Embed Size (px)

Citation preview

i

A Dynamic Model for determining Inward Foreign Direct Investment in Jordan

Ghaith N. Al-Eitana,*

Foreign direct investment has become an increasingly important channel for developing

countries to enhance their economic and financial systems. A significant part of economic

and financial research is the view that a host country's risks affect investment inflows. The

purpose of this paper is to test the argument that Jordan’s country risk, stock market price and

macroeconomic variables determine inward FDI in Jordan. Models are formalised based on

the theory of foreign direct investment and the missing gaps in the literature. This study

covered the period from 1996 to 2010. Monthly data of collective country risk,

macroeconomic variables and the price of stock market sectors were obtained from risk

rating agencies, Central Bank of Jordan and the Jordan Securities Commission respectively.

Moreover, the following methods are applied: Ordinary Least Squares (OLS) regression

analysis (unlagged monthly data), Co-integration and exogeneity analysis based on

multivariate models (lagged monthly data) such as vector autoregressive (VAR) and Granger

Causality. ). Based on the analysis, the results showed that Jordan economic risk, the price of

stock market sectors and two of the macroeconomic variables (inflation and GDP)

significantly caused inward FDI in Jordan. Also, the variables appear to have a long run

relationship. Some strategic implications have been drawn in conclusion for FDI attraction

policy in Jordan.

Keywords: foreign direct investment, stock market price, financial risk, economic risk,

political risk, inflation, GDP, VAR

aSchool of Economics and Finance, Curtin University, Perth, Western Australia, 6001, Australia. E-mail:

ii

PREFACE

Thesis title: Modelling Inward Foreign Direct and Indirect Investment for Jordan and

Australia (Policy Implications)

Supervisor: Associated Professor John Simpson

Previous studies have determined the effects of country risk, macroeconomic factors and

globalisation on inward foreign direct and indirect investment (FDI and FII) in host

economies. Some researchers study one or two countries risks like political and economic

risk as well as including macroeconomic factors such as inflation and GDP to investigate

their effects on (FDI and FII) in foreign countries. However, a few studies have analysed

the relationship between FII, a country’s risk, macroeconomic factors and globalisation to

determine the extent to which a country’s business environment influences FII in host

country. For example, the assumption common to these studies is that a country’s risks

affect FII negatively, some macroeconomic and globalisation factors positively and

negatively affect FII. This means that conclusions have been mixed. Therefore, this study

investigates the main determinants of inward FDI and FII in Jordan and Australia as

developed economies in order to obtain some policy implications by using advanced

econometric techniques such as vector autoregressive model, impulse response functions,

variance decomposition, Granger causality, co-integration and error correction model.

The thesis examines a number of key issues over the period 1996-2010 within the above

context: firstly, investigating the true state of inward foreign direct and indirect investment

in Jordan and Australia. Secondly, identifying the major determinants affect inward foreign

direct and indirect investment in Jordan and Australia. .Thirdly, identifying the country's

risk factors that influence inward foreign direct and indirect investment. Finally, analysing

macroeconomic factors affect inward foreign direct and indirect investment.

The thesis has been taken the following Structure:

I. Chapter One: Introduction

II. Chapter Two: Study Background

III. Chapter Three: Theoretical Base and Literature Review

IV. Chapter Four: Empirical Models and Hypothesises

V. Chapter Five: Data and Methodology

VI. Chapter Six: Main Empirical

VII. Chapter Seven: Discussion

VIII. Chapter Eight: Conclusion and Final Remark

This paper based on advance econometric techniques (lagged models) such VAR, VECM,

Co-integration, Granger causality

1

1. Introduction

Foreign direct investment (FDI) is the most significant factor of economic growth, which

encourages productivity of the national economy, augment’s the use of technology,

reducing unemployment by creating new jobs and other encouraging output that

differentiate this form of investment from other funding sources.

Consequently, most developing countries realised the need for FDI to increase rates of

economic growth. Despite the race among Arab economies to improve its business

environment to pull foreign investment via contemporary legislations to attract this form of

investment and increase the competitiveness of their national economy, most of these

countries are still suffering from a low volume of inward FDI compared to other

economies. This is due to the absence of efficient legislation that should support the process

of attracting inward FDI. For example, impose higher taxes, the absence of political and

economic stability in some countries and the existence of administrative and financial

corruption.

Like the rest of the world, foreign investment plays a vital economic role in Jordan and

remains one of the main sources to enhance economic development. Therefore, the main

aim of this paper is to investigate the dynamic movements of inward FDI in Jordan, country

risk (financial, economic and political risk), macroeconomic factors (inflation, interest rate

and GDP) and stock market price by implementing VAR, ECM, co-integration test and

Granger causality test.

Politically, Jordan’s foreign policies play a major role in making Jordan highly attractive

for (FDI). For instance, in 1996, Jordan signed a peace agreement with Israel accompanied

by Bill Clinton. As a result the Qualifying Industrial Zones (QIZ) was created by the U.S.

Congress to support the peace process. In 1998, the United States Trade Representative

(USTR) designated Jordan's Al-Hassan Industrial Estate in the northern city of Irbid as the

world's first QIZ (CRS Report for Congress 2001, 2).

Economically, Jordan is an open economy and has undertaken a program of economic

reform covering most features of Public Finance Management. The three core objectives of

the program of reform are to ensure fiscal sustainability, efficient resource allocation and

operational efficiency. The economy has experienced sustained economic growth in recent

2

years due to a combination of strong economic policies nationally and spillover from

regional growth, mainly by the rich Gulf economies. Annual real GDP growth doubled

during 2000-05 from the earlier five years (Jordan Performance Report 2007, 8).

The growth of Jordan’s Gross Domestic Product (GDP) was recorded at 7.6% percent

and 2.9% percent respectively for the years 2008 and 2009, with a total contribution from

Transport, storage and communication, manufacturing and the produce of government

services sectors amounting to almost 16% percent, 17% percent and 18% percent for 2009 (

Treasury Jordan 2009, 36). The global financial crisis has affected Jordan’s GDP by 4.7%.

However, Jordan economy is recovering from the effects of this. For example, Jordan’s

GDP was estimated at 3.4% in 2010 and the International Monetary Fund (IMF) forecasted

by 4.2% by 2011(Central Bank of Jordan 2010).

The Jordan government has eliminated most fuel and agricultural subsidies, passed

legislation targeting corruption, and begun tax reform. It has also worked to liberalize trade,

joining the World Trade Organization (WTO) in 2000; signed an Association Agreement

with the European Union (EU) in 2001; and also signed the first bilateral free trade

agreement (FTA) between the U.S. and an Arab country, which entered into force in 2001.

Jordan has established some economic regions and promotional institutions such as the

Aqaba Special Economic Zone (ASEZ) and the Jordan Investment Board (JIB) in order to

attract the foreign investors’ attention. First of all, ASEZ was inaugurated in 2001 as a bold

economic initiative by the government of Jordan. A liberalized, low tax duty-free and

multi–sector development zone, the ASEZ offers multiple investment opportunities in a

strategic location on the Red Sea covering an area of 375 km² and encompassing the total

Jordanian coastline (27 km), the sea-ports of Jordan and an international airport. Secondly,

JIB was established in 1995. The Jordan Investment Board is a government institution

committed to working with the private sector to promote Jordan for its unique, friendly

business environment, diverse investment opportunities and attract foreign investments.

Financially, the most important reason to attract foreign investors to the Amman

financial market is there is a need to invest in portfolio diversifications on the basis of the

principle of diversifications investment, which is part of the basic principles of investment

policy. A foreign investor seeking markets does not have a connection with the advance

markets, which are not affected by increasing and decreasing them. In addition, foreign

investors search for companies or sectors that have prospects of a future boom. Moreover,

3

investors look for the markets which provide accurate and quick information in an

appropriate time in order to control their investments (Amman financial market, 2009).

Public shareholding companies were set up and their shares were traded in long before the

setting up of the Jordanian securities market. In the early thirties the Jordanian public

already subscribed to and traded in the shares. For example, Arab Bank was the first public

shareholding company to be established in Jordan in 1930, followed by Jordan Tobacco and

Cigarettes in 1931, Jordan Electric Power in 1938 and Jordan Cement Factories in 1951. In

the 1975 and 1976, the Jordan Central Bank cooperated with the World Bank’s

International Finance Corporation to establish the Amman financial market (Amman

financial market, 2009).

Jordan has done well in catching the attention of foreign investors as a consequence of

numerous factors, such as internal and external political stability, supported investment

legislations, privatisation plans, advanced private sectors, joining and merging with a

variety of unilateral, bilateral and multilateral trade agreements. Moreover, foreign capital

has been attracted by some factors such as the legal system, developed infrastructure, cheap

and skilled labour, and feasible projects to be undertaken (Investment Encouragement

Corporation, Amman, Jordan).

The rest of the paper is organised as follows: section 2 describes the literature review and

theoretical framework and hypotheses. Section 3 presents the research methodology

including research models, the mechanism used to measure the extent of risk, data analysis

method and methods of gathering data. Section 4 shows the results and discussion and

section 5 conclusion.

2. Theoretical Framework and Review of Literature on FDI and Country Risk.

Numerous studies have analysed the relationship between FDI, country risk,

macroeconomic factors and stock market price to determine the extent, if any, to which

country risk influences FDI in host economies. The assumption common to these studies is

that country risk affects inward FDI. Overall, conclusions have been mixed, but most

research find that country risk prevent FDI to flow into hot countries. The differences in the

findings could arise from a number of methodological and conceptual factors such as lack

of comprehensive, different definitions of FDI and different econometric specifications.

4

2.1Theoretical Framework

The theory of FDI noted by Dunning 1977 that the structure market failure hypotheses of

Hymer and Caves or the internalization approach of Buckley and Casson was very much

couched. In that case, Dunning brought the computing theories together to build a new

single theory. Dunning's new theory shaped via combining Hymer's ownership advantages

with the internalization school meanwhile added a location dimension to the new theory.

Also, he considers the impact of Country's and industry's characteristics on the ownership

location and internalization advance of FDI (Dunning and Lundan 2008, 86).

This paper has been focused on a host country’s characteristics. This is an interesting

topic, as while virtually all countries now compete energetically for FDI inflows, the

distribution of those inflows is far from uniform. While some countries pull in massive

amounts of FDI inflows, but others such as those in developing countries lag far behind.

Thus, it is vital for FDI-seeking policymakers to have a good grasp of the underlying

drivers of the MNEs’ location decisions in order to attract inward FDI. According to

Dunning's eclectic paradigm of FDI shows that a firm will directly invest in a foreign

country if it ensures three conditions (Jones and Wren 2006, 36): An ownership-specific

asset must be possessed by the firm, which gives it advantages over other firms. Secondly,

these assets must be internalized within the firm. Finally, there must be a benefit in setting-

up production in a foreign country rather than relying on exports.

In particular, this paper has been focused on a country’s risk which is closely related with

the level of business risk. It seems intuitively plausible to believe that a sound institutional

environment (efficient bureaucracy, low corruption, secure property rights, etc.) should

attract more FDI. Similarly, higher business risk due to high country risk would discourage

foreign investment by multinationals. Hence, there are several ways of characterizing a

country's L specific advantages; one of them is ESP paradigm. According to economic

environment, economic system and government policies, countries are classified in the ESP

paradigm of Koopmans and Montias (1971). Here environment encompasses the resources

and capabilities, including a wide range of intangible assets to a particular country as well

as the ability of its enterprises to use these to service domestic or foreign markets. System

means the macro-organizational mechanism within which the allocation of these resources

and capabilities is decided. Policy means the strategic objective of government and the

5

macro or micro measures taken by them, to implement and advance these objectives within

the system and environment of which they are part (Dunning and Lundan 2008, 223).

2.2 Literature Review and Hypotheses

2.2.1 Political risk

Political risk is a type of risk faced by foreign investors, MNfs and governments. It is a risk

that can be understood and managed via reasoned foresight and investment. Many studies

have examined the determinants of FDI in a host country. Using different econometric

techniques and periods, Harms and Ursrung (2000), Jensen (2003) and Busse (2004) point

out that MNfs are more likely to be attracted to a democracy. Nevertheless, Egger and

Winner explore the relationship between corruption and inward FDI by using general

equilibrium models and data of 73 developed and less developed countries. They highlight

a clear positive relationship between corruption and FDI which means corruption is a

stimulus for FDI (2005, 935-949). The analysis comprises the primary data from 145

affiliates of western MNEs in Turkey via a survey by Demirbag et al, who find that political

risk, financial incentives and culture distance do not have any significant impact on the

perceived performance of affiliates (2007, 330). On the other hand, according to Busse and

Hefeker political risks have a significant impact on FDI inflows (2007, 401). Institutional

quality and democracy appear more important for FDI in services than general investment

risk or political stability (Kolstad and Villanger 2008, 530). According to Cuervo-Cazurra,

corruption, arbitrary corruption and pervasive corruption have a negative influence on FDI.

However, transition economies show high levels of corruption and also high levels of FDI

(2008, 25). Asiedu et al state that the optimal levels of FDI decrease as the risk of

expropriation rises (2009, 269). Consequently, based on this overview of the related

literature, the corollary hypothesis is as follows:

H1a: There is a negative relationship between political risks and inward foreign direct

investment.

2.2.2 Economic risk

Economic risk could be manifested in assessing a country's economic strengths and

weaknesses, which include real gross domestic product (GDP), growth, the annual inflation

rate, and gross national product per head. The previous studies consider that economic risk

as an important variable for foreign investors to make a decision about investment in a host

6

country. Alfaro et al study the various links among FDI, financial market and economic

growth. The authors find that countries with well-developed financial markets gain

significantly from FDI (2004, 108). Jinjarak studies FDI and macroeconomic risk for each

US multinational industry via measuring vertical FDI share as a ratio of exports to a parent

country relative to local sales by foreign affiliates. He finds that FDI activities of US

multinationals in industries with a higher share of vertical FDI respond more

disproportionately to negative effects of macro level demand, supply and sovereign risks

(2007, 509-511). However, establishing an investment promotion agency is an effective

way to attract FDI flows. This is achieved by collecting the IPA data via questionnaires

from 68 countries where the Korean KTIPA maintains an overseas office and macro data

from published sources and conducting a series of path analysis with maximum-likelihood

estimation (Lim 2008, 44-50). Moreover, Speed and Kenisarin establish quantitative

relationships between levels of FDI per capital to the year 2004, and three sorts of

indicators relating, respectively to governance, economic freedom and corruption

perception. Based on this, they highlight that the level of FDI in the Former Soviet Union

states has been determined significantly via a planned economy moving towards a market

economy(2008, 306). Azemar and Delios test the influence of corporate taxes on FDI in

developing countries. They find a strong negative correlation between FDI and corporate

tax rates (2008, 92). On the other hand, if the MNFs’ probability of taking part in the

production process is reported as high then the MNfs pay a high level of tax (Karabay 2010,

222). Hence, after discussing the associated literature and theories, this leads to the

following hypothesis:

H2a: There is a negative relationship between economic risks and inward foreign direct

investment.

2.2.3 Financial risk

Financial risk is an umbrella term for any risk associated with any form of financing.

Typically, in finance, risk is synonymous with downside risk and is intimately related to the

shortfall or the difference between the actual return and the expected return. Estrin and

Bevan employ data to determine FDI inflows from western countries, mainly in the

European Union and in central Eastern Europe. They find that the host country risk proves

not to be a significant determinant (2004, 785). On the other hand, Xing uses panel data

covering Japanese direct investment in China's nine major manufacturing sectors from 1981

to 2002. This is in order to examine how FDI inflows from Japan were affected by the real

7

exchange rate between the Japanese Yen and Chinese Yuan. He suggests that the real

exchange rate is one of the significant factors affecting Japanese FDI in China (2006, 207).

What is more, Demmirbag et al use primary data from 145 affiliates of western MNfs in

Turkey via a survey for the purpose of exploring the institutional incorporation of the host

country and firm variable as determinants of the factors influencing perceptions of foreign

affiliate performance. They find that financial incentives do not have any significant impact

on the perceived performance of the affiliate (2007, 330). However, Tomlin uses the

implications of the model of investment under uncertainty to examine the relationship

between exchange rates and FDI in 207 U.S industries. He states that dollar appreciations

are positively correlated with service FDI flows into the U.S (2008, 537). Additionally,

Alfaro et al formalize a mechanism that emphasizes the role of the local financial market in

enabling FDI to promote growth through linkages. They conclude that there is an increase

in the share of high level growth in financially developed economies by using realistic

parameter value (2010, 248). Nevertheless, Arratibel et al highlight that a negative effect of

exchange rate volatility on FDI stock and negative relation between exchange rate volatility

and FDI is even more negative for more open economies (2010, 11). Thus, after reviewing

the related literature, the hypothesis is as follows:

H3a: There is a negative relationship between financial risks and inward foreign direct

investment.

2.2.4 Stock Market Price

De Santis et al. (2004) and Klein et al. (2002) test stock market valuations as a determinant

of aggregate and firm-level FDI, respectively, but use these valuations as proxy for

traditional FDI determinants – in particular intangible assets – or do not control for

traditional FDI determinants, and therefore do not test for a strict finance-FDI effect in the

sense of Baker et al (2009). Baker et al note that relative wealth shocks of the type that

results from exchange rate changes in Froot and Stein (1991) may also originate in stock

market price misalignments. They discuss the possibility of an effect on FDI through a

‘cheap finance’ channel (source-country overvaluation) or a ‘cheap assets’ channel (target-

country undervaluation5), and find strong evidence in favour of a ‘cheap finance’ effect on

annual aggregate US FDI flows over the 1974–2001 period.

H5a: There is a positive relationship between stock market price and inward foreign direct

investment.

8

2.2.4 Gross Domestic Product

GDP is the market value of all final goods and services produced within an economy in a

given period of time. Several studies have shown that the importance of GDP in attracting

FDI. For example, Bitzenis et al highlights that the economic variables such as GDP is

considered as first order in determining FDI (2007, 693; Caves, 2007; Dunning and

Lundan, 2008). In addition, Asiedu points out that the size of a country’s market as

measured by GDP is a key determinant of FDI inflows (2006, 73). Blonigen et al conduct a

general examination of spatial interaction in empirical FDI models using data on US

outbound FDI activity. As a result, they state that the traditional determinant of FDI such a

host country’s GDP has a strong positive and significant coefficient FDI (2007, 1314).

Consequently, based on this overview of the related literature, the hypothesis has been

formulated as follows:

H5a: There is a positive relationship between Gross Domestic Product and inward foreign

direct investment.

2.2.5 Inflation

The inflation rate means that the general level of price for goods and services is rising and

subsequently purchasing power is falling. The Inflation rate is frequently used as an

indicator of macroeconomic instability reflecting the presence of internal economic tension

of the inability or unwillingness of government. Therefore, Central banks attempt to stop

severe inflation, along with severe deflation, in an attempt to keep the excessive growth of

prices to a minimum (Mankiw 2007, 76-85). Rammal and Zurbruegg examine the

determinants of FDI for five Asian economies namely: Indonesia, Malaysia, Philippines,

Singapore and Thailand, by using a panel data set containing information on FDI flows

from home to host countries. As a result, the negative relationship shows that an increase in

the inflation rate lessens FDI in that country (2006, 409). However, Trevino et al

investigate the process of institutionalization and legitimization in countries in Latin

America and its impact on organizational decision-making regarding inward foreign direct

investment (FDI).They highlight that control variable inflation insignificant support that

lower inflation leads to greater levels of FDI.

H6a:The level of inflation in the host country is negatively associated with its level of

inward FDI.

9

Research Methodology and Empirical Analysis

3.1 Variables

The main variables used to explain the drives of foreign direct investment inflows to Jordan

are country risk ( finance, economic and political risk), macroeconomic factors (inflation,

gross domestic products GDP and interest rate) and stock market price of following sectors

(banks, services, industries and general sectors).

3.1.1 International Country Risk Guide

ICRG gathers monthly data on a variety of financial, economic and political risk variables

to calculate risk indexes in each of these categories. For instance, five financial, six

economic and 13 political factors are used. Each factor is assigned a numerical rating

within a specified range. The specified allowable range for each factor reflects the weight

attributed to that factor. As high score indicates low risk. The Financial Risk on 50 points,

Economic Risk on 50 points and Political Risk index is based on 100 points.

First of all, the financial risk’s aim is to provide a means of assessing a country’s ability

to pay its way. In essence, this needs a system of quantifying a country’s ability to finance

its official, commercial, and trade debt obligations. Secondly, the economic risk is aimed at

assessing a country’s current economic strengths and weaknesses. In general, if its strengths

outweigh its weaknesses, it will present a low economic risk and if its weaknesses outweigh

its strengths, it will present a high economic risk. Finally, the political risk is purposed to

deliver a means of assessing the political stability of the countries covered by ICRG on a

comparable basis. This is done by assigning risk points to a pre-set group of factors, termed

political risk components.

3.1.2 Stock Market Price

Stock prices shed light on the connection with FDI. Host country stock market valuations

contain relatively more information about the marginal productivity of FDI, while source

country valuations are likely to be more relevant to a foreign investor’s cost of capital.

Thus, price of different stock market sectors are used including stock mark price of

Jordanian bank, services, industries and general sectors.

10

3.1.3 Macroeconomic Variables

To improve the empirical analysis, three macroeconomic variables are considered: GDP,

inflation and interest rate. There several studies have used GDP as control variable in

determining inward FDI in a host economy such as (2007, 693; Caves, 2007; Dunning and

Lundan, 2008) interest rate and as well as inflation for example, (Rammal and Zurbruegg

2006; Mankiw 2007). Table 2 lists these variables and identifies the sources of data for

each.

3.2 Methods of Gathering Data

Monthly data for collective financial, economic and political risk are obtained from the

International Country Risk Guide (ICRG)2. As for foreign direct investment inflows to

Jordan, GDP, (GDP data are converted to monthly) and inflation data are collected from the

Central Bank of Jordan (CBJ). The sample covered period of time from 1996 to 2010.

According to the definition of the International Foreign Direct Investment Bank (IFDIB),

the percentage is the net flow of investments directed to obtain constant returns of (10%) or

more of shares with voting power at organizations functioning in a foreign economy to the

investor. This variable is share capital, reinvested returns; long and short term capital

shown in the payables balance, and this series, according to (IFDIB) indicates the net flow

of investments in the country.

Third: Data Analysis Methods

The current paper investigates the behaviour of inward foreign direct investment in Jordan

by illustrating the effects of country risk (financial, economic and political risk), the price

of different stock market sectors (banks, services, industries and general sectors) and

macroeconomic factors such as inflation, interest rate and GDP. As the data are gathered, it

was entered into Eviews-7 program in order to analyse and apply different statistical

methods. In the first stage, OLS, diagnostic tests (serial correlation, heteroskedasticity

white test, unit root test ADF) are implemented to analyse the unlagged model. In the

second stage, vector autoregressive model (VAR), co-integration test, Granger causality

2Country risk rating consists of three variables: firstly, political risk provides a mean of assessing the political stability of the

countries including government stability, corruption, and democratic accountability …exe. Secondly, economic risk provides

a means of assessing a country’s current economic strengths and weaknesses including GDP per head, real GDP and annual

inflation rate …exe. Thirdly, financial risk provides a means of assessing a country’s ability to pay its way which means the

country’s ability to finance its official, commercial and trade debt obligations …exe.

11

and error correction model (ECM) are applied to explain the dynamic movement of the

variables in the lagged system.

The quarterly GDP time series data are converted into monthly using Chow and Lin

(1971 372-375) procedure. The idea is that the GDP is observable at the quarterly

frequency, but the indicators used the indicators employed to disaggregate it are observable

at a highest frequency, the data are available on a monthly basis, and are potentially

informative variables.

In order to illustrate the method, is monthly values of one of the GDP components

and n are set of variables available monthly and contain information about .

( )

Where ( ). The monthly error term is ( )with unknown serial correlation

coefficient and V is the error covariance matrix formulated as follows:

[

]

( )

Taking quarterly averages of equation number (4.50) to obtain the following equation:

( ) or y.=X.β+μ.

Where is the matrix that converts monthly observations to quarterly averages,

where a dot subscript is a quarterly average. ( ) ( ) is the quarterly

error covariance matrix. Finally, the estimated monthly values for the GDP component

are computed by Chow-Lin’s formula as follows:

( )

12

Table 1: Description and Sources of Data

*: Not applicable

Variable Sub-variables Description Source of Data

FDI NP* Inward Foreign Direct Investment Central Bank of Jordan

Country Risk

(FR) Jordan Financial Risk International Country Risk Guide

(ER) Jordan Economic Risk International Country Risk Guide

(PR) Jordan Political Risk International Country Risk Guide

Stock Market Price

(BS) banks Stock Market Valuation Amman Stock Exchange

(SS) Services Stock Market Valuation Amman Stock Exchange

(IS) Industries Stock Market Valuation Amman Stock Exchange

(GS) General Stock Market Valuation Amman Stock Exchange

Macroeconomic

Factors

(GDP) Jordan Gross Domestic Products Central Bank of Jordan

(INF) Jordan Inflation Rate Central Bank of Jordan

(INT) Jordan Interest Rate Central Bank of Jordan

13

3 Model Specifications

3.3.1 Unlagged Model Specification

The empirical literature on the determinants of foreign direct investment inflows to

developing countries has generally focused on identifying the location specific factors and

relevant government policies that influence FDI and use models that do not have strong

macro-foundations and all country risk variables and all country risk variables (financial,

economic and political risk) such as (Alfaro et al 2004; Lim 2008; Asiedu et al 2009; Alfaro

et al 2010; and Karabay 2010; are examples of such studies). The specification of the

equation and choice of variables are inspired by the extensive empirical literature and

theories on FDI. In order to study the impact of country risk on foreign direct investment

inflows to Jordan there are two stages. The first stage involves a general form (unlagged

mode), the model is specified as follows:

( ) ( ) ( ) ( ) ( ) ( ) ( )

( ) ( ) ( ) ( ) ( )

Where represents the inward foreign direct investment in Jordan, the country risks

variables is as follows: stands for Jordan financial risk; means Jordan economic risk

and represents Jordan political risk. The stock market price variables are namely: where

refers to banks stock market price, represents services stock market price, stand

for industries stock market price and means stock market price of general sectors.

Finally, the macroeconomic factors as follows: where is Jordan gross domestic

products, is measured the inflation rate in Jordan and is the interest rate in Jordan

market

All variables in the above model have been selected on the basis of how frequently they

were cited in previous applied studies and how important (significant) were in determining

inward foreign direct investment.

Country risks such as financial, economic and political risk are included in the model

as several studies have found connection between inward foreign direct investments in host

economies. For example, Xing (2006, 2007) highlights that the real exchange rate risks as

one of the significant factors affecting Japanese FDI in China. , Busse and Hefeker (2007,

401) found that the political risks have significant impact on foreign direct investment

14

inflows. Kaisaris and Speed (2008, 309) point out that the level of FDI in the FSU states is

determined significant via a planned economy towards and a market economy. Awokuse

and Yin (2010, 222) indicate that the strengthening of intellectual property right (IPR)

protection in China has a positive and significant effect on FDI. Thus, it could be argued

that the country’s risk variables have a negative influence on inward FDI.

The model also includes the price of stock market sectors such as banks, services,

industries and general sectors. There are many researchers who have used stock market

valuations as determinants of inward FDI in host countries. For instance, Froot and Stein

1991; De Santis et al 2004and Baker et al 2009)

Some of macroeconomic factors are introduced to the model such as inflation, interest

rate and GDP, in order to improve the empirical analyses. Inflation and interest rate are

frequently used as indicator of macroeconomic instability. A high rate of inflation and

interest ( ) is a sign of internal economic tension and of the inability of the

government and central bank to balance the budget and to restrict money supply. As a rule,

the higher the rate of inflation and interest, the less foreign direct investment inflow to host

countries.

Gross Domestic Products (GDP) is included in the model as control variable in

determining inward FDI in Jordan, (2007, 693; Caves, 2007; Dunning and Lundan, 2008).

Also, inward FDI is expected to be positively related to this control variable, (Asiedu 2006;

Blonigen et al 2007).

An important consideration to be made in relation to estimating the unlagged model is

to do with the existence of spurious regression. Results of Augment Dickey-Fuller test (see

table 3) indicate that the variables should be estimated using the log first differences. The

final version of the unlagged model has the following form:

( ) ( ) ( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( )

Where: denotes the first differences of natural logarithm. The possible existence

of heteroskedasticity is a major concern in the application of ordinary least squares (OLS)

analysis, including the analysis of variance, because the presence of heteroskedasticity can

invalidate statistical tests of significance that assume that the modelling errors are

15

uncorrelated and normally distributed and that their variances do not vary with the effects

being modelled. Therefore, the White test was applied to detect whether the errors are

heteroskedasticity or homoskedasticity

( ) (

Where

The ARCH (1) model indicates that when a big shock happens in period , it is

more likely that the value of will be bigger as well. This is, when is large or small,

the variance of the next error term is also large or small. The estimated coefficient of

has to be positive for positive variance. The ARCH model implanted in E-view in the mean

and variance equations where stated above respectively. The results of ARCH show that the

model is stable.

3.3.2 Lagged Model Specification

In the second stage the lagged model is introduced to explore the dynamic behaviour of

Jordanian country risk (financial, economic and political risk), stock market price (banking,

industry, services and general sectors) and macroeconomic factors (inflation, interest rate

and GDP). Testing for long and short run relationships the following dynamic methods are

implemented: firstly, vector autoregressive (VAR) model, Granger causality, Johansen’s

Co-integration test and Error Correction Model.

3.3.2.1 Vector Autoregressive model

VAR model has the advantage of treating each variable under the study as an endogenous

variable when economic theory cannot offer a priori information regarding the variables

used in the VAR. This makes VAR estimation simple and OLS estimation method can be

used provided all variables included in the VAR are integrated of the same order Gujarati

(1995 749). In this case, the time series is affected by current and past values of ,

simultaneously, as well as the time series is a series affected by current and past values

of the series. Therefore, the following simple bivariate VAR model is considered

(Brooks 2008 290, 291)

( )

( )

16

Where and are stationary and and are uncorrelated white-noise error

terms. These equations constitute a first order of VAR model as the longest lag length is

unity. Hence, equations (7) and (8) are not reduced form since the gives a

contemporaneous effect on and gives a contemporaneous effect on .

3.3.2.2 Lag Order Selection Criteria for Vector Autoregressive Model

The selection criteria for the appropriate lag length are used to avoid over parameterising

the model and produce a parsimonious model. The Bayesian Schwartz (BSC), The Hannan-

Quinn Criterion (HQ) and the Akaike Information Criterion (AIC) are often used as

alternative criterion. They rely on information similar to the Chi-Squared test and are

derived as follows (see table 5):

( ) ( )

( ) ( ) ( )

( ) ( ) ( ( ))

3.3.2.3 Error Correction Model and Co-integration

Clearly, a good time series modelling should define both short-run dynamic movements and

the long-run equilibrium simultaneously. For this purpose, the error correction model is

introduced in this study. The error correction model is a dynamical system with the

characteristics that the deviation of the current state from its long-run relationship will be

fed into its short-run dynamics. The error correction model can be used to conduct the short

effect of the endogenous variables on the exogenous variables and as wall as the speed

adjustment at which the exogenous variable return to equilibrium after a deviation has

occurred.

There are two different ways to conduct the co-integration test. Engle and Granger

(1987) based on single equation and Johansen (1998) based on systems of equation. Engle

and Granger test the stationary of residual based on single-equation static regression of one

variable. Therefore, Johansen estimation technique is better in the sense that it uses

maximum likelihood of a full system that provides test of Max-Eigen and Trace statistics

(shown in equations 7 and 8 respectively) to determine the number of co-integrating

vectors. Therefore, in this paper the Johansen and Jesulius estimation technique has been

applied in order to determine the co-integration and the number of co-integrating vectors.

17

( ) ( ) ∑ ( )

( ) ( ) ( )

Where is the sample size, is the number of co-integrating vectors under the null

hypothesis and is the estimated value for the row of matrix ordered eigenvalue from the

matrix. Thus, a significantly non-zero eigenvalue indicates a significant co-integrating

vector.

4. Empirical Analyses

The aims of this paper are that: to identify the major determinants of foreign direct and

indirect investment, to analyse macroeconomic factors influencing inward foreign direct

investment and to identify the country's risks factors that have an effect on foreign direct

and indirect investment flows.

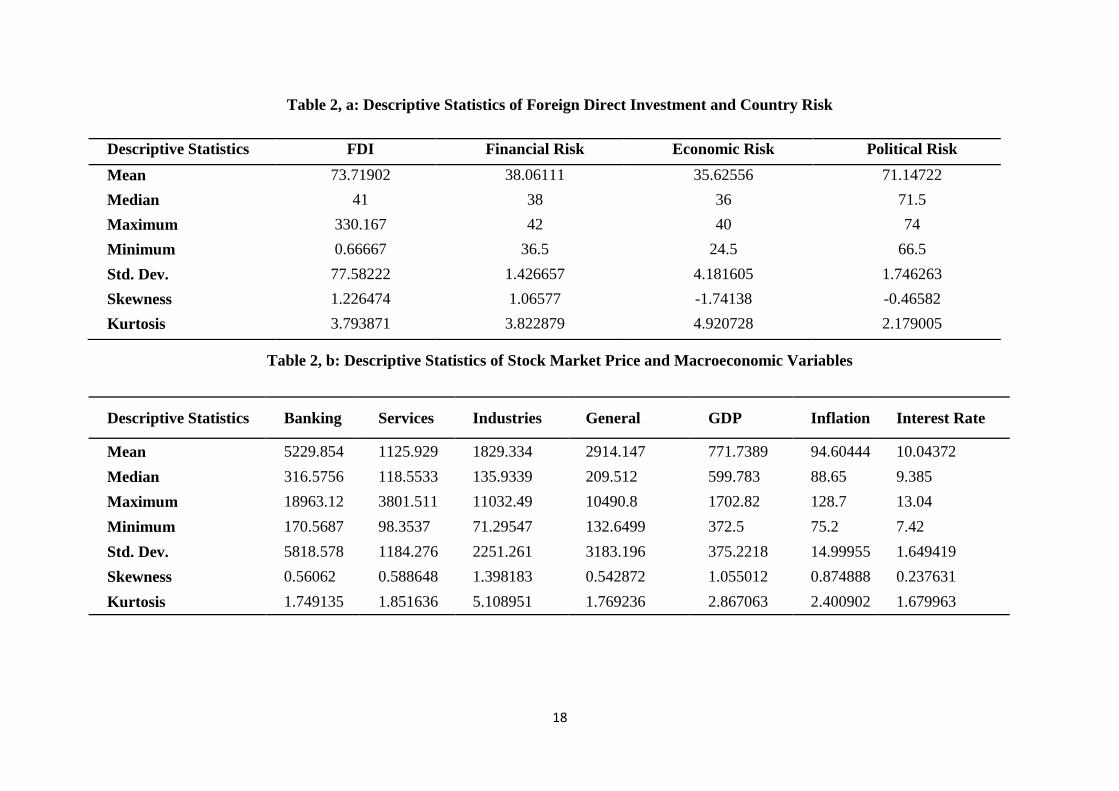

4.1 Descriptive Statistics

The descriptive statistics shown in table (2, a) reveal that the average inward foreign direct

investment (FDI) in Jordan is about 41with a sample range of almost 0.67 and 330.167

maximum. This implies that Jordan receives a good amount of inward FDI. According to

World Investment Report in 2010 Jordan has been ranked 14th regarding inward FDI

performance among Middle East countries. For instance, Saudi Arabia, Qatar and Lebanon

have been levelled 17th, 13th and 6th respectively. The country risks play a major role in

attracting foreign direct investment to inflow a host country. The three major variables of

Jordan country risk explain also the reasonable amount of inward FDI in Jordan. The

median of Jordan financial, economic and political risk are (38, 36, and 71.5) respectively,

this shows that Jordan has sensible business environment to attract foreign investors. Table

(3, b) presents the stock market price sectors and macroeconomic variables descriptive

statistics. The standard deviations of stock market price sectors (banks, services, industries

and general sectors) are more than the mean. This indicates a good variance. Table 2, b

indicates the range price of the stock market price in Amman Stock Exchange

18

Table 2, a: Descriptive Statistics of Foreign Direct Investment and Country Risk

Table 2, b: Descriptive Statistics of Stock Market Price and Macroeconomic Variables

Descriptive Statistics Banking Services Industries General GDP Inflation Interest Rate

Mean 5229.854 1125.929 1829.334 2914.147 771.7389 94.60444 10.04372

Median 316.5756 118.5533 135.9339 209.512 599.783 88.65 9.385

Maximum 18963.12 3801.511 11032.49 10490.8 1702.82 128.7 13.04

Minimum 170.5687 98.3537 71.29547 132.6499 372.5 75.2 7.42

Std. Dev. 5818.578 1184.276 2251.261 3183.196 375.2218 14.99955 1.649419

Skewness 0.56062 0.588648 1.398183 0.542872 1.055012 0.874888 0.237631

Kurtosis 1.749135 1.851636 5.108951 1.769236 2.867063 2.400902 1.679963

Descriptive Statistics FDI Financial Risk Economic Risk Political Risk

Mean 73.71902 38.06111 35.62556 71.14722

Median 41 38 36 71.5

Maximum 330.167 42 40 74

Minimum 0.66667 36.5 24.5 66.5

Std. Dev. 77.58222 1.426657 4.181605 1.746263

Skewness 1.226474 1.06577 -1.74138 -0.46582

Kurtosis 3.793871 3.822879 4.920728 2.179005

19

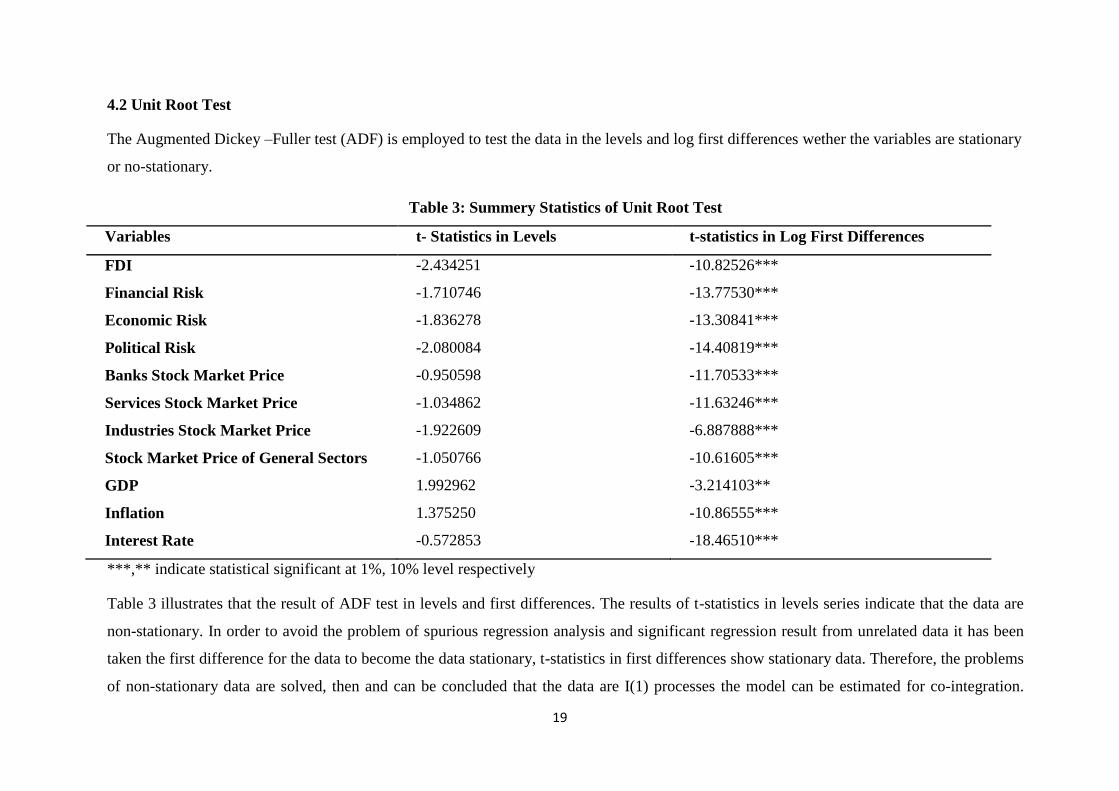

4.2 Unit Root Test

The Augmented Dickey –Fuller test (ADF) is employed to test the data in the levels and log first differences wether the variables are stationary

or no-stationary.

Table 3: Summery Statistics of Unit Root Test

Variables t- Statistics in Levels t-statistics in Log First Differences

FDI -2.434251 -10.82526***

Financial Risk -1.710746 -13.77530***

Economic Risk -1.836278 -13.30841***

Political Risk -2.080084 -14.40819***

Banks Stock Market Price -0.950598 -11.70533***

Services Stock Market Price -1.034862 -11.63246***

Industries Stock Market Price -1.922609 -6.887888***

Stock Market Price of General Sectors -1.050766 -10.61605***

GDP 1.992962 -3.214103**

Inflation 1.375250 -10.86555***

Interest Rate -0.572853 -18.46510***

***,** indicate statistical significant at 1%, 10% level respectively

Table 3 illustrates that the result of ADF test in levels and first differences. The results of t-statistics in levels series indicate that the data are

non-stationary. In order to avoid the problem of spurious regression analysis and significant regression result from unrelated data it has been

taken the first difference for the data to become the data stationary, t-statistics in first differences show stationary data. Therefore, the problems

of non-stationary data are solved, then and can be concluded that the data are I(1) processes the model can be estimated for co-integration.

20

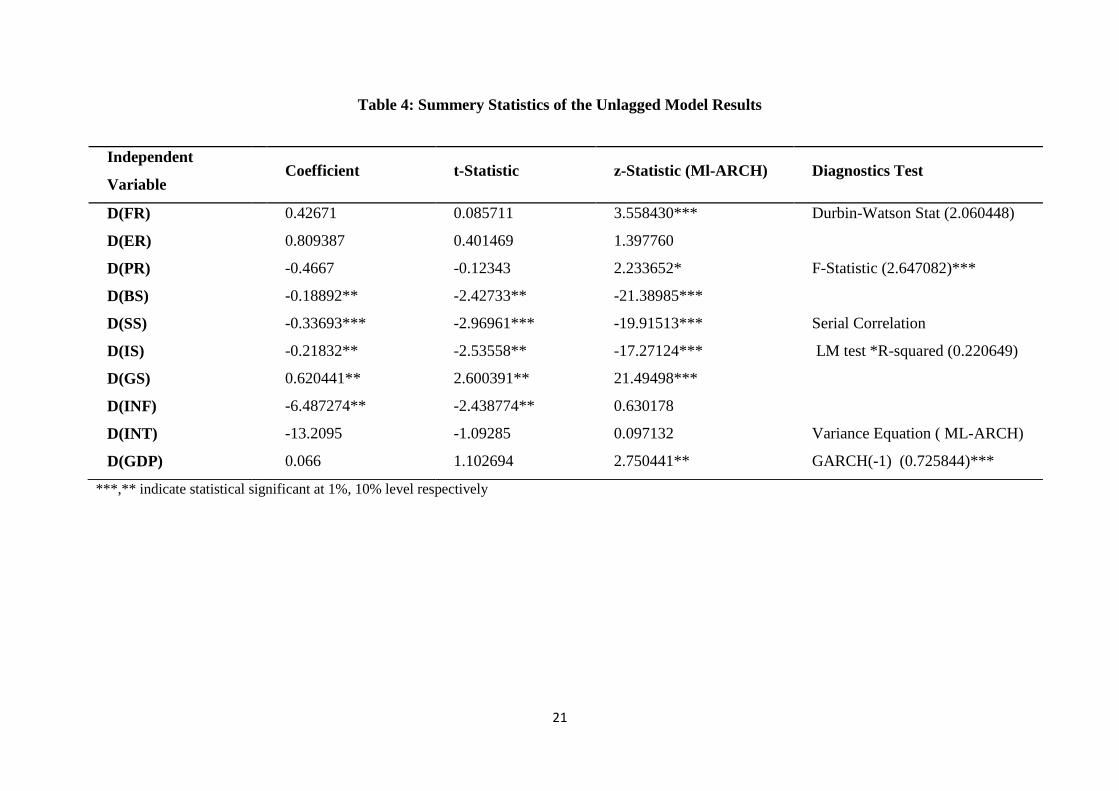

4.3 Unlagged Model

The results of OLS regression in levels show that Jordan economic risk has significant

impact on inward FDI in Jordan. Also, the stock market sectors price (banks, services,

industries and general sectors) have significant influence on inward FDI in Jordan.

Moreover, interest rate is significantly determining inward FDI. However, the D.W test

indicates a serial correlation problem and white test indicates a heteroskedasticity problem.

In order to solve these problems, the unlagged model is specified in log first differences to

remove the serial correlation and non-stationary in order to obtain robust results of OLS regression.

The Durbin Watson test (2.060448) shows that the model does not have a serial correlation

problem, but there is no significant impact of the country risk on inward FDI. The null

hypothesis of the diagnostic white test is rejected which indicates that the model suffers

from Heteroskedasticity. Therefore, ML-ARCH model is applied to solve the problem of

heteroskedasticity. According to GARCH result in table (4) the model is stable.

The results in table (4) provide the first evidence that stock market price play an important

role in FDI patterns in Jordan. The coefficient of banking, services and industry stock

market price sectors are negatively significant. This indicates that a cheap assets channel for

foreign investors. However, the coefficient of general stock market price sector is

significantly positive which consider as a cheap capital channel. Therefore, this adds a new

dimension to the FDI literature

The inflation is negatively significant affect inward FDI and this is consistent with Rammal

and zurbruegg (2006, 409) show a negative relationship between annual inflation rate and

FDI. This means that an increase in the inflation rate lessens FDI in the host country. This

is consistent with Hasen and Gianlulgi (2007, 23) findings. They study the determinants of

FDI inflows to Arab Maghreb Union (AMU) countries. They highlight that the annual

inflation rate has a negative effects and significant which explain why Maghreb countries

attract FDI less than other countries at a similar stage of development. Tevino et al (2008,

131) find insignificant direction that a lower level of inflation rate in host Latin American

economies leads to greater level of FDI. Asiedu and Lien (2011, 104) indicate that a less

inflation attract more foreign investors and promote FDI.

.

21

Table 4: Summery Statistics of the Unlagged Model Results

***,** indicate statistical significant at 1%, 10% level respectively

Independent

Variable Coefficient t-Statistic z-Statistic (Ml-ARCH) Diagnostics Test

D(FR) 0.42671 0.085711 3.558430*** Durbin-Watson Stat (2.060448)

D(ER) 0.809387 0.401469 1.397760

D(PR) -0.4667 -0.12343 2.233652* F-Statistic (2.647082)***

D(BS) -0.18892** -2.42733** -21.38985***

D(SS) -0.33693*** -2.96961*** -19.91513*** Serial Correlation

D(IS) -0.21832** -2.53558** -17.27124*** LM test *R-squared (0.220649)

D(GS) 0.620441** 2.600391** 21.49498***

D(INF) -6.487274** -2.438774** 0.630178

D(INT) -13.2095 -1.09285 0.097132 Variance Equation ( ML-ARCH)

D(GDP) 0.066 1.102694 2.750441** GARCH(-1) (0.725844)***

22

4.4 Lagged Model

In this study dynamic models are introduced such as vector autoregressive model (VAR), Granger causality, error correction model (ECM) and

co-integration test. In order to shed the light on the interaction and dynamic movements of inward foreign direct investment in Jordan, country

risk (financial, economic and political risk), stock market price( banking, services, industry and general sectors) and macroeconomic factors

(inflation, interest rate and GDP).

Table 5: Vector Autoregressive Lag Length Order Selection Criteria

*Indicates lag order selected by the criterion. LR: sequential modified LR test statistic (each test at 5% level), FPE: Final prediction error, AIC:

Akaike information criterion, SC: Schwarz information criterion, HQ: Hannan-Quinn information criterion

Lag LogL LR FPE AIC SC HQ

0 -8836.62 NA 4.88E+30 104.7173 104.9396 104.8075

1 -6928.6 3522.496 4.20E+21 83.84138 86.73052* 85.01385

2 -6800.11 218.96 5.17E+21 84.02497 89.581 86.27971

3 -6640.5 249.327 4.56E+21 83.84027 92.0632 87.17729

4 -6482.6 224.236 4.36E+21 83.67578 94.5656 88.09507

5 -6268.96 273.0611 2.34E+21 82.85158 96.4083 88.35315

6 -6084.36 209.7221 1.99E+21 82.37111 98.59473 88.95496

7 -5869.77 213.3195 1.40E+21 81.53574 100.4262 89.20186

8 -5664.7 174.737 1.36E+21 80.81298 102.3704 89.56138

9 -5357.01 218.4786 5.42E+20 78.87581 103.1001 88.70649

10 -4927.33 244.0774 8.10E+19 75.495 102.3862 86.40796

11 -4515.16 175.5975* 3.17e+19* 72.32144* 101.8795 84.31667*

23

Table (5) presents results of VAR lag order selection criteria for three tests. The

maximum possible lag length considered was eleven (months). The first column provides

the lag length for each test and the last three columns of the table illustrate the test statistics.

In this case the choice is ambiguous, because the reveal only one lag is needed by the SC,

eleven lags with the AIC and HQ. Further examination found serial correlation at one lag.

Therefore, the eleven lags length of VAR have been selected by AIC and HQ information

criterion, since they are not serially correlated.

Having confirmed the existence of unit roots for all the data series (see table 3). The next

step is to check the existence of long-run relationship among the variables. The estimated

results of Johansen co-integration test are reported in table (6). Since calculated λmax

(405.585) and Trace (1694.175) are above the critical values (70.53513) and (285.1425)

respectively at 1 percent, it can be clearly rejected the null hypothesis stating there is no co-

integration. Moreover, the second null hypothesis stating two versus three co-integrating

vectors, it also can be rejected the null hypothesis since calculated λmax (336.8631) and

Trace (1288.59) are above the critical values (64.50472) and (239.2354) respectively.

Thus, it could be seen from the table 6 that Johansen Co-integration analyses based on

unrestricted VAR results indicate 11 co-integrating equations in the system. That means the

results confirmed that foreign direct investment and its determinants, share a long run

equilibrium relationship in Jordan. This indicates that there is possibility of causality

between inward foreign direct investment in Jordan, country risk, macroeconomic factors

and stock market price. Therefore, Error Correction Model (ECM) is implemented to

investigate the direct of causality between inward FDI and its determinants.

24

Table 6: Johansen Co-integration Analysis, Unrestricted Co-integration Rank of Trace and Max-Eigen Test (VAR Lag=11)

Hypothesized No of CE(s) Eigenvalue Trace Statistic 0.05 Critical Value Max-Eigen

Statistics

0.05 Critical

Value

None * 0.96623 2263.388 334.9837 569.2128*** 76.57843

At most 1 * 0.910561 1694.175*** 285.1425 405.585*** 70.53513

At most 2 * 0.865358 1288.59*** 239.2354 336.8631*** 64.50472

At most 3 * 0.810217 951.7268*** 197.3709 279.1944*** 58.43354

At most 4 * 0.605425 672.5324*** 159.5297 156.2311*** 52.36261

At most 5 * 0.564063 516.3013*** 125.6154 139.4833*** 46.23142

At most 6 * 0.524498 376.8179*** 95.75366 124.8885*** 40.07757

At most 7 * 0.491871 251.9294*** 69.81889 113.7393*** 33.87687

At most 8 * 0.331241 138.1902*** 47.85613 67.59171*** 27.58434

At most 9 * 0.191416 70.59847*** 29.79707 35.69512*** 21.13162

At most 10 * 0.109291 34.90335*** 15.49471 19.44397*** 14.2646

At most 11 * 0.087913 15.45938*** 3.841466 15.45938*** 3.841466

Trace test indicates 11 co-integrating equations at the 0.05 level

*denotes rejection of the hypothesis at 0.05 level

**Mackinnon-Haug-Michelis (1999) p-value, (*** indicates significant at 1%)

25

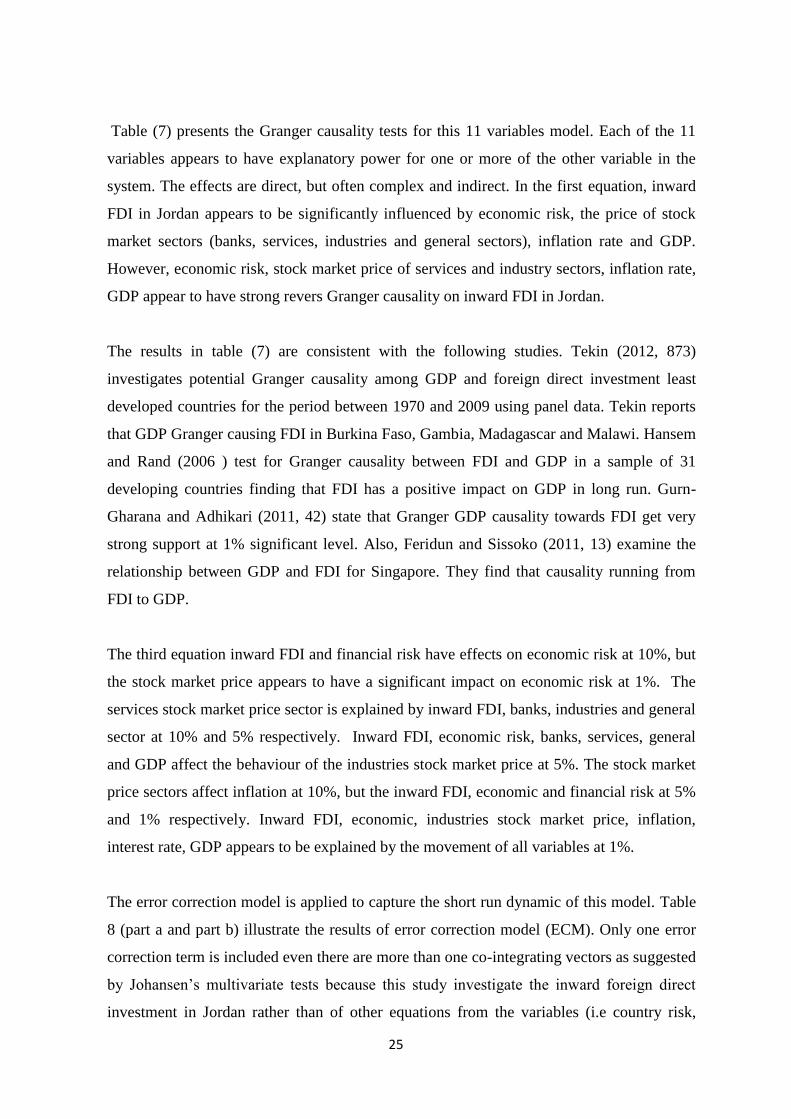

Table (7) presents the Granger causality tests for this 11 variables model. Each of the 11

variables appears to have explanatory power for one or more of the other variable in the

system. The effects are direct, but often complex and indirect. In the first equation, inward

FDI in Jordan appears to be significantly influenced by economic risk, the price of stock

market sectors (banks, services, industries and general sectors), inflation rate and GDP.

However, economic risk, stock market price of services and industry sectors, inflation rate,

GDP appear to have strong revers Granger causality on inward FDI in Jordan.

The results in table (7) are consistent with the following studies. Tekin (2012, 873)

investigates potential Granger causality among GDP and foreign direct investment least

developed countries for the period between 1970 and 2009 using panel data. Tekin reports

that GDP Granger causing FDI in Burkina Faso, Gambia, Madagascar and Malawi. Hansem

and Rand (2006 ) test for Granger causality between FDI and GDP in a sample of 31

developing countries finding that FDI has a positive impact on GDP in long run. Gurn-

Gharana and Adhikari (2011, 42) state that Granger GDP causality towards FDI get very

strong support at 1% significant level. Also, Feridun and Sissoko (2011, 13) examine the

relationship between GDP and FDI for Singapore. They find that causality running from

FDI to GDP.

The third equation inward FDI and financial risk have effects on economic risk at 10%, but

the stock market price appears to have a significant impact on economic risk at 1%. The

services stock market price sector is explained by inward FDI, banks, industries and general

sector at 10% and 5% respectively. Inward FDI, economic risk, banks, services, general

and GDP affect the behaviour of the industries stock market price at 5%. The stock market

price sectors affect inflation at 10%, but the inward FDI, economic and financial risk at 5%

and 1% respectively. Inward FDI, economic, industries stock market price, inflation,

interest rate, GDP appears to be explained by the movement of all variables at 1%.

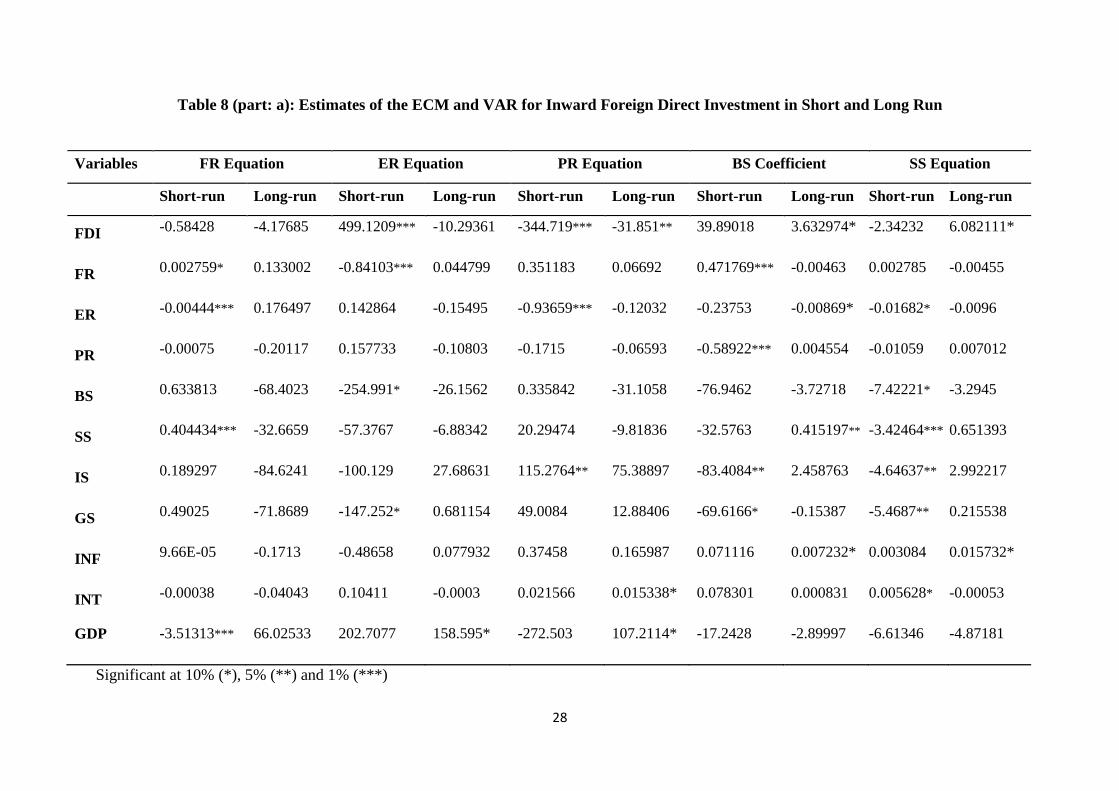

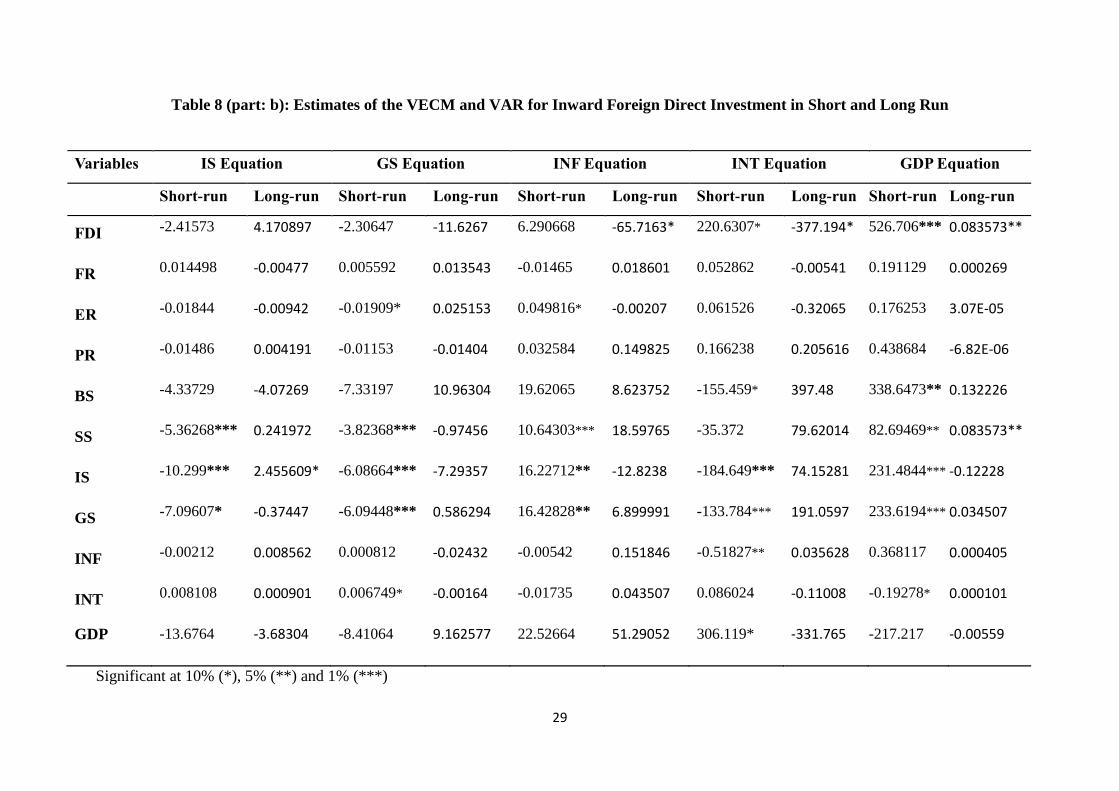

The error correction model is applied to capture the short run dynamic of this model. Table

8 (part a and part b) illustrate the results of error correction model (ECM). Only one error

correction term is included even there are more than one co-integrating vectors as suggested

by Johansen’s multivariate tests because this study investigate the inward foreign direct

investment in Jordan rather than of other equations from the variables (i.e country risk,

26

inflation, interest rate, GDP and so on). More precisely, financial risk has negative effect on

inward FDI and political risk significantly influences inward FDI with negative sign, but

the economic risk has a significant positive sign in determining inward FDI. This seems to

indicate that foreign investors would continue investing in Jordan although economic risk

perceptions have worsened in the short-run. Nevertheless, this empirical observation does

not encourage economic risk, but to highlight the short-run responses of inward FDI to

Jordan’s economic risk. In the long run, the economic risk has negative impacts on the

inward FDI in Jordan. It can be explained by Uctum and Uctum (2011, 475) study that

economic risk reduces the inflow of FDI.

Services, industry and general stock market price sectors affect inward FDI negatively, but

the banking stock market positively influences Inward FDI and statistically insignificant. In

the short-run high interest rate attracts more inward FDI. This shows that foreign investors

would remain investing in Jordan. It can be explained by Farrell et al (200, 17); Pan (2003,

832); Tolentino (2010, 114) and Uctum and Uctum (2011, 466) who report that interest rate

increase the inflow of FDI to host country. However, high interest rate would discourage

the inflow of FDI in the long-run as it considers high borrowing cost. This conclusion

supports Cuyvers et al (2011, 255) study the effects of interest rate on inward FDI in a

developing economy such as Cambodia. Cuyvers et al point out that a negative nexus

between interest rate and the level of inward FDI in a host country. Also, Wei and Liu

findings (2001); they indicate economic linkages between FDI and cost of borrowing. This

specifies that a lower cost of borrowing in the home country than in host country gives the

home country firms a cost advantage over their rivals in the host economy.

The significance of the error correction terms of these ECMs further reveals the following

interpretations. Firstly, it confirms the presence of a long –run equilibrium relationship

among the inward FDI and its determinants. Secondly, Jordan country risks,

macroeconomic factors and stock market price do jointly Granger causes the level of

inward FDI in Jordan. Finally, the estimated coefficient of error correction term indicate the

speed of adjustment among the variables towards long run equilibrium take 2 years to 2.5

years (58 months) approximately to return to equilibrium.

27

Table7: Vector Autoregressive (VAR) Granger Causality/ Block Exogeneity Wald Test

The Chi-square tests are reported in each cell with their associated p-value. Significant at 10% (*), 5% (**) and 1% (***)

Equations FDI FR ER PR BS SS IS GS INF INT GDP

FDI 21.35447* 22.92724* 25.2104** 29.84367** 39.17632***

FR 20.75454* 24.30078* 19.93121*

ER 29.21642** 27.27689** 26.3925** 19.97094*

PR

BS 34.61184*** 43.15024*** 20.22188** 28.55694** 23.27832* 25.60021**

SS 34.52445*** 30.65587** 28.45206** 23.4917* 26.55821**

IS 35.52189*** 57.01017*** 18.648** 23.83057* 23.53805*

GS 34.40376*** 42.53835*** 19.38172** 28.65669** 23.55297* 24.77008**

INF 18.46742* 19.13671* 23.60268* 19.72975* 27.92124**

INT 20.73333* 26.89246**

GDP 17.58099* 25.57754** 52.80833***

Joint 405.9396*** 141.0835 681.7122*** 90.45212 127.8285 125.1251 301.3650*** 127.4321 280.6545*** 179.0602*** 456.8541***

28

Table 8 (part: a): Estimates of the ECM and VAR for Inward Foreign Direct Investment in Short and Long Run

Variables FR Equation ER Equation PR Equation BS Coefficient SS Equation

Short-run Long-run Short-run Long-run Short-run Long-run Short-run Long-run Short-run Long-run

FDI -0.58428 -4.17685 499.1209*** -10.29361 -344.719*** -31.851** 39.89018 3.632974* -2.34232 6.082111*

FR 0.002759* 0.133002 -0.84103*** 0.044799 0.351183 0.06692 0.471769*** -0.00463 0.002785 -0.00455

ER -0.00444*** 0.176497 0.142864 -0.15495 -0.93659*** -0.12032 -0.23753 -0.00869* -0.01682* -0.0096

PR -0.00075 -0.20117 0.157733 -0.10803 -0.1715 -0.06593 -0.58922*** 0.004554 -0.01059 0.007012

BS 0.633813 -68.4023 -254.991* -26.1562 0.335842 -31.1058 -76.9462 -3.72718 -7.42221* -3.2945

SS 0.404434*** -32.6659 -57.3767 -6.88342 20.29474 -9.81836 -32.5763 0.415197** -3.42464*** 0.651393

IS 0.189297 -84.6241 -100.129 27.68631 115.2764** 75.38897 -83.4084** 2.458763 -4.64637** 2.992217

GS 0.49025 -71.8689 -147.252* 0.681154 49.0084 12.88406 -69.6166* -0.15387 -5.4687** 0.215538

INF 9.66E-05 -0.1713 -0.48658 0.077932 0.37458 0.165987 0.071116 0.007232* 0.003084 0.015732*

INT -0.00038 -0.04043 0.10411 -0.0003 0.021566 0.015338* 0.078301 0.000831 0.005628* -0.00053

GDP -3.51313*** 66.02533 202.7077 158.595* -272.503 107.2114* -17.2428 -2.89997 -6.61346 -4.87181

Significant at 10% (*), 5% (**) and 1% (***)

29

Table 8 (part: b): Estimates of the VECM and VAR for Inward Foreign Direct Investment in Short and Long Run

Variables IS Equation GS Equation INF Equation INT Equation GDP Equation

Short-run Long-run Short-run Long-run Short-run Long-run Short-run Long-run Short-run Long-run

FDI -2.41573 4.170897 -2.30647 -11.6267 6.290668 -65.7163* 220.6307* -377.194* 526.706*** 0.083573**

FR 0.014498 -0.00477 0.005592 0.013543 -0.01465 0.018601 0.052862 -0.00541 0.191129 0.000269

ER -0.01844 -0.00942 -0.01909* 0.025153 0.049816* -0.00207 0.061526 -0.32065 0.176253 3.07E-05

PR -0.01486 0.004191 -0.01153 -0.01404 0.032584 0.149825 0.166238 0.205616 0.438684 -6.82E-06

BS -4.33729 -4.07269 -7.33197 10.96304 19.62065 8.623752 -155.459* 397.48 338.6473** 0.132226

SS -5.36268*** 0.241972 -3.82368*** -0.97456 10.64303*** 18.59765 -35.372 79.62014 82.69469** 0.083573**

IS -10.299*** 2.455609* -6.08664*** -7.29357 16.22712** -12.8238 -184.649*** 74.15281 231.4844*** -0.12228

GS -7.09607* -0.37447 -6.09448*** 0.586294 16.42828** 6.899991 -133.784*** 191.0597 233.6194*** 0.034507

INF -0.00212 0.008562 0.000812 -0.02432 -0.00542 0.151846 -0.51827** 0.035628 0.368117 0.000405

INT 0.008108 0.000901 0.006749* -0.00164 -0.01735 0.043507 0.086024 -0.11008 -0.19278* 0.000101

GDP -13.6764 -3.68304 -8.41064 9.162577 22.52664 51.29052 306.119* -331.765 -217.217 -0.00559

Significant at 10% (*), 5% (**) and 1% (***)

30

5. Conclusion

The present work investigates the determinants of inward foreign direct investment in Jordan over

the period 1996-2010. Using vector autoregressive model (VAR), Johansen co-integration test,

Granger causality and error correction model (lagged model). They suggest the following findings:

Johansen co-integration test confirmed the existence of a long run equilibrium relationship

among inward FDI and endogenous variables (.Jordanian country risk (financial, economic,

and political risk), macroeconomic factors (inflation, interest, GDP) and stock market price.

The Granger causality finds the presence of bidirectional causality between inward FDI,

Jordanian economic risk, the price of stock market sectors (banking, services, industry and

general sectors), inflation rate and GDP, but for other determinants, there is presence of

unidirectional causality only. Error correction models captures the short run relationship

among the exogenous and endogenous variables.in the short-run inward FDI in Jordan is

significantly influenced by financial risk, political risk, interest rate, GDP. Vector

autoregressive model capture the long run relationship in the system. In the long-run

political risk, banking and services stock market price, interest rate, inflation rate and GDP

appear to influence the flow of FDI.

The results suggest inward foreign investment in Jordan are largely influenced by financial,

economic and political risks, inflation, interest rate, GDP, stock market price. Therefore, in order to

attract more FDI inflows to Jordan the following actions should be taken into account: insisting on

opening policy, taking investment incentives (fiscal incentives and financial incentives),

sustaining stable economic growth, limiting inflation, improving competitiveness,

strengthening the protection of intellectual property rights, overcoming bureaucratic

corruption phenomenon, making further deepening of economic reforms, enforcing hard

budget constraints, etc. Of these factors, protecting intellectual property right and striking

bureaucratic corruption are especially important. This is because a weak protection of

intellectual property right will increase the probability of imitation and thus make a host

country a less attractive location for foreign investors.

The policy makers should concentrate on creating the conditions, such as improving

shareholder rights and the quality of local legal system, that allow corporations to issue and

trade shares abroad efficiently. In addition, they should encourage that its local trading

system is linked tightly or merged with global markets. Furthermore, the government

should encourage foreign trading system and clearing and settlement operators to provide

31

services locally, remove any impediments against foreign participation. Finally, illiquid and

non-transparent local market, portfolio restrictions that require investment in local

instruments more than 10% should be lifted to attract more FDI.

References:

Alfaro, Laura, AreendamChanda, SebnemKalemli-Ozcan, and SelinSayek. "Does Foreign Direct

Investment Promote Growth? Exploring the Role of Financial Markets on Linkages."Journal

of Development Economics 91, no. 2: 242-56.

Alfaro, Laura, AreendamChanda, SebnemKalemli-Ozcan, and SelinSayek. "Fdi and Economic

Growth: The Role of Local Financial Markets." Journal of International Economics 64, no. 1

(2004): 89-112.

Arratibel, Olga, DavideFurceri, Reiner Martin, and Aleksandra Zdzienicka."The Effect of Nominal

Exchange Rate Volatility on Real Macroeconomic Performance in the

CeeCountries."Economic Systems In Press, Corrected Proof.

Asiedu, Elizabeth. "Foreign Direct Investment in Africa: The Role of Natural Resources, Market Size,

Government Policy, Institutions and Political Instability." The World Economy 29, no. 1

(2006): 63-77

Asiedu, Elizabeth, and Donald Lien. "Democracy, Foreign Direct Investment and Natural Resources."

Journal of International Economics 84, no. 1 (2011): 99-111.

Asiedu, Elizabeth, Yi Jin, and Boaz Nandwa. "Does Foreign Aid Mitigate the Adverse Effect of

Expropriation Risk on Foreign Direct Investment?" Journal of International Economics 78,

no. 2 (2009): 268-75..

Awokuse, Titus O., and Hong Yin. "Intellectual Property Rights Protection and the Surge in Fdi in

China." Journal of Comparative Economics 38, no. 2: 217-24.

Azémar, Céline, and Andrew Delios. "Tax Competition and Fdi: The Special Case of Developing

Countries." Journal of the Japanese and International Economies 22, no. 1 (2008): 85-108.

Azman-Saini, W. N. W., Ahmad ZubaidiBaharumshah, and Siong Hook Law. "Foreign Direct

Investment, Economic Freedom and Economic Growth: International Evidence." Economic

Modelling 27, no. 5: 1079-89.

Baker, Malcolm, C. Fritz Foley, and Jeffrey Wurgler. "Multinationals as Arbitrageurs: The Effect of

Stock Market Valuations on Foreign Direct Investment." Review of Financial Studies 22, no.

1 (2009): 337-69.

Bevan, Alan A., and Saul Estrin."The Determinants of Foreign Direct Investment into European

Transition Economies."Journal of Comparative Economics 32, no. 4 (2004): 775-87.

Bitzenis, Aristidis, AntonisTsitouras, and Vasileios A. Vlachos. "Decisive Fdi Obstacles as an

Explanatory Reason for Limited Fdi Inflows in an Emu Member State: The Case of Greece."

Journal of Socio-Economics 38, no. 4 (2009): 691-704.

Blonigen, Bruce A., Ronald B. Davies, Glen R. Waddell, and Helen T. Naughton. "Fdi in Space:

Spatial Autoregressive Relationships in Foreign Direct Investment." European Economic

Review 51, no. 5 (2007): 1303-25.

32

Brooks, Chris. Introductory Econometrics for Finance Second edition ed. Melbourne: Cambridge

University Press, 2008.

Busse, Matthias, and CarstenHefeker."Political Risk, Institutions and Foreign Direct

Investment."European Journal of Political Economy 23, no. 2 (2007): 397-415.

Caves, Richard E. Multinational Enterprise and Economic Analysis. 3 ed. UK: University Press,

Cambridge 2007.

Chow, G.C. Best Linear Unbiased Interpolation, Distribution, and Extrapolation of Time Series by

Related Series. Princeton University., 1971.

Cuervo-Cazurra, Alvaro. "Better the Devil You Don't Know: Types of Corruption and Fdi in

Transition Economies." Journal of International Management 14, no. 1 (2008): 12-27.

Cuyvers, Ludo, Reth Soeng, Joseph Plasmans, and Daniel Van Den Bulcke. "Determinants of Foreign

Direct Investment in Cambodia." Journal of Asian Economics 22, no. 3 (2011): 222-34.

Demekas, Dimitri G., BalázsHorváth, ElinaRibakova, and Yi Wu."Foreign Direct Investment in

European Transition Economies--the Role of Policies."Journal of Comparative Economics

35, no. 2 (2007): 369-86.

Demirbag, Mehmet, EkremTatoglu, and Keith W. Glaister. "Factors Influencing Perceptions of

Performance: The Case of Western Fdi in an Emerging Market." International Business

Review 16, no. 3 (2007): 310-36.

De Santis, R.A., Anderton, R., & Hijzen, A. (2004). On the determinants of Euro area FDI to the

United States: The knowledge-capital—Tobin’s Q framework (Working Paper 329).

European Central Bank.

De Santis, Roberto A., and Melanie Lührmann. "On the Determinants of Net International Portfolio

Flows: A Global Perspective." Journal of International Money and Finance 28, no. 5 (2009):

880-901.

Dunning, J, H andLundan, S, M. Multinational Enterprises and Global Economy Second Edition.

UK: Edward Elgar, 2008.

Egger, Peter, and HannesWinner."Evidence on Corruption as an Incentive for Foreign Direct

Investment."European Journal of Political Economy 21, no. 4 (2005): 932-52.

Engle, Robert F., and C. W. J. Granger. "Co-Integration and Error Correction: Representation,

Estimation, and Testing." Econometrica 55, no. 2 (1987): 251-76.

Froot, Kenneth A., and Jeremy C. Stein. "Exchange Rates and Foreign Direct Investment: An

Imperfect Capital Markets Approach." Quarterly Journal of Economics 106, no. 4 (1991):

1191-217.

Feridun, Mete, and Yaya Sissoko. "Impact of Fdi on Economic Development: A Causality Analysis

for Singapore, 1976 - 2002." International Journal of Economic Sciences & Applied Research

4, no. 1 (2011): 7-17.

Farrell, R., Gaston, N., & Sturm, J. E. "Determinants of Japan’s Foreign Direct Investment: A Panel

Study, 1984–1995." Centre for Japanese Economic Studies, no. CJES research papers no.

2001-1. (2000): 1-28.

Gujarati, Damodar N. Basiceconometrics. 3rd. New York: McGraw-Hill, 1995.

33

Guru-Gharana, Kishor K., and Deergha R. Adhikari. "Econometric Investigation of Relationships

among Export, Fdi and Growth in China: An Application of Toda-Yamamoto-Dolado-

Lutkephol Granger Causality Test." Journal of International Business Research 10, no. 2

(2011): 31-50.

Hasen, B., Gianluigi, G. the determinants of foreign direct investment a panel data study on

AMU countries. Liverpool Business School(2007).

Hansen, Henrik, and John Rand. "On the Causal Links between Fdi and Growth in Developing

Countries." World Economy 29, no. 1 (2006): 21-41.

Jinjarak, Yothin. "Foreign Direct Investment and Macroeconomic Risk."Journal of Comparative

Economics 35, no. 3 (2007): 509-19.

Johnston, J. and DiNardo. J. Econometric Methods. Fourth edition ed. Sydney: McGraw-Hill, 1997.

Jones, J and Wren, C. Foreign Direct Investment and the Regional Economy. USA: Ashgate

publishing company, 2006.

Kang, Yuanfei, and Fuming Jiang. "Fdi Location Choice of Chinese Multinationals in East and

Southeast Asia: Traditional Economic Factors and Institutional Perspective." Journal of

World Business In Press, Corrected Proof.

Karabay, Bilgehan. "Foreign Direct Investment and Host Country Policies: A Rationale for Using

Ownership Restrictions." Journal of Development Economics 93, no. 2: 218-25.

Katz, Barbara G., and Joel Owen. "Should Governments Compete for Foreign Direct Investment?"

Journal of Economic Behavior& Organization 59, no. 2 (2006): 230-48.

Kenisarin, Murat M., and Philip Andrews-Speed. "Foreign Direct Investment in Countries of the

Former Soviet Union: Relationship to Governance, Economic Freedom and Corruption

Perception." Communist and Post-Communist Studies 41, no. 3 (2008): 301-16.

Kinda, Tidiane. "Investment Climate and Fdi in Developing Countries: Firm-Level Evidence." World

Development 38, no. 4 (2010): 498-513.

Kolstad, Ivar, and EspenVillanger."Determinants of Foreign Direct Investment in Services."European

Journal of Political Economy 24, no. 2 (2008): 518-33.

Lim, Sung-Hoon. "How Investment Promotion Affects Attracting Foreign Direct Investment:

Analytical Argument and Empirical Analyses." International Business Review 17, no. 1

(2008): 39-53.

Lin, Feng-Jyh."The Determinants of Foreign Direct Investment in China: The Case of Taiwanese

Firms in the It Industry."Journal of Business Research 63, no. 5 (2010): 479-85.

Majocchi, Antonio, and Manuela Presutti. "Industrial Clusters, Entrepreneurial Culture and the Social

Environment: The Effects on Fdi Distribution." International Business Review 18, no. 1

(2009): 76-88.

Mankiw, N.Gregory. Macroeconomics. 6th ed. New York: Worth Publishers, 2007.

Meschi, Pierre-Xavier, and Edson LuizRiccio."Country Risk, National Cultural Differences between

Partners and Survival of International Joint Ventures in Brazil."International Business Review

17, no. 3 (2008): 250-66.

34

Moosa, Imad A., and Buly A. Cardak. "The Determinants of Foreign Direct Investment: An Extreme

Bounds Analysis." Journal of Multinational Financial Management 16, no. 2 (2006): 199-

211.

Neumayer, Eric, and Laura Spess. "Do Bilateral Investment Treaties Increase Foreign Direct

Investment to Developing Countries?" World Development 33, no. 10 (2005): 1567-85.

Pan, Yigang. "The Inflow of Foreign Direct Investment to China: The Impact of Country-Specific

Factors." Journal of Business Research 56, no. 10 (2003): 829.

Rammal, HussainGulzar, and Ralf Zurbruegg."The Impact of Regulatory Quality on Intra-Foreign

Direct Investment Flows in the AseanMarkets."International Business Review 15, no. 4

(2006): 401-14.

Ruebner, Joahua. "U.S.-Jordan Free Trade Agreement." In CRS report for congress, 2, 2001.

Russ, Katheryn Niles. "The Endogeneity of the Exchange Rate as a Determinant of Fdi: A Model of

Entry and Multinational Firms." Journal of International Economics 71, no. 2 (2007): 344-72.

Tomlin, Kasaundra M. "Japanese Fdi into U.S. Service Industries: Exchange Rate Changes and

Services Tradability." Japan and the World Economy 20, no. 4 (2008): 521-41.

Tekin, Rıfat Barış. "Economic Growth, Exports and Foreign Direct Investment in Least Developed

Countries: A Panel Granger Causality Analysis." Economic Modelling 29, no. 3 (2012): 868-

78.

Tolentino, Paz Estrella. "Home Country Macroeconomic Factors and Outward Fdi of China and

India." Journal of International Management 16, no. 2 (2010): 102-20.

Trevino, Len J., Douglas E. Thomas, and John Cullen. "The Three Pillars of Institutional Theory and

Fdi in Latin America: An Institutionalization Process." International Business Review 17, no.

1 (2008): 118-33.

Uctum, Merih, and Remzi Uctum. "Crises, Portfolio Flows, and Foreign Direct Investment: An

Application to Turkey." Economic Systems 35, no. 4 (2011): 462-80.

Wei, Y., Liu, X. Foreign Direct Investment in China: Determinants and Impact. Cheltenham: Edward

Elgar., 2001.