Embed Size (px)

Citation preview

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 1/9

Assignment Assessment Report

Campus: Sainik Farms Year/semester 2011-12

Level: ACL-IIAssignmentType

Assignment B

Module Name: CMBCAssessor’sName

Ms. Monica

Student’sName:

Manish VermaReqdSubmissionDate

e-mail id & MobNo

9899715278/[email protected]

ActualSubmissionDate

Stream Business Submitted to : ewlci

Certificate by the Student:Plagiarism is a serious College offence.I certify that this is my own work. I have referenced all relevant materials.Manish Verma

(Student’s Name/Signatures)

Expected

Outcomes

Assessment

Criteria

Grade

based onD,M,P,Rsystem

Feedback

General ParametersClarity Clear

understandingof the concept

Analytical Thinking-

Ability toanalyze theproblemrealistically

Research Done- Research carried

out to solve theproblem

Formatting &Presentation-

Concise& clearthinking alongwithpresentation

Subject Specific Parameters

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 2/9

Assignment Grading Summary (To be filled by the Assessor)OVERALL ASSESSMENTGRADE:

TUTOR’S COMMENTS ONASSIGNMENT:

SUGGESTED MAKE UP PLAN(applicable in case thestudent is askedto re-do the assignment)REVISED ASSESSMENTGRADETUTOR’S COMMENT ONREVISEDWORK (IF ANY)

Date: Assessor’s Name / Signatures:

Assignment B

Ques 1 : Each student will be given one of the under mentionedindustry for assignment work.

• Education Industry

• Manufacturing Industry• Hospital Industry

• IT Industry

• Transport Industry

The students will have to visit a company from the assigned industry,meet the Accounts person and do the following:-

a. Find out and understand the Cost procedures followed by thecompany.b. If possible get a sample of cost sheet or Statement of Accounts

A presentation on the above and recommendation for areas of improvement has to be made.

Ans. Manufacturing Industry- Nestlé India Ltd.

Profile: Nestle India is a subsidiary of Nestle S.A. of Switzerland. NestleIndia manufactures a variety of food products such as infant food, milkproducts, beverages, prepared dishes & cooking aids, and chocolates &confectionary. Some of the famous brands of Nestle are NESCAFE,

Grades Grade DescriptorsAchieved Yes/No(Y / N)

PA Pass grade is achieved by meeting all the requirementsdefined.

MIdentify & apply strategies/techniques to find appropriatesolutions

D Demonstrate convergent, lateral and creative thinking.

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 3/9

MAGGI, MILKYBAR, MILO, KIT KAT, BAR-ONE, MILKMAID, NESTEA,NESTLE TOMATO KETCHUP, NESTLE Milk, NESTLE SLIM Milk, NESTLEFresh 'n' Natural Dahi and NESTLE Jeera Raita Cost procedure followed in Nestlé India Ltd.- TOMATO KETCHUPAnd CHOCOLATESA company’s production process helps in determine the best way of accounting for its costs. Process costing works well whenever relativelyhomogeneous products pass through a series of processes and theyreceive similar amount of manufacturing costs. Nestle accounts for its

vast chocolate chips production by using a process costing system.Sequential Processing: The units typically pass through a series of manufacturing or producing departments, in each departments orprocess is an operation that brings the product one step closer tocompletion.

Parallel Processing: This pattern require two or more sequentialprocesses to produce the finished goods. Partially completed units areworked on simultaneously in different processes and then broughttogether in a final process for completion.

FLOW OF MANUFACTURING COSTS THROUGH THE ACCOUNTS OFPROCESS COSTING(Tomato Ketchup)

Picking Department

Work in Progress

Flavoring Department

Work in Progress

Bottling Department

Work in Progress

Materials:Fresh tomatoes

Sugar

SaltDistillation –

Vinegar

Spices

Picking labour

Applied Overhead

Transferred in from picking (includes all

manufacturing costs)

Materials:

Ketchup

Flavoring Labour Applied Overhead

Transferred in fromFlavoring (includes

all manufacturing

costs from pickingand flavoring)

Materials:

BottlesBottling Labour

Applied Overhead

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 4/9

COST SHEET

Nestle India Ltd. (Chocolates)

Total output= 4,50,000 unitsParticulars Cost per unit Total CostRaw Material:Cocoa Butter=3,00,000Sugar=3,00,000Cocoa Solids= 3,20,000Peanuts= 2,00,000 5.16 23,20,000Chocolate coated resins= 4,00,000Almonds= 3,00,000Vanillin= 1,00,000

Honey=50,000Boston Baked Bean= 1,50,000

Direct Labour=7,00,000 1.56 7,00,000Carriage on Material= 2,42,500 0.53 2,42,500

Prime Cost 7.25 32,62,500Factory Expenses :Fixed:Depreciation on Plants &Machinery=2,57,500Rent= 1,50,000Power & ConsumablesStores=1,50,000Factory insurance=1,50,000Supervisors Salary=50,000 2.35 10,57,500

Variable:Electricity charges=50,000Power & Consumable stores=1,00,000Running Expenses of machines=1,50,000

Factory Cost 9.60 43,20,000Office Administration Expenses

Office staff salary=10,00,000Rent= 80,000Computer=1,20,000Furniture=3,00,000 4.40 19,80,000Telephone= 10,000Carriage outward=20,000Depreciation on furniture=50,000Salaries of administrative =3,70,000Rent, rates & taxes=30,000Office and Administration costs 14.00 63,00,000Selling & Distribution Expenses

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 5/9

Advertisement(print & local TVchannel)=4,00,000Petrol=1,00,000 2.00 9,00,000Delivery Vehicles=2,50,200Maintenance of deliveringVehicles=2,50,200Packing rates= 50,000Bad Debts written off= 1,00,000

Total Cost 16.00 72,00,000

Net Profit (20% on selling price) 4.00 18,00,000

Sales20.00 90,00,000

Ques 2 :1. Discuss the technique of marginal costing as a key for managementproblems.

2. The following is the trading and profit and loss account of M/s PremIndustries for the year ende2d 31 st March 2000.

To Material consumed 708000 By Sales 30000 units 1500000

To Direct wages 371000By Finished Stock (1000units) 40000

To Works overhead 213000 By work-in-progress

To Administration overheads 95500 Material 17000 To Selling & distributionoverheads 113500 Wages 8000

To Net profit for the year 69000 Works Overhead 5000

1570000 1570000

In manufacturing a standard unit, the company’s cost records show that:

a. Work overhead have been charged to work-in-progress at 20% on primecost.b. Administration overheads have been recovered as Rs.3 per finished unit.c. Selling and distribution overheads have been recovered as Rs.4 per unitsold.d. The under-absorbed or over-absorbed overheads have not been adjustedinto the costing P & L a/c.

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 6/9

Prepare:

1. A costing profit & loss account indicating net profits.2. A Statement reconciling the profit as disclosed by the cost accounts andthat

Shown in the financial accounts.

Ans.Techniques of Marginal costing:

Profit/volume ratio (P/V Ratio)When the contribution from sales is expressed as a percentage of salesvalue, it is known as Profit/Volume ratio (or P/V ratio). It expressesrelationship between contribution and sales. Better P/V ratio is an indexof sound ‘financial health’ of a company’s product. This ratio reflectschange in profit due to change in volume. Broadly speaking, it showshow large the contribution will appear, if it is expressed on equalfooting with sales.

P/V ratio may be expressed as:P/V ratio = (Sales - Marginal cost of sales)/Sales

or = Contribution/Salesor = Change in contribution/Change in salesor = Change in profit/Change in sales

Marginal Costing and CVP AnalysisCost-Volume -Profit analysis is an important tool for profit planning. Itprovides information about the following matters:

a) The behavior of cost in relation to volume.b) Volume of production or sales, where the business will break-

even.c) Sensitivity of profits due to variation in output.d) Amount for profit for a projected sales volume.e) Quantity of production and sales for a target profit level.

Cost-Volume-Profit analysis may therefore be defined as a managerialtool showing the relationship between profit planning, viz., cost (both

fixed and variable), selling price and volume of activity.

Break –Even AnalysisBreak-even analysis is a widely used technique to study Cost-volume-profit relationship. The narrower interpretation of the term Break evenanalysis is defined as a system of determination of that level of activitywhere total cost equals total selling price.The broader interpretationrefers to that system of analysis which determines probable profit atany level of activity.

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 7/9

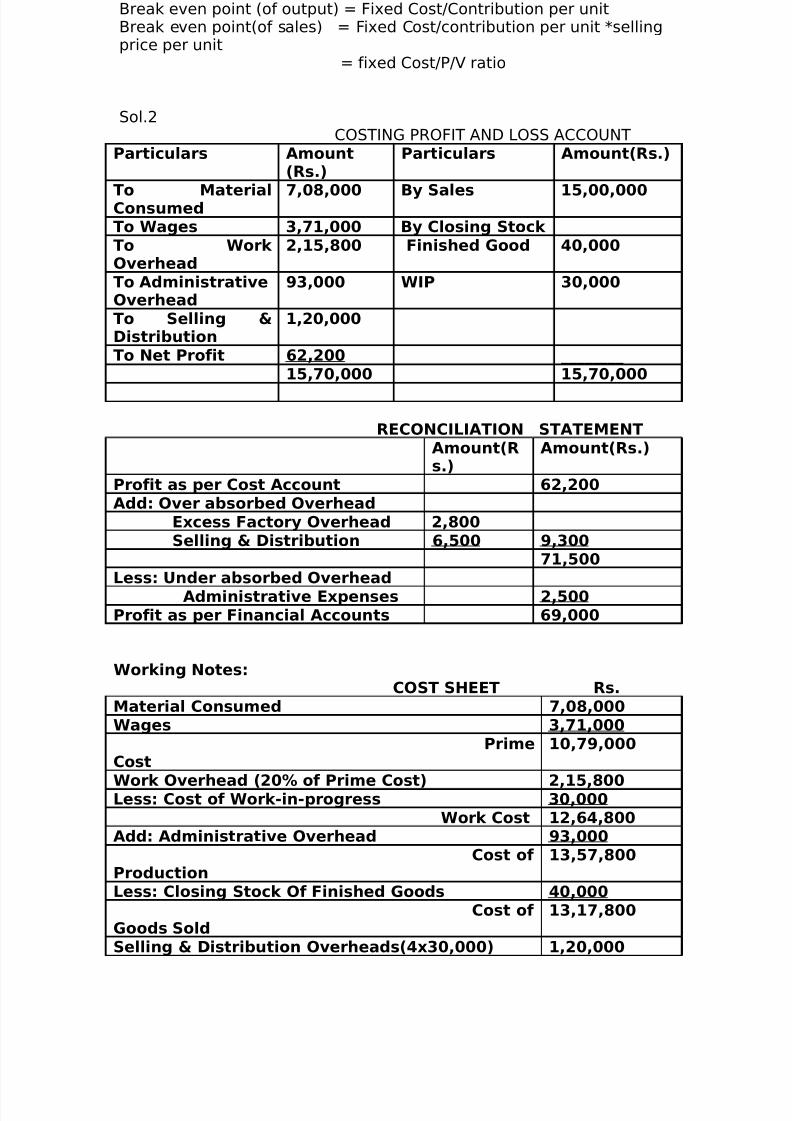

Break even point (of output) = Fixed Cost/Contribution per unitBreak even point(of sales) = Fixed Cost/contribution per unit *sellingprice per unit

= fixed Cost/P/V ratio

Sol.2COSTING PROFIT AND LOSS ACCOUNT

Particulars Amount(Rs.)

Particulars Amount(Rs.)

To MaterialConsumed 7,08,000 By Sales 15,00,000

To Wages 3,71,000 By Closing Stock To Work Overhead

2,15,800 Finished Good 40,000

To AdministrativeOverhead

93,000 WIP 30,000

To Selling &Distribution

1,20,000

To Net Profit 62,200 ________15,70,000 15,70,000

RECONCILIATION STATEMENTAmount(Rs.)

Amount(Rs.)

Profit as per Cost Account 62,200Add: Over absorbed Overhead

Excess Factory Overhead 2,800Selling & Distribution 6,500 9,300

71,500Less: Under absorbed Overhead

Administrative Expenses 2,500Profit as per Financial Accounts 69,000

Working Notes:COST SHEET Rs.

Material Consumed 7,08,000Wages 3,71,000

PrimeCost

10,79,000

Work Overhead (20% of Prime Cost) 2,15,800Less: Cost of Work-in-progress 30,000Work Cost 12,64,800

Add: Administrative Overhead 93,000Cost of

Production13,57,800

Less: Closing Stock Of Finished Goods 40,000Cost of

Goods Sold13,17,800

Selling & Distribution Overheads(4x30,000) 1,20,000

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 8/9

_________Cost of Sales 14,37,800

Profit 62,200

Sales 15,00,000

Total Finished good units during the year = Unit sold-Openingstock + Closing stock = 30000 - 0 + 1000

= 31000Administration overheads have been recovered as Rs.3 perfinished unit= 31000*3= 93000

Ques 3 :

Work out in appropriate cost sheet from the unit cost per passenger km for

the year 2006-07 for a fleet of passenger buses run by a Transport Companyfrom the following figures extracted from its books.

5 passenger buses costing Rs.50000, Rs. 120000, Rs. 45000, Rs.55000 andRs.80000 respectively. Yearly depreciation of vehicles 20% of the cost.Annual repair, maintenance and spare parts – 80% of depreciation. Wages of 10 drivers @ Rs.100 each per month, wages of Rs.20 cleaners @ Rs. 50 eachper month. Yearly rate of interest @ 4%on capital. Rent of six garages @Rs.50 each month. Director’s fees @ Rs.400 per month, office establishment@ Rs.1000 per month, licences and taxes @ Rs.1000 every six months,realization by sales of old tyres and tubes @ Rs.3200 every six months, 900passengers were carried over 1600 kms during the year.

Sol.Cost of buses= Rs. 50,000 + 1,20,000 + 45,000 + 55,000 + 80,000

= Rs. 3,50,000

Yearly Depreciation(20% of cost) = Rs. 70,000Yearly Repairs(80% of Depreciation) = Rs. 56,000

Operating Cost- Sheet

For the year 2006-07

Particulars Amount (Rs.) Amount (Rs.)

(A)Standing Charges

Wages of

drivers(10x100x12)

12,000

Wages of cleaners

(20x50x12)

12,000

____________ 24,000

Interest(4% on capital) 14,000

Directors fees(Rs.400x12) 4,800

Licence & Taxes(Rs.

1000x2)

2,000

8/6/2019 ACL_II_Assignment_B_CMBC

http://slidepdf.com/reader/full/acliiassignmentbcmbc 9/9

Office establishment(Rs.

1000x12)

12,000

Garage rent(6x50x12) __ 3,600

60,400

(B) Maintenance Charges

Repairs, Spare parts etc. 56,000

(-) Sale proceeds from oldtyres & tubes

6,400

___________

49,600

(C) Operating ChargesDepreciation 70,000

Total(A+ B + C) 1,80,000

(E)Passenger Km.

Carried(900x1600)

14,40,000

(F) Cost per passenger Km.

Rs.(1,80,000/14,40,000) 0.125