Embed Size (px)

Citation preview

I

Civil Action No. 99- -1 744 ROSA E. GARZA, On Behalf of Herself and All Others Similarly c' Situated,

P l a i n t i f f ,

vs . J. D. EDWARDS t COMPANY, RICHARD E. ALLEN, PAUL E. COVELO, DAVID E. GIRARD, DOUGLAS S . MASSINGILL, C. EDWARD MCVANEY, ROBERT C. NEWMAN, MICHAEL A. SCHMITT, DANIEL 8 . SNYDER and JACK L. THOMPSON,

Defendants.

COMPLAINT FOR VIOLATION OF THE SECURITIES EXCHANGE ACT OF 1934 AND J U R Y DEMAND

SUMMARY

1. This is a class action on behalf of all purchasers of

J .D. Edwards & Company ( " J . D . Edwards") common stock between

1/22/98 and 12/3/98 ( t h e IIClass Period"). J.D. Edwards develops,

produces, sells and services Enterprise Resource Planning ( * @ E R P e l )

software, which provides businesses with tools to he lp automate and

control accounting, personnel, manufacturing, customer service and

other business functions. V i a a series of false and misleading

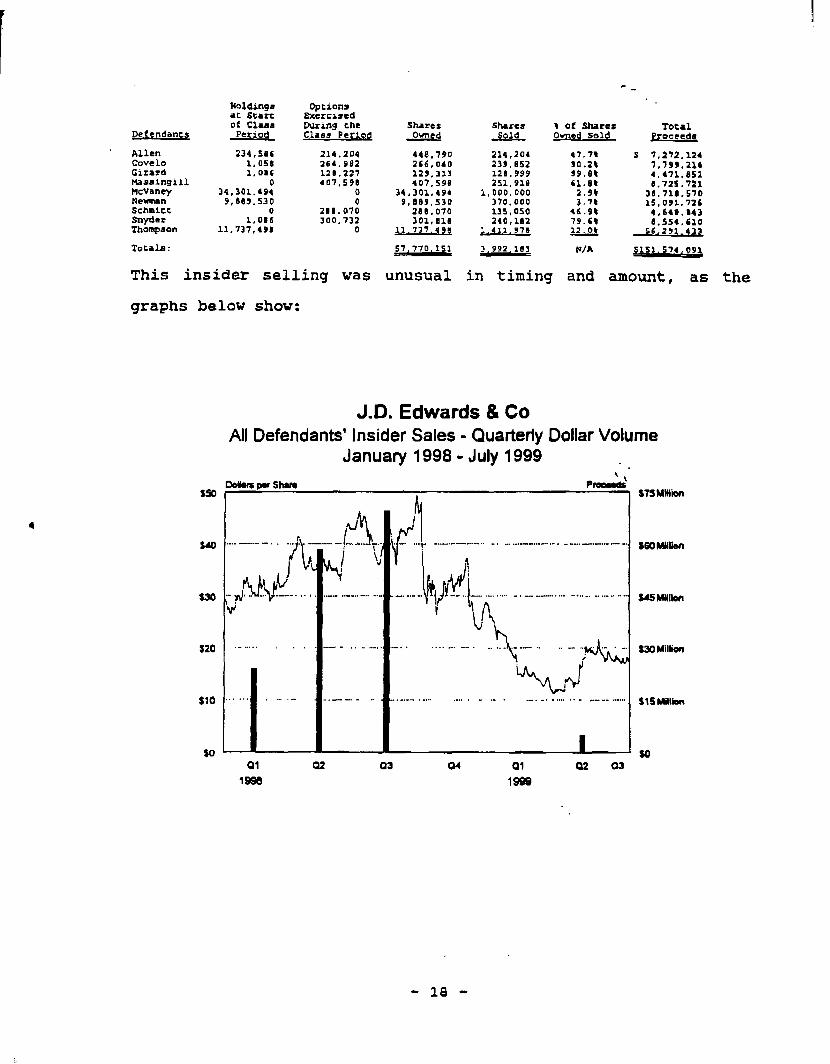

statements regarding the continued strong demand fo r J . D . Edwards'

core WorldSoftware product for the IBM A S / 4 0 0 operating system, the

- 1 -

successful introduction and technological superiority of its most

important new product -- OneWorld -- for the UNIX/Windows NT

operating systems, and the successful reorganization of its direct

sales force, which it forecast would lead to very strong softvare

license revenue growth, increased profit margins and EPS of

$.72-.$go in F99, defendants artificially inflated J.D. Edwards

stock from $ 2 4 - 7 / 8 in mid 1/98 to a Class Period high of $49-3/8 in

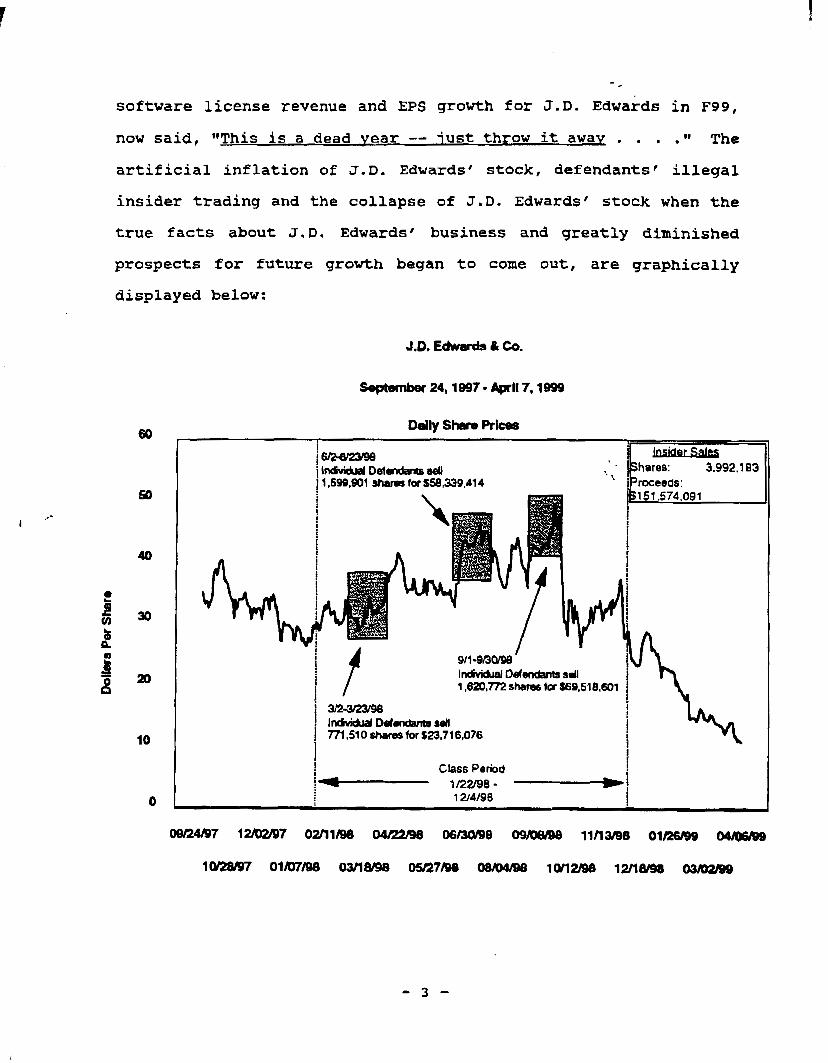

9/98. As J . D . Edwards stock soared to record levels, the nine top

insiders at J.D. Edwards unloaded 3,992,183 shares of their J.D.

Edwards stock at prices as high as $49 pocketing $151.5 million in

illegal insider-trading proceeds. But in 12/98, when J . D . Edwards

revealed that its growth of software l icense revenue had fallen

sharDlv, that t h e share of its license revenue represented by

Oneworld sales had also f a l l e n s h a m l v , indicating a lack of

success with t h i s vital new product, and that it was suffering from

sales force ' Iproduct ivi tv aroblems,'' its stock collapsed from $37

on 12/3/98 to $ 2 4 on 12/4/98, a 35% collaose. When J.D. Edwards'

results for t h e lstQ F99, ended 1/31/99, showed virtually no software license revenue srowth. continued stacrnation of OneWorlg

sales, continuing sales staff txoduct iv i tv txoblems, and a sham

decline in EPS, J.D. Edwards stock collapsed from $18-7/8 on

2/11/99 to $13-9/16 on 2/12/99, a 3 3 % fall. When J . D . Edwards

reDor ted a larue $lo+ m i l l i o n loss for the 2nd0 F99, ended 4 / 3 0 / 9 9 ,

due to sharply decreased software license revenues. indicatinu t h a t

J . D , Edwards would suffer a loss for all of F99. to be followed bv

F O O EPS of OnlV a few cents a t best, its stock f e l l to just $10-7/8

-- far below its C l a s s Period high of $ 4 9 - 3 / B . J.D. Edwards'

chairman, Edward McVaney, who had forecasted spectacularly strong

- 2 -

-

software license revenue and EPS growth f o r J.D. Edwards in F99,

now said, "This is a dead vear -- i u s t throw it away . . , .If The

artificial inflation of J.D. Edwards' stock, defendants' illegal

insider trading and the col lapse of J.D. Edwards' stock when the

true fact6 about J . D . Edwards' business and g r e a t l y diminished

prospects for future growth began to come out , are graphically

displayed below:

J.D. Edwards & CO.

60

!a

40

30

20

10

0

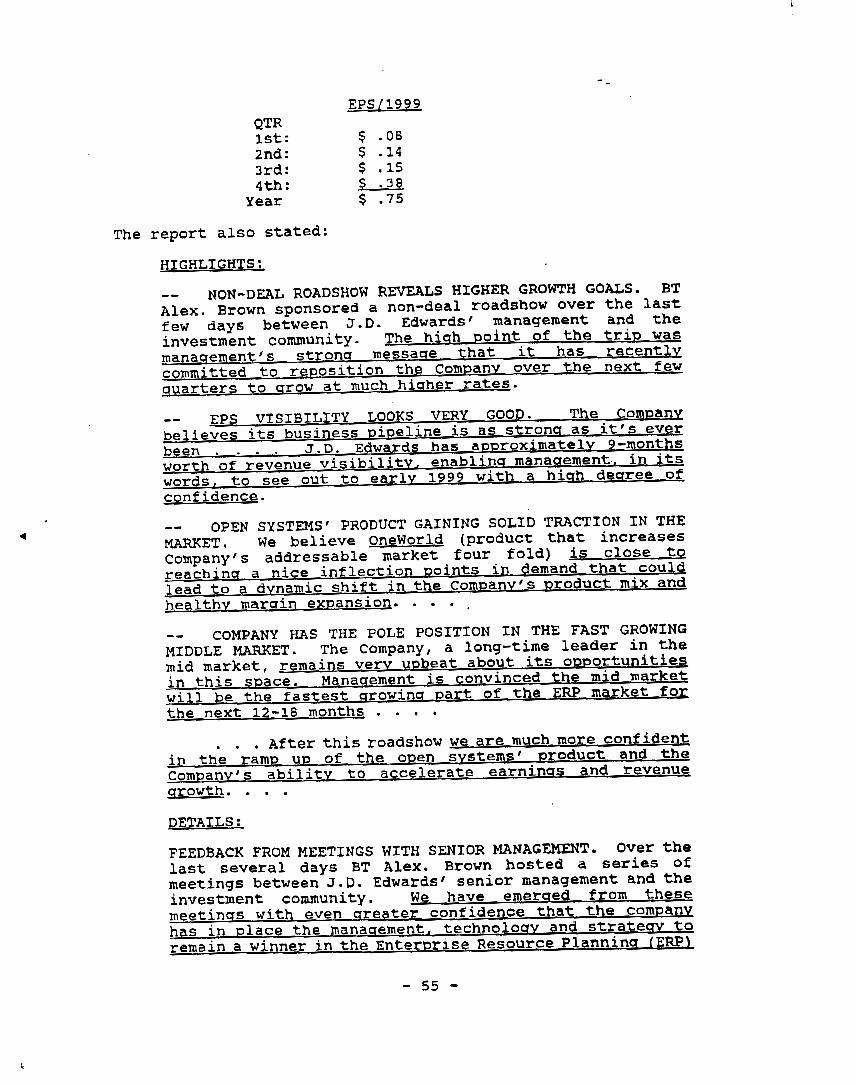

- 3 -

2. J . D . Edwards was founded in 1977 and became a successful

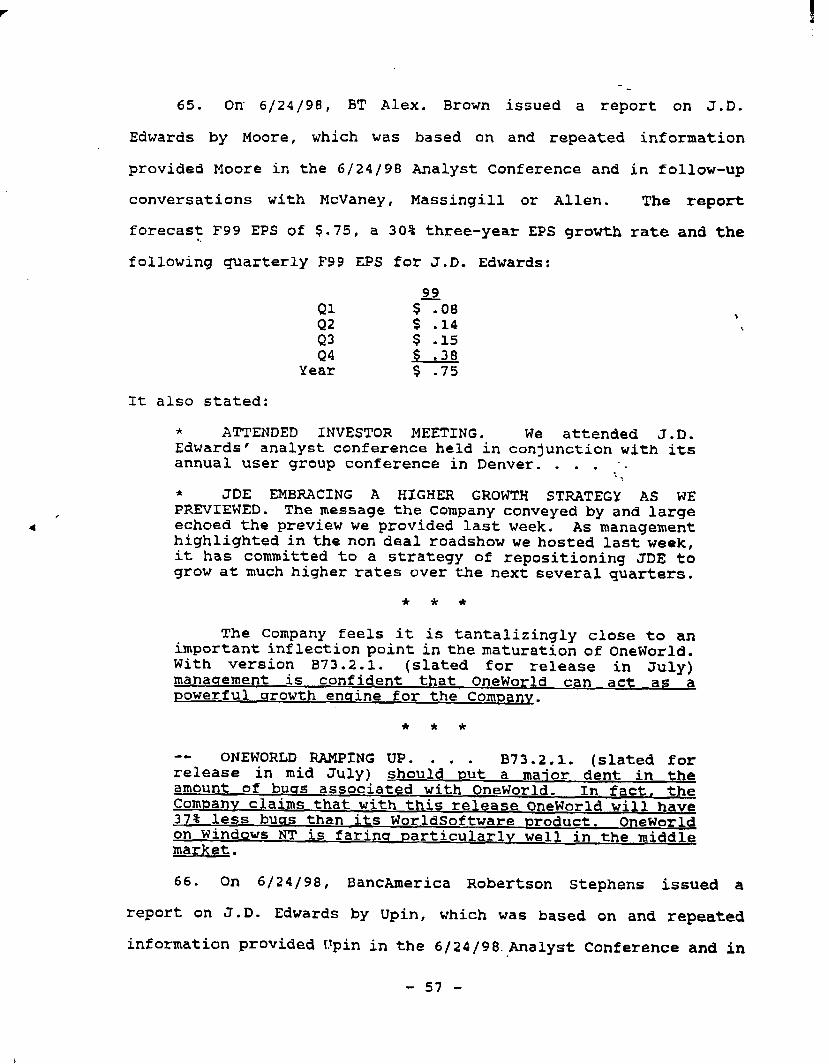

provider of ERP software to the so-called middle or mid-market,

&.g., companies with annual revenues between $ 2 5 0 million and $1.5-

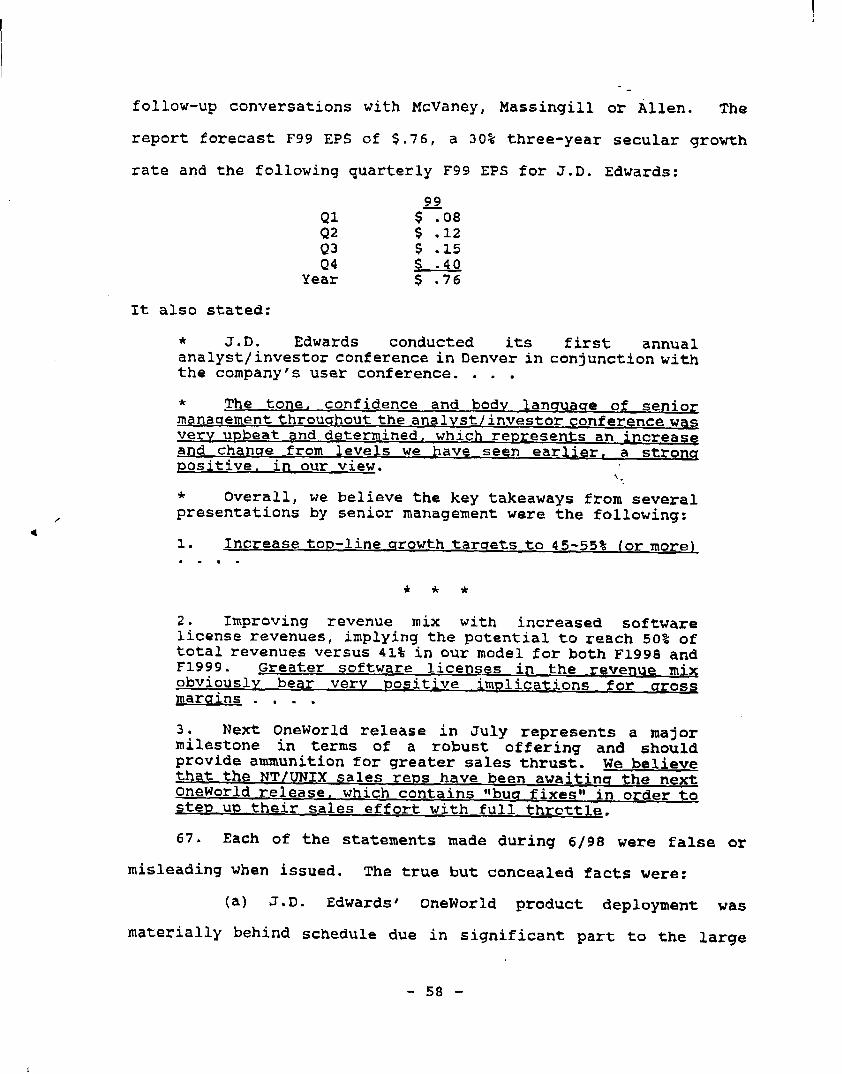

$2.0 billion, thus avoiding head-on competition with the largest

and most successful ERP software providers such as SAP, PeopleSoft,

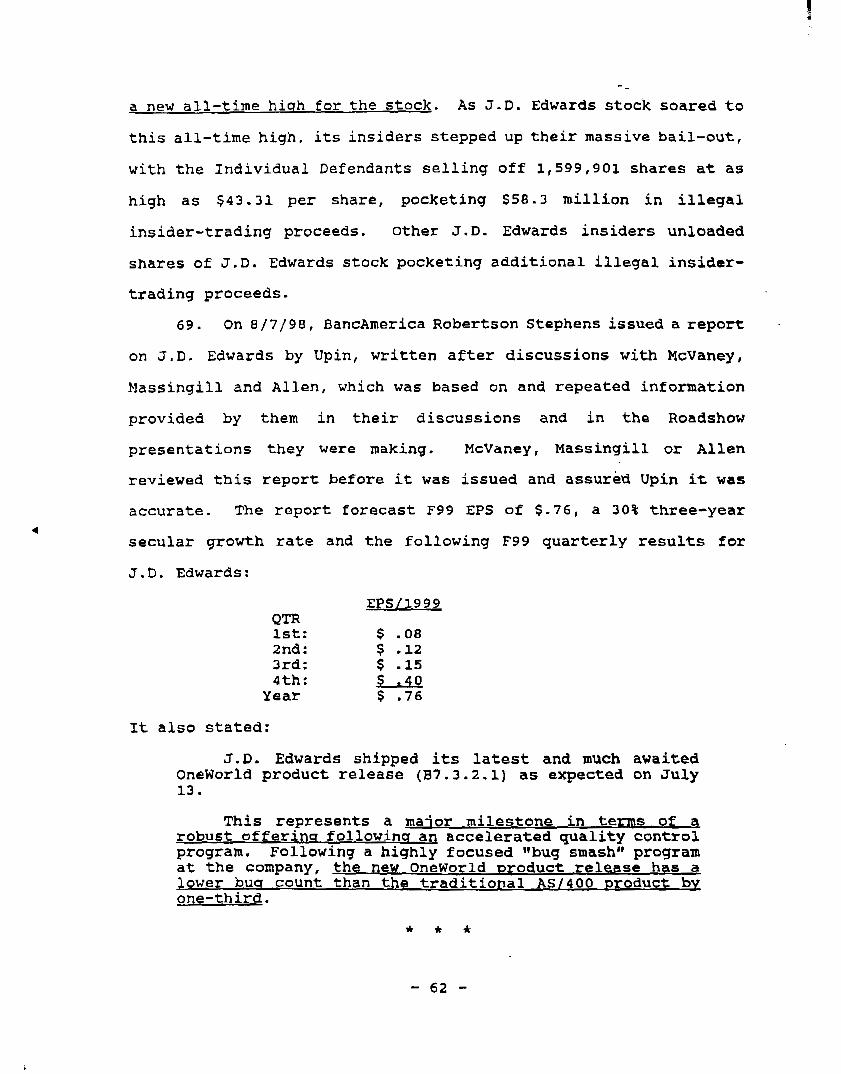

Baan and Oracle, which focused on t h e tthigh-end” market, i.~., large Fortune 1,000 corporat ions. Until l a t e 9 6 , J.D. Edwards’

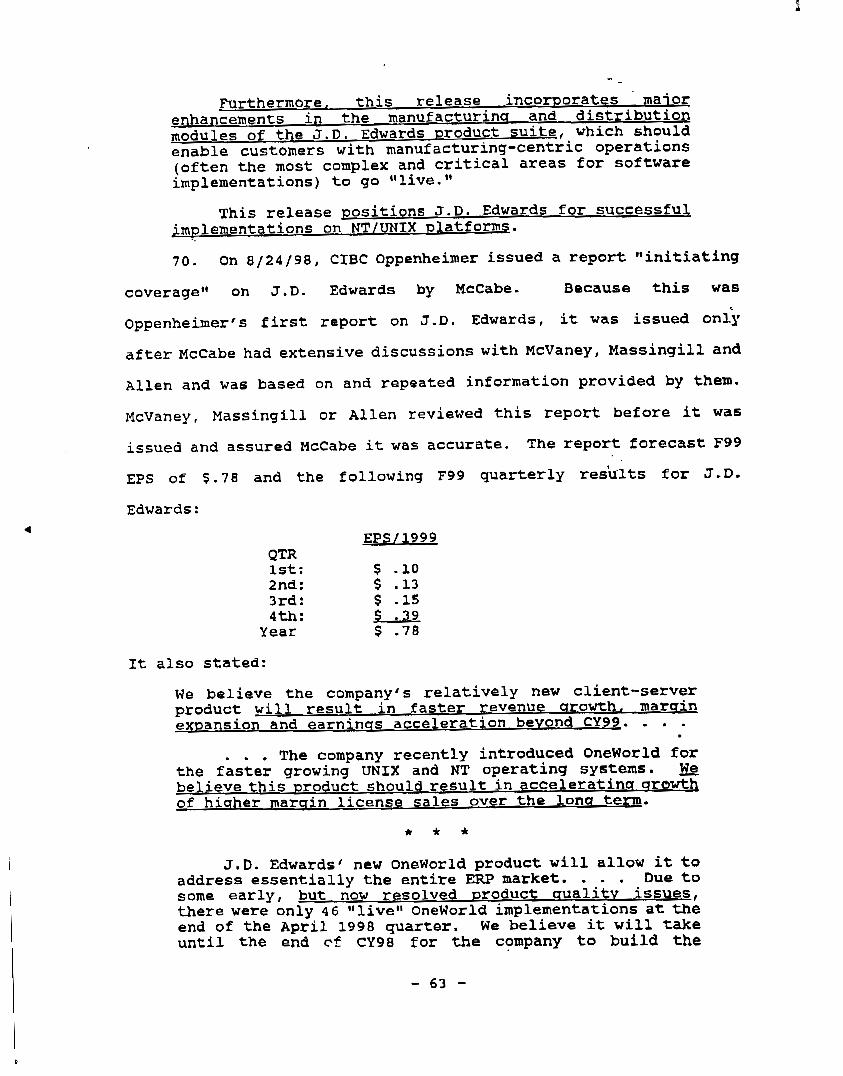

only ERP software product was Itworld Software,It which had been on

the market f o r many years, but worked o n l y on the “closedtt IBM

AS/400 operating system, which was an increasinglymature operating

system and was being increasingly eclipsed by the new UNIX and

Microsoft NT operating systems, so-called ‘‘open f o r which

J . D . Edwards had no product! This development placed J.D. Edwards

in an increasingly disadvantaged competitive p o s i t i o n , as it

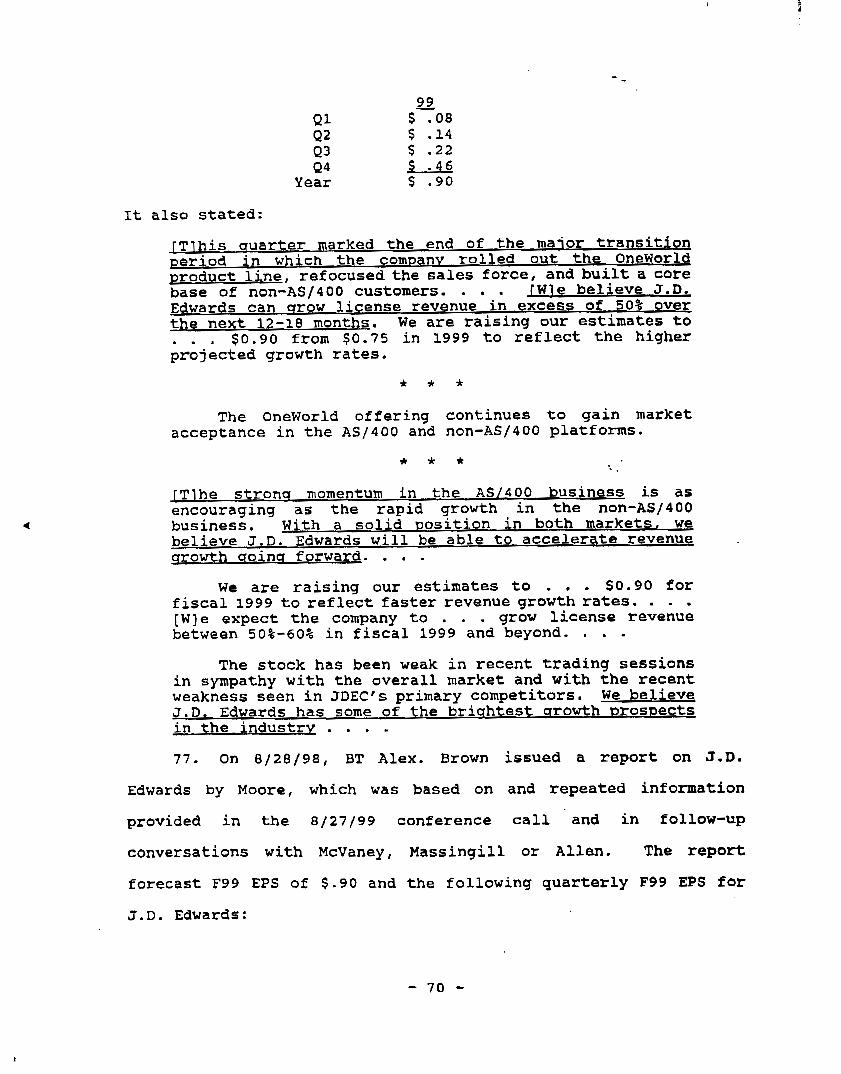

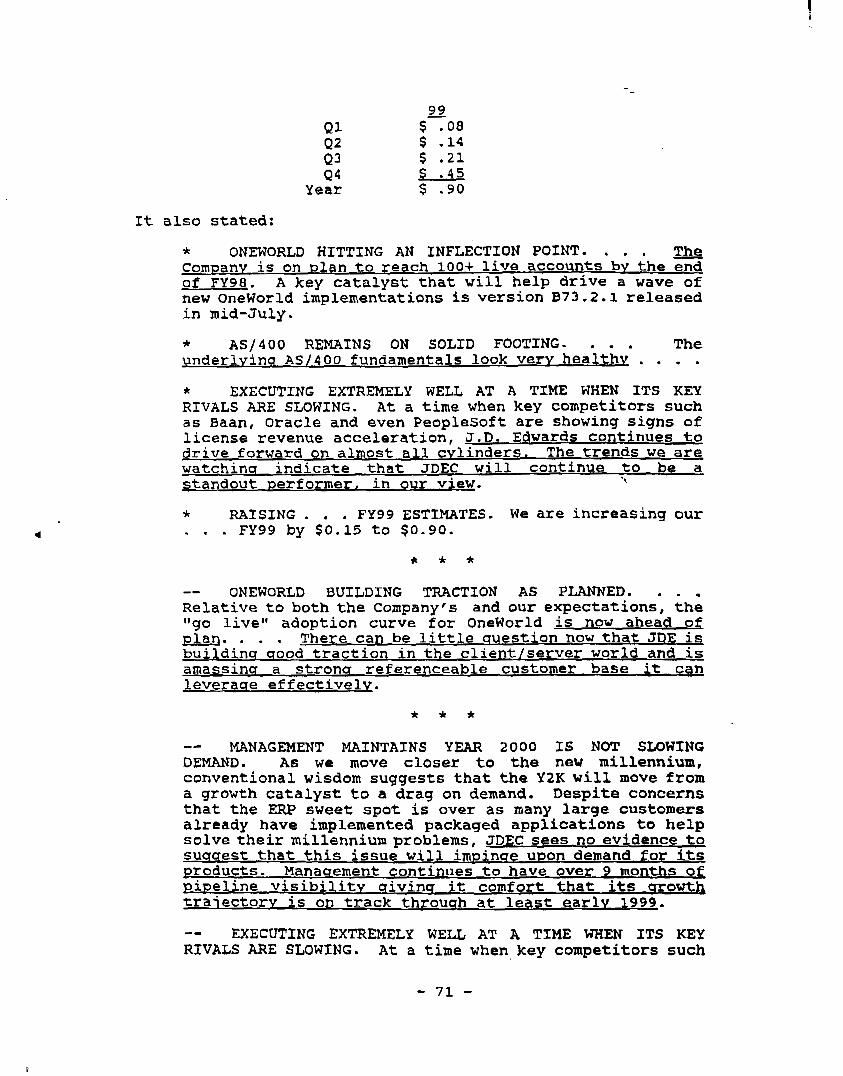

sharply limited the markets J . D . Edwards could sell to, leaving it

dependent upon one product which operated only on an increasingly

outmoded operating system. In a d d i t i o n , during 94-96, the por t ion

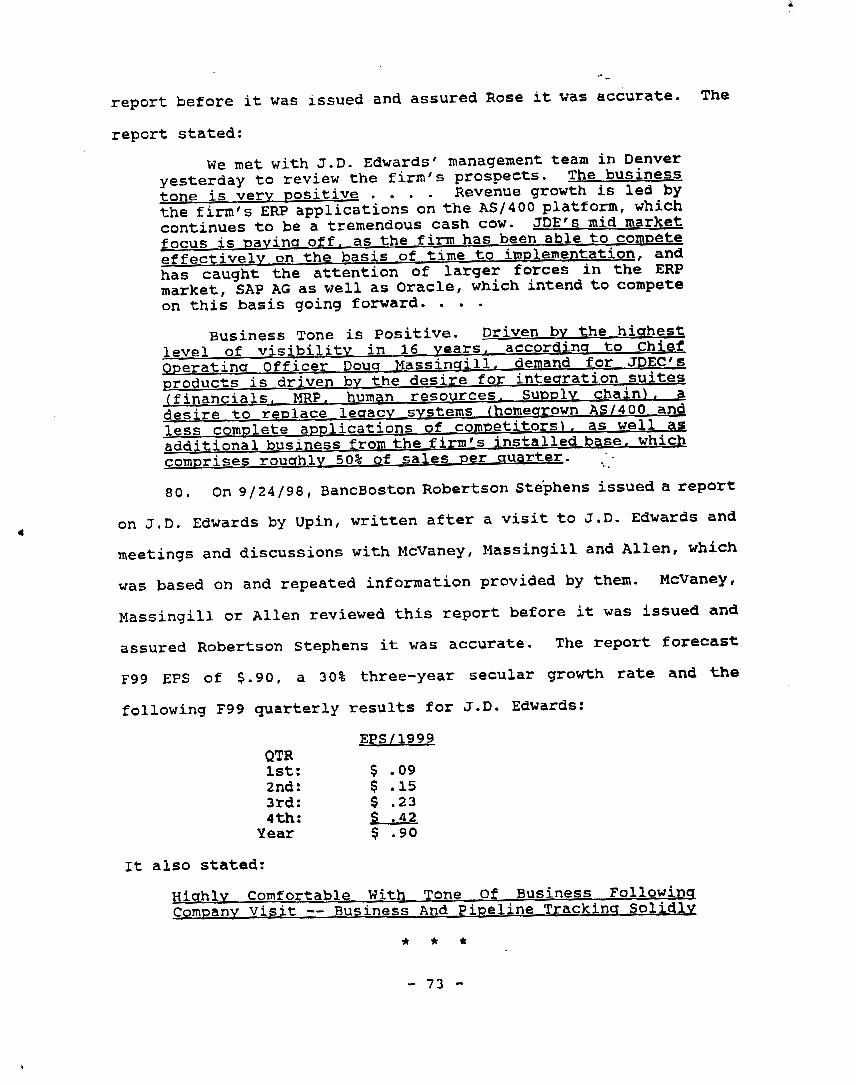

of J . D . Edwards‘ total revenues coming from service revenue, as

opposed to software licensing, increased from 55.3% of total

revenue to 62.3%. Since service revenue carried much lower profit

margins than software license fees, this resulted in J.D. Edwards’

n e t profit margins falling to 3 . 3 % in 9 6 , well below those achieved

in prior years, &.e . , 58 in 93, a trend which threatened J . D .

Edwards‘ ability to continue to achieve s t r o n g profitable growth

going forward, To make matters worse, because the tlhight’ end of

the ERP market was becoming increasingly saturated, S A P ,

- 4 -

- - Peoplesoft, Oracle and Baan were migrat ing into t h e mid-market and

i n t o i n t e n s i f i e d competition with J . D . Edwards.

. .

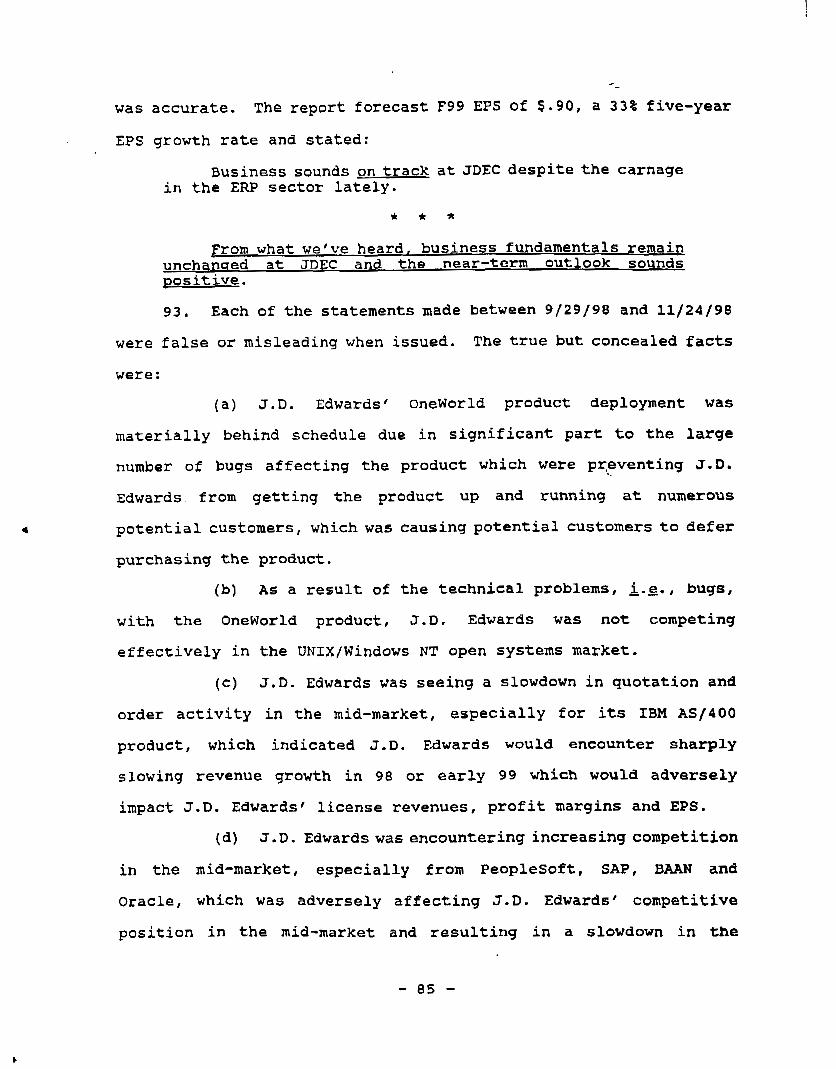

3 . TO t r y t o overcome t h i s s i t u a t i o n , J.D. Edwards developed

a new ERP sof tware p roduct , known as Oneworld, which was capable of

o p e r a t i n g on t h e U N I X and Microsoft NT opera t ing sys tems, as well

as the I B M AS/400 operat ing system. J . D . Edwards in t roduced the

i n i t i a l v e r s i o n OneWorld i n 12/96, hoping it would g r e a t l y increase

t h e s i z e of the market and number of p o t e n t i a l customers SOD- .

Edwards could sell i ts products t o and t h a t t h i s would r e s u l t in

g r e a t l y i n c r e a s e d software license revenues and strong EPS growth.'

when J.D. Edwards' i n s i d e r s r e a l i z e d t h a t there was a n i n c r e a s i n g

r i s k t h a t J.D. Edwards' business would encounter sharply slower

growth i n F99-00, J . D . Edwards' top i n s i d e r s d e c i d e d : t o t a k e J,D.

Edwards p u b l i c , raise millions i n new c a p i t a l f o r J . D . Edwards and

c r e a t e a t rad ing marke t i n J. D. Edwards s tock so its i n s i d e r s could

sel l off millions of s h a r e s of their J . D . Edwards. On 9 / 2 3 / 9 7 ,

J . D . Edwards went p u b l i c a t $23 per share v ia an i n i t i a l public

offering ( Ir IPOtt ) i n which J . D . Edwards and certain of its i n s i d e r s

s o l d m i l l i o n s of sha res of J . D . Edwards common stock to the

public . ' J .D. Edwards ' P rospec tus exp res s ly s t a t ed t ha t J.D.

Edwards' a b i l i t y t o achieve

a .. .

f u t u r e revenue growth rwasl s u b s t a n t i a l l v d e p e n d e n t upon t h e market acceptance of , I . oneworld 8 . and t h e a b i l i t v of t h e Company t o l i c e n s e OneWorld . . t o new customers . . . . If, f o r any reason, the Company is

1 J.D. year .

Edwards o p e r a t e s on a f i s c a l y e a r e n d i n g 10/31 of each

2 In connec t ion wi th t h e IPO, J.D. Edwards' i n s i d e r s were required to agree t o a "lock-up" of t h e i r shares by which they could n o t se l l any more of t h e i r J . D . Edwards s t o c k for approximately si% monrhs a f t e r t h e o f f e r i n g or u n t i l 3 / 2 4 / 9 8 ,

- 5 -

unable t o successfully sell . . . OneWorld in the U N I X or Windows NT (vvNT1l) markets . . . such failure would have a material adverse effect on the Company's business, operating results and financial condit ion. Moreover, if the Company fails to meet the expectations of market analysts or investors with regard to sales or implemen- t a t i o n s of OneWorld application suites, the market price of the Company's Common Stock would likely be materially adversely affected.

Thus, by late 97, J . D . Edwards' ability to achieve substantial

profitable growth was virtually completely dependent upon the

successful introduction and commercial acceptance of this new

OneWorLd product well as continued growth of and its a b i l i t y to

continue to compete successfully in the mid-market A S / 4 0 0 market.

4 . After jumping to as high as $40-5 /8 shortly after the

IPo, J.D. Edwards stock performed poorly over the next five months

and, by 1/12/98, was selling at as low as $24-7/8,"back down to

near its IPO price. This poor performance was due to investor

concerns that growth in the .overall ERP software market was t

slowing, that customers might cut back on ERP software purchases

due to concerns over Y 2 K problems and allocation of monies to solve

Y2K concerns, over increasing competition in J.D. Edwards' mid-

disappointing financial results, as well as the slower-than-

expected progress J . D . Edwards appeared to be making in getting

customers to llgo live" with i t 5 new OneWorld software product.

5. Because many of J.D. Edwards' top insiders were poised to

begin unloading millions of their shares of J . D . Edward6 stock as

soon as the IPO lock-up expired in 3 / 9 6 , t h e y viewed the decline of

the stock in 12/97-1/98 with concern and wanted to try to push J.D.

Edwards stock back up higher in price, as this would maximize their

insider selling proceeds. To accomplish.this, t h e s e insiders knew

- 6 -

t h a t it was imperative that J.D. Edwards falsely assure investors

t h a t J. D. Edwards' OneWorld product was a "breakthrought1

technology, was achieving significant commercial success and J.D.

Edwards would'achieve strongly increasing software license revenues

and EPS during F99-FOO and its EPS would show strong 30% growth

over the next three to five years .

6. To t r y to halt the decline in J.D. Edwards s tock and push

it back up higher, on 1/22/98, McVaney spoke to the Bloomber9 Forum

and assured investors "thinas are f i n e randl J . D . Edwards is aoinq

q u i t e w e l l , I l that J.D. Edwards was switching over to a "Qreat deal

more licensins fees, due t o the success of OneWorld -- which he represented was l1leaPfros technoloqy" by which "we have clearlv

leaped out ahead of t h e industrv.Il

7. During 2 / 9 8 - 5 / 9 8 , defendants assured investors that

OneWorld was progressing "on schedule" and J.D. Edwards expected

accelerated qrowth for this product in the future. They also

represented t h a t J.D. Edwards' A S / 4 0 0 business was very strong,

actually benefiting from Y2X concerns due to the quick

implementation available with J . D . Edwards' WorldSoftware product.

When J.D. Edwards reported its 2ndQ F98 results in 5/98, it

insisted Oneworld's sales were "riaht on Plan," that the rollout of

Oneworld had been 1tplanned8B to be slow, and that J.D. Edwards'

salesforce had been telling customers to wait on buying the

oneworld product until the July release of a new version of

Oneworld (B7.3.2.1), which would have 33% fewer buss than J.D.

Edwards' mature A S / 4 0 0 rmoduct. WorldSoftware. J. D. Edwards

cont inued to represent that OneWorld represented a major

technological advance and would hit a substantial "inflection

- 7 -

- _ pointB1 later in 9 8 . J.D. Edwards told investors t h a t its A S / 4 0 0

market remained very stronq, with no fall-off in demand due to Y2K

issues or concerns, t h a t J. D. Edwards' pipeline was very s tronq and

it was verv positive about F99. forecastina F99 revenue a a i n s of

30%-40%, F99 EPS of $ . 7 2 - $ . 7 5 and 3 0 % EPS qrowth for the next f e w

years, As J.D. Edwards stock moved higher in 3/99, the Individual

Defendants sold off 771,510 of their shares at as high as $32 per

share, pocketing $23.7 million i n illegal insider-trading proceeds.

8. In 6 / 9 8 , J . D . Edwards' t op executives conducted a multi-

city l'Roadshow'I and held J.D. Edwards' first investorlanalyst

conference in Denver to meet with a n a l y s t s , money and portfolio

managers and institutional investors and update them on its

business. J.D. Edwards said t h a t , due to the strenath of its

pusiness, it was forecasting much hisher r a t e s of srowth than

before and t h a t J.D. Edwards would m o w faster than the lamest ERP

providers -- Oracle. Baan. SAP or Peoplesoft. Defendants said J.D.

manaqement could see out to earlv F99 with a "hiah dearee of

conf idence ." They also represented t h a t J.D. Edwards' mid-market

was seeing verv strona clrowth, there was no slowdown due to Y2K

problems/issues, J.D. Edwards was successfully competing in the

mid-market against all comers, t h e July re lease of the oneworld

upgrade would have 33+% fewer bugs than J.D. Edwards' mature

WorldSoftware product and Oneworld was very close to a maior

inflection Doint. As a result, J. D. Edwards was now forecasting

F99 revenue growth of 45%-55% or more, F99 license revenue growth

of at l e a s t 5 0 & , which would be very posit ive for J . D . Edwards'

- 8 -

-

profit margins, and was very comfortable with forecastinq 30%

three- to five-vear EPS arowth. After the 7 / 9 8 introduction of

oneworld version B7.3.21, J.D. Edwards' management told analysts

they were Ilverv Dositive" on J. D. Edwards' F99 EPS prospects -- forecasting F99 EPS of $ .go+ as OneWorld had now reached the "e~@

of fits1 t r a n s i t i o n period,lI was gaining 9narket acceDtanceIl and

was "ahead of Dlan" -- hitting a "maior inflection point," which would result in J . D . Edwards achieving license revenue growth df 509-604 in F99. As J.D. Edwards s t o c k soared higher to its then

all-time high of $ 4 4 - 1 / 4 in late 6/98, the Individual Defendants

sold off 1,599,901 of their J.D. Edwards' shares at as high as $ 4 3

per share, pocketing $58.3 million in insider-trading proceeds.

9. During 8/98-9/98, J.D. Edward6 stressed the successful

7/96 release of Version B7.3.2.1 of Oneworld -- which it

represented had "resolved product aualitv issues" and had a 'lone-

t h i r d " lower bug count than J.D. Edwards' mature WorldSoftware

product. J . D . Edwards again assured investors that areat lv

increased license fees and thus higher profit margins would follow

in F99, that it continued to have hiah EPS visibilitv extendins o u t

nine months, that it was not seeing any slowdown in orders ox

demand due t o YZK problems or concerns, it continued t o have a very

strona competitive position in the mid-market and wa6 on track for

F99 EPS of $. 90+. As J.D. Edwards stock soared to its all-time

high of $ 4 9 - 3 / 8 on 9/24/98, the Individual Defendants sold off

another 1,620,772 of their J.D. Edwards shares at as high as $ 4 9 ,

pocketing $ 6 9 . 5 million i n insider-trading proceeds.

10. In late 9/98, PeopleSoft announced another major EPS

shortfall. A few days later, another.ERP vendor, Citrix, also

- 9 -

reported a . major EPS shortfall. ERP stocks plunged a s these

amounts ind ica ted a l l ERP providers were having problems with their

business which would hurt t h e i r EPS. J . D . Edwards stock fell from

$49-3/8 on 9 / 2 4 to $27 on 10/8/98. To h a l t the collapse in J.D.

Edwards stock, during 10/98, J.D. Edwards held a conference call

with analysts and others, interviews wi th the financial media, and

stepped-up their contacts wi th analysts, telling them that:

0 J . D . Edwards had seen no slowdown in its bus iness or markets and saw no slowdown on t h e horizon.

e J . D . Edwards' p i p e l i n e remained extremelv stronq.

3-D. Edwards' main market -- the mid-market -- had only besun to acce lera te .

a J. D. Edwards was successfullv competinq a g a i n s t P e o p l e s o f t , SAP and others in the mid-market .and, i n fact, competition from them had decreased in the mid-inarket.

J.D. EUwards still saw acceleratina srowth and was expecting software license s a l e s to increase 50%+ in F99.

0 oneWorld uptake remained on track.

0 By the end of the year, J . D . Edwards' OneWorld sof tware will be lion Dar or better" t han WorldSoftware.

a J.D. Edwards' AS/400 business was solid, enioyina stronq demand.

J.D. Edwards still expected t o achieve F99 EPS of $.go+ and three- to five-year EPS growth of 30%+.

11. In 11/98 , McVaney res igned as J.D. Edwards' CEO.

However, J.D. Edwards assured investors this change was not due to

any financial problems or poor performance and J. D. Edwards was nat seeins any kind of slowdown in its business. J. D . Edwards

represented it was l l 'd i f ferent '** from S A P , Peoplesoft, etc. , as its markets and customers were 'l'verv robust and cxowinq,rpl and demand

for its AS/400 product and OneWorld had been and remained llstronq.II

- 10 -

- _ 12. Due to Defendants' positive representations and

assurances, by 12/3/98 J.D. Edwards' stock had recovered to $37.

However, on 12/3/98, when J.D. Edwards reported its 4 t h ~ ~ 9 8

results -- traditionally J.D. Edwards' strongest quarter of the

year -- it revealed that its rate of growth of software license

revenue had f a l l e n sharDlv in the 4thQ and that the share of

software license revenue represented by OneWorld had also f a l l e n

shamlv, indicating a lack of s u c c e s s with this vital new product',

that J . D . Edwards was suffering from sales force productivity

problems, that 99 was a year of "uncertainty" and that J.D. Edwards

lacked visibilitv into f u t u r e sales and revenues, These

revelations caused J.D. Edwards s tock to fall from $37 on 12/3/98

to $ 2 4 on 1 2 / 4 / 9 8 , a 35% one-day collapse on volume 'of 8 .9 mil l ion

shares -- the larsest sinsle dav stock drop and tradins volume in

J . D . Edwards' historv as a Dublic comr>anv. After 12/4/98, t h e bad

news regarding J.D. Edwards has continued unabated. J.D. Edwards'

lStQ F99 results, i.g., the quarter ended 1/31/99, showed v i r t u a l l y

po software license revenue a r o w t h , continued stagnation of the

oneworld product and continuing sales staff productivity problems,

resulting in a s h a m decline in net income and EPS to $ 4 . 3 million

and $. 0 4 , respectively -- major decreases from its lstQ F98 n e t

income and EPS. When this shortfall was revealed on 2/11/99, J.D.

Edwards stock again collapsed, this time from $18-7/8 on 2/11/99 to

$13-9/16 on 2/12/99, a 33% one-day f a l l on extraordinary volume of

12.5 million shares -- setting a new one-day trading volume record

for J.D. Edwards s tock. Then J . D . Edwards astonished investors and

the markets by reportina a larue $IO+ million loss f o r its 2ndQ

F99, ended 4 / 3 0 / 9 9 , .due to S h a r R l V decreased software license

- 11 -

- revenues, indicatinq that J . D . Edwards now would suffer a loss f o r

a l l of F99 and achieve FOO earninss of only a few c e n t s a share, a t

- b e s t . As a r e su l t of this col lapse in J.D. Edwards' business, its

stock declined to $10-7/8 -- far below its Class Period high of

$ 4 9 - 3 / 8 . McVaney, who had forecasted spectacularly strong revenue

and EPS growth for J.D. Edwards, now said, "This is a dead vear -- just throw it awav . . . . I1

13. In 2/99 an article by Dennis Howlett appeared in World

Reporter on NewsWire which discussed J.D. Edwards' business and

s t a t e d IIOneworld is still verv much 'version one' w i t h Droblems

t h a t on lv now are beina satisfactorily addressed. . . . JRlecentlx JDE had to release an umtrade to solve over 2 , 5 0 0 buss. I' The

upgrade version referred to by Howlett in this article was a

version of Oneworld released in 12/98 after the Class Period ended!

According to Howlett, prior versions of OneWorld had been a

11nishtmare18 t o try to implement. In 7/99 an article by Craig

Stedman appeared in Computerworld which s t a t e d as to J.D. Edwards,

"An upgrade of the company's multiplatform OneWorld ERP suite was

released last month . . . The upgrade is supposed to resolve

stability issues in some modules and fill out Oneworld's

functionality so it's euuivalent to the older AS/400-based

WorldSoftware nroduct l i n e . "

14. Instead of the F99 EPS of S . 9 0 forecast during most of

the Class Period, J . D . Edwards has thus f a r reported losses of $. 06

and will ult imate ly report a larue loss f o r F99! J.D. Edwards'

financial decline is set forth below:

- 12 -

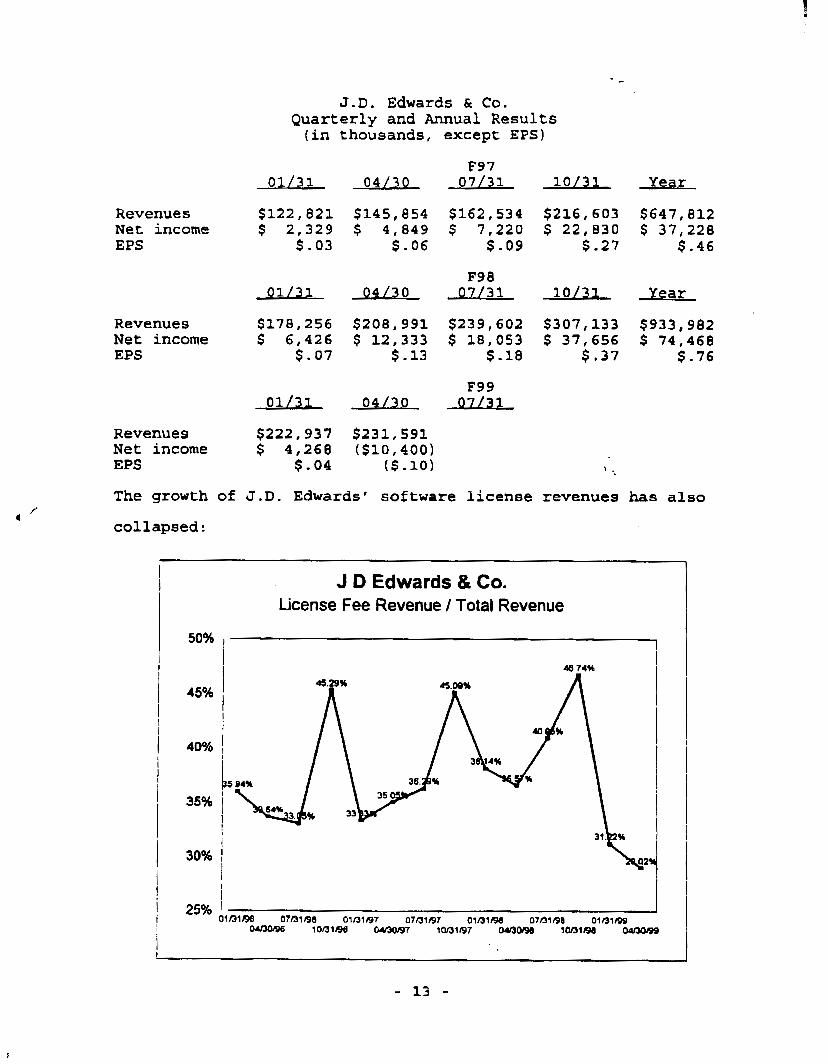

J.D. Edwards 6r Co. Quarterly and Annual Results (in thousands, except EPS)

F97 01/31 0 4 / 3 0 07/31 10/31 Year

Revenues $122,821 $ 1 4 5 , 0 5 4 $162,534 $216,603 $647,812 Net income -7 2,329 $ 4 , 8 4 9 $ 7 , 2 2 0 $ 22,830 $ 37,228 EPS $.03 $.06 s.09 $.27 $ . 4 6

F98 01/71 0 4 / 3 0 07/31 10131 Year

Revenues $178,256 $208,991 $239,602 $307,133 $933,902 N e t income S 6,426 $ 12,333 $ 18,053 $ 37,656 $ 74,460 EPS $.07 $.13 $.le $ .37 S.76

Revenues $222,937 $231,591 Net income $ 4 , 2 6 8 ( $ 1 0 , 4 0 0 ) EPS $ . 0 4 (S.10) ' -.

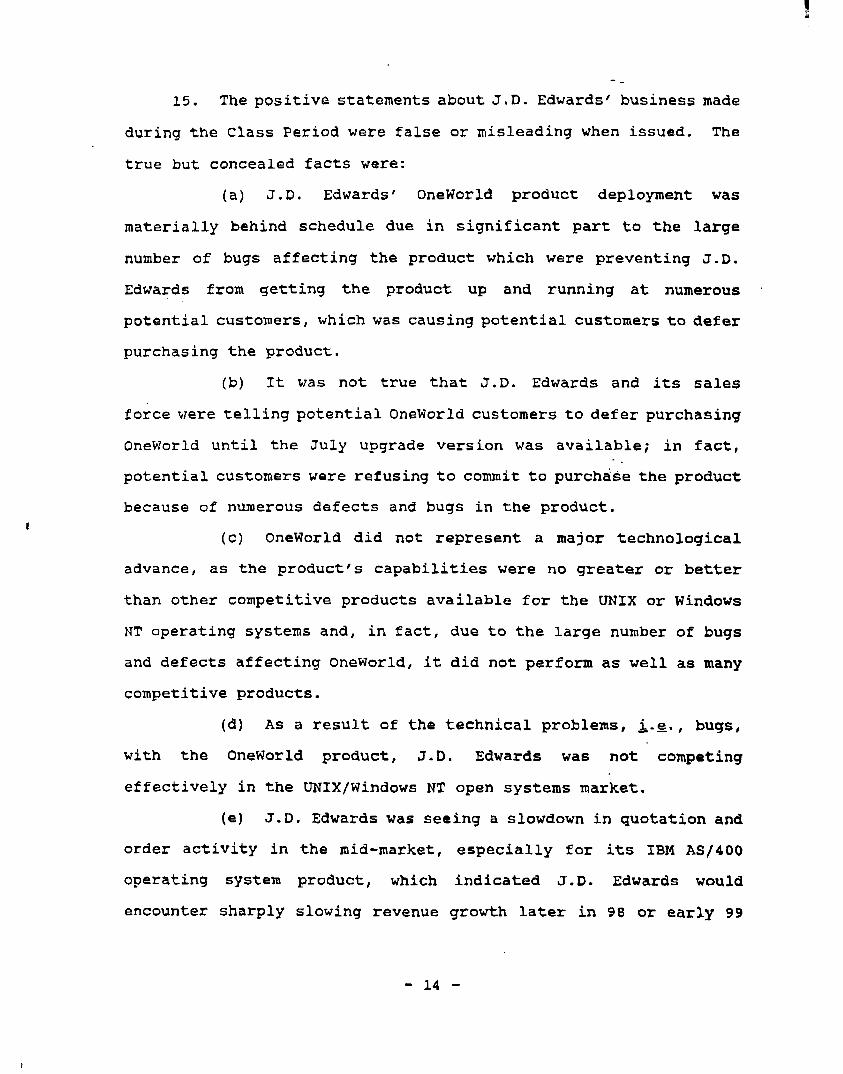

I J D Edwards & Co.

License Fee Revenue / Total Revenue

1 50% I

I i I

45%

40%

35%

30%

i dB 14%

- 13 -

- - 15. The positive statements ab0utJ.D. Edwards’ business made

during the Class Period were false or misleading when issued. The

true but concealed facts were:

(a) J.D. Edwards’ oneworld product deployment was

materially behind schedule due in significant part to the large

number of bugs affecting the product which were preventing J.D.

(b) It was not t r u e that J.D. Edwards and its sales

force were telling potential OneWorld customers to defer purchasing

Oneworld until t h e July upgrade version was available; in fact,

potential customers were refusing to commit to purchase the product

because of numerous defects and bugs in the product.

(c) OneWorld did not represent a major technological

advance, as t h e product’s capabilities were no greater or better

than other competitive products available for t h e UNIX or Windows

NT operating systems and, in f a c t , due to t h e large number of bugs

and defects affecting Oneworld, it did not perform as well as many

competitive products.

(d) As a result of the technical problems, I-e., bugs,

with the OneWorld product, J . D . Edwards was not competing

effectively in the UNIX/Windows NT open systems market.

(e) J . D . Edwards was seeing a slowdown in quotation and

order activity in the mid-market, especially for its IBM A S / 4 0 0

operating system product, which indicated J.D. Edwards would

encounter sharply slowing revenue growth later in 98 or early 99

(f) J.D. Eduards.was encountering increasing competition

in the mid-market, especially from PeopleSoft, SAP, €3- and

Oracle, which was adversely affecting J.D. Edwards’ competitive

position i n the mid-market and resulting in a slowdown in the

growth rate of its WorldSoftware product for the IBM AS/400

operating system and contributing to the slower-than-planned

deployment and acceptance of its OneWorld product for the U N I X and

windows NT operating systems.

(9) J.D. Edwards was encountering a slowdown in the

growth of its XBM A S / 4 0 0 platform due to the increasing maturity of

that platform and the increasing popularity of the UNIX and Windows

NT open system platforms f o r which J.D. Edwards did not yet have a

fully functional bug-free product.

(h) The manufacturing module of the Oneworld software

product was exceptionally bug-ridden and J.D. Edwards was having

substantial problems in getting the OneWorld product up and running

effectively in manufacturing-centric operations; this was an

especially serious problem for J.D. Edwards as historically it was

viewed as a specialist in ERP software for manufacturing and this

was one of its major markets.

(i) The B7.3.2.1 OneWorld product upgrade issued in 7/98

was rushed to market because of the continued problems with the

prior version of Oneworld, was released before necessary debugging

efforts had been completed and thus, contrary to J . D . Edwards’

claim that version B7.3.2.1 contained one-third fewer bugs than its

mature WorldSoftware .product, in fact, this upgraded version of

- 15 -

- - OneWorld contained numerous serious bugs and defects and'especially

in the manufacturing module and MRP, DRP and third party supply

chain integration functions, and w a s not fully functional.

(j) Due to bugs and other defects, the €37.3.2.1 version

of OneWorld shipped in 7/98 still lacked full functionality and, as

a result, J.D. Edwards was continuing to encounter significant

customer resistance to acceptance of this product.

(k) J. D. Edwards' ERP Software products were

encountering increased customer resistance because the products

lacked an internet portal and were not web compatible, a feature

that many potential customers were demanding due to the explosive

growth of web commerce during 97-96.

(1) J.D. Edwards' reorganization of its sAles force i n t o

llBluell (AS/400) and IVCreenV1 (non-AS/400) sales teams during 98 had

not succeeded, was resulting in diminished sales productivity and

would require a further disruptive reorganization o f J.D. Edwards'

sales force into vertical lines whereby sales personnel would focus

on customers in specific industries in specified geographic areas

which would further disrupt sales in the near ternr.

(m) As a result of t h e foregoing, the Individual

Defendants knew that J . D . Edwards' forecast of greatly increasing

software license revenue, of greatly increased OneWorld sales and

increased prof it margin were f a l s e when made as t h o s e increases

could not and would not be achieved.

(n) As a result of t h e foregoing undisclosed adverse

conditions which were negatively impacting J . D . Edwards' business,

the Individual Defendants knew that J.D. Edwards' forecasts of

16 -

- - sharply increased EPS during F99 to $.72-$.90 were false when made

as those EPS could not and would not be achieved.

(0) As a result of t h e foregoing undisclosed adverse

conditions which were negatively impacting J.D. Edwards' business,

the Individual Defendants knew that J . D . Edwards' forecasts of 30%

three- to five-year EPS growth were false when made as those EPS

could not and would not be achieved.

16. Public investors who invested based on J.D. Edwards'

representations about the successful development and launch of J.D.

Edwards' new OneWorld product, its technological superiority,

continuing strong demand for J.D. Edwards' ERP software products

and its continuing forecasts of strong license revenue and EPS

growth in F99, and thus paid as high as $49-3/8 per &hare for J.D.

Edwards' stock during the Class Period, have suffered millions in

damage. However, J . D . Edwards' insiders who knew the truth about

the continuing excessive bugs impacting Oneworld, t h e failure of

OneWorld to achieve "livel1 sites in accordance with J.D. Edwards'

plans, weakening demand and slowing orders f o r a l l of J.D. Edwards'

software products, including its A S / 4 0 0 system WorldSoftware

product, and the increasing competition in and J.D. Edwards'

impaired competitive position in the middle market, did not fare

n e a r l y so poorly. Before the startling revelations beginning on

12/3/98 occurred, and J.D. Edwards' stock price collapsed, the

Individual Defendants unloaded 3,992,183 shares of their J.D.

Edwards stock at astificiallv inflated Drices as hiah as $ 4 9 Der

s h a r e , Docketina over $151 million in illeaal insider-tradinq

proceeds, while J , D . Edwards stock was selling at artificially

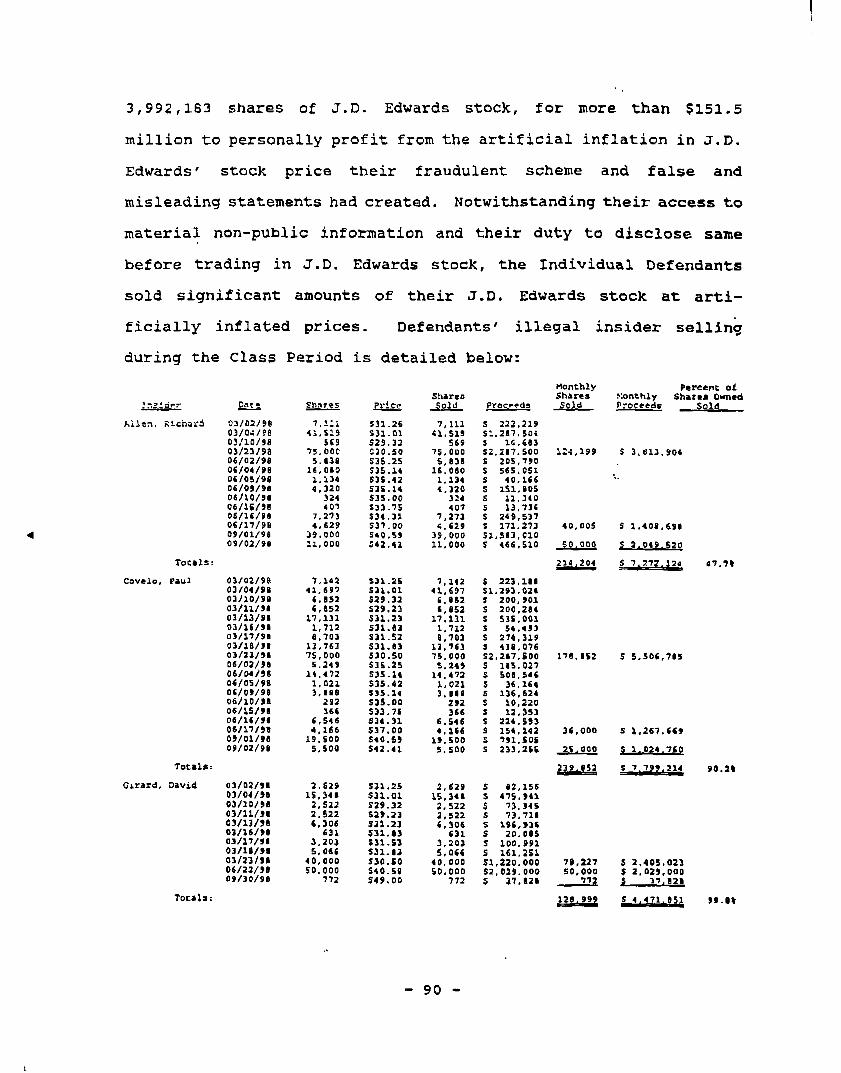

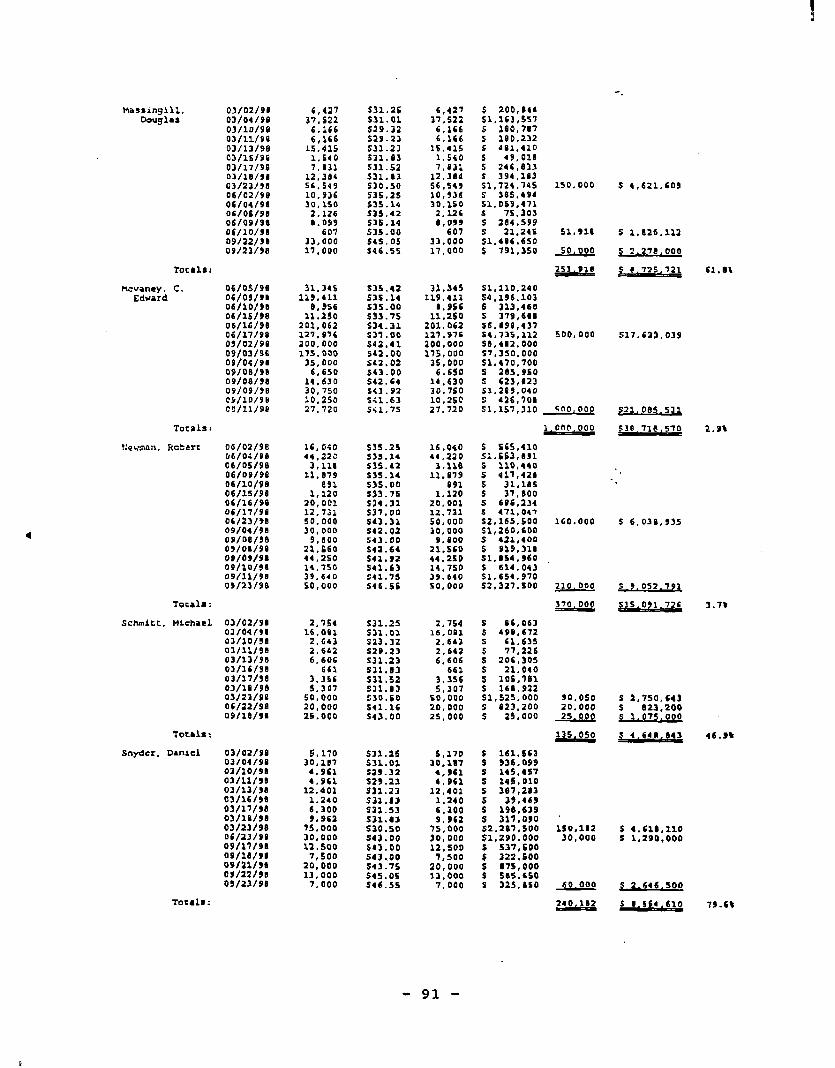

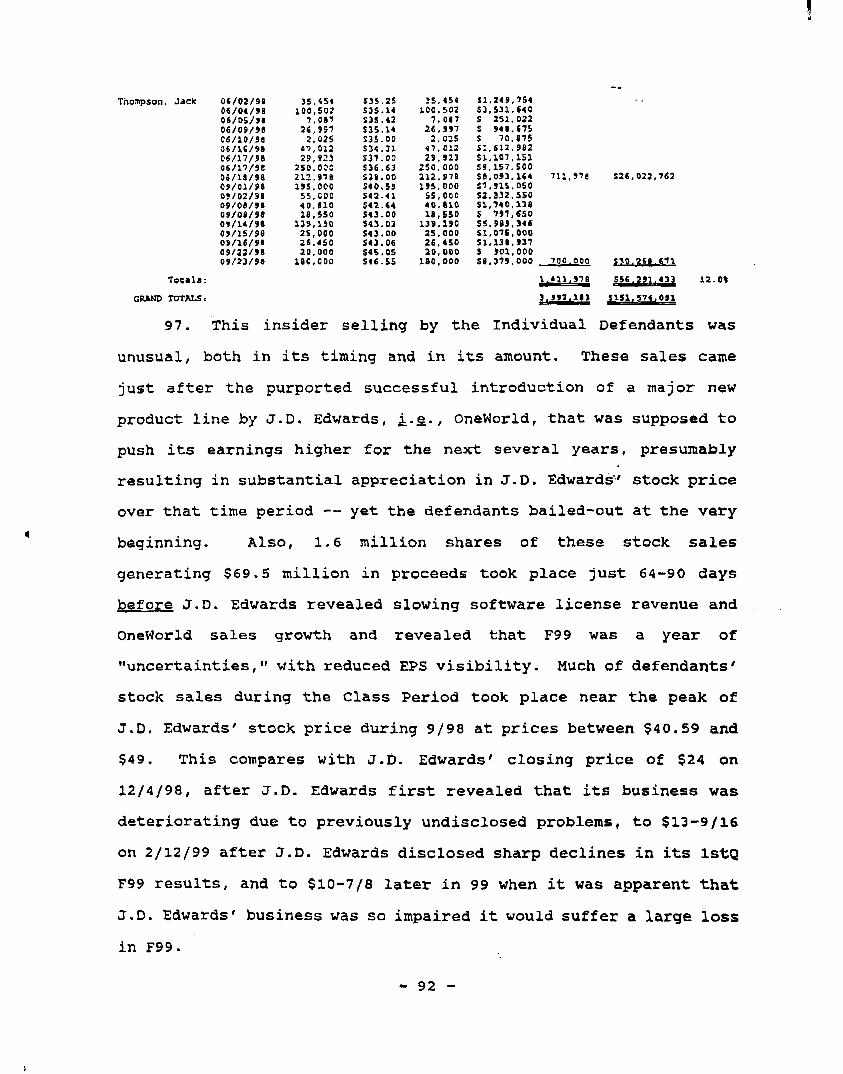

in f la ted levels. These sales are s e t forth below:

17 -

DcLendancS

Allen

Girard Covcla

13aSBinQill kcvaney N e m n Schmicc Snyder Thompson

Totsle:

Holdings at Star t of C h B 8 Period

214,586 1 , 0 5 8 1 , 0 1 6

0 3 4 , 3 0 1 . 4 9 4

9 , 0 4 3 . 5 3 0 0

1 1 . 7 3 7 . 4 3 1 1,016

Excrsased Options

During the Class Parlag

2 1 4 . 2 0 4 2 6 0 . 9 6 2

4 0 7 , 5 9 0 121,227

0 0

211 .070 3 0 0 . 7 3 7

0

Shares

239. e52 214,204

m . 9 9 9 251.928

I, 000.000 370.000 135,050 240,112

1.011.978

O-ned sold t of Sharer

47.7* Y0.2t w . e t 61. e t

2 . ¶ t 3 . 7 t

46 . 9 t 7 9 . C t 1 2 . O I - N/A

Doceeds Total

-. 3 0 . 7 1 # . 5 7 0 1 5 , 0 9 1 . 7 7 6 * 641 .143 v , ,

O.JS4.610 56.2Y1.033

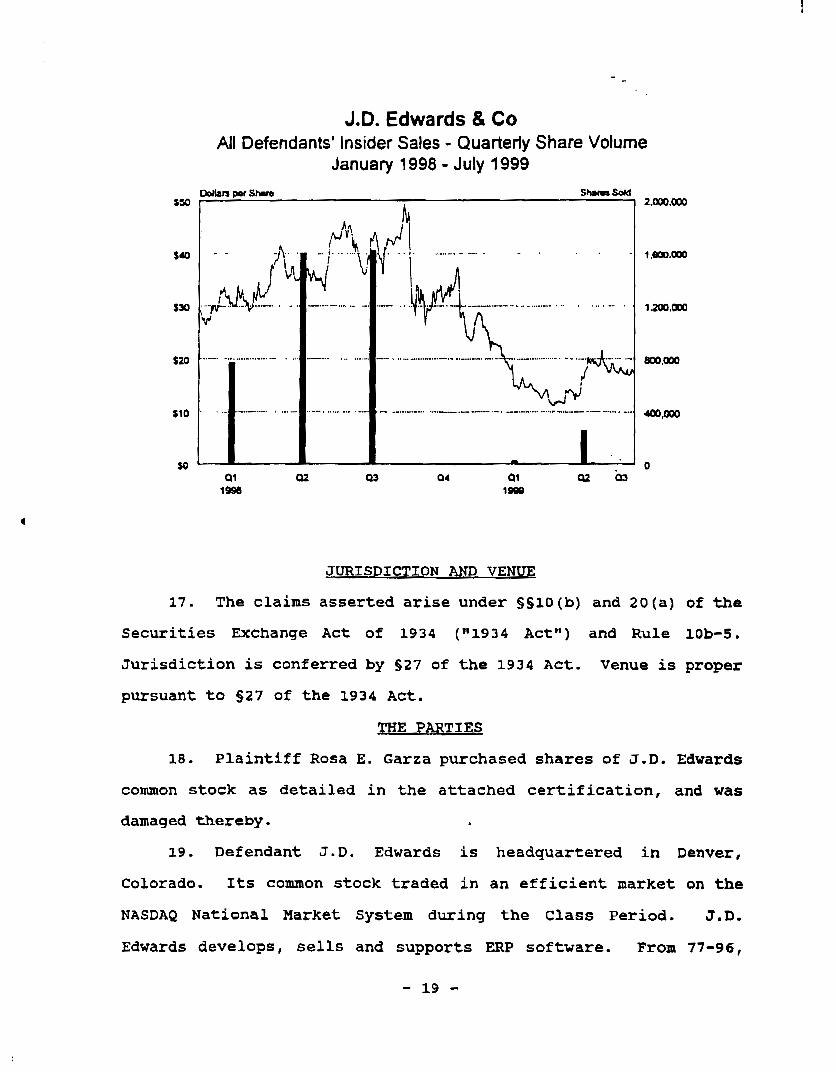

This insider s e l l i n g was unusual in t iming and amount, as the

graphs below show:

J.D. Edwards & Co All Defendants' Insider Sales - Quarterly Dollar Volume

January 1998 - July 1999

so STSMrni

- 38 -

J.D. Edwards 61 Co All Defendants' Insider Sales - Quarterly Share Volume

January 1998 - July 1999

$SO

sa

$30

520

$10

to

17.

I

\

..........................

... ........ L ._..-..

JURISDICTION-

The claims asserted arise under § S l O ( b ) and 2 0 ( a ) of the

securities Exchange Act of 1934 ("1934 A c t " ) and Rule 10b-5.

Jurisdiction is conferred by S 2 7 of the 1934 A c t . Venue is proper

pursuant to 527 of the 1934 Act.

THE PARTIES

16. Plaintiff Rosa E. Garza purchased shares o f J.D. Edwards

common stock as detailed in the attached certification, and was

damaged thereby. . 19. Defendant J .D . Edwards is headquartered in Denver,

Colorado. Its common stock traded in an efficient market on the

NASDAQ National Market System during the Class Period. J . D .

Edwards develops, sells and supports ERP software. From 77-96,

- 19 -

J . D . Edwards so ld an ERP

operated on the IBM ASj4OO

Edwards' introduced a new

product ( "WorldSoftwaretf) ' t h a t only

operating system. In late 9 6 , J.D.

ERP product, I8OneWorld, which also

operated on U N I X and Windows NT operating systems.

20. (a) Defendant C. Edward McVaney ( l1McVaneyt1) was a co-

founder of J.D. Edwards and served as President, Chief Executive

Officer and Chairman of J.D. Edwards until 11/98, when he resigned

as CEO and President, remaining as Chairman. During the Class

Period, McVaney s o l d 1,000,000 shares of h i s J . D . Edwards s tock

based on inside information, pocketing over $38.7 million in

illegal insider-trading proceeds. These sales constituted 2.9% of

the J.D. Edwards stock actually owned by McVaney.

(b) Defendant Douglas S. Massingill (llMassingillwv) was

Executive Vice President and Chief Operating Officer of J . D .

Edwards until 11/98, when he became President and CEO. During the

Class Period, Massingill sold 251,918 shares of h i s J.D. Edwards

s tock based on i n s i d e information, pocketing over $8.7 million in

illegal insider-trading proceeds. These sales constituted 61.6% of

the J.D. Edwards stock actua l ly owned by Massingill.

( c ) Defendant Richard E. Allen ( 'lAllen'l) was Vice

President-Finance and Administration, Chief Financial Officer and

a director of J . D . Edwards. Allen was in charge of J.D. Edwards'

financial statements and reports and its financial forecasts.

During the Class Period, Allen sold 2 1 4 , 2 0 4 shares of h i s J.D.

Edwards stock based on inside information, pocketing over $ 7 . 2

million in illegal insider-trading proceeds. These sales

constituted 47.7% of the J . D . Edwards stock actually owned by

Allen.

- 2 0 -

- - (d) Defendant Paul E. Covelo ("COVelo") ' was Vice

President of International Operations of J.D. Edwards and in charge

of marketing and selling J . D . Edwards' software products in that

area. During t h e Class Period, Covelo sold 239,852 shares of h i s

J.D. Edwards stock based on inside information, pocketing $ 7 . 8

million in illegal insider-trading proceeds. These sales

constituted 90.19% of the J . D . Edwards stock actually owned by

Covelo,

(e) Defendant David E. Girard (tfiGirardt') was Vice

President and General Manager of the East Area of J.D. Edwards and

in charge of marketing and selling J.D. Edwards' software products

in t h a t area. During the class Period, Girard sold 128,993 shares

of his J . D . Edwards stock based on inside information, pocketing

Over $ 4 . 4 million in illegal insider t r a d i n g proceeds. These sales

constituted 9 9 . 8 8 of the J.D. Edwards stock actually owned by

Girard.

(f) Defendant Daniel B. Snyder (ftSnyderfv) was Vice

president and General Manager of the Midwest Area of J.D. Edwards

and in charge of marketing and selling J . D . Edwards' software

products in that area. During t h e Class Period, Snyder sold

2 4 0 , 1 8 2 shares of h i s J.D. Edward6 stock based on ins ide

information, pocketing over $ 8 . 5 million in illegal insider trading

proceeds. These s a l e s constituted 79.68 of the J . D . Edwards stock

actually owned by Snyder.

(9) Defendant Michael A. Schmitt (ttSchmittff) was Vice

PresidentlGeneral Manager of European Operations until 2/13/98 and

after t h a t date was Senior Vice President, Open systems Solutions

of J . D . Edwards, and.thus in charge of OneWorld marketing and

- 21 -

- sales. During the Class Period, schmitt sold 1 3 5 , 0 5 0 shares of his

J . D . Edwards stock based on inside information, pocketing Over $ 4 . 6

million in illegal insider-trading proceeds. These sales

constituted 4 6 . 9 % of the J . D . Edwards stock actually owned by

schmitt.

(h) Defendant Robert C. Newman ( tlNewmanuu) was a co-

founder of J . D . Edwards and served as a director and member of the

Finance Committee of J . D . Edwards’ Board. During the Class Period,

Newman sold 370,000 shares of his J.D. Edwards stock based on

inside information, pocketing over $15 million in illegal insider-

trading proceeds. These sales constituted 3.7% of the J.D. Edwards

stock actually owned by Newman.

(i) Defendant Jack L. Thompson (VhompsonBt) was a Co-

founde r of J.D. Edwards and served as a director of the Company.

During the Class Period, Thompson sold 1,411,978 shares of h i s J . D .

Edwards stock based on inside information, pocketing over $ 5 6 . 2

million in illegal insider-trading proceeds. These sales

constituted 12% of the J.D. Edwards stock actually owned by

Thompson.

21. The above individuals are the llIndividual Defendants-ll

2 2 . Individual Defendants McVaney, Newman and Thompson, by

reason of their roles as co-founders of J.D. Edwards, their J.D.

Edwards stock ownership and positions with J.D. Edwards, were

controlling persons of J . D . Edwards. J . D . Edwards controlled each

of the Individual Defendants. These controlling persons are liable

under the 1934 Act S 2 0 ( a ) .

- 22 -

SCIENTER AND SCHEME ALLEGATIONS

Scheme

23. Each defendant is liable for making fa lse statements or

fo r f a i l i n g to disclose adverse facts while selling J.D. Edwards

stock and f o r participating in a scheme which operated as a fraud

or deceit on purchasers of J.D. Edwards stock.

Knowledae

2 4 . McVaney, Massingill, Allen, Covelo, Girard, Snyder and

Schmitt were the top executives of J . D . Edwards. They ran J.D.

Edwards as 18hands-on18 managers, dealing with important issues

facing J . D . Edwards’ business, i . g . , the development, commercial

introduction, performance and s a l e s of Oneworld, the continued

sales of J.D. Edwards AS/400 product, WorldSoftwake, demand and

orders for J . D . Edwards’ Oneworld and Worldsoftware products, J.D.

Edwards‘ sales and orders compared to forecasted levels, the

success of J.D. Edwards’ reorganization of its sales force into

I1Green” (non A S / 4 0 0 products) and ‘IBlueo1 (AS/400 products) teams

and J.D. Edwards‘ competitive position, especially in the vital

mid-market.

2 5 . Thompson was a co-founder of J.D. Edwards and was one of

the largest individual shareholders of J.D. Edwards. Thompson was

concerned over t h e s t a t u s of his large investment in J.D. Edwards,

was much more involved in i ts day-to-day operations than is

normally the case with an outside director and constantly monitored

J.D. Edwards‘ operations by way of conversations w i t h McVaney,

Massingill and Allen and by receiving copies of J.D. Edwards‘

operating and budget reports circulated to J.D. Edwards top

executives.

- 23 -

-

26. Newman was a co-f ounder of J. D. Edwards and was one of

4

the largest individual shareholders of J.D. Edwards. Newman was

a l so concerned over h i s large investment in J.D. Edwards and he was

much more involved in its day-to-day operations than is normally

the case with an outside director. Newman was in frequent contact

with McVaney, Massingill and Allen to get information concerning

J.D. Edwards' business and received copies O f J.D. Edwards'

internal operating and budget reports circulated to top executives.

27. Because t h e successful development and introduction of

upgraded versions of OneWorld and sharply increased sales of

Oneworld, continued strong sales of J . D . Edwards' WorldSoftware

product, increased software license revenues, the continued

successful competition by J . D . Edwards in the mid-market and the

successful reorganization of J . D . Edwards sales force were

indispensable elements to J.D. Edwards meeting its internally

budgeted and publicly disseminated F98-00 revenue and EPS

forecasts, defendants constantly monitored each of these key

factors affecting J.D. Edwards, business.

28. Because of their top executive pos i t ions with J.D.

Edwards and involvement in the day-to-day management of i t s

business, each Individual Defendant actually knew from internal

corporate documents and conversations with other corporate officers

and employees and their attendance at management and Board

meetings, and in the case of Thompson and Newman, the information

they got from McVaney, Massingill and Allen, the adverse non-public

information about J.D. Edwards' problem w i t h its OneWorld product,

impaired competitive position, weakening orders and demand for i t s

products and its deteriorating revenue and EPS prospects. Thus,

- 2 4 -

- - each Individual Defendant actually knew or was dkliberately

reckless in disregarding that the public statements about J.D.

Edwards pleaded at gf42-46, 48-50, 5 2 - 6 0 , 62-66, 69-80 and 8 3 ,

85-92 were fa lse or misleading when made.

29, By l a t e 97, the growth of J.D. Edwards' business was

completely dependent on two factors -- continued strong growth of

the IBM AS/400 market i n t o which J.D. Edwards sold its

WorldSoftware product and the successful introduction and strong

sales of its new OneWorld product f o r the UNIX/Windows NT market.

However, by l a t e 97, defendants realized from their long-term

involvement in J.D. Edwards, b u s i n e s s and exposure to the ERP

industry that the rate of growth of J.D. Edwards' IBM AS/400 market

was slowing due to t h e maturation of that operating system and Y 2 K

concerns, Defendants also knew that J.D. Edwards' new OneWorld

product was not nearly as successful as hoped, due to the bug-

filled nature of the product plus increased competition. As a

result, J. D. Edwards would not be able to achieve the F98-FOO

license sales and EPS growth being forecast.

30. Because ERP software is a "big ticket" item, often

cos t ing hundreds of thousands of dollars, J.D. Edwards had a long

sales cycle f o r its products involving a lengthy multi-month sales

solicitation, quotation and potential customer interaction period

before a customer would commit t o order this expensive product. As

a result of this lengthy s a l e s cycle process, J . D . Edwards had the

ability to accurately determine its revenues 9-12 months in advance

because it was aware of how many potential orders and sales it had

i n the q u o t a t i o n process, i.g., the pipeline, and knew from

historical trends and experience approximately what percentage of

- 2 5 -

r

- those potential orders would turn i n t o actual orders. In fact,

dur ing t h e C l a s s Per iod J.D. Edwards executives frequently stressed

to analysts and investors J.D. Edwards’ unique pipeline visibility

stretching out f o r at least nine months into t h e future as being

one factor which gave J. 0. Edwards an ability to forecast future

revenue and EPS growth with a hiah decrsee of confidence or

certainty. In other words, J.D. Edwards’ sales cycle was such that

at any given point in time its revenues for the next three to s i x

months were relatively f ixed or already in place as a result of the

maturation of previously placed sales quotations which were moving

toward or had become firm orders. Thus, by early calendar 9 8 , J . D .

Edwards insiders were aware that due to a slowdown in quotation

activity for its ERP software due to Y2K concerns:of potent ia l

customers and their reallocation of information technology

resources toward Y2K solutions and away from ERP software,

significantly increased competitive activity in mid-market from

SAP, PeoplaSoft, Oracle and Baan and t h e persistent problem J . D .

Edwards was having in getting its Oneworld software product

debugged to the p o i n t where customers were willing to commit to

purchase it, that it was very likely, if n o t certain, that later on

in calendar 9 8 , L.g., by J.D. Edwards‘ lstQ F99 beginning on

11/1/98, that J.D, Edwards would suffer a sharp slowdown in revenue

growth which would adversely impact its EPS.

31. J.D. Edwards’ main niche in the ERP software market was

the manufacturing module for its ERP software which enabled

manufacturing centric companies to monitor and effectively control

t h e i r manufacturing processes. By their na tu re , manufacturing

models are extremely complex and must be capable of being

- 26 -

4

- customized to meet widely divergent individual customer needs.

Because of this requirement, any substantial number of software

bugs in the manufacturing module will create a very serious problem

in attempting to customize t h e product to an individual customer's

specific needs, and r e s u l t in a refusal by t h e customer to purchase

the software. J.D. Edwards' OneWorld product, when originally

introduced, did n o t have a functioning manufacturing module due to

numerous bugs which affected this module. This was supposed to b'e! corrected by t h e upgraded 87.3.2.1 version to be released in 7/98.

Thus it was indispensable f o r t h e commercial success of the

upgraded version of OneWorld 87.3.2.1 t h a t it be virtually defect

free. Unfortunately, in order to hurry the product to market to

meet competitive threats, 3.D. Edwards issued the product before

its "bug smashing" program had had sufficient time to eliminate

most of the bugs from t h i s product, and as a result, efforts to

sell the upgraded Oneworld software product subsequent to 7/98 were

adversely affected by t h e large number o f continuing defects in the

product, especially those in the new manufacturing model.

32. The Individual Defendants closely monitored the

performance of J.D. Edwards' business v i a reports which J.D.

Edwards' Finance Department (under Allen) generated on a weekly and

monthly basis. There were "order reportsq1 and lfbacklog reports"

that summarized orders, dollar volume and product type, as well as

u n i t 'lshipmentl' reports. The Finance Department also distributed

monthly financial reports comparing J.D. Edwards' actual financial

results and orders to projected results and orders, i.g., backlog.

Thus, each Individual Defendant was apprised of t h e status of

orders for and sales . o f every J. D. Edwards Droduct so that they

- 27 -

- - knew where'J.D. Edwards stood in terms of the s a l e of and orders

4

for, i .g., demand f o r , i ts WorldSoftware and OneWorld products as

well as J.D. Edwards' actual final resul ts and product orders and

shipments compared to budget. Thus, the defendants were constantly

aware of the current order rate for J.D. Edwards' products and knew

that orders for its OneWorld and WorldSoftware products were weaker

than forecast, and thus that 3.D. Edwards' F99-00 software license

sales and EPS forecasts could and would not be achieved.

Motive/Omortunity

3 3 . In addition to having actual knowledge of the falsity of

their statements, each of the defendants had the motive and the

opportunity to perpetrate the fraudulent scheme and course of

business described herein.

3 4 . Defendants' fraudulent scheme was a success -- for them. The Individual Defendants sold 3,992,183 shares of their J . D .

Edwards stock during the Class Period at artificially i n f l a t e d

prices as high as $49, pocketing $151.5 million in illegal insider-

trading proceeds.

35. During 1977-1996, J . D . Edwards operated as a private

company. Until late 9 6 , J . D . Edwards' only ERP software product

was IIWorld Software, which had been on the market for many years,

but worked only on the "closed" IBM AS/400 operating system, which

was an increasingly mature operating system and was being

increasingly eclipsed by the new UNIX and Microsoft NT operating

systems, so-called "open systems, for which J . D . Edwards had no

product! This placed J.D. Edwards in an increasingly disadvantaged

competitive position, as it sharply limited the markets J.D.

Edwards could Sell to, leaving it dependent upon one product which

- 28 -

4

- operated only on an increasingly outmoded operating system. In

addition, during 9 4 - 9 6 , the portion of J . D . Edwards' total revenues

coming from service revenue, as opposed to software licensing,

increased from 55.3% of total revenue to 62.3%. Since service

revenue carried much lower profit margins than software license

fees, in 96 this resulted J.D. Edwards' net profit margins falling

to levels well below those achieved in prior years,' which

threatened J . D . Edwards' ability to continue to achieve strong

profitable growth going forward. To make m a t t e r s worse, because

the ''high" end of the ERP market was becoming increasingly

saturated, SAP, Peoplesoft, Oracle and Baan were migrating into the

mid-market and into intensified competition with J.D. Edwards.

36. These negative conditions in J . D . Edwards' business posed

a significant danger to J . D . Edwards and its top insiders. J-D.

Edwards' controlling shareholders and insiders were locked into an

illiquid and threatening situation. Since J . D . Edwards was a

p r i v a t e company, there was no trading market into which they could

sell their J . D . Edwards s h a r e s to salvage t h e i r investment.

3 7 . In order to escape from this dangerous situation,

McVaney, Thompson and Newman decided to do an 1PO of J.D. Edwards.

This would enable J . D . Edwards to raise millions of dollars,

providing capital to J.D. Edwards it could not otherwise raise, and

would permit them to s e l l off some of their J.D. Edwards shares in

the IPO at inflated prices. The IPO would create a trading market

in J. D. Edwards stock into which they and J.D. Edwards other top

insiders would be a b l e t o later sell off J.D. Edwards shares at

artificially inflated prices.

- 29 -

3 8 . In the f a l l of 9 7 , the defendants hurried to take J . D .

Edwards public as they realized that t h e risks to J.D. Edwards

business had increased materially and it was likely that due to the

adverse factors and risks pleaded herein that i n the neat future

J .D. Edwards‘ business growth would slow or even stop and t h a t J.D.

Edwards’ profitable growth would slow or even end. They hired

Morgan S tan ley , Deutsche Morgan Grenfell and Robertson Stephens to

be investment bankers for the IPO. To get the J . D . Edwards IPO,

Morgan Stanley, Deutsche Morgan Grenfell and Robertson Stephens

agreed t o h e l p support J . D . Edwards stock after t h e IPO, including

helping write and issue research reports on J.D. Edwards to help

support J . D . Edwards’ stock.

39. J.D. Edwards went public at $23 on 9 /23 /9Y in a publ ic

offering underwritten by Morgan S t a n l e y , Deutsche Morgan Grenfell

and Robertson Stephens. While J,D. Edwards stock i n i t i a l l y jumped

to over $ 4 0 immediately following t h e IPO, the stock then began a

long decline, falling back to as low a5 $24-$25 in mid-l/98. This

decline was due to other ERP software providers reporting

disappointing financial results, concern over the ability of the

ERP software market to continue i t s strong growth and concern Over

t h e market success of J . D . Edwards’ new Oneworld software Product

and thus, J . D . Edwards’ ability to achieve strong growth in license

revenue and EPS in F98-FOO.

4 0 . This decline in J . D . Edwards stock was a matter of great

concern to J . D . Edwards‘ top officers and o the r insiders. While a

few of J . D . Edwards‘ top insiders had been able t o sell some shares

o f their J.D. Edwards stock in the IPO at S23 all the other top

insiders had not been permitted t o se l l any of their stock and they

.. 30 -

- and those insiders who had been permitted to sell stock in t h e IPO

desired to se l l more s tock on the open market, However, as is

customary in IPOs , J . D . Edwards' officers and directors had been

required to agree to a fifilock-uptfi provision in connection with t h e

IPo, whereby they would not sell any' of their s t o c k on the open

market f o r at least 180 days after t h e date of the IPO, f.g., until

3 / 2 4 / 9 8 , without the prior written consent of the underwriters.

4 1 . J . D . Edwards' t o p insiders hoped that J.D. Edwards stock

would advance strongly in price after the IPO and be a t levels well

above $23 per share when t h e lock-up expired and they would first

become legally able to begin to sell off their J.D. Edwards stock

into the market. Therefore, the decline in J.D. Edwards stock

after the IPO, which took the stock back down to as low as $24-$25

in 1/98 -0 j u s t a few dollars over the IPO price -- was a matter of concern to J.D. Edwards' insiders. They realized that if they were

to maximize their own personal profits from the wave of ins ider

sales they were then planning, they would have to drive J.D.

Edwards' stock price back up much higher. Thus, beginning in late

1/98, the defendants began a concerted effort to push J.D. Edwards

s tock up higher, to artificially inflate it, to maximize their

insider-trading profits. To do this they began to falsely reassure

the market that whatever difficulties other ERP software providers

were encountering, those problems were unique to their businesses

as J . D . Edwards was not suffering similar problems, that J.D.

Edwards' recruitment of its sales force i n t o alBlueat (AS/400 sales

force) and @@Green" (non-AS/400 sales force) teams had been

SUccessful, J . D . Edwards was continuing to enjoy very s t rong demand

for its traditional software product, WorldSoftware, for the AS/400

- - platform, was achieving increasing success with the’commercial

introduction of its new Oneworld ERP software product f o r the UNIX

and windows/NT platforms and t h a t J.D. Edwards was continuing to

compete successfully in the ‘mid-market for ERP softvare and thus

was poised for and well positioned to achieve strong growth in

software license revenue which would lead to strong revenue and EPS

growth for J . D . Edwards i n F99 and FOO.

FALSE OR MISLEADING STATEMENTS

42. On 1/22/98, J.D. Edwards Chairman McVaneywas interviewed

by Bloomberq.

McVaney:

Question:

McVaney :

He stated as follows:

rTlhinas are fine. J . D . Edwards is soins m i t e well. . . . We‘re definitely uoinq throuuh p switch, that switchins over t o a areat deal Ore licensina fees and reducinu our service

FomDonent and t h a t transition is C r O i n q on now and will QO on fo r the next several Years. I . .

NOW, might that mean then, then that You might also be able to keep boosting profits, since those new customers who provide new Sources of license fees . . . therefore, it becomes a more profitable company?

YOU hit it riaht on the head. . . . [OJur operating margins now are in the 9% range and over a period o f time, meaning three or four years, we expect t h a t to shift to the 12 or 16% range, so we emect considerable irnDrovement, but that’s over a Period of time.

* * * Oneworld is what we think of as leaDfroq technoloav. that w e have clearly leaBed out ahead of the industrv and as recently as 18 months ago, J. D. Edwards was considered a technological laggard and now w e are verv much in the l e a d on these thinas, so it’s v e m imDortant.

43. On 2/23/98, subsequent to the release of its 1stQ F98

results, J.D. Edwards held a conference call f o r analysts, money

and portfolio managers, institutional investors and 'large J.D.

Edwards shareholders to discuss J . D . Edwards's lstQ results, its

business and its prospects. During the call -- and in follow-up

one on one conversations with analysts from Morgan Stanley and

Deutsche Morgan -- McVaney, Massingill or Allen stated: 0 "Rollout" and customer acceptance o f J.D. Edwards' new EFQ software product for the UNIX/Windows NT operating systems -- oneworld -- was proceeding according to plan .

e J. D. Edwards' oneworld software product represent& leapfrog technology -- a major technological advance over existing competitive products which gave J.D. Edwards a competitive advantage and positioned J.D. Edwards to succeed in the UNIX/Windows NT market.

0 J. D. Edwards' Oneworld product would lead to J.D. Edwards achieving very strong software licensing revenue growth in F99 and oneworld software sales comprising a much larger percentage of J.D. Edwards' overall software licensing revenue going forward. ..

0 The percentage of J.D. Edwards' total revenues comprised of software licensing revenues would increase dramatically in F99-FOO which would materially boost J.D. Edwards' profit margins -

J. D. Edwards' product for the IBM A S / 4 0 0 operating system -- WorldSoftware -- was continuing to enjoy very strong demand and stronger-than-anticipated sales.

Due to the continued s u c c e s s of WorldSoftware f o r the IBM A S / 4 0 0 operating system, J.D. Edwards was continuing to compete very successfully in the mid-market even against PeopleSoft, SAP, BAAN and Oracle.

J.D. Edwards was continuing to enjoy very strong demand for its software products.

J.D. Edwards' reorganization of its sales force into Blue ( A S / 4 0 0 ) and Green (non=AS/400) sales force teams had gone very well-

0 J. D. Edwards would achieve 30% EPS growth during the next three to five years .

J.D. Edwards would achieve F99 EPS Of $ a n + =

- 3 3 -

4

- 4 4 . On 2 / 2 4 / 9 8 , Morgan Stanley issued a report c on J.D.

Edwards by Phillips, which was based on and repeated information

provided in the 2/23/98 conference call and in follow-up

conversations w i t h McVaney, Allen or Massingill. The report

forecast F99 EPS of $.72, a 50% five-year EPS growth rate and the

following quarterly F99 EPS for J . D . Edwards:

22 Q1 $ .07 Q2 $ .12 43 $ .13 4 4 $ . 4 0

Year $ -72

It also stated:

OneWorld continues to gragress on schedule.

* * * we . , . continue to anticipate increasing margins .. and accelerating top line growth as OneWorld gets more seasoned. Initial feedback on the product based [on] Our discussion with early sites is positive. DesDite the exDected number of bua issues to be dealt with over time. t h e architecture a m e a r s sound . . . 45. On 2/24/98, Deutsche Morgan Grenfeli issued a report on -

J .D. Edwards by Gilbert, which was based on and repeated

information provided in the 2 / 2 3 / 9 8 conference call and in follow-

up conversations with McVaney, Allen or Massingill. The report

forecast F99 EPS of $-72 and the following quarterly F99 EPS for

J . D m Edwards :

Q1 9 9

$ 7 0 8 Q2 Q3

$ .i2 4 4

$ .15 s - 3 8

Year s - 7 2

It a l s o stated: comDlete . . I .

- 3 4 -

The availability of trained open systems implementation personnel, both internally and with partners, remains a potential capacity constraint on OneWorld revenue growth. . . Fully experienced personnel remain at a premium because field implementation experience i s critical, and the number of live installations is still only 26.

4 6 . On 3/2/98, Morgan Stanley issued a report on J.D. Edwards

by Phillips, which was based on and repeated information provided

in the recent conference call and in follow-up conversations with

McVaney, Massingill and Allen. The report forecast F99 EPS of S.72

and a 5 0 % five-year EPS growth rate for J.D. Edwards, and stated:

"OneWorld continues to uroqress on schedule. It

4 7 . So they could begin their insider bail out earlier, J.D.

Edwards insiders got the underwriters to release the'TPO "lock-upl'

of their stock early . Then, during 3/2/98-3/24/98, the J.D.

Edwards' insiders named as defendants s o l d off 771,510 shares of

J .D. Edwards stock at as high as $31.83 per share, pocketing $23 .7

million in i l l e g a l insider-trading proceeds. Other insiders also

unloaded large numbers of shares for additional illegal insider-

trading proceeds.

4 8 , On 3 / 2 0 / 9 8 , Deutsche Morgan Grenfell issued a report on

J.D. Edwards by Gilbert , written after a v i s i t to the Company and

a meeting and discussions with McVaney, Massingill and Allen, which

was based on and repeated information provided by them. McVaney,

Massingill or Allen reviewed this report before it was issued and

assured Gilbert it was accurate. The report forecast F99 EPS of

$. 72 and' the following F99 quarterly results f o r J.D. Edwards:

- 3 5 -

EPS/1999 QTR 1st: $ .oa 2nd: $ .12 3rd: $ .15 4th: $ - 3 8

Year S -72

The report also s t a t e d :

Oneworld shipments . - . the company continues to steadily increase shipments.

* * * In addition to the srowina momentum behind Oneworld,

the A S / 4 0 0 business has a Y 2 K opportunity t h a t accelerates s t a r t i n q this summer . . . . Paul Covello [ s ic ] , the senior vice pres ident of the A S / 4 0 0 div i s ion t o l d us t h a t he expects the so-called " Y 2 K bubble" to start as procrastinators begin hasty replacements this summer. I , . TTlhe companv is suite confident of its abilitv to brina implementation times down to 3 months or less dependina on the customer's umencv.

49. On 4/3/98, Deutsche Morgan Grenfell issued a report on

J.D. Edwards by Gilbert, written after a meeting and discussions

with McVaney, Massingill or Allen, which was based on and repeated

information provided by them. McVaney, Massingill or Allen

reviewed this report before it was issued and assured Gilbert it

\

was accurate. The report f o r e c a s t F99 EPS of $. 7 2 , a 3 0 % five-year

EPS growth ra te and the fallowing F99 quarterly results for J . D .

Edwards :

FPS11999

1st: $ . 0 8 2nd: $ .12 3rd: S .15 4th: S . 3 8

Year $ .72

The report also s ta ted:

* Momentum buildinq: . . . We recently caught up with JDEC management fo r an update . . . We believe .- ~ - business momentum is buildinq with the pipeline Of new business a c t i v i t y . . . .

4

* OneWorld maturing: sales constrained more bv implementation caDacitv t h a n bY number of currently live reference sites.

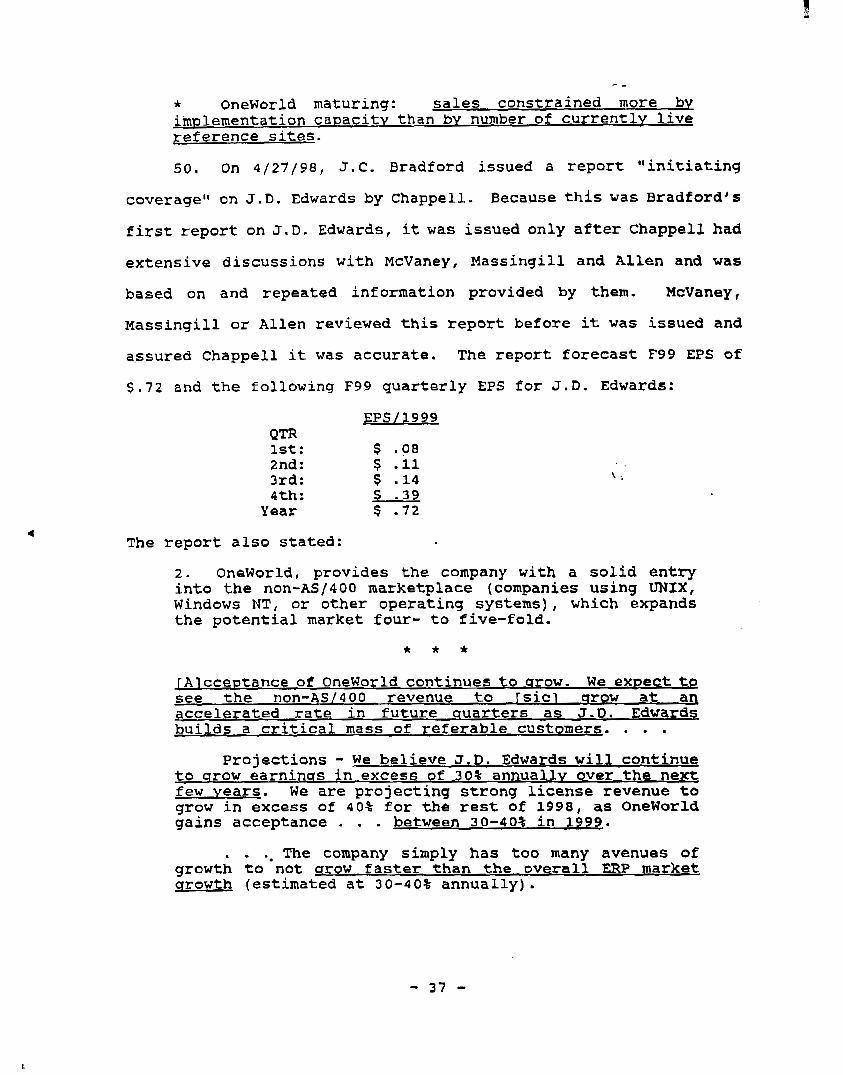

5 0 . On 4 / 2 7 / 9 8 , J . C . Bradford i s sued a report ''initiating

coverage" on J.D. Edwards by Chappell- Because this was Bradford's

first report on 5 . D. Edwards, it was issued only after Chappell had

extensive discussions with McVaney, Massingill and Allen and was

based on and repeated information provided by them. McVaney,

Massingill or Allen reviewed t h i s report before it was issued and

assured Chappell it was accurate. The report forecast F99 EPS of

$.72 and the following F99 quarterly EPS for J.D. Edwards:

EPS/1999 QTR 1st: $ . 0 8 2nd: $ .ll 3rd: $ .14 4th: s -39

Year $ .72

The r epor t also stated:

' '.

2 . Oneworld, provides the company with a solid entry into the non-AS/400 marketplace (companies using UNIX, Windows NT, or other operating systems), which expands the potential market four- to five-fold.

* * * rAlcceDtance of OneWorld con t inues to m o w . We expect to see t h e non-AS/4OO revenue to [Sic1 qrow at aq accelerated rate in future quarters as J.D. Edwards builds a critical mass of referable customers. . . .

Projections - we believe J.D. Edwards will continue to m o w earninas in excess of 304 annually over the n e x t few years. we are projecting strong license revenue to grow in excess of 4 0 % f o r the rest of 1 9 9 8 , as OneWorld gains acceptance . . . between 30-40% in 1992.

. - The company simply has too many avenues of growth to n o t arow faster than the overall ERP market arowth (estimated at 30-40% annually).

- 37 -

4

- - 51. The statements made between 1/22/98 and 4 / 2 7 / 9 6 set forth

above were false or misleading when issued. The true but concealed

facts were:

( a ) J . D . Edwards' OneWorld product deployment was

materially behind schedule due in significant part to the large

number of bugs affecting the product which were preventing J,D.

Edwards from g e t t i n g the product up and running at numerous

potential customers, which was causing potential customers to defer

purchasing the product.

(b) OneWorld did not represent a major technological

advance, as the product's capabilities were no greater or better

t h a n o t h e r competitive products available for the UNIX or Windows

KT operating systems and, in fact, due to the large 'number of bugs

and defects affecting Oneworld, it did not perform as well as many

competitive products.

(c) As a result of the technical problems, L.g., bugs,

with the OneWorld product, J . D . Edwards was not competing

effectively in t h e UNIX/Windows NT open systems market.

(d ) J.D. Edwards was seeing a slowdown in quotation and

order activity in the mid-market, e s p e c i a l l y f o r its IBM AS/400

operating system product, which indicated J.D. Edwards would

encounter sharply slowing revenue growth later in 9 8 or early 99

which would adversely impact J. D. Edwards' license revenues, profit

margins and EPS.

(e) J - D . Edwards was encountering increasing competition

in the mid-market, especially from Peoplesoft, SAP, BAAN and

Oracle, which was adversely affecting J .D. Edwards' competitive

p o s i t i o n in t h e mid-market and resulting in a slowdown in the

- 3 8 -

- *

growth rate of its Worldsoftware product f o r the 'IBM AS/400

o p e r a t i n g system and contributing to the slower-than-planned

deployment and acceptance of its OneWorld product for the UNIX and

Windows NT operating systems.

(f) J.D. Edwards was encountering a slowdown in the

growth of its IBM A S / 4 0 0 platform due to the increasing maturity of

t h a t platform and the increasing popularity of the WIX and Windows

NT open system platforms for which J.D. Edwards d i d not yet have e

fully functional bug-free product.

I

(9) The manufacturing module of the OneWorld software

product was exceptionally bug-ridden and J.D. Edwards was having

substantial problems in gettingthe Oneworld product up and running

effectively in manufacturing-centric operat ions; "this was an

especially serious problem for J . D . Edwards as historically it was

viewed as a specialist in ERP software for manufacturing and this

was one of its major markets.

(h) J.D. Edwards' reorganization of its sales force i n t o

"Blue" ( A S / 4 0 0 ) and "Green" (non-AS/400)' sales teams had not

succeeded, was resulting in diminished s a l e s productivity and would

require a further disruptive reorganization of J . D . Edwards' sa l e s

force i n t o vertical lines whereby sales personnel would focus on

customers i n specific industries in specified geographic areas

which would f u r t h e r disrupt sales in t h e near term.

(i) As a result of the foregoing, the Individual

Defendants knew that J.D. Edwards' forecast of greatly increasing

software license revenue, of greatly increased Oneworld sales and

increased profit margin were false when made as those increases

could not and would r?>t be achieved.

- 39 -

4

- (j) As a r e s u l t of t h e foregoing undisclosed adverse

conditions which were negatively impacting J .D. Edwards' business,

t h e Individual Defendants knew that J.D. Edwards' forecasts of

sharply increased EPS f o r J.D. Edwards during F99 to S .72+ were

f a l s e when made as t h o s e EPS could not and would n o t be achieved.

(k) As a result of the foregoing undisclosed adverse

conditions which were negatively impacting J . D . Edwards' business

during the Class Per iod , t h e Individual Defendants knew t h a t J.D.

Edwards' forecasts of to 30% three- to five-year EPS growth were

f a l s e when made as those EPS could not and would n o t be achieved.

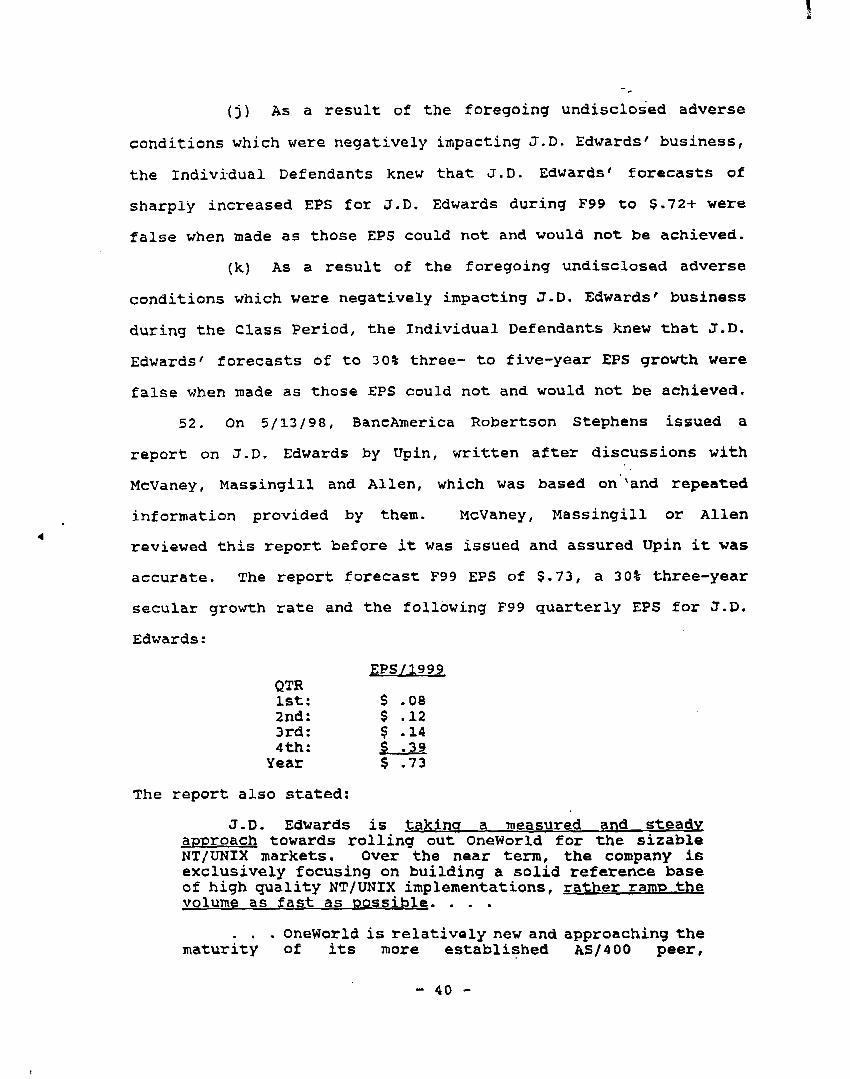

52. On 5/13/98, BancAmerica Robertson Stephens issued a

report: on J-D. Edwards by Upin, written a f t e r discussions with

McVaney, Massingill and Allen, which was based on 'and repeated

information provided by them. McVaney, Massingill or Allen

reviewed this report: before it was issued and assured Upin it was

accurate. The report forecast F99 EPS of $.73, a 30% three-year

secular growth rate and the following F99 quarterly EPS for J . D .

Edwards :

E P S / 1 9 9 9 QTR 1st: $ . 0 8 2nd: s .12 3rd: $ .14 4th: s .39

Year $ .73

The report also stated:

J.D. Edwards is takina a measured and steady approach towards rolling out OneWorld for the sizable NT/UNIX markets. Over the near term, the company is exclusively focusing on building a solid reference base of high quality NT/UNIX implementations, r a t h e r ramD the volume as fast as oossible. . . .

. . . OneWorld is relatively new and approaching t h e maturity of i ts more established AS/400 peer,

- 4 0 -

4

Worldsoftware. "Bug count" is a common product metric in the software industry -- where (the] lower the bug count, the better, Progressive "bug count" reduction is the natural life cycle outcome of sustained software development. I n order to ready OneWorld for larae scale NT/UNIX implementations. J.D. Edwards has acceleratedthe quality control Drocess over t h e past several weeks throuah a hiahlv focused "buq smashn1 Droqram -- resultinq in lower bua coun t than the traditional A S / 4 0 0 rxoduct bv one-third. . . .

The next major OneWorld release (scheduled €or July 9 8 ) represents a maior milestone in terms of a robust offering and should provide sufficient ammunition for greater field sales thrust. We believe that the NT/UNIX sales reus have been awaitinq the next Oneworld release, which contains "buq fixes" and enhanced functionality, in order to step UP their sales effort with full throttle.

customers that thev wait till the July 98 release in order to QO live.

. . . The companv has been recommendina to - , .

f * *

1. A S / 4 0 0 market growth. We believe J.D. Edwards is capable of achieving our estimates in t h i s market segment alone. Although somewhat obscured by the high prof i le uNIX and NT market segments, the A S / 4 0 0 market represents a compellina o m o r t u n i t v for J.D. Edwards . . . . J . D . Edwards is well-aositioned to capitalize w o n omor- tunities in what is estimated to be aDproximatelv a S1.4 - S1.6 billion market for vendor-developed ERP solutions.

* * * 3. The mid-tier market is a potential high growth segment moving forward . . . . 4. Major New product cycle -- J. D. Edwards has recently entered the high growth UNIX/NT market with its nev product release, OneWorld . . . . 5. Triple play on earnings upside potential -- . . . we believe t h a t significant upside potential exists over the long term to our earnings projections n o t only based on revenue growth c a t a l y s t s outlined above but also based on: margin expansion, following a snore favorable mix of higher margin software license revenues and emphasis on transferring lower margin services revenues to third party consulting and systems integration firms and expense leverage, following investments in sales and international expansion.

- 41 -

4

- 53. On 5/18/98, Deutsche Morgan Grenfell issued - a report on

J . D . Edwards by Gilbert, written after discussions with McVaney,

Massingill and Allen, which was based on and repeated information

provided by them. McVaney, Massingill or A l l e n reviewed this

report before it was issued and assured Gilbert it was accurate.

The report forecast F99 EPS of $.72, a 30% three-year EPS growth

rate and the following F99 quarterly EPS €or J . D . Edwards:

EPS/1999 QTR

2nd: $ -12 3rd: $ .15 4th: s - 3 8 Year $ .72

1st: $ . 0 8

The report a l s o stated:

5 4 . On 5 / 2 2 / 9 8 , BT Alex. Brown issued a report on J . D .

Edwards by Moore, written after discussions with McVaney,

Massingill and Allen, which was based on and repeated information

provided by them. McVaney, Massingill or Allen reviewed this

report before it was issued and assured Moore it was accurate. The

report forecast F99 EPS of $ . 7 4 , a 30% three-year EPS growth rate

and the following F99 quarterly results for J.D. Edwards:

1st: s . 0 8 2nd: $ .12 3rd: $ .15 4th: s .39

Year $ . 7 4

f

- - The report a l so stated:

-- FORECAST STRONG 30%+ EPS GROWTH OVER NEXT 3 YEARS. . . . [W]e expect J D E to generate over 30% compound annual growth over the next 3 years.

* * + JDE IS A DOMINANT FORCE IN THE MIDDLE MARKET. Most experts would agree that growth at t h e high end is slowing due t o saturation and t h a t the middle marker is becoming the "sweet spot" of t h e packaged enterprise applications market. . . . While large players such as SAP and Oracle are t ry ing to adapt their s a l e s organizations to descend into and penetrate the mid- market, J.D. Edwards is alreadv well entrenched in t h i s seament.

ONEWORLD ENHANCES THE COMPANY'S PRODUCT BREADTH AND EXPANDS ITS ADDRESSABLE MARKET TREMENDOUSLY. In CY96 the Company introduced a new product technology c a l l e d OneWorld that extended JDE's footprint to distri- buted computing environments. The Company now has a full fledged client/server solution, reassuring .existing A S / 4 0 0 users that the Company has a sound, lbns-term technolouv road ma13 and is remaining cuttina edae in terms of technoloav. . . . JDE IS ALREADY THE ACKNOWLEDGED LEADER ON THE A S j 4 O O PLATFORM.

headroom l e f t" to caDitalize on in this market. . . . JTlhe ComDanv believes it can s u s t a i n 25b+ license arowth in the A S / 4 0 0 m a c e over the next few years ,

. . . JTlhe Company still believes it has 'blentv of

* * * SALES STRUCTURE, DIRECT SALESFORCE. The Company possesses an experienced, productive sales oraanization . . . . The company began splitting its s a l e s organization by product line i n t o blue^^ (AS/400) and @'green'' (open systems) teams for the first time beginning in November 1997. . . . [T]he Company believes the transition has sone r e l a t i v e l v srnoothlv.

* * * The Company believes it possesses strong order visibility , . . . [Mlanagement is beginning to have success building a backlog of business to provide it with more visibility from quarter to quarter.

55. On 5/28/98, subsequent to the release of its 2ndQ F98

results, J.D. Edwards held a conference.cal1 for analysts , money

- 4 3 -

r - and portfolio managers, institutional investors and large J.D.

4 ...

business and its prospects. During the call -- and in follow-up conversations with analysts from Alex. Brown, Robertson Stephens,

J,C. Bradford and Deutsche Morgan -- McVaney, Allen or Massingill stated:

e "Rollout" and customer acceptance of J.D. Edwards' new ERp software product forthe UNIX/Windows NT operating systems -- OneWorld -- was proceeding according to plan. e J.D. Edwards had intentionally planned a slow rollout of its Oneworld software product and was advising customers to defer ordering the product until the upgraded 87.3.2.1 version became available in 7/98.

J.D. Edwards' Oneworld software product represented leapfrog technology -- a major technological advance over existing competitive products which gave J.D.. Edwards a competitive advantage and positioned J.D. E d w a k i i s to succeed in the UNIXjWindows NT market.

e That oneworld version B7.3.2.1 to be released in 7/98 was the result of an extensive "bug smashing@' program by J.D. Edwards and ' would contain fewer bugs than J. D. Edwards existing and mature WorldSoftware product.

e J.D. Edwards' Oneworld product was close to a major inflection point in terms o f customer acceptance and market success which would lead to J. 0. E d w a r d s achieving very strong software licensing revenue growth in F99 and Oneworld software sales comprising a much larger percentage of J.D. Edwards' overall software licensing revenue going forward.

J. D. Edwards' product for the IBM AS/400 operating system -- Worldsoftware -0 was continuing to enjoy very strong demand and stronger-than-anticipated sales.

e Due to the con t inued success of WorldSoftware f o r the IBM A S / 4 0 0 operating system and Oneworld for t h a t system as well as the UNIX and Windows NT operating systems, J . D . Edwards was continuing to compete very successfully in the mid-market, even against Peoplesoft, SAP, B M N and Oracle.

- 4 4 -

4

e J.D. Edwards was competing successfully against Peoplesoft, SAP, Oracle and BAAN especially in the mid-market.

e J.D. Edwards was continuing to enjoy very s t rong demand for all of its software products in the mid-market.

0 J.D. Edwards was not seeing any overall slowdown in its business or softening i n demand or drop-off in orders of its products .

0 Due to the long sale cycles associated with its s a l e of ERP software, J . D . Edwards possessed unusually good order, revenue and EPS visibility extending out at least nine months in the future which enabled it to forecast future orders, revenues and EPS with great confidence and accuracy.

e J.D. Edwards' reorganization of its sales force into Blue (AS/400) and Green (non-AS/400) sales force teams had gone very well.

e J . D . Edwards would achieve 30% EPS growth during the next three to five years.

0 J.D. Edwards would achieve F99 EPS of $.75-$ .78 . ..

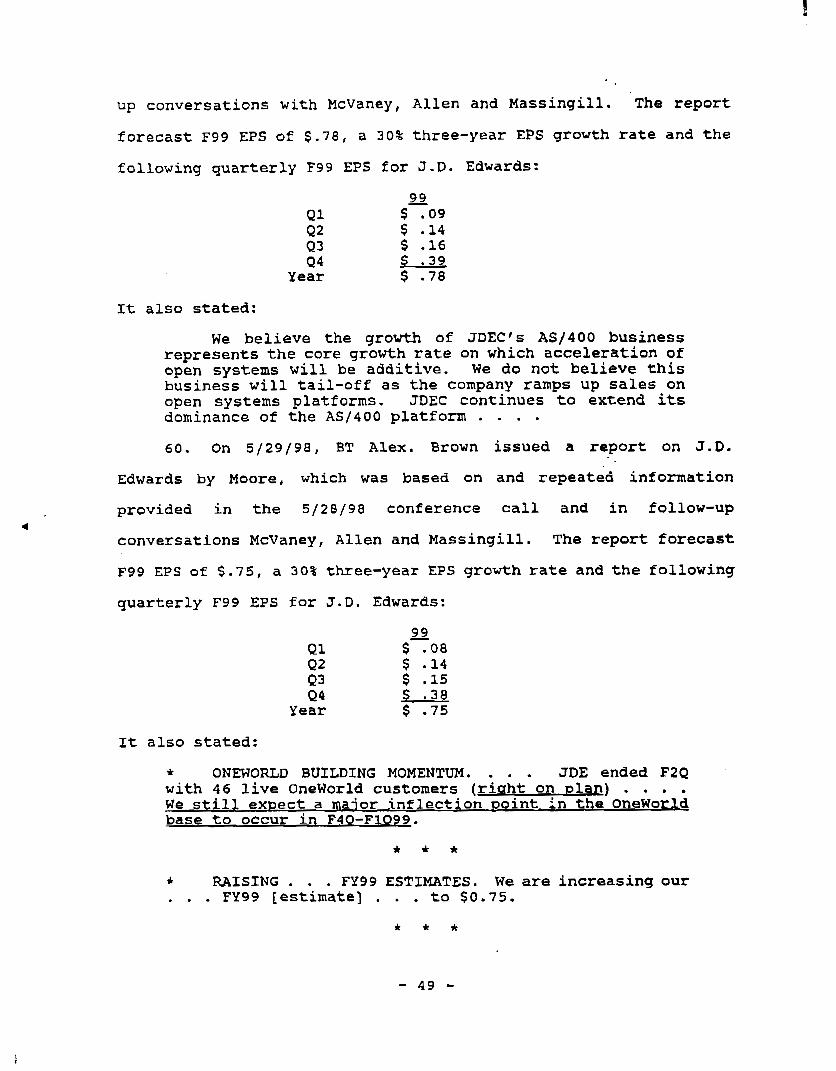

56. On 5 / 2 8 / 9 8 , ET Alex. Brown issued a report on J . D .

Edwards by Moore, which was based on and repeated information

provided in the 5/28/98 conference call and in follow-up

conversations with McVaney, Allen and Massingill. The report

forecast F99 EPS of $ . 7 5 , a 30% three-year EPS growth rate and the

following quarterly F99 EPS for J . D . Edwards:

99 Q1 $ T O 8 42 $ -14 Q3 $ .15 Q4 S . 3 8

Year s .75