Embed Size (px)

Citation preview

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 1/24

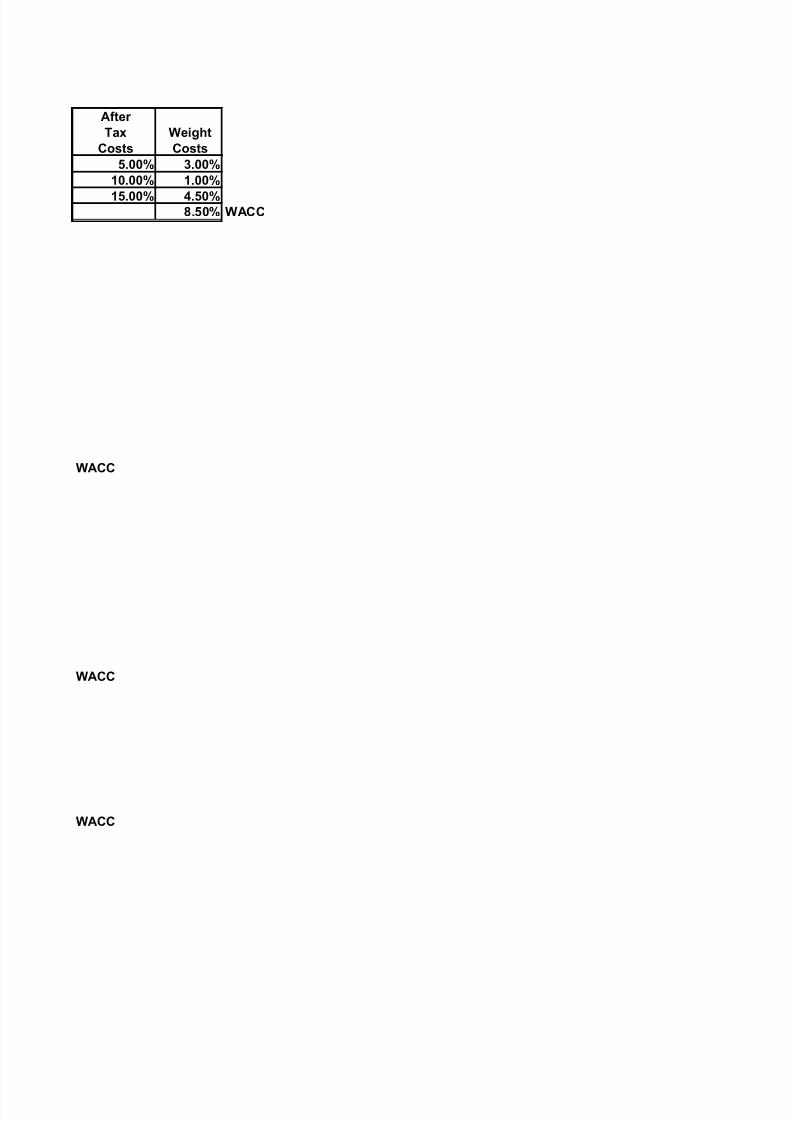

1a

Capital Capital After

Structure Structure Tax Weight

Source of Capital Book Value Weight Weight Costs Costs

LTD 6,000,000.00 6/10 0.60 5.00% 3.00%

PS 1,000,000.00 1/10 0.10 10.00% 1.00%

CS 3,000,000.00 3/10 0.30 15.00% 4.50%TOTAL 10,000,000.00 1.00 8.50% WACC

1b

WACC dictates that all investments should have an internal rate of return above 8.5%.

1c

Debt is less costly because it is less risky from an investor's standpoint thus a lower

return iis demanded by investors. Moreover, interest expense is deductible for tax

purposes creaing cash savings from tax payment reduction.

2a

Capital Capital After Structure Structure Tax Weight

Source of Capital Book Value Weight Weight Costs Costs

LTD 3,000,000.00 6/10 0.30 5.00% 1.50%

PS 1,000,000.00 1/10 0.10 10.00% 1.00%

CS 6,000,000.00 3/10 0.60 15.00% 9.00%

TOTAL 10,000,000.00 1.00 11.50% WACC

2b

There was an increase in WACC in No. 2

The higher the risks the higher the return. Risk and return trade-off.

3a

Capital Capital After

Structure Structure Tax Weight

Source of Capital Book Value Weight Weight Costs Costs

LTD 3,000,000.00 6/10 0.30 5.00% 1.50%

PS 1,000,000.00 1/10 0.10 10.00% 1.00%

CS 6,000,000.00 3/10 0.60 15.00% 9.00%

TOTAL 10,000,000.00 1.00 11.50% WACC

3b

Capital Capital After

Structure Structure Tax Weight

Source of Capital Book Value Weight Weight Costs Costs

LTD 2,500,000.00 6/10 0.19 5.00% 0.96%

PS 1,500,000.00 1/10 0.12 10.00% 1.15%

CS 9,000,000.00 3/10 0.69 15.00% 10.38%

TOTAL 13,000,000.00 1.00 12.50% WACC

3c

Market values are more reliable as they reflect the true value of the net assets.

3d

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 2/24

Investments with IRR of 12% will be wrongfully accepted by using book values.

4a

Selling price 1,010.00

Less

Floatation cost 30.00

Net proceeds, Nd 980.00

4b

t1 t2 t3 … t15

980.00 (120.00) (120.00) … (120.00)

(1,000.00)

4c

Appproximation cost of debt formula:

kd = I + P1,000-Nd/n ki = kd x (1-tax rate)

Nd + P1,000

'2

kd = before tax cost of debt

I = stated interest

Nd = Net proceeds

n = term of the bond

P1,000 = assuimed face value of the bonds

2 = constant

ki - after tax cost of debt

kd= P120 + P1,000 - P980/15 years ,= P120 + 1.3333333 0.122556

P980 + P1,000 990 12.26%

'2

ki= 12.26% x 1-.40 = 0.073533

7.35%

4d

Cost to Maturity:

Step 1: Try 12%

V = 120 (6.811) + 1,000 (0.183)V = 817.32 + 183

V = $1,000.32

(Due to rounding of the PVIF, the value of the bond is 32 cents greater than expected.

At the coupon rate, the value of a $1,000 face value bond is $1,000.)

Try 13%:

V = 120 (6.462) + 1,000 (0.160)

n

ot n

t 1

I MB

(1 k) (1 k)=

= + + +

15

t 15t 1

$120 $1,000$980

(1 k) (1 k)=

= + + +

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 3/24

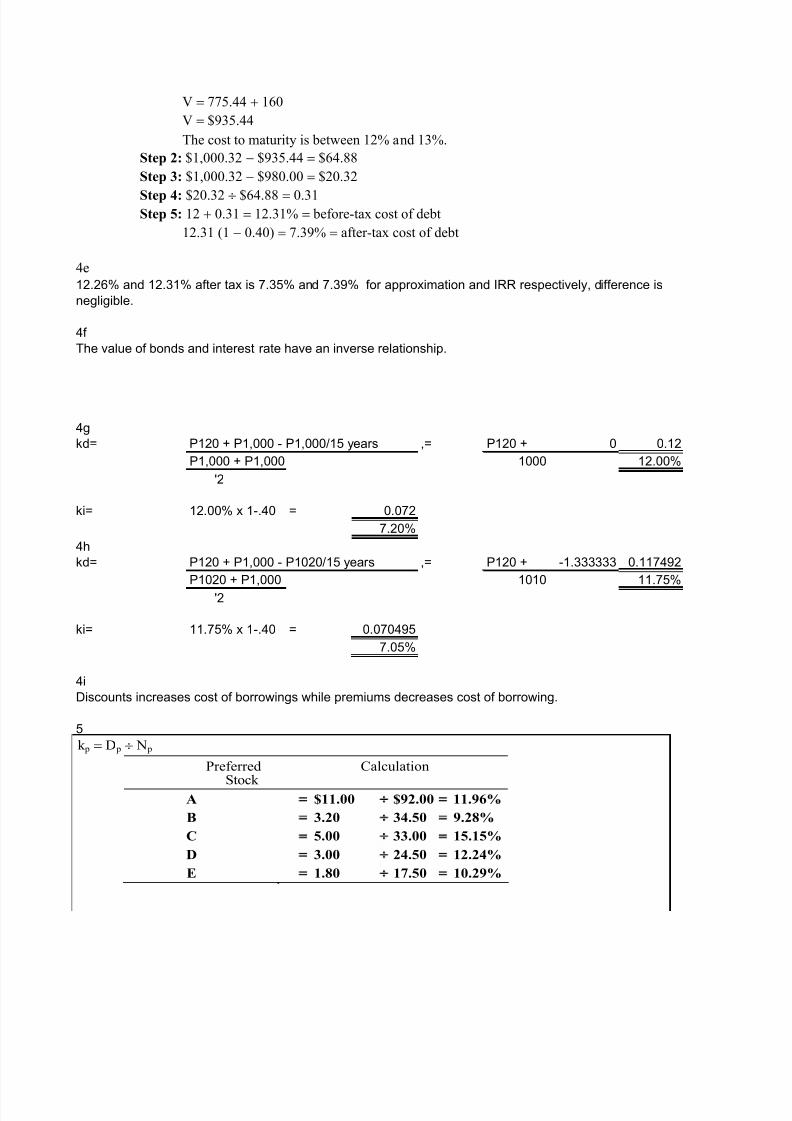

V = 775.44 + 160

V = $935.44

The cost to maturity is between 12% and 13%.

Step 2: $1,000.32 $935.44 = $64.88

Step 3: $1,000.32 $980.00 = $20.32

Step 4: $20.32 $64.88 = 0.31Step 5: 12 + 0.31 = 12.31% = before-tax cost of debt

12.31 (1 0.40) = 7.39% = after-tax cost of debt

4e

12.26% and 12.31% after tax is 7.35% and 7.39% for approximation and IRR respectively, difference is

negligible.

4f

The value of bonds and interest rate have an inverse relationship.

4g

kd= P120 + P1,000 - P1,000/15 years ,= P120 + 0 0.12

P1,000 + P1,000 1000 12.00%

'2

ki= 12.00% x 1-.40 = 0.072

7.20%

4h

kd= P120 + P1,000 - P1020/15 years ,= P120 + -1.333333 0.117492

P1020 + P1,000 1010 11.75%

'2

ki= 11.75% x 1-.40 = 0.070495

7.05%

4i

Discounts increases cost of borrowings while premiums decreases cost of borrowing.

5

k p = D p N p

Preferred

Stock

Calculation

A $11.00 $92.00 11.96%

B 3.20 34.50 9.28%

C 5.00 33.00 15.15%

D 3.00 24.50 12.24%

E 1.80 17.50 10.29%

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 4/24

6a&b

6c

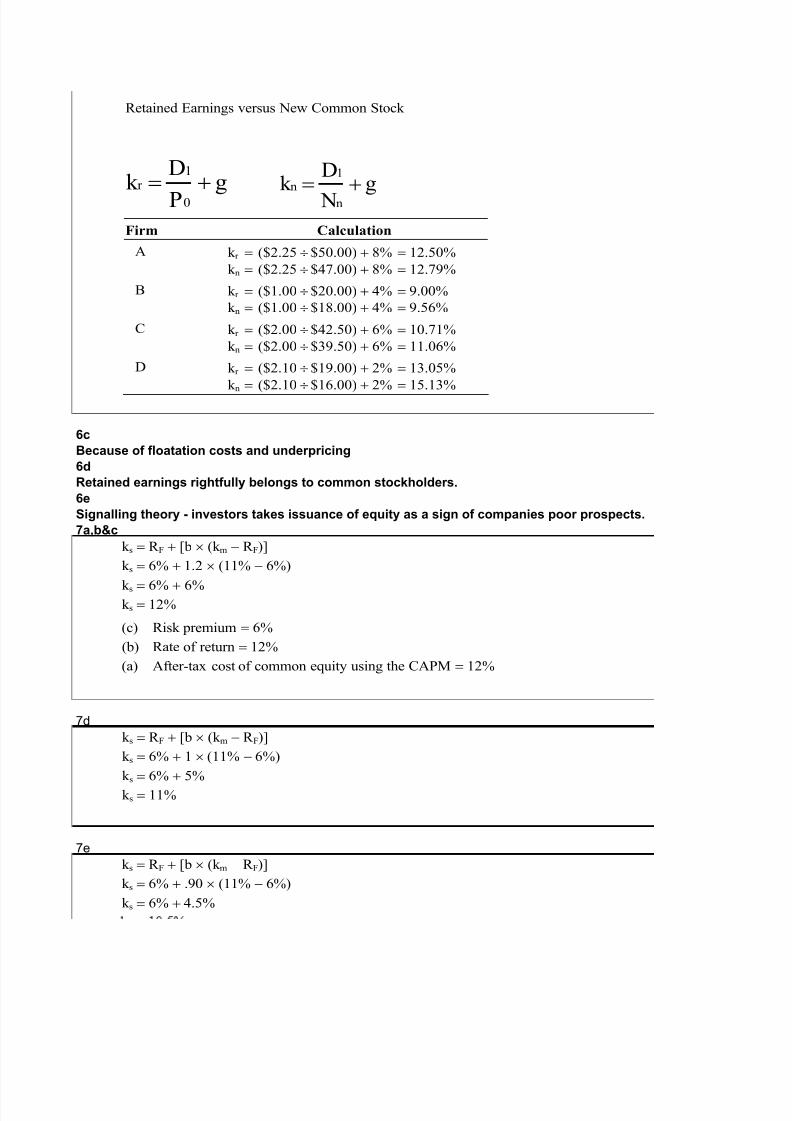

Because of floatation costs and underpricing

6d

Retained earnings rightfully belongs to common stockholders.

6e

Signalling theory - investors takes issuance of equity as a sign of companies poor prospects.

7a,b&c

7d

7e

Retained Earnings versus New Common Stock

1r

0

Dk g

P= +

1n

n

Dk g

N= +

Firm Calculation

A k r = ($2.25 $50.00) + 8% = 12.50%

k n = ($2.25 $47.00) + 8% = 12.79%

B k r = ($1.00 $20.00) + 4% = 9.00%

k n = ($1.00 $18.00) + 4% = 9.56%

C k r = ($2.00 $42.50) + 6% = 10.71%

k n = ($2.00 $39.50) + 6% = 11.06%

D k r = ($2.10 $19.00) + 2% = 13.05%

k n = ($2.10 $16.00) + 2% = 15.13%

k s = R F + [b (k m R F)]

k s = 6% + 1.2 (11% 6%)

k s = 6% + 6%

k s = 12%

(c) Risk premium = 6%

(b) Rate of return = 12%

(a) After-tax cost of common equity using the CAPM = 12%

k s = R F + [b (k m R F)]k s = 6% + 1 (11% 6%)

k s = 6% + 5%

k s = 11%

k s = R F + [b (k m R F)]

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 5/24

7f

Risk free rate is the rate from t-bills or govt. bonds, market return is the return paid by the market whichis higher than the risk free rate and beta is a measure of volatility of the stock price which is measure of

risk.

8

9

k s = 6% + .90 (11% 6%)

k s = 6% + 4.5%

k s = 10.5%

(a)2006

k%,4

2002

Dg FVIF

D= =

$3.10g 1.462

$2.12= =

From FVIF table, the factor closest to 1.462 occurs at 10% (i.e., 1.464 for 4 years).Calculator solution: 9.97%

(b) Nn = $52 (given in the problem)

(c) 2007r

0

Dk g

P= +

r $3.40

k 0.10 15.91%$57.50

= + =

(d) K n 2007r

n

Dk g

N= +

K n=$3.40/$52+.10 = 16.54%

(a) Cost of Retained Earnings

r $1.26(1 0.06) $1.34

k 0.06 3.35% 6% 9.35%

$40.00 $40.00

+= + = = + =

(b) Cost of New Common Stock

s$1.26(1 0.06) $1.34

k 0.06 4.06% 6% 10.06%$40.00 $7.00 $33.00

+= + = = + =

(c) Cost of Preferred Stock

p$2.00 $2.00

k 9.09%= = =

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 6/24

10a

It’s a wrong decision because an investment with an IRR of 8% was accepted while an investment with

10b

Capital Capital After

Structure Structure Tax Weight

Source of Capital Book Value Weight Weight Costs Costs

LTD 60,000.00 6/10 0.60 7.00% 4.20%

PS - 0 0.00 0.00% 0.00%

CS 40,000.00 4/10 0.40 16.00% 6.40%

TOTAL 100,000.00 1.00 10.60% WACC

Reject project Apple and acccept project Mona.

$25.00 $3.00 $22.00

(d) d

$1,000 $1,175$100

$65.005k 5.98%$1,175 $1,000 $1,087.50

2

+

= = =

+

k i = 5.98% (1 0.40) = 3.59%

(e) common equity$4,200,000 ($1.26 1,000,000) $2,940,000

BP $5,880, 0000.50 0.50

= = =

(f) WACC = (0.40)(3.59%) + (0.10)(9.09%) + (0.50)(9.35%)

WACC = 1.436 + 0.909 + 4.675

WACC = 7.02%

This WACC applies to projects with a cumulative cost between 0 and $5,880,000.

(g) WACC = (0.40)(3.59%) + (0.10)(9.09%) + (0.50)(10.06%)

WACC = 1.436 + 0.909 + 5.03

WACC = 7.375%

This WACC applies to projects with a cumulative cost over $5,880,000.

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 7/24

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 8/24

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 9/24

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 10/24

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 11/24

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 12/24

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 13/24

1a

Liabilities Capital Capital

And Equity Structure Structure

Assets Source of Capital Book Value Weight Weight

Current Assets - C 10,000,000.00 Long Term Debt 6,000,000.00 6/10 0.60

Fixed Assets Preferred Stock 1,000,000.00 1/10 0.10

Common Stock 3,000,000.00 3/10 0.30TOTAL ASSETS 10,000,000.00 TOTAL 10,000,000.00 1.00

1b

WACC dictates that all investments should have an internal rate of return above 8.5%.

1c

Debt is less costly because it is less risky from an investor's standpoint thus a lower

return iis demanded by investors. Moreover, interest expense is deductible for tax

purposes creaing cash savings from tax payment reduction.

2a

Capital Capital After

Structure Structure Tax WeightSource of Capital Book Value Weight Weight Costs Costs

LTD 3,000,000.00 6/10 0.30 5.00% 1.50%

PS 1,000,000.00 1/10 0.10 10.00% 1.00%

CS 6,000,000.00 3/10 0.60 15.00% 9.00%

TOTAL 10,000,000.00 1.00 11.50%

2b

There was an increase in WACC in No. 2

The higher the risks the higher the return. Risk and return trade-off.

3a

Capital Capital After

Structure Structure Tax Weight

Source of Capital Book Value Weight Weight Costs Costs

LTD 3,000,000.00 6/10 0.30 5.00% 1.50%

PS 1,000,000.00 1/10 0.10 10.00% 1.00%

CS 6,000,000.00 3/10 0.60 15.00% 9.00%

TOTAL 10,000,000.00 1.00 11.50%

3b

Capital Capital After

Structure Structure Tax Weight

Source of Capital Market Value Weight Weight Costs Costs

LTD 2,500,000.00 0.19 0.19 5.00% 0.96%

PS 1,500,000.00 0.12 0.12 10.00% 1.15%CS 9,000,000.00 0.69 0.69 15.00% 10.38%

TOTAL 13,000,000.00 1.00 12.50%

3c

Market values are more reliable as they reflect the true value of the net assets.

3d

Investments with IRR of 12% will be wrongfully accepted by using book values.

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 14/24

4a

Selling price 1,010.00

Less

Floatation cost 30.00

Net proceeds, Nd 980.00

4b

t0 t1 t2 …

980.00 (120.00) (120.00) …

4c

Appproximation cost of debt formula:

kd = I + P1,000-Nd/n ki = kd x (1-tax rate)

Nd + P1,000

'2

kd = before tax cost of debt

I = stated interest

Nd = Net proceeds

n = term of the bond

P1,000 = assuimed face value of the bonds

2 = constant

ki - after tax cost of debt

kd= P120 + P1,000 - P980/15 years ,= P120 +

P980 + P1,000 990

'2

ki= 12.26% x 1-.40 = 0.073533333

7.35%

4d

Cost to Maturity:

Step 1: Try 12%

V = 120 (6.811) 1,000 (0.183)

V = 817.32 183V = $1,000.32

(Due to rounding of the PVIF, the value of the bond is 32 cents greater than expected.

At the coupon rate, the value of a $1,000 face value bond is $1,000.)

Try 13%:

V = 120 (6.462) 1,000 (0.160)

V = 775.44 160

V = $935.44

n

ot n

t 1

I MB

(1 k) (1 k)=

= + + +

15

t 15t 1

$120 $1, 000$980

(1 k) (1 k)=

= + + +

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 15/24

The cost to maturity is between 12% and 13%.

Step 2: $1,000.32

$935.44=

$64.88

Step 3: $1,000.32

$980.00=

$20.32

Step 4: $20.32

$64.88=

0.31

Step 5: 12 0.31=

12.31%=

before-tax cost of debt

12.31 (1 0.40) = 7.39% = after-tax cost of debt

4e

12.26% and 12.31% after tax is 7.35% and 7.39% for approximation and IRR respectively, differ

negligible.

4f

The value of bonds and interest rate have an inverse relationship.

4gkd= P120 + P1,000 - P1,000/15 years ,= P120 +

P1,000 + P1,000 1000

'2

ki= 12.00% x 1-.40 = 0.072

7.20%

4h

kd= P120 + P1,000 - P1020/15 years ,= P120 +

P1020 + P1,000 1010

'2

ki= 11.75% x 1-.40 = 0.0704950697.05%

4i

Discounts increases cost of borrowings while premiums decreases cost of borrowing.

5

6a&b

k p = D p N p

PreferredStock

Calculation

A $11.00 $92.00 11.96%

B 3.20 34.50 9.28%

C 5.00 33.00 15.15%

D 3.00 24.50 12.24%

E 1.80 17.50 10.29%

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 16/24

6c

Because of floatation costs and underpricing

6d

Retained earnings rightfully belongs to common stockholders.

6e

Signalling theory - investors takes issuance of equity as a sign of companies poor prospects.

7a,b&c

7d

7e

Retained Earnings versus New Common Stock

1r

0

Dk g

P= +

1n

n

Dk g

N= +

Firm Calculation

A k r = ($2.25 $50.00) + 8% = 12.50%

k n = ($2.25 $47.00) + 8% = 12.79%

B k r = ($1.00 $20.00) + 4% = 9.00%

k n = ($1.00 $18.00) + 4% = 9.56%

C k r = ($2.00 $42.50) + 6% = 10.71%

k n = ($2.00 $39.50) + 6% = 11.06%

D k r = ($2.10 $19.00) + 2% = 13.05%

k n = ($2.10 $16.00) + 2% = 15.13%

k s = R F + [b (k m R F)]

k s = 6% + 1.2 (11% 6%)

k s = 6% + 6%k s = 12%

(c) Risk premium = 6%

(b) Rate of return = 12%

(a) After-tax cost of common equity using the CAPM = 12%

k s = R F + [b (k m R F)]

k s = 6% + 1 (11% 6%)

k s = 6% + 5%

k s = 11%

k s = R F + [b (k m R F)]

k s = 6% + .90 (11% 6%)

k s = 6% + 4.5%

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 17/24

7f

Risk free rate is the rate from t-bills or govt. bonds, market return is the return paid by the mark

is higher than the risk free rate and beta is a measure of volatility of the stock price which is m

risk.

8

9

s = .

(a)2006

k%,4

2002

Dg FVIF

D= =

$3.10g 1.462

$2.12= =

From FVIF table, the factor closest to 1.462 occurs at 10% (i.e., 1.464 for 4 years).Calculator solution: 9.97%

(b) Nn = $52 (given in the problem)

(c) 2007r

0

Dk g

P= +

r $3.40

k 0.10 15.91%$57.50

= + =

(d) K n 2007r

n

Dk g

N= +

K n=$3.40/$52+.10 = 16.54%

(a) Cost of Retained Earnings

r $1.26(1 0.06) $1.34

k 0.06 3.35% 6% 9.35%$40.00 $40.00

+= + = = + =

(b) Cost of New Common Stock

s$1.26(1 0.06) $1.34k 0.06 4.06% 6% 10.06%$40.00 $7.00 $33.00

+= + = = + =

(c) Cost of Preferred Stock

p$2.00 $2.00

k 9.09%$25.00 $3.00 $22.00

= = =

$1,000 $1,175$100

+

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 18/24

10a

It’s a wrong decision because an investment with an IRR of 8% was accepted while an investment with

10b

Capital Capital After

Structure Structure Tax Weight

Source of Capital Book Value Weight Weight Costs Costs

LTD 60,000.00 6/10 0.60 7.00% 4.20%

PS - 0 0.00 0.00% 0.00%

CS 40,000.00 4/10 0.40 16.00% 6.40%

TOTAL 100,000.00 1.00 10.60%

Reject project Apple and acccept project Mona.

(d) d.

k 5.98%$1,175 $1,000 $1,087.50

2

= = =

+

k i = 5.98% (1 0.40) = 3.59%

(e) common equity$4,200,000 ($1.26 1,000,000) $2,940,000

BP $5,880, 000

0.50 0.50

= = =

(f) WACC = (0.40)(3.59%) + (0.10)(9.09%) + (0.50)(9.35%)

WACC = 1.436 + 0.909 + 4.675

WACC = 7.02%

This WACC applies to projects with a cumulative cost between 0 and $5,880,000.

(g) WACC = (0.40)(3.59%) + (0.10)(9.09%) + (0.50)(10.06%)

WACC = 1.436 + 0.909 + 5.03

WACC = 7.375%

This WACC applies to projects with a cumulative cost over $5,880,000.

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 19/24

After

Tax Weight

Costs Costs

5.00% 3.00%

10.00% 1.00%

15.00% 4.50%8.50% WACC

WACC

WACC

WACC

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 20/24

t15

(120.00)

(1,000.00)

1.333333333 0.122556

12.26%

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 21/24

nce is

0 0.12

12.00%

-1.33333333 0.117492

11.75%

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 22/24

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 23/24

8/12/2019 6 Cost of Capital Solution

http://slidepdf.com/reader/full/6-cost-of-capital-solution 24/24

WACC