Embed Size (px)

DESCRIPTION

This is a manifesto outlining a fundamental rewriting of the social contract, based on taxation and redistribution of rents, and of taxation of money's liquidity premium.

Citation preview

A WEALTH OF LABOUR

IntroductionWe are facing numerous crises – billions in poverty; wars for resources; environmental degradation; underprovision of public services; underinvestment; unemployment and financial insecurity. These problems are all connected, and however much they seem insurmountable, they are all manmade. Finding a solution is within our collective grasp.

The key administrative reform is to democratise use of scarce resources. The most important common resource is the land, since it is required for almost everything we do. It is objectionable on counts of justice that land is treated as private property. This convention is the gravest faultline in society, dividing people into those who pay and those who receive ground rents.

Parcelling the land into private estates may once have been justified as the sole means of providing security of tenure as well as security in improvements made on the land. Such justification is no longer supportable now that we have the administrative technology capable of managing resources without violating natural justice.

For land to be managed as a public resource, rent must be taxed. Subsequently redistributing to all equally would subsidise vital services cradle-to-grave: maternity/paternity leave and childcare; primary, secondary and tertiary education; universal health insurance; and pension allowance. It also provides a safety net through working years. Rent is the natural source of public finance.

It is not just a question of social justice. Entitlement to a share of future rent provides all with the collateral to finance investment, democratising value creation while providing savers with secure instruments to hold. This financial market, in which transactions of generic rental instruments are cleared, is free from the destabilising effects of banking, and open to all.

Finally, by taxing land, and other scarce resources, there is an incentive to sustain productivity, both in how resources are rationed and how they are cared for. Extending this universal contract would involve non-market rationing of depleting resources such as hydrocarbons; imposing fees on polluters; and protecting wildernesses, all in the public interest. One by one the social problems faced by mankind would be addressed, which is the impetus for this work.

As the work progresses, a second major reform is introduced: taxation of another public resource, money. The principle is similar in that it deters harmful hoarding, only this time it is the “liquidity preference” that banking caters to that is deterred. With low risk alternatives unearthed by the fiscal reforms outlined above, money would no longer be in demand as a malfunctioning saving vehicle, and could therefore act as a medium of exchange and unit of account.

http://wealthoflabour.wordpress.com 1

In this way, taxing money would stabilise the velocity of circulation, helping to grease the wheels of commerce by regulating demand. Moreover, neutral money provides the platform for interest rates to be set in functioning financial markets rather than by a central authority.

Included as an appendix are some provisional ideas regarding how a working model of society ordered along these lines could work. In it, familiar public and private institutions are redesigned - in some cases, using broad brushes; in others, in detail - so as to promote the outcome intended by implementing the main reforms at the heart of this work. Success in this effort will be measured against the goal of a just, productive, harmonious, healthy, secure, free and contented population living in a sustainable environment – a tall order perhaps, but nevertheless within our collective grasp.

The technical proposals listed in the appendix are not intended to be the final word on such matters; numerous experts in their respective fields will be better-placed to opine than I am. The scope of work that is designed to be read as complete is thus limited to Parts I and II, although a richer sense both of their foundations and their implications may be gained by reviewing the appendix.

Lastly a word on style. Throughout this paper I am re-examining the principles of economics from the vantage point of the universal contract. In setting out my arguments, I have attempted to define core concepts with particular precision; this may have left the work with a rather dry finish, reinforced by the use of bullet points instead of open prose. Besides my interest in brevity, I am keen also to prevent conflation in the use of key terms within economics – terms such as capital or value whose recurrent and wanton misuse over the years has corrupted meaning. This has shrouded economics in great mystery, and at times leached it of wider significance.

Loose language detracts greatly from intellectual progress, and so wherever I have sought to anchor meaning explicitly (telegraphed by use of italics), it is because subsequent arguments hinge on the intended meaning being retained. I have interest neither in reinventing the wheel nor in adding density where it scarcely belongs. Nevertheless, the cost of leaving some references implicit and some meaning ambiguous I view as a greater burden on the message than the dryness in style created by this approach.

E.G. 2012

http://wealthoflabour.wordpress.com 2

Part 1: The Principles Underpinning a Functioning Economy

Self-Ownership and the Universal Contract Value is an abstract measure of the increase in usefulness of basic materials

following an application of labour. According to the labour theory of value, all value is produced by labour.

Value is realised in consumption, with the utility drawn in the process a primary component of human welfare. Production and consumption are both private activities, the rewards from the latter motivating the toils of the former. This hints at the role of labour in securing entitlement.

Economics is primarily an inquiry into the production, exchange and consumption of value, whether congealed as goods or else discharged as services. By introducing relations of property, political-economy addresses the moral question of entitlement to this productive output.

All production requires access to natural resources i.e. materials that cannot be produced or consumed and are thus both scarce and value-less. At the very least, there must be access to land. The production of goods establishes additional demand for mobile natural resources, whose contribution to the creation of value hinges on the transformative power of labour.

The effects of scarcity include that productive resources are competed over. In the process of auctioning natural resources, rent is bid progressively higher until it meets resistance from the margin of cultivation, above which rental level insufficient value would remain to cover wages (w), and labour would thus be withdrawn.

As output rises over time, rents tend to rise faster than wages. This, the iron law of wages, is the logical consequence of resource scarcity. Population growth can also drive up rents by forcing down the margin of cultivation (and thus wages) as people compete more fiercely over resources.

The rental bidding process serves to allocate scarce resources towards those capable of paying the most, and by extension, to the more productive members of a community. In this way, the law of rent tends to drive production upwards.1

Property relations govern who is permitted to claim and ultimately consume value. For property to be legitimate, it must respect self-ownership, which upholds that each individual’s rights in his or her own labour-power is limited geometrically by the rights of others in their respective toils. This is the basis of a free society.

Respecting self-ownership is the ‘golden rule’ of justice in political-economy. The terrain where such claims under natural rights must come into conflict is in the domain of scarce natural resources i.e. all the materials that predate human creativity and therefore fall under no private jurisdiction.

According to this golden rule, anyone who takes absolute possession of natural resources injures the rights of everyone else. To avoid such injury, any rights in natural resources are to be held in common, the institution of which requires that the proportion of value conceded as rent is enjoyed equally by all.

Public confiscation and redistribution of rent is the basis of the universal contract , the primary reform proposed in this paper. Accordingly, everyone would be secured a minimum rental income to supplement earned wages.

1 This is not absolutely deterministic because one bidder’s lower margin of cultivation may be enough to offset his lower productivity.

http://wealthoflabour.wordpress.com 3

As long as we fail to enforce the universal contract, landowners not only tax productive activity but also govern who do and do not produce. To this breach of self-ownership are attributed all manner of social problems besides the economic concerns discussed in this paper.

Saving and Capital A desire to secure a level of future consumption, particularly in advance of

future forced unproductivity (retirement), prompts most people into saving. An individual’s propensity to save is subject to “time preference”, so called because it describes his relative demand for consumption over time.

Saving represents desire for future consumption on the part of those prepared, for the time being at least, to consume less than 100% of their income. An individual’s saving ratio, s, measures the proportion of income that is not consumed.

By rescheduling consumption, people do not forfeit but merely postpone utility. Welfare is preserved by virtue of the rate of interest, i, which measures how much more someone would wish to consume in the future in relation to how much he is prepared not to consume in the meantime. For a typical saver, his marginal rate of interest varies with his saving ratio, as described by the following saving function:

The propensity to save is an upwards-sloping function of interest because savers demand greater compensation for the additional austerity of saving a higher share of income. The shape of the function varies from person to person

http://wealthoflabour.wordpress.com

Rate of interest (i) Saving ratio (s)

i

s

The propensity to save

Margin of subsistence

4

and over time; its curvature reflects the margin of subsistence, a minimum level of consumption that no amount of interest can erode.

The means of future consumption are not conveniently preserved in a direct manner: services are discharged and consumed immediately, while goods succumb to the forces of decay and depreciation. Thankfully, in order to save it is not necessary to retain theses sources of utility pending consumption, as we will see below.

Nevertheless, almost everyone at some point will have saved some proportion of income as durable personal possessions, to be consumed over an unspecified period of time (including as depreciation). For all but the poorest, not saving would require conscious effort. And far from earning interest, the lowest saving ratio typically implies a negative rate comprising ‘costs of carry’ such as storage, transport, depreciation, insurance, etc.

Consequently, most true hoarders are destined to consume fewer goods in the future than they have in their possession today. Not only this, but hoarders prevent other people from consuming the goods in question in the interim, which makes purposeful hoarding an especially regressive means of saving.

Some seemingly hoarding behaviour is rewarded – however, holding certain goods while they are appreciating (e.g. wines or whisky) is best considered not as hoarding but as part of the productive process, the fruits of past labour. In this respect it can be equated for instance with farming timber, which continues to grow in value as it grows organically, long after the major input of labour.

Some goods, such as urban housing and fine art, may accumulate purchasing power without growing in value. For homes in prized locations, physical depreciation may be offset by their capture of rising ground rents for their owners – a matter that would be abolished under the proposed universal contract. An original work of art is, by definition, not reproducible, and therefore fetches whatever anyone is prepared to offer. Living in a home or hanging up a painting is not hoarding, but rather prolonged consumption.

Instead of hoarding a constrained quantity of goods and bearing associated costs of carry, savers might prefer to exchange them for an unconstrained quantity of future goods and services, that is, by accumulating capital instead. Capital is immaterial, taking the form of instruments (e.g. bonds, receivables, etc) or money.

By seeking capital, savers allow others to increase consumption of goods, whose value is, after all, constrained by past production. In return, savers accumulate purchasing power, the amount of which is notionally unconstrained in the present, and actually discovered over the course of future production.

Summing the purchasing power of capital (financial instruments; money) with the value of (unconsumed) goods (inventories awaiting consumption; personal possessions; housing; commercial buildings; factories; equipment; transportation vehicles; etc) gives a measure of wealth. As a subjective quantity, fluctuations in wealth (and in resulting micro-economic behaviour) cannot be fully explained in reference to production.

Investment The exchange between savers and consumers - trading value for purchasing

power as a means of expressing their respective time preferences - describes

http://wealthoflabour.wordpress.com 5

the function played by finance. Functional finance gives savers a stake in a future they help to shape by promoting productivity.

Productivity is influenced by a number of conditions. Some are embodied in the worker (e.g. education, healthcare, etc), and are not exchangeable. They directly influence the quality of labour that the worker can contribute towards production. Others take a physical form, including tools, equipment, workplaces, transportation vehicles, etc. These goods can be manipulated by workers in order to produce more value.

Metaphysical/embodied conditions are sometimes referred to as ‘human’ capital; physical/commoditised ones as ‘physical’ or ‘productive’ capital. Both designations are avoided here in order to avoid confusion and preserve the pure meaning of ‘capital’ used in this work. What unites the metaphysical with the physical productivity-raising condition is an origin in a time-consuming (“high-order”) process.

As raising productivity largely depends on improving these conditions, whether by equipping workers with machine-tools or educating them through university, it typically takes time. An investment of time is always made if productivity is to be successfully raised, and ultimately the time is sourced from savers called on to finance the high-order processes at work.

High-order forms of production absorb some factors of production (labour, land and productive goods). These resources must come from lower-order processes, namely those methods that entail less delay between expenditure of labour and consumption of value.

Low-order methods that are typically directed towards producing consumable goods, whose supply will naturally come under strain as investment increases. But since it is always saving that finances investment, a reduced supply of consumable goods ought to coincide with a period of reduced demand. We will explore this relationship later when discussing the role of interest rates expressed in financial markets.

Saving is not a permanent decision, but one made in anticipation of a period of “negative” saving. And by the same token, when the investment comes to fruition, the restraint in both supply and demand, at least in static terms, reverses. Converting farmland into fertiliser factories, for example, will tend to reduce food supplies in the short-run, but output should recover once fertiliser production can commence and enter the food supply chain.

Consumable goods are not fungible. Subsiding demand for one particular good may account for the increase in saving, and ideally it is the supply of this good - not others - that should make way. Any new investment may well also be directed towards entirely different ends. Functioning goods markets signal fluctuations in supply and demand for different goods separately, as prices, which help people judge which ventures to discontinue and which to launch. We will come to these topics later.

In reality there are considerable frictions even in functional markets, and few supply chains operate on a just-in-time basis. Consumption - of one good as much as across all goods - may be sustained even as production falls, which implies a level of hoarding. If this goes into reverse, stockpiles will be drawn down until either consumption falls or - more benignly - past investments pay off as increased production.

A level of physical storage is appropriate for all societies as a contingency against breaks in supply chains. However, pre-emptive physical hoarding is a

http://wealthoflabour.wordpress.com 6

highly inefficient method of financing investment, and much more productive are societies that encourage savers to accumulate capital in lieu of actual goods.

During the course of investment, financiers relinquishing goods accumulate other property. This could be unfinished goods, that is, a share of ownership; however by holding equity the saver merges with the investor. In this paper, for the sake of clarity we assume that investors are financed by third-party (non-investing) savers, who accumulate financial instruments including familiar ones such as credit (a bilateral claim on the investor) and money (an official public token, discussed below).

“Financialisation” of the desire to save (i.e. its satisfaction with financial instruments) promotes economic growth by allowing productive resources to be allocated to investors according to productivity. When goods are free to circulate, they can be reproduced in railways, education, factories, machinery, and all the other stimulants of labour-productivity, and wider economic growth. By providing finance, savers open up a new frontier of production possibilities within society.

Acquisitions of High-Order Goods Post-production, acquisition of high-order finished goods such as housing

typically requires credit. Unlike investment finance, extending credit does not impinge on savings: the home has already been built, testament to the providence of previous saving.

By contrast, for investment finance low-order goods are released by savers and reproduced in higher-order forms. In the process, these goods are consumed out of wages, interest and any other revenue earned by those contributing to the productive process (as well as by rent-earners).

Credit, meanwhile, is merely a highly structured form of exchange, one in which the purchaser defers part of a payment. The availability of credit is constrained by bilateral perceptions of borrower/collateral risk. Note that under the universal contract a high-quality asset class – namely shares in future ground rent – is bequeathed to all, reducing reliance on external credit for the making of large ticket purchases.

The Supply of Finance Capital typically yields a positive rate of interest, which is supportive of

saving ratios. Earning interest is not the only driver of higher saving ratios, however. An individual’s propensity to save may grow (shifting the saving function from left to right) on account of actual or anticipated changes in material circumstances.

A driver of saving ratios is growth in income. Pending productive innovation, increased consumption offers “diminishing returns”, and so becomes increasingly decadent as income rises. The saving ratio is therefore often a positive function of income in the short run…

…though in the longer run, increased affluence may dampen saving ratios - or perhaps make them less volatile. This is because by allaying fears for the future, accumulating assets inhibits an active driver of saving.

Pessimists “purchase insurance”, as it were, by lowering their required rates of interest and wages in a bid to extract additional assets by saving and working more, thus sacrificing some discretionary consumption and leisure time in

http://wealthoflabour.wordpress.com 7

order to safeguard future welfare. Optimists require higher rates of interest and wages, and as a result enjoy greater consumption and leisure – at the expense of fewer assets.

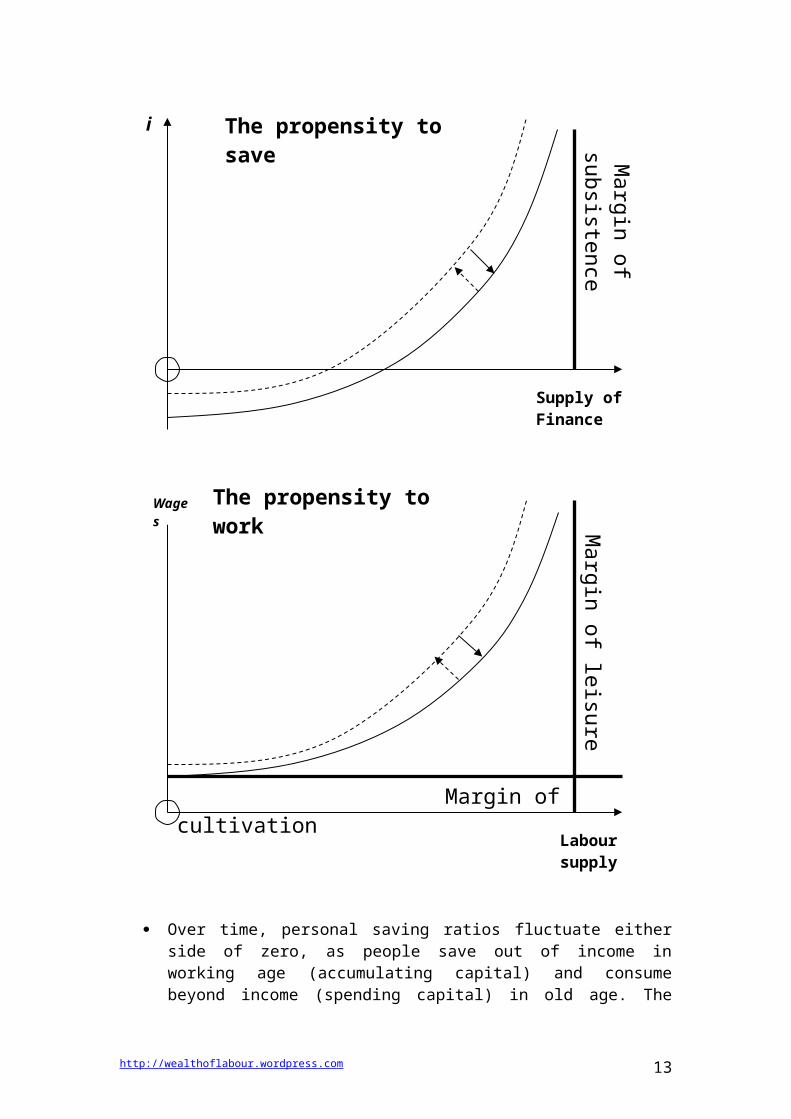

In general, if individuals’ asset portfolios shrink and/or if pessimism takes root, rising demand for insurance will tend to depress required marginal rates of interest and wages, thus increasing the supply of finance and labour. Both effects are bounded, the former by the margin of subsistence, and the latter by both the margin of cultivation and the margin of leisure (i.e. the minimum time needed to rest).

Conversely, if individuals’ asset portfolios grow and/or if optimism takes root, falling demand for insurance will enhance required marginal rates of interest and wages, thus reducing the supply of goods and labour. For many, growing consumption and leisure will be moderated by puritanical instincts, diminishing returns on gluttony and a love of work - the flint and steel sparking innovation into life.

The effects of changes in individuals’ wealth, actual or expected, on the propensity to save or to work

http://wealthoflabour.wordpress.com

Poorer/pessimism

Richer/optimism

Supply of Finance

Margin of subsistence

i The propensity to save

8

Over time, personal saving ratios fluctuate either side of zero, as people save out of income in working age (accumulating capital) and consume beyond income (spending capital) in old age. The aggregate supply of finance must be considered in terms of the net effect of microeconomic choices, i.e. as the “social saving ratio” summed up across all members of society.

This social saving ratio, which is expressed over the total value of finished goods, is far more stable than personal ratios, ranging from mildly negative levels (as aggregate inventories are run down) to a modestly positive proportion (as spare capacity is built up).

When the social saving ratio is falling, interest rates and consumer prices will tend to rise, and vice versa. Only when the social saving ratio is positive can the “term-structure” of production be raised - that is, can the proportion of high-order goods increase in proportion to low-order ones - through net investment.

Demand for Finance The emergence of financial instruments paved the way for higher saving

ratios: instead of being saddled with carry costs associated with hoarding, savers could share in the fruits of increased productivity by earning interest. In the final analysis, savers can earn interest so long as investment adds value i.e. provided the value of future output grows more than the production costs incurred.

The excess in the value added over the cost of finance rewards the investor for his efforts with a profit. Therefore finance will be in demand provided projected profit, p, is sufficient to justify the investment risks involved - a

http://wealthoflabour.wordpress.com

Labour supply

Margin of cultivation

Margin of leisure

Wages The propensity to work

9

judgment complicated by the uncertainty embedded in any projection of profit (even assuming full confidence in technical proficiency).

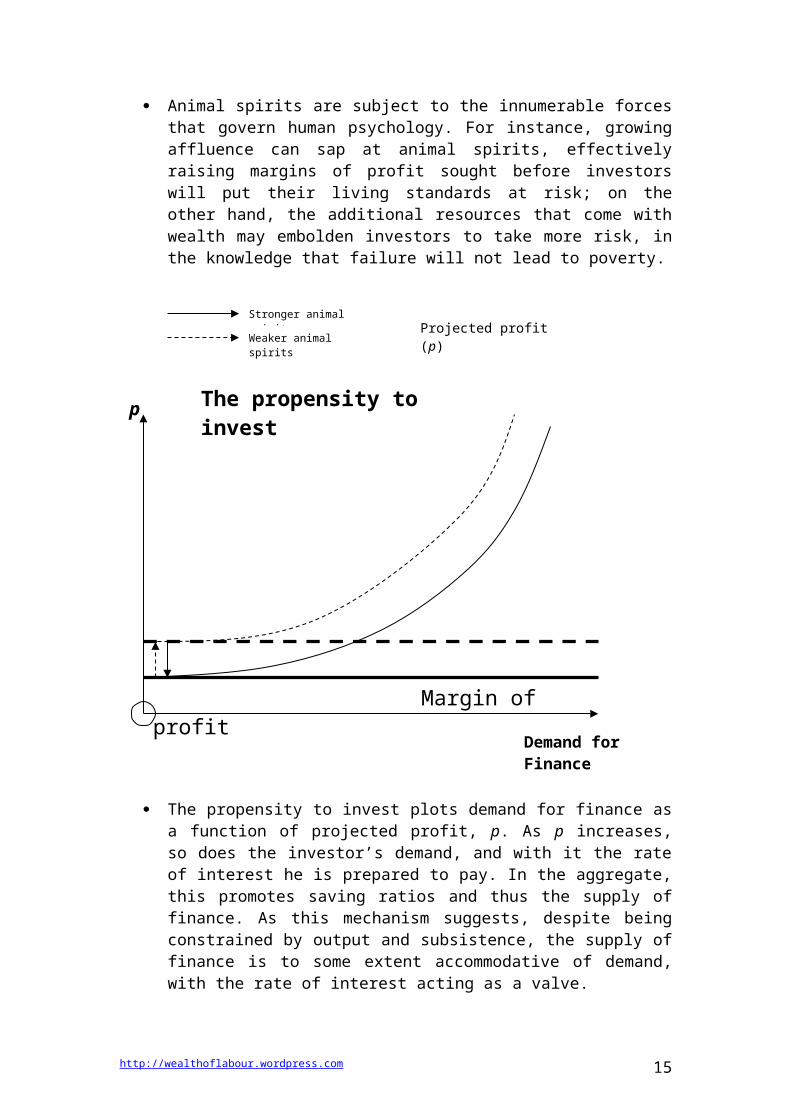

A proxy for demand for finance is ‘animal spirits’, the strength of which determines the minimum level of projected profit required in order to invest i.e. the margin of profit. The stronger are animal spirits, the lower this margin, reflecting greater confidence in projections of profit.

Animal spirits are subject to the innumerable forces that govern human psychology. For instance, growing affluence can sap at animal spirits, effectively raising margins of profit sought before investors will put their living standards at risk; on the other hand, the additional resources that come with wealth may embolden investors to take more risk, in the knowledge that failure will not lead to poverty.

The propensity to invest plots demand for finance as a function of projected profit, p. As p increases, so does the investor’s demand, and with it the rate of interest he is prepared to pay. In the aggregate, this promotes saving ratios and thus the supply of finance. As this mechanism suggests, despite being constrained by output and subsistence, the supply of finance is to some extent accommodative of demand, with the rate of interest acting as a valve.

In the next section devoted to the financial market, we explore the complex interplay between financial supply and demand, connected intertemporally by the rate of interest. The less volatile the rate of interest, the more flexible is the

http://wealthoflabour.wordpress.com

Stronger animal spirits

Weaker animal spiritsProjected profit (p)

p

Demand for Finance

Margin of profit

The propensity to invest

10

term-structure of production, which creates more scope for economic expansion – and collapse.

The Financial Market To recap, the marginal rate of interest measures how much more value a

would-be saver would expect to consume at a defined time in the future in order to forgo an incremental unit today. For investors, the corresponding expected unitary investment return signals how much future value he expects to create, after deducting associated wage and rental outlays.

Provided what value the investor expects to add exceeds what the saver demands - leaving sufficient margin of profit to justify the risk - there is scope for financing. Within the constraints set by the shape of the aggregate saving function and output, how much finance is supplied is driven by investors’ demand, which is in turn a positive function of projected profit.2 Negotiation between savers and investors determines the marginal rate of interest.

For all the financial transactions that take place, there are countless proposals foiled because what the investor is willing to pay falls short of the marginal rate of interest. A saver whose marginal rate of interest is not met will refuse to supply additional finance; an entrepreneur whose projected value added less finance costs leaves too little to cover his margin of profit will not demand finance.

2 Unlike the rate of interest or rate of return on investment, which relate one quantity to another, p is not a ratio but rather a special form of wage, compensating the investor for his particular ingenuity and for the risks assumed in the process.

http://wealthoflabour.wordpress.com

Stronger animal spirits

Weaker animal spiritsRate of interest (i)

Demand for Finance

Margin of subsistence

i Marginal Demand at Different Interest Rates

11

A key function of the financial market is to allow prospective investors to signal to would-be savers what rates they are willing to pay for finance. Provided required rates of interest are covered, savers will seek capital offering the highest risk-adjusted rate of interest. This is the allocative principle that dictates to whom finance is supplied.

This mechanism does not guarantee that finance is allocated appropriately, just as auctioning plots of land does not ensure it is leased to the most productive user. Appropriateness cannot be known in advance given an uncertain future; nevertheless, the allocative principle according to which resources are supplied to those bidding the most is the most efficient available.

Perhaps surprisingly, the job of a financial market is not to ensure stability but instead that the preferences of savers and investors determine the use of financial resources, the effect of which is to bring the social saving ratio towards zero. At this equilibrium point one might say that saving equals investment, although in reality the market is in continuous flux.

The social saving ratio cannot stay negative for longer than inventory allows. On the other hand, inventory can go on rising for much longer, albeit at the cost of wasteful hoarding. Once these carry costs become prohibitive, either consumption will increase or low-order production decline – the latter ideally as a result of strengthening investment activity causing the term-structure of production to extend and the social saving ratio to fall.

Preferences are the best guide to equilibrium, although as we will shortly see this varies according to the cohesiveness of society. In forming preferences, savers and investors take various cues. For the purposes of this analysis, these cues are categorised solely according to whether they strengthen or weaken the confidence of the typical saver and investor; any whose preferences are not expressed in a transaction are temporarily excluded.

The degree to which financial supply accommodates desired demand is driven by whether the sentiment of savers is positively or negatively correlated with that of investors, on average. The closer the correlation, the more sensitive interest rates will be to changes in the underlying cues, the less that financial supply will accommodate desired demand and the less that the term-structure of production will either extend or compress.

To examine this, aggregate functions are derived from the marginal functions described above, always recognising an (eventual) identity between the supply of and demand for value i.e. that all finished goods are destined for consumption. The point of this elaboration is that the more value is supplied by savers, the less that must be produced to meet demand, and therefore the more productive capacity that investor-led high-order processes can absorb away from lower-order ones.

Let us examine a period of general optimism as well as one of general pessimism:

o (A) General optimism - animal spirits strengthen and savers become less fearful, so that less finance is supplied at the same time as more is in demand. An increase in desired consumption competes with raised desired investment, causing interest rates to increase, which moderates extension of the term-structure of production. In graphical terms, a shift in the propensity to save from right to left reinforces the reverse shift in the propensity to invest, thus tightening financial conditions.

http://wealthoflabour.wordpress.com 12

o (B) General pessimism - animal spirits weaken and savers become more fearful, so that more finance is supplied at the same time as less is demanded. A decrease in desired consumption alongside reduced desired investment leads to a glut in finance, with resultant falls in interest rates warding off a collapse of the term-structure of production. In graphical terms, a shift in the propensity to save from left to right reinforces the reverse shift in the propensity to invest, thus loosening financial conditions.

Correlation among savers and investors means interest rates are elastic, which militates against sudden swings in discretionary behaviour, either in the propensity to save or to invest. Greater stability in the term-structure of production is indicative of a cohesive society – one that is more resistant to change.

If instead there is a structural division between savers and investors – e.g. on the basis of class, age, nation etc – then their respective responses to the same cues may differ. Let us examine negative correlation in two scenarios:

o (A) Investor pessimism/saver optimism - animal spirits weaken while savers become less fearful, so that growing consumption makes up for contracting investment. This props up aggregate demand while holding interest rates in check, ushering in a compression in the term-structure of production towards lower-order forms. In graphical terms, shifts in

http://wealthoflabour.wordpress.com

Weakening sentiment

Strengthening sentimentRate of interest (i)

Term-structure of production (Saving = Investment)

iFinancial supply

Financial demand

A

B

A – Rising aggregate demand increases interest ratesB – Falling aggregate demand depresses interest rates

Positive correlation in saver/investor sentiment

13

both the propensity to save and invest from right to left cancel out the effects of either on interest rates.

o (B) Investor optimism/saver pessimism - animal spirits strengthen while savers become more fearful, allowing the supply of finance to accommodate growing desired investment. With aggregate demand and interest rates in check, production is able to extend into a higher-order term-structure. In graphical terms, shifts in both the propensity to save and invest from left to right cancel out the effects of either on interest rates.

Supply Shocks The degree of cohesion in society as described in terms of saver-investor

correlation (interest rate elasticity) provides context and explanatory power for observed changes in interest rates as well as the underlying social and economic structure. In a global financial system, there is enormous scope for division, not least between surplus and deficit countries.

http://wealthoflabour.wordpress.com

Weakening animal spirits alongside increasing saver risk appetite

Strengthening animal spirits alongside increasing saver risk-aversionRate of interest (i)

iFinancial supply

Financial demand

A B

A – Consumption increases at the expense of falling investmentB – Investment growth accommodated by rising saving ratios

Negative correlation in saver/investor sentiment

Term-structure of production

14

The more polarised the financial system, the longer that social and economic transformation can be sustained, which may of course be welcome. However, it should be noted that in these circumstances evolution in the term-structure of production will go largely unannounced by interest rates – until it grinds to a halt.

For the term-structure of production to lengthen, the social saving ratio needs to remain in positive territory. As productive forces organise themselves into progressively higher-order processes, per capita output of consumables falls (at least relative to other goods), putting downwards pressure on the social saving ratio (recall that this is in relation to finished goods).

The social saving ratio must not dip below zero if the term-structure of production is to lengthen further. However, the more austerity is endured, the more top-heavy the structure of production, the more consumption demand becomes pent-up, and the more likely the social saving ratio is to collapse as consumption demand picks up. A divided society is more susceptible to a supply shock.

When consumer demand picks up, the narrower the base of low-order production, the sharper the increase in interest rates, and the more forceful the compression in the productive term-structure. Shocks to production are not smooth or swift, and until the social saving ratio is brought back above zero, allowing rates to stabilise, there will be a surge of business failures and rising unemployment, a recipe for social unrest.

In the classic Austrian School version of this, the supply shock is brought on or compounded by government policy. By keeping interest rates too low, central bank action is believed to lead inevitably to bouts of private ‘malinvestment’ in quixotic projects for which there is insufficient final demand. There is proportionately less production of mundane goods for which an ample demand has, paradoxically, not been signalled by interest rates.

There is some substance to this assertion, as will be outlined below. However, fixating on supply-side constraints distracts many economists from fully appreciating the separate (and often primary) role of demand as a driver of recession. Attributing all recessions to deficient supply promotes an intractable

http://wealthoflabour.wordpress.com

Interest rate elasticity

– +Change in the term-structure of production

15

view that demand-side stimulus can only postpone a return to economic health.

Hayek was successful in establishing the possibility of a tumultuous supply-driven recession rooted in interest rate distortion. However, dysfunctional finance is not only responsible for malinvestment; it also destabilises demand and, with it, our economic health, as we shall see.

Functional versus Dysfunctional Finance In a functioning financial system, the marginal rate of interest expresses the

relative consumer demand through time for the prevailing productive output of the population. While saving is a key driver of interest rates, this information does not denote actual goods being set aside for the future.

As has been discussed, one person’s saving ought to rest not on hoarding but rather on another person’s investment, with a virtue of a financial market in steering the social saving ratio towards zero. The marvel of functional interest rates is in providing signals that enable members of society to structure production so that desired consumption over time can be met.

When rates are high, production of consumables – for which there is implicitly excess demand – are stimulated by virtue of the negative effect of elevated financing costs on investment. The mechanism works indirectly by lowering the opportunity cost of low-order production.

Conversely, in making financing cheaper, low rates encourage higher-order production, the fruits of which can ideally be consumed by the time correspondingly high saving ratios decline. By raising the opportunity cost of low-order production, a glut of consumable output works itself out of the system as investment becomes more profitable.

Interest rates help to inform society how much high-order production to set in motion in relation to low-order alternatives, all on the basis of the population’s desired consumption schedules as expressed in the financial market. The term-structure of production evolves according to myriad underlying time-preferences, helping calibrate the quantity of goods and services in supply with the quantity in demand.

The emphasis on quantity is very important, since supply and demand both denote an amount (and by abstraction, value). If, over time, the quantities of goods and services in supply and in demand are equal – with any remaining productive capacity invested in meeting projected future demand – ipso facto economic welfare in aggregate cannot be surpassed.

Unlike, say, labour productivity, the rate of interest is a not an index of welfare but rather a condition for it.3 What makes the virtue of functional interest rates all the more fascinating is that it does not make itself known to those whose cumulative decisions are responsible for its operation. The lack of visible virtue is also the source of the function’s vulnerability to manipulation.

If the interest rate function is suppressed, welfare will be silently eroded. For instance, if rates are somehow artificially low, too few goods will be produced in the near term and too many in the future (at least in relation to the best estimates available in the present). Some near-term consumer demand will be unnecessarily left unfulfilled as consumption is made more expensive in the short-term and cheaper in the future.

3 How welfare is subsequently distributed across society is governed by the laws of political-economy that determine how output is divided up into wages, rents and interest.

http://wealthoflabour.wordpress.com 16

With rates held too low, the general price of current goods in terms of future goods (i.e. capital) rises. Consumer price inflation favours low-order production over investment, and although this basic outcome would also follow from a rise in the rate of interest (were it not suppressed), unlike with a functioning financial system the quantity of consumable output has first to dip below demand.

Substituting inflation for interest rates is like a pedestrian closing his eyes and relying on coming up against the curb in order to walk along a road. The collective faculty of sight, as it were, is the rate of interest: by distorting its function, society fails to husband its productive resources in an efficient manner but can only react to shocks as they occur. Retaining the example of rates held too low, the shock is felt as a shortfall in consumable output, the general price of which is thus bid higher.

So we see that when interest rates do not function well, consumer prices are less stable; this is because the key forward-looking mechanism to align the quantity of supply with demand is deactivated. In the next chapter we will discover how policymakers try (but fail) to make up for this by explicitly aiming for consumer price stability.

The value of a good reflects the cumulative productivity of labour involved in its production, which we have not changed in the examples. So if value is unchanged, the phenomenon of changing prices reveals something else: a fall in the purchasing power of capital (a notional quantity). Claims in still-to-be-produced goods, denoted as bonds and stocks, are worth less, not because labour is expected to become less productive, but because the future has had to be discounted in product markets.

Reconciling price with value has pitted different schools of economic thought against one another for centuries. Changing prices does not undermine the labour theory of value, as “marginalist” economists contend; nor should the quantity of labour expended determine a good’s price, since this depends on prevailing supply and demand. With functional interest rates, supply is better able to meet demand, allowing consumer prices to stabilise in relation to value.

Roots of Distortion Interest rate distortion rests on the exercise of monopoly in the financial

market. While it is all but impossible to monopolise either the supply of goods and services (modern production is too complex) or capital (it is virtual and immaterial), a convenient proxy for both exists: money. Private use of money as mandated by taxation confers to government monopolistic control over financial conditions.

This control is exercised by centralised setting of the “money rate of interest”, as cascaded via the banking system. But as alluded to above when introducing inflation, the interest rate function ceases to be confined to the financial system – which becomes dysfunctional as a result – and leaks instead into the real economy. If money rates are held too low, consumer price inflation boosts profits available to low-order producers in the short-term, thus attracting new entrants from higher-order projects.

By itself, this works to compress the term-structure of production, which helps to reduce consumer prices. However, besides its lagged effect, any rebalancing comes into conflict with the depressive effect of low money rates on the

http://wealthoflabour.wordpress.com 17

nominal cost of finance, which stimulates investment. Conversely, while consumer price deflation deters low-order production, its corollary, an excessive money rate of interest, discourages investment. The financial system creates mixed signals.

With a functioning financial market, in which the marginal interest rate is freely struck by savers and investors, changes in time preference produce negative feedback administered by the effect of interest rates. The effects of behavioural changes are felt by those responsible in real time, allowing time preferences to be refined in light of new information. There are no mixed signals.

Such a financial system is self-regulating, promoting stability in the term-structure of production and prices, while averting severe upheavals in patterns of saving and investment. This is true regardless of how elastic interest rates are: the more efficiently rates are set, the lower the risk of disruptive readjustments in product markets – in prices and employment – that stem from that Austrian bête noire, malinvestment.

By contrast, with rates set centrally, the effects of discretionary behaviour are externalised, creating moral hazard; and rather than acting as a self-correcting system exposing decision-makers to the results of their actions, a bank-centric financial system may engender positive feedback.

The cumulative effect of prolonged interest rate distortion can snowball into indiscriminate financial storms. No less insidious, the very foundations of society – the geoscape of town and country, the public infrastructure, our experience of education and healthcare, the entire mode of productive life – are warped by short-termism.

Policymakers cannot hope to correct for market failure. Cross-border financial flows in a multi-polar world populated by multiple political units are highly complex phenomena. Understanding what forces are at work is next to impossible given the countless economic decisions responsible. And whether the term-structure of production is appropriate depends on whether it accurately corresponds to people’s preferences, which are indecipherable.

Policymakers should instead seek to establish functional institutions founded on freedom and justice. Enforcing the universal contract outlined in this paper is a precondition for self-ownership, the keystone on which rest all the ingredients of a sane society, of which a functioning financial market is of paramount importance.

To establish functional finance requires a fundamental and comprehensive rewriting of the rules governing use of common resources, including money. The required reforms will be discussed in the next chapter. Failure to address these shortcomings condemns all to economic crisis made endemic to the structure of money and its perversion of prices. Monetary disorder and proposed reforms are topics of the next chapter.

http://wealthoflabour.wordpress.com 18

Part 2: Monetary Malaise and Reform

The Invention of Money While in theory the function provided by the rate of interest does not depend

on money, in practice any efficient market presupposes a common system of pricing that is available only after the invention of money. The classical explanation given for the existence of money is in the elimination of various transaction costs.

Absent money, any financial instrument that is redeemed only by way of delivery (to its holder) of a specified quantity of a given class of good will only perform if the good can be sourced as scheduled. Such an instrument would not appeal to a broad range of savers. A more flexible basis of saving is needed to boost investment and trade.

That basis is provided by money, which offers a linear scale on which value and purchasing power can be described and units in which they can be quoted (as a price). As such money is the universal unit of exchange (“numeraire”) in which transactions are denominated.

Moreover, it assumes a physical form in the shape of a permanent, fungible (interchangeable) token - currency. With money, all manner of contracts can be entered into with reference to this numeric scale, and subsequently settled by delivering a corresponding quantity of currency as payment.

Money not only facilitates trade by eliminating the ‘double coincidence of wants’ that hampers barter exchange; it also helps the financing of investment by enabling investors to issue financial instruments that appeal to a broader range of savers. The efficiency of money is explained partly by the fungibility of currency, allowing it to be sourced readily in markets. This makes honouring contracts easier for the financial system to accommodate.

Acceptance of money is a major innovation in society as it promotes economisation of goods transportation and warehousing. More importantly, by deterring physical hoarding as a means of saving, money unlocks the financial capacity of society.

With money, transactions can be settled unambiguously. Given that currency offers its bearers neither yield nor consumable value, its generalised acceptance is rooted in the requirement for all to settle legal obligations monetarily. Ultimately, it is tax that inheres in money the credibility needed to circulate: since everybody must pay tax, all are prepared to accept money.

So, contrary to some theories, money does not have to function as a savings vehicle (as ‘a store of value’) in order to act as a medium of exchange. In this paper it will become apparent that the two uses are actually in conflict with each other, and that ‘storing value’ is an abuse of money. Money should perform only two narrow functions: it should act as a legal means of payment and serve as a common unit of account.

A corollary of money is a common language of market exchange, most commonly detected in the price of purchased goods and services. But prices also apply when financial instruments are subscribed (quoted as yields) and when labour, land and goods are hired (quoted as wages, rent and leasing rates respectively).

Whereas bids and offers can be advertised at any time, prices are only struck when money changes hands. Simply being held does not allow money to

http://wealthoflabour.wordpress.com 19

participate directly in price formation: the quantity of money is entirely arbitrary (although knowledge of it may influence the parameters of pricing). The speed at which money changes hands – the velocity of circulation – is an index of the economy of money as a medium of exchange, and therefore of the efficacy of money.

Liquidity Preference Money is unique in being designed to stand in for goods as well as capital.

And by revealing countless prices in real-time in the process, as resources are continually allocated and utilised, money holds a useful mirror to economic activity.

Money is able to perform this vital role because of its exceptional liquidity, a measure of how close people’s estimates of its purchasing power are. Convergence is aided by the numeric ‘face value’ inscribed for all to see on the specimen, and the sole means by which it can be distinguished from other such denominations.

Allowing for quantitative difference, all denominations in the same currency (i.e. sharing a common unit scale) are perfectly fungible. Together with the exclusive requirement to deliver money for the purposes of tax settlement, fungibility allows it to act as the unit of account, or numeraire, for virtually all transactions.

Accordingly, prices are generally quoted as quantities of currency, allowing money’s purchasing power to be detected at any time from prevailing prices. This applies especially for the price of low-order consumables, on which the deleterious effects of carry costs (storage and depreciation) are highest.

Minimising carry costs encourages purchases to be made as close as possible to scheduled consumption (of which a good deal is essentially non-postponable). Carry costs therefore expedite goods “price discovery” by encouraging price-taking, so that money’s continuously-evolving purchasing power is always being advertised, cementing its liquidity.

Non-monetary capital (bonds, receivables, etc) do not receive this support. Whereas there is continual, diffuse demand for money because of its transactional functions over the life-cycle of a good, demand for other financial assets is limited to savers, and exerted more opportunistically. Holders often enjoy discretion about when to dispose, while buyers can pick among a range of options.

The more opportunistic trading is in a given asset, the less frequently will pricing information be disclosed, and therefore the less that is known about estimates of purchasing power - which impinges on liquidity. However liquidity cannot be observed, since the majority of estimates of purchasing power pass unannounced, with only successful transactions marked as prices.

Liquidity is intangible and must be proxied from other attributes. Yet its meaning is concrete: the more liquid a saving good, the ‘deeper’ is the market for it at its prevailing price, and the more that can be sourced or placed without disturbing its price. Money can be spent in vast quantities without impairing its purchasing power.

Conversely, illiquidity acts as a constraint on volumes that can be traded at any point in time without disturbing the price. For illiquid assets, placing high volumes depresses prices, while ordering in quantity raises prices. Thus bulk

http://wealthoflabour.wordpress.com 20

sales are often staggered in order to preserve purchasing power, which encourages liquidity to be imagined in terms of time.

Liquidity is naturally of considerable appeal to savers since it implies low price volatility, and therefore improved visibility in projecting purchasing power at the moment of liquidation (e.g. consumption). Savers are clearly sensitive to future purchasing power, since this is a key motivation to save in the first place.

Such is their “liquidity preference” that savers will forgo an ostensibly certain return in exchange for the spending convenience offered by (non-yielding) money. This difference is known as the liquidity premium. Differences in yields are useful indicators of relative liquidity, although higher yields are also required to compensate for counterparty risk stemming from the variable credit condition of investors.

Monetary Misuse and the Liquidity Trap Healthy demand for money is in anticipation of imminent outgoings (i.e.

transactional demand). In excess of this, demand for money may reflect precautionary demand in case of unscheduled outlays (i.e. liquidity preference). It may also reflect credit risk aversion ('flight to quality'), since unlike financial instruments, money lacks counterparty risk.

Indulging this behaviour among savers (e.g. through banking) is hugely costly. Having so much capital held dormant as money is the financial equivalent of stockpiling huge volumes of gunpowder when in fear of an assault – it increases the risk of explosion. In a financial context, among the most dramatic are episodic crises of confidence when savers express their acute liquidity preference by simultaneously withdrawing credit from the financial system.

We have already alluded to another effect - less explosive but more pernicious - of dysfunctional money: rampant volatility in the velocity of circulation. Allowing savers to express changes in discretionary behaviour first by adjusting monetary holdings externalises costs, felt as changing basic prices, which, when rising, threaten essential consumption, and when falling, disrupt employment.

Fairer and more efficient, as discussed, would be a financial system in which the consequences of discretionary behaviour feed back to decision-makers in real time, buffering essential functions performed by consumers and producers against swings in sentiment. The key point here is to recognise that money is a public good.

A generalised increase in saving should be telegraphed as falling interest rates, deterring further saving while encouraging investment. Conversely, rather than creating externalities a sudden and coordinated increase in discretionary spending (say as savers’ confidence improves) ought, by increasing interest rates, to expose marginal savers to market value declines should they liquidate their assets.

Projections of market value changes influence savers' behaviour in the current system too. When rates are expected to rise, savers will tend to sell financial instruments (offering fixed yields) in advance of feared falls in prices; meanwhile when rates are expected to fall, demand for money tends to decline.

http://wealthoflabour.wordpress.com 21

However, the current system warps expectations in a specific way: at very low nominal levels, further falls in interest rates may seem highly remote, in which case demand for fixed-rate instruments will peter out. This is because unlike money they offer savers little hope of gain and much to lose (should interest rates subsequently rise). Instead of expressing this by lowering savings, savers can simply hoard money, holding interest rates above the level able to stimulate investment demand further. The effect is akin to the propensity to save lowering (i.e. shifting from right to left) insofar as it raises interest rates demanded from investors.

This is the “liquidity trap” since although investment is depressed, there is no offsetting increase in consumption and money is instead hoarded. Insufficient demand is a troubling symptom of the failure of our financial system to cater for negative nominal interest rates, and a cause of economic stagnation.

In the current financial system, money is theoretically limitless. Therefore there is no prospect of saver demand bidding up the price of money above par, and thus its yield into negative territory. The mere knowledge of this asymmetry is sufficient, in certain circumstances, to induce a downwards spiral into the liquidity trap.

Policymakers may attempt to engineer expectations of rising prices in a bid to increase spending4, yet this does not combat the liquidity trap so much as penalise saving: any increased spending will be to bring forward purchases of goods as opposed to buying financial instruments i.e. if “successful”, the policy will reduce the propensity to save. Prodding risk-averse savers into greater consumption is financial repression.

To escape the narrow confines of the liquidity trap, risk-averse savers must be enticed to rebalance their portfolio out of money and into financial instruments – they must be disabused of any belief that risk-free interest rates are floored at zero – or, conversely, that the price of fixed-income instruments are subject to caps.

The proper way to allow negative nominal interest rates to emerge is to economise on money. This requires taxing holders of money for its liquidity premium. Money would no longer act as a safe haven in times of risk-aversion (taxing it means it would function poorly as a saving vehicle), so other financial instruments would be in proportionally higher demand, bringing down their yields, occasionally even below zero.

Just as consumables’ costs of carry expedite price discovery in product markets, so imposing an analogous monetary cost of carry would expedite price discovery in the financial market, promoting the liquidity of capital generally.

At the same time, to prevent taxation of money succumbing to charges of financial repression, the financial system would have to cater to saver risk-aversion by providing alternative counterparty risk-free assets. A non-money safe haven would have the virtue of allowing interest rates to be negative in times of distress, provided savers are so inclined. These risk-free assets will be outlined later.

With these reforms, desired holdings of money would fall to reflect more closely transactional demand (including for purposes of tax settlement). The inverse, the velocity of circulation, would therefore become less volatile - with

4 This mechanism is by no means certain – rising prices might encourage people to save more in order to safeguard essential consumption in the future.

http://wealthoflabour.wordpress.com 22

major economic dividends. At the same time, by economising on money, the liquidity of other assets -in particular the risk-free alternative variety- would increase.

Money would function as an effective means of payment and unit of account, but no longer as a decrepit store of value. This is the basis of neutral money (also examined below). Before outlining the proposed financial market reforms in more detail, let us complete the critique of the current financial system.

Fractional-Reserve Banking Having evolved from distant and scattered origins, banks have been

accumulating ever more powers along the way. Yet the essence of banking continues to be to preside over the great financial contract struck between savers and investors. This exchange relies on banks being perceived as sufficiently creditworthy for savers to entrust them with their savings.

A central feature of any form of banking is its accommodation of liquidity preference. In effect, banks accept from savers their heterogeneous holdings of illiquid assets and offer in return a homogeneous, liquid asset that is their own liability. The liquidity of bank liabilities is underpinned by banks’ promise that savers can withdraw their savings at any time in full and on demand.

Banks take deposits and make loans. The source of the credit quality any bank needs to take deposits is the law of large numbers as applied to its loan portfolio: banks derive an insurance benefit by pooling together credit risks. Competition will pass some of the credit and liquidity premium on to borrowers, although a minimum margin is required to cover the basic operating cost of managing a liquidity mismatch.

Any doubts about the creditworthiness of banks would act as a constraint on the scale of bank deposits in relation to aggregate capital. However, a lasting legacy of the bank runs that afflicted populations in the 19th and early 20th

centuries has been an encouragement on the part of policymakers of a widespread perception that taxpayers will stand behind the nominal price of bank deposits.

Not only does this lift the main constraint on the scale of banks - rendering their liabilities practically abundant – it also qualifies them as broad money, acceptable in settling payments (including tax) at par. Owing to this, banks effectively operate the payment system, with only those payments made in physical notes and coins (cash) taking place outside their control.

In order to process payments for their clients, banks are obliged to transact with one another in bank reserves - base (or narrow) money deposited with the central bank. Together with cash, bank reserves comprise the monetary base, issued by the central bank. As commercial banks settle payments on behalf of depositors, the central bank accounts for changes in the corresponding reserve balances in its respective ledgers.

Base money may be considered a liability of the central bank for accounting purposes, but it functions as a token. Ever since the monetarist-inspired ejection of gold as an international unit of account in 1971, base money has been being brought into existence “ex nihilo” i.e. at no cost to the central bank responsible. There is no other species into which base money must be converted by the central bank, which can therefore exert full control over the

http://wealthoflabour.wordpress.com 23

size of the monetary base by transacting with bank clients e.g. by advancing loans or by buying and selling financial instruments.

Unlike the central bank, a commercial bank handling a depositor’s payment cannot present its own debt to the recipient’s bank as evidence of settlement. Instead it must transfer a corresponding sum of base money (unless it happens to be both the buyer’s and seller’s bank), thus depleting its reserves. A bank will therefore aim to have sufficient base money at its disposal in order to meet calls on its reserves on demand. The requirement to remain “liquid” acts as a discipline on commercial banking - in spite of no constraints on the quantity of base money other than the volition of the central bank.

If banks issued deposits only when base money was paid in, they would have no difficulty honouring their liabilities on demand. However, most deposits are issued without receipt of base money: they are created each time a bank makes a loan to a customer. This is because (at least initially) the borrower holds the loaned money on deposit with the bank. Making (bank) loans tends to increase the quantity of broad money; repaying them does the reverse.

Fractional-reserve banks are virtual accounting entities. They hold only a fraction of their deposits in base money, with the difference comprising illiquid assets (mainly loans and bonds). So-called ‘maturity transformation’ – borrowing ‘short’ and lending ‘long’ – exposes banks to sudden calls which may exceed their reserves. If the bank is unable to obtain the shortfall in reserves by selling assets, issuing equity or borrowing, it faces collapse.

So important has the banking system become in processing payments and extending credit that the State (in the guise of the central bank) has to act as ‘lender of last resort’ to banks. But since banks are not immune from making bad loans, the State in effect has to underwrite banks to preserve the payment and credit system (and thus avoid social collapse) during financial crises. This hidden contingent liability can occasionally place public finances under immense strain.

In spite of its obvious shortcomings – inherent instability, recurrent systemic failure, contamination of public finances, contribution to economic downturn – modern ‘fractional reserve’ banking has proved to be enduring. Part of its appeal reflects the banking system’s ability to increase the quantity of broad money and thereby accommodate rising liquidity preference without explicit intervention by government or immediate ramifications for output or prices.

Indulging shifts in liquidity preference destabilises the velocity of circulation, and introduces cyclicality in prices and production. By oversupplying it, modern banking makes liquidity artificially cheap and longer-term borrowing too expensive. The lasting effect is to compress the term-structure of production, deterring higher-order investment.

Monetarism and Financial Repression We have already hinted at the fallout - as measured by financial volatility,

short-termist decision-making and economic injustice - from repressing the vital function played by interest rates in coordinating savings and investment. In this section we examine how monetarism applied the finishing touches to a bank-centric financial system that propagates such financial repression in the name of liquidity.

The liquidity of capital is not fixed or given, but depends on the various forms that financial instruments take. The greater the absorption of savings by

http://wealthoflabour.wordpress.com 24

modern bank deposits, say, the greater the fungibility of savers’ assets, and the greater the overall ‘level’ of liquidity. Any challenge to the assumed virtue of accommodating liquidity preference at all cost is deemed unworthy of inspection by the policymaking elite – which goes some way towards explaining the evolution of our financial system.

However between WWII and the early 1970s, the US dollar could purchase a weight of gold from the Federal Reserve on periodically fixed terms; and similarly had exchange rates with other currencies fixed. The visibility of official devaluation limited the freedom with which any single government could alter its monetary base; in effect, countries were operating within an international fractional-reserve system, with gold as the base. This constraint forced prudence upon commercial banks and kept the broad money supply in check.

All this changed when monetarists took charge of US monetary policy and abandoned dollar convertibility into gold. The post-WWII fixed exchange rate regime agreed at Bretton Woods was duly dissolved, allowing central banks to create domestic base money arbitrarily and ex nihilo. The birth of fiat money released governments and commercial bankers alike from the straitjacket of gold, allowing banks to indulge liquidity preference - with which monetarists saw little problem. Precautionary demand for money - even for cash - could rise without causing monetary conditions to tighten.

Monetarists did advocate other restrictions on central banking designed to safeguard monetary soundness without recourse to artificial exchange rates or indeed gold. The orthodox tools are the rates of interest at which the central bank charges for or pays on reserves borrowed or deposited respectively by commercial banks. Although these rates may differ, they will be referred to herein as the base rate.5

In this paper, unless otherwise specified, references to the rate of interest denote the ideal rate freely negotiated between savers and investors - not the base rate set by policymakers. However, with the colonisation of the financial market by fractional-reserve banking, the classical rate of interest has been emasculated.

With fiat money, commercial banks have exclusive unlimited access to central bank short-term borrowing and lending rates. Just as other providers of short-term credit cannot hope to earn more than the base rate when it is low (banks will undercut them), so other users cannot expect to pay less when the base rate is high (banks will outbid them). In this way, within the confines of a currency union, banks dominate short-term funding, both as borrower and lender i.e. they act as credit intermediaries.

However, as far as it goes this should not qualify as financial repression: consumers “holding over” over short periods are more concerned with liquidity than with earning interest. (Indeed, for the most liquid assets savers may accept negative returns; a high liquidity premium would make any yield on deposit highly attractive.) As for short-term borrowers, while “working capital” may lubricate supply chains and help cover short-term payment timing mismatches, it plays only a minor role in genuine investment activity.

5 In the UK, the base rate applies to ‘normal’ levels of reserves either borrowed from or deposited with the Bank of England overnight. If a commercial bank wishes to borrow additional reserves from the BoE, it will face a higher rate; conversely if it seeks to deposit additional reserves, it will earn a lower rate. In this way, the central bank effectively sets a floor and a cap on overnight interbank lending.

http://wealthoflabour.wordpress.com 25

More germane for the considerations within this paper are longer-term interest rates. Here, too, banks are a distorting influence: their relation with the central bank has the effect of subordinating genuine long-term rates of interest (reflecting the preferences of marginal savers and investors) beneath banks’ expectations of the future base rate (and related short-term rates).

While expectations become decreasingly reliable over longer terms, insurance (in the form of swaps and other derivatives) can be bought against the risk of errors in projecting the course of short-term rates (typically interbank rates, a tradable proxy for the base rate). By “locking in” a projection of future short-term rates, banks are emboldened to transact over longer terms. While the risk of error is simply transferred to other entities, these forward contracts help banks to compete as long-term credit intermediaries too.

When average future base rates are expected to be low, banks can undercut marginal savers, and when expected to be high, they can outbid marginal investors. Since savers and investors may still seek long-term exchanges, this has the effect simply of overriding long-term interest rates with expectations of future policy. The propensities to save and invest are distorted, forcing adjustments in the cost of finance through product and labour markets.

When banks are able to undercut marginal savers, savings tend to fall short of desired investment. Since, on account of the role of banks, the rate of interest cannot be relied on to increase, the price of (low-order) goods will increase. If unchecked, this reduces the real return available to savers, although because intermediaries such as banks will be unaffected, investment demand will remain strong.

When banks are able to outbid marginal investors, savings tend to be greater than desired investment. Since the rate of interest cannot be relied on to fall to allow the financial market to clear, a glut means the price of consumables will decline. If unchecked, this raises the real return available to savers, which will tend to reduce consumption without an offsetting increase in investment – a recipe for recession.

As we can see, there are several implications of fractional-reserve banking irrespective of base rates and their projected course. Owing to how cheap liquidity is, an excessive proportion of savers’ assets are held as money – exposing the velocity of circulation to sudden shifts.

Since liquidity is not rationed, consumption demand can swing wildly, dissipating price changes across all agents. Price volatility makes long-term planning more expensive, at unknown cost to all. Far from buffering risk and coordinating savings with investment, the monetarist financial system is an additional source of shock.

At least under Bretton Woods base rates varied inversely with the central bank’s gold reserves; if base rates were hiked up, this was typically in response to a trade deficit. Under a simplified model of fixed exchange rates, such action would reduce domestic demand and lead to a glut of domestic goods at lower prices. This would help restore trading competitiveness and replenish gold reserves, allow policy to loosen; and vice versa.

Whatever the deficiencies of this now-defunct model – and there are many – under monetarism the policy stakes rose dramatically. This is because with fiat money, the negative feedback on base rates previously (and imperfectly) provided by reserves of gold has been replaced by reliance on policymakers’ interpretation of conditions.

http://wealthoflabour.wordpress.com 26

Much less fearful about the monetary base taking flight now that it has been domesticated (at least outside the Eurozone), central bankers enjoy many more degrees of freedom within which to set policy, which raises the risk that interest rates disconnect from myriad microeconomic decision-making on which economic health depends.

No matter how sound and widely-understood central bank objectives are, a financial system based on policy projections is doomed to be a poor impostor for one built on actual preferences. No central banker can dictate how much finance is in supply and demand, or its cost, the outcome of myriad choices and actions of real actors, which if suppressed in the financial market will be expressed in the market for goods and labour.

In the following sections we will discuss what signals orthodox policymakers respond to in setting the base rate, and why such a framework is structurally handicapped by the very nature of modern money. We will see that the potentially adverse consequences of this arrangement for output and employment render base rate calibration no substitute for functioning interest rates.

The Limits of Monetarism According to classical economic models, a price measures the rate at which

one species of good or service can, at the margin, be exchanged for another. In a theoretical barter system, it is self-evident that when something rises in price, something else has to be depreciating. A uniform shift in “general prices” cannot take place under barter conditions.

We should, however, recall that exchange is capable of transcending time - that current utility can be traded for future utility, which is indeed the very essence of saving and investment and allows for narrow forms of price inflation or deflation to occur (even in a barter economy6).

As discussed in the previous chapter, when general consumer prices rise, this signals that current goods can be exchanged for a higher number of still-to-be-produced (future) goods today than was the case yesterday. Consumer price inflation speaks to a decline in the purchasing power of capital (vice versa for deflation).

Changes in consumer prices reflect disturbances in the balance between how much consumable output is being produced and how much is in demand. As we have discussed, a functioning financial market would stand a better chance at moderating these disturbances through the normal operation of the rate of interest.

Changes in this rate provide useful negative feedback by moderating underlying microeconomic behaviour that determines the cost of finance. As such, the rate of interest is a valve that tempers actual consumer price changes by helping supply to match demand over time, in terms of quantities.

This cushions less or non-discretionary economic processes (essential consumption; basic production) from changes in savers’ and investors’ preferences, which become shock-absorbers rather than generators. If this role

6 With a money economy, nominal prices are more changeable still. Unless the velocity of circulation is stabilised along the lines outlined herein, the price of money is liable to move upwards or downwards in relation to goods and capital alike. What seems to be inflation or deflation, but has another origin, makes the task of interpreting price signals much more difficult for policymakers.

http://wealthoflabour.wordpress.com 27

for interest rates is inhibited, consumer prices will accordingly be much more volatile, destabilising output and employment.

Product markets cannot perform the same moderating role as interest rates. The effect of inflation on savers is ambiguous: it might provoke austerity or else encourage physical hoarding (as discretionary purchases are brought forward). Raised basic prices encourage low-order production, while low rates promote investment – the mixed signals discussed earlier. In the mean time, essential consumption is more expensive, which penalises the poor in particular.

Conversely, deflation might well boost consumption; however, this is not guaranteed and instead non-essential purchases may be postponed in anticipation of cheaper goods in the future. Producers too are faced with falling basic prices alongside elevated financing costs – with the level of employment likely to be the main casualty.