Embed Size (px)

Citation preview

1

Access to Finance

Access to finance has always been one of the most challenging aspects for SMEs. The high cost of credit is dangerously stifling the drive of entrepreneurs; threatening the growth, profitability and competitiveness of the SME sector. In order to remedy this situation, the Government has put in place several schemes aimed at maintaining the flow of credit to SMEs and improving their access to capital markets, namely:-

RWG Credit financing scheme (Factoring)

SME Financing Scheme (Window 1 - Turnover < 10 M)

SME Financing Scheme (Window 2 - 10 M > Turnover < 50 M)

Equity Participation in enterprises

Import Loan Facility

SME Partnership Fund

DBM - Booster Micro Credit Loan Scheme

DBM - Quasi-Equity Financing Scheme

DBM - Business Development Scheme

DBM - Normal Scheme for the Agricultural Sector

2

RWG Credit Factoring Scheme

What is factoring?

Factoring is a financial transaction whereby a business sells its accounts receivable (i.e. invoices) to a third party (called a factor) at a discount in exchange for immediate money with which to finance business transactions.

Scheme RWG Credit financing scheme (Factoring)

Objective of scheme To provide cash flow to entrepreneurs via the factoring of their credit sales invoices through Non-Bank Financial Institutions (NBFIs).

Benefits of the Scheme to entrepreneurs & SMEs

- The SME is freed of administrative tasks of monitoring debtors.

- A professional team of the NBFIs takes charge of the SME debtors and debt collection.

Implementing Agency - Restructuring Working Group (RWG)

Conditions of the scheme

- Maximum single Client Funding Limit: Rs10M.

- Maximum single Debtor Factoring Limit: Rs2M.

- Maximum credit invoice period: 90 days.

- Maximum % financing: 90% of invoice amount. Remaining 10% kept in a Reserve Account and released to the beneficiary (less accrued interests and any outstanding charges) once the invoice is paid in full.

Interest Rate Interest rate: 7.5% p.a. (on invoice amount)

Factoring Fee Factoring fee: 1.5% of invoice amount.

Share of Contribution - Upfront and one-off fee of Rs 5000 for SMEs with a turnover below Rs 5M

- Upfront and one-off fee of Rs 10, 000 for SMEs with a turnover above Rs 5M

Eligibility Criteria - SME with an annual turnover not exceeding Rs 50M.

- SMEs in operation for at least 1 year.

- All sectors, except trading.

- Selling products and services to other business houses, i.e., B2B on credit terms not exceeding 90 days (3 months).

Mode of Application - The SME should apply directly to the NBFI, e.g. CIM Finance. (Please see List of Partners for contact details)

Validity period of the scheme

- Scheme will end by 31December 2014

3

Scheme SME Financing Scheme (Window 1 )(Turnover < 10 M)

Objective of scheme To assist SMEs in raising finance from commercial banks to meet their working capital needs and their expansion as well as create new jobs. It covers overdrafts, existing and new loans.

Benefit of the Scheme - The SME Financing Scheme provides low cost financing to entrepreneurs and SMEs.

- It consolidates the relationship and trust between the banker and the SME.

- Saves time, as the bank already possesses the KYC information (Know-your-customer).

Implementing Agency Restructuring Working Group (RWG)

Interest Rate Interest rate at repo+3 % (presently at 7.65 %.)

Security As may be required by the Bank.

Eligibility Criteria - SMEs with a turnover of less than Rs10M.

- SMEs in operation for at least one year

- Excludes Employment, Religious or Charitable Institutions, Trading and Real Estate.

- Excludes luxury items, including, luxury vehicles.Mode of Application The SME should apply directly to any of the following Banks,

involved in the scheme:1. ABC Banking Corporation Ltd2. AfrAsia Bank Limited3. Bank One Limited4. Bank of Baroda5. Banque des Mascareignes Ltée6. Barclays Bank PLC7. Bramer Banking Corporation Ltd8. Habib Bank Limited9. Mauritius Post and Cooperative Bank Ltd10. SBI (Mauritius) Ltd11. Standard Bank (Mauritius) Limited12. State Bank of Mauritius Ltd13. The Hongkong and Shanghai Banking Corporation Limited14. The Mauritius Commercial Bank Limited

Validity period of the scheme

Scheme will end by 31 December 2014

SME Financing Scheme

4

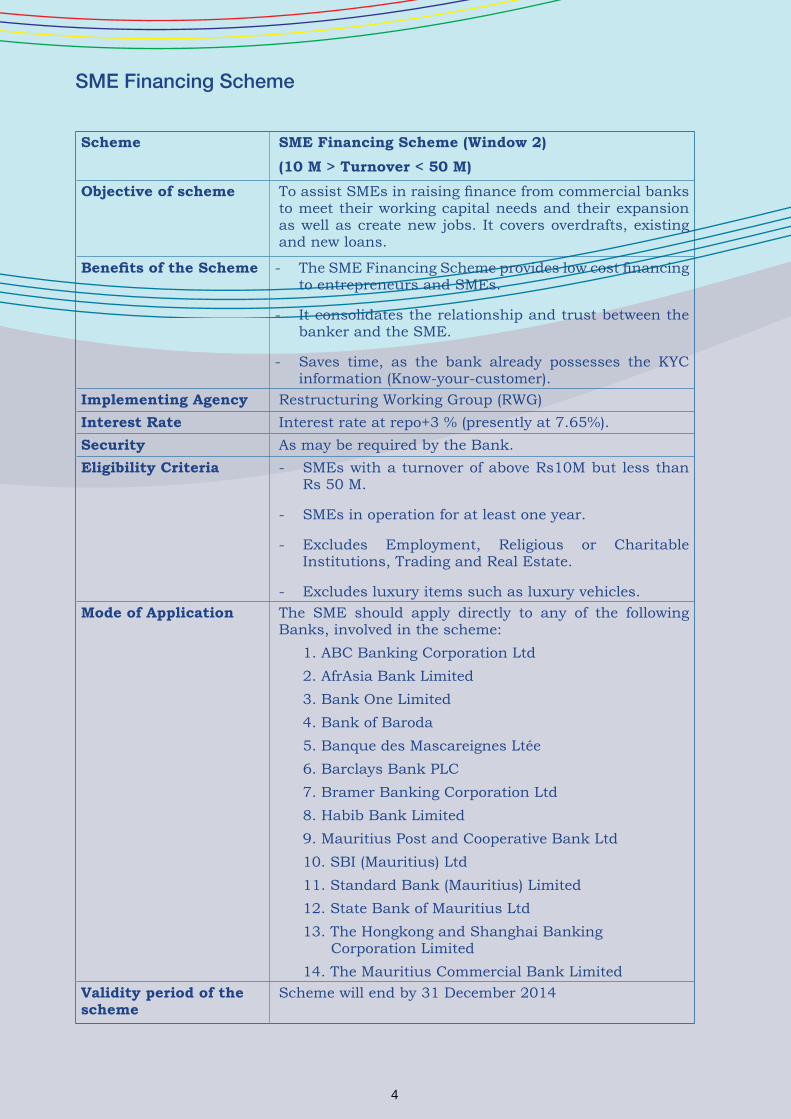

SME Financing Scheme

Scheme SME Financing Scheme (Window 2)(10 M > Turnover < 50 M)

Objective of scheme To assist SMEs in raising finance from commercial banks to meet their working capital needs and their expansion as well as create new jobs. It covers overdrafts, existing and new loans.

Benefits of the Scheme - The SME Financing Scheme provides low cost financing to entrepreneurs and SMEs.

- It consolidates the relationship and trust between the banker and the SME.

- Saves time, as the bank already possesses the KYC information (Know-your-customer).

Implementing Agency Restructuring Working Group (RWG)Interest Rate Interest rate at repo+3 % (presently at 7.65%). Security As may be required by the Bank. Eligibility Criteria - SMEs with a turnover of above Rs10M but less than

Rs 50 M.

- SMEs in operation for at least one year.

- Excludes Employment, Religious or Charitable Institutions, Trading and Real Estate.

- Excludes luxury items such as luxury vehicles.Mode of Application The SME should apply directly to any of the following

Banks, involved in the scheme:1. ABC Banking Corporation Ltd2. AfrAsia Bank Limited3. Bank One Limited4. Bank of Baroda5. Banque des Mascareignes Ltée6. Barclays Bank PLC7. Bramer Banking Corporation Ltd8. Habib Bank Limited9. Mauritius Post and Cooperative Bank Ltd10. SBI (Mauritius) Ltd11. Standard Bank (Mauritius) Limited12. State Bank of Mauritius Ltd13. The Hongkong and Shanghai Banking Corporation Limited14. The Mauritius Commercial Bank Limited

Validity period of the scheme

Scheme will end by 31 December 2014

5

Equity Participation in enterprises

Scheme Equity Participation in Enterprises

Objective of scheme To invest as a shareholder in enterprises having a future and growth potential but which are highly indebted and have a low share capital.

Implementing Agency NRF Equity Investment Ltd

Facilities / conditions - Beneficiary to bring in a contribution (to be agreed upon between NRF Equity Investment Ltd and the SME).

- Participation in an enterprise should be between 25 % and 49 %.

- Payment of 5% cumulative dividend.

- Shares may be bought back by the enterprise at Year 10 or at an earlier date at the request of the company.

- Amount to be repaid on redemption: 10% IRR or NAV, whichever is higher.

Eligibility Criteria - SMEs with a turnover between Rs10M and Rs 50M.

- Well established small or medium sized enterprise incorporated in Mauritius, with a minimum 3 years proven track record.

- Looking to expand, to upgrade or move up the value chain.

- Good fundamentals and a pro-active management, willing to consider independent and external advice and implement changes to improve productivity and efficiency.

- Start-up projects will not be considered. Mode of Application - An application form which can be downloaded from the

NRF Equity Investment Ltd website should be submitted.

- Audited financial statements, business plan, growth plan and financial plans (3 years) should also be submitted along.

- A processing fee of Rs 10 000 need to submitted along with the application form, which will be refundable in case the project is not approved.

Contact Details NRF Equity Investment Ltd (Please see List of Partners for contact details)

6

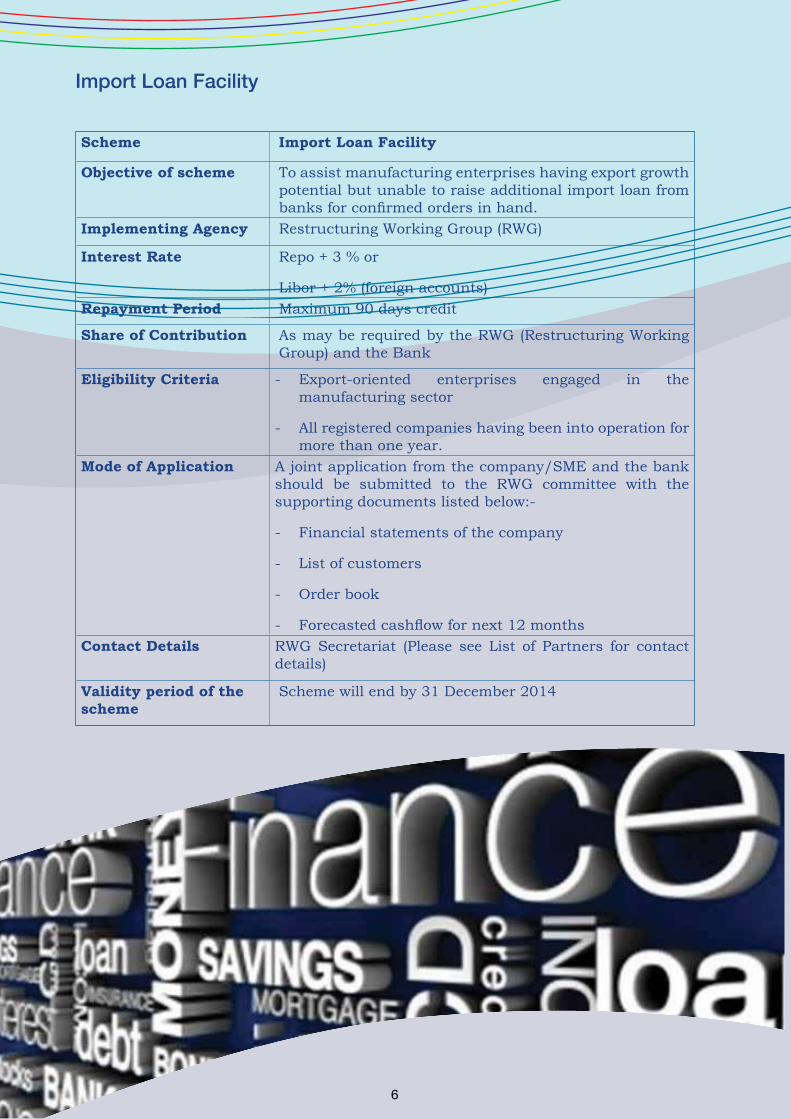

Import Loan Facility

Scheme Import Loan Facility

Objective of scheme To assist manufacturing enterprises having export growth potential but unable to raise additional import loan from banks for confirmed orders in hand.

Implementing Agency Restructuring Working Group (RWG)

Interest Rate Repo + 3 % or

Libor + 2% (foreign accounts) Repayment Period Maximum 90 days credit

Share of Contribution As may be required by the RWG (Restructuring Working Group) and the Bank

Eligibility Criteria - Export-oriented enterprises engaged in the manufacturing sector

- All registered companies having been into operation for more than one year.

Mode of Application A joint application from the company/SME and the bank should be submitted to the RWG committee with the supporting documents listed below:-

- Financial statements of the company

- List of customers

- Order book

- Forecasted cashflow for next 12 months Contact Details RWG Secretariat (Please see List of Partners for contact

details)

Validity period of the scheme

Scheme will end by 31 December 2014

7

SME Partnership Fund

Objective of Scheme To foster the creation, restructuration and consolida-tion of small and medium enterprises.

Implementing Agency SME Partnership Fund Ltd

Scheme SME Partnership Fund Ltd participates in the share capital of SMEs. Participation in a project can vary from Rs 300,000 to Rs 10M representing up to 49% of the SME share capital. The promoters of the SME must invest a minimum of 51% in the share capital.

The total project cost should exceed Rs 600,000.

Terms and Conditions SME should be incorporated as a company in Mauritius.

Project should be viable, sustainable and entailing value creation.

Eligibility Criteria SMEs operating in various business fields. Priority sectors are manufacturing, agro-industry, tourism, ICT and the services industry.

Mode of application Applicants must contact the SME Partnership Fund Ltd.(Please see List of Partners for contact details)

8

Booster Micro Credit Loan Scheme

Scheme Booster Micro Credit Loan Scheme

Objective of Scheme To finance projects with value addition including:

- Small enterprises in the manufacturing, agricultural, agri-business, handicraft

- Small tourism and tourism-related activities

- Small plant nurseries, vegetables, fruits and flower cultivation on a small scale, small livestock breeding activities

- Kindergartens

- ICT and ICT-related activities and E-commerce

- Services (including training)

- Small trades (excluding hawkers)

- Working capital requirements for manufacturing/ processing/handicraft or other projects with value addition up to a ceiling of Rs 75,000

Implementing Agency Development Bank of Mauritius (DBM)Maximum Loan Amount Rs 150,000 (covering up to 100% of cost of project)Interest Rate Repo Rate + 3 % p.a (presently 7.65 % )Repayment Period Up to 5 yearsMoratorium Period Up to 1 yearSecurity - General Floating Charge

- Decreasing Term AssuranceEligibility - Entrepreneurs registered with NEF, SMEDA, AREU,

IVTB, Tourism Authority, NCB, etc.,

- Women entrepreneurs registered with NWEC or NEF

- Any other micro/small entrepreneurs holding a Business Registration Card and having a viable project

- Existing value-added activities requiring working capital finance

- Any other project with value addition recommended by National Empowerment Foundation (NEF), National Women Entrepreneur Council (NWEC) or Small and Medium Enterprises Development Authority (SMEDA)

Mode of Application The Application can either be:Completed online on the DBM website, by filling an online registration form. ORCompleted at the DBM office(Please see List of Partners for contact details)

9

Quasi-Equity Financing Scheme

Scheme Quasi-Equity Financing Scheme

Objective of Scheme Providing equity and quasi-equity to SMEs

Implementing Agency Development Bank of Mauritius (DBM)

Maximum Investment 75% of project cost up to a ceiling of Rs 500,000 as follows:

(i) 49% in the form of quasi-equity, namely Redeemable Preference Shares or debentures with an appropriate coupon rate.

(ii) 26% in the form of an equity loan to enable the promoter/s to buy shares in the company

Interest Rate - Quasi-Equity: Coupon rate ranging from 7.65 % to 13.0 % depending upon time of repayment.

- Equity Loan:Repo Rate + 3 % p.a (presently 7.65% )Repayment Period - Quasi-Equity: Exit at the end of five years with a

conversion clause at our option

- Equity Loan: The loan along with unpaid interests accrued thereon shall be repayable after five years. Interest will be payable yearly after a moratorium of one year.

Security - Quasi-Equity: None

- Equity Loan:

(i) General Floating Charge on promoter’s/borrower’s assets

(ii) Pledge of the shares

(iii) Decreasing Term Assurance

Eligibility - SMEs involved in the manufacturing, agri-business, tourism, trade or service sectors and holding an acceptable business plan.

- Companies registered with the Registrar of BusinessesExit Strategy Quasi-Equity: Exit will be subject to repayment according to

the coupon rate of the quasi-equity.

In case of non payment at the end of 5 years, quasi-equity will be convertible into ordinary shares.

Equity Loan: The equity loan shall be repayable along with unpaid interest accrued at the end of five years.

Mode of Application The application can either be:

Completed online on the DBM website by filling an online registration form.

OR

Completed at the DBM office (Please see List of Partners for contact details)

10

Business Development Scheme

Scheme Business Development SchemeObjective of Scheme To finance projects in the following sectors:

Manufacturing - start-ups, expansion, modernisation, computerisation, working capital finance

Trade and service - setting up, expansion, modernisation, computerisation, working capital finance

Transport - purchase of public service vehicle (taxis, buses, lorries etc), installation of GPS-based security, anti-theft and energy-saving devices

Printing and publishing - setting up, expansion, modernisation, computerisation

Health – setting-up, expansion, refurbishment of clinics, pharmacies

Tourism – setting-up, expansion, refurbishment of hotels/restaurants, purchase of contract cars

Any other tourism-related activity

Professionals - setting up of office

ICT - start-ups, expansion, modernisation and other ICT-related projects

Art – art exhibition, recordings, stage plays, publication of books

Participation in overseas trade fairs and surveys

Purchase of land for industrial, agricultural or commercial purpose for own use

Purchase or construction of industrial, commercial or office building for own use

Implementing Agency Development Bank of Mauritius (DBM)

Maximum Loan Amount 75% of project cost up to a ceiling of Rs 5 M

Interest Rate Repo Rate + 3 % p.a (presently 7.65 % )

Repayment Period Up to 8 years

Moratorium Period Up to 3 years

Security - General Floating Charge and /or Fixed Charge on immovable property

- Personal Guarantee, where applicable- ‘Gage sans deplacement’ on vehicle, where applicable- Pledge of rights to the lease, where applicable- Fixed Charge on Pledge of rights to the lease- Any other collateral security acceptable to the DBM- Decreasing Term Assurance

11

Eligibility - Individuals, Partnerships or Companies holding valid licences/permits

- Registered local and export-oriented SMEs - Projects recommended by Enterprise Mauritius, BOI,

SMEDA, Tourism Authority, NWEC and other relevant institutions

- Any small viable enterprise holding a Business Registration Card

Mode of Application The application can either be:

Completed online on the DBM website by filling an online registration form. ORCompleted at the DBM office (Please see List of Partners for contact details)

12

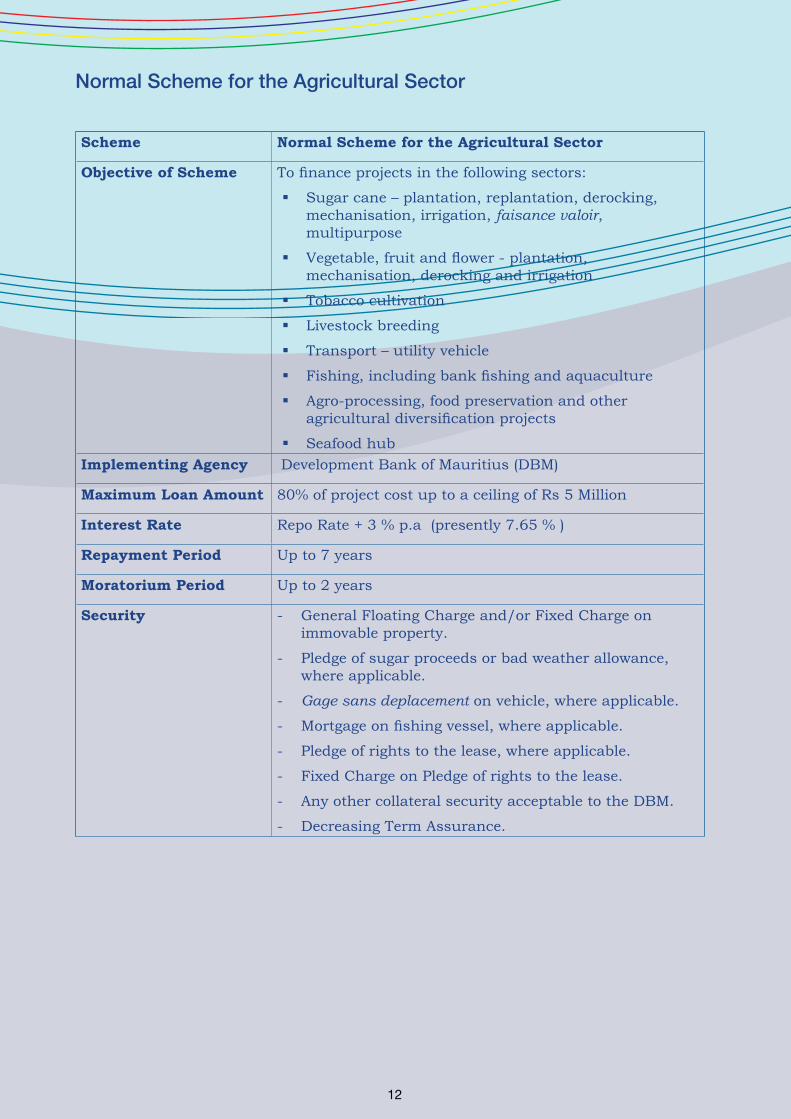

Normal Scheme for the Agricultural Sector

Scheme Normal Scheme for the Agricultural Sector

Objective of Scheme To finance projects in the following sectors:

Sugar cane – plantation, replantation, derocking, mechanisation, irrigation, faisance valoir, multipurpose

Vegetable, fruit and flower - plantation, mechanisation, derocking and irrigation

Tobacco cultivation

Livestock breeding

Transport – utility vehicle

Fishing, including bank fishing and aquaculture

Agro-processing, food preservation and other agricultural diversification projects

Seafood hubImplementing Agency Development Bank of Mauritius (DBM)

Maximum Loan Amount 80% of project cost up to a ceiling of Rs 5 Million

Interest Rate Repo Rate + 3 % p.a (presently 7.65 % )

Repayment Period Up to 7 years

Moratorium Period Up to 2 years

Security - General Floating Charge and/or Fixed Charge on immovable property.

- Pledge of sugar proceeds or bad weather allowance, where applicable.

- Gage sans deplacement on vehicle, where applicable.

- Mortgage on fishing vessel, where applicable.

- Pledge of rights to the lease, where applicable.

- Fixed Charge on Pledge of rights to the lease.

- Any other collateral security acceptable to the DBM.

- Decreasing Term Assurance.

13

Eligibility - Planters/farmers registered with AREU, SPWF, SIFB, FSC

- Operators registered with the Ministry of Agro-Industry and Food Security

- Operators registered with the Ministry of Fisheries

- Other operators in the agri-business, fishing and seafood hub sector holding valid licences

- Other projects recommended by AREUMode of application The application can either be:

Completed online on the DBM website by filling an online registration form.

OR

Completed at the DBM office (Please see List of Partners for contact details)

14

Special Loan Scheme for the Agricultural Sector

Scheme Special Loan Scheme for the Agricultural Sector

Objective of Scheme To finance projects in the following sectors:

Sugar cane - fine derocking and irrigation

Potato or onion cultivation

Fruit and flower - cultivation, fine derocking, irrigation

Biotechnology - hydroponics, tissue culture etc

Off-lagoon fishing - purchase of fishing vessel and en-gine/s

Storage of agricultural produce - construction of shed/store

Production of agricultural seedlingsImplementing Agency Development Bank of Mauritius (DBM)

Maximum Loan Amount 80% of project cost up to a ceiling of Rs 1.0 M

Interest Rate Repo Rate + 3 % p.a (presently 7.65 % )

Repayment Period Up to 7 years, including a moratorium of up to 2 years

Security - General Floating Charge and/or Fixed Charge on im-movable property.

- Pledge of sugar proceeds, where applicable

- Any other collateral security acceptable to the DBM

- Insurance of fishing vessel

- Decreasing Term AssuranceEligibility - Planters/farmers registered with AREU, SPWF, SIFB,

FSC

- Operators registered with the Ministry of Agro-Industry and Food Security

- Operators registered with the Ministry of Fisheries

- Other operators in the agri-business sector holding valid licences

- Other projects recommended by AREUMode of application The Application can either be:

Completed online on the DBM website by filling an online registration form.

OR

Completed at the DBM office (Please see List of Partners for contact details)

1515

Loan Guarantee Scheme

Scheme Loan Guarantee Scheme

Objective of scheme To assist SMEs in raising finance from commercial banks to meet their working capital needs and their expansion as well as create new jobs.

Facilities The Loan Guarantee Scheme provides financing to entrepreneurs without the need to provide collateral and third party guarantees.

Implementing Agency Restructuring Working Group (RWG)

Interest Rate Interest rate at repo+3 % (presently at 7.65 %.)

Eligibility Criteria SMEs with a turnover less than Rs10M

Mode of Application The SME should apply directly to any commercial banks, which is involved in the scheme.

Validity period of the scheme

Scheme will end by 31 December 2016.

16