∂y1

. . . ∂x1∂yn... . . . . . .

∂xn∂y1

. . . ∂xn∂yn

Example:

y = Ax

x = A−1y

where abs(det(J)) i.e., the absolute value of thedeterminant is the Jacobian of x to y;

abs(det(J)) = abs(det(A−1)) =1

abs(det(A))

Let us now turn to the case of distributions.

Assume that x1 and x2 are random variableswith a joint distribution fx(x1, x2) and y1 andy2 are two monotonic functions of x1 and x2:

y1 = y1(x1, x2)

y2 = y2(x1, x2)

20

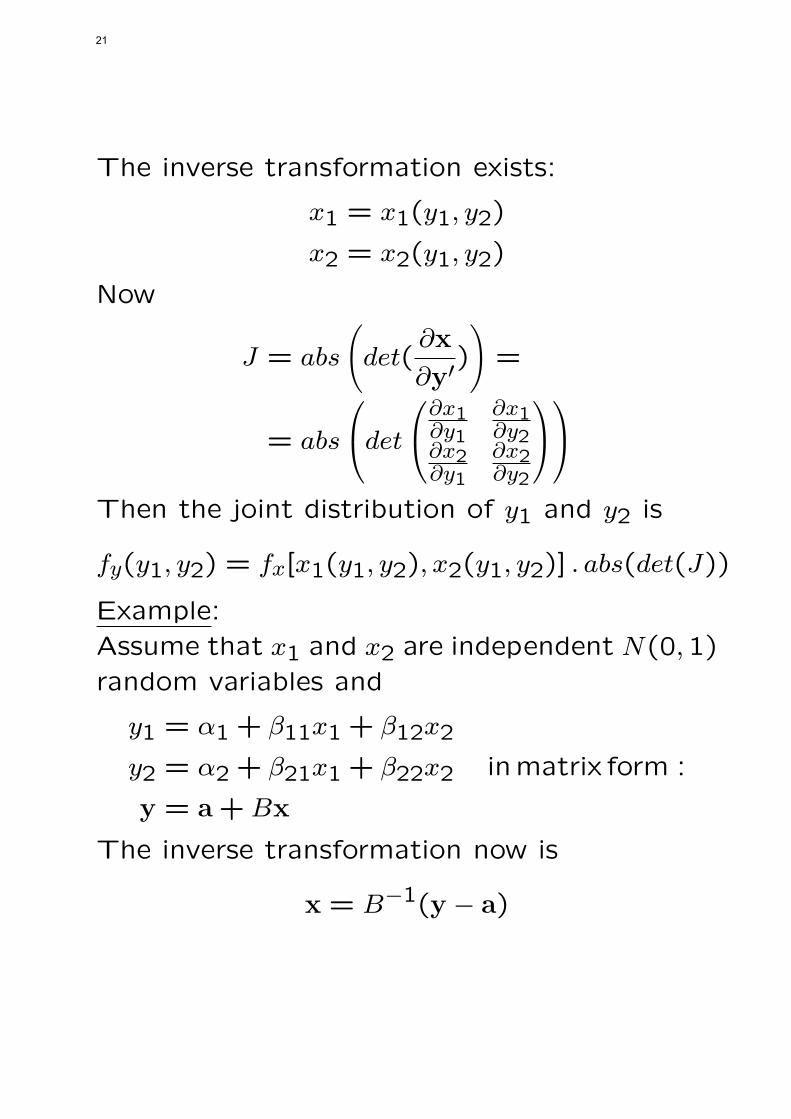

The inverse transformation exists:

x1 = x1(y1, y2)

x2 = x2(y1, y2)

Now

J = abs

(det(

∂x

∂y′)

)=

= abs

det∂x1

∂y1∂x1∂y2

∂x2∂y1

∂x2∂y2

Then the joint distribution of y1 and y2 is

fy(y1, y2) = fx[x1(y1, y2), x2(y1, y2)] . abs(det(J))

Example:

Assume that x1 and x2 are independent N(0,1)

random variables and

y1 = α1 + β11x1 + β12x2

y2 = α2 + β21x1 + β22x2 inmatrix form :

y = a+Bx

The inverse transformation now is

x = B−1(y − a)

21

and the Jacobian

J = abs(det(B−1)

)=

1

abs (det(B))

The joint distribution of x is the product of

the marginals since they are assumed to be

independent:

fx(x) = (2π)−1e−(x21+x22)/2

= (2π)−1e−X ′X/2

and so

fy(y) = (2π)−1 1

abs(det(B))e−((y−a)′(BB′)−1(y−a))/2

In general: If x is a continuous r.v. with pdf

fx(x) and y = g(x) is an invertible function of

x then the density of y is

fy(y) = fx(g−1(y)).abs

(det(d g−1(y))

)where d stands for the first derivative.

22

Example:

Let be

x ∼ N(0, I) y = A′x+ µ

y ∼ N(µ, V ), V = A′A

The Jacobian from y to x is now abs(det(A−1)).

The density of y in then

y = (2π)−n/2abs(det(A)−1

)×

× exp[−1/2(y − µ)′A−1A−1′(y − µ)]

= (2π)−n/2abs(det(V )−1/2

)×

× exp[−1/2(y − µ)′V −1(y − µ)]

Likelihood estimation

Reminder: Analytically the joint density func-

tion and the likelihood function are the same.

The difference is in how we look at it. In the

density function the parameters are known and

the variables are unknown. In the likelihood

23

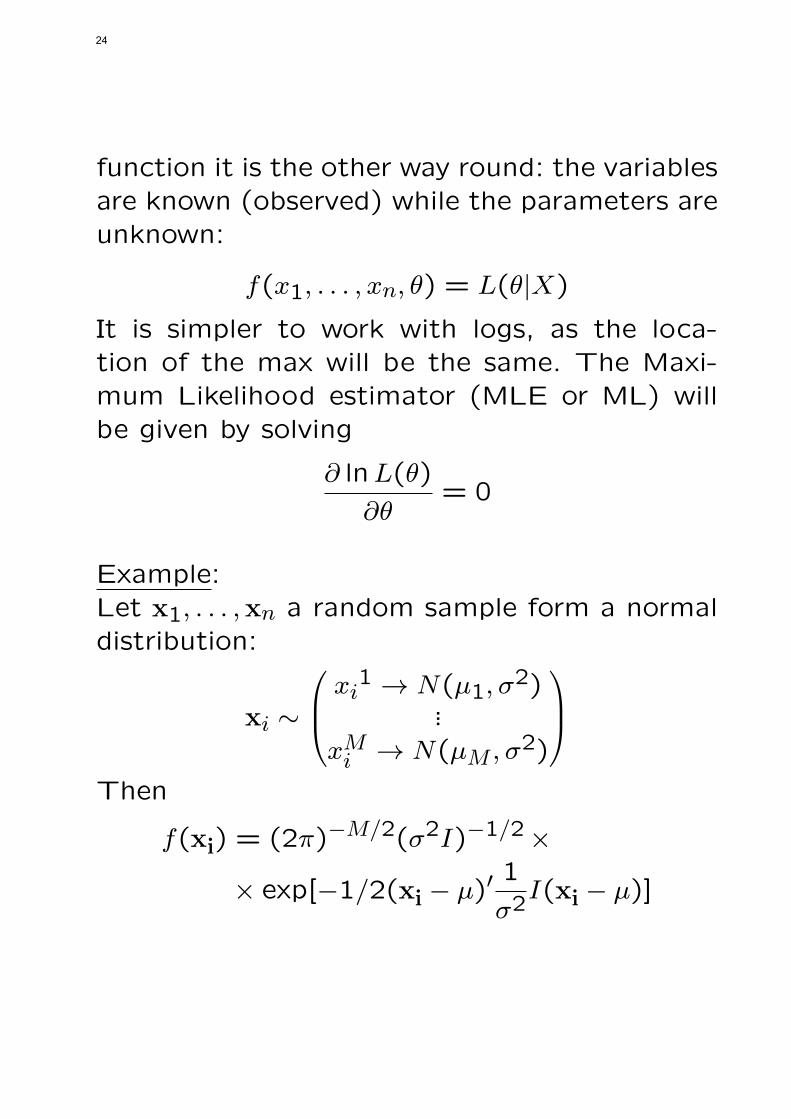

function it is the other way round: the variablesare known (observed) while the parameters areunknown:

f(x1, . . . , xn, θ) = L(θ|X)

It is simpler to work with logs, as the loca-tion of the max will be the same. The Maxi-mum Likelihood estimator (MLE or ML) willbe given by solving

∂ lnL(θ)

∂θ= 0

Example:Let x1, . . . ,xn a random sample form a normaldistribution:

xi ∼

xi1 → N(µ1, σ

2)...

xMi → N(µM , σ2)

Then

f(xi) = (2π)−M/2(σ2I)−1/2×

× exp[−1/2(xi − µ)′1

σ2I(xi − µ)]

24

Now taking the logs and summing over the

sample gives

lnL = −nM

2ln(2π)−

nM

2lnσ2−

−1

2σ2∑i

(xi − µ)′(xi − µ)

For the MLE

∂ lnL

∂µ=

1

σ2

∑i

(xi − µ)

∂ lnL

∂σ2= −

nM

2σ2+

1

2σ4∑i

(xi − µ)′(xi − µ)

Solving these equations gives:

µMLE,m = xm =1

n

∑i

xi,m

σ2 =

∑i∑

m(xim − xm)2

nM

ML estimation of the linear regressionmodel

25

y = Xβ + u

L(β, σ2|y, X) → L(β, σ2) → L

= (2πσ2)−n/2 exp[−(y −Xβ)′(y −Xβ)/2σ2]

The log-likelihood is

lnL = −n/2 ln(2π)− (n/2) lnσ2

− (y −Xβ)′(y −Xβ)/2σ2

To maximise it:

∂L

∂β=

1

σ2X ′(y −Xβ) = 0

∂L

∂σ2= −

n

2σ2+

(y −Xβ)′(y −Xβ)

2σ4= 0

Solving this gives

βML = (X ′X)−1X ′y

σ2ML = (y −XβML)′(y −XβML)/n

In most of the cases maximising the likelihooddoes not give a closed analytical form. Often tocarry out the max one needs numerical tools.

26

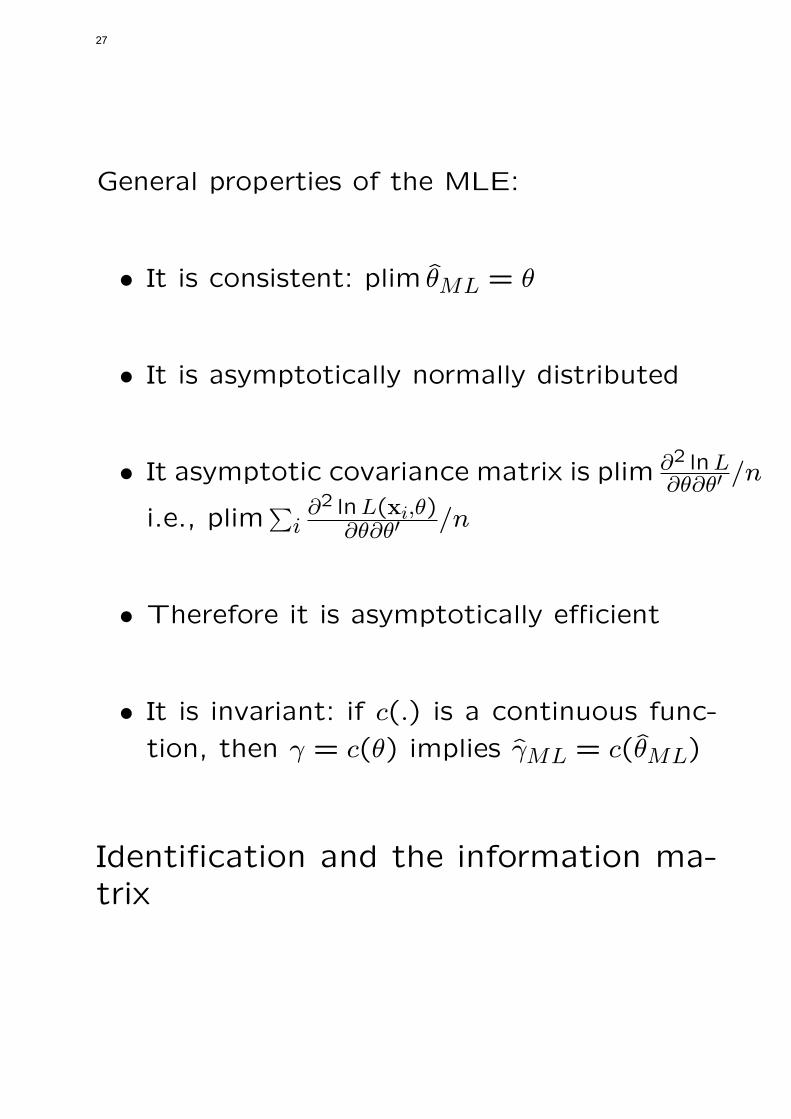

General properties of the MLE:

• It is consistent: plim θML = θ

• It is asymptotically normally distributed

• It asymptotic covariance matrix is plim ∂2 lnL∂θ∂θ′ /n

i.e., plim∑

i∂2 lnL(xi,θ)

∂θ∂θ′ /n

• Therefore it is asymptotically efficient

• It is invariant: if c(.) is a continuous func-

tion, then γ = c(θ) implies γML = c(θML)

Identification and the information ma-trix

27

Let θ0 a point of the information matrix I(θ).

Assuming that the distribution of y, f(y, θ) is

continuously differentiable in the parameter space,

similarly as it log, then θ0 is locally identified

only, and only if (iff) I(θ0) is non-singular.

Estimation of non-linear models

Assume we have a general non-linear model of

the form:

g(yi, θ) = h(xi, β) + ui (1)

where g(.) and h(.) are arbitrary non-linear func-

tions. Then the Non-linear Least Squares (NLLS)

estimator of this model is given by∑i

[g(yi, θ)− h(xi, β)]2 → min

To simplify a bit assume that the model is

yi = h(xi, β) + ui

28

Now the NLLS is given by∑i

[yi − h(xi, β)]2 → min

The first order condition now is

−2∑i

(yi − h(xi, β))∂h(xi, β)

∂β= 0

As far as the properties of the NLLS go, weonly have asymptotic results. For these, like inthe case of linear models (where we assumedthat plim(1/n)X ′X = Q positive definite ma-trix) here we have to assume that

plim1

n

∑i

[∂h(xi, β

0)

∂β0

] [∂h(xi, β

0)

∂β0

]′= Q

where β0 is the true parameter value and Q isa positive definite matrix. The problem is thatmany βNLLS satisfy the first order condition→ only local identification around the true pa-rameter value. Under the regularity conditionsseen previously

βNLLSa−→ N(β, σ2Q−1)

29

Let us now turn back to the MLE and model(1). Assuming that the ui disturbance termsare normally distributed, the Jacobian is

J(yi, θ) = Ji = abs

(det(

∂g(yi, θ)

∂yi)

)so the log-likelihood is

lnL = −n/2 ln(2π)− n/2 lnσ2 +∑i

ln J(yi, θ)−

−1

2σ2∑i

[g(yi, θ)− h(xi, β)]2

The first order conditions are

∂ lnL

∂β= 1/σ2

∑i

ui∂h(xi, β)

∂β= 0

∂ lnL

∂θ=∑i

1

Ji(∂Ji∂θ

)− 1/σ2∑i

ui∂g(yi, θ)

∂θ= 0

∂ lnL

∂σ2= −

n

2σ2+

1

2σ4∑i

u2i = 0

(2)

In general numerical procedures are required tosolve it and to maximise the likelihood func-tion.

30

Concentrated likelihood

Many problems can be formulated by parti-

tioning the parameter vector θ = [θ1θ2] such

that the maximisation problem for θ2,ML can

be written as a function of θ1,ML:

θ2,ML = f(θ1,ML)

Then the concentrate likelihood is

Lc((θ1, θ2) = Lc(θ1, f(θ1))

Example 1:

From (2)

σ2ML = 1/n∑i

[g(yiθML)− h(xiβML)]2

Substituting this back into the lnL gives

lnLc =∑i

ln J(yi, θ)− n/2(1 + ln(2π))

− n/2 ln[1/n∑i

u2i ]

31

This concentrated log-likelihood is only a func-

tion of θ and β but not of σ2.

Example 2:

Estimation of the first two moments of a nor-

mal population:

lnL(µ, σ2) = −n

2[ln(2π) + lnσ2]−

−1

2σ2∑i

(xi − µ)2 which gives

σ2ML =1

n

∑i

(xi − µML)2

Now putting this back into the log-likelihood

we get

lnLc = −n

2

1+ ln(2π) + ln[1

n

∑i

(xi − µML)2]

The solution now for µ now is x. We can also

concentrate the log-likelihood over µ instead

of σ2.

32

Topic : 4

Pseudo Maximum Likelihood andExtremum Estimation

33

Pseudo (Quasi) Maximum Likelihood

The Kullbac–Leibler index/measure of prox-

imity/discrepancy measures the similarity be-

tween two distributions/densities. Let p(y) and

π(y) be two probability distributions for the

random variable Y . The KL index is:

KL(p, π) = Ep[ln(p(y)/π(y))]

where Ep[.] denotes the expectation taken with

respect to the density p(y).

The closer KL(p, π) to zero the more similar is

p(y) to πy. KL= 0 iff p(y) = π(y). If Ep[.] does

not exist, we take KL= ∞.

Application of the KL

Let us have the density f(z, θ0) and any other

density f(z, θ). Then

KL = E0[ln f(z, θ0)]− E0[ln f(z, θ)]

34

This means that searching for the maximumof the log-likelihood is in fact searching for theminimum KL!

Now let us turn to the Pseudo (Quasi) ML.Let us assume that the true pdf behind ourmodel is p(y) but our estimation, the pseudolikelihood, is based on the π(y, θ) pdf θ ∈ Ω. Letθ∗ be the value (called pseudo-true value)thatminimises the KL p(y) relative to π(y, θ):

θ∗ = minθ∈Ω

[Ep(ln(p(y)/π(y, θ))]

and pseudo/quasi ML based on the π(y, θ)

θQML → maxθ∈Ω

[lnLQ(θ, y, x)]

θQML consistently estimates θ∗ and it can beshow easily that

θQMLA∼ N(0, h(θ∗)−1Σ∗h(θ∗)−1]

where

Σ∗ =1

n

(∂ lnLQ(θ, y,X)

∂θ|θ∗

)(∂ lnLQ(θ, y,X)

∂θ|θ∗

)

35

and

h(θ∗) =1

n

(∂2 lnLQ(...)

∂θ∂θ′

)The main question now is how far the pseudo-

true value θ∗ is from the true value θ0?

Let us consider the “usual” model

yi = h(x,β0) + ui

with no endogeneity. Then, under the usual

regularity conditions (to be seen later on):

Theorem

The Pseudo (Quasi) ML estimator is “fully”

consistent (i.e., it is a consistent estimator of

the true parameter value θ0) if the pseudo-

likelihood is based on the exponential family

of distributions:

f(x, θ) = exp [A(θ).B(x) + C(x) +D(θ)]

36

where A(.), B(.), C9.) and D(.) are real val-ued functions. Examples of such distributions:Normal, Gamma, Binomial, Poisson, Geomet-ric, etc....

Extremum Estimation (or M-estimation)

Any estimator that can be written in the form

θ = argmaxθ∈Ω[m(θ, y,X)]

where m(.) is the objective function is an Ex-tremum Estimator (EE) also called M-estimator.The properties of the EE depends on someregularity conditions.

Examples

ML → m(θ, y,X) = L(θ, y,X)

OLS → m(θ, yX) = (y −Xβ)′(y −Xβ)

Asymptotic Properties

37

Consistency

Intuition: The criterion function m(.) converges

to a non-stochastic function of θ that is max-

imised uniquely at the true parameter value θ0if the limit of the max of m(.) = the max of

the limit of m(.), then the max of the objective

function converges to the max of m0(θ) which

is θ0.

Two sufficient (but not necessary) conditions

for the consistency of the EE (plim θ = θ0):

Theorem 1

a) m(θ, y,X) converges uniformly in probabil-

ity to a function of θ, say m0(θ),

[m(, θ, ...)p−→ m0(θ)]

b) m0(θ) is continuous in θ

38

c) m0(θ) is uniquely maximised at θ

d) The parameter space Ω is compact (closed

and bounded)

Theorem 2

a)-c) a) and c) the same as above

b) m0(θ) is concave in θ

d) Ω is a convex set with θ0 inside

Asymptotic normality

Intuition: EE is an asymptotically linear func-

tion of a multivariate normal r.v. so it is itself

as. normally distributed.

39

Theorem 3: Conditions for the asymptotic nor-

mality

a) plim(θ) = θ0

b) θ0 is inside Ω

c) m(.) is twice continuously differentiable in

θ in the neighborhood (κ(θ0)) of θ0

d)

√n∂m(θ, y,X)

∂θ|θ0

d−→ N(0,Σ)

e)

limn→∞P

supθ∈κ(θ)

||∂2m(...)

∂θ∂θ′− h(θ)|| < ε

= 1

∀ε > 0

40

where h(θ) is a function and ||...|| is the Eu-

clidean distance from zero, if C is a matrix

→ [vec(C)′vec(C)]1/2

f) h(θ) is continuous and non-singular at θ0

Then√n(θ − θ0)

d−→ N(0, h(θ0)

−1Σh(θ0)−1)

Application

The ML estimator is consistent if

a) 1/n lnL(θ) converges uniformly in proba-

bility to L0(θ)

b) L0(θ) is continuous in θ

c) L0(θ) is uniquely maximised at θ0

41

d) Ω is compact

The ML estimator has an asymptotic normal

distribution if

a) θp−→ θ0

b) θ0 is inside Ω

c) 1/n lnL(θ) is twice differentiable

d)

(1/√n)

∂ lnL(...)

∂θ|θ0

d−→ N(0,Σ)

e)

1/n∂2 lnL(...)

∂θ∂θ′

42

converges in probability to h(θ)

f) The same as in Theorem 3

43

Topic : 6

Elements of Hypothesis Testing inEconometrics

44

Hypothesis testing

Hypothesis testing is based on a test-function

(or test statistic) with known distribution un-

der the H0 hypothesis.

Type I error → when we reject the null hypoth-

esis when in fact it is true.

Type II error → when we do not reject the null

hypothesis when in fact it is not true.

Significance level of a test (1%,5%,10%) is

the probability of Type I error. This is also

called the size of the test.

The power of a test is 1− the probability of

Type II error: 1− Prob(Type II error).

Uniformly Most Powerful (UMP) test has greater

power than any other test of the same size for

all admissible values of the parameter(s).

Unbiased test: It has greater power than size

for all admissible parameter values (quite weak

45

requirement!). If a test is biased for some pa-

rameter values we are more likely to accept the

null when it is false than when it is true.

Consistent test: Power → 1 as n → ∞.

Some important types of tests

Simple/composite hypotheses: A hypothesis that

completely specifies the distribution of the r.v

Z (the test statistic) is called simple, otherwise

it is composite. Example → simple: H0 : θ = θ0;

composite H1 : θ = θ0.

Nested hypotheses: When the Ωθ parameter

space is made up of two disjoint subsets Ωθ0and Ωθ1 with Ωθ1 = Ωθ − Ωθ0 the H0 related

on Ωθ0 is nested in HA related to Ωθ.

When both the null and the alternative hy-

potheses are simple (e.g., H0 : θ = θ0 and

46

HA : θ = θ1 then the Neyman-Pearson theo-

rem guarantees the existence of a UMP test.

On the other hand, when the alternative is

composite there is a UMP test only iff the crit-

ical region is the same for each simple alter-

natives that make up HA. → This is a very

exceptional case, in practice does not happen.

Testing for parameter restrictions

Consider the ML estimation of the parame-

ter(s) θ and test

H0 : C(θ) = 0

where C(.) are a set of restrictions on the pa-

rameter(s).

1. The Likelihood Ratio (LR) test

Intuition: If the restrictions C(θ) are valid

(true) in the sample, imposing them for

47

the estimation should not lead to a large

change in the log-likelihood. → (lnL−lnLR),

where lnLR is the likelihood when imposing

the restrictions and lnL is the unrestricted

one, should be small.

2. The Wald test

Intuition: If the restrictions C(θ) are valid

(true) in the sample, C(θML should be close

to zero (asymptotically), since the MLE is

consistent. The null hypothesis of restric-

tions is rejected if C(θML) is significantly

different from zero.

3. The Lagrange multiplier (LM) test

Intuition: If the restrictions C(θ) are valid

(true) in the sample, the restricted estima-

tor should be close to the point that max-

imises the log-likelihood → The slope of L

should be 0 at θR.

48

1. The LR test:

λ =L(θ)RL(θ)

0 < λ < 1

If λ is too small the restriction are probably not

true. Under the usual regularity conditions

−2 lnλA∼ χ2

with DF equal to the number of restrictions.

2. The Wald test.

To deal with this we need a technical detour!

Full rank quadratic form. If

u ∼ N(µ,Σ)

then

Σ−1/2(u− µ) ∼ N(0, I)

and

(u− µ)′Σ−1(u− µ) ∼ χ2(n)

Now if the H0 hypothesis that E(u) = µ is true,

this will have a χ2 distribution, if false the form

49

will likely to be large.

Let us go now back to the Wald test and the

θ be the unrestricted parameter estimate.

H0 : C(θ) = q

If true (C(θ)− q) should be close to zero.

W =[(C(θ)− q)′(V ar(C(θ − q))−1(C(θ)− q)

]A∼ χ2

if the null is true, with DF equal to the number

of restrictions, i.e., the number of equations in

(C(θ)− q))

Let us have a small detour again!

if√n(θ − θ)

d−→ N(0, σ2)

and g(θ) is a continuous function then

g(θ)d−→ N

(g(θ),plim(

g′(θ)2σ2

n)

)

50

and so

√n(g(θ)− (g(θ)

) d−→ N(0,plim(g′(θ)2σ2)

)Now let us go back to the Wald test using

these results:

V ar(C(θ)− q) = C V ar(θ)C′; C = [∂C(θ)

∂θ′]

(3)

where in C the jth row is the derivative of the

jth constraint with respect to the kth parame-

ter (k = 1, . . . ,K). If the restrictions/constraints

are linear

H0 : (Rθ − q) = 0

then

W = [Rθ − q]′[RV ar(θ)R′]−1[Rθ − q]

where DF is the number of rows in R.

3. The LM test

51

The Lagrangian formulation:

maxθ

f(θ, . . . ) subject to

C1(θ) = 0...

CJ(θ) = 0

constraints is the same as

maxθ,λ

L∗(θ, λ) = f(θ) + λ′C(θ)

where L∗ is the Lagrangian and has a ∗ in ordernot to confused with the likelihood. First orderconditions are

∂L∗

∂θ=

∂f(θ)

∂θ+

∂λ′C(θ)

∂θ= 0

∂L∗

∂λ= C(θ) = 0 with

∂λ′C(θ)

∂θ= λ′C = C′λ

with C defined in (3). If the restriction aretrue/valid imposing them will have little effecton the estimation so λ is going to be small:

H0 : λ = 0

52

We know that

∂ lnL(θR)

∂θR≈ 0

I.e., the derivatives of the log-likelihood evalu-

ated at the restricted parameters will be ≈ 0.

This is also called the score test as

∂ lnL(θ)

∂θ

is the score. So similarly to the case of the

Wald test, the test statistic now is

LM =

(∂ lnL(θR)

∂θR

)′[I(θR)]

−1(∂ lnL(θR)

∂θR

)A∼ χ2

with DF equal to the number of restrictions.(The

variance of the first derivative vector here is the

Information matrix!)

In finite samples:

W ≥ LR ≥ LM

53

Asymptotically:

W = LR = LM

EXAMPLE 1

Let be a random sample x1, . . . , xn from a nor-

mal distribution with 1st moment µ and σ2 =

4. The H0 : µ = 2. For the LR test

maxLR =(1/2√2π)n exp[−1/8

∑i

(xi − 2)2] = LR

maxL =(1/2√2π)n exp[−1/8

∑i

(xi − x)2] = L

λ = exp[−1/8∑i

(xi − 2)2 +1/8∑i

(xi − x)2] =

= exp[−n/8(x− 2)2 so

LR = −2 lnλ =(x− 2)2

4/n∼ χ2(1) under H0

54

Now turning to the Wald test

W = (µML − 2)′V ar(µML)(µML − 2) with

V ar(µML) = E(∂2 lnL(µ)

∂µ2) = (

n

4) so

W = (x− 2)2(n

4)

And finally the LM (score) test. The score nowis

s(µ) =∂ lnL(µ)

∂µ=

=

∑i(xi − µ)

4= n

(x− µ)

4so under H0

s(2) =n(x− µ)

4and the LM

LM =n2(x− 2)2

16

4

n=

n(x− 2)2

4

EXAMPLE 2The same as above, but now the sample is

55

from a N(µ, σ2) distribution.

LR = N2 ln

∑i(xi − 2)2∑i(xi − x)2

W =N2(x− 2)2∑

i(xi − x)2

LM =N2(x− 2)2∑

i(xi − 2)2

56

Topic : 7

Instrumental Variables Estimation

57

IV estimation

The consistency of the LS methods rely on

plim1

TX ′u = 0 (4)

i.e., that all explanatory variables are indepen-

dent from (orthogonal to) the disturbance terms.

This condition cannot directly be verified as

by construction uLS residual is always uncorre-

lated with u → LS will not provide evidence of

the inconsistency. When this condition is not

satisfied, we talk about endogeneity.

Examples

Examples when this (4) condition is not satis-

fied.

1. Simple measurement error.

Let us have the simple relationship

yt = β0 + β1xt + ut

58

but only

x∗i = xi + vi

is observed where vi is a white noise. So in fact

we estimate the model

yi = β0 + β1x∗i − β1vi + ui︸ ︷︷ ︸

u∗i

with u∗i being the new disturbance term. Clearly

now x∗ and u∗ are correlated as there is a neg-

ative correlation.

2. Autocorrelation in the disturbances and lagged

dependent variable(s) in the model.

Let us have the model

yt = β0 + β1xt + β2yt−1 + εt

with εt = ρεt−1 + vt, where vt is a white noise

and ρ < 1, β2 < 1. Then

E(xtεt) = 0 but now

E(yt−1εt) = 0

59

and even

plim(yt−1εt) = 0

3. SimultaneityLet us have a classical Keynesian consumptionfunction:

Ct = β0 + β1Yt + εt

where Ct and Yt are the per capita consumptionand income respectively. However

Yt = Ct + It

where It is the investment. Then clearly Yt andεt are correlated, regardless the sample size.

Let us assume that there is a matrix Z of size(T ×K∗) such that

plim1

TZ′u = 0

plim1

TZ′X = 0 = QZX and

plimZ′Z

T= QZ

60

where QZ is a positive definite matrix. I.e., theZ instrumental variables (IVs) are uncorrelatedwith the disturbance terms but are correlatedwith the explanatory variables. If these condi-tions are satisfied we say the IVs are admissible.Let us assume that K∗ = K, then if we trans-form the y = Xβ+u model (with K explanatoryvariables and T observations) like

Z′y = Z′Xβ + Z′u (5)

and estimate this model with OLS we get

βiv = (X ′ZZ′X)−1X ′ZZ′y

= (Z′X)−1(X ′Z)−1X ′ZZ′y

= (Z′X)−1Z′y

(6)

and

plim βiv = plim(Z′X

T)−1 plim(

1

TZ′(Xβ + u)) =

= β +plim(Z′X

T)−1(

Z′u

T) = β

and

βivA∼ N

(0, σ2Q−1

ZXQZQ−1ZX

)(7)

61

The number of IVs can be larger than the num-

ber of (stochastic) explanatory variables (that

need to be instrumented for). For the non-

stochastic explanatory variables the instruments

are themselves. (But the number of IVs must

be < T .) Next let us assume that K∗ > K.

Then the transformed model (5) should be es-

timated by GLS instead of OLS. This gives

βiv = [X ′Z(Z′Z)−1Z′X]−1[X ′Z(Z′Z)−1Z′]y(8)

When K∗ = K this gives back estimator (6).

The asymptotic covariance matrix of this es-

timator is also (7). When X and Z are not

strongly correlated the standard errors based

on (7) can be very large. → in this case we

talk about weak instruments.

For this estimator (8) in fact we minimise the

quadratic form

(y −Xβ)PZ(y −Xβ) where

PZ = Z(Z′Z)−1Z′

62

So far we have implicitly assumed that the dis-

turbance term of the untransformed model u

has a scalar covariance matrix, i.e., E(uu′) =

σ2I. When this is not the case and E(uu′) = Ω

the covariance matrix of model (5) is (Z′ΩZ).

Therefore the GLS estimator becomes

βiv = [X ′Z(Z′ΩZ)−1Z′X]−1×× [X ′Z(Z′ΩZ)−1Z′]y

with asymptotic covariance matrix

σ2

Q−1ZX plim(

Z′ΩZ

T

−1

)Q−1ZX

If K∗ = K this gives back (6). Now let us look

at another type of IV estimator. Let us call it

“GLS analog” IV. We know that a covariance

matrix Ω can be decomposed as

P ∗ΩP ∗ = IT and P ∗′P ∗ = Ω−1

First let us transform the model as

P ∗y = P ∗Xβ + P ∗u︸ ︷︷ ︸Scalar cov.matrix

63

So if we transform with P ∗ the instruments as

well and then instrument this model we get

Z′P ∗′P ∗y = Z′P ∗′P ∗Xβ + Z′P ∗′P ∗u

Z′Ω−1y = Z′Ω−1Xβ + Z′Ω−1u leading to

βiv = [X ′Ω−1Z(Z′Ω−1Z)−1Z′Ω−1X]−1×× [X ′Ω−1Z(Z′Ω−1Z)−1Z′Ω−1]y

Why is this “GLS analog”? Because if we have

K∗ = K we get back a GLS type estimator:

βiv = (Z′Ω−1X)−1Z′Ω−1y

The orthogonality condition needed for consis-

tency is

plim1

TZ′Ω−1u = 0

Non-linear IVLet be the general non-linear model

yi = g(xi, β) + ϵi

64

and

vi(xi, β) = y − g(xi, β) or v(x, β) = y − g(x, β)

The

plimZ′v(x, β) = 0

orthogonality must hold for Z to be a valid set

of IVs. Z must also be correlated with v0(β0)

the Jacobian of v(x, β). Then the appropriate

non-linear IV is obtained by

(Z′v(β))′(Z′Z

T)−1(Z′v(β)) → min

which usually has no closed form.

65

Topic : 8

Generalised Method of MomentsEstimation – GMM

66

GMM estimation

One of the most important tasks in econo-

metrics and statistics is to find techniques en-

abling us to estimate, for a given data set,

the unknown parameters of a specific model.

Estimation procedures based on the minimi-

sation (or maximisation) of some kind of cri-

terium function (EE or M–estimators) have

successfully been used for many different types

of models. The main difference between these

estimators lies in what must be specified of

the model. The most widely applied such esti-

mation, the maximum likelihood, requires the

complete specification of the model and its

probability distribution. The Generalised Method

of Moments (GMM) does not require this sort

of full knowledge. It only demands the speci-

fication of a set of moment conditions which

the model should satisfy.

67

Let us start with the Method of Moments (MM)

estimation.

The Method of Moments – MM

The Method of Moments is an estimation tech-

nique which suggests that the unknown param-

eters should be estimated by matching popula-

tion (or theoretical) moments (which are func-

tions of the unknown parameters) with the ap-

propriate sample moments. The first step is to

properly define the moment conditions.

Moment Conditions

Assume that we have a sample xt : t = 1, . . . , Tfrom which we want to estimate an unknown

p×1 parameter vector θ with true value θ0. Let

f(xt, θ) be a continuous q × 1 vector function

68

of θ, and let E(f(xt, θ)

)exist and be finite for

all t and θ. Then the moment conditions are

E(f(xt, θ0)

)= 0

ExampleConsider the linear regression model

yt = x′tβ0 + ut,

where xt is a p× 1 vector of stochastic regres-sors, β0 is the true value of a p × 1 vector ofunknown parameters β, and ut is an error term.In the presence of stochastic regressors, we of-ten specify

E(ut|xt) = 0,

so that

E(yt|xt) = x′tβ0.

Using the Law of Iterated Expectations we find

E(xtut) = E

(E(xtut|xt)

)= E

(xtE(ut|xt)

)= 0

69

The equations

E(xtut) = E

(xt(yt − x′tβ0)

)= 0,

are moment conditions for this model. That is,θ = β and f

((xt, yt), θ

)= xt(yt − x′tβ).

Notice that in this example E(xtut) = 0 con-sists of p equations since xt is a p × 1 vector.Since β is a p × 1 parameter, these momentconditions exactly identify β. If we had fewerthan p moment conditions, then we could notidentify β, and if we had more than p momentconditions, then β would be over–identified.Estimation is feasible if the parameter vectoris exactly or over–identified.Compared to the maximum likelihood approach(ML), we have specified relatively little infor-mation about ut. Using ML, we would be re-quired to give the distribution of ut, as wellas parameterising any autocorrelation and het-eroskedasticity, while this information is not re-quired in formulating the moment conditions.

70

The MM estimation

Consider first the case when q = p, that is,

where θ is exactly identified by the moment

conditions. Then the moment conditions

E(f(xt, θ)

)= 0

represent a set of p equations for p unknowns.

Solving these equations would give the value of

θ which satisfies the moment conditions, and

this would be the true value θ0. However, we

cannot observe E(f(., .)

), only f(xt, θ). The ob-

vious way to proceed is to define the sample

moments of f(xt, θ)

fT (θ) = T−1T∑

t=1

f(xt, θ),

which is the Method of Moments (MM) esti-

mator of E(f(xt, θ)

).

Example 1

For the linear regression model, the sample

71

moment conditions are

T−1T∑

t=1

xtut = T−1T∑

t=1

xt(yt − x′tβT ) = 0,

and solving for βT gives

β =

T∑t=1

xtx′t

−1 T∑t=1

xtyt = (X ′X)−1X ′y.

That is, OLS is an MM estimator.

Example 2

The linear regression with q = p instrumental

variables is also exactly identified. The sample

moment conditions are

T−1T∑

t=1

ztut = T−1T∑

t=1

zt(yt − x′tβT ) = 0,

and solving for β gives

β =

T∑t=1

ztx′t

−1 T∑t=1

ztyt = (Z′X)−1Z′y,

72

which is the standard IV estimator.

Example 3

The Maximum Likelihood estimator can be given

an MM interpretation. If the log–likelihood for

a single observation is denoted l(θ|xt), then the

sample log–likelihood is T−1∑Tt=1 l(θ|xt). The

first order conditions for the maximisation of

the log–likelihood function are then

T−1T∑

t=1

∂l(θ|xt)∂θ

|θ=θT

= 0.

These first order conditions can be regarded

as a set of moment conditions.

The GMM

The GMM estimator is used when the θ param-

eters are over–identified by the moment condi-

tions, i.e., there are more moment conditions

73

than unknown parameters. Now, unlike in the

case of the MM, we can not find a vector θ

that satisfies fT (θ) = 0. Instead, we will find

the vector θ that makes fT (θ) as close to zero

as possible. This can be done by defining

θGMM = argminθQT (θ)

where

QT (θ) = fT (θ)′ATfT (θ), (9)

and AT is a stochastic positive definite Op(1)

weighting matrix (whose role will be discussed

later). Note that QT (θ) ≥ 0 and QT (θ) = 0

only if fT (θ) = 0. Thus, QT (θ) can be made

exactly zero in the just identified case, but is

strictly positive in the over–identified case.

Example

For the linear regression model with q > p validinstruments, the moment conditions are

E(ztut) = E

(zt(yt − x′tβ0)

)= 0,

74

and the sample moments are

fT (β) = T−1T∑

t=1

zt(yt−x′tβ) = T−1(Z′y−Z′Xβ).

Suppose we choose

AT =

T−1T∑

t=1

ztz′t

−1

= T (Z′Z)−1,

and assume we have a weak law of large num-

bers for ztz′t so that T−1Z′Z converges in prob-

ability to a constant matrix A. Then the crite-

rion function is

QT (β) = T−1(Z′y−Z′Xβ)′(Z′Z)−1(Z′y−Z′Xβ).

Differentiating with respect to β gives

∂QT (β)

∂β= T−12X ′Z(Z′Z)−1(Z′y − Z′Xβ) = 0.

Setting this derivative to zero and solving for

βT gives

βT =(X ′Z(Z′Z)−1Z′X

)−1X ′Z(Z′Z)−1Z′y.

75

This is the standard IV estimator for the case

where there are more instruments than regres-

sors.

Properties of the GMM

The GMM is a EE estimator → it is consistent

and has an asymptotic normal distribution.

Let us assume that plimAT = AT a non-random

positive definite matrix. Also let

FT (θ) =∂fT (θ)

∂θ′

where

∂fT (θ)

∂θ′=

1

T

∑t

∂f(xt, θ)

∂θ′

Further, also assume that for any sequence

plim θT = θ0

there is

plimFT (θ) = FT

76

where FT is a sequence of matrices that do notdepend on θ. And finally, let

plimV arfT (θ0) = VT

Since θ0 is unknown, this can consistently beestimated by

plim V arft(θGMM) = VT

TheoremUsing the EE results, the covariance matrixof the GMM estimator for a given AT weightmatrix and given moment conditions is

(F ′T AT FT )

−1F ′T AT VT AT FT (F

′T AT FT )

−1

The optimal choice of AT → V −1T so the opti-

mal GMM is a two-step procedure: in the firststep estimate θ with GMM and AT = IT andthen get V −1

T . Using this as a weight matrixresults in the optimal GMM estimator. The co-variance matrix for this is then

(F ′T V

−1T FT )

−1

77

.

Testing for over-identifying restrictions

This is in fact specification testing.

The idea: Divide the restrictions (for “historic”

reasons we talk usually here of “restrictions”

while in fact we mean moment or orthogonality

conditions) into two groups: identifying restric-

tion and over-identifying restrictions. Estimate

the unknown parameters using the identifying

restriction and then test whether the estimated

parameters satisfy the over-identifying ones. If

so the identification is regarded as correct.

Assume that θT is the estimated parameter ob-

tained using GMM and the identifying restric-

tions. Then the test statistic

JT = QT (θT )A∼ χ2

q−p

78

where QT is (9), q is the number of over-identifying restrictions and p is the number ofparameters.

A special case of this test is the Hausman spec-ification test:

H0 : ML and E(f(xt, θ0)) = 0 are correct

HA : only E(f(xt, θ0)) = 0 is correct

Then the test statistic is

HT = (θT,ML − θT,GMM)′(VT,ML − VT,GMM)−1 .

. (θT,ML − θT,GMM)A∼ χ2

p

where V are consistent estimator of the respec-tive covariance matrices. In the original Haus-man paper the OLS and IV estimation werecompared → with the null that both the OLSand IV are consistent so there is no measure-ment error.

Let us have a look at another version of thetesting for over ident. restrictions called con-ditional moment test.

79

Let us have a model estimated by ML. Theconditional density of the explanatory variableXt, given the sample is pt(xt, θ0) and E[Lt(θ0)] =0 where now

Lt(θ0) =∂ ln(pt(xt, θ0))

∂θ

which (as seen in earlier lectures) are the or-thogonality conditions on which the ML is based.Now assume that if the model is correctly spec-ified, the data also satisfy the (q × 1) momentconditions E[f(xt, θ0)] = 0. So we would liketo test the null hypothesis

H0 : E[f(xt, θ0)] = 0

The test statistic now is

CMT =1

T

∑t

h(θT,ML)′V −1

T ×

× h(θT,ML)A∼ χ2

q

where

ht(θ) = [f(xt, θ)′, Ft(θ)

′]′

and VT is a consistent estimator of lim V ar(ht(θ0)).

80

Topic : 9

Biased Estimation

81

Biased estimation

A good estimator → likely to be in a small

neighbourhood of the true parameter value with

high probability. A biased estimator therefore

may be better than an unbiased one as the

smaller 2nd moment may “compensate” for

the inaccuracy caused by the bias.

Definition: Loss function: A function of the un-

known parameters of the model, their estima-

tor(s) and other parameters which expresses

the difference between the parameter estimates

and the true parameter values. → Reflects the

loss caused by the imprecision of an estimator.

Definition: Risk function: The expected value

of the Loss function (expected loss) → this in

fact measure the “goodness” of an estimator,

the smaller the risk the better.

82

Example: Weighted quadratic loss

L(β, β) = (β − β)′W (β − β)

if W = I we talk about squared error loss. Let

us have the “usual” linear model and we are

looking for an estimator of the form β = Ay

with the smallest risk.

minβ

E[(β − β)′(β − β)] = σ2tr(A′A)+

β′(AX − I)′(AX − I)β

which of course gives A = (X ′X)−1X.

The most straightforward way to improve on

any estimation is to use additional information.

The simplest way is to include in the estimation

process some parameter restrictions:

Rβ = r

where R is a known matrix of size (J×K), r is

a known vector of size (J ×1) both containing

83

the prior information, with J the number of

restrictions. So we want to estimate the model

y = Xβ+u under the restrictions Rβ = r which

will result in the called Restricted estimator:

minβ

(y−XβRLS)′(y−XβRLS) subject to Rβ = r

Using the Lagrangian formulation

L∗ = (y −XβRLS)′(y −XβRLS)− 2λ′(Rβ − r)

∂L∗

∂β= −2X ′(y −Xβ)− 2R′λ = 0

∂L∗

∂λ= 2(RβRLS − r) = 0

which gives

βRLS = βOLS + (X ′X)−1R′λ

Solving this for λ → pre-multiply by R and

Rβ = r is satisfied:

RβRLS = RβOLS +R(X ′X)−1R′λ = r

λ = −[R(X ′X)−1R′]−1[RβOLS − r]

84

That is

βRLS = βOLS + (X ′X)−1R[R(X ′X)−1R′]−1××(r −RβOLS)

Now about its properties. The 1st moment is

E(βRLS) = β + (X ′X)−1X ′u+

+ (X ′X)−1R[R(X ′X)−1R′]−1×× [r −R(X ′X)−1X ′Xβ +R(X ′X)−1X ′u]

= β +(I − (X ′X)−1R′[R(X ′X)−1R′]−1R

)×

× (X ′X)−1X ′u

This means that the estimator is unbiased onlyif RβRLS = r, i.e., the restrictions are true/correctin the sample. Then RβOLS = r and βRLS =βOLS.Let us turn now to the 2nd moment

E[(βRLS − β)(βRLS − β)′] =(I − (X ′X)−1R′[R(X ′X)−1R′]−1R

)(X ′X)−1X ′u︸ ︷︷ ︸

A

A′

= σ2(X ′X)−1××(I −R′[R(X ′X)−1R′]−1R(X ′X)−1

)

85

It can be shown that thew difference between

the covariance matrix of the OLS estimator

σ2(X ′X)−1 and the of the RLS is positive semi-

definite. This means that the variance of the

RLS is less than equal to the variance of the

OLS. When the restrictions are true/correct in

the sample the RLS is BLUE, consistent and

asymptotically efficient, using the information

in the sample and the restrictions.

The next question is what is going to hap-

pen when the restrictions are not true/correct,

Rβ − r = 0, Rβ − r = δ?! Obviously RLS → bi-

ased.

Intuition: If the restrictions are “somewhat”

not correct, although the RLS is biased, we

still may be better of using it, as the smaller

bias may “compensate” for this. So the valid-

ity of the restriction should be tested in the

sample.

86

The pretest estimator

We are testing the null hypothesis: H0 : Rβ =

r. The test statistic

µ =1

Jσ2[(RβOLS−r)′(R(X ′X)−1R′)(RβOLS−r)]

(10)

has an F distribution under the null with DF

(J, T−K) and a non-central F distribution with

the same DF and

λ =1

2σ2δ′[R(X ′X)−1R′]−1δ

non-centrality parameter under HA. Using this

we can define the pretest estimator which is

the RLS estimator if H0 is accepted and the

OLS if not using (10):

βpt =

βRLS if H0 accepted

βOLS if H0 rejected

This is a two-steps procedure. In the 1st step

we (pre-)test the restrictions with OLS and

87

(10) and in the 2nd step, depending on the

outcome, the RLS or OLS is applied for infer-

ence.

1. If δ = 0 the pretest estimator is unbiased.

2. The risk of the pretest estimator, based on

the weighted quadratic loss, is smaller that the

risk of the OLS and is a decreasing function

of the critical value of the test (10).

3.With the increase of δ the risk of the pretest

estimator increases, but after reaching its max-

imum (which is higher that that of the OLS)

it decreases to the level of the OLS.

Stochastic restrictions

Assume now that our prior information, i.e.,

our restrictions are not deterministic, but stochas-

tic:

r = Rβ + v

where v is a vector of random variables, E(v) =

0 and E(vv′) = Ψ. Taking our usual linear

88

model with E(uu′) = Σ we have(yr

)=

(XR

)β +

(uv

)Then the so called mixed estimator of the model

is

βmx =

(X ′R′)

(Σ 00 Ψ

)−1(XR

)−1

×

×

(X ′R′)

(Σ 00 Ψ

)−1(yr

)or

βmx = (X ′Σ−1X+R′Ψ−1R)−1(X ′Σ−1y+R′Ψ−1r)

with a covariance matrix

(X ′Σ−1X +R′Ψ−1R)−1

1. If the restriction are correct and Σ and Ψ

are known has the same properties as the GLS

but it is more efficient as it uses more infor-

mation.

2. If the restriction are correct but Σ and Ψ are

89

unknown, if we have consistent estimators of

them, by using them the mx estimator is going

to have the same properties as the FGLS but

it is going to be asymptotically more efficient.

3. If the variance of v → 0, i.e., the prior infor-

mation becomes deterministic, the mixed esti-

mator approaches the restricted one.

4. If the variance of v → ∞, i.e., the prior in-

formation becomes diffuse or non-informative

the mixed estimator approaches the OLS.

The pretest estimator related to stochastic re-

strictions is testing H0 : E(r − Rβ) = δ = 0

with

µ =1

σ2[(r −RβOLS)

′(R(X ′X)−1R′ +Ψ)−1×

× (r −RβOLS)]

which has a χ2(J) under the null. If the vari-

ances are estimated we end up with an F dis-

tribution.

90

Topic : 10

Some Non-linear Models

91

Non-Nested model selection

Non-nested model selection most frequently is

base on information criteria.

To start with, let us remind ourselves the KL

measure, see when we dealt with the Pseudo

ML: The Kullback–Leibler index/measure of

proximity or discrepancy measures the simi-

larity between two distributions/densities. Let

g(y) and f(y, θ) be two probability distributions

for the random variable Y . The KL index is:

KL(g(.), f(.)) =∫yg(y) ln

g(y)

f(y, θ)d y =

= Eg[ln(g(y)/f(y, θ))] =

=∫yg(y) ln(g(y))d y︸ ︷︷ ︸

A

−∫yg(y) ln f(y, θ)d y︸ ︷︷ ︸

B

where Eg[.] denotes the expectation taken with

respect to the density g(y), which is the true

unknown distribution of y. f(y, θ) is the para-

metric distribution of the model, θ is the ML

92

estimate of the unknown parameters. The smaller

KL the closer the model is to the true distri-

bution. Task → find an f(y, θ) that min KL

→ minf B, as A is a constant from the view

point of this operation. Unfortunately this is

not possible as g(y) is unknown.

Different information criteria are drawn by “es-

timating” this B.

1.

B = −2 ln

L(y,θ)︷ ︸︸ ︷f(y, θ)+2j

where j is the size of θ. This is the so called

Akaike Information Criteria – AIC.

Model selection → calculate the AIC for all rel-

evant model alternatives and pick the model

with the smallest AIC

2. In many application the above B is consid-

ered “biased”. So there are alternatives, mostly

by using different “penalties” on the likelihood:

B = −Ln(y, θ) +j

2lnn

93

which is the Bayesian (Schwartz) Information

criteria or BIC.

Binary choice models – a quick reminder

y =

1 Prob(y = 1) = f(β′x)

0 Prob(y = 0) = 1− f(β′x)

Linear probability model: f(β′x) = β′x:1. No linear model would generate such depen-

dent variable.

2. Can yield negative probabilities, β′x may not

be in (01).

3. There is heteroscedasticity → V ar(u) = β′x(1−β′x).So why so people still use it? Because in a

non-linear model

∂E(y)

∂x= f ′(β′x)β

not the marginal effect we are used to → it

varies with x, which can be inconvenient in

some applications.

94

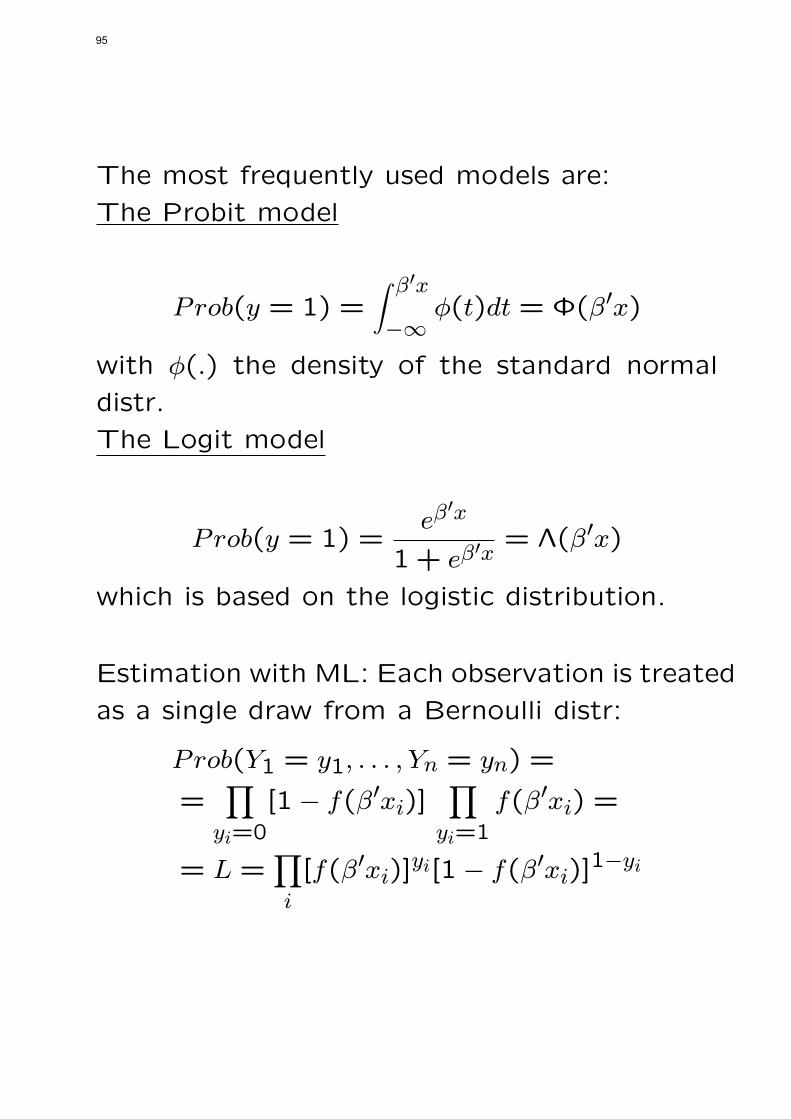

The most frequently used models are:

The Probit model

Prob(y = 1) =∫ β′x

−∞ϕ(t)dt = Φ(β′x)

with ϕ(.) the density of the standard normal

distr.

The Logit model

Prob(y = 1) =eβ

′x

1+ eβ′x

= Λ(β′x)

which is based on the logistic distribution.

Estimation with ML: Each observation is treated

as a single draw from a Bernoulli distr:

Prob(Y1 = y1, . . . , Yn = yn) =

=∏

yi=0

[1− f(β′xi)]∏

yi=1

f(β′xi) =

= L =∏i

[f(β′xi)]yi[1− f(β′xi)]

1−yi

95

Multiple choice modelsLet Yi a random variable indicating the choiceof the ith consumer in a choice set j. For exam-ple the choice of individual i between transportmodes j = 1, . . . , J. We are interested in

Prob(Yi = j|xij)where xij is a (1 × K) vector, e.g., the com-mute time of i over transport choice j, theprice, etc. To get a “real” model some dis-tributional assumptions are needed. Often theWeibull assumption is made:

F (ϵij) = exp[e−ϵij]

Prob(Yi = j) =eβ

′xij∑j e

β′xij

This is called the Conditional Logit Model.Next, assume that we are modelling occupa-tional choice:

y =

1 1st wage category

2 ......

J

or

0

1...

J

96

This type of problem is dealt with the Multi-

nomial logit model: Assuming again a Weibull

distribution

Prob(Yi = j) =eβ′jxi

J∑k=0

eβ′kxi

To make the model identified some some re-

strictions on the βs are needed, like β0 = 0.

Then

Prob(Yi = j) =eβ′jxi

1+J∑

k=1eβ

′kxi

j = 1, . . . , J

and

Prob(Yi = 0) =1

1+J∑

k=1eβ

′kxi

97

The log-likelihood now is

ln∑i

J∑j=0

dijProb(Yi = j)

dij

1 if i choses j

0 otherwise

When normalized at β0 = 0 the jth log-odd

ratio is

ln

[Pij

Pi0

]= β′

jxi

when we normalize on any other parameter

(say the k-th)

ln

[Pij

Pik

]= x′i(β

′j − βk)

The odds ratios do not depend on the other

choices (what the others have chosen). This is

called the Independence of Irrelevant Alterna-

tives.

98

Ordered multiple choice models

The model again is y∗ = β′x+ ϵ, but y∗ is not

observed, instead we observe, for example,

y = 0 if y∗ ≤ 0

y = 1 if 0 < y∗ ≤ µ1...

y = J if µJ−1 ≤ y∗

where the µ-s can be known or unknown! Es-

timation → standard ML!

Let us make now a technical detour! Condi-

tional distribution.

When r.v X and Y are a bivariate normal dis-

tribution, the have the following joint density

f(x, y) =1

2πσxσy

exp[−

1

2(1− ρ2)[(x− µx

σx)2 + (

y − µy

σy)2

− 2ρ(x− µx

σx)(

y − µy

σy)]]

99

where ρ is the correlation between X and Y .

This joint density can be re-written as

f(x, y) = f(y|x)︸ ︷︷ ︸conditional

.

marginal︷ ︸︸ ︷f1(x) =

=1

√2πσy

√1− ρ2

exp[−

1

2σ2y(1− ρ2)

[y − µy − ρσy

σx(x− µx)]

2]×

×1√2πσx

exp[−1

2σ2y(x− µx)

2]

Let us next turn to the conditional moments.

The conditional 1st moment is

E(y|x) =∫yyf(y|x)dy

when y is continuous and

E(y|x) =∑y

yf(y|x)

when y is discrete. the conditional variance now

100

is

V ar(y|x) = E[(y − E(y|x))2|x]

=∫y(y − E(y|x))2f(y|x)dy or∑

y(y − E(y|x))2f(y|x)

The actual computation can be simplified by

using

V ar(y|x) = E(y2|x)− (E(y|x))2

and the Law of Iterated Expectations

E(y) = Ex(E(y|x))

where Ex(.) indicates the expectations wrt the

values of x. In the above bivariate normal case

E(Y |X) = µy + ρσy

σx(x− µx)

V (Y |X) = σ2y(1− ρ2)

and similarly for f(x, y) = f(x|y)f2(y).

Example: Uniform–Exponential mixture

101

f(y|x) =1

α+ βxexp[−

y

α+ βx]

y ≤ 0, 0 ≤ x ≤ 1

E(y|x) = α+ βx

if x is uniform (0,1) the f(x) = 1. f(x, y) =f(y|x)f(x) so

E(y) =∫ ∞

0

∫ 1

0y(

1

α+ βx).

. exp[−y

α+ βx]dx dy

So

E(y) = Ex(E(y|x))= E(α+ βx)

= α+ β E(x)︸ ︷︷ ︸1/2

= α+ β1/2

Now about the variance

V ar(y) = V arx(E(y|x)) + Ex(V ar(y|x))

102

So

V ar(y) = α(α+ β) +5β2

12

Truncation

For example: incomes over/below a given limit

are not observed, etc.

Definition: Truncated distribution: part of an

un-truncated distribution, above or below some

specific values.

Definition: Density of a truncated r.v.:

If continuous r.v. x has a pdf f(x) and a is a

constant

f(x|x > a) =f(x)

Prob(x > a)

which amounts to nothing more that scaling

the density so its∫= 1. (Truncated from above

→ the same.)

103

Example: Uniform x truncated at 1/3.

So x is U(01), f(x) = 1

f(x|x >1

3) =

f(x)

Prob(x > 13)

=123

,1

3< x ≤ 1

1st moment of a truncated r.v.

E(x|x > a) =∫ ∞

axf(x|x > a)dx

Example: Uniform distribution

E(x|x >1

3) =

∫ 1

1/3x(.)dx =

2

3

For the variance calculations are similar.

Truncation from below → increases mean

Truncation from above → decreases mean

Truncation → reduces variance.

104

Truncated normal distr:

Prob(x > a) = 1−Φ(a− µ

σ)

= 1−Φ(α)

f(x|x > a) =f(x)

1−Φ(α)

where Φ(.) is the normal cdf.

E(x|x > a) = µ+ σλ(α)

V ar(x|x > a) = σ2(1− δ(α))

with

λ(α) =ϕ(α)

1−Φ(α)if x > a

λ(α) = −ϕ(α)

Φ(α)if x < a

δ(α) = λ(α)(λ(α)− α) and

0 < δ(α) < 1 ∀αand λ(α) → inverse Mills ratio.

Truncated regression.

yi = β′xi + εi

105

εi ∼ N(0, σ2) →(yi|xi) ∼ N(β′xi, σ2). With a truncation point a

E(yi|yi > a) = β′xi + σ

λi︷ ︸︸ ︷λ(αi)

αi =a− β′xi

σV ar(yi|yi > a) = σ2(1− δ(αi))

LS estimation

(yi|yi > a) = β′xi + σλi + ui

where σλi is a function of x and if omitted →omitted variable bias; and ui is heteroscedastic:

V ar(ui) = σ2(1− λ2i + λiαi)

ML estimation

f(yi|yi > a) =1σϕ(yi − β′xi)/σ)

1−Φ(a− β′xi)/σ)

106

lnL = −n

2[ln(2π) + lnσ2]−

−1

2σ2∑i

(yi − β′xi)2−

−∑i

ln[1−Φ(a− β′xi

σ)] → max

Censoring

Let us have a continuous r.v y∗ and a new one

y transformed from the original as

y = 0 if y∗ ≤ 0

y = y∗ if y∗ > 0(11)

This is censoring at 0, but it can be at any

other value.

Lemma:

If y∗ ∼ N(µ, σ2) then

Prob(y = 0) = Prob(y∗ ≤ 0)

= 1−Φ(µ

σ)

and if y∗ > 0 y has the density of y∗. → mix-

ture of continuous and discrete distributions.

107

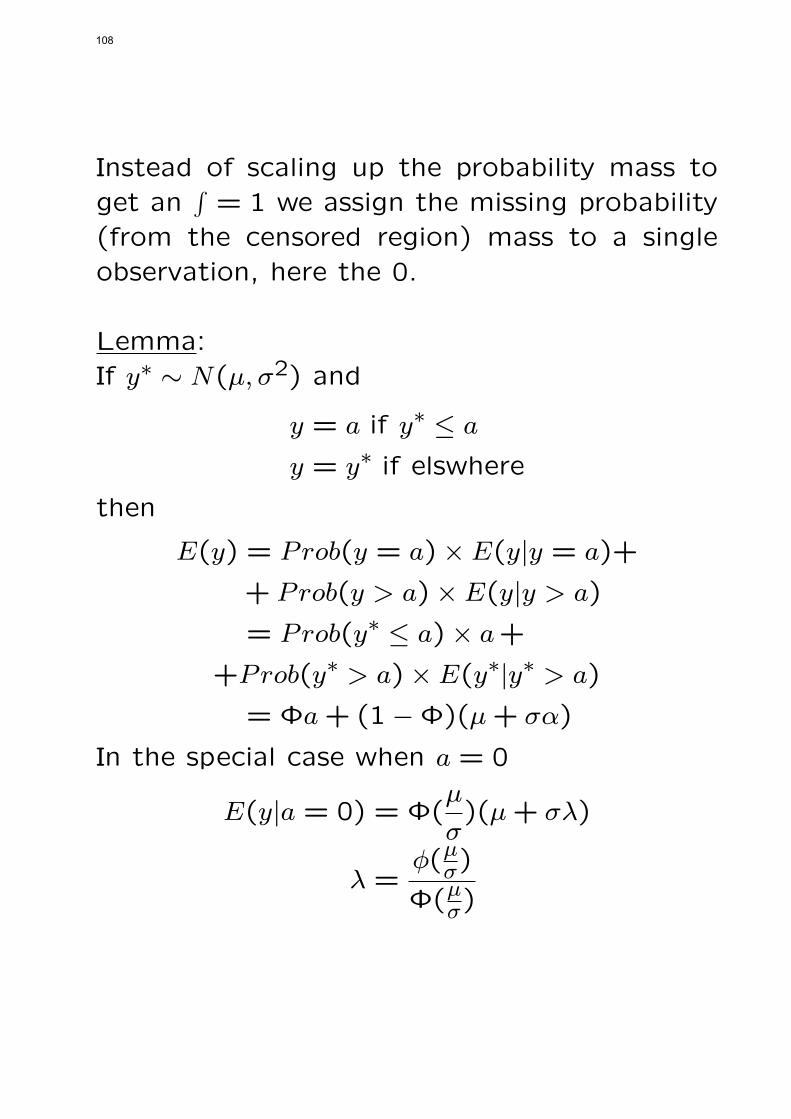

Instead of scaling up the probability mass toget an

∫= 1 we assign the missing probability

(from the censored region) mass to a singleobservation, here the 0.

Lemma:If y∗ ∼ N(µ, σ2) and

y = a if y∗ ≤ a

y = y∗ if elswhere

then

E(y) = Prob(y = a)× E(y|y = a)+

+ Prob(y > a)× E(y|y > a)

= Prob(y∗ ≤ a)× a+

+Prob(y∗ > a)× E(y∗|y∗ > a)

= Φa+ (1−Φ)(µ+ σα)

In the special case when a = 0

E(y|a = 0) = Φ(µ

σ)(µ+ σλ)

λ =ϕ(µσ)

Φ(µσ)

108

And for the variance

V ar(y) = σ2(1−Φ)((1− δ) + (α− λ)2Φ)

where

Φ = Φ(α) = Prob(y∗ ≤ a)

= Φ(a− µ

σ)

λ =ϕ

1−Φand

δ = λ2 − λα

Censored regression (the Tobit model)

Let us have now a linear regression model with

dependent variable as in (11):

E(yi|xi) = Φ(β′xiσ

)(β′xi + σλi)

λi =ϕ(β

′xiσ )

1−Φ(β′xiσ )

109

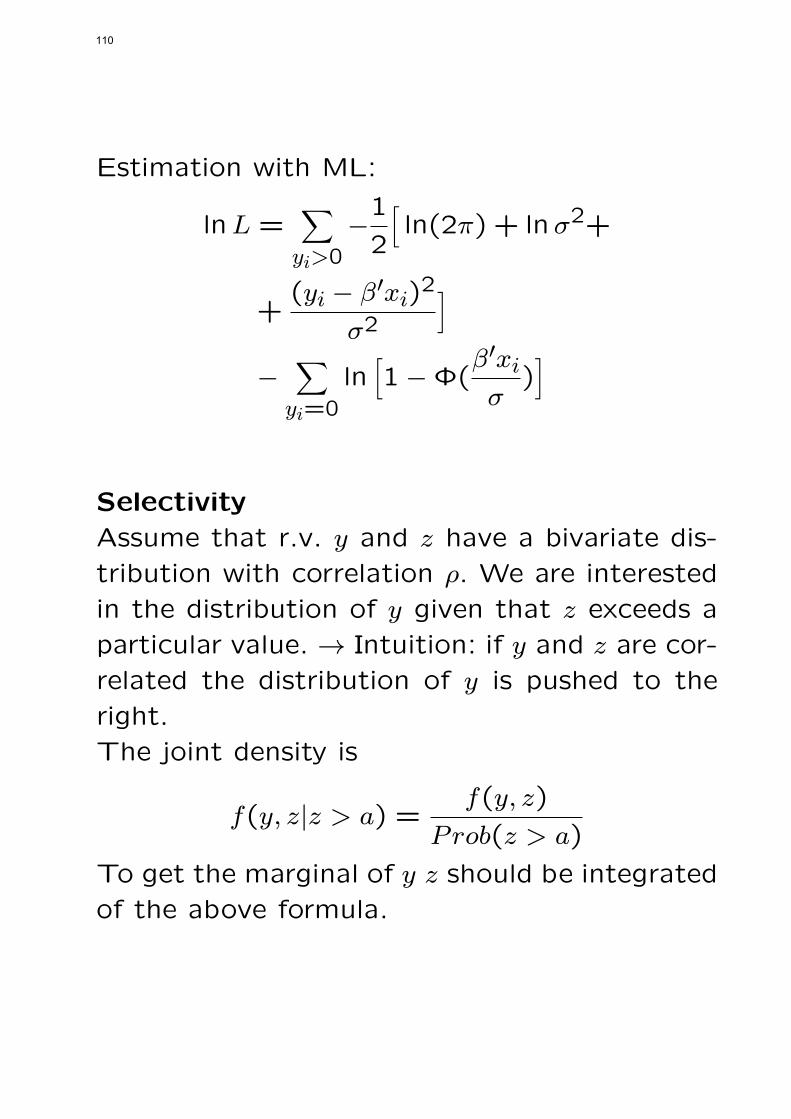

Estimation with ML:

lnL =∑yi>0

−1

2

[ln(2π) + lnσ2+

+(yi − β′xi)2

σ2

]−

∑yi=0

ln[1−Φ(

β′xiσ

)]

Selectivity

Assume that r.v. y and z have a bivariate dis-

tribution with correlation ρ. We are interested

in the distribution of y given that z exceeds a

particular value. → Intuition: if y and z are cor-

related the distribution of y is pushed to the

right.

The joint density is

f(y, z|z > a) =f(y, z)

Prob(z > a)

To get the marginal of y z should be integrated

of the above formula.

110

Theorem: Moments of a bivariate normal dis-

tribution with selectivity (also called: incidental

truncation):

E(y|z > a) = µy + ρσyλ(αz)

V ar(y|z > a) = σ2y(1− ρ2δ(αz)) where

αz =a− µz

σz

λ(αz) =ϕ(αz)

1−Φ(αz)and

δ(αz) = λ(αz)(λ(αz)− αz)

which is similar to the truncation → if ρ = 0

we get back the “usual” case, when ρ = 1 we

get back the truncation case.

Regression with selectivity (or incidental trun-

cation):

yi = β′xi + ϵi focus equation

z∗i = γ′wi + ui selection equation(12)

and yi is only observed when z∗i > 0. Now as-

sume that ui and ϵi are bivariate normal with

111

correlation ρ. Then

E(yi|yi is observed) = E(yi|z∗i > 0)

= E(yi|ui > −γ′wi)

= β′xi + E(ϵi|ui > −γ′wi)

= β′xi + ρσϵ︸︷︷︸βλ

λi(αu) where

αu = −γ′wi

σuand

λ(αu) =ϕ(γ′wi/σu)

Φ(γ′wi/σu)

So the model with selectivity is

(yi|z∗i > 0) = β′xi + β′λλi(αu) + vi (13)

Estimation: ML or the Heckman two-step pro-cedure:1. Estimate the selection equation by ML andthe compute

λi =ϕ(γ′MLwi)

Φ(γ′MLwi)

and

δ∗i = λi(λi + γ′wi)

112

2. Estimate (13) using λi and δi.

The Heckman 2-step procedure is consistent,

but the standard errors need to be corrected

as there is heteroscedasticity.

Nonresponse – Ignorable selectivity

The most important types of nonresponse that

can occur in panel data sets (and mostly in

other types of data sets as well)

1. Initial nonresponse occurs when individu-

als contacted for the first time refuse (or

are not able) to cooperate with the sur-

vey, or—for some reason—can not be con-

tacted at all. Because only very limited in-

formation is recorded for this group of non-

respondents this type of nonresponse is one

of the most difficult to deal with during

the analysis stage. Usually, the researcher

is not even aware of the problem of initial

113

nonresponse and implicitly assumes that it

does not distort his analysis.

2. Unit nonresponse is initial nonresponse that

results in missing data on all variables for

a particular unit. Only in cases where the

persons in question are interviewed at a

later stage both concepts do not coincide.

3. Item nonresponse occurs when information

on a particular variable for some individ-

ual is missing. For example, individuals may

refuse to report their income, while provid-

ing data for all other questions, like age,

education, family size, expenditure patterns,

etc.

4. Wave nonresponse is typical for panel data

and occurs when units do not respond for

114

one or more waves but participate in the

preceding and succeeding wave. In a monthly

panel a typical situation where this occurs

is that where an individual is on vacation

for a couple of weeks.

5. Attrition occurs when individuals having par-

ticipated one or more waves leave the panel.

These individuals do not return in the panel.

This can be caused by removal, emigration

or decease, but also by the fact that indi-

viduals are just “tired” of answering similar

questions each time.

Standard econometric methods are usually based

on a rectangular data set in which no data are

missing. If a data set with missing values is

used, for example, in statistical software, usu-

ally all observations are discarded for which one

115

or more of the variables under analysis is miss-ing. This is not only inefficient (because in-formation loss), but, more importantly, the re-maining cases may no longer be representativefor the population. Therefore, it is importantfor a researcher to pay attention to the natureof the nonresponse whether selection is likelyto be present or not.

Now let us assume that in (12) the dependentvariable of the selection equation is a binaryvariable r = 1 if all our variables are observedand r = 0 if an observation for any of the vari-ables in the model is missing. Let us call theselection mechanism to be ignorable if con-ditioning on the response indicator variable r

does not affect the joint distribution of y andx, i.e., if

f(y, x | β) = f(y, x | r;β),which implies that r is independent of (y, z).This in practice can be tested with the use ofa binary choice model.

116

Topic : PD0

Matrix Algebra Notes for LinearPanel Data Models

117

In these notes we review the main matrices

used when dealing with linear models, their

behaviour and properties.∗

Notation

• A single parameter (or scalar) is always

a lower case Roman or Greek letter;

• A vector is always an underlined lower

case Roman or Greek letter;

• An element of a vector is [ai];

• A matrix is always an upper case letter;

• An element of a matrix is [aij];

∗This appendix is based on Alain Trognon’s unpub-lished manuscript.

118

• An estimated parameter, parameter vec-

tor or parameter matrix is denoted by a

hat;

• The identity matrix is denoted by I and

if necessary I with the appropriate size

(N ×N) → IN ;

• The unit vector (all elements = 1) of

size (N × 1) is denoted by lN and the

unit matrix of size (N × N) is denoted

by JN .

119

In a two-dimensional panel data set (2D) all

variables look like this:

x =

x11x12...

x1T...

xN1xN2...

xNT

or

[xit] i = 1, . . . , N t = 1, . . . , T

120

The matrices used

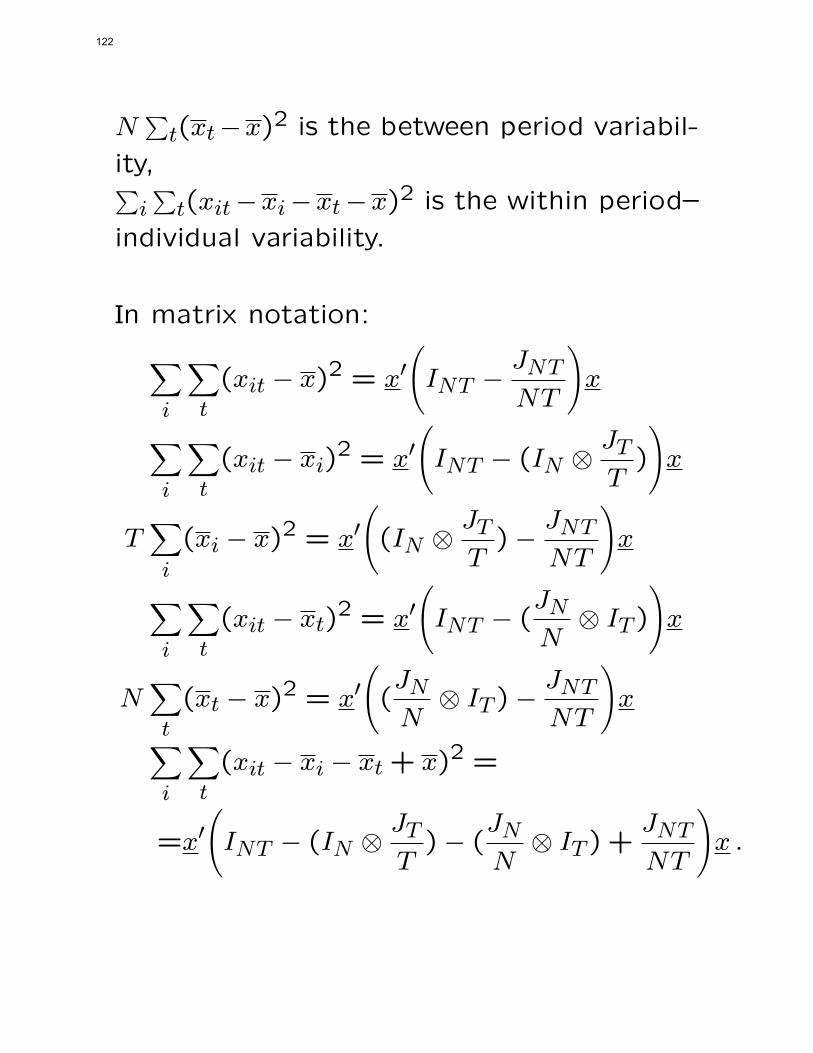

It is well known that the total variability of

a vector (of N individuals for T periods) can

be decomposed as∑i

∑t

(xit − x)2 =

∑i∑

t(xit − xi)2 + T

∑i(xi − x)2∑

i∑

t(xit − xt)2 +N∑

t(xt − x)2∑i∑

t(xit − xi − xt + x)2 + T∑

i(xi − x)2+

+N∑

t(xt − x)2 ,

where

xi =1T

∑t xit is the mean of the individual i,

xt =1N

∑i xit is the mean of the period t,

x = 1NT

∑i∑

t xit is the overall mean, and∑i∑

t(xit−x)2 is the total variability (around

the general mean),∑i∑

t(xit − xi)2 is the within individual vari-

ability,

T∑

i(xi − x)2 is the between individual vari-

ability,∑i∑

t(xit−xt)2 is the within period variabil-

ity,

121

N∑

t(xt−x)2 is the between period variabil-

ity,∑i∑

t(xit−xi−xt−x)2 is the within period–

individual variability.

In matrix notation:∑i

∑t

(xit − x)2 = x′(INT −

JNT

NT

)x

∑i

∑t

(xit − xi)2 = x′

(INT − (IN ⊗

JTT

)

)x

T∑i

(xi − x)2 = x′((IN ⊗

JTT

)−JNT

NT

)x

∑i

∑t

(xit − xt)2 = x′

(INT − (

JNN

⊗ IT )

)x

N∑t

(xt − x)2 = x′((JNN

⊗ IT )−JNT

NT

)x∑

i

∑t

(xit − xi − xt + x)2 =

=x′(INT − (IN ⊗

JTT

)− (JNN

⊗ IT ) +JNT

NT

)x .

122

The abbreviation and the rank of these ma-

trices are

T ∗ = INT −JNT

NTrank :NT − 1

Bn = (IN ⊗JTT

)−JNT

NT= (IN −

JNN

)⊗JTT

rank :N − 1

Bt = (JNN

⊗ IT )−JNT

NT=

JNN

⊗ (IT −JTT

)

rank :T − 1

Wn = INT − (IN ⊗JTT

) = IN ⊗ (IT −JTT

)

rank :N(T − 1)

Wt = INT − (JNN

⊗ IT ) = (IN −JNN

)⊗ IT

rank :T (N − 1)

W ∗ = INT − (IN ⊗JTT

)− (JNN

⊗ IT ) +JNT

NT

= (IN −JNN

)⊗ (IT −JTT

)

rank : (N − 1)(T − 1).

123

These matrices can be considered as or-

thogonal projectors into a subspace of RNT ,

where the dimension of these subspaces equals

the rank of the projector.

The main properties of these projector ma-

trices are:

T ∗ =

Wn +Bn

Wt +Bt

W ∗ +Bn +Bt ,

and

WnBn = WtBt = W ∗Bn = W ∗Bt = BnBt = 0

T ∗JNT

NT= W ∗JNT

NT= Wn

JNT

NT=

= WtJNT

NT= Bn

JNT

NT= Bt

JNT

NT= 0 .

The matrices T ∗, W ∗, Wn, Wt, Bn, and Bt

are symmetric and idempotent.

124

For the non–centered case the variability de-composition is

∑i

∑t

x2it =

∑

i∑

t(xit − xi)2 + T

∑x2i∑

i∑

t(xit − xt)2 +N∑

x2t .

The necessary non–centered transformationmatrices are

T∗ = INT , Bn = IN ⊗

JTT

,

Bt =JNN

⊗ IT , W∗ = W ∗ +

JNT

NTWn = Wn, W t = Wt .

The total variability in this case is made upas

T∗ =

Wn +Bn

Wt +Bt

W∗ +Bn +Bt .

The properties of these matrices are:

WnBn = WtBt = 0

W∗Bn = W

∗Bt = 0

and T∗, Bn, and Bt are symmetric and idem-

potent.

125

Partitioned inverse of matrices

Let

B = A−1 =

[B11 B12B21 B22

], and

[A11 A12A21 A22

]Then

B11 =(A11 −A12A

−122A21

)−1

B12 = −A−111A12

(A22 −A21A

−111A12

)−1

B21 = −A−122A21

(A11 −A12A

−122A21

)−1

B22 =(A22 −A21A

−111A12

)−1

126

The necessary spectral decompositions

In the case of the error components mod-

els, in order to derive the GLS and FGLS

estimators it is necessary to elaborate the

inverse of the covariance matrix of the dis-

turbance terms. This is based on the spec-

tral decomposition of these matrices.

Assume we have a symmetric matrix S. De-

composition QSQ = Λ always exists, where

Q contains the orthogonal eigen vectors of

S and λ is diagonal with the eigen values in

its elements.

S = QΛQ =∑

λiqiq′i

where λi are the eigen values, and qi the

appropriate eigen vectors

127

Topic : PD1

Linear Panel Data Models withFixed Effects – FE Models

128

Model with individual effects only

Let the basic FE model be:

yit = αi + x′itβ + uit

the˜notes that x does not contain the col-

umn of 1-s of the regression constant. We

will not use this just “simply”

yit = αi + x′itβ + uit

where αi are the individual effects. In fact

the regression constant is broken up into N

fixed effects. For individual i the model is:

yi = lTαi +Xiβ + ui ,

where yi is the T × 1 vector of the yit, lT is

the unit vector of size T , Xi is the T×(K−1)

matrix whose t–th row is x′it and ui, is the

T × 1 vector of disturbances.

129

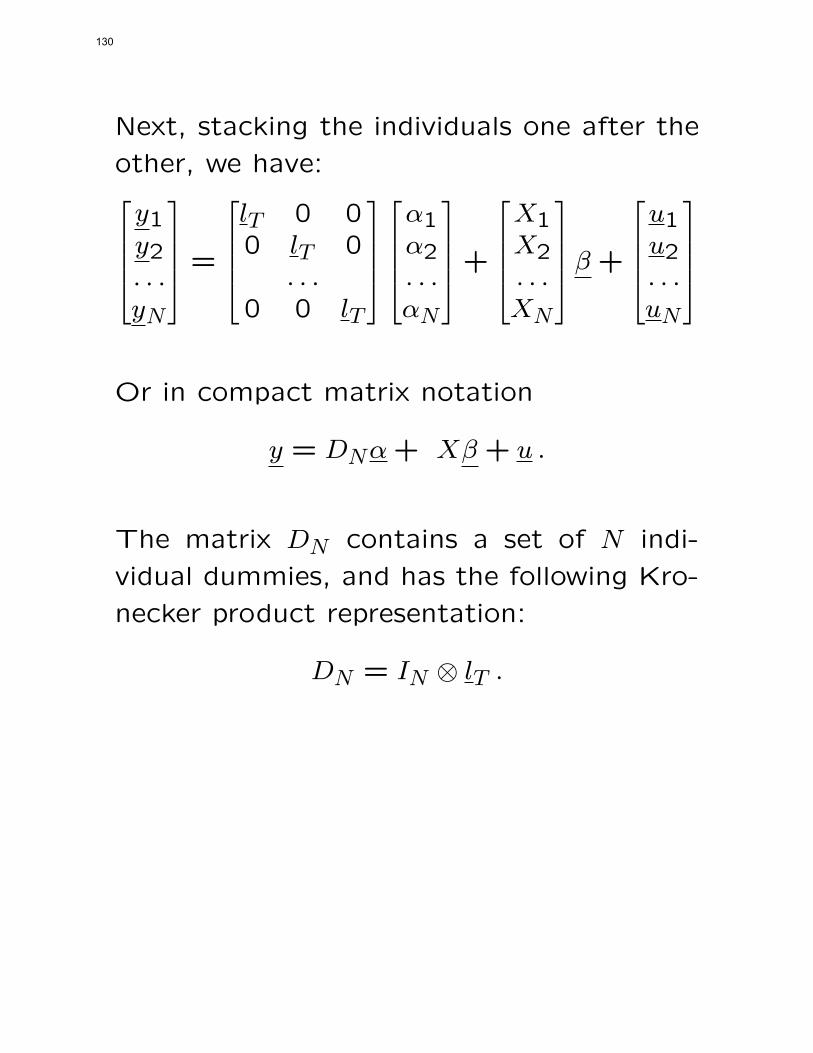

Next, stacking the individuals one after the

other, we have:y1y2. . .yN

=

lT 0 00 lT 0

. . .0 0 lT

α1α2. . .αN

+

X1X2. . .XN

β +

u1u2. . .uN

Or in compact matrix notation

y = DNα+ Xβ + u .

The matrix DN contains a set of N indi-

vidual dummies, and has the following Kro-

necker product representation:

DN = IN ⊗ lT .

130

It can easily be verified that the following

properties hold:

1. DN lN = lN ⊗ lT = lNT

2. D′NDN = TIN

3. DND′N = IN ⊗ lT l

′T = IN ⊗ JT

4. 1TD

′Ny = [y1, . . . , yN ]′

where yi =1T

∑Tt=1 yit and, by definition, JT =

lT l′T (the unit matrix of order T ).

131

Note (!!!):

We assume NT > N +K (which is satisfied

for large N whenever T ≥ 2), this requires

that the columns of X be linearly indepen-

dent from those of DN . For this to be the

case, the matrices Xi must not contain the

constant term (an obvious restriction) nor a

column proportional to it (which precludes

any variable, such as years of schooling, that

is constant for a given adult individual, al-

though varying from individual to individ-

ual).

Next let us turn to the estimation of this

model

132

y = DNα+ Xβ + u .

Let us simplify and not underline when not

really needed

y = (DN , X)

(αβ

)+ u (1)

y = (DN , X)γ + u

Estimating this model with OLS

γ =

[(D′

NX ′

)(DN , X)

]−1(D′

NX ′

)y =

[D′

NDN D′NX

X ′DN X ′X

]−1(D′

NX ′

)y

which gives

β = (X ′WnX)−1X ′Wny

This is called the WITHIN estimator!

133

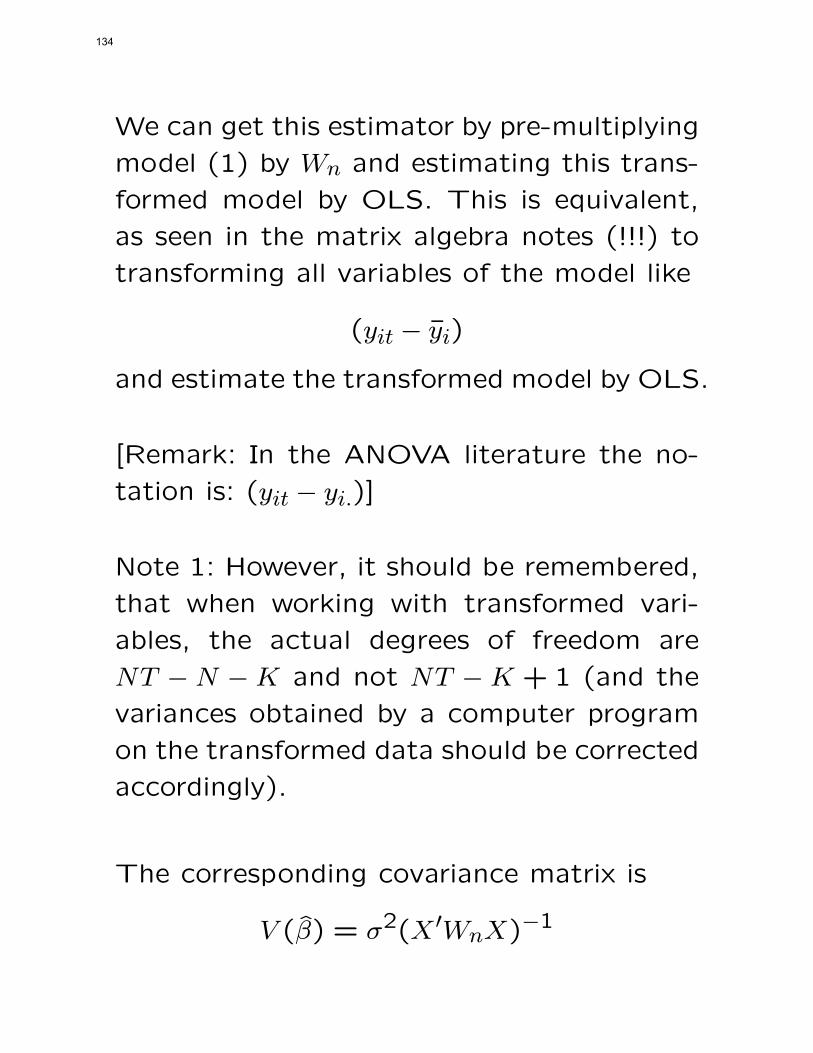

We can get this estimator by pre-multiplying

model (1) by Wn and estimating this trans-

formed model by OLS. This is equivalent,

as seen in the matrix algebra notes (!!!) to

transforming all variables of the model like

(yit − yi)

and estimate the transformed model by OLS.

[Remark: In the ANOVA literature the no-

tation is: (yit − yi.)]

Note 1: However, it should be remembered,

that when working with transformed vari-

ables, the actual degrees of freedom are

NT − N − K and not NT − K + 1 (and the

variances obtained by a computer program

on the transformed data should be corrected

accordingly).

The corresponding covariance matrix is

V (β) = σ2(X ′WnX)−1

134

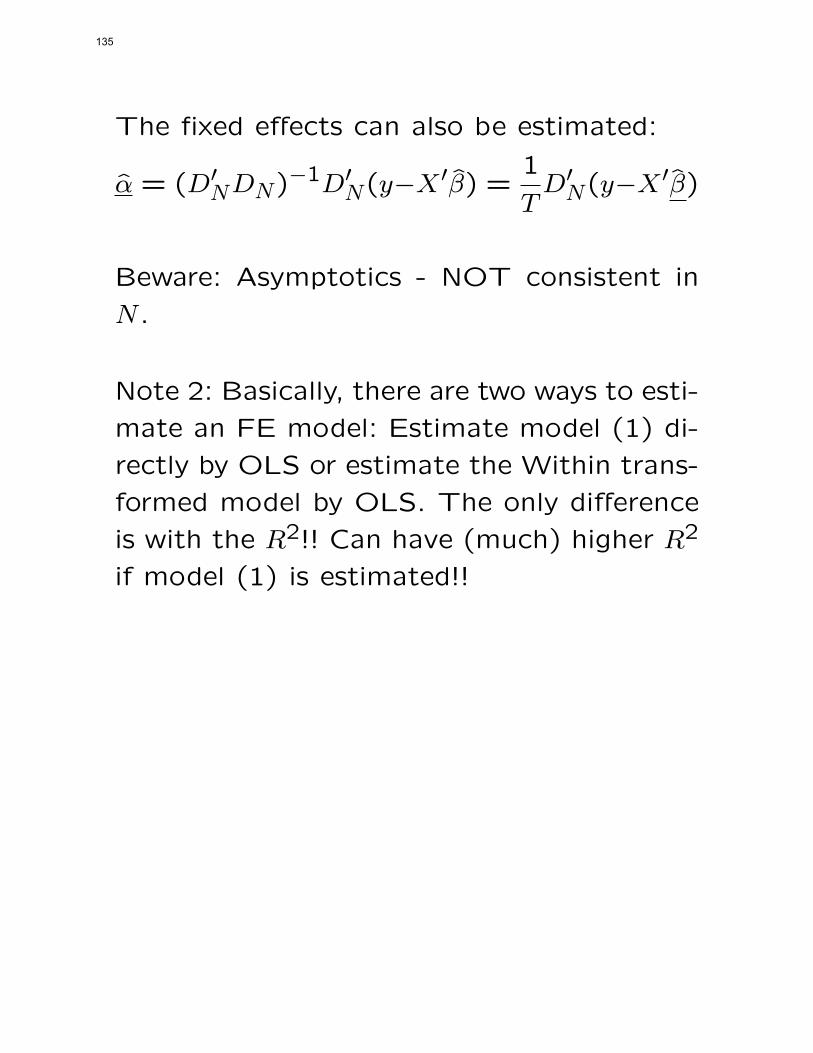

The fixed effects can also be estimated:

α = (D′NDN)−1D′

N(y−X ′β) =1

TD′

N(y−X ′β)

Beware: Asymptotics - NOT consistent in

N .

Note 2: Basically, there are two ways to esti-

mate an FE model: Estimate model (1) di-

rectly by OLS or estimate the Within trans-

formed model by OLS. The only difference

is with the R2!! Can have (much) higher R2

if model (1) is estimated!!

135

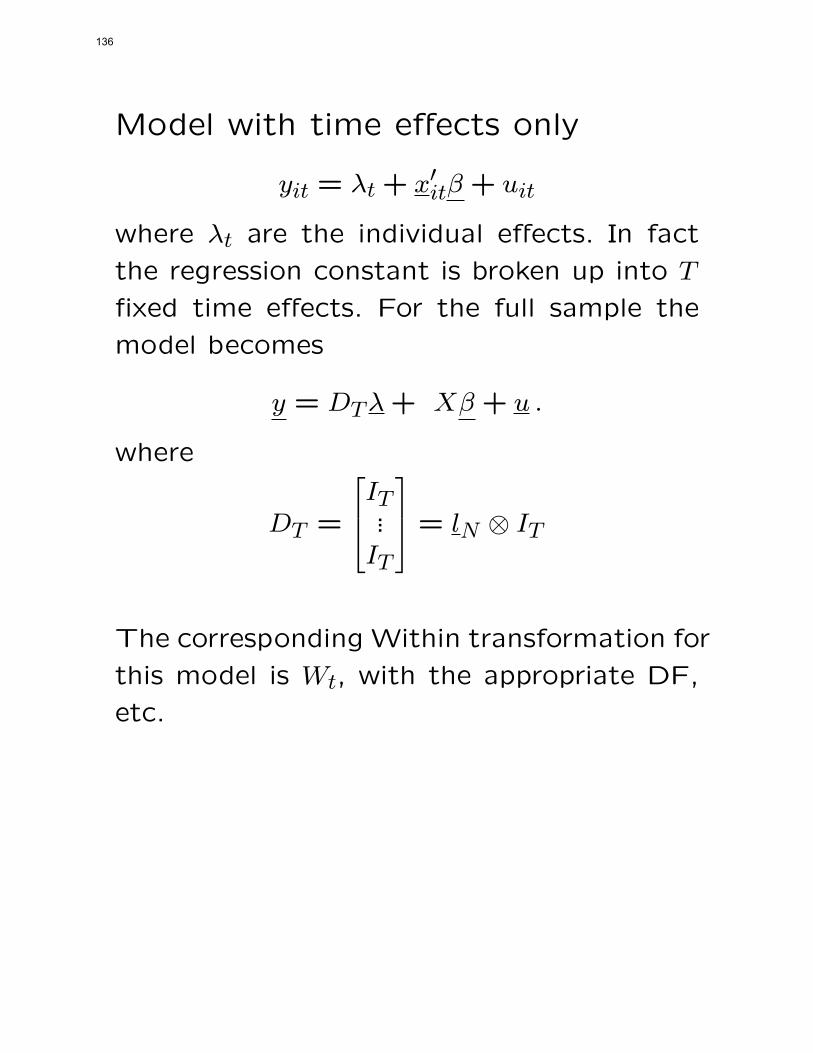

Model with time effects only

yit = λt + x′itβ + uit

where λt are the individual effects. In fact

the regression constant is broken up into T

fixed time effects. For the full sample the

model becomes

y = DTλ+ Xβ + u .

where

DT =

IT...IT

= lN ⊗ IT

The corresponding Within transformation for

this model is Wt, with the appropriate DF,

etc.

136

Model with individual and time ef-fects

yit = αi + λt + x′itβ + uit

or

y = DNα+DTλ+ Xβ + u .

Beware of the Dummy Variable Trap!!

Appropriate operator is the transformed W ∗,for identification.

Asymptotic properties: N → ∞ and T finite.

T → ∞ N finite. N and T go to ∞ then the

rates should be evaluated.

Separability of the parameter estimates!!

137

Some extensionsConstant Variables in One Dimension

The generic fixed individual effect consid-

ered may be the result of some factors (such

as sex, years of schooling, race, etc.) which

are constant through time for any individual

but vary across individuals. If observations

are available on such variables, we might

wish to incorporate them explicitly in the

regression equation. The model may thus

be written as:

yit = z′iδ + x′itβ + uit