Embed Size (px)

Citation preview

A STUDY ON THE GROWTH OF FINANCIAL DERIVATIVES IN

INDIA

Dr.N. MOSES 1 PROF. B. PHANISWARA RAJU

2

1 Teaching Assistant, Department of Commerce, Rayalaseema University, Kurnool-518002, AP

2 HOD, Department of Commerce, Sri Krishnadevaraya University, Anantapuramu, AP

ABSTRACT

Integration of economies world over has brought in multiple growth in the volume of

international trade and business. This in turn has led to increase in the demand for international money

and need for innovative financial instruments both at national and global level. Changes in the interest

rates, exchange rates and equity prices in different financial markets led to increase in the volatility

and manifold increase in the financial risk to the individual as well as institutional investors. Adverse

changes in these variables have even threatened the very survival of the business world. To manage

these risks, new financial instruments have been developed in the financial market, which are

popularly known as Financial Derivatives. In this paper more emphasis is given the growth and

development of financial derivatives in India in terms of turnover and number of contracts traded in

derivatives segment of two premier stock exchanges in India namely NSE and BSE

Keywords: Financial Derivative, Index Future, Index Options, Stock Options, Stock Futures

INTRODUCTION

As the name indicates, derivatives are the imitative financial products, which derive their value from

some other assets called ‗underlying‘. These are believed to be the effective tools of risk-

management. The basic purpose of Financial Derivatives is to provide commitments to prices for

future dates for giving protection against adverse movements in the future prices of underlying assets

thereby reduce/manage/control the extent of financial risk. Derivatives allow investors to establish, at

low cost, return distributions that matchup with their levels of risk aversion. Derivative instruments

are different from Insurance, in that they cover general risks whereas the latter covers specific risks.

Financial Derivatives also provide an opportunity to earn profit for those persons who have higher

risk appetite. These instruments indeed facilitate to transfer the risk from those who wish to avoid it to

those who are willing to accept the same. In the stock market, derivative instruments have emerged as

the most important speculative vehicles and as risk management tools. These products are also used

by risk-taking investors for availing arbitrage and speculative opportunities. Such uses of derivative

products are believed to be helpful in building of a strong relationship between the cash and derivative

market segments leading to more efficient price-discovery in both the markets. It is also believed that

introduction of derivative products increase liquidity in the market. Derivative market segment is

dominated by informed institutional investors and therefore, this market segment is expected to be

more efficient in price discovery. Many researchers have proposed the hypothesis that derivative

markets lead the price movements in cash segment. Financial derivatives have become increasingly

popular and most commonly used in the world of finance. The rate of growth of derivatives is so

phenomenal all over the world that now it is called as the derivatives revolution.

The Security and Exchange Board of India (SEBI) permitted the trading on index futures on May 25,

2000. The trading of BSE Sensex futures commenced at Bombay Stock Exchange (BSE) on June 9,

2000 and on June 12, 2000 trading of Nifty-futures commenced at National Stock Exchange (NSE). In

the June 2001 index options and in July 2001 stock options were introduced. Futures on individual

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 54 [email protected]

stocks were introduced in November 2001. In fact, stock-futures were introduced in India well before

their introduction in the USA and many other developed markets. The volume of trading in derivative

segment, particularly in stock-futures, took momentum quit rapidly. At NSE trading volume of

derivatives has exceeded the volume of cash segment. According to an estimate recorded in the NSE

Fact Book, the present annual trading turnover of derivative market has reached . 55,606,453 Cr for

the year 2014-15.

Concept of Derivatives

The term ‗derivatives, refers to a broad class of financial instruments which mainly include options

and futures. These instruments derive their value from the price and other related variables of the

underlying asset. They do not have worth of their own and derive their value from the claim they give

to their owners to own some other financial assets or security. A simple example of derivative is

butter, which is derivative of milk. The price of butter depends upon price of milk, which in turn

depends upon the demand and supply of milk. The general definition of derivatives means to derive

something from something else. Some other meanings of word derivatives are:

A. derived function: the result of mathematical differentiation; the instantaneous change of one

quantity relative to another; df(x)/dx,

B. derivative instrument: a financial instrument whose value is based on another security,

(linguistics) a word that is derived from another word; "`electricity' is a derivative of

‗electric‘.

The asset underlying a derivative may be commodity or a financial asset. Derivatives are those

financial instruments that derive their value from the other assets. For example, the price of gold to be

delivered after two months will depend, among so many things, on the present and expected price of

this commodity.

Definition of Financial Derivatives

Section 2(ac) of Securities Contract Regulation Act (SCRA) 1956 defines Derivative as:

A. ―a security derived from a debt instrument, share, loan whether secured or unsecured, risk

instrument or contract for differences or any other form of security;

B. ―a contract which derives its value from the prices, or index of prices, of underlying

securities‖.

Review of Literature

Gulen and Mayhew1 (2000) examine stock market volatility before and after the introduction of

index futures trading in twenty-five countries, using various GARCH models They found that futures

trading is related to an increase in conditional volatility in the U.S. and Japan, but in nearly every

other country, no significant effect could be found. Joel Hasbrouck2 (2001) studied on intraday price

formation in US equity index markets. This study empirically investigated in the price discovery of

US equity index market in the new environment where the mirror of index with exchange traded

funds, electronically traded markets, small denomination futures contracts and a family of sector ETF

that break the index into nine components. Isakov and Morard3

(2001) in their paper have

investigated the performance of option strategies especially covered call strategy on Swiss exchange

during 1989-1996. They concluded that the use of option strategies consistently increase the

performance of stock portfolios even in the presence of transaction cost.

Gong-meng Chen, Michael Firth and Oliver Rui4 (2001) have examined the dynamic relationship

between returns, volume, and volatility for major nine national stock indexes for the period from 1973

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 55 [email protected]

to 2000. Their results show a positive correlation between trading volume and absolute value of stock

price change. The results of the study were found robust across all nine major stock markets, implying

that there are similar returns, trading volume, and volatility patterns across all markets under study.

Bhanupant5 (2001) investigated the dynamic relationship between stock index returns and trading

volume using the Augmented Dickey-Fuller (ADF), Linear and Non-Linear Granger Causality

hypothesis test on the National Stock Exchange (NSE) data. The period, when rolling settlement was

introduced, there found no evidence of linear causality in either direction. The shift in linear causal

relationship indicates that efficiency at NSE has improved with introduction of rolling settlement

mechanism.

Pilar and Rafael6 (2002), examined the effect of introduction of derivatives on the volatility and

trading volume of underlying Ibex-35 index by using GJR model and result that trading volume

increased significantly but conditional volatility decreased after introduction of derivatives. Varma7

(2002) examined the mispricing of volatility in the Indian index options market using closing Nifty

futures and options prices from June 2001 to February 2002. The result suggests that the Indian

market stands almost exactly half way between a naive market where the pricing completely ignores

the downside protection provided by options and a mature market where the pricing reflects a

reasonable theoretical model of the value of the downside protection. Nath Golaka C8 (2003), his

paper on ―Behaviour of Stock Market Volatility after Derivatives‖, examined the behaviour of

volatility in equity market in pre and post derivatives period in India using static and conditional

variance. It observed that for most of the stocks, the volatility had come down in the post derivative

period while for only few stocks in the sample, the volatility in the post derivatives has either stayed

more or less same or has increased marginally.

Mukherjee and Mishra’s9 (2006) study empirically investigated the usefulness and impact of two

non-price variables-open interest and trading volume from option market preceding the Nifty index in

underlying cash market in India. The empirical findings confirm that the open interest based

predictors are significant in predicting the spot price index in underlying cash market in both the

periods, just after the initiation of the index option in the market and in the later sub period. Gahlot

Ruchika, Datta Saroj and K. Kapil Sheeba10

(2010), have examined the impact of derivative

trading on stock market volatility by taking closing prices of S&P CNX Nifty as well as closing prices

of five derivative stocks and five non derivative stocks. The results showed mixed effect in case of 10

individual stocks.

Need for the study

From the review of literature, it can be observed that, researchers both in India and abroad

have carried out research studies covering various aspects of Financial Derivatives. However, the

present study is different from the above research studies in terms of both period and the sample

chosen. This study emphasis on the growth of financial derivatives in India, the NSE and the BSE are

selected as these exchanges are premier stock exchanges in India. The study is based mainly on

secondary data, which have been collected from websites of NSE, BSE and SEBI.

Methodology:-

To carry the study of the growth in Financial Derivatives in India the Cumulative Average Growth

Rate (CAGR) method has applied for the four products traded in both stock exchanges in India for

entire study period and also year to year growth rate also calculated. Financial Derivative market of

NSE is also compared with Cash market of NSE to know the detailed growth of NSE Financial

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 56 [email protected]

Derivative market. Instruments wise growth also carried out i.e. Index Futures, Index Options, Stock

Futures and Stock Options.

DATA ANALYSIS

Table 1 depicts the total number of derivative contracts traded and Table 2 depicts the turnover both

in NSE and BSE from 2000-01 to 2014-15. It could be observed that the total number of contracts

have registered 97.7 per cent growth during 2000-01 to 2014-15. From 1,67,315 contracts in 2000-01,

the number increased to 2,342,520,000 in 2014-15. As expected the growth rate in number of

contracts traded is more in NSE (103.07 per cent) compared to BSE (87.40 per cent). In terms of

absolute number of derivative contracts traded, BSE stands no-where near the NSE. While the number

in contracts traded BSE in 2000-01 was 76,735 representing a value of .1,653cr, which rose to

50,54,78,869 with a value of .20,362,741.25 cr only in 2014-15, that of the number in NSE rose from

90,850 representing a value of .2,265 cr in 2000-01 to 1,837,041,131 with a value of .55,606,453.39

cr in 2014-15. The number of derivatives contracts in these exchanges reached a milestone of

2,342,520,000 in 2015 since the inception of derivatives. These results are presented in Graph 1 and

Graph 2

Growth of Financial Derivatives in terms of No. of Contracts in NSE and BSE

Year NSE BSE Total

2000–01 90,580 (54.14) 76,735 (45.86) 1,67,315 (100)

2001-02 41,96,873 (97.55) 1,05,607 (2.45) 43,02,480 (100)

2002-03 1,67,68,909 (99.18) 1,38,037 (0.82) 1,69,06,946 (100)

2003-04 5,68,86,776 (99.33) 3,82,258 (0.67) 5,72,69,034 (100)

2004-05 7,70,17,185 (99.31) 5,31,719 (0.69) 7,75,48,904 (100)

2005-06 15,76,19,271 (99.9999) 203 (0.0001) 15,76,19,474 (100)

2006-07 21,68,83,573 (99.19) 17,81,670 (0.81) 21,86,65,243 (100)

2007-08 42,50,13,200 (98.28) 74,53,371 (1.72) 43,24,66,571 (100)

2008-09 65,73,90,497 (99.92) 4,96,502 (0.08) 65,78,86,999 (100)

2009-10 67,92,93,922 (99.999) 9028 (0.001) 679302950 (100)

2010-11 1,03,42,12,062 (99.999) 5,623(0.001) 1,03,42,17,685 (100)

2011-12 1,20,50,45,464 (97.40) 3,22,22,825 (2.60) 1,23,72,68,289 (100)

2012-13 1,13,14,67,418 (81.17) 26,24,59,311 (18.83) 1,39,39,26,729 (100)

2013-14 1,284,424,321 (80.97) 301,942,441 (19.03) 1,586,366,762 (100)

2014-15 1,837,041,131 (78.42) 505,478,869 (21.58) 2,342,520,000 (100)

CAGR 103.07 87.40 97.77

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 57 [email protected]

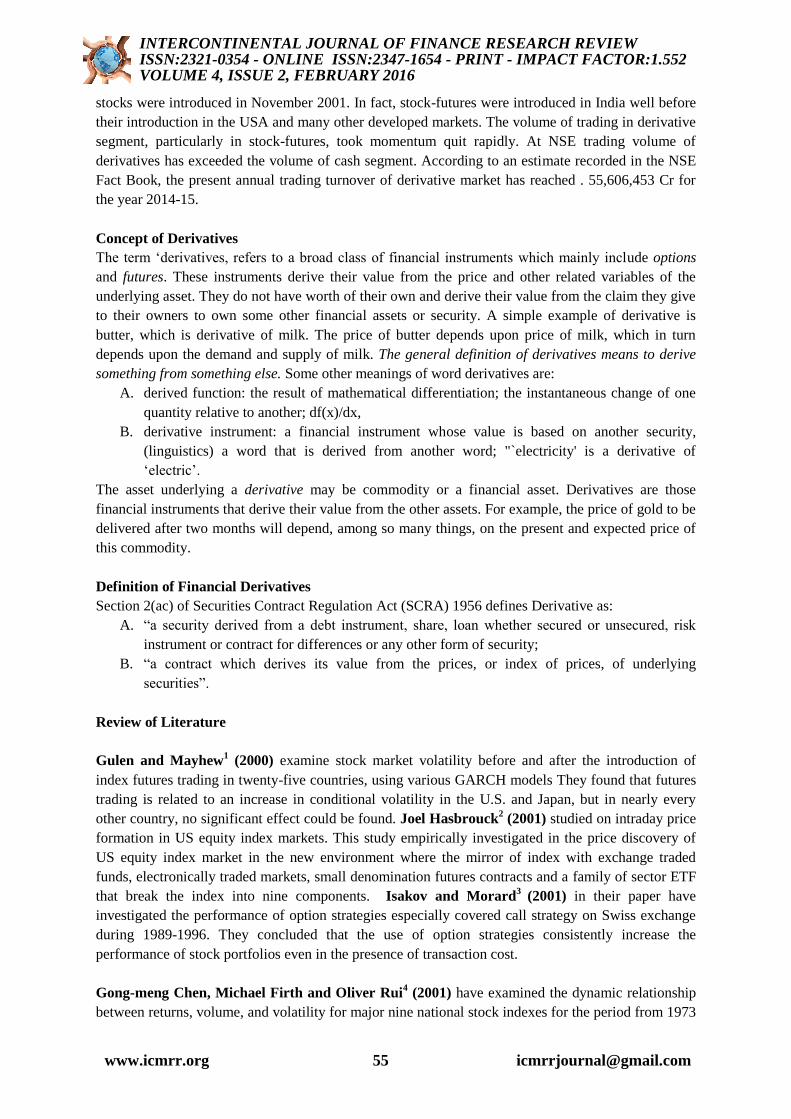

Table 2.2: Growth of Financial Derivatives in terms of Turnover ( in Cr) in NSE and BSE

Year NSE BSE Total

2000–01 2,365 (60.36) 1,653 (41.14) 4,018 (100)

2001-02 1,01,926 (98.15) 1,923 (1.85) 1,03,849 (100)

2002-03 4,39,862 (99.44) 2,479 (0.56) 4,42,341 (100)

2003-04 21,30,610 (99.46) 11,620 (0.54) 21,42,230(100)

2004-05 25,46,982 (99.33) 17,074 (0.67) 25,64,056 (100)

2005-06 48,24,174 (99.9998) 8.77 (0.0002) 48,24,183 (100)

2006-07 73,56,242 (99.20) 59,007 (0.80) 74,15,249 (100)

2007-08 1,30,90,478 (98.18) 2,42,308 (1.82) 1,33,32,786 (100)

2008-09 1,10,10,482 (99.89) 11,775 (0.11) 1,10,22,257 (100)

2009-10 1,76,63,665 (99.9987) 234.13 (0.0013) 1,76,63,899 (100)

2010-11 2,92,48,221 (99.9995) 154.00 (0.0005) 2,92,48,375 (100)

2011-12 3,13,49,732 (97.49) 8,08,477 (2.51) 3,21,58,209 (100)

2012-13 3,15,33,004 (81.49) 71,62,523 (18.51) 3,86,95,527 (100)

2013-14 38,211,408.05 (80.56) 9,219,434.42 (19.44) 47,430,842.47(100)

2014-15 55,606,453.39 (73.20) 20,362,741.25(26.80) 75,969,194.64 (100)

CAGR 105.23 95.97 102.06

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

Graph 2.1: Percentage of growth in NSE and BSE (No of contracts)

0

20

40

60

80

100

Rat

e o

f G

row

th

Time Period

Percentage of growth of No of Contract in NSE and BSE

NSE

BSE

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 58 [email protected]

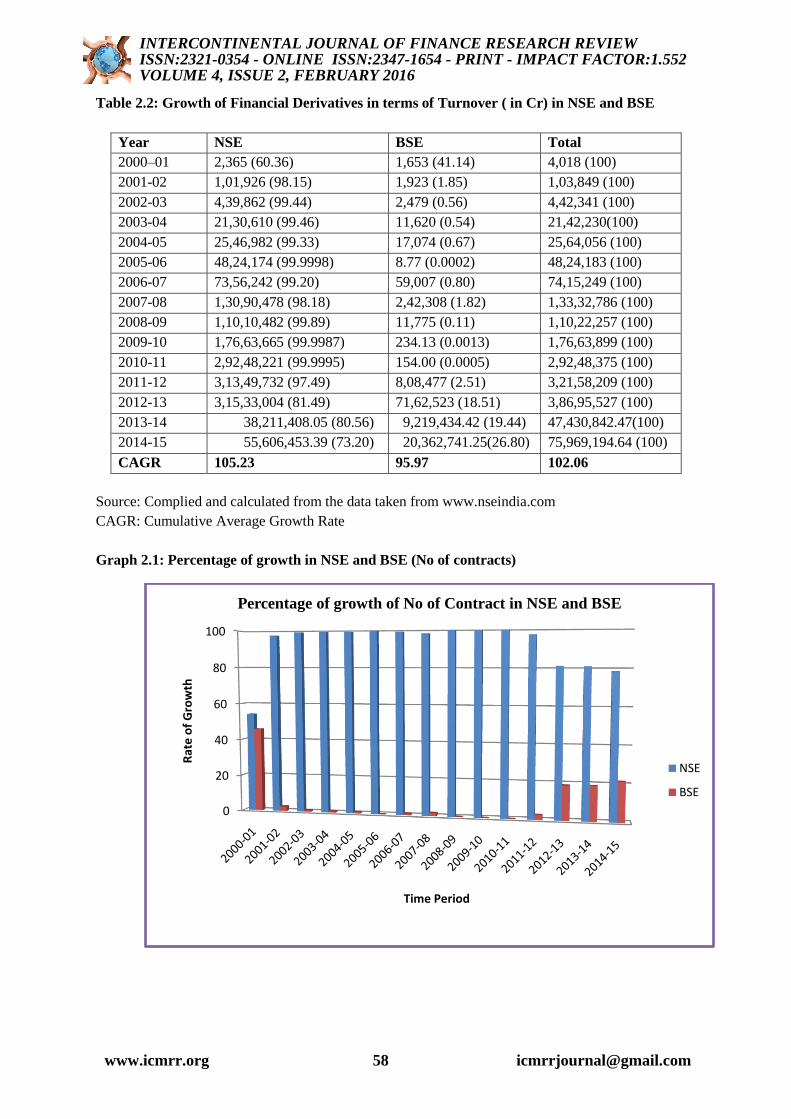

Graph 2.2: Percentage of growth of turnover (.in Cr) in NSE and BSE

Table 3 depicts the explosive growth of Derivative segment since their introduction in Indian

Capital Market in comparison with Cash segment. The share of Derivative segment, which was just

0.18 per cent of total turnover in 2000-2001, increased to 92.78 per cent by 2014-2015. On the other

hand the turnover of Cash segment, which was 99.82 per cent in the total turnover in 2000-2001

declined sharply to just 6.85 per cent. An important observation here is that the total turnover has

registered a substantial growth of 31.18 per cent over a period of 15 years, which could be mainly

attributed to the growth of turnover in derivatives, which has registered a growth of 105.23 per cent

during the same period. From the average daily turnover in both cash and derivative segments shown

the table, it is very clear that the daily average turnover registered many ups and downs in the cash

segment. From an average daily turnover of .5, 337 cr in 2000-01 it rose to .17, 818 cr by the end of

the year 2014-15. In other words, there is no-consistency in the average daily turnover in the cash

segment. On the other hand, there is a consistent increase in the average daily turnover registered in

derivative segment. From just .11cr in 2000-01 it increased to .2, 28,833 cr in 2014-15 and throughout

the study period of 15 years this has been continuously on increasing in trend except in 2008-09.This

shows the increasing interest and growing confidence of the market participants in Derivative

Instruments which helps in managing stock market risk to their advantage. These results are shown in

Graph 3

0

10

20

30

40

50

60

70

80

90

100

Ra

te o

f G

row

th

Time Period

Percentage of growth of turnover ( in Cr) in NSE and BSE

NSE

BSE

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 59 [email protected]

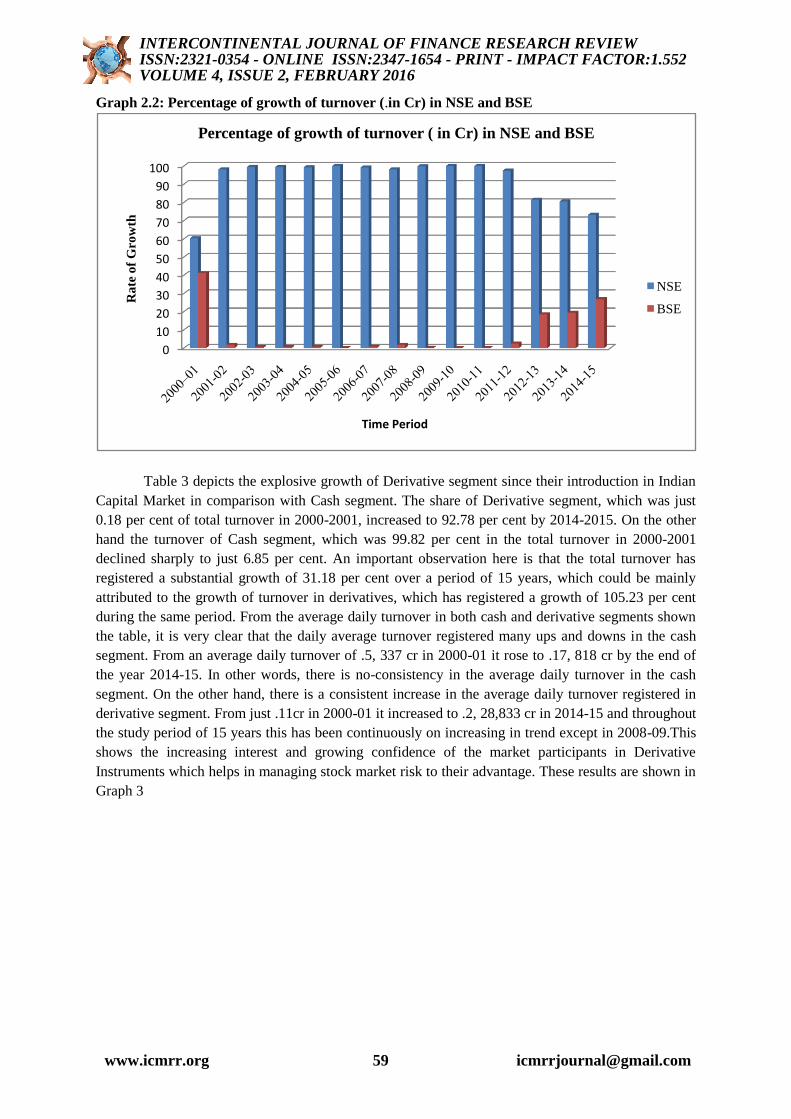

Table 2.3: Growth of Cash and Derivatives segments in terms of turnover (. in Cr) in NSE

Year

No. of

Trading

Days

Cash Derivatives

Total

(. in Cr) Yearly(. in Cr)

Daily

Average(.

in Cr)

Yearly(. in Cr)

Daily

Average(.

in Cr)

2000-01 204 13,39,510 (99.82) 5,337 2,365 (0.18) 11 13,41,875 (100)

2001-02 247 5,13,167 (83.43) 2,078 1,01,926 (16.57) 410 6,15,093 (100)

2002-03 251 6,17,989 (58.42) 2,462 4,39,862 (41.58) 1,752 10,57,851 (100)

2003-04 254 10,99,535 (34.04) 4,328 21,30,610 (65.96) 8,388 32,30,145 (100)

2004-05 253 11,40,071 (30.92) 4,506 25,46,982 (69.08) 10,107 36,87,053 (100)

2005-06 251 15,69,556 (24.55) 6,253 48,24,174 (75.45) 19,220 63,93,730 (100)

2006-07 249 19,45,285 (20.91) 7,812 73,56,242 (79.09) 29,543 93,01,527 (100)

2007-08 251 35,51,038 (21.34) 14,148 1,30,90,478 (78.66) 52,153 1,66,41,516 (100)

2008-09 243 27,52,023 (20) 11,325 1,10,10,482 (80) 45,311 1,37,62,505 (100)

2009-10 244 41,38,024 (18.98) 16,959 1,76,63,665 (81.02) 72,392 2,18,01,689 (100)

2010-11 255 35,77,412 (10.90) 14,048 2,92,48,221 (89.10) 1,15,150 3,28,25,633 (100)

2011-12 249 28,10,893 (8.23) 11,289 3,13,49,732 (91.77) 1,25,903 1,40,99,080 (100)

2012-13 250 27,08,279 (7.91) 10,833 3,15,33,004 (92.09) 1,26,639 3,42,41,283 (100)

2013-14 251 28,08,488 (6.85) 11,189 3,82,09,215 (93.15) 1,52,237 4,10,17,703 (100)

2014-15 243 43,29,655 (7.22) 17,818 5,56,04,197 (92.78) 2,28,833 5,99,33,852(100)

CAGR 8.74 105.23 31.18

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

Graph 3: Percentage of growth of turnover in Cash and Derivatives segments

Table 4 and 5 depicts the growth in number of contracts traded and turnover for the four

major derivative instruments which are also the instruments covered under the present study – Index

0

10

20

30

40

50

60

70

80

90

100

Rate

of

Gro

wth

Time Period

Growth of Cash and Derivatives marketsCash Turnover (₹. in Cr) Derivatives Turnover (₹. in Cr)

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 60 [email protected]

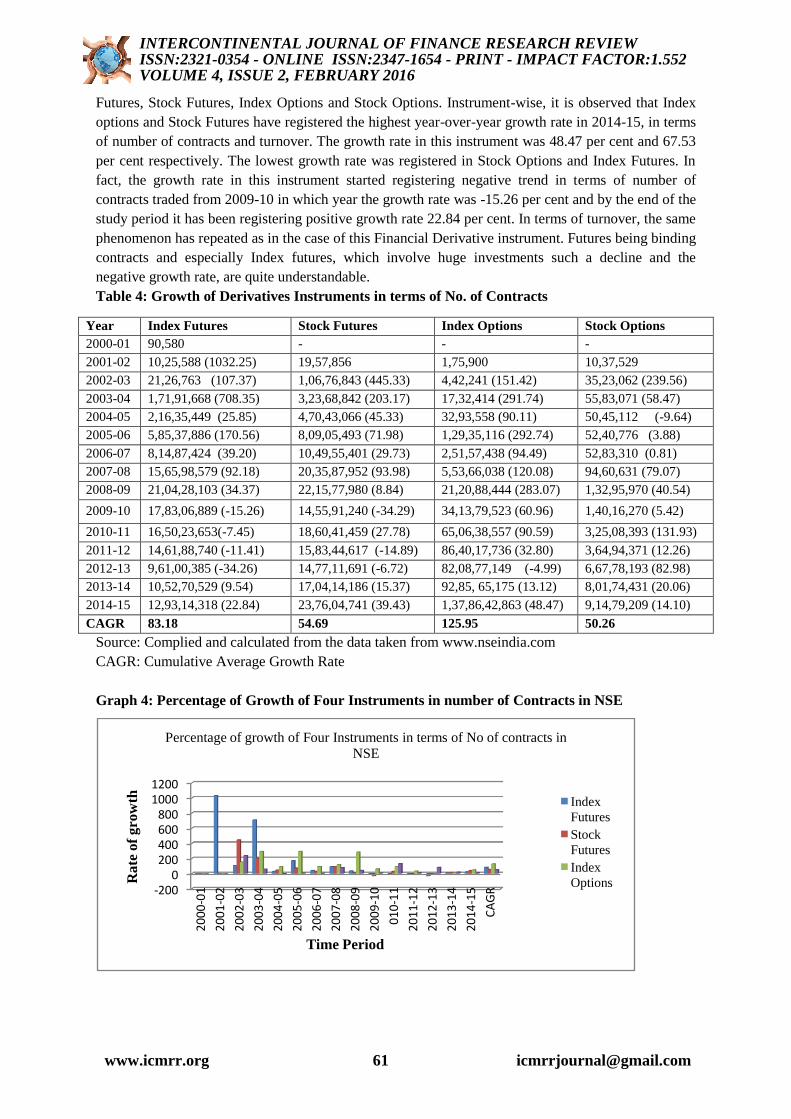

Futures, Stock Futures, Index Options and Stock Options. Instrument-wise, it is observed that Index

options and Stock Futures have registered the highest year-over-year growth rate in 2014-15, in terms

of number of contracts and turnover. The growth rate in this instrument was 48.47 per cent and 67.53

per cent respectively. The lowest growth rate was registered in Stock Options and Index Futures. In

fact, the growth rate in this instrument started registering negative trend in terms of number of

contracts traded from 2009-10 in which year the growth rate was -15.26 per cent and by the end of the

study period it has been registering positive growth rate 22.84 per cent. In terms of turnover, the same

phenomenon has repeated as in the case of this Financial Derivative instrument. Futures being binding

contracts and especially Index futures, which involve huge investments such a decline and the

negative growth rate, are quite understandable.

Table 4: Growth of Derivatives Instruments in terms of No. of Contracts

Year Index Futures Stock Futures Index Options Stock Options

2000-01 90,580 - - -

2001-02 10,25,588 (1032.25) 19,57,856 1,75,900 10,37,529

2002-03 21,26,763 (107.37) 1,06,76,843 (445.33) 4,42,241 (151.42) 35,23,062 (239.56)

2003-04 1,71,91,668 (708.35) 3,23,68,842 (203.17) 17,32,414 (291.74) 55,83,071 (58.47)

2004-05 2,16,35,449 (25.85) 4,70,43,066 (45.33) 32,93,558 (90.11) 50,45,112 (-9.64)

2005-06 5,85,37,886 (170.56) 8,09,05,493 (71.98) 1,29,35,116 (292.74) 52,40,776 (3.88)

2006-07 8,14,87,424 (39.20) 10,49,55,401 (29.73) 2,51,57,438 (94.49) 52,83,310 (0.81)

2007-08 15,65,98,579 (92.18) 20,35,87,952 (93.98) 5,53,66,038 (120.08) 94,60,631 (79.07)

2008-09 21,04,28,103 (34.37) 22,15,77,980 (8.84) 21,20,88,444 (283.07) 1,32,95,970 (40.54)

2009-10 17,83,06,889 (-15.26) 14,55,91,240 (-34.29) 34,13,79,523 (60.96) 1,40,16,270 (5.42)

2010-11 16,50,23,653(-7.45) 18,60,41,459 (27.78) 65,06,38,557 (90.59) 3,25,08,393 (131.93)

2011-12 14,61,88,740 (-11.41) 15,83,44,617 (-14.89) 86,40,17,736 (32.80) 3,64,94,371 (12.26)

2012-13 9,61,00,385 (-34.26) 14,77,11,691 (-6.72) 82,08,77,149 (-4.99) 6,67,78,193 (82.98)

2013-14 10,52,70,529 (9.54) 17,04,14,186 (15.37) 92,85, 65,175 (13.12) 8,01,74,431 (20.06)

2014-15 12,93,14,318 (22.84) 23,76,04,741 (39.43) 1,37,86,42,863 (48.47) 9,14,79,209 (14.10)

CAGR 83.18 54.69 125.95 50.26

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

Graph 4: Percentage of Growth of Four Instruments in number of Contracts in NSE

-2000

200400600800

10001200

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

01

0-1

1

20

11

-12

20

12

-13

20

13

-14

20

14

-15

CA

GR

Ra

te o

f g

row

th

Time Period

Percentage of growth of Four Instruments in terms of No of contracts in

NSE

Index

Futures

Stock

Futures

Index

Options

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 61 [email protected]

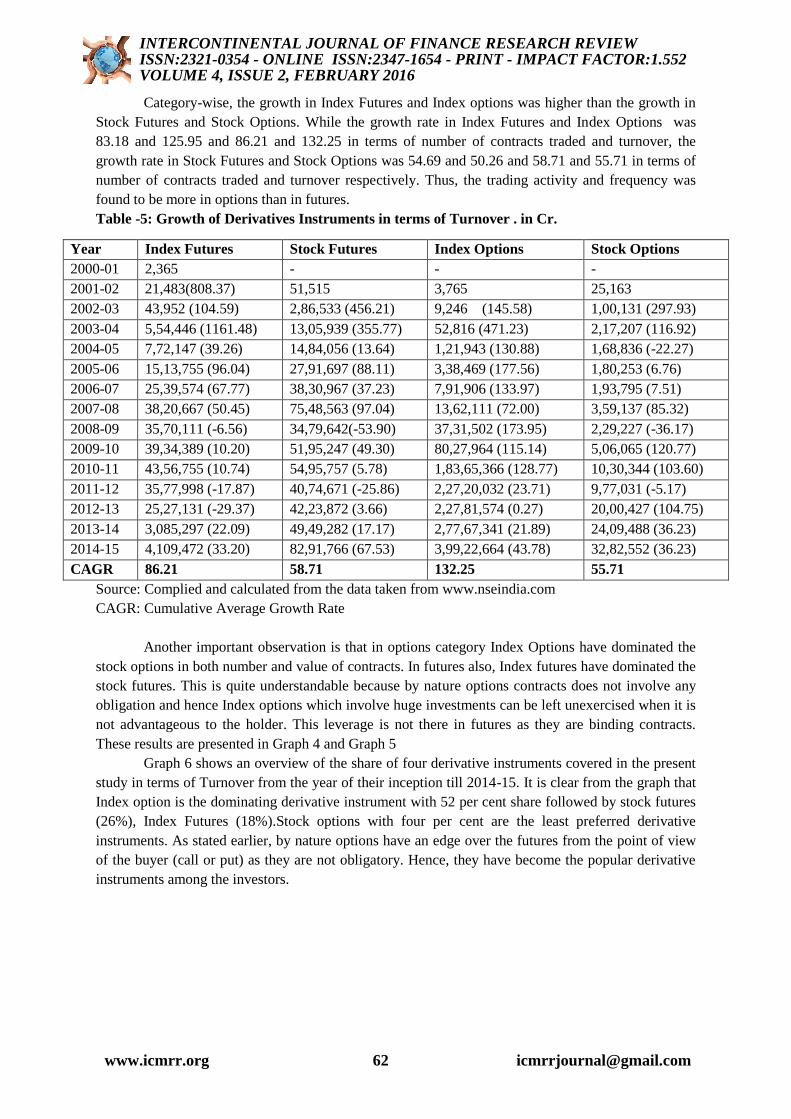

Category-wise, the growth in Index Futures and Index options was higher than the growth in

Stock Futures and Stock Options. While the growth rate in Index Futures and Index Options was

83.18 and 125.95 and 86.21 and 132.25 in terms of number of contracts traded and turnover, the

growth rate in Stock Futures and Stock Options was 54.69 and 50.26 and 58.71 and 55.71 in terms of

number of contracts traded and turnover respectively. Thus, the trading activity and frequency was

found to be more in options than in futures.

Table -5: Growth of Derivatives Instruments in terms of Turnover . in Cr.

Year Index Futures Stock Futures Index Options Stock Options

2000-01 2,365 - - -

2001-02 21,483(808.37) 51,515 3,765 25,163

2002-03 43,952 (104.59) 2,86,533 (456.21) 9,246 (145.58) 1,00,131 (297.93)

2003-04 5,54,446 (1161.48) 13,05,939 (355.77) 52,816 (471.23) 2,17,207 (116.92)

2004-05 7,72,147 (39.26) 14,84,056 (13.64) 1,21,943 (130.88) 1,68,836 (-22.27)

2005-06 15,13,755 (96.04) 27,91,697 (88.11) 3,38,469 (177.56) 1,80,253 (6.76)

2006-07 25,39,574 (67.77) 38,30,967 (37.23) 7,91,906 (133.97) 1,93,795 (7.51)

2007-08 38,20,667 (50.45) 75,48,563 (97.04) 13,62,111 (72.00) 3,59,137 (85.32)

2008-09 35,70,111 (-6.56) 34,79,642(-53.90) 37,31,502 (173.95) 2,29,227 (-36.17)

2009-10 39,34,389 (10.20) 51,95,247 (49.30) 80,27,964 (115.14) 5,06,065 (120.77)

2010-11 43,56,755 (10.74) 54,95,757 (5.78) 1,83,65,366 (128.77) 10,30,344 (103.60)

2011-12 35,77,998 (-17.87) 40,74,671 (-25.86) 2,27,20,032 (23.71) 9,77,031 (-5.17)

2012-13 25,27,131 (-29.37) 42,23,872 (3.66) 2,27,81,574 (0.27) 20,00,427 (104.75)

2013-14 3,085,297 (22.09) 49,49,282 (17.17) 2,77,67,341 (21.89) 24,09,488 (36.23)

2014-15 4,109,472 (33.20) 82,91,766 (67.53) 3,99,22,664 (43.78) 32,82,552 (36.23)

CAGR 86.21 58.71 132.25 55.71

Source: Complied and calculated from the data taken from www.nseindia.com

CAGR: Cumulative Average Growth Rate

Another important observation is that in options category Index Options have dominated the

stock options in both number and value of contracts. In futures also, Index futures have dominated the

stock futures. This is quite understandable because by nature options contracts does not involve any

obligation and hence Index options which involve huge investments can be left unexercised when it is

not advantageous to the holder. This leverage is not there in futures as they are binding contracts.

These results are presented in Graph 4 and Graph 5

Graph 6 shows an overview of the share of four derivative instruments covered in the present

study in terms of Turnover from the year of their inception till 2014-15. It is clear from the graph that

Index option is the dominating derivative instrument with 52 per cent share followed by stock futures

(26%), Index Futures (18%).Stock options with four per cent are the least preferred derivative

instruments. As stated earlier, by nature options have an edge over the futures from the point of view

of the buyer (call or put) as they are not obligatory. Hence, they have become the popular derivative

instruments among the investors.

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 62 [email protected]

Graph 5: Percentage of Growth of Four Instruments in terms of Turnover (. in Cr)

Graph 6: Share of Derivatives Instruments in Turnover (. in Cr.) over the years from 2000-01 to

2012-13

.

Source:compiledfrom the data taken from www.nseindia.com

THE MAJOR FINDINGS

It is observed that though the BSE and the NSE started derivative trading during the same

year i.e. 2000-01, NSE has over taken BSE in terms of number of contracts traded and the turnover.

-200

0

200

400

600

800

1000

12002

00

0-0

1

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

20

09

-10

01

0-1

1

20

11

-12

20

12

-13

20

13

-14

20

14

-15

CA

GR

Rat

e o

f gr

ow

th

Time Period

Percentage of growth of Four Instruments in terms of No of

contracts in NSE

Index Futures

Stock Futures

Index Options

Stock Options

Index Futures14%

Stock Futures22%

Index Options59%

Stock Options5%

Share of Derivatives Instruments in Turnover (₹ in Cr.) over the years

from 2000-01 to 2014-15

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 63 [email protected]

The number of contracts registered in BSE in 2000-01 was 76,735 with a value of .1,653 cr and in

NSE, it was 90,580 with a value of 2,365 cr respectively. In the initial year of introduction of

derivatives, BSE had 45.86 per cent and NSE had 54.14 per cent share. By the year 2014-15, NSE

captured more than 78 per cent share of total derivative market both in terms of absolute number of

derivative contracts traded and volume. BSE with a volume of 505,478,869 contracts stands no-where

near the NSE‘s volume of 1,837,041,131 contracts. The Derivative segment of NSE registered

explosive growth since their inception compared with the Cash market. The share of Derivative

segment, which was just 0.18 per cent in NSE‘s total turnover in 2000-01 increased to 92.78 per cent

by 2014-15. It is also observed that there is no consistency in the average daily turnover in cash

segment. But, there is a consistent increase in the average daily turnover registered in derivative

segment. This shows that there is an increasing interest and growing confidence of the market

participants in Derivative instruments, which helps in managing stock market risk to their advantage.

This study revealed that Index Options dominate the derivative markets in India with 132.25 per cent

of total turnover from 2000-01 to 2014-15 followed by Index Futures. The CAGR of Index Options

registered 125.95 per cent and 132.25 per cent in terms of number of contracts and turnover

respectively. An important observation is that in the Options category, Index Options have dominated

the Stock Options both in number and value of contracts. In Futures also, Index futures have

dominated the stock Futures. This is quite understandable because by nature option contracts does not

involve any obligation and hence Index Options, which involve huge investments can be left

unexercised when it is not advantageous to the holder.

CONCLUSION

On the basis of above discussion and data analysis, it is clear that the Financial Derivatives are rapidly

growing financial instruments. The comparison between the turnover, traded quantity of Financial

Derivatives market and Cash market also have also shown the tremendous growth in these

instruments. In other word, it is clearly evident that the Financial Derivative instruments have gained

the interests of public within short period as no instrument in financial world gained so far.

Reference:-

1. Gulen, H. and Mayhew, S. (2000): ―Stock Index Futures Trading and Volatility in International

Equity Markets,‖ The Journal of Futures Markets, Vol. 20, No. 7, 661-685.

2. Joel Hasbrouck (2001), Intraday price formation in US &equity index markets, Working Papers

Series, ssrn.com, pp.1-28.

3. Isakov, D. and Morard, B., (2001), Improving portfolio performance with option strategies:

Evidence from Switzerland, European Financial Management, Vol 7, no 1, March 2001, pp. 73-

91

4. Gong-Meng Chen et.al (2001), ―The Dynamic Relation between Stock Returns, Trading Volume

and Volatility‖, The Financial Review, 38 Pp: 153 - 1174.

5. Bhanupant (2001), "Testing Dynamic Relationship between Returns and Trading Volume on the

National Stock Exchange", http://www.nseindia.com/ content/research/res_paper_final226.pdf

6. Pilar Corredor and Santamaria Rafael (2002), ―Does derivatives trading destabilize the

underlying assets? Evidence from the Spanish stock market‖, Applied Economics Letters, 9, 107-

110

7. Varma, J.R. (2002), ―Mispricing of volatility in the Indian Index options market‖, Working paper

No.2002-04-01, IIM-A, Ahmedabad.

8. Golaka C Nath (2003), ―Behaviour of Stock Market Volatility after Derivatives‖, NSE Working

Paper, http://www.nse-india.com/content/press/ nov2003a.pdf

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 64 [email protected]

9. Mukherjee, K.N and Mishra, R.K. (2006), ―Lead-Lag Relationship between Equities and Stock

Index Futures Market and its Variation around Information Release: Empirical Evidence from

India‖. www.nseindia.com

10. Ruchika Gahlot, Saroj K. Datta and Sheeba Kapil (2010), Impact of Derivative Trading On Stock

Market Volatility in India: A Study of S&P CNX Nifty, Eurasian Journal of Business and

Economics 2010, 3 (6), 139-149.

INTERCONTINENTAL JOURNAL OF FINANCE RESEARCH REVIEWISSN:2321-0354 - ONLINE ISSN:2347-1654 - PRINT - IMPACT FACTOR:1.552VOLUME 4, ISSUE 2, FEBRUARY 2016

www.icmrr.org 65 [email protected]