Embed Size (px)

Citation preview

1

RECOMMENDATION PAPER

“SMEs & Access to Finance”

Thematic Pole 2

2

TABLE OF CONTENTS

Introduction ...................................................................................................................................................................... 4

Chapter 1 - SME’s and finance in the EU: the state of the art ................................................................................ 5

1.1 The approach ........................................................................................................................................................ 5

1.2 Perceptions about the future ............................................................................................................................. 7

1.3 Summary of the state of the art ......................................................................................................................... 9

Chapter 2 - Focus area: Finance and social entrepreneurship ........................................................................... 11

2.1 SMEs, Social Enterprises and Finance .............................................................................................................. 11

2.2 Social Enterprises and new financial instruments ......................................................................................... 12

2.3 The future .............................................................................................................................................................. 15

2.3.1 Vision .............................................................................................................................................................. 15

2.3.2 Actions ........................................................................................................................................................... 16

2.3 SMEs and Social Enterprises: common challenges and common facilitators ......................................... 17

Chapter 3 – The role of the EU .................................................................................................................................... 17

3.1 EU’s institutional action until today .................................................................................................................. 17

3.2 SMEs & Finance and the MFF 2014 2020 period ............................................................................................ 19

3.3 SMEs&Finance in the new transnational cooperation programmes ........................................................ 20

3.3 Summary of the role of the EU .......................................................................................................................... 25

Chapter 4. Insights from Thematic Capitalization Pole Members ........................................................................ 27

4.1 VIBE PROJECT ....................................................................................................................................................... 27

The future role of Transnational Cooperation Programmes on Finance .................................................... 27

4.2 I3E Project ............................................................................................................................................................. 28

Specific Focus Areas and main evidences ...................................................................................................... 28

The future role of Transnational Cooperation Programmes on Finance .................................................... 28

4.3 APP4INNO ............................................................................................................................................................. 29

The future role of Transnational Cooperation Programmes on Finance .................................................... 30

4.4 FOROPA ................................................................................................................................................................ 30

The future role of Transnational Cooperation Programmes on Finance .................................................... 30

4.5 IDWOOD ................................................................................................................................................................... 31

The future role of Transnational Cooperation Programmes on Finance .................................................... 31

4.6 EVLIA .......................................................................................................................................................................... 32

The future role of Transnational Cooperation Programmes on Finance .................................................... 33

4.7 CLOUD .................................................................................................................................................................. 34

Specific Focus Areas and main evidences ...................................................................................................... 34

The future role of Transnational Cooperation Programmes on Finance .................................................... 34

Chapter 5. Insights from Pole Leaders’ Project Partners ........................................................................................ 35

3

5.1 PBN - Hungary ...................................................................................................................................................... 35

The future role of Transnational Cooperation Programmes on Finance .................................................... 35

5.2 RRA - Slovenia ...................................................................................................................................................... 36

The future role of Transnational Cooperation Programmes on Finance .................................................... 36

5.3 ARGE - Austria ...................................................................................................................................................... 36

The future role of Transnational Cooperation Programmes on Finance .................................................... 37

5.4 CCIS ....................................................................................................................................................................... 37

The future role of Transnational Cooperation Programmes on Finance .................................................... 37

Chapter 6 – Other Perspectives ................................................................................................................................. 39

6.1 SEE Thematic Capitalization Pole 1 ................................................................................................................. 39

6.2 SEE Thematic Capitalization Pole 5 ................................................................................................................. 40

6.3 SEE Thematic Capitalization Pole 8 ................................................................................................................. 42

6.4 SEE Thematic Capitalization Pole 9 ................................................................................................................. 42

6.5 Insights from other Transnational Cooperation Programmes – Interreg IVc ............................................ 43

6.5.1 Policy Recommendations for fostering entrepreneurship.................................................................... 43

6.5.2 Policy Recommendations for creating innovation systems ................................................................. 44

6.5.3 Policy Recommendations for boosting innovation capacity in SMEs ............................................... 44

7. Conclusions ................................................................................................................................................................ 45

7.1 Recommendations for policy/ programme makers .................................................................................... 45

7.2 Recommendations for the financial sector ................................................................................................... 50

7.3 Financing SMEs and Social Enterprises: final reflections and possible tools ............................................. 50

7.4 Some ideas to inspire new thinking ................................................................................................................. 52

Bibliography ................................................................................................................................................................... 53

4

Introduction

SMEs in Europe

With over 20 million SMEs in the EU representing 99% of businesses, they are key for economic growth,

innovation, employment and social integration. The European Commission is clearly focused in its aims to

promote successful entrepreneurship and the South East Europe Programme is supporting this in the

region by addressing deficits with improved supporting structures and processes for SMEs.

Projects on the programme include topics around SME financing, IPR, clusters/business parks, social

enterprises, technology platforms, ICT support. With a wide range of complementary SME support

measures necessary for a developed innovative SME sector there exists capitalization and synergy

possibilities between projects but also other initiatives and programmes that project provider

organizations are involved with.

The focus of the Thematic Pole

Based on the main evidences of the SEE Annual Conference 2013 as well as the contributions that have

been sent after it, the “Competitive SME Support Service” Thematic Pole has decided to focus its work

on the relationship between SMEs and Finance.

Specifically, it has been decided to jointly work on a Recommendation Document targeted to a)

Managing Authorities, b) Public policy makers, c) SMEs themselves.

The document aims to be a light insight on how project leaders see the future evolution of the

relationship between SMEs and the financial industry.

It does not have the ambition of being persuasive with the financial industry or change the way SMEs

refer to banks or investors but to provide insights about a) how transnational programmes may

contribute to tackle specific issues and b) how new relationships SMEs and the financial sector may be

created.

The structure of the document

Chapter 1 aims at providing a short overview of the state of the art of SME’s perceptions on finance and

how external financing is (or not) happening in the EU. The main evidences for this first part have been

extracted from the SMEs’ Access to Finance survey – Analytical Report, November 2013.

Chapter 2 provides a specific focus on “finance and social entrepreneurship”: this part has been

developed as a specific added value provided by the Ease&See project coordinated by the Thematic

Pole 2 Leader City of Venice.

Chapter 3 provides insights on progress done at institutional level by the EU and how the new

programming period will (or not) facilitate the implementation of initiatives opening new financial

perspectives for SMEs’ owners or financial managers. Comments on some specific objectives of the most

relevant Transnational Cooperation Programmes (relevant also for SEE Programme Area members) with

5

the goal of explaining if and how those priorities may be relevant to improve SME’s capacity to increase

their “financial appeal”.

Chapters 4, 5 and 6 collect the evidences and proposals provided by four levels of stakeholders: Pole

Leader project partners, Thematic Pole members, SEE Thematic Pole Leaders. The chapter has been

enriched also with contributions extracted from Capitalization Documents of Interreg IVc and Interreg

Central Europe.

Conclusions summarize Recommendations in order to provide an easy and quick to use roadmap for

future action.

Chapter 1 - SME’s and finance in the EU: the state of the art

The Directorate General for Enterprise and Industry of the European Commission, in cooperation with the

European Central Bank, requested a study on SME’s access to Finance in 2013. The survey was

conducted by Ipsos MORI.

All SME managers who participated in the survey were asked to evaluate a pre-supplied list of eight

potential problems that their companies may currently be facing on a 10 point scale. Fifteen per cent of

SMEs in the EU cited access to finance, which placed it second just after finding customers (22%).

The analysis provided evidence about the fact that the approach to finance remains “traditional”, in

other terms it is still focused on traditional channels like bank overcrafts, leasing, trade credit and bank

loans.

1.1 The approach

A traditional approach to finance

6

Only 5% of EU SMEs had used equity financing in the last six months. It was nearly twice as

common among larger businesses (9% of those with 250+ employees) in the EU.

What was the purpose?

Also the purpose confirms a sort of traditional approach to finance. The analysis shows that the main

reasons for financial resources from 2011 to 2013 was mainly related to purchase of land, buildings and

equipment while “business development related activities” (like research, purchase of other businesses,

promotion and training) are limited to 2-4%.

SMEs’ perceptions on finance

It is also interesting to highlight what the perception of SME’s managers in Europe was in 2013: there was

a negative perception in terms of availability of external financing and the banks’ willingness to provide

a loan was seen to have deteriorated over the last 6 months. Additionally those EU SMEs who could

make a judgment for the mentioned analysis, they were four times as likely to judge that it had

deteriorated (17%) rather than improved (4%), whilst 29% assessed it as unchanged. Last but not least,

only 16% of EU SMEs were able to give an opinion about the willingness of investors to invest in equity in

the past 6 months (in 2013), the great majority of SMEs considering this as not applicable to their firm.

Changes in the availability of external financing

In 2013 the majority opinion (43%) was that the availability of bank loans had not changed but the SMEs

were still more likely to have seen availability deteriorate (15%) rather than improve (9%). A similar

7

balance of opinion was also valid for availability of bank overdrafts, where 9% reported improvement

and (15%) reported deterioration.

Almost half of EU SMEs (47%) were not able to give an opinion on the availability of trade credit, stating

this was not applicable to their firm. From those who gave an opinion, a majority (37% overall) said that

the availability of trade credit remained unchanged. One in ten SMEs (8%) reported that availability had

deteriorated, slightly higher than those who reported an improvement (5%).

For equity investment and debt securities, those who were not able to give an opinion due to this type of

financing not being applicable to their firm stood at 78 per cent, and for debt securities this figure rose to

86 per cent. Looking at those who were able to give an opinion, the SMEs were evenly divided as to

whether availability of these finance sources had improved or deteriorated over the past 6 months.

Improvement and deterioration scores for both were very low, varying between 0% and 2%. The

proportion of SMEs indicating that the availability of equity investments had remained unchanged has

remained the same over the three waves of the survey, at 17% of SMEs surveyed. Debt securities also

followed the same trend in 2013 as in 2009 and 2011 with around one in ten SMEs reporting no change in

availability in the past 6 months.

Although just under half of EU SMEs (47%) were unable to give an opinion on the availability of other

sources in 2013, opinions were fairly evenly divided as to whether the availability of these sources had

improved (7%) or deteriorated (6%).

1.2 Perceptions about the future

SME’s outlook for the future

SMEs’ confidence in obtaining future financing from banks has remained static since 2011, with almost

two thirds (63%). Similarly, the proportion not confident with talking to banks has remained broadly the

same, declining one percentage point to 24%.

The proportion of SME managers who did not think that talking to equity investors and venture capital

firms for financing was applicable to their firm has risen to 63% - this is a statistically significant increase on

2011, which was itself a significant rise on 2009.

Overall, one in seven (15%) of SME managers felt confident in talking to equity investors about financing,

and one in five or 19% were not confident. Both represent reductions from 2011, explained by the

increase in SMEs who feel that it is not relevant to them.

As with the previous survey years, bank loans are the most preferred type of external financing amongst

SMEs that expect to grow in the next two to three years. In 2013, the proportion was two-thirds (67%),

which is a small increase on 63% from 2011.

The next most popular source of external financing was other types of loans, such as trade credit or a

loan from a related company, shareholders, or public sources, which was favored by around one in

eight (12%) of managers. Only 6% favored equity investments, down from 7% in 2011.

8

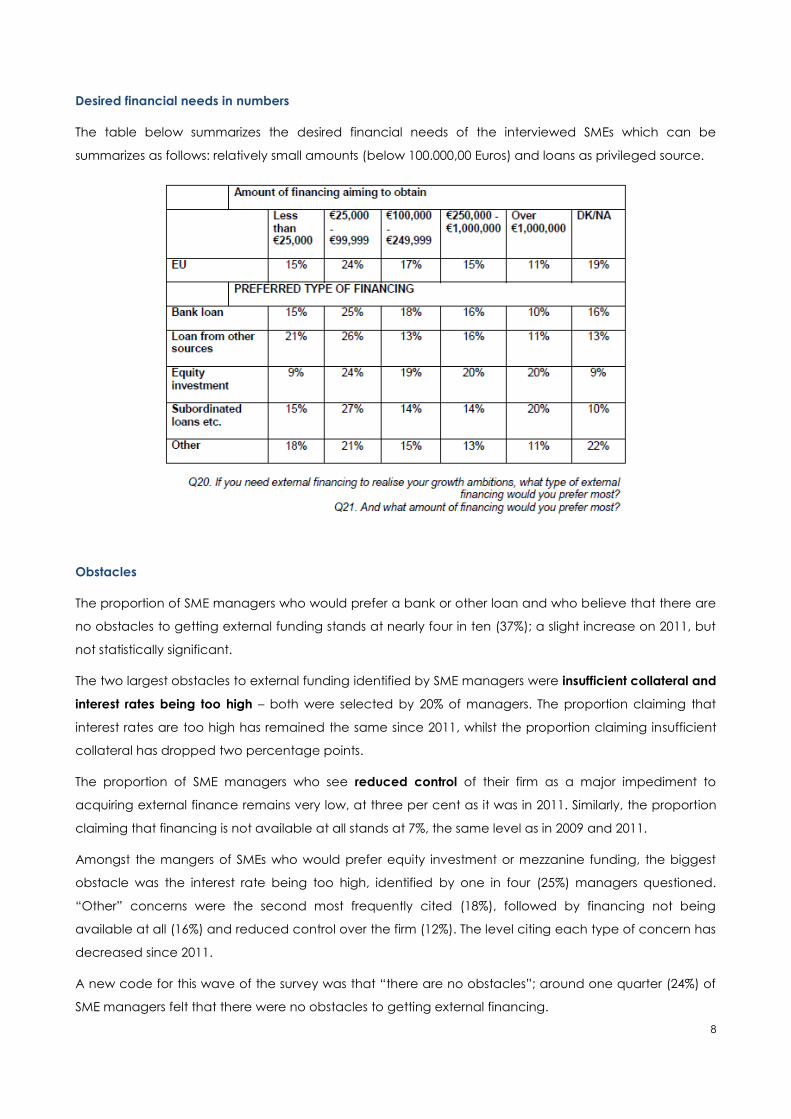

Desired financial needs in numbers

The table below summarizes the desired financial needs of the interviewed SMEs which can be

summarizes as follows: relatively small amounts (below 100.000,00 Euros) and loans as privileged source.

Obstacles

The proportion of SME managers who would prefer a bank or other loan and who believe that there are

no obstacles to getting external funding stands at nearly four in ten (37%); a slight increase on 2011, but

not statistically significant.

The two largest obstacles to external funding identified by SME managers were insufficient collateral and

interest rates being too high – both were selected by 20% of managers. The proportion claiming that

interest rates are too high has remained the same since 2011, whilst the proportion claiming insufficient

collateral has dropped two percentage points.

The proportion of SME managers who see reduced control of their firm as a major impediment to

acquiring external finance remains very low, at three per cent as it was in 2011. Similarly, the proportion

claiming that financing is not available at all stands at 7%, the same level as in 2009 and 2011.

Amongst the mangers of SMEs who would prefer equity investment or mezzanine funding, the biggest

obstacle was the interest rate being too high, identified by one in four (25%) managers questioned.

“Other” concerns were the second most frequently cited (18%), followed by financing not being

available at all (16%) and reduced control over the firm (12%). The level citing each type of concern has

decreased since 2011.

A new code for this wave of the survey was that “there are no obstacles”; around one quarter (24%) of

SME managers felt that there were no obstacles to getting external financing.

9

Important factors on future financing

Last but not least, we would like to highlight which factors – according to SMEs – may contribute to

facilitate access to financial resources.

The first 2 most relevant measures rely on an active role of public actors while there are 2 factors which

refer to a proactive role of service providers (also specialist ones).

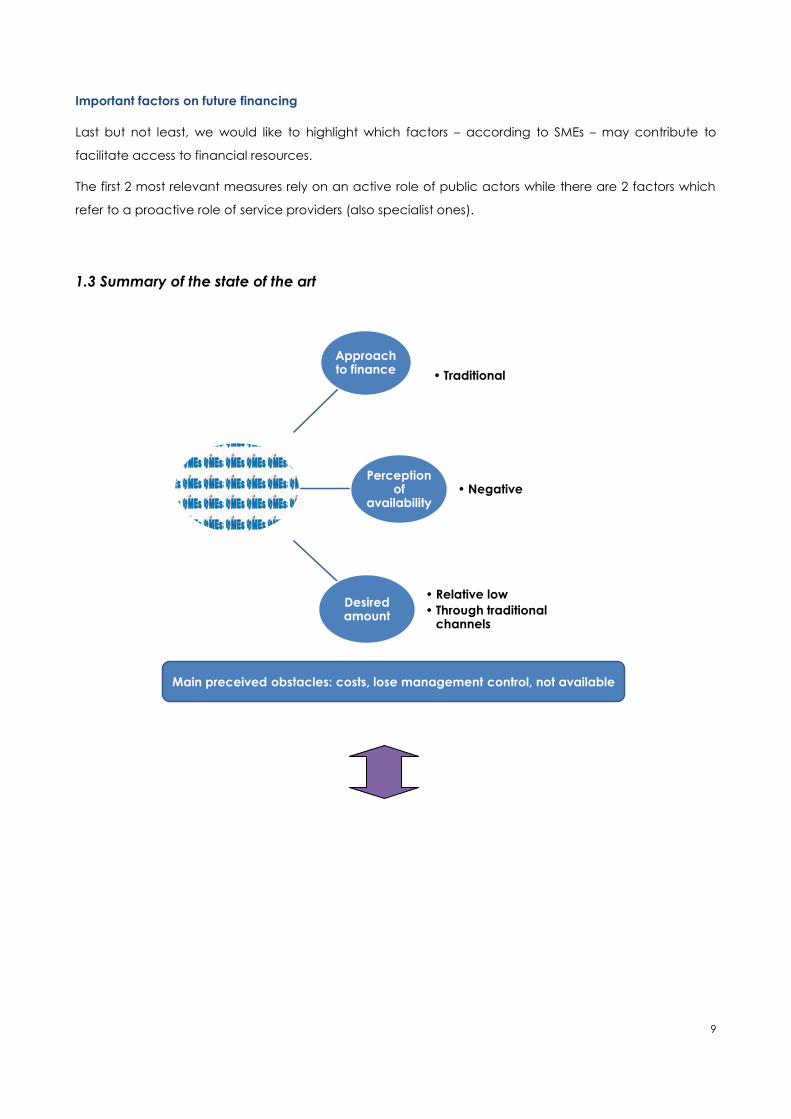

1.3 Summary of the state of the art

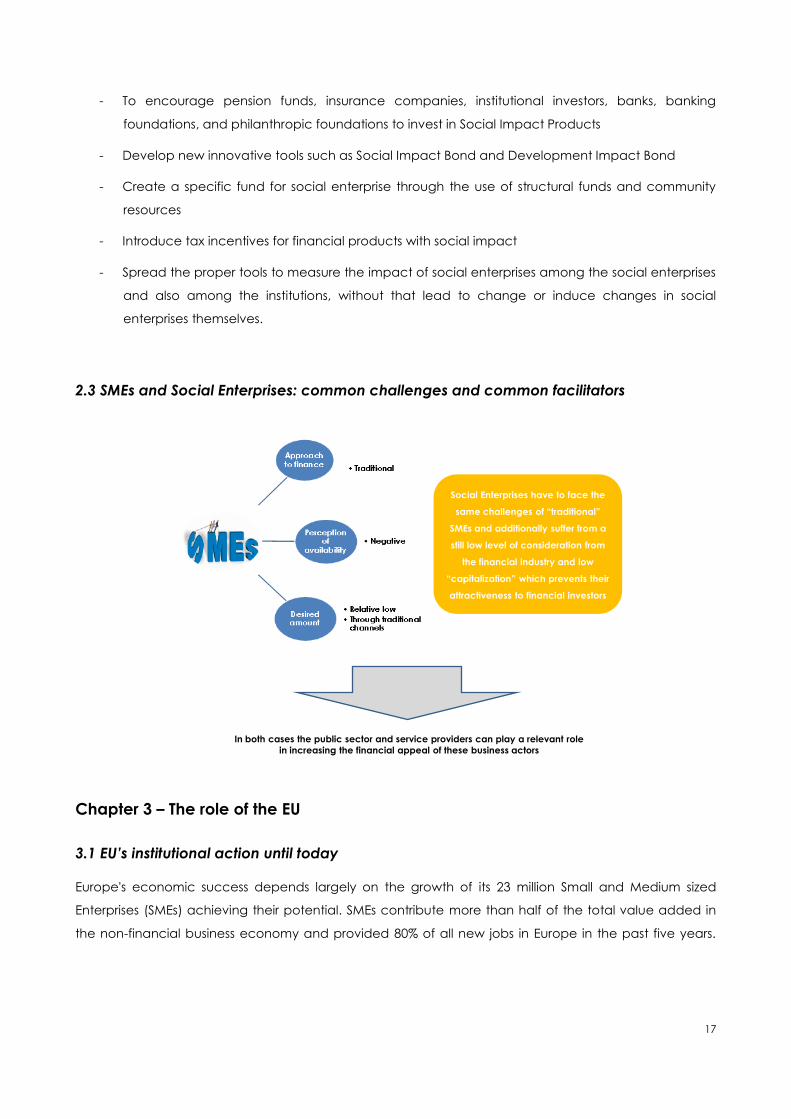

Approachto finance

• Traditional

Perceptionof

availability• Negative

Desiredamount

• Relative low

• Through traditionalchannels

Main preceived obstacles: costs, lose management control, not available

10

11

Chapter 2 - Focus area: Finance and social entrepreneurship

Social enterprises confirm to be productive and competitive undertakings, thanks to the high level of

personal motivation of their staff and the European Commission acknowledges that the social economy

players are able to produce social innovation, inclusion and to find original and sustainable solutions for

the needs of citizens. But there is also a general consensus about the fact that we can’t ask social

enterprises to have a big impact if they can’t get the resources they need to grow bigger.

The EASE&SEE project provided evidence about the fact that the financial industry, at least in some

countries, is more and more looking at social enterprises as a potential new market. If we look at what is

happening in Italy or in some central and northern countries we may observe for instance ventures

which are pro-actively investigating the phenomenon (to understand if there is a market potential),

regional bodies launching tenders to review public financial mechanisms which may be used also by

social enterprises, new approaches to micro-credit and its impact on social enterprises, private banks

arranging road-shows to provide evidence about their interest in supporting development strategies of

social enterprises and again private banks developing dedicated financial instruments as a means to

support SE development.

2.1 SMEs, Social Enterprises and Finance

The relationship between SMEs (Small Medium Enterprises), SEs (Social Enterprises) and finance has been

subjected to various innovations during the nineties, able to join and support the evolution in progress in

these areas.

In terms of SMEs and SE, not to mention the differences between the dynamics of the two sectors, the

consolidation of a dual structure has taken place in Europe. On one side we find the creation of large

companies and organizations (districts, consortia, networks, etc.) able to achieve significant forms of

self-financing (fundraising, donations, privileged access to foundations, public procurements, etc.); on

the other side we have witness the diffusion of co-operative structures at the local level to meet the

growing demand for goods and services in the public and private sectors.

This is due to the processes of privatization and the so-called 'modernization' of the public sector, as well

as and to the new quality demand for goods and services (eco-friendly products, local economies,

direct producer-consumer relationship, etc.) by households and enterprises.

In terms of the credit institutions there has been a consolidation of the traditional relationship between

cooperative banks and local credit and the rise of new initiatives in these areas and sectors (ethical

banks, microcredit, etc.). In this process we register also initiatives taken by large banks creating

specialized services for the ‘third sector’ and the local economies.

Both processes outlined here bore the imprint: 1) a negative one, to be the by-product of privatization of

public welfare, and therefore to be influenced by political dynamics and lobbied that this entails and

the neo-liberal ideology of competitiveness and the 'price'; 2) a positive one, to be stimulating factors to

12

the renewal of the SMEs and SEs role and function, and that is the awareness of the need for

modernization of management and financial factors that support their activities.

At European and national level this is reflected in the conflict between two trends: a) The approach

prevailing in the European Commission and the European Central Bank for the integration of the

financial systems according to the logic of international finance, more or less regulated by itself

(profitability, technocratic control of the central banking system, etc.); b) the position advocated by the

big organizations of credit unions (cooperative credit) (especially in Italy, Germany, Netherlands, France,

Austria), which seek to protect the specificity, autonomy and strength of action of this sector.

At the beginning of the millennium the financial flows toward SMEs /SEs were as follows:

1. public procurement;

2. lending from the banking system

3. self-financing

4. Volunteering (defined undeclared work in the SMEs).

The 2008 crisis dries up these streams:

- Public procurement shrinks because of the cuts imposed on public spending (3% etc.). The

rhetoric to speedy up the payments of government’s debt to SMEs and IS is blurred by the fact

that in addition to not paying the public sector is generally reducing its demand.

- The big banks suspended lending to enterprises, particularly SMEs / SEs, encouraged by the ECB,

prompting them to channel funds received towards itself, or big financial operations and

investments.

- The territorial link between cooperative, ethical credit system and SMEs / SEs remain active

during the crisis in financing these sectors. But it is precisely for the reason to put an end to such

‘distorsion’ of a consistent part of the general saving that ECBs initiative for a European Union

Bank was conceived. It is used as a tool to delegitimize the cooperative banking sector (see the

results of the first audit report on European banks) and to return this large area of savers and

savings in the area of finance altogether. Applied across the banking sector - large and small

companies, investment banks and commercial banks, profit, non-profit and for-profit - to the

criteria of efficiency of the big banks and speculative finance means to get their hands on the

mass of the credit cooperative sector, bringing it back into the flow of speculative finance

indistinct.

2.2 Social Enterprises and new financial instruments

Social Venture Capital

13

The social venture capital addresses a varied market, from traditional target VC sectors – like ICT

(information communication technology) and more recently bio-technologies and alternative energies –

strictly speaking the third sector. The VC’s aim is to grant risk capital (or equity) to new or expanding

enterprises, in high development-potential sectors. Moreover, a VC fund plays the role of “active”

investor in the financed business, giving the new enterprise specialist know-how, which is essential to

strengthen the management activity and as a consequence its financial returns (for a traditional VC)

and its financial and social returns (for a social VC).

Venture Philanthropy (VP) consists in the application of VC’s policies to the non-profit sector, not in order

to gain returns from invested capital, but to obtain the best result in terms of entrepreneurial activity and

economic and social development.

The VP invests in purely non-profit organizations or non-profit organizations which manage trade activities

with a reinvestment of profit in their own business to which profit logics are applied in order to maximize

their social value on cost-performance conditions.

In real terms, the VP imports into the third sector methods and instruments of enterprise support and

measurement of performances typical of VC, including, amongst other things: due diligence,

benchmarking, monitoring of objectives, preparation of a business plan and in general greater attention

for accountability. The VP translates into an actual partnership between the investor, the philanthropic

organization which manages the fund and the financed enterprise.

Social Impact Bond

A SIB, in its original version, is a contract between the Public Administration and investors where the

former raises funds to achieve a social objective and undertakes to repay the obligation undertaken

within set times. A public authority issues a bond to raise capitals which will be used to finance a specific

project which can produce savings for the authority and a better social outcome. In exchange the

authority undertakes to pay part of any savings gained to investors. Repayment is proportional to results.

Social investors, when subscribing a SIB, achieve both a social and a financial return which will be the

greater the better the result of the financed programme.

Social enterprises, finally, thanks to the resources they raised, receive payment for the services they

supply while being made able to pursue their mission.

The main focus shall be social value creation, additional objectives such as the improvement of the

efficiency and effectiveness of the public action are functional to achieving the former.

Social return on investment

Social return on investment (SROI) is a principles-based method for measuring extra-financial value (i.e.,

environmental and social value not currently reflected in conventional financial accounts) relative to

resources invested. It can be used by any entity to evaluate impact on stakeholders, identify ways to

improve performance, and enhance the performance of investments.

14

The SROI method as it has been standardized by the SROI Network provides a consistent quantitative

approach to understanding and managing the impacts of a project, business, organisation, fund or

policy. It accounts for stakeholders' views of impact, and puts financial 'proxy' values on all those

impacts identified by stakeholders which do not typically have market values. The aim is to include the

values of people that are often excluded from markets in the same terms as used in markets, that is

money, in order to give people a voice in resource allocation decisions.

Some SROI users employ a version of the method that does not require that all impacts be assigned a

financial proxy. Instead the "numerator" includes monetized, quantitative but not monetized, qualitative,

and narrative types of information about value.

Social Impact Investment

Impact investing is one form of socially responsible investing and serves as a guide for various investment

strategies. According to the definition of the Global Impact Investing Network (GIIN): "Impact

investments are investments made into companies, organizations, and funds with the intention to

generate a measurable, beneficial social and environmental impact alongside a financial return.

Impact investments can be made in both emerging and developed markets, and target a range of

returns from below-market to above-market rates, depending upon the circumstances." Impact

investing tends to have roots in either social issues or environmental issues, and has been contrasted with

microfinance.

Impact investing occurs across asset classes; for example, private equity/venture capital, debt, and

fixed income.

Impact investors are primarily distinguished by their intention to address social and environmental

challenges through their deployment of capital.

Impact investing is distinguished from crowdfunding sites, such as Indiegogo or Kickstarter, because

impact investments are typically debt or equity investments (with longer-than-traditional venture capital

payment times) and an "exit strategy" (traditionally an initial public offering (IPO) or buyout in the for-

profit startup sector) may be non-existent. Although some social enterprises are nonprofits, impact

investing typically involves for-profit, social- or environmental-mission-driven businesses. Impact investing

is distinguished from microfinance primarily by deal size, and secondarily by the investment for equity

rather than debt.

Hybrid organization

The organization of the commercial and social sectors has long been governed by an assumption of

independence between commercial revenue and social value creation. For more than a century,

activities necessary to create commercial revenue, it was assumed, could not substantially affect or

improve on social welfare, and vice versa. Thus most organizations that sought to pursue social value

and commercial revenue simultaneously pursued differentiated strategies.

15

For instance, venture philanthropy programs were viewed as a nonbusiness activity and were

conducted at arm’s length from corporations’ core activities. On the other hand, many nonprofit

organizations attempted to sell products or services, creating revenue streams to reduce dependence

on philanthropic and public funders. Yet earned income programs, often unrelated to the core activities

of nonprofits, did not always live up to expectations.

Hybrid organizations combine the social logic of a non-profit with the commercial logic of a for-profit

business, but are still very difficult to finance.

2.3 The future

2.3.1 Vision

The historical experience of co-operative production and credit movements, shows that they are an

important means of containment and innovation in the economy. They are the essential tools, especially

in a modern economy, to create the substrate on which finance and credit for SMEs and SEs can exist

and develop. An anti-crisis model that draws strength and effectiveness through the relationship with the

territory and the ability to extend credit to households and small and medium-sized enterprises. A real

alternative to the system of investment banks increasingly involved in speculative operations.

The European dimension of the financial cooperative system has been known since the nineteenth

century. The existing system has its strengths in Germany, the Netherlands, France, Austria and Italy. Its

viability depends on the ability to have followed a number of paths due to the diversity of the historical

reasons for their foundation, and having to provide answers to the needs and opportunities of various

territories.

In the EU the system of credit cooperatives, on the eve of the crisis (2007), consisted of 4,000 local and

regional banks, 62,000 branches and 49 million members. The market shares amounted to 60% in France,

50% in Austria, 40% in Germany and the Netherlands, 39% in Italy and 10%% in Spain and Portugal. (2007

data).

In Italy, recent data provided by Giulio Sapelli, indicate just under 12.5 million customers, distributed

among more than 9 thousand branches of 72 banks, which are governed mainly due to the nearly 1.4

million members and work of 82 thousand employees. The contribution of cooperative institutions is 460

billion Euros of assets and loans that reach € 400 billion, or about 25% of the national total.

The key to this lies in the sustainability of their traditional and historical commitment to the territory in

which they are rooted, in support for small and medium-sized enterprises and households. The data of

the years of the crisis show that it is the banking sector that has not speculated, which maintains a base

of shareholders and customers for their peoples and local businesses, as demonstrated by the 200 billion

euro in new loans to small businesses, provided a total of 2008 onwards, so keeping a level of

commitment similar to that available to most of the companies' smaller in the years preceding the crisis.

The cooperative credit system confirms its cyclical behavior. And thereby going opposite the behavior

of the banks that have significantly reduced their efforts in these areas.

16

The cooperative credit system, SMEs and SEs can try to negotiate niche areas, restricted by definition,

fitting, however, in the flow determined by big business and its logic of financing. This can be attempted

in the forms of representation that exist today that do not distinguish these areas from the rest of the

economy (in Italy, Confindustria, ABI, and so on). This would be the case if the SMEs / SEs embrace the

ideology of growth (‘big is beautiful’), which is equivalent to plan their disappearance is at the local

level and national level.

Alternatively, the cooperative credit system, SMEs and SEs agree on a pact of solidarity, but not for

survival but for the revival of an economy model - national and European - based on the regionalization

of production systems and markets to manage and revive its areas of activity extended to new areas of

culture, tourism, services for the citizens, and so on.

This is not a project for the 'third sector' or for SMEs, but to rebuild the foundations of the European

project on the object of cooperation, solidarity, and social and territorial cohesion.

2.3.2 Actions

The list of intervention typologies required for this specific enterprises may be summarized as follows:

1) Promotional initiatives are needed and an appropriate informative system still has to be put in

place at least in the Programme Area in order to allow social enterprises to be “educated” and

properly informed about finance and its role in contributing to enterprise development and

strategies;

2) Financial Governance mechanisms: the financial industry should be involved when it goes to

prepare, design and implement financial mechanisms and tools at local, regional and National

level which are targeted to social enterprises;

3) Financial instruments and incentives should be rationalized at all levels (fund of funds).

Concrete financial options to be activated:

1) Innovation should be primarily supported (prices, prototypes, co-innovation practices);

2) Capitalization should be strengthened;

3) Financing risk capital through venture capitalists and business angels;

4) Corporate restructuring should be incentivized (where relevant) in order not to lose value;

Support services should be strengthened or implemented (even better if they had previous financial

experiences) to support social enterprise financial officers or to support financial programs.

Additional possible proposals for developing social enterprises (in the broad sense) in relation to the

investments (impact funds):

17

- To encourage pension funds, insurance companies, institutional investors, banks, banking

foundations, and philanthropic foundations to invest in Social Impact Products

- Develop new innovative tools such as Social Impact Bond and Development Impact Bond

- Create a specific fund for social enterprise through the use of structural funds and community

resources

- Introduce tax incentives for financial products with social impact

- Spread the proper tools to measure the impact of social enterprises among the social enterprises

and also among the institutions, without that lead to change or induce changes in social

enterprises themselves.

2.3 SMEs and Social Enterprises: common challenges and common facilitators

Social Enterprises have to face the

same challenges of “traditional”

SMEs and additionally suffer from a

still low level of consideration from

the financial industry and low

“capitalization” which prevents their

attractiveness to financial investors

In both cases the public sector and service providers can play a relevant role

in increasing the financial appeal of these business actors

Chapter 3 – The role of the EU

3.1 EU’s institutional action until today

Europe's economic success depends largely on the growth of its 23 million Small and Medium sized

Enterprises (SMEs) achieving their potential. SMEs contribute more than half of the total value added in

the non-financial business economy and provided 80% of all new jobs in Europe in the past five years.

18

SMEs often face significant difficulties in obtaining the financing they need in order to grow and

innovate1.

One of the key priorities set out in Europe 2020, the EU's growth strategy for the coming decade, as well

as in the Commission's Single Market Act2 and the Small Business Act3 is to facilitate access to finance for

SMEs. The Annual Growth Survey has underlined the crucial role of a healthy financial system to support

growth and set out priorities for action in the short-term perspective.

In this context the reform programme for financial services, implemented as a response to the financial

crisis, can bring about regulatory benefits to SMEs. In addition, the Commission is proposing to release

new targeted funding at EU level to address the key market failures that limit the growth of SMEs.

On 7 December 2011 the Commission has adopted an Action Plan outlining the various policies that it is

pursuing to make access to finance easier for European SMEs. Proposed regulatory and other measures

aimed at maintaining the flow of credit to SMEs and to improving their access to capital markets, by

increasing the visibility to investors of SME markets and SME shares, and by reducing the regulatory and

administrative burden.

The reform programme for financial services, implemented as a response to the financial crisis, included

a number of proposals that will positively stimulate the financial sector's contribution to funding the real

economy and will bring about regulatory benefits to SMEs.

Specifically the document proposed to

- Improve the regulatory framework for venture capital

- Work on State aid rules relevant for SME access to finance

- Improve SME access to capital markets through some regulatory changes

- Review the impact of bank capital requirements on SMEs

- Accelerate the implementation of the Late Payments Directive

- Introduce an innovative regime for European Social Entrepreneurship Funds

Here follows a short overview of the most relevant measures.

Regulation on European Venture Capital Funds

On 17/04/2013 the EU Parliament and the Council adopted a regulation which sets out a new

“European Venture Capital Fund” label and includes new measures to allow venture capitalists to

market their funds across the EU and grow while using a single set of rules

1 COMMUNICATION FROM THE COMMISSION TO THE COUNCIL, TO THE EUROPEAN PARLIAMENT, TO THE COMMITTEE OF THE

REGIONS, AND TO THE EUROPEAN AND SOCIAL COMMITTEE. An action plan to improve access to finance for SMEs

{SEC(2011) 1527 final}

2 COM 2011 206

3 COM (2011) 78

19

This Regulation lays down uniform requirements and conditions for managers of collective investment

undertakings that wish to use the designation ‘EuVECA’ in relation to the marketing of qualifying venture

capital funds in the Union, thereby contributing to the smooth functioning of the internal market.

It also lays down uniform rules for the marketing of qualifying venture capital funds to eligible investors

across the Union, for the portfolio composition of qualifying venture capital funds, for the eligible

investment instruments and techniques to be used by qualifying venture capital funds as well as for the

organization, conduct and transparency of managers that market qualifying venture capital funds

across the Union.

European long term investment funds

On 26 June 2013, the European Commission proposed a new investment fund framework designed for

investors who want to put money into companies and projects for the long term. These private European

Long-Term Investment Funds (ELTIFs) would only invest in businesses that need money to be committed to

them for long periods of time

The document lays down uniform rules on the authorization, investment policies and operating

conditions of EU alternative investment funds (AIFs) that are marketed in the Union as European long-

term investment funds (ELTIFs).

Additionally the EU has been working on regulatory benefits for SMEs in the fields of

- Markets in financial instruments (MiFID)

- Transparency Directive

- Capital Ratios Directive (CRD IV)

- Crowdfunding

- Social entrepreneurship funds (see below)

3.2 SMEs & Finance and the MFF 2014 2020 period

Finding appropriate ways to finance the real economy and especially SMEs is a priority for the European

Union4. Under this perspective, “finance” is both a means as well as a working-topic within the new

multiannual financial framework.

If we look at finance as a “means”, the 2014-2020 programming period foresees an increased use of FI

for all Thematic Objectives (Transnational Cooperation) and across all sectors (Thematic Funds). A

number of FIs are foreseen to provide financing to SMEs with the objective of moving away from grant

4 Financial instruments means Union measures of financial support provided on a complementary basis from

the budget to address one or more specific policy objectives of the Union. Such instruments may take the form

of equity or quasi-equity investments, loans or guarantees, or other risk-sharing instruments, and may, where

appropriate, be combined with grants

20

mechanisms towards FIs, namely revolving funds focused on productive investment that also allows for

greater participation of the private sector. Furthermore, there is a wide interest in ensuring the strong

commitment of the financial intermediaries in taking the role of bodies implementing FIs, in order to

increase efficiency in the delivery of funds and leverage the amount of funds made available through

private participation.

Indeed, SMEs play an important role in the new programming period 2014-2020. The largest and the most

important program is Horizon 2020, in which the European Commission has provided the appropriate

tools for the support of small and medium-sized enterprises. This program has a special measure (SME

Instrument) to encourage small and medium size enterprises to participate on it and to enhance their

innovative potential, making funding mechanisms simpler and more responsive to their needs.

The EC has also developed financial instruments in the two main programs (COSME and Horizon 2020)

with the aim of improving the access to credit for businesses and in particular for SMEs, which provide a

way of facilitating credit and equity instruments risk.

The list of available options for SMEs to directly join EU funded initiatives which may contribute to their

investment and development plans include:

- Life 2014 2020

- Creative Europe

- Erasmus Plus

- COSME

- Horizon

Additionally, other programmes sector specific programs may be considered like

- AAL

- IMI

- Eurotransbio

3.3 SMEs&Finance in the new transnational cooperation programmes

Adriatic Ionian

Evidences of the SWOT and Needs Analysis

The “challenges and needs” analysis included in the draft programming document evidence under the

“smart growth” goals the difficulties of businesses to access finance as one of the threats related to

increase the “competitiveness of SMEs” and, under the “inclusive growth” goal, a Poor disposition of

SMEs to invest in vocational and dual training under the “skills and education” item.

21

Among the needs which have been associated to smart and inclusive growth goals, quite many are

referred (directly or indirectly) to the necessity of identifying ways to foster investments at different levels

(R&D, technology, business development).

Potential Priority Axis to be used

Priority Axis 1 - Innovative region, and its specific objective 1.1: “Support the development of innovation

networks and clusters among regions, academia and enterprises in the AIO region” could probably be

the ideal arena to work on the different roles of “finance” and the mechanisms to be implemented in

order to make real investments happen.

The expected results listed in the Programme indeed may require an in-depth analysis of

a) how, when and through which mechanisms finance may play a role in increase new innovation

approaches in the fields of EcoInnovation; Public Procurement for Innovation; Creative Industry;

Service Industry and Social Innovation, Procurement and Social Innovation;

b) the necessity of improving the framework conditions also to facilitate access to finance

c) the role of financial stakeholders in the fields of research, innovation and utilisation

d) the necessity of involving financial stakeholders to fully take advantage of emerging market

opportunities in the Programme Area

Please note that SMEs are a target group for the Programme, not direct beneficiaries.

Danube Transnational Programme

Challenges

The Programme document provides evidence (among many other factors) of the necessity of

diminishing hindering factors in the diffusion of knowledge and innovations (ability to implement

knowledge-based and technology intense activities).

In the field of research and innovation, important disparities, both in terms of its resources allocated but

also in its structures and human resources available are evidenced. The uneven distribution of research

and innovation capital is mainly due to the different framework conditions the sector is facing

throughout the region. The wide range of financial allocations and policies governing the research

sector are determining the institutional capacities of the actors involved, leading to different levels of

performance.

These disparities may be addressed by an increased level of interconnectivity among the actors active

in the sector, creating the conditions to better use the potential existing in the less developed regions.

Potential Priority Axis to be used

Priority axis 1: Innovative and socially responsible Danube region (working title) and its specific objective

1: “Improve framework conditions and a balanced access to knowledge Improve the institutional and

infrastructural framework conditions and policy instruments for research & innovation and ensure a

22

broader access to knowledge for the development of new technologies and the social dimension of

innovation (SP1)” could probably be the ideal arena to work on the different roles of “finance” in this

Programme Area.

As the program document states, the innovative capacity and sustainable structures for research and

innovation are determined by the interplay of factors which enable knowledge to be converted into

new products, processes and organisational forms which in turn enhance economic development and

growth. One of the factors to be taken into consideration is also the financial sector and its

organizations.

Through Transnational cooperation the program aims at evaluating the feasibility of transnational tools

and services also in the field of a) better access to innovation finance, subsidies and incentives for R&D,

access to venture capital (access to finance), b) support for innovative public procurement (which

could be seen as an indirect financial instrument) as driver for innovative products and services

Among the listed actions to be supported the programme mentions: a) Improve the access to finance

through the establishment of a Danube Region Research and Innovation fund; b) support for innovative

public procurement: Improved public procurement practices can help foster market uptake of

innovative products and services. At the same time these practices will raise the quality of public

services in markets where the public sector is a significant purchaser. It is therefore important to mobilise

public authorities to act as "launching customers" by promoting the use of innovation-friendly

procurement practices

Please note that SMEs are a target group for the Programme, not direct beneficiaries.

Balkan Mediterranean Programme

Evidences of the SWOT and Needs Analysis

Under the Competitiveness axis, the SWOT analysis evidences among the weaknesses a) strong

economic regional disparities & areas with low competitiveness’ performance as well as b) difficulties to

access credit. While among the threats there is evidence of Access to credit hampered by the crisis

(contracting financial markets).

Potential Priority Axis to be used

Priority Axis 1: Entrepreneurship& Innovation and its Specific Objective 1.1 “Promote entrepreneurship

and business creation on the basis on new ideas, innovation and new types of business models” are

suggested as the main playground even though the action level will be mainly focused on SME’s

capacity building.

23

The Balkan-Mediterranean region is characterized by strong entrepreneurial spirit and diverse economic

activity. SMEs and microenterprises in particular, represent a substantial part of all economic sectors in

participating countries and though they form more than 60% share of the total value added they suffer

from recession and low growth levels, structural markets’ weaknesses with respect to unemployment and

limited access to financing.

The enhancement of SMEs’ capacity is crucial and can be achieved through a comprehensive set of

actions linking overall business’ support to education and training. The exploitation of new ideas,

innovation and new types of business models enables the differentiation of innovation patterns

according to the potentials and needs of a specific territory.

The Programme suggests to leverage on a transnational approach in a) supporting new business

models, ideas and innovations and at the same time enhancing the SMEs’ capacity of SMEs by

implementing also actions related to education and training in order to enable SMEs acquire the

necessary skills/tools to boost their competitiveness; b) linking business’ support and businesses ’ training

helps to create new business models. Promoting entrepreneurship through clusters and cluster policies,

by facilitating the economic exploitation of new ideas will help to overcome strong economic regional

disparities prevailing in the region.

Among the types of actions which are considered to be privileged, the program document lists

a) Joint actions to assist fast access to various financial and development instruments supporting

SMEs;

b) Enhancement and support of business information and centres, including virtual ones, to

promote innovative and new business models’ applications;

c) joint organisation of promotional activities in identified target markets;

Please note that SMEs are a target group for the Programme, not direct beneficiaries.

Interreg Europe

Evidences of the Needs and Challenges analysis

The programme area consists of 286 regions10. The situation and prospects of these regions in light of

these challenges are very diverse. The 8th progress report on cohesion also underlines this picture and

identifies the need for cohesion programmes to support growth-enhancing and job-creating

investments, with an emphasis on a few important areas such as innovation and SMEs, energy efficiency

and a low-carbon economy, employment and education.

Potential Priority Axis to be used

Priority Axis 2: competitiveness of SMEs and its Specific Objective 2.1: Improve the implementation of

regional development policies and programmes, in particular programmes for Investment for Growth

and Jobs and, where relevant, ETC programmes, supporting SMEs in all stages of their life cycle to

24

develop and achieve growth and engage in innovation” are suggested as the main playground where

the main actors involved will be regional policy and programming bodies .

The main change sought under this axis is an improved implementation of regional policies and

programmes, in particular programmes for Growth and Jobs and ETC, that support the creation,

development and growth of small and medium sized enterprises. The potential for enterprises to create

new or use existing market opportunities begins with the presence of entrepreneurial skills (including,

according to us, financial management skills). Regional policies therefore need to actively support

entrepreneurship development and capacity building as a building block for business creation and

growth.

It is equally crucial that regional authorities and business support actors respond adequately to the key

challenges that obstruct businesses on their path to growth, such as access to finance (e.g. through

facilities for start-up capital or guarantees) and knowledge and to international markets. Certain priority

target groups of entrepreneurship policies (e.g. young people, migrants or female entrepreneurs) may

also require specific support.

A transparent and dependable business climate is crucial for all economic actors. Regional procedures

can be made more business-friendly, e.g. related to public procurement or e-invoicing.

The document describes that the programme will support exchange of experiences and sharing of

practices between actors of regional relevance with the aim to prepare the integration of the lessons

learnt in regional policies and actions for entrepreneurship and SME support and the programme will

facilitate policy learning and capitalisation by making relevant practices and results from interregional

cooperation and other experiences widely available and usable for regional actors involved in

innovation support in G&J, ETC and other programmes.

Please note that SMEs are a target group for the Programme, not direct beneficiaries.

Central Europe 2020

Evidences of needs analysis

Under the Thematic objective “Strengthening research, technological development and innovation”,

the needs analysis highlighted that a) there is an uneven distribution of R&D activities across Central

Europe, b) There is a high potential for mobilizing synergies between business and research and

investments in product and process innovations but linkages are not sufficiently established, c) the lack

of innovative skills and knowledge is a major shortcoming in regions lagging behind, d) Potentials of

transnational and regional clusters remain unused, e) A lack of cooperation and common innovation

strategies hinders the use of synergies. According to us all these needs indirectly send us back to the

necessity of introducing the role of financial institutions in contributing to mind these gaps.

Potential Priority Axis to be used

Priority Axis 1 – “Cooperating on innovation to make CENTRAL EUROPE more competitive”

25

Under this priority, the CENTRAL EUROPE Programme addresses key socio-economic challenges and

needs within central Europe that are related to smart growth as defined in the Europe 2020 Strategy. It

aims at more effective investment in research, innovation and education.

The programme will help strengthening potentials of technology - oriented areas that are destinations of

foreign investments and capital flows, notably through better linking actors of innovation systems. This will

enhance the transfer of research and development (R&D) results and the set-up of cooperative

initiatives and clusters. It will also address regional disparities in knowledge and education such as brain

drain, and strengthen capacities and competences for entrepreneurship and social innovation, also

responding to challenges related to demographic change.

Specific Objective 1.1: To improve sustainable linkages among actors of the innovation systems for

strengthening regional innovation capacity in central Europe

This will be achieved through transnational and internationalized regional networks and clusters fostering

technology transfer and the development and implementation of new services supporting innovation in

businesses. Increased cooperation between actors of the innovation systems, especially between

business and research, will improve access to research results for enterprises, notably SMEs, thus

stimulating further investment in innovation. Furthermore, the link between research and public

administration will be strengthened (e.g. by setting up specific mechanisms and promoting public

procurement of innovation) which could positively contribute to both economic and social innovation

transfer

3.3 Summary of the role of the EU

Ask and need

support to increase

access to finance

Are recognized as

yey actor in the

EU growth strategy

Financial support as

a means to

develop

Finance as part of

the thematic

strategy

Thematic

Programmes

Cooperation

Programmes

26

The list of programs and the abstracts of the priority axis show that the relationship between Finance and

SMEs in Europe is based on a double approach.

On one side the EU is extending the array of financial instruments available to SMEs and which can be

used to make their development processes more and more European.

On the other side, the EU continues to work on innovation, competitiveness and entrepreneurship thus

opening the ground to “finance” as at least a strategic topic which has to be addressed by proposals.

27

Chapter 4. Insights from Thematic Capitalization Pole Members

4.1 VIBE PROJECT

Lead Partner: Slovenian Public Agency for Entrepreneurship, Innovation, Development, Investment and

Tourism

SMEs and Finance: main perceived constraints

Generally speaking SMEs have different financing opportunities: Structural Funds, ERDEF, state aid. In

reality, possibility for access of different funds is difficult: high rate of co-financement is required and

if you are a start-up you are not able to get credit from banks or from other sources. This happens

not for textile sector but for all type of activities. SMEs from textile have to cope with problems of

low financing of innovation (at national level), lack of business-angels or investors, difficult access or

no access to bank funds (depending on company’s assets). Pre-seed or seed funding for start-ups

are also very difficult to find.

The VIBE project addressed the challenge of developing the innovation and entrepreneurship system

across the SEE by enabling private investment into innovative entrepreneurial companies in partnership

with smart public initiatives and investment. VIBE offered a transnational integrated approach, mobilizing

a critical mass of the regional investment, innovation agencies and providing efficient support to

investors, policy makers and agencies with the aim to encourage high-growth of entrepreneurs across

the Regions.

Start-ups were the main beneficiaries of the VIBE project.

The future role of Transnational Cooperation Programmes on Finance

Priorities and objectives

Access to finance is consistently rated as the biggest challenge for high-growth innovative companies.

Fostering both access to venture capital, corporate investment, business angel activity and linking in

with international investors as well as increasing the growth potential of innovative companies and their

investor-readiness are crucial to the development of a knowledge-based economy in the SEE region

Transnational cooperation programmes could be a possibility for innovative SMEs, but they need most

of all support at national level to go internationally (level advice3, coaching, incubation services).

Business angel networks and brokerage events are really needed by SMES.

The Innovation Union is a very nice objective for all EU countries, but not easy to reach by every country.

Innovation should have more funding actors and instruments in order to boost the innovation and

blooming innovative companies, with high growth potential (“gazelles”) and start-ups.

Project typologies

Is difficult to answer. Looking from an SMES point of view, a small dedicated program will be useful.

28

Involvement and contribution of the financial sector

Financial actors should directly be involved as partners in transnational cooperation projects. They can

participate in different phases of the project implementation and benefit from the results in respect of

IPR.

Additionally they should play a more important role in carrying out policies in industrial sector, in

strategies for development, in higher education, in business coaching and mentoring.

4.2 I3E Project

Lead Partner: ISI - Industrial Systems Institute / Research Centre ATHENA

Specific Focus Areas and main evidences

SMEs and Finance: main perceived constraints

Financing is scarce for SMEs mainly due to the economic crisis. Banks are lending less and less money,

which has created a very difficult situation for all companies, but mainly SMEs. In the sector of micro-

electronics, ICT and embedded systems, SMEs face further problems as they have to finance innovation

as well. This appears to be quite difficult to be done via traditional financing instruments. The anticipated

sources of financing, i.e. business angels or venture capitals, for such types of companies are quite few

and do not provide sufficient funding for innovative SMEs in Europe like for instance in USA Achievements

The main focus of the I3E project was twofold: the elaboration of a Strategic Research Agenda in the

thematic areas of Embedded Systems and Industrial Informatics out of a wide consensus building activity

in the area of South East Europe involving stakeholders from academia / research, policy making and

enterprises, including SMEs, and the elaboration of a methodological guide addressing the process for

the transformation of research to innovation. The latter comprised a part for the financing of innovation

at the seed, start-up, early-growth and expansion stages. In this context, it provided information on the

different forms of financing innovation, also applicable to innovative SMEs.

The I3E methodology guide on innovation comprises a chapter on financing innovation detailing the

different stages that an innovative SME has to go through and the difficulties that it faces when in comes

to financing its activities at the different stages before its viability is ascertained. In this context the

methodology guide helps develop a good understanding of the financing needs of an innovative

enterprise during the seed, the start-up, the early-growth and the expansion stages. Different financing

instruments are explained comprising feasibility grants, microcredit, business angels and venture capital,

while successful experiences in innovation financing are presented and highlighted.

The future role of Transnational Cooperation Programmes on Finance

Priorities and objectives

Transnational cooperation programmes could surely address certain issues associated with financing of

innovative SMEs. By helping build or reinforcing the innovation support framework in an area, they can

29

influence the provision of much needed services to innovative SMEs, like incubation, legal / advisory /

mentoring / coaching support services, capacity building services related to innovation etc.

Furthermore, they may be helpful for the creation of local funds or business angel networks that can

provide direct financing to SMEs.

An important priority for all Europe is enhancing innovation in SMEs. This is in turn associated among other

things with the financing of innovation, which needs special instruments and approaches. Helping

develop such approaches for increasing financing of innovation in the seed, start-up and early-growth

phases would be beneficial for Europe and could be an objective for the new period. Specific actions

associated with this could be supporting projects for the provision of microcredit, or formulation of

business angel networking

Project typologies

I think that addressing the field of finance requires the selection of a small number of large strategic

projects acting as mini-programmes, i.e. funding sub projects through them. In this context, I believe that

this would be the most suitable project typology to follow.

Involvement and contribution of the financial sector

Directly involving the private financing sector in transnational cooperation projects would be beneficial

and could create added value in projects. The role of such participation would be to enable the set up

and enforcement of SME financing mechanisms. In this context, their participation should be limited to

large strategic projects and with reference to specific carefully designed actions. Yet, the usual

bureaucracy of transnational cooperation programmes may inhibit the active participation of the

financing industry in projects.

The role of the Public Sector

Innovating SMEs by default lack at the early stages of their development the capacity to get a bank

loan as they cannot present prove of evidence of their success. In this context, there is a need to

develop support mechanisms and financing mechanisms to provide them with the needed resources at

the seed, start-up and early-growth stages of their development. The public sector should address this

issue, possibly by providing tools for supporting innovation financing, so that the absence of the private

sector in many countries of SEE is efficiently dealt with. Furthermore, and with reference to general SME

financing and taking into account also the economic crisis and the pressure that it has imposed on

banks, alternative tools of SME financing should be sought as well.

4.3 APP4INNO

Lead Partner: Veneto Agricoltura

SMEs and Finance: main perceived constraints

The project did not focus directly on finance but nevertheless an internal investigation on the topic has

been done with a view to contribute to the capitalization work.

30

During the last years, access to medium term credit has been difficult for farmers: the amount of loans

granted per year nearly halved and access to favorable credit decreased by one sixth.

This was mainly caused by the uncertainty of return on investments, less availability of favorable credit

and difficulty in demonstrating farm capital solvency.

The future role of Transnational Cooperation Programmes on Finance

Priorities and objectives

No, because access to credit is often regulated at national level.

Project typologies

Mainly be on experience and knowledge sharing. Lack of evidence of practices limits adoption of

solutions in financial management.

Involvement and contribution of the financial sector

Financial institutions may be involved on demand” when financial issues can manifestly hinder the

project accomplishment.

Financial actors can provide useful consultancy in order to study new financial tools, tailor made for the

project’s partners and objectives.

4.4 FOROPA

Lead Partner: Holzcluster Steiermark GmbH

SMEs and Finance: main perceived constraints

Financing instruments for SMEs are not covered by FOROPA. However, for the implementation of pilot

cases relevant stakeholders (forest-based SMEs, scientific experts) are subcontracted in the project

countries.

With regard to the Austrian bio-energy sector a real lack of finance cannot be observed. Meaningful

and well prepared projects in this sector usually do not face a shortage in finance. For SEE countries it is

to say, that basically investors are available – the barriers that exist are either investors with too little local

knowledge/unrealistic expectations or administrative barriers/unstable political situation in the countries.

The future role of Transnational Cooperation Programmes on Finance

Priorities and objectives

In general, we would not expect transnational cooperation programmes to be a suitable instrument to

overcome the issues outlined above.

Naturally, at project level opportunities exist to establish and bring forward investments/business

partnerships, although experience says that many of such success stories depend on the persons

involved and often happen ad hoc.

31

Project typologies

No recommendations as I think the ETC programme and the derived projects are hardly suitable to

tackle such issues.

Involvement and contribution of the financial sector

We don’t think that a direct involvement in projects is part of their business. In addition, the financial

industry probably lacks of staff to be able to contribute to such projects as a partner.

However, it makes sense to involve representatives of the financial industry as external experts to provide

their experience to projects.

As a cluster organization, we have financial institutions as cluster partners and from time to time we

organize courses for SMEs lectured by bank representatives, tax advisers, insurances, lawyers etc. Typical

topics of those courses are “how to apply for a bank credits”, “practical guidance on how to deal with

banks on various topics”, “What to consider in terms of company insurances”, “Guidance on how to

hand over the company ownership to a successor”, “How to evaluate the value of a company”, etc.

Often those courses are in cooperation with other associations like the Chamber of Commerce.

4.5 IDWOOD

Lead Partner: Slovenian Forestry Institute

SMEs and Finance: main perceived constraints

SMEs facing financial draught nowadays find it difficult to access support services helping to innovate in

technological and non technological aspects. Fund schemes supporting access to “development

services” usually have limited resources and timelines. It would be interesting to gather experience on

funding schemes that with some form of participation from SMEs can be long-lasting and outside usual

bank circuits: some kind of revolving schemes with participation of SMEs.

The future role of Transnational Cooperation Programmes on Finance

Priorities and objectives

Transnational programmes should provide some resources especially to develop activities towards Start-

up phases and R&D (pilot projects) and human capital development of SMEs. Developing Framework

conditions, the core business of TC is essential but launching some more structured operational phase

thanks to the newly created framework conditions would be great opportunity and would grant

commitment from SMEs

Start up: it depends on the project objectives; some time in some sectors it would be ok.

R&D: This is the real thing. Support Framework conditions relates mostly to that but after two or more

years of work you have no resources to operationalize and grant real access to services. There should be

small financial schemes to develop relations R&D Institutes - SMEs that seldom have their research

facilities. Schemes should be regulated by standard procedures and control.

32

Project typologies

The focus could be on elaborating some standard SME financial schemes to support the operativization

of activities: a sort of sustainability launch

The access to this co-financing of some activities by SMEs would be also proof of the targeted approach

of the project

Financing R&D access for SMEs, Banks are usually not competent in this fields as they are simple sellers of

financial instruments elaborated in the main office, There should be some specific parallel activities for

developing banks knowledge how to serve SMEs in specific sectors relevant for the single territories,

technical and technology needs and market chances.

Involvement and contribution of the financial sector

Not as partners but subcontractors. If this possibility would exist, there should be the possibility, for

example, to select in an open competition the financial institutions working within the project. Financial

Institutions must never control project activities.

4.6 EVLIA

Lead Partner: Camera di Commercio di Venezia

SMEs and Finance: main perceived constraints

Considering the activities carried out in our projects, the most important issues for SMEs are linked to the

find possibilities to access finance more easily to get financing for their innovation processes.

In particular, we discover how Intangible Assets are important for SMEs when trying to access financing,

together with the value of a correct and complete valuation of Intellectual Property Rights for the

business of enterprises.

Starting from the difficulties that new and innovative SMEs experienced when attracting external

financing to grow, EVLIA project aims at developing a standardized methodology and tool for the