Embed Size (px)

Citation preview

In This IssueTourism looks to the future

page 1

“A new beginning,”Dr. Seiji Naya

page 2

Measuring the economicimpact of tourism

page 5

Tourism initiatives and issues – theHTA tourism plan

page 9

The emerging cruise ship marketpage 12

Developing the niche marketspage 15

Is the convention centerpaying its way?

page 18

Air service to Hawaii –seats, comfort and cost

page 21

State and countydata tables

pages 23 & 24

Hawaii’s Economyis published by the Department of Business,

Economic Development & Tourism; Research &Economic Analysis Division

BENJAMIN J. CAYETANOGovernor

SEIJI F. NAYADirector

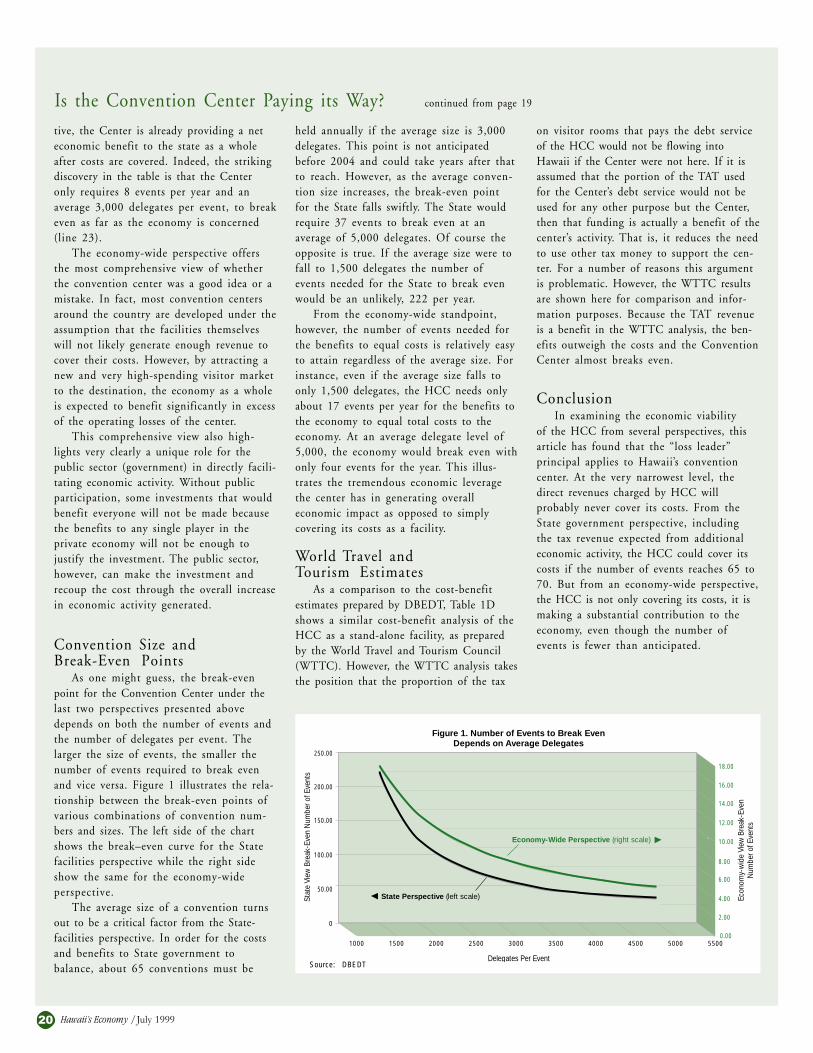

BRADLEY J. MOSSMANDeputy Director

PEARL IMADA IBOSHIDivision Head

ROBERT SHOREEditor

Direct Inquiries to:Hawaii’s Economy

DBEDTP.O. Box 2359

Honolulu, Hawaii 96804Fax: (808) 586-8449

E-mail: [email protected] report is also available on the internet at:

http://www.hawaii.gov/dbedt/hecon.html

1Hawaii’s Economy /July 1999

EC NOMYA Report from the Department of Business, Economic Development & Tourism

HAWAII’S July 1999

Tourism Looks tothe Future

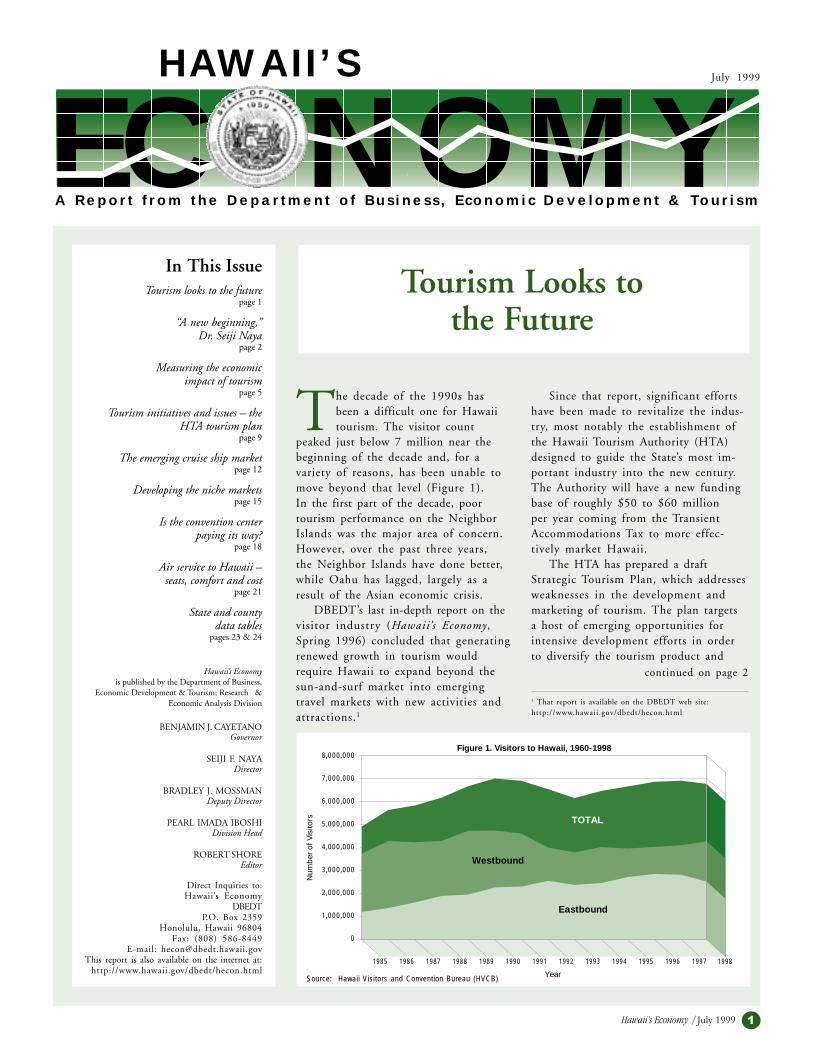

The decade of the 1990s hasbeen a difficult one for Hawaiitourism. The visitor count

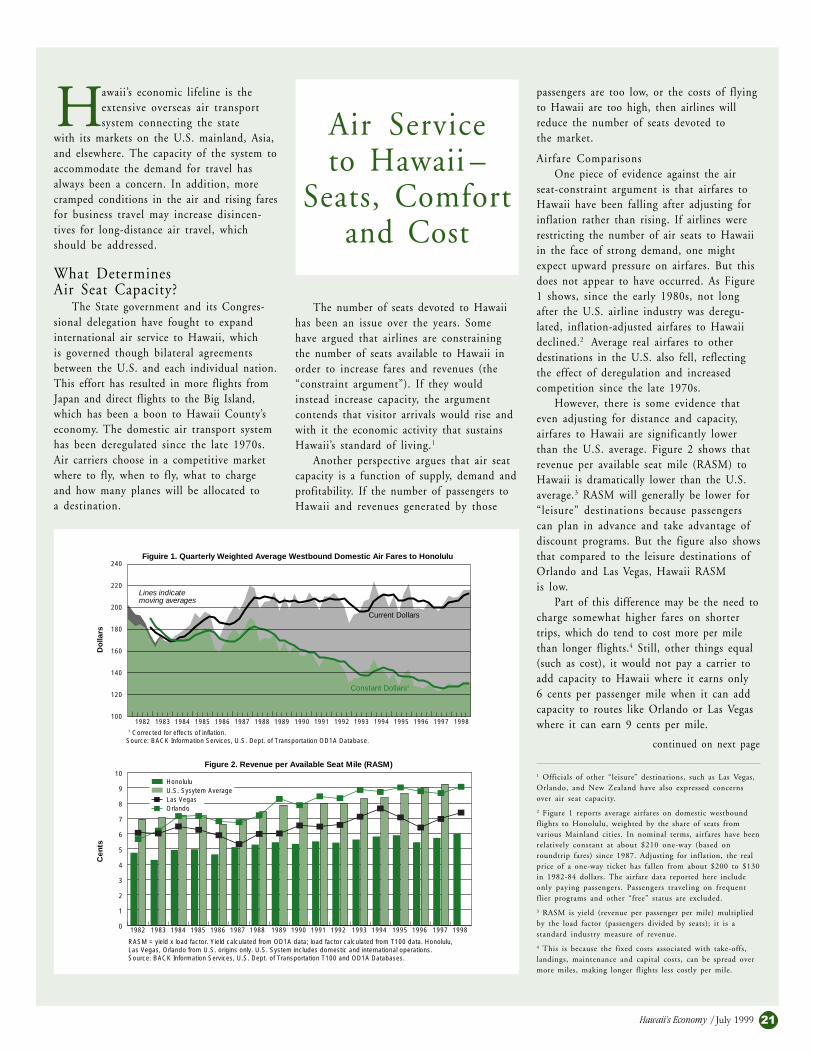

peaked just below 7 million near thebeginning of the decade and, for avariety of reasons, has been unable tomove beyond that level (Figure 1).In the first part of the decade, poortourism performance on the NeighborIslands was the major area of concern.However, over the past three years,the Neighbor Islands have done better,while Oahu has lagged, largely as aresult of the Asian economic crisis.

DBEDT’s last in-depth report on thevisitor industry (Hawaii’s Economy,Spring 1996) concluded that generatingrenewed growth in tourism wouldrequire Hawaii to expand beyond thesun-and-surf market into emergingtravel markets with new activities andattractions.1

continued on page 2

Since that report, significant effortshave been made to revitalize the indus-try, most notably the establishment ofthe Hawaii Tourism Authority (HTA)designed to guide the State’s most im-portant industry into the new century.The Authority will have a new fundingbase of roughly $50 to $60 millionper year coming from the TransientAccommodations Tax to more effec-tively market Hawaii.

The HTA has prepared a draftStrategic Tourism Plan, which addressesweaknesses in the development andmarketing of tourism. The plan targetsa host of emerging opportunities forintensive development efforts in orderto diversify the tourism product and

8,000,000

7,000,000

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

1985

Figure 1. Visitors to Hawaii, 1960-1998

Num

ber

of V

isito

rs

Year

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

TOTAL

Westbound

Eastbound

1 That report is available on the DBEDT web site:http://www.hawaii.gov/dbedt/hecon.html

Source: Hawaii Visitors and Convention Bureau (HVCB)

2 Hawaii’s Economy /July 1999

Tourism Looks to the Futurecontinued from page 1

strengthen Hawaii as a top competitor intourism worldwide.

This report updates the situation intourism, including the strategies pro-posed by the Tourism Strategic Plan toaddress the situation and move forward.The report also presents new estimates oftourism’s economic impact on the statebased on DBEDT’s newly revised HawaiiInput-Output Model. Other sections dis-cuss a number of tourism topics of par-ticular interest, many of which paralleltopics addressed in the Tourism StrategicPlan. These include the emerging cruiseship segment, niche markets and airservice to Hawaii.

Long-term StructuralChange Continues

The formation of the HTA andcreation of the new funding source areefforts to address structural changes thatare impacting the industry and ultimatelythe entire state economy. At the root ofthat structural change, and the difficultiestourism has experienced in the 1990s,has been the long-term maturing of theindustry in Hawaii and the gradualslowing of its growth rate. As Figure 2illustrates, tourism growth slowed consis-tently from the mid-1950s through themid-1980s.

The slowing trend was interrupted bya temporary period of renewed growth inthe second half of the 1980s as the Japanmarket took off. This surge in tourismfrom Japan was the result of a sharpincrease in the value of the yen, coupledwith a policy by the Japanese govern-ment to lower its foreign trade surplusby encouraging foreign travel. This wasalso a period of very high investment inboth Hawaii and U.S. real estate bythe Japanese.

The long-term slowdown in visitorindustry growth resumed in the 1990s asfirst the U.S. economy and later theAsian economies experienced a series ofeconomic and financial crises. The long-term slowing of tourism appears to haveleveled out at one to two percent peryear, although arrivals actually declinedin 1998, due to the Asian crisis.

Reaching the bottom of the declininggrowth curve signals the end of the

Tourism – “A New Beginning”This update report on Hawaii’s visitor industry comes at a time of significant change

in tourism and the economy. About eight years ago Hawaii’s post-statehood boom period,

fueled by tourism, came to an abrupt end. Since then, both business and government have

been struggling to adjust to a new economic era. Companies in all industries are learning

to compete in a global marketplace by becoming more efficient and more relevant to their

markets. In the meantime, State government has halted its

decades of continuous growth and has sought to become a

facilitator of business and economic activity rather than

primarily a regulator.

Tourism has been undergoing its own adjustment and

transition. Hawaii is no longer the fast-growing resort destina-

tion it was in the 1960s, 70s and 80s. We have reached a level

of maturity as a destination and have found ourselves relying

much more on repeat business than in the past. Moreover, we

find that we must compete vigorously for visitors with the many

established and new destinations that have entered the world

tourism market in recent years. We know that to keep and expand our visitor markets in

the face of this competition, Hawaii must maintain its reputation for high quality and

become more efficient. We must revitalize our visitor infrastructure and provide an

ever-changing menu of attractions and events for new and repeat visitors.

One of the most important milestones so far in this period of transition has been the

creation of the Hawaii Tourism Authority (HTA). This agency is a product of the public-

private sector effort over the past several years to rethink our approach to the economy.

With a dedicated funding source and a mostly private sector membership, the HTA has

assumed responsibility for leading the future development and marketing of tourism.

The Authority has risen boldly to this challenge and produced a strategic plan designed to

launch a “New Beginning” for Hawaii tourism. Moreover, the Authority intends to refine

and carry out this plan in cooperation with the community.

While the leadership for tourism policy and marketing has shifted to the Authority,

DBEDT still has important responsibilities in tourism. First, we will be working closely with

the Authority to make sure marketing and promotion of Hawaii’s developing industries

such as technology, film, health, education and other emerging export activity are coordi-

nated well with tourism marketing. In this way marketing efforts can be leveraged to

provide a boost to economic diversification as well.

In addition, DBEDT will be maintaining the critical base of statistical information on

visitor activity that serves to measure the industry’s performance and provide information

for marketing and development purposes. Since assuming this responsibility earlier this

year, DBEDT’s new Tourism Research Branch has made improvements in the data collection

process and, with the help of the Department’s Business Resource Center, has established

an internet web site for disseminating the information.

The revitalization of Hawaii tourism for the 21st century is essential for our economic

wellbeing. But it must be compatible with the imperative need to develop new industries

and with our environmental and social values, and must be a positive benefit to all

residents of Hawaii. The Hawaii Tourism Authority is committed to these challenging goals

and I urge the cooperation and goodwill of all residents, businesses and government

agencies to help the Hawaii Tourism Authority succeed in these goals.

Dr. Seiji NayaDirectorDept. of Business, Economic Development & Tourism

Seiji Naya

3Hawaii’s Economy /July 1999

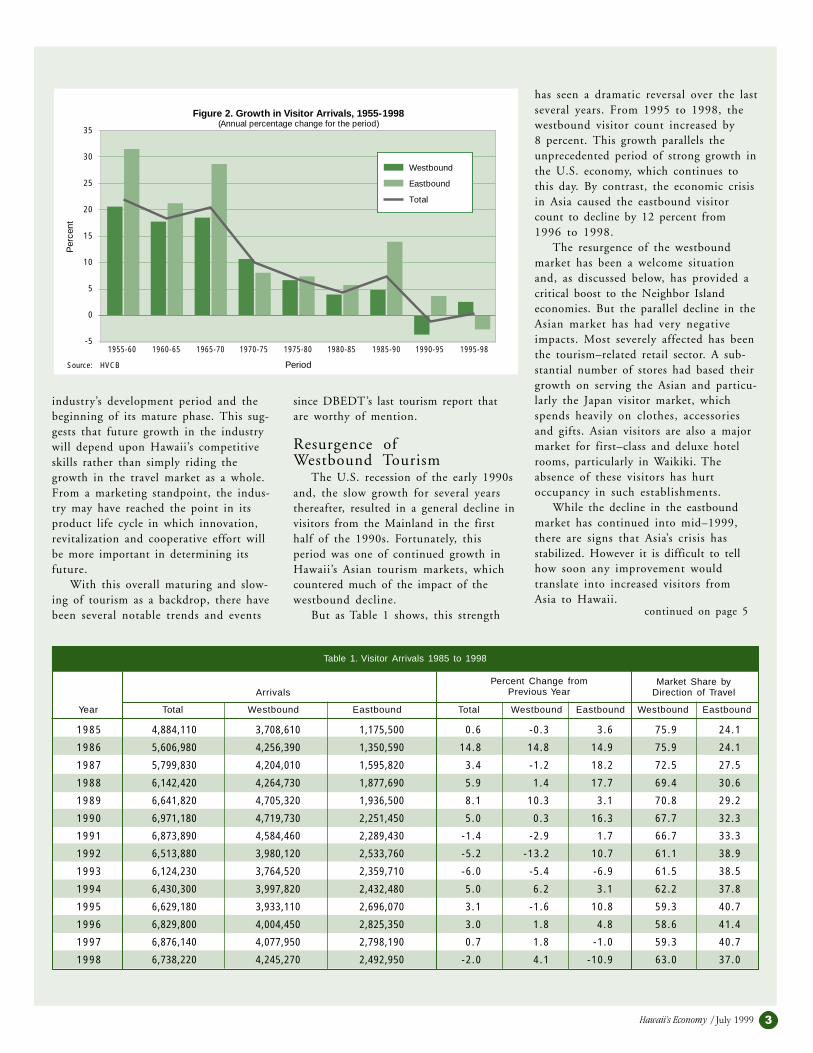

industry’s development period and thebeginning of its mature phase. This sug-gests that future growth in the industrywill depend upon Hawaii’s competitiveskills rather than simply riding thegrowth in the travel market as a whole.From a marketing standpoint, the indus-try may have reached the point in itsproduct life cycle in which innovation,revitalization and cooperative effort willbe more important in determining itsfuture.

With this overall maturing and slow-ing of tourism as a backdrop, there havebeen several notable trends and events

since DBEDT’s last tourism report thatare worthy of mention.

Resurgence ofWestbound Tourism

The U.S. recession of the early 1990sand, the slow growth for several yearsthereafter, resulted in a general decline invisitors from the Mainland in the firsthalf of the 1990s. Fortunately, thisperiod was one of continued growth inHawaii’s Asian tourism markets, whichcountered much of the impact of thewestbound decline.

But as Table 1 shows, this strength

has seen a dramatic reversal over the lastseveral years. From 1995 to 1998, thewestbound visitor count increased by8 percent. This growth parallels theunprecedented period of strong growth inthe U.S. economy, which continues tothis day. By contrast, the economic crisisin Asia caused the eastbound visitorcount to decline by 12 percent from1996 to 1998.

The resurgence of the westboundmarket has been a welcome situationand, as discussed below, has provided acritical boost to the Neighbor Islandeconomies. But the parallel decline in theAsian market has had very negativeimpacts. Most severely affected has beenthe tourism–related retail sector. A sub-stantial number of stores had based theirgrowth on serving the Asian and particu-larly the Japan visitor market, whichspends heavily on clothes, accessoriesand gifts. Asian visitors are also a majormarket for first–class and deluxe hotelrooms, particularly in Waikiki. Theabsence of these visitors has hurtoccupancy in such establishments.

While the decline in the eastboundmarket has continued into mid–1999,there are signs that Asia’s crisis hasstabilized. However it is difficult to tellhow soon any improvement wouldtranslate into increased visitors fromAsia to Hawaii.

continued on page 5

Table 1. Visitor Arrivals 1985 to 1998

ArrivalsPercent Change from

Previous YearMarket Share by

Direction of Travel

Year Total Westbound Eastbound Total Westbound Eastbound Westbound Eastbound

1 9 8 5 4,884,110 3,708,610 1,175,500 0 . 6 - 0 . 3 3 . 6 7 5 . 9 2 4 . 1

1 9 8 6 5,606,980 4,256,390 1,350,590 1 4 . 8 1 4 . 8 1 4 . 9 7 5 . 9 2 4 . 1

1 9 8 7 5,799,830 4,204,010 1,595,820 3 . 4 - 1 . 2 1 8 . 2 7 2 . 5 2 7 . 5

1 9 8 8 6,142,420 4,264,730 1,877,690 5 . 9 1 . 4 1 7 . 7 6 9 . 4 3 0 . 6

1 9 8 9 6,641,820 4,705,320 1,936,500 8 . 1 1 0 . 3 3 . 1 7 0 . 8 2 9 . 2

1 9 9 0 6,971,180 4,719,730 2,251,450 5 . 0 0 . 3 1 6 . 3 6 7 . 7 3 2 . 3

1 9 9 1 6,873,890 4,584,460 2,289,430 - 1 . 4 - 2 . 9 1 . 7 6 6 . 7 3 3 . 3

1 9 9 2 6,513,880 3,980,120 2,533,760 - 5 . 2 - 1 3 . 2 1 0 . 7 6 1 . 1 3 8 . 9

1 9 9 3 6,124,230 3,764,520 2,359,710 - 6 . 0 - 5 . 4 - 6 . 9 6 1 . 5 3 8 . 5

1 9 9 4 6,430,300 3,997,820 2,432,480 5 . 0 6 . 2 3 . 1 6 2 . 2 3 7 . 8

1 9 9 5 6,629,180 3,933,110 2,696,070 3 . 1 - 1 . 6 1 0 . 8 5 9 . 3 4 0 . 7

1 9 9 6 6,829,800 4,004,450 2,825,350 3 . 0 1 . 8 4 . 8 5 8 . 6 4 1 . 4

1 9 9 7 6,876,140 4,077,950 2,798,190 0 . 7 1 . 8 - 1 . 0 5 9 . 3 4 0 . 7

1 9 9 8 6,738,220 4,245,270 2,492,950 - 2 . 0 4 . 1 - 1 0 . 9 6 3 . 0 3 7 . 0

35

30

25

20

15

10

5

0

-51955-60 1960-65 1965-70 1970-75 1975-80 1980-85 1985-90 1990-95 1995-98

Figure 2. Growth in Visitor Arrivals, 1955-1998(Annual percentage change for the period)

Westbound

Eastbound

Total

Per

cent

PeriodSource: HVCB

4 Hawaii’s Economy /July 1999

As in 1998, visitor industry perfor-mance in 1999 has hinged on the bal-ance between an Asian market inrecession and generally thriving marketsin the U.S. and Canada. Table A summa-rizes tourism performance for the first sixmonths of 1999. The results are mixed,with visitor arrivals flat or down, butwith the daily visitor census generally up

Tourism in 1999: Performance and Outlookparticularly Japanese visitors, wererunning about 7.7 percent behind thesame 1998 period. However a modestincrease in length of stay by those east-bound visitors who did arrive helpedkeep the decline in the average dailycensus for this group to just 3.3 percent.The overall result has been a 0.6 percentincrease in the statewide visitor count in1999, with an increase in the dailyvisitor census of 2.7 percent.

The decline in eastbound visitors hasbeen most serious for Oahu, sinceroughly half of the City and County’svisitors come from Asia and the Pacific.Consequently, while Oahu showed gainsin westbound tourism for the first sixmonths, the double-digit decline in theeastbound direction pulled the overallarrival total down 3.1 percent for thefirst six months of the year. Yet, like thestate, Oahu experienced a gain in theoverall visitor census (a 3.4 percentincrease for the period) thanks to theincreased length of stay.

Among the Neighbor Island counties,the strong westbound market was ableto counter eastbound declines on Mauiand Kauai but not in Hawaii County. Ha-waii was also the only county to registera decline in the overall visitor censusduring the first six months of 1999.

Short-Term Outlook for TourismDBEDT’s economic forecast for 1999

expects some improvement in the visitorcount in the second half of the year,leading to a slight increase for statewidetourism in 1999. However it is not clearwhether the improvement will be consis-tent among the counties. It is hoped thatthe Asian market will stabilize this yearand begin a gradual recovery thereafter,although the schedule for that recoverydepends on how quickly the Asianeconomies, particularly Japan, can solvetheir economic problems.

around the state.The strength in the U.S and Canadian

markets has helped westbound visitorarrivals increase by 5.4 percent for theperiod. With a slight decrease in thewestbound length of stay, the dailywestbound visitor census was up by4.5 percent. Eastbound visitor arrivals,which are dominated by Asian and

Table A. Visitor Industry Performance IndicatorsJanuary to June 1999

(all data are preliminary)

Arrivals

Indicator Number % Change

Statewide visitor arrivals (by air)1 3,368,040 0.6%

Westbound 2,228,970 5.4%

U.S. 1,849,810 5.5%

Canada 163,180 15.6%

Europe 88,730 0.1%

Eastbound 1,139,070 -7.7%

Intended visitors by county

Oahu 2,288,400 -3.1%

Westbound 1,207,210 5.8%

Eastbound 1,081,190 -11.4%

Maui (Maui, Molokai & Lanai Islands) 1,178,130 0.5%

Westbound 1,008,460 4.1%

Eastbound 169,670 -16.4%

Hawaii 626,980 -3.0%

Westbound 500,490 1.2%

Eastbound 126,490 -16.7%

Kauai 536,340 6.5%

Westbound 477,700 9.0%

Eastbound 58,640 -10.2%

Statewide daily visitor census 162,630 2.7%

Westbound 126,630 4.5%

Eastbound 36,000 -3.3%

Oahu 75,655 3.4%

Maui County 45,547 1.3%

Hawaii County 23,277 -1.9%

Kauai County 18,151 9.5%

1 About 26,000 visitors arr ived on cruise ships in the first six months of 1999. This was 58.0 percent more than in thesame 1998 period.

Source: DBEDT

5Hawaii’s Economy /July 1999

Tourism Growth Now Favorsthe Neighbor Islands

Oahu was the primary beneficiary ofthe surge in eastbound visitors duringthe first half of the 1990s. From 1990to 1997, the proportion of Oahu arrivalsaccounted for by eastbound visitorsincreased from 41 percent to nearly55 percent. But as a result of the shift inthe growth from eastbound to westboundvisitors since 1997, the visitor count onOahu has fallen, while Neighbor Islandshave experienced stronger growth onaverage. This trend has restored confi-dence in the tourism sectors of theNeighbor Islands and provided a neededeconomic boost. However, the impact onOahu, which accounts for more thanthree-quarters of the state’s economy,has been the opposite.

Policy TrendsFormation of the Hawaii Tourism

Authority (HTA) may be the most signifi-cant change in tourism marketing sincethe formation of the Hawaii VisitorsBureau in 1903. This thirteen-memberauthority was created through Act 156HSL 1998, as an outgrowth of recom-mendations by the Economic Revitaliza-tion Task Force of the previous year. Theformation of the HTA reflects the notionthat tourism is entering a new stage and

that pro-active, cooperative effort by theprivate and public sectors will determinethe long-run future of Hawaii’s majorindustry.

The HTA has been given the author-ity to develop and administer marketingand promotional efforts on behalf ofHawaii’s visitor industry. The HTA mayalso develop plans for the future develop-ment of tourism in terms of both industryproducts and infrastructure support. TheAuthority was finalizing its first strategicplan for tourism as of June 1999.

The HTA assumes responsibilities thatwere previously shared among severalpublic and private agencies, most notablyDBEDT, through its State Tourism Office,and the Hawaii Visitors and ConventionBureau. The legislation establishing theHTA also designated DBEDT to maintainand report visitor statistics as well asconduct tourism–related research.

Tourism Financing ReformOne of the issues raised in DBEDT’s

1996 report on tourism was the need toprovide more stability in the fundingprocess for tourism marketing. In addi-tion to establishing the HTA, Act 156also shifted the burden of funding tour-ism promotion and marketing activitiesfrom the State General Fund, where itcompeted with all other state spending

Tourism Looks to the Future continued from page 3

TheEconomicImpact ofTourism:

An Update

Tourism spending in Hawaiiaccounted directly and indirectlyfor about 22 percent of both Gross

State Product (GSP) and labor income in1998. This updated estimate is based onDBEDT’s State of Hawaii Input-Output(I-O) Model which was recently revisedto reflect valuable new information.1

The “Visitor Industry”Tourism is not an industry in the strict

sense of the term. A search of the Stan-dard Industrial Classification manual orthe U.S. Bureau of Economic Analysis’sindustrial structure will not turn up anindustry called “tourism” or “visitors”.What Hawaii defines as the visitor indus-try is made up of parts of many different

industries ranging from agriculture tomanufacturing to government. The visi-tor component of each industry is calcu-

lated as a proportion of the industry’ssales to visitors. Thus, estimating thesize of the “visitor industry” and its rela-tionship to other industries is particularlychallenging, since it requires estimatingthe visitor-related portion of each of the118 industries that are part of theI-O model.

Visitor SpendingMeasuring the economic impact of

the visitor industry starts with visitorexpenditures — that is, the amount of

priorities, to the Transient Accommoda-tions Tax (TAT). A new Tourism SpecialFund was created to absorb about 38percent of the TAT, which was adjustedupwards to 7.25%. It is expected that thefund will provide between $50 and $60million per year for tourism marketingand development.

Previously, tourism marketing fundswere appropriated by the Legislaturefrom the General Fund each year, andthis meant that tourism marketing needscompeted with all other state priorities.The special fund establishes a dedicatedfinancing source that can assure a con-sistent long-run marketing and promo-tion effort even as year-to-year statepriorities change. The section of thisreport on tourism issues explores thesignificance of the policy changes inmore detail.

ConclusionSince 1996 tourism has shown only

modest improvement. However with anew Tourism Authority, more funding formarketing, and a Tourism Strategic Planto set the direction, there is reason foroptimism about reinvigorating this essen-tial industry. The next several articleslook at particular areas of interest inthe emerging tourism market of the21st century.

1 A report on the 1992 I-O model can be found at http://www.hawaii.gov/dbedt under Statistics & Publications.The new information are based on the 1992 EconomicCensus and other sources. Before the revisions, the modelwas based on 1987 relationships.

continued on page 6

6 Hawaii’s Economy /July 1999

money that out-of-state visitors spend inHawaii.2 Table 1 shows expendituresmade by visitors arriving by air. Inaddition to visitor spending in Hawaii,the visitor–related portion of overseasairline expenditures in Hawaii is alsoincluded as a component of visitorexpenditures.

The sum of the components in Table 1equals Gross Visitor Expenditures, whichinclude the portion of spending on prod-ucts or services that were imported andresold to the visitor. As the table indi-cates, gross expenditures increased in allbut two of the last six years and in 1998were about 4 percent below their peakin 1995.

While gross visitor expenditurescorrectly represent the total sales made tovisitors by Hawaii businesses, it does notnecessarily represent the economic con-tribution of tourism to Hawaii. If we areinterested in the contribution of the visi-tor industry to goods and services pro-duced by Hawaii, we must exclude thevalue of goods that were imported fromelsewhere and sold to visitors.

Table 2 shows estimates of theportion of gross visitor expendituresaccounted for by imports. When this issubtracted from gross expenditures, theresult is a measure of net visitor expendi-tures. Net visitor expenditures representthe value added to the economy by thevisitor industry as measured by GSP. Netvisitor expenditures declined in two ofthe past six years and in 1998, it was4 percent below its peak in 1995.

GSP, Jobs, Income and TaxesVisitor expenditures stimulate the

economy in three major ways. First, aportion of visitor spending directlysupports the jobs and income of visitorindustry employees, managers and smallbusiness owners.3 These are the peopleand firms that deal directly with the visi-tor. The operation might be a hotel inWaikiki, deriving most its income fromvisitors, or a convenience store in Aiea,with only occasional visitor sales.

Second, visitor spending stimulatesthe economy indirectly when firms inthe visitor industry and their businesssuppliers replenish inventories and main-tain their facilities. The indirect impactstimulates the inter-business income andproduction chain by re-circulating visitordollars to industries and workers whosupply goods and services to the visitorsector. For example, cases of macadamianut candies purchased in a store bymembers of a tour group are replaced by

ordering more of the product. This im-pacts local companies all the way downthe business-distribution chain, andeventually to the macadamia orchardson the Big Island and Kauai.

The third effect of visitor spending,called the induced effect, is felt whenemployees of firms in both tourism andits business-distribution chain spendtheir household income for goods andservices in the community. The inducedeffect spreads throughout the economy,far beyond the tourism industry and itssupply chain. In times of rapid increasein visitor activity, the indirect and in-duced effect can stimulate incomes andspending throughout the state in all in-dustries with most people and businessesunaware that their prosperity is linked tovisitor spending.

Of course the process also works inreverse. That is, a decline in visitorspending will not only reduce the directeffect on the industry; it will also reducethe indirect and induced effects, and thecommunity will eventually see declinesin sales and probably job losses in areasthat are not directly related to visitoractivity. While this lack of visible linkagemay help explain why many residents donot think they are or will be affected bydeclines in the visitor industry, in fact,most residents are vitally affected by thehealth of this industry.

Table 1. Hawaii Visitor-Related Expenditures1

Overseas Airl ine Gross Visi torExpendi tures Expendi tures

Ye a r Visitors by Air ($mil.) ($mil.)

Table 2. Direct Contribution of Tourism to Hawaii’s Economy

Gross Visi tor Visi tor-Related Net Visi torExpendi tures Impor t s Expendi tures

Ye a r ($mil.) ($mil.) ($mil.)

GSP ($mil.) Jobs (1,000)1 Labor Income ($mil.) S&L Taxes ($mil.)

Direct , Direct , Direct , Direct ,Direct & Indirect, Direct & Indirect, Direct & Indirect, Direct & Indirect,

Year Indirect & Induced Indirect & Induced Indirect & Induced Indirect & Induced

Table 3. Economic Impact of Tourism in Hawaii

2 While residents can certainly be viewed as tourists whenthey use hotels and visit tourist attractions, this analysisfocuses on sales to out-of-state visitors, which brings newmoney into the state.

3 Of course, visitor spending also supports stockholderdividends and retained corporate earnings of businessesdirectly involved in providing goods and services to visitors.However, these are relatively small compared to payroll andinter-business purchases.

The Economic Impact of Tourism continued from page 5

1 9 9 2 9 ,558 .9 4 6 1 . 2 10 ,020 .1

1 9 9 3 8 ,677 .6 4 4 7 . 5 9 ,125 .1

1 9 9 4 10 ,603 .2 4 3 2 . 5 11 ,035 .7

1 9 9 5 11 ,587 .7 4 3 9 . 3 12 ,027 .0

1 9 9 6 10 ,684 .8 4 4 1 . 8 11 ,126 .6

1 9 9 7 10 ,770 .1 4 6 1 . 6 11 ,231 .7

1 9 9 8 2 11 ,133 .3 4 6 1 . 4 11 ,594 .7

1 Visitors came to Hawaii by Air only.2 Preliminary estimate.

Source: DBEDT

1 9 9 2 10 ,020 .1 3 ,757 .5 6 ,262 .6

1 9 9 3 9 ,125 .1 3 ,421 .9 5 ,703 .2

1 9 9 4 11 ,035 .7 4 ,138 .4 6 ,897 .3

1 9 9 5 12 ,027 .0 4 ,510 .1 7 ,516 .9

1 9 9 6 11 ,126 .6 4 ,172 .5 6 ,954 .1

1 9 9 7 11 ,231 .7 4 ,211 .9 7 ,019 .8

1 9 9 8 11 ,594 .7 4 ,348 .0 7 ,246 .7

1 9 9 2 6 ,262 .6 9 ,872 .7 1 8 1 . 6 3 2 3 . 2 3 ,952 .0 6 ,069 .1 7 5 2 . 7 1 ,112 .6

1 9 9 3 5 ,703 .2 8,990.9 1 7 6 . 3 3 1 2 . 3 3 ,599 .0 5 ,527 .0 6 8 7 . 2 1,015.0

1 9 9 4 6 ,897 .3 10 ,873 .4 1 7 6 . 4 3 1 1 . 7 4 ,352 .6 6 ,684 .3 8 2 6 . 4 1 ,222 .8

1 9 9 5 7 ,516 .9 11 ,850 .1 1 7 7 . 7 3 1 4 . 0 4 ,743 .5 7 ,284 .7 9 1 2 . 0 1 ,344 .0

1 9 9 6 6 ,954 .1 10 ,962 .9 1 7 9 . 6 3 1 7 . 2 4 ,388 .4 6 ,739 .3 8 7 0 . 0 1 ,269 .7

1 9 9 7 7 ,019 .8 11 ,066 .5 1 8 0 . 7 3 1 9 . 2 4 ,429 .9 6 ,803 .0 8 8 0 . 0 1 ,283 .4

1 9 9 8 2 7 ,246 .7 11 ,424 .2 1 8 0 . 1 3 1 8 . 2 4 ,573 .0 7 ,022 .9 9 0 3 . 3 1 ,319 .8

1 Includes self-employed jobs.2 Preliminary estimates.Source: DBEDT

Source: DBEDT

7Hawaii’s Economy /July 1999

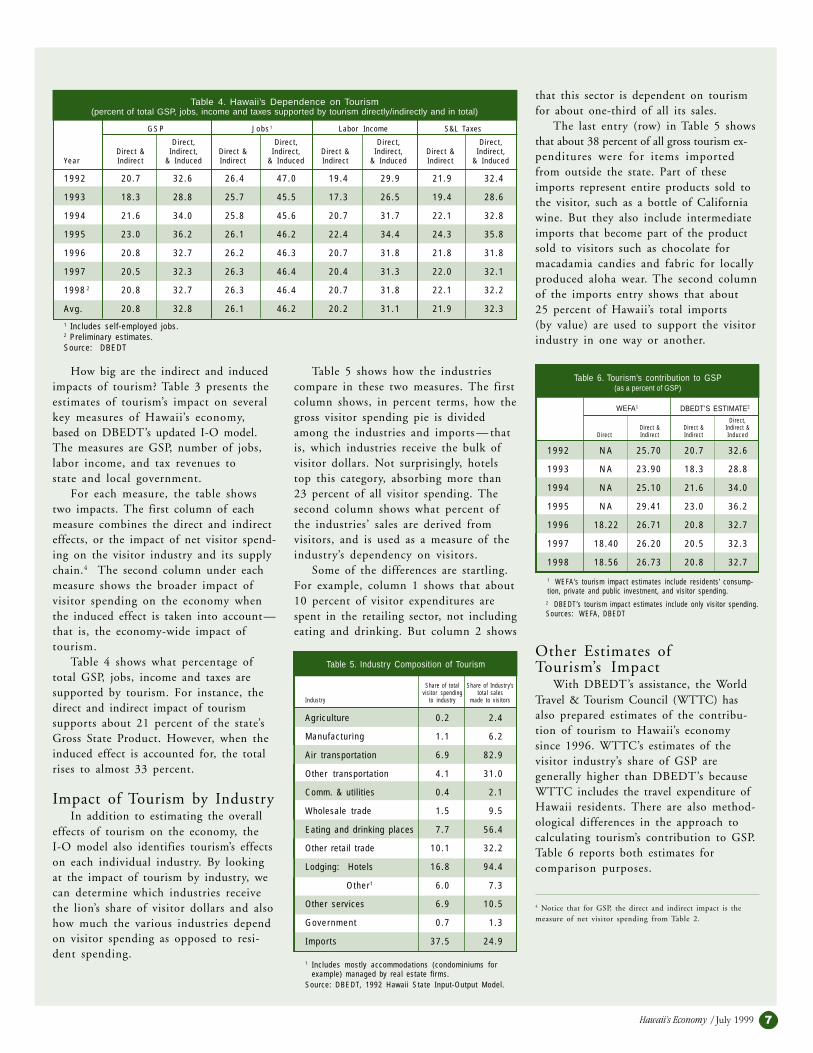

How big are the indirect and inducedimpacts of tourism? Table 3 presents theestimates of tourism’s impact on severalkey measures of Hawaii’s economy,based on DBEDT’s updated I-O model.The measures are GSP, number of jobs,labor income, and tax revenues tostate and local government.

For each measure, the table showstwo impacts. The first column of eachmeasure combines the direct and indirecteffects, or the impact of net visitor spend-ing on the visitor industry and its supplychain.4 The second column under eachmeasure shows the broader impact ofvisitor spending on the economy whenthe induced effect is taken into account—that is, the economy-wide impact oftourism.

Table 4 shows what percentage oftotal GSP, jobs, income and taxes aresupported by tourism. For instance, thedirect and indirect impact of tourismsupports about 21 percent of the state’sGross State Product. However, when theinduced effect is accounted for, the totalrises to almost 33 percent.

Impact of Tourism by IndustryIn addition to estimating the overall

effects of tourism on the economy, theI-O model also identifies tourism’s effectson each individual industry. By lookingat the impact of tourism by industry, wecan determine which industries receivethe lion’s share of visitor dollars and alsohow much the various industries dependon visitor spending as opposed to resi-dent spending.

Table 5 shows how the industriescompare in these two measures. The firstcolumn shows, in percent terms, how thegross visitor spending pie is dividedamong the industries and imports — thatis, which industries receive the bulk ofvisitor dollars. Not surprisingly, hotelstop this category, absorbing more than23 percent of all visitor spending. Thesecond column shows what percent ofthe industries’ sales are derived fromvisitors, and is used as a measure of theindustry’s dependency on visitors.

Some of the differences are startling.For example, column 1 shows that about10 percent of visitor expenditures arespent in the retailing sector, not includingeating and drinking. But column 2 shows

that this sector is dependent on tourismfor about one-third of all its sales.

The last entry (row) in Table 5 showsthat about 38 percent of all gross tourism ex-penditures were for items importedfrom outside the state. Part of theseimports represent entire products sold tothe visitor, such as a bottle of Californiawine. But they also include intermediateimports that become part of the productsold to visitors such as chocolate formacadamia candies and fabric for locallyproduced aloha wear. The second columnof the imports entry shows that about25 percent of Hawaii’s total imports(by value) are used to support the visitorindustry in one way or another.

Table 4. Hawaii’s Dependence on Tourism(percent of total GSP, jobs, income and taxes supported by tourism directly/indirectly and in total)

G S P J o b s 1 Labor Income S&L Taxes

Direct , Direct , Direct , Direct ,Direct & Indirect, Direct & Indirect, Direct & Indirect, Direct & Indirect,

Year Indirect & Induced Indirect & Induced Indirect & Induced Indirect & Induced

Table 5. Industry Composition of Tourism

Share of total Share of Industr y’svisitor spending total sales

Indust ry to industry made to visitors

Table 6. Tourism’s contribution to GSP(as a percent of GSP)

Direct ,Direct & Direct & Indirect &

Direct Indi rect Indi rect I nduced

WEFA1 DBEDT’S ESTIMATE2

1 9 9 2 2 0 . 7 3 2 . 6 2 6 . 4 4 7 . 0 1 9 . 4 2 9 . 9 2 1 . 9 3 2 . 4

1 9 9 3 1 8 . 3 2 8 . 8 2 5 . 7 4 5 . 5 1 7 . 3 2 6 . 5 1 9 . 4 2 8 . 6

1 9 9 4 2 1 . 6 3 4 . 0 2 5 . 8 4 5 . 6 2 0 . 7 3 1 . 7 2 2 . 1 3 2 . 8

1 9 9 5 2 3 . 0 3 6 . 2 2 6 . 1 4 6 . 2 2 2 . 4 3 4 . 4 2 4 . 3 3 5 . 8

1 9 9 6 2 0 . 8 3 2 . 7 2 6 . 2 4 6 . 3 2 0 . 7 3 1 . 8 2 1 . 8 3 1 . 8

1 9 9 7 2 0 . 5 3 2 . 3 2 6 . 3 4 6 . 4 2 0 . 4 3 1 . 3 2 2 . 0 3 2 . 1

1 9 9 8 2 2 0 . 8 3 2 . 7 2 6 . 3 4 6 . 4 2 0 . 7 3 1 . 8 2 2 . 1 3 2 . 2

Avg . 2 0 . 8 3 2 . 8 2 6 . 1 4 6 . 2 2 0 . 2 3 1 . 1 2 1 . 9 3 2 . 3

1 Includes self-employed jobs.2 Preliminary estimates.Source: DBEDT

Agr iculture 0 . 2 2 . 4

Manufactur ing 1 . 1 6 . 2

Air transportation 6 . 9 8 2 . 9

Other transportation 4 . 1 3 1 . 0

Comm. & uti l i t ies 0 . 4 2 . 1

Wholesale trade 1 . 5 9 . 5

Eating and drinking places 7 . 7 5 6 . 4

Other retail trade 1 0 . 1 3 2 . 2

Lodging: Hotels 1 6 . 8 9 4 . 4

Other1 6 . 0 7 . 3

Other services 6 . 9 1 0 . 5

Gove r nmen t 0 . 7 1 . 3

Impor ts 3 7 . 5 2 4 . 9

1 Includes mostly accommodations (condominiums for example) managed by real estate firms.Source: DBEDT, 1992 Hawaii State Input-Output Model.

1 9 9 2 N A 2 5 . 7 0 2 0 . 7 3 2 . 6

1 9 9 3 N A 2 3 . 9 0 1 8 . 3 2 8 . 8

1 9 9 4 N A 2 5 . 1 0 2 1 . 6 3 4 . 0

1 9 9 5 N A 2 9 . 4 1 2 3 . 0 3 6 . 2

1 9 9 6 1 8 . 2 2 2 6 . 7 1 2 0 . 8 3 2 . 7

1 9 9 7 1 8 . 4 0 2 6 . 2 0 2 0 . 5 3 2 . 3

1 9 9 8 1 8 . 5 6 2 6 . 7 3 2 0 . 8 3 2 . 7

1 WEFA’s tourism impact est imates include residents’ consump-tion, private and public investment, and visitor spending.

Other Estimates ofTourism’s Impact

With DBEDT’s assistance, the WorldTravel & Tourism Council (WTTC) hasalso prepared estimates of the contribu-tion of tourism to Hawaii’s economysince 1996. WTTC’s estimates of thevisitor industry’s share of GSP aregenerally higher than DBEDT’s becauseWTTC includes the travel expenditure ofHawaii residents. There are also method-ological differences in the approach tocalculating tourism’s contribution to GSP.Table 6 reports both estimates forcomparison purposes.

4 Notice that for GSP, the direct and indirect impact is themeasure of net visitor spending from Table 2.

2 DBEDT’s tour ism impact estimates include only visitor spending.Sources: WEFA, DBEDT

8 Hawaii’s Economy /July 1999

Understanding Tourism Niche Marketswith Input-Output Analysis

Because tourism is Hawaii’s largesteconomic activity, DBEDT’s Research andEconomic Analysis Division (READ)conducts economic impact analyses ofvisitor-related events. To conduct theseanalyses, READ economists frequentlyuse the State Input-Output (I-O) model.This article looks at the application ofthese I-O techniques in analyzing twotourism-related activities: cruise shipactivity and the Ironman Triathlon.

In most cases, the analysis beginswith an estimate of the expected directdollar impact of the event. In our ex-amples, estimates must be made of cruiseship visitor expenditures or the spendingof participants and related visitors for theIronman. These direct spending estimatesare often constructed from informationoutside the I-O model. The I-O modelthen converts these direct dollar impactsinto additional indirect and inducedeffects on sales, income, jobs, and so on.

Cruise ShipsHawaii’s cruise industry consists of

two components: (1) the domesticoperations of American Hawaii Cruises(AHC), and (2) foreign-flagged cruiseships that visit Hawaii from foreignports. AHC currently operates one,U.S.-flagged cruise ship in its interislandcruise operations, the S.S. Independence(see article on page 12 for more infor-mation on the cruise and AHC). TheIndependence leaves Honolulu’s AlohaTower Marketplace each Saturday andcruises to Kauai, Maui, Hilo and Konabefore returning to Honolulu thefollowing Saturday.

In addition to AHC operations, foreigncruise vessels regularly visit Hawaii andtour among the islands. Indeed, thecruise industry has been growing rapidlyfor many years. In 1998, 21 foreigncruise ships visited Hawaii, making atotal of 220 port calls — up from just56 port calls in 1994.

Taking into account information onlengths of stay and average spending inport, DBEDT has estimated the totalannual expenditures of cruise visitors inHawaii to be about $51 million in 1998.Using economic multipliers determinedthrough the I-O model, the impact ofthis $51 million expenditures can beestimated on Hawaii’s economy.

As shown in Table 1, spending bycruise ship visitors in 1998 was esti-mated to have increased the output(sales) in the economy by $86 million.This spending supported $31 million inhousehold income, more than 1,200 jobsand about $5 million in state and countygovernment tax revenues.

The relationship between the initialspending by cruise ship visitors and theamount of economic activity generated inthe community can be expressed in theform of multipliers. The output multiplierof 1.71 in Table 1 means that for every$1 of spending by cruise ship visitorsan additional 71 cents of spending willbe generated elsewhere in the economyfor a total of $1.71 generated. The addi-tional 71 cents is composed of increasedinter-industry sales and sales inducedby the re-spending of income generatedby the initial $1 of cruise visitorspending.1

Type of Impact Value

Table 1. Estimation of Economic Impact of Cruise Visitor Spending

The “income” multiplier of 0.62 has asimilar interpretation, with $1 of visitorspending leading to $0.62 in income.Here, the multiplier is lower, rather thanhigher, than one because a significantportion of the $1.71 in sales generatedwill not become household income. Partof the sales revenues will go to profits,taxes and other business expenses. Aneven larger amount of revenues will“leak” out of the economy before creat-ing income, in order to pay for businesspurchases from outside Hawaii and alsopayment for goods brought in to sell tovisitors.

The “employment” multiplier isexpressed as jobs per $1 million of cruisevisitor spending. However, an adjust-ment is made to account for wage andprice increases by adjusting the multiplier(downwards) to reflect the higher cost ofsupporting a job in 1998 compared with1992. Because of higher wages over theyears fewer jobs can be created for eachmillion dollars of visitor spending andthis needs to be reflected in the multi-plier. Thus, after “deflating” the multi-plier, it is estimated that 24.7 jobs weresupported in 1998 for every $1 million ofcruise ship visitor spending.

Finally, the ratio of state and countytax receipts to income (which is esti-mated at about 17%) is used to calculatethe impact of visitor spending on govern-ment revenue.

The effects of cruise ship operationsin Hawaii, paid for through passengerrevenues, also add to the economy. Themajor impact in this area are the opera-tions of AHC, which hires and purchasesmost of what it uses locally. The effectsof AHC operations on the economy arecalculated in Table 2.2 AHC has passen-ger revenues of about $69 million peryear. Applying the I-O multipliers for

1 Some sales transactions are not included in the “output”measure of input-output analysis. For instance retail salesare not counted since the value of the goods sold at retail isalready counted in other areas of the I-O such as agriculture,manufacturing or imports. Thus I-O “sales” cannot be com-pared to the Gross Excise Tax Sales Base or other morecomprehensive measures of total sales transactions.

2 Data are not readily available on the purchases in Hawaii offoreign cruise ships, but they are likely modest in comparisonto the other impacts estimated in this analysis.

Output generated in the economy ($millions) 8 6Household income generated in the economy ($mill ions) 3 1Jobs supported in the economy 1 , 2 4 2State and county taxes generated ($millions) 5

Cruise Ship Visitor Multipliers

Output multipl ier 1 . 7 1Income multipl ier 0 . 6 2Employment multiplier (adjusted to 1998 value of the dollar) 2 4 . 7Ratio between tax and income (includes all State and county taxes) 0 . 1 7

Source: DBEDT

9Hawaii’s Economy /July 1999

ocean transportation, the model indicatesthat interisland cruise operations accountfor $155 million of sales, $42 million ofhousehold income, and 1,200 jobs inHawaii’s economy.

The economic impacts of cruise shipvisitor expenditures and AmericanHawaii Cruises operations may be addedtogether to estimate the total effect of thecruise industry on Hawaii’s economy.Table 3 summarizes these results.

The estimates show that the industrycurrently generates nearly 2,500 jobs inthe state, as well as $240 million in out-put, $73 million in household incomeand close to $13 million in state andlocal government revenues.

Ironman TriathlonInput-output analysis can also be

used to calculate the economic impact onthe economy of events held in Hawaii.One example is the Ironman Triathlonwhich has been held in Hawaii since1978. Held on the Big Island, the eventhas grown steadily over the years andnow averages about 1,400 participants.

About 95 percent of the participantscome from out-of-state. They are accom-panied by family, friends, other visitors,and media personnel covering the event.All of these people spend money inHawaii and thereby contribute to theeconomy. In order to estimate the impactof the Ironman on the economy, anestimate must first be made of how muchthose associated with the event spend inHawaii. This estimate has been calcu-lated at $14.9 million.

Understanding Tourism Niche Markets continued from page 8

Table 2. Impact of American Hawaii Cruises Operations

Type of Impact Value

Table 3. Total Economic Impact of Cruise Industry in Hawaii

Applying the estimated tourismmultipliers for total sales (1.71) andhousehold income (0.62) to the $14.9million spent, it is estimated that theIronman event results in total output/sales of $25.4 million and householdincome of $9.2 million. Since approxi-mately 17 percent of visitor expendituresbecome state and local tax revenue, theevent generated about $1.6 million instate and local revenue.

The employment multiplier is gener-ally not applied to annual or one-timeevents such as the Triathlon. Such eventsdo not generally result in permanent or

ongoing positions. Instead, the economyresponds by creating opportunities forovertime and temporary jobs that maylast only during the event.

ConclusionThe I-O model provides a powerful

tool for estimating the impact of industryactivity and events on the economy. Italso allows comparison among alterna-tive activities, particularly as to whichones generate the most economic activityfor a given amount of export revenue orspending by outsiders in the localeconomy.

TourismInitiativesand Issues

In the last issue of Hawaii’s Economydevoted to tourism, four issues wereidentified as worthy of special atten-

tion by policy makers and planners.Those were 1) the need to boost activityon the Neighbor Islands, 2) increasingthe proportion of deluxe rooms in theWaikiki area, 3) working for more airseat capacity, and 4) restructuring tour-ism promotion financing to provide amore stable marketing effort.

Encouraging progress has been madein most of these areas. Neighbor Islandtourism now leads growth statewide.

Tourism marketing is now fundedthrough a portion of the TransientAccommodations Tax (TAT) which will

provide about twice the level of previouspublic sector support. Air seat capacitydoes appear to be improving as the west-bound market recovers (see p. 21). Somemodest progress in establishing incen-tives for renovation and upgrading ofroom quality in Waikiki has been made.However, the sharp decline in the Asianmarket, which favors first–class accom-modations, has eased the potential short-age for now. Nevertheless, as the Asianmarket recovers and the convention cen-ter bookings increase, the potential for ashortage of high-end rooms will remain.

Output generated ($mill ions) 2 4 1 . 2Household income generated ($mill ions) 7 3 . 3Jobs supported 2 , 4 5 0State and local taxes generated ($millions) 1 2 . 5

Source: DBEDT

Type of Impact Value

Estimated annual passenger revenure ($million) 6 9

Output generated ($mill ion) 1 5 5Household income generated ($mill ion) 4 2

Jobs supported 1 , 2 0 9State and local taxes generated ($million) 7 . 2

Cruise Ship Operations Multipliers (for ocean transportation)Output multipl ier 2 . 2 5Income multipl ier 0 . 6 1Employment multipl ier for ocean transportation 1 7 . 3 1Ratio between tax and income (includes all state & county taxes) 0 . 1 7

Source: DBEDT

continued on page 10

10 Hawaii’s Economy /July 1999

New InitiativesThe primary responsibility for antici-

pating and addressing Hawaii’s tourismdevelopment needs now rests with thenew Hawaii Tourism Authority. The HTAhas developed a Tourism Strategic Planwhich evaluates the state of the industryand establishes priority needs and issuesthe Authority will address under itsresponsibilities and with the resourcesof the Tourism Special Fund.

Formulated as Strategic Initiatives,the priorities and issues on which theHTA intends to focus address issuesraised in the earlier DBEDT tourismreport and add a comprehensive set ofnew priorities which were developedthrough the Authority’s extensive situa-tion analysis of tourism. Rather thanattempt to add to the HTA list of initia-tives and issues, it is more useful for thisreport to help foster an understanding ofthe content and rationale of theAuthority’s intended initiatives.

HTA Strategic InitiativesA : Communication and

Community RelationsThe HTA recognizes that public

support and participation are essentialto the goal of reinvigorating tourism.There are many stakeholders in Hawaiitourism — visitors, residents, privatebusinesses, and government agencies —all of whom have different issues ofinterest and concern. As the overallgovernment authority responsible fortourism, the HTA will need to link stake-holders and their interests to a commondirection. This will mean facilitating rela-tionships among community, industryand government stakeholders to addressrelevant tourism issues. To accomplishthis strategic initiative, the Authorityproposes development of a communica-tion plan to increase public awarenessand understanding of tourism, andobtain input on issues of concern.

B : M a r k e t i n gMarketing and promotion of Hawaii

to the world is the HTA’s primary respon-sibility. In the past few years Hawaii’spromotional efforts have been overshad-owed by those of competing destinationsand the state has not been able to keep

its high–quality product offerings in frontof consumers. The Authority believesthis situation has been a factor in thedecline of visitor expenditures andmarket share in recent years. With thecreation of the dedicated Tourism SpecialFund, Hawaii will have the capability todeliver a more globally competitivemarketing and promotional effort.

But with the ability to apply addi-tional resources comes the need to bemore sophisticated about the approachto marketing and the responsibility tomeasure the effectiveness of marketingexpenditures. The HTA’s strategy formarketing is to increase promotionalpresence and “brand identity” to morecompetitive levels and to optimize theeffectiveness of promotion in each MajorMarket Area, or “MMA,” as the HTArefers to them. The HTA’s aim is toallocate marketing resources so as toincrease the total expenditures made byvisitors in Hawaii, thus creating jobs andgenerating tax revenues.

The HTA has segmented the worldinto 10 MMAs. Two U.S. regions includethe western and eastern halves of thecountry. Japan and Canada are singledout as MMAs. Europe, Oceania, otherAsia and Latin America are each a sepa-rate MMA. The Hawaii ConventionCenter is designated as an MMA, and allremaining markets are contained in an“other” MMA category. Resource alloca-tions to the MMAs will be based onobtaining the highest return on invest-ment in terms of visitor expenditures,not just arrivals.

The challenge for the HTA will be thedevelopment of promotional programs toaccomplish the goal of increasing expen-ditures in each of the MMAs.

C: E v e n t sHawaii has a multitude of events that

vary in their degree of impact on the visi-tor industry. Most industry experts agreethat events for visitors, and especiallyevents that attract national media, are animportant part of a destination’s market-ing arsenal. In the past, many eventshave been funded through the State tour-ism budget. However, it has not alwaysbeen clear how the funded events wereexpected to contribute to the overall

marketing effort or how Hawaii’s fundingof such events could be optimized toincrease the marketing value.

The HTA’s Tourism Plan proposes astrategy to develop and support eventsthat generate cost–effective awareness ofthe Hawaii brand through national andinternational exposure. The Authorityintends to focus first on a year-roundseries of signature events that willbecome an integral part of the overallmarketing plan for the state. These willinclude significant and prestigious eventsin professional and college football,college basketball, professional golf,triathlon and marathon, and oceansports. The national and internationaltelevision and other media coverageassociated with such events can show-case Hawaii as the premiere locationfor recreation and sports activity.

The HTA also plans to support visitorattraction and cultural events, which willprovide incremental visitor expendituresto the state, particularly during times ofthe year when visitor counts are season-ally low. These include, among others,the Honolulu Festival and French Festi-val, and major island events like theMaui Writers Conference, A Taste ofLahaina, Kapalua Wine & Food Sympo-sium, Savor the Flavors of Kauai and theHawaiian Paniolo Music Festival. Theyalso include cultural events such as theAloha Festivals, Merrie Monarch andKing Kamehameha celebrations, whichprovide unique insight into Hawaii’s hostculture. Additionally, there is a wide-spread desire to increase the number of,and attention to, other special eventsand festivals.

D: Product DevelopmentThe HTA proposes to serve as a cata-

lyst for product and community-basedtourism development. The Authorityplans to focus on the development ofnew tourism events and experiences, andalso develop community-based tourismprograms. The HTA will particularly seekto develop programs in specialty or nichemarkets related to agriculture, culture,education, health and wellness, nature,sports, and science and technology, tocomplement Hawaii’s traditional leisureproduct offerings. There are existing

Tourism Initiatives and Issues continued from page 9

11Hawaii’s Economy /July 1999

attractions in each niche area whichhave developed more or less on theirown. However, the HTA plans to channelresources into creating a firm base for thegrowth of these and additional products.(A detailed description of the targetedniche markets can be found on pages 15to 17.)

The HTA also plans to work withisland advisory groups to establishmarkets for each product area. Thestrategy includes building on synergiesbetween tourism products well as provid-ing for a coordinated, easily accessibleinformation base.

E : A i r l i f tAs the article on Air Service (p. 21)

discusses, in marketing a leisure visitordestination the availability of affordable,convenient and comfortable transporta-tion to and from the destination is animportant competitive factor. Not eventhe most effective marketing programcan succeed if the air capacity to thedestination is insufficient.

Decisions to fly routes with particularfrequency and equipment depend oncomplex factors, including marketingcosts, distribution networks, airport is-sues, route and hub strategies, interna-tional agreements, and yields. Hawaii’sdependence on air transportation make itcritical that tourism planners and policymakers understand airline economics andthe carrier’s decision-making processwith respect to service levels. The HTAplans to address this issue through directcommunication with airline companiesand by efforts to increase awareness ofair transportation issues among theindustry and public.

The HTA will also advocate changesin airport operations and policies to makeit more cost–effective for airline compa-nies to operate and expand service in theHawaii market. The HTA will supportefforts to initiate new direct and/or non-stop service from cities not adequatelyconnected to Hawaii. The HTA will bal-ance efforts to improve direct overseasservice into Neighbor Island airports withthe impact it may have on the viability ofHawaii’s critical inter-island air system.

F : Infrastructure and Support ServicesThe quality of the infrastructure can

be a major factor in the success or failure

of tourism product development andmarketing. Consequently, the Authorityintends to become a strong advocate forinvestments in infrastructure and supportservices to strengthen tourism andenhance residents’ quality of life. Ofparticular interest is the revitalization ofWaikiki and other key visitor destinationareas of the state. HTA’s assessment ofthe infrastructure and support servicesfor tourism has highlighted several areasof concern that the Authority intendsto address.

Sa fe tyThe HTA is concerned about enhanc-

ing Hawaii’s reputation as a relativelysafe destination. Providing a safe, secureenvironment for visitors and residents isimportant in any economy, but it is criti-cal for a resort destination. An actual oreven perceived increase in crimes againstvisitors can cripple a destination longafter the problem is mitigated. TheAuthority intends to proactively workwith industry and government to findways to maintain and improve that levelof safety and to ensure that safety inHawaii remains a positive factor in thevacation decision of visitors.

Waikiki RevitalizationWaikiki is the premier symbol and

usually the initial gateway for visitors tothe islands. Hawaii’s reputation as aresort destination is unavoidably linkedto the reputation of Waikiki. TheAuthority views the revitalization and“re-enchantment” of Waikiki as para-mount to the health of Hawaii’s visitorindustry, now and into the future. TheHTA intends to be proactive in advocat-ing tax and zoning initiatives to stimu-late capital investment in Waikiki toreconfigure and restore its lost attributes.

Hawaii’s AirportsThe HTA concludes that the arrival

experience of visitors and residents at theHonolulu International Airport and atother state airports is in need of improve-ment, particularly with the creation of a“Hawaiian sense of place” at thesefacilities. The Authority intends toactively promote improvements in archi-tecture, landscaping, art and airportsignage, to create “a Hawaiian experi-ence” for arriving passengers. The HTAwill also advocate infrastructure improve-ments at Neighbor Island airports. These

measures will help ensure that arriving,departing and traveling inter–island inHawaii enhances, rather than detracts,from the visitor experience and contrib-utes to the state’s competitive edge inthe world market.

Maintenance of Public FacilitiesHawaii’s parks, beaches, and other

facilities are key visitor and residentresources. However, the HTA has con-cluded that they are inadequately funded,developed, and maintained. The Author-ity intends to aggressively seek federalfunds for preservation of specific naturalattraction sites as well as for highwaybeautification and trail systems and otherinitiatives. The HTA believes this fundingcould help resolve some of the debateover funding for tourism development“vs.” preservation of natural resources.

Cruise Ship FacilitiesThe Authority has determined that

Hawaii’s cruise facilities are unattractiveand inadequate for the current andprojected needs of the industry. The HTAwill advocate multiple island ports andthe development of Neighbor Islandcruise facilities. The Authority alsointends to explore federal fundingopportunities for harbors and facilities toenhance and expand Hawaii’s marketshare in this burgeoning market.

G: Regulations and InvestmentI n c e n t i v e sThe HTA has found that tourism

policy and planning has been marked bytension both within government andamong government, private sector andcommunity stakeholders. The HTA willattempt to act as a catalyst for ongoingeducation and consensus building inrelationships for the development oftraditional and new tourism products.The Authority has expressed its commit-ment to the meaningful participation oflocal communities in planning new typesof tourism products.

The Authority also expressed concernthat the existing State land use systempresents fundamental obstacles to thedevelopment of non-traditional, low–impact forms of tourism. Existing landuse laws, in the Authority’s view, favoragriculture conservation over other useson lands controlled by the State. Thoselaws have not been substantially

continued on page 12

12 Hawaii’s Economy /July 1999

changed since their initial adoption,despite a fundamental shift in Hawaii’seconomy from agriculture to tourism.Moreover, the HTA found that Countyland use laws and approval processes arevery inflexible and make it difficult topermit, much less encourage, new formsof visitor accommodations andattractions.

The HTA has expressed its intentionto exercise a leadership role in securingchanges in planning, coordination oflaws and permitting procedures, in orderto support sustainable land uses relatedto tourism. The Authority argues thatrestructuring of these regulations wouldstimulate substantial capital investmentand permit the opening of private landfor diverse forms of eco–, edu–, and agri–tourism. The HTA believes this can beaccomplished while sustaining Hawaii’snatural and cultural resources, andcommunity values.

Finally, the Authority recognizes thestrong link between the goals of diversi-fying both tourism and the economy.The HTA will seek to link tourism witheconomic diversification by using tourismadvertising as a means to promoteHawaii products and to attract investorsin technology and other diversifiedeconomic activity.

ConclusionsSince the last report in Hawaii’s

Economy on revitalizing tourism, therehas been measurable progress towardsthe goal of revitalizing this critical indus-try. Most of the overall issues raised inthat report are being addressed.

In particular, the progress in restruc-turing tourism marketing and promotionsupport has resulted in a single agency,the Hawaii Tourism Authority, respon-sible for the development and marketing

of tourism. In addition the agency willhave roughly twice the annual fundingresources that were available in the past.With input from a broad spectrum ofcommunity interests, the HTA has estab-lished seven priority initiatives it willpursue, in order to discharge its responsi-bility to revitalize Hawaii’s rourismindustry. The Authority intends topursue these initiatives in cooperationwith the community, the industryand government.

The Hawaii Tourism AuthorityEstablished: By Act 156 State of Hawaii Legislature, 1998.Membership: Thirteen members appointed by GovernorMission Statement: To manage the strategic growth of Hawaii’s visitor

industry in a manner consistent with the economicgoals, cultural values, and community interests ofthe people of Hawaii.

Goa l s : Achieve managed growth of Hawaii’s tourism industry by focusingon increasing visitor expenditures. Average an annual growth rateof 4.6 percent in visitor expenditures through 2005.

Funding Source: Dedicated Tourism Funding: 2.75 percentage points of theTAT was dedicated to create an annual tourism fund ofapproximately $50 to $60 million.

Tourism Initiatives and Issues continued from page 11

The EmergingCruise Ship

Market

dedicated to recreation rather thantransportation. These new ships weredesigned to be floating resorts withswimming pools, gyms, restaurants, andin most cases, full-service casinos. Atypical cruise lasts a week or more andincludes one- or two-day stops at variousnon-U.S. Caribbean and Gulf ports.

Today the North American cruisemarket represents 90 percent of the

worldwide market. Caribbean cruises stillrepresent a sizable (46 percent) share ofthat market, but European cruises nowclaim a 20 percent share. Alaska hascarved out an 8 percent share of themarket. Mexico has about 5 percent,while Hawaii attracts about 2 percent ofthe North American market.

In an effort to improve efficiency in acompetitive market, ship owners arecommissioning increasingly largervessels — up to 3,100 passengers.These mega-ships can be built for anaverage cost of $160,000 per passengercompared with an average cost of$245,000 per passenger for ships de-signed to carry fewer than 1,500 people.Of course improved profitability from thenew larger ships depends on runningthese ships as close as possible to their3,000-plus passenger capacity.

The cruise ship industry has be-come a major force in the NorthAmerican vacation market. The

Cruise Lines International Associationestimates that just over 5 million Ameri-cans and Canadians took overnight orlonger cruises in 1997, up nearly9 percent from the year before.

Reinvention of theCruise Industry

In the early 1970s, the cruisebusiness began to reinvent itself in theCaribbean as a vacation format ratherthan as primarily a form of transporta-tion. As the market grew, cruise shipcompanies like the Carnival and HollandAmerica lines began upgrading theirfleets from the classic 600- to 800-passenger ship designs of the 1950s, tohuge 1,500- to 2,000-passenger ships

13Hawaii’s Economy /July 1999

American Hawaii CruisesThroughout the 1970s and 1980s,

Hawaii received periodic cruise ship visitsfrom overseas. While a strong tour boatindustry had developed for day orevening excursions, the availability ofovernight cruising was virtually non-existent. However, in 1985 AmericanHawaii Cruises (AHC) began operatingtwo 800-passenger cruise ships in Ha-waiian waters, the S.S. Constitution andthe S.S. Independence. In 1997, AHCtook the Constitution out of service dueto the high cost of refurbishing the ship.In 1988 a competing ship, the S.S.Monterey, entered the interisland market.But financial problems forced the with-drawal from service of the Monterey onlya year later. Since then, AHC has com-missioned construction of two new U.S.-built cruise ships of 2,000 passengerseach. The first is scheduled to enterservice in 2003 with the second shipentering service the next year. In themeantime, special federal legislation willpermit AHC to acquire a re-flagged,2,000-passenger foreign cruise ship forservice beginning in January 2000 tosupplement the Independence. The twoolder vessels would then be phased outof service. This same legislation will giveAHC exclusive rights to the Hawaii inter-island cruise market for at least 25 years.

AHC offers a seven-day cruise withstops at all major islands, starting atabout $1,230 per person. Variations in-clude “theme” cruises, which offer eitherbig band, whale watching, or HawaiianHeritage as the entertainment and activ-ity focus. These cruises do not permitgaming. AHC registered about 46,000passengers in 1998 but expects over140,000 for the year 2000 with theadditional ship. The passenger count isexpected to level off at about 190,000per year under the two-ship operation.

Hawaii andForeign Cruise Ships

Passengers on foreign cruise ships toHawaii jumped from about 28,000 in1997 to 42,000 in 1998. Under the U.S.Passenger Services Act (PSA) of 1886and the Jones Act, only U.S.-built and-operated ships may embark and debark

The Emerging Cruise Ship Market continued from page 12

passengers between U.S. ports. Foreignpassenger ships can stop at any numberof U.S. ports but passengers mustre-board the ship before it leaves port.This has required some rather creativelogistics to enable foreign ships to cruiseHawaii economically.

Passengers on foreign cruise shipswill either fly to Hawaii first, or fly homefrom Hawaii after their cruise. A typicalcruise scenario is a two-phase operationfrom the ship’s point of view. In the firstphase, U.S. and other passengers areembarked from either Ensenada, Mexicoor Vancouver, British Columbia. The ves-sel then spends about four days at seaand stops at Hawaii ports for the remain-ing four to five days of the ten-day tour,ending the cruise in Honolulu. Passen-gers then debark to either fly home orspend additional time in Hawaii. In phaseII, a new group of passengers whoarrived in Hawaii by air are embarked,tour the island ports, and finally spendfour days at sea, to be debarked inVancouver or Ensenada.

Building Cruise ShipInfrastructure

Consultants for the State HarborsDivision (the firm of Leo A. Daly) antici-pate that passengers on foreign cruiseships visiting Hawaii could reach100,000 by 2004, 200,000 by 2013,and as many as 340,000 by 2020.Coupled with American Hawaii Cruisesexpectations, Hawaii could be hostingnearly 400,000 cruise passengers in2005, before AHC’s Independence andtemporary foreign ship are decommis-sioned. The level might drop to about300,000 in 2006 but build slowly backup to over 500,000 by 2020.

To accommodate this potentialgrowth, the consultant report recom-mends about $54 million in a phase Iimprovement program for seven majorports in Hawaii from now through 2004,and an additional $43 in improvementsduring a phase II program from 2004 to2020. Phase I improvements would in-clude new terminal facilities at HonoluluHarbor’s Pier 2 and renovations andretrofits to Neighbor Island ports. Phase IIwould make major improvements to the

ports of Hilo, Hawaii, Kahului, Maui,Port Allen, Kauai, and Piers 19/20in Honolulu.

The report stressed that the improve-ments do not reflect an “if we build it,they will come” strategy, but are rather avery selective set of investment optionsdesigned to make the most productiveand resource–conserving improvementsto stay competitive in this market. Never-theless, the report expects that eitheradditional sources of revenues will beneeded to fund the improvements, orarrangements made for development offacilities by a t hird party.

Potential Impacts of theCruise Market

Should Hawaii aggressively court thismarket? One concern commonly raisedabout the increase in cruise activity is itspotential competition with land-basedresorts and hotels. The fear is that cruisesmay be diverting vacationers away fromhotels and local restaurants. On the otherhand, the cruise may be attracting visi-tors who were specifically looking for acruise opportunity and would have other-wise chosen a cruise to somewhere elserather than a land-based Hawaii vaca-tion. It is also argued that cruises couldprovide new visitors with a taste of whatHawaii has to offer and encourage repeatvisits to Hawaii’s land–based resortslater on.

Even though they do not stay inhotels, cruise passengers do add to theeconomy through their direct purchasesin the ports they visit and indirectlythrough the business spending by cruiseship operators. As the analysis on page___ shows, cruise ship activity in 1998supported an estimated 2,500 jobs in thestate and generated $73 million inhousehold income and more than $12million in revenues to the public sector.At a level of 400,000 cruise visitors inthe year 2005, as suggested by theHarbor’s consultant study, the numberof jobs generated could exceed 10,000,accompanied by over $300 million inhousehold income and $60 million inpublic revenues.

Another benefit of cruise ships is theircontinued on page 14

14 Hawaii’s Economy /July 1999

positive economic impact on the portsthat they visit. More cruise ship visitscould be a revitalizing agent for the com-munities of Hilo, Hawaii, Kahului, Mauiand Port Allen-Hanapepe on Kauai,which are outside of land-based resortareas. For the merchants of downtownHonolulu, a larger volume of frequentcruise ship passengers could create a newmarket for business during the eveningsand weekends. It could also provide abase for new visitor attractions. Finally, alarge number of visiting and home-portedcruise ships in Hawaii suggests an oppor-tunity to regenerate Hawaii’s ship repair

and maintenance industry, which hasbeen contracting for several decades.

Thus, it would appear that the cruisemarket could represent a very valuablenew visitor segment for the economy asa whole, although there is the possibilityof some diversion of visitors from land-based resorts. Cruises could introducenew visitors to Hawaii’s beauty andattractions. They may also offer theadded benefit of directing economicstimulus to geographical areas,businesses, and industry that have beenbypassed by the development of tourismover the past several decades.

Taking advantage of the cruise shipopportunity will mean making a commit-ment to improving the quality of portfacilities. It will also mean workingclosely with the cruise ship industry todevelop marketing strategy, new attrac-tions and special events. Such coordina-tion and planning could help ensure thatcruises are a profitable investment forHawaii and the industry, and a memo-rable experience for cruise passengersthat will motivate them to return to theislands and recommend Hawaii tofriends.

The U.S. Passenger Services ActIntroduct ion

The United States is one of many nationsthat protects its domestic transportationindustries through cabotage laws. Theselaws reserve to U.S.-flagged vessels the rightto transport cargo and passengers betweenU.S. ports. (Cabotage laws also apply toforms of transportation other than watercarriers such as airlines, but this articlefocuses exclusively on water carriers.)Cabotage has a long history in the UnitedStates. The current cabotage statute fortransportation of cargo is the MerchantMarine Act of 1920 and its amendmentspopularly known as the Jones Act. Thestatute covering cabotage as it applies topassengers is known as the PassengerServices Act and became law in 1886.1

Proponents of cabotage laws make twomain arguments. First, cabotage laws protectnational defense interests by preserving bothan active merchant marine and a domesticshipbuilding industry. In the past, bothindustries proved vital to the efficient pros-ecution of national defense interests duringtimes of war. Second, cabotage laws protectnational economic interests in the form ofAmerican jobs and businesses from low-wage, subsidized, unsafe and/or environ-mentally reckless foreign competitors.

Those advocating reform of the cabotagelaws take issue with these points. Someargue that much of the defense justificationno longer applies because technological

change has made ocean shipping a non-viable method for achieving many nationaldefense goals. Further, defense needs requirespecially-built craft rather than modifiedcommercial vessels. No U.S.-flagged, ocean-going passenger vessels have been built inthe United States since 1951, and thereexists only one U.S.-flagged passengervessel currently in operation (the S.S. Inde-pendence operating in Hawaii). Others arguethat maritime wages are increasingly set inan international marketplace and thatforeign government subsidies of foreignvessels accrue to the benefit of consumers.Finally, opponents argue that there are other,more efficient and direct methods than cabo-tage of enforcing safety and environmentallaws in the United States.

The Passenger Services ActThe PSA became law in 1886 and has

been a part of U.S. cabotage law since. Thefull text of the statute as it now applies inthe U.S. reads as follows:

No foreign vessel shall transpor tpassengers between ports or placesin the United States, either directly or byway of a foreign por t, under apenalty of $200 for each passengerso transported and landed.

Over time, a number of exceptions havebeen made to this requirement. Canadianvessels may transport passengers between

Rochester and Alexandria Bay, New Yorkand between southern Alaska and U.S. portsuntil an American carrier enters the markets.Similarly, foreign vessels may transport pas-sengers between Puerto Rico and the U.S.mainland as long as a U.S. carrier does notprovide such service.2 Foreign-flagged cruiseships may carry passengers from a U.S. portas long as they return them to the same port(a “cruise to nowhere”). Foreign vesselsmay also call at intermediate U.S. ports aslong as no passenger permanently leaves thevessel at those ports and the vessel makes atleast one call at a foreign port.

The PSA operates in conjunction with theJones Act and other shipping laws to definevessels authorized to carry passengers in thecoastwise trades. Under the Jones Act, U.S.-flag vessels must be built in the UnitedStates, owned by U.S. citizens, and docu-mented under the laws of the United States.Documentation means “registered, enrolled,or licensed under the laws of the UnitedStates.” In addition, all officers and 75% ofthe crew must be U.S. citizens. Vessels thatsatisfy these requirements comprise the“Jones Act fleet.”

1 The Passenger Services Act has also been referred to as thePassenger Vessel Act and the Passenger Ship Act.

2 These exceptions are discussed in C. Todd Jones (1995),“The Practical Effects on Labor of Repealing American Cabo-tage Laws,” 22 Transportation Law Journal 403, 412-413.

The Emerging Cruise Ship Market continued from page 13

15Hawaii’s Economy /July 1999

Economic ImplicationsThere are two important economic impli-

cations of the PSA as it applies to Hawaii.First the PSA prevents foreign cruise shipsfrom transporting passengers betweenAlaska or the U.S. West Coast and Hawaii.Second, the law prevents foreign cruisevessels from picking up and transportingpassengers for cruises among the HawaiianIslands. As a consequence, there currently isno cruise ship offering service from Alaskaor the West Coast to Hawaii, and there isonly one cruise ship line that operatesamong the Hawaiian Islands.

Currently the Jones Act fleet containsonly one ocean-going passenger vessel, andit operates exclusively in Hawaii. Untilrecently Great Hawaiian Cruise Line Inc.,doing business as American Hawaii Cruises,operated the S.S. Constitution and the S.S.Independence offering cruises among theHawaiian Islands. Both ships were built in1951 and are relatively small by today’sstandards for cruise vessels (the Indepen-

dence has 747 berths and the Constitutionhad 779 berths, compared with morerecently-built ships with 1,800 to 2,000berths each). In 1996, American HawaiiCruises announced that the Constitutionwould not return to service because ofexcessive cost of repairs.

While the PSA prevents foreign cruiseships from carrying passengers directly fromAlaska and the West Coast to Hawaii andfrom competing with American HawaiiCruises for interisland cruise traffic, foreignvessels do visit Hawaii. Between 20 and 25foreign cruise ships visit Hawaii in a givenyear. American passengers on foreign cruiseships to Hawaii must board in anothercountry—typically, Vancouver, Canada orEncinada, Mexico. These ships cannot pickup a passenger in one U.S. port and drop offthe passenger in another U.S. port. However,after arriving from Canada or Mexico, theymay tour the islands and drop off passengersin Hawaii. They may then pick up newpassengers, tour the islands, and return to

The U.S. Passenger Services Act continued from page 14

Canada or Mexico. As a consequence, theseforeign cruise ships made approximately 230calls in Hawaii portsduring 1998.

Recent LegislationIn October 1997, federal legislation was

passed that permits a person to operate aforeign-built cruise ship in the U.S. coast-wise trade provided that the person hasentered a binding contract for the delivery oftwo U.S.-built cruise ships. The first shipmust be delivered no later than January 1,2005, and the second ship must be deliveredno later than January 1, 2008. Moreover, inHawaii, only the existing cruise ship opera-tor may operate a foreign-built ship amongthe islands unless a new U.S.-built cruiseship is placed into regular service outside ofHawaii. This legislation makes it possible totemporarily employ a foreign-built vesselamong the Hawaiian Islands despite thePassenger Services Act while new U.S.-builtcruise ships are constructed.

Developingthe NicheMarkets

cultural trip or both. Finally, almost 62million Americans reported taking anaverage of 2.5 “romantic” trips in themost recent year. Foreign travelers are alsogravitating towards more specialized andinvolved vacation experiences. 1

Niche MarketsThe emerging demand for such specialty

vacations is referred to as the tourism“niche” markets in the HTA’s TourismStrategic Plan. The Authority has identifiedseven niche markets upon which it willfocus its product development efforts. Theplan offers a number of “strategic directions”for each niche market.

Agri–TourismThe HTA plan notes that Hawaii has a

rich tradition of agricultural activities, manyof which are unusual in the U.S. and whichmany visitors may find very interesting.Hawaii has its share of traditional ranchingand crop raising. But our varied climate andresources enable the state to also produce ahost of unusual products such as pineapple,coffee, macadamia nuts, taro, and varietiesof fish in fishpond environments.

Of course, pineapple has been an attrac-tion for visitors for many years, particularlythe Dole Visitor Center in Central Oahu.Visitor sites also exist for ranching andcoffee growing on the Big Island. The vastinventory of agricultural activity around theislands could attract a wider niche market,

Warm sunny weather and picture–postcard white sand beaches arenot unique to Hawaii. Competi-

tion has increased significantly from newresorts in Mexico, Guam, Okinawa, theCaribbean, and Australia that possess andmarket similar assets. An important strategyfor reinvigorating Hawaii tourism is to carveout new markets based on unique assets ofthe islands, which would permit the state todevelop and maintain a stronger competitiveadvantage.

Increasing Sophisticationof Travelers

Fortunately for Hawaii, Americans andforeign travelers are becoming very sophisti-cated. They are not only looking for differentexperiences, but are also looking for moremeaningful experiences. A recent survey forthe U.S. Travel Data Center shows that verylarge numbers of Americans are seeking outmore active and interesting vacation experi-ences. For instance, in the past five years,98 million Americans have taken an adven-ture vacation ranging from camping towhite-water rafting. Nearly 66 millionAmericans have taken either a historical or