Embed Size (px)

Citation preview

ACUIA – Region 5 Meeting

Compliance Update

September 28, 2015

Topics

• TILA/RESPA Rule

• Privacy

• IOLTA

• Fixed Assets

• TCPA

• Risk-Based Capital – 2 Proposal

• Regulation CC Proposal

• HMDA Proposal

• Member Business Loan Proposal

• Other things that might be coming

TILA/RESPA

Integration

General Information

• Final rule issued November 20, 2013

• Effective Date October 3, 2015

• Amends Reg Z and RESPA

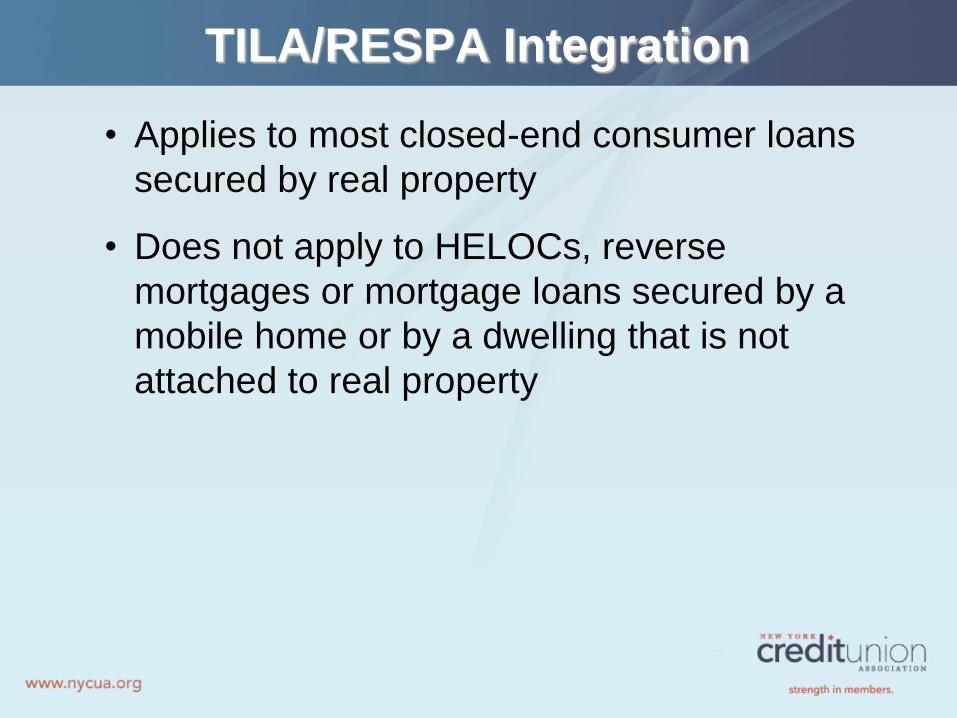

TILA/RESPA Integration

• Applies to most closed-end consumer loans

secured by real property

• Does not apply to HELOCs, reverse

mortgages or mortgage loans secured by a

mobile home or by a dwelling that is not

attached to real property

Record Retention

• Retain copies of the Closing Disclosure (and all

documents related to the closing disclosure) for

five years after consummation;

• Post-Consummation Escrow Cancellation Notice

for 2 years.

• All other evidence of compliance with the

Integrated Disclosure provisions creditors must

maintain records for three years after

consummation of the transaction;

• Electronic recordkeeping is permissible

Disclosures for Non-Covered Transactions

• Credit unions will continue to use Good Faith

Estimates, HUD-1 and Truth-in-Lending

disclosures

TILA/RESPA Integration

• Provision of Loan Estimate must be sent within 3 business days of

receiving an application and not later than the seventh business day

before closing, may only be waived if member has a bona fide

personal emergency;

• The Loan Estimate integrates and replaces the existing RESPA

GFE and the initial Truth-in-Lending disclosures;

• Disclosure must be in writing and must be based on the best

information reasonably available at the time the disclosure is

provided if the amount is unknown;

• Application - name, income, SSN, property address, property value

estimate, loan amount sought (removes and all other information

needed to make a credit decision;

• Limited to collecting a credit report fee until members have been

given the Loan Estimate and communicated their intent to proceed.

TILA/RESPA Integration

• Must use model form H-24 for a federally related

mortgage loan (most loans);

• Business day for the loan estimate is any day on

which the credit union’s offices are open for

carrying out substantially all of its business

functions;

• Business day for the closing disclosure is all

calendar days except Sundays and legal public

holidays.

Good Faith Requirement

• Whether or not a Loan Estimate was made in good faith

is determined by calculating the difference between the

estimated charges originally provided in the Loan

Estimate and the actual charges paid by or imposed on

the member in the Closing Disclosure;

• Generally, if the charge paid by or imposed on the

consumer exceeds the amount originally disclosed on

the Loan Estimate it is not in good faith, regardless of

whether the creditor later discovers a technical error,

miscalculation, or underestimation of a charge;

• However, a Loan Estimate is considered to be in good

faith if the creditor charges the consumer less than the

amount disclosed on the Loan Estimate, without regard

to any tolerance limitations.

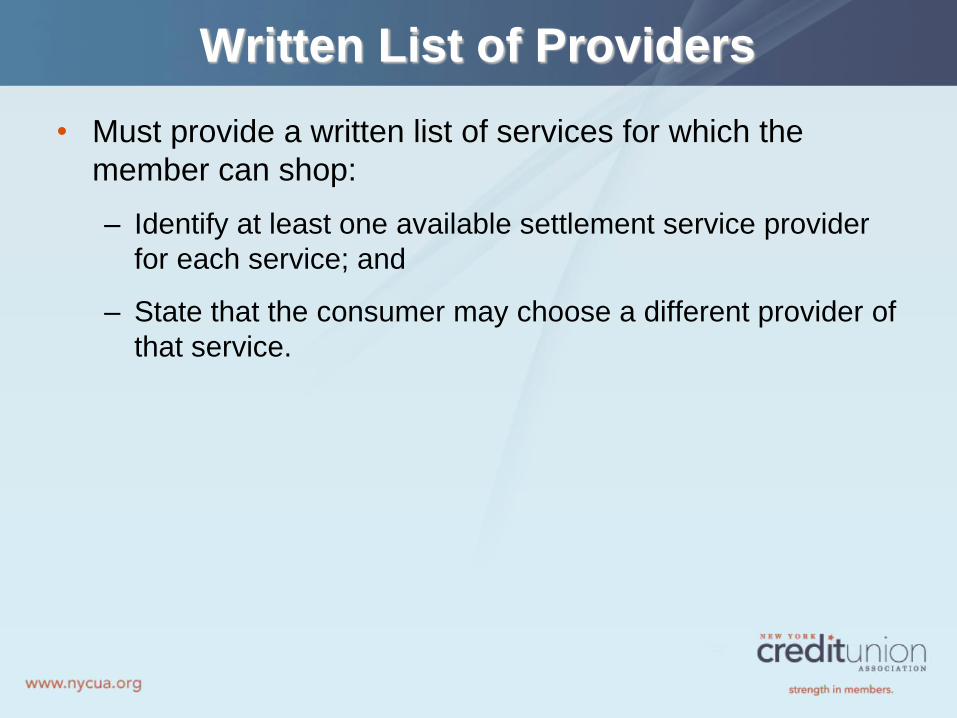

Written List of Providers

• Must provide a written list of services for which the

member can shop:

– Identify at least one available settlement service provider

for each service; and

– State that the consumer may choose a different provider of

that service.

TILA/RESPA Integration

• Restrictions on Charging Higher Settlement Costs than

Initially Disclosed

• Lender charges cannot exceed estimates (zero

tolerance) include

– Fees paid to the creditor, mortgage broker or an affiliate;

– Fees paid to an unaffiliated third party if the creditor did

not allow the member to shop for the service;

– Transfer taxes.

TILA/RESPA Integration

• Limited increases are allowed for certain charges. The

actual charges cannot exceed the estimates by more

than 10% (10% cumulative tolerance) in sum. These

include:

– Charges for third-party services where:

• The charge is not paid to the credit union or the credit

union’s affiliate and;

• The consumer is permitted by the creditor to shop for

the third-party service, and the consumer selects a

third-party service provider on the creditor’s written list

of service providers.

• Recording fees

TILA/RESPA Integration

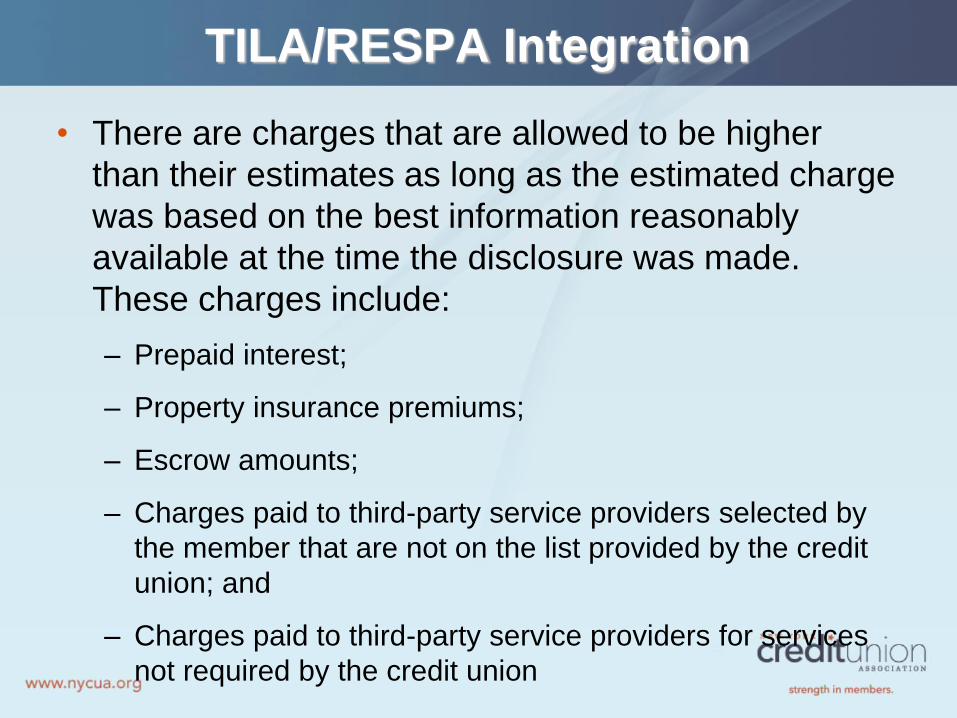

• There are charges that are allowed to be higher

than their estimates as long as the estimated charge

was based on the best information reasonably

available at the time the disclosure was made.

These charges include:

– Prepaid interest;

– Property insurance premiums;

– Escrow amounts;

– Charges paid to third-party service providers selected by

the member that are not on the list provided by the credit

union; and

– Charges paid to third-party service providers for services

not required by the credit union

TILA/RESPA Integration

• If amounts paid by the member exceed the

amounts specified in the GFE beyond the

tolerance limits the excess must be refunded no

later than 60 days after closing and new

disclosures must be provided showing the

refund.

Revised Loan Estimates

• The following are reasons that loan estimates may be

revised and only to the extent of the changed

circumstance:

– Changed circumstances that occur after the Loan Estimate

is provided to the member cause estimated settlement

charges to increase more than is permitted under the

TILA-RESPA rule;

– Changed circumstances that affect the member’s eligibility

for the terms they applied or the value of the security;

– Revisions requested by the member;

– The interest rate was not locked when the loan estimate

was provided and locking causes points or lender credits

to increase

Revised Loan Estimates

• The consumer indicates an intent to proceed

with the transaction more than 10 business days

after the Loan Estimate was originally provided;

• The loan is a new construction loan, and

settlement is delayed by more than 60 calendar

days, if the original Loan Estimate states clearly

and conspicuously that at any time prior to 60

calendar days before consummation, the

creditor may issue revised disclosures.

Examples

• The creditor relied on the consumer’s

representation to the creditor of a $90,000

annual income, but underwriting determines that

the consumer’s annual income is only $80,000.

• There are two co-applicants applying for a

mortgage loan and the creditor relied on a

combined income when providing the Loan

Estimate, but one applicant subsequently

becomes unemployed.

Timing

• Must provide a revised loan estimate no later

than 3 business days after receiving information

establish one of the reasons allowed;

• May not provide a revised loan estimate on or

after the date the closing disclosure is provided;

• Must be received no later than 4 business days

prior to consummation (Sundays and federal

holidays). If being mailed it must be placed in

the mail no later than 7 business days before

consummation to allow 3 business days for

receipt.

TILA/RESPA Integration

• Provision of Settlement Disclosure combines the final

Truth in Lending disclosure and the HUD-1 and must be

received 3 business days prior to consummation (must

take mailing time into consideration so for mail it should

be sent 6 business days prior to closing);

• Consummation is defined by state law;

• The closing disclosure generally must contain the actual

terms and costs of the transaction;

• Waiving the three business day waiting period can be

only for a bona fide personal emergency;

• Significant changes to the closing disclosure (APR

above 1/8%, changes to loan product, prepayment

penalty) require another 3 business days.

TILA/RESPA Integration

• Credit unions may continue to use settlement

agents to provide closing disclosure but the

credit union is responsible for ensuring

compliance.

• No fees may be charged for preparing the

closing disclosure.

Intent to Proceed

• A member indicates intent to proceed with the

transaction when the member communicates, in any

manner, that the member chooses to proceed after the

Loan Estimate has been delivered, unless a particular

manner of communication is required by the credit union;

– Oral communication in person immediately upon delivery

of the Loan Estimate;

– Oral communication over the phone, written

communication via email, or signing a preprinted form after

receipt of the Loan Estimate;

– A consumer’s silence is not indicative of intent to proceed.

Special Information Booklet

• Credit unions must provide a copy of the special information

booklet to consumers who apply for a consumer credit

transaction secured by real property, except in certain

circumstances (see below). The special information booklet is

required pursuant to Section 5 of RESPA (12 U.S.C. 2604)

and is published by the Bureau to help consumers applying

for federally related mortgage loans understand real estate

transactions;

– If the consumer is applying for a HELOC, the creditor can

provide a copy of the brochure entitled “When Your Home is On

the Line: What You Should Know About Home Equity Lines of

Credit” instead of the special information booklet.

– Need not be provided in a refinance, subordinate lien or reverse

mortgage.

Post-Consummation Escrow

Cancellation

• Not required when a loan has been repaid,

refinanced, rescinded or foreclosed;

• If the creditor or servicer cancels escrow at the

borrower’s request the disclosure must be

provided no later than three business days

before closure of the escrow account;

• If the cancellation is not at the borrower’s

request then the disclosure must be provided no

less than 30 days before closure of the escrow

account

Contents of Disclosure

• Under the heading “Escrow Closing Notice”:

– A statement informing the borrower of the date on

which the escrow account will be closed;

– A statement that an escrow account may also be

called an impound or trust account;

– The reason why the escrow account will be closed;

– A statement that without an escrow account the

borrower is responsible for all property costs directly,

possibly in one or two large payments a year.

Contents of Disclosure

• A table titled “Cost to you”, that includes:

– An itemization of the amount of any fee the creditor or

servicer imposes on the borrower for closing the

escrow account labeled “Escrow Closing Fee”;

– A statement that the fee is for closing the account.

Contents of Disclosure

• Under the reference “In the future”:

– A statement of the consequences if the borrower fails to

pay property costs including actions that can be taken by

the state or local government and a statement of actions

the creditor or servicer may take (adding amounts to the

loan balance, adding an escrow account to the loan,

purchasing property insurance that is more costly);

– A telephone number the borrower may call to get more

information about escrow cancellation;

– A statement on whether the creditor or servicer offers an

option to keep escrow open, a number the borrower may

call and the cut-off date to request the escrow be kept

open.

Privacy – Alternative

Delivery Method

Privacy Notice Eligibility

• Eligibility Criteria:

– Information sharing does not trigger opt-out rights. Joint

marketing agreements, process and servicing transactions

and for security or confidentiality purposes do not trigger

opt-out rights;

– Must not be required to include the FCRA affiliate sharing

opt-out notice on your annual privacy notice;

– FCRA affiliate marketing privacy notice requirements have

been met or the annual privacy notice is not the only

notice provided to satisfy the requirements;

– Your privacy notice cannot have changed since your

members last received the notice (initial, annual or

revised)

– Use the model form

Alternative Delivery Method

• Inform members:

– In a clear and conspicuous manner;

– Not less than annually;

– On an account statement, coupon book or a notice or

disclosure require or allowed by law –

• The privacy notice is available on your website;

• The notice will be mailed if requested by telephone;

• The notice has not changed;

• A specific web address that takes the member directly

to the page where the notice is posted;

• A telephone number to request the notice.

Alternative Delivery Method

• Post the notice on your website:

– Post your current notice in a continuous, clear and

conspicuous manner on a page of the website;

– On which only the content is the privacy notice;

– Without requiring any login name, password or similar

steps;

– No other information may appear

Interest on Lawyer’s

Trust Accounts (IOLTA)

What Are They?

• Attorneys handle funds for clients, such as

settlement checks, fees advanced for services

not yet performed or money to pay various court

fees;

• Attorneys open IOLTA accounts to hold these

funds. The funds belong to their clients until

such time that they need to be paid out;

• There are rules for attorneys to open and

maintain these accounts but this is not the credit

union’s concern.

Titling

• IOLTA accounts must be titled as follows:

– The attorney or firm’s name;

– The acronym – “IOLA”; and

– Either of the following:

• Attorney Trust Account

• Attorney Escrow Account

• Attorney Special Account

Share Insurance

• The Credit Union Share Insurance Fund Parity

Act allows for IOLTA accounts to be federally

insured by the NCUSIF up to the limit allowed by

law;

• The account is insured up to $250,000 per

owner (client) funds in the account;

• NCUA will be issuing regulations to implement

the Act however IOLTA accounts are insured as

of the date of the signing of the Act.

Fixed Assets

Final Rule

• Effective October 2, 2015

• Provides regulatory relief – no FAM

• Eliminates the five percent aggregate limit

• NCUA will oversee ownership of fixed assets

through the supervisory process and guidance

• Changes the partial occupancy requirement

from 3 years to 6 years

Telephone Consumer

Protection Act

FCC Ruling

• FCC rules that you can contact members,

without consent, in the following circumstances:

– Transactions and events that suggest a risk of fraud

or identity theft; (2)

– Possible security breaches of consumers’ personal

information;

– (3) Steps consumers can take to prevent or remedy

harm caused by data security breaches; and

– (4) Actions needed to arrange for receipt of pending

money transfers.

Homeownership Counseling

Interpretive Rule

• Credit unions must provide a list of housing

counselors under RESPA in one of two ways:

• Must generate a list of 10 counselors

– Using the tool located on the CFPB’s website; or

– Using the member’s zip code with data available on

the HUD website;

Information Required

• The following information must be provided to

the member:

– Agency name;

– Phone number;

– Street address;

– City;

– State;

– Zip code;

– Website URL;

– E-mail address;

– Counseling services provided;

– Languages spoken

Quarterly Submission

of Credit Card

Agreements

One-Year Suspension

• The CFPB issued a final rule adopting a one-

year suspension of the requirement for certain

credit card issuers to send their agreements to

the CFPB quarterly. This is effective for the

dates April 30, July 31 and October 31 of 2015

and March 31, 2016. The suspension does not

affect the requirement for issuers to post their

agreements on their websites.

• The requirement to send agreements to the

CFPB applies only to issuers with 10,000 or

more open credit card accounts.

Proposed Rules

Member Business Loan

Proposal

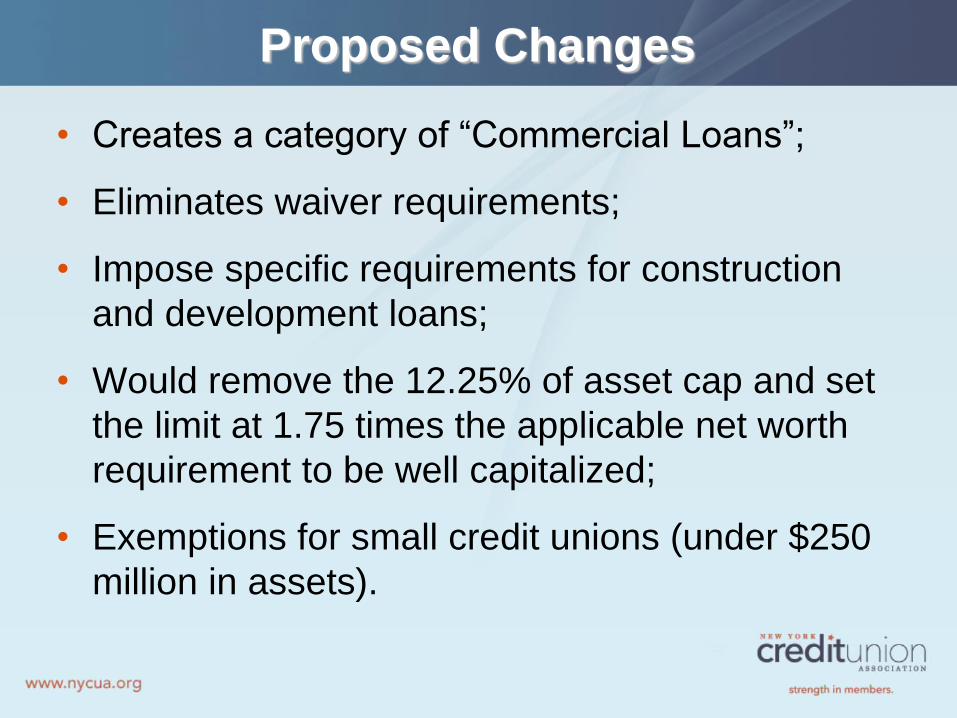

Proposed Changes

• Creates a category of “Commercial Loans”;

• Eliminates waiver requirements;

• Impose specific requirements for construction

and development loans;

• Would remove the 12.25% of asset cap and set

the limit at 1.75 times the applicable net worth

requirement to be well capitalized;

• Exemptions for small credit unions (under $250

million in assets).

Commercial Loans

• “Commercial loans” are defined as any credit extended

to a borrower for commercial, industrial, agricultural, and

professional purposes except:

– Loans made by a corporate credit union;

– Loans made by a federally insured credit union to another

federally insured credit union;

– Loans made by a federally insured credit union to a

CUSO;

– Loans secured by a 1- to 4- family residential property

(whether or not it is the borrower’s primary residence);

Commercial Loans

• Loans secured by a vehicle manufactured for household

use;

• Any loan duly secured by shares in the credit union

making the extension of credit or deposits in other

financial institutions; and

• Any loan to a borrower or an associated borrower, the

aggregate of which is equal to less than $50,000.

Commercial Loans

• Must have a commercial loan policy similar to a

member business loan policy;

• Must have qualified staff;

• Senior executive officers overseeing commercial

loan area;

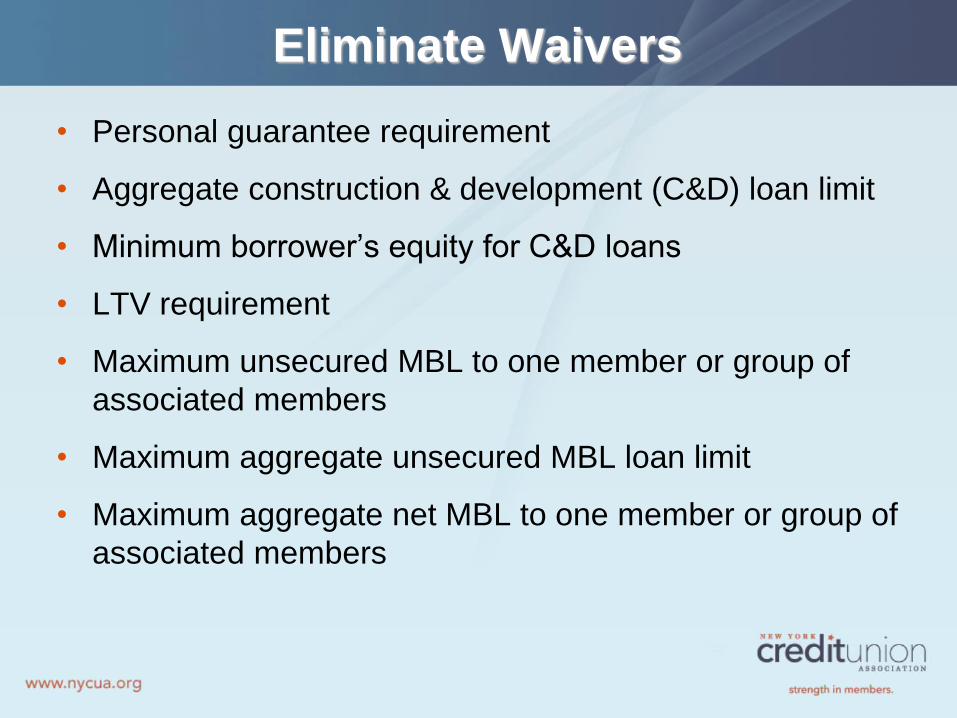

Eliminate Waivers

• Personal guarantee requirement

• Aggregate construction & development (C&D) loan limit

• Minimum borrower’s equity for C&D loans

• LTV requirement

• Maximum unsecured MBL to one member or group of

associated members

• Maximum aggregate unsecured MBL loan limit

• Maximum aggregate net MBL to one member or group of

associated members

Loan Participations

• Nonmember business loan participations will no

longer count against the cap.

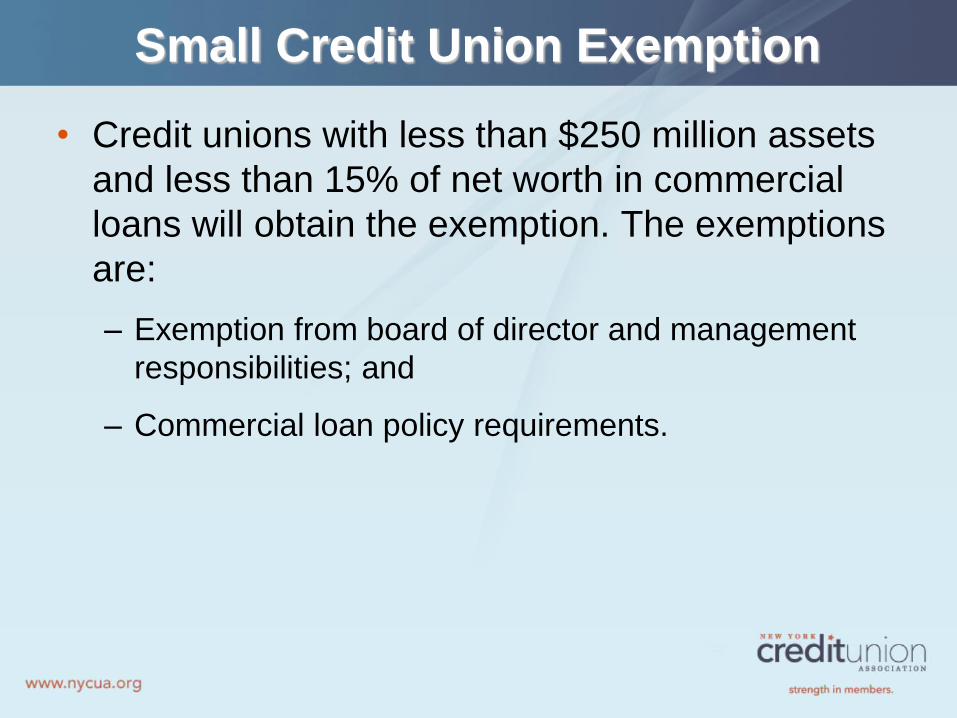

Small Credit Union Exemption

• Credit unions with less than $250 million assets

and less than 15% of net worth in commercial

loans will obtain the exemption. The exemptions

are:

– Exemption from board of director and management

responsibilities; and

– Commercial loan policy requirements.

Regulation CC Proposal

Reg. CC

• Proposed by the Federal Reserve Board

• Required by Dodd-Frank

• Comment period closed May 2, 2014

• CFPB will finalize rule – when? Maybe summer

2015.

• Purpose: to amend Regulation CC to increase

next business day availability and encourage

electronic check processing and returns

Reg. CC

• Specifics:

– Increased the amount of funds available for next day

availability from $100 to $200, July 2011.

– Must update disclosures (model forms available) and

provide change in terms notice

– Only entitled to expeditious check returns (two day

test) if agree to receive returned checks electronically

Reg. CC

• Specifics:

– Additional hold extension shortened from 5 to 2

business days for most checks

– Permits paying institutions for same-day settlement to

require electronic presentment of checks

– Removes references to ‘nonlocal’ checks (due to

consolidation of Federal Reserves check-processing

regions)

– Provides a 12 month safe harbor for credit unions that

use the model forms

Reg. CC

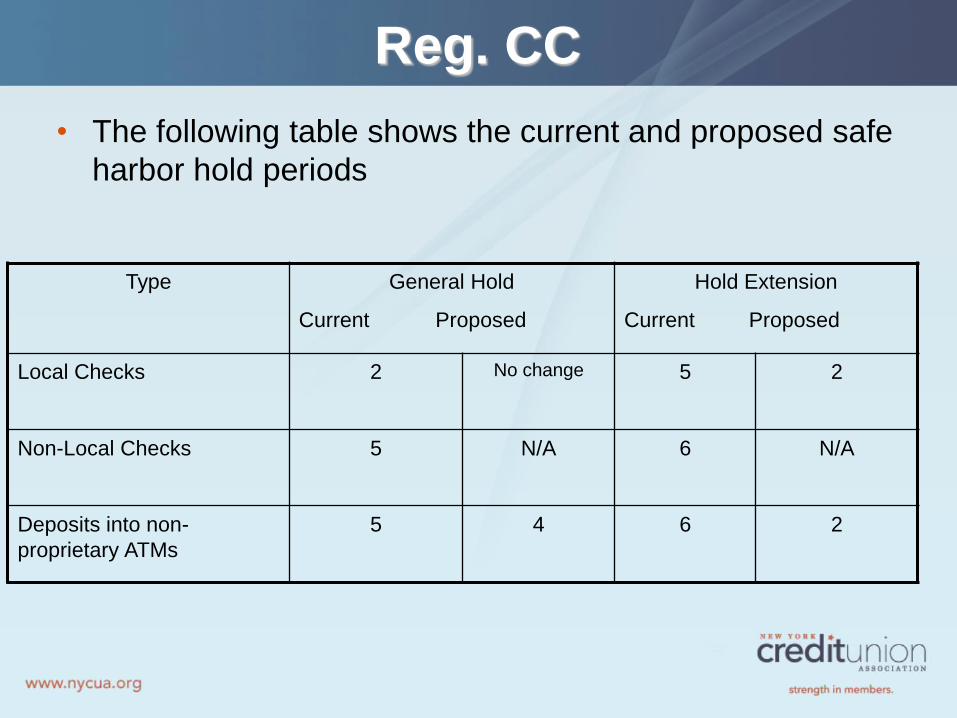

• The following table shows the current and proposed safe

harbor hold periods

Type General Hold

Current Proposed

Hold Extension

Current Proposed

Local Checks 2 No change 5 2

Non-Local Checks 5 N/A 6 N/A

Deposits into non-

proprietary ATMs

5 4 6 2

Remote Deposit Capture

• Remote deposit capture is where a financial institution permits

its member or member to make a deposit by sending an

electronic image of the front and back of a check. For remote

deposit capture, the proposal would allow a depositary

financial institution that accepts deposit of an original check to

recover directly from a financial institution that permitted its

member or member to deposit the check through remote

deposit capture. The Fed believes the depositary financial

institution that accepts an original paper check should not

bear the loss if that check has been deposited multiple times.

The proposal also provides for a new indemnity relating to

remote deposit capture to cover depositary financial

institutions that receive deposit of an original paper check

returned unpaid, because it was previously deposited (and

paid) using remote deposit capture.

Prepaid Accounts

Prepaid Account Proposal

• Would extend to prepaid accounts many consumer

protections under Regulation E and Regulation Z;

• Prepaid card definition –

– A card, code or other device that is not already an account

under Regulation E that is established primarily for

personal, family or household purposes that is “either

issued on a prepaid basis to a consumer with a specified

amount, or not issued on a prepaid basis but capable of

being loaded with funds thereafter and redeemable upon

presentation at multiple, unaffiliated merchants for goods

or services, usable at ATMs or for person-to-person

transfers.

Examples of Covered Prepaid Accounts

• General purpose reloadable cards;

• Certain non-reloadable accounts;

• Payroll cards;

• Certain federal, state and local government

benefit cards;

• Student financial aid disbursement cards;

• Tax refund cards;

• Certain person-to-person products or transfers.

Not Prepaid Accounts

• Gift certificates;

• Store gift cards;

• Loyalty, award or promotional gift cards;

• Certain general use prepaid cards that are both

marketed and labeled as gift cards or gift

certificates.

Consumer Protections

• Easy and free access to account information: Financial

institutions would be required to either provide periodic

statements or make account information easily

accessible online and for free. If issuers choose to not

provide periodic statements, issuers must provide

consumers with their account balances at an ATM or by

telephone, and consumers must have access to an 18-

month history of their transactions. In addition, the

periodic statements, electronic history, and requested

written history of transactions must include disclosures

about fees assessed and a summary of fees assessed.

Consumer Protections

• Error resolution rights: Financial institutions would be

required to work with consumers who encounter errors

with their account (e.g., alleged incorrect amount

charged or multiple charges). The proposed rule

generally extends the protections, timeframes, and

procedures under Regulation E to prepaid accounts.

This includes investigating and resolving errors in a

timely manner. If the financial institution cannot resolve

an alleged error within 10 business days, it would be

required to temporarily credit the disputed amount to the

consumer to use while the institution finishes its

investigation (i.e., provisional credit).

Consumer Protections

• Fraud and lost-card protection: The proposed rule would

protect consumers against unauthorized, erroneous, or

fraudulent withdrawals or purchases, including when

registered prepaid cards are lost or stolen. If consumers

lose their card or find erroneous or fraudulent charges,

the rule would limit their responsibility for unauthorized

transactions and create a timely method for the return of

funds associated with such transactions. The

consumer’s responsibility for unauthorized charges

would be limited if the consumer promptly notifies their

financial institution of any unauthorized transfers within a

60-day period. The proposed rule extends the liability

limits that current apply to payroll cards and government

benefit cards to other prepaid accounts.

Consumer Protections

• Inclusion of All Fees and Regulation DD: The agency

proposes that all periodic statements and histories of

account transactions for all prepaid accounts include all

fees, not just those related to electronic fund transfers

and account maintenance. This is intended to cover

some prepaid accounts that may be covered under

Regulation E but may not be considered accounts under

Regulation DD.

Disclosures

• Proposed Short Form – This would concisely and clearly

highlight key account information, including common

costs such as the monthly fee, fee per purchase (PIN or

Signature), ATM withdrawal costs (in-network or out of

network), and fee to reload cash onto the account.

Consumers would have to receive or have access to a

full set of the account’s fees and related information

before acquiring the account. The short-form disclosure

is required to disclose potential fees, as applicable,

which include: balance inquiry fees; member service

fees; inactivity fees; and any overdraft fees.

Disclosures

• Incidence-based Fees – Financial institutions must also

disclose up to three “incidence-based” fees on the short

form, which are the three fees that are most frequently

incurred during the prior 12-month period by consumers

using a particular prepaid account, excluding fees that

are already required to be disclosed. At the same time

each year as determined by the issuer, the issuer would

need to assess the “incidence based” fees and would be

required to update their disclosures within 90 days.

Disclosures

• Proposed Long Form – This would include all of the fees

on the short form, and any other potential fees that could

be imposed in connection with the prepaid account and

the conditions under which the fees could be imposed.

The long form would include fees charged by a third

party that are known to the financial institution, which

include the amount of the fee and the conditions under

which the fee may be imposed.

Posting Account Agreements

• Posted Account Agreements: Prepaid issuers would be

required to post their account agreements on their own

websites, and would be required to submit those

agreements to the CFPB for posting on a public website

on a quarterly basis. These requirements are generally

similar to the rules under the CARD Act. There is a de

minimis exception for prepaid issuers with less than

3,000 accounts open, or for a single product not offered

to the public other than in connection with a test and with

fewer than 3,000 accounts open. An issuer would also

have to promptly provide a copy of the agreement 5

upon request

• Home Mortgage Disclosure Act

(HMDA)-Proposal

HMDA Proposal

• Proposed changes:

– The tests for determining which institutions are

covered will be revised. Along with the asset

requirement (currently $43 million) the credit union

would also have to have originated 25 covered loans

other than open-end lines of credit and commercial

lines of credit.

– Unsecured lines of credit would no longer need to be

reported

– All closed-end loans, open-end lines of credit and

reverse mortgage secured by a dwelling would be

required to be reported.

– Comment period closed October 29.

HMDA Proposal

• Much more information would need to be reported:

– Applicant age;

– Applicant credit score;

– Debt-to-income ratio;

– Application channel;

– Postal address and location of subject property;

– Property value;

– Points and fees;

– Introductory period;

– Non-amortizing features

HMDA Proposal

• Prepayment penalty;

• Universal loan identifier;

• Reasons for denial;

• Loan term;

• Occupancy type;

• Lien priority;

• HOEPA status;

• Loan type;

• Loan amount;

• Automated underwriting system results.

HMDA Proposal

• Construction method;

• Number of individual units;

• Loan originator identifier; and

• Legal entity identifier.

NCUA’S Proposal on

Risk-Based Capital

Risk-Based Capital

• NCUA issued a proposal in early 2014 that was met with

significant opposition. The proposal would have required

credit unions $50 million and over to have a minimum

10.5% risk-based capital in order to be considered well-

capitalized. The Agency also proposed a number of risk-

weightings to all risk asset accounts. After receiving

more than 2,000 comment letters and numerous letters

from Congress, the Agency issued a new proposal and

comment period.

Risk-Based Capital - 2

• Notable changes:

– Increases asset threshold from $50 million to $100 million;

– Lowers the RBC requirement from 10.5% to 10%;

– Improves the risk weighting in most areas;

– Removes Interest Rate Risk;

– Delays compliance until January 2019.

Issues

• Credit unions appreciate the changes that NCUA has

made, but have not been convinced that NCUA has the

authority or the need to make such changes in this area;

• Raising the threshold for compliance should be raised

even higher than $100 million and should be coupled

with consideration of the types of investment and

activities that credit unions engage in.

Issues

• NCUA should clarify what powers it feels it has to

impose buffer requirements for individual credit unions, if

it feels it has the power to do so, then credit unions

should be provided guidance as to when this power can

be exercised;

• Credit unions are in favor of making the proposal more

complicated if it results in a better RBC framework, for

instance they support creating a category of commercial

loans distinct from member business loans.

Definition of Small

Credit Union

Proposed Rule

• NCUA issued a proposal on at the February

board meeting that would define a small credit

union as one with assets under $100 million as

opposed to $50 million.

• The definition does not have any real effect in

terms of regulatory relief currently but may in the

future.

• This may be a bone of contention with the NCUA

Board.

Looking Forward

Things on the Radar

• CFPB on Mortgage Closings;

• CFPB on Credit Cards;

• Payday loans – already a proposed proposal;

• Overdrafts and checking accounts;

• Privacy legislation;

• CDD under BSA;

Things on the Radar

• NCUA is looking into Field of Membership,

Supplemental Capital and Small Credit Union

Regulatory Relief

Thank You!

Any Questions?