Embed Size (px)

DESCRIPTION

financial accounting

Citation preview

CHAPTER 1Decision Making and

the Role of Accounting

PowerPoint Presentation by Matthew Tilling

©2012 John Wiley & Sons Australia Ltd

2

YOUR JOURNEY INTO ACCOUNTING

• Accountants– Not ‘Bean Counter’ or ‘Number Crunchers’– Rather Problem Solvers and Decision Makers– Who work in a range of organisations– In a variety of roles

• Accounting– The language of business– More than just bookkeeping

3

THE DECISION-MAKING PROCESS

• Life is full of decisions• Decisions mean making choices– We must choose how to spend our time– We must choose how to spend our resources

• Decisions affect the future• Good decisions require good processes

4

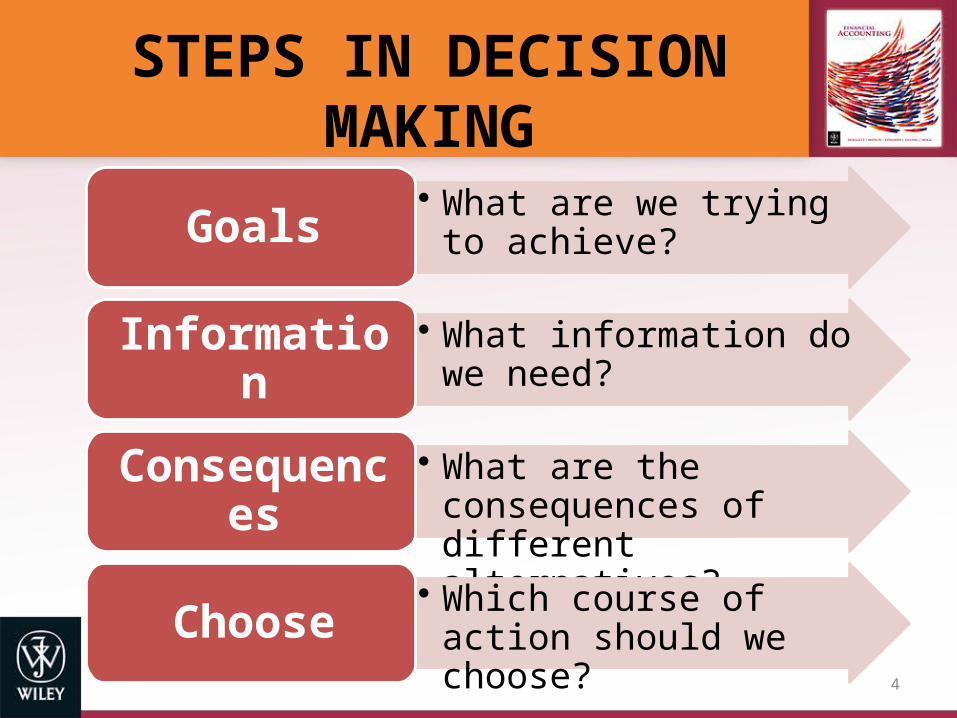

STEPS IN DECISION MAKING

• What are we trying to achieve?Goals

• What information do we need?Information

• What are the consequences of different alternatives?Consequences

• Which course of action should we choose?Choose

5

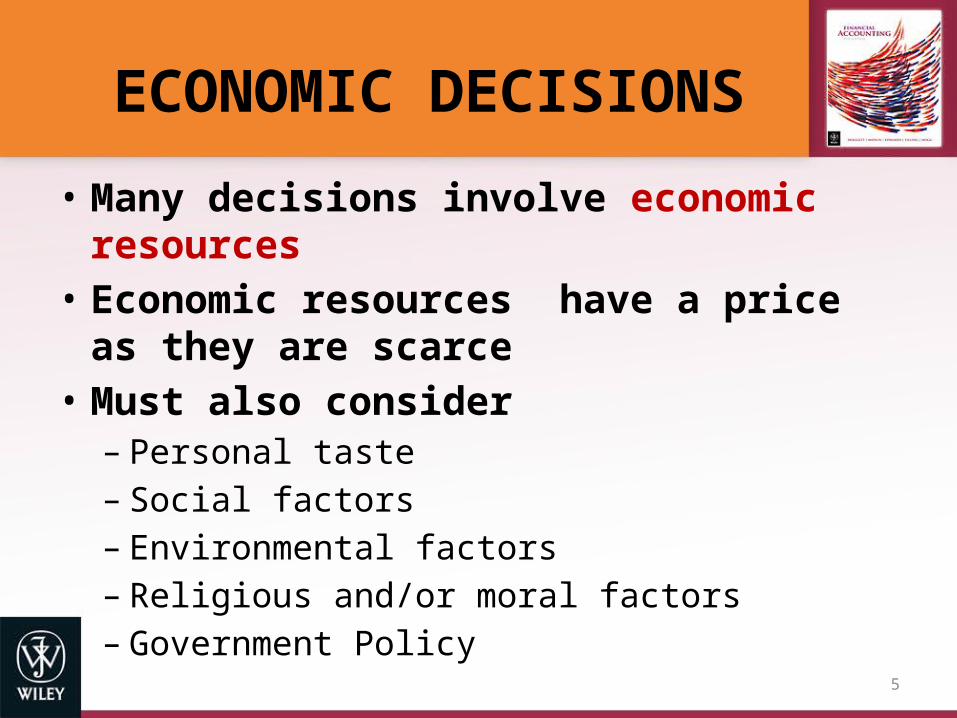

ECONOMIC DECISIONS

• Many decisions involve economic resources• Economic resources have a price as they are

scarce• Must also consider– Personal taste– Social factors– Environmental factors– Religious and/or moral factors– Government Policy

6

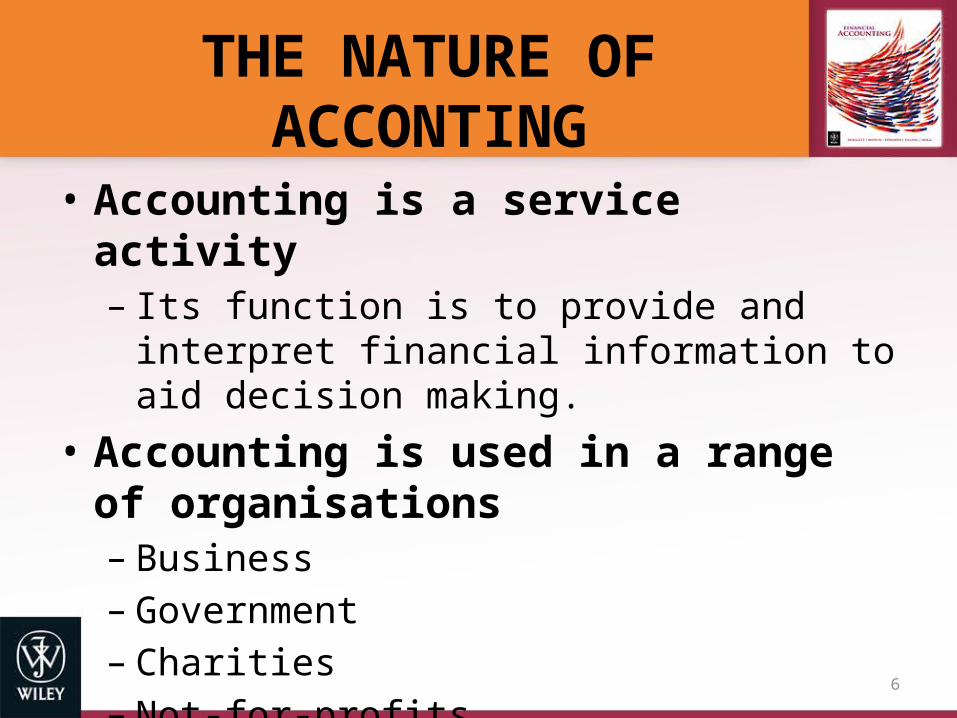

THE NATURE OF ACCONTING

• Accounting is a service activity– Its function is to provide and interpret financial

information to aid decision making.• Accounting is used in a range of organisations– Business– Government– Charities– Not-for-profits

7

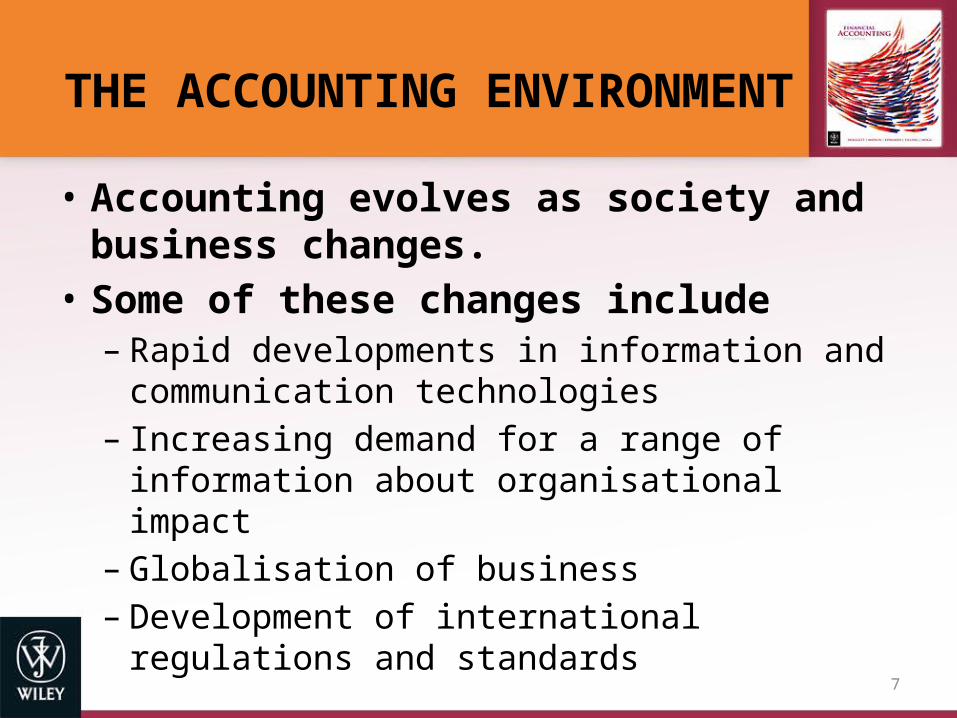

THE ACCOUNTING ENVIRONMENT

• Accounting evolves as society and business changes.

• Some of these changes include– Rapid developments in information and

communication technologies– Increasing demand for a range of information

about organisational impact– Globalisation of business– Development of international regulations and

standards

8

THE ACCOUNTING PROCESS

9

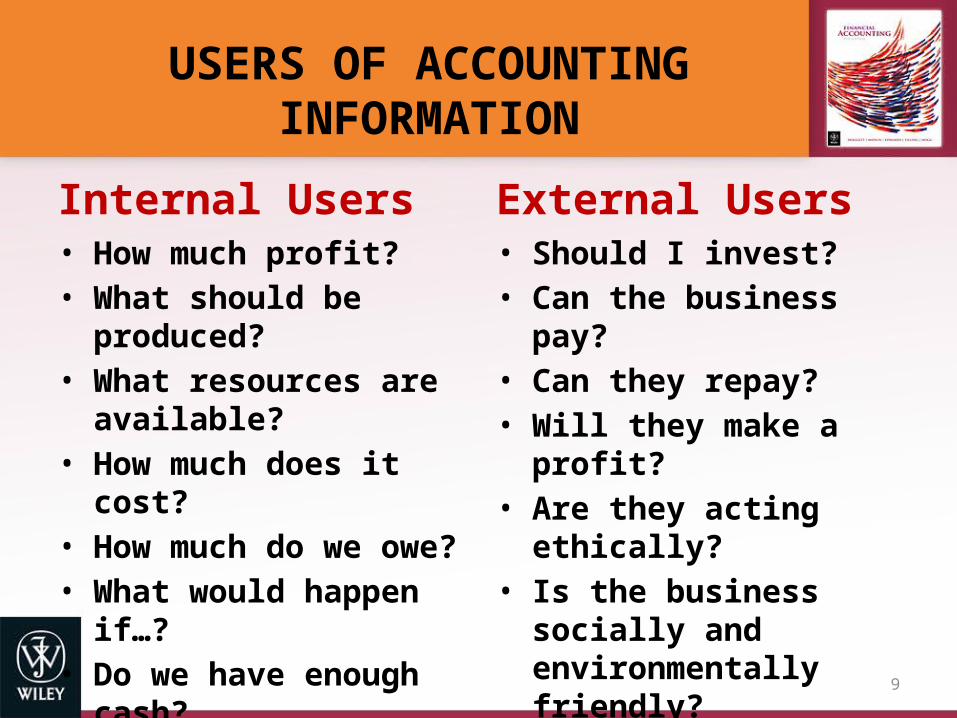

USERS OF ACCOUNTING INFORMATION

Internal Users• How much profit?• What should be produced?• What resources are

available?• How much does it cost?• How much do we owe?• What would happen if…?• Do we have enough cash?

External Users• Should I invest?• Can the business pay?• Can they repay?• Will they make a profit?• Are they acting ethically?• Is the business socially and

environmentally friendly?

10

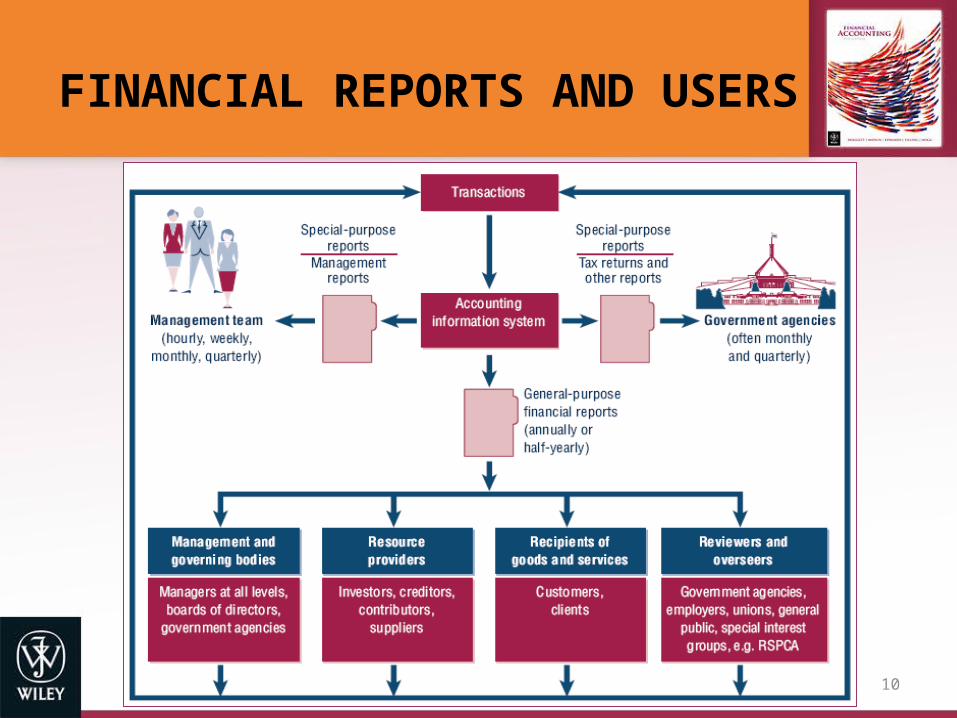

FINANCIAL REPORTS AND USERS

11

USING INFORMATION IN ECONOMIC DECISIONS

• Consider Darren, a hard-working editor, who is ready to take on a new career.

• He has the opportunity to start his own gardening business.

• Using the decision making process already outlined he needs to decide if this is the right decision for him.

12

GOALS

• Darren wants to do something different to sitting behind a desk. So clearly a gardening business will meet this goal.

• He also wants to be financially secure. To establish this will require additional information

13

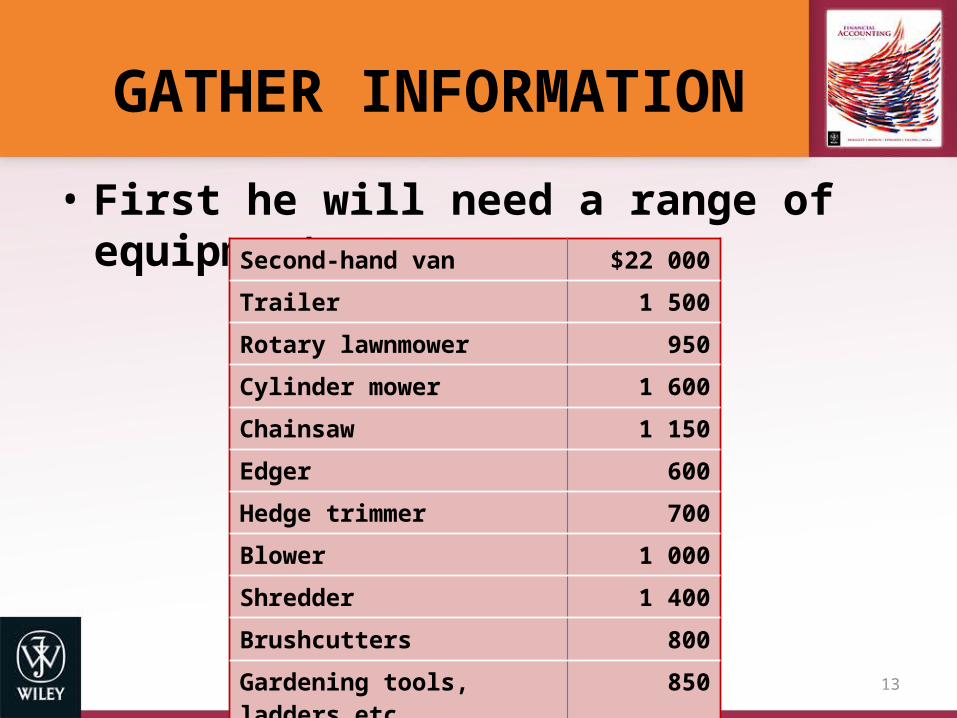

GATHER INFORMATION

• First he will need a range of equipment:Second-hand van $22 000

Trailer 1 500

Rotary lawnmower 950

Cylinder mower 1 600

Chainsaw 1 150

Edger 600

Hedge trimmer 700

Blower 1 000

Shredder 1 400

Brushcutters 800

Gardening tools, ladders etc. 850

$32 550

14

GATHER INFORMATION

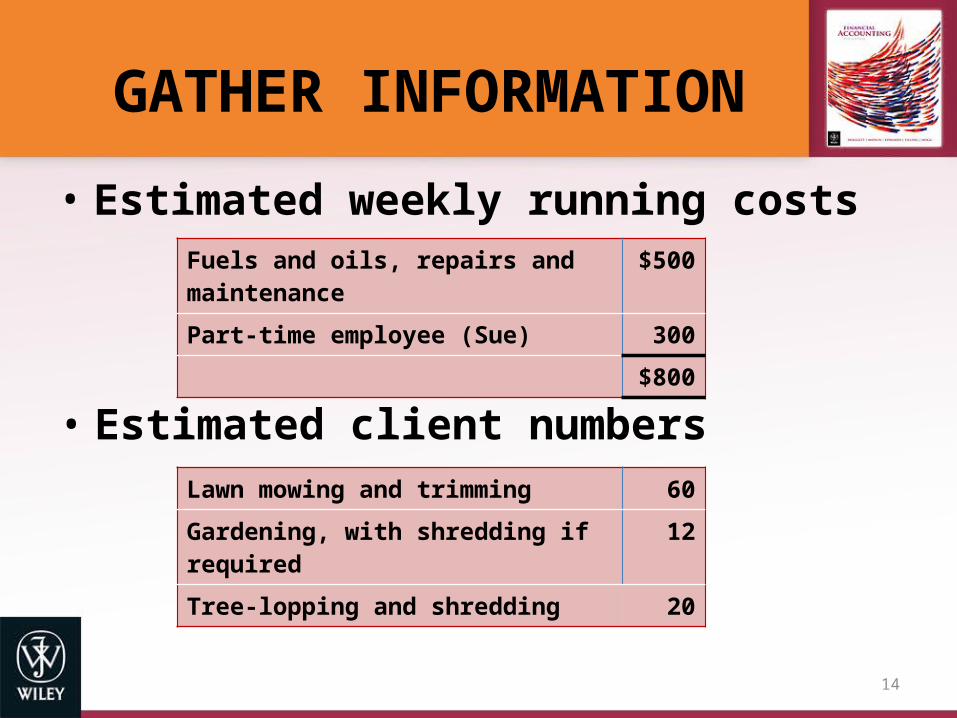

• Estimated weekly running costsFuels and oils, repairs and maintenance $500Part-time employee (Sue) 300

$800

• Estimated client numbersLawn mowing and trimming 60Gardening, with shredding if required 12Tree-lopping and shredding 20

15

GATHER INFORMATION

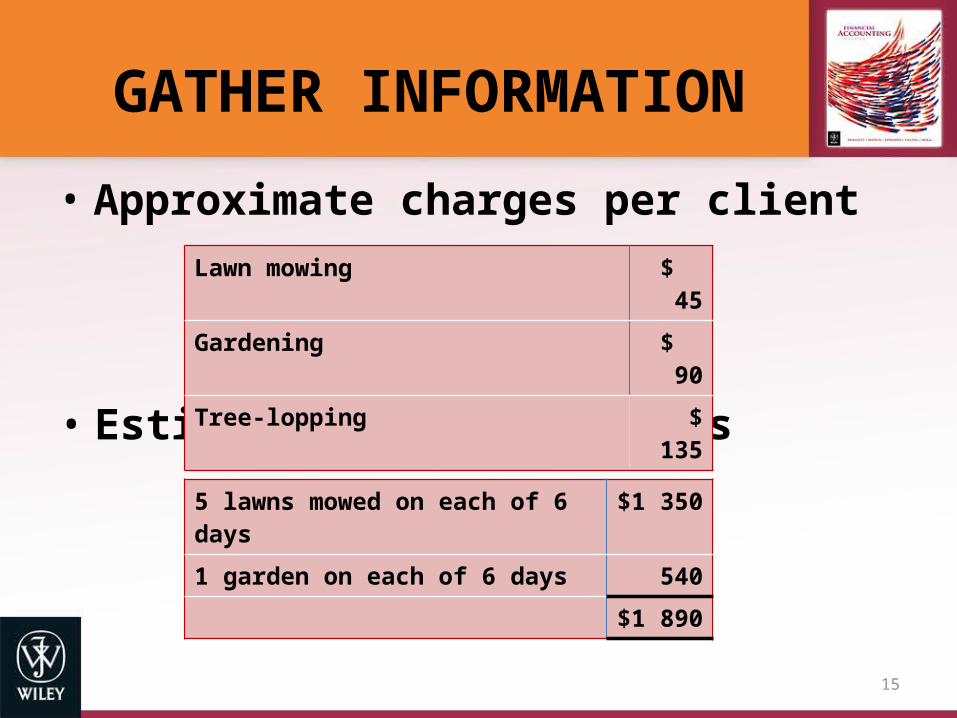

• Approximate charges per client

5 lawns mowed on each of 6 days $1 3501 garden on each of 6 days 540

$1 890

• Estimated weekly receipts

Lawn mowing $ 45Gardening $ 90Tree-lopping $ 135

16

DETERMINE CONSEQUENCES

• Based on these estimates Darren would expect gross annual turnover for a 48 week year of $90 720.

• This is before including additional income from tree-lopping.

• After taking into account costs this should equate to a net weekly cash inflow of at least $1 040 before tax.

17

CHOOSE

• With all these factors in mind Darren can now make an informed decision about his future.

• Would also include non-financial factors.

18

ACCOUNTING INFORMATION AND DECISIONS

• Many decisions require significant amounts of financial information– Accounting information is very important

• Accountants report on the past– Still useful for making decisions about the future– Also useful for assessing past decisions

• Accountants also look to the future– Budgeting; strategy and planning

19

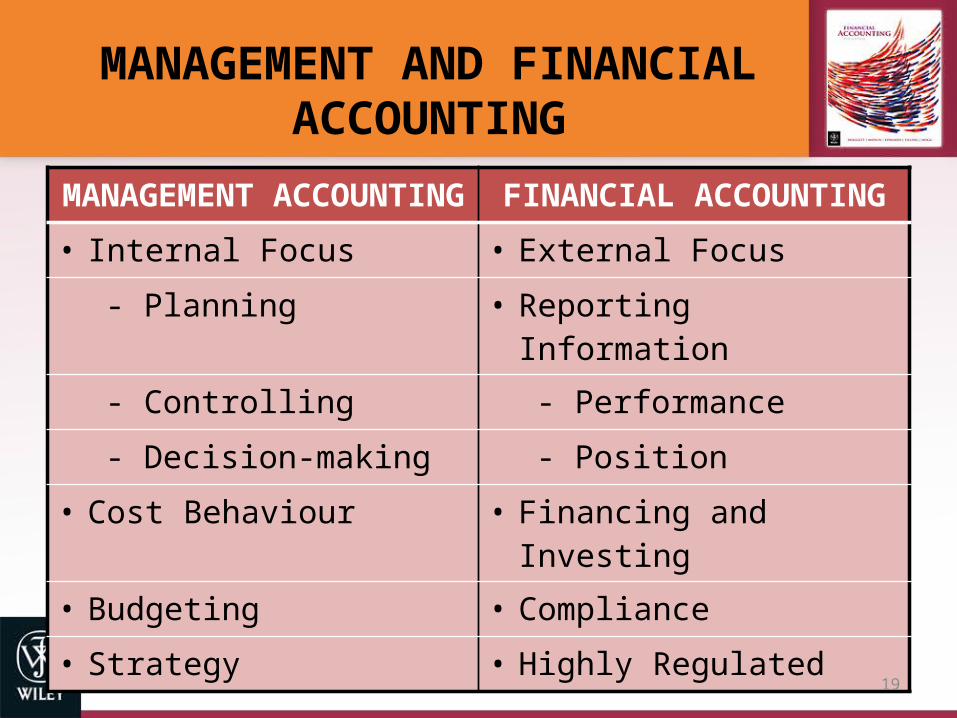

MANAGEMENT AND FINANCIAL ACCOUNTING

MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

• Internal Focus • External Focus

- Planning • Reporting Information

- Controlling - Performance

- Decision-making - Position

• Cost Behaviour • Financing and Investing

• Budgeting • Compliance

• Strategy • Highly Regulated

20

ACCOUNTING AS A PROFESSION AUSTRALIAN PERSPECTIVE

• Self-regulated profession– Similar to law and medicine

• Two major professional associations– CPA Australia (CPA)– Institute of Chartered Accountants Australia

(ICAA)• Membership requires– Tertiary qualification– Ongoing professional development

21

PUBLIC ACCOUNTING

• Accountants who offer their professional services to the public for a fee

• Four main areas with many specialties– Auditing and assurance services– Taxation services– Advisory services– Insolvency and administration

22

ACCOUNTING IN COMMERCE AND INDUSTRY

• Accountants who are employed in business entities

• Many areas of interest– General accounting– Cost accounting– Accounting information systems– Budgeting– Taxation accounting– Internal auditing and audit committees

23

NOT-FOR-PROFIT ACCOUNTING

• Many accountants work in the not-for-profit area

• This requires a slightly different approach as profit is not the primary focus

• Includes a range of organisations– Government– NGO– Charities

24

TYPES OF BUSINESS ENTITIES

• Single proprietorship or sole trader– Owned by one person

• Partnership– Owned by two or more partners

• Company or corporation– Owned by shareholders– Separate legal entity– Limited liability

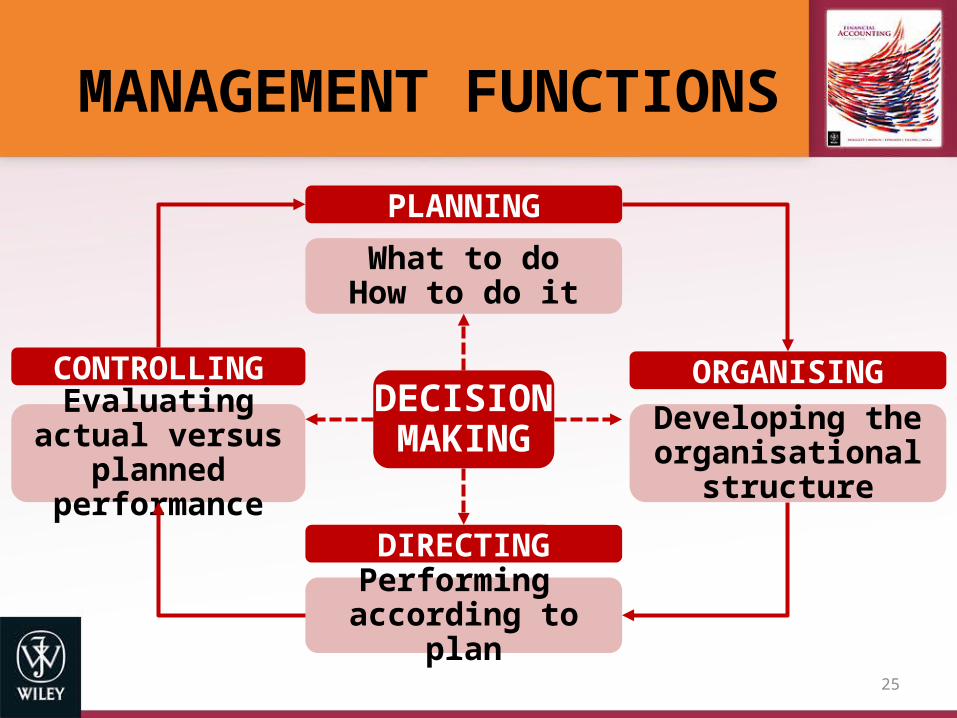

MANAGEMENT FUNCTIONS

Performing according to plan

Evaluating actual versus planned performance

Developing the organisational

structure

What to doHow to do it

DIRECTING

CONTROLLING ORGANISING

PLANNING

DECISIONMAKING

25

26

ETHCS AND ACCOUNTANTS

• Ethics in business– Important in all business dealings

• Ethics and professional accounting bodies– Important for the standing of the profession

• Ethics in practice– Identify the ethical issue– Analyse key issues and stakeholders– Select appropriate course of action