Embed Size (px)

Citation preview

9M16 Results

The ugly duckling is growing up

2

Disclaimer and safe harbour statements

These slides have been prepared by Anima Holding S.p.A. (“Anima”, the “Company” and together with its subsidiaries the “Group”), solely for a presentationto investors. These slides are being shown for information purposes and neither this document nor any copy thereof may be reproduced, further distributed toany other person or published, in whole or in part, for any purpose. The information contained in this document (“Information”) has been provided by theCompany or obtained from publicly available sources and has not been independently verified.None of the Company or any of their respective affiliates, directors, officers, advisers, agents or employees, nor any other person make any representation orwarranty, express or implied, as to, and no reliance should be placed on, the fairness, accuracy, materiality, completeness or correctness of the Informationor any opinions contained herein. This presentation may contain financial information and/or operating data and/or market information regarding thebusiness, assets and liabilities of the Company and its consolidated subsidiaries and the results of operations and markets in which the Company and itsconsolidated subsidiaries are active. Such financial information may not have been audited, reviewed or verified by any independent accounting firm and/orsuch operating or market information may be based on management estimates or on reports prepared by third parties which neither the Company nor theBanks have independently verified. It is not the intention of the Company to provide, and you may not rely on these materials as providing, a complete orcomprehensive analysis of the Company’s financial or trading position or prospects. This presentation speaks as of its date and will not be updated. TheInformation included in this presentation may be subject to updating, completion, revision and amendment and such Information may change materiallywithout notice. No person is under any obligation to update or keep current the Information contained in this presentation and any estimates, opinions andprojections expressed relating thereto are subject to change without notice. Neither the Company nor any of their respective affiliates, directors, officers,advisers, agents or employees, nor any other person shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from anyuse of these materials or its contents or otherwise arising in connection with this presentation.

This document includes forward-looking statements which include statements regarding ANIMA’s business strategy, financial condition, results of operationsand market data, as well as other statements that are not historical facts. By their nature, forward-looking statements are subject to numerous factors, risksand uncertainties that could cause actual outcomes and results to be materially different from those projected. Readers are cautioned not to place unduereliance on these forward-looking statements. Except for any ongoing obligation to disclose material information as required by the relevant regulations,ANIMA does not have any intention or obligation to publicly update or revise any forward-looking statements after ANIMA distributes this document, whetherto reflect any future events or circumstances or otherwise.

Any projections, estimates, forecasts, targets, prospects, returns and/or opinions contained in this presentation involve elements of subjective judgment andanalysis and are based upon the best judgment of the Company as of the date of this presentation. No representation or warranty is given as to theachievement or reasonableness of, and no reliance should be placed on, any valuations, forecasts, estimates, opinions and projections contained in thispresentation. In all cases, recipients should conduct their own investigation and analysis on the Company and the Information contained in this presentation.Forward-looking statements concern future circumstances and results and other statements that are not historical facts, sometimes identified by the words“believes”, “expects”, “predicts”, “intends”, “projects”, “plans”, “estimates”, “aims”, “foresees”, “anticipates”, “targets”, and similar expressions.A multitude of factors can cause actual events to differ significantly from any anticipated development. Forward-looking statements contained in thispresentation regarding past trends or activities should not be taken as a representation that such trends or activities will continue in the future. No oneundertakes any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You shouldnot place undue reliance on forward-looking statements, which speak only as of the date of this presentation and are subject to change without notice.

3

9M16 - Table of contents

1

2

Anima…who

Anima…what

Anima…why

Anima…how much3

4

4

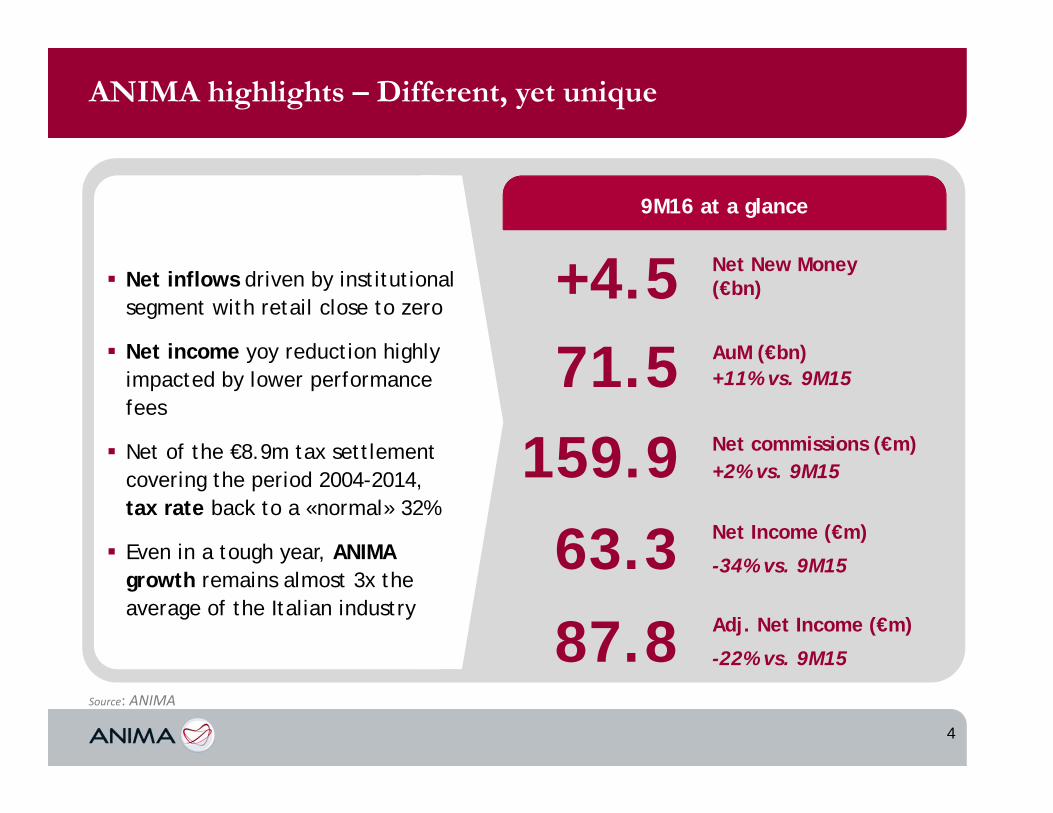

ANIMA highlights – Different, yet unique

Source: ANIMA

Net inflows driven by institutional segment with retail close to zero

Net income yoy reduction highlyimpacted by lower performance fees

Net of the €8.9m tax settlementcovering the period 2004-2014, tax rate back to a «normal» 32%

Even in a tough year, ANIMA growth remains almost 3x the average of the Italian industry

71.5 AuM (€bn)

159.9 Net commissions (€m)+2% vs. 9M15

63.3 Net Income (€m)

-34% vs. 9M15

+4.5 Net New Money (€bn)

+11% vs. 9M15

9M16 at a glance

87.8 Adj. Net Income (€m)

-22% vs. 9M15

5

9M16 - Table of contents

Anima…who

Anima…what

Anima…why

Anima…how much

1

2

3

4

6

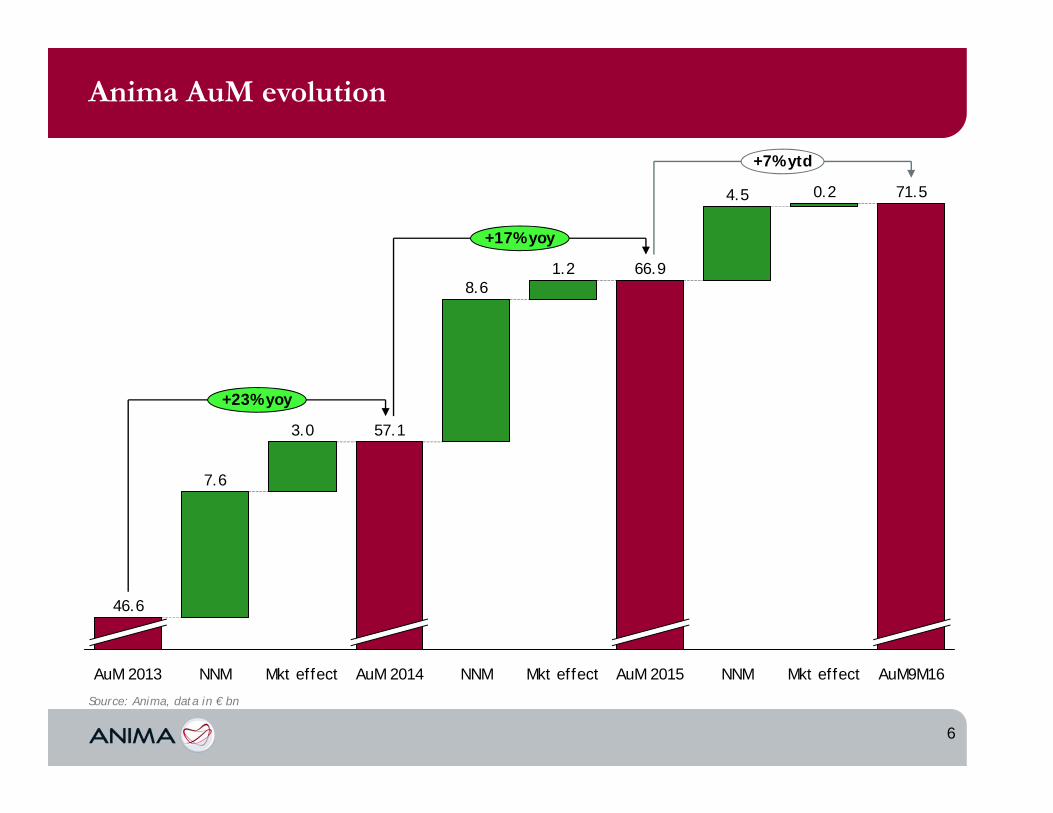

Anima AuM evolution

Source: Anima, data in € bn

7.6

AuM 2013

46.6

AuM9M16

+7% ytd

+17% yoy

71.5

+23% yoy

NNM Mkt effect

0.2

1.2

4.5

AuM 2015

66.9

Mkt effectNNM

57.1

Mkt effect

3.0

NNM

8.6

AuM 2014

7

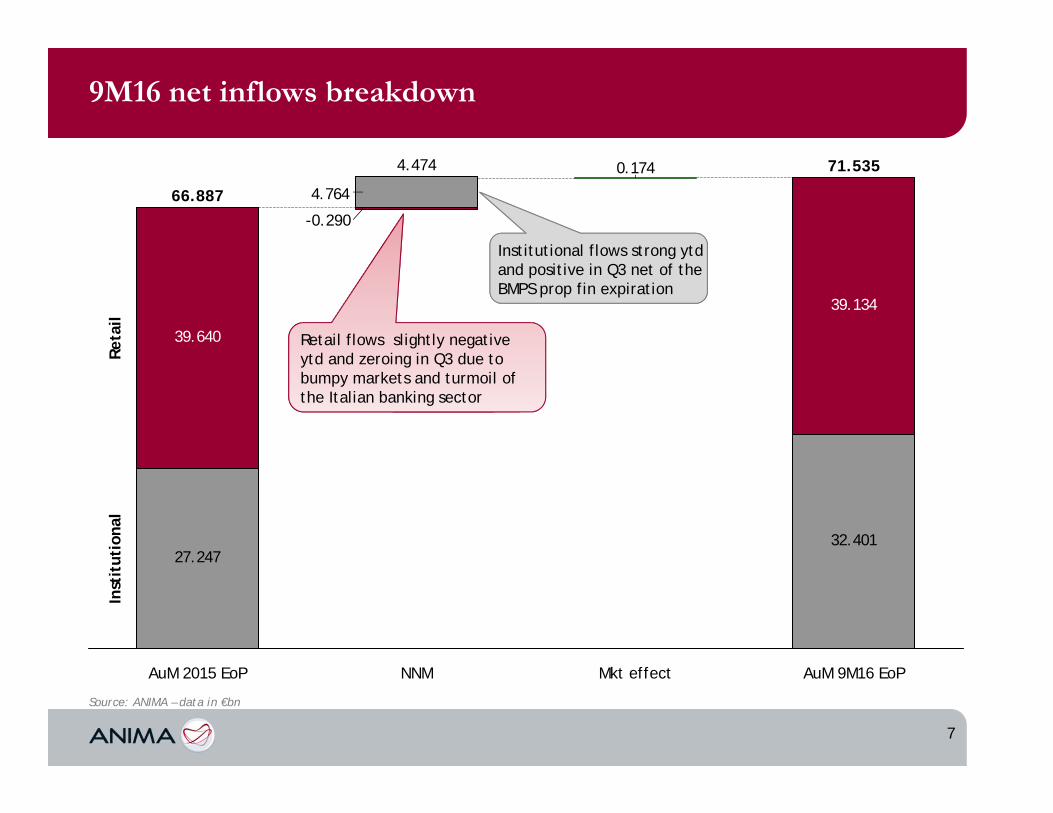

9M16 net inflows breakdown

Source: ANIMA – data in €bn

27.24732.401

39.640

39.134

0.174

4.764

Inst

itut

iona

lRe

tail

71.535

AuM 9M16 EoPMkt effectNNM

4.474

-0.290

AuM 2015 EoP

66.887

xxxx

Retail flows slightly negative ytd and zeroing in Q3 due to bumpy markets and turmoil of the Italian banking sector

Institutional flows strong ytdand positive in Q3 net of the BMPS prop fin expiration

8

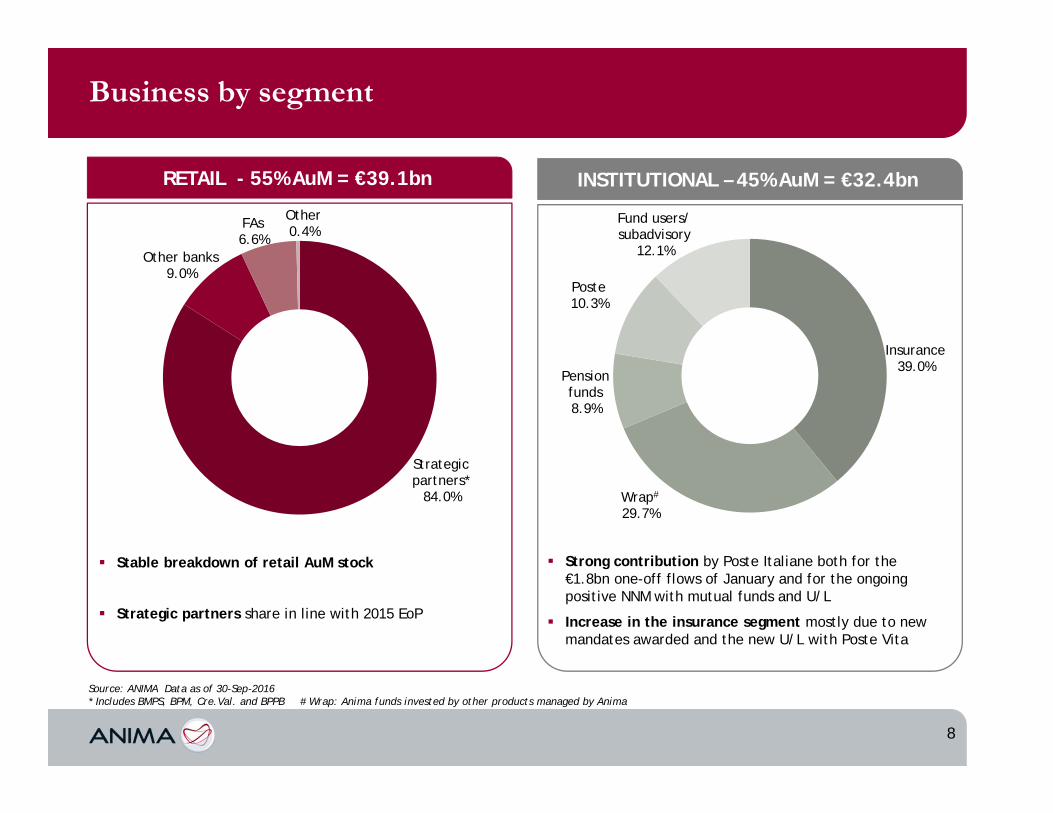

INSTITUTIONAL – 45% AuM = €32.4bnRETAIL - 55% AuM = €39.1bn

Strategic partners*

84.0%

Other banks9.0%

FAs6.6%

Other0.4%

Insurance39.0%

Wrap#

29.7%

Pension funds 8.9%

Poste10.3%

Fund users/subadvisory

12.1%

Source: ANIMA Data as of 30-Sep-2016* Includes BMPS, BPM, Cre.Val. and BPPB # Wrap: Anima funds invested by other products managed by Anima

Strong contribution by Poste Italiane both for the €1.8bn one-off flows of January and for the ongoingpositive NNM with mutual funds and U/L

Increase in the insurance segment mostly due to new mandates awarded and the new U/L with Poste Vita

Stable breakdown of retail AuM stock

Strategic partners share in line with 2015 EoP

Business by segment

9

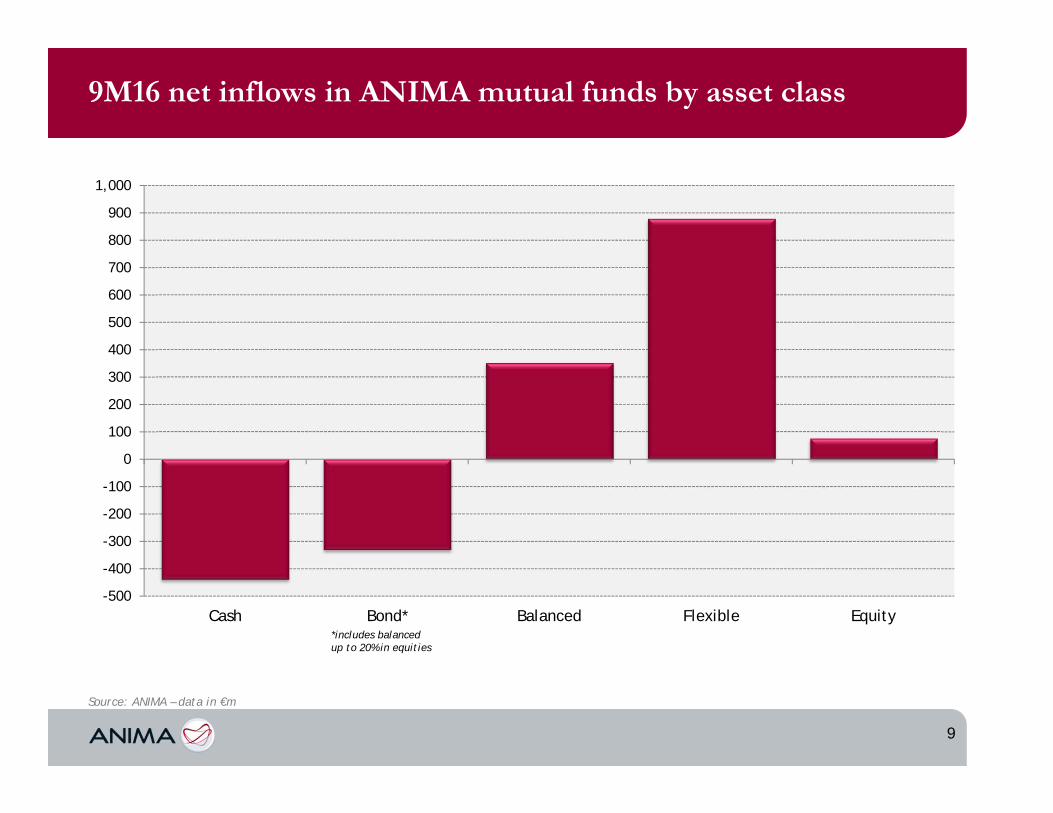

9M16 net inflows in ANIMA mutual funds by asset class

Source: ANIMA – data in €m

*includes balanced up to 20% in equities

-500

-400

-300

-200

-100

0

100

200

300

400

500

600

700

800

900

1,000

Cash Bond* Balanced Flexible Equity

10

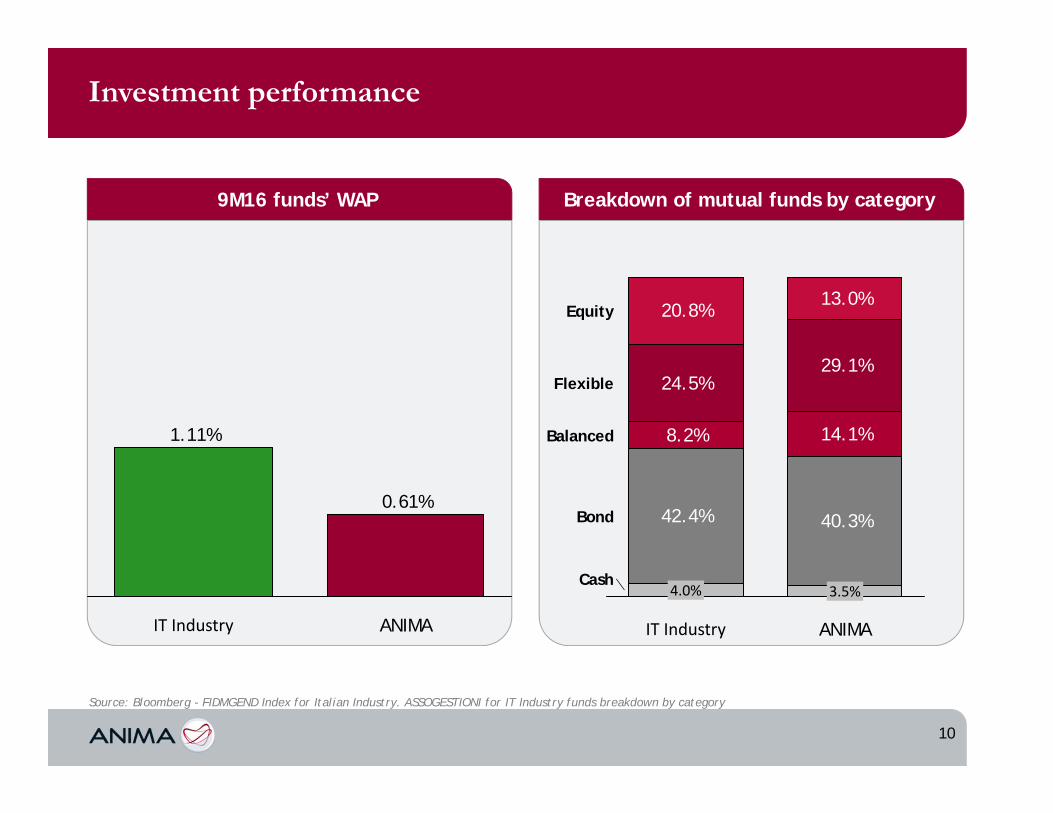

9M16 funds’ WAP Breakdown of mutual funds by category

Investment performance

Source: Bloomberg - FIDMGEND Index for Italian Industry. ASSOGESTIONI for IT Industry funds breakdown by category

ANIMA

0.61%

IT Industry

1.11%

42.4% 40.3%

8.2% 14.1%

24.5%29.1%

20.8%13.0%

Balanced

Bond

Cash

Equity

Flexible

ANIMA

3.5%

IT Industry

4.0%

11

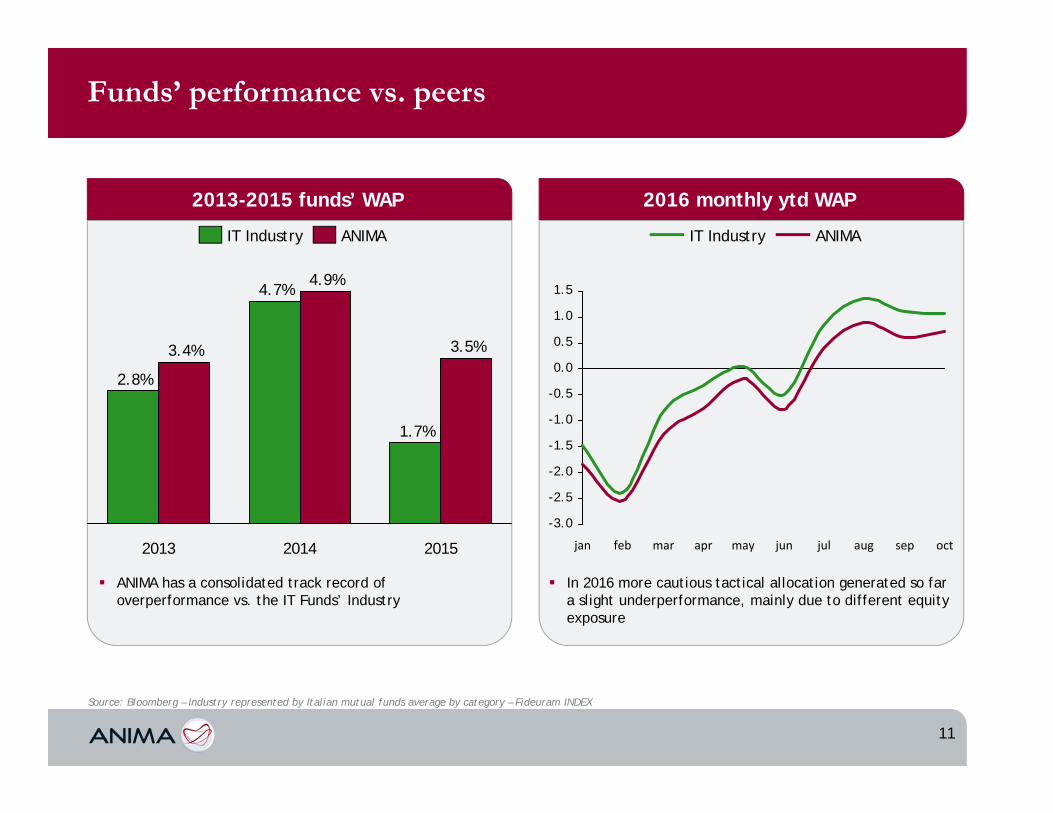

Funds’ performance vs. peers

Source: Bloomberg – Industry represented by Italian mutual funds average by category – Fideuram INDEX

2013-2015 funds’ WAP 2016 monthly ytd WAP

2015

3.5%

1.7%

2014

4.9%4.7%

2013

3.4%

2.8%

ANIMAIT Industry

ANIMA has a consolidated track record of overperformance vs. the IT Funds’ Industry

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

octsepaugjulfebjan junapr maymar

IT Industry ANIMA

In 2016 more cautious tactical allocation generated so far a slight underperformance, mainly due to different equityexposure

12

9M16 - Table of contents

Anima…who

Anima…what

Anima…why

Anima…how much

1

2

3

4

13

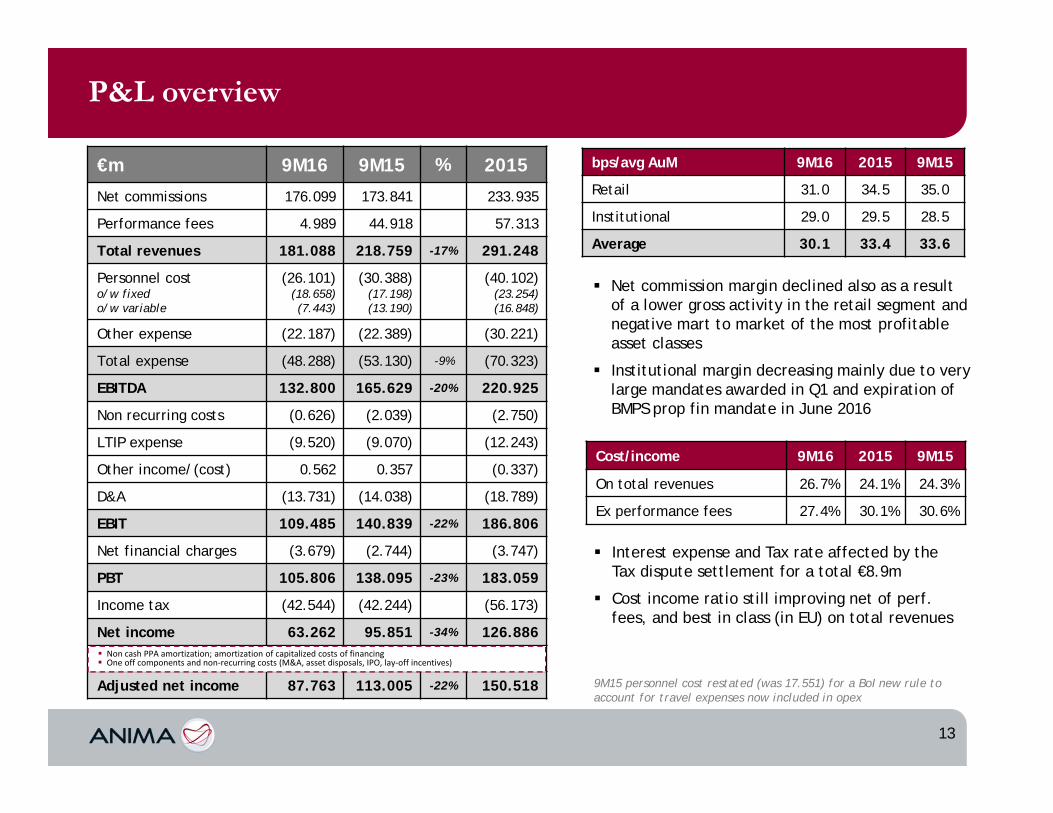

€m 9M16 9M15 % 2015

Net commissions 176.099 173.841 233.935

Performance fees 4.989 44.918 57.313

Total revenues 181.088 218.759 -17% 291.248

Personnel costo/w fixedo/w variable

(26.101)(18.658)(7.443)

(30.388)(17.198)(13.190)

(40.102)(23.254)(16.848)

Other expense (22.187) (22.389) (30.221)

Total expense (48.288) (53.130) -9% (70.323)

EBITDA 132.800 165.629 -20% 220.925

Non recurring costs (0.626) (2.039) (2.750)

LTIP expense (9.520) (9.070) (12.243)

Other income/(cost) 0.562 0.357 (0.337)

D&A (13.731) (14.038) (18.789)

EBIT 109.485 140.839 -22% 186.806

Net financial charges (3.679) (2.744) (3.747)

PBT 105.806 138.095 -23% 183.059

Income tax (42.544) (42.244) (56.173)

Net income 63.262 95.851 -34% 126.886

Adjusted net income 87.763 113.005 -22% 150.518

P&L overview

Non cash PPA amortization; amortization of capitalized costs of financing One off components and non‐recurring costs (M&A, asset disposals, IPO, lay‐off incentives)

bps/avg AuM 9M16 2015 9M15

Retail 31.0 34.5 35.0

Institutional 29.0 29.5 28.5

Average 30.1 33.4 33.6

Cost/income 9M16 2015 9M15

On total revenues 26.7% 24.1% 24.3%

Ex performance fees 27.4% 30.1% 30.6%

Net commission margin declined also as a resultof a lower gross activity in the retail segment and negative mart to market of the most profitableasset classes

Institutional margin decreasing mainly due to verylarge mandates awarded in Q1 and expiration of BMPS prop fin mandate in June 2016

Interest expense and Tax rate affected by the Tax dispute settlement for a total €8.9m

Cost income ratio still improving net of perf. fees, and best in class (in EU) on total revenues

9M15 personnel cost restated (was 17.551) for a BoI new rule to account for travel expenses now included in opex

14

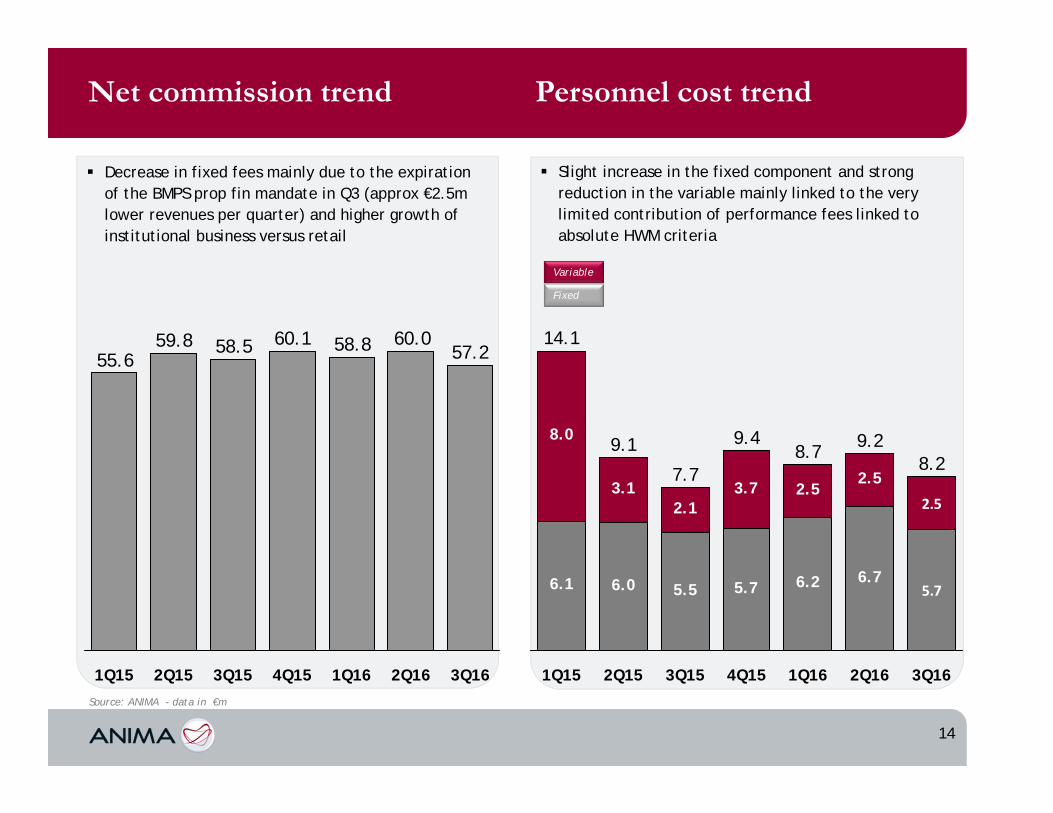

Net commission trend Personnel cost trend

Source: ANIMA - data in €m

60.058.860.158.559.855.6 57.2

2Q161Q164Q153Q152Q151Q15 3Q16

Decrease in fixed fees mainly due to the expiration of the BMPS prop fin mandate in Q3 (approx €2.5m lower revenues per quarter) and higher growth of institutional business versus retail

6.1 6.0 5.5 5.7 6.2 6.7

8.0

3.12.1

3.7 2.52.5

5.7

2.5

2Q16

9.2

1Q16

8.7

4Q15

9.4

3Q15

7.7

2Q15

9.1

1Q15

14.1

3Q16

8.2

Slight increase in the fixed component and strong reduction in the variable mainly linked to the verylimited contribution of performance fees linked to absolute HWM criteria

Fixed

Variable

15

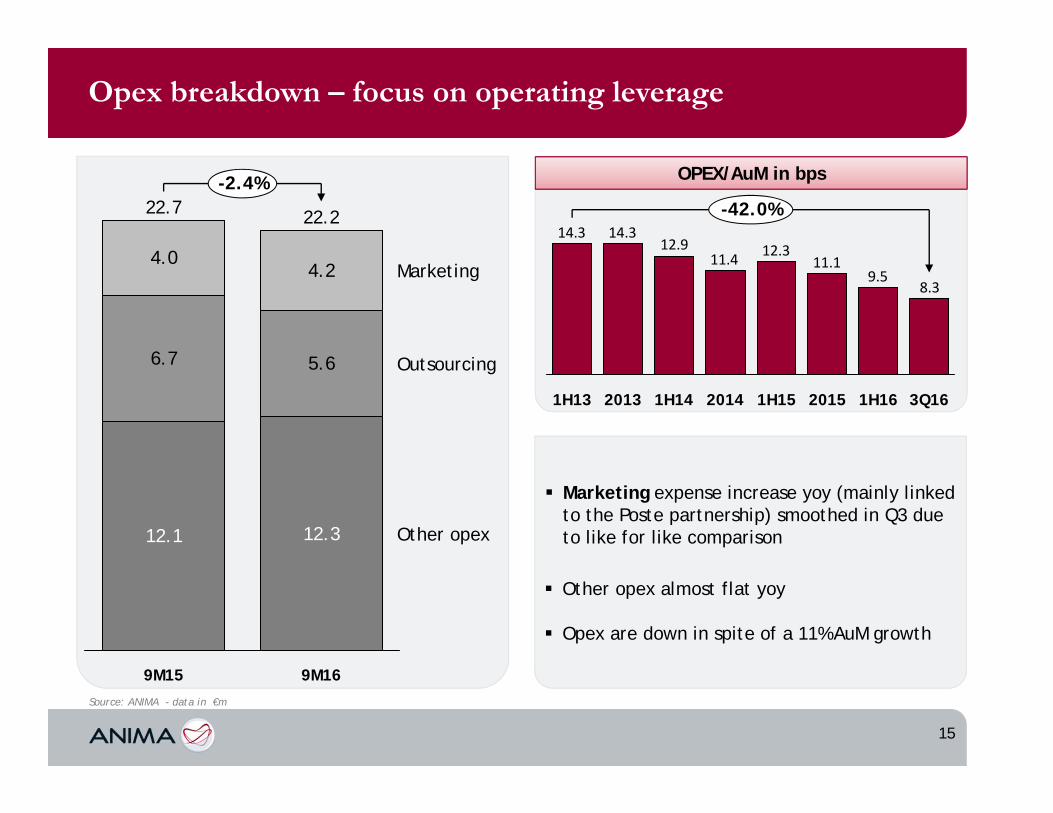

Opex breakdown – focus on operating leverage

Source: ANIMA - data in €m

12.1 12.3

6.7 5.6

4.04.2

22.2

-2.4%

Other opex

Outsourcing

Marketing

9M169M15

22.7

Marketing expense increase yoy (mainly linkedto the Poste partnership) smoothed in Q3 due to like for like comparison

Other opex almost flat yoy

Opex are down in spite of a 11% AuM growth

8.39.5

11.112.311.4

12.914.314.3

1H1620151H1520141H1420131H13 3Q16

-42.0%

OPEX/AuM in bps

16

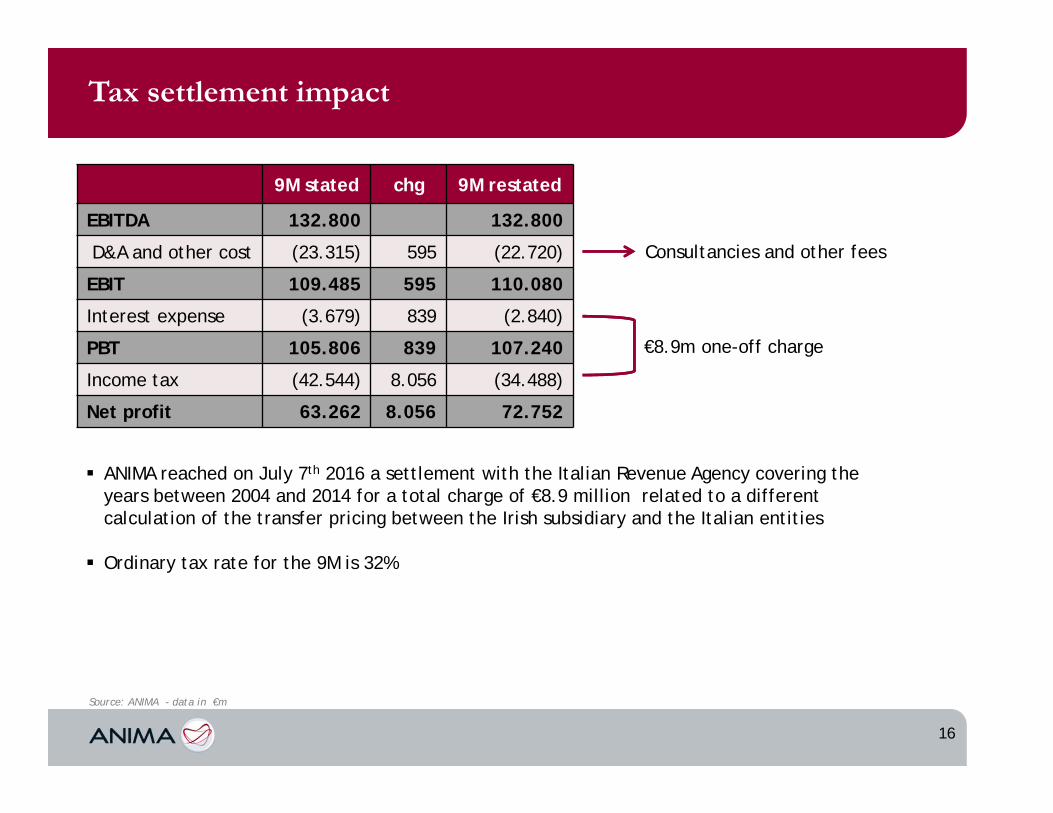

Tax settlement impact

Source: ANIMA - data in €m

9M stated chg 9M restated

EBITDA 132.800 132.800

D&A and other cost (23.315) 595 (22.720)

EBIT 109.485 595 110.080

Interest expense (3.679) 839 (2.840)

PBT 105.806 839 107.240

Income tax (42.544) 8.056 (34.488)

Net profit 63.262 8.056 72.752

ANIMA reached on July 7th 2016 a settlement with the Italian Revenue Agency covering the years between 2004 and 2014 for a total charge of €8.9 million related to a differentcalculation of the transfer pricing between the Irish subsidiary and the Italian entities

Ordinary tax rate for the 9M is 32%

€8.9m one-off charge

Consultancies and other fees

17

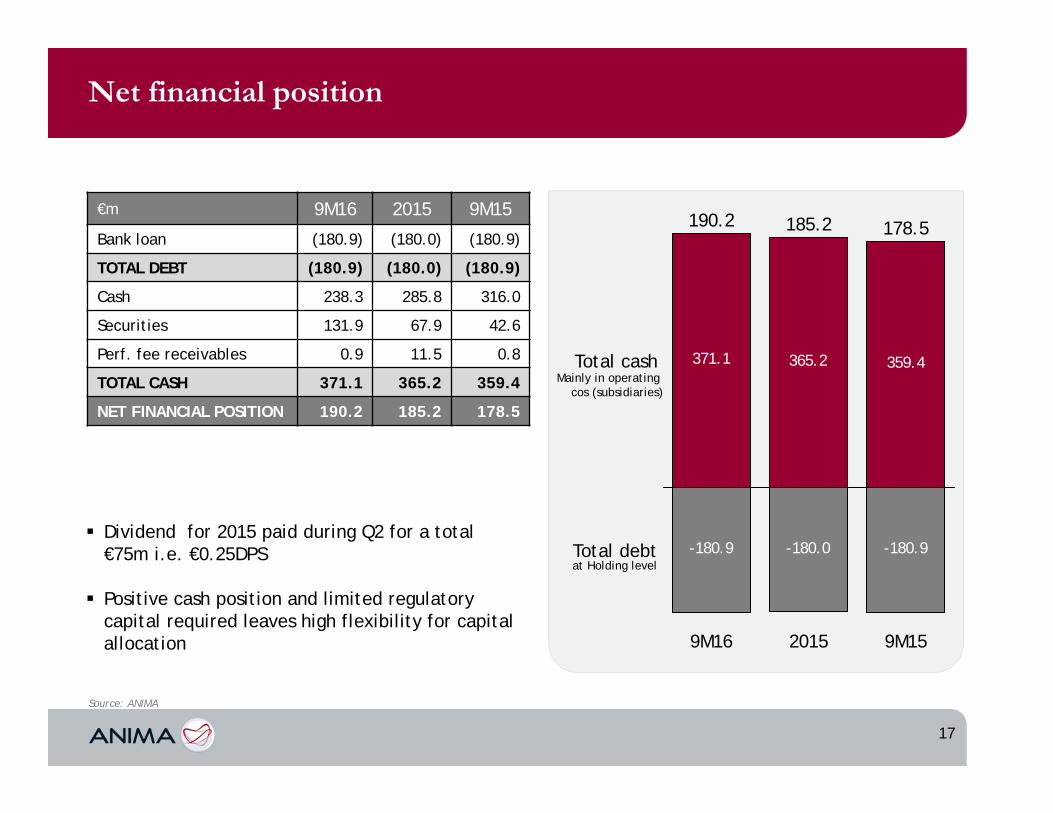

Net financial position

€m 9M16 2015 9M15

Bank loan (180.9) (180.0) (180.9)

TOTAL DEBT (180.9) (180.0) (180.9)

Cash 238.3 285.8 316.0

Securities 131.9 67.9 42.6

Perf. fee receivables 0.9 11.5 0.8

TOTAL CASH 371.1 365.2 359.4

NET FINANCIAL POSITION 190.2 185.2 178.5

Source: ANIMA

-180.9 -180.0 -180.9

371.1 365.2 359.4

2015

185.2

9M16

190.2

9M15

178.5

Total cash

Total debtat Holding level

Mainly in operatingcos (subsidiaries)

Dividend for 2015 paid during Q2 for a total€75m i.e. €0.25DPS

Positive cash position and limited regulatorycapital required leaves high flexibility for capital allocation

18

9M16 - Table of contents

Anima…who

Anima…what

Anima…why

Anima…how much

1

2

3

4

19

Closing remarks

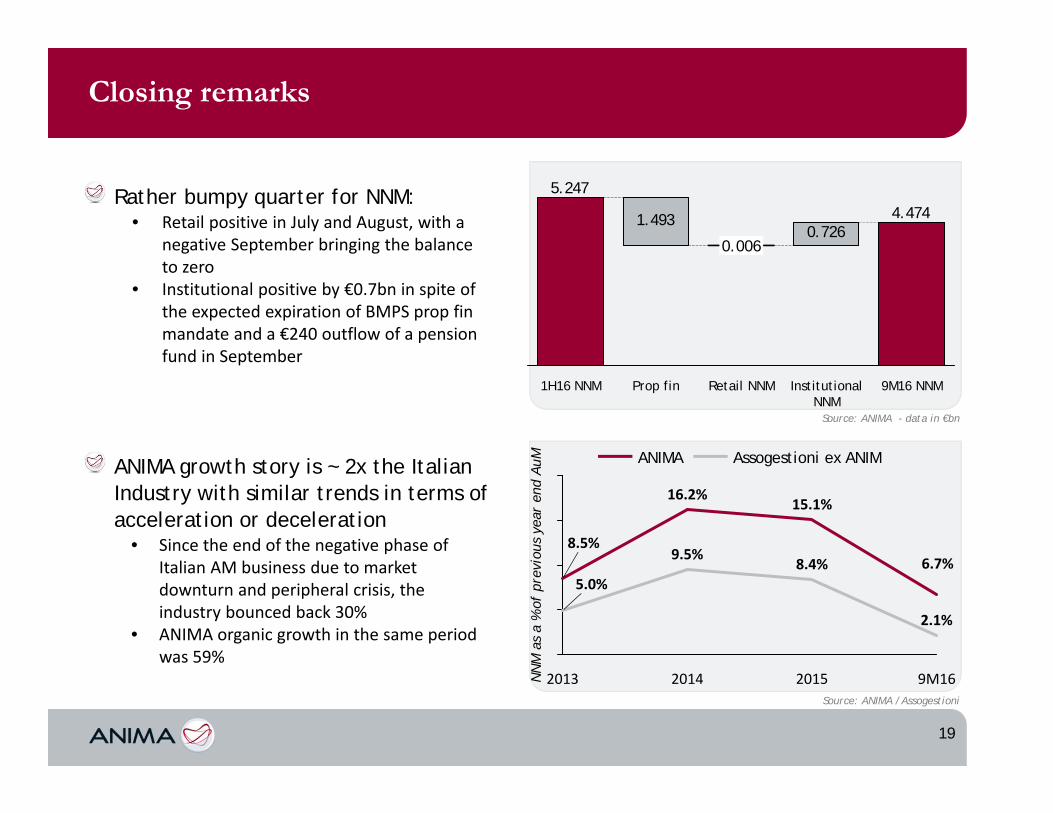

Rather bumpy quarter for NNM: • Retail positive in July and August, with a

negative September bringing the balance to zero

• Institutional positive by €0.7bn in spite of the expected expiration of BMPS prop fin mandate and a €240 outflow of a pension fund in September

4.4740.726

5.247

1.493

9M16 NNMInstitutional NNM

Retail NNM

0.006

Prop fin1H16 NNM

9M16

2.1%

6.7%

2015

8.4%

15.1%

2014

9.5%

16.2%

2013

5.0%

8.5%

ANIMA growth story is ~2x the Italian Industry with similar trends in terms of acceleration or deceleration

• Since the end of the negative phase of Italian AM business due to market downturn and peripheral crisis, the industry bounced back 30%

• ANIMA organic growth in the same period was 59%

Assogestioni ex ANIMANIMA

Source: ANIMA - data in €bn

Source: ANIMA /Assogestioni

NN

M a

sa

% of

pre

viou

sye

aren

d A

uM

20

Closing remarks

Focus for the remaining few weeks of 2016 is on planning the activity for the next year, deeply committed to explore additional growth drivers, with further improvement of our existing strategic partnerships and possibly leveraging a very solid expertise of value creating M&A to enjoy the harvest of our flexible and cost efficient organisation

Retail business reduced their appetite for financial products after the summerconcerned by the markets’ beta and with renewed uncertainty surrounding Italianbanks

Institutional business remains healthy especially thanks to the steadily growingproductivity of the agreement with Poste Italiane

ANIMA: different, yet unique!

21

Don’t leave during the credits…

On November 10th ANIMA and Poste Italiane together with CDP signed an agreement to develop a common project aimed at creating a leading asset management Group, further strengthening ANIMA leadership in the Italian AM industry

Based on the project, Poste, CDP and ANIMA submitted to Unicredit an offer for the acquisition of the asset management business currently belonging to Pioneer Global Asset Management

In 2017 Poste will contribute its asset management company (BancoPosta Fondi SGR) to ANIMA Holding, thus increasing the stake in ANIMA, that will almost double the size of the AuM to around €147bn

Not only the existing commercial relationship with Poste will be ultimately consolidated, but the contribution will significantly boost and increase the potential of future growth within the pool of clients’ assets (mutual funds, life insurance and deposits) available at Poste network

This agreement is consistent with our strategy to pursue the diversification and increase our distribution channels

Il presente materiale non può in nessun caso essere interpretato come consulenza, invito all’investimento, offerta o raccomandazione per l’acquisto o la vendita di strumentifinanziari, né costituisce sollecitazione al pubblico risparmio. ANIMA è esonerata da qualsiasi responsabilità derivante da un uso improprio del presente materiale al pubblico,effettuato in violazione delle disposizioni degli Organi di Vigilanza anche in materia di pubblicità. I rendimenti passati non sono indicativi di quelli futuri. Prima di aderire leggereil Prospetto, disponibile presso la sede della società, i collocatori e sul sito www.animasgr.it.

This document is not intended to be an offer or solicitation, investment advice or recommendation for the purchase or sell any financial instruments and it cannot be disclosed tothird parties and/or distributed to the public.This is an informative report and its content is not intended and cannot be used improperly, also as advertising, for the placementof any fund managed by ANIMA Sgr, accordingly to Italian law. The Company assumes the hereby given information as accurate and reliable, but it does not guarantee itsprecision and it shaIl not therefore be liable for its use by the addressees. Past performance is not indicative of future returns.For detailed information, please consult the sales prospectus available at ANIMA Headquarter, third parties distributors and on our corporate website www.animasgr.it.

Anima Holding spaCorso Garibaldi, 99I – 20121 Milanowww.animaholding.it

Investor RelationsFabrizio ArmoneTel. [email protected]