Embed Size (px)

Citation preview

A community outreach program of the

Get Smart About Credit

In 2015 American consumers owed $889 billion in credit card debt.

That’s…$889,000,000,000!

Why CARE?

Debit cards are different from credit cards

⦿A debit card works just like a check⦿The money for the purchase comes directly from your

bank account⦿You must have money in the bank account to use the card

•can’t spend what you don’t have⦿Many places prefer debit cards over checks or do not

accept checks at all

⦿Emergencies

⦿Large Purchases

⦿Internet Purchases

⦿Establish a Credit History

⦿Identification

⦿Safety

Some Good Reasons to have Credit Cards

⦿It is very easy to lose track of your purchases

•You end up spending more than you think

⦿The convenience of a credit card can be overpowering

•leads to unnecessary and even foolish purchases.

Some Downsides to Credit Cards

⦿As you enter adulthood, you will begin to receive credit card offers.

⦿Understanding how credit works and what kinds of things to avoid when using credit cards is essential before the damage is done.

There is a big problem in this country with credit card abuse

⦿And why should you care about the interest rate on a credit card? Or other fees?⦿Let’s find out in the next slides

So how does a credit card work?

⦿Credit is the ability to borrow money⦿Borrowing money creates debt

•Debt is what you owe⦿It costs to borrow money

What is credit?

⦿Interest is the amount that a lender charges to borrow money⦿The higher the interest rate, the more

money you pay⦿Interest rates vary from credit card

company to credit card company⦿ Card companies charge compound

interest—that’s interest on interest

What is Interest?

Here is an example that shows that compound interest piles up FAST:

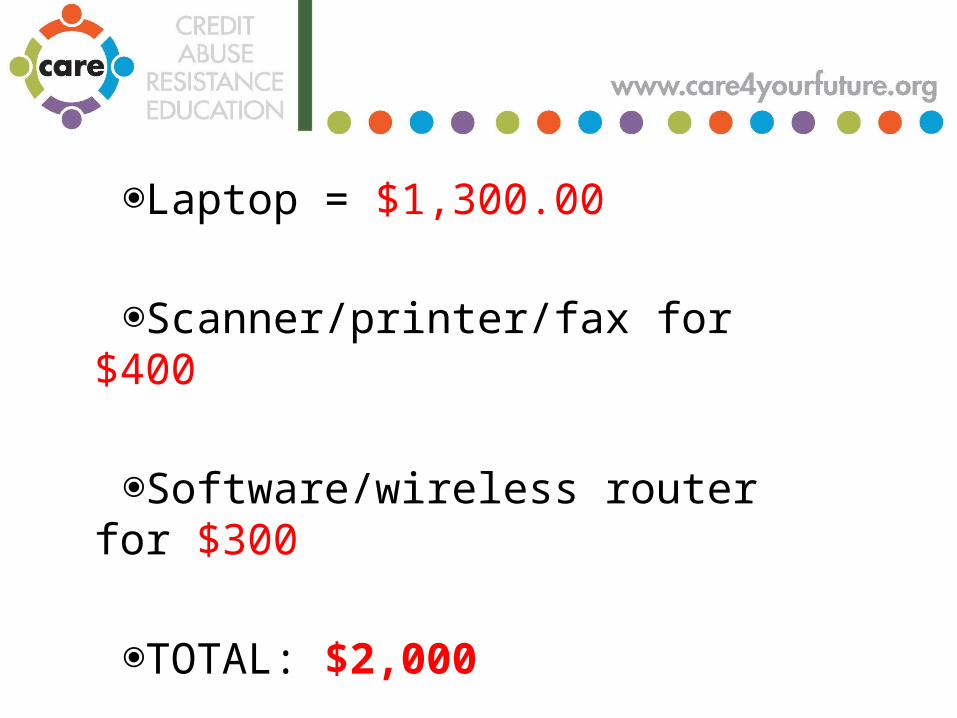

What if you bought…

⦿Laptop = $1,300.00

⦿Scanner/printer/fax for $400

⦿Software/wireless router for $300

⦿TOTAL: $2,000

⦿you used your credit card

⦿you make monthly payments of $300

⦿you never miss a payment

⦿annual percentage rate on your card is 8%

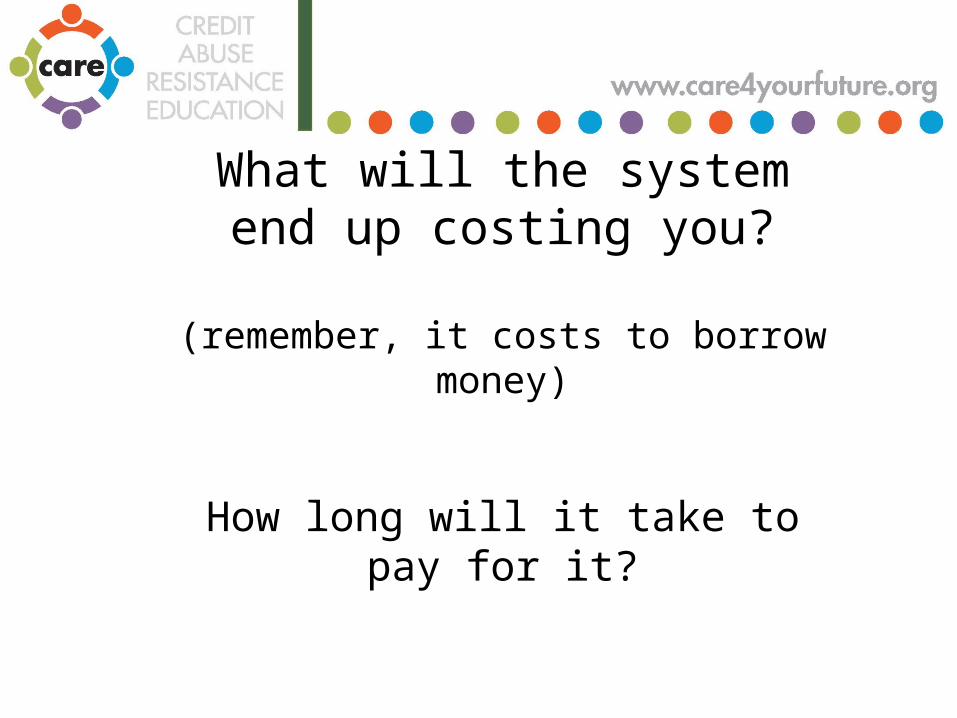

What will the system end up costing you?

(remember, it costs to borrow money)

How long will it take to pay for it?

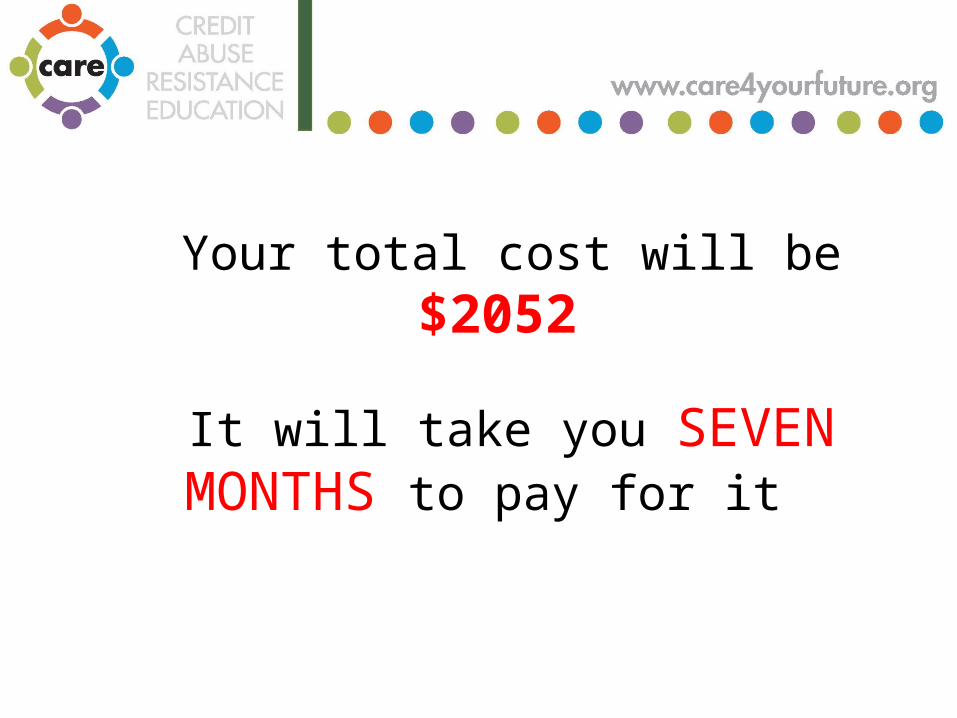

Your total cost will be $2052

It will take you SEVEN MONTHS to pay for it

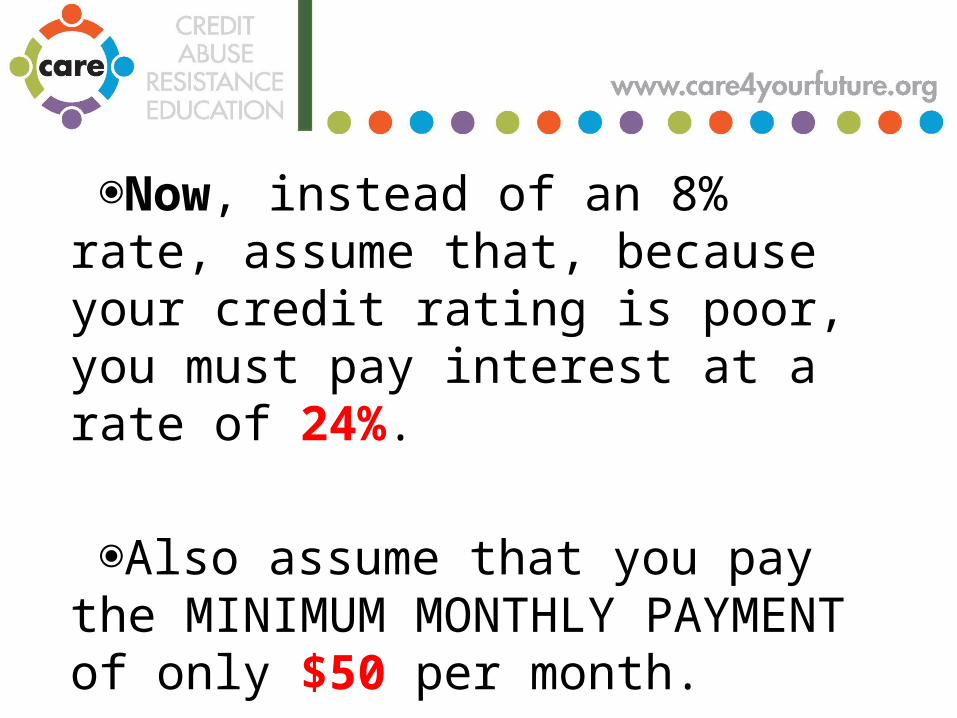

⦿Now, instead of an 8% rate, assume that, because your credit rating is poor, you must pay interest at a rate of 24%.

⦿Also assume that you pay the MINIMUM MONTHLY PAYMENT of only $50 per month.

⦿It will take you 82 MONTHS (almost SEVEN YEARS) to pay for it

⦿Total payment: $4,085!

How Minimum Payments Won’t Get You Out of Credit Card Debt

So what’s our point?

Pay your balance in full and on time every month – the single most important point of this presentation

Credit Card Costs and Fees If you are smart, you can avoid paying unnecessary credit card fees • E.g., avoid cards that charge an annual fee

Other fees you can avoid by paying in full and on time• Finance charges• Universal default rate

Fees you avoid when you don’t use your card for these unnecessary services

Balance Transfer Fees • Over-the-Limit Fees

•Cash Advance Fees •Document and Research Fees

Reissued Card Fees •Returned Check Fees

How do you find the best card?

Shop around at card comparison sites such as

creditkarma.comnerdwallet.comcreditcards.combankrate.comcardhub.com

Credit Card Control

Reasons to reduce or eliminate the credit card habit:

1.Improve your credit rating

2.Save more money and pay less interest

3.Regain control over your life when you control your spending

Credit Cards Are Only One of Many Forms of Credit

What are some others?

1. Long Term Credit - payments made over several months or years

⦿Mortgages ⦿Car Loans⦿Student Loans

2. Short Term Credit – single payments

⦿Charge cards⦿Utility Bills⦿Cable/Satellite⦿Cellular phone bills

Types of Credit

Credit Reports and Credit Scores are Key Instruments By Which You Are Measured in the Business World

⦿Summary of a consumer’s financial reliability

⦿Prepared by credit reporting companies for use by credit grantors and other parties with permissible purpose

What is a Credit Report?

⦿Four primary credit bureaus in the US: Equifax, Experian, Innovis, and TransUnion⦿Companies update and distribute

consumers’ information

Credit Reporting Companies

Check Your Credit

⦿ Ensure all credit reports are accurate: www.annualcreditreport.com

⦿ Avoid credit “repair” scams—these often participate in illegal activities to initiate fraudulent accounts and should not be trusted with your personal information

Want to learn more about credit reports? Continue advancing slides.

Otherwise, continue to a discussion of saving and budgeting by clicking here Skip Credit Report

Section

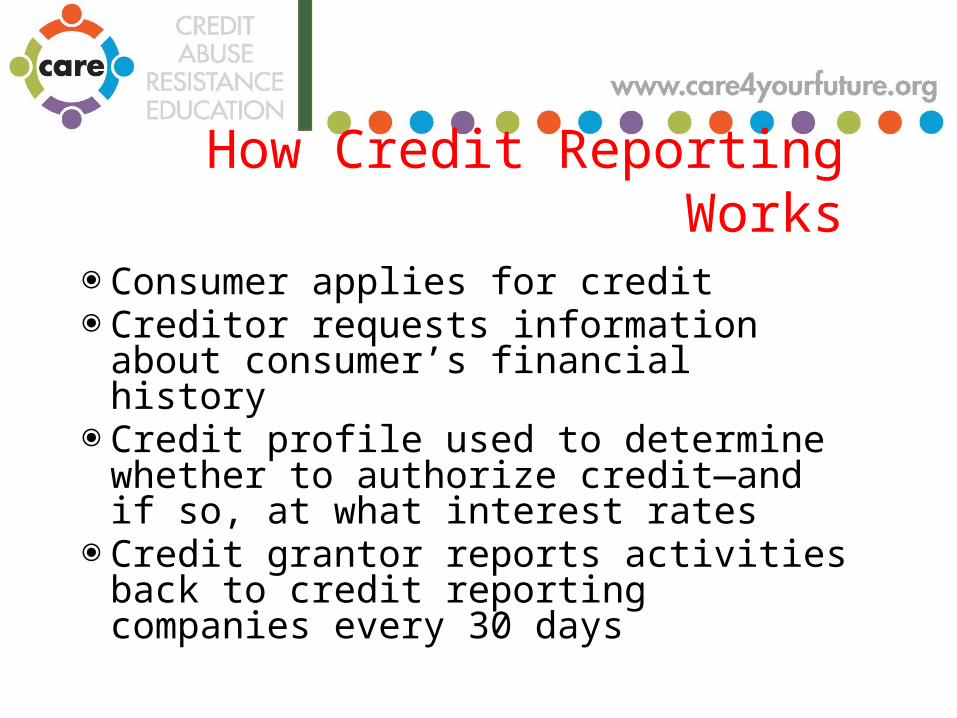

⦿Consumer applies for credit⦿Creditor requests information about consumer’s

financial history⦿Credit profile used to determine whether to

authorize credit—and if so, at what interest rates⦿Credit grantor reports activities back to credit

reporting companies every 30 days

How Credit Reporting Works

⦿ Sum calculated by credit scoring company and used by lenders as an indicator of how likely consumer is to repay loans

⦿ Generated by a mathematical formula – FICO is the most common credit score

⦿ Each credit grantor has its own strategy for interpreting the credit score

⦿ If credit is denied after reviewing the score, credit grantors must disclose the reasons for the decision

What is a Credit Score?

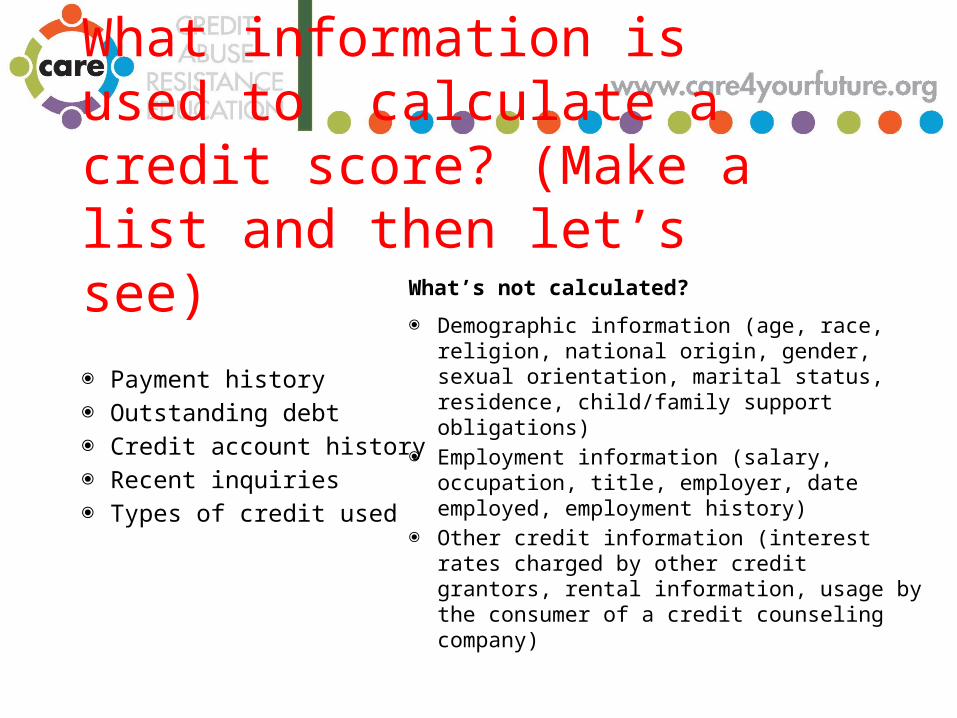

What information is used to calculate a credit score? (Make a list and then let’s see)

What’s not calculated?

⦿ Demographic information (age, race, religion, national origin, gender, sexual orientation, marital status, residence, child/family support obligations)

⦿ Employment information (salary, occupation, title, employer, date employed, employment history)

⦿ Other credit information (interest rates charged by other credit grantors, rental information, usage by the consumer of a credit counseling company)

⦿ Payment history⦿ Outstanding debt⦿ Credit account history⦿ Recent inquiries⦿ Types of credit used

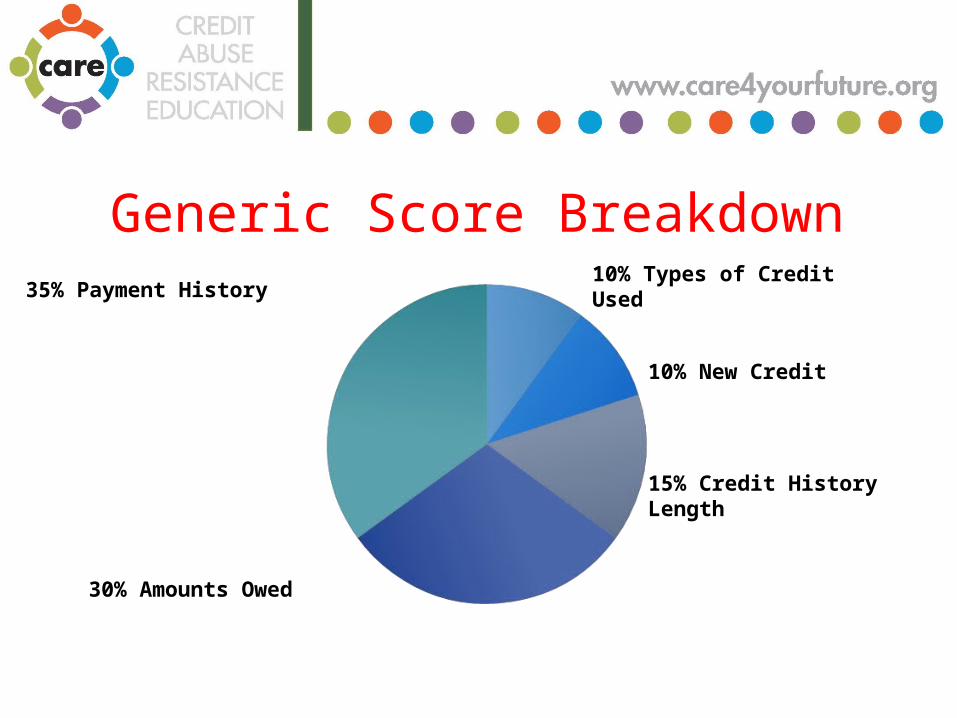

Generic Score Breakdown35% Payment History

30% Amounts Owed

15% Credit History Length

10% New Credit

10% Types of Credit Used

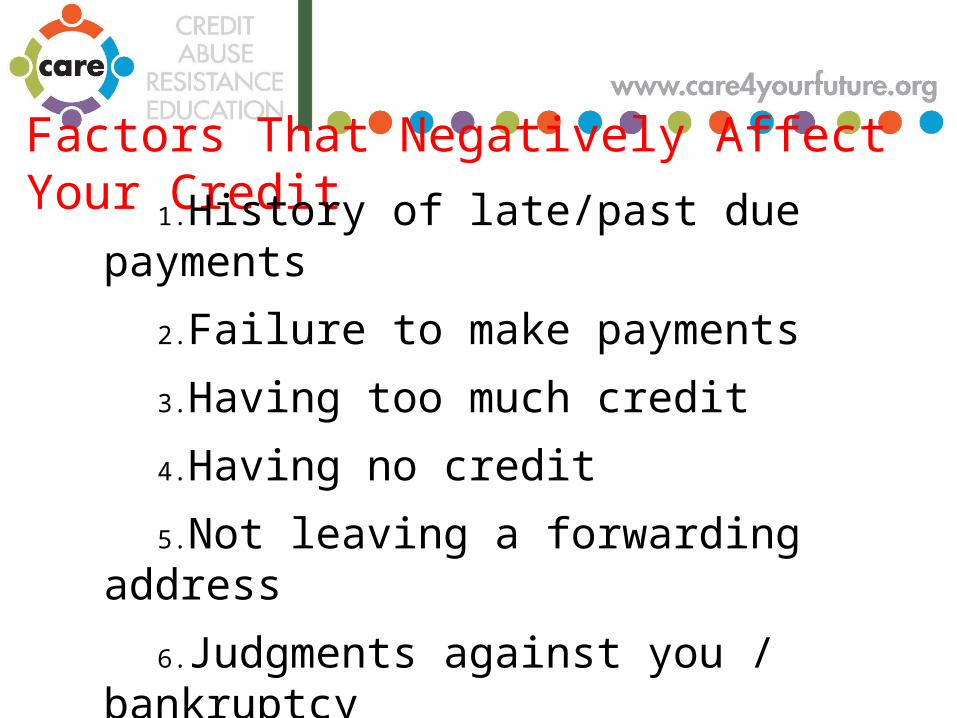

Factors That Negatively Affect Your Credit

1.History of late/past due payments

2.Failure to make payments

3.Having too much credit

4.Having no credit

5.Not leaving a forwarding address

6.Judgments against you / bankruptcy

Credit Dispute Resolution

⦿ Remember, you have the right to dispute inaccurate information on your credit report

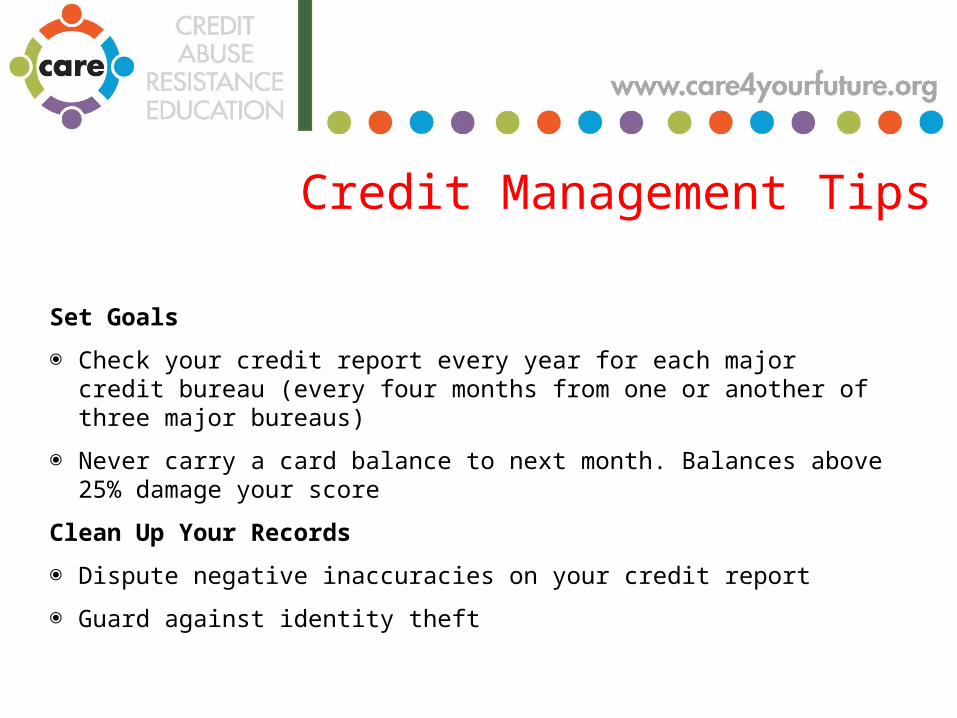

Credit Management Tips

Set Goals

⦿ Check your credit report every year for each major credit bureau (every four months from one or another of three major bureaus)

⦿ Never carry a card balance to next month. Balances above 25% damage your score

Clean Up Your Records

⦿ Dispute negative inaccuracies on your credit report

⦿ Guard against identity theft

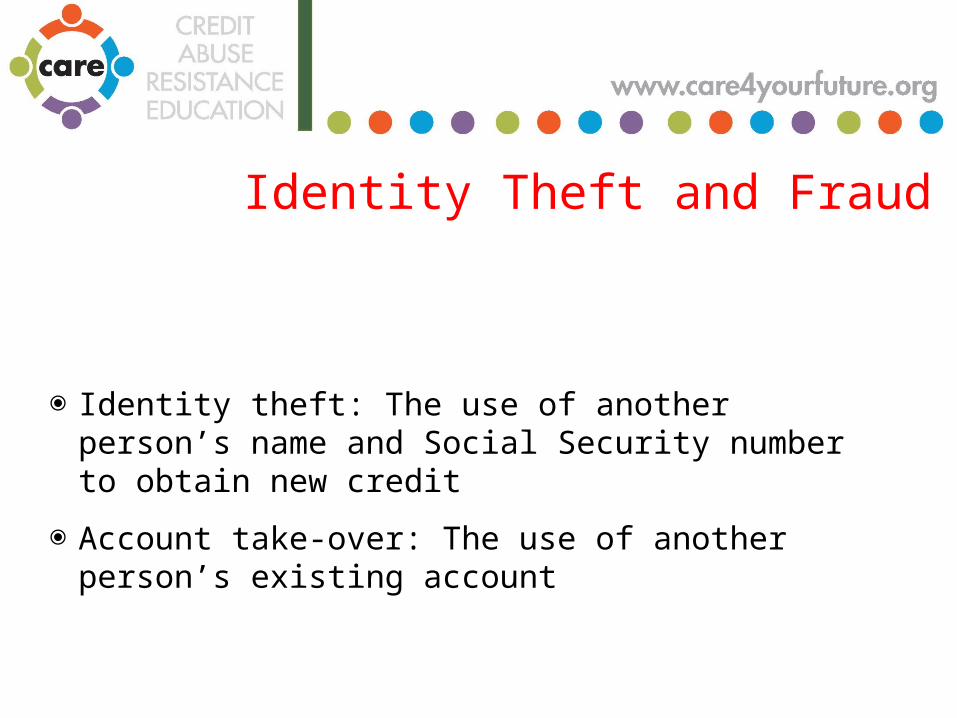

Identity Theft and Fraud

⦿ Identity theft: The use of another person’s name and Social Security number to obtain new credit

⦿ Account take-over: The use of another person’s existing account

Keep Accurate Records

⦿ Keep important records in a safe place—available when needed and not easily taken

⦿ Balance checkbook—watch for missed check numbers or mystery charges

Good records make it easier to identify and resolve fraud

Act Fast When Fraud is Suspected

Prevent further fraud damage

⦿ Acting quickly will ease the resolution greatly with creditors and the credit bureaus

⦿ It is much easier to prevent damage than remove it

⦿ Don’t wait until it costs you thousands on a loan

⦿Learning to live within your means will help you get ahead (wants vs. needs)

⦿Budgeting creates financial security

⦿Budgeting will keep you out of debt

Saving for the Future

⦿Keep track of what you make.⦿Keep track of what you spend.⦿Ask yourself, how close are they?

SO, how do you budget??

To make your budget work,

you must equalize what you spend with what you make by:

1)Making more2)Spending less

(Sounds easy, huh?)

Start making adjustments…

•Earn more by working more hours

•Reduce expenses by buying your coffee at 7/11 instead of Starbucks

•Be honest with yourself: Do I really need this or do I simply want this?

Then, stick to your budget!

•Sticking with a budget is a lifelong process• Be flexible

◉your budget will change as your life changes

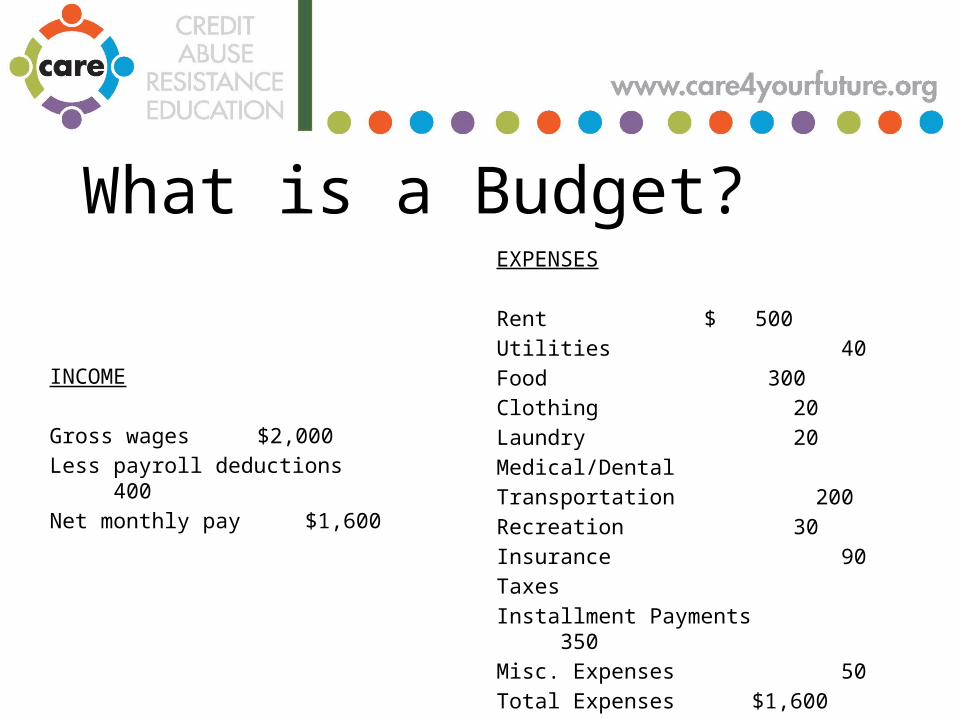

What is a Budget?

INCOME

Gross wages $2,000

Less payroll deductions 400

Net monthly pay $1,600

EXPENSES

Rent $ 500

Utilities 40

Food 300

Clothing 20

Laundry 20

Medical/Dental

Transportation 200

Recreation 30

Insurance 90

Taxes

Installment Payments 350

Misc. Expenses 50

Total Expenses $1,600

Many useful budgeting apps and web sites are available

Try mint.com – widely-used, user-friendly and free

Budgeting help is on the way

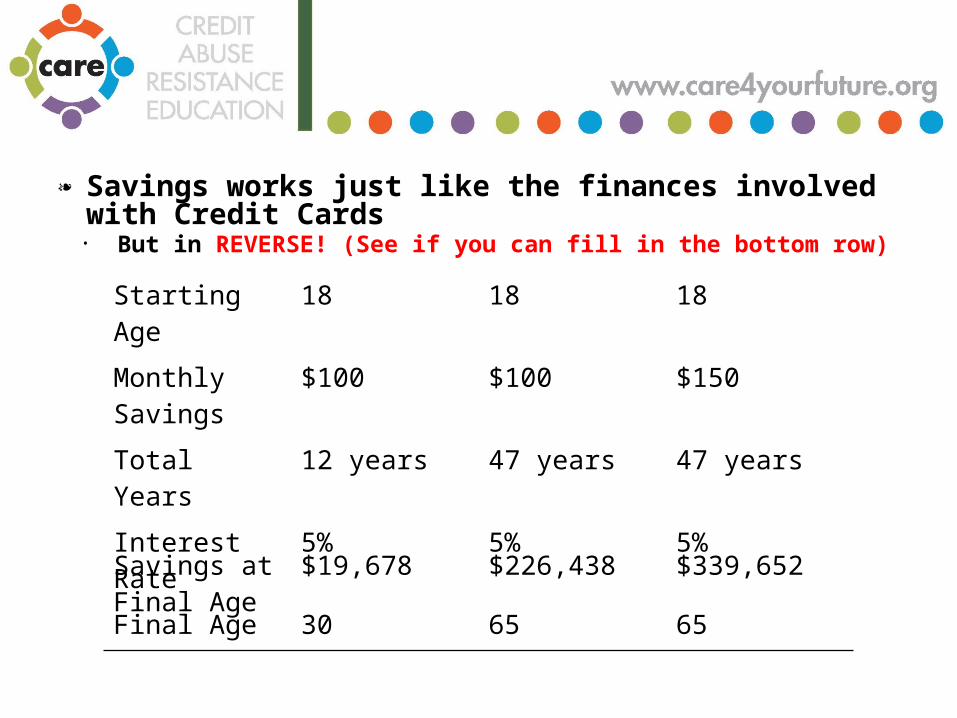

❧ Savings works just like the finances involved with Credit Cards• But in REVERSE! (See if you can fill in the bottom row)

Starting Age 18 18 18

Monthly Savings

$100 $100 $150

Total Years 12 years 47 years 47 years

Interest Rate 5% 5% 5%

Final Age 30 65 65

Savings at Final Age

$19,678 $226,438 $339,652

Just as time – and compound interest - can work against you when you borrow money (remember the $2000 laptop system that doubled in cost), it can be your best friend when it comes to saving.

A 22 year old who saves $20 a week could have as much as $1 MILLION by retirement age. A person who waits until the age of 45 to start saving, would have to save $245 a week to accumulate the same amount.

True or FalseYou pay no interest on a debit card

purchase.

TRUE!A debit card

works just like

a check.

True or False There is a credit report for everyone

over age 18.

FALSEThere is a credit report only for

people who have established a credit

history. Having no credit history can have

adverse consequences.

True or FalseIf you are late in making a

few payments on your credit card, the interest rate you pay

may increase sharply.

TRUEFor example, on one

Platinum VISA card, the interest rate jumps from 4.9% to 30% if you pay late or miss even one payment. Late charges also

accrue.

True or FalseIf you miss just one or two

payments on your credit card, it won’t hurt your credit rating.

FALSE

That negative information can legally remain on your report

for up to 7 years.

Last one…promise!

True or FalseNo one really looks at credit

reports.

FALSE People who lend you money will almost

always review your credit report. Car, home, credit cards.

More prospective employers also look at credit reports.

You can receive free copies of your credit report each year—worth reviewing!

●{

Stay Connected!

Like us! www.facebook.com/careforyourfuture

Follow us! @care4yourfuture

Connect to us on LinkedIn!

Visit! www.care4yourfuture.org

www.CAREChicago.org