Embed Size (px)

Citation preview

1

FRAUD Detection & Incident Response

for Fraud Examiners & Auditors

ACFE Omaha Chapter

June 30, 2020

John J. Hall, CPA [email protected]

(312) 560-9931 www.FraudPreventionPro.com

Precision & Clarity

• Thinking • Planning • Actions • Solutions

2

$2.75 FARE EVASION

3

9

Estimated ‘Fraud’ Losses

Most Recent Fiscal Year

$ ________

POP QUIZ #1

Types of fraud that account

for most of your losses

POP QUIZ #2

11

Fraud Loss Scorecard HIGH LOW

1 Disbursements $ XXX $ XXX 2 Inventory

3 Construction/Facilities

4 Health Care Costs

5 Payroll

6 T&M contracts

7 T&E reimbursement

8 Other – Unique to You

TOTAL $ XXX $ XXX

12

Fraud Loss Scorecard HIGH LOW

1 Disbursements $ XXX $ XXX 2 Inventory

3 Construction/Facilities

4 Health Care Costs

5 Payroll

6 T&M contracts

7 T&E reimbursement

8 Other – Unique to You

TOTAL $ XXX $ XXX

4

13

ACFE.com

14

Fraud Loss Scorecard HIGH LOW

1 Disbursements $ XXX $ XXX 2 Inventory

3 Construction/Facilities

4 Health Care Costs

5 Payroll

6 T&M contracts

7 T&E reimbursement

8 Other – Unique to You

TOTAL $ XXX $ XXX

1%2% 1%

15 16

DETECTED

NOTDETECTED

5

17

#1: Shrink the Pie

18

#2: Find More of What’s Left FASTER

DETECTED

19

1. Managers and staff 2. Examiners & internal audit 3. External auditors 4. Other third parties 5. The thief (fraudster) 6. Luck or accident

How Fraud is Found

1. Deterrence and Prevention

2. Early Detection

3. Effective Handling

Fraud Risk Management Framework

ORGANIZATIONS MUST BE PREPARED AT ALL THREE LEVELS

6

1. Deterrence and Prevention

2. Early Detection

3. Effective Handling

Fraud Risk Management Framework

ORGANIZATIONS MUST BE PREPARED AT ALL THREE LEVELS

Law Enforcement

Insurance Company

Control Weakness

Audit

Exception

Pattern

Review Of Records

Interviews

Interrogation

Tip

Case File

Bonding Claim

Audit Report

DetectionMode

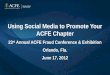

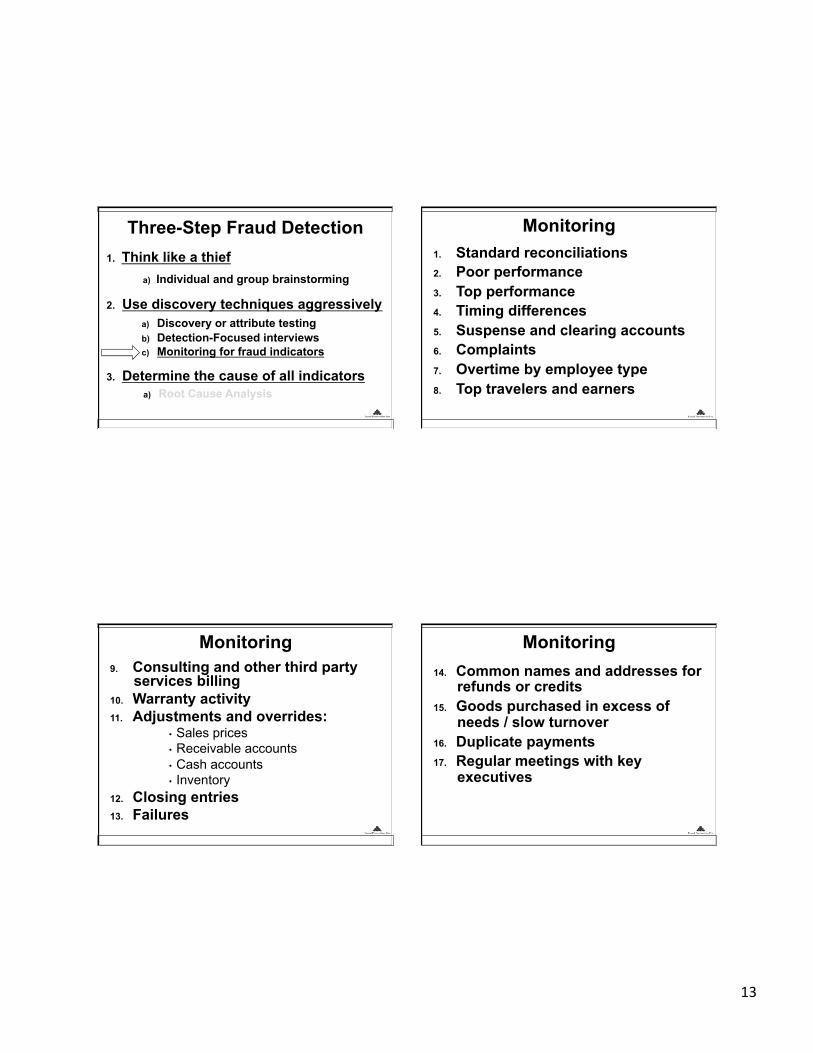

Three-Step Fraud Detection 1. Think like a thief

a) Individual and group brainstorming

2. Use discovery techniques aggressively a) Discovery or attribute testing b) Detection-Focused interviews c) Monitoring for fraud indicators

3. Determine the cause of all indicators a) Root Cause Analysis

Three-Step Fraud Detection 1. Think like a thief

a) Individual and group brainstorming

2. Use discovery techniques aggressively a) Discovery or attribute testing b) Detection-Focused interviews c) Monitoring for fraud indicators

3. Determine the cause of all indicators a) Root Cause Analysis

7

Fraud Risk Brainstorming:

Think Like A Thief (when we don’t know how)

THE CHALLENGE

W.C.G.W. What Could Go Wrong

W.W.I.L.L. What Would It Look Like

Ask and Answer

The Beauty of “Hey Boss!” Questions

Easy Path to Clarity …begin (plan)

with the PRESUMPTION

that a fraud event has already occurred

THE SECRET SAUCE

8

Assume you are committing

the fraud

THE SECRET SECRET SAUCE

Commit Convert Conceal

THE THREE C’s

RED FLAGS

Observablesignsinrecordsorbehaviors

Nature Extent Timing

Backend of Brainstorming

9

Really Getting Probabilities

2 x Sauce + 3C + N.E.T.

Three-Step Fraud Detection 1. Think like a thief

a) Individual and group brainstorming

2. Use discovery techniques aggressively a) Discovery or attribute testing b) Detection-Focused interviews c) Monitoring for fraud indicators

3. Determine the cause of all indicators a) Root Cause Analysis

Discovery- Based Tests

A

B

C

ALL TRANSACTIONS

OK

KNOWN PROBLEMS

HIDDEN PROBLEMS

10

Create ‘Valid’ Tests 1. There are only two types of samples:

ü Valid ü Invalid

2. Constant focus on test ‘purpose’ 3. Should answer “Do we have this

issue?” 4. Make sure every sample chosen has

a ‘valid’ chance of success

Fraud Risk

Cash Disbursements – Fake Vendor: • Fake documents are introduced

into the payments system, • The invoice is from a “consultant”

for “services rendered” • Approval signatures are forged • Funds are disbursed by check, • The check is deposited into the

personal checking account of a volunteer

• The transaction is charged to Consulting Expenses in the accounting system

Fraud Risk

Cash Disbursements – Fake Vendor: • Fake documents are introduced

into the payments system, • The invoice is from a “consultant”

for “services rendered” • Approval signatures are forged • Funds are disbursed by check, • The check is deposited into the

personal checking account of a volunteer

• The transaction is charged to Consulting Expenses in the accounting system

Indicator

Symptoms

Red Flags

What would it LOOK like?

Fraud Risk

Cash Disbursements – Fake Vendor: • Fake documents are introduced

into the payments system, • The invoice is from a “consultant”

for “services rendered” • Approval signatures are forged • Funds are disbursed by check, • The check is deposited into the

personal checking account of a volunteer

• The transaction is charged to Consulting Expenses in the accounting system

Indicator

• Generic looking invoice • Unknown vendor / contractor • Address:

ü Same as employee or volunteer ü PO Box ü “Mailboxes, Etc.”, etc. ü “Hold check for pickup”

• No phone number on invoice • Unknown charges on cost

center reports • Check:

ü Clears too fast ü Funny endorsements ü Geography

(AICPA, ACFE, IIA, others)

11

Detection Steps

Indicator

Fraud Risk

Cash

Disbursements – Fake Vendor: • Fake

documents are introduced into the payments system,

• The invoice is from a “consultant” for “services rendered”

• Approval signatures are forged

• Generic looking invoice

• Unknown vendor / contractor

• Address: ü Same as employee or volunteer

ü PO Box ü Mailboxes, Etc.

ü Prison… ü “Hold check for pickup”

• No phone number on invoice

A

Detection Steps

Indicator

Fraud Risk

Cash

Disbursements – Fake Vendor: • Fake

documents are introduced into the payments system,

• The invoice is from a “consultant” for “services rendered”

• Approval signatures are forged

• Generic looking invoice

• Unknown vendor / contractor

• Address: ü Same as employee or volunteer

ü PO Box ü Mailboxes, Etc.

ü Prison… ü “Hold check for pickup”

• No phone number on invoice

• Reconcile all bank accounts immediately upon receipt of the bank statement

• Examine all cancelled checks • Periodically review all vendors

and contractors for existence and legitimacy

• REVIEW ALL MONTH END TRANSACTION REPORTS 100%

• “Positive Pay” • Use Computer Data Mining

Techniques to Surface Fraud Indicators

Detection Steps

Indicator

Fraud Risk

• Reconcile all bank accounts immediately upon receipt of the bank statement

• Examine all cancelled checks

• Periodically review all vendors and contractors for existence and legitimacy

• REVIEW ALL MONTH END TRANSACTION REPORTS 100%

• “Positive Pay” • Use Computer Data Mining

Techniques to Surface Fraud Indicators

Cash Disbursements – Fake Vendor:

• Fake documents are introduced into the payments system,

• The invoice is from a “consultant” for “services rendered”

• Approval signatures are forged

• Funds are disbursed by check,

• The check is deposited into the personal checking account of a volunteer

• The transaction is charged to Consulting Expenses in the accounting system

• Generic looking invoice • Unknown vendor /

contractor • Address:

ü Same as employee or volunteer

ü PO Box ü Mailboxes, Etc. ü Prison… ü “Hold check for

pickup” • No phone number on

invoice • Unknown charges on cost

center reports • Check:

ü Clears too fast ü Funny endorsements ü Geography

12

Three-Step Fraud Detection 1. Think like a thief

a) Individual and group brainstorming

2. Use discovery techniques aggressively a) Discovery or attribute testing b) Detection-Focused interviews c) Monitoring for fraud indicators

3. Determine the cause of all indicators a) Root Cause Analysis

Four Powerful Words

“Tell me what happened”

Powerful Follow-Up Question

“How could we prove that?”

ACFE Self Study “Finding the Truth”

www.ACFE.com

A Great Resource

13

Three-Step Fraud Detection 1. Think like a thief

a) Individual and group brainstorming

2. Use discovery techniques aggressively a) Discovery or attribute testing b) Detection-Focused interviews c) Monitoring for fraud indicators

3. Determine the cause of all indicators a) Root Cause Analysis

1. Standard reconciliations 2. Poor performance 3. Top performance 4. Timing differences 5. Suspense and clearing accounts 6. Complaints 7. Overtime by employee type 8. Top travelers and earners

Monitoring

9. Consulting and other third party services billing

10. Warranty activity 11. Adjustments and overrides:

• Sales prices • Receivable accounts • Cash accounts • Inventory

12. Closing entries 13. Failures

Monitoring 14. Common names and addresses for

refunds or credits 15. Goods purchased in excess of

needs / slow turnover 16. Duplicate payments 17. Regular meetings with key

executives

Monitoring

14

Three-Step Fraud Detection 1. Think like a thief

a) Individual and group brainstorming

2. Use discovery techniques aggressively a) Discovery or attribute testing b) Detection-Focused interviews c) Monitoring for fraud indicators

3. Determine the cause of all indicators a) Root Cause Analysis

Determine the Real Cause

of Indicators

Root Cause Analysis

If a condition exists is interesting

Why it exists is important

Root Cause Analysis 1. What happened? 2. What were the root causes?

===============================================================

3. What options are available that will deal with the problem?

4. What is the cost of acting upon each of the available options?

5. Which decision options will provide the best solution?

15

Three-Step Fraud Detection 1. Think like a thief

a) Individual and group brainstorming

2. Use discovery techniques aggressively a) Discovery or attribute testing b) Detection-Focused interviews c) Monitoring for fraud indicators

3. Determine the cause of all indicators a) Root Cause Analysis

Go DEEP

Purchasing Cards ‘The 3 C’s’

Commission Conversion

Concealment

16

I . ,IIi

l.. t

dst41;ut i r " ' i ' : ' i l re l { r r ' *_ ' - \ l

,

THI ' t , inr t 'ot*ot 0554-,,11['F riiiailipn xs. inrn]ncr.cA.e0040(?lir'trt:iit^irii*'i-o - - "' - iszs:,t z7 -e500

0554 000?2 07785 0?128105'SALE

vsra v---- iHiizu o5:06 Pl'l

THE Hsl4E DE PEIT o6q1zdri't rliEsR'tptl RD. colll'lERcE'94,?0919-iiofir-ionldnec ttunro (323)727'e500

0554 00022 9s228 03/14106SAIE 51 JC45X0 01:58 Pl' l

}lr 2\tu459. 00

'3 .843.493.99

470,3238.80

$509,12509.12

4TA

II

II

II

iIIIIIlkI r lIi

8lll83iffiffi l5i?;[li'?i82 0 r .92

037U004e9029 0lJ'lN 38037000800E8? uornSir?3r^,-

s{LEs IAXTOTAL

xxxn0fixxxxloo7 Al{EXluttt coor s39593/8221858

NOht IIIRIIIG SPRING 5EASON ASSOCIATESpiiir"iFilv ToDAv IN-sToRE 0R 0N-LINEiri r' iionrc,tnEERs. HoI'IEDEP0I . c0l'l/HouRLY

*Ii******* i*** f ,**** ********* ***** * * * ** *

ENTER FgR A CHAHCE--rs wrt l A $s r 999nOr.te DEPOT GI FT

CARtr g

Ycur Oplnlon Counts! He vould l lks t0herr about your shopping sxp€r l6nce'

Enter to v1n a $5'000 I ' lone uepot hlr tc i i i -uv- iotplEt lns a br lef survev about

Your store v ls l t at l

r lvt.HomeDePctOPi ni on' com

Vou vi l l need the-fol lovlng to enteron- t I n0:

User IDIL3L399 7"TJ's767

Pae surqrcl :6164 L90745

Entr les nust be entEred bv 04/13/2006'E'i i i ' i t i . must be lts or older to enter'-" i ie- ' iomptt te rul€s on vEbsl te ' No

Purchase ngcqssarY'

(Estr cncuesta tanbl6n se encuentra.en' i l i lni i- . .- i i piglna del internet')

nqnoztrr53s8 2 GAL vAc::H ;'.i;'r;to 7 1 /4t{Rl{onvsflX;i;i;3;tb,'d so5 CLE^NERXiiliiirrose PflB.Bnool.lX::;t;;;iits tgv E TooL Kusqe. ' '?r- ' SUBT0TAL

SALES IAXTOT,\L

H+lY[ily{igBl,,!}EIu,u

99.00159.00

?.8829,97

629.00'919.9s75.89

$9.95.74995.74'

^ IA,iltHltlt!iltt[![wl illll

:: jtt;1tilrit{,l!.,$ifl filri#'\Tlu,'rlt"ffi"Hol'lE BFE" t

Your Opinion Counts! lie vould ll!:^to,*r tr11i:* if ltllllx*:f :iii.card bv *}:l:tlH.l iisrt at:

v,rv.HoneDePotOPl nl on ' cottt

Vou vlll "".0 lll,lillovlns to enter

User ID:1t ' -5t3 a5€!41

Pa'seurr>rcl ;dT?e l545e

Etlil;i,'xi:fi #i'"r::"**l ill -:."'Seg co$Plcts rulgs oPurchase necessdrY',

,Esta encuesE l*?l:"d:i il?lilllill-'' . , . r . . - IA rrqlna

{

,1 )

i

I

Dallas ISD Purchasing Cards

“Secretary charges

$383,788, has no receipts”

Dallas Morning

News July 2, 2006

Web Search by Yahoo!

Search Blog Keywords

Comments You may comment, if you are logged in, with any of the following:

Home > Education Blog

Dallasnews.com is now using Facebook Comments, but users of the Education Blog may log in using a few other services, too. To use another service,you first will need to log out of Facebook. Comments are subject to Facebook's Privacy Policy and Terms of Service on data use. If you don't want your comment toappear on Facebook, uncheck the 'Post to Facebook' box. To find out more, read the FAQ.

News Sports Business Entertainment Life Health Travel Opinion Autos Real Estate Jobs Shopping Classifieds

Elections Weather Traffic Investigations Obituaries Celebrations Photos Video Blogs eBooks Contact Us Subscribe

By Tawnell [email protected]:52 pm on April 29, 2009 | Permalink

comments (0)

DISD auction of p-card repos has ended

DISD’s auction of p-card repos ended today. In all, it lookslike the district made $12,175 off the loot. The diamondjewelry set (pictured at right) brought in the most moneyat $2,900. Other items that sold on the high end include adiamond ring ($850) and a diamond bangle bracelet($550).

But the amount made from the auction barely puts a dentin the amount of money that Gloria Orapello, a formerDISD secretary, owes for abusing her district credit card.Orapello was sentenced to a year in prison and ordered tomake $100,000 restitution to the district. Some of theauctioned items were illegally purchased by her.

The 72 items that were up for bid were turned over toDISD by the FBI. The district will keep the money madefrom the auction and proceeds from the sale will reducethe restitution owed by that amount.

This entry was posted in Waste and abuse and tagged P-card auction by Tawnell Hobbs. Bookmark the permalink[http://educationblog.dallasnews.com/2009/04/disd-auction-of-p-card-repos-h.html/] .

00 0

17

Purchasing, Accounts Payable &

Vendor Fraud

RED FLAGS

Observablesignsinrecordsorbehaviors

Wrongdoing and

Bad Practices Often Look The Same

ü ValidbusinesslicenseandTINü Sentonelowvalueitemü UPSreceipt–Falsesecurity

18

Phantom or Fake Vendor

My Favorite

Charity Adams +2 = $540,000

Only One Supplier

The Controller

19

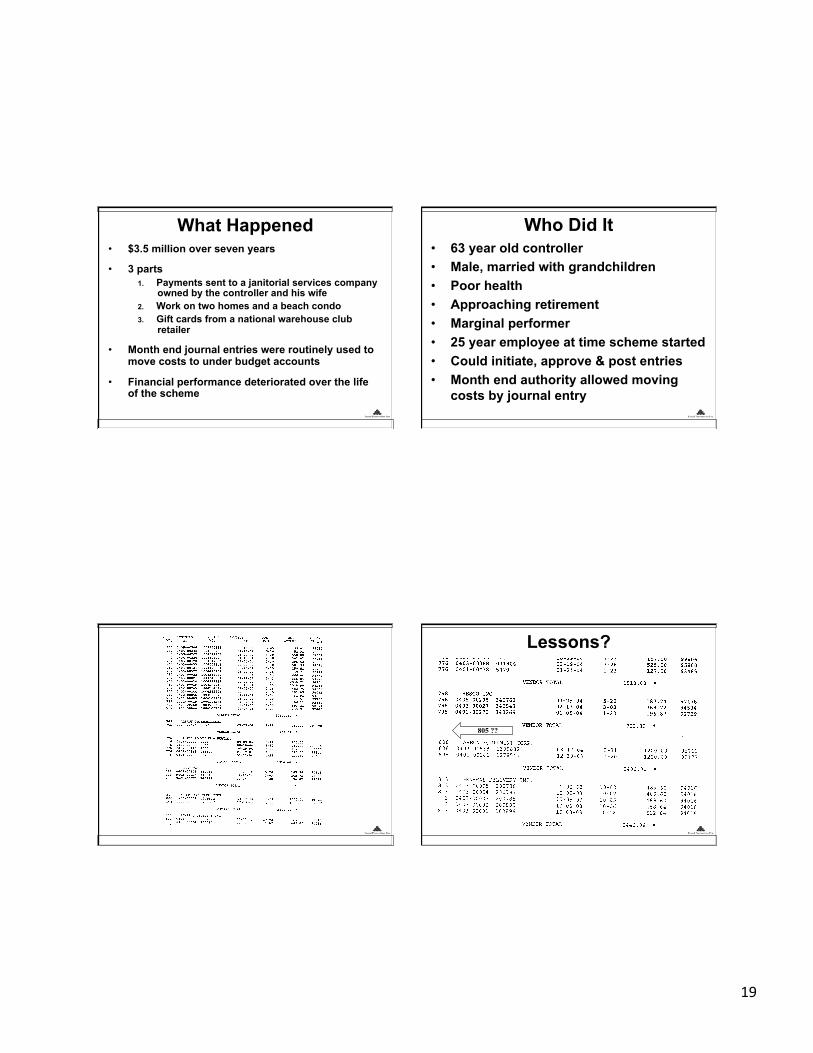

What Happened • $3.5 million over seven years

• 3 parts 1. Payments sent to a janitorial services company

owned by the controller and his wife 2. Work on two homes and a beach condo 3. Gift cards from a national warehouse club

retailer

• Month end journal entries were routinely used to move costs to under budget accounts

• Financial performance deteriorated over the life of the scheme

Who Did It • 63 year old controller • Male, married with grandchildren • Poor health • Approaching retirement • Marginal performer • 25 year employee at time scheme started • Could initiate, approve & post entries • Month end authority allowed moving

costs by journal entry

VEITDORNO.

767767

;77

767767767767767767767767767767767'7 67767'7 67'767

769769

REGISTERNO.

IIr,11/OICENO.

0405-00345 L0047505850405-00238 10046587950405 -a0202 10046993020404 -00320 10046242980403 -04470 10043470960403-00433 10045023450403 -00421 10044955510403-00327 L0044863610403-00022 1004341-0340403 -00021 10043400510403-00020 r_0042694tt0403-000r_9 L0042767t3o402-00245 L0042546j.7o402-00244 L0042s292L0402-00055 L0042035760401-00505 10041583610401-00419 1004]- t42760401 -00260 1003911307040r_-00044 1004100367

VENDOR

ALBA}IY INTERNATIONAL0408-00404 31871_

09-09-0408-r_8-0406-29-0403-19-0407-2L-04

VENDOR TOTAL

03-25-0402-L7 -0401-05-04

VENDOR TOTAL

nav5-Lt-u+Lz- r>-u3

VENDOR TOTAL

INC.10_02_0310_02_0310_05_0310_05_0310_08_03

VENDOR TOTAL

NETAMOUNT

33.41az.rL

550.00342 .42295 .63501.33r50.51

39.7t666.84666.84

2836.7L1048.98

482,75181.05

6t- .011r.4 .5L

96.31592.2L258.9L

L2t42.37

239 . OL

239.0L *

4s0.00250.00157.50525.00L27.50

1510.00 *

787 .74368.72]-96 .87

753 .33 *

1200.001200.00

2440 .00 *

489.60489 .60489.60458 .645r2 .64

2440 .08 *

ITirVOICEDATE

05-14-0404-26-0405-04-0404-19-0402 -24- 0403-24-0403 -23 - 0403-22-0402-23 - 0402 -23 - 0402-09-0402-10-0402-05-0402-05-040]--27 -04ot-20 - 0401-09-04r_1- 07 - 0301-07-04

TOTAL

07 -23-04

DUEDATE

E AP3-Z)5-205-204-303-303-303-303 -263-033-033-033-03z- L62-!62-04r_-30]--2Lr-201- 13

8-31

9-248-307 -23

. 3-26L-23

5-203-03L-20

J-JI-

L-20

70-02LV-VZ

10-0510-0510-08

CHECKIF PAI

980309733397 66L97 04495A299603 r95955958 999477t9477L9420L94258940329403293550933 559286092!9492860

10L190

L0L97 69990695800934 85

97J,7 g9453492729

>) I LI92l-7 1

94016940I6:r.* u .L b940r5944l-6

VENDOR TOTAL

-',16 WINTER PI.JUMBTNG & HEATING5 0409-00200 4to4

. t6 0408-00352 5844776 0407 -00140 4037776 0403-00368 031_904776 0401-00438 5470

798 HESCO INC.798 0405-00206 340763798 0403 -00027 340543798 0401 -00275 340269

808 ARBON EQUIPMENT CORP.808 0403-00538 1309832B0B 0401-00281 1278547

813 GENERAL DELIVERY813 0403-00005 200786813 0403-00004 200'781

3 0403-00003 2aff i88,3 0403-00002 200895

813 0403-0000r 200895

VEITDORNO.

767767

;77

767767767767767767767767767767767'7 67767'7 67'767

769769

REGISTERNO.

IIr,11/OICENO.

0405-00345 L0047505850405-00238 10046587950405 -a0202 10046993020404 -00320 10046242980403 -04470 10043470960403-00433 10045023450403 -00421 10044955510403-00327 L0044863610403-00022 1004341-0340403 -00021 10043400510403-00020 r_0042694tt0403-000r_9 L0042767t3o402-00245 L0042546j.7o402-00244 L0042s292L0402-00055 L0042035760401-00505 10041583610401-00419 1004]- t42760401 -00260 1003911307040r_-00044 1004100367

VENDOR

ALBA}IY INTERNATIONAL0408-00404 31871_

09-09-0408-r_8-0406-29-0403-19-0407-2L-04

VENDOR TOTAL

03-25-0402-L7 -0401-05-04

VENDOR TOTAL

nav5-Lt-u+Lz- r>-u3

VENDOR TOTAL

INC.10_02_0310_02_0310_05_0310_05_0310_08_03

VENDOR TOTAL

NETAMOUNT

33.41az.rL

550.00342 .42295 .63501.33r50.51

39.7t666.84666.84

2836.7L1048.98

482,75181.05

6t- .011r.4 .5L

96.31592.2L258.9L

L2t42.37

239 . OL

239.0L *

4s0.00250.00157.50525.00L27.50

1510.00 *

787 .74368.72]-96 .87

753 .33 *

1200.001200.00

2440 .00 *

489.60489 .60489.60458 .645r2 .64

2440 .08 *

ITirVOICEDATE

05-14-0404-26-0405-04-0404-19-0402 -24- 0403-24-0403 -23 - 0403-22-0402-23 - 0402 -23 - 0402-09-0402-10-0402-05-0402-05-040]--27 -04ot-20 - 0401-09-04r_1- 07 - 0301-07-04

TOTAL

07 -23-04

DUEDATE

E AP3-Z)5-205-204-303-303-303-303 -263-033-033-033-03z- L62-!62-04r_-30]--2Lr-201- 13

8-31

9-248-307 -23

. 3-26L-23

5-203-03L-20

J-JI-

L-20

70-02LV-VZ

10-0510-0510-08

CHECKIF PAI

980309733397 66L97 04495A299603 r95955958 999477t9477L9420L94258940329403293550933 559286092!9492860

10L190

L0L97 69990695800934 85

97J,7 g9453492729

>) I LI92l-7 1

94016940I6:r.* u .L b940r5944l-6

VENDOR TOTAL

-',16 WINTER PI.JUMBTNG & HEATING5 0409-00200 4to4

. t6 0408-00352 5844776 0407 -00140 4037776 0403-00368 031_904776 0401-00438 5470

798 HESCO INC.798 0405-00206 340763798 0403 -00027 340543798 0401 -00275 340269

808 ARBON EQUIPMENT CORP.808 0403-00538 1309832B0B 0401-00281 1278547

813 GENERAL DELIVERY813 0403-00005 200786813 0403-00004 200'781

3 0403-00003 2aff i88,3 0403-00002 200895

813 0403-0000r 200895

Lessons?

805 ??

20

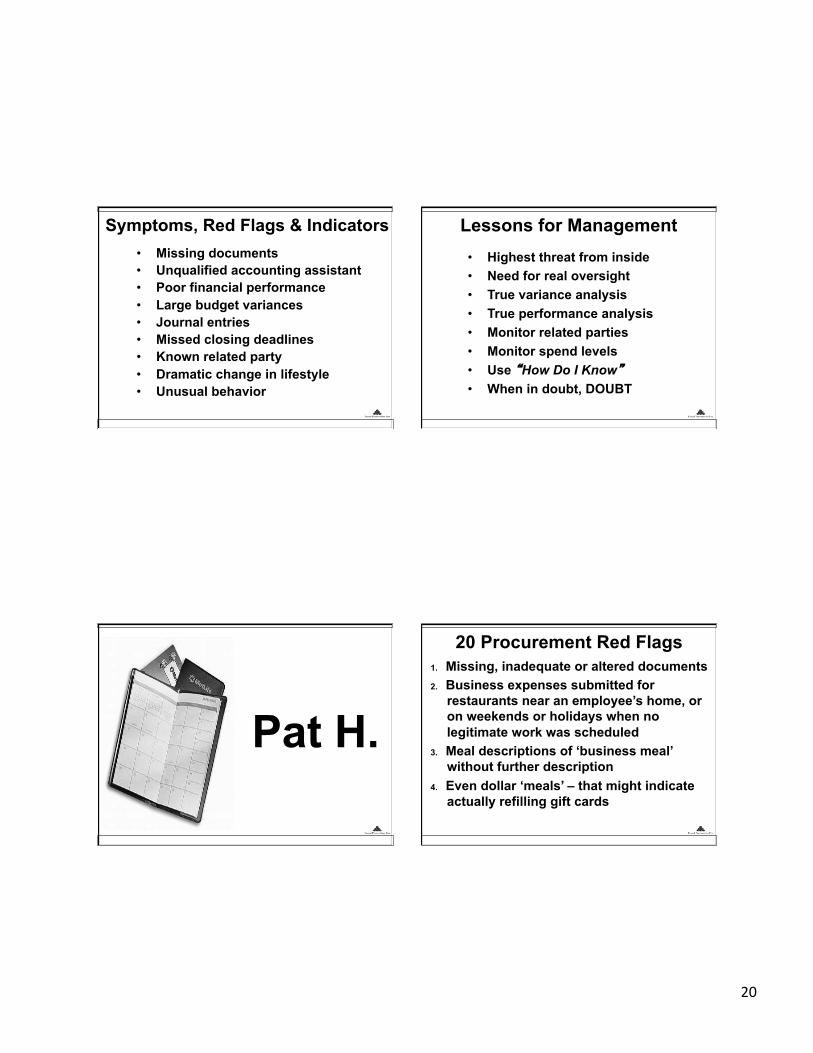

Symptoms, Red Flags & Indicators • Missing documents

• Unqualified accounting assistant • Poor financial performance • Large budget variances • Journal entries • Missed closing deadlines • Known related party • Dramatic change in lifestyle • Unusual behavior

Lessons for Management

• Highest threat from inside • Need for real oversight • True variance analysis • True performance analysis • Monitor related parties • Monitor spend levels • Use “How Do I Know” • When in doubt, DOUBT

Pat H. 1. Missing, inadequate or altered documents 2. Business expenses submitted for

restaurants near an employee’s home, or on weekends or holidays when no legitimate work was scheduled

3. Meal descriptions of ‘business meal’ without further description

4. Even dollar ‘meals’ – that might indicate actually refilling gift cards

20 Procurement Red Flags

21

5. Duplicate charges for meals, transportation and accommodations

6. Counts of supplies, equipment or other assets show a pattern on missing items

7. Unusually high labor hours or rates – especially compared to a baseline norm

8. Unusual quantity or type of supplies, tools, or other small-dollar items

20 Procurement Red Flags 9. Change in banking or other payment

information for existing suppliers and contractors (especially for low-frequency or inactive/dormant entities)

10. Charges from unknown suppliers found on management reports

11. Unexpected charges in excess of budgeted or otherwise planned amounts

12. Good or services purchased in excess of needs or normal volumes

20 Procurement Red Flags

13. Amounts of invoices fall just below the threshold for review

14. Employee handles all matters related to a vendor even though it might be outside or below his or her normal duties

15. Vendors with an unusual business volume for no apparent reason

16. ‘Customer’, employee and third-party complaints (including credit card charges)

20 Procurement Red Flags 17. Adjustments that override original

transactions 18. Cash over or under 19. Common names or addresses for refunds

or credits (including bank accounts) 20. Significant unexplained items in

reconciliations

20 Procurement Red Flags

22

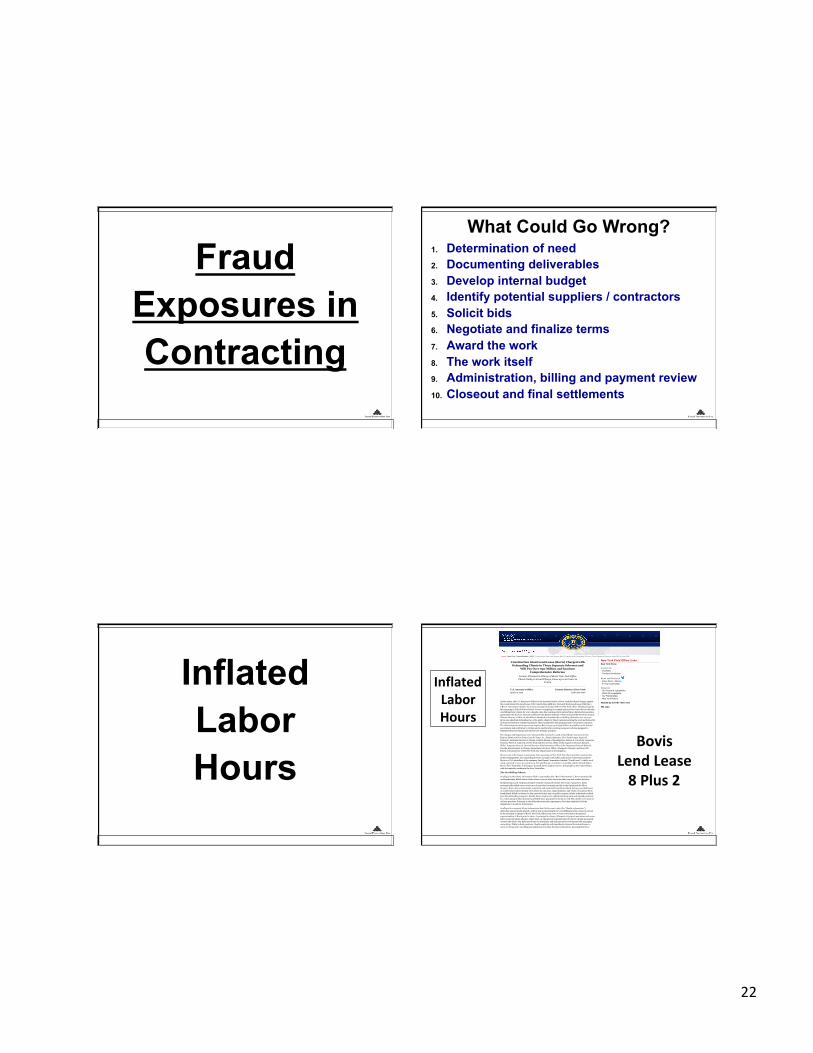

Fraud Exposures in Contracting

What Could Go Wrong? 1. Determination of need 2. Documenting deliverables 3. Develop internal budget 4. Identify potential suppliers / contractors 5. Solicit bids 6. Negotiate and finalize terms 7. Award the work 8. The work itself 9. Administration, billing and payment review 10. Closeout and final settlements

Inflated Labor Hours

Construction Giant Lend Lease (Bovis) Charged withDefrauding Clients in Three Separate Schemes and

Will Pay Over $50 Million and InstituteComprehensive Reforms

Former Principal in Charge of Bovis’ New York OfficePleads Guilty to Fraud Charge, Faces up to 20 Years in

Prison

U.S. Attorney’s OfficeApril 24, 2012

Eastern District of New York(718) 254-7000

Earlier today, the U.S. Attorney’s Office for the Eastern District of New York filed fraud charges againstthe construction firm Lend Lease (US) Construction LMB Inc. (formerly Bovis Lend Lease LMB Inc.)(“Bovis”) and James Abadie, the former principal in charge of Bovis’ New York office. Abadie pled guiltythis morning in United States District Court to conspiring to commit mail and wire fraud by fraudulentlyoverbilling Bovis’ clients for over a decade. Also this morning, Bovis entered into a deferred prosecutionagreement with the U.S. Attorney’s Office for the Eastern District of New York and the New York CountyDistrict Attorney’s Office in which Bovis admitted to fraudulently overbilling clients for over 10 years.Bovis also admitted defrauding two of its public clients by falsely misrepresenting the work performed byits minority business enterprise partners, thus fraudulently obtaining payments on lucrative contracts.The deferred prosecution agreement requires Bovis to pay up to $56 million in penalties to the federalgovernment and restitution to victims and to institute far-reaching corporate reforms designed toeliminate future problems and enforce best industry practices.

The charges and dispositions were announced by Loretta E. Lynch, United States Attorney for theEastern District of New York; Cyrus R. Vance, Jr., District Attorney, New York County; Janice K.Fedarcyk, Assistant Director in Charge, Federal Bureau of Investigation; Robert E. Van Etten, InspectorGeneral, The Port Authority of New York and New Jersey, Office of the Inspector General; Brian D.Miller, Inspector General, General Services Administration, Office of the Inspector General; Robert L.Panella, Special Agent in Charge, Department of Labor, Office of Inspector General; and Rose GillHearn, Commissioner of the New York City Department of Investigation.

Bovis is one of the largest construction firms operating in New York City. Bovis provides construction,project management, and consulting services on large-scale public and private construction projects.Bovis is a U.S. subsidiary of the company Lend Lease Corporation Limited (“Lend Lease”), which, as of2009, operated in over 40 countries in Asia and Europe, as well as in Australia and the United States.Bovis’s New York office is its largest. In 2008, Bovis employed over 1,000 people in the United States,with the majority working in the New York office.

The Overbilling Scheme

As alleged in the felony information filed in court today (the “Bovis Information”), Bovis intentionallyand fraudulently billed clients, from at least 1999 to 2009, for hours that were not worked by labor

foremen from Local 79 Mason Tenders’ District Council of Greater New York (“Local 79”). Bovissystematically added one to two hours of unworked overtime per day to the timesheets for laborforemen. Bovis also systematically completed and submitted timesheets falsely listing unworked hoursas worked when labor foremen were absent for sick days, major holidays, and weeks of vacation. Bovisfraudulently billed its clients for this unworked time and, on public projects, falsely submitted certifiedpayrolls, defrauding taxpayers. Finally, Bovis made extra, undisclosed lump sum and stipend paymentsto a select group of labor foremen and billed those payments to clients as well. The clients were unawareof these practices. Pursuant to the deferred prosecution agreement, Bovis has admitted all of theallegations in the Bovis Information.

As alleged in a separate felony information also filed in court today (the “Abadie information”),defendant James Abadie played a critical role in executing Bovis’s overbilling practices when he servedas the principal in charge of Bovis’ New York office from 2002 to June 2009 and as the generalsuperintendent at Bovis prior to 2002. As principal in charge, all aspects of project operations and unionlabor issues fell under Abadie’s supervision. As the general superintendent for Bovis, Abadie personallyoversaw the day-to-day field operations on all projects and had extensive involvement with managingunion labor. While in both positions, Abadie explicitly and fraudulently directed his subordinates tocarry out the practice of adding unworked hours to labor foremen’s timesheets, knowing that these

New York Field Office LinksNew York Home

Contact Us- Overview- Territory/Jurisdiction

News and Outreach - Press Room | Stories- In Your Community

About Us- Our People & Capabilities- What We Investigate- Our Partnerships- New York History

Wanted by the FBI - New York

FBI Jobs

Home • New York • Press Releases • 2012 • Construction Giant Lend Lease (Bovis) Charged with Defrauding Clients in Three Separate Schemes and Will Pay Over $50...

BovisLendLease8Plus2

InflatedLaborHours

23

Inflated Labor & Burden

Rates

T&M$RATE$SHEETUNION$WORKERS

Millwright$$$$$$$$Rate$Buildup Basis Level$4

BASE$RATE$(including$vacation) 45.87$''''''''''''

FRINGE$BENEFITS 14.99$''''''''''''

ADMIN/PROFIT/OVERHEAD 0.00% ,$''''''''''''''''

SMALL$TOOLS 4.00% 1.83$''''''''''''''

CONSUMABLES 4.00% 1.83$''''''''''''''Total$Fee 8.00% 3.67$''''''''''''''

PAYROLL$TAXES$(At$Net$Tax$Rates)Social'Security

(Gross'Tax'Rate'='___'%) 7.65% 3.51$''''''''''''''State'Unemployment'Compensation

(Gross'Tax'Rate'='___'%) 6.55% 3.00$''''''''''''''Federal'Unemployment'Compansation

(Gross'Tax'Rate'='___'%) 0.80% 0.37$''''''''''''''Total$Taxes 15.00% 6.88$''''''''''''''

INSURANCEWorker's'Compansation','Rate 7.45% 3.42$''''''''''''''General'Liability'&'Misc.'Insurances 7.21% 3.31$''''''''''''''

Umbrella/LiabilityTotal$Insurance 14.66% 6.72$$$$$$$$$$$$$$$

TOTAL$STRAIGHT$TIME$BILLING$RATE 78.13$''''''''''''

Time$and$1/2$Premium:Time'and'1/2'Base'Rate 22.94$''''''''''''Unbrella/Liability'Insurance ,$''''''''''''''''Payroll'Taxes 3.44$''''''''''''''

Subtotal 26.38$''''''''''''TOTAL$TIME$AND$1/2$BILLING$RATE 104.51$''''''''''

Double$Time$Premium:Double'Time'Base'Rate 45.87$''''''''''''Unbrella/Liability'Insurance ,$''''''''''''''''Payroll'Taxes 6.88$''''''''''''''

Subtotal 52.75$''''''''''''TOTAL$DOUBLE$TIME$BILLING$RATE 130.89$''''''''''

InflatedLaborRates

Subcontracts

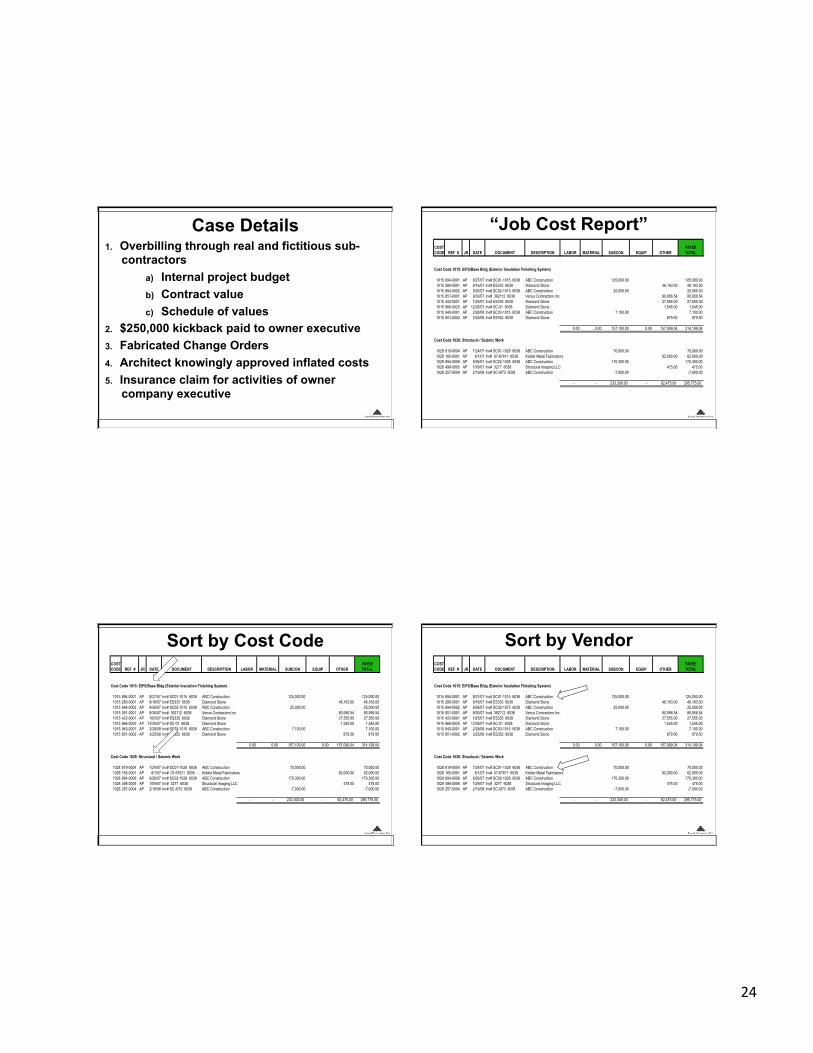

Project Background 1. Renovation of two existing client facilities 2. Collusion between client executive and

long-term trusted construction company executive (25 year relationship)

3. Sole source contract award (no bid) 4. Not managed by construction department 5. Overcharges of over $3 million on

contract value of $14.5 million (21%)

24

Case Details 1. Overbilling through real and fictitious sub-

contractors a) Internal project budget b) Contract value c) Schedule of values

2. $250,000 kickback paid to owner executive 3. Fabricated Change Orders 4. Architect knowingly approved inflated costs 5. Insurance claim for activities of owner

company executive

COST PAYEECODE REF # JR DATE DOCUMENT DESCRIPTION LABOR MATERIAL SUBCON EQUIP OTHER TOTAL

Cost Code 1015: EIFS/Base Bldg (Exterior Insulation Finishing System)

1015 894-0001 AP 8/27/07 Inv# SC01-1015 6038 ABC Construction 125,000.00 125,000.001015 280-0001 AP 9/16/07 Inv# ES333 6038 Diamond Stone 46,163.00 46,163.001015 894-0002 AP 9/26/07 Inv# SC02-1015 6038 ABC Construction 25,000.00 25,000.001015 051-0001 AP 9/30/07 Inv# 392112 6038 Venus Contractors Inc. 80,956.54 80,956.541015 422-0001 AP 10/5/07 Inv# ES335 6038 Diamond Stone 27,555.00 27,555.001015 966-0025 AP 12/26/07 Inv# SC-01 6038 Diamond Stone 1,545.00 1,545.001015 940-0001 AP 2/28/08 Inv# SC03-1015 6038 ABC Construction 7,100.00 7,100.001015 851-0002 AP 3/25/08 Inv# ES352 6038 Diamond Stone 879.50 879.50

0.00 0.00 157,100.00 0.00 157,099.04 314,199.04

Cost Code 1028: Structural / Seizmic Work

1028 819-0004 AP 7/24/07 Inv# SC01-1028 6038 ABC Construction 70,000.00 70,000.001028 165-0001 AP 8/1/07 Inv# 07-67611 6038 Kidder Metal Fabricators 62,000.00 62,000.001028 894-0008 AP 9/26/07 Inv# SC02-1028 6038 ABC Construction 170,300.00 170,300.001028 498-0005 AP 10/9/07 Inv# 3277 6038 Structural Imaging LLC 475.00 475.001028 257-0004 AP 2/19/08 Inv# SC-I073 6038 ABC Construction -7,000.00 -7,000.00

- - 233,300.00 - 62,475.00 295,775.00

“Job Cost Report”

COST PAYEECODE REF # JR DATE DOCUMENT DESCRIPTION LABOR MATERIAL SUBCON EQUIP OTHER TOTAL

Cost Code 1015: EIFS/Base Bldg (Exterior Insulation Finishing System)

1015 894-0001 AP 8/27/07 Inv# SC01-1015 6038 ABC Construction 125,000.00 125,000.001015 280-0001 AP 9/16/07 Inv# ES333 6038 Diamond Stone 46,163.00 46,163.001015 894-0002 AP 9/26/07 Inv# SC02-1015 6038 ABC Construction 25,000.00 25,000.001015 051-0001 AP 9/30/07 Inv# 392112 6038 Venus Contractors Inc. 80,956.54 80,956.541015 422-0001 AP 10/5/07 Inv# ES335 6038 Diamond Stone 27,555.00 27,555.001015 966-0025 AP 12/26/07 Inv# SC-01 6038 Diamond Stone 1,545.00 1,545.001015 940-0001 AP 2/28/08 Inv# SC03-1015 6038 ABC Construction 7,100.00 7,100.001015 851-0002 AP 3/25/08 Inv# ES352 6038 Diamond Stone 879.50 879.50

0.00 0.00 157,100.00 0.00 157,099.04 314,199.04

Cost Code 1028: Structural / Seizmic Work

1028 819-0004 AP 7/24/07 Inv# SC01-1028 6038 ABC Construction 70,000.00 70,000.001028 165-0001 AP 8/1/07 Inv# 07-67611 6038 Kidder Metal Fabricators 62,000.00 62,000.001028 894-0008 AP 9/26/07 Inv# SC02-1028 6038 ABC Construction 170,300.00 170,300.001028 498-0005 AP 10/9/07 Inv# 3277 6038 Structural Imaging LLC 475.00 475.001028 257-0004 AP 2/19/08 Inv# SC-I073 6038 ABC Construction -7,000.00 -7,000.00

- - 233,300.00 - 62,475.00 295,775.00

Sort by Cost Code COST PAYEE

CODE REF # JR DATE DOCUMENT DESCRIPTION LABOR MATERIAL SUBCON EQUIP OTHER TOTAL

Cost Code 1015: EIFS/Base Bldg (Exterior Insulation Finishing System)

1015 894-0001 AP 8/27/07 Inv# SC01-1015 6038 ABC Construction 125,000.00 125,000.001015 280-0001 AP 9/16/07 Inv# ES333 6038 Diamond Stone 46,163.00 46,163.001015 894-0002 AP 9/26/07 Inv# SC02-1015 6038 ABC Construction 25,000.00 25,000.001015 051-0001 AP 9/30/07 Inv# 392112 6038 Venus Contractors Inc. 80,956.54 80,956.541015 422-0001 AP 10/5/07 Inv# ES335 6038 Diamond Stone 27,555.00 27,555.001015 966-0025 AP 12/26/07 Inv# SC-01 6038 Diamond Stone 1,545.00 1,545.001015 940-0001 AP 2/28/08 Inv# SC03-1015 6038 ABC Construction 7,100.00 7,100.001015 851-0002 AP 3/25/08 Inv# ES352 6038 Diamond Stone 879.50 879.50

0.00 0.00 157,100.00 0.00 157,099.04 314,199.04

Cost Code 1028: Structural / Seizmic Work

1028 819-0004 AP 7/24/07 Inv# SC01-1028 6038 ABC Construction 70,000.00 70,000.001028 165-0001 AP 8/1/07 Inv# 07-67611 6038 Kidder Metal Fabricators 62,000.00 62,000.001028 894-0008 AP 9/26/07 Inv# SC02-1028 6038 ABC Construction 170,300.00 170,300.001028 498-0005 AP 10/9/07 Inv# 3277 6038 Structural Imaging LLC 475.00 475.001028 257-0004 AP 2/19/08 Inv# SC-I073 6038 ABC Construction -7,000.00 -7,000.00

- - 233,300.00 - 62,475.00 295,775.00

Sort by Vendor

25

COST PAYEECODE REF # JR DATE DOCUMENT DESCRIPTION LABOR MATERIAL SUBCON EQUIP OTHER TOTAL

Cost Code 1015: EIFS/Base Bldg (Exterior Insulation Finishing System)

1015 894-0001 AP 8/27/07 Inv# SC01-1015 6038 ABC Construction 125,000.00 125,000.001015 280-0001 AP 9/16/07 Inv# ES333 6038 Diamond Stone 46,163.00 46,163.001015 894-0002 AP 9/26/07 Inv# SC02-1015 6038 ABC Construction 25,000.00 25,000.001015 051-0001 AP 9/30/07 Inv# 392112 6038 Venus Contractors Inc. 80,956.54 80,956.541015 422-0001 AP 10/5/07 Inv# ES335 6038 Diamond Stone 27,555.00 27,555.001015 966-0025 AP 12/26/07 Inv# SC-01 6038 Diamond Stone 1,545.00 1,545.001015 940-0001 AP 2/28/08 Inv# SC03-1015 6038 ABC Construction 7,100.00 7,100.001015 851-0002 AP 3/25/08 Inv# ES352 6038 Diamond Stone 879.50 879.50

0.00 0.00 157,100.00 0.00 157,099.04 314,199.04

Cost Code 1028: Structural / Seizmic Work

1028 819-0004 AP 7/24/07 Inv# SC01-1028 6038 ABC Construction 70,000.00 70,000.001028 165-0001 AP 8/1/07 Inv# 07-67611 6038 Kidder Metal Fabricators 62,000.00 62,000.001028 894-0008 AP 9/26/07 Inv# SC02-1028 6038 ABC Construction 170,300.00 170,300.001028 498-0005 AP 10/9/07 Inv# 3277 6038 Structural Imaging LLC 475.00 475.001028 257-0004 AP 2/19/08 Inv# SC-I073 6038 ABC Construction -7,000.00 -7,000.00

- - 233,300.00 - 62,475.00 295,775.00

Duplicate Charges Surface

Billed and Paid Costs

Actual Costs

Total

Overcharge

A - $10,110,000 $8,660,000 $1,450,000

B - $4,410,000 $2,825,000 $1,585,000

Total - $14,520,000 $11,485,000 $3,035,000

Summary of Losses

Plus: 30% Penalty $910,000 Audit and legal costs $250,000

Non- Reimbursable

Costs

26

The Fishing Trip(s) Falsification of Records

Insurance Records

4Post-ItNotes3yellow1pink

Change Order Risk

27

1. Not priced in accordance with contract 2. Markups for fee billed incorrectly 3. Material prices do not reflect actual cost

due to trade discounts & other issues 4. Material quantity estimates not accurate 5. Labor hours overstated due to poor

estimating techniques

10 Change Order Exposures 6. Labor rate and/or burden exceeds actual 7. Improper charges for overtime versus

premium time 8. Buyouts of lower-tiered subcontractors

not disclosed 9. Change orders for work already included

in the base contract 10. Fabricated change orders

• Move water line

10 Change Order Exposures

Varsity Contractors, Inc.401 NE Northgate Way 1Seattle, WA 98125 Contract No. 1472602045

Phone: Date: 11/25/XXXX

Previous Approved Changes: -$ 36,479.00$

8,323.37$

To: 44,802.37$

1 243.52$

2 1,875.50$

3 3,115.75$

4 574.75$

5 2,513.85$

Subtotal 8,323.37$

$ 8,323.37

Varisty Contractors, Inc.Tony Homan/ Project Manager

R.E Crawford Construction, General Corporation

Total:

Breaking out of concrete from sidewalk for asphalt prep

Crushed rock import for trench backfill

Subtotal of all of the above added expenses due to changes to contract

Furnish all necessary labor, material and equipment to provide the following additional work as approved by the OWNER:

Terms and conditions of original contract apply to all Change Orders.

Changes Approved Changes ApprovedJoel Senchur

Install new gate valve, tee, 6" DI pipe w/mega lugs and (2) 45 degree bends for unknown 6 inch service line for hydrant.

Reconnect unkown 2" water service to Bank Of America

CONTRACT CHANGE ORDER AUTHORIZATION

Change Order

Original Contract Amount:

Add:

General Contractor:Address:

Total Revised Contract Amt.:

Project Address:Gottschalks 8 inch water relocate

VARSITY CONTRACTORS, INC.

Project Name:

Locate services

401 NE Northgate WaySeattle, Wa 98125

R.E C.

Varsity Contractors, Inc.401 NE Northgate Way 1Seattle, WA 98125 Contract No. 1472602045

Phone: Date: 11/25/XXXX

Previous Approved Changes: -$ 36,479.00$

8,323.37$

To: 44,802.37$

1 243.52$

2 1,875.50$

3 3,115.75$

4 574.75$

5 2,513.85$

Subtotal 8,323.37$

$ 8,323.37

Varisty Contractors, Inc.Tony Homan/ Project Manager

R.E Crawford Construction, General Corporation

Total:

Breaking out of concrete from sidewalk for asphalt prep

Crushed rock import for trench backfill

Subtotal of all of the above added expenses due to changes to contract

Furnish all necessary labor, material and equipment to provide the following additional work as approved by the OWNER:

Terms and conditions of original contract apply to all Change Orders.

Changes Approved Changes ApprovedJoel Senchur

Install new gate valve, tee, 6" DI pipe w/mega lugs and (2) 45 degree bends for unknown 6 inch service line for hydrant.

Reconnect unkown 2" water service to Bank Of America

CONTRACT CHANGE ORDER AUTHORIZATION

Change Order

Original Contract Amount:

Add:

General Contractor:Address:

Total Revised Contract Amt.:

Project Address:Gottschalks 8 inch water relocate

VARSITY CONTRACTORS, INC.

Project Name:

Locate services

401 NE Northgate WaySeattle, Wa 98125

R.E C.

BOGUS

28

1. Unclear or unreasonable specifications 2. No audit terms in contact 3. Atypical ‘application of payment’ forms 4. Missing or disorganized backup 5. Failure to track or report use of

allowances and contingencies 6. Undocumented workers on project 7. Changes in schedule of values without

explanation

20 Contracting Red Flags

Example Allowances

29

8. Subcontractor complaints about payments from general contractor

9. Missing lien waivers 10. Unusual bid patterns 11. Bid losers hired as subcontractors 12. Missing documents 13. Undisclosed related parties

20 Contracting Red Flags 14. Material substitutions without approval 15. Excess material purchases 16. Change order manipulation 17. Front end loading in billing 18. Overstated units, hours, equipment used 19. Undervalued deductive change orders 20. Diverting lump sum work to T&M projects

20 Contracting Red Flags

1. Analyze bids looking for patterns by vendor or purchasing agent

2. Confirm losing bids, failure to respond 3. Audit vendors - transactions, T&Es, 1099s 4. Surprise inspect at receiving points 5. Match PO, proof or receipt, & invoice 6. Observe inventory held by others 7. Observe highly tempting items

20 Detection Suggestions 8. For sole source suppliers, confirm

existence, prove ownership, test prices, find other sources, analyze usage volume

9. Reconcile inventory, purchases and usage of items subject to pilferage

10. Audit rental of equipment (including equipment used by contractors)

11. Verify accuracy of items stored in containers (gas, liquids, other)

20 Detection Suggestions

30

12. Audit areas where vendors come in, take stock, and replenish on their own

13. Audit purchases that do not go through normal purchasing procedures

14. Audit maintenance agreements 15. Audit property management agreements 16. Audit costs on cost-plus agreements to

original documentation. Look for creative interpretations of the term “Cost”

20 Detection Suggestions 17. Pull LexisNexis and D&B reports, and

enter vendor names into press databases 18. Use computer to look for multiple PO and

split bills 19. Confirm delivery locations 20. Verify address and other master file

changes by vendors

20 Detection Suggestions

1. Deterrence and Prevention

2. Early Detection

3. Effective Handling

Fraud Risk Management Framework

ORGANIZATIONS MUST BE PREPARED AT ALL THREE LEVELS

Law Enforcement

Insurance Company

Control Weakness

Audit

Exception

Pattern

Review Of Records

Interviews

Interrogation

Tip

Case File

Bonding Claim

Audit Report

DetectionMode

InvestigativeMode

31

1. Know what happens at alarm 2. Investigation 3. Loss recovery 4. Control weaknesses 5. External parties 6. Publicity 7. HR issues 8. Employee morale issues

Effective Fraud Handling

1. Denial–Dismay–Anger–Empathy 2. Confusion 3. In some – paralysis of thought

and action 4. Fear

What We Can Expect

1. Calm, objective leadership 2. Protection of the innocent 3. Certainty 4. Confident consistent action 5. Resources

What We Need to Provide 1. Experienced investigators 2. Forensic accountants 3. Information technology experts 4. Computer forensics specialists 5. Other technical specialists 6. Security / loss prevention 7. Internal auditors 8. Human resources 9. Legal and Compliance

Investigative Resources

32

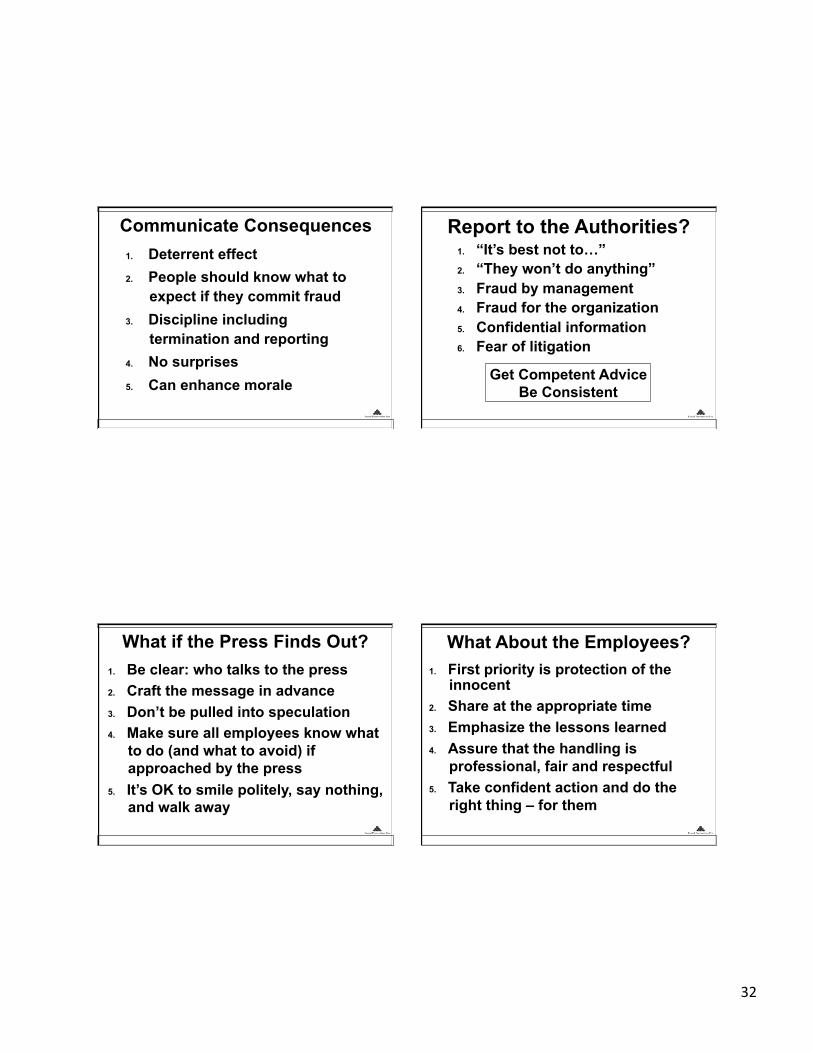

1. Deterrent effect 2. People should know what to

expect if they commit fraud 3. Discipline including

termination and reporting 4. No surprises 5. Can enhance morale

Communicate Consequences 1. “It’s best not to…” 2. “They won’t do anything” 3. Fraud by management 4. Fraud for the organization 5. Confidential information 6. Fear of litigation

Report to the Authorities?

Get Competent Advice Be Consistent

1. Be clear: who talks to the press 2. Craft the message in advance 3. Don’t be pulled into speculation 4. Make sure all employees know what

to do (and what to avoid) if approached by the press

5. It’s OK to smile politely, say nothing, and walk away

What if the Press Finds Out? 1. First priority is protection of the

innocent 2. Share at the appropriate time 3. Emphasize the lessons learned 4. Assure that the handling is

professional, fair and respectful 5. Take confident action and do the

right thing – for them

What About the Employees?

33

1. Deterrence and Prevention

2. Early Detection

3. Effective Handling

Fraud Risk Management Framework

ORGANIZATIONS MUST BE PREPARED AT ALL THREE LEVELS

Together – on our watch –

we will no longer tolerate Lies, Deception,

Wrongdoing, Misconduct, Theft, or Outright Fraud

Fraud Prevention Pro Manifesto

John J. Hall

www.JohnHallSpeaker.com

www.FraudPreventionPro.com

(312) 560-9931

Questions, Comments, Feedback Let me know how I can help! Thank You

www.JohnHallSpeaker.com www.FraudPreventionPro.com

JOHN J.HALL