Embed Size (px)

Citation preview

The Business Impactof ‘Basel III’Risk Insights

• The proposed ‘Basel III’ regulation will raise capital requirements for banks, thus strengthening thestability of the global financial system.

• The new rules will affect mostly smaller financial institutions and, as a result, credit conditions forsmall and medium-sized companies.

• Countries such as the US and the UK could adopt tighter regulations than recommended by Basel III,which will impact on the availability of financing in these economies.

• Non-bank financial institutions, such as investment banks and hedge funds, will play an increasinglyactive role (as the new provisions do not concern them), raising the risks associated with this sector.

• New rules on trade financing are likely to result in tighter trade credit conditions, encouraging companies to use less secure instruments.

• As trade credit conditions tighten, country risk information is set to become even more essential tocompanies dealing with foreign counterparties.

Recommendations

Background: What is Happening and Why?

3

Outlook: What Will Happen Next?

3

3

3

Implications for D&B Customers

Contents

A D&B Special ReportOctober 2010

Recommendations

The proposed new regulations on the banking sector, known as ‘Basel III’, will improve global financialstability. However, a by-product of the regulation will be the adoption of tighter credit conditions for certain business activities. Banks will have to comply gradually with the new, stricter rules, as the fullimplementation of Basel III is not expected before 2019. Nevertheless, corporate borrowers need to beaware of the risks (and opportunities) implicit in the new context and prepare for more expensive financing terms.

1. In the medium term, as banks increase their capital ratios by reducing lending, access to credit islikely to become more difficult and borrowing costs are liable to increase.

2.However, the long implementation timeline and the fact that many major banks’ capital ratios areabove the Basel III standards will probably soften the impact of the new regulation on lending, particularly for major companies; moreover, as the new rules leave out non-bank financial institu-tions, bigger companies might consider other ways of financing, such as by raising equity or issuingdebt (i.e. selling debt bonds on the open market to finance their operations).

3. Small and medium-sized firms are likely to experience more difficult credit conditions, as the newrules affect mostly small financial institutions; moreover, raising equity or issuing debt will continueto be a much more expensive option for small and medium-sized businesses than for major companies.

4. The proposed new regulation is likely to result in significantly higher trade financing costs and tighteraccess to traditional trade financing instruments, such as letters of credit. Companies might find itmore convenient to use other forms of trade financing, such as overdraft, factoring, cash-in-advanceterms and export credit insurance.

5. As trade financing costs are liable to rise, country risk information and market intelligence will playan increasingly essential role for companies that aim to minimise costs and risks when dealing withforeign counterparties. Country Risk Services’ products, such as monthly Country Riskline Reports,can provide this information.

6. This reform also offers opportunities for companies providing services to banks, such as legal consultancies and IT firms; in particular, experts estimate that in order to comply with the new ruleslarge banks will spend around USD100m over the next ten years to adopt and integrate new datasources and forms of modelling.

New regulation willimprove financialstability but also

tighten access to credit

© Dun & Bradstreet Limited 2

Country Risk ServicesA D&B Special ReportOctober 2010

The financial sectorplays a crucial role in

the functioning ofthe economy

Background: What is Happening and Why?

Market Turmoil and Rescue PackagesIn addition to being a major employer, the financial sector is responsible for enormous amounts of money(people’s savings, for example) and, among other things, the payments system that is crucial to thesmooth functioning of the economy. As a result, maintaining the confidence of all economic actors inthe banking system is essential. For this reason, the authorities use financial regulation as a means to ensure the stability of the banking system and to promote healthy competition within it, and to correctthose ‘market failures’ that would otherwise threaten the solidity of financial institutions.

The 2007 collapse ofthe US housing

market triggered a global credit

crunch…

© Dun & Bradstreet Limited 3

Country Risk ServicesA D&B Special ReportOctober 2010

…that had a severeimpact on trade

finance

Governments unsuccessfully tried

to boost trade creditconditions

The Financial Crisis And Its Impact On Trade Finance

Some of these market failures emerged clearly during the latest financial crisis, which highlighted theneed for government and central banks to revise the sector’s regulation. In particular, the collapse ofUS housing prices in 2007 caused the decline in value and the sell-off of mortgage-backed securities,underwritten by the financial sector; this triggered a series of defaults and, in general, a confidence crisis in the liquidity and solvency of the banking sector. In this context, many banks tried to reducetheir exposure through asset fire-sales, thus accelerating the downward spiral of asset prices. As institutions restrained credit to maintain their capital ratios (the ratio of a bank’s capital to its risk; a coremeasure of financial strength) above the regulatory minimum in the face of falling asset value, a creditcrunch followed that affected lending conditions (by decreasing credit supply and increasing the costof lending) and triggered a major global economic downturn.

Declining confidence in the banking sector and the liquidity squeeze also severely impacted the avail-ability of trade finance, particularly as counterparty risk increased significantly. In 2008 the gap between demand for trade credit and supply provided by financial institutions was estimated to beUSD100-300bn, according to a 2009 survey conducted by the IMF and the Bankers’ Association for Tradeand Finance; spreads (the cost) on new letters of credit for emerging markets also rose significantly,from 10-15 basis points over the London Inter-Bank Overnight Rate (LIBOR) to 300 basis points aboveLIBOR at the peak of the crisis (LIBOR is the daily benchmark rate at which banks borrow from eachother in the London interbank market).

As a result, governments had to intervene to restore the flow of trade credit and avoid even greater disruption to the economy. Regional development banks and export-credit agencies stepped in to provide liquidity and guarantees and fill, at least partially, the gap between supply and demand. More-over, in 2009 the G20 summit agreed on a USD250bn package to support trade finance. That said, tradefinancing conditions remained negative throughout 2009 and the first half of 2010, with the exceptionof lending to top-tier firms, which has recovered relatively strongly since end-2009.

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Q1-

10Q4

Q3

Q2

Q1-

09Q4

Q3

Q2

Q1-

08Q4

Q3

Q2

Q1-

07Q4

Q3

Q2

Q1-

06

2,500

3,000

3,500

4,000

4,500

5,000

USDm USDbn

Trade Credit (left axis) World Trade (right axis)

Trade Credit

Sources: Joint OECD-BIS-IMF-WB Statistics on External Debt, www.jedh.org; IMF, International Financial Statistics

The Shortcomings of Basel II

The devastating impact of the financial crisis and the ensuing global recession prompted the authori-ties to reconsider the international framework regulating the banking system, known as Basel II. Theseaccords, developed by the Basel Committee on Banking Supervision, deal with the whole spectrum ofregulatory and supervisory issues, including liquidity standards, credit, operational and market riskmanagement and accounting standards. However, the main feature of these regulations is that bankshave to comply with a minimum Tier 1 capital requirement ratio to their risk-weighted assets of 4.0%(Tier 1 capital is core capital, consisting of equity, retained earnings and other instruments); the risk-weighting is calculated by using a standardised or internal-ratings based approach. The goal of thiscapital requirement is for the bank to be able to absorb unexpected losses, such as those that occurredduring the latest financial crisis.

However, the crisis highlighted a series of shortcomings in the Basel II accords:

• The capital requirement ratio of 4% was inadequate to withstand the huge losses that were incurred.

• Responsibility for the assessment of counterparty risk (essential to the risk-weighting of banks’ assets and therefore in assessing the capital requirement) is assigned to the ratings agencies, whichproved to be vulnerable to potential conflicts of interest.

• The capital requirement is ‘pro-cyclical:’ if the global economy expands and asset prices rise, the country and counterparty risks associated with a borrower tend to decrease and thus the capital requirement is lower; however, in the event of a recession, the reverse is also true, thus raising thecapital requirement for banks and further restraining lending.

• Basel II incentivises the process of ‘securitisation,’ as financial institutions that repackage their loansinto asset-backed securities are then able to move them off their balance sheets and thus reduce theassets’ risk-weighting. As a result, this process enabled many banks to reduce their capital require-ment, take on growing risks and increase their leverage.

© Dun & Bradstreet Limited 4

Country Risk ServicesA D&B Special ReportOctober 2010

The financial crisishighlighted the

weaknesses of theBasel II rules

Outlook: What Will Happen Next?

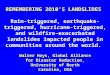

Against this background, since 2009 the Basel Committee on Banking Supervision has issued a seriesof consultative documents with the aim of reviewing the existing guidelines on the banking sector. Theproposed regulations have been widely debated, as central bankers, experts, journalists and lobby representatives have tried to contribute to the new set of rules that should address the shortfalls highlighted in the recent financial crisis. In November 2010, at the G20 summit in Seoul, the nationalauthorities will finally approve the final version of the Basel III accords.

The Capital Requirements Under Basel III

In September 2010 the Basel Committee released a consultative document on new rules for capital requirements, the core of the Basel III reform. According to the suggested new rules:

• The definition of capital will be narrowed to common shares and retained earnings; and the Tier 1capital requirement ratio will increase from 4.0% to 6.0%.

• The required ratio of equity to risk-weighted assets will rise from 2.0% to 4.5%. Under Basel III, equityover risk-weighted assets will be considered as the benchmark ratio, replacing the Tier 1 capital ratio.

• The new rules will introduce a ‘capital conservation’ buffer that will have to be above 2.5% and be metwith common equity; in periods of stress (when the banks’ capital ratio falls below 7.0%), financialinstitutions will be authorised to draw upon this capital buffer by curtailing the distribution of dividends or bonuses. These measures are supposed to address the problem whereby, under Basel II,capital requirements were inadequate to withstand significant losses.

• The Basel Committee also proposes to set up a counter-cyclical capital buffer of between 0% and 2.5%,to be in effect only in periods of excessive credit growth (based on the national regulators’ discretion).The goal of this rule is to correct the pro-cyclicality of Basel II, particularly in periods of economic expansion. In addition, the proposed regulations aim to strengthen this system by introducing a lever-age ratio of 3.0%: in any case, the ratio of capital to total assets will have to be above this threshold.

• Finally, major banks will have to comply with higher capital requirements (these are yet to be defined).

Overall, we believe that these regulations on capital requirements represent a major step forward instrengthening financial sector stability. That said, we remain wary of the risks entailed in this reform.First, the implementation timeline for these regulations is relatively loose, in order to avoid any negative impact on credit conditions and the hesitant economic recovery. Most regulations will be implemented gradually between 2013 and 2019, leaving plenty of time for national regulators and mostfinancial institutions to prepare for the higher capital requirements without affecting lending significantly. However (and as many sectoral studies have warned), we are wary of the risk that the implementation of Basel III might force certain overleveraged and smaller banks to restrict access tocredit, at least temporarily; in particular, this is likely to create tighter credit conditions for small andmedium-sized firms, and for start-up businesses.

© Dun & Bradstreet Limited 5

Country Risk ServicesA D&B Special ReportOctober 2010

Basel III aims to address the

problems of thebanking system

The new rulesstrengthen financial

stability…

Second, the impact of Basel III on economic growth in the medium to long term is less clear. The BaselCommittee and the Institute of International Finance (IIF) have published two conflicting studies onthis; although neither denies the positive effects of higher capital requirements on long-term growthby reducing the likelihood of financial crises, views on the cost of implementation differ significantly.According to the Basel Committee’s scenario a 2.0-percentage point (pp) increase in capital require-ments would negatively affect real GDP growth by subtracting just 0.04pp on an annual basis over a period of four years. In contrast with this optimistic view, the IIF argues that the same increase in capital requirements would entail an annual reduction in real GDP growth of 0.6pp over the same period. Although the risk of a significant impact on growth prospects cannot be discounted, we considerthe Basel Committee’s scenario more probable.

Third, Basel III leaves unanswered questions about non-bank financial institutions, as they fall beyondthe scope of the new regulations. Shadow banking (such as insurance firms, hedge and pension funds,and investment banks) played a central role in the latest financial crisis and has become a majorprovider of credit. However, the Basel Committee’s proposals do not concern this increasingly importantsector of the financial system; this means that Basel III affords shadow banking a competitive advantage and is likely to incentivise risk taking in this sector. Moreover, in the event of an insolvencycrisis in the non-bank financial sector, the banking system will be unlikely to remain immune to the riskof contagion.

Finally, ‘regulatory arbitrage’ will remain a problem, as some governments (such as the US and the UK)are likely to approve tougher terms or shorter timetables for the implementation of the new regulations. As a result, although Basel III promotes a set of common standards to avoid the possibilitythat banks might take advantage of regulatory differences between countries, this risk remains concrete.

© Dun & Bradstreet Limited 6

Country Risk ServicesA D&B Special ReportOctober 2010

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%8.0%

9.0%

10.0%

Capital Conservation Buffer

Minimum Common Equity Capital Ratio

2018201820172016201520142013

Risk

-wei

ghte

d A

sset

s

Basel III Implementation Timeline

Sources: Basel Committee on Banking Supervision

…but will tightencredit conditions forsmall and medium-

sized companies

The impact onmedium-term

economic growth isunlikely to be

significant

Non-bank financialinstitutions will

continue to pose athreat to stability

The Effects On Trade Finance

One of the outstanding issues highlighted by the latest financial crisis is the impact of securitisation onthe stability of the banking system. Under Basel II banks resorted to securitisation in order to reducetheir capital requirements by moving their assets off balance sheet; inevitably, this led to a significantincrease in financial sector risk, as exemplified during the sub-prime mortgage crisis. As a result, theBasel Committee is now proposing to increase the risk-weighting attached to all off-balance sheet items.The idea is to raise the credit conversion factor (the risk-weighting) of these items from the current 20%to 100%; this means that banks will have to increase their capital for asset-backed loans by a factor offive. Thus, Basel III tries to curtail leveraging and increase financial stability.

That said, as the Basel Committee’s definition of off-balance sheet items include standby letters of creditand trade letters of credit (among others), the risk-weighting of traditional trade finance instruments(which represent around 30% of world trade) is set to increase significantly as well. The implication of thisproposed rule is that banks will face a five-fold increase in the cost of trade finance; this will leave financial institutions with two options: either they will pass the costs onto their customers, or they willhave to focus on other, more profitable activities and reduce their trade credit exposure, thus restrictingaccess to letters of credit.

In either case, trade financing conditions are likely to deteriorate for most companies; in particular, businesses with exposure to emerging markets are likely to be affected, as letters of credit are usually employed in trade transactions with firms based in developing economies. As a result, we believe that,as letters of credit become more expensive, exporters are likely to switch to less expensive trade financ-ing instruments, such as open account terms, which carry less strict documentary requirements, or otherforms of unsecured financing, such as forfeiting. However, this also means that companies that willchoose less expensive trade financing products will also need to evaluate counterparty and country riskeven more carefully.

Unsurprisingly, trade finance specialists have criticised these provisions. Although off-balance sheet items have been a source of leverage in recent years, trade bills are supported by underlying trans-actions. For example, letters of credit have collaterals and a detailed documentation, are traditionally regarded as low-risk products and are extremely unlikely to become a source of potential leverage forbanks. Going forward, we warn of the risk that this five-fold increase in the credit conversion factor fortrade credit instruments might significantly restrict access to trade finance and is thus liable to havenegative knock-on effects on world trade.

© Dun & Bradstreet Limited 7

Country Risk ServicesA D&B Special ReportOctober 2010

With the cost andavailability of tradefinance likely to in-

crease significantly…

…counterparty andcountry risk

information is set to become even

more crucial

Tighter access totrade credit will

have knock-on effects on global

trade

Implications for D&B Customers

The complex architecture of Basel III will have tangible effects on the banking system and its creditconditions for the corporate world in the medium to long term: the proposed regulations are set to beapproved at the G20 Seoul summit in November.

1.We believe that the new capital requirements will have only a limited impact on access to credit, as the long-term execution of these rules should relieve pressure on most banks and, therefore, on corporate borrowers.

2. That said, small institutions and banks with lower capital ratios are more likely to restrain lending inorder to comply with the new regulations, thus impacting mainly on borrowing by small andmedium-sized firms.

3. Conventional trade credit tools, such as letters of credit, might become more expensive, particularlycompared with other financing arrangements, impacting mostly on North-South trade and, to a lesserdegree, on North-North trade.

4. As Basel III does not target non-bank financial institutions, we expect the shadow banking sector toplay an increasingly active role at the expense of traditional banking institutions.

5. The governments or central banks of some countries are liable to adopt tighter regulations, whichrepresent a potential additional cost for banks and, therefore, companies.

© Dun & Bradstreet Limited 8

Country Risk ServicesA D&B Special ReportOctober 2010

D&B Country Risk Services

At D&B Country Risk Services we have a team of economists dedicated to analysing the risks of doingbusiness across the world (we currently cover 132 countries). We monitor each of these countries on adaily basis and produce both shorter analytical pieces (Country RiskLine Reports), at least one per country per month for most countries, as well as more detailed 50-page Country Reports. For further details please contact Country Risk Services on +44 (0)1628 492595 or email [email protected].

Additional Resources

The information contained in this publication was correct at the time of going to press. For the most up-to-date information on any country covered here, refer to D&B’s monthly International Risk & PaymentReview. For comprehensive, in-depth coverage, refer to the relevant country’s Full Country Report.

CONFIDENTIAL & PROPRIETARYThis material is confidential and proprietary to D&B and/or third parties and may not be reproduced,published or disclosed to others without the express authorization of D&B.

Credits: This paper was produced by D&B Country Risk Services, and was written by Riccardo Fabiani.

© Dun & Bradstreet Limited 9

Country Risk ServicesA D&B Special ReportOctober 2010