Embed Size (px)

DESCRIPTION

working capital management

Citation preview

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 1

INTRODUCTION TO THE STUDY

“FINANCE” is the lifeblood and nerve system of any business organization. just as

circulation of blood is necessary in human body to maintain life, finance is very essential

to the organization for smooth running of the business.

Kenneth midgely and Ronald bums define financing as “a process of organizing the flow

of funds so that a business can carry out its objectives in the most efficient manner and

meet its obligations as they fall due”

“FINANCE”, thus, can be considered to be set of activities dealing with the management

of funds. More specifically, it is the decision of the collection and use of funds. It is a

branch of economics that studies the management of money and other assets.

Financial management involves managerial activities concerned with the acquisition of

fund for business purposes. The finance function does with procurement of money taking

into consideration today as well as future needs and finance is required to purchase a

machinery and raw materials to pay salaries and wages and also for day-to-day expenses.

Management of working capital refers to the management of current assets as well as

current liabilities. The major trust is of course, on the management of current assets. This

is understandable because current liabilities arise in the context of current assets. Its

importance stems from two reasons.

► Investment in current assets represents a substantial portion of total investment.

► Investment in current assets and level of current liabilities has to be geared quickly

to changes in sales.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 2

The importance in working capital management is reflected in the fact that financial

managers spend a great deal of time in managing the current assets and current liabilities.

Arranging short term financing, negotiating favorable credit terms, controlling the

movement of cash, administering the accounts receivable and monitoring the investment

in inventories consumes a great deal of time of financial managers liabilities.

The study is carried out at Eicher Motors which manufactures a range of reliable,

fuel-efficient commercial vehicles of cotemporary technology. The unit manufactures and

markets commercial vehicle with Gross Vehicle Weight (GVW) ranging from 5-25 tons.

The study was conducted in Eicher Motors, to assess the financial position and also was

aimed at the application of theoretical knowledge to the practical working of finance

department in the company.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 3

INDUSTRY PROFILE

Eicher Motor is one of the prominent commercial vehicle manufacturers in India. The

companies origins date back to 1948, when Goodearth Company was established for the

distribution and service of imported tractors.

In 1959 the Eicher Tractor Corporation of India Private Ltd. was established, Jointly

with the Gebr. Eicher company, a German tractor manufacturer. In 1960 the first tractor

ever produced in India was put on the market.

Since 1965 Eicher In India has been completely owned by Indian shareholders. The

German Eicher tractor being part of Massey-Ferguson from 1970 when they bought 30%

before buying the German company out in 1973.

In 2005, Eicher Motors Ltd sold the Tractors & Engines business to TAFE, (Tractors And

Farm Equipment Ltd), of Chennai, India, the Indian licencee of Massey Ferguson

tractors.

German car manufacturer Daimler holds a 20% stake in Eicher Motors.

Eicher Motors began its business operations in 1959 in India with the roll out of India’s

first tractor. Today the Eicher Group is a significant player in the Indian auto mobile

industry with a gross sales turnover of over INR 19,000 million ($424 million (US)) in

the year 2005-06.

GROUP STRUCTURE

The Eicher Group has diversified business interests in design & development,

manufacturing and local/ international marketing of Trucks & Buses, Motorcycles,

Automotive Gears and components. In addition to this, Eicher has also invested in the

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 4

potential growth areas of Management Consultancy Services, Customised Engineering

Solutions, City Maps & Travel Guides.

The activities of the Group are divided into the following business units covering all the

business interests.

• Eicher Goodearth Limited

• Eicher Motors Limited

o Eicher Motors - Commercial Vehicles

o Royal Enfield - Motorcycles

o Eicher Engineering Components - Gears

• Eicher Limited - Investments in Group companies

• Eicher Engineering Solutions - Customised Engineering Solutions

• Good Earth Publications - City Maps & Travel Guides

• ECS Limited - Management Consulting

The Eicher company has around 2500 employees located in 4 manufacturing facilities

and 49 marketing & area offices all around India. The Group has around 600 suppliers of

components and sub-assemblies. The Group’s products are supplied by a network of

around 381 dealers distributed across India. Eicher is present in over 40 other countries

across the world

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 5

Introduction to working capital

Working Capital means the amount of funds necessary to cover the cost of operating the

enterprise. Working Capital is the amount of capital required for the smooth and

uninterrupted functioning of normal business operations of a company ranging from the

procurement of the raw-material, converting the same into finished products for sale and

realizing cash along with the profit from the accounts receivable that arise from the sale

of finished goods on credit.

Capital required for a business can be classified under two categories:

1) Fixed Capital

2) Working Capital

Every business needs funds for two purposes – for its establishments and to carry out its

day-to-day operations. Long term funds are required to create production facilities

through the purchase of fixed assets. Funds are also needed for short term purposes for

the purchase of raw materials and other day-to-day expenses. These funds are known as

Working Capital

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 6

Concepts of Working Capital:-

There are two concepts of working capital:

1. Gross Working Capital:

The Gross Working Capital is a capital invested in total current asset of an enterprise.

2. Net Working Capital:

Net Working Capital is the excess of current assets over current liabilities.

Net Working Capital = Current Assets – Current Liabilities

Types of Working Capital:-

1) Permanent Working Capital:

It means the minimum amount of investment in all current assets, which is regarded as

necessary at all times to carry out minimum level of business. The operating cycle is a

continuous process and thus the maintenance of current assets is needed. Current Assets

increases and decreases over time. This minimum level of current assets is known as

Permanent Working Capital or Fixed Working Capital.

2) Temporary Working Capital:

This is called as Fluctuating or Variable working capital. The amount of working capital

keeps on changing depending upon the changes in production and sales. The extra

working capital required to support the changing production and sales activities is known

as Temporary Working Capital.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 7

3) Gross Working Capital:

It is the amount of working capital invested in the various components of current assets.

4) Net Working Capital:

It is the difference between the current assets and current liabilities. The concept of net

working capital enables the firm to determine the exact amount available as its disposal

for operational requirements.

5) Negative Working Capital:

When the current liabilities exceed current assets, negative working capital emerges.

Such a situation occurs when a firm is nearing crisis of some magnitude.

Working Capital Cycle:

The duration of the time required to complete the following cycle of events in a firm is

called the working capital cycle.

1. Conversion of cash into raw materials.

2. Conversion of raw materials into work in process.

3. Conversion of work in process into finished goods.

4. Conversion of finished goods into bills receivables through sales.

5. Conversion of debtors and bills receivables into cash.

Management of Working Capital:

Management of working capital is concerned with the problems arising in attempting to

manage the current assets/current liabilities and the interrelationships existing between

them.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 8

Principles of Working Capital Management Policy:

The following are the principles of a sound working capital management policy:

Principles of risk variation.

Principles of cost of capital.

Principles of equity position.

Principles of maturity of payments.

The working capital requirements of concern can be classified as:

► Permanent or Fixed working capital.

► Temporary or Variable working capital.

The fixed proportion of working capital should be generally financed from fixed capital

sources while the temporary or variable working capital requirements of a concern may

be from the short term sources of capital.

Financing of Permanent or Fixed Working Capital:

Shares:

Issue of shares is the most important source of raising long term capital. A company can

issue various types of shares such as equity, preference and deferred shares. A company

should try to raise the maximum amount by issue of shares.

Debentures:

A debenture is an instrument issued by a company acknowledging its debt to its holders.

The firm issuing debentures enjoys a number of benefits such as trading on equity,

retention of benefits, tax controls, etc.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 9

Public Deposits:

Public Deposits are the fixed deposits by a business enterprise directly from the public.

According to The Reserve Bank of India, a non-banking concern cannot borrow by the

way of public deposits more than 25% of the paid up capital and free reserves.

Ploughing back of profits:

It means the reinvestment by a concern of its surplus earnings in the business. It is an

internal source of finance and is more suitable for an established firm for its expansions.

Loans:

Financing Institutions like commercial banks, Life Insurance Corporation provide short

term, long term loans. This source of finance is more suitable to meet the medium term

demands of the working capital.

Financing of Temporary or Variable Working Capital:

Commercial banks:

The different forms of loans provided by commercial banks are as follows:

1. Loans

2. Cash Credit

3. Over Drafts

4. Purchasing and Discounting of bills.

Indigenous Bankers:

It refers to private money lenders and other country bankers. The interest rates are very

high in such cases.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 10

Trade Creditors:

It refers to the credit extended by the suppliers of goods in the normal course of business.

When a firm delays payment beyond the due date, it is called “Stretching”.

Installment Credit:

It is a method by which assets are purchased and the possession of goods is taken

immediately but the payment is made in installment over a period of time.

Factoring:

A commercial bank may provide finance by discounting the bills or invoice to its

customers. Thus a firm gets immediate payment for sale made on credit. A factor is a

financial institution, which offers services relating to management and financial debts

arising out of credit sales.

Commercial Papers:

It represents unsecured promissory notes issued by the firms to raise short term funds.

The Reserve Bank of India introduced commercial paper India on recommendations from

VAGHUL COMMITTEE.

Security Required In Bank Finance:

Following are the most important modes of security requirements –

1. Hypothecation:

Under this agreement, bank provides working capital against the security of moveable

property usually inventories. The borrower does not give the possession of the property to

the bank.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 11

2. Pledge:

Under this agreement the borrower is required to transfer the possession of the property

or goods to the bank as security.

3. Mortgage:

It is a transfer of a legal or equitable interest in a specific immovable property for the

payment of debt. The possession of the property remains with the borrower but the total

legal title is transferred to the lender.

Importance of Working Capital:

Working Capital is the life blood and nerve system of any business organization. Just as

circulation of blood is necessary in human body to maintain life, working capital is very

essential to the business organization for smooth running of the business. No business can

run successfully without and adequate working capital. The main advantage of

maintaining adequate amount of working capital is as follows:-

1. Solvency of the business:

Adequate working capital helps in maintaining solvency of the business by providing

uninterrupted flow of production.

2. Goodwill:

Sufficient working capital enables a business concern to make prompt payments and

hence helps in creating and marinating goodwill.

3. Easy Loans:

A concern having adequate working capital, high solvency and good credit standing

can arrange loans from banks and other financial institutions on easy and favorable

terms.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 12

4. Cash Discounts:

Adequate working capital also enables a concern to avail cash discounts on the

purchase and hence it reduces cost.

5. Regular Supply of Raw Materials:

Sufficient working capital ensures regular supply of raw materials and continuous

production.

6. Regular Payment of Salaries, Wages And Day-to-Day Commitments:

A company which had ample working capital can make regular payment of salaries,

increase their efficiency, reduces wastage costs and enhances production and profile.

7. Exploitation of Favorable Market Conditions:

Only concerns with adequate working capital can exploit favorable market condition

such as purchasing its requirements in bulk when the prices are lower and by holding

its inventories for higher prices.

8. Ability to Face Crises:

Adequate working capital enables a concern to face business crisis in emergencies

such as depreciation because during such periods, generally, there is much presence

on working capital.

9. Quick and Regular Return On Investment:

Every investor wants a quick and regular return on his investments. Sufficient

working capital enables a concern to pay quick dividends to its investors as there may

not be much pressure to plough back profit. This gains the confidence of its investors

and creates favorable markets to raise additional markets to raise additional funds in

future.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 13

10. High Morale:

Adequacy of working capital creates an environment of securities, confidence and

high morale and creates overall efficiency in business.

Need or Objectives of Working Capital:

The need for working capital arises to run day-to-day business activities of production

and sales. Firms differ in their requirement of the working capital. To maximize

shareholders wealth, a firm should earn sufficient returns from its operations. Earnings a

steady amount of profit require successful sales activity. Current assets are needed

because sales do not convert into cash immediately. There is always an Operating Cycle

involved in the conversion of sales into cash.

Thus working capital is needed for the following purposes:

1. For the purchase of raw materials, components and spares.

2. To pay wages, salaries, etc...

3. To incur day-to-day expenses and overhead costs such as fuel, power, office

expenses, etc…

4. To meet the selling cost such as packaging, transport, advertising, etc.

5. To provide credit facilities to customers.

For studying the need of working capital in business, one has to study the business under

varying circumstances such as new concern, as a growing concern and as one, which has

attained maturity. A new concern requires a lot of livid funds to meet initial expenses like

promotion, formation, etc. these expenses are called “Preliminary Expenses” and

are capitalized. The amount needed as working in a new concern depends primarily upon

its size and ambitions of its promoters. Generally, the working capital needed goes on

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 14

increasing with the growth and expansion business till it attains maturity. At maturity, the

amount of working capital needed is called “Normal Working Capital”.

ESTIMATION OF WORKING CAPITAL REQUIREMENTS:

The working capital requirements of a concern depend upon a number of factors such as

size of the business unit, the length of production cycles the character of their operation,

the rate of stock turnover and the state of economic situation. It is not possible to rank

them because all such factors generally influence the working capital requirements.

1. Nature of the business:

The nature of the business affects the working capital requirements of a concern to a

great extent. For instance, public utilities like railways, electricity companies, etc

need very little working capital, because they need not hold inventories and their

operations are mostly on cash basis. On the other hand, ordinary manufacturing and

trading firms requires large working capital as they have to invest substantially.

2. Scale of operations:

The scale of operations affects the working capital requirements of a concern.

Concern carrying on small activities needs less working capital. On the other hand, a

concern undertaking activities on large scale needs large amount of working capital.

3. Growth and expansion of business:

The growth and expansion of business also affects the working capital requirements.

When there is growth and expansion in the business of a firm, the working capital

needs of the firm increases.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 15

4. Manufacturing Process:

In manufacturing business the requirement of working capital increases in proportion

to length of manufacturing process. Longer the process period of manufacturer, larger

the amount of working capital required. The longer the manufacturing time, the raw

material and other supplies have to be carried out for a longer period in the process

with progressive increment of labor and service cost before the finished product

finally obtained. Therefore the process with the shortest production period should be

chosen.

5. Production Policies:

The production policies followed by a firm will also affect the working capital

requirement. For example, a capital intensive industry requires more of fixed capital

and vice versa.

6. Rapidity of turnover:

There is a high degree of co-relation between rapidity of turnover and the amount of

working capital requirements. Generally firms having a high rate of turnover need

lower amount of working capital than the firm having a low rate turnover.

7. Seasonal fluctuations in demand:

Seasonal fluctuations in demand for the products affect the amount of working capital

requirements of a concern. For instance, the demand of goods for woolen cloths

increases during winter and decreases in summer. As a result its working capital need

will increase during winter and decrease during summer. Similarly, cyclical factors

also affect the amount of working capital of a concern.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 16

8. Fluctuation in supplies:

Fluctuation on supplies affects the working capital requirement of a firm. For

instance, certain raw materials may be available only during certain seasons. Such

materials have to be necessarily be obtained and stored in large quantities to provide

for periods when supplies will not be available. This will cause fluctuation in the

working capital requirements.

9. Operating efficiency:

The operating efficiency of a firm affects its working capital requirements. A firm

enjoying operating efficiency has reduced working capital needs. On the other hand,

the firm which does not enjoy operating efficiency has more wastage and thus, needs

more working capital.

10. Credit Policy:

The credit policy of a firm affects its working capital requirements. A firm, which

allows more credit to its customer, requires more working capital compared to a firm

which allows less credit. The credit facilities enjoyed by a firm from its creditors also

affect the working capital requirement of a firm. A firm enjoying liberal credit

facilities from its suppliers or creditors will need lower working capital than a firm

that does not enjoy liberal credit facilities from its suppliers.

Management of Working Capital

Working Capital is essentially the difference between current assets and current

liabilities. There are two broad sources of capital – fixed capital represented by

investments made in fixed assets like plant, machinery, land, buildings, furniture, etc.

working capital, on the other hand, is for short term and is used for meeting regular

operating expenditures or commitments to suppliers, government dues and other short

term liabilities. Efficiency of working capital is judged using following ratios-

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 17

1) Current Ratio

2) Liquid Ratio (Acid Test Ratio)

3) Sales to Working Capital Ratio

4) Finished Goods Turnover

5) Cash to Average Daily Cost Of Sales

6) Bank Finance as % of Working Capital

Management of working capital is concerned with the problems that arise in attempting

to manage the current assets, current liabilities and the inter-relationship that exits

between them. It sees to it that there is neither excess nor inadequate working capital.

Working Capital management is the most critical issue in any company. Companies have

seasonality in their sales or revenues find it much more challenging to meet liquidity

requirements compared to firms have non-seasonal businesses.

Financing working capital is yet another aspect of working capital management. There

are various ways of financing it-trade credit, bank finance, cash credit, overdraft, export

financing (letter of credit), bank guarantees. As per RBI guidelines, working capital loans

are granted on the basis of certain calculations/ analysis submitted by companies to

banks/ financial institutions. The formats in which these reports are given are as per –

CMA format, and the financing methodology is known as Maximum Permissible Bank

Finance (MPBF).

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 18

Principles Working Capital Management

The following are the principle of a sound working capital management policy:

Principle of Risk Variation:

There is an inverse relationship between the degree of risk and profitability. A

consecutive management prefers less risk by maintaining a high level of current assets,

while a liberal management assumes greater risk by having low working capital.

Principle of Cost of Capital:

The various source of raising working capital have different cost of capital and risk

involved. Generally, higher the risk lower is the cost of capital and lower the risk higher

the cost of capital.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 19

Principle of Equity Position:

According to this principle, the amount of working capital invested in each component

should be adequately justified by a firm’s equity position. Every rupee invested in current

assets should contribute to the net worth of the firm.

Principle of Maturity Payment:

According to this principle, a firm should make every effort to relate maturities of

payment to its flow of internally generated funds.

Importance of working capital

Even though the skill of maintaining the working capital are somewhat unique, the goal

are the same-viz.to make an efficient use of funds for minimizing the risk of loss to attain

profit objectives.

Firstly, the adequate of working capital contributes a lot in raising the credit standing of a

corporation in terms of favorable rates of interest on bank loan, better terms on goods

purchased, reduced cost of production on account of the receipt of cash discount etc.

Secondly, a company with sufficient working capital is always in a position to take

advantage of any favorable opportunity either to purchase raw material or to execute a

special order or to wait for better market position.

In the third place, the ability to meet all reasonable demands for cash without inordinate

delay is a great psychological factor to improve the all rounds efficiency of the business.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 20

Lastly, during slump the demand for working capital, instead of coming down, shoots up.

A good amount of working capital is locked up in the inventories and book debts.

Concern having ample resources can tide over that period of depression.

Thus, working capital is regarded as one of the conditioning factors in the long run

operations of the firm, which is often inclined to treat it is an issue of short-run analysis

and decision making.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 21

Working Capital Measurement

The analysis of working capital can be conducted through a number of devices such as:

RATIO ANALYSIS:

A ratio is a simple arithmetical expression of the relationship of one number to another.

The technique of ratio analysis can be employed for measuring short-term liquidity or

working capital position of a firm. The following ratio’s may be calculated for this

purpose:

Current Ratio.

Acid Test Ratio.

Absolute Liquid Ratio or Cash Position Ratio.

Inventory Turnover Ratio.

Receivables Turnover Ratio.

Payables Turnover Ratio.

Working Capital Ratio.

Ratio of Current Liabilities to Tangible Net Worth.

FUND FLOW ANALYSIS:

Fund flow analysis is a technical device designated to study the resources from which

additional funds were derived and the use to which these resources were put. It is an

effective management tool to study changes in the financial position (working capital) of

a business enterprise between beginning and ending financial statement dates. It consists

of preparing schedule of changes of working capital, statement of sources and

application of funds.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 22

WORKING CAPITAL BUDGET:

Working capital budget is a part of total budgeting process of a business, is prepared

estimating future long term and short term working capital needs and the sources of

finance them, and then comparing the budgeted figures with the actual performance for

calculating the variances, if any, so the corrective actions may be taken in the future.

CASH MANANGEMENT

In United States banking, cash management, or treasury management, is a marketing

term for certain services offered primarily to larger business customers. It may be used to

describe all bank accounts (such as checking accounts) provided to businesses of a

certain size, but it is more of an used to describe specific services such as cash

concentration, zero balance

Accounting and automated clearing house facilities. Sometimes, private banking

customers are given cash management services.

Cash management deals with the following:

Cash inflows and outflows.

Cash flows within the firm.

Cash balances held by the firm at a point of time.

RECEIVABLES MANAGEMENT

Accounts receivable are unpaid customer invoices, and any other money owed to the

organization by customers. The sum of all customer accounts receivable is listed as a

current assets on balance sheet.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 23

RESEARCH DESIGN

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 24

Introduction to Design:

What is Research Design?

Research design can be thought of as the structure of research – it is the “glue” that holds

all the elements in a research project together. We often describe a design using a concise

notation that enables us to summarize a complex design structure efficiently. What are

the “elements” that a design includes? They are:

Title of the study

A study of Working Capital Management at, EICHER MOTORS Ltd, using ratio

analysis.

Statement of the Problem

The study is done to review the Working Capital Management at EICHER MOTORS

Ltd. Working Capital is considered as the life blood of the business. The firm should

maintain a sound working capital position and should have an adequate working capital

to run its business operations.

An appropriate level of working capital is to be maintained to run the business smoothly

as excessive working capital interrupts the smooth flow of the business.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 25

Objectives of the Study

The following are the objectives of the study conducted:

1) To compare the financial position of the company for the past 3 years with the

help of ratios concerned with the working capital and turnover.

2) To identify liquidity, turnover in terms of stock and working capital.

3) To study the method of financing of working capital and to find the flow of

funds.

4) To identify, understand and interpret the problem and put forward suggestions.

5) To make a proper analysis of the gross and net working capital through proper

scrutiny.

Research Methodology

3 years of Balance Sheet and Profit and Loss a/c were used stated in the Annual Reports

for analysis.

Working Capital and concerned ratios used as a tool of analysis. Based on the

computation, the financial position and performance of the business was evaluated and

suggestions were made. Regarding the financing of working capital, both the methods

were evaluated by extracting information from the Balance Sheet for 3 years, then the

best alternative was chosen and based on the company’s position regarding the financing

of working capital was known.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 26

Reference Period

The study period in this case study is for 3 financial years i.e., from 2008 to 2010.

Scope of the Study

The study of analysis of working capital management is limited to the specific bank,

EICHER MOTORS Ltd.

Data collection

The required data has been collected from secondary sources of information such as the

Balance Sheet and Profit and Loss a/c. the secondary data has also been collected from

business journals, magazines, internet, and other published information. The analysis has

been made by referring to the secondary data and also under the guidance of my guide

and the manager of EICHER MOTORS Ltd. There was a use of primary data in the case

of financing of working capital through the use paper work and discussion held with the

senior financial management.

Tools of Analysis

Working capital cycles, schedule of changes in working capital, composition of current

assets & liabilities, gross & net working capital and ratio analysis were used as a tool of

analysis. The data analyzed is presented in the form of tables and charts. Further, ratio’s

and percentages are used to interpret the data.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 27

Limitations of the Study

The study was subjected to following limitations:

1).The information is availed from the statements, annual reports and records of the

company.

2).One of the constraints of the study was that of the time factor, which was very short.

3). The focus is only on working capital of the company

4). The data’s are randomly selected from the annual reports.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 28

COMPANY PROFILE

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 29

EICHER MOTORS: Eicher Motor is one of the prominent commercial vehicle manufacturers in India. The

success and growth of this unit is a result of various customer-driven strategies. The

manufacturing facility is situated in Central India – Pithampur, Madhya Pradesh. Eicher

Motors has stepped into the Heavy Commercial Vehicle segment with its state-of-the-art

HCV, the "Eicher 20.16", the first commercial vehicle designed and developed

indigenously. Recently, Eicher Motors has emerged with Volvo to form another HCV.

Eicher Motors functions through a strong three-tier service network consisting of

authorized distributors, service centers and company trained private mechanics. The

vehicles are sold and serviced through a network of over 576 Authorized Contact Points

all over India, supported by service centers and over 4500 company trained private

mechanics, which are close at hand on all major highways throughout India to

provide initial "first aid" to the vehicles if required.

Eicher Motors has acquired formidable expertise in designing and developing

commercial vehicles. It has a world-class R&D centre manned by a team of brilliant

engineers and equipped with latest Computer Aided Design (CAD) and Computer Aided

Engineering facilities like NASTRAN, FEM analysis packages. Leveraging its in-house

expertise, this unit has successfully developed a wide range of commercial vehicles to

meet varying customer needs. The product range includes Trucks : Eicher 10.50, Eicher

10.75, Eicher 10.90, Eicher 11.10, Eicher 20.16 & 30.25; Buses: Eicher Skyline, Eicher

Cruiser and Eicher School Bus range of buses. Besides the basic models, it offers over 85

models of ready-to-use custom-built vehicles for various specialized applications. Eicher

Motors’ products have been well accepted in the market. This is also demonstrated by

significant sales of its commercial vehicles in export markets where the company

competes with reputed international brands.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 30

EICHER MOTORS: COMPANY HISTORY

1948 The Company, Goodearth was set up to sell and service imported tractors.

1959 First indigenous Eicher tractor built.

1952 - 1957 Goodearth imported and sold about 1500 tractors in India.

1958 Incorporation of Eicher Tractor Corporation of India Ltd.

Apr. 24, 1959 Eicher launched the first indigenously built tractor from its Faridabad factory.

Sept.3, 1960 Changed name to Eicher Tractors India Ltd.

1965 - 1975 100% indigenization achieved in Eicher Tractors.

1980 Eicher Goodearth Limited name given to Eicher.

1982 Collaboration with Mitsubishi.

Oct. 4, 1982 Collaboration agreement for the manufacture of Light Commercial Vehicles

signed with Mitsubishi in Tokyo.

Oct. 14, 1982 Eicher Motors Limited was incorporated.

1985 Silver Jubilee Year for Eicher.

1986 Eicher Motors Limited springs into operation.

Dec., 1987 Eicher Tractors went public.

Feb. 2, 1990 Eicher Goodearth buys 26% equity stake in Enfield India Ltd.

1991 ECS launched

1991 Eicher takes over Ramon & Demm

Apr.1, 1991 Formal launch of Management Consulting division of Eicher - ECS

Aug.24, 1993 Eicher acquires majority stake in Enfield India (60% equity shareholding)

Mar. 1994 End of the technical assistance Agreement with Mitsubishi after successful

transfer of technology and achieving total indigenization.

Jun. 23, 1994 Enfield India Limited changed its name to Royal Enfield Motors Limited

Dec.20, 1995 Eicher City Map - Delhi launched

1996 Eicher Tractors Limited amalgamated with Royal Enfield Motors to form Eicher

Limited on Jun. 1, 2005.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 31

Jun. 1, 2005 Eicher Motors Limited disinvested the businesses of Tractors & Engines to TAFE

Motors and Tractors Limited (TMTL)

Apart from the above table:

The company has entered into a technical collaboration agreement with the FINLAND

based VALTRA Inc. for the manufacture of 61 and higher to HP tractors.

The company has been awarded Certificate of Merit for improving the overall

productivity in the Automobile sector by the National Productivity Council of

Government of India.

Eicher has tied up with Volkswagen to enter the passenger car segment.

In 2003, UBI tied up with Eicher and L&T for financing equipments and farm vehicles.

In 2005, Eicher acquired DESIGN, USA. Eicher buys US Design company for $2.5m.

In 2006, Eicher joined hands with WIPRO to source Hydraulic Kits.

Board of Directors:

S Sandilya – Chairman

Siddhartha Lal – Managing Director & Chief Executive Officer

P N Vijay – Director

Priya Brat – Director

M J Subbaiah – Director

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 32

PRODUCT RANGE:

Leveraging its in house expertise, Eicher Motors has successfully developed a wide range

of commercial vehicles to meet the varying customer needs. These vehicles deliver value

by providing low cost of ownership and increased profitability to our customers. The

range offered include fully built up trucks – ranging from 6T to 25T, buses and chassis.

All these products can be offered in BSII compatible options. Eicher Motors arguably

have the best CNG technology in the world.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 33

SERVICE AND MAINTAINANCE:

Eicher has an extensive service reach and no matter the problem is, Eicher service is

never too far away. Eicher provides its customer the benefit of an extensive sale and

service network, customized solutions and an efficient cost of ownership. Our

manufacturing capabilities are backed by a sales and service network of our 950 contact

points across India and over 8000 private mechanics trained Eicher ensuring that your

vehicle is in safe hands.

SERVICE INITIATIVES:

Eicher Genuine Spares – available across all Eicher authorized representatives, service

centers, spares distributors, satellite service outlets and retail outlets.

Fully equipped modern workshops for quick and quality service.

Driver training for drivers to impart safe driving skills and to enhance fuel efficiency.

Regular free check up and service camps.

Regular customer needs and contacts.

A comprehensive service Audit System, which oversees the physical infrastructure and

service quality of Eicher service network.

Highway check up campaigns.

Eicher Motors is the first company in the Commercial Vehicle industry to introduce

warranty operation through Electronic Media.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 34

MANUFATURING FACILITIES:

The manufacturing facility of Eicher Motors is located in PITAMPUR, MADHYA

PRADESH. This is a state – of – the – art plant which has a total area of 72 acres with

18000 sq.mts as the covered area. The plant houses some top of the line equipment, a

robust infrastructure and has an annual production capacity of 30000 vehicles.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 35

SPARES:

Eicher products are engineered to perfections, incorporating the best of technology and

the state of the art manufacturing facilities. It is thus a privilege itself to maintain any

product in a perfect condition. This can be done by using specified Eicher Genuine Parts,

which meets the required engineering precision standards.

The most important element of this new light blue color packaging is the bright hologram

which glitters. When viewed from angles, the hologram reflects different colors

providing a 3-dimensional feel, thus giving it a more professional and user-satisfactory

results.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 36

DATA ANALYSIS AND

INTERPRETATION

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 37

RATIO ANALYSIS

FINANCIAL ANALYSIS

Financial analysis is the process of identifying the financial strengths and weaknesses of

the firm and establishing relationship between the items of the balance sheet and profit &

loss account.

Financial ratio analysis is the calculation and comparison of ratios, which are derived

from the information in a company’s financial statements. The level and historical trends

of these ratios can be used to make inferences about a company’s financial condition, its

operations and attractiveness as an investment. The information in the statements is used

by

• Trade creditors, to identify the firm’s ability to meet their claims i.e. liquidity

position of the company.

• Investors, to know about the present and future profitability of the company and

its financial structure.

• Management, in every aspect of the financial analysis. It is the responsibility of

the management to maintain sound financial condition in the company.

RATIO ANALYSIS

The term “Ratio” refers to the numerical and quantitative relationship between two items

or variables. This relationship can be exposed as

• Percentages

• Fractions

• Proportion of numbers

Ratio analysis is defined as the systematic use of the ratio to interpret the financial

statements. So that the strengths and weaknesses of a firm, as well as its historical

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 38

performance and current financial condition can be determined, Ratio reflects a

quantitative relationship helps to form a quantitative judgment

STEPS IN RATIO ANALYSIS

• The first task of the financial analysis is to select the information relevant to the

decision under consideration from the statements and calculates appropriate

ratios.

• To compare the calculated ratios with the ratios of the same firm relating to the

pas6t or with the industry ratios. It facilitates in assessing success or failure of the

firm.

• Third step is to interpretation, drawing of inferences and report writing

conclusions are drawn after comparison in the shape of report or recommended

courses of action.

BASIS OR STANDARDS OF COMPARISON

Ratios are relative figures reflecting the relation between variables. They enable analyst

to draw conclusions regarding financial operations. They use of ratios as a tool of

financial analysis involves the comparison with related facts. This is the basis of ratio

analysis. The basis of ratio analysis is of four types.

• Past ratios, calculated from past financial statements of the firm.

• Competitor’s ratio, of the some most progressive and successful competitor firm

at the same point of time.

• Industry ratio, the industry ratios to which the firm belongs to.

• Projected ratios, ratios of the future developed from the projected or pro forma

financial statements

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 39

INTERPRETATION OF THE RATIOS

The interpretation of ratios is an important factor. The inherent limitations of ratio

analysis should be kept in mind while interpreting them. The impact of factors such as

price level changes, change in accounting policies, window dressing etc., should also be

kept in mind when attempting to interpret ratios. The interpretation of ratios can be made

in the following ways.

• Single absolute ratio

• Group of ratios

• Historical comparison

• Projected ratios

Inter-firm comparison

GUIDELINES OR PRECAUTIONS FOR USE OF RATIOS

The calculation of ratios may not be a difficult task but their use is not easy. Following

guidelines or factors may be kept in mind while interpreting various ratios are:

• Accuracy of financial statements

• Objective or purpose of analysis

• Selection of ratios

• Use of standards

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 40

IMPORTANCE OF RATIO ANALYSIS

• Aid to measure general efficiency

• Aid to measure financial solvency

• Aid in forecasting and planning

• Facilitate decision making

• Aid in corrective action

• Aid in intra-firm comparison

• Act as a good communication

• Evaluation of efficiency

• Effective tool

LIMITATIONS OF RATIO ANALYSIS

• Differences in definitions

• Limitations of accounting records

• Lack of proper standards

• No allowances for price level changes

• Changes in accounting procedures

• Quantitative factors are ignored

• Limited use of single ratio

• Background is over looked

• Limited use

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 41

CLASSIFICATIONS OF RATIOS

The use of ratio analysis is not confined to financial manager only. There are different

parties interested in the ratio analysis for knowing the financial position of a firm for

different purposes. Various accounting ratios can be classified as follows:

1. Traditional Classification

2. Functional Classification

3. Significance ratios

1. Traditional Classification

It includes the following.

• Balance sheet (or) position statement ratio: They deal with the relationship

between two balance sheet items, e.g. the ratio of current assets to current

liabilities etc., both the items must, however, pertain to the same balance sheet.

• Profit & loss account (or) revenue statement ratios: These ratios deal with the

relationship between two profit & loss account items, e.g. the ratio of gross profit

to sales etc.,

• Composite (or) inter statement ratios: These ratios exhibit the relation between a

profit & loss account or income statement item and a balance sheet items, e.g.

stock turnover ratio, or the ratio of total assets to sales.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 42

2. Functional Classification

These include liquidity ratios, long term solvency and leverage ratios, activity ratios and

profitability ratios.

3. Significance ratios

Some ratios are important than others and the firm may classify them as primary and

secondary ratios. The primary ratio is one, which is of the prime importance to a concern.

The other ratios that support the primary ratio are called secondary ratios.

IN THE VIEW OF FUNCTIONAL CLASSIFICATION THE RATIOS

ARE:

1. Liquidity ratio

2. Leverage ratio

3. Activity ratio

4. Profitability ratio

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 43

TABLE REPRESENTING COMPOSITION OF CURRENT ASSETS (Rs. In millions) Table – 4.1

ELEMENTS MAR

2010

% MAR

2009

% MAR

2008

%

INVENTORIES 1612.3 33.28 1612.5 31.15 1262.5 29.06

DEBTORS 1176 27.28 1580.8 30.53 1549.3 35.6

CASH & BANK

BALANCE

261 5.39 310.4 6.00 331.5 7.63

OTHER

CURRENT

ASSETS

77 1.59 - - - -

LOAN

ADVANCES

1718.1 35.47 1547.1 32.32 1014 27.65

TOTAL 4844.4 100 5050.8 100 4157.3 100

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 44

GRAPHICAL REPRESENTATION OF COMPOSITION OF

CURRENT ASSETS

Graph – 4.1

0

200

400

600

800

1000

1200

1400

1600

1800

2010 2009 2008

inventories

debtors

cash&bankbalanceother currentassetsloans andadvances

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 45

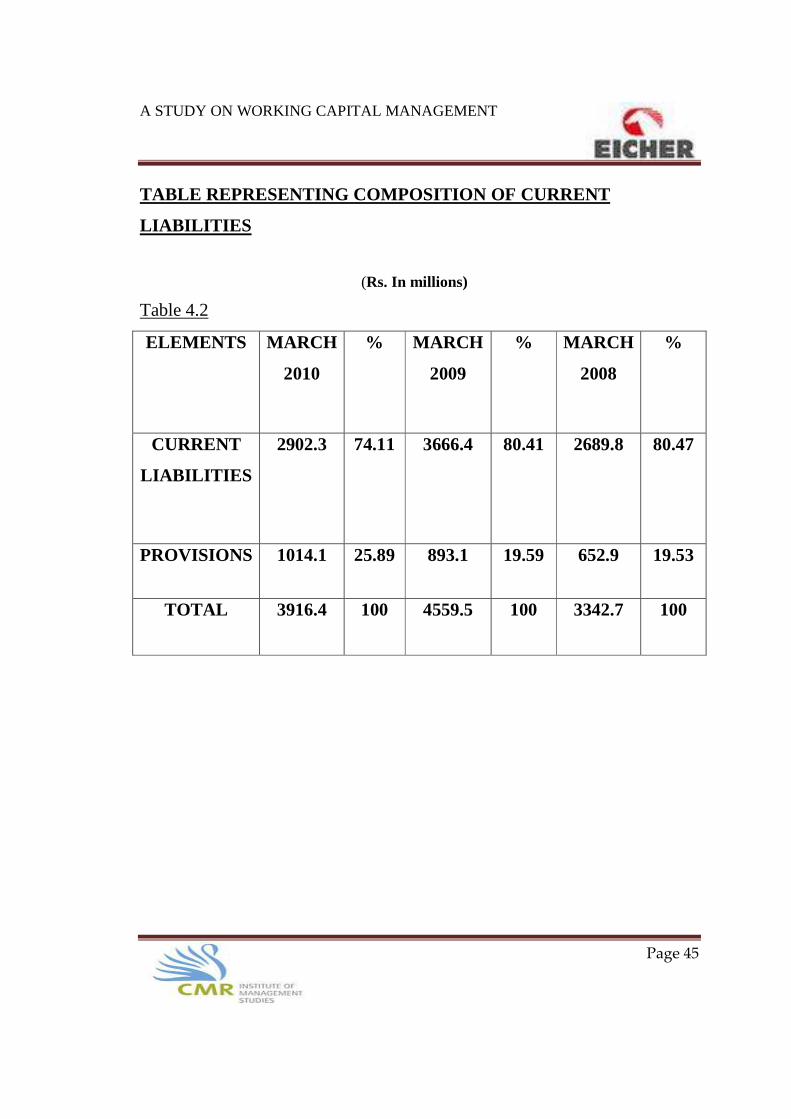

TABLE REPRESENTING COMPOSITION OF CURRENT

LIABILITIES

(Rs. In millions)

Table 4.2

ELEMENTS MARCH

2010

% MARCH

2009

% MARCH

2008

%

CURRENT

LIABILITIES

2902.3 74.11 3666.4 80.41 2689.8 80.47

PROVISIONS 1014.1 25.89 893.1 19.59 652.9 19.53

TOTAL 3916.4 100 4559.5 100 3342.7 100

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 46

GRAPHICAL REPRESENTATION OF COMPOSITION OF

CURRENT LIABILITIES

Graph – 4.2

2008 20092010

0

500

1000

1500

2000

2500

3000

3500

4000

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 47

TABLE REPRESENTING WORKING CAPITAL CYCLE FOR 2010

WORKING CAPITAL CYCLE (2010)

TABLE – 4.3

ELEMENTS DAYS

Raw Materials Storage Period 49

Conversion Period 3

Finished Goods Storage Period 14

Average Collection Period 27

Average Payment Period 73

ANALYSIS

From the above table it can be observed that the company stores its raw material for 49

days before it is converted into finished goods, and then the company takes 3 days for

conversion of raw material into finished products, it takes 14 days to store the finished

goods before it is delivered to the final consumer. Next it shows the average collection

period from debtors was 27 days and average payment period to creditors was 73 days.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 48

GRAPHICAL REPRESENTATION OF WORKING CAPITAL

CYCLE FOR 2010(in days)

GRAPH – 4.3

0

10

20

30

40

50

60

70

80

R.M.S.P C.P F.G.S.P A.C.P A.P.P

Working CapitalCycle(2010)

49

3

14

27

73

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 49

TABLE REPRESENTING WORKING CAPITAL CYCLES

TABLE – 4.4

YEAR 2010 2009 2008

Raw materials

storage period (days

– A)

49 37 32

Conversion period

(days – B)

3 3 3

Finished goods

storage period (days

– C)

14 9 7

Average collection

period (days – D)

27 26 24

Gross working

capital cycle (days –

A+B+C+D = X)

93 75 66

Average payment

period (days – E)

73 64 62

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 50

ANAYLSIS

The proper analysis of the working capital management can be made through the proper

study of working capital cycles which help to ascertain the no of days the company takes

to complete once such cycle.

It can be observed from the table and the chart that the Gross working capital cycle has

been increasing every year for the years 2007 – 2010. Thus it has an increasing trend.

Also, from the table it can be noticed that the raw materials storage period have been

increasing for the years 2008 – 2010. It can also be observed from the table and the chart

that the Net Working Capital Cycle has been increasing every year for the years 2007 –

2010. Thus it has an increasing trend. Moreover, from the table we can see that the

average payment period have been increasing for the years 2008 – 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 51

GRAPHICAL REPRESENTATION OF GROSS WORKING

CAPITAL CYCLE (in days)

Graph – 4.4

2010 20092008

0102030405060708090

100 93

7566

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 52

GRAPHICAL REPRESENTATION OF NET WORKING CAPITAL (in days) Graph – 4.5

20102009

2008

02468

1012

14

16

18

2020

11

4

INFERENCE From the table and the charts, it can be seen that the Gross Working Capital cycles as

well as raw material storage period have been increasing over the financial years, thus

showing an increasing trend. This is not good from the company’s point of view because

more is being blocked in the storage of raw materials rather than the finished goods

storage period. When compared among the three financial years, it can be observed that

the Net Working Capital cycle as well as the average payment period shows an increase

in trend. This proves that good for the company, but not from the creditors point of view.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 53

TABLE REPRESENTING VARIOUS TRENDS (Rs. In millions) Table – 4.5 PARTICULARS 2010 2009 2008

Inventories 1612.3 1612.5 1262.5

Sundry Debtors 1176 1580.8 1549.3

Cash & Bank Balances

261 310.3 331.5

Creditors 2350.5 2846.9 2446.3

ANALYSIS It can be observed from the table and the chart that the trends for inventories, sundry

debtors and creditors has been increasing and decreasing alternatively for the years

2008 – 2010, whereas, cash and bank balance has a decreasing trend. The proper scrutiny

of this trend is of at most important because this constitute the working capital of the

company and have a direct bearing on its level.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 54

GRAPHICAL REPRESENTATION OF VARIOUS TRENDS Graph – 4.6

0

500

1000

1500

2000

2500

3000

Inventories Sundry Debtors Cash & BankBalances

Creditors

2010

2009

2008

INFERENCE

From the data above i.e. the table and the chart, it’s seen the inventories, sundry debtors

and creditors fluctuate over the financial years, whereas cash and bank balance shows a

decreasing trend. An appropriate inspection should be done as the entire result shows

upon the working capital of the company.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 55

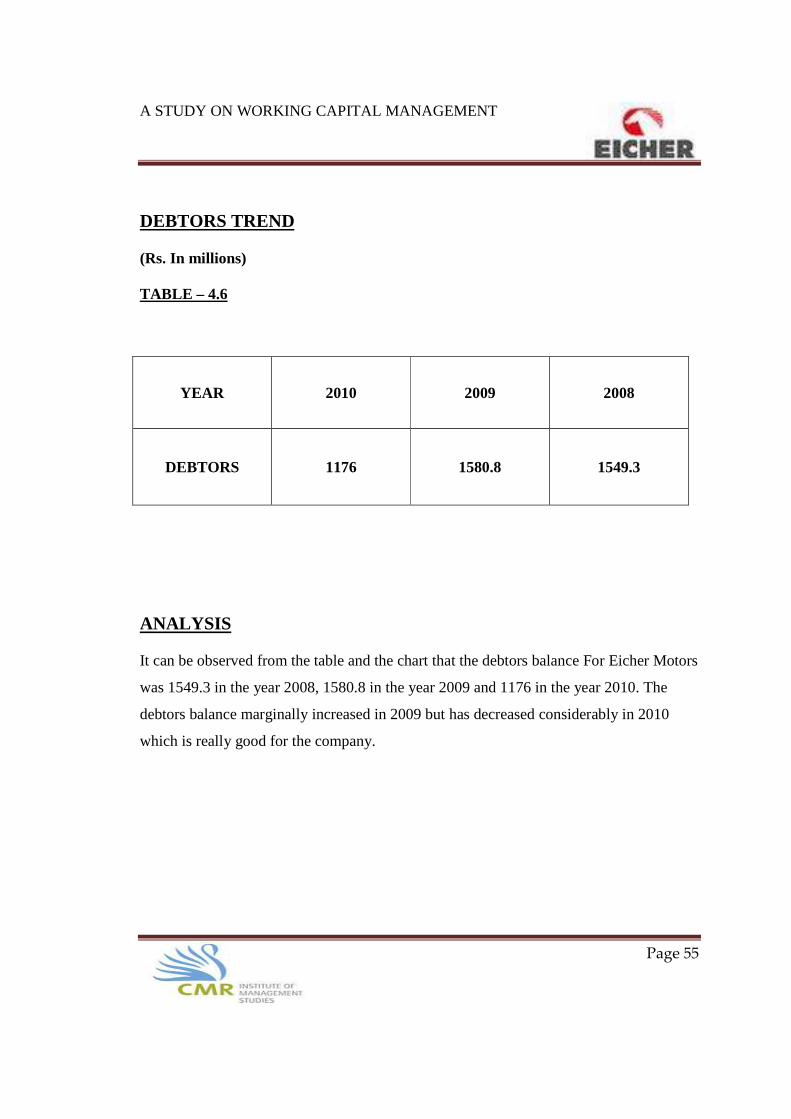

DEBTORS TREND (Rs. In millions) TABLE – 4.6

YEAR 2010 2009 2008

DEBTORS 1176 1580.8 1549.3

ANALYSIS It can be observed from the table and the chart that the debtors balance For Eicher Motors

was 1549.3 in the year 2008, 1580.8 in the year 2009 and 1176 in the year 2010. The

debtors balance marginally increased in 2009 but has decreased considerably in 2010

which is really good for the company.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 56

GRAPH – 4.7

20102009

2008

0

500

1000

1500

2000

AMOUNT

1176

1580.81549.3

INFERENCE It can be observed here, that in the last financial year the debtors balance is showing a

decreasing trend. This gives a positive note to the company as the debtors or receivables

imply credit sales and the decrease in debtors balance shows that the company has now

shifted its focus on making more of cash sales which helps it to recover its money in a

lesser period of time.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 57

INVENTORIES TREND (Rs. In million) TABLE – 4.7

YEAR 2010 2009 2008

INVENTORIES 1612.3 1612.5 1262.5

ANALYSIS It can be observed from the table and the chart that the inventories of Eicher Motors was

1262.5 in 2008, 1612.5 in 2009 and 1612.3 in 2010. the inventories balance has increased

remarkably from 2008 to 2010, which does not prove to be good as the operation of the

company might show problems in functioning.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 58

GRAPH – 4.8

20102009

2008

0

500

1000

1500

2000

INVENTORIES

1612.3 1612.5

1262.5

INFERENCE Although inventories involve blocking of a firm’s funds and the costs of storage and

handling but every business enterprise has to maintain certain level of inventories to

facilitate uninterrupted production and smooth running of business. Here the data shows

the rapid increase in 2009 as compared to 2008 and the stability of inventories between

2009 and 2010, which is not good for the company as more funds are now blocked in

inventories in the form of raw materials and work in progress.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 59

CASH AND BANK BALANCE TREND (Rs. In million) TABLE – 4.8

YEAR 2010 2009 2008

CASH AND BANK BALANCE 261 310.4 331.5

ANALYSIS From the table and the chart it can be seen that the trend of cash and bank balances of

Eicher Motors shows a decrease trend. It was 331.5 in the year 2008, 310.4 in 2009 and

261 in 2010. In a more optimistic way, this shows a significant mindset of the company

as the money is not being kept idle, but instead they are invested in areas such as

production, etc for incurring profit.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 60

GRAPH – 4.9

2010 20092008

0

100

200

300

400

CASH AND BANKBALANCE

261 310.4 331.5

INFERENCE Cash and bank balances are important assets to the company because they are the best

form of liquid assets and thus, play an important role in fulfilling the working capital

requirements of the company. It further helps to smoothen the functioning of the

company. Moreover, it shows a decreasing trend which is again good for the company

since they are utilizing more of their funds for the production.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 61

CREDITORS TREND (Rs. In million) TABLE – 4.9

YEAR 2010 2009 2008

CREDITORS 2350.5 2846.9 2446.3

ANALYSIS It can be observed from the table and the chart that the creditors balance for Eicher

Motors was 2446.3 in 2008, 2846.9 in 2009 and 2350.5 in 2010. This is not a good sign

as it cannot afford to block its capital by making cash purchases.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 62

GRAPH – 5.0

20102009

2008

0

500

1000

1500

2000

2500

3000

CREDITORS

2350.5

2846.9

2446.3

INFERENCE Creditors form one of the most important components of liabilities of the company. The

creditors balance has been increasing and decreasing over the past years. The creditors

balance imply credit purchase and has decreased in 2010 which is not good for the

company and thus, needs to revamp its purchase policy because it cannot afford to block

up its capital by making cash purchases. But for creditor’s point of view, it is good for the

company since it is dealing more in cash which is obviously more viable for the creditors

as they would like to deal with the company.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 63

WORKING CAPITAL RATIOS CURRENT RATIO This ratio is a rough indication of a firm’s liability to service its current obligations.

Generally, the higher is the current ratio, the greater the “cushion” between current

obligations and a firm’s ability to pay them. The stronger ratio reflects a numerical

superiority of current assets over current liabilities. However, the composition and quality

of current assets is a crucial factor in the analysis of an individual firm’s liquidity.

Current Ratio = Total Current Assets Total Current Liabilities TABLE REPRESENTING CURRENT RATIO (Rs. In million) TABLE – 5.0

YEAR 2010 2009 2008

Current Assets 4844.4 5050.8 4157.3

Current Liabilities 3916.4 4559.5 3342.7

Current Ratio 1.237 1.108 1.244

ANALYSIS It can be observed from the table and the chart that the current ratio for Eicher Motors

was 1.237 in 2010, 1.108 in 2009 and 1.244 in 2008. The current ratio has been

decreasing and increasing alternatively for the period 2008 – 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 64

Graphical Representation of Current Ratio

GRAPH – 5.1

20102009

2008

1

1.05

1.1

1.15

1.2

1.25 1.237

1.108

1.244

INFERENCE The ideal current ratio for the company is 2: 1. Eicher Motors has not been able to reach

this value from 2008 to 2010. Though there has been increase in the ratio in 2008

compared to previous year but still the company has not been able to maintain its current

assets and liabilities.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 65

QUICK RATIO

Quick Ratio is also known as “ACID RATIO”. It is a more severe conservative measure

of liquidity. The ratio expresses the degree to which a company’s quick liabilities are

covered by the quick assets. The quick ratio is a form of derivative. It excludes

inventories from the current assets, considering only assets which are most swiftly

realizable. Quick Liabilities refer to all the current liabilities except for bank overdraft.

Quick Ratio = Quick Assets Quick Liabilities TABLE REPRESENTING QUICK RATIO (Rs. In million) TABLE – 5.1

YEAR 2010 2009 2008

QUICK ASSETS 3232.5 3438.3 2894.8

QUICK LIABILITIES

3916.4 4559.5 3342.7

QUICK RATIO 0.83 0.75 0.87 ANALYSIS It can be observed from the table and the chart that the quick ratio for Eicher Motors was

0.87 in 2008, 0.75 in 2009 and 0.83 in 2010. The quick ratio has increased and decreased

alternatively for the period 2008 – 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 66

GRAPHICAL REPRESENTATION OF QUICK RATIO GRAPH – 5.2

2010 2009 2008

0.65

0.7

0.75

0.8

0.85

0.9

Quick Ratio

0.83

0.75

0.87

INFERENCE The ideal quick ratio for any company is 1:1. Eicher Motors has never been able this

value during the past three years. In all the three years the company hasn’t managed to

reach the ideal level. Thus, it becomes important for the company to maintain more liquid

assets as any further decline in the years to come may prove detrimental to the growth for

the company.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 67

ABSOLUTE LIQUID RATIO The ratio is also known as super quick ratio or cash ratio. In calculating this ratio, both

inventories and receivables are deducted from current assets to arrive at absolute liquid

assets such as cash and easily marketable securities.

Absolute Liquid Ratio = Cash & its Equivalent Current Liabilities TABLE REPRESENTING ABSOLUTE LIQUID RATIO (Rs. In millions) TABLE – 5.2

YEAR 2010 2009 2008

Cash & its equivalent 261 310.4 331.5

Current Liabilities 3916.4 4559.5 3342.7

Absolute Liquid Ratio 0.067 0.068 0.099

ANALYSIS It cab be observed from the table and the chart the absolute quick ratio for Eicher Motors

was 0.099 for the year 2008, 0.068 fir the year 2009 and 0.067 for the year 2010. The

quick ratio has decreased steadily over the past three years.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 68

GRAPHICAL REPRESENTATION OF ABSOLUTE LIQUID RATIO GRAPH – 5.3

2010 20092008

0

0.02

0.04

0.06

0.08

0.1

Absolute Liquid Ratio

0.067 0.068

0.099

INFERENCE

Higher the absolute quick ratio, higher is the cash liquidity. A low ratio is not a serious

matter because the company can always borrow from the bank for short term

requirements.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 69

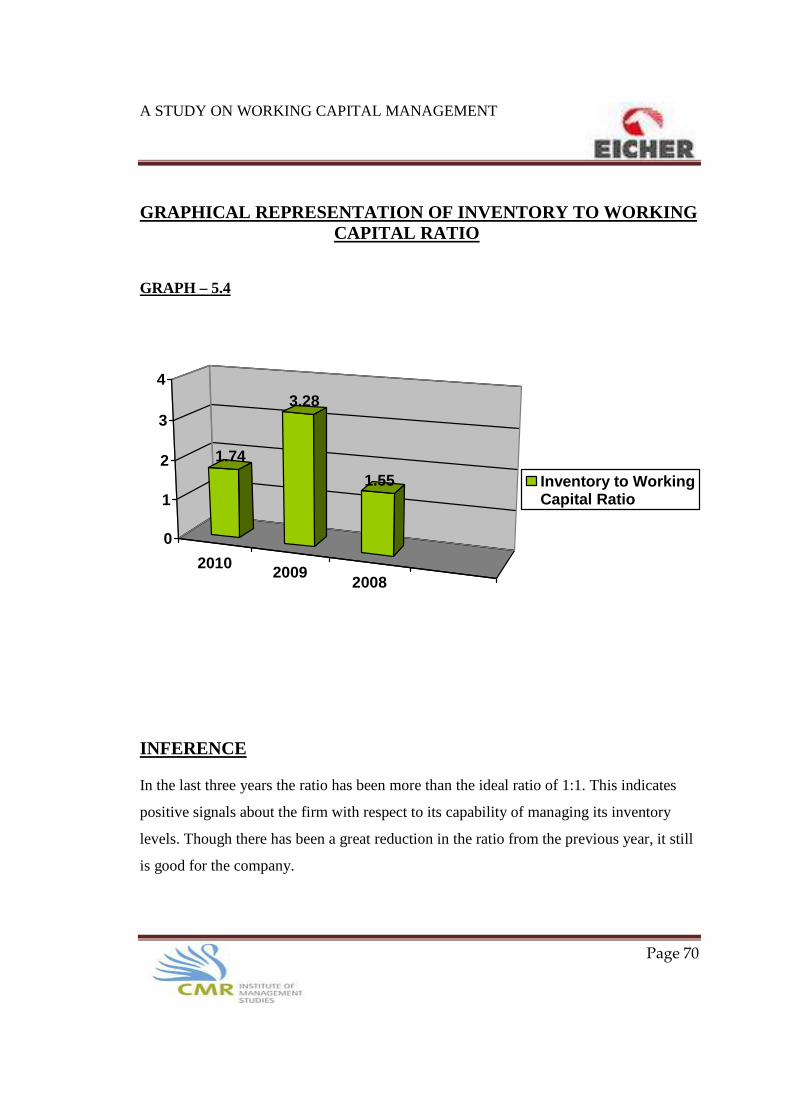

INVENTORY TO WORKING CAPITAL RATIO This ratio is calculated to prevent over stocking. Increase in volume of sales results in

increase in size of inventories. But from a sound financial point of view, inventory should

not exceed amount of working capital.

Inventory to Working Capital Ratio = Inventories Net Working Capital TABLE REPRESENTING INVENTORY TO WORKING CAPITAL RATIO (Rs .In million) TABLE – 5.3

YEAR 2010 2009 2008

Inventories 1612.3 1612.5 1262.5

Net Working Capital 928 491.3 814.6

Inventory to Working Capital

Ratio 1.74 3.28 1.55

ANALYSIS It can be observed from the table and chart that the Inventory to Working Capital

Turnover Ratio for Eicher Motors was 1.55 in 2008, 3.28 in 2009 and 1.74 in 2010. The

inventory to stock turnover ratio has been increasing and decreasing alternatively

between the periods 2008 to 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 70

GRAPHICAL REPRESENTATION OF INVENTORY TO WORKING CAPITAL RATIO GRAPH – 5.4

20102009

2008

0

1

2

3

4

Inventory to WorkingCapital Ratio

1.74

3.28

1.55

INFERENCE In the last three years the ratio has been more than the ideal ratio of 1:1. This indicates

positive signals about the firm with respect to its capability of managing its inventory

levels. Though there has been a great reduction in the ratio from the previous year, it still

is good for the company.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 71

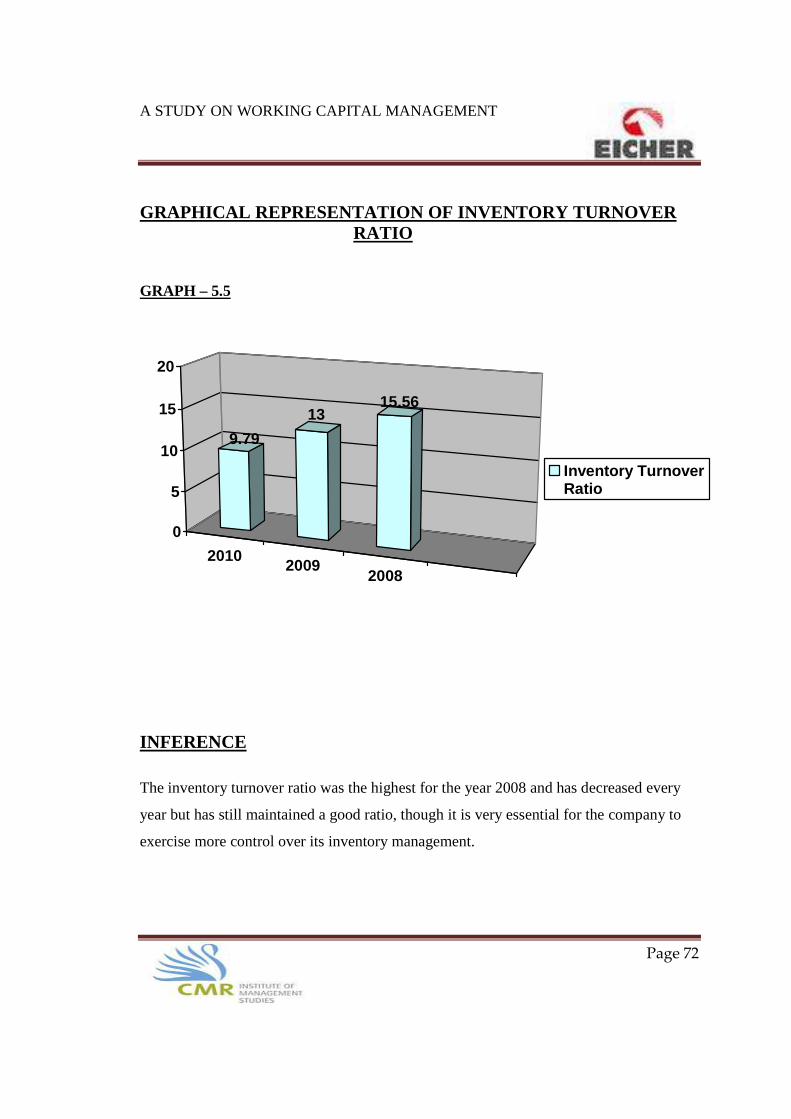

INVENTORY TURNOVER RATIO This ratio measures the number of times inventory is turned over during the year. High

inventory turnover can indicate a shortage of needed inventory for sales. Low inventory

turnover can indicate poor liquidity, possible overstocking and obsolescence or in

contrast to these negative interpretations, a planned inventory buildup in the case of

material shortages.

Inventory Turnover Ratio = Cost of Sales Inventory TABLE REPRESENTING INVENTORY TURNOVER RATIO (Rs.In millions) TABLE – 5.4

YEAR 2010 2009 2008

Cost of Goods Sold 15779.6 18684.8 12627.1

Average Stock 1612.4 1437.5 811.5

Inventory Turnover Ratio 9.79 13 15.56

ANALYSIS It can be observed from the table and the chart that the inventory turnover ratio for Eicher

Motors was 15.56 in 2008, 13 in 2009 and 9.79 in 2010. The inventory turnover ratio has

shown a decreasing trend for the period 2008 to 2010 which does not prove good for the

company.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 72

GRAPHICAL REPRESENTATION OF INVENTORY TURNOVER RATIO GRAPH – 5.5

20102009

2008

0

5

10

15

20

Inventory TurnoverRatio

9.79

1315.56

INFERENCE

The inventory turnover ratio was the highest for the year 2008 and has decreased every

year but has still maintained a good ratio, though it is very essential for the company to

exercise more control over its inventory management.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 73

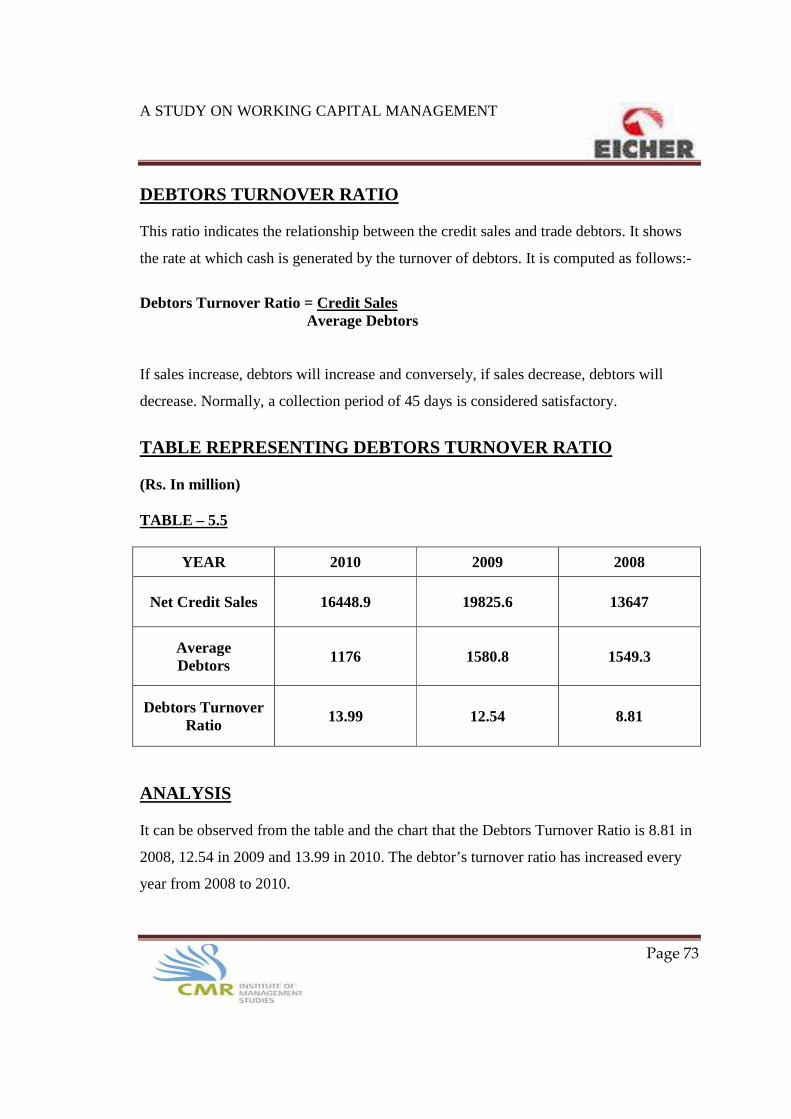

DEBTORS TURNOVER RATIO This ratio indicates the relationship between the credit sales and trade debtors. It shows

the rate at which cash is generated by the turnover of debtors. It is computed as follows:-

Debtors Turnover Ratio = Credit Sales Average Debtors If sales increase, debtors will increase and conversely, if sales decrease, debtors will

decrease. Normally, a collection period of 45 days is considered satisfactory.

TABLE REPRESENTING DEBTORS TURNOVER RATIO (Rs. In million) TABLE – 5.5

YEAR 2010 2009 2008

Net Credit Sales 16448.9 19825.6 13647

Average Debtors 1176 1580.8 1549.3

Debtors Turnover Ratio 13.99 12.54 8.81

ANALYSIS It can be observed from the table and the chart that the Debtors Turnover Ratio is 8.81 in

2008, 12.54 in 2009 and 13.99 in 2010. The debtor’s turnover ratio has increased every

year from 2008 to 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 74

GRAPHICAL REPRESENTATION OF DEBTORS TURNOVER RATIO GRAPH – 5.6

20102009

2008

02468

10

12

14

Debtors TurnoverRatio

13.99

12.54

8.81

INFERENCE

There is a big increase in Debtors Turnover Ratio in 2009 compared to 2008 and a steady

increase in 2010 as compared to 2009, which proves to be very effective. Thus it can be

seen that the management of debtors has been good for the company and has been

improving over the period of time.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 75

CREDITORS TURNOVER RATIO This ratio expresses the relationship between credit purchase and the liability as creditors.

It can be stated as the number of days the credit purchases are carried on in the books.

Credit Turnover Ratio = Credit Purchases Average Creditors Note that non-credit purchases (salaries) and non cash expenses (depreciation) need to be

excluded from the credit purchases and any provisions need to be excluded from

creditors.

There is no need to pay the creditors before payment is due. The department’s objective

should be to make effective use of this source of free credit, while maintaining a good

relationship with the creditors.

Credit purchases should not be carried on the books for more than an average of 45 days.

If payment is withheld within 60 days or more it is likely that the creditors will become

impatient and impose stricter and less convenient trading terms, for example, cash on

delivery, etc.

The public finance act 1989 (section 49) places a legal constraint on the amount of credit

allowed to a department. It restricts to a maximum of 90 days the purchase of goods and

services through the use of credit card or supplier’s credit.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 76

TABLE REPRESENTING CREDITORS TURNOVER RATIO (Rs. In million) TABLE – 5.6

YEAR 2010 2009 2008

Credit Purchases 12662.8 14924.8 9585.3

Average Creditors 2350.5 2846 2446.3

Credit Turnover Ratio 4.87 5.64 5.77

ANALYSIS It can be observed from the table and the chart that the Creditors Turnover Ratio for

Eicher Motors was 5.77 in 2008, 5.64 in 2009 and 4.87 in 2010. The credit turnover ratio

has been showing a decreasing trend for the time period between 2008 – 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 77

GRAPHICAL REPRESENTATION OF CREDIT TURNOVER RATIO GRAPH – 5.7

20102009

2008

4

4.5

5

5.5

6

Credit Turnover Ratio

4.87

5.64 5.77

INFERENCE

There has been a steady decrease in the Creditors Turnover Ratio in the period

2008 – 2010 which is not quite good for the company. Thus it is seen that the

management has not been improving the company for the year 2008 – 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 78

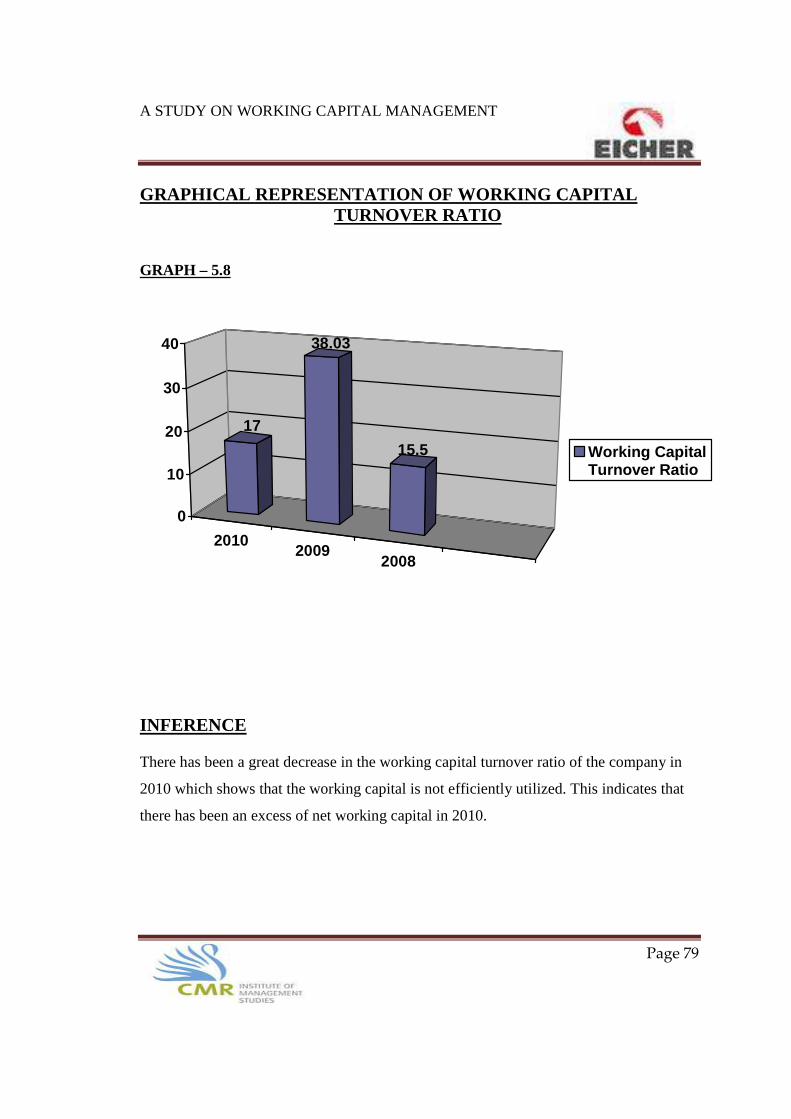

WORKING CAPITAL TURNOVER RATIO This ratio indicates the efficiency or inefficiency in the utilization of working capital in

making sales. A high working capital turnover ratio shows the effective utilization of

working capital in generating sales. A low ratio, on the other hand, may indicate excess

of net working capital. This ratio, thus, shows whether the working capital is efficiently

utilized or not.

Working Capital Turnover Ratio = Cost of Sales Net Working Capital TABLE REPRESENTING WORKING CAPITAL TURNOVER RATIO (Rs. In million) TABLE – 5.7

YEAR 2010 2009 2008

Cost of Goods Sold 15779.6 18684.8 12627.1

Net Working Capital 928 491.3 814.6

Working Capital Turnover Ratio 17 38.03 15.5

ANALYSIS It can be observed from the table and the chart that the Working Capital Turnover Ratio

was 15.5 in 2008, 38.03 in 2009 and 17 in the year 2010. The working capital turnover

ratio has shown an increasing and decreasing trend over the period between 2008 and

2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 79

GRAPHICAL REPRESENTATION OF WORKING CAPITAL TURNOVER RATIO GRAPH – 5.8

20102009

2008

0

10

20

30

40

Working CapitalTurnover Ratio

17

38.03

15.5

INFERENCE There has been a great decrease in the working capital turnover ratio of the company in

2010 which shows that the working capital is not efficiently utilized. This indicates that

there has been an excess of net working capital in 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 80

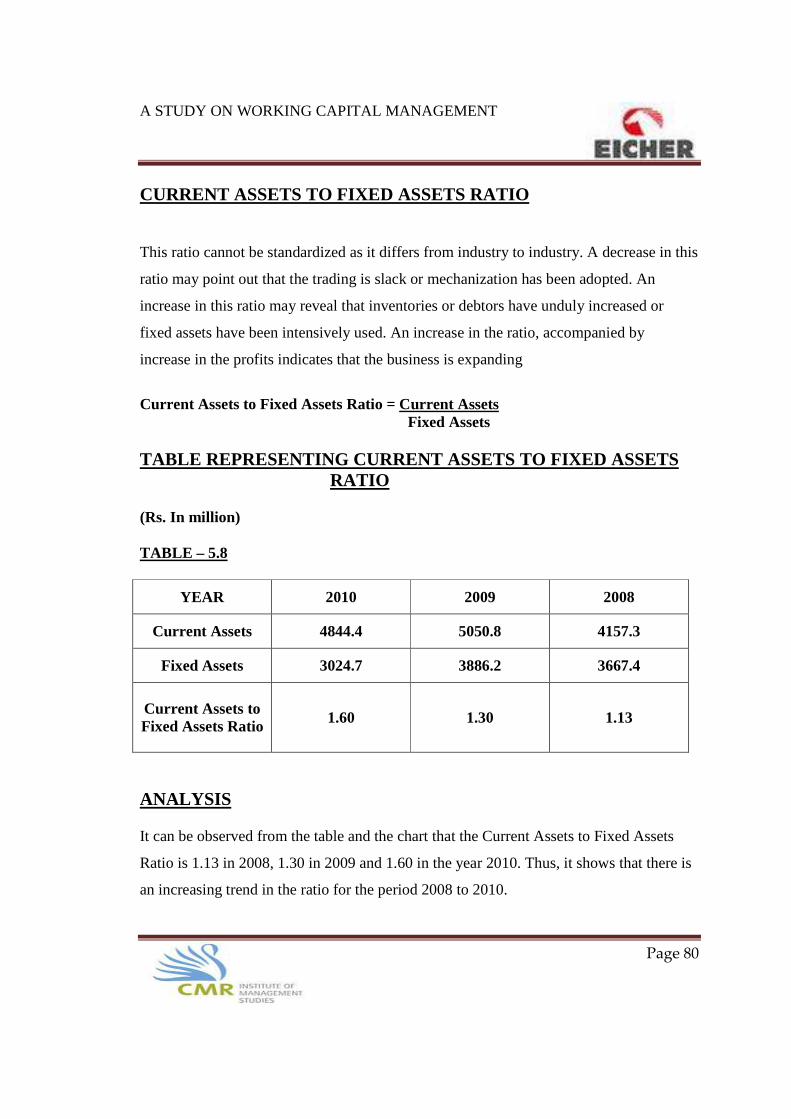

CURRENT ASSETS TO FIXED ASSETS RATIO This ratio cannot be standardized as it differs from industry to industry. A decrease in this

ratio may point out that the trading is slack or mechanization has been adopted. An

increase in this ratio may reveal that inventories or debtors have unduly increased or

fixed assets have been intensively used. An increase in the ratio, accompanied by

increase in the profits indicates that the business is expanding

Current Assets to Fixed Assets Ratio = Current Assets Fixed Assets TABLE REPRESENTING CURRENT ASSETS TO FIXED ASSETS RATIO (Rs. In million) TABLE – 5.8

YEAR 2010 2009 2008

Current Assets 4844.4 5050.8 4157.3

Fixed Assets 3024.7 3886.2 3667.4

Current Assets to Fixed Assets Ratio 1.60 1.30 1.13

ANALYSIS It can be observed from the table and the chart that the Current Assets to Fixed Assets

Ratio is 1.13 in 2008, 1.30 in 2009 and 1.60 in the year 2010. Thus, it shows that there is

an increasing trend in the ratio for the period 2008 to 2010.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 81

GRAPHICAL REPRESENTATION OF CURRENT ASSETS TO FIXED ASSETS RATIO GRAPH – 5.9

20102009

2008

0

0.5

1

1.5

2

Current Assets to FixedAssets Ratio

1.6

1.31.13

INFERENCE The ratio has been on a continuous uptrend over the past three years indicating that there

is a continuous increase in current assets but not proportionate increase in fixed assets.

This indicates that the firm has used its funds more towards carrying out its day-to-day

operations and not so much on its fixed assets.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 82

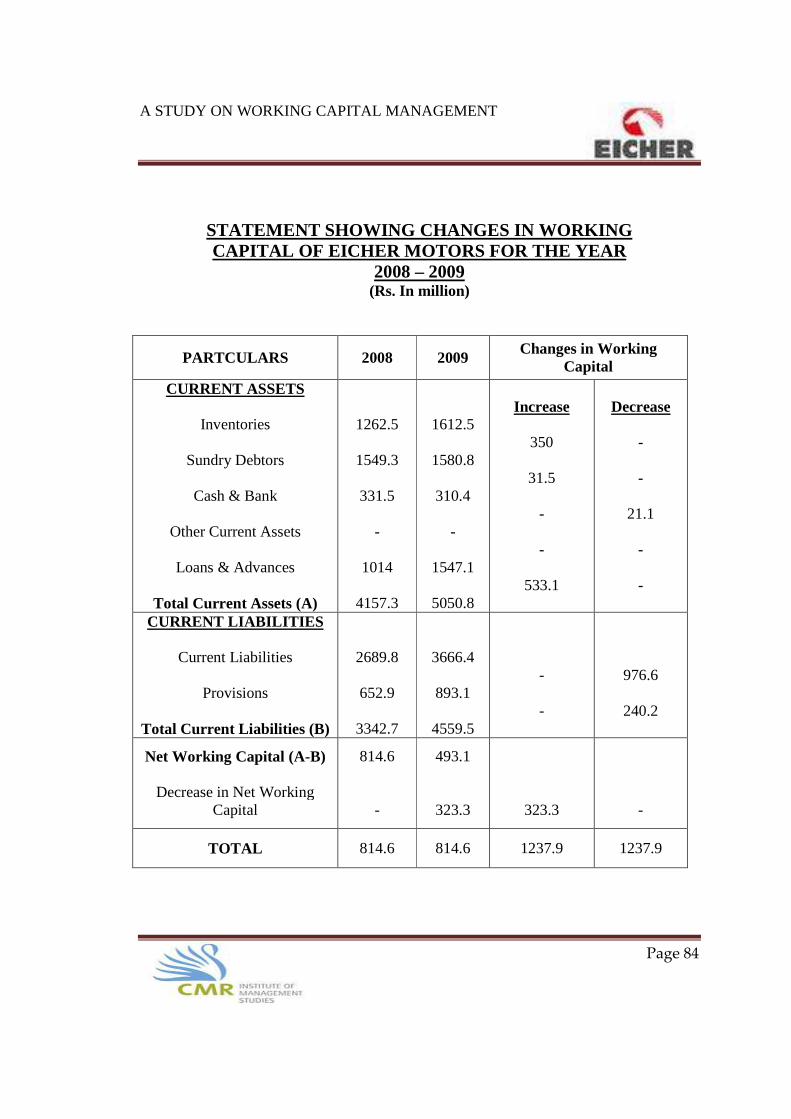

STATEMENT SHOWING CHANGES IN WORKING CAPITAL OF EICHER MOTORS FOR THE YEAR

2009 – 2010 (Rs. In millions)

PARTCULARS 2009 2010 Changes in Working

Capital CURRENT ASSETS

Inventories

Sundry Debtors

Cash & Bank

Other Current Assets

Loans & Advances

Total Current Assets (A)

1612.5

1580.8

310.4 -

1547.1

5050.8

1612.3

1176

261

77

1718.1

4844.4

Increase - - -

77

171

Decrease

0.2

404.8

49.4 - -

CURRENT LIABILITIES

Current Liabilities

Provisions

Total Current Liabilities (B)

3666.4

893.1

4559.5

2902.3

1014.1

3916.4

764.1 -

-

121

Net Working Capital (A-B)

Increase in Net Working Capital

491.3

436.7

928 -

-

436.7

TOTAL 928 928 1012.1 1012.1

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 83

ANALYSIS

It can be observed from the table that Net Working Capital was 491.3 million in 2009 and

928 in 2010. Thus there has been an increase in the Net Working Capital of 436.7 in 2010

compared to 2009. This is good for the company as it has more surplus funds for carrying

out its operations and it can invest its surplus funds for new operations.

INFERENCE From the table it can be observed that the debtors balance has decreased which is good

for the company as it shows that it is able to get all its payment on time. Cash & Bank

balance has decreased which is again good for the company as it shows that the cash is

not being kept idle. Loans and Advances have increased which also proves to be good as

extra cash has been utilized and since it bears interest, it adds to extra revenue to the

company. Current Liabilities have decreased which is good for the company as it shows

that the company pays its dues on time, thus, enhancing the goodwill of the company.

A STUDY ON WORKING CAPITAL MANAGEMENT

Page 84

STATEMENT SHOWING CHANGES IN WORKING CAPITAL OF EICHER MOTORS FOR THE YEAR

2008 – 2009 (Rs. In million)

PARTCULARS 2008 2009 Changes in Working

Capital CURRENT ASSETS

Inventories

Sundry Debtors

Cash & Bank

Other Current Assets

Loans & Advances

Total Current Assets (A)

1262.5

1549.3

331.5 -

1014

4157.3

1612.5

1580.8

310.4 -

1547.1

5050.8

Increase

350

31.5 - -

533.1

Decrease - -

21.1 - -

CURRENT LIABILITIES

Current Liabilities

Provisions

Total Current Liabilities (B)