Embed Size (px)

Citation preview

Advance Pricing Agreements,

Mutual Agreement Procedures

and Safe Harbour Rules

Alpana Saksena

11th April 2014

Chamber of Tax Consultants

4th INTENSIVE STUDY COURSE ON

TRANSFER PRICING

1 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN

BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING

PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii)

PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY

ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons, without

limitation, the tax treatment or tax structure, or both, of any transaction described in the

associated materials we provide to you, including, but not limited to, any tax opinions,

memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are subject

to change. Applicability of the information to specific situations should be determined through

consultation with your tax adviser.

2 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Indian Transfer Pricing environment

TP Adjustment scenario at present

“TP adjustments amounted to Rs 60,000 crore in FY 2013-

14 i.e. declined by 14% compared to

FY 2012-13.

(Source: Financial Express newspaper 10 March 2014)

3 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Indian Transfer Pricing Environment (Continued)

Hot Topics

R&D cost plus mark-up

Royalty

Advertising, Marketing, Promotion expenses

Management Fee

Marketing Intangibles

Attributing Global Profit

to India

4 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

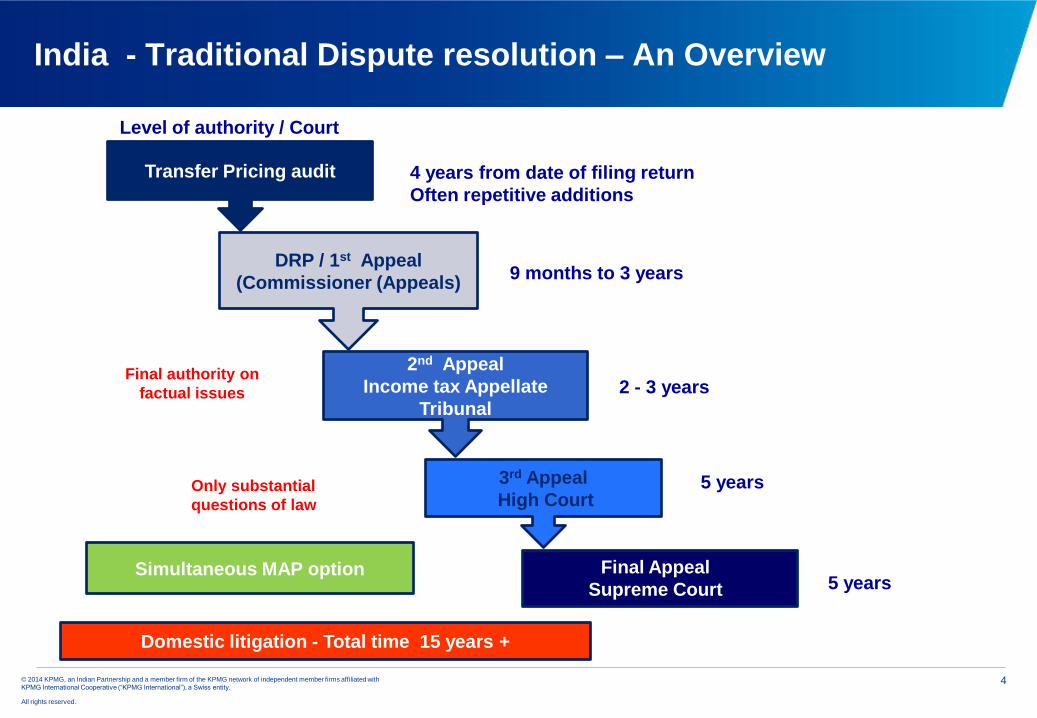

India - Traditional Dispute resolution – An Overview

Transfer Pricing audit

DRP / 1st Appeal

(Commissioner (Appeals)

2nd Appeal

Income tax Appellate

Tribunal

3rd Appeal

High Court

Final Appeal

Supreme Court

Level of authority / Court

Simultaneous MAP option

4 years from date of filing return

Often repetitive additions

9 months to 3 years

2 - 3 years

5 years

5 years

Domestic litigation - Total time 15 years +

Only substantial

questions of law

Final authority on

factual issues

5 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Mutual Agreement Procedure (MAP) – To avoid double taxation and provide relief

MAP is an alternate mechanism incorporated into tax treaties for the resolution of international

tax disputes

Resolution of disputes through the intervention of competent authorities of each country who

evolve a mutually acceptable solution

Relief through MAP possible irrespective of remedies available under domestic tax laws

Mutual Agreement Procedures

6 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Overview of MAP procedure

MAP request

Tax payer makes MAP application in prescribed form to CA of home country

Request can be made where there is double taxation or taxation inconsistent with treaty

Consultation

Host country CA called upon for dispute resolution where issue cannot be resolved unilaterally by home country CA,

Admission

Acceptance of Application at CA’s discretion

CA can call for additional information from tax payer at this stage

Representation

Tax payer may be called for making written or oral representations

Negotiations

CAs initiate negotiation and attempt to reach an amicable resolution

The tax payer is not involved in the negotiation process however he may be called upon to make submissions

Solution

Proposed agreement communicated to the Taxpayer for his acceptance

Solution to be given effect to within 90 days, if taxpayer consents

Generally the entire process takes 2 – 3 years for completion

7 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Safe Harbour Rules - Applicability

The below Safe Harbour margins shall be applicable:

Eligible International Transaction Safe Harbor Margin

IT & ITES Services with significant risks where the aggregate value of

such transactions

• < INR 500 crore

• > INR 500 crore

Operating profit margin to operating

expense :

20 percent or higher

22 percent or higher

KPO services, with insignificant risks Operating profit margin to operating

expense is 25 percent or higher

Intra group loan to wholly owned subsidiaries where the amount of loan

• < INR 50 crore

• > INR 50 crore,

Interest rate equal to or greater that the

base rate of SBI as on 30 June of the

relevant previous year:

• plus 150 basis points

• plus 300 basis points

8 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Safe Harbour Rules - Applicability

Eligible International Transactions Safe Harbour Margin

R&D services with insignificant risks, wholly or partly relating to

software development.

Operating profit margin to operating

expense is 30 percent or higher

Contract R&D services, with insignificant risks, wholly or partly

relating to generic pharmaceutical drugs.

Operating profit margin to operating

expense is 30 percent or higher.

Manufacture and export of :

• Core auto components

• Non core auto components

Where 90% or more of total turnover relates to Original equipment

manufacturer sales

Operating profit margin to operating

expense :

12 percent or higher

8.5 percent or higher

Explicit corporate guarantee to wholly owned subsidiaries where the

amount is guaranteed

• < INR 100 crore

• > INR 100 crore,

And the rating of the borrower, by SEBI registered agency is of the

adequate to highest safety

•Commission /fee of 2 % or more per annum

•Commission /fee of 1.75 % or more per

• annum

9 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

9

Safe Harbours are said to be convenience prices which are higher than the Arm’s Length Price.

The option of being governed by Safe Harbour Rules shall be valid for a period of five years starting with

AY 2013-14 or for a lesser period at the option of the taxpayer.

No economic or other adjustments allowed to taxpayers opting for Safe Harbour.

Range of +/-3% not allowed.

No respite is provided from maintenance of mandatory documentation.

A taxpayer opting for Safe Harbour rules will not be able to avoid possibility of economic double

taxation.

Companies opting for Safe Harbour not allowed to opt for MAP proceedings

Due to apprehension in various industry sectors - Government has issued instructions that Safe

Harbour margins not to be followed for general Audit or APA purposes.

Tepid response to Safe Harbour option due to very high markups

Safe Harbour Rules – Our observations

10 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Safe Harbour Rules – Key considerations

Sub-categorization of sectors

Increased litigation as interpretations and

justifications can vary

High Margins

Loans

The provisions are meant only for rupee

denominated loans to WOS.

The SBI base rate as on 30th June of the

previous year has been recommended as

the Base Rate with no justification

Guarantees

Corporate guarantee rate of 2% is higher

than the prevailing bank charges.

Compliance burden

Does not relieve the assessee from

documentation requirements as provided

under Sec 92D.

Basic objective of simplicity and easy

compliance is not being met

Legislative Provisions and

Procedure

(Announced in Budget of

March 2012)

APA Program in India

12 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

12

Purpose

Basis

Validity

Post APA

APA Program – Basic Legislative Provisions

Sections 92CC to 92CD of Income Tax Act 1961

• APA to be entered into with Central Board of Direct Taxes (CBDT) :

for either determining the Arm’s length price (‘ALP’) or

specifying the manner in which the ALP is to be determined

• Arm’s Length Price will be determined on the basis of methods prescribed in the Income Tax act or

any other method suitable to determine the ALP

In arriving at ALP suitable adjustments / variations can be claimed

• Valid for a maximum of five consecutive years

• Binding on taxpayer and Commissioner and subordinate authorities

• Not binding if there is a change in law or facts having bearing on APA

If an APA covering a particular year is obtained after filing of tax return

a modified return is to be filed based on the APA and

an assessment is to be completed based on such modified return

13 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

APA Rules – Operating Guidelines

(Announced 30th Aug 2012)

13

APAs can be unilateral as well as bilateral / multilateral

Model Article 9(2) necessary for Bilateral APA – India Practice makes it essential

Transactions to be covered

existing transactions (application to be filed by March 31 for transactions beginning 1st April)

new international transactions (application can be filed before undertaking transactions)

Pre-filing consultation mandatory - specified format (anonymous option available)

Specified format for APA application - withdrawal / renewal of APA possible

Schedule of APA fees

Annual compliance report required , compliance audit would follow.

Particulars Fees

Transaction value up to INR 1 bn (approx USD 20 mn) INR 1 million (approx USD 20,000)

Transaction value up to INR 2 bn (approx USD 40 mn); INR 1.5 million (approx USD 30,000)

Transaction value above INR 2 bn (approx USD 40 mn) INR 2 million (approx USD 40,000)

Rules 10F to 10T of the Income Tax Rules 1962

The Process and Features

APAs in India

15 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

APA Process – A quick overview

Application for pre-filing

consultation

Pre-filing Post-prefiling Phase

Pre-filing Consultation (Form 3CEC)

Pre-filing Process and Outcome

The APA Application (Form

3CED)

Negotiation & Settlement

Annual Compliance (Form 3CEF)

Key milestones

Taxpayer to file a YOY

compliance report

with to demonstrate

compliance with APA

terms

TPO to conduct

compliance audit, to

verify compliance

with APA terms

TPO to submit audit

report to DGIT within

6 months

Concluding pre-filing

consultation

Formal APA application

lodged Concluding APA

Detailed

application

developing

information

provided at pre-

filing stage

Forecasts

estimates required

• Submission reviewed by

APA Team

Site visits, discussions,

joint meetings to gain a

better understanding

After review, analysis &

evaluation stage,

positions of the APA

team is discussed and

agreed with the

taxpayer

APA signed

Prescribed format

requires details of:

Covered transactions,

Functions, assets,

risks

Proposed

benchmarking

methodology, PLI,

Comparables

Critical assumptions

Past audit history

APA team holds

consultations to

Explore suitability

of APA

identify issues for

detailed discussion

Discuss scope of

covered

transactions

Are non binding

Outcome will be

conveyed in writing

Key details

15

16 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

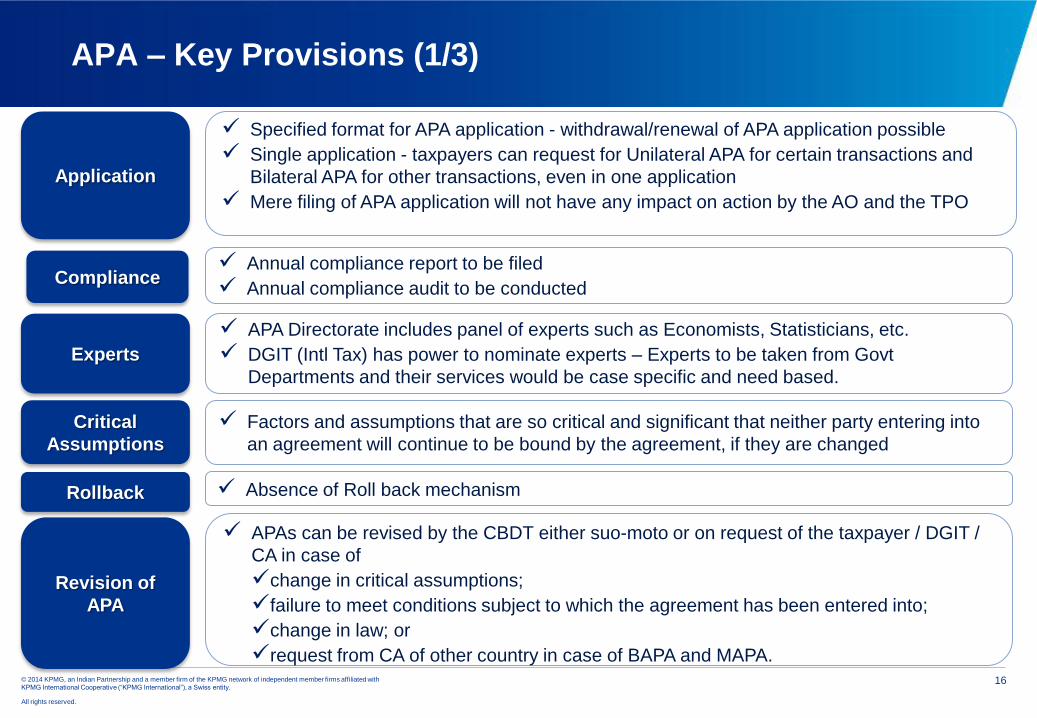

Application

Specified format for APA application - withdrawal/renewal of APA application possible

Single application - taxpayers can request for Unilateral APA for certain transactions and

Bilateral APA for other transactions, even in one application

Mere filing of APA application will not have any impact on action by the AO and the TPO

Experts

APA Directorate includes panel of experts such as Economists, Statisticians, etc.

DGIT (Intl Tax) has power to nominate experts – Experts to be taken from Govt

Departments and their services would be case specific and need based.

Compliance Annual compliance report to be filed

Annual compliance audit to be conducted

Critical

Assumptions

Factors and assumptions that are so critical and significant that neither party entering into

an agreement will continue to be bound by the agreement, if they are changed

Revision of

APA

APAs can be revised by the CBDT either suo-moto or on request of the taxpayer / DGIT /

CA in case of

change in critical assumptions;

failure to meet conditions subject to which the agreement has been entered into;

change in law; or

request from CA of other country in case of BAPA and MAPA.

Rollback Absence of Roll back mechanism

APA – Key Provisions (1/3)

17 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Cancellation of

APA

APA may be cancelled in case of

failure of the taxpayer to comply with the terms of the agreement;

failure to file the annual compliance report in time;

annual compliance report filed contains material errors; or

the applicant does not agree for revision of the APA

Cancellation of agreement by CBDT No appeal possible. Taxpayer can take recourse to constitutional remedies.

Fees

Fees (only at APA Application stage)

APA fees based on expected value of transactions – If value of the international

transactions eventually happens to be more than what was earlier projected, it

would have no effect on the quantum of fee which has already been paid.

Transaction Value Fees

Up to Rs 1 billion / approx US$ 20 million Rs 1 million / approx US$ 20,000

Up to Rs 2 billion / approx US$ 40 million Rs 1.5 million / approx US$ 30,000

Over Rs 2 billion / approx US$ 40 million Rs 2 million / approx US$ 40,000

APA – Key Provisions (2/3)

18 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

APA guidance

with FAQs –

Issued by

CBDT

APA for PE profit attribution - if taxpayer admits having PE, APA request could be

filed for profit attribution to PE.

Impact of past year’s litigation - past history is one of will be discussed during the

APA process. However, it is not mandatory that the same position as taken in

the past shall guide or decide the APA process. The APA authorities would look

at the evidences and information with an open mind

No surprise field visits

Interlinked transactions - If one international transaction is intrinsically linked with

another and cannot be benchmarked independently, both the international

transactions need to be covered.

MAP not available for concluded Unilateral APAs

No benefit of +/- 3 percent variation – Once ALP is determined in accordance

with an APA agreement, there is no provision for allowance of 3% variation

APA – Key Provisions (3/3)

Practical Aspects

APAs in India

20 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

20

Why Advantageous?

Anonymous

Preparation required

Mandatory Prefiling – The gateway to APA

Advantageous even if

APA not pursued

Requires similar preparation as for TP Audit report

Structured format gives clarity in respect of information required

Affords an opportunity to test waters, gauge receptivity of revenue

Identify issues that will require specific development

Can help taxpayer decide whether APA can be achieved

No fees for prefiling

Advantageous to taxpayers with difficult dispute history

Veil of anonymity could help in frank discussions

Pre-filing could be instructive

Could provide valuable insights into strength and weakness of APA

proposal and business strategies and models

Assist in being better prepared for TP audit

21 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Typical Transactions for APAs

21

India specific transactions suitable for APAs

Software development & ITES services

Management services and royalty pay outs

Contract R&D (Pharma / Software)

Contract manufacturing

Intercompany loans, advances and guarantees

Distributors and marketing intangibles

Start up companies with losses

Any new transactions - no dispute history

22 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Are you ready for an APA? Options to pursue?

22

Probably

Yes

Nature of

transactions

Transactions critical to business

In perpetual dispute and litigation

New transaction – possibility of dispute

Losses / contentious audit triggers

Cost benefit

Analysis versus

outcome

Time / expense/ resources vs size of transactions

Transactions too small and simple

No disputes with tax authorities

Outcome of audit vs APA would be similar

Looking for

certainty ?

Regardless of nature of transactions

Tax authorities habitually aggressive

Litigation processes lengthy / outcomes uncertain

Goal is to manage potential controversy

Probably

Yes

Probably

NO

When unilateral

When the dispute is primarily in India

If relationships between CAs strained

If APA program new in country of operation

Other

cases

Bilateral

When bilateral

Transactions are interdependent

Where the anticipated outcome in India may be different and

therefore needs to be agreed upon with overseas CA

When possibility of economic double taxation exists

Bilateral

23 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Pros & Cons of an APA

P

R

O

S

C

O

N

S

Certainty for 5 years with simpler compliances after the APA has been entered into

Reduces risk of double taxation

Reduces documentation burden

Time and cost saving

Preferred by tax authorities

Mandatory pre-filing consultation helps in taking a decision for entering into an APA

Possible persuasive value in litigation and open audit years

High upfront cost

No time limit prescribed under the APA rules

Onerous details required in Pre-filing / APA application

No Rollback provisions

Experience thus far

APAs in India

25 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

APA Program – Experience (1/2)

APA pre-filing meetings do not bind either party to the APA Program

Government sources - hardly any anonymous applications have been filed, which is a pointer that taxpayers

have posed faith in the program

Preparation

• Capture core arguments powerfully to enable negotiating parties to assess information efficiently.

• Caution while relying on methodologies followed in past TP documentation especially in case of adverse outcome in the preceding years.

Filling the form

• Key - how the taxpayer structures answers to the information requirements –

• Caution for areas which require subjective analysis or estimation.

• Ambiguity should be avoided

• Prescribed form should be filled up accurately, consistent with regulatory requirements.

Discussion Process

• Pre-filing meetings should be used to up front clarify what both sides expect from the APA process.

• Several back and forth queries

26 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

26

Discussions

• First round of discussions already in process - experience satisfactory so far

• International TP experts have welcomed the collaborative approach of the Indian APA team

FAR

• strong emphasis on finalizing mutually agreeing on detailed FAR

• Economic analysis will be done post FAR analysis followed by rounds of discussions and negotiations

Site Visits

• Site visits by the APA teams in progress - helpful in assessing the correct functional profile.

• Visits scheduled in consultation with taxpayers - conducted in a cordial and un-intrusive manner.

Applications

• 146 APA applications filed for last year (150 prefilings had been received)

• MNC giants from pharma, consumer electronics, media, cement, telecom, etc. have filed applications

• In several cases, position papers sent to CBDT for approval/recommendations –

Revenue perspective

• Due to sensitivity of business information highest level of confidentiality will be maintained

• Cancellation of APA could be done only by CBDT - APA will not be cancelled for any arbitrary reason

5 Unilateral APAs signed on 31 March 2014

APA Program – Experience (2/2)

27 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

APA – Regulatory Set up in India

Chairman CBDT

DGIT (Intl Tax)

Commissioner APA

Delhi Mumbai Bengaluru

Competent Authority

Director APA

Under

Secretary APA - I

Under

Secretary APA - II

Additional Commr (APA)

Joint

Commr (APA)

Deputy Commr (APA)

Joint

Commr (APA)

Additional Commr (APA)

Assistant Commr (APA)

Deputy Commr (APA)

Deputy Commr (APA)

BILATERAL

28 © 2014 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

Questions & Answers

Questions

&

Answers

Thank You Presenter’s details

Alpana Saksena

Executive Director,

Global Transfer Pricing Services

(Transfer Pricing)

India / USA

Phone: +91 9619888716

E-mail: [email protected]