Embed Size (px)

Citation preview

Abraxas Youth & Family ServicesA Division of Cornell Companies, Inc.

2008 Avondale Behavioral Healthcare Conference

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 1 -

Forward-looking Statements and Non-GAAP Measures

Statements made during this presentation regarding the company, its expected future earnings, operations, strategic direction, and any other statements that are not historical facts are forward-looking statements within the meaning of applicable securities laws. These statements involve certain risks, uncertainties and assumptions including changes in demand for our services, actions by governmental agencies and other third parties and other factors detailed in our most recent Form 10-K and other filings with the Securities and Exchange Commission, which are available free of charge on the SEC's website at http://www.sec.gov. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those indicated. Each forward looking-statement speaks only as of the date of the particular statement, and we undertake no obligation to update or revise any forward looking-statement, whether as a result of new information, future events or otherwise. A reconciliation of all non-GAAP financial measures used in this presentation, including EBITDA, is attached to this presentation.

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 2 -

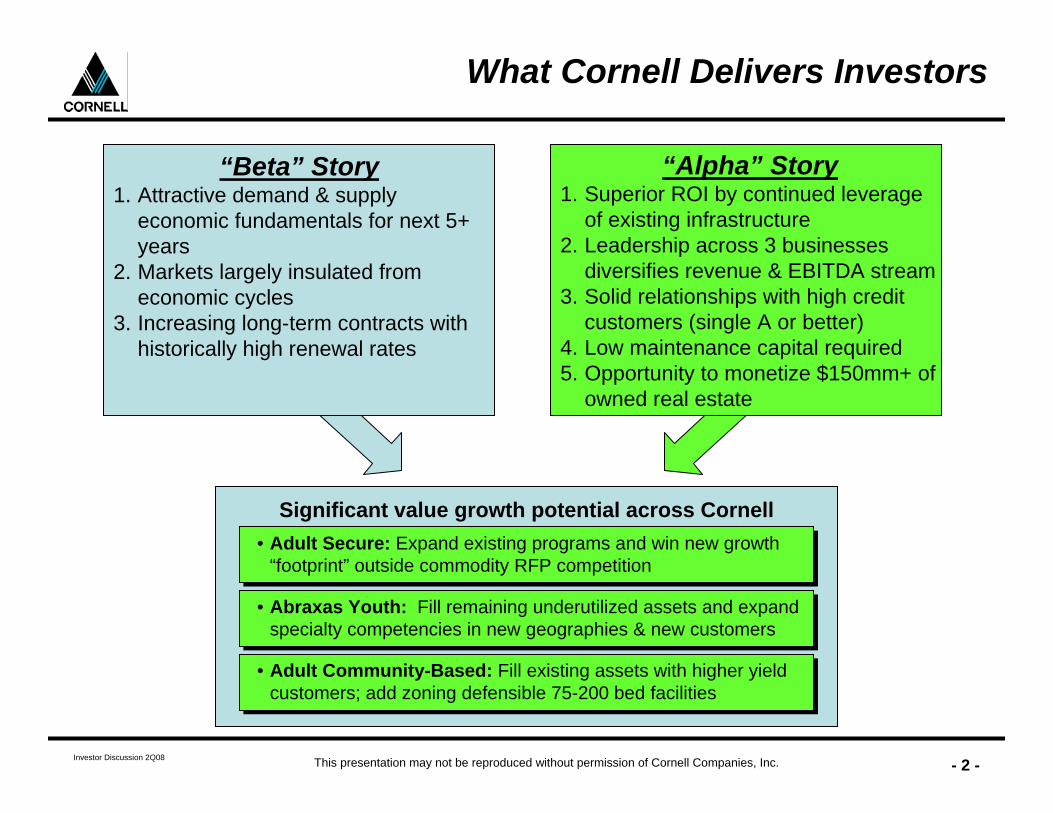

“Alpha” Story1. Superior ROI by continued leverage

of existing infrastructure2. Leadership across 3 businesses

diversifies revenue & EBITDA stream3. Solid relationships with high credit

customers (single A or better)4. Low maintenance capital required5. Opportunity to monetize $150mm+ of

owned real estate

What Cornell Delivers Investors

“Beta” Story1. Attractive demand & supply

economic fundamentals for next 5+ years

2. Markets largely insulated from economic cycles

3. Increasing long-term contracts with historically high renewal rates

Significant value growth potential across Cornell• Adult Secure: Expand existing programs and win new growth

“footprint” outside commodity RFP competition

• Abraxas Youth: Fill remaining underutilized assets and expand specialty competencies in new geographies & new customers

• Adult Community-Based: Fill existing assets with higher yield customers; add zoning defensible 75-200 bed facilities

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 3 -

• Abraxas History

• Abraxas Today

• Abraxas’ Future Growth

• Supporting Data

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 4 -

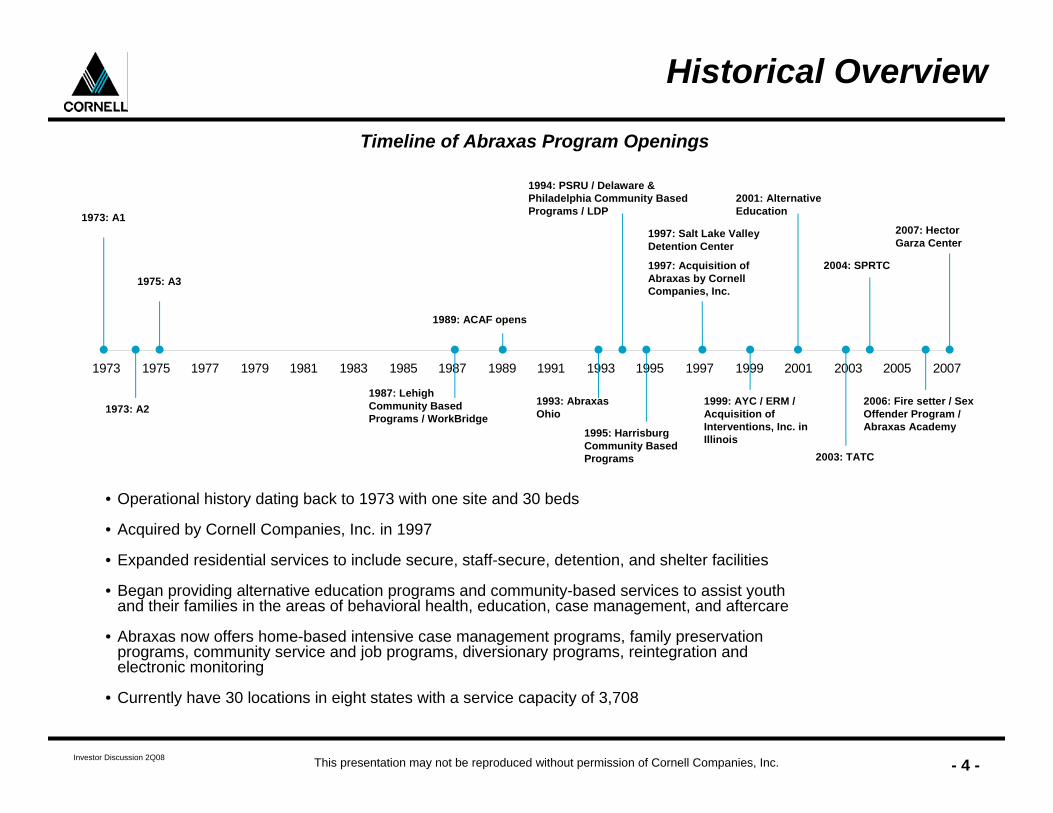

Historical Overview

1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

1973: A1

1973: A2

1975: A3

1999: AYC / ERM / Acquisition of Interventions, Inc. in Illinois

1997: Salt Lake Valley Detention Center

1997: Acquisition of Abraxas by Cornell Companies, Inc.

1995: Harrisburg Community Based Programs

1994: PSRU / Delaware & Philadelphia Community Based Programs / LDP

1993: Abraxas Ohio

1989: ACAF opens

1987: Lehigh Community Based Programs / WorkBridge

2007: Hector Garza Center

2006: Fire setter / Sex Offender Program / Abraxas Academy

2004: SPRTC

2003: TATC

2001: Alternative Education

Timeline of Abraxas Program Openings

• Operational history dating back to 1973 with one site and 30 beds

• Acquired by Cornell Companies, Inc. in 1997

• Expanded residential services to include secure, staff-secure, detention, and shelter facilities

• Began providing alternative education programs and community-based services to assist youth and their families in the areas of behavioral health, education, case management, and aftercare

• Abraxas now offers home-based intensive case management programs, family preservation programs, community service and job programs, diversionary programs, reintegration and electronic monitoring

• Currently have 30 locations in eight states with a service capacity of 3,708

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 5 -

Reduced Portfolio & Operating Risk

• Exited programs where risk-adjusted returns deemed not likely to be achieved

• Restructured or replaced underperforming contracts

• Implemented automated Cornell Incident Reporting System– Improved immediacy of communication– Permit early identification of trends to proactively manage and

reduce potential exposure • Improved leadership development and review processes to

increase performance and accountability• Instituted financial and leadership training for organizational leaders• Created Abraxas Performance Improvement Department

Reduced Portfolio Risk:

Reduced Operating Risk:

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 6 -

• Abraxas History

• Abraxas Today

• Abraxas’ Future Growth

• Supporting Data

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 7 -

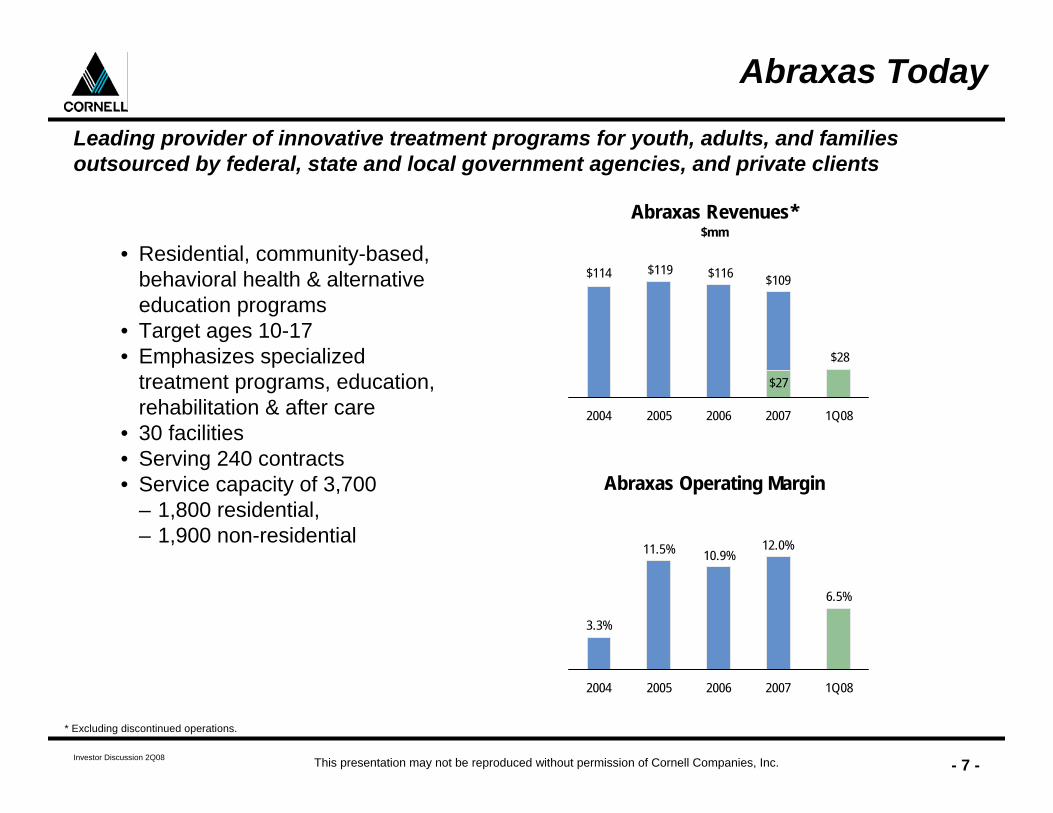

• Residential, community-based, behavioral health & alternative education programs

• Target ages 10-17• Emphasizes specialized

treatment programs, education, rehabilitation & after care

• 30 facilities• Serving 240 contracts• Service capacity of 3,700

– 1,800 residential, – 1,900 non-residential

Abraxas Today

* Excluding discontinued operations.

Leading provider of innovative treatment programs for youth, adults, and familiesoutsourced by federal, state and local government agencies, and private clients

Abraxas Revenues*$mm

$28

$27

$116$119$114 $109

2004 2005 2006 2007 1Q08

Abraxas Operating Margin

6.5%

12.0%10.9%11.5%

3.3%

2004 2005 2006 2007 1Q08

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 8 -

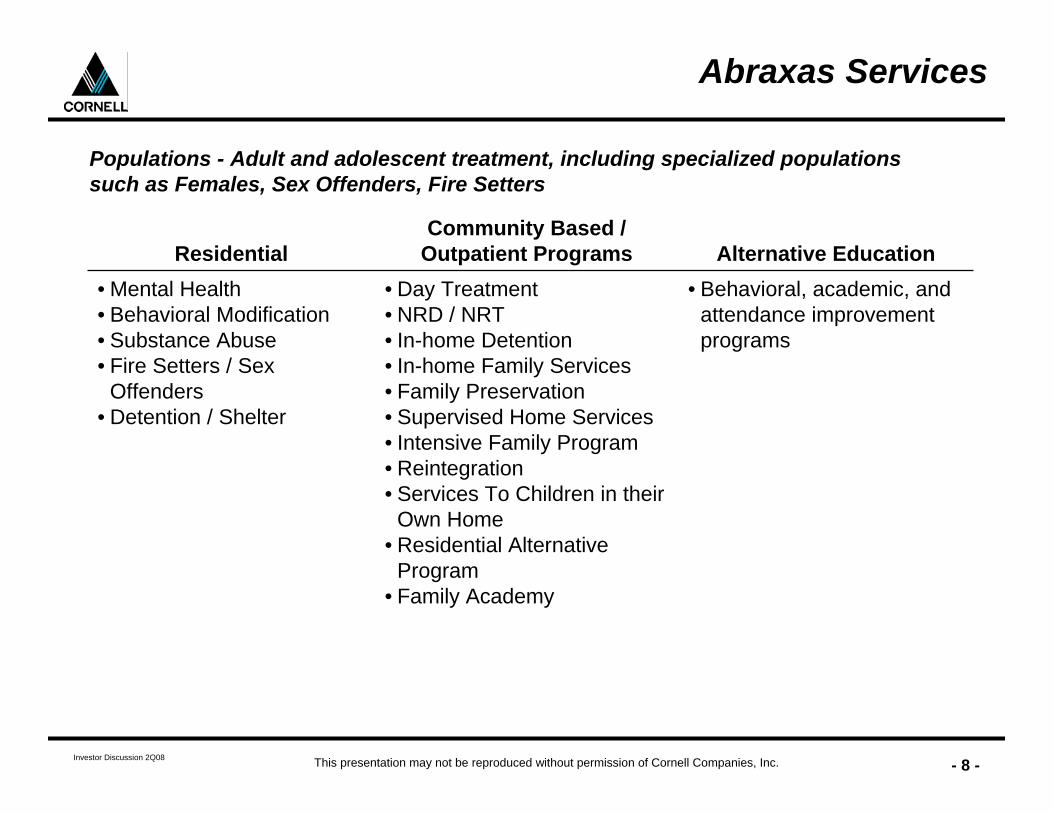

Abraxas Services

• Behavioral, academic, and attendance improvement programs

• Day Treatment• NRD / NRT• In-home Detention• In-home Family Services• Family Preservation• Supervised Home Services• Intensive Family Program• Reintegration• Services To Children in their

Own Home• Residential Alternative

Program• Family Academy

• Mental Health• Behavioral Modification• Substance Abuse• Fire Setters / Sex

Offenders• Detention / Shelter

Alternative EducationCommunity Based /

Outpatient ProgramsResidential

Populations - Adult and adolescent treatment, including specialized populations such as Females, Sex Offenders, Fire Setters

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 9 -

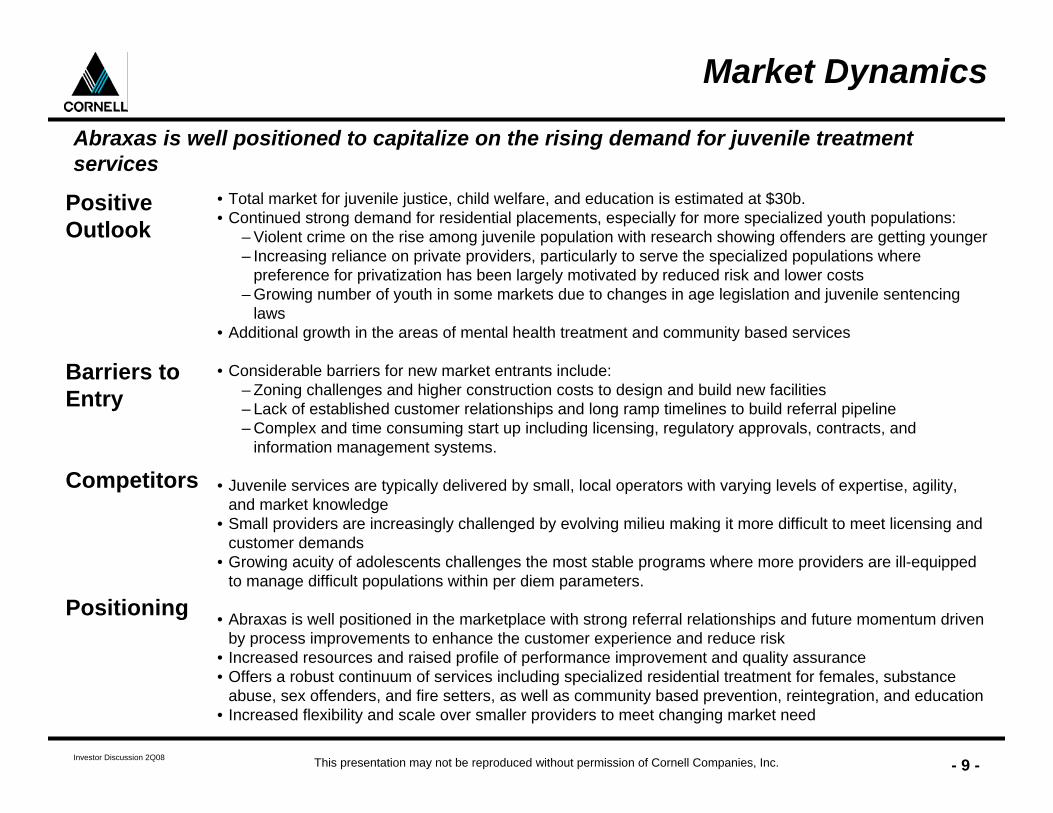

Market Dynamics

• Total market for juvenile justice, child welfare, and education is estimated at $30b. • Continued strong demand for residential placements, especially for more specialized youth populations:

– Violent crime on the rise among juvenile population with research showing offenders are getting younger– Increasing reliance on private providers, particularly to serve the specialized populations where

preference for privatization has been largely motivated by reduced risk and lower costs– Growing number of youth in some markets due to changes in age legislation and juvenile sentencing

laws• Additional growth in the areas of mental health treatment and community based services

• Considerable barriers for new market entrants include:– Zoning challenges and higher construction costs to design and build new facilities – Lack of established customer relationships and long ramp timelines to build referral pipeline– Complex and time consuming start up including licensing, regulatory approvals, contracts, and

information management systems.

• Juvenile services are typically delivered by small, local operators with varying levels of expertise, agility, and market knowledge

• Small providers are increasingly challenged by evolving milieu making it more difficult to meet licensing and customer demands

• Growing acuity of adolescents challenges the most stable programs where more providers are ill-equipped to manage difficult populations within per diem parameters.

• Abraxas is well positioned in the marketplace with strong referral relationships and future momentum driven by process improvements to enhance the customer experience and reduce risk

• Increased resources and raised profile of performance improvement and quality assurance• Offers a robust continuum of services including specialized residential treatment for females, substance

abuse, sex offenders, and fire setters, as well as community based prevention, reintegration, and education• Increased flexibility and scale over smaller providers to meet changing market need

Positive Outlook

Barriers to Entry

Competitors

Positioning

Abraxas is well positioned to capitalize on the rising demand for juvenile treatment services

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 10 -

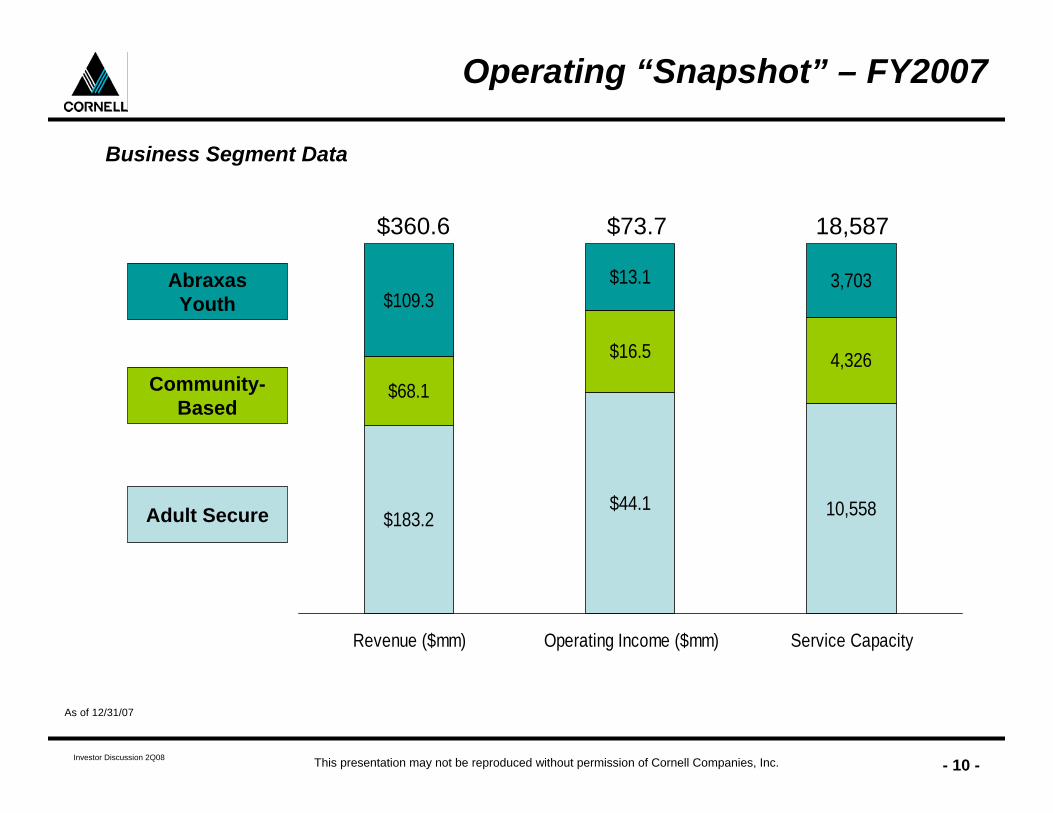

Operating “Snapshot” – FY2007

As of 12/31/07

$183.2$44.1

$16.5

$109.3$13.1

10,558

4,326$68.1

3,703

Revenue ($mm) Operating Income ($mm) Service Capacity

$360.6 $73.7 18,587

Adult Secure

Community-Based

Abraxas Youth

Business Segment Data

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 11 -

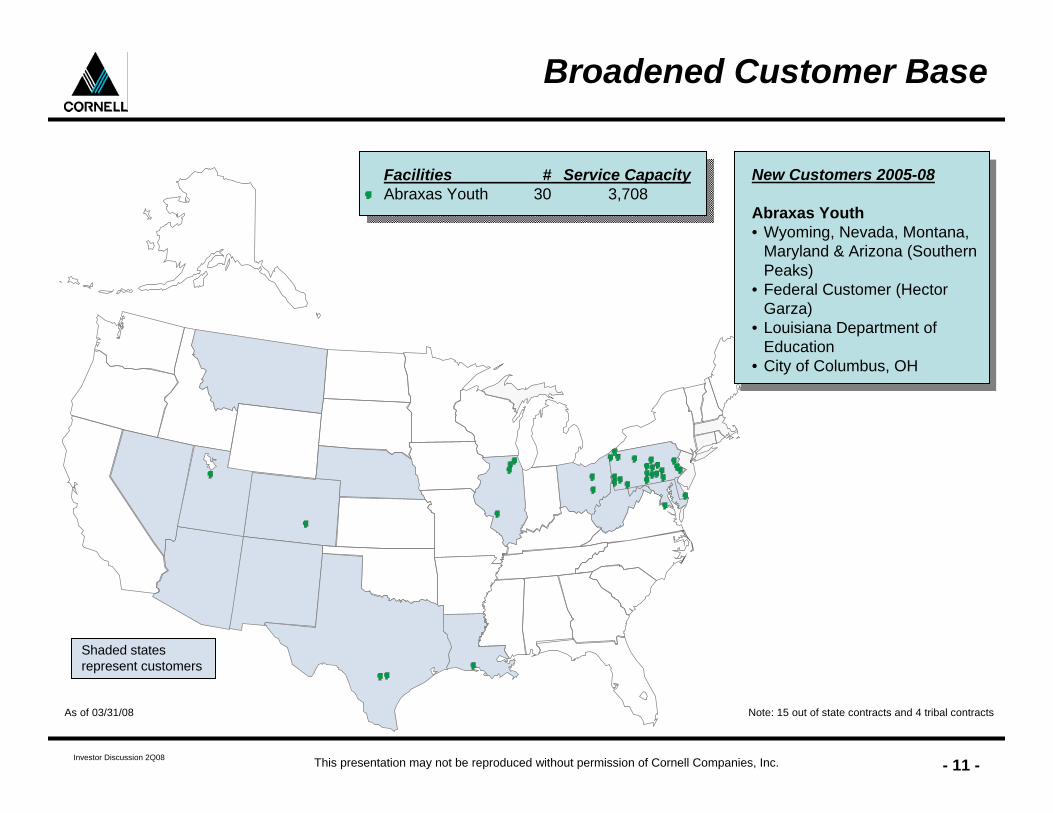

Broadened Customer Base

New Customers 2005-08

Abraxas Youth• Wyoming, Nevada, Montana,

Maryland & Arizona (Southern Peaks)

• Federal Customer (Hector Garza)

• Louisiana Department of Education

• City of Columbus, OH

Facilities # Service CapacityAbraxas Youth 30 3,708

Shaded states represent customers

As of 03/31/08 Note: 15 out of state contracts and 4 tribal contracts

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 12 -

Abraxas Example: “Leadership Development Program”

• Staff-secure 128 bed residential program• Adjudicated delinquent and dependent 13-18 year old males and females• Primarily first and second time offenders• 8:1 client to direct care staff ratio• Year-round, licensed, private onsite school• Multi-disciplinary, professional treatment staff• Medical, psychological, psychiatric and dental services• Addressing market opportunities has resulted in a shift in program mix and increased

per diems

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 13 -

• Abraxas History

• Abraxas Today

• Abraxas’ Future Growth

• Supporting Data

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 14 -

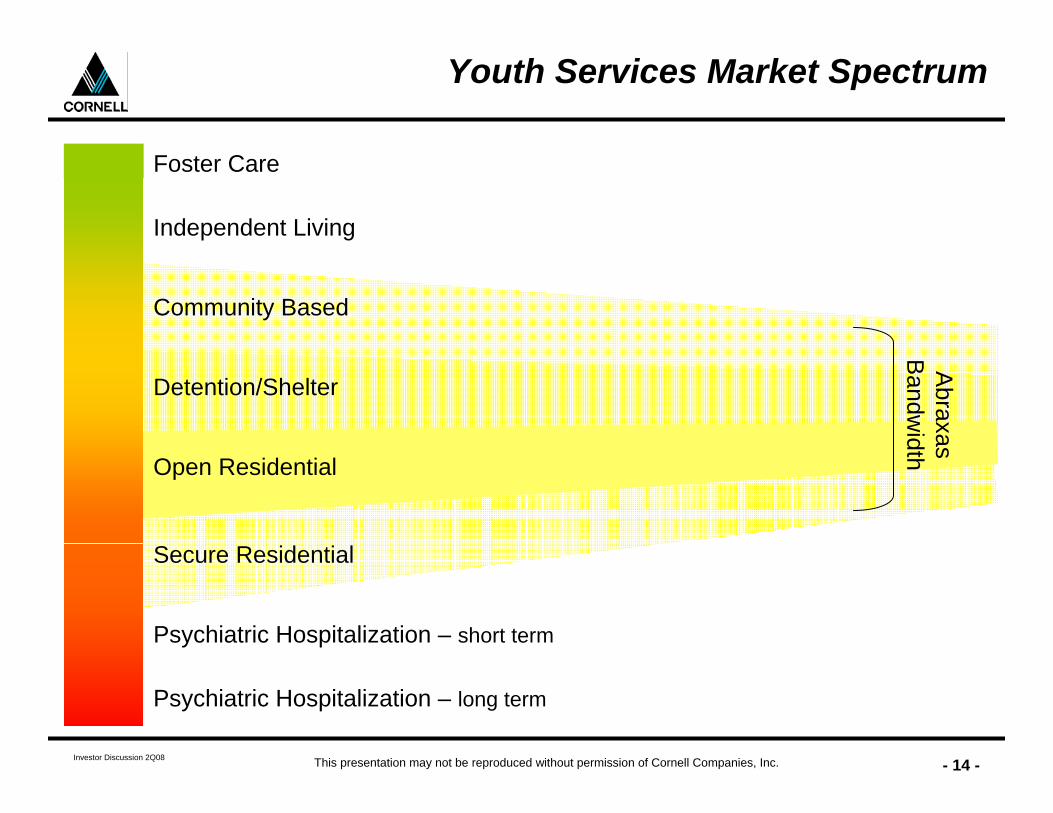

Youth Services Market Spectrum

Detention/Shelter

Open Residential

Community Based

Independent Living

Foster Care

Secure Residential

Psychiatric Hospitalization – short term

Abraxas

Bandw

idth

Psychiatric Hospitalization – long term

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 15 -

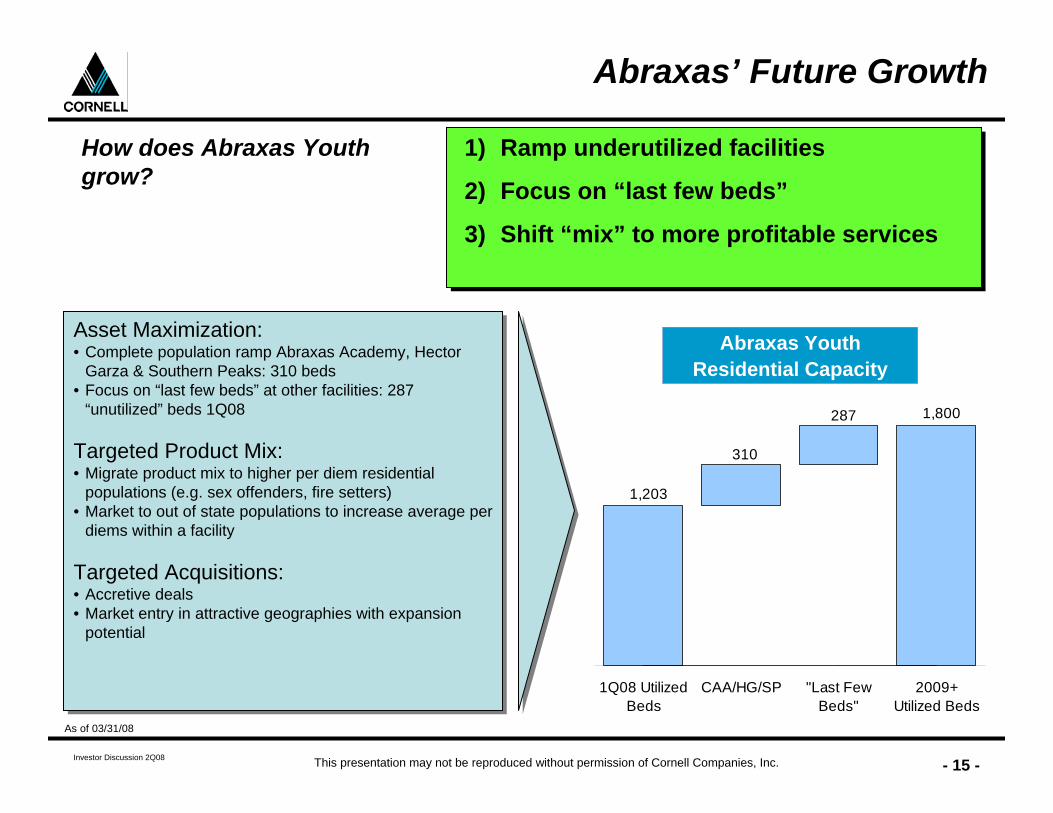

Abraxas’ Future Growth

Asset Maximization:• Complete population ramp Abraxas Academy, Hector

Garza & Southern Peaks: 310 beds• Focus on “last few beds” at other facilities: 287

“unutilized” beds 1Q08

Targeted Product Mix:• Migrate product mix to higher per diem residential

populations (e.g. sex offenders, fire setters) • Market to out of state populations to increase average per

diems within a facility

Targeted Acquisitions:• Accretive deals• Market entry in attractive geographies with expansion

potential

How does Abraxas Youth grow?

Abraxas YouthResidential Capacity

1) Ramp underutilized facilities

2) Focus on “last few beds”

3) Shift “mix” to more profitable services

1,203

310

287 1,800

1Q08 UtilizedBeds

CAA/HG/SP "Last FewBeds"

2009+Utilized Beds

As of 03/31/08

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 16 -

• Cornell History

• Cornell Today

• Cornell’s Future Growth

• Supporting Data

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 17 -

P&L Overview

($mm) 2003 2004 2005 2006 2007 1Q08

Revenue $258.2 $277.2 $310.8 $360.9 $360.6 $95.4Adult Secure 102.1 114.8 128.5 178.8 183.2 49.9Adult Community Based 49.5 48.6 63.3 66.3 68.1 17.7Abraxas Youth 106.5 113.8 119.0 115.8 109.3 27.8

Operating Income 24.5 14.5 27.9 44.8 45.0 14.5Adult Secure 25.6 24.9 26.2 44.8 44.1 15.1Adult Community Based 10.6 9.2 11.9 12.4 16.5 4.8Abraxas Youth 14.2 3.8 13.7 12.6 13.1 1.8

Operating Margin 9.5% 5.2% 9.0% 12.4% 12.5% 15.2%Adult Secure 25.1% 21.7% 20.4% 25.1% 24.1% 30.3%Adult Community Based 21.4% 18.9% 18.8% 18.7% 24.2% 27.1%Abraxas Youth 13.3% 3.3% 11.5% 10.9% 12.0% 6.5%

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 18 -

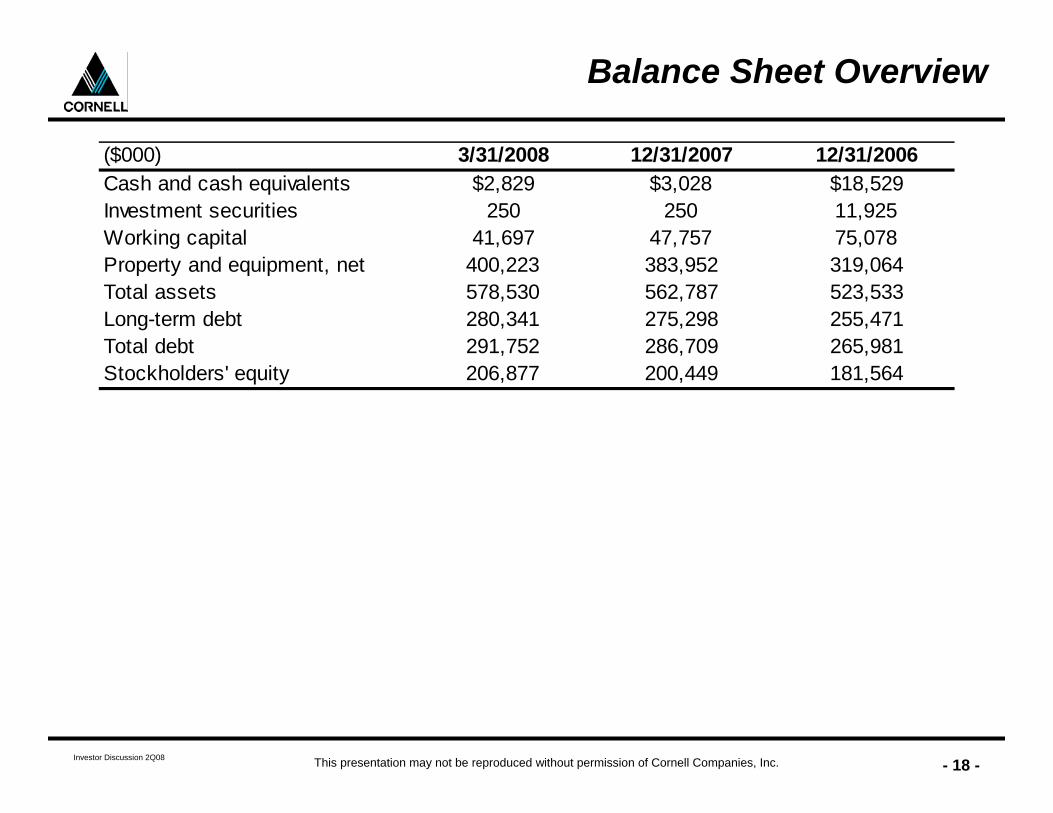

Balance Sheet Overview

($000) 3/31/2008 12/31/2007 12/31/2006Cash and cash equivalents $2,829 $3,028 $18,529Investment securities 250 250 11,925Working capital 41,697 47,757 75,078Property and equipment, net 400,223 383,952 319,064Total assets 578,530 562,787 523,533Long-term debt 280,341 275,298 255,471Total debt 291,752 286,709 265,981Stockholders' equity 206,877 200,449 181,564

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 19 -

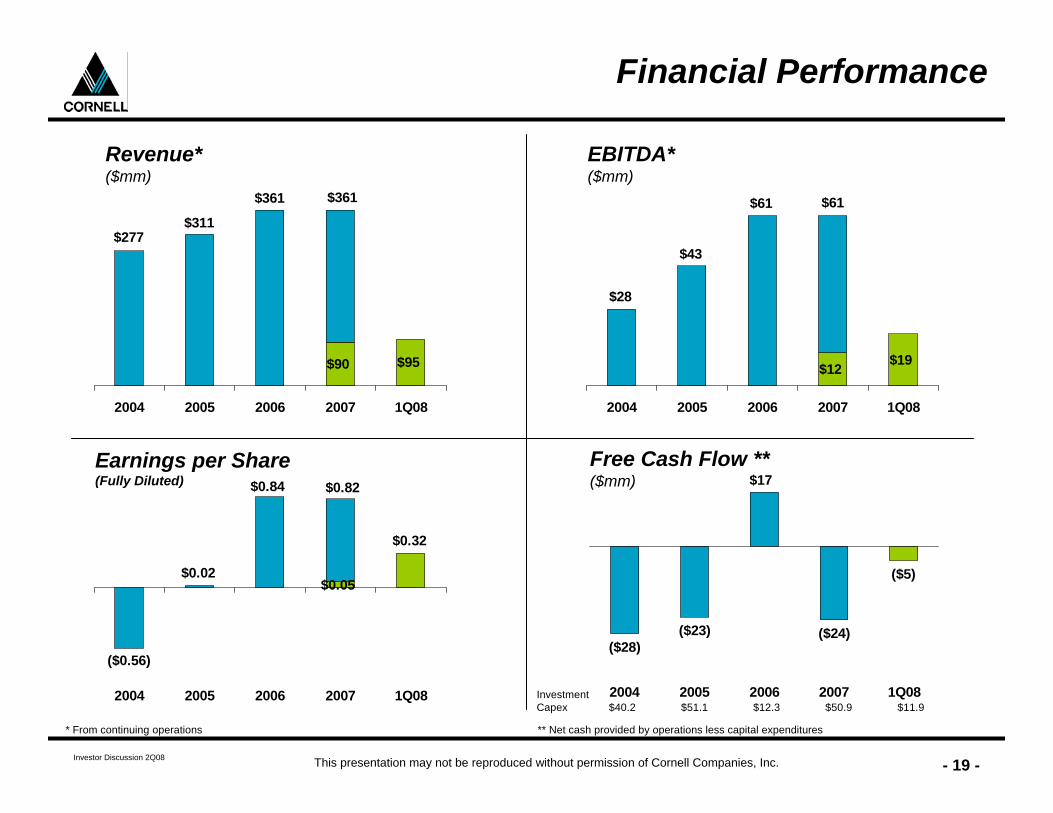

Financial Performance

$90 $95

$361 $361

$277$311

2004 2005 2006 2007 1Q08

Revenue* ($mm)

$12 $19

$61 $61

$43

$28

2004 2005 2006 2007 1Q08

EBITDA* ($mm)

$0.05

$0.32

($0.56)

$0.02

$0.84 $0.82

2004 2005 2006 2007 1Q08

Earnings per Share(Fully Diluted)

($28)($23) ($24)

($5)

$17

2004 2005 2006 2007 1Q08

Free Cash Flow **($mm)

* From continuing operations ** Net cash provided by operations less capital expenditures

Investment Capex $40.2 $51.1 $12.3 $50.9 $11.9

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 20 -

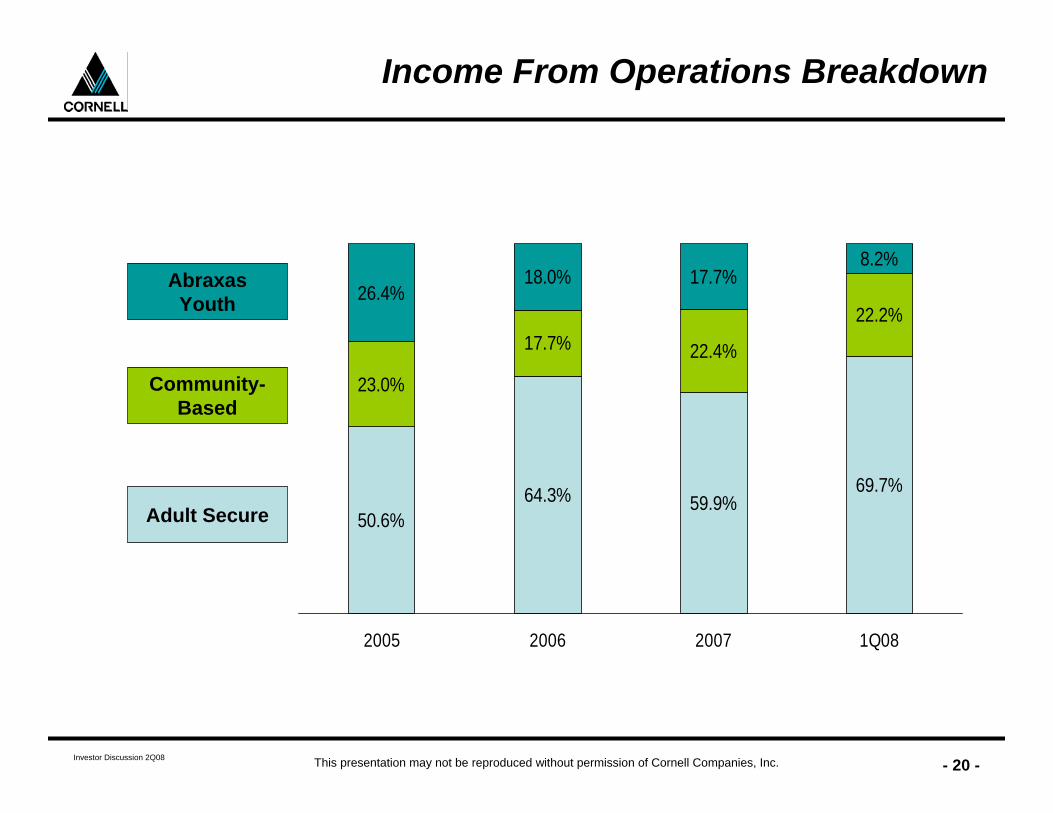

Income From Operations Breakdown

50.6%64.3% 69.7%

17.7%22.2%

26.4%18.0%

8.2%

59.9%

22.4%

23.0%

17.7%

2005 2006 2007 1Q08

Adult Secure

Community-Based

Abraxas Youth

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 21 -

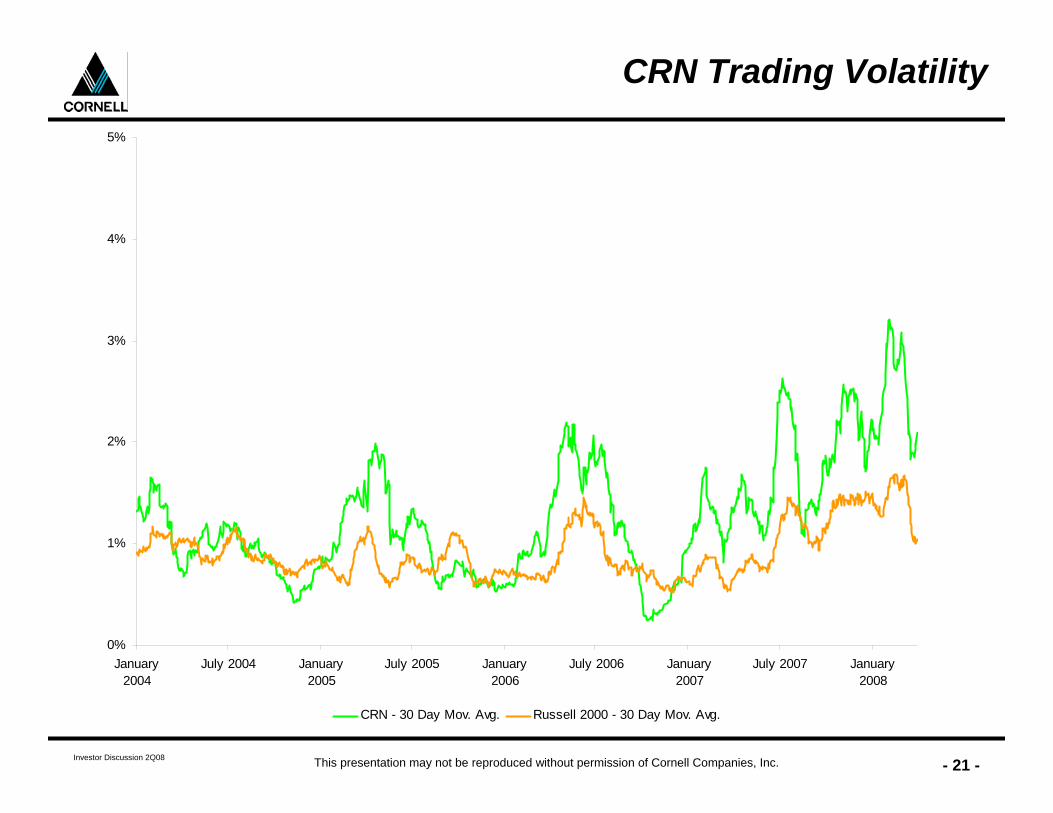

CRN Trading Volatility

0%

1%

2%

3%

4%

5%

January2004

July 2004 January2005

July 2005 January2006

July 2006 January2007

July 2007 January2008

CRN - 30 Day Mov. Avg. Russell 2000 - 30 Day Mov. Avg.

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 22 -

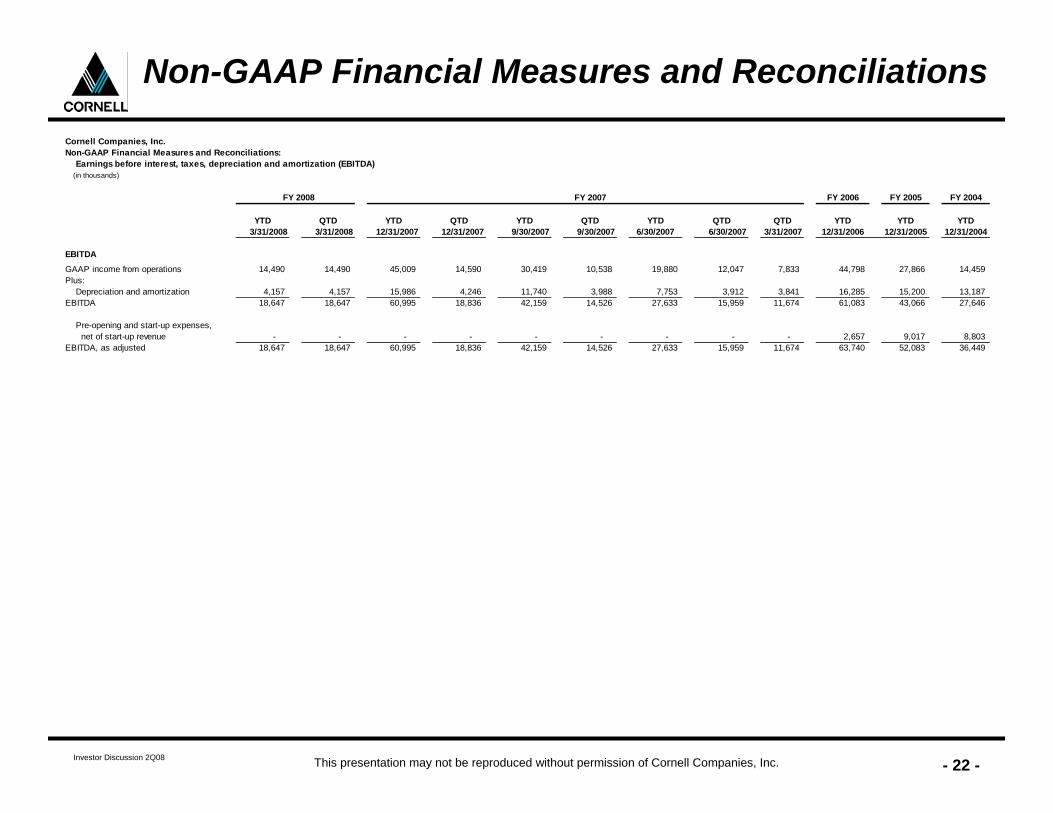

Non-GAAP Financial Measures and Reconciliations

Cornell Companies, Inc.Non-GAAP Financial Measures and Reconciliations: Earnings before interest, taxes, depreciation and amortization (EBITDA) (in thousands)

FY 2008 FY 2007 FY 2006 FY 2005 FY 2004

YTD QTD YTD QTD YTD QTD YTD QTD QTD YTD YTD YTD3/31/2008 3/31/2008 12/31/2007 12/31/2007 9/30/2007 9/30/2007 6/30/2007 6/30/2007 3/31/2007 12/31/2006 12/31/2005 12/31/2004

EBITDA

GAAP income from operations 14,490 14,490 45,009 14,590 30,419 10,538 19,880 12,047 7,833 44,798 27,866 14,459Plus: Depreciation and amortization 4,157 4,157 15,986 4,246 11,740 3,988 7,753 3,912 3,841 16,285 15,200 13,187EBITDA 18,647 18,647 60,995 18,836 42,159 14,526 27,633 15,959 11,674 61,083 43,066 27,646

Pre-opening and start-up expenses, net of start-up revenue - - - - - - - - - 2,657 9,017 8,803EBITDA, as adjusted 18,647 18,647 60,995 18,836 42,159 14,526 27,633 15,959 11,674 63,740 52,083 36,449

Investor Discussion 2Q08 This presentation may not be reproduced without permission of Cornell Companies, Inc. - 23 -

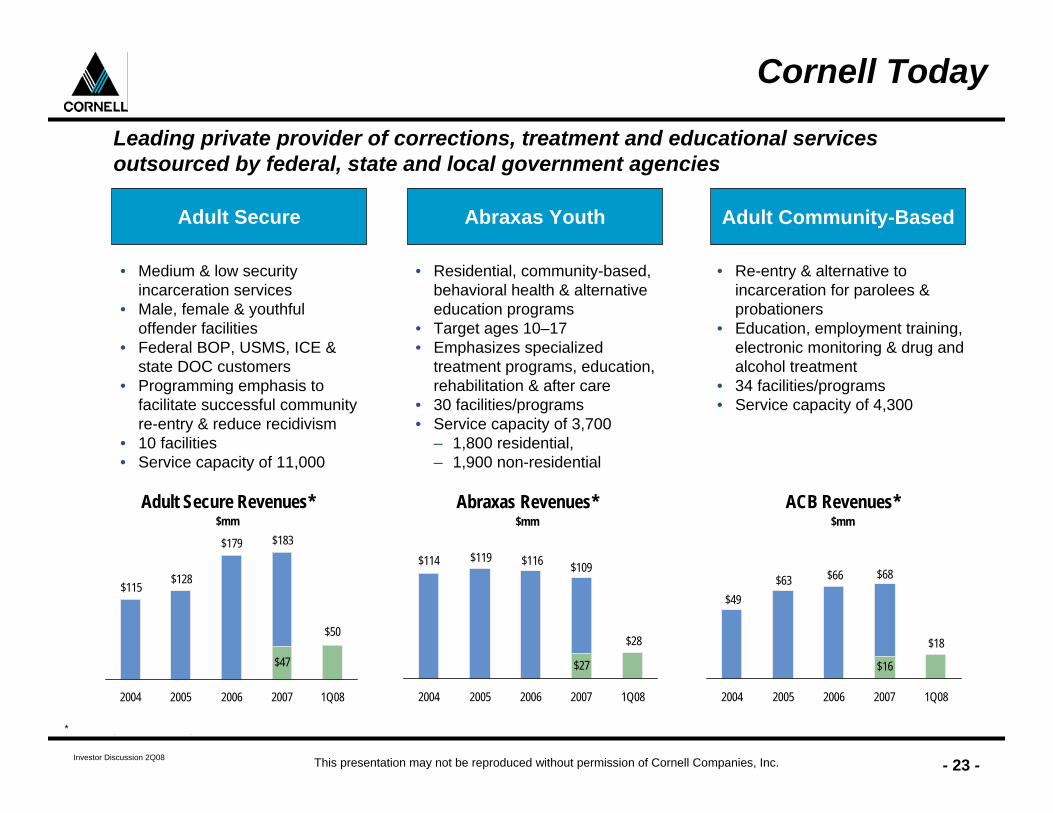

Adult Secure

• Re-entry & alternative to incarceration for parolees & probationers

• Education, employment training, electronic monitoring & drug and alcohol treatment

• 34 facilities/programs• Service capacity of 4,300

• Residential, community-based, behavioral health & alternative education programs

• Target ages 10–17• Emphasizes specialized

treatment programs, education, rehabilitation & after care

• 30 facilities/programs• Service capacity of 3,700

– 1,800 residential, – 1,900 non-residential

Cornell Today

Abraxas Youth Adult Community-Based

• Medium & low security incarceration services

• Male, female & youthful offender facilities

• Federal BOP, USMS, ICE & state DOC customers

• Programming emphasis to facilitate successful community re-entry & reduce recidivism

• 10 facilities• Service capacity of 11,000

* Excluding discontinued operations.

Leading private provider of corrections, treatment and educational services outsourced by federal, state and local government agencies

Adult Secure Revenues*$mm

$50

$179

$47

$128$115

$183

2004 2005 2006 2007 1Q08

Abraxas Revenues*$mm

$28

$27

$116$119$114 $109

2004 2005 2006 2007 1Q08

ACB Revenues*$mm

$18

$66

$16

$63$49

$68

2004 2005 2006 2007 1Q08