Embed Size (px)

Citation preview

Opportunities for Optimism?

A New Vision for Value in Asset Management

EXECUTIVE SUMMARY

Fit to Win

Positive Outlook

Asset Managers

New Rivalries

Featuring the findings of the State Street 2015 Asset Manager Survey.

Asset managers are on the threshold of a new era. As assets under management continue to rise, State Street’s research finds the industry’s leading players jostling to catch the next wave of growth.

79%

of asset managers expect new competition from a non-

traditional market entrant such as a technology firm

ASSET MANAGERS EXECUTIVE SUMMARY

OPPORTUNITIES FOR OPTIMISM?

Our global survey of 400 asset managers shows that leading players in the industry are finding new ways to create value for their clients.1 They are revamping their investment strategies, upgrading their capabilities, and hunting for acquisitions that could extend their expertise or reach.

Optimism must be tempered by an awareness of new risks. Costs are under scrutiny. Clients want “more bang for their buck.” Competition is also intensifying — not just from traditional rivals but from tech-savvy challengers. Indeed, a comparison with our 2014 study shows some significant shifts in asset managers’ perceptions of risk and opportunity.

The most enterprising asset managers are responding by “bringing more to the table” in their client relationships. Delivering greater value to customers doesn’t just mean achieving consistently high returns. It means forging closer partnerships with investors based on a transparent dialogue around risk and performance. It will also require asset managers to develop the capabilities to customize their investment solutions around their clients’ long-term needs.2

New Sources of Value, New Forces for ChangeAsset managers are playing for high stakes. A rising market creates opportunities on multiple fronts — for those that are agile enough to seize them. Over four-fifths of asset managers (88 percent) in our survey see opportunity for profitable growth in the next 12 months.

Asset managers are racing to develop new offerings to meet changing client demands. Over three-quarters of asset managers (78 percent) say that a greater proportion of client assets will move to bespoke solutions over the next five years. They are also improving their distribution networks and operational capabilities to support these new areas of growth.

At the same time, the industry faces new competitive pressures. Almost four out of five executives (79 percent) in our survey say they will face direct competition from non-traditional market entrants. Technology players like Google, Apple and Alibaba Group could mount a serious challenge. Asset managers also find themselves competing with their clients’ own investment talent, as large investors bring more asset management in-house.

1 State Street 2015 Asset Manager Survey conducted by FT Remark in April and May 2015. Unless otherwise noted, all data in this summary originates from this survey. See back cover for full methodology.

2 See The Folklore of Finance: How Beliefs and Behaviors Sabotage Success in the Investment Management Industry, Center for Applied Research, 2015. This report explores some of the steps that the industry can take to improve long-term outcomes for investors.

1

2 OPPORTUNITIES FOR OPTIMISM?

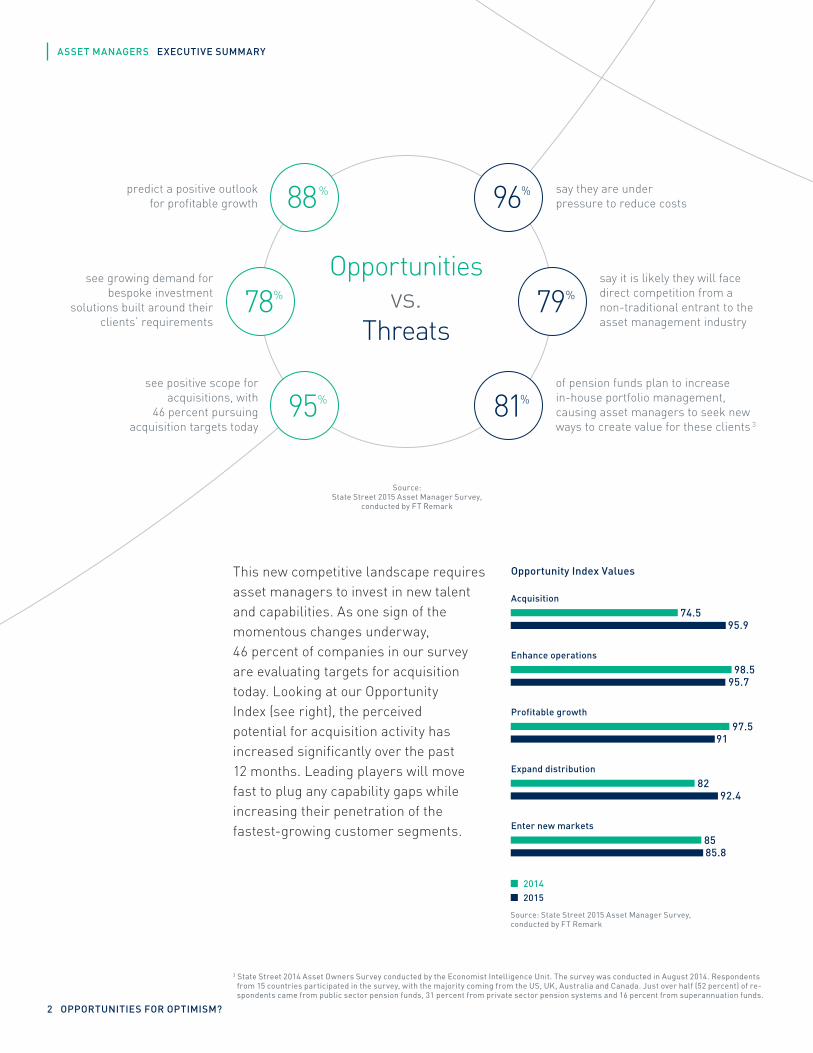

Opportunitiesvs.

Threats

96%

79%

81%

say they are underpressure to reduce costs

say it is likely they will face direct competition from anon-traditional entrant to theasset management industry

of pension funds plan to increasein-house portfolio management,causing asset managers to seek newways to create value for these clients 3

95%see positive scope for

acquisitions, with46 percent pursuing

acquisition targets today

78%see growing demand for

bespoke investmentsolutions built around their

clients’ requirements

88%predict a positive outlookfor profitable growth

Source: State Street 2015 Asset Manager Survey,

conducted by FT Remark

3 State Street 2014 Asset Owners Survey conducted by the Economist Intelligence Unit. The survey was conducted in August 2014. Respondents from 15 countries participated in the survey, with the majority coming from the US, UK, Australia and Canada. Just over half (52 percent) of re-spondents came from public sector pension funds, 31 percent from private sector pension systems and 16 percent from superannuation funds.

Acquisition

74.595.9

Enhance operations

98.595.7

Profitable growth

8292.4

Expand distribution

Enter new markets

8585.8

20142015

Opportunity Index Values

97.591

This new competitive landscape requires asset managers to invest in new talent and capabilities. As one sign of the momentous changes underway, 46 percent of companies in our survey are evaluating targets for acquisition today. Looking at our Opportunity Index (see right), the perceived potential for acquisition activity has increased significantly over the past 12 months. Leading players will move fast to plug any capability gaps while increasing their penetration of the fastest-growing customer segments.

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

ASSET MANAGERS EXECUTIVE SUMMARY

Asset managers reshape the product mix around new client needsAsset managers are adapting their capabilities to meet investors’ growing demands for multi-asset, outcome-oriented solutions. This is a major test of their capabilities. Instead of selling by product line, solution providers need to consult, design and market investment strategies around investors’ long-term objectives.

There is more than one way to create value for clients, and low-cost passive strategies are part of the growth story for many asset managers. The industry is also investing heavily in hybrid products that combine some of the strengths of active and passive management.

Large numbers of asset managers in the survey are expanding their presence in smart beta mutual funds. They are also positioning themselves to capture growing demand for liquid alternatives.

Asset managers are rethinking their product mix to address their clients’ changing requirements. Indeed, product innovation, rather than new markets, is increasingly viewed as the primary route to growth.

• 42 percent of asset managers in our survey are preparing to enter a new product category for the first time

• Almost a fifth (19 percent) will launch a product in the multi-asset solutions space for the first time over the next three years

• More than one in five (22 percent) will launch a liquid alternative product for the first time

• Smart beta mutual funds and smart beta exchange-traded funds (ETFs) are other areas that asset managers are considering for product launches

• 52 percent of respondents plan to expand their existing distribution network, while only 35 percent are preparing to enter new markets

“If you’re not a mega-firm or a low-cost provider, then you’ll need to have a specialty that you are renowned for. Mid-level players that can’t differentiate are going to come under real pressure.”

NEIL BATHON

Founder, FUSE Research Network

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

For each of the following product types, pleaseindicate whether your firm expects to launch aproduct for the first time in the next three years.

Smart/strategic beta mutual funds

5%

Multi-asset solutions

19%

Liquid alternative strategies

22%

Smart/strategic beta ETFs

7%

7%Offshore-domiciled funds

Other ETFs

9%

Our research identifies four emerging “value drivers” that may shape success in the future industry landscape:

VALUE DRIVER

#1

3

Client services become more personalized and transparentClients are being more hands-on with their portfolios. They want more information and insight from their asset managers to help them manage their money. Leading asset managers are ready to be more transparent about all aspects of investment performance and risk. They are learning to work in close partnerships with their institutional clients.

• 79 percent of asset managers say client demands for increased transparency on how their money is managed are having a moderate to significant impact on their business strategy

• 77 percent now offer their clients more transparency on sources of risk and return

• 74 percent say their clients’ growing need for customized solutions and services is shaking up their business models

• Only 36 percent are highly confident in their ability to use advanced analytics to segment clients according to their characteristics and needs

• Only 10 percent rate their process for gathering client feedback on how they are delivering against expectations at more than 8 out of 10

Despite a willingness to work more closely with their clients, few asset managers in our survey are gaining the customer insight

required to drive strategic decision-making around investor needs.

Asset managers will need customer analytics tools that can segment clients according to their characteristics and needs. The desire to build long-term partnerships with their customers will also require asset managers to develop better feedback mechanisms to understand how they are delivering against client expectations.

VALUE DRIVER

#2

For each of the following investor trends, please indicate the extent to which it is impacting your firm’s business strategy, in terms of shaping your products and how you deliver them.

(% indicating "significant impact")

Investor demand for more transparency into the investment process

44%

Investor demand for multi-asset, outcome-oriented investment strategies

36%

Investor adoption of factor-based allocation models

34%

Investor demand for impact investing strategies

32%

Investor demand for liability-driven investing strategies

31%

Investor demand for increased customization

31%

Investor demand for passive investment strategies

24%

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

ASSET MANAGERS EXECUTIVE SUMMARY

4 OPPORTUNITIES FOR OPTIMISM?

77%

of asset managers now offer their clients

more transparency on risk and return

Leading asset managers are ready to be more transparent about all aspects of investment performance and risk. They are

learning to work in close partnerships with their

institutional clients.

5

“We’ve created a specialized team to deliver bespoke asset allocation solutions for institutional clients, and customized risk management is a key part of our value proposition there.”FERDINAND HAAS

Global Co-Head of Active Investments at Deutsche Bank Asset Management

ASSET MANAGERS EXECUTIVE SUMMARY

6 OPPORTUNITIES FOR OPTIMISM?

VALUE DRIVER

#3New ideas around risk will shape the dialogue with investorsRisk issues are at the heart of the conversation between asset managers and their clients. Asset managers with the analytics tools to support new levels of risk insight may gain a competitive edge.

While our survey respondents report that their concerns around regulatory risk have subsided to some extent over the last 12 months, this is partly because the industry continues to make substantial investments in compliance.

• 72 percent of asset managers say their conversations with clients have evolved to focus more heavily on risk

• 61 percent say clients are demanding a more personalized approach to help them understand their risks

• 64 percent say that heightened risk and compliance demands threaten to divert resources from critical business areas

Leading asset managers will need more robust methods to understand risks across complex multi-asset portfolios. This entails being able to integrate their risk analytics across multiple asset classes. The leaders are also designing more advanced risk models that can be customized to their clients’ needs.

Our conversations with clients have evolved to focus more heavily on risk

50%22%

Our clients are demanding a more personalized approach to help them understand their risks

38%23%

We have increased the level of transparency we offer to clients on their sources of risk and return

37%41%

Heightened risk and compliance demands threaten to divert our firm’s resources away from other critical business areas

39%25%

Our firm is spending more time and resources on educating the boards of our institutional clients on risk issues

44%31%

Somewhat agreeStrongly agree

Please rate your level of agreement or disagreement with the following statements, relative to one year ago.

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

7

VALUE DRIVER

#4Advanced operations can deliver value at scaleDespite the positive outlook, asset managers see no relief from the pressure to bring down costs. Investors are willing to reward managers that can deliver discernible value, yet as competition increases there is no room for complacency.

Asset managers must support demand for outcome-oriented solutions at the same time as improving cost efficiency. Leading players are pursuing the operational efficiencies that will enable them to provide personalized service and better investment insights at a competitive price point.

Advanced technology will underpin the new offerings, providing investment managers with a much richer and more complete view of risk and performance across their client portfolios. Another recent State Street survey showed that 81 percent of asset managers have increased their investment in technology by more than 5 percent over the past three years.4 Managers may also need to find more cost-effective ways to keep pace with technology innovation — for example by outsourcing or by partnering with fintech start-ups.

• Only 4 percent of asset managers in our survey feel no pressure to reduce costs

• Only 36 percent are highly confident they have the analytical tools to segment their clients according to their characteristics and needs

• Only 33 percent are highly confident that their current operating infrastructure will support their future distribution strategy

Source: State Street 2015 Asset Manager Survey, conducted by FT Remark

Thinking about the cost pressures facing your business today, how would you describe the environment?

33%Slight pressure to reduce costs

15%High pressure to reduce costs

4%No pressureto reduce costs

48%Moderate pressureto reduce costs

4 State Street 2014 Data and Analytics Survey conducted by Longitude Research. This global survey of 400 senior executives at investment firms was conducted in October and November 2014. The respondents were drawn from 11 countries, with the majority from the US, China, France, Germany and the UK. The full survey sample is split evenly between asset managers and asset owners.

ASSET MANAGERS EXECUTIVE SUMMARY

8 OPPORTUNITIES FOR OPTIMISM?

Moving Up the Value ChainAsset managers see opportunities ahead. But they will need to demonstrate where and how they create enduring value for their clients to achieve long-term success.

Our research sheds light on several important questions as asset managers adapt to the new landscape:

• How should asset managers improve their client proposition and competitive positioning, based on their specific capabilities?

• How can asset managers forge closer partnerships with investors, and develop the skills needed to thrive in the new environment?

• What steps can asset managers take to provide clients with the integrated yet highly granular view of portfolio risk they need?

• How can asset managers develop innovation models that will fend off the threat from new market entrants?

• Where should asset managers prioritize their infrastructure investment to be more transparent, insightful and cost efficient for their investors?

To learn more, request our report: “Opportunities for Optimism? A New Vision for Value in Asset Management.” statestreet.com/assetmanagers

Asset managers must support demand for outcome-oriented solutions at the same time as

improving cost efficiency.

9

Investing involves risk including the risk of loss of principal. The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Corporation’s express written consent. The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor. All material has been obtained from sources believed to be reliable. There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information. The views expressed in this material are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

© 2015 State Street Corporation - All Rights ReservedCORP-1474

Expiration date: 06/30/2016

About the Research

This report is based on a State Street survey of 400 senior executives in the asset management industry. The State Street 2015 Asset Manager Survey was conducted by FT Remark in April and May 2015. Respondents from 23 countries participated, with the majority from Australia, Canada, China, Germany, Japan, Switzerland, the UK and US. Respondents manage assets for both institutional and retail clients, spanning traditional and alternative strategies.

Request our report: “Opportunities for Optimism? A New Vision for Value in Asset Management.” statestreet.com/assetmanagers

For more information about our solutions for asset managers, please contact:

Kevin Sek Chun Wong+852 2103 0203 [email protected]

Jane Mancini+1 617 662 2476

Jörg Ambrosius+49 89 55878 133 [email protected]