Embed Size (px)

Citation preview

A COMPARATIVE STUDY OF CAPITAL BUDGETING AND CAPITAL RATIONING MODELS AS AN ANALYSIS FOR CAPITAL INVESTMENT DECISIONS

A literature study

done by: ,Churiah Agustini Santoso

\9f199 \2.-1 Pls:rp

UNIVERSITAS KATOLIK PARAHYANGAN FAKULTAS ILMU SOSIAL DAN ILMU POLITIK

BAN DUNG 1984

9-1 <;;. . [)'6

No. Klass ?~.~.:.(,(:') .. 9.:t.-: ... ;:;. No. Induk.l?:\!~c~ Tgi .~~.:~.;~. t-Iadioh/lleli ........................... .

TAiLE Of CONTENTS

page

ABSTRACT i

TABLE Of CONTENTS ii

CHAPTER 1

CHAPTER 2. 2.1 2.2 2.3 2 4 2.5 2.6

CHAPTER 3. 3.1 3.2 3 3 3.4

3.5 36

CHAPTER 4. 4.1 4.2

. 4.3

CHAPTER 5 5.1 5.2 5.3 5 4

CHAPTER 6.

6.1 6.2 6.3 64 6.5

CHAPTER 7

INTRODUCTION ..... 1

CAPITAL BUDGETING UNDER CERTAINTy •........••.•••... 4 Net Present Value ................................ 4 Payback ..•••..•••.....•••...•••••...•.•.••.•.•.•.• 5 Average Return on Book Value ....................... 6 Internal Rate of Return ..•.......•.......•..••..•• 8 Profitability Index ....................... 10 Application on The Investment Analys:'.s •.....••.. Program .................................... 11

CAPITAL RATIONING UNDER CERTAINTy ....•.••.••...... 16 Definition ...................................... 16 Structure ...................................... 17 Profitability Index. . ........................ 17 Ma themetica 1 Programming Linea r ....•........•... Programming. . • . . • . . . . . . • . . . • . . . . . • . . . . • . . . . . .. .. 19 Integer Programming ............................. 29 Goal Programm:'.ng •.......•.................• 34

CAPITAL BUDGETING UNDER UNCERTAINTy ..•......•..... 40 Sen~i~ivi~y Analysis/ Break-even Analysis ........ 40 DeCl.S10n frees .•.................................. 42 Simulation ........................................... 5

CAPITAL RATIONING UNDER UNCERTAINTy ..........•.... 52 Stochastic Li.near Programmi.ng ....................• 52 Chance-contra:'.ned Programming ..................... 53 Quadratic Programming ............................. 53 An Example by Salazar and Sen .................... 54

DESCRIPTION OF THE SENSITIVITY ANALySIS; ......... . PROGRAM .................... ; •......•....•..•... 59 Assumptions .....•.....•...........•............... 59 In pu t D a t a ..•.........•......•.......•.•.....•.... 59 Flowchart of The Program ....................•..... 60 Output Data ....•.............•.....•..•........... 63 Example ...............•.........................• 63

SUHt·1ARy ........................................... 67

i(i'""""RFNC' . --.c.. bS ............•...........•........................... 68

Ai)P[\DIX . . . ...........................•.............•............ 70

. . 1 1

ABSTRACT

lhe process of planning and evaluating

is called capital budget~ng. Capital

proposals t6r ~nvestments

budgeting dec~sions are

important because large 880unt ot money are committee tor long

periods of time and because these type ot decis~on are often

difficult or impossible to reverse once the funds have been

committee.

Th~s stUdy surveys difterent models dnd techniques that are used

to solve several types of ~~~i_a. bld~eting problems These types

are of simple capital budgeting and capital rationing; under

conditions ot certainty and uncertainty

·lhe analysis helps on the difficult and critical deCisions

management has to make

_ 1

The field

comprehensive and

in assisting most

goals.

or ~s~~_~_ ~nvesLment analysis is both

c~s~~=~~~=g. It clearly plays a vital role

tus~~ess ~~~ms to achieve their various

Capital budgec~=~ ~s :~e

management which esta~~~shes

investing

investment

resources

projects

long

co~conly

t~e

decision area in financial

goals and criteria for

term projects. Capital

include land, buildings,

like. These assets are facilities, equipmeD~, and

extremely important ~o :~e

all of the firm's ?r0f~t

fir~ because, in general,

are derived from the use nearly

of its capital investments; ~hese assets represent very large

commitments of resources; and c~e funds ~ill usually remain

invested over a long ?eriod of time. The future development

investment of the firm hinges on the selection of capital

projects, and the decision to abandon previously

undertakin~s which turn out to be less attractive

firm than was originally thought~

accepted

to the

The benefits of capital projects are received Over some future period, and the time element lies at the core of

capital budgeting. The firm must time the start of a project

to take advantage of short-ter~ business conditions

(construction costs for example vary ~ith the stage of

business cycle) and financing of the project to capitalize

on trends in the money markets (such as the pattern of short

and long term interest ra(2), In addition, the longevity of

capital assets and the ~3rge outlays required for their

acquisition suggest tha: :je estimates of income and cost

aSSOCiated with the pro:e:: to be documented for the time

are

:.~ons

--::..ence

2

received or out Moreover, investment

are al~ays bas~: JPon incomplete information using

of fut~re reve=':~s and costs. It is known from the

that such fC~~:25~s will always err on one side

~~e other, and the de;=~e of error may correlate "(but not

:'J.J;':;1"S) with the durat:::: of the projects. Short-term

(1 year or ::'''5S) generally display greater

than long-ter::! =stimates (S years or more). The

:; dimly seen enta:":"~ risk, and any appraisal of a

(_~:. ~ "'_21 project 1 therefo::;;;:. must necessarily comprehend some

,,"';'" ",ocsment of the risk =.c::ompanying the project. Finally,

.... ,~:;.tment , " decisions mus::. be matched aga~nst some future

to ascertain t~e accur~cy of the forecast and the

·/j;:.;",,:·.L~ty of evaluating c::~teria. In summary, the components

'if '.cpital budgeting

cost.s of

a=E~ysis involve n forecast of the

and project, discounting the funds

j fl 'f!-; .~ ted in the project 8,\:. an appropriate

project and

rate, assessing

following up to 1 11 {- associated wit:: the

Ill" I~:~i.ne if the project pe~:orm cs expected.

The application of capital budgeting are many

'I ;; r : .~ rj • In theory, a :arge n urn be r or problems

and

lend

1 J I 1". /f, .'~ e 1 v e s to analysis by 'lar~ous methods. Analysis absorbs

! i I:, (:

I!! 1/ :~ !.

,,,

and ::noney, especiall J :he more

ranking and risk management. The

sophisticated tec~niques

cost of these approaches

be justified by the ?erceived benefits~ Theory adapts

costly circumstances. Conceptually appealing but

! P' :Jniques of analysis do not merit ac=oss-the-board

:\ !' jI j j r:: a t ion. Accordingly, in establishing a cutoff by .size

(~xpenditure; that is, projects requiring an investment

,,\, ': [ a specified amount ..,il1 be subject to searching.

.; 1 I {j!. 1 n y ; below this amount, less costly criteria of

1'1 l~ptahce will be applied.

This study is an attempt to survey dif£ere~t models

.\ 11.1 t~c.hniques tha~ are used to solve several types or , 'li I 1..j 1 budgetiag problems. In the first place we make a

3

~~~~~~ction between conditions of certainty and

_ -c:: certain t y . Another important distinction

conditions

is bet;..reen

budgeting problems (no capital restriction) and

~~o~tal rationing problems (capital restriction).

Chapter 2 summarizes some techniques to solve the

s~~ital budgeting problem under certainty. Five alternatives

discussed net present value, payback period. average

on book value, internal rate of return and

~r~f~tability index.

These simple techniques cannot be used in situations

where the capital budget is limited. Chapter 3 investigates

30me techniques that can be used to solve the capital

rationing problem under certainty. Simple techniques, like

the ranking based on the profitability index proposed by

Lorie-Savage, can be used when there is a restriction in

()nl'f one

be used:

period. Otherwise mathematical programming should

this can be linear programming, integer programming

or goal programming.

Chapters 4 and 5 handle conditions or uncertainty.

Techniques

budgeting

;J n (] 1 y sis,

problem

break

that can be used to -solve the capital

under uncertainty are: sensitivity

even analysis, decision trees and

~imulation. These techniques are described in chapter 4.

Finally,

uncertainty is

't" .lne capital rationing problem under

discussed in chapter 5~ He~e, a combination

llf mathematical programming and simulation can be used, like

S.llazar and Sen proposed in their paper.

Most of the discussed techniques are illustrated with

t~xamples • For this purpose,programs available on the apple

(.omputers of the department Industrieel 3eleid have been

:lsed. The' existing capital budgeting package did not include

3 sensitivity analysis. That is why a new program was

jt~veloped • This program and some examples are discussed in

: ~1.) pte r 6.

Chapter 2.

CAPITAL 3CDGETI~G UNDER CERTAINTY.

In order to be 301e to perform an economic evaluation

of a project's desiraDil~ty. it is necessary to understand

the decision rule for accepting or rejecting investment

projects. Some methods whic~ guide management in the

acceptance or rejecc~on of proposed investments are

explained in this chapter.

2.l.Net present value.

This measure is a direct application of the present

value concept. Its computation requires the following steps:

first, choose an appropriate rate of interest4 Second,

compute the present value of the substr~ction of the cash

outl~ys from the invescment from the cash proceeds ex"ected

from the inves~ment. This gives the present value or cash flows·. The present value of the cash flows minus

initial investment is the net present value of

investment.

The recommended accept or reject criterion is

the

the

the

to

accept all independent investments whose net present value

is g,reater or equal to zero and reject all invest~ents ~hose

net present value is less than zero.

The formula for calculating PV and NPV can simply be written

as:

P'I ~ C1/0+r) + C2!(l+r;: + ••. + Cn/(l+r)'.'I.

~iPV ~ - CO + PV

4

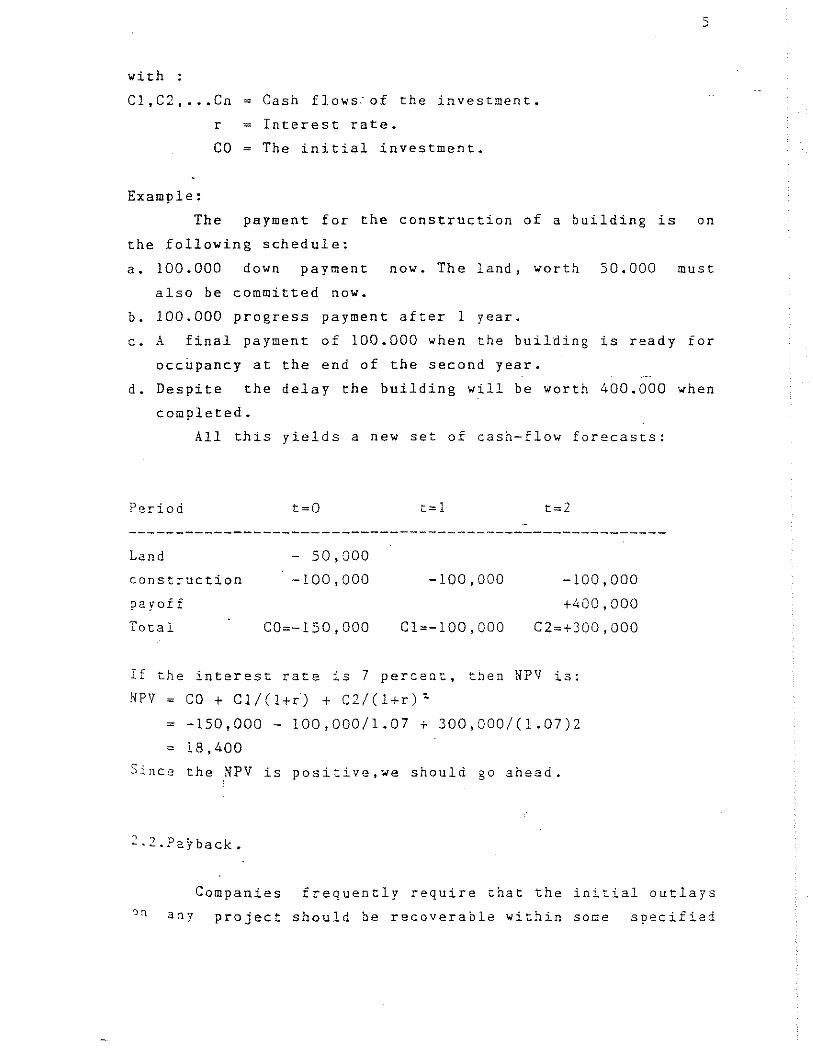

with :

C1.C2 •••• Cn - Cash flows:of the investment.

r - Interest rate.

CO - The initial investment.

Example:

5

The payment for the construction of a building is on

the following schedule:

a. 100.000 down payment now. The land. worth 50.000 must

also be committed now.

b. 100.000 progress payment after 1 year.

c. A final payment of 100.000 when the building is ready for

occupancy at the end of the second year.

d. Despite the delay the building will be worth 400.000 when

completed.

All this yields a new set of cash-flow forecasts:

Period t==l

Land - 50.000

const:-uction

payoif

Total

-100.000

CO--150.000

-100.000

C1--100,000

-100.000

+400.000

C2-+300,000

If the interest rate is 7 percent, then NPV is:

NPV CO + Cl/Cl+r) + C2/(l+r)'

- -150.000 - 100,000/1.07 + 300,000/(1.07)2

- 18,400

Since the NPV is positive,we should go ahead.

1 1 P . b ... --. 201 ack.

Companies frequently require that the initial olltlays

a:1Y project should be recoverable within some specified

cutoff period.

counting the number

:;eriod

-~"rs it

- - 3 project is

~:'!kes before

forecasted cash flows e~'~~--_ :~e init~21 investment.

Example:

Consider projects A and --

Project

A

B

Cash f::.~.:~llars

========;;:;;=====:;;;;====.=========

CO

-2000

-2000

Cl

+2000

+1000

C3

o +5000

Payback

?eriod,years

1

2

6

found by

cumulated

NPV at

10 :

-182

+3492

The NPV rule tells

project A, we take 1 ye~~

B we take 2 years.

uS to reject A and accept B. With

cO recover our 2000, with project

If the firm use= the pavback rple with a cutoff

period of 1 year, it woc~d accept only project A. If it used

the payback rule with a 2utoff period of 2 or more years it

would accept both A an& 3. The reason for the difference is

that payback gives equal weight to all cash flows before

payback date and no weight at all to subsequent flows.

order to use the payback rule the firm has to decide on

appropriate cutoff date.

2.3.Average retur~ on book value.

the

In an

Some companies jud~= an investment project by looking

at its book rate of retur~. To calculate book rate of return

it is necessary to divide :ie average forecasted profits of

a project after deprec:~::on and taxes, by the average

r~turn on book value of ::e investment. This ratio is then

7

measured against the book rate of ~etu~c the firm as a

whole or against some external such as the

average book rate of return for the ~nd~2:~7.

This criterion ignores the :ppor~~~~~! cost of money

and is not based on the cash flovs o~ ;-:--eject, and the

investment decision may be relatec to -~C ~rofitability of

the firm's existing business.

Ex amp Ie:

The table below shows projected ir,==~e statements for

project A over its 3-year life4 Its 2'~r3ge net income is

2000 per year. The required in~est~~~~ ~s 9000 at t=O.

_This amoun t is then depreciated a~ ~ constant rate of

3000 per year.

Cash ~:J~ ex 1000)

----------------------------------Project A Year 1 Year 2 Year3

--------------------------------------------------------Revenue

Out-of-pocket_ cost

Cash flow

Depreci~tion

Net income

12

6

6

3

3

10

5

5

3

2

8

4

4

3

1

So the book value of the new investment will decline from

9000 in year 0 :0 zero in year 3

Yearl Year2 Year3 Year4

---------------------------------------------------------Gross book val'Je of investment 9000 9000 9000 9000

A"ccumula teed de:,J:eciation 0 3000 6000 9000

Net book value: of investment 9000 6000 3000 a Average 12: book value=4500

8

The average net income is 2000, and the average net

investment is 4500. Therefore the average book rate of

return in 2000/4jOO = 0.44. Project A ~ould be undertaken

if the firm's target book rate of return were less

44%.

2.4.Internal Rate of Return.

than

The internal rate of return is defined as the

discount rate which makes NPV=O. This means that to find the

internal rate of return for an investment lasting T years,

~e must solve for the IRR in the following expression

NPV = Co + Cl/(l+IRR) + C2/(1+IRR)'+ .•• +CT/(1+IRR)t = 0

Actual calculation of IRR usually involves trial and

error. The easiest way to calculate IRR, if we have to do it

by h • uano, is to plot three or four combi~ations of ~PV ana

disr:ount , . . ..... lne,ana.

rate on a graph, connect the points with a

read off the discount rate at which NPV=O

smooch

The rule for Invest~ent decisions on tlle basis of IR~

is to aCcEpt an investmenL project if the opportunity cost

of capital is less than the IRR. If the opportunity cost of

capital is less than t!l.e IRR f then the project has a

positive NPV ~hen discounted at the opportunity cost of

capital. If it is equal to TiR, tl.e project ~as a zero NPY.

And if it is greater than the IRR,the projec~ has a negative

NPV. Therefore when we compare the opportunity cost of

capital wirh the IRR .Qn our project, W~ are effectivel]

asking whether our pr?j~ct has a~·positive NPV.

2xample:

;\ neW' pr.oject has an af~~r-tax cost of 10,000 and

result in after-tax cash inflows of 3,000 in year 1,

i~ year 2, and 6,000 in year 3.

will

5,000

9

NPV = -10,000 (l-;-IRR) + S,OOO/(I+IRR)" +

6,OOO/(1+IRR "

By trial and erra,," :::--- ~o find the IRR which gives result

close to zero. Uo-- ~ ~ -::; IRR, the NPV is close to zero but

negative (-38). T:=~ ,-::, for IRR 16% is positive (146). The

actual IRR is be!:-.~",-:: : 6% and 1 17% and may be found using

linear interpolatio a •

Example: NPV versuS ---

Consider two projec-::oo ~ and B which are mutually exclusive.

The cost of capital '--'" - '.J%.

Project year a ::ear 1 year 2 year 3

---------------------------------------------------------A

B

- 1, 000

-11, 000

The NPVs and the IRRs

IRR

50S

5,000

50S

5,000

the two projects are

NPV

---------------------------------A

B

24%

17%

256

1,435

505

5,000

If the firm uses the NPV criterion, project B will be

chosen, However if the firm uses the IRR criterion project A

will be preferred.

Now, ~e consider the incremental cash flow

Project year a year 1 year 2 year 3 IRR

------------------------------------------------------------3-A -10,000 4,495 4,495 4,495 16,58%

The IRR on this incremental cash flow is l6,58%, and

given a 10% cost of capital, this represents a profitable

10

opportunity and shoul~ be ac=epted. This results in a total

to the firm of A -;. (B-A) ~ B. Thus, the IRR rule cash

when

flow

used properly (i.e.on incremental basis) leads the firm

to prefer project B, but this is precisely the project which

has the higher NPV.

2.S.Profitability index.

The profitability index is the present value or the

forecasted cash flows divided by the initial investment

Profitability_index ~ present value/investment = PV/CO

The profi ta bili ty i~dex rule tells us to accept all

projects with an index greater than 1. If the profitability

index is greater than I, the present value is greater than

the initial invest::nent, and so the project must have a

positive NPV. The proritabi2..ity index! there:orc, leads to

exactly the same decisions as NPV.

For many people the profitability index is illore

intuitively appealing than t~e NPV criterion. The statement

that a P?rticular investme~t has a NPV of say $20 is not

sufficiently clear to man~ people who prefer a relative

measure of profitability. B~ adding the inior3ation that the

projectfs initial outlay (CO) is $lOO,the profitability

index (120/100 = 1.2) provides a meaningful ~easure or the

project's relative profitability in more readily

understandable terms. It is then only a small step to

convert the index of 1.2 to 20%.

However once again problems can arise ~hen mutually

excl~sive alternatives are considered. The profitability

index may be useful f,or exposition, it should not be used as

a measure of investment wor:i for projects of di££~ring size

when mutually exclusive choices have to be made.

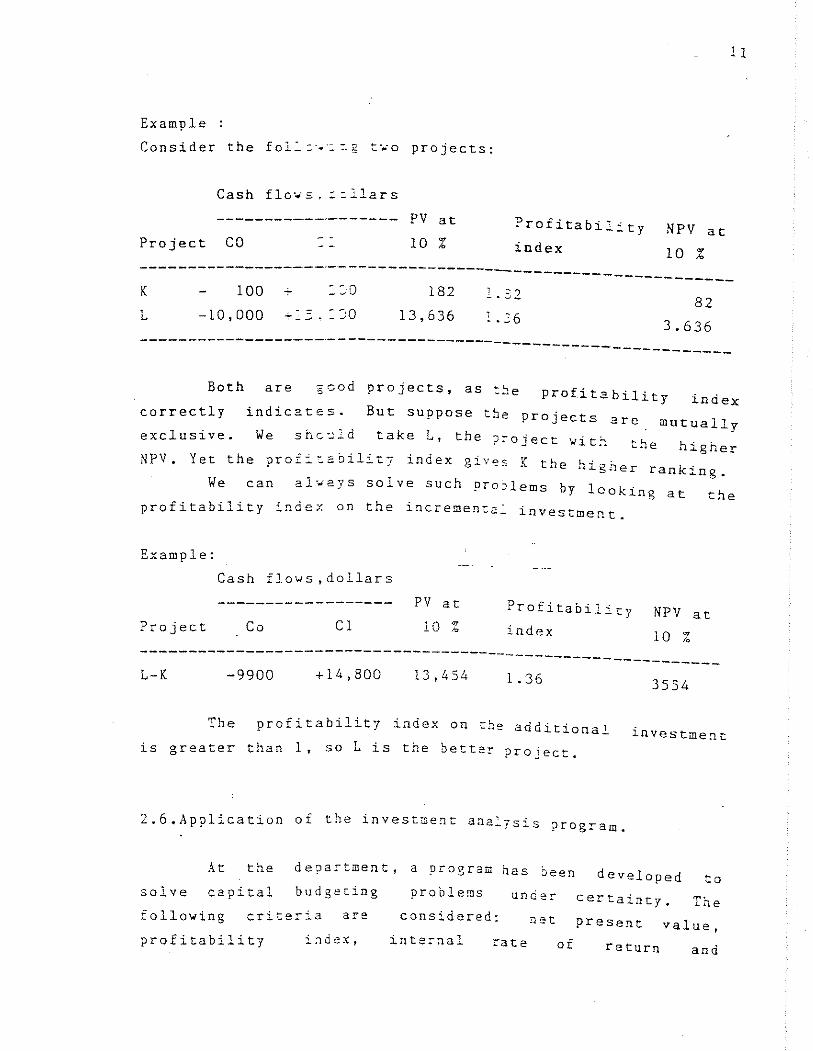

Example :

Consider the fol::"~:i t~o projects:

Cash flo·.'s. ~ :llars

Project CO

PV at

10 % ?rofitabil:'ty

index NPV at

10 %

11

------------------------------------------------------------K 100 ::"0

L -10,000 -~ = JO

182

13,636

1 :- '? - . -' ....

! .26 82

3.636 ---------------------------------------------------------

Both are 5 cod projects, as :~e profitability index correctly indicates.

exclusive. We shG~ld take L, the ?~oject ~it~ the higher

NPV. Yet the prof:':abilit7 index gives K the higher ranking.

We can always solve such pro~lems by looking at the

profitability index on the increment2~ investment.

But suppose tbe projects are mutually

Example:

Cash flows,dollars

Project Co Cl

PV at

10 % Profitability

index NPV at

10 % ------------------------------------------------------------L-K -9900 +14,800 13,454 1.36 3554

The profitability index on the additional

is greater than 1, so L is the bette~ project. investment

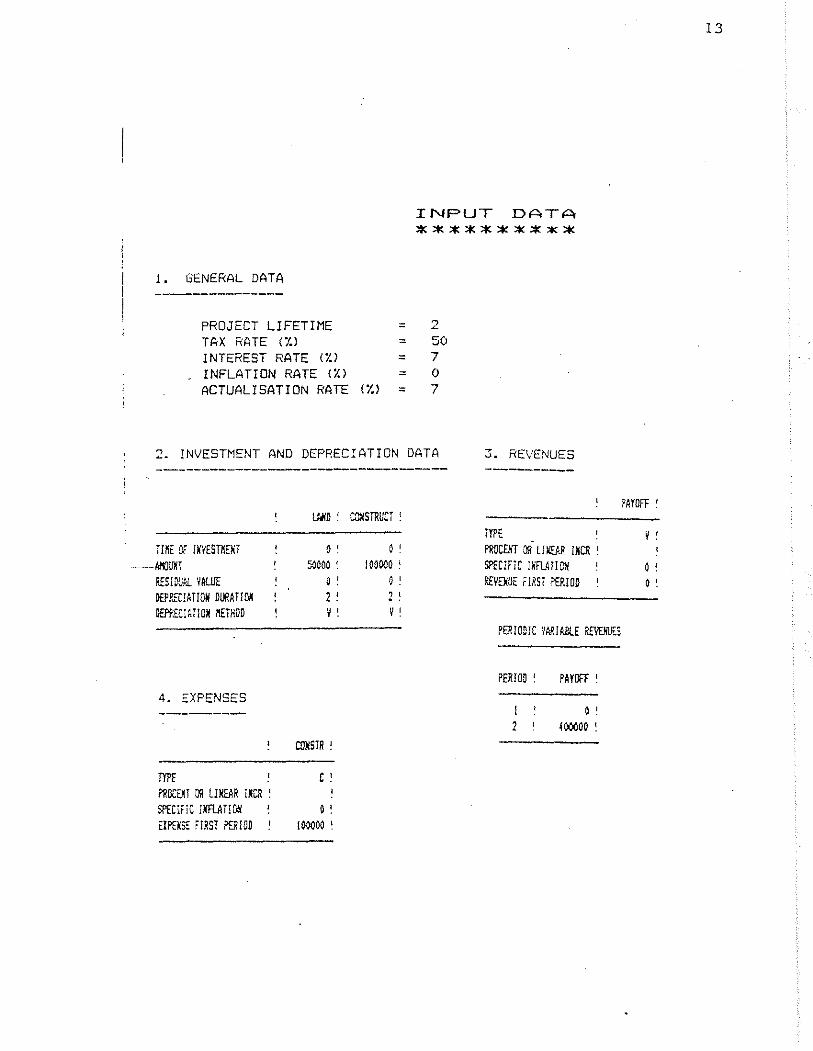

2.6.Application of tbe investme~t ana:ysis program.

At the department, a program has been developed to solve capital budgeting under Certainty. The following criter::'a are!

problems

considered: net present value, profitability inte:-nal rate of return and

12

(discounted) payback period.

Figure 2.6 is based on example 2.1 ~tax effects are

also considered now) and illustrates input and output data.

The program allows several depreciation

different

concerned,

types

not

of revenues and expenses.

schemes and

As output is

only the investment criteria are given, but

also a detailed picture of the periodic cash flows.

1. GENERAL DATA ----------

PROJECT LIFETIME TAX RATE ( %) INTEREST RATE (;.)

INFLATION RATE (I.)

ACTUALISATIoN RATE

= = = =

(;. ) =

INPUT DATA **********

2 50 7 0 7

2. INVESTMENT AND DEPRECIATION DATA 3. REVENUES

Tm Of jrIESTl!E~,

--··AI()L~l

P£SJ WAL 'IAWE O£PP.ITlATlOW DOOATlM DEP!'£CrmOH XETHOD

4. EXPENSES

TYl'f ?IUlCE!! OR ll~R iXCR ! SPfC~FiC IKFlATlOH EllUl: fIRST ?SHOD

lM'D ~

o ' 50000 '

o ~ 2 ! ~ !

COlIS,R !

r , " .

o ! 100000 '

CD:/STRUCT '

o ~ 100000 '

o ' 2 ! V '

-------

TYPE PROWIT OR ll)(SlR 1 XCR ' SPECIfiC lliFUTION REVElWE FJRSi i'EP.lOD

PERIODIC '1A!1JI.liU Rfl'ElllF.3

PERIOD !

I 2

PAYOFF !

o ' HIOOOO '

13

PAYOFF'

o ! o '

PERIODIC DEPRECIATIONS

PERIOD'

1 1

LAAD! CCXSTRUCT!

o ! o ! o ! o !

15

1. EVALUATION CRITERIA

PROJECT LIFETIME 2 TAX RATE ::.0 ACTUALISATrON RATE 7

NET ?'RESENT YALUE PROFITABILITY INDEX INTERNAL RATE OF RETURN PA)'8AQ( PERIOD

PERIODIC FLOWS

OUTF"UT DATA *********'*"*

WITHOUT TAXES

18574 1.124 11.96 1.929

WITH TAxES

-~11S .562

NEGATIVE > 2

PO/II! """" """" ! [l'{11T!/E I !'O'm:TA- I fRHAI Tim ! If!U ru ' CASI! P J:w ~

''"'' " o ' " o ' 100000 ~ -l~!

""'" . 1000») ! ;~~

PERIODIC R£VENUES

. ' -, 4. PERIODIC EXPENSES

nlJOS PR!llT "",n , , ' , ' "

, , " " -1@lQ1 ..,..., --. -~' , ' ~~ 1~1. l~~ l~~

:""'- 11O"' ! rAIB ;,! EU2I or Wv~

, ilJlI

I~I " " -l~'_ .. " , ' ~! " j' , ' !~!

Chapter 3.

CAP~TAL RATIONING UNDER CERTAINTY

3.l.DefinitiDn

The capital budgeting prDblem involves the allocatiDn

of scarce capital resources amDng cDmpeting eCDnomically

desirable projects, nDt all of which can be carried out due

to a capital (or other) constraint. This problem is referred

to as capital rationing.

is often that the restriction on the supply of

b.ottlenecks capital reflects non capital constraints or

within the firm. For example, the supply of key personnel to

carry out

restricting

Similarly,

Df

the projects maybe severely limited, thereby

the dollar amount of feasible investment.

consideration of management time may preclude the

programs beyond some level. This should more adoption

properly be called lahor Dr management constraincs rat.her

than capital cons~raints. These restrictions limit or

the maximum amau'nt of investment which can be undertaken by

the firm.

Many firms capital constraints are soft. They ~eflect

no imperfection i.:1 the capital market. Instead they are

provisional limits adopted by management as an aid to

fin2ncial control. Soft rationing should never cost t~e firm

If capital constraints become tigh~ enough to

hu:-:, then

constraints ..

the firm raises mDre money and loosens

But what if it cannot raise more money-what

the

if

it :aces hard rationing?

Hard rationi~g implies market imperfect~on-a barrier

be:'""'een the firm and capital markets. If that barrier also

that the £:~mts shareholders lack free access to a

wel:-runctioning ca?ital market, the very foundacion of net

present value crumble.

16

3.2.Structure.

The entire discussion of methods of capital

rests on the proposition tha t the wealth of

17

rationing

a firmts

shareholder is highest if the firm accepts every projects

that has a positive net present value. Suppose, however,that

there are limitations on the investment program that prevent

the company to undertake all such projects. If this is the

case, we need a method of selecting the package of projects

that is within the company's resources yet gives the highest

possible net present value.

We will survey several techniques which are applied

to the capital budgeting problem setting, under conditions

of certainty and under conditions of risk

- Capital rationing under conditions of certainty:

Lorie and Savage proposed profitabi~ity index

techniques for the single period case and the multi

period case. Weingartner formulates th-e capital ratloning

problem

model.

Since

advances

to the

model.

first as an LP theh as an integer programming

these pioneering works, there have been many

in the area of mathematical programming applied

capital budgeting problem, e.g. goal programming

Capital rationing under condi~ions of uncertainty

(see c.hapter 5).

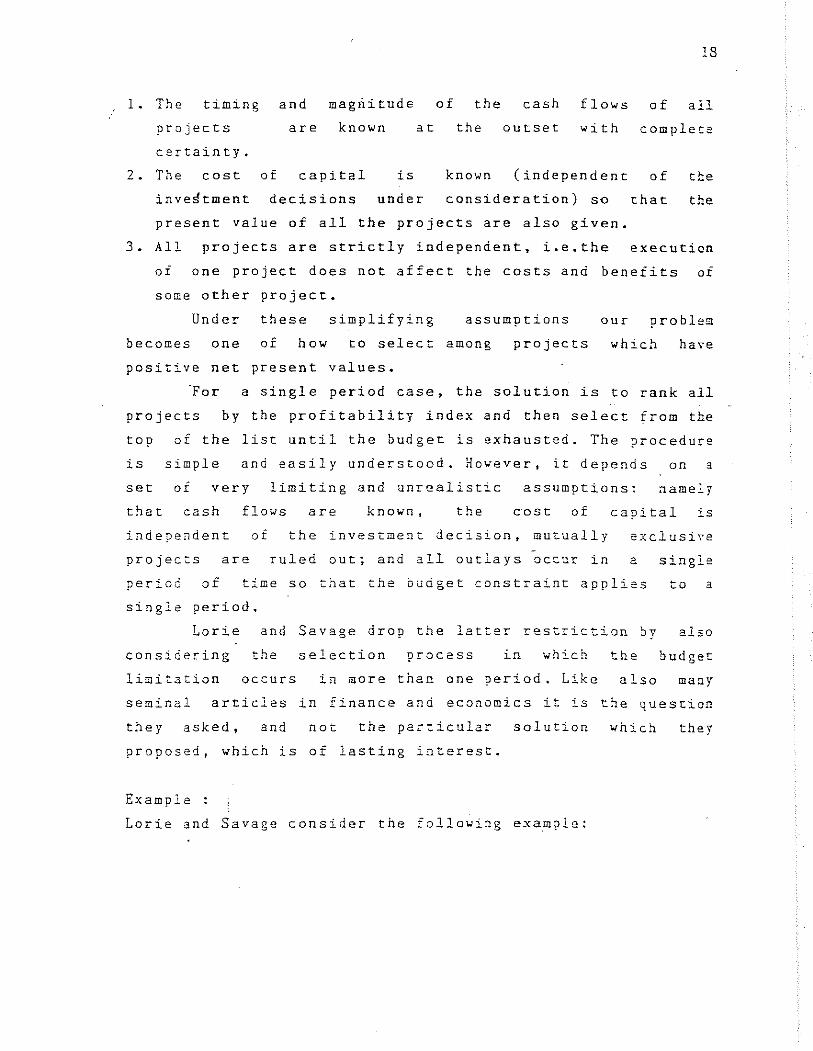

3.3.Profitability Index.

Lorie and Savage proposed a solution to ~he capital

rationing problem for the single period case and the multi

period case, on the assumption that

18

l. The timing and magnitude of the cash flows of all

projects are known at: the outset with complet2

certainty.

2. The cost of capital is known (independent of the

inve~tment decisions under consideration) so that the

present value of all the projects are also given.

3. All projects are strictly independent, i.e.the execution

oi one project does not affect the costs and beneiits or

some other project:.

Under these simplifying assumptions our problem

becomes one of how to selec:: among projects which ha,"e

positive net present values.

For a single period case, the solution is to rank all

projects by the profitability index and then select from the

top of the list until the budget is exhausted. The ?rocedure

is simple and easily understood. However, it depends

set of very limiting and unrealistic assumptions:

on a

name!.y

that cash flows are known, the eost of capital is

independent of the investment decision, mutually excl usi \'e

projects are ruled out; and all outlays occur in a single

period of time so that the budget constraint applies

single period.

Lorie and Savage drop the latter restriction by

considering

limitation

the selection process in which

occurs in more than one ?eriod~ Like

the

also

to a

also

budget

many

seminal articles in finance and economics it is the question

they asked, and not the par~icular solution which they

proposed, which is of lasting interest.

Example

Lorie and Savage consider the followi~g example:

Project /

1

2

3

4

5

6

7

8

9

Suppose

NPV

14

17

17

15

40

12

14

10

12

the

are selected,

Cash. outflow

in period 1

12

54

6

6

30

6

48

36

18

budget is 100. This

and the budget used

PI

1 • 167

0.314

2.83

2.5

1.33

2.0

0.292

0.277

0.666

means projects

is 98.

3.4.Mathematical Programming: Linear Programming.

19

Ranking

5

7

1

2

4

3

8

9

6

3,4,6,5,1,

By the linear programming(LP) the firm can examine

very large-scale choice problem in which the number or

alternatives is virtually unlimited in the relevant range.

It helps allocating and evaluating scarce resources and

provides decision makers .... ith some very insightful

information regarding the ~arginal value of resources.

The LP formulation of capital rationing is as follows:

fI max NPV = I OJ xJ

(1)

J>' II

s.t I C v ~ K, t=l,2, ... T (2 ) Jt

., J

J"

0 ~ v " ~J - 1 ( 3 )

XJ

= percent of projec~ j that is accepted

bJ

= NPV of project j over its usef~l life

.I

CJ~ = cash outflow requireC: by project

Kt = budget available in year t

in year t

The following aspects should )e noted about

problem formulation above:

20

the

1. The x J decision var~ables are assumeQ to be continuous-

that is, partial projects are a~lowed in the LP formulation.

2. The usual nonnegativity constant or L? is modified as

shown in equation(3) to also show an ,oper limit for each

project.

3. It is assumed that all the input par=.neters - DJ ,C J' .K~

,are known with certainty.

4. The b J parameter shows the NPV of project over its useful

life. where all cash flows are discounted at the cost of

capital, which is kno~n with certainty.

The marginal value to the ::c~ of the budget

constraints are obtained by comparing the total NPV with and

without an extra dollar of resources. In .L? such values are

referred to as dual 'lariables

represent the opportunicy costs

firm's resources~

or s~adow prices.

of us:~g a unit of

~. .. ney

~he

The dual LP formulation for the cap~:al ~3tioning proble~ is

as follows

K II

Min I P~ Kt + I YJ t .. t J., s. t

(a)

V

I P, Cjt + \l j ~ ':J. j :;;;lt2,.",~~ ,., .; ( b )

P" IJ) ~ 0 t =1 2 , l' =1 , .N ( c )

• • . . • - j . - , . where:

P.,. = dual decision va~iable whic~ re?::-esent3 the cost.

associaced with resource of type t.

21

/ .-IJ = dual decision variable associated with project j.

The dual formulation has important implications for

the financial manager. Namely, the dual L? and its optimal

solution provide valuable information for both planning and

control functions in the capital budgeting

This optimal solution gives the shadow

accepted and rejected projects.

decision process.

prices for the

These values enable the decision maker to rank all

projects according to their relative attr3c~iveness.

under

For accepted projects

the slack variables ( S,,) the shadow prices are found

for the following constraint:

The shadow prices are computed using the following

expression

= shadow price associated with accepted project

(shown under the slack variable associated with

project j)

= NPV for project j shown in the objective function.

p: = shadow price in the optimal solution associated with

each resource t which is required to accept a

project. (shown under the slack variable associated

with the corresponding resources).

C[\. = quantity of

j .

resources of type t required by project

The shadow prices YJ

may very well give a ranking for

the projects which di£fe~s from that given by any of the

simple models as payback, NPV, IRR,or the profitability

index. Such differences in ranking will exist because the

latter models look at projects independently.

,/

22

The shadow pric.es show interrelationships among

projects by means of the budget constraints. They evaluate

the projects at cost of capital ( p~) that is implied by the

optimal use of resources of type t.

For the rejected projects the shadow prices are

computed in an analogous way as for accepted project.

llJ = T

I P'" ,

= shadow prices associated with rejected project

j (shown in the objective function row in the column

for x J ).

The llJ value shows the amount by which the objective

funtion would decrease if the firm were forced to accept the

unattractive

would mean

project

that the

j. If such projects were accepted,this

scar~e capital budget dollars would be

used in a suboptimal way, since the- opportunity cost

with the cash outflows C-Ip" c.,\:---) exceeds , . associated the

present value of the benefits generated by the projects.

It should be mentioned that the values must be zero

for all projects that are accepted (including partially

accepted projects) because the benefits of these projects

must justify the cash outlays in the various periods of the

planning horizon (C)~ ) when they are evaluated at the

implied cost of capital ( p~) when the budgets each year are " llsed in an optimal way~

Example:

Lorie and Savage nine-project problem.

Project NPV

1 14

2 17

3 17

4 15

5 40

6 12

7 14

8 10

9 12

Cas.h outflow

in period 1

12

54

6

6

30

6

48

36

18

Budget available I c.Jx) ~50

The LP formulation is as follows :

Cash outflow

in period 2

3

7

6

2

35

6

4

3

3

Max NPV ~ 14x, + 17x~ +17x~ +lSx~ +4Cx r +12xb

s • t •

, 1 " ..... T.l."' .... '3

12x, + 54x, +6x l +6x ... +30x s

+6x& +48x, +36x& +18x~ ~ SI ~ 50.

3x, + 7X, +6x, +2x.., +35x,.

+6x, +4x 1 +3x 8 +3x, + 5,

x, + S:; ~ 1 x., + S , ~ 1

x, + S ... ~ 1 x, 51 ~ 1

X 3 + S 5' = 1 x '" + Sa = 1

::: 20~

x1 + S"

x& .;- S '\0

x, .;- S"

x S ) 0 i ::;; 1 ,2 t .. ,11. J

, ~ • j ::;; 1 f 2 , ,9.

= =

=

budget constraint

year 1

budget constraint

year 2

1 Upper limits

1 on project

1 acceptance

Non negativity

constra.int

23

The problem has been solved with a package on Apple

II developed at the department.

24

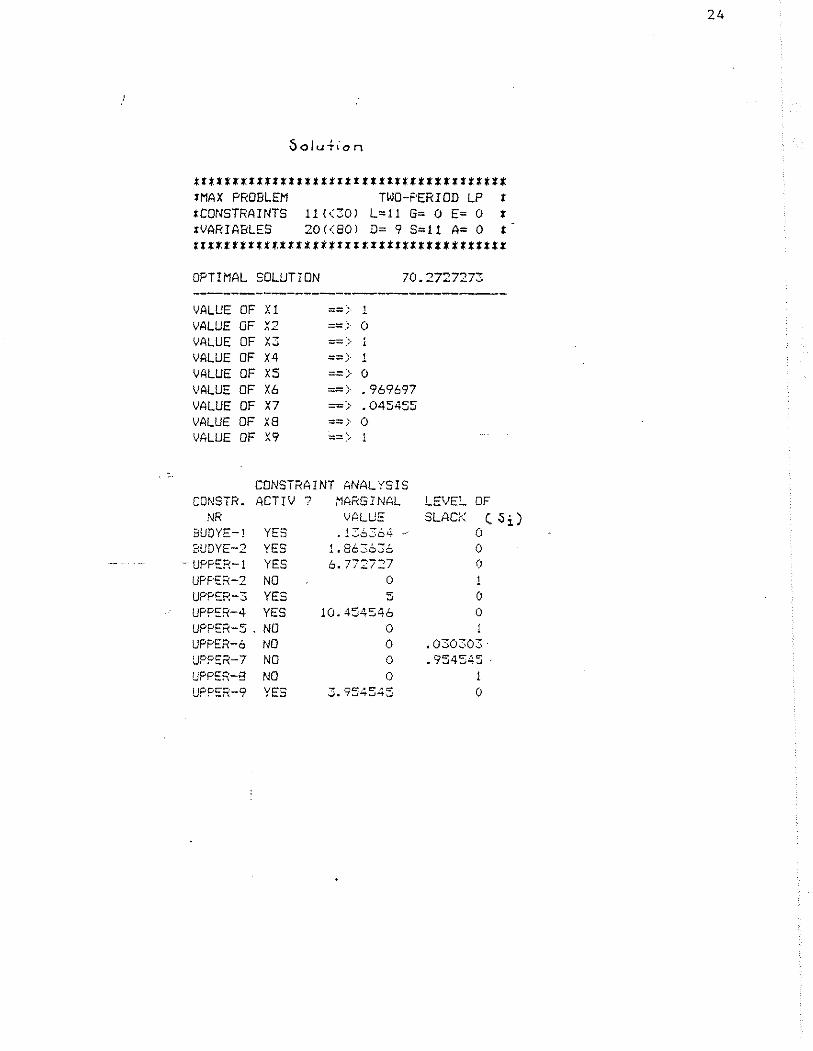

5olu·hon

ttlttttttttttttttlllllllltltttttl'ttttt lMAX PROBLEM TWO-PERIOD LP 1 tCONSTRAINTS 11 «30) L=ll G= 0 E= 0 i ,VARIABLES 20«80) D= 9 S=11 A= 0 1 tttfftil1itttllittltltlltlllttttttttt'l

OPTIMAL SOLUTION 70.2727273 --------------------------VALUE OF Xl ;:::;=;. 1 VALUE OF v.,

"~ ==.;. 0

VAl.UE OF v_ "" ::=::>

VALUE OF X4 :::=> 1 VALUE OF X5 => 0 VALUE OF X6 ==} .969697 VALUE OF X7 =} .. 045455 VALUE OF XS ==;- 0 VALUE OF X9 ==>

--CONSTRAINT ANALYSIS

CONSTR .. ACTIV ? MARGINAL LEVEL. OF NR VALUE SLACK Ui)

8UDYE-j YES .. 1:6364 -- ()

BUDYE-2 YES 1.863636 0 -tJPPER-l YES 6.77:727 (l

UPF'£R-2 NO 0 UPPER-3 YES 5 0 UPPER-4 YES 10.454546 0 UPPER-5 NO 0 1 UPPER-6 NO 0 .030303-UPPER-? NO 0 .. 954545 UPPER-8 NO 0 1 UPPER-9 YES 3.954545 0

25

We see that the basic variables, that is f the

variables that are equal to a positive value in the ~pt=-mal

solution are ! x." x~, x~, x" x 1 , x~ (column value or x)

and S."S1' S" S~, S,o (column level of slack).

Any of the variables in the problem which are equal

to zero, are in fact, non basic va~iables in the opt:.mal

solution. Thus, X 1. = xI" = xa = 0, which shows that these

three projects should be completely rejected; in addition

S,= S~ = 0, shows that the entire budget of 50 in year 1 and

20 in year 2 has been spent on the six projects that have

been designated lor acceptance. Further-, S; = Ss- = S6 = S" = 0, since the project corresponding

100% accepted.

to these slack

variabl~s have been

These projects require the use of the entire budget

in both years and generate the maximuQ objective func~ion

value of 70,2727273, which is the NPV of the accepted

projects.

The marginal value of const~aint ~umber 1 (the shadow

price of s, ) is O~136364 which means that the object:"ve

func~ion would increase by this amount (b.136364) for each

dollar of additional budget they could obtain.

constraint is active because any changes in tha cons~raint

can change the objective function.

The same explanation can

conseraints.

be used

LP models seem tailor-made :or

for the other

solving capi'L.al

budgeting

they not

problems when resources are 1~3ited. Why then are

universally accepted either in theory or in

practice? .One reason is that these models are often not

cheap to use. LP is considerably c~eaper in terms of

computer time, but it cannot be used when large t indiviSible

projec'L.3 are involved.

As with any sophisticated long-~3nge planning too 1

there is the general problem of getting good data. It is not

just worth applying costly, sophisticatad methods for poor

26

data. Furthermore, these models are based on the assumDtion

that all future investment opportunities are known. In reality,

process.

the discovery of investment ideas is an unfolding

Before we leave the area of linear programming a

appropriate LP noteworthy controversy relative to the

formulation should be mentioned. Under capital rationing,the

appropriate discount rate to use in determining the net

present values of projects under consideration cannot be

determined until the optimal set of projects is determined,

so that

well as

the size of the capital budget is ascertained as

the sources of the subsequent finanCing and hence

the cost of capital (or the appropriate discount rate to use

in calculating NPVs). This is a simultaneous problem wherein

the firm· should concurrently determine through an iterative

mathematical programming process bot~ the optimal set of

capital projects and the optimal finanCing package, with its

associated cost of capital to be used in the discounting

process.

Weingartne~ suggested an operational approach; his

model assumes %hat a:1 shareholders have the same linear

utility preferences for consumption~ And it makes the period-

by-period .utilities iadependent of one another. He t.hen

proposes

dividends

a more operational mode1 1 which maximizes the

to be paid in a terminal ye~r, where throughout

the planning horizon dividend are nondecreasing and can be

required to achieve a specified annual growth rate. Over the

past decade, several other authors have jumped into the

c~n,troversy, each suggesting his own reformulation.

The Weingartner 1 s basic horizon model is as follows

Max Z = -; 11, x J i- v, - w_ - ,

J s • t •

.1 a 'J J

Xl i- v, - w, 1. - D, (a)

27

~ a'l X J - (l+r)v t •. 1 + v .. + (l+r)w •. , - WI. 1. D"

t = 2, •• o,T ( b )

j:::;: l, .... ,n ( c )

t = 1, .•• ,T ( d )

where: ~ value of all cash flows of project j subsequent to a J =

the horizon discounted to the horizon at the market

rate of interest, r •

x J = fraction of project j accepted.

T = horizon year.

vt = amount available for lending in period t .

w ... = amount borrowed in period t.

a 'J = cash flow in period t from project

j.(pos-expenditure!outflow, neg-revenue/inflow)

D t - anticipated cash t~row-off in period t.

The dual of the basic horizon model is as follows:

T n Min p. D-t, +

s. t

2. J' ,

,. J.., p. j =l, ... ,n .. (1)

~ 1 ( 2)

). -1 "

(3)

p. .. , - O+r)p. ,. 0 • (4)

;;. 0 • t -2 ••••• T ( 5 )

( 6 )

28

The following derivations help to understand the meaning of

the dual variables

(2)and(3) Po'" = 1 (7)

(4)and(5) p:- ,

(1+r) (8) = f\

(7)and(8) P+..~ = (1+r) f: ~~ (1 +r) ,

.. = ft. >.

= i-l f~ (l+r) t + r-t.

= (l+r)r-~

So, one can see that f. is the compounded rate of

interest which expresses the yield at the horizon of an

additional dollar in year t.

• When a project is

corresponding restriction

fully accept.ed ,- that: is, x_ = 1 J

of the form of (a) becomes

.-t,P~a"J

~

= a J

,. T_ t

+ I (-a,,)(1+r) ~

= a J t: "'-.

This is the value of the projec~ a~ time T. This

the same as saying that the NPV of the ?roject should

positive.

...

,the

is

be

For the rejected project we know that x J = O,and also ~ • ~ 11 x J ' i, and therefore ,oJ = 0.

This is the same as saying that the NPV is smaller than O.

29

3.S.Integer programming .applied

problem.

to the capital rationing

The main mocivations for the use of IP in the capital

rationing problem setting are the following

1. Difficulties imposed by the acceptance of partial

projects in LP are eliminated.

2. All the project interdependencies can be formally

included in the constraints of ILP, while the same is not

true for LP due to the possibility of accepting partial

projects.

In using the simple capital budgeting models

(NPV,IRR,PI.etc) it is assumed that all the investment

projects are independent each other (i.e.that project cash

flows are not related to each other and do not influence or

one another if various projects are accepted). In change

using ILP, virtually any project dependencies (mut:lally

exclusive, prerequisite, complementary) can be incorporated

on the model.

The general ILP formulation for :he capital rationing:

N

Max NPV = l . j-1

st

t=1,2, ..... T

j=1.2 •••• N

There are three types of project dependencies:

a. MutuallY exclusive projects.

A set of projeccs wherein the acceptance of one project

in the set includes the simultaneous acceptance or any

other project in the set. It is incorporated in the model

by the following constraint:

J

l.. x ~ 1 J.;:.J

~ set of mutually

consideracion

30

exclusive projects under

jb:J ~ chat project j is an element of the set of mutually

exclusive project J.

This constraint states that at most one project from set

J can be accepted; this means that the firm could choose

not to accept any project from set J. On the other hand,

if it was necessary to select: one project from the set,

the above contraint would appear as a strict equality

2.. X' ~ 1 jE.J J

b. Prerequisite/contingent projects.

Two or more projects wherein the acceptance of one

project (A) necessitates the prior acceptance of some

other project(s) (Z):

x"" ~ X '1..

If project A cannot be accepted unless project Z is

accepted, we could say that project Z is a prerequisite

project for acceptance of- project"-A; alternatively, we

could

upon

say that the accept:ance of project A is contingent

the acceptance of project Z. However project Z can

be accepted on its own and project A rejected.

c. Complementary projects.

Wherein the acceptance of one ~rojec~ enhances the cash

flows of one or more other projects.

There are t~o complementary projects,7 and 8. Either of

these projec=s can be accepted in isolation. However, if

both are accepted simultaneously : the COSt will be

r~duced by say 10%. The net cash inflow will be increased

by 15%. To handle the problem, a ne~ project (project 78)

would be constracted. The constraint below is needed to

preclude acceptance of both projects 7 and 8 as well as

78; because the latter is the

consisting of the t~o former projects.

xl + x 8 + x r8 ::i 1

The shortcomings of the ILP:

31

composite project

a. ILP is probably only feasible for small to medium size

capital budgeting problems (25 constraints and 100

projects).

be paid

We have to think whether the price that has to

in moving to ILP from LP is worth the benefit

gained.

b. 'leaningful shadow prices (which show the marginal change

in the value of the objective function for an incremental

change in the right hand side of various constraints)

are not available in ILP. That is, many of the

constraints on ILP problem which are not binding on the

optimal

of zero,

integer solution

whic!) indicates

will be assigned shadow

that these resources are

prices

"free

goods fT• In reality this is not true since the objective

function would clearly decrease if the availability of

such resources were decreased.

Example:

Consider the following 15 projects

32

Cash outilows

P,oject Clj C2j Cj NPV

------------------------------------------------------------1 40 80 0 24

2 50 65 5 38

3 45 55 10 40

4 60 48 8 44

5 68 42 0 20

6 75 52 20 64

7 38 90 14 27

8 24 40 70 48

9 12 66 20 18

10 6 88 17 29

11 0 72 60 32

12 0 50 80 38

13 0 34 56 25

14 0 22 76 18

15 0 12 104 28

Budget

constraints: L CljXj~300; L C2jXH540; Z C3jX] ~380

Project interrelationships :

1. Of the set of projects 3, 4, and 8, at mos~ two can be

accepted.

2. ?rojects 5 and 9 are mutually exclusive, bu: one of the

two must be accepted.

3. ?roject 6 cannot be accepted unless both projects 1 and

14 are accepted.

4. Project 1 can be delayed 1 year, the same cash outflows

will be required, but the NPV will drop to 22.

5. Projects 2 and 3 and projects ]0 and 13 can be combined

into complementary or composite projects wherein total

cash outflows will be reduced by 10% and NP'/ increased by

12% compared to the total of the separate projects

33

6. At least one of the two composite projects above must be

ac~epted

Solu1:~on:

Maximize NPV :

24:>::, + 38X .. + 40X!J + 44X .. + 20X s + 64X, + 27X, (a)

+ 48X8 + 18X .. .;. 29X,0+ 32X,,+ 38X".+ 2SX,"!> + 18X, ...

+ 28X,\"+ 22X.,.+ 87 • 36X<7 + 60.48X,8

subject to

40X, + SOX. + 45X, + 60X .. + 68X ... + 75X. + 38X7 (b)

+ 24X8 + 12X~ + 6X,0+ 85.5X'7+ 5.4X,8 ~ 300

80X, + 6SX,,- + 55X 5 .,. 48X.., + 42X ,.- + 52X ~ + 90X -r + 40X e + 66X ., + 88X,o + 7 2X" + 50X,>.+ 34X .. ~

- + 22X '\"i + 12X,s-+ 40X ". + 108X'7+ 109.8X,8

5X, + lOX 3 + 8X", + 20X" + 14X 7 + 70X8 f 20X,

+ 1 7X 10 + 60X.n + BOX "1'1.,. + S6X 1~ + i6X-1 "'t + to"ttX 1~

v X., + Xi ~ 2 -' I

X ,+ v A":j ~ 1

2X to ~ X, + X' ... ei'cher constraint (g) or

2X ~ v

H2o+" X, .. (h ) must be satisfied " A

X , .,. X 1(, ~ 1 v + v X17 ~ 1 -'2 A> v A f~ +- X,~. + X,g i. 1 v A~? +- X18 S 1

Xi. ~ [0,1] i ~ 1 , ? . . . , 18 - ,

~. 540

~ 380

(c)

(d)

(e)

Cf) (g)

(h)

( i)

(j)

(k)

(1)

(m)

X 16 is a decision variable to denote the delay of project

for 1 year

34

X 11' is a decision variable to denote the acceptance of

the composite of projects 2 and 3

X 18 is a decision variable to denote the acceptance of

the composite of projects 10 and 13

3.6.Goal Programming applied

problem.

to the capital rationing

Under conditions of certainty and perfect capital

the selection of the set of capital projects that market.s,

maximize NPV will guarantee maximization of shareholder's

wealth or utility.

However, if capital market imperfections exist (such

as capital

rates, etc)

rationing, differences in lending

then the maximization of NPV may

and borrowing

very well not

lead to the maximization of shareholders' wealth.

addition,

motivated

investors and managers are interested in

by several objectives as follows

stability of earnings and dividend per share;

growth

growth

In

and

and

in

sales, market share and total assets; growth and stability

of reported earnings or accounting profit; favorable use of

financial leverage; and return on sale, equity and operating

assets.

Thus anI y a model that incorporates mul~iple

c.riteria as objective can be a robust, yet. operational,

representation of the pluralistic design environment found

in real-world capital budgeting problem setting.

Goal programming is such a multi criteria model. It

is capable of handling decision situations which invol ve a

Single. goal or mUltiple goals. Frequently the multiple goals

of a decision maker must be measured by different

standal"ds. Often one goal or set of goals can be achieved

only at the expense

progl"amming allows

of other goals or set of goals.

for an ordinal ranking of goals so

Goal

that

35

lo~ priority goals are considered only after higher priority

goals have been satisfied to the fullest extent possible.

The general Goal programming (GP) model.

The basic assumptions underlying the LP model are

also valid for the GP model. The significant difference in

structure is that the GP does not attempt to maximize or

minimize the objective criterion directly as does the LP

model. It rather,seeks to minimize the deviations bet· .. een

the desired goals and the actual results according to the

priorities aSSigned. The general GP model is expressed as

follows

It'

Min I (di+di)

s. t .. n

I J>1

~here

8ij x j

. b .

1.

xJ,di,di ~ 0

i==l, ..... ,n

d represents degree of over achievement of a goal.

d represents degree of under achievement of a goal.

i goals

bi~ target value.

GP will move the values of the deviational variables

as close to zero as possible within the environmental

constraints and the goal structure outlined in the model.

Example:

The

GP Formulation and Solution of the Lorie-Savage

Problem

same fir~ that ~as evaluating the nine projects

now feels that the NPV objective should be supplemented with

four other goals ~hich reflect the short-run attractiveness

of the projects. Specifically, the firm feels that stability

and growth in sales as well as net income are very important

vehicles to assist. the firm in maximizing shareholders'

wealch.

36

The following table shows the contribution that each

of the projects will make to net income and sales growth in

the next 2 years.

Net Income Sales Growth

Project Year 1 Year 2 Year 1 Year 2

------------------------------------------------------------1 2.0 4.0 0.02 0.03

2 2.0 4.2 0.01 0.03

3 1.6 2.5 0.02 0.02

4 1.2 2.8 0.01 0.02

5 3.0 5.0 0.03 0.04

6 1.1 1.4 0.01 0.01

7 1.5 3.0 0.01 0.02

8 1.2 1.8 0.01 0.015

9 1.3 2.4 0.01 0.018

The firm wants to achj.eve net income levels of 8 and 16,

respectively, lTI years 1 and 2, and sales growth of 0.08 in

each year, as well as to maximize NPV.

Two objectives are considered

1. Placing the net income goals on priority 1, the sales

2 •

g.oa13 on priority 2, and the ~PV goal on priority 3; on

the first two priority levels the year 1 goals should be

weighted twice as importantly as the year 2 goals.

All £ i ve goals placed on priority level 1 but wi ttl

relative weights of 10 for net income in year 1 , 2 for

net income in 2,5 for sales growth in year 1 , and 2 for

sales growth in year , " , and 1 for }iP'l.

37

Solution:

The GP formulation is a~ follows:

X 1

X ~

12X, + 54X~ + 6X 3 + 6X" + 30X~ -+- 6X b

+ 48X 7 + 36X6' + 18X 9 + S, = 50

Budget constraint year 1

3X 1 + 7X .. + 6X:I + 2X ... + 35X ... + 6X ..

+ 4X 7 + 3X B + 3X"l + S ~ = 20

Budget constraint year 2

+ S3 = 1 X" + S ~ = 1 XT + S 9 = I Upper limits

+ S" = 1 X S" + S 1 = 1 Xe + S 1O = 1 on project

X 3 + S ,- = 1 X 4 + S B = 1 X9 + S 11 = 1 acceptance

j = 1 , 2, ,9 Nonnegativity

X j , Si ~ 0 i = 1 • 2 , ,11 constraint

2X, + 2X,- + 1.6X 3 + 1.2X", + 3X, + 1.1X b Net income

+1.5X7 + 1.2X8 + 1.3X"j + d1 d1 = 8 year 1

4X + 4.2X + 2.5X + 2.8X + 5X + 1;4X Net income

+3X + 1.8X + 2.4X

0.02X, + 0.01X 2 + 0.02.'::; + O.OlX.,

+ 0.03 X' 10 + O. 01 X 6 + O. 01 X 7 + 0.01 x 8

+ O.OIX~ + d; - d; = 0.08

0.03X, + 0.03X2. + 0.02X J + 0.02X""

+ 0.04X, -;. O.OlXi, + 0.02X 7 + 0.015X8

+ 0.018X 9+ d~ - d; = 0.08

year 2

Sales growth

year 1

Sales growth

year 2

14X, + 17X,- + 17X} + 15X", + 40X, + 12X. + 14X 7

+ 10X8 .,. 12X'l + d~ - d~ = 40 NPI(

Notice again that the goal level for the NPV goal i,,<:J

arbitrary achievable value.

The two objective functions are as follows:

1. Minimize weighted deviations =

P 1 ( 2d;- + d'; ) + P,.( 2 d; + d':;; ) + P;; ( d ~ + d; )

2. Minimize weighted deviations =

P,(10d; + 2d; + Sd; + 2d~ + d~ - d~)

The optimal solution for the two objestive functions are:

Objective function 1

Project

acceptance

Goal levels

achieved

---------------------------------------------------~--------

x, = 1.0000 7.231 Net income year 1

,X t 0.0426

X3 = 1.0000 13.209 Net income year 2

X.., = 1.0000

X, = 0 0.0699 Sa'les growth year I

X" = 0.9504 -

X7 = 0 0.0988 Sales growth year

XI? = O.

X" = 1.0600 70.129 NPV

Objective function 2

Project

acceptance

x, = 1 . 0000

Xt. = a X3 = 1.0000

X-'1 = 1 .0000

X, = 0

Xi, = 0.9697

X7 = 0.0455

Xa = O.

X", = 1.0000

Goal levels

achieved

7.235

13.194

0.0702

0.0986

70.273

3S

Net income year 1

Net income year 2

Sales growth year 1

Sales growth year 2

NPV

The optimal LP solution showed 100% acceptance of

projects 1.3.4 and 9, as well as 97% acceptance of project 6

and 4.5% acceptance of project 7,which generated an NPV

level of 70.273. All the GP solution above also accept 100%

of projects 2,3,4 and 9. The only difference among the

solutions is in the area of the partially accepted projects.

In the first G? solution (objective function 1) project 2

enters into the solution because of its contribution to- tile

achievement of the new goals in the GP formulation.

The other GP solution is virtually the same as the LP

solution. 'Greater variation in the optimal solution would

probably have been found if more projects were under

evaluation and/or greater diversity of goals were included

in the formulation.

Chapter 4

CAPITAL BUDGETING UNDER UNCERTAINTY.

4.l.Sensitivit7 analysis/break even analysis.

will

Uncertainty means

happen. Therefore,

that more things can happen tha:

whenever we are confronted with

cash-flow

happen. If

find that

forecast, we should try to discover what else caj

we can identify the major uncertainties, ve rna;

it is worth undertaking some adtitiona,

preliminary research that will confirm whether the ?rojec:

is worthwhile. And even if we decided that we have done aI'

we can to resolve the uncertainties, we still want to be

aware of the ?otential problems. We do not want to be caugh'

by surprise if things go wrong~ we want to be ready to tak(

corrective action.

Companies try to identify the principal threacs to

project's suc~ess. The simplest way to do it is to undertakl

a sensitivity analysis. In this case the manager consider!

in tura each of the determinants of the project's succes!

and estimates how far the present value of the project WQul(

be altered by taking a very optimistic view of tha t.

variable.

Sensitivity analysis or this kind is easy, but it i~

not always helpful. Variables do not usually change onp. at <

time4 If costS are higher than we expec~, it is a good be~

that sales volumes will be lower.

Many companies try to cope with this problem

examining the effect on the project of alternative plausiblt

combinations of variables. In other 'Words, they wiI:

estimate

different

case.

the net present value of the project

scenarios and compare this estimate with the

und e:r

bas ~

In a sensitivity analysis we change variables one a:

a time: when we analyze scenarios, we look at a limite'

40

41

number ot alternat~ve co~binations of variables.

Sensitivity analysis Jails down to expressing cash

flows in terms of unknown var~ables and then calculating the

concequences of misestimating the variables. It forces the

manager to identify the underlying variables,indicates ~here

additional information would be most useful, and helps to

expose confused or inappropriate forecasts.

One drawback to sensitivity analysis is that it

always

exactly

gives

does

some~hat ambiguous results. For exam~le,"'hat

optimistic or pesimiscic mean? The market.ing

depar'tment :nay be .interpreting the cerro in a different

from the production devartment.

When we undertake a sensitivity analysis of a project

we are ask~ng. how serio~~-it ~ould be if sales on costs turn

out to lie worse than we forecasced. Managers sometimes

prefer to rephrase this question and ask how ~ad sales can

get. before the project begins to lose moneY4 This is kno',./n

as break even analysis.

The break-~ven point is locaced ~here t~e ~otal cost

curve i.!1t2rsects =he total revenue curVe, or equi.?alent.ly

·,.,.here t:ctal '""Tevenue ~e:-quals tOLal cost.. Convent.ional hreak-

even analysis 'represents t..oLal revenue and i::ot:al Cost

scraight li,nes. This assumes ~hat output and sales can be

iilcreased . without changing ?r~ca (at. least, ~he ~£f~c.t. of

price changes are ~ot shown) and t~ac t~e f~=~ operates al:

the same efficiency at all le'rels. T:1US, t:o inc:::'ease profit

it is rrecessary merely to inc=ease t~e number or units sold.

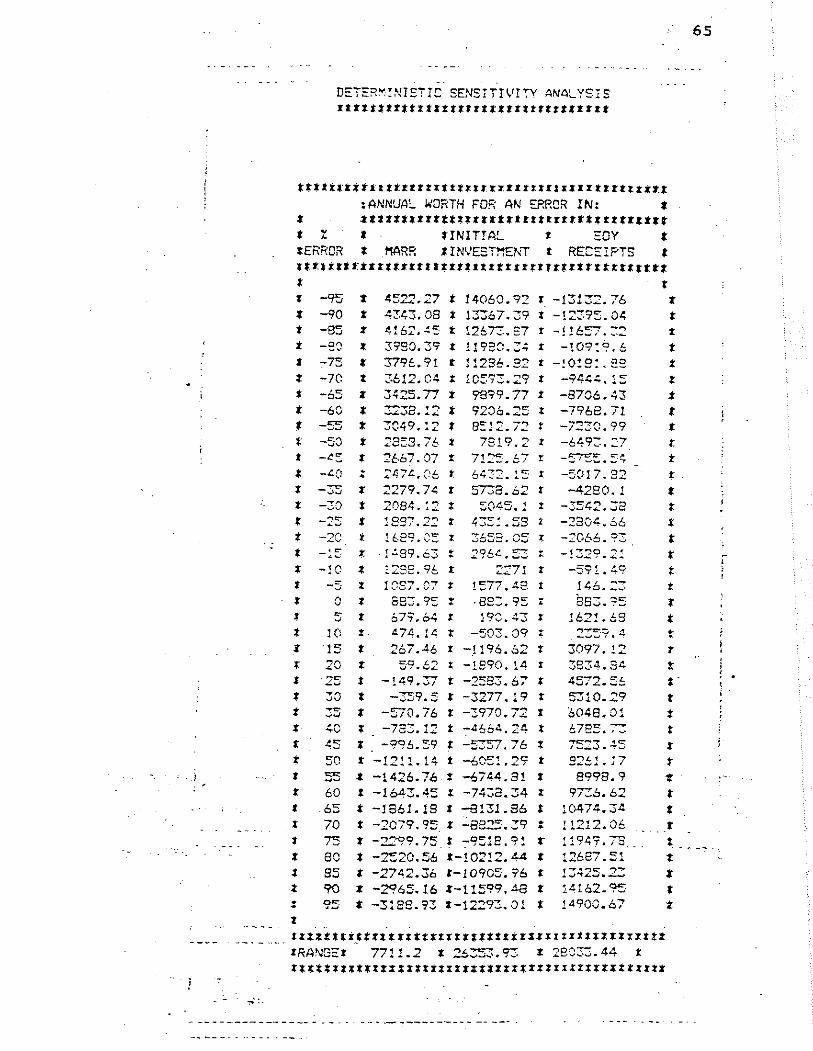

Exam'ple :"

Suppose a f~r~ Ls 91anning to buy a 3umer~cal control ,

for 50,000. It is ex?ec~ed' to be used for 5 years and have

receipt:s of 15,000; 15,000; L:;,OOO; ~4,500 and l"-OOO ac t!1e

end of eac~ year.

It is t-ne, company' s policy to use a 11: :ni.r1i.:num att.::act:::'ve

Management. wants e:O conduce: a sensi:ivi~1 analysis

42

respect to error in the forecast of initial investment,1if~

time, end or year receipt and minimum rate of return.

Solution:

The solution to this problem was solved by a program

developed for this purpose. The dicussion of this program

and the solution to this problem can be seen in chapter 6

4.2.Decision trees.

A that has been recommended to handle

complex,

technique

sequential decisions over time is the use of

d ecislon trees.

A decision tree is a formal representation of

available decision alternatives at various points through

time which Bre followed by c~ance events that may occur with

some probability. A ranking of the available decision

alternatives is usually ac~ieved by finding the expected

returns of the alternatives, which merely requires

multiplying the returns earned by ea~h alternative for

various chance events by the probability that the event will

occur and·summi~g over all possible events.

Managers may be tempted to think only about the ~irst

accept-rejec: decisions and La ignore the subsequent

investment decisions that ~ay be tied to it. Bu c if

subsequent investment decisions depend on those made toda.y,

then today's decision may depend on what we plan to do

tomorrow.

Of course, it would be imprudent for the fir:;, to

immediate~y impleme~t the project with the higest expected

return. This optimal ac:::'on with ·the unidimensional

cr:':'erion c::-ies out for £ur~jer analySis. Namely we should

investigate the following

1. The degree to which the estimated probabilities of the

various states of the economy would have to change for

43

the optimal solutio~ to no longer be optimal.

2. The

the

extent to which the estimated returns associated with

alternatives and states of the economy would have to

change in order to shift the optimal decision.

3. The

4. The

degree of risk associated with lack of alternatives.

utility that the firm attaches to each Of the returns

for each of the states of the economy based on the firm's

goals, risk, posture, risk-return preferences and so on.

Thus decision tree analysis is advocated as an

initial step which requires further analysis rather than the

final word in the firm's effort to maximize shareholder's

expected _utility

Example:

A firm is considering three alternative single-period

investments, A, B, and C, whose returns are dependent upon

the state of the economy in the coming period. The state of

the economy is known only by a probability distribution:

State of the economy Probability

.l:'a1r 0.25

Good 0.40

Very good 0.30

Super 0.05

1.00

The returns for each alternative under each possible state'

of the economy are as follows:

44

State of the economy

Alternative

A

B

C

Fair

10

-20

-75

Good

40

50

60

very

good

70

100

120

The decision tree for this problem is shown below.

super

90

140

200

Square nodes represent decision alternatives and round nodes

show chance events.

Decision State of probability of return weighted

alternative the economy state of the earned return

economy

-----------------------------------------------------------

.;::- ~ i r .25 10 2.50

ooad 0.4Q 40 16.00 , pr~:! 0" " 0":3.0- --- 70 21. 00

~" or 0.05 90 4.50

------E(R ) = 44.00

:::: 0.25 -20 - 5.00

* 0.40 SO 20.00

'1A;~ <;QQQ 0.30 100 30.00

'\ "''!In.o.l'''' 0.05 140 7.00

------E(R ) = 52.00

.;~..;..,.. 0.25 -75 -18.75

0 0.40 60 24.00

ve~7 0 d 0.30 120 36.00

- , or .D.05 200 10.00

------

E(R ) = 51.25

Decision alternative

A B

C

Expected return

44.00

52.00

51.25

Thus, the best alternative is B.

4.3. Simulation.

45

'Simulation is the imitation of a real~world system by

using a mathematical model which captures the critical

operating characteristics of the system as it moves through

time er.countering random events.

Major uses of simulation models

1. To determine improved operating conditions (i.e. system

design).

2. To demonstrate how a proposed change i~ policy will work

and or how the new policy compares with t~e existing

policies(i.e.,~ystem analysis or sensitivity analysis).

3. To train operating personnel to make better ciecisions,to

react to emergencies in a more efficient and effective

manner, and to utilize different kinds or information

(i.e. simulation games and heuristic programmi~g).

Simulation in capital budgeting can be done

following steps:

step l:Modeling the project.

The 'first step in any simulation is to give the

~omputer a precise model of the project.

step 2:Specifying probabilities.

stap 3:Simulate the cash flows.

by

A simulation model is composed of the following

the

four

46

major elements

1. Parameters, which are input variables specified by the

all decision maker which will be held constant over

simulation runs.

2. Exogenous variables, which are input variables outside

the control of the decision maker and are subject to

random variation - hence, the decision maker must specify

a probability distribution which d esc ri bes possible

events that may occur and their associated likelihood of

occurrence.

3. Endogenous variables, which are output or performance

variables describing the operations of the system and how

effectively the system achieved various goals as it

encountered the random events mentioned above.

4. Identities and operating equations which are mathematical

expressions making up the heart of the simulation model

by showing how the endogenous variables are functionally

related to the parameters and exogenous variables.

General flowchart of a simulation:

r I

·1 read in:

I.parameters

2.probability distributions

of exo enous variables

DO

to max

generate values for all

endogenous variables by

using the identities and

operating equations

T 47

compute values for all

endogenous variables by

using the identities and

operating equations

1. ___ _ gather statistics J

perform statistical analysis

print output,and plot

empirical distributions

- -,. '

( stop

The focus of the simulation is to develop empirical

distributions for each endogenous vaFiables in order to

describe how efficiently and system

operates.

Simulation can be a very useful tool. The discipline

of builddng a model of the project can in itself lead us to

a deeper understanding of the project. And once we

C onstr'lC t ed our

outcomes would

project or the

marine engineer

model,it is a simple matter to see how the

be affected by altering the scope of the

distribution or any of the variables. A

uses.a tank to simulate the performance OI

alternative hull designs but knows that it is impossible to

fully replicate the conditions that th~ ship will encounter.

In ~he same way,the finanCial manager can learn a lot from

laboratory

accurately

tests but cannot hope to build a model that

captures all the uncertainties and

interdependencies that really surround a project.

48

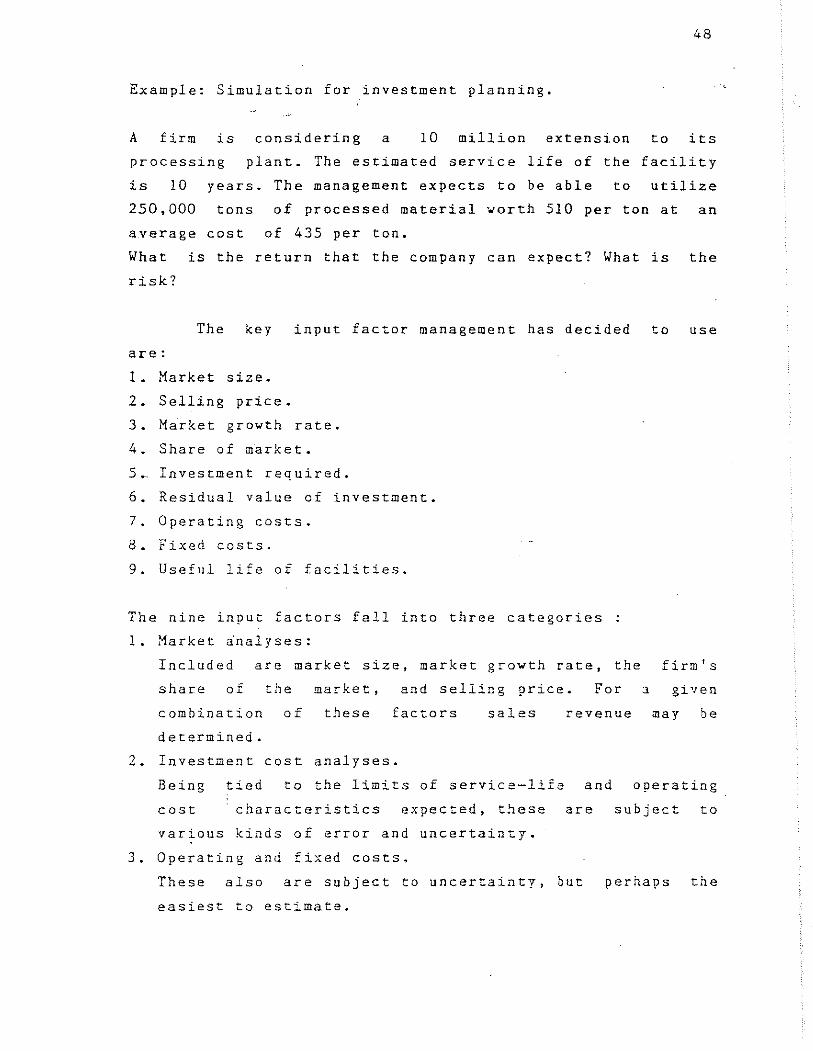

Example: Simulation for investment planning.

A firm is considering a 10 million extension to its

processing plant. The estimated service life of the facility

is 10 years. The management expects to be able to utilize

250,000 tons of processed material ~orth 510 per ton at an

average cost of 435 per ton.

What is the return that the company can expect? What is the

risk?

The key input factor management has decided to use

are:

1. Market size.

2. Selling price.

3. Market growth rate.

4. Share of market.

5_ Investment required.

6. Residual value of investment.

7. Operating costs.

8. Fixed costs.

9. Useful life of facilities.

The nine input factors fall into three categories

1. Market ~nalyses:

2.

Included are market size, market growth rate, the

share of the market, and selling price. For

combination of

determined.

these factors

Investment cost analyses.

sales revenue

firm's

given

may be

Being tied to the limits of service-life

cost characteristics expected, t~ese

and

are

operating

subject to

various kinds of error and uncertainty~

3. Operating and fixed costs.

These also are subject to uncertainty, but

easiest to estimate.

perhaps the

49

Result or the market research:

Key factor Expected value Range

------------------------------------------------------------A.Market analyses:

l. Market size

(in tons)

2. Selling price

(in $/ton)

3. Market growth

rate

4. Eventual share

of market

250,000

510

3%

12%

B.lnvestment cost analyses: ~-

1. Total investment

required

(in millions)

2. Useful life of

facilities

(in years)

3. Residual value

at 10 years

(in mil'lions)

C.Other costs:

1. Operating cost

(in $/ton)

2. Fixed costs

(in thousands)

$9.5

10

4.5

435

300

100,000 - 340,000

385 - 575

o - 6%

3% - 7%

$7.0 - $10.5

5 - 15

3.5 - 5.0

370 - 545

250 - 375

Range figures represent apprOXimately 1% to 99%

probabilities. That is, There is only a 1 in a 100 chance

that the value actually achieved will be respectively

greater or less than the range.

50

The next step is to determine the returns thet ¥ill

result from random combinations of the factors invol".ed.

This

the

requires realistic restrictions, such as not alloving

total market to vary more than some reasonable amount

from year to year. Of course, any method of rating the

return which is suitable to the company may be used at this

point, in the actual case management preferred discounted

cash flow.

For one trial actually made in this case, 3,500

discounted cash flow calculations, each based on a selection

of the nine input factors, were run in two minutes. The

resulting rate-of-return probabilities were

immediately and graphed in the following table:

Uncertainty portrayal:

Percent returns

0%

5%

10%

15%

20%

25%

30%

Risk profile:

Chances that

ROR . will be

Probability of achieving

at least the return shown

100%

75%

96.5%

80.6%

75.2%

53.8%

43.0%

12.6%

o %

I~I I ,

I

,

~ i I I I !

! " I :

I i I

I I

i

I I i 11 I I !

I I i , I

achived 50%

25%

0% -10%

,

0% 10% 20%

Anticipated ROR

~

read out

I !

I I , I

30%

51

Under the method using single expected values,

management arrives

after taxes (which

no variability in

unlikely event).

only at hoped for expectation of 25.2%

as we have seen, is wrong unless there is

the various input'factors a highly

Chapter S.

CAPITAL RATIONING UNDER UNCERTAINTY.

In this case mainly mathematical

simulation are used.

programming and

The major applications of mathematical programming

models under condition of risk in the capital budgeting area

have been in stochastic LP, chance contrained programming

and quadratic programming under uncertainty.

5.1. Stochastic Linear Programming.

In stochastic linear programming (SLP) a LP model

replaces the identities and operating equations of the

simulation model and the two-stage process proceeds as

follo ... s. In stage l,we first set a number of decision

variables and consider that they w~ll be fixed (just like

f'parameters,t in a simulation model) for all subsequent

observations of random events. In stage 2,random events are

generated and these values plus the parameters from stage i

are substituted into the LP model. The LP is solved ... hich

provides one empirical observation of the optimal value of

the LP objective function and the optimal values of the

decision variables. Next,we go back and repeat the process

of generating random events and solving LP problems some

desired numbers of times,thereby deriving a complete

empirical distribution for the LP objective function.

Finally,we compare this empirical distribution with other

empirical distribution arrived at using different stage 1

decisions in order tn ascertain tha t set of stage 1

decisions which optimizes the decision maker's utility

function.

52

53

5.2. Chance-constrain~d programming.

The

budgeting

programming

nex~ majo~

application

category

is that

which has seen capital

of chance-constrained

(CCP). The approach of CCP is to maximize the

expected value of the objective

allowed to be

function

violated

subject to

constraints that are some given

percentage of the time due to random variation in the

system. Chance constraints are arrived at as follows.

Consider the usual constraints of LP:

~

1 aij Xj ~ b i. J"

Owing to randomness in either the a coefficients or

the b right hand side values,we show that the constraints

do not have to be satisfied all the time by associating a

probability statement with the following constraint :

where:

p =

0;.; =

In would mean

probability

minimum probability that the decision maker is

willing to accept that a given constraint is

satisfied.

such constraints, if O\i = O .. 90,ior example,this

that the decision maker requires that tbe

constraint be satisfied at least 90% of the time and that he

is willing to allow l.. a\) x J to exceed hi up to 10% of the

time.

5.3.Quadratic programming.

Quadratic programming (QP) is the mathematical

programming model wherein a non linear objective function is

optimized subject to linear constraints. This model is

54

far easier

model,because

convexcivity

the global

to solve than the non linear programming

the feasible region is convex. The

assures that a local optimal solution is also

optimal solution. This greatly facilitates the

optimization process since the feasible region for

linear model is not necessary convex.

a non

5.4. An example by Salazar and Sen.

An interesting example that shows how capital

rationing under uncertainty can be solved by a combination

of mathematical programming techniques and simulation is the

article written by Salazar and Sen.

Techniques of simulation and stochastic LP (using

Weingartner's Basic Horizon model of capital budgeting) are

employed to compute the expected return (with an associated

measure of the risk involved) of different portfolios of

projects. The manager can then select the portfolio which is

closest to his personal risk return preference. The model

provides a practical guide to management in the entire

process of proj~ct search,portfolio gener~tion,and portfoliO

evaluation which characterizes the capital budgeting

decision.

Salazar and Sen incorporate two kinds of uncertainty

into their model: uncertainty related to significant

economic and competitive variables which are likely to

affect project cash flows and uncertainty related to the

cash flows of the projects under consideration based OD

these variables.

Salazar and Sen handle the first type of uncertainty

by a ·tree diagram similar to those introduced in the

preeceding

branches

chapter, shown in figure 5.4. There

in the tree diagram ~ith their respec~ive

are 12

joint

probabilities of occurence shown on the far right of tie

tree, the derivation or those probabilities is based on the

table below the tree. In the stochastic LP framework, the

branches in this tree diagram will be considered as stage

decisions that will be fixed; for each branch in the tre,

cash flows for each project under consideration will

randomly generated and then plugged into the LP model.

To elaborate, consider tbe flowchart used by Salaz,

and