Embed Size (px)

Citation preview

Money Matters: Number 00.07December 2000

This glossary is a resource document containing terms and acronyms commonly used by and inlegislative fiscal committees, and in the discussion of state budget and tax issues. The firstsection contains terms and abbreviations used in all fiscal committees. The remaining sectionscontain terms for particular budget subject areas, organized according to fiscal committeejurisdictions.

For further information, please contact the Chief Fiscal Analyst or the fiscal analyst assigned tothe respective House fiscal committee and subject area. A directory of the House Fiscal AnalysisDepartment personnel and their assignments appears on the next page.

Fiscal Analysis DepartmentMinnesota House of Representatives

A Glossary of Fiscal Terms & Acronyms

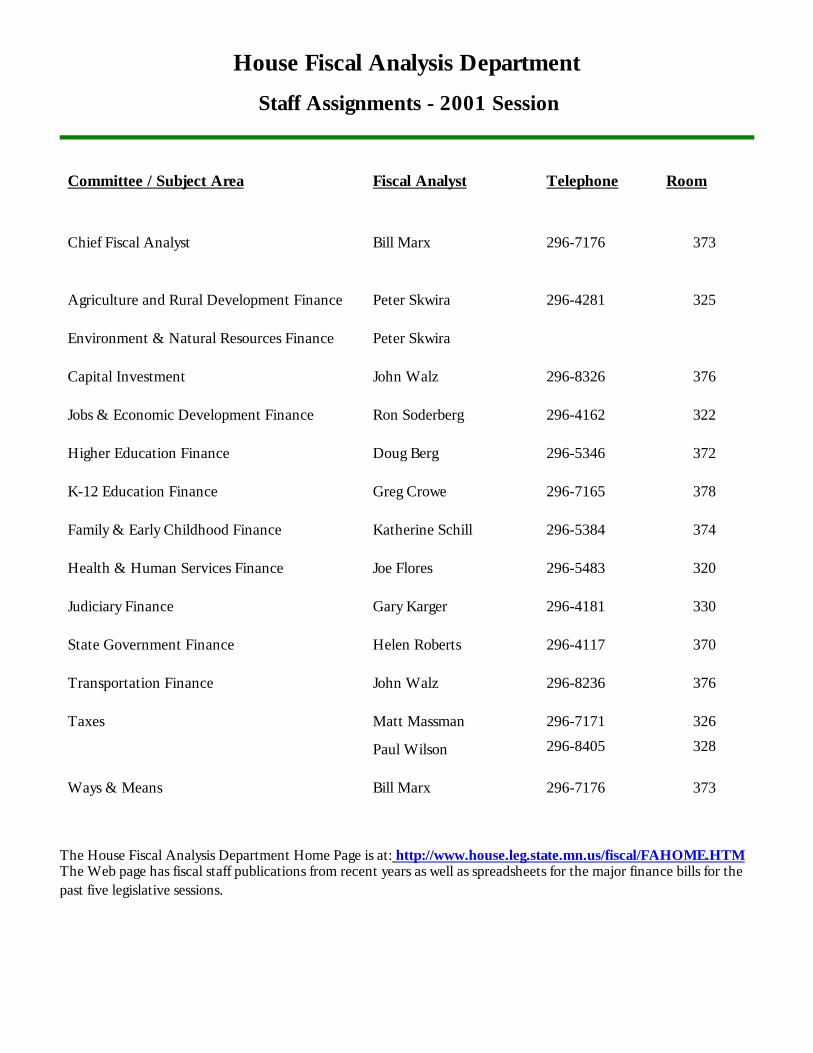

House Fiscal Analysis Department

Staff Assignments - 2001 Session

Committee / Subject Area Fiscal Analyst Telephone Room

Chief Fiscal Analyst Bill Marx 296-7176 373

Agriculture and Rural Development Finance Peter Skwira 296-4281 325

Environment & Natural Resources Finance Peter Skwira

Capital Investment John Walz 296-8326 376

Jobs & Economic Development Finance Ron Soderberg 296-4162 322

Higher Education Finance Doug Berg 296-5346 372

K-12 Education Finance Greg Crowe 296-7165 378

Family & Early Childhood Finance Katherine Schill 296-5384 374

Health & Human Services Finance Joe Flores 296-5483 320

Judiciary Finance Gary Karger 296-4181 330

State Government Finance Helen Roberts 296-4117 370

Transportation Finance John Walz 296-8236 376

Taxes Matt Massman

Paul Wilson

296-7171

296-8405

326

328

Ways & Means Bill Marx 296-7176 373

The House Fiscal Analysis Department Home Page is at: http://www.house.leg.state.mn.us/fiscal/FAHOME.HTM The Web page has fiscal staff publications from recent years as well as spreadsheets for the major finance bills for thepast five legislative sessions.

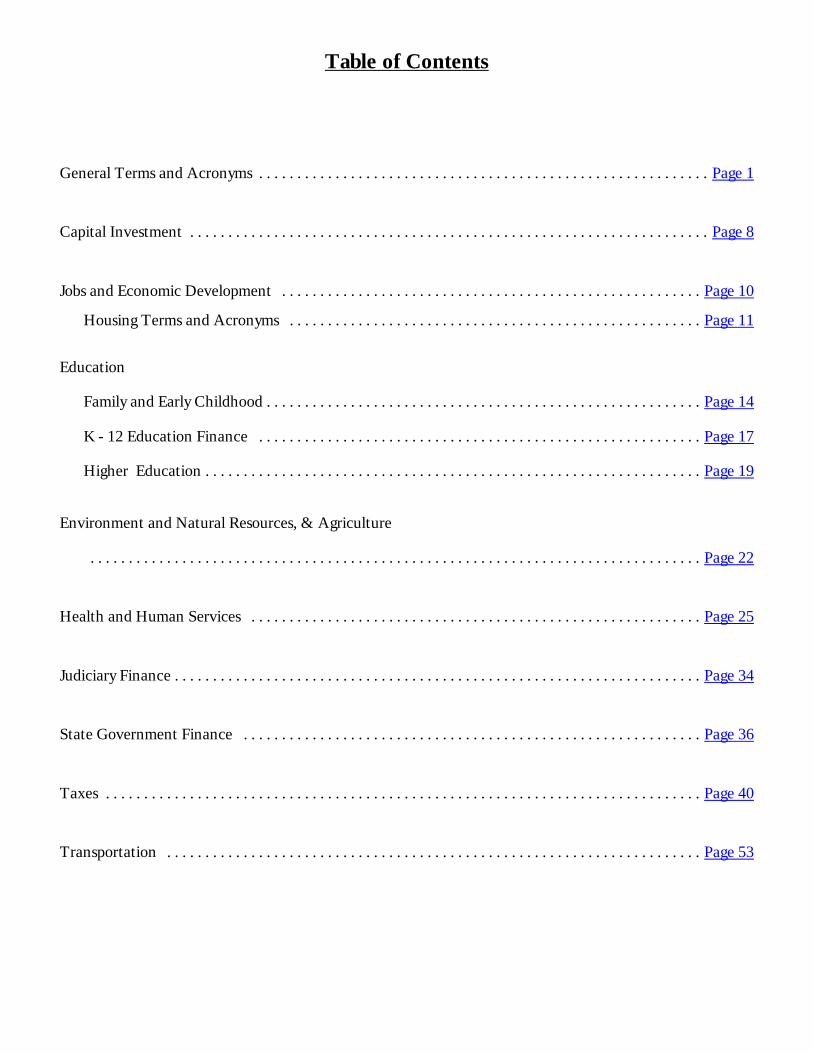

Table of Contents

General Terms and Acronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 1

Capital Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 8

Jobs and Economic Development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 10

Housing Terms and Acronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 11

Education

Family and Early Childhood . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 14

K - 12 Education Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 17

Higher Education . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 19

Environment and Natural Resources, & Agriculture

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 22

Health and Human Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 25

Judiciary Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 34

State Government Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 36

Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 40

Transportation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 53

General Fiscal and Budget Terms, Page 1

General Terms and Acronyms

Appropriation - Authorization by the Legislature tospend money from the state treasury for purposesestablished in law. The Minnesota Constitution prohibitspayment of money out of the treasury unless authorizedby an appropriation. (Also see standing appropriation anddirect appropriation.)

Appropriations Cap - Legislatively-placed limits onspending in the biennium following the budget periodunder consideration (i.e., budget “tails”). Caps allowspending projections to be lower than they wouldotherwise be under current law; that is, lower than ifcurrent spending levels were projected forward.

Allotment - Administratively-placed limits on theamount to be spent or encumbered for a legislatively-authorized purpose. Agencies develop a spending planbased on appropriations; then money is allotted for eachexpenditure. In the accounting system, allotments act asa control, prohibiting spending beyond the establishedlimits.

Annualization - The practice of adjusting spendingtotals to determine the annual costs of programs thatwere funded for only a portion of the previous year. Forexample, the annualized cost of a program that cost$500,000 for six months of operation is $1,000,000.

Balanced Budget - The requirement imposed on thestate’s general fund biennial budget that revenues mustbe greater than or equal to expenditures. Theconstitution authorizes borrowing for cash flow purposeswithin a biennium only (Article XI, Section 6).

Base - Usually calculated from the most recent amountspent by an agency for a program, the base is the agency’scurrent spending level with adjustments made for costsnot likely to recur. The base is determined frominformation in legislative tracking spreadsheets andlanguage in appropriations bills.

Base Adjustments - Adjustments to the base budgetallowed by the Executive Branch in the Governor’sbudget recommendations. “Technical” base adjustments

are those that make adjustments to a base to conformwith legislative directions. “Policy” or “Current ServiceLevel” base adjustments allow the Governor to recognizecertain cost adjustments (such as salary increases or leasecost increases) as part of the budget base rather than asa change request.

Biennial Budget Documents - Budget documentscontain narrative and fiscal information at the budgetactivity level for each state agency and is distributed inseveral loose-leaf notebooks. M.S. 16A.11 requires theGovernor to submit his budget message and detailedoperating budget recommendations by the fourthTuesday in January in odd-numbered years. (However, inthe year following the election of a new Governor, thebudget recommendations must be submitted by the thirdTuesday in February.) The Department of Finance isrequired to submit the final budget format, agency plansand budget estimates to the Legislature by November 30of the year prior to release of the Governor’s budget. TheFinance Department is also required to seek theinvolvement of the Legislature in developing budgetforms and instructions, and in designing the budgetdocument format.

BBS, Biennial Budget System - The informationsystem used by the Department of Finance to prepare thebudget documents, and by the executive and legislativebranches of government to keep track of appropriations.

Biennium - Minnesota has a two year (biennial) budgetperiod. The Legislature appropriates the major portionof the budget in the odd-numbered year session, andmakes adjustments as needed during the even-numberedyears. For example, the FY 2002-03 biennium wouldbegin at midnight on June 30, 2001 and would end atmidnight June 30, 2003.

Budget - The plan or authorization for revenues andexpenditures in a fixed period of time. State law (M.S.16A.11 Subd.2) requires the Governor to present abalanced budget to the Legislature for consideration inJanuary of each odd numbered year. The budget issubmitted in three parts: (1) the Governor’s budgetmessage, including a summary and the Governor’s

House Fiscal Analysis Department, December 2000

General Fiscal and Budget Terms, Page 2

recommendation on state financial policy, (2) thedetailed operating budget and (3) the detailed capitalbudget.

“Off-budget” - Non-General Fund revenues andexpenditures, pass-through funds, certain dedicatedmonies, intergovernmental revenues and inter-fundtransfers.

“On budget” - Part of the General Fund.

Supplemental Budget – Refers to either (1) thebudget considered in even-numbered years or (2)changes to the original budget documents submittedby the Governor (usually based on revised estimatesof forecasted revenues

and expenditures).

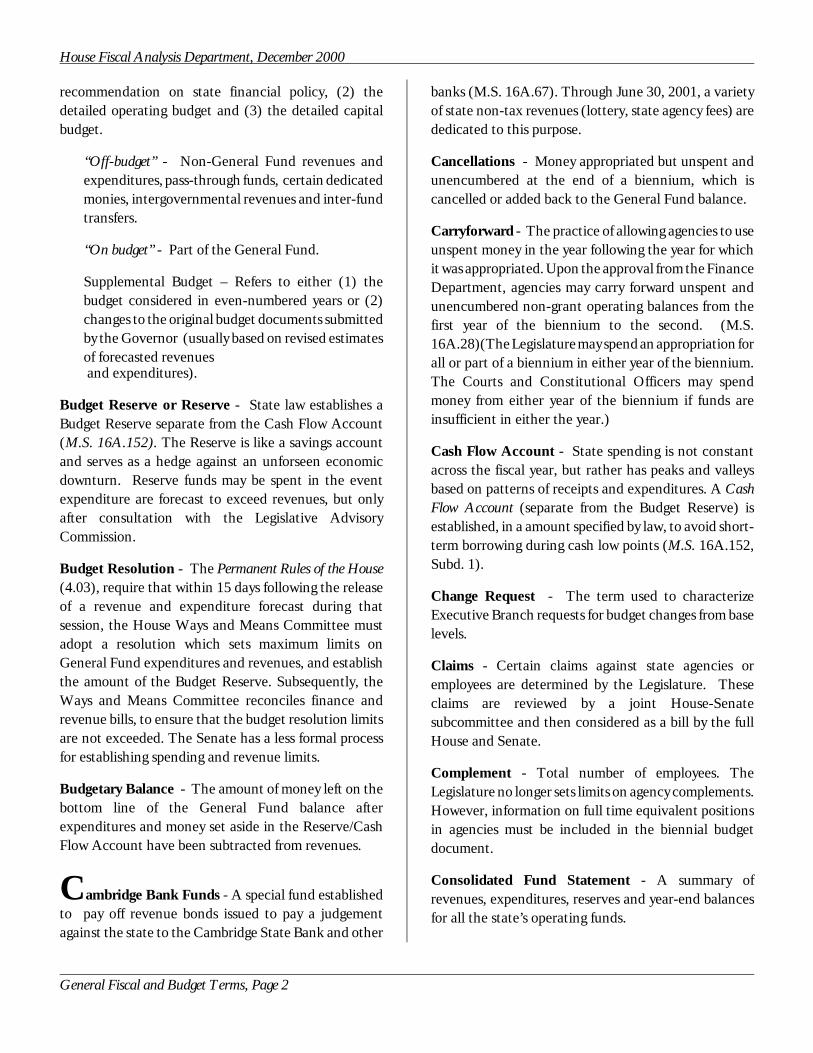

Budget Reserve or Reserve - State law establishes aBudget Reserve separate from the Cash Flow Account(M.S. 16A.152). The Reserve is like a savings accountand serves as a hedge against an unforseen economicdownturn. Reserve funds may be spent in the eventexpenditure are forecast to exceed revenues, but onlyafter consultation with the Legislative AdvisoryCommission.

Budget Resolution - The Permanent Rules of the House(4.03), require that within 15 days following the releaseof a revenue and expenditure forecast during thatsession, the House Ways and Means Committee mustadopt a resolution which sets maximum limits onGeneral Fund expenditures and revenues, and establishthe amount of the Budget Reserve. Subsequently, theWays and Means Committee reconciles finance andrevenue bills, to ensure that the budget resolution limitsare not exceeded. The Senate has a less formal processfor establishing spending and revenue limits.

Budgetary Balance - The amount of money left on thebottom line of the General Fund balance afterexpenditures and money set aside in the Reserve/CashFlow Account have been subtracted from revenues.

Cambridge Bank Funds - A special fund establishedto pay off revenue bonds issued to pay a judgementagainst the state to the Cambridge State Bank and other

banks (M.S. 16A.67). Through June 30, 2001, a varietyof state non-tax revenues (lottery, state agency fees) arededicated to this purpose.

Cancellations - Money appropriated but unspent andunencumbered at the end of a biennium, which iscancelled or added back to the General Fund balance.

Carryforward - The practice of allowing agencies to useunspent money in the year following the year for whichit was appropriated. Upon the approval from the FinanceDepartment, agencies may carry forward unspent andunencumbered non-grant operating balances from thefirst year of the biennium to the second. (M.S.16A.28)(The Legislature may spend an appropriation forall or part of a biennium in either year of the biennium.The Courts and Constitutional Officers may spendmoney from either year of the biennium if funds areinsufficient in either the year.)

Cash Flow Account - State spending is not constantacross the fiscal year, but rather has peaks and valleysbased on patterns of receipts and expenditures. A CashFlow Account (separate from the Budget Reserve) isestablished, in a amount specified by law, to avoid short-term borrowing during cash low points (M.S. 16A.152,Subd. 1).

Change Request - The term used to characterizeExecutive Branch requests for budget changes from baselevels.

Claims - Certain claims against state agencies oremployees are determined by the Legislature. Theseclaims are reviewed by a joint House-Senatesubcommittee and then considered as a bill by the fullHouse and Senate.

Complement - Total number of employees. TheLegislature no longer sets limits on agency complements.However, information on full time equivalent positionsin agencies must be included in the biennial budgetdocument.

Consolidated Fund Statement - A summary ofrevenues, expenditures, reserves and year-end balancesfor all the state’s operating funds.

House Fiscal Analysis Department, December 2000

General Fiscal and Budget Terms, Page 3

Contingency Funds - An appropriation(s) that may bespent with approval of the Legislative AdvisoryCommittee when the Legislature is not is session, tomeet emergencies. In a typical biennium, less than $1million in total is available for the contingency accountfrom the General Fund, the State Government SpecialRevenue Fund, and the Workers Compensation Fund

CPI-U, Consumer Price IndexSSUrban - A measure ofinflation intended to capture the increased prices facingconsumers for a fixed market basket of services andgoods, including food, housing, transportation, clothing,medical care, and entertainment.

Current Spending - Similar to “base” in meaning. TheDepartment of Finance defines current spending asactual spending with adjustments, such as removing one-time appropriations or non-recurring expenditures. Formost agencies, current spending is less than actualspending and usually is the base on which the budget isbuilt.

Debt Service Fund - See “Capital Investment” section.

Dedicated Revenue or Expenditures - Money raisedand earmarked to be spent for specific purposes.

Departmental Earnings - Money collected by stateagencies through service user fees, occupational licensecharges, regulatory charges, special taxes andassessments and other revenues. In general, agencies arerequired to set charges at levels that ?neithersignificantly over recovers nor under recovers costs,including overhead costs, involved in providing theservices” (M.S. 16A.1285).

Direct Appropriation - An appropriation for a specificamount of money, for use only during a specific timeperiod. Most appropriations in omnibus bills are directappropriations. Appropriations are usually for a singleyear of the biennium; however, legislation occasionallymakes single year appropriations available either year ofthe biennium.

Earmark - To dedicate or designate a revenue streamfor a specific purpose or expenditure.

Encumbrance - Commitment of money to meet anobligation that is expected to be incurred to pay forgoods or services received by the state, or to pay a grant.Encumbrance is the accounting control device thatagencies use to reserve portions of their allotments forexpenditures that will soon be incurred. Agencies mustencumber money before they can spend it, providing asystem to keep track of outstanding obligations.

Enterprise Funds - Funds that provide money forservices to the general public through programs that areexpected to recover their full costs, primarily throughuser charges. Examples include the Higher EducationServices Office Student Loan Fund, the State LotteryFund, the Chemical Dependency Treatment Fund, andthe Private Employers Insurance Fund.

EBO, Executive Budget Officer - Department ofFinance personnel who are assigned to specific budgetareas and who are responsible for developing theGovernor’s budget and tracking legislative actions.

Federal Funds - Revenues received by the state fromfederal government appropriations. Federal funds aredeposited in the state treasury and must be appropriatedto be spent.

Federal matching requirements - A requirement thatthe state commit a specific amount of state funds for aparticular purpose to obtain federal funds for the samepurpose. In general, percentages vary from 0 to 50percent. For example, a federal grant that requires a tenpercent match would involve $10 million (state funds)and $90 million (federal funds) for a $100 millionproject. The amount of funding the state must commitis often referred to as the “state match.”

Fiduciary Funds - Account for assets held by the statein a trustee capacity or as an agent for individuals,private organizations, other governmental units and/orfunds. These include pension trusts funds,nonexpendable trust funds (where the principal may notbe expended, e.g., the Permanent School Fund,Environmental and Natural Resources NonexpendableTrust Fund), expendable trust funds (e.g., the MunicipalState-aid Street Fund, County State-aid Highway FundEnvironment and Natural Resources Expendable Trust

House Fiscal Analysis Department, December 2000

General Fiscal and Budget Terms, Page 4

Fund, Reemployment Compensation Fund), and agencyfunds, such as the Deferred Compensation Fund.

Finance, Department of - The agency with broadpowers to administer the financial affairs of the state,among them the responsibility to develop and presentthe Governor’s budget, produce forecasts of staterevenues, expenditures, and debt capacity, to prepareand oversee fiscal notes, and to manage the state’scapital indebtedness and capital bonding. TheCommissioner of Finance is designated in statute as thestate’s chief accounting officer, principal financial officerand the state controller.

Fiscal Note - Official estimate of expenditures or non-tax revenues resulting from proposed legislation,prepared by agencies or fiscal staff. State statute (M.S.3.98) requires that fiscal notes be prepared at the requestof the chair of the standing committee to which a bill hasbeen referred, or by the chair of the Ways and MeansCommittee of the House or Finance Committees of theSenate. State law defines the required components of afiscal note. The Department of Finance is responsible foroversight of the processing, preparation, delivery andupdating of fiscal notes, and for assuring their accuracyand completeness. (For tax revenue estimates, seeRevenue Estimates.)

Fiscal Year - The 12-month period on which the statebudget is based; it runs from July 1 to June 30. Schooldistrict fiscal years are the same as the state fiscal year.County and city fiscal years are the same as the calendaryear. The federal fiscal year runs from October 1 toSeptember 30.

Forecast - Each year in November and February, theDepartment of Finance is required to predict staterevenues and expenditures based on current law (M.S.16A.103). This prediction is the “forecast” upon whichthe Governor and the Legislature base their budgetproposals. The State Economist uses both nationaleconomic forecasting data and Minnesota - specific data.Within the forecast process, the Department ofRevenue is required to forecast revenues to be receivedby school districts, counties and towns. The FinanceDepartment is also required to submit a debt capacity

forecast at the same times as the revenue andexpenditure forecast.

Fund Balance or Fund Statement - A summary ofrevenues, expenditures, reserves and year-end balancesfor a fund or funds. This term is most often used withthe general fund

GAAP, Generally Accepted Accounting Principles- uniform standards for government accounts. Most statefunds are accounted for using the modified accrual basisof accounting which recognizes the unique revenue andexpenditure issues for some state payments.

GDP, Gross Domestic Product - the total value of allgoods and services provided in a country by residents andnon-residents of that country.

GDP Implicit Price Deflator - An inflationary measureintended to capture changes in the average price ofgoods and services in the U.S. Unlike the CPI-U, whichmeasures changes in a fixed groups of goods and services,the price deflator measures a changing mix of goods andservices and includes consumer expenditures, privateinvestment, government spending and exports net ofimports.

General Fund - The largest fund in the state treasury,into which receipts from the major taxes are deposited(e.g., individual and corporate income, sales, motorvehicle, cigarette and liquor, etc.). Most of the money inthe General Fund is not earmarked for specific purposes.The General Fund is the major source of funding foreducation, health care and human services and othermajor functions of state government. (Also, see specialfunds.)

GSP, Gross State Product - A measure of stateeconomic output.

Internal Service Funds - Funds internal to theoperation of state government that provide a variety ofservices to state agencies, such as computer services,motor pool, and printing. The funds must recover thefull costs of services provided through billing back stateagencies.

House Fiscal Analysis Department, December 2000

General Fiscal and Budget Terms, Page 5

K-12 - Kindergarten through grade twelve.

Legislative Advisory Commission (LAC) - JointHouse-Senate legislative commission assignedresponsibility for approving the acceptance of federalgrants when the Legislature is not in session and theallocation of emergency contingent funds. The LAC alsoadvises the Governor on issues such as spending from theReserve when receipts are less than projectedexpenditures and on certain contingent appropriations.

Local Impact Notes - An estimate of the cost of certainlegislation or administrative rules (after December 31,1999) proposing state-mandates that have fiscal impactson political subdivisions. Notes are prepared by theDepartment of Finance at the request of the chair or theranking minority member of the House or Senate TaxCommittee.

Mandates - Requirements imposed by one level ofgovernment on another. “Mandate” may refer torequirements imposed by the funding level ofgovernment that must be met by the recipientgovernments in order to receive funds.

MAPS - See the “State Government Finance” section.

Object Code - The lowest level of detail provided inthe biennial budget document. Examples of object codesare personal services (salaries), contracts, and capitalequipment.

Omnibus Bill or Act - A collection of separate bills orappropriations in a single, large bill or act.

Open Appropriations - A form of standingappropriation where the level of funding necessary tofulfill the obligation is made available in the fiscal year.The state fund balance shows an estimate of the amountexpected to be spent. Many of the programs funded byformula (e.g., education aids and Homestead andAgricultural Credit Aid - HACA), and programsfunded through fees, are open appropriations.

Performance Based Budgeting - Settingappropriations based on expected agency performancelevels or with the intent of encouraging certainperformance. Performance base budgeting focuses onagency or program outcomes rather than inputs.

Performance Based Reporting - A system thatidentifies specific goals and objectives and attempts tomeasure progress toward those goals. The system isintended to focus on the outcomes, or effects, ofgovernment activities, rather than on inputs, such as thenumber of employees performing an operation.Performance data must be included in the biennialbudget documents.

Personal Income - In national economic accounting,personal income is the income received by persons:individuals, owners of unincorporated businesses(including partnerships), non - profit institutions, privatetrust funds, and private non - insured welfare funds.Personal income is the sum of wage and salarydisbursements, other labor income, proprietors’ income,rental income of persons, dividends, and personalinterest income and transfer payments, less personalcontributions for social insurance. —Dictionary of U.S.Government Statistical Terms, (Source: U.S. Departmentof Commerce, Bureau of Economic Analysis.)

Planning Estimates - Expenditure estimates for thenext biennium (FY 004-05 during the FY 2002-03biennium) that includes an estimate amount of inflationin the expenditures.

Price of Government, “POG” - M.S. 16A.102 requiresthe Governor and the Legislature to establish revenuetargets that prescribe total revenues for state and localgovernments in terms of the percent of total Minnesotapersonal income they represent. The price of governmentstatistic is an indicator of the capacity of the stateeconomy to support government. The target is expressedas a ratio, the numerator of which is state and localgovernment tax- and non-tax revenues, and thedenominator of which is aggregate Minnesota personalincome. (See personal income.)

House Fiscal Analysis Department, December 2000

General Fiscal and Budget Terms, Page 6

Real (Constant) Dollars - The value of money afteradjusting for inflation (vs. nominal, or current value —the price without adjusting for inflationary effects).

Reciprocity - A mutual action, exchange or agreement,usually between two states, such as mutual recognitionof residency for purposes of income tax liability,eligibility for resident tuition and the like.

RFP, Request for Proposal - A process used to solicitproposals from interested parties for specific agencyinitiatives. The RFP contains detailed information aboutthe proposals being sought including potential fundingavailable and required time lines. The process involvesthe submittal of detailed applications by interestedparties.

Revenue - Government revenue is money received by agovernment from external sources net of refunds andother correcting transactions, other than from theissuance of debt, liquidation of investments, and asagency and probate trust transactions. Governmentrevenue excludes non-cash transactions such as receiptof services, commodities or other receipts in kind.Government revenue includes intergovernmentalrevenue. —Source: Dictionary of U.S. GovernmentStatistical Terms, ibid.

Revenue Estimate - Official fiscal analysis prepared byan executive branch agency, forecasting the revenue lossor gain from the enactment of proposed tax legislation.Usually, revenue estimates are prepared by the ResearchDivision of the Department of Revenue. The revenueestimate does not identify the costs a state agency orlocal government may incur to implement the proposedchange; a fiscal note is required to obtain thatinformation.

Revolving Fund - Funds established in law in whichrevenue (including loan payments) is credited back tothe fund for the same use as the original appropriation.

Special Funds - A grouping of revenues from certainsources from which certain expenditures are made. Thestate of Minnesota has a general fund and a variety ofspecial funds. Revenues for these funds are usually

dedicated and expenditures from the special funds areusually restricted for certain purposes. Examples ofspecial funds include the Highway User Tax DistributionFund, Trunk Highway Fund, the Environmental Fund,Natural Resources Fund, the Game and Fish Fund, theHealth Care Access Fund, the State Government SpecialRevenue Fund and the Special Revenue Fund.

Special Revenue Fund - See Special Funds, above.

Spending Plan - Developed by state agencies after thelegislative appropriation process is completed. The plansmust specify the purpose and amount required for eachactivity and must be ?within the amount and purpose ofthe appropriation.” State law (M.S. 16A.14, subdivision3) requires that agency spending plans must be approvedby the Department of Finance before any money is spent.

Standing or Statutory appropriations - When languagein statute authorizes ongoing payment out of the treasuryfor a program. In contrast to direct appropriations,statutory appropriations need not be renewed everybiennium for funding to continue.

State Aids - Defined in statute as “programs by whichthe government provides financial assistance to politicalsubdivisions to assist them in delivering public services,financing public facilities or reducing property taxes inconnection with state mandates, programs andprocedures.”

State Government Special Revenue Fund - See SpecialFunds, above.

Structural Balance - Applying the balanced budgetrequirement to a biennium beyond the one for whichappropriations are being enacted.

Tail - (1) The future budget effects of anyappropriation or revenue provision; or, (2) anappropriation, funding formula, or tax expenditure thattakes effect in, or carries forward to a future biennium,at higher future costs/ revenue losses to the statetreasury than in the initial biennial budget period.

Targets - In the legislative process, specific limits onspending and revenues, assigned by the House Ways and

House Fiscal Analysis Department, December 2000

General Fiscal and Budget Terms, Page 7

Means Committee, to reconcile the fiscal actions ofcommittees and divisions with the Budget Resolution.The targets add up to the total limit on expenditures,revenues and the reserve level established in the BudgetResolution. The Senate has a less formal process forestablishing spending and revenue limits.

Transfers - M.S. 16A.285 allows agencies to transferoperations money between programs within the samefund. Agencies must notify the Commissioner of Financeof the transfer. A transfer must be consistent withlegislative intent and must be reported by the FinanceDepartment to the chairs of the House Ways and MeansCommittee and the Senate Finance Committees.Agencies may transfer funds within programs, withoutnotifying the Legislature, unless language in statute orlaw prohibits a specific transfer.

Unallotment - Statute allows the Commissioner ofFinance, with the approval of the Governor and afterconsulting with the Legislative Advisory Commission, toreduce unspent allotments if a deficit would otherwiseoccur (M.S. 16A.152, Subd. 4). The commissioner maydo so only after the Reserve account is used to balanceexpenditures and revenues.

Veto - The State Constitution allows the Governorto veto a bill or to veto one or more items ofappropriation in a bill while approving the rest of thebill (line-item veto). If the Governor signs a bill thatcontains vetoed provisions, a statement of the itemsvetoed must be attached to the signed bill. If theLegislature is in session, the Governor must transit thebill to the house where it originated and the vetoed itemsmay be reconsidered separately.

Zero Based Budgeting (ZBB) - A budgeting practicethat examines the total budget for a program or agency,not just changes from the base or previous level budget.In strict ZBB, the budget base would be zero. Inpractice, ZBB often means that a budget starting pointis some amount less than 100 percent of what wouldhave been the base.

Capital Investment Terms, Page 8

Capital Investment

Arbitrage - The financial gain that can be garnered byselling tax-exempt bonds and reinvesting the bondproceeds at a higher, taxable, interest rate. For example,if the principal of a 8 percent bond is invested at 10percent, the 2 percent profit that results is the arbitragegain. Arbitrage is regulated and limited by federal taxlaw.

Bond - A written promise to pay a specific sum ofmoney (the principal) at a date or dates in the future(the maturity) together with periodic interest at aspecified rate.

Bonding - Authorization to provide for issuance of debtinstruments, as well as the use of money raised throughthe issuance for capital projects.

Bond Rating - Rating for bonds to be issued thatprimarily reflects the ability of the issuer to repay thebonds. Better bond ratings result in lower interest ratesfor the bonds issued. Bond ratings are better when thestate follows its self-imposed debt managementguidelines. Current bond rates for the State are AAA byMoody’s, AA+ by Standard and Poor’s, and AAA byFitch.

Call option - A stipulation in a bond contract thatallows the issuer to buy back the bonds at a specifieddate. A call option gives the issuer flexibility to lowercosts if interest rates drop by issuing bonds at a lowerrate to “call” or buy back bonds that are paying a higherrate of interest. Call options typically are set at ten yearson Minnesota’s 20 year bonds. (See also refinance)

Capital Iceberg - See deferred maintenance.

Capital Projects Funds - three funds used to pay forcapital projects. The General Projects Fund pays forcapital projects from with General Fund money. TheBond Proceeds fund pays for non-transportation capitalprojects from the proceeds of a bond sale. TheTransportation fund uses bond proceeds to pay fortransportation related capital projects.

CAPRA - Capital Asset Preservation and RenewalAccount - Bond funds allocated to state agencies forthe purpose of restoring or maintaining buildings andother items of a capital nature. (See also, HEAPRA.)

Construction - The phase of a building project followingpredesign and design. It usually accounts for more than91 percent of the spending on a project, and is theimplementation of the predesign and design stagedecisions.

Debt Management Guidelines - Guidelines that theState imposes on itself to control its capital investment.Following the guidelines will generally result in a betterbond rating for the state, and thus, lower interest ratesfor state borrowing. The guidelines include: (1) totalannual debt service cannot exceed 3 percent of annualnon-dedicated receipts; (2) total debt cannot exceed 2percent of total State personal income; (3) State agencydebt cannot exceed 3.5 percent of State personalincome; and, (4) general obligation debt, moralobligation debt, bond guarantees, equipment capitalleases and real estate leases cannot exceed 5 percent ofState personal income.

Debt Capacity - The ability of the state to sell additionalbonds to pay for bonding projects. Debt capacity is basedon the amount of money available to pay off the bondswhich is based on a limit of approximately 3 percent ofthe state’s General Fund expenditures.

Debt Service - Money appropriated to pay the interestand principal on the money borrowed by the state for itscapital projects.

Defeasance - To set aside money in an escrow accountthat is sufficient to retire outstanding bonds. By settingaside funds to retire debt before the call date on thebonds, the bonds are in effect “taken off the books.”

Deferred Maintenance - Backlog or catch-upmaintenance of state buildings. The Department ofAdministration estimates that the state currently has$1.5 billion in deferred maintenance needs.

House Fiscal Analysis Department, December 2000

Capital Investment Terms, Page 9

Design - The second phase of a project, beforeconstruction, after predesign. Design usually is less than8 percent of the total budget of a project, and consists of3 phases: schematic design, design development andconstruction documents. The bulk of the spendingduring a project during the design phase is forarchitectural and engineering programming.

Design-Build - A way to build capital projects that mayoffer cost savings over traditional design-bid-buildmethods on some projects. This method allows design toproceed along with construction as apposed to having acomplete design first, and then bidding different parts ofthe project. One criticism of design-build is that itusually requires one of the major constructioncontractors to build a large projects and can squeeze outsome of the smaller contracting companies.

General Obligation Bonds, “GO Bonds” - Bondsthat the state stands behind with its taxing powers.

HEAPR - Higher Education Asset Preservation andRenewal Account. Bond funds allocated to the highereducation systems for the purpose of restoring ormaintaining buildings and other items of a capitalnature. (See also CAPRA.)

Planned Maintenance - Preventative maintenance ofa corrective and planned nature to repair and preventbuilding problems.

Predesign - First stage of a building project. Usuallyaccounts for less than 1 percent of total project spending.This stage is intended to determine a project’s feasibility,define the essential aspects of the project and prepareinstructions for the design phase. The predesigndocuments should include the rationale for the project,its use components, costs and scheduled cash flow. Inaddition, predesign should address possible operatingbudget implications of the project.

Refinance - Similar to home owners who refinancetheir home loans during periods of low interest rates, thestate can issue bonds at a lower rate to pay off bonds

issued earlier at a higher rate. However, the older bondscan not be repurchased until their call date, the earliestdate that bond holders have been told the bonds wouldbe refinanced, has been reached.

Revenue Bonds - Bonds for which the debt service ispaid by a specific revenue stream, and not out of theGeneral Fund. Revenue bonds are primarily issued bythe Minnesota Housing Finance Agency, which makeshome loans with the bond funds, for example, and usesthe mortgage repayments of those loans to service itsdebt, and the University of Minnesota and theMinnesota State College and Universities system, whichmight issue bonds for the purpose of building a parkinglot or dorm, and service those bonds with lot fees, ordorm rents.

Jobs & Economic Development Terms, Page 10

Jobs and Economic Development

Brownfields - Parcels of land that were used forindustrial or manufacturing purposes in the past, butnow are underutilized or have been abandoned. In manycases, soil under brownfields have been contaminatedwith pollutants. Redevelopment of brownfields is oftendifficult, because of the costs associated with cleaning upthe pollutants although all brownfields are notnecessarily contaminated.

DES - Acronym for the Minnesota Department ofEconomic Security. DES assists in increasing theeconomic independence of Minnesotans, concentratingon unemployed individuals and those that face specialbarriers to entering and staying in the workforce.

DPS - Acronym for the Minnesota Department ofPublic Service. DPS is currently only the weights andmeasures division. The agency’s energy, information andoperations management, telecommunication, andtelecommunications access for communications impairedpersons division were transferred to the Department ofCommerce by Governor’s executive order in 1999.

DTED - Acronym for the Minnesota Department ofTrade and Economic Development. DTED assists increating an economic environment that produces netnew job growth greater than the national average andincreases both non-resident and resident tourism withinthe state.

Dislocated Worker Program - The federal and statedislocated worker programs serve those dislocated fromlong held jobs because of factors such as technologicalchanges, investment decisions, and changes inconsumption and competition. Services provided toclients fit into three broad categories: readjustment,retraining and supportive services. This program isfunded by an employer tax, which is deposited into theWorkforce Development Fund. The program wastransferred to the Department of Trade an EconomicDevelopment by the 1999 Legislature.

EDA - Acronym for Economic DevelopmentAuthority.

HRA - Acronym for Housing and RedevelopmentAuthority.

IRRRB - Acronym for the Iron Range Resources andRehabilitation Board. The IRRRB is designed to helpstrengthen and diversify the economy of northeasternMinnesota. The IRRRB is funded predominately fromtaconite production taxes that are levied against miningcompanies in lieu of property taxes.

MHS - Acronym for the Minnesota HistoricalSociety.

Minnesota Investment Fund - Formerly the EconomicRecovery Fund. The purpose of the MinnesotaInvestment Fund is to create and retain jobs with a focuson industrial manufacturing and technology relatedindustries. The Department of Trade and EconomicDevelopment awards grants to local units of governmentthat, in turn, make loans to assist new or expandingbusinesses. Loans to businesses can be for land, buildings,equipment and training. Funds may also be used forinfrastructure improvements necessary to supportbusinesses located or intending to locate in Minnesota.

Minnesota Jobs Skills Partnership Program (JSP) - Atraining program operated by the Department of Tradeand Economic Development. JSP provides training fornew jobs or provides skills training in order to retainexisting employees.

Minnesota Workforce Center System - A servicedelivery system that provides a full array of employmentand training services in one location. This system’sapproach to service delivery avoids duplication ofservices and presents a structure for assuring a bettermatch between workers and jobs. This system is a stateand local partnership comprised of the MinnesotaDepartment of Economic Security and seventeen

House Fiscal Analysis Department, December 2000

Jobs & Economic Development Terms, Page 11

Workforce Service Areas. Primary partners include JobService/Reemployment Insurance and Veteransprograms, Rehabilitation Services, State Services for theBlind, local Workforce Councils/Private IndustryCouncils and local elected officials who work with theJob Training Partnership Act, Dislocated Worker andOlder Worker Programs. This multi-partnered systemalso includes county governments, post-secondary andsecondary education, county social service agencies,community action agencies, Displaced Homemakerprograms and other locally-based service providers. TheWorkforce Center System is funded through acompetitive grant from the United States Department ofLabor. As of January 1998, Minnesota established 35Workforce Centers throughout the state and expects toopen a total of 55 sites by July 1998.

PUC - Acronym for the Public Utilities Commission.The PUC creates and maintains a regulatoryenvironment that ensures safe, reliable and efficientelectric, natural gas and telephone services as a quasi-judicial/quasi-legislative board.

UI - Acronym for Unemployment Insurance,previously known as Reemployment Insurance. UI is ashort-term program administered by the Department ofEconomic Security that provides temporary income toindividuals looking for new jobs or awaiting recall totheir regular jobs. The benefits for this program comefrom taxes employers pay into the UnemploymentInsurance Fund. No deductions are taken from anyworker’s wages to pay for these benefits. (See Taxes,FUTA.)

WCRA, Workers’ Compensation ReinsuranceAssociation - A nonprofit association of all insurancecarriers that carry workers’ compensation insurance.WCRA is responsible for: establishing procedures underwhich claims are made and for reviewing claims;collecting data regarding liabilities against the insurers;and calculating and charging members premiumssufficient to cover expected liabilities that members willincur.

Workers’ Compensation Special Fund - Used to fundMinnesota’s workers’ compensation system, includingadministrative costs for the Department of Labor andIndustry, the Office of Administrative Hearings and theWorkers’ Compensation Court of Appeals. The fundalso provides benefits to injured workers whoseemployers do not have mandatory workers’compensations coverage and enforces mandatoryworker’s compensation insurance coverage. The fundconsists of assessments made against worker’scompensation insurers and self-insured employers on thebasis of their payments to injured workers for wages lostas a result of injuries.

Housing Terms and Acronyms

Amortization - Repayment of a mortgage loan byinstallments. Repayment installments include both theprincipal and interest of the loan.

ARIF, Affordable Rental Investment Program - AMinnesota Housing Finance Agency (MHFA) programthat provides zero percent interest-deferred loans for theproduction and rehabilitation of low and moderateincome rental housing.

Bridges Rental Assistance - A Minnesota HousingFinance Agency program that provides temporary rentalhousing payment assistance on behalf of an income-eligible participant until a permanent housing subsidybecomes available.

CDBG, Community Development Block Grant - Afederal entitlement program first authorized in 1974 andadministered by the Department of Housing and UrbanDevelopment (HUD). Local governments automaticallyreceive a portion of these funds and participate in eitherthe entitlement program or the states and small citiesprogram. Grant amounts are determined by a formulabased on the community’s populations, populationgrowth lag, the number of persons in poverty, the extentof overcrowded housing and the amount of housing builtprior to 1940. These funds are for improving

House Fiscal Analysis Department, December 2000

Jobs & Economic Development Terms, Page 12

communities by providing decent housing and suitableliving environment, and expanding economicopportunities, principally for persons with low andmoderate incomes.

Consolidated Plan - Developed by the Department ofHousing and Urban Development (HUD) in 1994 tojoin together application and submission requirementsfor the community development block grant program(CDBG), the HOME Investment Partnerships program(HOME), Emergency Shelter Grants (ESG) and HousingOpportunities for Persons with AIDS (HOPWA).

CRF, Community Rehabilitation Fund - A MinnesotaHousing Finance Agency program that provides grantsto cities and non profit agencies for the preservation orimprovement of designated neighborhoods or areas. ACRF grant may be used for single-family construction,acquisition, rehabilitation, demolition, permanentfinancing, and refinancing.

Equity - The difference between the fair market valueof the property and the amount still owed on itsmortgage. Equity Take-Out Loans - Minnesota Housing FinanceAgency (MHFA) loans offered as an incentive to keepowners of federal assisted properties from prepaying theirmortgage and discontinuing participation in federalaffordable housing program. Equity take-out loans arefrequently used for rehabilitation of rental housingproperty. The agency may make equity take-out loanson all federally assisted properties including propertieswhere the agency does not hold the first mortgage.

FMR, Fair Market Rent - An amount determined byHUD to be a fair amount on which to base its subsidycontribution. The amount determined by HUD to befair is derived from a survey of privately-owned , safe,non-luxury rental units to find out what it costs to rentin the area. The FMR is set as a percentile of rentsreported in the survey. Currently, the 40th percentilerepresents FMR. This percentile is used to figure outhow much to reimburse private property owners whorent to families or individuals with Section 8.

Fannie Mae - A congressionally chartered, shareholder-owned corporation that supplies mortgage funds tohome buyers and investors.

FHA mortgage - a mortgage that is insured by theFederal Housing Administration (FHA).

FHA - Acronym for Federal Housing Administration

Freddie Mac - A congressionally chartered,shareholder-owned corporation that supplies mortgagefunds to home buyers and investors.

Gap Financing - The difference between the cost ofproducing or rehabilitating a building and the appraisedvalue upon completion. When the cost of producing orrehabilitating a building is higher than the appraisedvalue upon completion, gap financing assistance isprovided in the form of grants or loans to help mitigatethe difference.

Housing Development Fund - A revolving fundunder the control and jurisdiction of the MinnesotaHousing Finance Agency (MHFA). Moneys depositedinto the revolving fund include: (1) moneysappropriated and made available by the state for thepurposes of the fund, (2) moneys which MHFA receivesin repayment of advances made from the fund, (3) othermoneys which may be made available to MHFA forpurposes of the fund from any other source or sources,(4) all fees and charges collected by MHFA, and (4) allinterest income or other income not required by theprovisions of a resolution or indenture securing notes orbonds to be paid into another special fund. M.S.462A.20

HRA - Acronym for the Housing and RedevelopmentAuthority.

HUD - Acronym for the Department of Housing andUrban Development.

MHFA - Acronym for Minnesota Housing FinanceAgency

House Fiscal Analysis Department, December 2000

Jobs & Economic Development Terms, Page 13

PHA, Public Housing Agency - Cities with publichousing will have a public housing agency to manage andoperate the building. Public housing is usually federally-built and locally-owned.

Neighborhood Land Trust - A neighborhood landtrust must have as one of its purposes the holding of landand the leasing of land for the purpose of preserving theaffordability of housing on that land for persons andfamilies of low and moderate income. MN. Stat.462A.31

RHS, Rural Housing Service - An agency withinthe U.S. Department of Agriculture, which operatesunder the Consolidated Farm and Rural DevelopmentAct of 1921 and Title V of the Housing Act of 1949,that provides financing to farmers and other qualifiedborrowers buying property in rural areas who are unableto obtain loans elsewhere.

Right of First Refusal - A provision in an agreementthat requires the owner of a property to give anotherparty the first opportunity to purchase or lease theproperty before he or she offers it for sale or lease toothers.

Section 236 - A federal insurance interest reductionprogram which subsidizes interest rates for owners ofhousing developments in exchange for restricting rentlevels to a certain level of affordability for low andmoderate income renters. The term of the mortgage isbetween 30-40 years and owners have the option toprepay the remaining balance of the mortgage at anytime after 20 years of affordable rents have beenprovided.

Section 8 - A federal rental assistance program thatallows participants to pay 30 percent of their income forrent and the remainder of the rent is subsidized by theSection 8 program.

Family & Early Childhood Terms, Page 14

Family and Early ChildhoodNote: Additional terms and acronyms relevant to family and early childhood fiscal policy may be found in the Education, Healthand Human Services, Housing and Taxes sections.

90/10 Split - Most state aid formulas are appropriated at90 percent of the estimated entitlement during the fiscalyear of the entitlement. The final (10 percent) paymentmust be the amount of the actual aid entitlement, afteradjustments for final data, minus the payments madeduring the fiscal year of the entitlement. With the finalpayment being based on actual data, rather than theestimated entitlement, it may be greater, less than orequal to 10 percent.

ABE - Adult Basic Education.

At-Home Infant Care (AHIC)- A family eligible toreceive assistance under the Basic Sliding Fee child careprogram may also be eligible for At Home Infant CareAssistance. A family in which a parent provides care forthe family’s infant child may receive a subsidy in lieu ofassistance if the family is eligible for, or receivingassistance under the basic sliding fee program. A familyis limited to 12 months of assistance. The maximumreimbursement rate to the participating AHIC family isequal to 75 percent of the rate established in theapplicant’s county of residence.

Basic Population Aid - A funding component of theAdult Basic Education state aid formula. For eachSchool district, basic population aid is equal to $1.80multiplied by the greater of 1) the population of theschool district according to the most recent censusestimate or; 2) 4,000.

Basic Sliding Fee Child Care - A state subsidized childcare assistance program for low-income families notenrolled in TANF/ MFIP Child Care assistance.Funding for this program is capped and allocated tocounties on a calendar year cycle. Counties are requiredto contribute a fixed minimum direct service match andin many cases choose to contribute additional countyfunds.

Basic Sliding Fee Uninterrupted Child Care - Fundsdesignated to provide uninterrupted child care assistancefor families completing their transition year from theMFIP program. These funds assure that familiescompleting their transition year will have a slot on theBasic Sliding Fee Child Care program and will notencounter a waiting list.

CAP, Community Action Program - A communityaction program is a community based and operatedprogram that provides a range of services and activitieshaving a major impact on the causes of poverty in thecommunity. Operated by community action agencies,community action programs are also designed to achieveincreased self sufficiency and greater participation in theaffairs of the community.

CCA, Community Action Agency - A communityaction agency is a political subdivision of the state, acombination of political subdivisions, a public agency, ora private non profit agency that receives funds to supportcommunity action programs.

CCDF, Child Care Development Fund - A five-yearfederal block grant for child care. The CCDF has threecomponents: discretionary, mandatory, and matchingfunds. Each component has separate requirements andMinnesota must comply with each component annuallythrough federal FY 2002 in order to leverage availablefederal block grant funding. This five year block grantwill be up for federal re-authorization by Congress afterfederal FY 2002.

Child Care Regional Resource & Referral Agencies -Regional organizations that work with existingcommunity based committees such as the interagencyearly intervention committees or neighborhood groupsto advocate for child care needs in the community aswell as serve as important local resources for childrenand families

House Fiscal Analysis Department, December 2000

Family & Early Childhood Terms, Page 15

Child Care Wraparound - A full day of child care usinga combination of state and federal Head Start and childcare assistance funding.

Child Care Fund - Funds designated to help lowincome families pay for child care so that parents maypursue employment or education and training leading toemployment. The Child Care Fund is composed of StateGeneral Fund appropriation and federal Child Care andDevelopment Fund (CCDF) monies.

CSBG, Community Services Block Grant - A federalblock grant, under P.L. 97-35, that supports theinfrastructure of community action agencies. Communityaction agency programs were established to help fightpoverty by providing low-income Minnesota citizenswith self sufficiency skills and training.

Early Childhood Health and DevelopmentalScreening - Minnesota school districts are required tooffer health and developmental screening for four-year-old children. The state provides $40 per child asreimbursement for health and developmental screeningfor children between the ages of 3.5 to 5 years old.

Educational Excess and Deficiency Transfer - At theend of a fiscal year, any excess general fundappropriations to the Department of Children, Families,& Learning for an aid or grant program specified in M.S.127A.41 (subd. 9) may be transferred to programs thathad deficiencies and could not sufficiently fund itsformula. There are K-12 and Family and EarlyChildhood Education programs eligible for transfers toprograms with excesses and deficiencies. Excessappropriations within the K-12 programs may not betransferred to deficient Family and Early ChildhoodEducation programs or vice versa. This transfer of excessfunds is sometimes referred to as the “commissioner’sreserve.”

Family Service Collaborative (FSC) - The FamilyService Collaborative program assists local communitiesto work with children and families, by creating a clientcentered integrated local service delivery system forchildren and their families, that coordinates serviceacross agencies. Each collaborative must consist of a at

least one school district, one county, one public healthentity, and one community action agency.

GED Test Reimbursement - Provides 60 percentreimbursement to eligible individuals for completing thefull battery of General Education Development tests.

IDA, Individual Development Accounts - A federalinitiative that enables low-income families to build assetsand save money for economic self sufficiency. Use ofsavings accrued in IDA’s is limited to post secondaryeducation related expenses and training, businessdevelopment and home ownership. In Minnesota, thefamily assets for independence initiative is modeled afterthat the federal IDA initiative.

Part C - An interagency effort between the MinnesotaDepartment of Children, Families and Learning and theMinnesota Department of Human Services. Thisprogram provides eligible young children, withdisabilities, age birth to 2, and their families withinteragency services in their local communitiesdeveloped through an individual family service plan(IFSP) process.

Portability Pool - Up to 5 percent of the annualappropriation for Basic Sliding Fee (BSF) may beearmarked for continuous child care assistance to eligiblefamilies who move between Minnesota counties. Underthe portability pool, the family must have been in BasicSliding Fee child care, moved to a county with a waitinglist, and apply for BSF within 30 days. The receivingcounty must accept responsibility after two months,continue basic sliding fee for the lesser of six months oruntil the family is under the regular county basic slidingfee program.

Proration - To distribute funding proportionately basedon the amount of funding available. For example, allproviders receive 98.6 percent of the amount they wouldbe entitled to under the funding formula.

School Age Care - Districts with a communityeducation program may offer a School Age Care program

House Fiscal Analysis Department, December 2000

Family & Early Childhood Terms, Page 16

for children in kindergarten through grade 6 for thepurposes of expanding learning opportunities. Districtsare eligible for school age care revenue for the additionalcost of providing services to children with disabilities orto children experiencing family or related problems of atemporary nature.

Sliding Fee Scale - A family’s monthly parent fee forbasic sliding fee child care services. Parent fees areestablished in rule and must provide for graduatedmovement to full payment. The minimum parent feesfor families between 75 percent and 100 percent ofpoverty level must be $5 per month.

Temporary Assistance for Needy Family (TANF)/Minnesota Family Investment Program (MFIP) ChildCare - TANF/MFIP Child Care helps cash assistancefamilies and families moving off of cash assistance(Transition Year Families) pay for child care whileparticipating in authorized activities. Families who areemployed or pursuing employment, or are participatingin employment and training activities authorized in anapproved employment services plan, or employedfamilies who are in their transition year are eligible toreceive cash assistance. MFIP Child Care is available asa forecasted program without an allocation ceiling.Counties are reimbursed, from state and federal funds,for 100% of their expenditures.

Transition Year Child Care - Transition year child careis available for up to one year for families who havereceived cash assistance for at least three of the last sixmonths before losing eligibility due to increased hours ofemployment, increased income or child or spousalsupport, or the loss of income disregards due to timelimitations.

K-12 Finance Terms, Page 17

K - 12 Education Finance

ANTC, Adjusted Net Tax Capacity - The propertyvalue used for assessing most school taxes. ANTCadjusts for differences in assessment practices andreflects the application of the classification rates to themarket value of property.

AP/IB, Advanced Placement/InternationalBaccalaureate - Programs that require more rigorousstudent achievement than regular programs and oftenwill count for college credit.

Basic Skills Test - Tests in math, reading and writingtaken by Minnesota students, passage of which isrequired in order to graduate. See also Profile of Learning

Compensatory revenue - A portion of generaleducation revenue based on the number of students in aschool district that qualify for free and reduced-pricelunches.

CFL or DCFL - The Department of Children, Families,and Learning (formerly the Department of Education).

Educational Excess & Deficiency Transfer - At theend of a fiscal year, any excess general fundappropriations to the Department of Children, Families,& Learning for an aid or grant program specified in M.S.124.14 (subd. 7 - 7a) may be transferred to programsthat had deficiencies and could not sufficiently fund itsformula. Excesses in K-12 programs can only be appliedto deficiencies in K-12 programs, and excesses in EarlyChildhood and Family Education Programs can only beapplied to deficiencies in Early Childhood and FamilyEducation programs. In the Early Childhood area, thistransfer of excess funds is sometimes referred to as the“commissioner’s reserve.”

Enrollment Options “Open Enrollment” - Theprogram that allows students to attend a school districtother than the one in which they reside.

Formula Allowance - Usually refers to the basicgeneral education formula allowance. For example,$3,964 per pupil unit in 2000 - 01.

General education allowance - The funding formulathat provides school districts with a majority of theirrevenue. For example, the general education formulaallowance for the 2000-01 school year is $3,964 per pupilunit. A district’s formula revenue is made up of a localproperty tax levy share and a state aid share.

General Education Program - The funding for schooldistricts which is the primary source of revenue for theirgeneral fund. The General Education Program includesthe General Education Formula Allowance, but alsoincludes other types of formula-generated revenue: BasicSkills, Sparsity, Operating Capital, Training andExperience, Transportation Sparsity, ReferendumAdjustment, Equity, Transition and Supplemental.

HSGI, High School Graduation Incentives - Agroup of alternative education programs designed toencourage students to complete graduationrequirements.

IEP, Individual Education Plan - The learning planrequired to be developed for each student withdisabilities.

LEP, Limited English Proficient - The term appliedto students who have limited English speaking ability.

Market Value - The value assigned to property by anassessor. The market value is intended to reflect the salesvalue of the property.

Marginal Cost Pupil Units - Used to indicate pupilcount. In school districts with declining studentenrollment from one year to the next, the districtsMarginal Cost Pupil Unit count is 77 percent of its

House Fiscal Analysis Department, December 2000

K-12 Finance Terms, Page 18

current year pupil count, plus 23 percent of its prior yearpupil count.

MARRS, Minnesota Automated Reporting StudentSystem - An automated process for school districts toreport pupil data to the state. This data is used forfunding calculations and other purposes.

Profile of Learning - In-depth content requirementsMinnesota students must meet, in a wide variety ofsubjects, in order to graduate. See also Basic Skills Test.

PSEO, Post Secondary Enrollment Options. (SeeHigher Education terms.)

Pupil Units - A weighted count of pupils used todetermine revenue in many formulas:

One Kindergarten Pupil = .557 pupil unitsOne Elementary Pupil (grade 1-3) = 1.115pupil unitsOne Elementary Pupil (grade 4-6) = 1.06 pupil unitsOne Secondary Pupil (grade 7-12) = 1.3 pupil units

Review & Comment - A process by which thecommissioner of Children, Families and Learningeducation reviews and comments on the feasibility andpracticality of school district building projects.

Sparsity revenue - The portion of the generaleducation formula that provides additional revenue toschool districts for schools that have relatively smallenrollments and are relatively far from other schoolbuildings.

T&E, Training and Experience revenue - A portionof the general education formula that compensatesschool district for a portion of the training or educationlevels and experience (number of years of service) levelsof school district staff. Began phasing out in the 1998-99school year.

Tax Capacity Rate - The rate of taxation for a specificprogram. Tax capacity rates are expressed as a percent ofthe adjusted net tax capacity. Many tax capacity ratesare set in law.

UFARS, Uniform Financial Accounting andReporting Standards - A statewide accountingprocedure that must be used by school districts to recordfinancial transactions and report financial informationto the State Department of Education.

Youth Works and AmeriCorps - The state and federalprograms that provide learning opportunities forstudents in conjunction with providing services to theircommunities.

Higher Education Terms, Page 19

Higher Education

Allocation Model - Proposed MnSCU methodologyfor internal distribution of state appropriations tocampuses.

Board of Trustees of the Minnesota State Collegesand Universities - Also known as the Higher EducationBoard (HEB), or “the Merger Board.” Newly created(1991) board that has governance authority over theState Universities, Community Colleges and TechnicalColleges after the formal merging of these three systemson July 1, 1995. Members of the Board of Trustees areappointed by the governor.

Board of Regents - Board which has governanceauthority over the University of Minnesota. Themembers of the Board of Regents are elected by bothhouses of the legislature meeting in joint convention.

Design for Shared Responsibility - Defines howstate financial aid is allocated to Minnesotaundergraduate students. This policy distributes theresponsibility for paying the cost of attending collegeamong the student, the student’s family, and the stateand federal governments. Shared Responsibility expectsthe student to finance 50 percent of the cost; the familyis expected to pay the other half. In general, grant aidfrom the federal and/or state government applies to thefamily share and loans or workSstudy apply to thestudent share.

EdVest - College savings program enacted by the1997 Legislature. Allows families to set up statemanaged, tax deferred, savings accounts for educationalexpenses. Contributions are matched by the state up toa maximum $300 annual benefit. Families with incomesunder $50,000 receive a 15% match, families withincomes between $50,000 and $80,000 receive a 5%match. The program is still in the set-up phase andaccounts will not be available until 2001.

FAFSA, Free Application For Federal Financial Aid- Federal form that provides financial information tocomplete the Federal Needs Analysis (see below) whenapplying for financial aid. Submitting this completedform with a copy of current tax information is aprerequisite for all state and federal need based aid.

Federal Needs Analysis - Federal Methodology Usedto assess a student eligibility for both state and federalneed based financial aid programs. Financialinformation about the student and/or family and thestudent’s cost of attendance are used to determine thestudents financial need.

Funding Formula - Method by which the Legislaturedetermines system allocations. Minnesota is in theprocess of converting from a formula that was known as“Average Cost Funding,” which based funding on the fullaverage cost per student and was entirely dependent onenrollment volume. The new formula is being called a“fixed and variable” cost model which recognizes that aportion of the cost of running a college does not varygreatly with minor differences in enrollment.

FYE - Full Year Equivalents. A measure of enrollmentequating total creditSbased enrollment (including fulland part time students) to the equivalent number of fulltime students. Calculated by taking total credit hoursgenerated and dividing by 45.

Gopher State Bonds - Program which will offer Stategeneral obligation bonds issued in small denominationsto help families save for college. These bonds are stateand federally tax exempt. Bonds are not yet availablebut should be late in 1998.

Headcount - Total number of students regardless oftheir enrollment status (number of individuals).

HEFA Higher Education Facilities Authority -Statutory entity which assists (primarily private) collegeswith financing of capitol projects. The Authority isempowered to issue revenue bonds which in aggregate do

House Fiscal Analysis Department, December 2000

Higher Education Terms, Page 20

not exceed $500 million. The Authority does notreceive an funding from the state.

HESO Higher Education Services Office, formerly theHigher Education Coordinating Board) - State agencythat is responsible for administering state financial aidprograms and collecting statewide data on enrollmentsand aid distribution.

Instructional Expenditure - Includes both direct (e.g.faculty salaries) and indirect costs (e.g. heat) assignableto academic programs.

Legislative Intent Tuition - Estimate of revenuescollected by the higher education systems attributable tothe student (tuition) portion of the formula (see UniformCost Related Tuition). Because system boards haveauthority in statute to set their own tuition rates, therevenue they collect may vary some from the tuitionassumptions made by the funding formula and thelegislature. The difference (if positive) is sometimesreferred to as excess tuition.

NonSSinstructional Expenditure - Includes fundingfor activities such as research, athletics, financial aid,and community service. NonSinstructional activities, asa percentage of total state appropriations, vary greatly bysystem and mission.

PELL Grant Program - Main Federal need basedfinancial aid program. Grants range from $400 to $3000annually and apply to undergraduate studies only.

Perkins Loan - Major supplemental federal loanprogram. Provides long term, low interest loans toundergraduate and graduate students. Students mustshow need (see Federal Needs Analysis). Undergraduatesmay borrow $3,000 annually up to $15,000 in total,graduates may borrow $5,000 annually up to $30,000 intotal.

PSEO Postsecondary Enrollment Options - Stateprogram that allows high school juniors and seniors toenroll in postsecondary courses. These students are

accepted on a space available basis and are funded atmarginal (32 percent) cost in the higher educationfunding formula.

Reciprocity - Agreements that Minnesota has withother states and provinces that allow students to attendcolleges in those areas at lower than nonresident costand vice versa. The agreements vary by state as to scopeand cost, but most include a provision for equalizationpayments between states based on enrollment volume.

SELF Loan, Student Educational Loan Fund - Staterun revolving loan fund. Loans are not need based butrequire a credit worthy co-signer (usually a parent).Interest on SELF loans is not deferred but must be paidquarterly while the student is in school. Undergraduatesmay borrow $4,500 annually for the first two years and$6,000 annually thereafter up to $25,000 in total.Graduates may borrow $9,000 annually up to $40,000total.

Series EE U.S. Savings Bonds - Federally issued savingsbonds. Bonds are available in small denominations andpurchase methods such as payroll deduction areavailable. Interest on EE bonds is state and federal taxexempt when used for educational purposes.

Stafford Loan Program - Federal loan program thatincludes both need based, subsidized loans and non-needbased, unsubsidized loans for undergraduate, graduateand professional students. Both programs are traditionalcollege loan programs handled through private lenders,however, since 1994, both programs are also available atcertain schools as Federal Direct Student Loans wherethe U.S. Department of Education is the lender. Annualloan amounts and aggregate limits vary by year in schooland dependancy status.

State Spending - Equals appropriations plus tuition.Tuition money is not appropriated, but is treated asdedicated revenue that is retained by the highereducation systems. Because Minnesota links tuition andstate funding levels (see Uniform Cost Related Tuition),the higher education funding bill appropriates the stateshare of costs, but also sets an expectation for overallstate spending (see Legislative Intent Tuition).

House Fiscal Analysis Department, December 2000

Higher Education Terms, Page 21

State Grant Program - Main state need based financialaid program. This program works in conjunction withthe federal PELL program to provide grants to studentswith assessed need (see Federal Needs Assessment andDesign for Shared Responsibility). After the amount oftotal grant aid that a student is eligible for is determinedany PELL grant which a student will receive is deductedand the remainder is the amount of the State Grant.

Uniform Cost Related Tuition - Relates the price ofpublic higher education (tuition) to the cost of providinginstruction. The state is expected to fund twoSthirds ofthe cost of instruction (slightly more at the TechnicalColleges) and students are expected to pay oneSthird.

Environment & Ag Terms, Page 22

Environment and Natural Resources, & Agriculture

AURI - Acronym for the Agricultural UtilizationResearch Institute.

BOWSR - Acronym for Board of Water and SoilResources.

Consolidated Conservation (Con-Con) Lands -State-owned lands that Minnesota received in exchangefor paying off ditch bonds issued by seven Minnesotacounties in the early 1930s. According to state law,these lands are to be used for "conservation purposes"and managed by the DNR.

Conservation Reserve Enhancement Program (CREP)The CREP program allows Minnesota to match federaldollars to put conservation easements on up to 100,000acres in the Minnesota River valley. The federalgovernment will provide up to $163 million toMinnesota for CREP; Minnesota must provide matchingfunds of $70 million and must allocate them beforeSeptember 2002.

DNR - Acronym for the Minnesota Department ofNatural Resources.

Ecosystem-Based Management (DNR) - TheMinnesota DNR defines Ecosystem-based Managementas the collaborative process of sustaining the integrity ofecosystems through partnerships and interdisciplinaryteamwork. The long-term goal is sustainability ofMinnesota's ecosystems, the people who live in them,and the economies founded on them.

Environmental Fund - Fund in the state treasury thataccounts for activities that monitor and controlenvironmental problems using taxes and fees fromactivities and industries contributing to environmentalproblems.

Environment and Natural Resources ExpendableTrust Fund - Fund in the state treasury that receivesthe investment earnings and a portion of the net lotteryproceeds deposited in the Environment and NaturalResources Non-expendable Trust Fund to be expendedin for natural resources purposes.

Ethanol Producer Payments - MDA - Provides a20-cent ethanol producer payment which providessecurity required by lenders to invest in ethanol facilities.Goals of the program include: C building a new market for the state's corn crop.C developing corn processing/ethanol production

facilities in Minnesota. C replacing 10% of imported petroleum we use for

gasoline. ($100 million annual savings) C helping the Twin City Area meet U.S. EPA

standards for carbon monoxide.

Feedlot and Manure Management AdvisoryCommittee (FMMAC) - FMMAC was created duringthe 1994 legislative session as an advisory body to theMDA and PCA. The committee was established to,"identify needs, goals, and suggest policies for research,monitoring, and regulatory activities regarding feedlotand manure management."

Game and Fish Fund - Fund in the state treasurythat receives revenues from license fees and fines relatedto hunting and fishing that are spent for relatedpurposes.

Integrated Pest Management (IPM) Program- MDA- The IPM Program develops and implements statewidestrategies for the increased use of IPM on private andstate managed lands.

Legislative Commission on Minnesota Resource(LCMR) - The commission consists of 18 legislatorsselected to serve by their respective body of the

House Fiscal Analysis Department, December 2000

Environment & Ag Terms, Page 23

legislature. The commission recommends a biennialbudget plan for the expenditure of the Environment andNatural Resources Trust Fund and Minnesota FutureResource Fund dollars.

Lottery-In-Lieu-of Tax - DNR - 2000 Sessionlegislation directs 6.5 percent in-lieu sales tax on lotterytickets directly to "natural resources programs." The tax,which amounts to roughly $25 million in FY01 and $22million in FY02 and thereafter, previously went to thestate general fund.

MDA - Acronym for the Minnesota Department ofAgriculture.

Minnesota Future Resources Fund - Fund in the statetreasury that receives a portion of the cigarette andtobacco taxes that are appropriated for various naturalresource development purposes.

Natural Resources Funds - Fund in the statetreasury that receives taxes from fuel used in recreationalvehicles, fees and donations that are used to fundmanagement of the related natural resource programs.

OEA - Acronym for the Minnesota Office ofEnvironmental Assistance.

PCA - Acronym for the Minnesota Pollution ControlAgency.

Petroleum Tank Cleanup Fund - Fund in the statetreasury that receives funding from a fee imposed onpetroleum distributors for the purpose of reimbursingresponsible parties for most of their costs to cleanupenvironmental contamination from petroleum tanks.

Reinvest In Minnesota (RIM) - RIM isMinnesota’s premier conservation program, designed toprotect, restore and improve the natural resourcehabitat.

Rural Finance Authority (RFA) - Loan programsoffered by the Department of Agriculture are located in

this division. The Rural Finance Authority offers avariety of loan programs.

Scientific and Natural Area (SNA) - DNR preservesnatural features and rare resources of exceptionalscientific and educational value through landacquisition. These areas are open to the public fornature observation and education.

Select Committee on Recycling and the Environment(SCORE) - OEA - In 1989, the Minnesota Legislatureadopted comprehensive waste reduction and recyclinglegislation based on the recommendations of theSCORE. This set of laws, commonly referred to asSCORE, is a part of Minnesota's Waste ManagementAct (WMA). The SCORE legislation has providedcounties with a funding source to develop effective wastereduction, recycling and solid waste managementprograms. The SCORE Report is an annual examinationof Minnesota programs and data.

Solid Waste Fund - Fund established in the statetreasury of monies credited to the account. Funding isfrom the solid waste fees and the proceeds of bond sales.The fund is used for costs associated with the closedlandfill cleanup program or other costs as appropriatedby law.

Solid Waste Investment Fund - Fund established in thestate treasury of monies credited to the account.$5 million is transferred from the Solid Waste Fund overfour years starting in FY2000. Transfers into andinvestment earned is to be used for future state liabilityto clean landfills.