Embed Size (px)

Citation preview

International Arbitrage Pricing Theory: An Empirical InvestigationAuthor(s): Sarath P. Abeysekera and Arvind MahajanSource: Southern Economic Journal, Vol. 56, No. 3 (Jan., 1990), pp. 760-773Published by: Southern Economic AssociationStable URL: http://www.jstor.org/stable/1059376 .

Accessed: 21/03/2013 05:47

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Southern Economic Association is collaborating with JSTOR to digitize, preserve and extend access toSouthern Economic Journal.

http://www.jstor.org

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

International Arbitrage Pricing Theory: An Empirical Investigation* SARATH P. ABEYSEKERA University of Manitoba Winnipeg, Manitoba, Canada

ARVIND MAHAJAN Texas A & M University College Station, Texas

I. Introduction

The Arbitrage Pricing Theory (APT) of Ross [23; 24], later refined and extended by Connor [8], Huberman [15], Huberman et al. [16], Dybvig [11], Stambaugh [29], Chamberlin and Rothchild [4], Grinblatt and Titman [14], Ingersoll [17], Chen, Roll, and Ross [5] among others, has attracted considerable attention as a testable alternative to the Sharpe [26]-Lintner [20]-Mossin [21] Capital Asset Pricing Model (CAPM).' The APT resembles the CAPM in the sense that both are linear models where the CAPM is a single factor (market) model while the APT assumes that m unobservable factors drive the security prices through time. The pricing equation of the APT is developed by imposing the "no arbitrage condition," resulting in a linear relationship between expected return and systematic risk.

Similar to the extensions of the single currency CAPM to a multicurrency environment, Solnik [27] extended the APT to the international capital markets, leading to the International Arbitrage Pricing Theory (IAPT).2 Since the IAPT provides a theoretical framework to investigate the existence of factors that generate returns, and to check whether these factors are "priced" in the international capital markets, it is possible to empirically test the validity of the IAPT jointly with the hypothesis that the international capital markets are integrated. The purpose of this study is to develop and empirically test these hypotheses and it is organized as follows. Section II provides a brief discussion of the IAPT. Section III describes the testable hypotheses implied by the IAPT and the data and the methodology utilized in this study to test these hypotheses. Empirical results obtained are reported in section IV and section V concludes the paper.

*The authors gratefully acknowledge the extremely helpful comments of an anonymous referee and the financial assistance from the Centre for International Business Studies in the Faculty of Management of the University of Manitoba.

1. In light of Shanken [25] and Dybvig and Ross [12], from an empirical standpoint, the APT pricing relationship should be viewed as an approximation rather than an identity.

2. For example, see Solnik [28], Grauer, Litzenberger, and Stehle [13] for problems encountered in empirically testing the CAPM and for ICAPM, see Solnik [28] and Adler and Dumas [3].

760

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

IAPT: AN EMPIRICAL INVESTIGATION 761

II. International Arbitrage Pricing Theory (IAPT)

As shown by Solnik and Ross, the APT, and hence the IAPT, overcomes the problem of ag- gregation when asset demands are summed over the universe of investors who use different numeraires to measure returns. This is because the portfolios in international CAPM context represent weighted averages of individual assets whereas the factors in the APT are theoretical constructs which are not constrained to be portfolios of original assets.

Besides the usual assumptions of the APT, Solnik's derivation of the IAPT further assumes perfect and integrated international capital markets, homogeneous expectations in a given country and that the returns are computed over a very short time interval.3 Given these assumptions it is shown that the returns of an asset i measured in a foreign currency j, Fr, is given by

where

rH = return on asset i measured in foreign currency j ri = return on asset i measured in its domestic currency

sj = (St - S,- 1 )/S, - 1 = random variation in S, the exchange rate of currency j expressed in units of the domestic currency

risj = Cij = covariance between ri and sj, and

0-2 = variance of si.

It is further assumed that the return generating process is an m-factor model and hence, for a domestic security i .4

ri = Fi + b i lf

+ + - "

+ bimfm + -i

(2)

where Fi is the mean return of security i. Combining equations (1) and (2) Solnik shows that even in foreign terms the domestic arbitrage portfolio entails no risk and hence should earn zero returns in equilibrium. Thus, the APT pricing relationship holds in a multicurrency environment as well. In specific, for a given security i,

ri = Ao + Albii + " + Aimbm. (3)

If a risk-free bill of foreign country j exists (and it is one of the many assets in j's economy) then its domestic currency return

Ry should follow the relationship (2) whose stochastic component

will be sj [27, 452, n.9]. Therefore,

s =

E(sj) +

bjlf

+ -.- - + bjmfm + i;. (4)

Substituting equation (4) in equation (1) it is shown that

ir = rj +

bllfi

+ --'

- + bmfm

+ vj (5)

3. For a concise development of the APT, see Roll and Ross [22]. 4. For simplicity, the time subscripts in the expression have been omitted.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

762 Sarath P. Abeysekera and Arvind Mahajan

where

bk = (bik - bjk) [k 1, 2,...,m], and vj = (ii- Uj).

This implies that the m -factor return generating process is invariant to the currency in which the returns are denominated and together with the original set of assumptions, gives the following pricing relation for a given security:

J = A + A bI + + AJ bj (6)

where Ao is the currency j risk free rate. Or in matrix notation,

EJ = LJB* (7)

where E/ is the N-element row vector of mean returns, N is the number of securities in the portfolio, B*j is the augmented loadings matrix and Lj is a row vector of (m + 1) elements.

A major consequence of the two pricing relationships (3) and (6) is that the risk premia (i.e., A's) represent the price implication of (or their contribution to) the covariance structure between asset returns and the currency j [27, 453]. That is:

Cij = (A1 - AJ )biI + ...

+ (Am - A )bim (8)

where Cij is the covariance between the return from asset i and the percent change in exchange rate of currency j measured in units of the domestic currency.

Cho, Eun, and Senbet [7] also tested the IAPT empirically and rejected the joint hypotheses that the international capital market is integrated and that the APT is valid internationally. How- ever, while Cho, Eun, and Senbet used international common factors for test purposes, this study utilizes domestic common factors and hence provides a direct test of Solnik's claims on the IAPT. The following sections discuss the empirical procedures applied to test the IAPT and the results obtained.

III. Empirical Tests

Hypotheses

This study empirically evaluates the validity of the IAPT (along with the joint hypothesis of international capital market integration) by testing the following four hypotheses Hi through H4:

H 1. The equality of the intercept terms and the corresponding risk free rates.

Ho : Ao = Rj

Ha: Ao Rj.

H2. The invariance of the number of factors to the currency chosen to express the returns.

Ho : m = mj

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

IAPT: AN EMPIRICAL INVESTIGATION 763

Ha : m # mj .

where m is the number of factors before converting the returns from one numeraire currency to another and mj is the number offactors after the conversion to currency j.

H3. The statistical significance of the estimated risk premia.

Ho: Ak = 0, k = 1,...,m

Ha : Ak # 0, k = 1,...,m,

H4. The equality of the currency-asset covariances estimated through the model (Cij) and those computed using observed data (Cij).

Ho0: Cij Cij Ha : Ci #

Cij.

Data

The basic data units used in the study are (a) the monthly returns on individual stocks (adjusted for dividends and stock splits) in three industrialized countries, viz., Canada, the U.K. and the U.S.; (b) the spot exchange rates; and (c) the Treasury bill rates in the three countries. The period of this study encompasses 168 months from January 1973 to December 1986-the whole span in which data were available during the flexible exchange rate regime. The security selection criterion in forming portfolios is based on random selection of securities listed continuously for the entire test period on each of the three countries' major stock exchanges, i.e., Toronto, London and NYSE and AMEX. The risk-free rate is proxied by the 90-day Treasury bill rate of each country. All data utilized in this study are based on month-end observations. The Canadian stock market data were obtained from the Stock Data Master File for the Toronto Stock Exchange, compiled by the Laval University, Quebec. The U.K. stock market data were provided by the London School of Business and the U.S. stock market data source was the Center for Research in Stock Prices, University of Chicago. Data on foreign exchange rates and Treasury bill rates were obtained from the U.S. Federal Reserve System, the Bank of Canada and the Bank of England.

Methodology

As the APT allows testing based on subsets of all existing assets, seven groups of securities (or portfolios) from each of the three countries' security universe were constructed (i.e., 21 portfolios in all), each consisting of 40 randomly selected securities.' Initially, the monthly returns on all securities in their home country currency as the numeraire were used in the analysis, where each portfolio was subjected to the Maximum Likelihood Factor Analysis (MLFA) by prespecifying the number of factors from one to eight to determine the factor loadings.

It should be noted that most of the existing tests of the APT are joint tests of the APT pricing

5. Lehmann and Modest [19] shows advantages of forming many portfolios with large number of securities. Our choice was based upon the availability of 168 monthly return observations per security and 318 Canadian securities which qualified for inclusion in our sample.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

764 Sarath P. Abeysekera and Arvind Mahajan

relationship and an assumed (or estimated) number of factors. As the theory does not address the issue of the number of relevant factors, the approaches taken by researchers are varied among different studies. For instance, Roll and Ross [22] determined 5 as the appropriate number of factors from a small sample of portfolios and utilized this as the appropriate number for all their portfolios. And for the precedence established by Roll and Ross, Dhrymes, Friend, and Gultekin [9] also used 5 factors. In a more recent study, Lehmann and Modest [19] assume 5, 10 and 15 factors in their study.' As the general approach to the determination of the number of factors is ad hoc, we conducted the MLFA for each of the 21 portfolios under study to determine the appropriate number of factors from one to eight. Not surprisingly, although we employed the usual criterion based on the Chi-square statistic in our Maximum Likelihood Factor Model to determine the model adequacy, the results obtained did not clearly provide a unique number of factors which was consistent for all the 7 portfolios of a particular country's securities. Rather than arbitrarily choosing a specific number of factors to represent all portfolios of a country, we analyzed each portfolio separately.

The monthly returns of each country's 7 portfolios were then transformed to the two foreign currencies as the numeraire.7 Each of the resulting 42 new portfolios thus formed with converted returns was also subjected to MLFA as before to determine its model adequacy and the factor loadings.

This study employs the Generalized Least Squares (GLS) regression procedure, following Roll and Ross and Dhrymes, Friend, and Gultekin [9; 10], to estimate the risk premia,

L* (B*'V- B*)-I B*'V'- 1R (9)

where L* is the matrix of time-series intercepts and risk premia, B* is the augmented factor loading matrix, V is the estimated covariance matrix and R is the matrix of returns.

To test H 1, the intercept terms extracted from L* are subjected to tests to determine their significance and their equality to the appropriate risk-free rates.8 The differences between the estimated intercept terms and the risk-free rates are computed for each month and these differences are subjected to a t-test to determine their level of significance. A more robust test is conducted by regressing the monthly time-series of the intercept terms on the risk-free rates in order to perform the joint test of a zero intercept and a slope coefficient of unity. This allows analyzing the "goodness-of-fit" and the time-series properties of the regression errors.

The Chi-square test is utilized for testing H3 to determine the significance of the vector of risk premia. The five series of risk premia or A's are extracted for this purpose from L* in relation (9) and the statistic to test the hypothesis that all factors are priced for each portfolio of securities with returns expressed in a given currency is:

TXkW- - X2

6. Trzcinka [30], based on the finding that one eigen value dominates the covariance matrix, came to the tentative conclusion that one factor model describes security pricing. It further found that the first five eigen values behave differently from the rest alluding to the fact that only the first five factors are relevant.

7. For instance, all U.S. security returns were translated into returns with the Canadian dollar and the pound ster- ling as the numeraire utilizing the appropriate month-end exchange rates. This transformation resulted in 42 (7 portfolios x 3 countries x 2 foreign currencies) new portfolios with returns expressed in a currency other than their home currency.

8. As all portfolio returns are monthly returns, proxy for the monthly risk-free rates in numeraire j, Ri, were calculated from the available annualized 90-day T-bill rate in numeraire j in the following manner:

Ri = (1 + annualized 90-day T-bill ratej)1/12 - 1.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

IAPT: AN EMPIRICAL INVESTIGATION 765

where

k = (I/T)>TIlAkt., W = covariance matrix of time series A's

(lI/T) (T=l(Akt - Ak)(kt -A Xk) Akt. = time series estimates of risk premia vector, k = 1,... m

T = number of observations = 168.

The test statistic is asymptotically Chi-square with m degrees of freedom. The null hypothesis that Ak = 0 for all k 1, ...., m is rejected at a given level of confidence if the computed Chi-square is greater than the critical value at that level.

In addition, to test the significance of the individual risk premium terms, a t -test is performed using the following procedure. In matrix notation, the vector of t-statistics is computed by:

t = T -M -(Diag(S))-1

where

T = number of observations M = vector of the means of the time series of each coefficient S = vector of standard deviations.

If the computed t-values are larger than the critical value at a given level of significance, then the null hypothesis that the given risk premium is not significantly different from zero is rejected.

In order to test H4, we utilize the relationship given by equation (8).

CiJ (A - k-k)bik k=1

where

Cij and sj are defined as before, and Ak = risk premia associated with factor k with asset returns measured in the domestic

currency. Ak = risk premia associated with factor k when asset returns are expressed in foreign

country j's currency as the numeraire. bik = the factor coefficient (or loading) for asset i estimated using its returns measured in

the domestic currency.

The left side of the above expression (equation (8)) is computed directly using observed data and the right side is obtained from the estimates of risk premia and the factor loadings. The equality of these two quantities is tested using a multivariate paired comparison based on Hotellings' T2 statistic.9 If the computed T2 value is larger than the critical value, then the null hypothesis of their equality is rejected.

9. For instance, in the case of a portfolio comprised of U.S. securities, Cij and Cij associated with Canadian dollar returns on this portfolio were obtained enabling us to have a vector of differences (dlk). Similarly, pound sterling returns of U.S. securities provide another vector of difference (d2k)-

d' = [dlk,d2k], k = 1, 2,... ,n = 40

with

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

766 Sarath P. Abeysekera and Arvind Mahajan

Table I. Summary Results of Testing Hi That the Intercept Terms Are Equal to the Risk-Free Rate a,b

Number of Securities and Currencies Used

Factors, m US USINCD USINUK CDN CDINUS CDINUK UK UKINCD UKINUS (1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

1 7 7 7 6 6 6 7 7 7 2 7 7 7 6 6 6 7 7 7 3 6 6 6 5 6 6 7 7 7 4 6 6 6 6 6 6 7 7 7 5 6 6 6 7 7 6 7 7 7 6 6 6 6 7 7 6 7 7 7 7 5 6 6 6 6 6 7 7 7 8 6 6 6 6 6 6 7 7 7

a. Ho : AJo = Rj, H, :Ago #Rj. b. Number of portfolios indicating that the Ho is true (i.e., fail to reject Ho at 90% level of confidence). c. US - U.S. security returns measured in U.S. $.

USINCD - U.S. security returns measured in Canadian $. USINUK - U.S. security returns measured in pound sterling. CDN - Canadian security returns measured in Canadian $. CDINUS - Canadian security returns measured in U.S. $. CDINUK - Canadian security returns measured in pound sterling. UK - U.K. security returns measured in pound sterling. UKINCD - U.K. security return measured in Canadian $. UKINUS - U.K. security return measured in U.S. $.

IV. Results

Table I summarizes the results of the test of H I that the intercept terms equate the appropriate risk- free rates.'0 Column 1 of Table I gives the number of factors used in the analysis while columns 2 through 10 show the number of portfolios in which we failed to reject the null hypothesis. For instance, in the case of the U.S. security returns measured in Canadian dollars (i.e., column 3) with a specification of 5 factors, we fail to reject the null hypothesis in 6 out of 7 U.S. security portfolios. In brief, we fail to reject the null hypothesis in 34 out of 72 cases for all 7 portfolios, in 36 out of the remaining 41 cases we fail to reject the null hypothesis for 6 portfolios, and in the remaining 2 cases, we fail to reject the null hypothesis for 5 portfolios. There was no instance

E(dk) = 8 = 1 and cov(dk)=

=

A test of Ho : 8 = 0 versus Ha :8 # 0 can be conducted using T2 statistic and Ho is rejected when:

T2 = n'Sd-S1d > [(n - 1)p/(n -p)]Fp,n-pa

where

d= (1/n)E dk k=1

Sd = (1/n - 1) E (dk - d)(dk - d)'. k=l

Since n - p (or 40 - 2) is large, normality of d' need not be assumed and T2 has a X2 distribution with a level of significance. See Johnson and Wichern [18, 227-30] for details.

10. Detailed results for all summary tables are available from the authors upon request.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

IAPT: AN EMPIRICAL INVESTIGATION 767

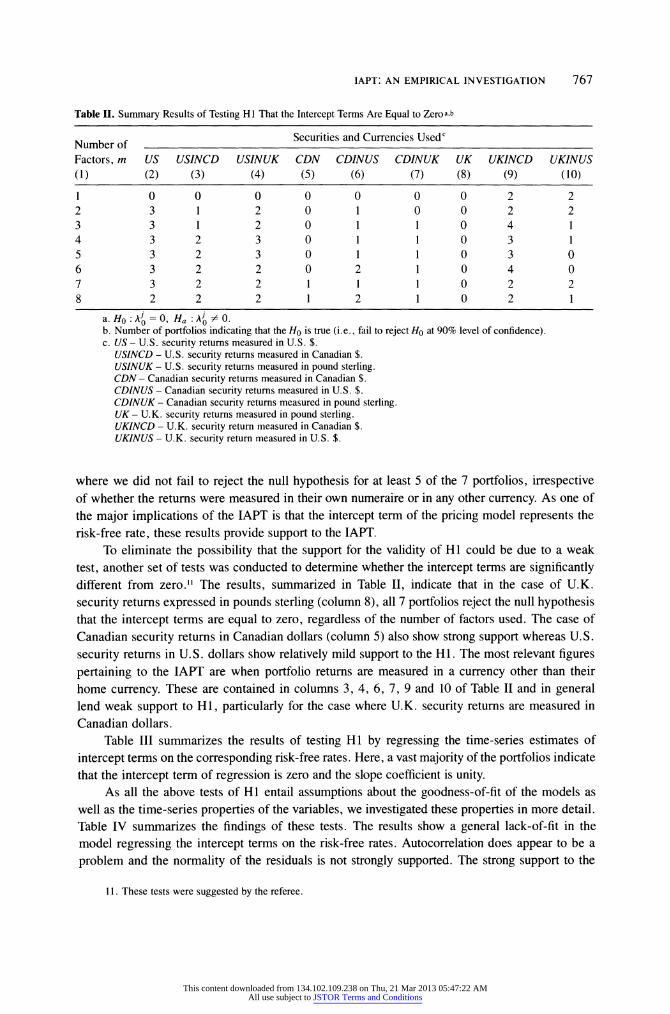

Table II. Summary Results of Testing Hi That the Intercept Terms Are Equal to Zero a,b

Number of Securities and Currencies Usedc

Factors, m US USINCD USINUK CDN CDINUS CDINUK UK UKINCD UKINUS (1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

1 0 0 0 0 0 0 0 2 2 2 3 1 2 0 1 0 0 2 2 3 3 1 2 0 1 1 0 4 1 4 3 2 3 0 1 1 0 3 1 5 3 2 3 0 1 1 0 3 0 6 3 2 2 0 2 1 0 4 0 7 3 2 2 1 1 1 0 2 2 8 2 2 2 1 2 1 0 2 1

a. Ho : Ah = 0, Ha: Ao 0. b. Number of portfolios indicating that the Ho is true (i.e., fail to reject Ho at 90% level of confidence). c. US - U.S. security returns measured in U.S. $.

USINCD - U.S. security returns measured in Canadian $. USINUK - U.S. security returns measured in pound sterling. CDN - Canadian security returns measured in Canadian $. CDINUS - Canadian security returns measured in U.S. $. CDINUK - Canadian security returns measured in pound sterling. UK - U.K. security returns measured in pound sterling. UKINCD - U.K. security return measured in Canadian $. UKINUS - U.K. security return measured in U.S. $.

where we did not fail to reject the null hypothesis for at least 5 of the 7 portfolios, irrespective of whether the returns were measured in their own numeraire or in any other currency. As one of the major implications of the IAPT is that the intercept term of the pricing model represents the risk-free rate, these results provide support to the IAPT.

To eliminate the possibility that the support for the validity of Hi could be due to a weak test, another set of tests was conducted to determine whether the intercept terms are significantly different from zero." The results, summarized in Table II, indicate that in the case of U.K. security returns expressed in pounds sterling (column 8), all 7 portfolios reject the null hypothesis that the intercept terms are equal to zero, regardless of the number of factors used. The case of Canadian security returns in Canadian dollars (column 5) also show strong support whereas U.S. security returns in U.S. dollars show relatively mild support to the H1. The most relevant figures pertaining to the IAPT are when portfolio returns are measured in a currency other than their home currency. These are contained in columns 3, 4, 6, 7, 9 and 10 of Table II and in general lend weak support to HI, particularly for the case where U.K. security returns are measured in Canadian dollars.

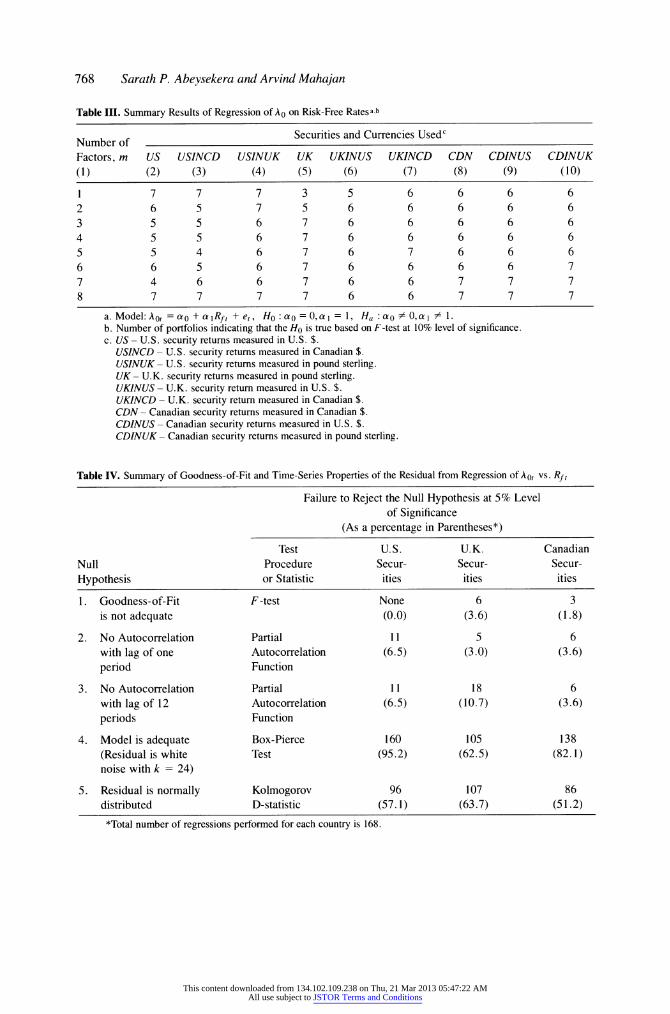

Table III summarizes the results of testing Hi by regressing the time-series estimates of intercept terms on the corresponding risk-free rates. Here, a vast majority of the portfolios indicate that the intercept term of regression is zero and the slope coefficient is unity.

As all the above tests of Hi entail assumptions about the goodness-of-fit of the models as well as the time-series properties of the variables, we investigated these properties in more detail. Table IV summarizes the findings of these tests. The results show a general lack-of-fit in the model regressing the intercept terms on the risk-free rates. Autocorrelation does appear to be a problem and the normality of the residuals is not strongly supported. The strong support to the

11. These tests were suggested by the referee.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

768 Sarath P. Abeysekera and Arvind Mahajan

Table III. Summary Results of Regression of A0 on Risk-Free Rates a,b

Number of Securities and Currencies Usedc

Factors, m US USINCD USINUK UK UKINUS UKINCD CDN CDINUS CDINUK (1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

1 7 7 7 3 5 6 6 6 6 2 6 5 7 5 6 6 6 6 6 3 5 5 6 7 6 6 6 6 6 4 5 5 6 7 6 6 6 6 6 5 5 4 6 7 6 7 6 6 6 6 6 5 6 7 6 6 6 6 7 7 4 6 6 7 6 6 7 7 7 8 7 7 7 7 6 6 7 7 7

a. Model: Aot = o + IRft + et, Ho : ao = 0, 1 = 1, Ha :ao = 0,a 1 1.

b. Number of portfolios indicating that the Ho is true based on F-test at 10% level of significance. c. US - U.S. security returns measured in U.S. $.

USINCD - U.S. security returns measured in Canadian $. USINUK - U.S. security returns measured in pound sterling. UK - U.K. security returns measured in pound sterling. UKINUS - U.K. security return measured in U.S. $. UKINCD - U.K. security return measured in Canadian $. CDN - Canadian security returns measured in Canadian $. CDINUS - Canadian security returns measured in U.S. $. CDINUK - Canadian security returns measured in pound sterling.

Table IV. Summary of Goodness-of-Fit and Time-Series Properties of the Residual from Regression of Aot vs. Rft

Failure to Reject the Null Hypothesis at 5% Level of Significance

(As a percentage in Parentheses*)

Test U.S. U.K. Canadian Null Procedure Secur- Secur- Secur- Hypothesis or Statistic ities ities ities

1. Goodness-of-Fit F-test None 6 3 is not adequate (0.0) (3.6) (1.8)

2. No Autocorrelation Partial 11 5 6 with lag of one Autocorrelation (6.5) (3.0) (3.6) period Function

3. No Autocorrelation Partial 11 18 6 with lag of 12 Autocorrelation (6.5) (10.7) (3.6) periods Function

4. Model is adequate Box-Pierce 160 105 138

(Residual is white Test (95.2) (62.5) (82.1) noise with k = 24)

5. Residual is normally Kolmogorov 96 107 86 distributed D-statistic (57.1) (63.7) (51.2)

*Total number of regressions performed for each country is 168.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

IAPT: AN EMPIRICAL INVESTIGATION 769

Table V. Summary Results of Testing H2 That the m-Factor Model Is Invariant to the Currency in Which the Returns Are Expressed a,b

U.S. Canadian U.K. Security Returns Security Returns Security Returns

Number of Denominated in Denominated in Denominated in

Factors, m US$ CDN$ ? CDN$ US$ ? ? CDN$ US$ (1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

1 0 0 0 0 0 0 0 0 0 2 0 0 0 0 0 0 0 0 0 3 0 0 0 0 0 0 0 0 0 4 0 0 0 3 3 1 0 0 0 5 1 1 1 3 3 1 2 2 2 6 2 2 2 4 4 4 4 4 4 7 4 4 2 6 6 6 4 4 4 8 5 5 5 7 7 7 6 6 6

a. Ho : m = m, Ha : m # mj b. Cumulative number of portfolios indicating m factors are sufficient (i.e., fail to reject Ho at 90% confidence

level).

IAPT provided by the F-tests (Table III) is weakened in light of these results, and in conjunction with the results of the t -tests (Table II), H1 is only mildly supported by our overall results.

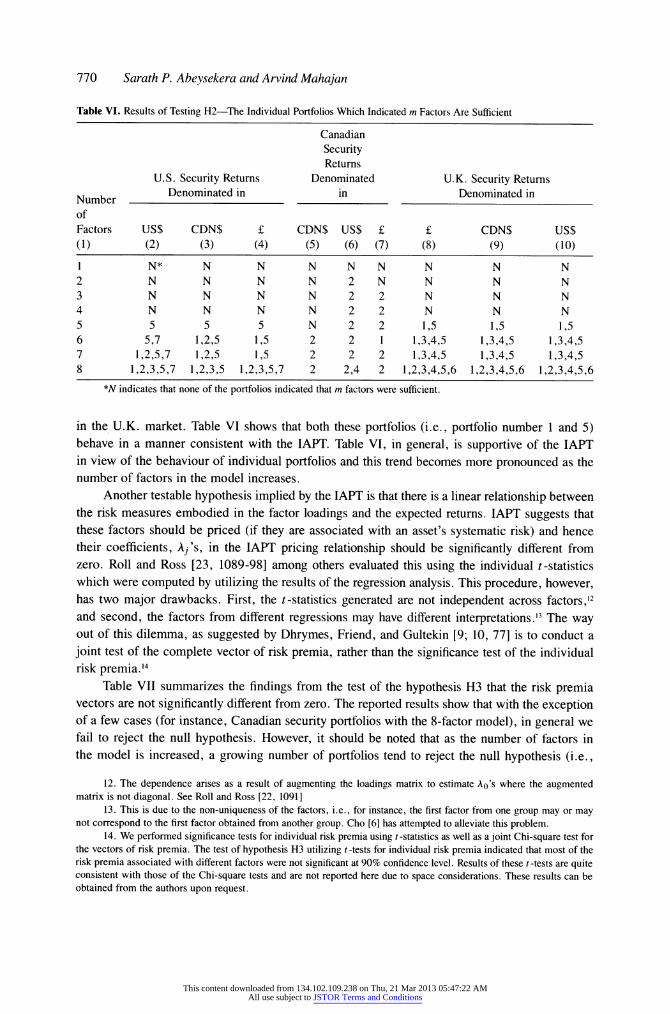

Table V summarizes the findings of the test of hypothesis H2 that the number of factors, m, before converting the returns to the foreign currency, equals the number of factors mj, after converting the returns to the foreign currency j as the numeraire. For instance, in column 2 (regarding U.S. security returns measured in U.S. dollars) none of the 7 portfolios indicates model adequacy when 1, 2, 3 or 4 factors are used and only 1 out of 7 portfolios indicated that 5 factors are sufficient. For these results to lend support to the IAPT one should observe that the number of portfolios of one country's securities with a specific number of underlying factors should be invariant to the currency in which their security returns are measured. For instance, when U.S. security returns are denominated in U.S. dollars (column 2), in Canadian dollars (column 3) and in pound sterling (column 4), the same number of portfolios indicate that 5, 6 and 8 factors are sufficient to explain the returns.

As postulated by the IAPT, the number of factors, m, is expected to remain unchanged, regardless of the currency in which the returns are denominated. One would expect, therefore, to observe the same figure as one moves across the columns in Table V for portfolios of a given country. The reported results do generally fulfill this requirement, and one can discern a pattern where figures in the columns move closely together as the number of factors prespecified is increased (i.e., moving down the three columns for a particular country's securities). The picture depicted by this, however, is clouded because the reported results are for the aggregate number of portfolios and ignore the behaviour of individual portfolios when returns are converted to different currencies.

Table VI sheds light on this by identifying the individual portfolios which comprised the aggregate figures reported in Table V. Column 1 of Table VI indicates the number of factors used in the model while columns 2 through 10 show the identity (i.e., the portfolio number) of the individual portfolios which met the Chi-square criterion. In the case of U.K. securities, for instance, when 5 factors are prespecified, only 2 portfolios (in aggregate terms) in columns 8, 9 and 10 in Table V indicated that 5 factors were sufficient to explain the return generating process

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

770 Sarath P. Abeysekera and Arvind Mahajan

Table VI. Results of Testing H2--The Individual Portfolios Which Indicated m Factors Are Sufficient

Canadian Security Returns

U.S. Security Returns Denominated U.K. Security Returns

Number Denominated in in Denominated in

of Factors US$ CDN$ ? CDN$ US$ ? ? CDN$ US$ (1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

1 N* N N N N N N N N 2 N N N N 2 N N N N 3 N N N N 2 2 N N N 4 N N N N 2 2 N N N 5 5 5 5 N 2 2 1,5 1,5 1,5 6 5,7 1,2,5 1,5 2 2 1 1,3,4,5 1,3,4,5 1,3,4,5 7 1,2,5,7 1,2,5 1,5 2 2 2 1,3,4,5 1,3,4,5 1,3,4,5 8 1,2,3,5,7 1,2,3,5 1,2,3,5,7 2 2,4 2 1,2,3,4,5,6 1,2,3,4,5,6 1,2,3,4,5,6

*N indicates that none of the portfolios indicated that m factors were sufficient.

in the U.K. market. Table VI shows that both these portfolios (i.e., portfolio number 1 and 5) behave in a manner consistent with the IAPT. Table VI, in general, is supportive of the IAPT in view of the behaviour of individual portfolios and this trend becomes more pronounced as the number of factors in the model increases.

Another testable hypothesis implied by the IAPT is that there is a linear relationship between the risk measures embodied in the factor loadings and the expected returns. IAPT suggests that these factors should be priced (if they are associated with an asset's systematic risk) and hence their coefficients, Aj's, in the IAPT pricing relationship should be significantly different from zero. Roll and Ross [23, 1089-98] among others evaluated this using the individual t-statistics which were computed by utilizing the results of the regression analysis. This procedure, however, has two major drawbacks. First, the t-statistics generated are not independent across factors,12 and second, the factors from different regressions may have different interpretations.'3 The way out of this dilemma, as suggested by Dhrymes, Friend, and Gultekin [9; 10, 77] is to conduct a joint test of the complete vector of risk premia, rather than the significance test of the individual risk premia.'4

Table VII summarizes the findings from the test of the hypothesis H3 that the risk premia vectors are not significantly different from zero. The reported results show that with the exception of a few cases (for instance, Canadian security portfolios with the 8-factor model), in general we fail to reject the null hypothesis. However, it should be noted that as the number of factors in the model is increased, a growing number of portfolios tend to reject the null hypothesis (i.e.,

12. The dependence arises as a result of augmenting the loadings matrix to estimate Ao's where the augmented matrix is not diagonal. See Roll and Ross [22, 1091]

13. This is due to the non-uniqueness of the factors, i.e., for instance, the first factor from one group may or may not correspond to the first factor obtained from another group. Cho [6] has attempted to alleviate this problem.

14. We performed significance tests for individual risk premia using t-statistics as well as a joint Chi-square test for the vectors of risk premia. The test of hypothesis H3 utilizing t-tests for individual risk premia indicated that most of the risk premia associated with different factors were not significant at 90% confidence level. Results of these t -tests are quite consistent with those of the Chi-square tests and are not reported here due to space considerations. These results can be obtained from the authors upon request.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

IAPT: AN EMPIRICAL INVESTIGATION 771

Table VII. Summary Results of Testing H3 That the Risk Premia Vectors Are Insignificantly Different from Zero a,b

Number of Securities and Currencies Usedc

Factors, m US USINCD USINUK CDN CDINUS CDINUK UK UKINCD UKINUS (1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

1 7 7 7 7 7 7 7 7 7 2 6 5 5 7 7 7 7 7 7 3 4 4 4 7 7 7 7 7 7 4 4 4 4 6 6 7 7 7 7 5 5 4 4 5 6 5 7 7 7 6 3 3 3 5 5 5 7 7 7 7 2 2 2 3 0 2 6 7 7 8 2 2 2 0 0 0 5 3 4

a. Ak = 0, k = 1,2,...,m, Ak # 0, k = 1,2,..., m b. Number of portfolios indicating that the Ho is true (i.e., fail to reject Ho at 90% level of confidence using the

Chi-square test). c. US - U.S. security returns measured in U.S. $.

USINCD - U.S. security returns measured in Canadian $. USINUK - U.S. security returns measured in pound sterling. CDN - Canadian security returns measured in Canadian $. CDINUS - Canadian security returns measured in U.S. $. CDINUK - Canadian security returns measured in pound sterling. UK - U.K. security returns measured in pound sterling. UKINCD - U.K. security return measured in Canadian $. UKINUS - U.K. security return measured in U.S. $.

support the IAPT). Overall, the results of H3 do not support the IAPT. Interestingly, these results are similar to those of previous studies for this particular hypothesis, but in the context of the domestic APT. For example, Dhrymes, Friend, and Gultekin conducted a similar test of the APT utilizing U.S. security returns data and found that in 36 out of 42 portfolios the risk premia were insignificantly different from zero. Abeysekera and Mahajan [1; 2] report similar findings from their tests of APT in the U.K. and Canada. Hence, this study's failure to reject the null hypothesis that the risk premia are equal to zero is not altogether surprising in light of the results obtained in previous empirical tests of the single currency APT.

The results of the multivariate test based on Hotelling's T2 statistic of H4 that the estimated and the observed currency-asset covariances are equal indicate rejection of the null hypothesis (at ac = .10) in all possible cases.'" This outcome clearly casts doubts on the joint hypothesis of integrated capital markets and the validity of the IAPT for pricing the U.S., Canadian and the U.K. securities.16

V. Summary and Conclusions

This paper derived four hypotheses to test the validity of the IAPT and subjected them to empirical scrutiny utilizing monthly individual security price data from Canada, the U.K. and the U.S. As

15. Due to their similarity, these results are not reported here but can be obtained from the authors upon request. We failed to reject the null hypothesis at a = .05 in only 4 out of 168 possible cases.

16. As Solnik [27] points out "that the assumption of only m common factors and independent residuals imply severe constraints on currency-asset covariance matrix", the test of H4 directly checks the adequacy of the model's underlying assumptions.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

772 Sarath P. Abeysekera and Arvind Mahajan

in all empirical tests of various pricing models, this study conducted joint tests of two hypotheses, viz., that the IAPT is a valid international capital asset pricing theory and that international capital markets are well integrated.

Results obtained in this study provide weak support to hypothesis H1 that the risk-free rates are equal to the corresponding estimated intercept terms of the models tested, thus weakly supporting the IAPT. The results generally indicate that the number of factors in a given economy is invariant to the currency in which the returns are denominated and, therefore are consistent with hypothesis H2. As data limitations precluded subjecting H2 to parametric testing, these results have to be cautiously interpreted. Regarding the third hypothesis H3, the test results from two different procedures (i.e., the t-test and the Chi-square test) show that the risk premia are not significantly different from zero. This finding does not support the IAPT and is similar to the results obtained by studies testing the domestic APT. The results of testing hypothesis H4 show that the assumption of an m -factor model and independent residuals do indeed impose constraints on the model.

On balance, the results of this study do not lend support to the IAPT. However, these results are subject to sample size constraints and the limited power of some tests. These caveats along with the well recognized problem of testing the joint hypothesis of the IAPT being valid and international capital markets being integrated should encourage further tests of the IAPT using more sophisticated test procedures and larger data sets.

References

1. Abeysekera, Sarath P. and Arvind Mahajan, "A Test of the APT in Pricing U.K. Stocks." Journal of Business Finance and Accounting, Autumn 1987, 377-91.

2. - , "A Test of the APT in Pricing Canadian Stocks." Canadian Journal of Administrative Sciences, June 1987, 186-98.

3. Adler, Michael and Bernard Dumas, "International Portfolio Choice and Corporation Finance: A Synthesis." Journal of Finance, June 1983, 925-84.

4. Chamberlin, Gary and Michael Rothchild, "Arbitrage Factor Structure, and Man-Variance Analysis on Large Assets Markets." Econometrica, September 1983, 1281-304.

5. Chen, Nai-Fu, Richard Roll and Stephen Ross, "Economic Forces and the Stock Market." Journal of Business, July 1986, 383-403.

6. Cho, David C., "On Testing the Arbitrage Pricing Theory: Inter-Battery Factor Analysis." Journal of Finance, December 1984, 1485-502.

7. - , Cheol S. Eun and Lemma W. Senbet, "International Arbitrage Pricing Theory: An Empirical Investi- gation." Journal of Finance, June 1986, 313-29.

8. Connor, Gregory, "A Unified Beta Pricing Theory." Journal of Economic Theory, October 1984, 13-31. 9. Dhrymes, Phoebus J., Irwin Friend and Mustafa N. Gultekin, "A Critical Examination of the Empirical Evi-

dence on the Arbitrage Pricing Theory." Journal of Finance, June 1984, 323-47. 10. - , - , and - , "An Empirical Examination of the Implications of Arbitrage Pricing Theory."

Journal of Banking and Finance, March 1985, 73-99. 11. Dybvig, Philip H., "An Explicit Bound on Individual Assets' Deviations from APT Pricing." Journal of Finan-

cial Economics, December 1983, 483-96. 12. - and Stephen Ross, "Yes, the APT is Testable." Journal of Finance, September 1985, 1173-88. 13. Grauer, Frederick, Robert Litzenberger and Richard Stehle, "Sharing Rules and Equilibrium in an Interntional

Capital Market Under Uncertainty." Journal of Financial Economics, June 1976, 233-56. 14. Grinblatt, Mark and Sheridan Titman, "Factor Pricing in a Finite Economy." Journal of Financial Economics,

December 1983, 497-507. 15. Huberman, Gur, "A Simple Approach to Arbitrage Pricing Theory." Journal of Economic Theory, October

1982, 183-91. 16. - , Shmuel Kandel and Robert F. Stambaugh, "Mimicking Portfolios and Exact Arbitrage Pricing."

Journal of Finance, March 1987, 1-7.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions

IAPT: AN EMPIRICAL INVESTIGATION 773

17. Ingersoll, Jonathan E., "Some Results in the Theory of Arbitrage Pricing." Journal of Finance, September 1984, 1021-39.

18. Johnson, Richard A. and Dean W. Wichern. Applied Multivariate Statistical Analysis. Englewood Cliffs, N.J.: Prentice Hall, 1982, pp. 227-30.

19. Lehmann, Bruce N. and David M. Modest, "The Empirical Foundations of the Arbitrage Pricing Theory." Journal of Financial Economics, September 1988, 213-54.

20. Lintner, John, "The Valuation of Risky Assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets." Review of Economics and Statistics, February 1965, 13-37.

21. Mossin, Jan, "Equilibrium in Capital Asset Market." Econometrica, October 1966, 763-83. 22. Roll, Richard and Stephen Ross, "An Empirical Investigation of the Arbitrage Pricing Theory." Journal of

Finance, December 1980, 1073-103. 23. Ross, Stephen, "The Arbitrage Theory of Capital Asset Pricing." Journal of Economic Theory, December 1976,

341-80. 24. - "Return Risk and Arbitrage," in Risk and Return in Finance, Vol. 1, edited by Irwin Friend and James

Bricksler. Cambridge, Mass.: Ballinger 1977, pp. 189-218. 25. Shanken, Jay, "Multivariate Tests of the Zero Beta CAPM." Journal of Financial Economics, September 1985,

327-48. 26. Sharpe, William F., "Capital Asset Prices: A Theory of Market Equilibrium Under Conditions of Risk." Journal

of Finance, September 1964, 425-42. 27. Solnik, Bruno H., "International Arbitrage Pricing Theory." Journal of Finance, May 1983, 449-57. 28. . "Testing International Asset Pricing: Some Pessimistic Views." Journal of Finance, May 1977, 503-

11. 29. Stambaugh, Robert, "Arbitrage Pricing with Information." Journal of Financial Economics, 12, 1983, 357-69. 30. Trzcinka, Charles, "On the Number of Factors in the Arbitrage Pricing Model." Journal of Finance, June 1986,

347-68.

This content downloaded from 134.102.109.238 on Thu, 21 Mar 2013 05:47:22 AMAll use subject to JSTOR Terms and Conditions