Embed Size (px)

Citation preview

Makai Marine Advisors LLC

Product Tanker Outlook

6th Chemical and Product Tankers Conference

London, 11-12 March 2014

Jeff McGee

Makai Marine Advisors

2Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

Topics for discussion

• Macro & Demand Outlook

• Refining Developments

• Product Trade

• Product Tanker Supply

• Freight & Asset Price Outlook

• Conclusions

3Makai Marine Advisors LLC March 2014

Macroeconomic & Oil Demand Outlook

4Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

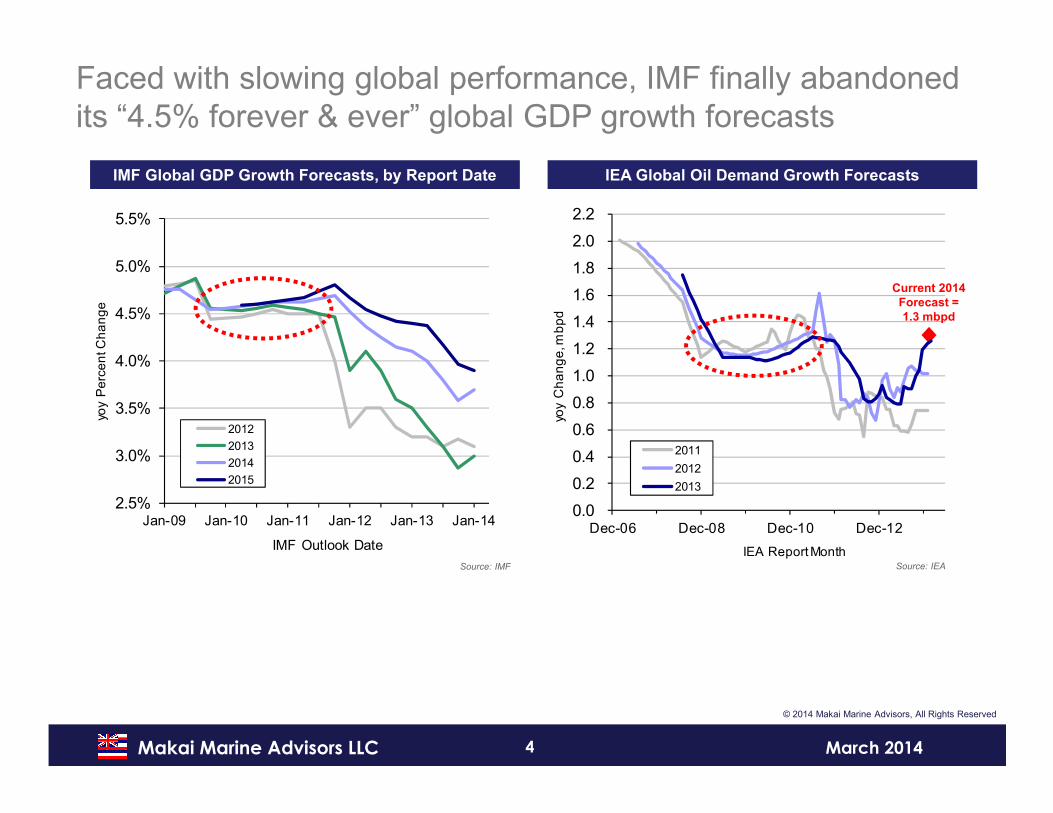

Faced with slowing global performance, IMF finally abandoned its “4.5% forever & ever” global GDP growth forecasts

IMF Global GDP Growth Forecasts, by Report Date IEA Global Oil Demand Growth Forecasts

Source: IMF Source: IEA

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

yoy

Pe

rce

nt C

ha

ng

e

IMF Outlook Date

2012

2013

2014

2015

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Dec-06 Dec-08 Dec-10 Dec-12

yoy

Ch

an

ge

, mb

pd

IEA Report Month

2011

2012

2013

Current 2014

Forecast =

1.3 mbpd

5Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

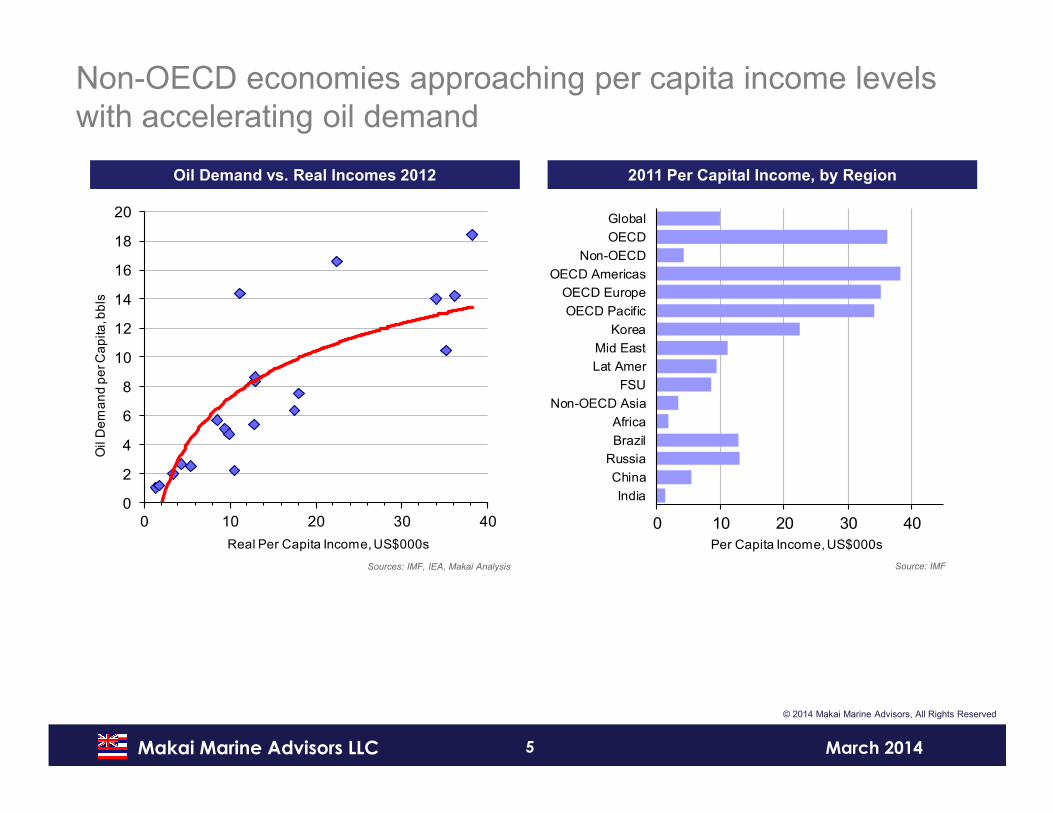

Non-OECD economies approaching per capita income levels with accelerating oil demand

Oil Demand vs. Real Incomes 2012 2011 Per Capital Income, by Region

Sources: IMF, IEA, Makai Analysis Source: IMF

0

2

4

6

8

10

12

14

16

18

20

0 10 20 30 40

Oil

De

ma

nd

pe

r Ca

pita

, bb

ls

Real Per Capita Income, US$000s

0 10 20 30 40

India

China

Russia

Brazil

Africa

Non-OECD Asia

FSU

Lat Amer

Mid East

Korea

OECD Pacific

OECD Europe

OECD Americas

Non-OECD

OECD

Global

Per Capita Income, US$000s

6Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

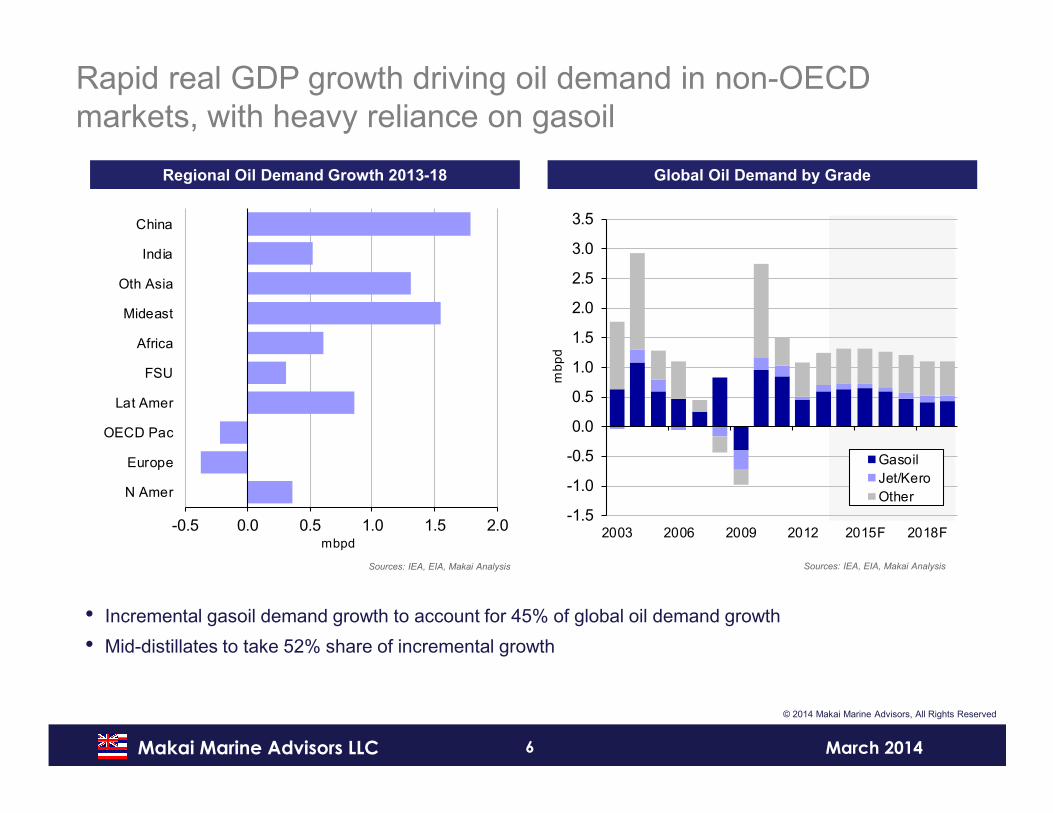

Rapid real GDP growth driving oil demand in non-OECD markets, with heavy reliance on gasoil

Regional Oil Demand Growth 2013-18 Global Oil Demand by Grade

Sources: IEA, EIA, Makai Analysis Sources: IEA, EIA, Makai Analysis

• Incremental gasoil demand growth to account for 45% of global oil demand growth

• Mid-distillates to take 52% share of incremental growth

-0.5 0.0 0.5 1.0 1.5 2.0

N Amer

Europe

OECD Pac

Lat Amer

FSU

Africa

Mideast

Oth Asia

India

China

mbpd

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2003 2006 2009 2012 2015F 2018F

mb

pd

Gasoil

Jet/Kero

Other

7Makai Marine Advisors LLC March 2014

Refining Developments

8Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2003 2007 2011 2015F 2019F

yoy

Ch

an

ge

, mb

pd

Atl Basin Other Asia

China Mideast

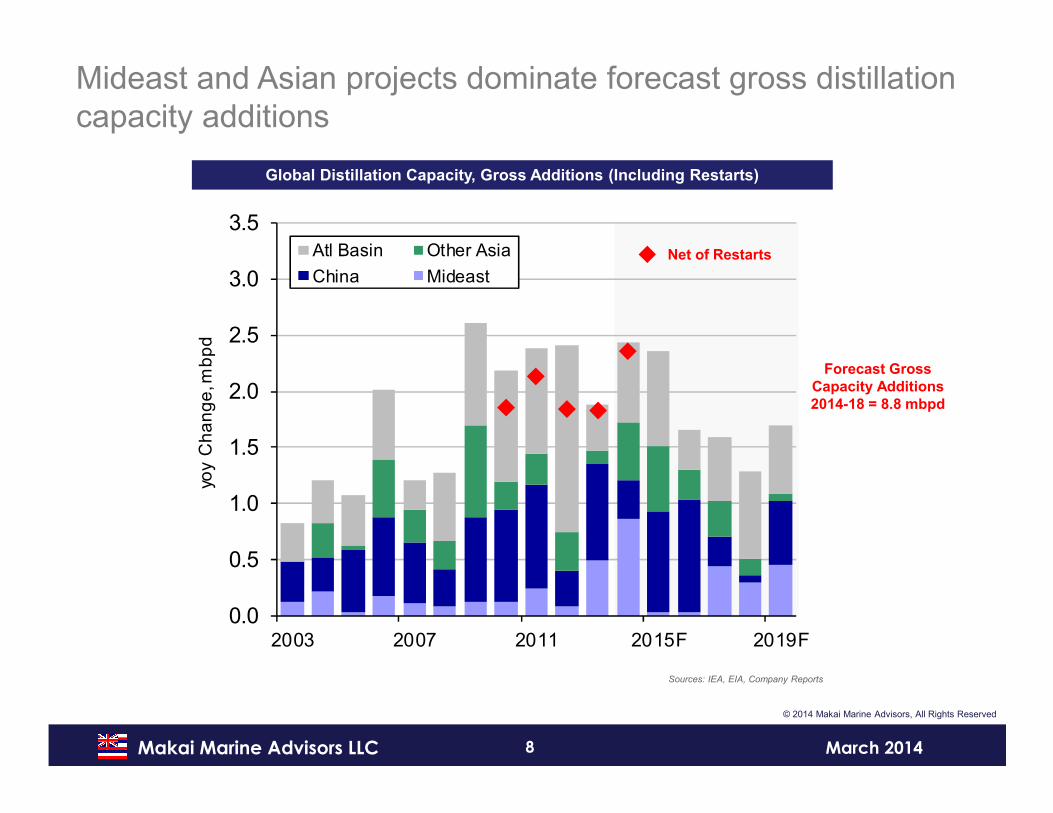

Mideast and Asian projects dominate forecast gross distillation capacity additions

Global Distillation Capacity, Gross Additions (Including Restarts)

Sources: IEA, EIA, Company Reports

Forecast Gross

Capacity Additions

2014-18 = 8.8 mbpd

Net of Restarts

9Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

0.0

0.5

1.0

1.5

2.0

2.5

2002 2006 2010 2014F 2018F

mb

pd

AsiaOth EuropeLat AmerEU-15US/Canada

0.0

0.5

1.0

1.5

2.0

2.5

2003 2007 2011 2015F 2019F

yoy

Ch

an

ge

, mb

pd

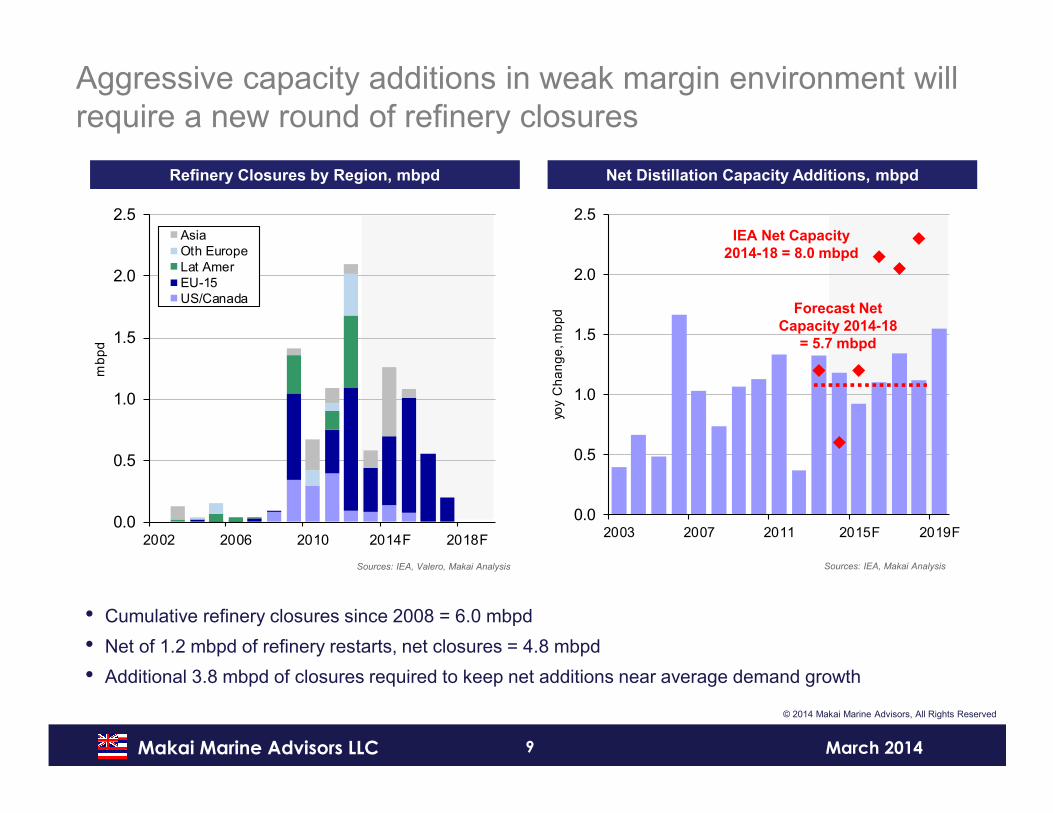

Aggressive capacity additions in weak margin environment will require a new round of refinery closures

Refinery Closures by Region, mbpd Net Distillation Capacity Additions, mbpd

Sources: IEA, Valero, Makai Analysis Sources: IEA, Makai Analysis

• Cumulative refinery closures since 2008 = 6.0 mbpd

• Net of 1.2 mbpd of refinery restarts, net closures = 4.8 mbpd

• Additional 3.8 mbpd of closures required to keep net additions near average demand growth

Forecast Net

Capacity 2014-18

= 5.7 mbpd

IEA Net Capacity

2014-18 = 8.0 mbpd

10Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2006 2009 2012 2015F 2018F

mb

pd

Atl Basin

OECD Pac

China

Oth Asia

AG

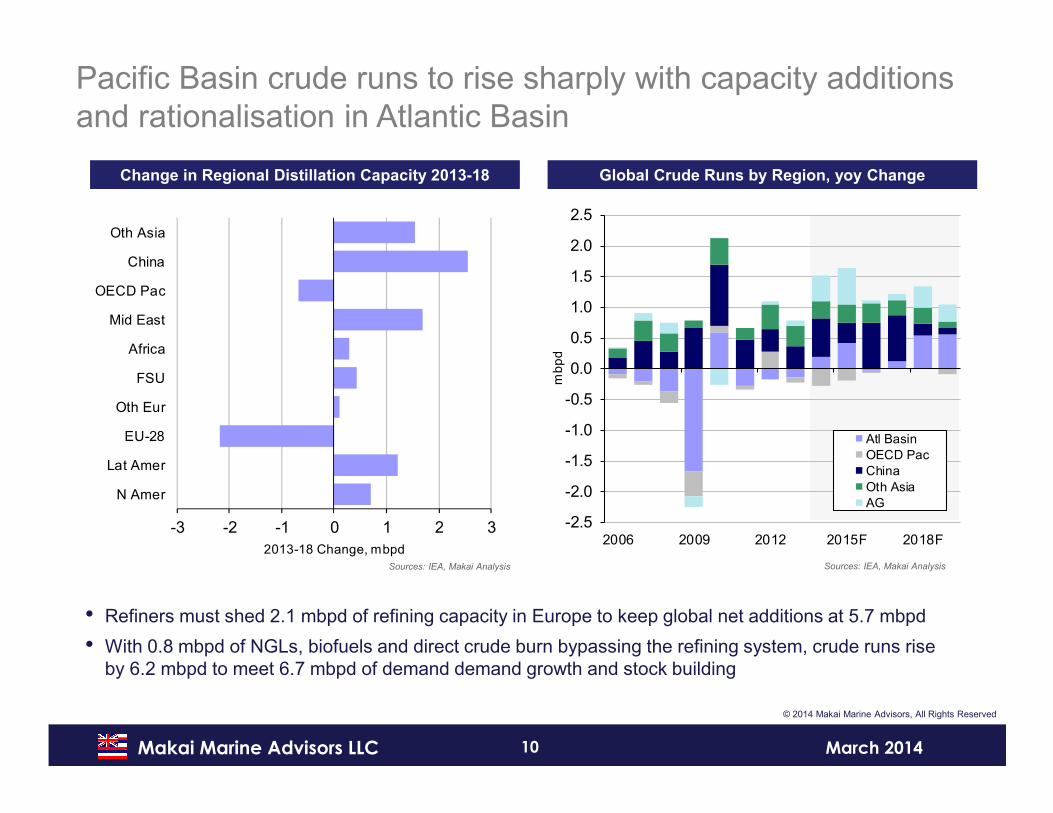

Pacific Basin crude runs to rise sharply with capacity additions and rationalisation in Atlantic Basin

Change in Regional Distillation Capacity 2013-18 Global Crude Runs by Region, yoy Change

Sources: IEA, Makai Analysis Sources: IEA, Makai Analysis

-3 -2 -1 0 1 2 3

N Amer

Lat Amer

EU-28

Oth Eur

FSU

Africa

Mid East

OECD Pac

China

Oth Asia

2013-18 Change, mbpd

• Refiners must shed 2.1 mbpd of refining capacity in Europe to keep global net additions at 5.7 mbpd

• With 0.8 mbpd of NGLs, biofuels and direct crude burn bypassing the refining system, crude runs rise by 6.2 mbpd to meet 6.7 mbpd of demand demand growth and stock building

11Makai Marine Advisors LLC March 2014

US Refining

12Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

-400

-200

0

200

400

600

800

1,000

1,200

2004 2008 2012 2016F 2020F

kbpd

Tight Oil

GoM

Alaska

Other US

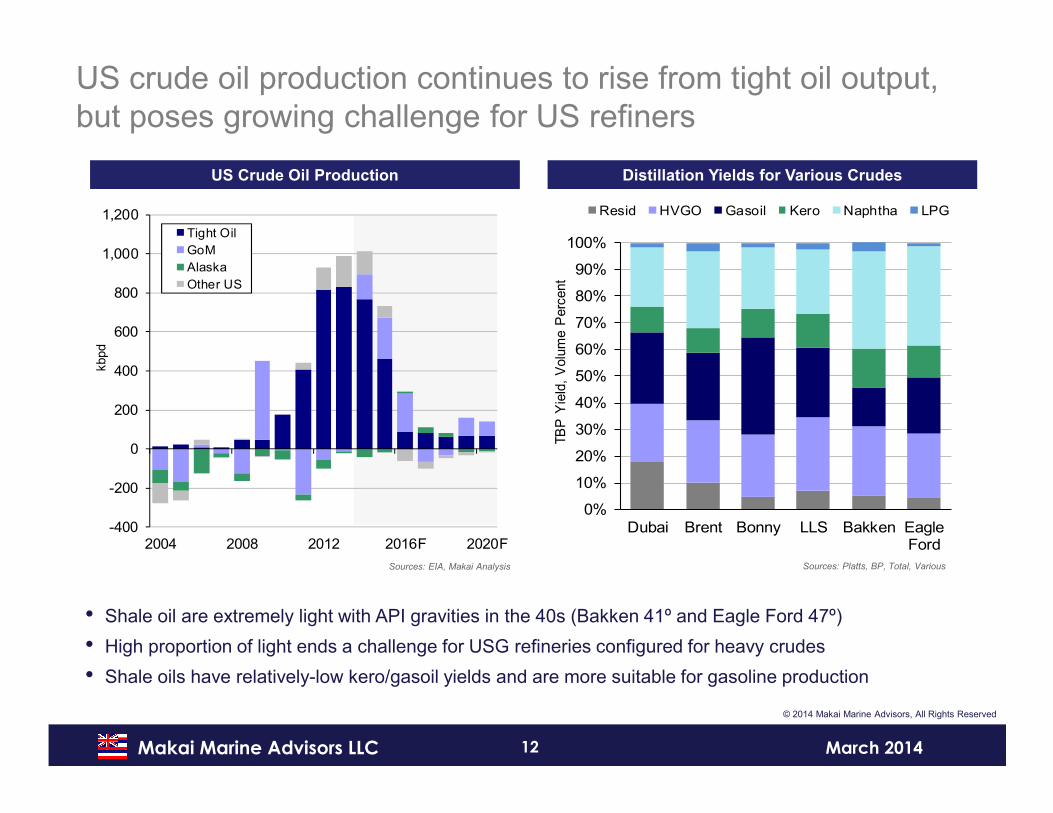

US crude oil production continues to rise from tight oil output, but poses growing challenge for US refiners

US Crude Oil Production Distillation Yields for Various Crudes

Sources: EIA, Makai Analysis Sources: Platts, BP, Total, Various

• Shale oil are extremely light with API gravities in the 40s (Bakken 41º and Eagle Ford 47º)

• High proportion of light ends a challenge for USG refineries configured for heavy crudes

• Shale oils have relatively-low kero/gasoil yields and are more suitable for gasoline production

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dubai Brent Bonny LLS Bakken EagleFord

TB

P Y

ield

, V

olu

me P

erc

ent

Resid HVGO Gasoil Kero Naphtha LPG

13Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

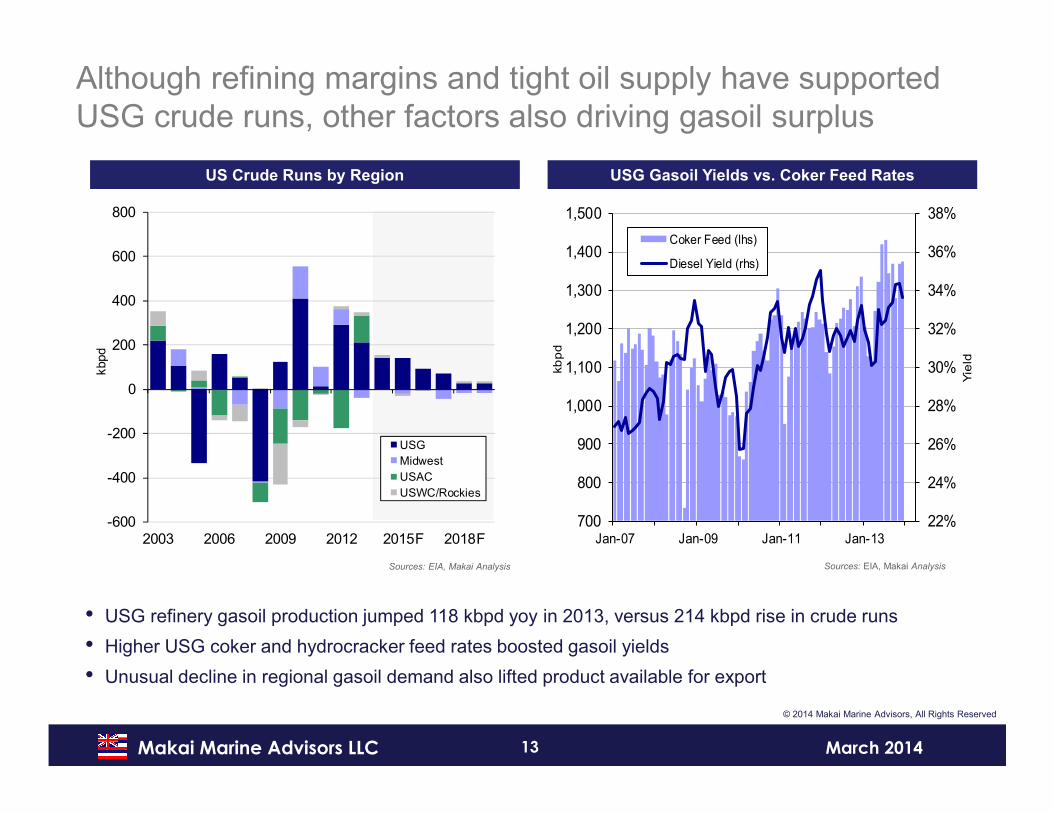

-600

-400

-200

0

200

400

600

800

2003 2006 2009 2012 2015F 2018F

kbpd

USG

Midwest

USAC

USWC/Rockies

US Crude Runs by Region USG Gasoil Yields vs. Coker Feed Rates

Sources: EIA, Makai Analysis Sources: EIA, Makai Analysis

• USG refinery gasoil production jumped 118 kbpd yoy in 2013, versus 214 kbpd rise in crude runs

• Higher USG coker and hydrocracker feed rates boosted gasoil yields

• Unusual decline in regional gasoil demand also lifted product available for export

22%

24%

26%

28%

30%

32%

34%

36%

38%

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

Jan-07 Jan-09 Jan-11 Jan-13

Yie

ld

kb

pd

Coker Feed (lhs)

Diesel Yield (rhs)

Although refining margins and tight oil supply have supported USG crude runs, other factors also driving gasoil surplus

14Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

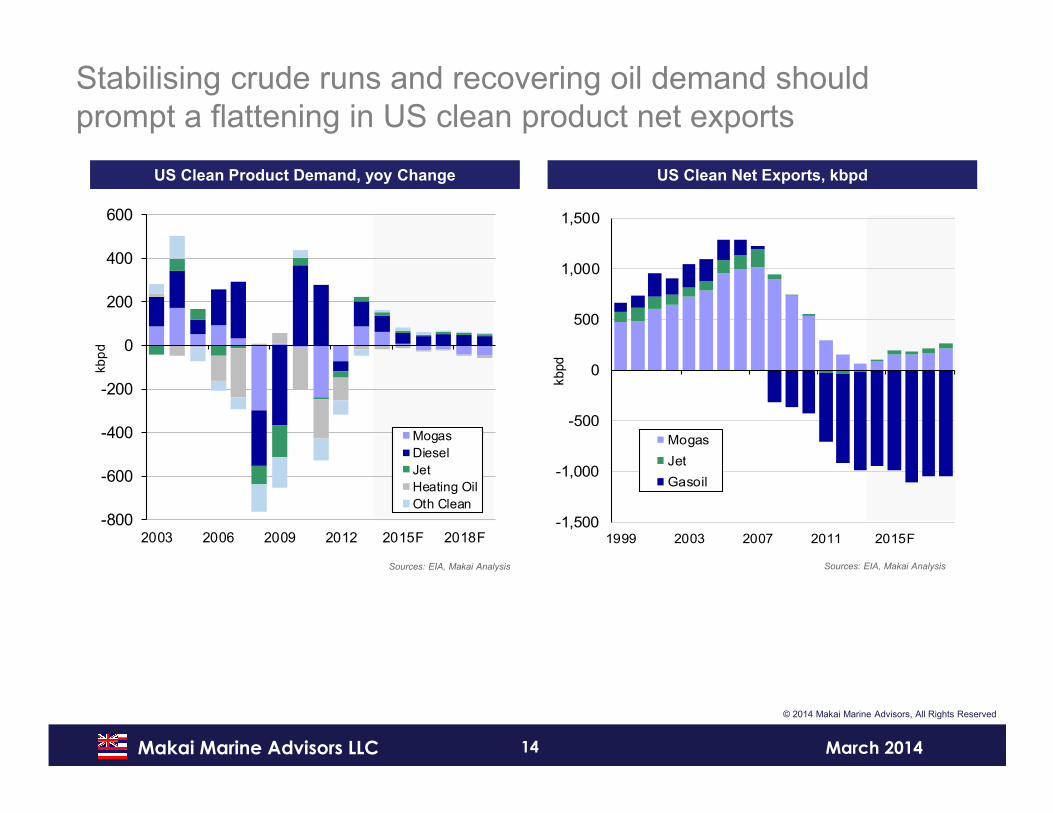

-800

-600

-400

-200

0

200

400

600

2003 2006 2009 2012 2015F 2018F

kb

pd

Mogas

Diesel

Jet

Heating Oil

Oth Clean

-1,500

-1,000

-500

0

500

1,000

1,500

1999 2003 2007 2011 2015F

kbpd

Mogas

Jet

Gasoil

Stabilising crude runs and recovering oil demand should prompt a flattening in US clean product net exports

US Clean Product Demand, yoy Change US Clean Net Exports, kbpd

Sources: EIA, Makai Analysis Sources: EIA, Makai Analysis

15Makai Marine Advisors LLC March 2014

Product Trade

16Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

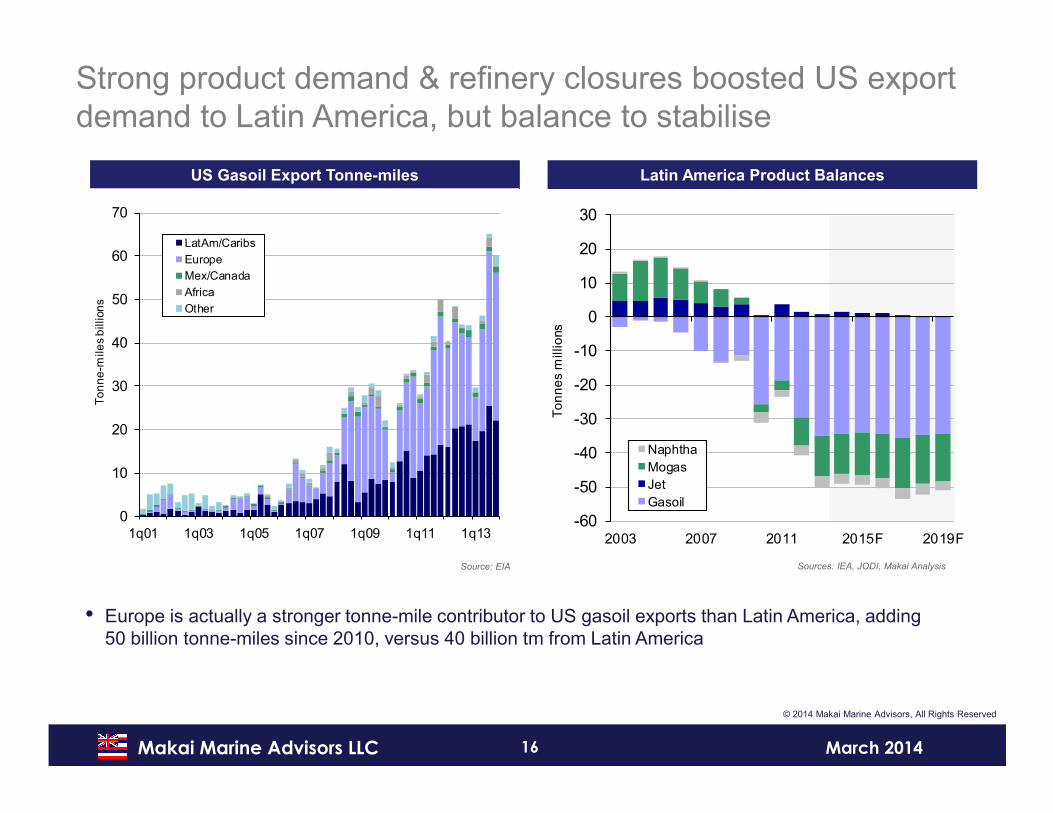

Strong product demand & refinery closures boosted US export demand to Latin America, but balance to stabilise

US Gasoil Export Tonne-miles Latin America Product Balances

Source: EIA Sources: IEA, JODI, Makai Analysis

• Europe is actually a stronger tonne-mile contributor to US gasoil exports than Latin America, adding 50 billion tonne-miles since 2010, versus 40 billion tm from Latin America

0

10

20

30

40

50

60

70

1q01 1q03 1q05 1q07 1q09 1q11 1q13

To

nn

e-m

ile

s b

illio

ns

LatAm/Caribs

Europe

Mex/Canada

Africa

Other

-60

-50

-40

-30

-20

-10

0

10

20

30

2003 2007 2011 2015F 2019F

To

nn

es

millio

ns

Naphtha

Mogas

Jet

Gasoil

17Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

0

10

20

30

40

50

60

70

2003 2007 2011 2015F 2019F

To

nn

es

millio

ns

Jet

Gasoil

Weak

Strong

-50

0

50

100

150

200

250

2003 2007 2011 2015F 2019F

yoy

Ch

an

ge

, kb

pd

Mogas Jet/Kero Gasoil

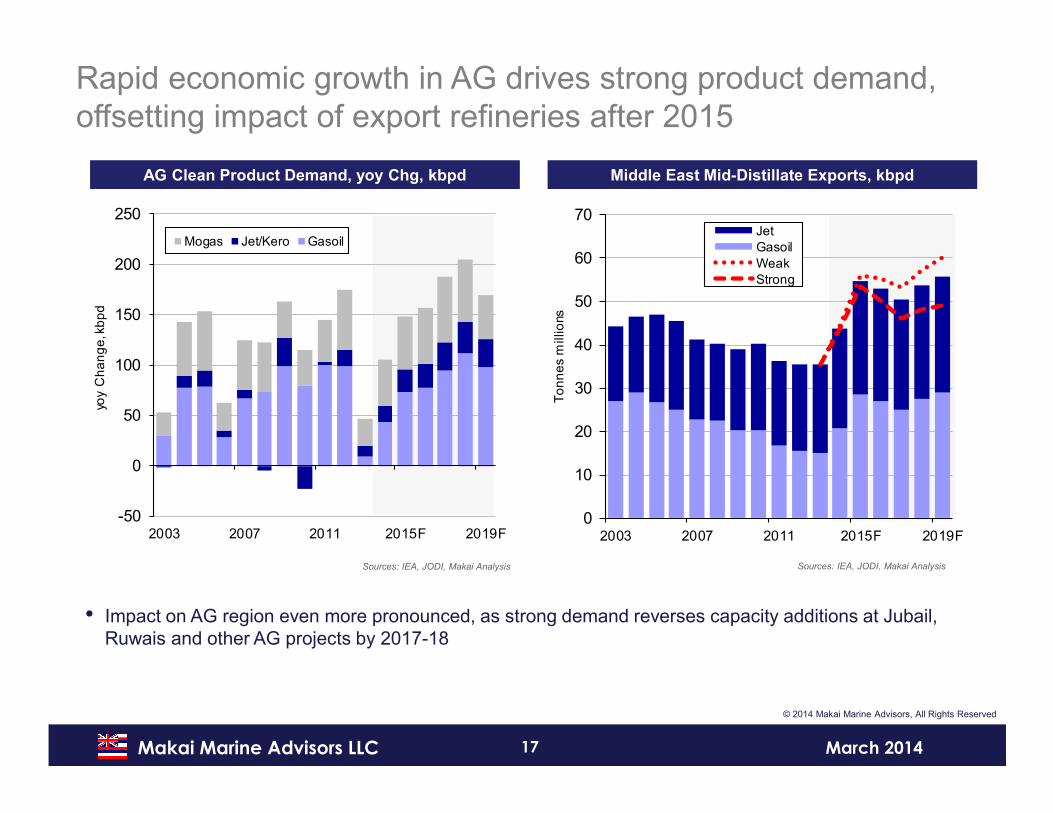

Rapid economic growth in AG drives strong product demand, offsetting impact of export refineries after 2015

AG Clean Product Demand, yoy Chg, kbpd Middle East Mid-Distillate Exports, kbpd

Sources: IEA, JODI, Makai Analysis Sources: IEA, JODI, Makai Analysis

• Impact on AG region even more pronounced, as strong demand reverses capacity additions at Jubail, Ruwais and other AG projects by 2017-18

18Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

-30

-20

-10

0

10

20

30

40

50

60

70

2003 2006 2009 2012 2015F 2018F

To

nn

es

millio

ns

N Amer FSU

Mideast India

-100

-80

-60

-40

-20

0

20

2003 2006 2009 2012 2015F 2018F

To

nn

es

millio

ns

Europe

Africa

Lat Amer

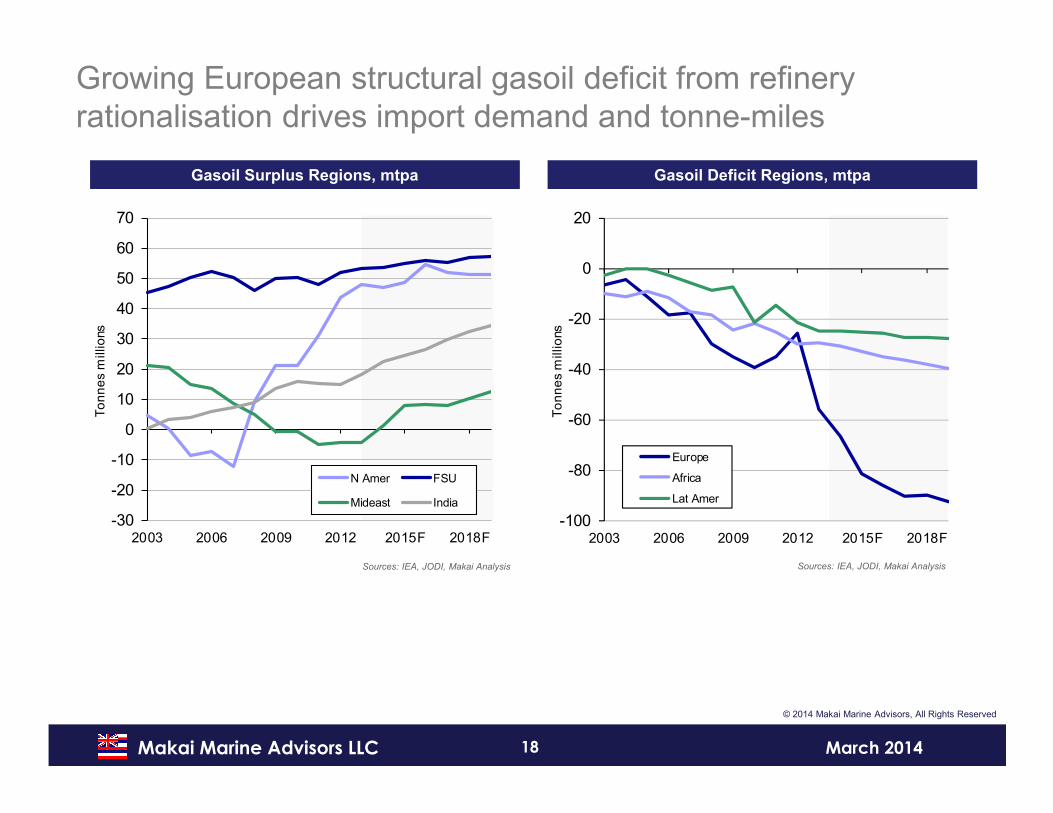

Growing European structural gasoil deficit from refinery rationalisation drives import demand and tonne-miles

Gasoil Surplus Regions, mtpa Gasoil Deficit Regions, mtpa

Sources: IEA, JODI, Makai Analysis Sources: IEA, JODI, Makai Analysis

19Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1999 2003 2007 2011 2015F 2019F

mb

pd

-10%

-5%

0%

5%

10%

15%

20%

1999 2003 2007 2011 2015F 2019F

yoy

Pe

rce

nt C

ha

ng

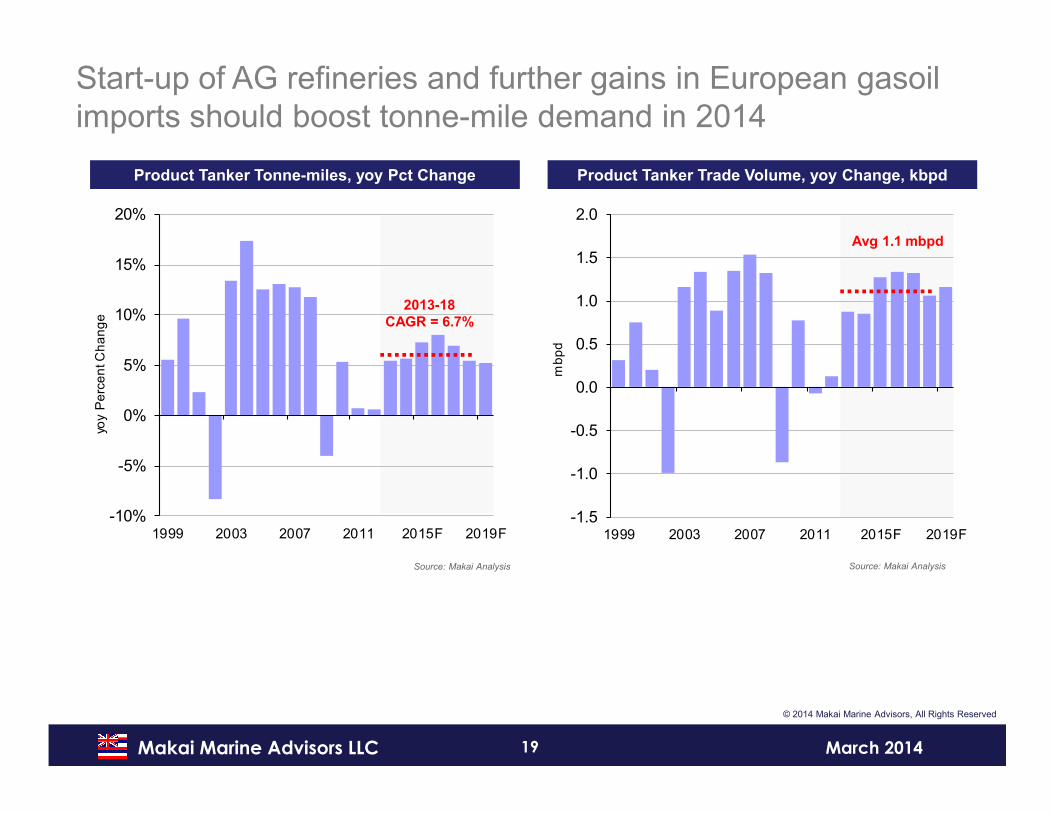

eStart-up of AG refineries and further gains in European gasoil imports should boost tonne-mile demand in 2014

Product Tanker Tonne-miles, yoy Pct Change Product Tanker Trade Volume, yoy Change, kbpd

Source: Makai Analysis Source: Makai Analysis

2013-18

CAGR = 6.7%

Avg 1.1 mbpd

20Makai Marine Advisors LLC March 2014

Product Tanker Supply

21Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

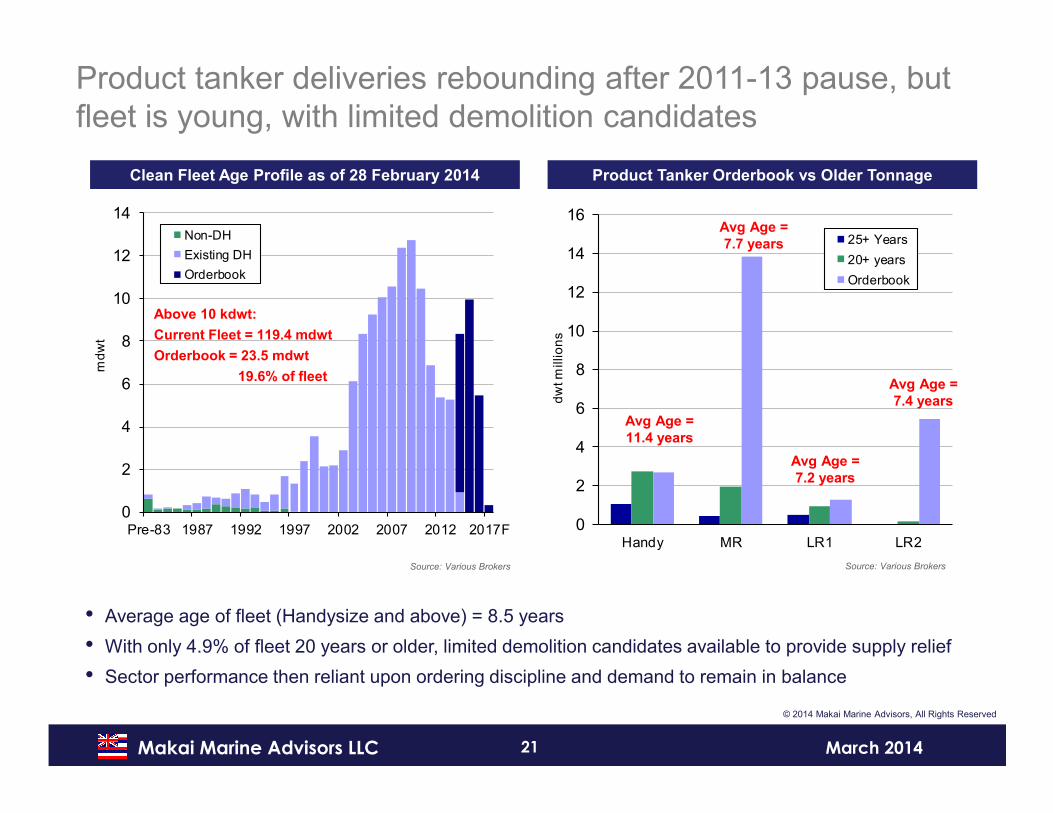

Product tanker deliveries rebounding after 2011-13 pause, but fleet is young, with limited demolition candidates

Clean Fleet Age Profile as of 28 February 2014 Product Tanker Orderbook vs Older Tonnage

Source: Various Brokers Source: Various Brokers

• Average age of fleet (Handysize and above) = 8.5 years

• With only 4.9% of fleet 20 years or older, limited demolition candidates available to provide supply relief

• Sector performance then reliant upon ordering discipline and demand to remain in balance

0

2

4

6

8

10

12

14

16

Handy MR LR1 LR2d

wt m

illio

ns

25+ Years

20+ years

Orderbook

0

2

4

6

8

10

12

14

Pre-83 1987 1992 1997 2002 2007 2012 2017F

md

wt

Non-DH

Existing DH

Orderbook

Above 10 kdwt:

Current Fleet = 119.4 mdwt

Orderbook = 23.5 mdwt

19.6% of fleet

Avg Age =

11.4 years

Avg Age =

7.7 years

Avg Age =

7.2 years

Avg Age =

7.4 years

22Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

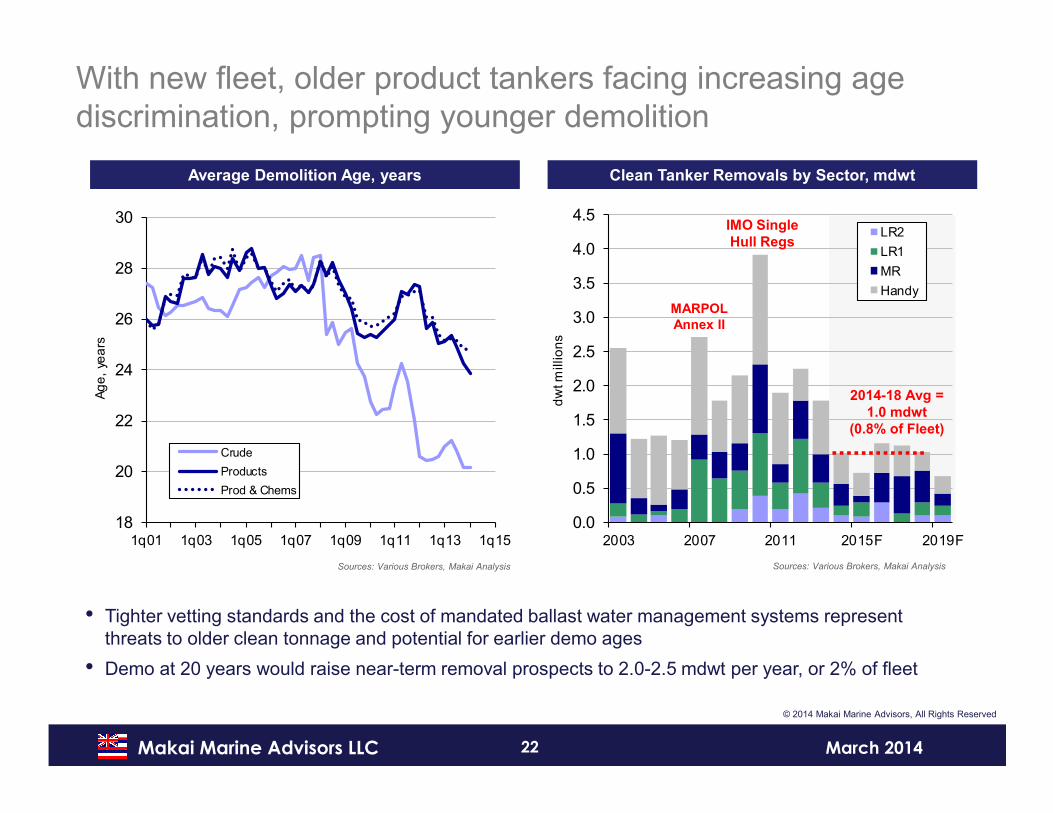

With new fleet, older product tankers facing increasing age discrimination, prompting younger demolition

Average Demolition Age, years Clean Tanker Removals by Sector, mdwt

Sources: Various Brokers, Makai Analysis Sources: Various Brokers, Makai Analysis

• Tighter vetting standards and the cost of mandated ballast water management systems represent threats to older clean tonnage and potential for earlier demo ages

• Demo at 20 years would raise near-term removal prospects to 2.0-2.5 mdwt per year, or 2% of fleet

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2003 2007 2011 2015F 2019Fd

wt m

illio

ns

LR2

LR1

MR

Handy

18

20

22

24

26

28

30

1q01 1q03 1q05 1q07 1q09 1q11 1q13 1q15

Ag

e,

yea

rs

Crude

Products

Prod & Chems

2014-18 Avg =

1.0 mdwt

(0.8% of Fleet)

MARPOL

Annex II

IMO Single

Hull Regs

23Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

0

5

10

15

20

25

30

35

40

0%

1%

2%

3%

4%

5%

6%

7%

8%

1q08 1q10 1q12 1q14F 1q16F

Re

al W

td S

po

t E

arn

ing

s, U

S$

00

0s/d

ay

Ord

eri

ng

, Pe

rce

nt o

f F

lee

t

Ordering (lhs)

Avg Earnings (rhs)

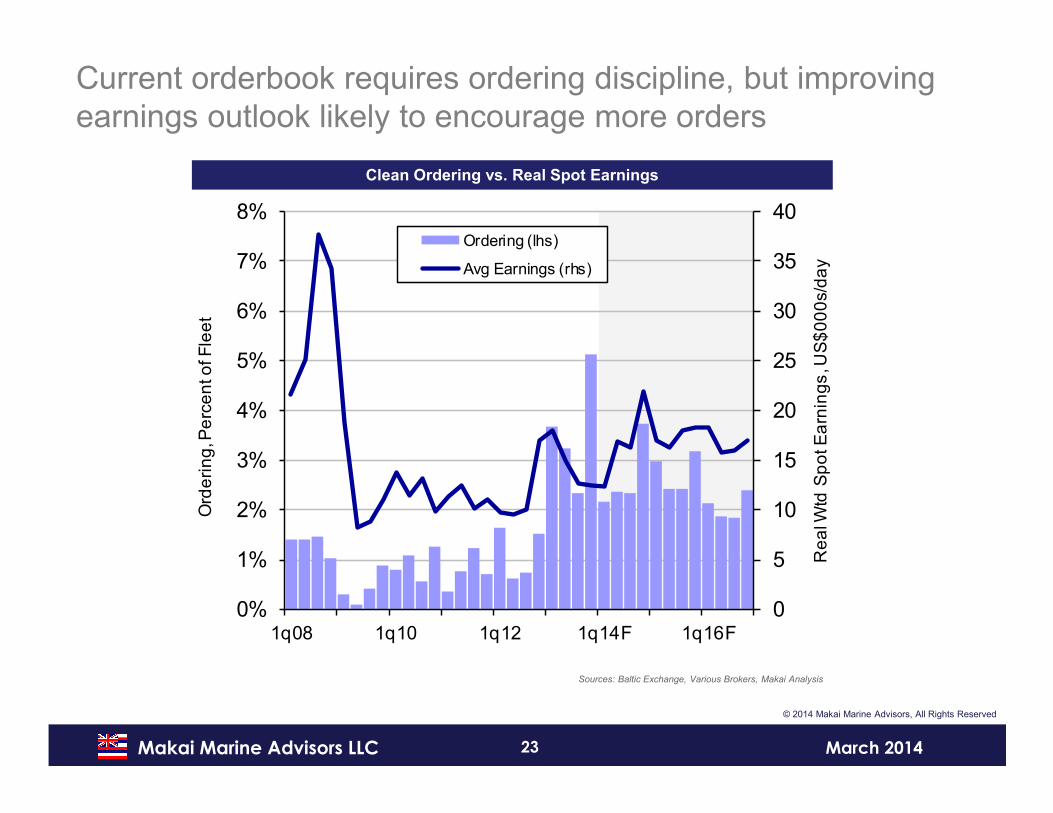

Current orderbook requires ordering discipline, but improving earnings outlook likely to encourage more orders

Clean Ordering vs. Real Spot Earnings

Sources: Baltic Exchange, Various Brokers, Makai Analysis

24Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

0%

2%

4%

6%

8%

10%

12%

14%

16%

1998 2003 2008 2013F 2018Fyo

y P

erc

en

t Ch

an

ge

0%

5%

10%

15%

20%

25%

30%

35%

0

5

10

15

20

25

30

35

2005 2008 2011 2014F 2017F 2020F

Pe

rce

nt o

f F

lee

t

dw

t m

illio

ns

LR2 LR1MR HandyPct of Fleet (rhs)

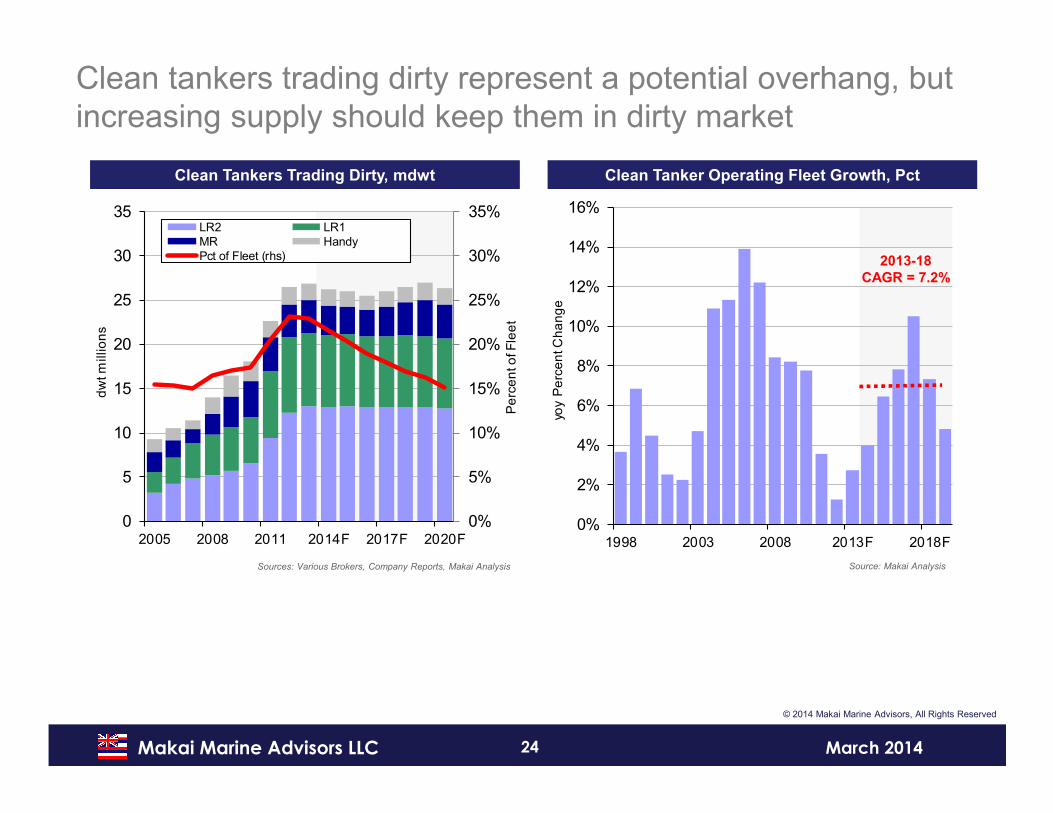

Clean tankers trading dirty represent a potential overhang, but increasing supply should keep them in dirty market

Clean Tankers Trading Dirty, mdwt Clean Tanker Operating Fleet Growth, Pct

Sources: Various Brokers, Company Reports, Makai Analysis Source: Makai Analysis

2013-18

CAGR = 7.2%

25Makai Marine Advisors LLC March 2014

Freight & Asset Price Outlook

26Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

0

5

10

15

20

25

30

1999 2004 2009 2014F 2019F

Ind

exe

d N

om

ina

l US

$0

00

s/d

ay

78%

80%

82%

84%

86%

88%

90%

92%

94%

1999 2004 2009 2014F 2019F

Utilis

atio

n R

ate

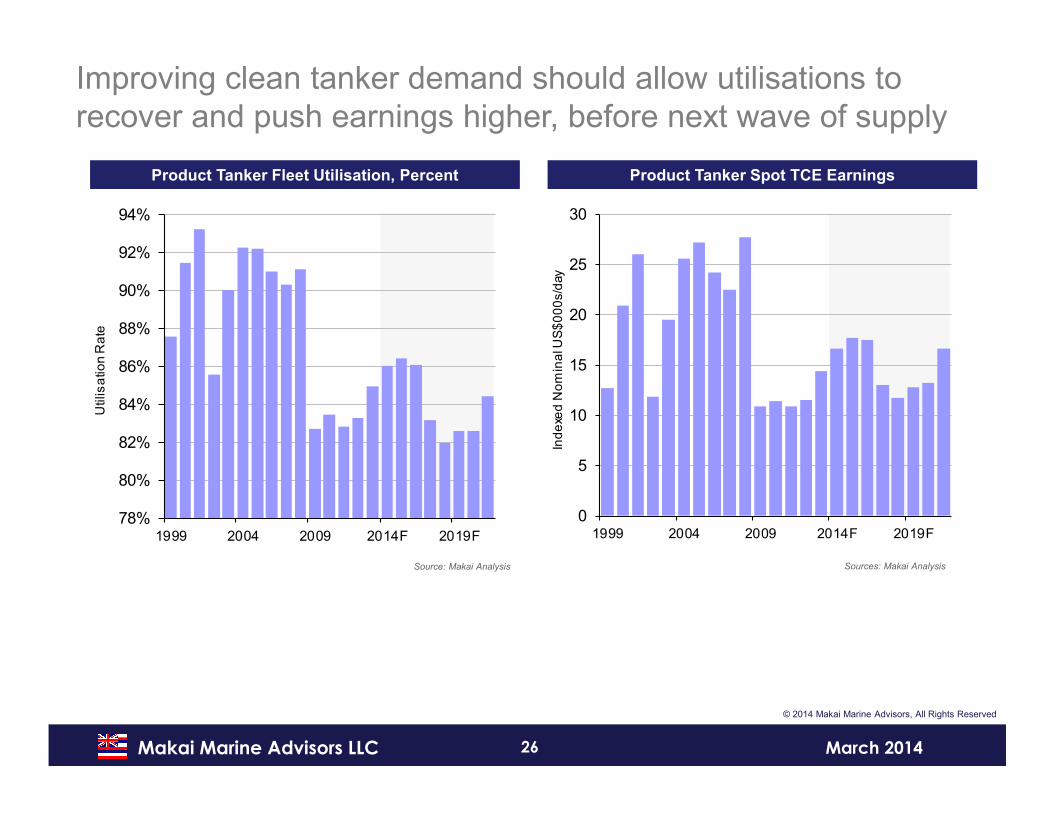

Improving clean tanker demand should allow utilisations to recover and push earnings higher, before next wave of supply

Product Tanker Fleet Utilisation, Percent Product Tanker Spot TCE Earnings

Source: Makai Analysis Sources: Makai Analysis

27Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

1q09 1q11 1q13 1q15F 1q17F 1q19F

No

min

al 1

2-m

o T

C R

ate

s, U

S$

00

s/d

ay

LR2

LR1

MR

Handy

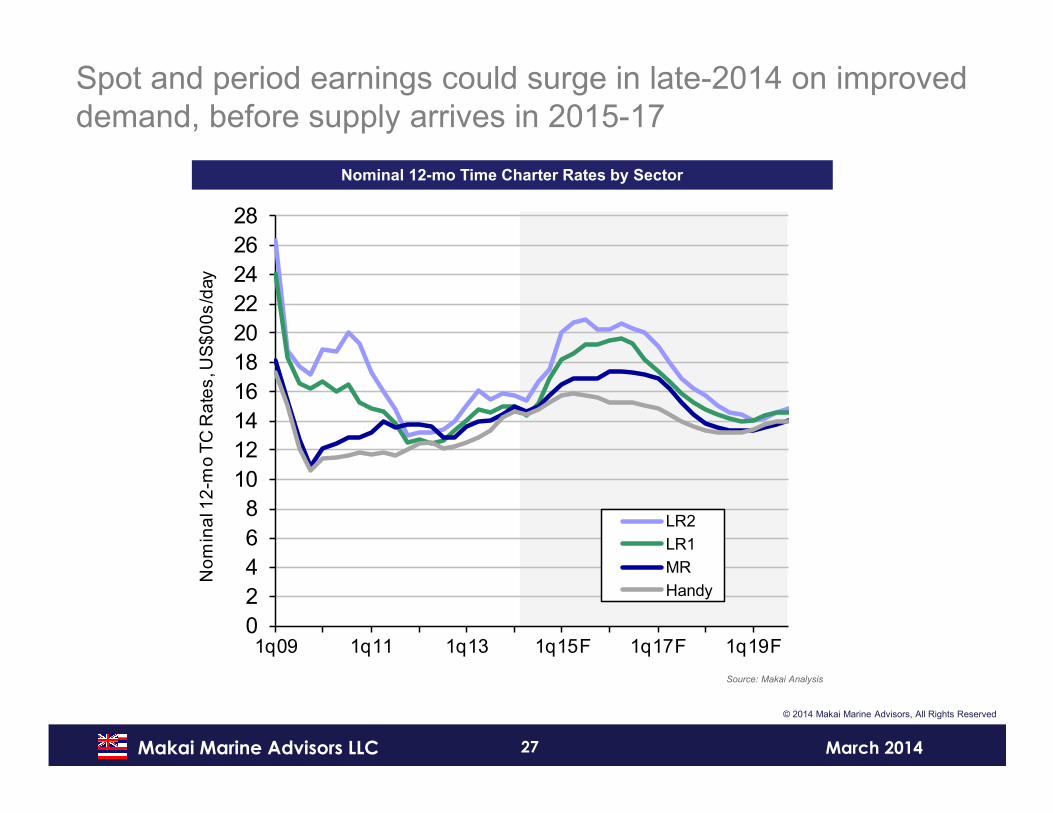

Spot and period earnings could surge in late-2014 on improved demand, before supply arrives in 2015-17

Nominal 12-mo Time Charter Rates by Sector

Source: Makai Analysis

28Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

0

10

20

30

40

50

60

1q09 1q11 1q13 1q15F 1q17F 1q19F

No

min

al 5

-yr V

es

se

l Pri

ce

s, U

S$

million

s

LR2

LR1

MR

Handy

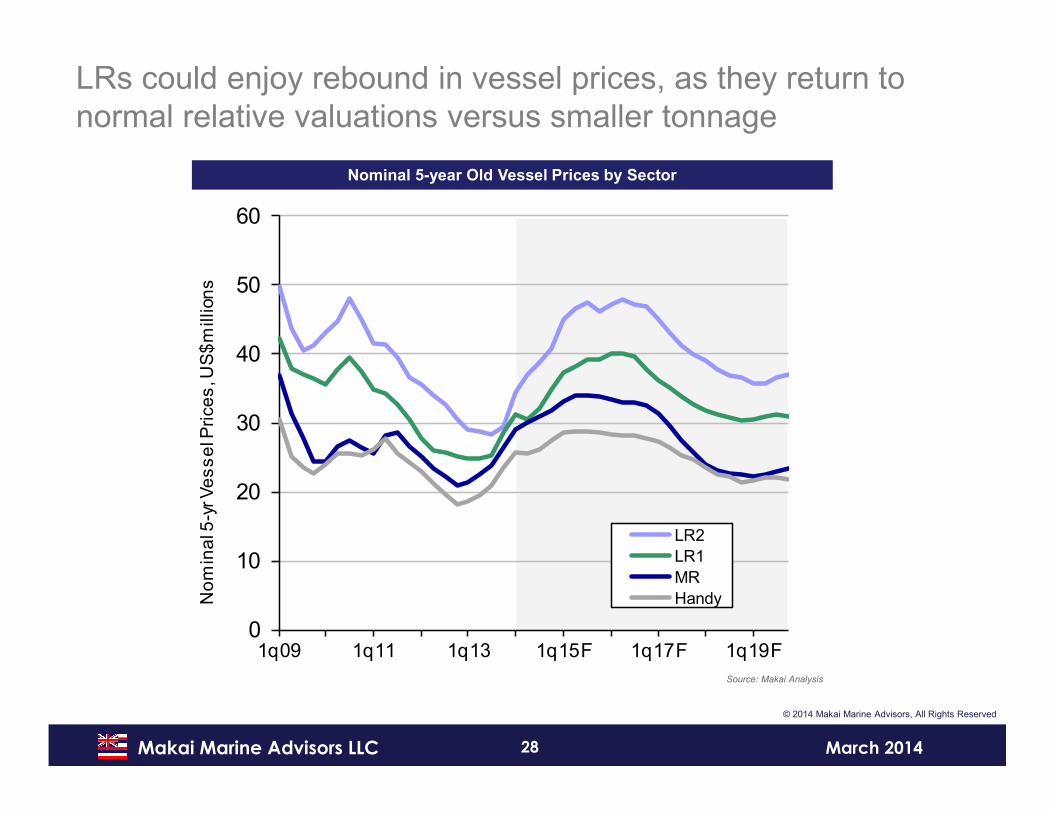

LRs could enjoy rebound in vessel prices, as they return to normal relative valuations versus smaller tonnage

Nominal 5-year Old Vessel Prices by Sector

Source: Makai Analysis

29Makai Marine Advisors LLC March 2014

© 2014 Makai Marine Advisors, All Rights Reserved

Key Observations

• Gasoil remains a key driver for product tanker demand

• Refinery geographic displacement hypothesis still intact, with new Pacific Basin capacity likely to prompt Atlantic Basin refinery rationalisation

- Growing structural mid-distillate deficit in Europe, from rationalisation, is critical element to demand growth

• Strong enthusiasm for product tanker sector in capital markets and private equity sector, based upon this investment hypothesisM

• Mbut ardour may be cooling

• Recognition that upcoming supply growth from over-ordering may outpace these positive demand fundamentals

• Ordering discipline could still protect markets from 2018-19 downturn

30Makai Marine Advisors LLC March 2014

Thank you!

(Mahalo Nui!)

Contact Details:

Makai Marine Advisors LLC5200 Martel AvenueDallas, Texas 75206

US Mobile +1 914 218 7579UK Mobile +44 7976 738 [email protected]

www.makaimarine.com

Twitter: @MakaiMarine